Estimating the predictability of economic and financial time series

Abstract: The predictability of a time series is determined by the sensitivity to initial conditions of its data generating process. In this paper our goal is to characterize this sensitivity from a finite sample by assuming few hypotheses on the data generating model structure. In order to measure the distance between two trajectories induced by a same noisy chaotic dynamic from two close initial conditions, a symmetric Kullback-Leiber divergence measure is used. Our approach allows to take into account the dependence of the residual variance on initial conditions. We show it is linked to a Fisher information matrix and we investigated its expressions in the cases of covariance-stationary processes and processes. Moreover, we propose a consistent non-parametric estimator of this sensitivity matrix in the case of conditionally heteroscedastic autoregressive nonlinear processes. Various statistical hypotheses can so be tested as for instance the hypothesis that the data generating process is “almost” independently distributed at a given moment. Applications to simulated data and to the index illustrate our findings. More particularly, we highlight a significant relationship between the sensitivity to initial conditions of the daily returns of the and their volatility.

Keywords: Chaos theory; Sensitivity to initial conditions; Non-linear predictability; Time series.

Introduction

Stock price dynamics are difficult to approximate because of various factors influencing the supply-demand interactions. These factors can be from a political, monetary, economic or psychological nature and are difficultly measurable in real-time. However, for an investor wishing to preserve his capital, modelling the price dynamics is a necessary task to quantify investment risks and to hedge his portfolio. In this regard, the existence of exploitable deterministic chaotic dynamics has become one of the key questions in the academic literature investigating nonlinear dynamics in financial and economic time series (see Brock (1986), Hsieh (1991), Peters (1994), Hommes (2001), Shintani and Linton (2003), Kyrtsou et al. (2004), Hommes and Manzan (2005)).

The idea behind a chaotic data generating process is that future realizations of this process can be approximated by realizations following past realizations close to the current realizations. Forecasts of such a time series can so be performed just by weighting some selected past observations. This is due to the fact that two trajectories induced by a same nonlinear chaotic dynamic will be close, until a certain time horizon, if they are generated from two close initial conditions. In contrast, when the data generating process is independent from initial conditions as in the case of independently distributed processes, further realisations cannot be determined from past values. Measuring the sensitivity of a time series to initial conditions can so indicate if it can be predicted just by using its past values.

In the literature, numerous nonlinear parametric models have been proposed to model economic and financial time series as the GARCH models (Engle (1982), Bollerslev (1986)), the threshold models (Tong (1983)) or the hidden Markov models (Mamon and Elliott (2007)). However, when we observe real-world time series, we do not know the structure of the data generating process. Nonparametric regression techniques represent an alternative to these nonlinear parametric models assuming fewer hypotheses on the model structure. When time series are generated from a deterministic chaotic system added by a stochastic measurement noise, these regression methods can be applied to estimate the underlying chaotic dynamic. In this framework, the chaotic component, also called the “skeleton” (Tong (1990)), models the sensitivity of the considered system to its initial conditions until a certain time horizon while the stochastic component introduces a part of unpredictability within data. More particularly, the stochastic perturbation can display heteroscedasticity, i.e. a time-varying conditional variance, which is a common feature in economic and financial time series (see Bollerslev, Chou and Kroner (1992)). In that case the conditional expectation of the process and the conditional variance of the dynamic noise can both depend on initial conditions. That is why we were interested to estimate the dependence on initial conditions of such a noisy chaotic dynamic by using nonparametric regression techniques.

Several method already exist to measure the dependence of a time series on initial conditions. Two widely used methods are the correlation dimension introduced by Grassberger and Procaccia (1983) and the Lyapunov exponent (see Wolf et al. (1985), Rosenstein, Collins and Deluca (1993)). Such methods have initially been created for deterministic data generating process which are not perturbed by dynamic noises (see Dämming and Mitschke (1993), Tanaka, Aihara and Taki (1998)). Nonetheless, when a stochastic noise is assumed, several studies have proposed to estimate the deterministic conditional expectation of the process and its derivatives by using some non-parametric regression tools (as local polynomial non-parametric regressions, neural networks regressions, etc.). It has to be remarked that they generally assume a constant residual variance. They next compute a correlation dimension (Kawaguchi and Yanagawa (2001), Kawaguchi et al. (2005)) or a Lyapunov exponent (McCaffrey et al. (1992), Nychka et al. (1992), Gençay (1996), Lu and Smith (1997), Shintani and Linton (2004)) from the estimated conditional expectation of the process.

Anyway, these methods were originally developed for deterministic systems that is why several studies question their estimation in a stochastic context. For instance, Schittenkopf, Dorffner and Dockner (2000) used neural networks regression to estimate the Lyapunov exponent of random dynamical systems and found difficulty interpretable results. Dennis et al. (2003) developed examples of ecological population models in which a Lyapunov exponent estimated from raw data leads to conclusions opposite to those that can be deduced with a Lyapunov exponent estimated from the deterministic conditional expectation of the process. Kyrtsou and Serletis (2006) estimated a significantly negative Lyapunov exponent from daily returns of the USD/CAD exchange rate and remark that the presence of dynamic noise makes it impossible to distinguish between noisy chaos and pure randomness. Then it seems interesting to develop others methods to analyse the dependence of a noisy chaotic system on its initial values.

For this purpose, in this paper, we propose the use of a symmetric Kullback-Leiber divergence measure applied to two distributions having different initial conditions. This measure can be linked to a Fisher information matrix (see Yao and Tong (1994)). The charm of this method rests on the fact that it allows to take into account the dependence of the residual variance on initial conditions. Schittenkopf, Dorffner and Dockner (2000) already studied this approach and gave expressions of such a Fisher information matrix when data are generated by stationary autoregressive models. Here the Fisher information matrix is estimated with local polynomial regressions what allows to take into account some non-stationary time series. A test based on this approach is next proposed to quantify the dependence on initial conditions of the data generating process. The finite sample properties of our approach are investigated through a simulation study and an application to the .

Our paper proceeds as follows. In Section 2, a measure of the divergence of two initially nearby trajectories is introduced. We show that it is linked to a Fisher information matrix. Its expression is given in case of conditionally heteroscedastic nonlinear autoregressive process and in the particular cases of covariance-stationary and processes. In Section 3, an estimation of the Fisher information matrix characterizing the dependence of the data generating process on initial conditions is presented. The asymptotic properties of this estimator are studied. In Section 4, a statistical test is proposed with the aim to test the dependence on initial conditions of a data generating process from a finite sample of its realizations. In Section 5, applications on simulated data and to the index are performed. Finally, Section 6 corresponds to our conclusion.

1 Measuring dependences on initial conditions in a noisy chaos context

Let be an observed time series. According to the Taken’s delay embedding theorem (Takens (1981)) and its generalisations (Sauer et al. (1991)), if these observations are generated from a dynamic of states following some regularity conditions (see Takens (1981) for most details), the dynamic of these observations is fully captured in the -dimensional phase space defined by the delay vectors :

| (1.1) |

where is the time delay, is a sufficiently large embedding dimension and denotes the transposed vector of . In the sequel of this paper, will be denoted by in order to simply the notations. In this framework, we thus have for where is a deterministic function respecting some regularity conditions. However, real observations often display a behaviour which seems generated by a mix between a totally deterministic process and a totally stochastic process. That is why we consider the following conditionally heteroscedastic nonlinear autoregressive process in this paper :

| (1.2) |

where :

-

•

and belong to regular spaces of functions, being a strictly positive variance function.

-

•

is a random variable with an independent Gaussian distribution centered on 0 and with a variance of .

represents a component of the signal which is sensitive to initial conditions while represents a random component having its variance sensitive to the same initial conditions. In practice, the regular spaces of functions are generally specified in order to use a specific statistical method to estimate and from the observations. In the sequel of this paper, we will assume that and are four times differentiable on .

1.1 A divergence measure of two nearby trajectories

As remarked by Yao and Tong (1994), a symmetric Kullback-Leiber divergence, also known as the -divergence (see Jeffreys (1946)), can be used to quantify the divergence of two initially nearby trajectories in the framework (1.2). It equals to

| (1.3) |

where is the probability density function of conditioned on the delay vector , and where is a vector representing the difference between two initially nearby trajectories. More particularly, in our framework (1.2),

For a fixed , the more the system will depend on its initial conditions, the more will be high. It has to be noted that is non-negative, symmetric in and and equals to 0 if and only if . A Taylor expansion of up to the first order in (1.3) allows us to write that :

| (1.4) |

with the Fisher information matrix defined by :

where denotes the gradient operator with respect to the coordinates of . is a matrix of dimensions which we shall also call a sensibility matrix. The next proposition extracted of Schittenkopf, Dorffner and Dockner (2000) gives the expressions of in our framework (1.2) :

Proposition 1.

Let us assume that and . Hence

| (1.5) |

A proof of this proposition is given in the Appendix. More particularly, in the case of a constant variance , we have

| (1.6) |

Let us consider various situations to interpret in this case :

-

•

If and , the variance of masks the sensitivity of the system to its initial conditions and the symmetric Kullback-Leiber divergence will thus tend toward 0.

-

•

If and , the symmetric Kullback-Leiber divergence equals to 0 and the system is clearly not sensitive to its initial conditions since when .

-

•

If and , the system will be totally depending on its initial conditions because will tend to 0 in probability. Consequently, will tend to .

1.2 Dependence on initial conditions of covariance-stationary processes and processes

In this part, we study the dependence on initial conditions of specific random processes widely used in econometrics by computing the previously introduced sensibility matrix.

Covariance-stationary processes.

The Wold decomposition (see Hamilton (1994), p.109) ensures that any zero-mean covariance-stationary process can be represented as

where :

-

•

with a standard white noise, a variance parameter, and .

-

•

is a linearly deterministic component of which we denote by .

By considering our previous notations, we have , and . In that case, is clearly dependent on while is independent of . So we have and what give

where denotes the coefficient on the row and column of the matrix . The sensitivity to initial conditions is thus determined by the level of the ratio but also by the products of the parameters .

Remark 1.1.

Any ARMA(p,q) processes of the form

where is the lag operator, is a standard white noise and where () and () are real parameters, has a sensibility matrix equals to

In the specific case of an autoregressive process of order , we have

what means that the sensitivity to initial conditions of any autoregressive process is unchanging over time.

ARCH() processes.

Now, we consider an ARCH() process which can be noted by

where is a standard white noise and

where and . Let us recall that ARCH() and GARCH() processes can be considered as particular cases of such a process (see Hamilton (1994), p.665). Here, we have and what gives . Hence,

In that case, the dependence on initial conditions is function of the parameters but also of the past values of the time series. This dependence is thus time-varying similarly to a moving average process and contrary to an autoregressive process.

When we work with real time series, a major issue consists of estimating without knowledge of the data generating process. With this purpose, we propose, in the rest of this paper, a consistent estimator of the sensibility matrix displayed in Proposition 1.5 by using local polynomial non-parametric regressions. This estimator will allow to measure the dependence on initial conditions of any observed time series having a dynamic respecting our framework displayed in 1.2.

2 Local estimation of the sensibility matrix

The Fisher information matrix displayed in Proposition 1.5 depends on , and . In order to estimate these quantities, we propose to use local polynomial non-parametric regression which is a widely used method displaying various advantages (see Fan and Gijbels (1996) for most details).

2.1 Estimation by local polynomial regression

This method begins with the following two steps :

-

•

. This steps consists of estimating the time delay and the minimal embedding dimension . Some references can be made to Fraser and Swinney (1986) or Moon, Rajagopalan and Lall (1995) concerning the estimation of . Several algorithms are available for the estimation of (see for instance Fraser and Swinney (1986), Kennel, Brown and Abarbanel (1992), Cao (1997), Kantz and Shreiber (2003)). Popular methods are the False Nearest neighbors method (Fraser and Swinney (1986)) or the Cao method (Cao (1997)). When and are adequately chosen, the delay vectors can be reconstructed as in (1.1) by taking .

-

•

by using an Euclidean distance. If you compare each delay vector to each others, this method needs operations. The number of operations can be reduced to if you use the k-d. tree method (see Bentley (1975), Friedman, Bentley and Finkel (1977)). The C++ library ANN allows to use such algorithms (see Arya et al. (1998)). In the sequel, we will write for the instant of the nearest neighbor of .

Estimation of and .

Let be in a neighborhood of . can thus be approximated by the Taylor series expansion up to the second order given by :

| (2.1) |

where is the Hessian matrix of with respect to the coordinates of . The local non-parametric polynomial regression is based on this approach and consists of minimising the locally weighted sum of squared residuals :

| (2.2) |

where :

-

•

where denotes a vector containing the columns on and below the diagonal of a matrix . represents the nearest delay vectors of in the sense of an Euclidean distance.

-

•

contains the realizations following the nearest neighbors of the delay vector .

-

•

is a weighing matrix such that

(2.3) where with a kernel function and is an identity matrix of dimension . For simplicity we consider spherically symmetric and where in the sequel of this paper. A common choice for is the standard normal density function .

The first derivative of (2.2) with respect to allows to find that

| (2.4) |

where is an estimation of with if and if . The coordinate of corresponds to an estimation of , denoted in the case , while the to coordinates correspond to an estimation of denoted .

Estimation of and .

Now let us denote the residual vector and the vector containing the squares of the coordinates of .

With the aim of estimating and , we use the following local non-parametric estimator based on the residuals of the local non-parametric estimation of :

| (2.5) |

Similarly to , the coordinate of corresponds to an estimation of denoted by in the case , while the to coordinates correspond to an estimation of denoted by .

Remark 2.1.

It has to be noted that the matrices and need to be invertible in (2.4) and (2.5). When two nearest neighbours are close to each other, their respective columns in these matrices are also close and these one will thus have determinants close to . To by-pass this numerical problem, one of both close neighbours can be eliminated. An other method consists of using a regression on principal components by transforming the columns of the matrix into a matrix with orthonormal columns (see Jolliffe (2002) for most details).

2.2 Asymptotic consistency of

The following theorem gives the asymptotic consistency of under some general conditions.

Theorem 2.1.

Assume that and in model (1.2). Let us denote the convergence in probability, and where is the kernel function already introduced in (2.3) and is a vector of coordinates . Assume moreover that :

-

•

and for all .

-

•

is a multivariate i.i.d. sequence with a marginal density noted such as and .

-

•

, , , , and when .

Under these general conditions, we have

where and denote the coefficients on the row and column of the matrix and respectively.

A proof of Theorem 2.1 is given in the Appendix. It has to be noted that the assumption of i.i.d. nearest neighbors can be relaxed as in Lu (1999) (Condition C). In the next section, we propose to use a bootstrapping technique to test the local dependence on initial conditions for a finite-length time series.

3 Testing the local sensitivity to initial conditions within time series

The dynamics following two close delay vectors are considered similar if the symmetric Kullback-Leiber divergence presented in (1.3) between the densities and is close to 0 for and , where and are two close delay vectors in the sense of the Euclidean distance. Furthermore, let us recall from (1.4) that when is quite small.

That is why we consider the following statistic :

where

with and two selected bandwidths and a selected embedding dimension. Under the general conditions of Theorem 2.1 and from the continuous mapping theorem, we so have

Under the hypothesis that the time series is independent from initial conditions, i.e. for all , equals to 1. More the time series will be dependent on initial conditions, more will be low. If the process is totally deterministic, we have . In order to test the dependence of a time series on initial conditions, the following pair of hypotheses can so be tested :

where corresponds to a level of dependence on initial conditions. A p-value of this test can be obtained by estimating the probability . When is close to 1, this p-value corresponds to a probability that the data generating process is not independent from initial conditions. On the other hand, when is close to 0, this p-value corresponds to a probability that the data generating process is strongly dependent on initial conditions (almost totally deterministic).

However, the asymptotic distribution of depends on unknown quantities as the gradients and (see the proof of Theorem 2.1). Thus cannot directly be used to build a test and we consider a re-sampling procedure to provide reliable quantiles for testing the local sensitivity of a time series to initial conditions. This re-sampling method is inspired from Gençay (1996) who applied a similar method to approximate the distribution of a maximal Lyapunov exponent.

Firtsly delay vectors are selected with replacement from all the selected nearest neighbors of . The new selected set, denoted by , allows to estimate a new . This estimation allows to find a new and, finally, a new estimation of the Fisher information matrix and thus of , denoted respectively by and , are obtained. When this experiment is repeated a large number of time, it allows to approximate the distribution of . In practice, it has to be noted that the nearest neighbors of needs to be significantly close to while the number of selected delay vectors needs to be choose not too small to obtain significant approximations of the sensibility matrix.

4 Simulations and empirical applications

In this section, we firstly applied our approach to stationary AR(1) processes displaying a constant dependence on initial conditions and to a GARCH(1,1) process where this dependence is time-varying. We next test this dependence on the daily returns of the index. In all our experiments, we fixed the prediction horizon .

4.1 Results on AR(1) processes.

Firstly, let us consider the following AR(1) process :

| (4.1) |

where is a standard white noise. The Fisher information matrix measuring the sensitivity to initial conditions of this process is given by

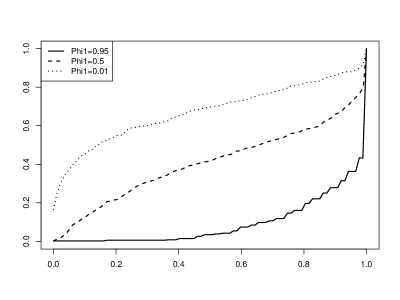

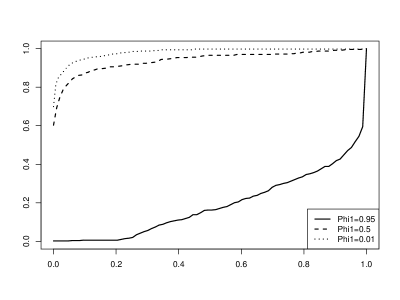

For our experiments, we fix the variance parameter and we consider three stationary AR(1) processes corresponding to the cases , and . For each stationary AR(1) process, 499 time series of size are generated. The values of their respective theoretical statistical index will thus be , and . In our experiments, we assume that the time delay and the embedding dimension . Estimations of the proposed statistic are done by using the standard normal density kernel function in the local polynomial non-parametric regressions and by fixing . In our re-sampling procedure (see section 3), we estimated the probabilities and from 199 iterations by choosing delay vectors with replacement from nearest neighbours of the current delay vector . The empirical cumulative distribution functions of these estimated probabilities, denoted by , are assessed by means of Monte Carlo experiments from the 499 generated time series. Figure 1 and Figure 2 display these distribution functions for the three stationary AR(1) processes.

In view of Figure 1 and Figure 2, we observe that

for all and . This illustrates the lower dependence on initial conditions for () than in the case () which has itself a lower dependence on initial conditions than in the case ().

It has to be noted that in the cases and , the theoretical statistical index is close to 0. However, Figure 2 clearly shows that the probability is approximatively equal to 0 for while it is close to 0.6 for . The finite sample estimation of is thus rather different from the theoretical statistical index in the case of . This difference can be due to the chosen bandwidths. Indeed, inappropriate hyper-parametrization can cause to give importance to delay vectors far from the current delay vector in our non-parametric regressions and finally to conclude spuriously on the independence from initial conditions.

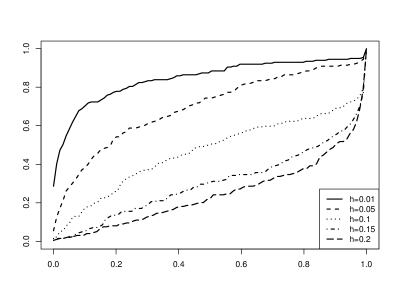

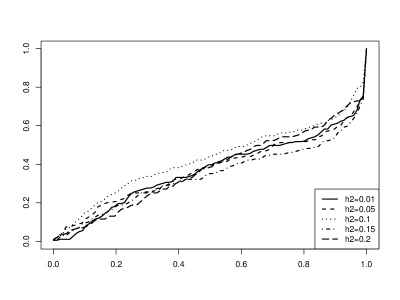

Figure 3 illustrates how the empirical cumulative distribution function of can be changed by making vary the bandwidth when the others parameters are fixed (, and ) in the case of . Figure 4 illustrates the same thing for the bandwidth (, and ). In view of Figure 3, increasing the bandwidth allows to conclude on higher dependence on initial conditions of the time series. This can be explained by the fact that a too small bandwidth will give importance to very few delay vectors what can lead to spurious conclusions. However, in view of Figure 4, changing seems to have few impact on the estimation of the empirical cumulative functions. It is logic because the AR process has not a time-varying residual variance. These observations show that the choice of hyper-parameters in the non-parametric regressions must be carefully made. More specifically, final conclusions are totally function of the chosen hyper-parametrization.

- Figure 1 around here -

- Figure 2 around here -

- Figure 3 around here -

- Figure 4 around here -

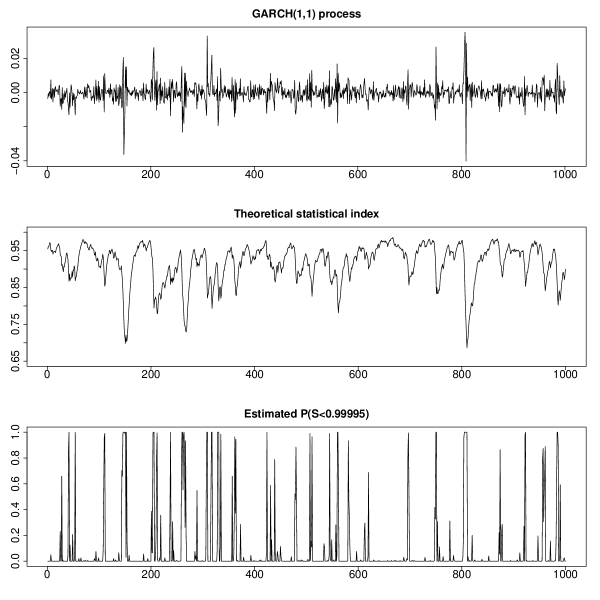

4.2 Results on GARCH(1,1) process.

Let us consider the following GARCH(1,1) process :

| (4.2) |

with , , and a standard white noise. This process is close to those that can be infer from daily returns of stock market indices. By using an inductive reasoning and since , this process can be re-written as

Consequently, a coefficient of the Fisher information matrix is given by

| (4.3) |

In order to illustrate the time-varying dependence on initial conditions of such a process, a time series of size 2000 following 4.2 is generated. We test an hypothesis that the time series is “almost” independently distributed by assessing the p-value where is close to 0. In our experiment, we fix . The theoretical statistical index and the estimated probability are next computed from 4.3 for by using a sliding windows of size 1000. The probability is estimated following the previous method used in the case of the AR(1) processes (, , ). If the probability , the time series can be considered similar to an “almost” independently distributed process. Figure 5 display the obtained outcomes. When the theoretical statistical index deviates from 1, we remark that the estimated p-value increases what indicates that our method allows to get well the moments when the series is more predictable. Although is never equal to 1, the estimated p-value is often close to 0 what means that the time series can often be considered as unpredictable from a past window of size 1000 with our hyper-parametrization.

- Figure 5 around here -

4.3 Empirical applications to the

In this section, we studied if the daily returns of the stock market index are sensitive to initial conditions by using our approach. The considered time series goes from the 04/01/1999 to the 18/02/2010 and has a size equals to 3051. It has been extracted from Datastream.

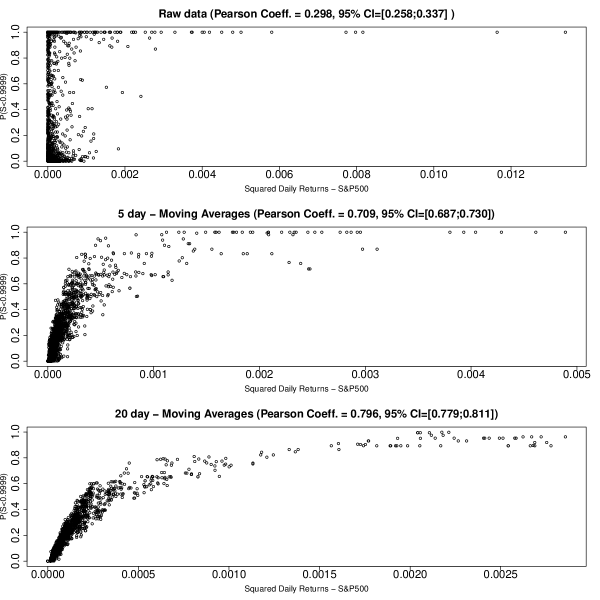

In order to investigate the predictability of the time series from a past data window of size 1000, we consider a sliding windows of size 1000 and apply our method with the same hyper-parameters used in the previous experiments (). The p-value is determined with and . Results are displayed in Figure 6. When , the p-value varies more between 0 and 1 than in the case where it is often equal to 0. The time series can so be considered predictable by using while it is considered unpredictable with .

The dependence on initial conditions is thus low but significant at certain moments. More particularly, we remark that the p-value is higher when the volatility of daily returns is higher what means that it is more sensitive to initial conditions in period of high volatility. Conversely, it is lower sensitive in period of low volatility. Figure 7 illustrates these observations by representing the probability in function of the squared daily returns of the . The Pearson’s correlation coefficient between these quantities is approximatively equals to 0.3 and significantly not null. More significant relationships are established by examining the Pearson’s correlation coefficients between their respective 5-day moving averages and 20-day moving averages (see Figure 7). In view of Figure 7, these relations are nonlinear. It has to be noted that these observations are similar to these done by LeBaron (1992) who showed that there are significant relations between volatility and serial correlations in stock market returns, serial correlations being a manner to measure the dependence on past conditions.

- Figure 6 around here -

- Figure 7 around here -

5 Conclusion

In this paper we studied the problem of testing the local sensitivity to initial conditions of time series. Our approach consists to measure the distance between two trajectories, having different initial conditions and following a same noisy chaotic dynamic, with a symmetric Kullback-Leiber divergence. We showed that this divergence can be characterized by a Fisher information matrix. In this way, we showed that autoregressive processes have a constant dependence on initial conditions while moving average processes or processes have a time-varying dependence on initial conditions. Because real-world time series have unkown data generating processes, we proposed a framework for testing the time-varying sensitivity to initial conditions of any conditionally heteroscedastic nonlinear autoregressive processes by using nonparametric regression techniques. More particularly, we propose a consistent estimator of the Fisher information matrix characterizing the dependence on initial conditions. We illustrated these theoretical results through a set of numerical experiments. We have remarked that the choice of hyper-parameters in the non-parametric regressions must be carefully made. The outcomes obtained on the daily returns of the index show that they are more sensitive to initial conditions in period of high volatility than in period of low volatility. Interesting further researches could be done by investigating the dependence on initial conditions of others time series with our method.

6 Appendix

Proof of Proposition 1.5. We have

Hence,

Because follows a Gaussian distribution centered on , we have , and what give the result for .

Proof of Theorem 2.1. In the next, denotes the convergence in distribution and denotes the convergence in probability. Let us consider the following theorem :

Theorem 6.1.

Assume that and in model (1.2). Let us denote and where is the kernel function already introduced in (2.3) and is a vector of coordinates . Assume moreover that :

-

•

and for all .

-

•

is a multivariate i.i.d. sequence with a marginal density noted such as and .

-

•

, , when .

Under these general conditions, we have

with :

-

•

and where the coordinate of is

-

•

and with

The proof of Theorem 6.1 is similar to the proofs which can be found in Masry (1996) or Lu (1999) and is thus omitted. It has to be noted that the assumption of i.i.d. nearest neighbors can be relaxed as in Masry (1996) or Lu (1999). We deduce directly from this Theorem 6.1 that each coefficient of the matrix converges in distribution toward the product of two normal distributions :

where denotes the coefficient of the row and the column of the matrix and where follows a Gaussian law with and the coordinates of and respectively. More particularly, we will have the following bias and variance for this estimator

By supposing that and when , the consistency of is thus obtained.

The asymptotic consistency of toward can also be achieved by using the general conditions of Theorem 6.1 if and when . This outcomes is obtained by replacing with and with a constant function in the statement of Theorem 6.1.

Because is a consistent estimator of if and when , we have under these conditions. Hence,

if , , and .

Similarly to , the asymptotic consistency of can also be achieved by assuming and when :

If is a consistent estimator of , we get the asymptotic consistency of toward .

Finally, from Theorem 6.1 and if we suppose , , , , and when , we have

where denotes the coefficient on the row and column of the matrix .

References

-

Arya S., Mount D. M., Netanyahu N. S., Silverman R. and Wu A. Y. (1998) An optimal algorithm for approximate nearest neighbor searching, Journal of the ACM, Vol.45, pp.891-923.

-

Bentley J.L. (1975) Multidimensional binary search trees used for associative searching, Commun. ACM 18, Vol.9, pp.509-517.

-

Bollerslev T. (1986) Generalized autoregressive conditional heteroskedasticity, Journal of Econometrics, Vol. 31, pp.307-327.

-

Bollerslev T., Chou R.Y. and Kroner K.F. (1992) ARCH modeling in finance : a review of the theory and empirical evidence, Journal of Econometrics, Vol.52, pp.5-59.

-

Brock W.A. (1986) Distinguishing random and deterministic systems, Journal of Economic Theory, Vol.40, pp.168-195.

-

Cao L. (1997) Practical method for determining the minimum embedding dimension of a scalar time series, Physica D : Nonlinear Phenomena, Vol.110, pp.43-50.

-

Dämmig M. and Mitschke F. (1993) Estimation of Lyapunov exponents from time series: the stochastic case, Physics Letters A, Vol.178, pp.385-394.

-

Dennis B., Desharnais R.A., Cushing J.M., Henson S.M., Costantino R.F. (2003) Can noise induce chaos?, Oikos, Vol.102, N°2, pp.329-339.

-

Engle R.F. (1982) Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation, Econometrica, Vol.50, N° 4, pp.987-1007.

-

Fan J. and Gibjels I. (1996) Local polynomial modelling and its applications, Chapman and Hall, London.

-

Fraser A. and Swinney H. (1986) Independent coordinates for strange attractors from mutual information, Physical Review A, Vol.33, pp.1134-1140.

-

Friedman J.H., Bentley J.L. and Finkel R.A. (1977) An algorithm for finding best matches in logarithmic expected time, ACM Transactions on Mathematical Software, Vol.3, pp.209-226.

-

Gençay R. (1996) A statistical framework for testing chaotic dynamics via Lyapunov exponents, Physica D : Nonlinear Phenomena, Vol.89, pp.261-266.

-

Grassberger P. and Procaccia I. (1983) Measuring the Strangeness of Strange Attractors, Physica D : Nonlinear Phenomena, Vol.9, pp.189-208.

-

Hamilton J.D. (1994) Time series analysis, Princeton University Press.

-

Hommes C.H. (2001) Financial markets as nonlinear adaptive evolutionary systems, Quantitative Finance Vol.1, Issue 1, pp.149-167.

-

Hommes C.H. and Manzan S. (2005) Testing for nonlinear structure and chaos in economic time series : a comment, CeNDEF Working Papers 05-14, Universiteit van Amsterdam, Center for Nonlinear Dynamics in Economics and Finance.

-

Hsieh D. A. (1991) Chaos and Nonlinear Dynamics: Application to Financial Markets, Journal of Finance, Vol. 46, No. 5, pp. 1839-1877.

-

Jeffreys H. (1946) An invariant form for the prior probability in estimation problems, Proceedings of the Royal Society of London Series A, Vol.186, pp.453-461.

-

Jolliffe I.T. (2002) Principal component analysis, Second Edition, Springer-Verlag, New-York.

-

Kantz H. and Schreiber T. (2003) Nonlinear time series analysis, Second Edition, Cambridge University Press, Cambridge.

-

Kawaguchi A. and Yanagawa T. (2001) Estimating correlation dimension in chaotic time series, Bulletin of informatics and cybernetics, Vol.33, pp.63-71.

-

Kawaguchi A., Yonemoto K. and Yanagawa T. (2005) Estimating the correlation dimension from a chaotic system with dynamic noise, Journal of Japan Statistical Society, Vol. 35, N° 2, pp.287-302.

-

Kennel M.B., Brown R. and Abarbanel H.D.I. (1992) Determining embedding dimension for phase-space reconstruction using a geometrical construction, Physical Review A, Vol.45, N° 6, pp.3403-3411.

-

Kyrtsou C., Labys W.C. and Terraza M. (2004) Noisy chaotic dynamics in commodity markets, Empirical Economics, Vol. 29, N° 3, pp. 489-502.

-

Kyrtsou C. and Serletis A. (2006) Univariate tests for nonlinear structure, Journal of Macroeconomics, Vol.28, N° 1, pp.154-168.

-

LeBaron B. (1992) Some relations between volatility and serial correlations in stock market returns, Journal of Business, Vol. 65, N° 2, pp. 199-219.

-

Lu Z.-Q. (1999) Multivariate local polynomial fitting for martingale nonlinear regression models, Annals of the Institute of Statistical Mathematics, Vol.51, N° 4, pp.691-706.

-

Lu Z.-Q. and Smith R.L. (1997) Estimating local Lyapunov exponents, in Nonlinear Dynamics and Time Series, editors Colleen D. Cutler and Daniel T. Kaplan. pp.135-151. Fields Institute Communications Vol. 11, American Mathematical Society, 1997.

-

Mamon R.S. and Elliott R.J. (2007) Hidden Markov models in finance, International Series in Operations Research Management Science, Springer.

-

Masry E. (1996) Mutivariate regression estimation: local polynomial fitting for time series, Stochastic Processes and their Applications, Vol.65, N° 1, pp.81-101.

-

McCaffrey D.F., Ellner S., Gallant A.R. and Nychka D.W. (1992) Estimating the Lyapunov exponent of a chaotic system with nonparametric regression, Journal of the American Statistical Association, Vol. 87, No. 419, pp.682-695.

-

Moon Y.-I., Rajagopalan B. and Lall U. (1995) Estimation of mutual information using kernel density estimators, Physical Review E, Vol.52, pp.2318-2321.

-

Nychka D.W., Ellner S., McCaffrey D.F. and Gallant A.R. (1992) Finding chaos in noisy systems, Journal of the Royal Statistical Society Series B, Vol.54, pp.399-426.

-

Peters E.E. (1994) Fractal market analysis : applying chaos theory to investment and economics, Wiley Finance Series, John Wiley Sons Inc.

-

Rosenstein M.T., Collins J.J. and DeLuca C.J. (1993) A practical method for calculating largest Lyapunov exponents from small data sets, Physica D : Nonlinear Phenomena, Vol.65, N° 1-2, pp.117-134.

-

Sauer T., Yorke J.A., Casdagli M. (1991) Embedology, Journal of Statistical Physics, Vol.65, pp.579-616.

-

Schittenkopf C., Dorffner G. and Dockner E.J. (2000) On nonlinear, stochastic dynamics in economic and financial time series, Studies in Nonlinear Dynamics and Econometrics, Vol.4, pp.101-121.

-

Shintani M. and Linton O. (2003) Is there chaos in the world economy? A nonparametric test using consistent standard errors, International Economic Review, Vol.44, N° 1, pp.331-357.

-

Shintani M. and Linton O. (2004) Nonparametric neural network estimation of Lyapunov exponents and a direct test for chaos, Journal of Econometrics, Vol.120, pp.1-33.

-

Takens F. (1981) Detecting strange attractors in turbulence, in Dynamical Systems and Turbulence edited by Rand D.A. and Young L.-S., Springer-Verlag, Berlin.

-

Tanaka, Aihara and Taki (1998) Analysis of positive Lyapunov exponents from random time series, Physica D : Nonlinear Phenomena, Vol.111, N° 1, pp. 42-50.

-

Tong (1983) Threshold models in non-linear time series analysis, Lecture notes in statistics, No.21. Springer-Verlag, New York, USA.

-

Wolf A., Swift J.B., Swinney H.L., Vastano J.A. (1985) Determining Lyapunov exponents from a time series, Physica D : Nonlinear Phenomena, Vol.16, N°3, pp.285-317.

-

Yao Q., Tong H. (1994) On prediction and chaos in stochastic systems, Philosophical Transactions: Physical Sciences and Engineering, Vol. 348, N° 1688, Chaos and Forecasting, pp.357-369.