Multifidelity variance reduction for pick-freeze Sobol index estimation

Abstract

Many mathematical models involve input parameters, which are not precisely known. Global sensitivity analysis aims to identify the parameters whose uncertainty has the largest impact on the variability of a quantity of interest (output of the model). One of the statistical tools used to quantify the influence of each input variable on the output is the Sobol sensitivity index, which can be estimated using a large sample of evaluations of the output. We propose a variance reduction technique, based on the availability of a fast approximation of the output, which can enable significant computational savings when the output is costly to evaluate.

Introduction

Many mathematical models encountered in applied sciences involve a large number of poorly-known parameters as inputs. It is important for the practitioner to assess the impact of this uncertainty on the model output. An aspect of this assessment is sensitivity analysis, which aims to identify the most sensitive parameters, that is, parameters having the largest influence of the output. In global stochastic sensitivity analysis (see for example [8] and references therein) the input variables are assumed to be independent random variables. Their probability distributions account for the practitioner’s belief about the input uncertainty. This turns the model output into a random variable, whose total variance can be split down into different partial variances (this is the so-called Hoeffding decomposition, see [14]). Each of these partial variances measures the uncertainty on the output induced by each input variable uncertainty. By considering the ratio of each partial variance to the total variance, we obtain a measure of importance for each input variable that is called the Sobol index or sensitivity index of the variable [11]; the most sensitive parameters can then be identified and ranked as the parameters with the largest Sobol indices.

Once the Sobol indices have been defined, the question of their effective computation or estimation remains open. In practice, one has to estimate (in a statistical sense) those indices using a finite sample (of size typically in the order of hundreds of thousands) of evaluations of model outputs [3]. Indeed, many Monte Carlo or quasi Monte Carlo approaches have been developed by the experimental sciences and engineering communities. Such an approach is the Sobol pick-freeze (SPF) scheme (see [11, 12]). In SPF a Sobol index is viewed as the regression coefficient between the output of the model and its pick-freezed replication. This replication is obtained by holding the value of the variable of interest (frozen variable) and by sampling the other variables (picked variables). The sampled replications are then combined to produce an estimator of the Sobol index.

The SPF method requires many (typically, around one thousand times the number of input variables) evaluations of the model output. In many interesting cases, an evaluation of the model output is made by a complex computer code (for instance, a numerical partial differential equation solving algorithm) whose running time is not negligible (typically in the order of a second or a minute) for one single evaluation. When thousands of such evaluations have to be made, one generally replaces the original exact model by a faster-to-run metamodel (also known in the literature as surrogate model or response surface [1]) which is an approximation of the true model. Well-known metamodels include Kriging [10], polynomial chaos expansion [13] and reduced bases [7, 5], to name a few. From a multifidelity point of view, the metamodel can also be viewed as a “coarse” (low-fidelity) version of the code; the metamodel, seen as a coarse version, may also be a “degraded” version of the code: for instance, it may be a solver for a simplified model (either mathematically simplified, or discretized on a coarser grid), an integrator for a function of lesser precision, or an optimizer stopped before its full convergence. In this paper, we designate by “coarse approximation” any of the above approximations (metamodels and degraded versions). When using a coarse approximation for sensitivity analysis, the original model is generally used only to define the metamodel, and not to perform the Sobol index estimation. This leads to a necessity of measuring the difference between the model and its approximation in order to certify the sensitivity index estimation [5, 6]. To our best knowledge, no approach for using both metamodel and model evaluations to estimate Sobol indices have been proposed yet.

In this work, we propose an approach, based on the asymptotic properties of the SPF scheme studied in [6] to optimally combine evaluations of the original model and evaluations of its approximation, in order to produce an asymptotically-justified confidence interval for the Sobol index of the original model. Our approach is inspired by the quasi-control variate method [2] which has been developed for Monte-Carlo estimation of means.

This paper is organized as follows: in the first section, we begin by setting up the notations and the context of the paper. Then we define the Sobol index estimator we wish to study. The main result is Theorem 1.1, which provides an asymptotic method to estimate a confidence interval for a Sobol index. The second section is a numerical illustration on a particular (but representative) kind of model output.

1 Motivation and definition of the estimator

1.1 Notation and context

We begin by setting up the usual notations in the sensitivity analysis contexts. The output of interest is a random variable , which is a deterministic function of the random inputs and :

where and are integers, and .

We assume that and are independent random variables and that has a finite and nonzero variance. We are interested in the (closed) Sobol index [9] with respect to , defined by:

This index, which is between 0 and 1, quantifies the influence of the input on the output : a value of that is close to indicates that is highly influential on .

This expression leads to different Monte-Carlo estimators of . For instance, the following estimator is studied in [6]:

where, and are independent samples of (resp. ), and, as in the rest of the paper, all sums are for from 1 to .

It is shown [op.cit., Proposition 2.2] that is asymptotically normal, with variance , where:

| (1) |

and [op.cit., Proposition 2.5] that this asymptotic variance is minimal among regular estimators that are functions of realizations of exchangeable pairs.

Note that a realization of the estimator, for a finite sample size , can be computed by making evaluations of the function.

In this paper, we suppose that we can evaluate, in addition to the function, an approximation of the function (the index is for coarse).

The usage of such an approximation has been motivated in the Introduction. A concrete and ubiquitous example of and will be presented in the next section. In the following section, we motivate and study our variance-reduced estimator of .

1.2 Variance-reduced estimator

Let:

and , be -samples of (resp. ).

The estimator:

consistently estimates the Sobol index of the coarse model:

by using evaluations of .

As mentioned in the introduction, our objective is to combine evaluations of and to estimate at a smaller cost than an estimation that would be performed from evaluations of only.

We take a function .

It is clear that the estimator defined by:

consistently estimates , and that a realization of can be obtained using evaluations of and evaluations of .

We propose a natural estimator of based on and , inspired by the quasi-control variate method [2], is thus:

This estimator can be computed by making evaluations of and evaluations of . As an evaluation of is more costly than one of , one can expect a computational gain if , and if the asymptotic variance of is less than the asymptotic variance of , so that asymptotic confidence intervals built upon are more precise than those built on alone.

The following theorem gives a method for estimating (conservative) asymptotic confidence intervals using . We denote by the cumulative distribution function of the Gaussian with zero mean and unit variance, and by its inverse.

Theorem 1.1.

Suppose that .

Then, for any and in :

for:

where , , , are the following random variables:

The same holds when and are replaced by any consistent estimators.

Sketch of proof.

Follow the proof of [6], Proposition 2.2, and apply the -method to to get the asymptotic variance of .

Then use that for any ,

1.3 Choice of , and

To convert the theorem above into a practical procedure, it remains to choose the parameters , and , so as to minimize the overall computational time.

We will assume that one evaluation of as a unit cost, and that an evaluation of has cost . We also set , where is to be found, and is the “ceiling” function.

We choose a target risk level and a target length for the confidence interval of Theorem 1.1.

It is clear these constraints force in function of and :

and that has to satisfy:

We approximate by . The cost of the required evaluations of and is thus, in the general case:

corresponding to the evaluations of and the evaluations of .

However, in some settings, the computations made to compute can be reused to compute , allowing to evaluate and for a unit cost, leading to:

Such a “hierarchical” property is beneficial to our estimation scheme and occurs naturally for some , as we will see in the numerical illustration section.

Now, one would obviously choose and so as to minimize the cost (or, depending on the case at hand, ). In practice, this is not possible, as and are unknown. Hence, approximately optimal parameters are found by empirically estimating these quantities, based on a small sample of realizations of , , and . This gives rise to and , and an estimated optimal costs:

2 Numerical illustration

2.1 Model set-up

In financial mathematics, the Heston model [4] is the following stochastic differential model for the price of a risky asset as function of the time :

where and are standard Brownian motions (under the risk-neutral probability measure ) whose correlation is .

We are interested in the price of an European call option of maturity and strike , which is given by .

Although a semi-analytical formula is available for the fast computation of this expectation (such a formula may not exist for more complex dynamics of the underlying asset, or for exotic options), we will use a numerical approximation so as to illustrate our methodology on a realistic model example. The expectation is approached by the following Monte-Carlo procedure:

with an Euler-Maruyama approximation of with timestep : for and :

where is the time discretization parameter, and are indepedent realizations of a standard Gaussian random variable.

We fix (the initial price of the asset), , , as well as the discretization parameters and . The uncertain parameters are and , which are given the uniform distribution probabilities summarized in Table 1.

| Name | Interpretation | Min. | Max. |

|---|---|---|---|

| Initial volatility | .2 | .25 | |

| Volatility convergence rate | 0 | 3 | |

| Volatility limit | .2 | .22 | |

| Correlation between Brownians | -1 | 1 | |

| Volatility of the volatility | 0 | .4 | |

| Risk-free rate | .08 | 1.1 |

The coarse approximation uses a reduced number of simulated trajectories to compute the empirical mean:

Note that for computing , the same time discretization parameter , as well as the same simulated Brownian increments are kept, hence our approximation is “hierarchical” in the sense of Subsection 1.3.

We chose , so that .

2.2 Results and discussion

We estimated and based on a sample of realizations of each variable and . The estimates are:

For comparison purposes, we also estimated :

We are interested in the (estimated) relative efficiency of the confidence intervals based on our variance-reduced estimator, as compared with those based on , that is:

where is the cost of the evaluations necessary to produce an asymptotic confidence interval of fixed length using only the estimator:

As the denominator and the numerator of Eff are proportional to , the relative efficiency is independent of the target length of the confidence interval .

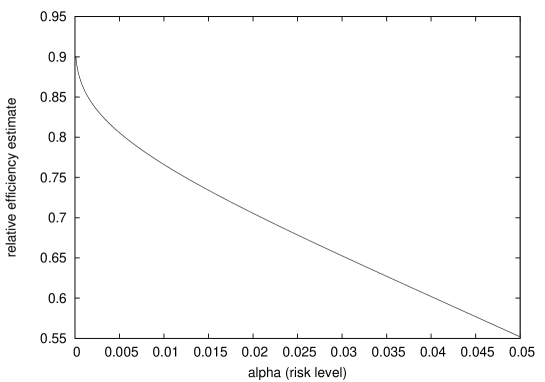

In Figure 1, we plot the estimated relative efficiency of our variance-reduced estimator, as function of the target risk level .

We see that, based on empirical estimations, our variance reduction enables an interesting reduction of the computational cost by more than for , and this reduction is even more significative for small risk levels (up to for ).

References

- [1] G.E.P. Box and N.R. Draper. Empirical model-building and response surfaces. John Wiley & Sons, 1987.

- [2] M. Emsermann and B. Simon. Improving simulation efficiency with quasi control variates. 2002.

- [3] J.C. Helton, J.D. Johnson, C.J. Sallaberry, and C.B. Storlie. Survey of sampling-based methods for uncertainty and sensitivity analysis. Reliability Engineering & System Safety, 91(10-11):1175–1209, 2006.

- [4] Steven L Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of financial studies, 6(2):327–343, 1993.

- [5] A. Janon, M. Nodet, and C. Prieur. Certified reduced-basis solutions of viscous Burgers equations parametrized by initial and boundary values. Preprint available at \urlhttp://hal.inria.fr/inria-00524727/en, 2010, Accepted in Mathematical modelling and Numerical Analysis.

- [6] Alexandre Janon, Thierry Klein, Agnès Lagnoux, Maëlle Nodet, and Clémentine Prieur. Asymptotic normality and efficiency of two Sobol index estimators.

- [7] N.C. Nguyen, K. Veroy, and A.T. Patera. Certified real-time solution of parametrized partial differential equations. Handbook of Materials Modeling, pages 1523–1558, 2005.

- [8] A. Saltelli, K. Chan, and E.M. Scott. Sensitivity analysis. Wiley Series in Probability and Statistics. John Wiley & Sons, Ltd., Chichester, 2000.

- [9] A. Saltelli, S. Tarantola, Campolongo F., and Ratto M. Sensitivity analysis in practice: a guide to assessing scientific models, 2004.

- [10] T. J. Santner, B. Williams, and W. Notz. The Design and Analysis of Computer Experiments. Springer-Verlag, 2003.

- [11] I. M. Sobol. Sensitivity estimates for nonlinear mathematical models. Math. Modeling Comput. Experiment, 1(4):407–414 (1995), 1993.

- [12] I.M. Sobol. Global sensitivity indices for nonlinear mathematical models and their Monte Carlo estimates. Mathematics and Computers in Simulation, 55(1-3):271–280, 2001.

- [13] B. Sudret. Global sensitivity analysis using polynomial chaos expansions. Reliability Engineering & System Safety, 93(7):964–979, 2008.

- [14] A. W. van der Vaart. Asymptotic statistics, volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 1998.

Acknowledgements. This work has been partially supported by the French National Research Agency (ANR) through COSINUS program (project COSTA-BRAVA nr. ANR-09-COSI-015).