Valuation of asset and volatility derivatives using decoupled time-changed Lévy processes 111A MATHEMATICA® online supplement to this paper containing numerical reuslts is available at the website: http://lorenzotorricelli.it/Code/DTC_TVO_Implementation.nb.

Abstract

In this paper we propose a general derivative pricing framework that employs decoupled time-changed (DTC) Lévy processes to model the underlying assets of contingent claims. A DTC Lévy process is a generalized time-changed Lévy process whose continuous and pure jump parts are allowed to follow separate random time scalings; we devise the martingale structure for a DTC Lévy-driven asset and revisit many popular models which fall under this framework. Postulating different time changes for the underlying Lévy decomposition allows the introduction of asset price models consistent with the assumption of a correlated pair of continuous and jump market activity rates; we study one illustrative DTC model of this kind based on the so-called Wishart process. The theory we develop is applied to the problem of pricing not only claims that depend on the price or the volatility of an underlying asset, but also more sophisticated derivatives whose payoffs rely on the joint performance of these two financial variables, such as the target volatility option (TVO). We solve the pricing problem through a Fourier-inversion method. Numerical analyses validating our techniques are provided. In particular, we present some evidence that correlating the activity rates could be beneficial for modeling the volatility skew dynamics.

Keywords: Derivative pricing; time changes; Lévy processes; joint asset and volatility derivatives; target volatility option; Wishart process

MSC: 91G20, 60G46

1 Introduction

The use of Lévy models in finance dates back to to the classic work of Merton (1976), who proposed that the log-price dynamics of a stock return should follow an exponential Brownian diffusion punctuated by a Poisson arrival process of normally distributed jumps. In that work, two of the main shortcomings of the Black-Scholes model, the continuity of the sample paths and the normality of returns, were addressed for the first time. Over the years, Lévy processes have proved to be a flexible and yet mathematically tractable instrument for asset price modeling and sampling. One of the easiest ways of producing a Lévy process is to use the principle of subordination of a Brownian motion . If is an increasing Lévy process independent of , then the subordinated process will still be of Lévy type. Subordination is the simplest example of a time change, that is, the operation whereby one considers the time evolution of a stochastic process as occurring at a random time.

Return models depending on time-changed Brownian motions have been conjectured since Clark (1973); further theoretical support to the financial use of time-changed models is given by Monroe’s (1978) theorem, asserting that any semimartingale can be viewed as a time change of a Brownian motion. Consequently, any semimartingale representing the log-price process of an asset can be considered as a re-scaled Wiener process. Empirical studies (Ane and Geman, 2000) confirmed that normality of returns can be recovered in a new price density based on the quantity and arrival times of orders, which justifies the interpretation of as “business time” or “stochastic clock”; the instantaneous variation of is hence the “activity rate” at which the market reacts to the arrival of information. Further advances were made by Carr and Wu (2004), who demonstrated that much more general time changes are potential candidates for asset price modeling, and effectively recovered many models from the standard literature by using a time-changed representation.

However, not all the possibilities in time change modeling have been exhausted by the current research. For example, the stochastic volatility model with jumps (SVJ) treated among the others by Bates (1996), and the stochastic volatility model with jumps and stochastic jump rate (SVJSJ) studied by Fang (2000), although retaining a time re-scaled structure, are not time-changed Lévy processes as they are understood in Carr and Wu (2004). Indeed, in these two classes of models the jump component does not follow the same time scaling as the continuous Brownian part: in the SVJ model the discontinuities have stationary increments, whereas in the SVJSJ model the jump rate is allowed to follow a stochastic process of its own. In other words, price models for which the “stochastic clock” runs at different paces for the “small” and “big” market movements have already been proposed and tested. The statistical analyses of Bates (1996) and Fang (2000) confirm that these models are capable of an excellent data fitting, in particular the SVJSJ model. As pointed out by Fang (2000), there are various other reasons for conjecturing a stochastic jump rate. If activity rates are to be interpreted as the frequencies of arrival of new market information, it seems unlikely that such rates could be taken as constant, as this would imply a constant information flow. Moreover, a constant jump rate implies stationary jump risk premia, which also seems unreasonable. Another stylized fact potentially captured by a model with a stochastic jump rate is the slow convergence of returns to the normal distribution, which is not a feature of stationary jump models. Despite all these considerations, the idea of a stochastic jump rate has never really caught on.

On the other hand, if we want to exogenously model the market activity, the hypothesis of independence between the jump and the continuous instantaneous rates as assumed by Fang (2000) seems to be overly simplistic, as in reality the two corresponding information flows may very well influence each other. For example, a crash or soaring of the market certainly impacts the day-to-day volume of trading in the days following such an event. Conversely, a sustained high activity trend over a long period, typically associated to falling prices, may eventually lead to a sudden, panic-driven plunge in the shares’ value. These and similar scenarios provide heuristic arguments for the assumption of a correlated pair of activity rates; nevertheless, to the best of this author’s knowledge, asset price models capturing this feature are not yet present in the literature.

Motivated by these arguments, the natural question that arises is whether it is possible to manufacture consistent general time-changed price processes in which the continuous and discontinuous parts of the underlying Lévy model follow two different, possibly correlated, stochastic time changes. We shall show that the answer is affirmative. The family of stochastic processes we investigate is that obtained by time-modifying the continuous and jump parts of a given Lévy process by two, in principle dependent, stochastic time scalings and satisfying a certain regularity condition (definition 3.1). We call such processes decoupled time changes. In a formula:

| (1.1) |

where and represent respectively the Brownian and jump components of .

The decoupled time-changed (DTC) approach suggested allows to embed in a unifying mathematical framework many previously-known models or classes of models, so that the DTC theory offers a natural generalization of some of the extant asset modeling research. In addition, the assumption of a pair of dependent activity rates can be captured by making use of decoupled time changes. To our knowledge, this last feature is new to the asset modeling literature. In section 7 we shall illustrate a practical example of a model having this property by considering an explicit asset evolution based on a multivariate version of the square-root process known as the Wishart process (e.g. Bru 1991; Gourieroux 2003; da Fonseca et al. 2007), which we use to model the instantaneous activity rates. In section 8.2 we provide some descriptive analysis showing that this model retains an increased flexibility for the purpose of modeling the volatility skew, compared to some popular existing jump asset price models.

A prior study supporting the financial use of DTC Lévy is given by the work of Huang and Wu (2004). The authors conduct a specification analysis of an SDE whose solution is equivalent to a DTC Lévy-based asset evolution as defined in this paper, give an overview of the “nesting” of models allowed by this setup, and then discuss the impact of various time change specifications in parameter estimation. However, their work does not provide any theoretical justification for the martingale property of the general asset price equation used. Furthermore, they do not explore the issue of dependence between the activity rates as related to analytical tractability, a natural ground of analysis provided by the model. Indeed, to ensure the existence of a semi-closed pricing equation for the “SV4” model in section E, the authors have to revert to a model with independent activities. By providing a general theoretical framework for DTC-based Lévy models, and devising an analytical DTC specification with true dependence between the stochastic volatility and the jump rate, this paper addresses both of these shortcomings.

From the perspective of the valuation of financial derivatives, the aim of this work is to gain some understanding of the impact on derivative pricing of the interactions between the volatility and the price of the underlying. To give an example, a recent market innovation is that of derivatives and investment strategies based on volatility-modified versions of plain vanilla products. Such contracts are able to replicate classic European payoffs under a perfect volatility foresight; at the same time, the component of the price that is due to a vega excess may be reduced by using the realized volatility as a normalizing factor. One example of such a product is the target volatility option. A target volatility (call) option (TVO) pays at maturity the amount:

| (1.2) |

for a strike price and a target volatility level , a constant that is written in the contract. Intuitively, the closer the realized volatility is to , the more this claim will behave like a call option; however, the presence of in the denominator decreases the sensitivity of to a change in volatility. It can be shown (Di Graziano and Torricelli, 2012) that the price of an at-the-money TVO is approximately that of an at-the-money Black-Scholes call having implied volatility ; such a constant thus represents the subjective volatility view of an investor, which may very well differ from the spot volatilities implied by the market.

In view of this increasing interaction between volatility and stock in the financial assets available in the market, being able to efficiently price derivatives like the TVO and other similar products is gaining relevance. The pricing problem of hybrid volatility/asset derivatives, with special emphasis on the target volatility option, has already been addressed by Di Graziano and Torricelli (2012) for a zero-correlation stochastic volatility model, and by Torricelli (2013), for a general stochastic volatility model. However, to our knowledge, a comprehensive pricing framework comparable to those available for plain vanilla derivatives (e.g Carr and Madan 1999; Lewis 2000; Lewis 2001; Carr and Wu 2004) has not yet been developed: this is one limitation we intend to overcome with this paper. The pricing technique we use is a well-known approach yielding a semi-closed analytical formula for the derivative price through an inverse Fourier integral. It should be apparent that in all the models we shall investigate there is no particular reason not to consider mixed price and volatility payoffs as the default input of pricing models e.g. for numerical implementation, as the introduction of the realized volatility does not cause the Fourier-inversion technique to break down. Clearly, pricing both vanilla and pure volatility derivatives is still possible within this framework, since the corresponding payoff types can be regarded as particular cases of our more general setting.

The remainder of the paper is organized as follows. In section 2 we lay out the assumptions; in section 3 we derive martingale properties for a decoupled time-changed Lévy model. Section 4 shows the fundamental relation linking the characteristic function of the log-price and its quadratic variation and the joint Laplace transform of the time changes as computed in an appropriate measure. Section 5 is dedicated to the derivation of a pricing formula for products whose payoffs depend jointly on and . We devote section 6 to characterizing the DTC structure of a number of known models and computing the joint characteristic function discussed in section 4 for each such model. In section 7 we introduce an exemplifying model of DTC type featuring correlation between the time changes/activity rates. In section 8 we implement our formulae to valuate different asset and volatility derivatives under various market conditions and asset price models. In this numerical section we also perform a sensitivity analysis of the model introduced in section 7 with respect to a correlation parameter. Finally, in section 9 we briefly summarize our work. The more technical proofs have been placed in the appendix.

2 Assumptions and notation

As customary, our market is represented by a filtered probability space satisfying the usual conditions. Throughout the paper we will assume that there exists a money market account process paying a constant interest rate .

Let be a non dividend-paying market asset. will denote its time-zero discounted value . The total realized variance on of is by definition the quadratic variation of the natural logarithm of , that is:

| (2.1) |

The limit runs over the supremum norm of all the possible partitions of . The total realized volatility is . The period realized variance and volatility (or realized variance/volatility tout court) are given respectively by and . If is a semimartingale, by taking the limit in (2.1) it is easy to check that:

| (2.2) |

The algebra of the square matrices of order with real entries is indicated by and the sub-algebra of the symmetric matrices by . Matrix product is denoted by juxtaposition; the scalar product between vectors is either indicated by multiplying on the left with the transposed vector or by the usual dot notation. The symbol stands for the trace operator.

If is an absolutely continuous random variable, we denote by its probability density function and by its characteristic function

| (2.3) |

For a Fourier-integrable function its Fourier transform will be denoted . For a complex-valued function or a complex plane subset, indicates the complex conjugate function or set.

When we say that a process is a martingale we mean a martingale with respect to its natural filtration. The notation for the conditional expectation of a stochastic process at time with respect to is . When the distribution of a process depends on other state variables (as in the case of a Markov process) the latter are implicitly understood to be given at time by . If is a process admitting conditional laws, the space of the integrable functions in the -conditional distribution of at time is indicated by . The notation for the bilateral Laplace transform of the distribution of conditional on is:

| (2.4) |

where for brevity we drop the dependence on and on the left hand side. The stochastic process of the left limits of is indicated . The symbol stands for the difference or for some prior time . Equalities are always understood to hold modulo almost sure equivalence.

If is an -dimensional Lévy process, the characteristic exponent of is the complex-valued function such that:

| (2.5) |

where lies in the subset of and where the left-hand side is finite.

For a given choice of truncation function (that is, a bounded function which is O around 0) the characteristic exponent has the unique Lévy-Khintchine representation:

| (2.6) |

where , is a non-negative definite matrix with real-valued entries, and is a Radon measure on having a density function that is integrable at and O around 0. We shall make the standard choice and drop the dependence of on . The triplet is then called the characteristic triplet or the Lévy characteristics of .

A stochastic time change is an -adapted càdlàg stochastic process, increasing and almost surely finite, such that is an -adapted stopping time for each . The time change of an -dimensional Lévy process according to is the -adapted process .

3 Definition, martingale relations and asset price dynamics

In this first section we introduce the notion of DTC Lévy process and devise an exponential martingale structure naturally associated to it. This construct serves a twofold purpose. In first place it allows to formulate a DTC-based asset price evolution whose discounted value enjoys the martingale property. According to general theory, this in turn enables to postulate the existence of a risk-neutral measure that correctly prices the market securities. Secondly, it defines a class of complex-valued martingales pivotal for the computations of the next section.

Let be the space of the -dimensional -supported Brownian motions with drift starting at , and be the space of the -supported pure jump Lévy processes starting at 0, that is, the class of the càdlàg -adapted processes with stationary and independent increments orthogonal333Two processes and are said to be orthogonal if for all . to all the elements of .

Every Lévy process such that can be decomposed as the orthogonal sum

| (3.1) |

with and . We shall refer to and respectively as the continuous and discontinuous parts of .

Time changes are fairly general mathematical objects, so we have to introduce some additional requirements in order for our discussion to proceed. One property we shall assume throughout is the so-called continuity with respect to the time change.

Definition 3.1.

Let be a time change on a filtration . An -adapted process is said to be -continuous444Jacod (1979) uses -adapted, and -synchronized is sometimes found; however, -continuous is also common in the literature, and in our view less ambiguous. if it is almost-surely constant on all the sets .

Obviously, a sufficient condition for -continuity is the almost sure continuity of . Hence, of particular relevance is the class of the absolutely continuous time changes, with respect to which every stochastic process is continuous. Given a pair of instantaneous rate of activity processes, that is, two exogenously-given càdlàg positive stochastic processes , valid time changes are given by the pathwise integrals:

| (3.2) |

| (3.3) |

The processes and describe the instantaneous impact of market trading and information arrival on the price, and formalize the concept of “business activity” over time.

A decoupled time change of a Lévy process is the sum of the (ordinary) time changes of its continuous and discontinuous part.

Definition 3.2.

Let be an -dimensional Lévy process and , two time changes such that is almost surely continuous and is -continuous. Then:

| (3.4) |

is the decoupled time change of according to and .

By (Jacod, 1979), corollaire 10.12, a first important property of is that it is an semimartingale.To avoid degenerate cases, in all that follows we always assume and to be such that and are Markov processes555In general, time changes of Markov processes are not Markovian; by using Dambis, Dubins and Schwarz’s theorem (Karatzas and Shreve 2000, theorem 4.6) one can manufacture a large class of counterexamples by starting from any continuous martingale that is not a Markov process..

We now define the class of exponential martingales canonically associated with when the time changes are absolutely continuous. The following proposition represents the main theoretical tool of this paper:

Proposition 3.3.

Let be an -dimensional Brownian motion with drift and a pure jump Lévy process in . Let and be two absolutely continuous time changes, set and ; define and denote by the domain of definition of . The process:

| (3.5) |

is a local martingale, and it is a martingale if and only if , where:

| (3.6) |

When , the exponential reduces to an ordinary time change of the type discussed by Carr an Wu (2004). Even in this simple case proposition 3.3 is not a consequence of applying Doob’s optional sampling theorem to the martingale , because the latter is not necessarily uniformly integrable. Indeed, time-transforming a process always preserves the semimartingale property, but the martingale property is only guaranteed to be maintained for uniformly integrable martingales; an actual example of an asset model of the form that is a strict supermartingale was given by Sin (1998). Hence, the set may very well trivialize to the empty set. This demonstrates that some choices of time changes are inherently unsuitable for time-changed asset price modeling. In the case of being a one-dimensional Brownian integral, sufficient requirements for (3.6) to be satisfied are the well-known Novikov and Kazamaki conditions (Karatzas and Shreve 2000, chapter 3), under which the set contains the whole of . The set is sometimes called the natural parameter set.

Having obtained martingale relations for a stochastic exponential involving , the risk-neutral dynamics for a DTC Lévy-driven asset are defined in the usual fashion. We have the following immediate corollary to proposition 3.3:

Corollary 3.4.

Let be a scalar Lévy process of characteristic triplet and a pair of absolutely continuous time changes. For a spot price value let, for :

| (3.7) |

with being such that (3.7) is a real number. The discounted process is a martingale, and therefore is a price process consistent with the no-arbitrage condition.

The stochastic process in (3.7) is the fundamental asset model we shall use throughout the rest of the paper.

4 Characteristic functions and the leverage-neutral measure

Characteristic functions of state variables are the essential component of the Fourier-inverse pricing methodology, because state price densities are analytically available only for a small number of models; in contrast, characteristic functions are computable in closed form in many instances (e.g. exponential Lévy models, Ito diffusions). This effectively means that in order to compute expectations (prices), the standard approach is not to integrate a payoff against a density function, but rather the payoff’s Fourier transform against the characteristic functions of the price transition densities. Famous examples include the FFT paper by Carr and Madan (1999), Lewis’s book (2000) and subsequent paper (2001).

The transform we are interested in is one associated with the price process (3.7). Compared to the usual inverse Fourier/Laplace framework the characteristic function we shall consider is not that of the discounted log-price alone, but one that incorporates also the quadratic variation of the log-process. Indeed, just as the characteristic function of the log-price allows for the derivation of pricing formulae for contingent claims , the joint characteristic function of and permits the valuation of payoffs of the form . This has been envisaged before by Carr and Sun (2007).

In the present section we compute this transform. There are normally two ways of computing characteristic functions/Laplace transforms of log-price densities. One is the analytical approach, which is popular for example in affine models, when the problem is ultimately reduced to solving a certain system of ODEs. The other is the probabilistic approach, in which the characteristic function of the log-price is linked with the Laplace transform of the integrated driving factors (where available) and then a change of measure is performed to keep track of correlations. As Carr and Wu (2004) show this technique is intimately connected with time-changed asset modeling; in what follows we extend it to the case of the underlying being modeled through a full DTC Lévy process.

First of all we must verify that the quadratic variation operator respects the additivity and time-changed structure of . We have the following “linearity/commutativity property”, of independent interest:

Proposition 4.1.

A DTC Lévy process is such that and are orthogonal. Furthermore, its quadratic variation satisfies:

| (4.1) |

That is, the quadratic variation of is the sum of the time changes of the quadratic variations of its continuous and discontinuous part.

Crucially, the processes and are orthogonal but not independent. Without the and -continuity assumption, this proposition would be false: a counterexample is provided in the appendix. Proposition 4.1 ensures that, in presence of time continuity of the Lévy continuous and jump parts with respect to the corresponding time changes, the quadratic variation of a DTC Lévy process is itself of DTC-type.

Now, for as in (3.7) define:

| (4.2) |

For each for which the right hand side is finite, is the Fourier transform is the joint transition function from time to time of and . The characteristic function can be completely characterized in terms of the Lévy triplet of and the joint -distribution of and by virtue of the following proposition.

Proposition 4.2.

Let be an asset evolution as in corollary 3.4, and define the family of absolutely-continuous measures having Radon-Nikodym derivative:

| (4.3) |

where , and is given by (3.5). For all such that , the characteristic function in (4.2) is given by:

| (4.4) |

with the notation indicating the bilateral Laplace transform of the conditional joint distribution of and taken under the measure , and

| (4.5) | ||||

| (4.6) |

Notice that unlike the density processes used for standard numéraire changes, the new distributions implied by (4.3) also accounts for the quadratic variation as a factor. If we assume and to be pathwise integrals of the form (3.2) and (3.3), it is possible to interpret the Laplace transform (4.4) as being the analogue of a bivariate bond pricing formula, where the short rates are replaced by the instantaneous activity rates, and the pricing measure is not given once and for all, but varies as an effect of the correlation of with the underlying Lévy process. The financial insight of (4.4) is that it is possible to formulate a valuation theory by just modeling the joint term structure of the activity rates and and their correlation with the stock.

Also of interest is the interpretation of the measure . Let us consider the special case of being independent of and . In such a case it is straightforward to prove, by using the laws of the conditional expectation, that one obtains (4.4) with . Therefore, whenever there is no dependence between the time changes and the underlying Lévy process, no change of measure is needed in order to extract the characteristic function . In contrast, in the presence of correlation between and the time changes, the family gives a measurement of the impact of leverage on the price densities. Furthermore, in some well-behaved cases this change of measure can be absorbed in the -dynamics of the asset through a suitable parameter alteration of the distributions of and . In accordance with Carr and Wu (2004), we call the leverage-neutral measure and the leverage-neutral characteristic function. Just as prices in a risky market can be equivalently computed in a risk-neutral environment according to a different price distribution, valuations in the presence of leverage can be performed in a different economy with no leverage by means of an appropriate distributional modification.

5 Pricing and price sensitivities

The characteristic function found in section 4 is needed to obtain analytical formulae for the valuation of European-type derivatives with a sufficiently regular payoff . In the present section we find a semi-analytical formula based on an inversion integral that extends the standard Fourier-inversion machinery to our multivariate context.

Recall that since all the involved processes are Markovian, it makes sense to treat like a Gauss-Green integral kernel depending only on some given initial states at time . The following proposition extends both theorem 1 of Lewis (2000) and proposition 3.1 of Torricelli (2013):

Proposition 5.1.

Let , with given in corollary 3.4. Let for all , be a positive payoff function having analytical Fourier transform in a multi-strip

| (5.1) |

Suppose further that is analytical in

| (5.2) |

and that . If , then for every multi-line:

| (5.3) |

we have that the time- value of the contingent claim maturing at time is given by:

| (5.4) |

It is clear that modifying the asset dynamics specifications only acts on , whereas changing the claim to be priced only influences . Also, by setting either variable to 0, we are able to extract from (5.4) the prices of both plain vanilla and pure volatility derivatives. For example, the pricing integrals by Lewis (2000, 2001) are special cases of the above equation when does not depend on the realized volatility and is either obtained from a diffusion or a Lévy process. Moreover, equation (3.10) of Torricelli (2013) is recovered when is assumed to follow a stochastic volatility model.

In addition, this representation is useful if we are interested in the sensitivities of the claim value with respect to the underlying state variables. Let us consider for instance the Delta (sensitivity with respect to the change in the value of the underlying) and Gamma (sensitivity with respect to the rate of change in the value of the underlying) of valuations performed through formula (5.4). Call the integrand on the right hand side of (5.4); by differentiating (if possible) under the integral sign and noting that has no dependence on we see that:

| (5.5) |

and

| (5.6) |

Mutatis mutandis we can repeat this argument if we want to determine the price sensitivity with respect to the quadratic variation . Finally, as could also depend on other variables (e.g. an instantaneous rate of activity ) known at time , by calling one such variable we have:

| (5.7) |

This is especially well-suited to the case in which is exponentially-affine in , i.e.

| (5.8) |

for some functions and , when we have:

| (5.9) |

In section 6 we shall explicitly calculate for a number of decoupled time-changed models.

6 Specific model analysis

We now determine the DTC Lévy structure (3.7) of various popular asset price processes, and find for each of them the corresponding leverage-neutral characteristic function . Such a derivation allows for the full implementation of equation (5.4) for the pricing of joint asset and volatility derivatives in all the cases we deal with. What the discussion below should make apparent is that decoupled time changes offer a natural unifying framework for a priori different strains of financial asset models (e.g. continuous/jump diffusions, jump diffusions with stochastic volatility, Lévy processes). By classifying models through their DTC structure it is possible to recognize a “nesting” pattern linking different models, in which some can be considered particular cases of some others. This is of use for numerical purposes: as we shall see in section 8, one single implementation of equation (5.4) can produce values for several models, each one obtained by using a different instantiation of the code. Four categories of asset models are discussed: standard Lévy processes, stochastic volatility models, DTC jump diffusions and general exponentially-affine asset models. Throughout this section we assume in (3.7), so that and all of the involved processes are real-valued. The domain where the price processes are martingales is the whole complex plane, provided that the stochastic time changes and the underlying Lévy components are sufficiently well-behaved, in the sense of the usual theory (e.g. Novikov condition for the stochastic variance, decay of the jump distributions, integrability conditions on the Lévy measure etc.)

6.1 Lévy processes

In case of the Lévy process the DTC structure coincides with the underlying Lévy process. To determine no change of measure is necessary, so this function represents the joint conditional characteristic function of the log-price and its quadratic variation as given in the risk-neutral measure. Below, are provided the calculations for some popular models.

6.1.1 Black-Scholes model

6.1.2 Jump diffusion models

In their classic works, Merton and Kou (1976, 2002) proposed modeling the log-price dynamics as a finite-activity jump diffusion. The risk-neutral asset dynamics are given by:

| (6.3) |

where is a standard Brownian motion, is a Poisson counter of intensity , and is the jump size distribution. and are assumed to be independent, and the compensator equals For the discounted price to be a true martingale, conditions on the asymptotic behavior of must be imposed (see e.g. Cont and Tankov, 2003). In the Merton model is normally distributed , whereas Kou assumed for it an asymmetrically skewed double-exponential distribution, that is, the density function as given by:

| (6.4) |

for and .

In these models no time change is involved, so coincides with the underlying Lévy process having characteristic triplet . To completely characterize , observe that is just a bivariate compound Poisson process of joint jump density and intensity , whence:

| (6.5) |

where is the joint characteristic function of and . We conclude from (4.4) that has the exponential structure:

| (6.6) |

Now for the Merton model we have

| (6.7) |

and the integral converges for Im. For the Kou model we can write:

| (6.8) |

the characteristic function of the positive and negative parts are:

| (6.9) | ||||

| (6.10) |

which both converge for Im.

6.1.3 Tempered stable Lévy and CGMY

Another way of obtaining Lévy distributions for the asset price is to directly specify an infinite activity Lévy measure . In such a case we have , with being a pure jump Lévy process of Lévy measure . The two instances we analyze here are the tempered stable Lévy process (e.g. Cont and Tankov 2003), and the CGMY (Carr et al. 2002) models. Both of these are obtained as an exponential smoothing of stable distributions; the latter can be viewed as a generalization of the former allowing for an asymmetrical skew between the distribution of positive and negative jumps. The Lévy density for a CGMY process is:

| (6.11) |

which is well defined for all , . When one has the tempered stable process. For simplicity in what follows we assume ; for such values the involved characteristic functions still exist, but lead to particular cases. Since

| (6.12) |

to fully characterize we only need to determine and . Letting , the exponent is given by the standard theory (Cont and Tankov 2003, proposition 4.2) as:

| (6.13) |

Set ; the positive part of is then seen to be:

| (6.14) |

Here is the Euler Gamma function and the confluent hypergeometric function. The multi-strip of convergence of (6.14) is the set . The determination has a similar expression.

6.2 Stochastic volatility and the Heston model

In a stochastic volatility model the asset process is given, in a risk neutral-measure, by the SDE

| (6.15) |

where is some continuous stochastic variance process. By the Dubins and Schwarz’s theorem any continuous martingale can be written as for a certain Brownian motion , which implies that the DTC structure of a stochastic volatility model corresponds to a standard Brownian motion time-changed by as in (3.2). In order to explicitly express the characteristic function we must make a specific choice for the dynamics in (6.15). For instance, we can make the popular choice of selecting a square-root (CIR) equation for the instantaneous variance:

| (6.16) |

for positive constants and a Brownian motion linearly correlated with through a correlation coefficient . For to be well-defined, the parameters , and need to satisfy the Feller condition . The system of SDEs (6.15)-(6.16) is the model by Heston (1993). As we change to the measure , the application of the complex-plane version of Girsanov’s theorem and a simple algebraic manipulation reveals that the leverage-neutral dynamics of are of the same form as (6.16), but with parameters:

| (6.17) |

| (6.18) |

(see also Carr and Wu 2004). Using equation (4.4), we determine as follows666Torricelli (2013) has independently found for the Heston model by augmenting the SDE system (6.15)-(6.16) with the equation , and solved the associated Fourier-transformed parabolic equation via the usual Feynman-Kac argument. As has to be the case, the two approaches coincide.:

| (6.19) |

where indicates the transform with respect to which is well-known analytically (e.g. Dufresne, 2001). The case reverts back to the Black-Scholes model, when (6.19) collapses to (6.2) with .

Other choices for are clearly possible, yielding different stochastic volatility models (the 3/2 model, GARCH, etc.). It is clear from the arguments above that, for an analytical expression for to exist it suffices that the Laplace transform of is known in closed form777See e.g. Lewis 2000, chapter 2, for the Laplace transform of the cited models. and that belongs to a class of models that are stable under the Girsanov transformation.

6.3 DTC jump diffusions

When the underlying Lévy process is represented by a finite activity jump diffusion, operating a decoupled time change amounts to either introducing a stochastic volatility coefficient in the continuous Brownian part, or making the intensity of the compound Poisson process stochastic, or both. Models carrying this structure have been prominently discussed by D.S. Bates (1996) and H. Fang (2000).

6.3.1 Stochastic volatility with jumps

The stochastic volatility model with jumps (SVJ) provides us with a first instance of a decoupled time change not otherwise obtainable as an ordinary time change. The SVJ model is in fact a Lévy decoupled time change with a time-changed continuous part and a time-homogeneous jump part. The dynamics for the asset price are given by the exponential jump diffusion:

| (6.20) |

for some Brownian motion , stochastic variance process , Poisson process and jump size having compensator . The underlying DTC structure of the Bates model is given by with the characteristic triplet for being and taking the form (3.2). By assuming as a jump distribution a normal random variable, and as a variance process the square-root equation:

| (6.21) |

we have the model by Bates (1996). For the discounted asset value to be a martingale, the parameters of the driving stochastic volatility and jump process must be subject to the requirements of both subsection 6.2 and subsection 6.1.2. It is straightforward to see that decomposes into:

| (6.22) |

where and are given respectively by (6.19) and (6.6)-(6.7). Therefore:

| (6.23) |

So far, we have encountered either exponential Lévy models, or exponentially-affine functions arising as solutions of a PDE problem. Here we have a mixture of the two: a time-homogeneous jump factor, modeled as a compound Poisson process, and a continuous diffusion factor, whose characteristic function solves a diffusion problem. The degenerate case , yields a Merton jump diffusion with diffusion coefficient .

6.3.2 Stochastic volatility with jumps and a stochastic jump rate

Another way of obtaining a DTC model is obtained by introducing a stochastic jump frequency into the jump diffusion of the log-price. A jump process with stochastic volatility and stochastic jump rate (SVJSJ) has been suggested and empirically studied by Fang (2000). For a time change , we assume to be a pure jump process of finite activity such that conditionally on , is distributed like a Poisson random variable of parameter , and is independent of every other involved process. We let be another continuous stochastic process; with the remaining notation as in subsection 6.3.1, we define the asset price dynamics as follows:

| (6.24) |

This model has a clear DTC Lévy structure given by , as in (3.2) and (3.3) with , and the characteristic triplet . The model by Fang is obtained by setting:

| (6.25) |

| (6.26) |

As usual we impose ; in contrast, the Brownian motion is assumed to be independent of all the other random variables. If both of the diffusion parameter sets obey Feller’s condition and the density of decays sufficiently fast, is a martingale. Like in the Bates model, the jumps are normally distributed. The function is then given by:

| (6.27) |

Again we recognize that we can decompose , where is the leverage-neutral characteristic function of a Heston process of variance , and that of a compound Poisson process time-changed with , whose argument was computed in subsection 6.1.2. The Laplace transforms of the integrated-square root processes arising from and are known, and the leverage-neutral version of has been given in subsection 6.2. Observe that there is no leverage effect in the jump part because of the assumptions on . Finally, notice that the case reduces to the Bates model with a jump activity rate equal to .

6.4 General exponentially-affine activity rate models

A general theory of affine models for the discounted asset dynamics has been laid out by Duffie et al. (2000), and Filipović (2001), as well as others. We briefly illustrate how this ties in with decouple time-changed processes. Suppose we have a Markov process given by the stochastic differential equation:

| (6.28) |

where is an -dimensional Brownian motion, is an -dimensional pure jump process of intensity and joint jump size distribution on . We fix a discount functional , and assume for the coefficients the following linear structure:

| (6.29) |

For some one-dimensional DTC process , let be the change of measure martingale in (4.3) and assume to be two-dimensional, so that the marginals of represent the instantaneous activity rates and .

The leverage-neutral characteristic function can be recovered as follows. By taking the Ito differential of one sees that is itself a linear jump diffusion; we can thus define the three-dimensional augmented process having some associated extended parameters in (6.29). Furthermore, we can rewrite as:

| (6.30) |

where . Now, according to the results of Duffie et al. (2000), appendix C, under the measure having Radon-Nikodym derivative , we have:

| (6.31) |

for all for which (6.31) is defined, and , following the Riccati system of ODEs888:

| (6.32) | ||||

| (6.33) |

for , with boundary conditions and . By choosing

| (6.34) |

one notices that:

| (6.35) |

The solvability of equations (6.32)-(6.33) is discussed and characterized in Grasselli and Tebaldi (2007). What we have just shown is that the class of the exponentially-affine processes and that of the DTC Lévy processes intersect in the class of the DTC processes whose instantaneous activity rates are given by affine jump diffusions of the form (6.28)-(6.29).

We remark that implicitly defines a price process through the instantaneous activity rates and the change of measure martingale accounting for the dependence structure between the time changes and the underlying Lévy process. The augmented diffusion is an exponentially-affine decoupled time change; all the models reviewed so far fall under this category999A model that can be written in DTC form falling outside this intersection is the linear quadratic-affine model by Santa Clara and Yan, [38]. However, such model does not possess an analytically tractable transform to be used for pricing purposes.. Another example of a model that can be represented in this form is the “double jump model” of Duffie et al. (2000), given by a jump diffusion with stationary jump intensity, whose stochastic volatility is itself a jump diffusion process having the same intensity as the stock.

7 A multifactor DTC jump diffusion

In this section we illustrate a theoretical model in the DTC framework admitting a closed formula for . The price evolution we consider has several attractive features: it is a DTC jump diffusion and therefore allows for the presence of a stochastic jump rate and a stochastic volatility; in addition, both of these processes are given through a multifactor specification. Regarding the correlation modeling, the dynamics we assume carry the usual linear correlation between the stochastic volatility and the Brownian motion driving the stock, as well as a dependence structure between the instantaneous rates of activity. Thus, the hypothesis of a market jump and continuous activity which are correlated with each other finds room in this model.

The case for multifactor volatility has been made by a number of authors. As pointed out by Bergomi 2005, a volatility specification of this kind overcomes the inability of single factor models to fit the current market skew, while at the same time predicting the future evolution of implied volatilities consistently with the historical data, which is of particular relevance in the pricing of certain forward-starting derivatives such as the cliquet option. Furthermore multifactor models make possible a long-term volatility specification that accounts for the slow decay of the autocorrelation function of the variance process (Gallant et al. 2013), as opposed to single factor models, whose autocorrelation function typical decay is exponential.

The price process we analyze links to a modern and currently very active strain of research, which makes use of the so-called Wishart process for financial modeling purposes. The Wishart process is a matrix-valued affine process, studied foremostly by M.F. Bru (1991), that can be thought as a multivariate extension of the CIR process. It has been used to model the driving factors of term structures and price processes by, among the others, da Fonseca et al. (2007, 2008), and Gouriéroux and Sufana (2003, 2010), among the others.

For commuting matrices and in , with invertible and negative definite (to capture mean-reversion), a Wishart process is defined by the following multi-dimensional SDE:

| (7.1) |

The Wishart process is thus a symmetric matrix-valued process. The matrix must satisfy the further constraint for some ; is here an matrix of Brownian motions.

We can use to build a one-dimensional DTC jump diffusion model as follows. We choose and let be a two-dimensional Brownian motion such that for some correlation parameter and is independent of all the other entries of . Let be a finite activity jump process like in subsection 6.3.2, which we further assume it to be independent of both and . As usual, the jump distribution is set to be independent of every other variable. Denoting by the positive-definite matrix square root of , we can define the risk-neutral dynamics of the log-price process as:

| (7.2) |

where equals . The process can be seen to be a local martingale of the form (3.7) by assuming the time changes in proposition 3.3 to be like those in equations (3.2) and (3.3) and letting:

| (7.3) |

where is a Poisson process of intensity 1. Multifactoriality is reflected in the fact that even though each activity rate is specified by a single factor, the correlation between them involves all the three components of . Indeed, let be the scalar Brownian motion driving : it can be proved that

| (7.4) |

Observe that this correlation is stochastic. The correlation between and its instantaneous variance is instead determined by the interplay between and ; we have:

| (7.5) |

By applying the Girsanov’s transformation, we see that the -dynamics of (7.1) are given by the complex-valued Wishart process:

| (7.6) |

where

| (7.7) |

whence:

| (7.8) |

Notably, the Laplace transform for and as in (7.3) can be derived in closed form (see the appendix), since it is a particular case of some well-studied transforms of the Wishart process. In the spirit of the previous section, we remark that when all the Wishart matrices are diagonal, an application of the Lévy theorem shows that this model reduces to a SVJSJ for some appropriate parameter choice (see section 8.2 below).

It is therefore possible to price, and find price sensitivities of, joint price/volatility contingent claims on an asset whose log-price process follows . The model just presented is a particular DTC jump diffusion featuring not only the usual leverage effect between the underlying jump diffusion and the continuous/jump market activity, given by (7.5), but also a correlation structure between the rates of activities themselves, as shown by equation (7.4). For practical financial modeling purposes, we shall see in section 8.2 below that this relationship positively impacts the ability of a jump model of capturing the volatility skew of a traded asset.

This asset pricing model provides an example of how non-trivial DTC modeling (i.e. achieved by using dependent time changes) might work in practice. As a general approach, one could start from a multivariate stochastic process whose integrated marginals have a known joint Laplace transform, and use these as time changes for the continuous and discontinuous parts of some given Lévy process. The underlying Lévy triplet will only appear as an argument of such a transform, and the characteristic function of the process is then completely determined up to a measure change. This and similar models are currently the subject of further research.

8 Numerical testing

8.1 Implementation of the pricing formula

For validation purposes, we numerically implemented equation (5.4) in MATHEMATICA® for various models and payoffs, and compared the analytical prices so obtained to a MATLAB® simulation following an Euler scheme. The results confirm the consistence of the pricing formula with the risk-neutral valuation theory.

We analyzed three different contingent claims: one on , one on , and one joint derivative on and . Namely, we accounted for three different kinds of options: a vanilla call option, a call option on the realized volatility, and a call TVO.

For a plain call option of maturity and strike , the function and its Fourier transform to be used in (5.4) are:

| (8.1) |

the function exists and is analytic for Im.

A possible volatility investment is to write a call option using as an underlying the total realized volatility of an asset, or to buy a call option directly on a volatility index such as the VIX. Hence, we would like to price the contingent claim paying at time for some strike realized volatility level . In our equation we would then need to take:

| (8.2) |

the Fourier transform here is well-defined and holomorphic in Im.

The target volatility option mentioned in the introduction is a natural candidate for testing mixed-claim structures, being an instance of a currently traded joint asset/volatility derivative. The payoff function and the Fourier transform for a call TVO of strike , maturing at with target volatility are:

| (8.3) |

Observe that, unlike the previous contracts, the payoff of a TVO shows explicit dependence on the expiry . The domain of holomorphy of is the strip .

We numerically tested these derivatives using five different stochastic models for the underlying asset processes: namely, the Black-Scholes, Heston, Merton, Bates and Fang models. All the prices have been produced with a single implementation of (5.4) with given by (6.27). All we had to do is changing/voiding the relevant parameters, and replacing the module for whenever we switched payoff. The parameter estimates have been taken from Fang’s fitting of the S&P 500 index, and are illustrated in table 1. Tables 2 to 6 summarize the result obtained for five different sets of observable market conditions and contract parameters . For each given , the maturity is the same for all the three options considered; a TVO is always compared to a vanilla call having same strike, and the target volatility is set to be constant across all the data sets.

We simulated 100.000 paths of step size . The figures show a good overall match between the analytical value (AV) and the Monte Carlo value (MC); the relative error AVMC/MC is shown in parentheses. For the call option on the volatility in some cases we almost attain four-digit precision. On the other hand, for some models and data sets the integrands for the TVO valuation remain highly oscillatory around the maximum integration range; when this occurs, a certain loss of accuracy is observed.

8.2 Leverage sensitivity of the model of section 7

In this section we try to provide further financial motivation for the model with correlated stochastic volatility and jump rate (CSVJA) of section 7 through a numerical exercise. Specifically, in what follows we analyze the sensitivity of the volatility skew of the Bates, Fang and CSVJA models with respect to variations in the “leverage parameter” . We define in this section as being the constant value giving the instantaneous correlation between the Brownian components of the stochastic variance and that of the log-returns of the accounted models.

Preliminarily, let us assume the following form for the matrices in the equations of section 7:

| (8.4) |

The jumps are assumed to be normally distributed with mean and variance . As already mentioned in section 6, an application of the Lévy theorem shows that when the parametrization above is equivalent to a Fang model with:

| (8.5) |

Clearly, by further assuming one recovers the Bates model. The example in (8.4) is then “minimal” in the sense that it represents the slightest possible modification of certain known models attaining a true CSVJA specification. We set the parameters in (8.4) as follows:

| (8.6) |

The market parameters have been chosen as and . According to the remarks above, by voiding the relevant matrix entries, we can use (8.6) to specify one instantiation each of the Bates, Fang and CSVJA models.

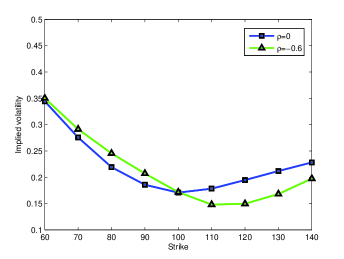

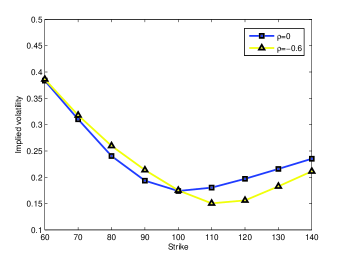

In figures 1 and 2 we show the 3-month volatility skew extracted from the call option prices generated by (5.1), respectively for the Fang and Bates model. The two curves correspond to a value of given respectively by and . As we can see, the skew is only marginally affected by the variation of the leverage parameter. We emphasize that, consistently with the standard representations given in section 6, a direct check confirms that we have here no correlation between the activity rates, that is, if then (7.4) vanishes.

The lack of sensitivity of the skew with respect to in jump models is a well understood fact. The reason is that for such a class of models the short term dynamics of the surface are generally handled by the jump parameters which unlike the leverage value, do not retain a clear economic interpretation. This is normally regarded as a shortcoming of the jump models, since an improvement in the short term smile fit is achieved at a cost of a loss of sensitivity with respect to the calibrated parameters, which can be problematic for e.g. skew hedging purposes. For a full discussion, see da Fonseca and Grasselli (2011).

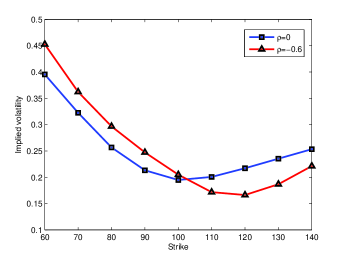

Interestingly, if we perform the same analysis for the full CSVJA parametrization (figure 3) we instead notice a considerable variation of the volatility skew when leverage is introduced. In particular, we see that when , which in this case is given by equation (7.5), is nonzero, the short term smile is much more negatively skewed than in the uncorrelated cases. Since we are exactly in the same situation as in the Fang model in terms of marginal distributions of the driving factors and values of , such an increased sensitivity of the skew can only be due to the correlation between the activity rates established when letting . The effect of this “second” correlation on the skew can be intuitively explained as follows. Because of the leverage effect, as prices go down the volatility spikes up, generating negative skewness in the returns distribution. But now the volatility is correlated with the jump activity; in particular, we see from (7.4) that this is most likely going to be a positive correlation. The reason for this is that the sign of (7.4) depends only on the sign of , which is a mean reverting process with a positive mean reversion level. Therefore, when the volatility increases, the jump intensity is likely to increases as well, and hence so does the probability of observing a (negative on average) jump. The latter contributes to the negative skewness of the asset returns and thus reinforces the negative skew of the volatility smile.

The test conducted reveals a very useful property of a DTC Lévy jump model of CSVJA type. As opposed to the standard jump models with independent activities, the underlying dynamics introduced are able to adequately match the convexity of a steep volatility skew without having to surrender the overall control on the surface of the correlation parameter . Unlike the traditional jump models, changes in the short term part of the surface can be achieved not only by a change in the distribution of the jump part, but also by varying a correlation parameter, much like what happens in a purely diffusive model. The ability of the surface to promptly respond to variations of financially meaningful variables is a property greatly appreciated by the practitioners; in this respect the CSVJA model may improve the jump asset modeling literature. An empirical study on this model is matter of ongoing research.

9 Conclusions

In this paper we have suggested a theoretical pricing framework that can easily be made to represent popular settings, but whose full model and payoff generalities were not possible by using the previous theory. We achieved this by introducing the concept of decoupled time change and by considering payoffs on an asset and its accrued volatility as the default target claims to be priced.

DTC processes provide a common time-changed representation for many models from the extant literature, and help to capture possible dependence relationships between the continuous and the jump market activities. We obtained martingale relations for stochastic exponentials of DTC Lévy processes, based on which we defined an asset price’s dynamics. We then linked the joint characteristic function of the log-price dynamics and the quadratic variation to the joint Laplace transform of the time changes. As a by-product, we extended the measure change technique of Carr and Wu (2004) to the class of DTC Lévy processes. In the DTC setup, we rigorously posed and solved the valuation problem of a derivative paying off on an asset and its realized volatility, by means of an inverse-Fourier integral relation that extends previously known formulae.

Several stochastic models and contingent claims have been analyzed. In all the accounted cases we outlined the underlying DTC structure and found the leverage-neutral characteristic function. In particular, the SVJ and SVJSJ models were shown to have their own time-changed Lévy structure. Furthermore, we have introduced a novel DTC Lévy theoretical model which illustrates how equity modeling could benefit from the idea of decoupled time changes.

For numerical comparison and validation purposes, we focused on specific instances from the three payoff classes allowed by our equation: plain vanilla claims, volatility claims, and joint asset/volatility claims. The results confirm the validity of our method. From a computational standpoint, a single software implementation can output prices for several different combinations of models and payoffs. Finally, we have presented some initial evidence that a model with correlation between the activity rates potentially allows a better management of the volatility skew compared to other jump models.

Appendix: proofs

We begin by recalling some basic definitions from the semimartingale representation theory; in particular, we refer to Jacod and Shiryaev (1987), chapters 2 and 3, and Jacod (1979), chapitre X.

We define the Doléans-Dade exponential of an -dimensional semimartingale starting at 0 as:

| (9.1) |

where denotes the continuous part of and the infinite product converges uniformly. This is known to be the solution of the SDE , .

Let be a truncation function and be a triplet of predictable processes that are well-behaved in the sense of Jacod and Shiryaev (1987), chapter 2, equations (2.12)-(2.14). For , associate with the following complex-valued functional:

| (9.2) |

This functional is well-defined on:

| (9.3) |

and because of the assumptions made it is also predictable and of finite variation.

Let be an -dimensional semimartingale. The local characteristics of are the unique predictable processes as above, such that and is a local martingale for all . The process in (9.2) arising from the local characteristics of is called the cumulant process of , and it is independent of the choice of . It is clear that the local characteristics of a Lévy process of Lévy triplet are .

If is a Borel space, the time change of a random measure on the product measure space according to some time change , is the random measure:

| (9.4) |

for , and all sets . A random measure is -adapted if for all and holds . This is equivalent to say that for each measurable random function , the integral of with respect to is -continuous (see Jacod 1979, chapitre X); conversely, if is a pure jump process that is -continuous, then its associated jump measure is -adapted (Kallsen and Shiryaev 2002, proof of lemma 2.7).

A semimartingale is said to be quasi-left-continuous if its local characteristic is such that for all , Borel sets in , and . Essentially, quasi-left-continuity means that the discontinuities of the process cannot occur at fixed times.

The following theorem clarifies the importance of continuity/adaptedness under time changing, i.e. that stochastic integration and integration with respect to a random measure “commute” with the time changing operation.

Theorem A.

Let be a time change with respect to some filtration .

-

(i)

Let be a -continuous semimartingale. For all -predictable integrands , we have that is -predictable, and:

(9.5) -

(ii)

Let be a -adapted random measure on . For all measurable random functions and it is:

(9.6)

Proof.

See Jacod (1979), théorème 10.19, (a), for part (i), and théorème 10.27, (a), for part (ii). ∎∎

In particular, from part (ii) of theorem A follows that if is a pure jump proces with associated jump measure adapted to some time change , then the time-changed process has associated jump measure .

It is essentially a consequence of theorem A that under the assumption of continuity with respect to , the local characteristics of a time-changed semimartingale are well-behaved, in the sense of the next theorem.

Theorem B.

Let be a semimartingale having local characteristics and cumulant process with domain , and let be a time change such that is -continuous. Then the time-changed semimartingale has local characteristics and the cumulant process equals , for all .

Proof.

See Kallsen and Shiryaev (2002), lemma 2.7. ∎∎

Proof of proposition 3.3.

Let and be the Lévy triplets of and . Because of the and -continuity assumption, we can apply theorem B and we immediately see that the local characteristics of and are respectively and . By a result on the linear transformation of semimartingales, such two sets of local characteristics are additive (in Eberlein et al. (2009), proposition 2.4, take to be the juxtaposition of two identity blocks and ), so that has local characteristics101010The process is a particular instance of an Ito semimartingale: see Jacod and Protter (2003).

Let be the cumulant process of ; by definition the exponential is well-defined if and only if . But now the fact that and are continuous implies that is quasi-left-continuous (Jacod and Shiryaev 1987, chapter 2, proposition 2.9), that in turn is sufficient for to be continuous (Jacod and Shiryaev 1987, chapter 3, theorem 7.4). Therefore, since is of finite variation, we have that ; in particular, this means that never vanishes. By definition of the local characteristics, we then have that is a local martingale for all , and thus it is a martingale if and only if . ∎∎

Proof of proposition 4.1.

An immediate consequence of theorem B is that, under the present assumptions, the class of continuous and pure jump martingales are closed under time changing, so that orthogonality follows. Therefore:

| (9.7) |

The equation can be established by the application of Dubins and Schwarz theorem. Regarding the discontinuous part, we notice that if is the jump measure associated to we have that is -adapted because is -continuous. Hence, the application of theorem A, part (ii), yields:

| (9.8) |

∎∎

Counterexample to proposition 4.1.

Let be a standard Brownian motion, and let be an inverse Gaussian subordinator with parameters and , independent of . The process is a normal inverse Gaussian process of parameters and is a pure jump process (Barndorff-Nielsen 1997). Therefore by letting and we have so that orthogonality does not hold; moreover while the left hand side of (4.1) equals . ∎∎

Proof of proposition 4.2.

Since and are of finite variation, the total realized variance of an asset as in (3.7) satisfies , so that by proposition 4.1 we have:

| (9.9) |

The application of proposition 3.3 to guarantees that the process in (4.3) is a martingale for all such that . By using relation (9.9) and operating the change of measure entailed by (4.3) we have:

To fully characterize all that is left is expressing in terms of . Since

| (9.10) |

we have that:

| (9.11) |

which completes the proof. ∎∎

Proof of proposition 5.1.

We follow the proof Lewis (2001), theorem 3.2, lemma 3.3 and theorem 3.4. By writing the expectation as an inverse-Fourier integral (which can be done by the assumptions on and because is a characteristic function) and passing the expectation under the integration sign we have:

| (9.12) |

All that remains to be proven is that Fubini’s theorem application is justified. Let be the discounted, normalized log-price; define the probability transition densities , and let be their characteristic functions. For all we have:

| (9.13) |

For , , set . We see that the integrand in the right-hand side of (Proof of proposition 5.1.) equals . But now is because is Fourier-integrable in (for take ); similarly, is because of the assumption on . Therefore, the application of Parseval’s formula yields:

| (9.14) |

since .

∎

Proof of the equations of section 7.

We can endow with a correlation structure as follows. Let be a two-dimensional matrix Brownian motion independent of . The matrix process:

| (9.15) |

is also a matrix Brownian motion enjoying the property that and is independent of for . Since , we have that is indeed a Brownian motion and the activity rates are connected through the element .

To verify equations (7.4) and (7.5), observe that for there exist some bounded variation processes such that

| (9.16) |

from which:

| (9.17) |

By taking the quadratic variation of the right-hand side we see that are two Brownian motions such that ; equations (7.4) and (7.5) then follow from a direct computation.

Since is orthogonal to every entry of the matrix Brownian motion , the change in the dynamics of under is only due to the correlation between and . Hence, for , the Radon-Nikodym derivative to be considered in (4.3) reduces to

| (9.18) |

Furthermore, for we have:

| (9.19) | ||||

| (9.20) |

so that application of Girsanov’s theorem tells us that

| (9.21) |

is a -matrix Brownian motion. Solving the above for and substituting in (7.1) yields (7.6). Equation (7.8) then follows from (4.4).

Finally, we give the formula for . For and consider the transform:

| (9.22) |

for every vector of complex numbers such that the above expectation is finite. The function is exponentially-affine of the form

| (9.23) |

since it is a particular case of the transforms studied in e.g. Grasselli and Tebaldi (2007), and Gouriéroux (2003). The ODEs for are given by:

| (9.24) |

| (9.25) |

Here is the diagonal matrix having the values on the diagonal. The solution of (9.24)-(9.25) is obtainable through a linearization procedure that entails doubling the dimension of the problem, which yields:

| (9.26) |

| (9.27) |

| (9.28) |

(see for example Gouriéroux 2003, proposition 7, or Grasselli and Tebaldi 2007, section 3.4.2). The formula for follows from (9.26)- (9.28) when we choose , in (9.22), and set , in (9.23). ∎∎

References

- [1] Ane, T. & Geman, H. (2000). Order Flow, Transaction Clock, and Normality of Asset Returns. The Journal of Finance, 55, 2259–2284.

- [2] Bates, D.S. (1996). Jumps and Stochastic Volatility: Exchange Rate Processes Implicit in Deutsche Mark Options. Review of Financial Studies, 9, 69–107.

- [3] Bergomi, L. (2005). Simle Dynamics I & II. Risk, 94.

- [4] Barndorff-Nielsen, O.E. (1997). Processes of normal inverse Gaussian type. Finance and Stochastics, 2, 41–68.

- [5] Bru, M.F. (1991). Wishart processes. Journal of Theoretical Probability, 4, 725–743.

- [6] Carr, P. & Madan, D.B. (1999). Option valuation using the fast Fourier transform. Journal of Computational Finance, 2, 61–73.

- [7] Carr P. & Sun, J. (2007). A New Approach for Option Pricing Under Stochastic Volatility. Review of Derivatives Research, 10, 87–150.

- [8] Carr, P., Geman H., Madan, D.B., Yor, M. (2002). The Fine Structure of Asset Returns: An Empirical Investigation. Journal of Business, 75, 305–332.

- [9] Carr, P. & Wu, L. (2004). Time-changed Lévy processes and option pricing. Journal of Financial Economics, 71, 113–41.

- [10] Clark, P.K. (1973). A Subordinated Stochastic Process Model with Finite Variance for Speculative Prices. Econometrica, 41, 135–155.

- [11] Cont, R. & Tankov, P. (2003). Financial Modelling With Jump Processes. Chapman and Hall / CRC Press, London.

- [12] da Fonseca, J. & Grasselli, M. (2011). Riding on the smiles, Quantitative Finance, 11(11), 1609–1632.

- [13] da Fonseca, J., Grasselli, M., Tebaldi, C. (2008). A multifactor Heston volatility model. Quantitative Finance, 8, 591–604.

- [14] da Fonseca, J., Grasselli, M., Tebaldi, C. (2007). Option pricing when correlation are stochastic: an analytical model. Review of Derivatives Research, 2, 151–180.

- [15] Di Graziano, G. & Torricelli, L. (2012). Target Volatility Option Pricing. International Journal of Theoretical and Applied Finance, 15(1).

- [16] Duffie, D., Pan,J., E., Singleton, K. (2000). Transform analysis and asset pricing for affine jump diffusions. Econometrica, 68, 1343–1376.

- [17] Dufresne, D. (2001). The Integrated Square-Root Process. University of Montreal Research Paper, 90.

- [18] Eberlein,E., Papapantoleon, A., Shiryaev, A.N. (2009). Esscher transforms and the duality principle for multidimensional semimartingales. The Annals of Applied Probability, 19, 1944–1971.

- [19] Fang, H. (2000). Option Pricing Implications of a Stochastic Jump Rate. University of Virginia Working Paper.

- [20] Filipović, D. (2001). A general characterization of one factor affine term structure models. Finance and Stochastics, 5, 389–412

- [21] Gallant, A.R., Hsu, C.T., Tauchen, G. (2013). Using Daily Range Data To Calibrate Volatility Diffusions And Extract The Forward Integrated Variance. The Review of Economics and Statistics, 81, 617–631.

- [22] Grasselli, M. & Tebaldi, C. (2007). Solvable Affine Term Structure Models. Mathematical Finance, 18, 135–153.

- [23] Gouriéroux, C. (2003). Continuous Time Wishart process for stochastic risk.. Econometric Review, 25, 177–217.

- [24] Gouriéroux, C. & Sufana, R. (2003). Wishart quadratic term structure models. CREF 03-10, HEC Montreal.

- [25] Gouriéroux, C. & Sufana, R. (2010). Derivative Pricing With Wishart Multivariate Stochastic Volatility. Journal of Business and Economic Statistics, 3, 438–451.

- [26] Huang, J. & Wu, L. (2004). Specification Analysis of Option Pricing Models Based on Time-Changed Lévy Processes. The Journal of Finance, 59, 1405–1440.

- [27] Heston, S.L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6, 327–343.

- [28] Jacod, J. (1979). Calcul Stochastique et Problèmes de Martingales. Lecture Notes in Mathematics, Springer, Berlin.

- [29] Jacod, J. & Protter, P. (2011). Discretization of Processes. Stochastic Modelling and Applied Probability, Springer, Berlin.

- [30] Jacod, J. & Shiryaev, A.N. (1987). Limit Theorems for Stochastic Processes. Grundlehren der Mathematischen Wissenschaften, 288, Springer, Berlin.

- [31] Kallsen, J. & Shiryaev, A.N. (2002). Time change representation of stochastic integrals. Theory of Probability and its Applications, 46, 522–528.

- [32] Karatzas, I. & Shreve, S.E. (2000). Brownian Motion and Stochastic Calculus. Springer, Berlin.

- [33] Kou, S.G. (2002). A Jump-Diffusion Model for Option Pricing. Management Science, 48, 1086–1101.

- [34] Lewis, A. (2000). Option Valuation under Stochastic Volatility. Finance Press.

- [35] Lewis, A. (2001). A simple Option Formula For General Jump-Diffusion And Other Exponential Lévy Processes. OptionCity.net Publications.

- [36] Merton, S.C. (1976). Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics, 3, 125–144.

- [37] Monroe, I. (1978). Processes that can be embedded in Brownian motions. The Annals of Probability, 6, 42–56.

- [38] P. Santa Clara & S. Yan (2010). Crashes, Volatility, and the equity premium: lessons from S & P 500 options, The Review of Economics and Statistics, 92, 435–451.

- [39] Sin, C.A. (1998). Complications with Stochastic Volatility Models. Advances in Applied Probability, 30, 256–268.

- [40] Torricelli, L. (2013). Pricing joint claims on an asset and its realized variance in stochastic volatility models. International Journal of Theoretical and Applied Finance, 16(1).

- [41] W., Zheng & L.K. Kwok (2014). Closed Form Pricing Formulas for Discretely Sampled Generalized Variance Swaps. Mathematical Finance, 24(4), 855–881.

Tables and figures

| Parameters | Black-Scholes | Heston | Merton | Bates | Fang |

|---|---|---|---|---|---|

| 0.14 | 0.15 | 0.12 | 0.15 | 0.14 | |

| 4.57 | 8.93 | 6.5 | |||

| 0.0306 | 0.0167 | 0.0104 | |||

| 0.48 | 0.22 | 0.2 | |||

| -0.82 | -0.58 | -0.48 | |||

| 1.42 | 0.39 | 0.41 | |||

| 0.0894 | 0.1049 | 0.2168 | |||

| -0.075 | -0.11 | -0.21 | |||

| 5.06 | |||||

| 0.13 | |||||

| 1.069 |

| Model | Vanilla Call | Volatility Call | TVO Call | |||

|---|---|---|---|---|---|---|

| AV | MC | AV | MC | AV | MC | |

| B-S | 24.7627 | 24.7775(0.05%) | 0.0847 | 0.0848(0.12%) | 17.5441 | 17.6982(0.87%) |

| Heston | 25.3893 | 25.3710(0.07%) | 0.1088 | 0.1084(0.37%) | 17.2248 | 17.6044(2.16%) |

| Merton | 25.3243 | 25.2290(0.38%) | 0.1192 | 0.1194(0.17%) | 17.7529 | 17.7922(0.22%) |

| Bates | 25.1166 | 25.0889(0.11%) | 0.1002 | 0.1005(0.30%) | 18.5980 | 18.7480(0.80%) |

| Fang | 25.5686 | 25.6508(0.32%) | 0.0907 | 0.0892(1.68%) | 24.0494 | 24.0764(0.11%) |

| Model | Vanilla Call | Volatility Call | TVO Call | |||

|---|---|---|---|---|---|---|

| AV | MC | AV | MC | AV | MC | |

| B-S | 8.4801 | 8.4784(0.02%) | 0.1672 | 0.1695(1.36%) | 5.7622 | 5.6957(1.17%) |

| Heston | 10.3063 | 10.3023(0.04%) | 0.2167 | 0.2172(0.23%) | 6.3815 | 6.7080(4.87%) |

| Merton | 11.5845 | 11.5713(0.11%) | 0.2357 | 0.2356(0.04%) | 7.4564 | 7.4239(0.44%) |

| Bates | 9.8607 | 9.8371(0.24%) | 0.2002 | 0.2001(0.05%) | 6.8180 | 6.9085(1.31%) |

| Fang | 8.8630 | 8.8737(0.12%) | 0.1827 | 0.1828(0.05%) | 7.4173 | 7.5046(1.16%) |

| Model | Vanilla Call | Volatility Call | TVO Call | |||

|---|---|---|---|---|---|---|

| AV | MC | AV | MC | AV | MC | |

| B-S | 3.7627 | 3.7346(1.02%) | 0.2300 | 0.2305(0.22%) | 0.9771 | 0.9437(3.54%) |

| Heston | 4.1390 | 4.1304(0.21%) | 0.2318 | 0.2320(0.09%) | 1.0480 | 1.0451(0.28%) |

| Merton | 4.4169 | 4.4435(0.60%) | 0.2348 | 0.2343(0.21%) | 1.1254 | 1.1235(0.17%) |

| Bates | 4.1842 | 4.1687(0.37%) | 0.2327 | 0.2328(0.04%) | 1.0593 | 1.0544(0.46%) |

| Fang | 4.3219 | 4.3420(0.46%) | 0.2362 | 0.2362(0.00%) | 1.0919 | 1.0987(0.62%) |

| Model | Vanilla Call | Volatility Call | TVO Call | |||

|---|---|---|---|---|---|---|

| AV | MC | AV | MC | AV | MC | |

| B-S | 42.6506 | 42.6452(0.01%) | 0.2670 | 0.2665(0.19%) | 19.7252 | 19.9181(0.96%) |

| Heston | 42.9595 | 43.0010(0.10%) | 0.2859 | 0.2858(0.03%) | 19.8454 | 19.6512(0.99%) |

| Merton | 42.8984 | 42.8580(0.09%) | 0.2955 | 0.2954(0.03%) | 19.4192 | 19.3975(0.11%) |

| Bates | 42.7768 | 42.7928(0.04%) | 0.2804 | 0.2802(0.07%) | 19.8042 | 19.8318(0.14%) |

| Fang | 43.0039 | 43.0252(0.05%) | 0.2793 | 0.2791(0.07%) | 20.5992 | 20.5998(0.01%) |

| Model | Vanilla Call | Volatility Call | TVO Call | |||

|---|---|---|---|---|---|---|

| AV | MC | AV | MC | AV | MC | |

| B-S | 2.3393 | 2.3080(1.36%) | 0.1590 | 0.1588(0.13%) | 1.9535 | 1.8622(4.90%) |

| Heston | 2.5098 | 2.5071(0.11%) | 0.1852 | 0.1862(0.54%) | 2.2190 | 2.1317(4.10%) |

| Merton | 3.7078 | 3.6843(0.64%) | 0.1983 | 0.1981(0.10%) | 3.0330 | 3.0165(0.55%) |

| Bates | 2.7416 | 2.7380(0.13%) | 0.1767 | 0.1769(0.11%) | 2.3727 | 2.3798(0.30%) |

| Fang | 1.9814 | 1.9410(2.08%) | 0.1664 | 0.1668(0.24%) | 1.9453 | 1.9167(1.49%) |