A penalized empirical likelihood method in high dimensions

Abstract

This paper formulates a penalized empirical likelihood (PEL) method for inference on the population mean when the dimension of the observations may grow faster than the sample size. Asymptotic distributions of the PEL ratio statistic is derived under different component-wise dependence structures of the observations, namely, (i) non-Ergodic, (ii) long-range dependence and (iii) short-range dependence. It follows that the limit distribution of the proposed PEL ratio statistic can vary widely depending on the correlation structure, and it is typically different from the usual chi-squared limit of the empirical likelihood ratio statistic in the fixed and finite dimensional case. A unified subsampling based calibration is proposed, and its validity is established in all three cases, (i)–(iii). Finite sample properties of the method are investigated through a simulation study.

doi:

10.1214/12-AOS1040keywords:

[class=AMS]keywords:

T1Supported in part by NSF Grants DMS-07-07139 and DMS-10-07703.

and

1 Introduction

In a seminal paper, Owen (1988) introduced the empirical likelihood (EL) method for statistical inference on population parameters in a nonparametric framework, and showed that it enjoyed properties similar to the likelihood-based inference methods in a more traditional parametric framework. Following Owen (1988), the EL method has been extended to various complex inference problems; see, for example, Diccicio, Hall and Romano (1991), Hall and Chen (1993), Qin and Lawless (1994), Owen (2001), Bertail (2006), Hjort, McKeague and Van Keilegom (2009), Chen, Peng and Qin (2009) and the references therein. An extension of the EL method in the high-dimensional context, where the dimension of the observations increases with the sample size , is given by Hjort, McKeague and Van Keilegom (2009). Hjort, McKeague and Van Keilegom (2009) derives the limit distribution of the EL ratio statistic based on -dimensional estimating equations when with at the rate . Chen, Peng and Qin (2009) improved upon the rate restriction in Hjort, McKeague and Van Keilegom (2009) and established a nondegenerate limit distribution of the EL ratio statistic, allowing under suitable regularity conditions.

For applications to high-dimensional problems, such as those involving gene expression data, one encounters a that is typically much larger than the sample size . However, extension of the EL to such high-dimensional problems is itself a daunting task because the (standard) EL method is known to fail in such situations. An important result of Tsao (2004) shows that the definition of the EL for a -dimensional population mean based on a sample size breaks down on a set of positive probability whenever ; further, this probability is asymptotically nonnegligible. The main reason for this surprising behavior of the EL is that for , the convex hull of random vectors in is too small a set to contain the true mean with high probability. As a result, the standard EL approach cannot be applied to the “large small ” problems with . An alternative formulation of the EL in such situations (called the adjusted EL) is given by Chen, Variyath and Abraham (2008), which is further refined and studied by Emerson and Owen (2009). The adjusted EL method adds additional pseudo-observations [a single one in Chen, Variyath and Abraham (2008) and two in Emerson and Owen (2009)] so as to cover a hypothesized value of the mean parameter within the convex hull of the augmented data set, thereby making the adjusted EL well-defined. A second approach, due to Bartolucci (2007), is to drop the convex hull constraint in the formulation of the EL altogether and redefine the likelihood of a hypothesized value of the parameter by penalizing the unconstrained EL using the Mahalanobis distance. The penalized EL (PEL) of Bartolucci (2007) is well defined for all values of , as long as the sample covariance matrix is nonsingular. However, due to the use of the inverse of the sample covariance matrix in its formulation, the PEL of Bartolucci (2007) is also not well defined for . Bartolucci (2007) establishes a chi-squared limit of the PEL for the population mean in the case where the dimension is fixed and finite for all . Other variants of the PEL where a penalty function is added to the standard EL, in the spirit of the penalized likelihood work of Fan and Li (2001) and Fan and Peng (2004), are considered by Otsu (2007) and Tang and Leng (2010). Both these papers consider the high dimensional set up and establish validity of their methods still requiring to grow at most as a fractional power of the sample size . In this paper, we introduce a modified version of the PEL method of Bartolucci (2007) that is computationally simpler and that is applicable to a large class of “large small ” problems, allowing to grow faster than . This is an important step in generalizing the EL in high dimensions beyond the threshold where the standard EL and its existing variants fail.

To briefly describe the proposed methodology and the main results of the paper, suppose that are independent and identically distributed (i.i.d.) -valued random vectors with mean , . Denote the th component of a -vector by , . The proposed PEL employs a multiplicative penalty term to penalize the likelihood of a hypothesized value of the population mean as a quadratic function of the distance between the sample mean and . However, unlike Bartolucci’s (2007) method, the use of the inverse sample covariance matrix is completely avoided, as consistency of the sample covariance matrix in the high dimensional case for all the dependence structures that we consider in this paper is not guaranteed. The proposed PEL instead uses a component-wise scaling to bring up the varying degrees of variability (variances) along different components to a common level, and then it applies an overall penalty on the sum of the squared rescaled differences; see (1) in Section 2 below. As a result, the proposed PEL is well-defined for all values of . Further, this approach has the added advantage that it does not require inversion of a high-dimensional matrix, and therefore, it is computationally much simpler.

For investigations into the theoretical properties of the proposed PEL method, we allow the components of to be dependent. The range of dependence that we consider covers the cases of: {longlist}[(iii)]

short-range dependence (SRD), where roughly speaking, the average of the components of satisfies a central limit theorem (CLT) under suitable moment conditions; cf. Ibragimov and Linnik (1971);

long-range dependence (LRD), where under suitable regularity conditions, the average of the components satisfies noncentral limit theorems [Taqqu (1975, 1977), Dobrushin and Major (1979)];

nonergodicity (NE), where the dependence is so strong that the average of the components even fails to satisfy a (strong) law of large numbers. We refer to the LRD and SRD cases collectively as the ergodic (E)-case, as the negative logarithm of the PEL ratio statistic (say) here satisfies a law of large numbers without further centering and scaling, for any rate of growth of ; cf. Remark 4.2 below. However, such degenerate limits laws are not always the most useful in practice as these only lead to conservative large sample inference procedures. By using suitable centering and scaling, we are able to further refine these results and establish convergence in distribution to nondegenerate limits. Specifically, we show that under SRD, with centering at 1 [for in condition (C.2)(ii) below] and scaling by square-root of the dimension of the observations converges to a Normal limit, very much like the results of Hjort, McKeague and Van Keilegom (2009) and Chen, Peng and Qin (2009), but allowing a much faster rate of growth of and allowing a more general dependence framework. In the long range dependent (also abbreviated as LRD) case, with a suitable normalization can have both Normal and non-Normal limits. For the Normal limit, the centering and the scaling sequences are the same as those used in the SRD case, except at the boundary layer of dependence where the Normal limit switches over to the non-Normal limit. For the non-Normal limit under LRD, the centering term is the same as that in the SRD case, but the scaling depends on the rate of decay of the auto-correlation coefficient of the components of (up to a possibly unknown permutation). Finally, in comparison to the E-case, in the NE-case is shown to converge in distribution to a stochastic integral, and it does NOT require any further centering and scaling.

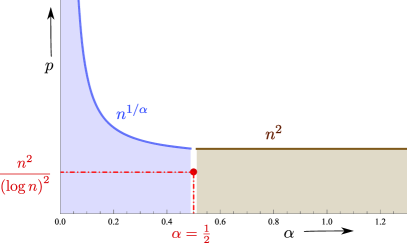

The growth rate of , for which a nondegenerate limit law holds for a suitably transformed , primarily depends on the strength of dependence among the components of the observations; cf. Figure 1. In the NE-case, can grow arbitrarily fast (e.g., polynomial, exponential, super-exponential, etc.) as a function of . In the E-case, although a degenerate limit law holds for an arbitrary growth rate of , for a nondegenerate limit, must admit a suitable upper bound. In particular, for the Normal limit in the E-case (excluding the boundary case), the growth rate of as a function of is . For the non-Normal limit under the E-case, for where, roughly speaking, denotes the exponent of the rate of decay of the autocorrelation among the components of , up to a permutation; cf. condition (C.4)α, Section 3. The boundary case is given by , where the growth rate is slightly smaller and is given by . From Figure 1, it follows that the stronger the dependence among the components of the observations, the higher is the allowable growth rate of as a function of for a nondegenerate limit. The limiting case is the NE-case. Here the nondegenerate limit for the the negative logarithm of the PEL ratio statistic holds for an arbitrary growth rate of as a function of .

It is worth pointing out that in most cases, the limit distribution of the PEL ratio statistic is not distribution free in the sense that the asymptotic approximation to the distribution of the PEL ratio statistic requires the knowledge of one or more unknown population parameters. As a result, the limit laws are not directly usable in practice. To address this issue, we propose a calibration procedure based on the subsampling method. We show that under mild conditions, the subsampling based calibration method is consistent under all three types of dependence structures.

The key step in the proofs is to derive a quadratic asymptotic approximation to under all three cases of dependence. This is presented in Lemma 6.2 for the NE-case and in the proof of Theorem 3.2 for the E-case. The derivation of the limit law in the NE-case uses some weak convergence and operator convergence results on Hilbert spaces. On the other hand, in the E-case, refined approximations to are required to go beyond their degenerate limits. See Section 6 for more details.

The rest of the paper is organized as follows. In Section 2, we describe the PEL methodology. In Section 3, we introduce the asymptotic framework and establish the limit distributions of the logarithm of the PEL ratio statistic under the three dependence scenarios. In Section 4, we describe the subsampling method and prove its validity for all three cases. We report the results from a moderately large simulation study in Section 5. Proofs of the results are given in Section 6.

2 Formulation of the PEL

Let be i.i.d. random vectors with mean . Let denote the th component of , , . Also, let denote the transpose of a matrix . We define the penalized empirical likelihood (PEL) of a plausible value of the population mean as

| (1) |

where : , ’s are component specific weights (which may be random), and is an overall penalty factor. Here we use

| (2) |

where is the sample variance of the th components of , and where denotes the indicator function. This choice of the component-wise scaling allows us to adjust for the heteroscedasticity along different co-ordinates of and therefore, the overall penalization parameter gives comparable weights to all components. In addition, the choice of the penalty function makes the proposed PEL invariant with respect to component-wise scaling, which is an inherently desirable property, particularly while dealing with high-dimensional variables, where the assumption of homoscedasticity among a large number of components is unrealistic. The maximizer of the product in (1) without the penalty term is given by for . Hence, the PEL ratio statistic at a plausible value of the mean vector is defined as

We now compare our formulation with the PEL of Bartolucci (2007), which is defined as

| (3) |

where , is the sample covariance matrix, and is a penalty parameter. Note that for a large , the sample variance matrix is ill-conditioned, if the smallest eigen-value of the underlying covariance matrix (say) of is not bounded away from zero, and it is always singular when , requiring further modifications to make (3) well defined. Under either of the two scenarios, the PEL based on (3) can be computationally demanding and unstable. In comparison, the component-wise scaling in (1) only involves -dimensional operations which is computationally much simpler and feasible even for a large . A second limitation of (3) is the lack of attractive theoretical properties of (or of its variants) in high dimensions. Indeed, consistency of the sample covariance matrix (and its banded or tapered versions) in the high-dimensional setting is questionable in presence of strong correlations among the components of that we consider here. Existing work on consistency of the sample covariance matrix is known only under suitable conditions of sparsity or weak dependence; cf. Bickel and Levina (2008), El Karoui (2008), Cai, Zhang and Zhou (2010). Our formulation also avoids this problem altogether by using component-wise scaling.

For the sake of completeness, we also briefly describe the penalized EL approach of Otsu (2007) and Tang and Leng (2010), specialized to the case of the mean parameter for simplicity of exposition. Let denote the standard EL for . Also, let be a penalty function, such as the smoothly clipped absolute deviation (SCAD) penalty function of Fan and Li (2001). Then, the penalized EL considered by Otsu (2007) and Tang and Leng (2010) is of the form

| (4) |

where . For the case of a more general parameter defined through a set of estimating equations, the formulation of Otsu (2007) and Tang and Leng (2010) replaces in (4) by the corresponding version of the standard EL for ; cf. Qin and Lawless (1994). As a result, irrespective of the target parameter, since (4) is directly based on the standard EL, this formulation of the penalized EL also suffers from the same limitations as the standard EL. In particular, this approach also fails in high dimensions whenever .

3 Limit distributions

3.1 General framework

We establish the limit distribution theory for the PEL ratio statistic in a triangular array set up, with denoting the variable driving the asymptotics. Thus, the vectors depend on as are their distributions and the dimension . However, we often suppress the dependence on for simplicity of notation. The limit distribution of the PEL ratio statistic depends on the degree of dependence among the components of . As stated in Section 1, we can broadly classify the dependence structure into two categories: (i) Non-Ergodic (NE) and (ii) Ergodic (E). In the NE-case, the dependence among the components of each is so strong [cf. condition (C.3) below] that even the law of large numbers fails. In this case, we show that under appropriate conditions, the PEL ratio statistic has a nondegenerate limit. In contrast, in the E-case, the corresponding limit is degenerate, and further centering and scaling are needed for nondegenerate limit laws which, in turn, depend the type of dependence (SRD or LRD). We begin with the NE-case.

3.2 Limit distribution for the nonergodic case

We need to introduce some notation at this stage. Let denote the correlation between and , . Let and , , . Write to denote a generic constant in . Also, for any two sequences and , write if as . Let denote the set of all square integrable functions on (with respect to the Lebesgue measure on ), equipped with the inner product , . Let denote a complete orthonormal basis of , where denotes the set of all positive integers. For any (bounded) jointly measurable function , define the operator on by for . For , let .

We shall make use of the following conditions for deriving the limit distribution of . The values of the integers and below will be specified later in the statements of the theorems.

-

[(C.3)]

-

(C.1)

(i) for a given .

-

[(ii)]

-

(ii)

.

-

-

(C.2)

(i) For a given ,

-

[(ii)]

-

(ii)

for some .

-

-

(C.3)

There exists a correlation function of a mean-square continuous process on , and for each , there exists a permutation of such that . Further, with as in (C.2), satisfies the following:

-

[(iii)]

-

(i)

;

-

(ii)

for all for some function satisfying as and for some function satisfying

-

(iii)

converges, where with .

-

We now briefly comment on the conditions. Condition (C.1)(i) is a moment condition on the scaled component-wise weights ’s and requires finiteness of the th negative moment of the sample variance ’s (scaled by the respective expected values ’s). This condition holds in the case of Gaussian ’s whenever the the sample size . Condition (C.1)(ii) is a mild condition—it says that none of the ’s take a single value with probability approaching one. This condition trivially holds if the components of are continuous and also in the discrete case, if the supports of ’s contain at least two values with asymptotically nonvanishing probabilities. Condition (C.2)(i) is a moment condition that will be used with different values of in the main theorems of this section, while (C.2)(ii) specifies the growth rate of the penalty parameter for a nondegenerate limit of . However, unlike the standard usage of the penalty parameter in the context of variable selection, where different choices of the parameter lead to different sets of variables being chosen, here the key role of the penalty parameter is to stabilize the contribution from the sum of component-wise squared differences to the overall “likelihood” in (1). Finally, consider condition (C.3) that specifies the nonergodic structure of the ’s. Note that, up to a (possibly unknown) permutation of the co-ordinates, the components of are essentially correlated as strongly as the variables ’s coming from a constant mean, mean-square continuous process (say) with covariance function . In this case, the dependence among the variables and , is so strong that the average may not converge to a constant as , as one would expect from the well-known ergodic theorems.

Under conditions (C.1)–(C.3), the limit distribution of the log-PEL ratio statistic is given by a stochastic integral, as shown by the following result.

Theorem 3.1

Let conditions (C.1), (C.2) and (C.3) hold with and , let denote the true value of and let as . Then

| (5) |

where is a zero mean Gaussian process on with covariance function and where the function is defined as

| (6) |

with , and for ,

For a general definition of a stochastic integral of the form (5), see Cramer and Leadbetter (1967). Note that under condition (C.3), by repeated application of the Cauchy–Schwarz inequality, for ,

and hence, the limiting stochastic integral is well defined.

Theorem 3.1 shows that under a suitable choice of the penalty parameter, namely, , the negative log PEL ratio statistic has a nondegenerate limit distribution. Note that, unlike the standard version of the EL, we do not use the multiple before . This is a direct artifact of the additional penalty term that we use in the formulation of PEL. Also, unlike most high-dimensional problems where the validity of a large sample inference procedure breaks down beyond a certain (often exponential) rate of growth of , the PEL and the associated limit distribution of in the NE-case remains valid for arbitrary rate of growth of as a function of the sample size. Thus, in the NE-case, it is possible to carry out simultaneous hypothesis testing for a very large number of parameters even with a moderately large sample.

3.3 Limit distribution for the ergodic case

In the E-case, we shall make use of the following conditions, for :

[(C.4)α]

There exists a covariance function on and for each , there exists a (possibly unknown) permutation of such that as and

There exists a constant such that

where denotes the -mixing coefficient of the variables , defined by . Here, denotes the -field generated by , , and is the inverse of the permutation in (C.4)α.

Condition (C.4)α says that up to a (possibly unknown) permutation of the coordinates, the components of the -vectors have a dependence structure that is asymptotically similar to the one given by . Note that the sum diverges if and only if , and therefore, we classify the dependence structure of the ’s as LRD or SRD according to or , respectively; cf. Beran (1994). Condition (C.5)α is a decay condition on the -mixing coefficient of the reordered variables . Note that by (C.4)α, the correlation coefficient between and is , and therefore, the re-ordered sequence behaves approximately like a stationary time series with the natural time-index . Thus, condition (C.5)α specifies the degree of dependence of the ’s, up to a permutation that need not be known to the user.

3.3.1 Results under short-range dependence

The following result shows that the log-PEL ratio statistic in the SRD case converges to a Normal limit after a suitable centering and after scaling by the “standard factor” .

Theorem 3.2

Let conditions (C.1), (C.2) and (C.4)α, (C.5)α hold for some , . Let . Then, for ,

| (7) |

We now comment on Theorem 3.2. From the proof, it follows that the distribution of the log-PEL ratio statistic, for a given sample size, is close to the sum of weakly dependent chi-squared random variables with one degree of freedom. As a result, centering at 1 and scaling by yields a nondegenerate Normal limit. The effect of the weak dependence shows up in the variance of the limiting Normal distribution, which depends on the correlation structure of the components of . It is worth noting that in the SRD case, one can use Normal critical points with an estimated variance to calibrate simultaneous tests of hypotheses using the EL.

Theorem 3.2 extends existing results on the EL in more than one direction. Hjort, McKeague and Van Keilegom (2009) and Chen et al. (2009) proved a version of the result (i.e., a Normal limit) for the standard log-EL ratio statistic in increasing dimensions with centering at 1 and scaling by . In comparison, Theorem 3.2 relaxes the restriction on the dimension of the parameter , by allowing it to grow faster than the sample size. This should be compared with the best available rate of , obtained by Chen et al. (2009). Further, Theorem 3.2 covers a wide range of dependence structures of the components of ’s which are not covered by the earlier results (e.g., here the minimum eigen-value of the covariance matrix of need not be bounded away from zero). However, the most important implication of Theorem 3.2 is that under SRD, the penalization step circumvents the limitation of the standard EL which is known to break down beyond the threshold , as shown by Tsao (2004).

3.3.2 Results under long-range dependence

For , the sum fails to converge absolutely, and we refer to this as the LRD case. Sums of LRD random variables are known to have either a Normal or a non-Normal limit, depending on the value of . The next result deals with the case where can be very small, and the limit law is non-Normal. Further, the scaling also depends on the correlation decay parameter , as shown by Theorem 3.3. Let and .

Theorem 3.3

Let conditions (C.1), (C.2) and (C.4)α, (C.5)α hold for some , and . If , then

| (8) |

where is defined in terms of a bivariate Wiener–Itô integral with respect to the random spectral measure of the Gaussian white noise process as

Theorem 3.3 shows that under very strong dependence (i.e., for small values of ) in the E-case, the log-PEL ratio statistic, with the same centering but a different scaling factor, has a nondegenerate limit distribution and the limit law is non-Normal. Further, the range for which the result holds is , which is a decreasing function of . Thus, the stronger the dependence among the co-ordinates of ’s, the larger is the allowable growth rate of as a function of for the validity of the limit distribution.

Theorems 3.2 and 3.3 exhaust the types of limit laws for the log-PEL ratio statistic in the E-case. However, in terms of the rate of decay of the correlation function, these leave out the case where . Although corresponds to LRD in the traditional sense, the centered and scaled versions of the log-PEL ratio statistic continue to have a Normal limit as shown by the following result. Curiously, the scaling sequence as well as the growth rate of depend on whether or .

Theorem 3.4

Let conditions (C.1), (C.2) and (C.4)α, (C.5)α hold for some , . {longlist}[(ii)]

If and , then (7) holds.

If and , then

| (9) |

Thus, it follows from Theorem 3.4 that the log-PEL ratio statistic is asymptotically Normal for all , although the components of ’s have LRD when . The peculiar behavior of the scaling sequence at the boundary value is essentially determined by the growth rate of the series as , which is asymptotically equivalent to for but it is bounded for .

Remark 3.1.

Proofs of Theorems 3.2–3.4 show that for any , , that is, the log-PEL ratio statistic has a degenerate limit under all sub-cases of the E-case, for arbitrarily large as a function of . However, for nondegenerate limits, refined approximations to the difference are needed. Here, we are able to show that an approximation of the form

| (10) |

holds for all sub-cases of the E-case, where is a centered sum and where is an error term, roughly of the order of . Further, has a nondegenerate limit up to a suitable scaling, as a function of , depending on the dependence structure of the ’s. The bounds on the growth rate of in the different sub-cases of the E-case are then determined by the requirement that the scaled error term be asymptotically negligible. For example, in the SRD case, and hence, if and only if , which is equivalent to the bound . Similar considerations lead to the respective upper bounds in the other sub-cases of the E-case.

Remark 3.2.

It is worth pointing out that the PEL can be used for constructing “conservative” large sample simultaneous tests of the hypotheses for arbitrarily large in the E-case. Indeed, for growing faster than the upper bounds given in Theorems 3.2–3.4, a conservative large sample simultaneous test of rejects if . Note that by (10), this test attains the ideal level asymptotically.

4 A subsampling based calibration

In this section, we describe a nonparametric calibration method based on subsampling to approximate the quantiles of the nondegenerate limit laws in both E- and NE-cases, which typically involve unknown population parameters and hence, cannot be used directly in practice. Let be a subset of where is of size and where (specific conditions on are given below). On each , we employ the PEL method and obtain a version of the PEL ratio statistic , by replacing with and by in the definitions . First consider the NE case. Here, the subsampling estimator of the distribution function under the null hypothesis is given by

where is a collection of subsets of of size and where denotes the size of a set . All possible subsets of size cannot be used mainly due to the sheer number of such sets, and hence, only a small fraction of these subsets are used to compute in practice. In view of the block resampling methods for time series data, here we shall take to be the collection of all overlapping blocks (subsets) of size contained in . Then, we have the following result in the NE case.

Theorem 4.1

Next consider the E-case. Note that for , the limit of the log-PEL ratio statistic is , which is distribution free. One can carry out a simple test [cf. Beran (1994)] to ascertain if “” is true and then use the limit distribution directly to conduct the PEL test of the simultaneous hypotheses using the critical points, without the need for an alternative calibration. As a result, we concentrate on the values of in the E-case. Let be an estimator of the correlation parameter ; cf. Remark 4.1 below. Let denote the PEL ratio statistic based on the subsample under , and define

where . Then, a subsampling estimator of the distribution of is given by and we have the following results.

Theorem 4.2

Suppose that there exists a such that

| (12) |

[(ii)]

Theorem 4.2 shows that for both Normal and non-Normal limit laws under the E-case, the subsampling method provides a valid approximation to the distribution of the log-PEL ratio statistic. Hence, one can use the quantiles of the subsampling estimators to calibrate simultaneous tests on in a unified manner. This is specially important in the case of non-Gaussian limit laws for which the quantiles are difficult to derive. However, for , the limit distribution is Gaussian, and an alternative approximation can be generated by using a Normal distribution with an estimated variance. Indeed, the latter may be preferable to subsampling from the computational point of view.

Remark 4.1.

In practice, the value of is not known and must be estimated. First consider the case where the permutation in (C.4)α is known. Then, we are essentially dealing with i.i.d. copies of a time series of length as observations. By using the replicates of the time series, it is easy to modify standard estimators of based on a single time series [cf. Beran (1994)] to construct an estimator of satisfying , which clearly satisfies (12) with .

Next consider the case where the permutations are unknown. In this case, it is not possible to identify pairs , that correspond to the lag- correlation . However, it is still possible to construct estimators of that satisfy (12). Define

| (14) |

where and (and and ) are as in (2). Note that is invariant under permutations of the components of ’s and also under component-wise location and scale transformations. In Section 6, we show that satisfies (12) under the conditions of Theorem 4.2, even when is unknown. In the same spirit, we may use the following estimator of the limiting variance in Theorem 3.2 in the case where is unknown:

| (15) |

where , . Consistency of holds under mild moment conditions; cf. Section 6.

Remark 4.2.

An important factor that impacts the accuracy of the subsampling method is the choice of the subsample size . Note that

| (16) |

satisfies the requirements of Theorem 4.2, where . At this point, we do not know the order of the optimal for the different cases considered here. In the next section, we address this through a numerical study and explore the effects of different choices of on the performance of the PEL method.

5 Numerical study

We assess finite sample performance of the PEL method by simulation in a variety of settings. We considered different combinations of the sample size and the dimension , with and and . The testing problem we considered is , although any other value of may be used in , as the PEL criterion is location invariant. We generated i.i.d. random -vectors where the coordinates of ’s had one of the three different types of dependence structures, namely: (i) non-Ergodic, (ii) LRD and (iii) SRD, as follows.

5.1 Algorithms for generating the data

5.1.1 The nonergodic case

[(1)]

Consider the basis functions in given by for and , for and .

Generate i.i.d. and let for all .

Define , where and where are scalars in . Then, is a nonergodic series. Replicates of yield in the NE-case.

5.1.2 Long-range dependence

For the LRD case, we follow a setup similar to that used in Hall, Jing and Lahiri (1998). We generate stationary increments of a self-similar process with self-similarity parameter (or Hurst constant) for . The algorithm is as follows: {longlist}[(1)]

Generate a random sample from .

Define , where is obtained by Cholesky factorization of into and where with , and

| (17) |

and . Note that .

Replicates of give the variables in the LRD case.

5.2 Choice of the subsample size

We also considered different choices of the subsample size in order to get some insight into its effects on the accuracy of the subsampling calibration. Note that the feasible choices of the subsample size depend on the relative growth rates of both and as well as on the strength of dependence, here quantified by . For each pair , we considered three choices of the subsample size (denoted by the generic symbols ), depending on the dependence structure. Specifically, for the SRD case (), we set

where , and . Note that in this case, the random variables in form a series of length and are weakly dependent. Further, the target parameter for the subsampling method in the SRD case (and also in the LRD case with ) is the variance of the limiting Normal distribution. Hence, in view of the well-known results on optimal block length (for variance estimation) [cf. Hall, Horowitz and Jing (1995), Lahiri (2003)], the above choices of the ’s are reasonable.

| 0.0092 | 0.0063 | 0.0190 | 0.0090 | 0.0114 | 0.0162 | 0.0089 | 0.0103 | 0.0091 | |

| 0.0099 | 0.0081 | 0.0171 | 0.0045 | 0.0069 | 0.0129 | 0.0149 | 0.0134 | 0.0094 | |

| 0.0079 | 0.0031 | 0.0061 | 0.0086 | 0.0042 | 0.0081 | 0.0101 | 0.0099 | 0.0190 | |

| 0.0059 | 0.0091 | 0.0010 | 0.0020 | 0.0104 | 0.0039 | 0.0091 | 0.0159 | 0.0078 | |

| 0.170 | 0.020 | 0.075 | 0.221 | 0.142 | 0.090 | 0.075 | 0.152 | 0.227 | |

| 0.030 | 0.033 | 0.033 | 0.012 | 0.005 | 0.011 | 0.112 | 0.133 | 0.066 | |

| 0.011 | 0.045 | 0.087 | 0.123 | 0.082 | 0.018 | 0.108 | 0.027 | 0.069 | |

| 0.138 | 0.135 | 0.065 | 0.050 | 0.011 | 0.003 | 0.048 | 0.054 | 0.026 | |

Next consider the case under LRD, where the limit distribution is non-Normal. From the proofs of Theorems 3.2 and 4.2, it follows that the prescription for in (16) attempts to balance the bias of the subsampling approximation to the limit distribution and its variance. However, for a very small value of , a direct application of (16) leads to a very small fractional exponent of , which may be too small in practice. In such situations, particularly where is not very large and the LRD exponent is small, we use the threshold and set

where ’s are as before. The rationale behind this modification is that for small, we simply treat as a weakly dependent multivariate time series and again employ the known results on the optimal block size.

Finally, consider the NE-case, . Note that for , can grow at an arbitrary rate with the sample size for the validity of Theorems 3.1 and 4.1. Hence, in this case, our choice of depends only on the sample size. We consider the “canonical” choice as well as the larger values and to explore the effects of a larger subsample size on the accuracy of the subsampling calibration method.

5.3 Results

5.3.1 Levels of significance in simultaneous tests

Here we consider finite sample accuracy of the proposed PEL method for simultaneous testing of the hypotheses

| (18) |

at the levels of significance . The correlation parameter for the subsampling based calibration was estimated by averaging the Taqqu, Teverovsky and Willinger (1995) estimator of the Hurst parameter () from each of the -time series and by setting . Further, we have used the interior-point method [cf. Wright (1997)] as a fast optimization tool for computing the PEL ratio statistic, which can handle high-dimensional optimization problems efficiently. Tables 1 and 2 report the attained levels of significance based on simulation runs and for the target significance levels of and , respectively, for different values of , , and .

| 0.569 | 0.681 | 0.929 | 0.515 | 0.643 | 0.791 | 0.87 | 0.834 | 0.766 | |

| 0.66 | 0.71 | 0.85 | 0.569 | 0.903 | 0.676 | 0.794 | 0.8 | 0.868 | |

| 0.515 | 0.883 | 0.688 | 0.75 | 0.997 | 0.488 | 0.70 | 0.87 | 0.90 | |

| 0.510 | 0.622 | 0.870 | 0.739 | 0.778 | 0.996 | 0.802 | 0.790 | 0.939 | |

From the tables, it follows that the PEL does a reasonable job of simultaneous testing of hypotheses for all cases of dependence, for appropriately chosen subsample size. Comparing the attained level of significance, it is clear that the best choice of the subsample size critically depends on the relative sizes of and , and more importantly, on the type of dependence among the components of . Further, rather surprisingly, the PEL tests at the level of significance turned out to be more accurate (on an absolute scale) than at the level , for the subsample sizes considered here.

We also considered the effect of the penalty parameter on the performance of the PEL test. In the supplementary material Lahiri and Mukhopadhyay (2012) (hereafter referred to as [LM]), we report the empirical levels of significance of the PEL test for and the target level for two other choices of the constant , namely, and . The results for the choice are qualitatively similar to those reported in Table 2 (with ); in comparison, the accuracy for the case appears to be slightly better than the case. A similar pattern was observed for the level of significance. We also considered the accuracy of the empirical significance levels of the PEL tests at a relatively smaller sample size , for and ; cf. [LM]. The PEL has a reasonable performance even at this low sample size; see [LM] for details.

5.3.2 Finite sample power properties

To get some idea about the power properties of the PEL tests, we computed the probability of Type II error for a level PEL test with and under the alternative where the first components of were equal to and the rest were . Table 3 gives the power of the PEL test at level under for different combinations of , and . From Table 3, it appears that the power can be reasonably high for a suitable choice of the subsample size, although the maximum value critically depends on the dimension of the parameters and the strength of dependence . In particular, the PEL attains a higher (maximum) power under weaker dependence () than under strong dependence ().

5.3.3 Comparison with Normal calibration

Note that for , the limit distribution of the logarithm of the PEL ratio statistic is Normal and therefore, one can use the limiting Normal distribution with an estimated variance to conduct the PEL test. In this section, we compare the performance of the subsampling-based calibration with the Normal distribution-based calibration. To estimate the asymptotic variance , we first estimate using the sample auto-covariance at lag- based on the components of individual ’s and then average them to get an estimate of for where . Since involves the squares of , the plug-in estimator is positive (with probability ). Tables 4 and 5 compare the best performance of the subsampling based PEL with the Normal, calibration-based PEL for and , respectively.

| G | SS | G | SS | G | SS | |

|---|---|---|---|---|---|---|

| 0.122 | 0.151 | 0.132 | 0.080 | 0.136 | 0.081 | |

| 0.098 | 0.092 | 0.030 | 0.111 | 0.076 | 0.093 | |

Tables 4 and 5 show that, except for the small values of , the subsampling-based PEL method has a better accuracy (marked as bold) than the Normal, calibration-based PEL. However, the computational burden associated with the subsampling method is typically larger than the Normal-based PEL.

| G | SS | G | SS | G | SS | |

|---|---|---|---|---|---|---|

| 0.150 | 0.113 | 0.141 | 0.082 | 0.174 | 0.127 | |

| 0.111 | 0.165 | 0.048 | 0.103 | 0.238 | 0.126 | |

6 Proofs

Note that for each , the PEL likelihood function in (1) is invariant with respect to (i) component-wise scaling and (ii) permutation of the components. Hence, all through this section, without loss of generality (w.l.g.), we set the component-wise variance and set the permutation for all and . Let denote generic constants that depend only on their arguments (if any), but not on . Unless otherwise specified, dependence on (limiting) population quantities [such as , mixing coefficients, etc.] are dropped to simplify notation, and limits in all order symbols are taken by letting . For , let denote the largest integer not exceeding and let .

6.1 Limit distribution in the nonergodic case

Lemma 6.1

For each , let {}, be a collection of -dimensional random vectors with and . Let where and . Also, let , , and . Suppose that (L.1) ; (L.2) , and (L.3) . Then: {longlist}[(a)]

For , .

.

.

For , .

.

By replacing ’s with for all , w.l.g., we can assume that for all . First consider part (a), ; the proofs of are similar. By repeated use of Hölder’s inequality,

which is , by (L.1), (L.2). This proves (a). Parts (b) and (c) follow by similar arguments. As for part (d), note that (for )

Finally consider part (e). Note that for

so that

| (19) |

Part (e) can now be proved using (L.1)–(L.3) and the Cauchy–Schwarz inequality. We omit the details to save space.

Lemma 6.2

W.l.g., let for all . Note that

| (20) |

where . Since is strictly convex in over a closed convex set , it has a unique minimizer in . [The maximum of over is .] To find the minimizer, we use a Lagrange multiplier and solve the set of equations

where . This leads to the equations

which, in turn, yield the implicit solution

where and . To obtain a more explicit approximation, we show that ’s are of the form uniformly in . In view of Brouwer’s fixed point theorem [cf. Milnor (1965)], it is enough to show that, with ,

| (22) | |||

whenever . To prove (6.1), we first show that

| (23) |

where for all . Note that for any . Also, if and only if (iff) and similarly, iff . Hence, using the bound “ for all ,” we have

By (6.1), . Hence by Lemma 6.1 and the Cauchy–Schwarz inequality,

uniformly in , for large. Consequently, (23) holds. Now using (23), (6.1), the Cauchy–Schwarz inequality and Lemma 6.1, (6.1) follows. Hence, by Brouwer’s fixed point theorem [cf. Milnor (1965)], there exists a solution of (6.1) satisfying the bound

| (24) |

Using the second derivative condition, it is easy to verify that is a local minimizer of . In view of the strict convexity of on , it also follows that is the unique minimizer of over .

Next let , where . Then, from (6.1), we have

where the remainder terms ’s are defined by subtraction. By the next lemma, for . Hence, Lemma 6.2 is proved.

Lemma 6.3

Under the conditions of Theorem 3.1, .

See [LM] for details.

Proof of Theorem 5 Recall that . We carry out the proof in 2 steps.

Step (I): Let , and let . Then, . The first step is to prove that as elements of . Recall that is a complete orthonormal basis for . By Theorem 1.84 of Van der Vaart and Wellner (1996), it enough to show that:

(i) For any , ,

| (25) |

(ii) For any , there exists such that

| (26) |

Part (i) can be proved using Theorem 11.1.6 of Athreya and Lahiri (2006); we omit the routine details. For part (ii), it is enough to show that

| (27) |

Let , . Then, by Fubini’s theorem and (C.3),

which equals . Next, using and , one can show that for each fixed ,

Step (II): Next we establish weak convergence of the quadratic form:

| (30) |

Note that by condition (C.3), . Hence there exists a nonrandom such that for any fixed and for n sufficiently large (not depending on ),

| (31) | |||

Next, let denote the th element of . Note that is uniformly continuous on . Hence, using induction and condition (C.3), it can be shown that for any ,

By the continuous mapping theorem, it now follows that for any fixed ,

Thus, by (6.1), partial sums of the infinite series in (30) converge to the partial sums of the limit series for any fixed . By (6.1), the tail of the infinite series in (30) is negligible. It can be shown (cf. [LM]) that the tail of the limit series is also negligible. Since, , by (30)–(6.1) and Lemmas 6.1, 6.3, the theorem is proved.

6.2 Limit distribution for the ergodic case

We prove Theorem 3.2 and 3.3, using different arguments than the proof of Theorem 3.1. This is necessitated by the fact that we need more accurate bounds on the remainder terms that must become negligible after the scaling (e.g., by ). We will also use the notation to denote a bound that holds uniformly over as . For example, means an . Similarly, define .

Proof of Theorem 3.2 For , let , and . Then, . Now using for , one can show (cf. [LM]) that

| (33) |

Hence, by Taylor’s expansion of around ,

There exist , , such that (cf. [LM])

Hence, from (6.2),

Next, define . Then,

| (37) |

Note that for any , . Let and . Then there exists a such that by using (19) and the conditions of Theorem 3.2, one gets (cf. [LM])

Using (6.2), (6.2) and the Cauchy–Schwartz inequality, one can show that

Also, from (6.2), for any , we have

where and are remainder terms satisfying (cf. [LM])

Next, using similar arguments and noting that and for all , one can show (cf. [LM]) that

| (40) | |||||

| (41) | |||||

Using (6.2), (6.2) and (40)–(6.2) and the fact that and for all , one can conclude (cf. [LM])

| (43) |

Set . Then , and there by making the last two terms in (43) whenever . Now Theorem 3.2 follows by adapting the proof of the CLT for a stationary sequence of -mixing random variables to triangular arrays.

Proof of Theorem 3.3 Arguments in the proof of Theorem 3.2 yield the asymptotic approximation for in (43) with for all . Now choose to satisfy , for example, . Then it follows that

In the case where ’s are Gaussian with , the leading term has the same distribution as , where is a stationary Gaussian process with correlation function . Then the result of Taqqu (1975) implies the , and the theorem follows. In the general case when ’s are not Gaussian, the theorem follows by using convergence of moments of to the moments of and a variant of the diagram formula; cf. Arcones (1994).

Proof of Theorem 4.1 Note that with . Let

for where is the smallest integer not less than . By the independence of and for , one can show (cf. [LM]) that for each ,

| (44) | |||

The next arguments are similar to the proof of the Glivenko–Cantelli theorem [cf. Theorem 13.3 of Billingsley (1999)] and the continuity of the limit distribution of ; one can complete the proof; see [LM].

Proof of Remark 4.1 Here we outline a proof of consistency of the permutation invariant estimators and of Remark 4.1. W.l.g, suppose that and for all , . First consider the estimator in (14). Let for all , . Then, by condition (C.1), for some . On the set , , and using arguments similar to those in the proof of Lemma 6.2, one can show that

where . Note that for and . Now it is easy to verify that satisfies (12).

To prove the consistency of of (14), using moderate deviation inequalities [cf. Götze and Hipp (1978)], one can conclude that

| (45) |

Next note that for all . This implies that only -many correlation terms contribute to , with probability tending to one. Now using (45) for the nonvanishing terms and the fact that , one can prove consistency of .

Acknowledgments

We thank three anonymous reviewers and Professors Peter Bühlmann and Art Owen for a number of constructive comments that improved an earlier version of the paper.

Numerical results and proofs \slink[doi]10.1214/12-AOS1040SUPP \sdatatype.pdf \sfilenameaos1040_supp.pdf \sdescriptionAdditional simulation results and some details of proofs.

References

- Arcones (1994) {barticle}[mr] \bauthor\bsnmArcones, \bfnmMiguel A.\binitsM. A. (\byear1994). \btitleLimit theorems for nonlinear functionals of a stationary Gaussian sequence of vectors. \bjournalAnn. Probab. \bvolume22 \bpages2242–2274. \bidissn=0091-1798, mr=1331224 \bptokimsref \endbibitem

- Athreya and Lahiri (2006) {bbook}[mr] \bauthor\bsnmAthreya, \bfnmKrishna B.\binitsK. B. and \bauthor\bsnmLahiri, \bfnmSoumendra N.\binitsS. N. (\byear2006). \btitleMeasure Theory and Probability Theory. \bpublisherSpringer, \blocationNew York. \bidmr=2247694 \bptokimsref \endbibitem

- Bartolucci (2007) {barticle}[mr] \bauthor\bsnmBartolucci, \bfnmFrancesco\binitsF. (\byear2007). \btitleA penalized version of the empirical likelihood ratio for the population mean. \bjournalStatist. Probab. Lett. \bvolume77 \bpages104–110. \biddoi=10.1016/j.spl.2006.05.016, issn=0167-7152, mr=2339024 \bptokimsref \endbibitem

- Beran (1994) {bbook}[auto:STB—2012/11/05—08:49:14] \bauthor\bsnmBeran, \bfnmJ.\binitsJ. (\byear1994). \btitleStatistical Methods for Long Memory Processes. \bpublisherChapman & Hall, \blocationLondon. \bptokimsref \endbibitem

- Bertail (2006) {barticle}[mr] \bauthor\bsnmBertail, \bfnmPatrice\binitsP. (\byear2006). \btitleEmpirical likelihood in some semiparametric models. \bjournalBernoulli \bvolume12 \bpages299–331. \biddoi=10.3150/bj/1145993976, issn=1350-7265, mr=2218557 \bptokimsref \endbibitem

- Bickel and Levina (2008) {barticle}[mr] \bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmLevina, \bfnmElizaveta\binitsE. (\byear2008). \btitleCovariance regularization by thresholding. \bjournalAnn. Statist. \bvolume36 \bpages2577–2604. \biddoi=10.1214/08-AOS600, issn=0090-5364, mr=2485008 \bptokimsref \endbibitem

- Billingsley (1999) {bbook}[mr] \bauthor\bsnmBillingsley, \bfnmPatrick\binitsP. (\byear1999). \btitleConvergence of Probability Measures, \bedition2nd ed. \bpublisherWiley, \blocationNew York. \biddoi=10.1002/9780470316962, mr=1700749 \bptokimsref \endbibitem

- Cai, Zhang and Zhou (2010) {barticle}[mr] \bauthor\bsnmCai, \bfnmT. Tony\binitsT. T., \bauthor\bsnmZhang, \bfnmCun-Hui\binitsC.-H. and \bauthor\bsnmZhou, \bfnmHarrison H.\binitsH. H. (\byear2010). \btitleOptimal rates of convergence for covariance matrix estimation. \bjournalAnn. Statist. \bvolume38 \bpages2118–2144. \biddoi=10.1214/09-AOS752, issn=0090-5364, mr=2676885 \bptokimsref \endbibitem

- Chen and Hall (1993) {barticle}[mr] \bauthor\bsnmChen, \bfnmSong Xi\binitsS. X. and \bauthor\bsnmHall, \bfnmPeter\binitsP. (\byear1993). \btitleSmoothed empirical likelihood confidence intervals for quantiles. \bjournalAnn. Statist. \bvolume21 \bpages1166–1181. \biddoi=10.1214/aos/1176349256, issn=0090-5364, mr=1241263 \bptokimsref \endbibitem

- Chen, Peng and Qin (2009) {barticle}[mr] \bauthor\bsnmChen, \bfnmSong Xi\binitsS. X., \bauthor\bsnmPeng, \bfnmLiang\binitsL. and \bauthor\bsnmQin, \bfnmYing-Li\binitsY.-L. (\byear2009). \btitleEffects of data dimension on empirical likelihood. \bjournalBiometrika \bvolume96 \bpages711–722. \biddoi=10.1093/biomet/asp037, issn=0006-3444, mr=2538767 \bptokimsref \endbibitem

- Chen, Variyath and Abraham (2008) {barticle}[mr] \bauthor\bsnmChen, \bfnmJiahua\binitsJ., \bauthor\bsnmVariyath, \bfnmAsokan Mulayath\binitsA. M. and \bauthor\bsnmAbraham, \bfnmBovas\binitsB. (\byear2008). \btitleAdjusted empirical likelihood and its properties. \bjournalJ. Comput. Graph. Statist. \bvolume17 \bpages426–443. \biddoi=10.1198/106186008X321068, issn=1061-8600, mr=2439967 \bptokimsref \endbibitem

- Cramér and Leadbetter (1967) {bbook}[mr] \bauthor\bsnmCramér, \bfnmHarald\binitsH. and \bauthor\bsnmLeadbetter, \bfnmM. R.\binitsM. R. (\byear1967). \btitleStationary and Related Stochastic Processes. \bpublisherWiley, \blocationNew York. \bptokimsref \endbibitem

- DiCiccio, Hall and Romano (1991) {barticle}[mr] \bauthor\bsnmDiCiccio, \bfnmThomas\binitsT., \bauthor\bsnmHall, \bfnmPeter\binitsP. and \bauthor\bsnmRomano, \bfnmJoseph\binitsJ. (\byear1991). \btitleEmpirical likelihood is Bartlett-correctable. \bjournalAnn. Statist. \bvolume19 \bpages1053–1061. \biddoi=10.1214/aos/1176348137, issn=0090-5364, mr=1105861 \bptokimsref \endbibitem

- Dobrushin and Major (1979) {barticle}[mr] \bauthor\bsnmDobrushin, \bfnmR. L.\binitsR. L. and \bauthor\bsnmMajor, \bfnmP.\binitsP. (\byear1979). \btitleNon-central limit theorems for nonlinear functionals of Gaussian fields. \bjournalZ. Wahrsch. Verw. Gebiete \bvolume50 \bpages27–52. \biddoi=10.1007/BF00535673, issn=0044-3719, mr=0550122 \bptokimsref \endbibitem

- El Karoui (2008) {barticle}[mr] \bauthor\bsnmEl Karoui, \bfnmNoureddine\binitsN. (\byear2008). \btitleOperator norm consistent estimation of large-dimensional sparse covariance matrices. \bjournalAnn. Statist. \bvolume36 \bpages2717–2756. \biddoi=10.1214/07-AOS559, issn=0090-5364, mr=2485011 \bptokimsref \endbibitem

- Emerson and Owen (2009) {barticle}[mr] \bauthor\bsnmEmerson, \bfnmSarah C.\binitsS. C. and \bauthor\bsnmOwen, \bfnmArt B.\binitsA. B. (\byear2009). \btitleCalibration of the empirical likelihood method for a vector mean. \bjournalElectron. J. Stat. \bvolume3 \bpages1161–1192. \biddoi=10.1214/09-EJS518, issn=1935-7524, mr=2566185 \bptokimsref \endbibitem

- Fan and Li (2001) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmLi, \bfnmRunze\binitsR. (\byear2001). \btitleVariable selection via nonconcave penalized likelihood and its oracle properties. \bjournalJ. Amer. Statist. Assoc. \bvolume96 \bpages1348–1360. \biddoi=10.1198/016214501753382273, issn=0162-1459, mr=1946581 \bptokimsref \endbibitem

- Fan and Peng (2004) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmPeng, \bfnmHeng\binitsH. (\byear2004). \btitleNonconcave penalized likelihood with a diverging number of parameters. \bjournalAnn. Statist. \bvolume32 \bpages928–961. \biddoi=10.1214/009053604000000256, issn=0090-5364, mr=2065194 \bptokimsref \endbibitem

- Götze and Hipp (1978) {barticle}[mr] \bauthor\bsnmGötze, \bfnmF.\binitsF. and \bauthor\bsnmHipp, \bfnmC.\binitsC. (\byear1978). \btitleAsymptotic expansions in the central limit theorem under moment conditions. \bjournalZ. Wahrsch. Verw. Gebiete \bvolume42 \bpages67–87. \bidmr=0467882 \bptokimsref \endbibitem

- Hall, Horowitz and Jing (1995) {barticle}[mr] \bauthor\bsnmHall, \bfnmPeter\binitsP., \bauthor\bsnmHorowitz, \bfnmJoel L.\binitsJ. L. and \bauthor\bsnmJing, \bfnmBing-Yi\binitsB.-Y. (\byear1995). \btitleOn blocking rules for the bootstrap with dependent data. \bjournalBiometrika \bvolume82 \bpages561–574. \biddoi=10.1093/biomet/82.3.561, issn=0006-3444, mr=1366282 \bptokimsref \endbibitem

- Hall, Jing and Lahiri (1998) {barticle}[mr] \bauthor\bsnmHall, \bfnmPeter\binitsP., \bauthor\bsnmJing, \bfnmB.-Y.\binitsB.-Y. and \bauthor\bsnmLahiri, \bfnmS. N.\binitsS. N. (\byear1998). \btitleOn the sampling window method under long range dependence. \bjournalStatist. Sinica \bvolume8 \bpages1189–1204. \bptokimsref \endbibitem

- Hjort, McKeague and Van Keilegom (2009) {barticle}[mr] \bauthor\bsnmHjort, \bfnmNils Lid\binitsN. L., \bauthor\bsnmMcKeague, \bfnmIan W.\binitsI. W. and \bauthor\bsnmVan Keilegom, \bfnmIngrid\binitsI. (\byear2009). \btitleExtending the scope of empirical likelihood. \bjournalAnn. Statist. \bvolume37 \bpages1079–1111. \biddoi=10.1214/07-AOS555, issn=0090-5364, mr=2509068 \bptokimsref \endbibitem

- Ibragimov and Linnik (1971) {bbook}[mr] \bauthor\bsnmIbragimov, \bfnmI. A.\binitsI. A. and \bauthor\bsnmLinnik, \bfnmYu. V.\binitsY. V. (\byear1971). \btitleIndependent and Stationary Sequences of Random Variables. \bpublisherWolters-Noordhoff Publishing, \blocationGroningen. \bidmr=0322926 \bptokimsref \endbibitem

- Lahiri (2003) {bbook}[mr] \bauthor\bsnmLahiri, \bfnmS. N.\binitsS. N. (\byear2003). \btitleResampling Methods for Dependent Data. \bpublisherSpringer, \blocationNew York. \bidmr=2001447 \bptokimsref \endbibitem

- Lahiri and Mukhopadhyay (2012) {bmisc}[auto:STB—2012/11/05—08:49:14] \bauthor\bsnmLahiri, \bfnmS. N.\binitsS. N. and \bauthor\bsnmMukhopadhyay, \bfnmS.\binitsS. (\byear2012). \bhowpublishedSupplement to “A penalized empirical likelihood method in high dimensions.” DOI:\doiurl10.1214/12-AOS1040SUPP. \bptokimsref \endbibitem

- Milnor (1965) {bbook}[mr] \bauthor\bsnmMilnor, \bfnmJohn W.\binitsJ. W. (\byear1965). \btitleTopology from the Differentiable Viewpoint. \bpublisherThe Univ. Press of Virginia, \blocationCharlottesville, VA. \bidmr=0226651 \bptokimsref \endbibitem

- Otsu (2007) {barticle}[mr] \bauthor\bsnmOtsu, \bfnmTaisuke\binitsT. (\byear2007). \btitlePenalized empirical likelihood estimation of semiparametric models. \bjournalJ. Multivariate Anal. \bvolume98 \bpages1923–1954. \biddoi=10.1016/j.jmva.2007.05.005, issn=0047-259X, mr=2396947 \bptokimsref \endbibitem

- Owen (1988) {barticle}[mr] \bauthor\bsnmOwen, \bfnmArt B.\binitsA. B. (\byear1988). \btitleEmpirical likelihood ratio confidence intervals for a single functional. \bjournalBiometrika \bvolume75 \bpages237–249. \biddoi=10.1093/biomet/75.2.237, issn=0006-3444, mr=0946049 \bptokimsref \endbibitem

- Owen (2001) {bbook}[auto:STB—2012/11/05—08:49:14] \bauthor\bsnmOwen, \bfnmA.\binitsA. (\byear2001). \btitleEmpirical Likelihood. \bpublisherChapman & Hall, \blocationBoca Raton, FL. \bptokimsref \endbibitem

- Qin and Lawless (1994) {barticle}[mr] \bauthor\bsnmQin, \bfnmJing\binitsJ. and \bauthor\bsnmLawless, \bfnmJerry\binitsJ. (\byear1994). \btitleEmpirical likelihood and general estimating equations. \bjournalAnn. Statist. \bvolume22 \bpages300–325. \biddoi=10.1214/aos/1176325370, issn=0090-5364, mr=1272085 \bptokimsref \endbibitem

- Tang and Leng (2010) {barticle}[mr] \bauthor\bsnmTang, \bfnmCheng Yong\binitsC. Y. and \bauthor\bsnmLeng, \bfnmChenlei\binitsC. (\byear2010). \btitlePenalized high-dimensional empirical likelihood. \bjournalBiometrika \bvolume97 \bpages905–919. \biddoi=10.1093/biomet/asq057, issn=0006-3444, mr=2746160 \bptokimsref \endbibitem

- Taqqu (1975) {barticle}[mr] \bauthor\bsnmTaqqu, \bfnmMurad S.\binitsM. S. (\byear1975). \btitleWeak convergence to fractional Brownian motion and to the Rosenblatt process. \bjournalZ. Wahrsch. Verw. Gebiete \bvolume31 \bpages287–302. \bidmr=0400329 \bptnotecheck year\bptokimsref \endbibitem

- Taqqu (1977) {barticle}[mr] \bauthor\bsnmTaqqu, \bfnmMurad S.\binitsM. S. (\byear1977). \btitleLaw of the iterated logarithm for sums of non-linear functions of Gaussian variables that exhibit a long range dependence. \bjournalZ. Wahrsch. Verw. Gebiete \bvolume40 \bpages203–238. \bidmr=0471045 \bptokimsref \endbibitem

- Taqqu, Teverovsky and Willinger (1995) {barticle}[auto:STB—2012/11/05—08:49:14] \bauthor\bsnmTaqqu, \bfnmM.\binitsM., \bauthor\bsnmTeverovsky, \bfnmV.\binitsV. and \bauthor\bsnmWillinger, \bfnmW.\binitsW. (\byear1995). \btitleEstimators for long-range dependence: An empirical study. \bjournalE. Fractals \bvolume3 \bpages785–798. \bptokimsref \endbibitem

- Tsao (2004) {barticle}[mr] \bauthor\bsnmTsao, \bfnmMin\binitsM. (\byear2004). \btitleBounds on coverage probabilities of the empirical likelihood ratio confidence regions. \bjournalAnn. Statist. \bvolume32 \bpages1215–1221. \biddoi=10.1214/009053604000000337, issn=0090-5364, mr=2065203 \bptokimsref \endbibitem

- van der Vaart and Wellner (1996) {bbook}[mr] \bauthor\bparticlevan der \bsnmVaart, \bfnmAad W.\binitsA. W. and \bauthor\bsnmWellner, \bfnmJon A.\binitsJ. A. (\byear1996). \btitleWeak Convergence and Empirical Processes. \bpublisherSpringer, \blocationNew York. \bidmr=1385671 \bptokimsref \endbibitem

- Wright (1997) {bbook}[mr] \bauthor\bsnmWright, \bfnmStephen J.\binitsS. J. (\byear1997). \btitlePrimal-dual Interior-point Methods. \bpublisherSociety for Industrial and Applied Mathematics (SIAM), \blocationPhiladelphia, PA. \biddoi=10.1137/1.9781611971453, mr=1422257 \bptokimsref \endbibitem