root’s barrier, viscosity solutions of obstacle problems and reflected FBSDEs

Abstract.

We revisit work of Rost [49], Dupire [22] and Cox–Wang [16] on connections between Root’s solution of the Skorokhod embedding problem and obstacle problems. We develop an approach based on viscosity sub- and supersolutions and an accompanying comparison principle. This gives a complete characterization of (reversed) Root barriers and also leads to new proofs of the existence as well as the minimality of Root solutions by pure PDE methods. The approach is self-contained, constructive and also general enough to cover martingale diffusions with degenerate elliptic or time-dependent volatility; it also provides insights about the dynamics of general Skorokhod embeddings by identifying them as supersolutions of certain nonlinear PDEs.

Key words and phrases:

Skorokhod embedding problem, Root barrier, reversed Root barrier, viscosity solutions of obstacle problems, reflected BSDEs.1. Introduction

This article revisits the dynamics of the Skorokhod embedding problem from a viscosity PDE perspective with an emphasis on Root’s solution. That is, under mild assumptions on the probability measures on and the volatility coefficient , we are interested in finding a (non-randomized) stopping time such that

| (SEP) |

For general background on (SEP) and its applications we refer to Hobson and Obłój [42, 31]. In the Brownian case, and , Root showed in 1969 [45] that the stopping time can be realized as the first hitting of a closed time-space set, the so-called Root barrier,

by the time-space process . Further important developments are due to Rost: firstly, he showed that Root’s solution minimizes

| (1) |

among all solutions of (SEP), [49]; secondly, he gave a new existence proof of Root’s barrier by using potential theory that generalizes to time-homogenous Markov processes [49, 46]; thirdly, he showed that there exist another barrier that solves (SEP) and minimizes the diffusion of , [48, 47]. Another important contribution concerning the uniqueness of the barrier was made by Loynes [38].

Already for Brownian motion it was not known how to construct except for a handful of simple cases. A completely new perspective that led to a revived interest in (SEP) came from the management of risk in mathematical finance. It was started by work of Hobson [32] that showed how model-independent bounds of exotic options can be obtained by “extremal solutions” of (SEP). Motivated by this, Dupire [22] showed formally that the barrier is naturally linked to a nonlinear PDE that allows to solve for . This was further developed by Cox–Wang [16] who use a variational formulation, as developed in the 1970’s by Bensoussan–Lions et. al. [10], to calculcate in case its existence is guaranteed by these classic results of Root and Rost. More recently, Gassiat–Mijatovic–Oberhauser [28] studied the barrier via integral equations, Cox–Peskir [17] studied reversed barriers, Beiglböck–Cox–Huesmann [9] develop an optimal transport perspective of (SEP) and Kleptsyn–Kurtzmann [37] use Root’s barrier to construct a counter-example to the Cantelli conjecture; there are also many more developments beyond the context of Root type solutions, see for example [1, 2, 3, 27, 29, 44] for interesting recent progress.

This article takes the PDE approach further by giving a self-contained approach to the embedding problem based on viscosity solutions. The parabolic comparison principle plays the key role. It allows us to provide new proofs of firstly, the existence of a Root solution, and secondly, its minimizing property (1). In the Brownian, or homogenous diffusion case, this recovers the classic results of Root and Rost [45, 49] by constructive methods and provides insights about the general dynamics of (SEP); in the time-inhomogenous case, already the existence and minimality results themselves are new to the best of our knowledge and would be hard to obtain otherwise, since the classic approaches break down111The most general existence proof is due to Rost [49] and relies heavily on time-homogenity (and to certain degree transience) of the underlying process, thereby excluding (SEP) for time-dependent .; however in the current setup they become simple consequences of a PDE existence and a comparison of sub- and supersolutions; see Theorem 1, Theorem 2 and Theorem 3. Moreover, the PDE methods we introduce also cover Rost’s reversed Root barriers, where already for the Brownian case, they might be an attractive, constructive(!) alternative to the classic “filling scheme” [14, 47] proof that relies on deep results from potential theory.

Structure of the article.

In Section 2 we introduce notation and our assumptions on . We then give our first main result, Theorem 1, which states that any solution of the Skorokhod embedding problem (SEP) is a viscosity supersolution of a certain obstacle PDE. If one thinks in potential theoretic terms, this can be seen as the PDE version of Rost’s approach [49] to (SEP) via excessive functions of Markov processes.

In Section 3 we introduce an extension of Loyne’s notion of regular Root barriers which allows to deduce the uniqueness of such barrier solutions. We then present our second main result, Theorem 2, which shows a one-on-one correspondence of regular Root barriers and viscosity solutions. This complete characterization allows us to firstly, prove the existence of Root barriers via PDE existence, Corollary 1, and secondly, show that the minimizing property (1) is a simple consequence of a parabolic comparison result, Theorem 4. We also briefly revisit and leverage results about reflected FBSDEs [24] which allows to use Monte-Carlo methods to calculate barriers and gives another interpretation as a stopping problem. We conclude this section by showing, how our approach also gives existence and minimalty proofs of Rost’s reversed barriers.

In Section 4 we implement numerical schemes to solve for the barrier and apply the Barles–Souganidis method to get convergence (+rates of convergence) which might be useful for practitioners in financial mathematics (bounds on options on variance).

2. Skorokhod embeddings as supersolutions

2.1. Notation and Assumptions

Denote with a filtered probability space that satisfies the usual conditions and carries a standard Brownian motion and a real-valued random variable that is independent of . We work under the following assumption on .

Assumption 1.

and are measures on that have a first moment and are in convex order, i.e.

Let be Lipschitz in space and of linear growth, both uniformly in time, that is

| (2) |

Further assume local ellipticity in the sense that for each compact , there exists some s.t.

The need for above assumptions is intuitively clear: convex order of is necessary by classic work of Chacon and Kellerer about the marginals of martingales [35, 12]; however we only assume first moments which is already for the Brownian case, , weaker than Root’s assumption [45]. Linear growth and Lipschitz property of are natural since we describe the evolution of the law of the strong solution by PDEs; some nondegeneracy of the diffusion is clearly required to be able to transport the mass to . (Note that what we call “local ellipticity” covers degenerate elliptic diffusions, e.g. for geometric Brownian motion, our assumption is fulfilled if and only if the support of is contained in the positive halfline which is in this case the sharp condition).

Definition 1.

Let fulfill Assumption 1. We denote with the set of -stopping times that solve the Skorokhod embedding problem

2.2. Recall on viscosity theory

Definition 2.

Let be a locally compact subset of and denote and for a given . Consider a function and define for the parabolic superjet as the set of triples which fulfill

| (3) | |||||

Similarly we define the parabolic subjet such that .

Definition 3.

A function is proper if

Denote the real-valued, upper semicontinuous functions on with and the lower semicontinuous functions with . A subsolution of the (forward problem)

| (4) |

is a function such that

The definition of a supersolution follows by replacing by , by and by If is a supersolution of (4) then we also say that holds in viscosity sense (similar for subsolutions). Similarly we call a function a viscosity (sub-,super-) solution of the backward problem

| (5) |

if

2.3. Skorokhod embeddings as PDE supersolutions

Chacon [13] showed that for , the potential function is a powerful tool to study the evolution of the law of the stopped (local) martingale . Theorem 1 captures the following intuition: is a concave function of , hence we expect it to be a supersolution (in some sense) of a Fokker–Planck equation. However, cannot be smooth for generic Skorokhod solutions due to kinks from stopping at . Further, since is the potential of the occupation measure of and , it follows that is bounded below by the potential of the measure and will converge to it as . We now make this rigorous under the generality of Assumption 1.

Theorem 1.

| (6) |

and

Proof.

We have to show that

The first inequality follows immediately via conditional Jensen

| (7) |

and the last one is immediate from properties of potential functions, see [13, 42]. For the second inequality we approximate by a sequence of regularizations . We show that each is a supersolution of a ”perturbed version” of (6) and we conclude by sending and using the stability of viscosity solutions.

Step 1. Convergence of

as

Define the sequence

as

where is the usual Gaussian scaled to the unit disc

Especially note that uniformly, is continuous, and (we could replace by any other sequence with this properties). Further introduce

Since uniformly we have -a.s.

hence we get uniform convergence of and , i.e.

Further, by the definition of and we see that ,

| (8) |

Step 2.

on .

We now fix and apply the Itô formula to

and the local martingale which, after taking expectations

and using Fubini, leads to the expression

It follows that has a right- and left- derivative ; to see this take

and similarly it follows that the left derivative is given as

| (9) |

Note that for every ; further, since is non-negative we conclude

From the definition of it follows that we can exchange differentiation in space and expectation to arrive at

| (10) |

which is a continuous function in . Lemma 4 shows that

Splitting the term inside the expectation gives

We conclude that is a supersolution of on . Further,

hence is also a viscosity supersolution of

Using the Lipschitz property of , and that we estimate

( and as defined in (2); for the second inequality we use the trivial estimate

combined with , Lipschitzness and linear growth of ). Now for every compact we have

since our Assumption 1 guarantees (via [40, Theorem 2.3.1]) that the process has a density for all with respect to Lebesgue measure and

uniformly in , therefore locally uniformly on . By step 1, and locally uniformly as . The usual stability of viscosity solutions, see [18], implies that is a viscosity supersolution of

| (11) |

which proves the desired inequality.∎

3. Root’s solution

In principle, a solution of the Skorokhod embedding problem, , could be a complicated functional of the trajectories of . Root [45] showed that the arguably simplest class of stopping times, namely the hitting times of “nice” subsets in time-space, so-called Root barriers, is big enough to solve Skorokhod’s embedding problem for Brownian motion. We now give a complete characterization of such barriers as free boundaries of PDEs.

3.1. Root barriers

Definition 4.

A closed subset of is a Root barrier if

-

(i)

implies ,

-

(ii)

,

-

(iii)

.

We denote by the set of all Root barriers . Given , its barrier function is defined as

Barrier functions have several nice properties such as being lower semi-continuous and that for any , see [38, Proposition 3].

3.2. Uniqueness of regular Root barriers

Different Root barriers can solve the same Skorokhod embedding problem222Let , then and any other Root barrier with a barrier function that coincides with on solves .. This problem of non-uniqueness was resolved in the Brownian case, , by Loynes [38, p215] in 1970 by introducing the notion of regular Root barriers.

Definition 5.

resp. its barrier function is Loynes–regular if vanishes outside the interval , where and are the first positive resp. first negative zeros of . Given we say that are Loynes-equivalent if on and333If are Loynes-equivalent then and . .

Loynes showed that if a Root barrier solves the embedding problem then there also exists a unique Loynes-regular barrier that solves (SEP). However, Loynes’ notion of regularity is tailor-made to the case of Dirac starting measures.

Example 1.

Let and . By symmetry properties of Brownian motion, for the barrier

solves , as does

However, neither is Loynes-regular and there cannot exist a Loynes-regular barrier444If solves then otherwise it would not be Loynes regular; now note that solves , hence every other that puts under more mass on than the required since the geometry of implies that only more trajectories can hit the line than in the case ; further, every solution must coincide with on ..

Motivated by the above we introduce the notion of -regular barriers.

Definition 6.

Define

We call a Root barrier -regular if [or equivalently if ] and denote with the subset of Root barriers that are -regular. Further, two Root barriers are said to be -equivalent if555We denote with the closure and with the interior of a given set . [or equivalently if ].

We first show that in the case of Brownian motion started at a Dirac in , the above notion of regularity coincides with Loynes regularity. We then show that for every Root barrier that solves there exist a unique -regular barrier that solves the same embedding.

Lemma 1.

Let and fulfill and . Then is Loynes-regular iff is -regular.

Proof.

If is Lyones regular then one has that for from Definition 5. This and the continuity of the potential functions mean that for and hence is -regular. For the inverse direction, just remark that by definition of -regularity and the convex order relation one has for some , in other words for any . Using convex ordering again yields that and are the first negative resp. positive zero of . Hence is Loynes-regular.∎

Lemma 2.

Let fulfill Assumption 1 and assume that there exists such that solves . Then there also exists unique -regular barrier such that solves .

Proof.

To see that is -equivalent to a -regular barrier just note that since (and we embed by assumption) the continuous time-space process does not enter , hence is a also an element of that solves .

Suppose there are two -regular barriers , each embedding (via ) with u.i. stopping times and respectively. Then also embeds with the u.i. stopping time , this statement is a straightforward extension of [38, Proposition 4] to our setting (the proof only requires continuity of the paths). Furthermore, since and are u.i. they are minimal (see [43, Proposition 2.2.2 (p23)]) then is also minimal, this in turn implies that . It remains to show that and are the same (outside since in this must hold) one argues as in the proof of [38, Lemma 2 (p215)] by proving that if then also . ∎

3.3. Root’s solution as a free boundary

We have already seen in Theorem 1 that every solution of (SEP) gives rise to a supersolution of an obstacle PDE. The theorem below gives a complete characterization of (regular) Root solutions.

Theorem 2.

Let fulfill Assumption 1. Then the following are equivalent:

-

(i)

there exists such that ,

-

(ii)

there exists a viscosity solution decreasing (in time) of

(12)

Moreover,

| (13) |

Proof.

We first show that (i) implies (ii): that is we have to show that the function

| (14) |

(identified with its limit resp. as resp. ) fulfills in viscosity sense

| (15) |

The first and second line in (15) follow from Theorem 1. To see that , note that by Tanaka’s formula

and letting gives

Subtracting from the above yields

and therefore it is sufficient to show that for , -a.s. To see this simply write

and note that the right hand side can only be strictly positive if the process crosses the line . However, since is a Root barrier and we have that and since is the first hitting time of this event is a null event. It now only remains to show

and to do this we argue again via stability as in Theorem 1. Therefore define , and as well as and exactly as in Theorem 1. From Lemma 4 it follows that if then (in which case we are done) and if then , and . Hence, in the latter case we have that

As in Theorem 1, we see that is a subsolution of

In Theorem 1 we have already shown that locally uniformly as and we now show that also locally uniformly on : since is a Root barrier we have

hence if and then . Therefore

which is enough to conclude that converges locally uniformly on to , i.e. for every compact

The stability results and the restatement for parabolic PDEs of Proposition 4.3, Lemma 6.1 and Remark 6.4 found in the User’s guide [18] imply that is a subsolution of

Putting the above together shows that is indeed a viscosity solution of the obstacle problem (12). To see that is of linear growth, recall that by the above , hence . Since and are of linear growth (see e.g. [43, Section 3.2],[30, Proposition 2.1],[8, Proposition 4.1]) we have shown that

| (16) |

This allows to use our comparison result, Theorem 5, to conclude that is not only a solution but the unique viscosity solution of linear growth. Thus we have shown that (i) implies (ii) and that the second equality in (13) holds.

We now show that (ii) implies (i). First note that since , has linear growth in space uniformly in time. Now set

and write as for closed sets . Note that since is decreasing in time, is actually a barrier, and it is clearly -regular. To see that the free boundary embeds , we introduce where and denote with and the distributions of and and with and the potential functions. Since , we already know that and we now show that

| (17) |

We then argue that the above have to be equalities which shows the desired embedding. To this end, consider for each the shifted barriers

and denote their corresponding hitting times by with , and the corresponding potential functions with ,. Note that

Let us first prove that

| (18) |

For the first equality, note that if then for all . Hence if , then for all , for all , i.e. . It follows that , and the reverse inequality is obvious since . For the second inequality, passing to the limit in the relation and using lower-semicontinuity of yields , i.e. , and again the reverse inequality is obvious.

Let us prove the first inequality in (19). It will follow from a simple application of viscosity comparison. Indeed, let , we now show that it satisfies in viscosity sense

| (20) |

Indeed, let be in . Then for all , one has by the arguments from (i) (ii), whereas by definition of , for all . Since in addition is nonincreasing in , it follows that . Hence by Lemma 4, satisfies in viscosity sense at . And one has on , again by respectively definition of and the arguments from (i) (ii). We have thus proved that on the whole space, one has , and therefore by comparison. The proof of the second inequality of (19) is essentially the same.

This finishes the proof of (17). Now note that since one-point sets are regular for our one-dimensional diffusion , one has a.s., so that the inequalities in (17) are actually equalities, which proves that the hitting time of embeds . To finish the proof, it remains to show that is uniformly integrable. But this is immediate since the family of laws is dominated in convex order by , and is therefore u.i. by de La Vallee Poussin’s theorem. ∎

Remark 2.

Work of Dupire and Cox–Wang [22, 16] showed that if classic existence results [45, 49] apply, the barrier can be calculated via a PDE. What is new here is that Theorem 2 provides a complete characterization; especially, it allows to the infer existence of a Root solution from the existence of a PDE solution. This also applies to the time-inhomogenous case where these classic approaches [45, 49] break down. As we will see below, together with Theorem 1 it recovers and extends the minimizing property of barrier solutions.

Theorem 2 allows to infer the existence of a Root solution for via the existence of viscosity solutions for in the full generality of Assumption (1).

Corollary 1 (Existence of Root solutions).

Proof.

Existence of a viscosity solution to

follows from standard results, for example by penalization and Perron’s method (see [23]). Hence it only remains to prove that the solution is decreasing in time, and satisfies .

1) is decreasing in time :

We first prove it in the case where does not depend on . Define for , the function . Since is concave, it is a supersolution of (12), and since and solves the very same PDE as , it follows by comparison that . Note in addition that since (in viscosity sense), the fact that is decreasing in is easily seen to imply that is concave in . Now consider piecewise-constant in . Then by iterating the above argument, one gets that is decreasing in and concave in . To obtain the general result, approximate the continuous function by a sequence each of these being piecewise-constant in . Then the corresponding solutions converge locally uniformly to , which therefore has the same monotonicity and concavity properties. (Note that since the are not continuous functions, one needs to use the existence/uniqueness/stability results for viscosity solutions with discontinuous coefficients, e.g. [41, 7])

2) :

Let , and assume that . Then by local ellipticity on , and one has on , (using concavity of for the first inequality). Hence for each , is dominated on by the solution to

But by standard computations, is the linear interpolation between and , so that by comparison and letting , we obtain

i.e. is convex on any connected component of . Now let be a connected component of . If , then one has and . But since is concave, it must necessarily dominate the convex function on , contradicting the fact that . Similarly when or is infinite one gets a contradiction using . Hence , and . ∎

Moreover, the proof of Theorem 2 also shows regularity properties about . They have a intuitive explanation by their representation as potential functions so we record them as a corollary.

3.4. Root’s solution as a minimizer

After Root [45] proved the existence of a barrier solution for the Brownian case, Rost [49] used potential theoretic methods to show that Root’s solution minimizes the residual expectation

(As is well known from old work of Dinge [21], minimizing above residual expectation implies that also minimizes for , convex)666Applied with , Rost thereby proved a conjecture made earlier by Kiefer [36], namely that Root’s solution minimizes the variance. This property is the one that makes Root’s solution give lower bounds on options on variance. Though strictly speaking, Rost [49] proved Kiefer’s conjecture only for measures with bounded support as pointed out by himself [49, ”Technical Remark” at the bottom of page 3].. The viscosity PDE characterization of Theorem 2 now allows to give a very short proof of the minimizing property of the Root barrier via our parabolic comparision result, Thereom 5. It immediately covers the time-inhomogenous and degenerate elliptic case (thereby generalizing Rost’s approach [49]) and is already for the simple Brownian case, and , the shortest minimality proof that we are aware of.

Theorem 3.

Let , and be as in Theorem 2.

-

(i)

The potential function of the Root solution is a minimizer, that is

(21) where .

-

(ii)

If we additionally assume that have second moments, then Root’s solution minimizes the residual expectation, that is

where is the hitting time of .

In both statements above, is taken over .

Proof.

From Theorem 1 we know that every is a supersolution of the obstacle PDE (12) and from Theorem 2 we know that is a solution of the obstacle PDE (12). Using our parabolic comparison result, Theorem 5, for the supersolution and subsolution shows (21).

To see the second claim, note that by Ito

and since we conclude that this is equivalent to the statement that the Root stopping time maximises

Here denotes local time . Hence it is sufficient to show that the Root stopping time minimises pointwise, i.e. that for all we have

However, this follows by (i). ∎

3.5. Root’s solution via RBSDEs

Using Theorem 2 we can give another characterization of the Root solution via Reflected FBSDEs by using [23]. Our main interest is that it gives rise to Monte-Carlo methods to solve for the barrier. However, it also clarifies further how the Root solution is naturally linked to a stopping problem777We point the reader to [11] for a finer analysis on the regularity of RFBSDE solutions and such connections; the analysis there though does not immediately cover the current case due to unboundedness of coefficients..

Corollary 3 (RBSDE representation).

Let fulfill Assumption 1. Then

-

(i)

there exists a unique such that ,

-

(ii)

and for every

where denotes the backward dynamics of the solution of the RBSDE888 denots the natural filtration of a Brownian motion augmented with the null sets of . The quadruple is -adapted and is an increasing and continuous process verifying . Note does not have to be defined on the same probability space as our forward martingale but with slight abuse of notation we denote the expectation still with .

(22)

Moreover, the solution of the obstacle problem (12) solves the stopping problem

where .

guides the evolution of and via the Itô integral so that hits the random variable at horizon time . Note that are -adapted, nonetheless, is attained at . The process ensures that does not go below the barrier ; it pushes upwards whenever touches and tries to go below the barrier , else it remains inactive (that is constant) — is minimal in this sense. Above interpretation as optimization problem on finite time horizon is a special case of

| (23) |

applied with ; here . Following the theory of Snell envelopes, is simply the smallest supermartingale which dominates the sum inside the expectation. Lastly, the optimal stopping time solving the above optimization problem (for ) is known to be

with if for all .

Remark 3.

This further clarifies the connection to optimal stopping that can be seen from the PDE (see also [16, Remark 4.4]). However note that the optimization problem is rather non-standard due to the time reversal and that many embeddings require us to include for which the time reversal and RBSDE representation breaks down (at least for time-inhomogenous ).

Remark 4.

The following formal argument gives at least an intuition why RBSDE and obstacle PDEs are in a similar relation as SDEs and linear PDEs: suppose a sufficiently regular solution of (24) exists. Via Itô’s formula it follows that

solves the RFBSDE. The last condition in (22) then reads as

and the rhs explains the form of the PDE fulfilled by .

Proof of Corollary 3.

In view of Theorem 2 we only need to show that there exists a quadruple that fulfills (22) and that yields a viscosity solution with linear growth uniform in time.

Existence & uniqueness in , : by time reversion of (12) shows that it is enough to deal with

| (24) |

where . Continuity, existence and uniqueness of the viscosity solution follows from Lemma 8.4, Theorems 8.5 and 8.6 in [23] respectively. The linear growth of in its spatial variable follows from standard manipulations for RBSDEs. [23, Proposition 3.5] applied to the RFBSDE setting above (i.e. using due to the time reversion argument) yields the existence of a constant such that

with and where the last inequality follows from the linear growth assumptions on and along with standard SDE estimates: (see e.g. [23, Equation (4.6)]). The solution to (12) now follows from [23].

Above estimate for the linear growth in the spatial variable can be made sharper in the sense that the constant is independent of . This follows via comparison results for RFBSDE (see [23, Theorem 4.1 (p712)]). Since , i.e. the terminal condition is non-positive, the component is also non-positive. On the other hand, the solution can not go below the barrier and hence .

Existence & uniqueness in : For any , and coincide on . Hence, we define a function by letting for arbitrary chosen . Then is the unique viscosity solution of linear growth uniformly in time of , (via our comparison Theorem 5). In Corrollary 1 we have already shown that under Assumption 1 the solution must be decreasing in time and converges to which already finishes the proof. ∎

3.6. Rost’s reversed Root barrier

Root’s solution lets diffuse as much as possible before it stops it. Rost [47] showed that one can also construct a closed subset of , the so-called reversed Root barrier that lets diffuse as little as possible. More precisely, we call a reversed Root barrier if it is relatively closed in and

Reversed barriers can always be represented as , where is upper-semicontinuous on . We now briefly show that under an additional assumption on the supports of and , the methods of the previous section immediately transfer; especially, this allows to give a (constructive) PDE proof of the existence of a solution to by a reversed Root barrier.

Assumption 2.

There exists open such that

| (25) |

Theorem 4.

Proof.

The proof of the first direction, (i) implies (ii), follows exactly as in Theorem 1 and Theorem 2: first one shows that every gives a supersolution and then shows that the potential function of the reversed Root barrier is a solution. To do so one defines approximations to via mollification and shows that they fulfill a perturbed version of the PDE (26) (at this point one use above properties of the Rost barrier), then one concludes by stability of viscosity solutions. In this case, the PDE is linear in and the uniqueness follows already from well-known results that can be found in the literature (e.g. [19, 25], though we note that the domain is unbounded which leads to some subtleties that are treated in [20]).

To see that (ii) implies (i) we argue similarly as in Theorem 2. Set

and note that since is decreasing (since in viscosity sense) is indeed a reversed barrier. It remains to prove that .

Step 1 : We claim that

| (28) |

| (29) |

The first property follows by a comparison argument : since is bounded and goes to for , for each it can be bounded by a function such that is bounded and concave on some interval , and identically equal to outside . Then is bounded from above by the solution with initial data to on , outside . But by ellipticity converges to as , so that , which proves (28) since was arbitrary.

For the second claim, note that by assumption , so that on , i.e. is concave on (any connected component of) . Then one can show that is concave on for all , and in fact solves on . Finally, by local ellipticity, comparing with the solution to the heat equation on we can deduce that for any , for all in , i.e. .

Step 2 : As in the Root barrier case, we will approximate by barriers

and letting , be the distributions of at the hitting times of these, prove that

| (30) |

To be precise, if is the barrier function for , the barrier functions for and are defined by

Let us prove that . We define . By the same arguments as in (i) -> (ii), one proves that satisfies the same PDE as , and that on one has and . Let , it will be enough to show that (since ). Since , one has that is constant in time on , and satisfies on . In particular, satisfies , so that by comparison . Noting that both and do not charge , is affine on (each component of) , so that . Then since is continuous and goes to at infinity, one can find achieving this maximum. Then if , by definition of , there exists . Then one has

a contradiction. So , and by (28) this implies . This finishes the proof of the second inequality in (30), and the first one is proved by similar arguments which we leave to the reader.

Step 3 : It just remains to prove that

| (31) |

This is easy, once one notices (as in [14, 9]) that shifting the barrier is the same as shifting the starting point. Indeed, extend to by . Then letting be the hitting time of by the space-time process (not necessarily started at time ), define for a fixed the function

Then one has , . But satisfies outside , so that by ellipticity it is in particular continuous on . This finishes the proof of (31), and of the theorem. ∎

A standard application of Perron’s method now implies the existence of a reversed barrier solution. Previous proofs of reversed barrier solutions are rather involved since they make use of a heavy potential theoretic machinery (“the filling scheme” [47, 14]; though we draw attention to the recent optimal transport approach [9] as well as work of McConnell [39] that is closest in spirit to our approach, though arguably more complicated).

Remark 5.

As is known since the work of Chacon [14], a sharp condition for the existence of the reversed Root barrier is that (the case of general , in convex order requires additional randomization at time ). Our proof of (ii) (i) above does not work in that case without modifications, since simple examples show that one could have while for all (where is the barrier shifted by outside of the support of ). It is reasonable to hope that a modification based on approximating by measures fulfilling Assumption 2 could give a PDE proof for existence also in that general case, but we do not pursue this here.

Remark 6.

The minimizing property of the reversed barrier follows exactly as in the case of Root barriers from parabolic comparison [20], so we do not discuss this any further. We also do not spell out the uniqueness of reversed barriers here, but we leave it for the reader to verify that (as in the case of Root barriers) the free boundary always gives the maximal version of the reversed barrier. Similarly we do not pursue the interpretation of as generalized value function of a stopping problem.

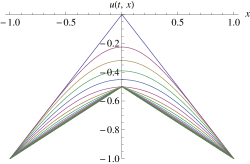

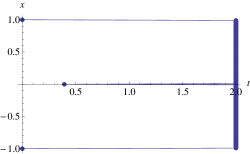

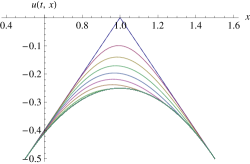

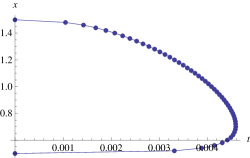

4. Numerics: root barriers via barles–souganidis methods

While it falls outside the scope of this article to study numerics of the obstacle PDE (12) in full generality we briefly give two applications: firstly we show that classic Barles–Souganidis method [5, 6] can be easily adapted to our setting; secondly we give some concrete examples by implementing these schemes for rather generic embedding problems.

4.1. and of bounded support

We give a quick construction by adapting [5, 6, 4, 25] to our setting and implementing an explicit finite differences scheme. On and setting for large enough we define the time-space mesh of points

Let be the set of bounded functions from to and the subset of bounded uniformly continuous functions. Take , we define its projection on by with as when for some and ; of course . Denote the approximation to the solution of (12) by . Define the operator as

where we assume that the usual CFL condition holds. The values of are computed by solving for in where is defined as

By [5, 6] we only have to guarantee that the operator and the PDE (12) satisfies along some sequence converging to the following properties:

-

•

Monotonicity. whenever with (and for finite values of );

-

•

Stability. For every , the scheme has a solution on that is uniformly bounded independently of (under the CFL condition, see above);

-

•

Consistency. For any and , we have (under the condition, see above):

-

•

Strong uniqueness. if the locally bounded USC [resp. LSC] function [resp. ] is a viscosity subsolution [resp. supersolution] of (12) then in ;

Proposition 1.

Proof.

This follows by verification of the assumptions in [5, 4, Theorem 2.1]: strong uniqueness comes from our comparison theorem, existence from Corollary 1. Monotonicity, stability and consistency follow by a direct calculation which we do not spell out here. The rest of the proof is given by following closely [5, 4, Theorem 2.1] combined with the remarks on the first example in [4, Section 5]: one first shows that the operator approximates the diffusion component of (12) and subsequently adds the barrier to recover the full equation (12). One finally concludes as in [4, p130] by semi-relaxed limits in combination with our comparison result, Theorem (5). ∎

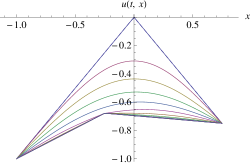

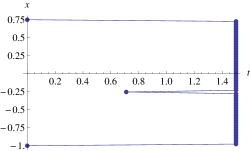

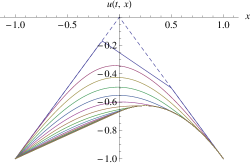

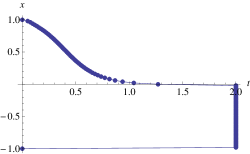

4.2. and of unbounded support

For simplicity we restrict ourselves to embeddings into Brownian motion (i.e. ). In this case recent results of Jakobsen [33] apply and give a convergence rate of order . Denote and consider schemes of the type

where is the (formal) solution operator associated to the heat equation . In the case that we use a finite difference method this scheme can be written as

| (32) |

A direct calculation also shows that this is equivalent to (see Jakobsen [33, page 11 in Section 3])

and above representation is advantageous for the proof.

Proposition 2 ([33, Section 3]).

5. a comparison for obstacle pdes and a lemma about jets

Comparison theorems for obstacle problems can be found in the literature, see [34, 33, 23]. However, due to the unboundedness of the coefficients as well as space they do not cover our setup. We provide a complete proof by revisiting work of [34, 33, 20]. It also establishes Hölder regularity in space of viscosity solutions.

5.1. A Comparison Theorem for the obstacle problem

Theorem 5.

Let be of linear growth, i.e. such that

and Lipschitz in space, uniformly in time (). Define

Let be a viscosity subsolution and a viscosity supersolution of the PDE

Further assume that , for some constant and that and are -Hölder continuous. Then there exists a constant s.t.

Direct consequences of this estimate are

-

(i)

implies on ,

-

(ii)

if is also a supersolution (viz. is a viscosity solution) then is -Hölder continuous in space uniformly in time on , i.e.

Proof.

Wlog we can replace the parabolic part in with (by replacing resp. with resp. ). Further we can assume that , is a subsolution of

| (33) | |||||

(by replacing with ). Define for ,

and

The growth assumptions on and together with (33) guarantee for every , the existence of a triple s.t.

The proof strategy is classic: the above implies that and

| (34) |

Using the Hölder continuity of and we immediately get an upper bound for

and below we use the parabolic theorem of sums to show that

| (35) |

where is a modulus of continuity for every . Plugging these two estimates into (34) gives

Now letting and subsequently optimizing over yields the key estimate

Applying it with gives point ((i)) of our statement. Applying it with a viscosity solution gives

and the estimate yields the -Hölder regularity.

It remains to show (35). Below we assume and derive the upper bound (35) (which then also holds if ). Note that implies . The parabolic Theorem of sums [18, Theorem 8.3] shows existence of

such that

| (36) |

Since is a subsolution resp. is a supersolution

and subtracting the second inequality from the first leads to

First assume the second term in the is less than or equal to . This gives

hence we get the estimate

| (37) |

Now assume the first term in the is less than or equal to . This gives

hence from the definition of resp. it then follows that

Estimate the rhs by multiplying the matrix inequality (36) from the left respectively right with the vector resp. to get

| (38) | |||||

By adding (37) and (38) together and choosing we finally get

We estimate the sum of the first two terms on the rhs by using that and the last term using linear growth of to arrive at

By lemma (3) we can replace by a modulus (i.e. for every , , and is non-decreasing), i.e.

Hence we have shown that

and

∎

Lemma 3.

Let and bounded from above. Set

Denote with points where the is attained. Then

-

(i)

,

-

(ii)

.

Proof.

By definition of a supremum there exists for every a triple such that . Fix and take small enough s.t. . Then we have

Since can be arbitrary small and is non-increasing the first claim follows. From the above estimate and the boundedness of from above also show that

is bounded. Hence there exists a subsequence of which we denote with slight abuse of notation again as which converges to some limit denoted (). Now

and from the first part we can send to along the subsequence and see that , hence . Since we have shown that every subsequence converges to the second statement follows. ∎

5.2. A Lemma about sup- and superjets

We now provide the proof of the Lemma that plays a crucial role in the proof of Theorem (2). It describes the elements in the sub and superjets and for functions which are only left- and right-differentiable.

Lemma 4.

Let and assume that , has a left- and right-derivative, i.e. the following limits exist

If then

If then and if then , (). In all the above cases, if is additionally twice continuously differentiable in space then

Proof.

Every element fulfills

Applied with a sequence it follows after dividing by and letting that . If then for we have

which leads after taking resp. to

and hence contradicts the assumption . The other statements follow similarly.∎

Acknowledgement 1.

PG is grateful for partial support from the European Research Council under the European Union’s Seventh Framework Programme (FP7/2007–2013)/ERC grant agreement nr. 258237. and nr. 291244. HO is grateful for partial support from the European Research Council under the European Union’s Seventh Framework Programme (FP7/2007–2013)/ERC grant agreements nr. 258237 and nr. 291244. GdR is also affiliated with CMA/FCT/UNL, 2829-516 Caparica, Portugal. GdR acknowledges partial support by the Fundação para a Ciência e a Tecnologia (Portuguese Foundation for Science and Technology) through PEst-OE/MAT/UI0297/2011 and PEst-OE/MAT/UI0297/2014 (CMA - Centro de Matemática e Aplicações).

Acknowledgement 2.

The authors would like to thank Alexander Cox, Martin Keller–Ressel, Jan Obłój and Johannes Ruf for helpful conversations.

References

- [1] S. Ankirchner, D. Hobson, and P. Strack. Finite, integrable and bounded time embeddings for diffusions. ArXiv e-prints, June 2013.

- [2] Stefan Ankirchner, Gregor Heyne, and Peter Imkeller. A BSDE approach to the Skorokhod embedding problem for the Brownian motion with drift. Stoch. Dyn., 8(1):35–46, 2008.

- [3] Stefan Ankirchner and Philipp Strack. Skorokhod embeddings in bounded time. Stochastics and Dynamics, 11(02n03):215–226, 2011.

- [4] G. Barles, Ch. Daher, and M. Romano. Convergence of numerical schemes for parabolic equations arising in finance theory. Math. Models Methods Appl. Sci., 5(1):125–143, 1995.

- [5] G. Barles and P. E. Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Anal., 4(3):271–283, 1991.

- [6] G. Barles and P.E. Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. In Decision and Control, 1990., Proceedings of the 29th IEEE Conference on, pages 2347 –2349 vol.4, dec 1990.

- [7] Guy Barles. A new stability result for viscosity solutions of nonlinear parabolic equations with weak convergence in time. C. R. Math. Acad. Sci. Paris, 343(3):173–178, 2006.

- [8] M. Beiglböck and N. Juillet. On a problem of optimal transport under marginal martingale constraints. arXiv 1208.1509, August 2012.

- [9] Mathias Beiglböck and Martin Huesmann. Optimal transport and skorokhod embedding. arXiv preprint arXiv:1307.3656, 2013.

- [10] A. Bensoussan and J.L. Lions. Applications of variational inequalities in stochastic control, volume 12. North Holland, 1982.

- [11] R. Buckdahn, J. Huang, and J. Li. Regularity properties for general HJB equations: a backward stochastic differential equation method. SIAM J. Control Optim., 50(3):1466–1501, 2012.

- [12] R. Chacon and J. Walsh. One-dimensional potential embedding. Séminaire de Probabilités X Université de Strasbourg, pages 19–23, 1976.

- [13] R. V. Chacon. Potential processes. Trans. Amer. Math. Soc., 226:39–58, 1977.

- [14] Rene Chacon. Barrier stopping times and the filling scheme. PhD Dissertation, University of Washington, 1985.

- [15] A. M. G. Cox and J. Wang. Optimal robust bounds for variance options. ArXiv e-prints, August 2013.

- [16] Alexander M. G. Cox and Jiajie Wang. Root’s barrier: Construction, optimality and applications to variance options. The Annals of Applied Probability, 23(3):859–894, 06 2013.

- [17] AMG Cox and G Peskir. Embedding laws in diffusions by functions of time. arXiv preprint arXiv:1201.5321, 2012.

- [18] M. G. Crandall, H. Ishii, and P.-L. Lions. User’s guide to viscosity solutions of second order partial differential equations. Bull. Amer. Math. Soc. (N.S.), 27(1):1–67, 1992.

- [19] Michael G. Crandall, Hitoshi Ishii, and Pierre-Louis Lions. User’s guide to viscosity solutions of second order partial differential equations. Bull. Amer. Math. Soc. (N.S.), 27(1):1–67, 1992.

- [20] J. Diehl, P. Friz, and H. Oberhauser. Parabolic comparison revisited and applications. 2014. In press.

- [21] Hermann Dinges. Stopping sequences. In Séminaire de Probabilités VIII Université de Strasbourg, pages 27–36. Springer, 1974.

- [22] B. Dupire. Arbitrage bounds for volatility derivatives as free boundary problem. Presentation at PDE and Mathematical Finance, KTH, Stockholm, 2005.

- [23] N. El Karoui, C. Kapoudjian, E. Pardoux, S. Peng, and M.C. Quenez. Reflected solutions of backward SDEs, and related obstacle problems for PDEs. the Annals of Probability, 25(2):702–737, 1997.

- [24] N. El Karoui, S. Peng, and M. C. Quenez. Backward stochastic differential equations in finance. Math. Finance, 7(1):1–71, 1997.

- [25] W. H. Fleming and H. M. Soner. Controlled Markov processes and viscosity solutions, volume 25 of Stochastic Modelling and Applied Probability. Springer, New York, second edition, 2006.

- [26] Wendell H. Fleming and H. Mete Soner. Controlled Markov processes and viscosity solutions, volume 25 of Stochastic Modelling and Applied Probability. Springer, New York, second edition, 2006.

- [27] A. Galichon, P. Henry-Labordère, and N. Touzi. A stochastic control approach to no-arbitrage bounds given marginals, with an application to lookback options. The Annals of Applied Probability, 24(1):312–336, 02 2014.

- [28] Paul Gassiat, Aleksandar Mijatovic, and Harald Oberhauser. An integral equation for Root’s barrier and the generation of Brownian increments. Annals of Applied Probability (in press), 2014.

- [29] Pierre Henry-Labordere, Jan Obloj, Peter Spoida, and Nizar Touzi. Maximum maximum of martingales given marginals. arXiv preprint arXiv:1203.6877, 2012.

- [30] F. Hirsch and B. Roynette. A new proof of Kellerer’s theorem. ESAIM: Probability and Statistics, to appear, 2012.

- [31] D. Hobson. The Skorokhod Embedding Problem and Model-Independent Bounds for Option Prices. In Paris-Princeton Lectures on Mathematical Finance 2010, volume 2003 of Lecture Notes in Mathematics, pages 267–318. Springer Berlin / Heidelberg, 2011.

- [32] David G Hobson. Robust hedging of the lookback option. Finance and Stochastics, 2(4):329–347, 1998.

- [33] E.R. Jakobsen. On the rate of convergence of approximation schemes for bellman equations associated with optimal stopping time problems. Mathematical Models and Methods in Applied Sciences, 13(05):613–644, 2003.

- [34] E.R. Jakobsen and K.H. Karlsen. Continuous dependence estimates for viscosity solutions of fully nonlinear degenerate parabolic equations. Journal of Differential Equations, 183(2):497–525, 2002.

- [35] Hans G Kellerer. Markov-komposition und eine Anwendung auf Martingale. Mathematische Annalen, 198(3):99–122, 1972.

- [36] Jack Kiefer. Skorohod embedding of multivariate rv’s, and the sample df. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 24(1):1–35, 1972.

- [37] Victor Kleptsyn and Aline Kurtzmann. A counter-example to the cantelli conjecture. arXiv preprint arXiv:1202.2250, 2012.

- [38] R. M. Loynes. Stopping times on Brownian motion: Some properties of Root’s construction. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 16:211–218, 1970.

- [39] Terry R McConnell. The two-sided stefan problem with a spatially dependent latent heat. Transactions of the American Mathematical Society, 326(2):669–699, 1991.

- [40] D. Nualart. The Malliavin calculus and related topics. Probability and its Applications (New York). Springer-Verlag, Berlin, second edition, 2006.

- [41] Diana Nunziante. Existence and uniqueness of unbounded viscosity solutions of parabolic equations with discontinuous time-dependence. Nonlinear Anal., 18(11):1033–1062, 1992.

- [42] J. Obłój. The Skorokhod embedding problem and its offspring. Probab. Surv., 1:321–390, 2004.

- [43] J. Obłój. On some aspects of Skorokhod embedding problem and its applications in mathematical finance. Notes for the students of the 5th European summer school in financial mathematics, 2012.

- [44] Jan Obłój and Peter Spoida. An iterated Azéma–Yor type embedding for finitely many marginals. arXiv preprint arXiv:1304.0368, 2013.

- [45] D. H. Root. The existence of certain stopping times on Brownian motion. Ann. Math. Statist., 40:715–718, 1969.

- [46] H. Rost. Die Stoppverteilungen eines Markoff-Prozesses mit lokalendlichem Potential. Manuscripta Math., 3:321–329, 1970.

- [47] H. Rost. The stopping distributions of a Markov Process. Invent. Math., 14:1–16, 1971.

- [48] H. Rost. Skorokhod’s theorem for general Markov processes. In Transactions of the Sixth Prague Conference on Information Theory, Statistical Decision Functions, Random Processes (Tech. Univ. Prague, Prague, 1971; dedicated to the memory of Antonín Špaček), pages 755–764. Academia, Prague, 1973.

- [49] H. Rost. Skorokhod stopping times of minimal variance. In Séminaire de Probabilités, X (Première partie, Univ. Strasbourg, Strasbourg, année universitaire 1974/1975), pages 194–208. Lecture Notes in Math., Vol. 511. Springer, Berlin, 1976.