Analysis of short term price trends in daily stock-market index data

Abstract

In financial time series there are periods in which the value increases or decreases monotonically. We call those periods elemental trends and study the probability distribution of their duration for the indices DJIA, NASDAQ and IPC. It is found that the trend duration distribution often differs from the one expected under no memory. The expected and observed distributions are compared by means of the Anderson-Darling test.

pacs:

02.50.-r 02.50.Ey 89.65.GhI Introduction

One of the goals of financial-market analysis is to predict the future movements of prices and financial indices. In order to achieve this goal, a huge variety of methods to forecast markets behavior were developed, ranging from complex mathematical models even to astrological pseudo-scientific techniques. An approach that has been recently growing in popularity is the statistical analysis of large sets of data, which has become now possible due to the increasing availability of computer power and high quality data sets. This approach has benefited from the contributions not only from economists, but also from many physicists and mathematicians who have applied methods and ideas of probability theory and statistical physics to finance. A set of nontrivial statistical properties of historical data was observed and classified as “stylized facts” Rama , which are expected to provide a better insight on market structure and behavior.

When observing the time series of the prices of an asset on a chart, it is common to see “trends” in which most of the values are greater (or smaller) than the previous ones. These trends are very popular within the so-called technical analysis. Trends as those studied by technical analysis can be seen as composed by smaller elemental trends, periods in which the value increases or decreases monotonically. These kind of trends are the ones that will be studied in the present work. Among other things, technical analysts seek patterns in the charts of financial data, that are believed to be indicators of changes in the trend direction. The effectiveness of technical analysis is disputed and put at a stake by what is known as the Efficient Market Hypothesis (EMH). Before going further, it is necessary to give some definitions. In Subsections I.1, I.2 and I.3 of this introduction these definitions and other useful information will be presented. In Section II, a model for the distribution of trends durations will be developed from the EMH. Section III will explain how the data were analyzed and section IV will provide an interpretation of the analysis.

I.1 Definitions

Let be the price of an asset or an index value at time and its logarithm. The log-return at time is defined as:

| (1) |

for a given time sampling scale . If the price variation is small, the log-return is a good approximation of the return

| (2) |

In this paper, we consider equal to 1 trading day and we use the daily close values of the indices to build the series . More details on the data sets will be given in section III.

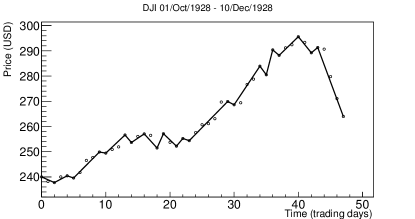

An elemental trend of duration will be defined here as a subseries of values within the series in which every value is greater (for an uptrend) or smaller or equal (for a downtrend) than the preceding one (Figure 1). The aim of this work is to study with a statistical approach the kind of short term trends defined above.

I.2 The Efficient Market Hypothesis

The EMH claims that the market quickly finds the rational price for a traded asset Mantegna . The most important consequence of this hypothesis was shown by P. Samuelson Samuelson 2 and it is the fact that the best forecast for the future price of an asset is its present price.

| (3) |

where is the conditional expectation with respect to the filtration , namely with respect to the known history up to time . Indeed, it is easy to derive the EMH from a simple no-arbitrage argument. Suppose we have two assets, a risky one, with price and a risk-free one giving a constant interest rate . To avoid arbitrage, one has to require that the expected return of the risky asset is equal to the risk-free interes rate, that is

| (4) |

the latter equation immediately yields, for non vanishing ,

| (5) |

which reduces to (3) for . Equations (3) and (5), jointly with the integrability of the process , are known as martingale and sub-martingale (remember that ) conditions, respectively.

The EMH would invalidate the attempts of technical analysis to predict future prices or trends; in fact, in Samuelson’s words, “there is no way of making an expected profit by extrapolating past changes in the futures price, by chart or any esoteric devices of magic or mathematics” Samuelson 2 as the best forecast of the future price would be the current price.

I.3 Stylized facts

As mentioned before, financial time series share some nontrivial statistical properties called stylized facts. Although those properties are often formulated qualitatively, they are so constraining that it is difficult to reproduce all of them by means of a stochastic process Rama . As a matter of fact, none of the market models, including analytical models, Monte Carlo simulations and multi-agent based models, created before 1990, when awareness of such regularities gradually started to appear, could reproduce all of these stylized facts Lux . As an interesting issue, some studies suggest that stylized facts appear not only in financial time series, but also in other complex systems such as Conway’s Game of Life Hernandez . To fix the ideas, some of the stylized facts, taken from reference Rama , are listed below:

- Absence of linear autocorrelations:

-

Autocorrelations of returns are often negligible, except for very small time scales, depending on the market and on the time horizon.

- Heavy tails:

-

The return distribution is leptokurtic and some authors claim that the tails decay as a power-law.

- Gain-loss asymmetry:

-

Large downward jumps in stock prices and stock index values are observed, but not equally large upward movements. (In exchange rates there is a higher symmetry in up/down movements).

- Volatility clustering:

-

High volatility events do cluster in time.

II An ‘Efficient Market’ model for the duration distribution

Among all the possible martingale or sub-martingale models that can describe price fluctuations, the geometric random walk is the simplest one. A geometric random walk is just a product of independent and identically distributed positive random variables. If the expected value of these variables is , then the geometric random walk is a martingale; otherwise, if the expected value is larger than , the geometric random walk is a submartingale. However, the geometric random walk hypothesis is neither necessary nor sufficient for an efficient market, as shown by many authors among whom Leroy leroy , Lucas lucas and Lo and Mckinlay lo . To understand this point, it is enough to consider Equation (5) allowing for any martingale model.

At each step of a series of index values, there are two possible outcomes: the index either increases or does not increase. In an efficient market, the expected future price depends only on information about the current price, not on its previous history. Therefore, it should be impossible to predict the expected direction of a future price change given the history of the price process. In formula, from Equation (3) (after discounting for the risk-free rate), we have

| (6) |

if we consider the sign of the price change , which coincides with the sign of returns, we accordingly have

| (7) |

If the price follows a geometric random walk, then the series of price-change signs can be modeled as a Bernoulli process. This process could be biased to take the presence of a risk free interest rate into account. To be more specific, let us consider a log-normal geometric random walk and let us use the assumption . Let be the initial price. The price at time will be given by

| (8) |

where are independent and identically distributed random variables following a log-normal distribution with parameters and . These two parameters come from the corresponding normal distribution for log-returns. As a direct consequence of the EMH in the form (5), we have

| (9) |

and for a log-normal distributed random variable, we have also

| (10) |

This leads to a dependence between the two parameters

| (11) |

Note that, when , it is impossible to get . This reflects a more general result, if the price process is a martingale, the log-price process cannot be a martingale and viceversa. Starting from the cumulative distribution function for a log-normal random variable

| (12) |

the probability of a negative sign would be given by

| (13) |

which yields for .

It becomes natural to use the biased Bernoulli process as the null hypothesis for the time series of signs scalasold . It is well known that the distribution of the number of failures needed to get one success for a Bernoulli process with success probability is the geometric distribution ; the number of failures is given by

| (14) |

The duration of an elemental downward trend is the number of days before the price increases, so the distribution of such trend durations should follow a geometric distribution. An identical argument applies to the duration of an upward trend. Such sequences of identical outcomes are also known as runs or clumps in the mathematical literature.

III Methodology

III.1 Data

Three indices were analyzed, namely Dow Jones Industrial Average (DJIA), NASDAQ Composite and the Mexican Índice de Precios y Cotizaciones (IPC) during the periods 1 October 1928 - 7 July 2011, 5 February 1971 - 30 September 2011 and 30 October 1978 - 7 April 2011, respectively. The data were taken from Yahoo Finance.

III.2 Price and time scales

The prices were expressed in terms of “constant money” using the consumer price indices from references cpi and inpc . Since the values of those indices were delivered monthly, linear interpolation was used in order to express the daily values. The time was measured in trading days as discussed above.

III.3 Building the sample

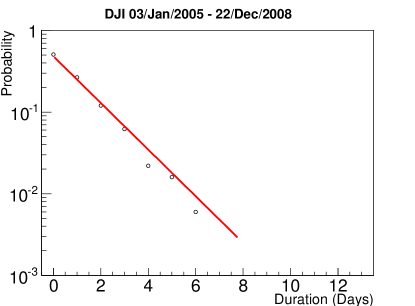

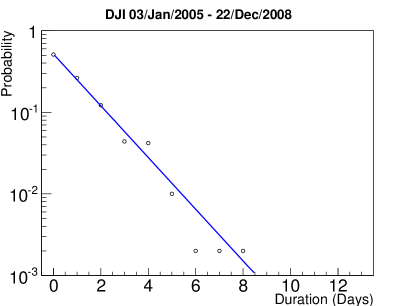

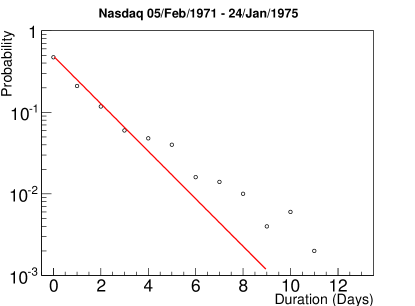

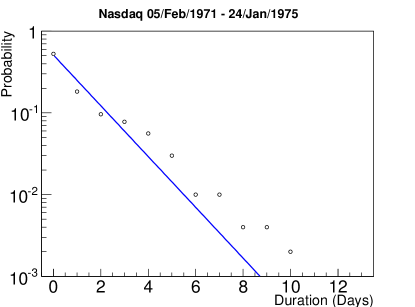

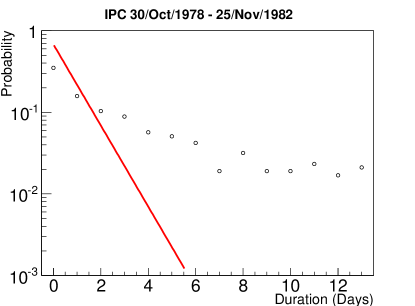

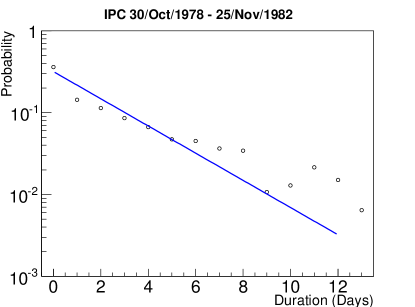

For each series of index values, several time windows of 1000 trading days were created, each one shifted forward by one trading day with respect to the previous one. This procedure resulted in 20785 time windows for the DJIA, 10282 for the NASDAQ and 4997 for the IPC. Two histograms were built for each time window, one for upward trends and the other one for downward trends. For upward trends, 500 points within each time window were selected at random, and the number of days before the first time decrease were measured. Such waiting times were the entries for each histogram. For instance, given the sequence , assume that the fourth entry is randomly chosen. Then the recorded waiting time is 4. The histograms for downward trends were built in the same way. Finally, all the histograms were normalized. Examples of both uptrend and downtrend histograms for different time windows are shown in Figure 3.

III.4 The Anderson-Darling goodness of fit test

In order to compare the observed and expected distributions of trend durations, the Anderson-Darling test described in references Anderson ; Choulakian was used. The Anderson-Darling test was found to be the most suitable for this purpose because it places more weight on the tails of a distribution than other goodness of fit tests. The critical values of the Anderson-Darling statistic were dependent on the parameter of the geometric distribution, and they were estimated using Monte Carlo simulations.

IV Discussion

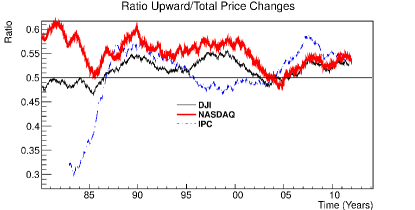

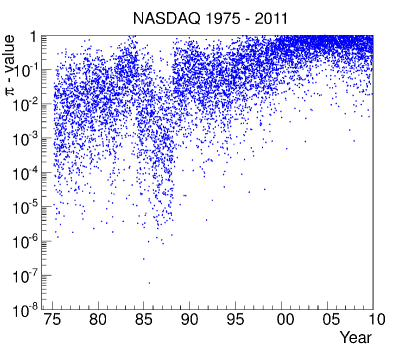

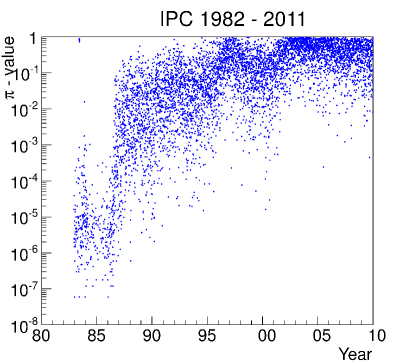

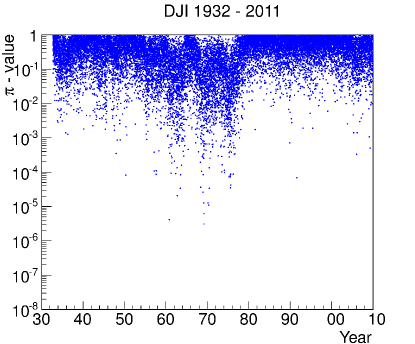

In Figure 2, the ratio of the upward to total price changes in daily data is plotted against time for the years 1980 - 2011. This ratio is calculated over a time window of 1000 trading days. It can be seen that variations are greater than those expected for the same time windows in a Bernoulli process with parameter (), but it might be interesting to find out whether the hypothesis of a geometric distribution holds for smaller periods (such as each of the 1000 days time windows individually), because it would mean that in those periods the direction of price changes was not predictable using historical prices of the index. Figure 3 show the distribution of trend durations corresponding to different indices and periods of 1000 days. Figure 4 displays the -values of the Anderson-Darling statistic for different periods. In order to avoid confusion between the parameter of the geometric distribution and the -values for the distribution of , the latter will be referred to as -values. The meaning of -values is the probability of obtaining a value of at least as big as the one that was really obtained, given that the probability distribution is actually geometric.

It was observed that as time passes, the direction of price changes for the IPC and the Nasdaq is better described by a geometric distribution (Figure 4). The distribution of trend durations for the Dow Jones is generally reasonably well fitted by the geometric distribution. This fact can be interpreted as a possible evidence that the Mexican stock market (that has become public and regulated since 1975) has been increasing its efficiency, as reported by previous research Achach . The same claim can be made about the NASDAQ, given that it is also a market of relatively recent creation. In contrast, the Dow Jones Industrial Average index represents a more mature market. However, there is also evidence that the New York Stock Exchange, represented by the Dow Jones, has swiftly increased its efficiency between the beginning of the 1980s and the end of the 1990s NYSE . Figure 4 shows that for the Dow Jones, the greatest deviations from the geometric distribution in the studied period (almost the whole XXth Century) occurred between the years 1960-1980.

V Conclusions

The probability distributions for the duration of elemental trends were studied for the market indices Dow Jones Industrial Average (DJIA), NASDAQ Composite and for the Mexican Índice de Precios y Cotizaciones (IPC). These distributions are expected to be geometric and memoryless according to the discussion in section II. The IPC and the NASDAQ present periods in which the memoryless hypothesis must be definitely rejected.

Acknowledgements

This work was supported by Conacyt-Mexico and MAE-Italy under grant 146498. We also thank Conacyt-Mexico for the support under project grant 155492, Universidad Veracruzana under project 41504 and PRIN 2009 Italian grant “Finitary and non-finitary probabilistic methods in Economics”. The IPC daily data set from 1978 to 2006 was provided by P. Zorrilla-Velasco, A. Reynoso del Valle and S. Herrera-Montiel, from BMV at that time. We are grateful to all of them.

References

- (1) Bracquemond C, Crétois E and Gaudoin O 2002 ‘A comparative study of goodness-of-fit tests for the geometric distribution and application to discrete time reliability’ Preprint http://www-ljk.imag.fr/SMS/preprints.html.

- (2) V Choulakian, R A Lockhart, M A Stephens 1994 ‘Cramer-von Mises Statistics for Discrete Distributions’ Canadian Journal Of Statistics 22 125–137

- (3) Cont R 2001 ‘Empirical properties of asset returns: stylized facts and statistical issues’ Quantitative Finance 1 223–236

- (4) Coronel-Brizio H F, Hernández-Montoya A R, Huerta-Quintanilla R, and Rodríguez-Achach M E 2007 ‘Evidence of increment of efficiency of the Mexican Stock Market through the analysis of its variations’, Physica A (380) 391–398

- (5) Hernández Montoya A R, Coronel-Brizio H F, Rodríguez-Achach M E, Stevens-Ramírez G A, Politi M, and Scalas E 2011 ‘Emerging properties of financial time series in the Game of Life’ Phys. Rev. E 84 066104

- (6) Leroy S F 1973, ‘Risk aversion and the martingale property of stock prices’ International Economic Review 14 436–446.

- (7) Lucas R E 1978, ‘Asset prices in an exchange economy’ Econometrica 46 1429–1445.

- (8) Lo A W and Mackinlay A C 1999, A Non-Random Walk Down Wall Street, (Princeton: Princeton University Press).

- (9) Hołyst J A and Sieczka P 2008 ‘Statistical properties of short term price trends in high frequency stock market data’ Physica A 387 1218–1224

-

(10)

Instituto Nacional de Estadística, Geografía e Informática. Índice Nacional de Precios al Consumidor. (Retrieved on 2011, 5 November).

http://www.inegi.org.mx/est/contenidos/

proyectos/inp/inpc.aspx. - (11) Jensen M H, Johansen A and Simonsen I 2002 ‘Inverse Statistics in Economic: The gain-loss asymmetry’, Physica A 324 6.

- (12) Levy M, Levy H and Solomon S 2000 Microsimulations of Financial Markets: From Investor Behavior to Market Phenomena (London (UK): Academic Press)

- (13) Mantegna R N and Stanley H E 2000 An Introduction to Econophysics. (Cambridge (UK): Cambridge University Press)

- (14) Samanidou E, Zschischang E, Stauffer D and Lux T 2006 ‘Microscopic Models of Financial Markets’. Economics Working Paper 2006-15. Department of Economics, University of Kiel.

- (15) Samuelson P A 1965 ‘Proof that Properly Anticipated Prices Fluctuate Randomly’, Industrial Management Rev. 6 41–45.

- (16) Samuelson P A and Nordhaus W D 2005 Economics (New York: McGraw-Hill).

- (17) Scalas E 1998, ‘Scaling in the market of futures’, Physica A 253 394–402.

- (18) Toth B and Kertesz J ‘Increasing market efficiency: Evolution of cross-correlations of stock returns’ Physica A 320 505–515

-

(19)

U. S. Bureau of Labor Statistics, Consumer Price Index. (Retrieved on 2011, 5 November). http://data.bls.gov/timeseries/

CUSR0000SA0?output_view=pct_1mth. - (20) Voit J 2003 The Statistical Mechanics of Financial Markets. (New York: Springer-Verlag).