DISCRETE OPTIMIZATION

OF STATISTICAL SAMPLE

SIZES

IN SIMULATION BY USING

THE HIERARCHICAL

BOOTSTRAP METHOD

††thanks: We are very thankful to Latvian Council of Science for

the Grant Nr.97.0798 within which the present investigation is worked out.

A. Andronov and M. Fioshin

Riga Technical university,

Riga, LV-1658, 1, Kalku Str., Latvia

e-mail: andronow@rau.lv, mf@rau.lv

Abstract

The Bootstrap method application in simulation supposes that value of

random variables are not generated during the simulation process but

extracted from available sample populations. In the case of

Hierarchical Bootstrap the function of interest is calculated recurrently

using the calculation tree. In the present paper we consider the

optimization of sample sizes in each vertex of the calculation tree.

The dynamic programming method is used for this aim. Proposed method

allows to decrease a variance of system characteristic estimators.

Keywords:

Bootstrap method, Simulation, Hierarchical Calculations, Variance Reduction

1 INTRODUCTION

Main problem of the mathematical statistics and simulation is connected with

insufficiency of primary statistical data. In this situation, the Bootstrap

method can be used successfully (Efron, Tibshirani 1993,

Davison, Hinkley 1997). If a dependence between characteristics

of interest and input data is very composite and is described by numerical

algorithm then usually it applies a simulation. By this the probabilistic

distributions of input data are not estimated because the given primary

data has small size and such estimation gives a bias and big variance.

The Bootstrap method supposes that random variables are not generated

by a random number generator during simulation in accordance with the estimated distributions

but ones are extracted from given primary data at random.

Various problems of this approach were considered in previous papers

(Andronov et al. 1995, 1998).

We will consider the known function

of m independent continuos random variables It is assumed that distributions of random

variables are unknown, but the sample population

is available for each

. Here is the size of the sample .

The problem consists in estimation of the mathematical expectation

(1)

The Bootstrap method use supposes an organization of some realizations

of the values

. In each realization the values of

arguments are extracted randomly from the corresponding sample populations

. Let be a number of elements which were

extracted from the population in the -th realization.

We denote

and name it the l-th subsample. The estimator of the mathematical

expectation is equal to an average value for all r realizations:

(2)

Our main aim is to calculate and to minimize the variance of this estimator. The variance will

depend upon two factors: 1) a calculation method of the function ;

2) a formation mode of subsamples .

The next two Sections will

be dedicated to these questions.

In Section 4 we will show how to decrease variance using

the dynamic programming method.

2 THE HIERARCHICAL BOOTSTRAP METHOD

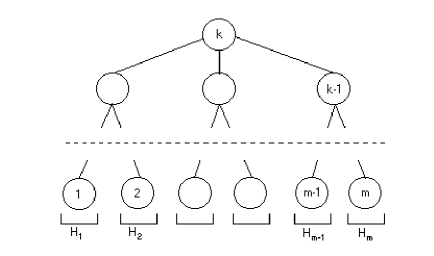

We suppose that the function is calculated by a calculation tree.

A root of this tree corresponds to the computed function

. It is the vertex number k. The vertices numbers

correspond to the input variables . The rest vertices

are intermediate ones. They correspond to intermediate functions

(see Fig.1).

Figure 1: Calculation tree

Only one arc comes out from each vertex , . It

corresponds to a value of the function . We suppose that

.

We denote as a set of vertices from which arcs come into the vertex

, and as a corresponding set of variables (arcs):

. It is clear that for

; , . We suppose that

a numbering of the vertices is correct: if than .

Now, function value can be calculated by the sweep method. At the

beginning, we extract separate elements from populations , then calculate the

function values , successively.

After r such runs the estimator is computed according to the

formula (2). An analysis of this method was developed in

the previous papers of authors.

The Hierarchical Bootstrap method is based on the wave algorithm. Here

all values of the function for each vertex should be calculated all at once. They form the set ,

where is number of realizations (sample size). Getting one realization consists

of choosing value from each corresponding population , and

calculation of value. By this we suppose that a random sample

with replacement is used when each element from is choosen

independendly with the probability . Further on, this procedure

is repeated for next vertex. Finally we get as values of the population . Their average gives

the estimator by analogy with formula (2).

3 EXPRESSIONS FOR VARIANCE

The aim of this section is to show how to calculate variance

of the estimator (2).

It is easy to see that in the case of Hierarchical Bootstrap

the variance

is function of sample sizes .

In the previous papers of authors the variance was calculated

using the -pairs notion (Andronov et. al, 1996, 1998). Then, it was

considered as continuos function of variables ,

and reduced gradient method was used. But now we need other approach

for the calculation of .

We use Taylor decomposition of function in respect to

mean :

(3)

where

is the matrix of second derivatives of

the function ,

is Euclidean norm of vector .

It gives the following decomposition:

If is a random vector with mutual independent components

, , , then

(5)

(6)

Now we suppose that and are some values from sample population

. Let denote the covariance

of two elements and with different numbers and :

(7)

Let and correspond to the elements and

accordingly. Because we extract and from at random and

with replacement, then the event occurs with the

probability . Then

(8)

Therefore

(9)

If the values and correspond to subfunction

and the sample population , then formulas (3), (5) and (6)

give

where the variance can be determined from (10) by :

(12)

Finally we have

(13)

or

(14)

By this we suppose that variances of input random variables are

known. For example, it is possible to use estimators of these variances,

calculated on given sample populations .

If the vertex belongs to the initial level of the calculation

tree (it means that ) then ,

is known value, . Therefore

(15)

Another covariances and variances are calculated recurrently in accordance

with formulas (10),(12), (14), (15)

from vertices with less numbers to vertices with great numbers. Finally

we get the variance of interest as the variance for root of the

calculation tree:

(16)

where .

As it was just mentioned, we will consider the variance as

a function of sample sizes and denote it

. Our aim is to minimize this function in respect to variables

by linear restriction, or, by other words, to solve

the following optimization problem:

(17)

by restriction

(18)

where , and are integer non-negative numbers.

Now we intent to apply the dynamic programming method (Minox 1989).

4 THE DYNAMIC PROGRAMMING METHOD

Let us

solve the optimization problem (17), (18).

Our function of interest is calculated and simulated

recurrently, using the calculation tree (see Section 2).

In accordance to the dynamic programming technique, we have

”forward” and ”backward” procedure.

During ”backward” procedure, we calculate recurrently so-called Bellman

function , , , .

Let us consider the subfunction , that corresponds to the

vertex . This subfunction directly depends on variables , ,

which correspond to incoming arcs for the vertex . Additionally

depends on variables and from which there exists path from leaves to the

vertex of our calculation tree. Let denote corresponding set

of variables and .

Now we need to denote some auxiliary functions. Let us introduce the following

notation

(19)

Then we are able to write in accordance with (13):

Note that it follows from (11) and (19) that our variance

of interest (16) is

(22)

Values depend on the sample sizes for all .

We will mark this fact as .

Now we are able to introduce above mentioned Bellman functions:

(23)

where minimization is realized with respect to non-negative integer

variables that are satisfied the linear restriction

(24)

It is clear that optimal value of variance for the problem

(17), (18) is equal to .

Bellman functions are calculated recurrently

from to for and .

Basic functional equation of dynamic programming has the

following form:

(25)

where minimaiztion is realized with respect to non-negative

integer variables and that satisfy the

linear restriction

(26)

The initial values of are determined with the tree leaves

by formulas (15), (19) and (23):

(27)

where - integer part of number ,

Thus the ”backward” procedure is a recurrent calculation of Bellman

functions for , ,

by using formulas (27), (25). Finally we get the minimal

variance

(28)

To calculate the optimal sample sizes we should

apply ”forward” procedure of dynamic programming technique.

At first, we find and by solving the

equation

(29)

where minimization is realized by condition

(30)

Let , .

Then we recurrently determine by analogy the rest and

for :

(31)

by condition

(32)

Moreover we put

(33)

Finally the optimal sizes for are determined by the

following way:

(34)

References

Andronov, A., Merkuryev, Yu. (1996) Optimization of Statistical Sizes

in Simulation. In: Proceedings

of the 2-nd St. Petersburg Workshop on Simulation, St. Petersburg

State University, St. Petersburg, 220-225.

Andronov, A., Merkuryev, Yu. (1998) Controlled Bootstrap Method and

its Application in Simulation of Hierarchical Structures. In: Proceedings

of the 3-d St. Petersburg Workshop on Simulation, St. Petersburg

State University, St. Petersburg, 271-277.

Davison, A.C., Hinkley, D.V. (1997) Bootstrap Methods and their

Application. Cambridge university Press, Cambridge.

Efron, B., Tibshirani, R.Y. (1993) Introduction to the Bootstrap.

Chapman & Hall, London.

Minox, M. (1989) Programmation Mathematique. Teorie et Algorithmes.

Dunod.