Bertrand Networks

Abstract

We study scenarios where multiple sellers of a homogeneous good compete on prices, where each seller can only sell to some subset of the buyers. Crucially, sellers cannot price-discriminate between buyers. We model the structure of the competition by a graph (or hyper-graph), with nodes representing the sellers and edges representing populations of buyers. We study equilibria in the game between the sellers, prove that they always exist, and present various structural, quantitative, and computational results about them. We also analyze the equilibria completely for a few cases. Many questions are left open.

1 Introduction

Competition is known to reduce prices and decrease sellers’ profits. The simplest model to this effect contrasts a seller with a captive market to two competing sellers, where the competition is on price alone, a model known as Bertrand competition. While the seller with a captive market would sell at the “monopoly price” and make a profit, the only equilibrium that the competing sellers may reach is one where they charge the marginal cost, extracting no profit if they have identical constant marginal costs. There is of course much work in the economic literature that deals with various variants of this model as well as with alternative assumptions about the competition (e.g. Cournot competition.)

In this paper we study scenarios in which parts of the market are shared between sellers and other parts are captive. We model the structure of sharing in the market as a hyper-graph where the vertices are sellers, and each hyper-edge represents a market segment, henceforth just market, that is shared by these sellers. The sellers each announce a single price (i.e., price discrimination is impossible111Where price discrimination is possible, the seller simply optimizes in each market separately.) and every buyer buys from the lowest price seller that has access to his market (with some tie breaking rule). The idea is that sellers must balance between competition in each of the markets they compete in and their captive market, and this trade-off will in turn affect those competing with them. In this paper we wish to study how the structure of this graph affects prices and profits of the different sellers.

One may think of many scenarios that are captured – to a first approximation – by such a model. Consider several Internet vendors for some good, where users do not always compare prices among all vendors but rather different subsets of users do their price-comparisons only between a subset of vendors. One may also think about geographic limitations to competition where buyers can only buy from a “close” vendor. Another scenario may involve technology constraints where buyers must choose between essentially equivalent products, but are limited to buying from the subset of those that are “compatible” with their existing systems or that have a certain “feature” that they need. In all these cases, and many others, price discrimination would be quite difficult to do.

Taking a higher-level point of view, this work falls into a more general agenda that attempts “decomposing” a global economic situation into a network of local economic interactions and extracting some global economic insights from the structure of the interaction graph, studied in various models, e.g., in [2, 9, 1, 8, 10, 5] and many others. This agenda is distinct from agendas that consider network formation or network-structured goods, agendas that have also received much attention, including in models related to Bertrand competition [3, 4, 7] as well as in [6] that is this paper’s starting point.

|

|

| (a) | (b) |

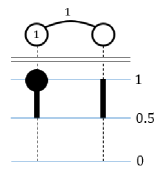

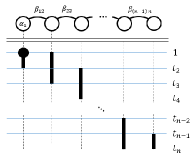

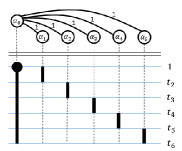

Let us start with the simplest scenario that combines a captive market and a competitive one. Consider the case of two sellers that share a market, but where one of the two sellers also has a captive market of the same size as the shared one. In our simple scenario both sellers have zero marginal cost (i.e., for producing the good) and the buyers in each market will all buy from the seller that asked for the lowest price, as long as that price is at most 1. The two sellers are thus playing a game, where the strategy of each seller is its requested price which lies in the interval . What will the equilibrium look like? It is easy to verify that no pure equilibrium exists. However, a mixed equilibrium does exist and was only recently described in [6] (for more general demand and supply curves). In this unique equilibrium both sellers randomize their asked price in the range in the following way222One may be somewhat skeptical of the relevance of a mixed Nash equiliribrium with continuous support, however we would like to mention that we have run simulations and found that this mixed continuous support equilibrium was closely approximated by the empirical distribution of a simple fictitious play in a discretized version of the game.: the price of the seller that has the captive market satisfies for and , and that of the seller without a captive market satisfies for all . We say that the seller with the captive market has an atom at price , meaning that the seller selects price with positive probability. See Figure 1(a). It may be somewhat surprising that the seller with no captive market gets positive utility (of ) despite having no captive market. This may be contrasted with what would happen if he also succeeds in gaining access to the other seller’s captive market, in which case they would be put in a classic Bertrand competition and all prices would go down to 0.

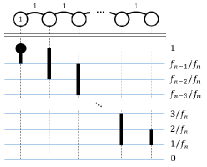

Let us continue with another example: a line of sellers, where each two consecutive ones share a market, and the first one also has a captive market, with all markets being of the same size. It turns out that the unique equilibrium has each seller randomizing his price (according to a specific distribution that we derive) in the interval where is the ’th Fibonacci number starting with (except for the first seller whose bid is capped at 1, with an atom there). See Figure 1(b). The equilibrium utilities of the players in this network are given by , where is the golden ratio.

The paper attempts analyzing what happens in more general situations with multiple sellers and markets where different sellers are connected to different subsets of markets. To focus on the structure of the graph, we keep everything else as simple as possible, in particular sticking to zero marginal costs as well as to a a demand curve where all buyers are willing to buy the good for at most .333 This implies that there are no efficiency issues in this model, and our focus is on prices and revenues. Furthermore, as the main distinction we wish to capture is that of monopoly as opposed to competition, we focus on the case where each market is either captive to one seller or shared between exactly two sellers. This leads us to modeling the network of sellers and markets by a graph whose vertices are the sellers and where each edge corresponds to market that is shared between the two sellers. Each seller (vertex) may have a weight indicating the size of its captive market and each edge will have a weight indicating the size of the pair’s shared market.444In the more general model of an hyper-graph will indicate the size of the market that is shared by the set of sellers. We will analyze Nash equilibria of the game between the sellers. To begin with, it is not even clear that a Nash equilibrium exists: the game has a continuum of strategies (the price is a real number) and discontinuous utilities (slightly under-pricing your opponent is very different than slightly overpricing him). Nevertheless we invoke the results of [11] and show:

Theorem 1.1.

In every network of sellers and markets there exists a mixed Nash equilibrium. Moreover, every equilibrium holds for every tie breaking rules.555 This theorem also holds in the general hyper-graph model.

We then start analyzing the properties of these equilibria. Extending the well known result about Bertrand competition, we show that if no seller has a captive market then the only equilibrium is the pure one where each seller sells at 0 (his marginal cost) and gets 0 utility. We observe the following converse:

Theorem 1.2.

In every connected network of at least two sellers where at least one seller has a captive market, there does not exist any pure Nash equilibrium. In every mixed-Nash equilibrium of this network no seller has any atoms, except perhaps at 1. Moreover, all sellers have their infimum price bounded away from zero, and get strictly positive utility.666 The fact that lack of captive markets implies zero prices extends to the general hyper-graph model but this theorem does not, nor do the ones below.

We do not have a general algorithm for computing an equilibrium of a given network, however we do show that the problem can be completely reduced to finding the supports of the sellers’ strategies and the set of sellers that have an atom at 1.

Theorem 1.3.

Given the supports of sellers’ strategies, with finitely many boundary points, and the set of sellers that have an atom at 1, it is possible to explicitly, in polynomial time, compute an equilibrium of the network if such exists. Generically this equilibrium is unique for this support and set of sellers with atoms at 1.

Generally speaking there may be different equilibria for a network with different supports of sellers’ strategies, with seller’s utilities varying between them. We next embark on an analysis of a set of networks for which we can effectively analyze and prove uniqueness of the equilibrium.

Theorem 1.4.

Every network of sellers and markets that has a tree structure and a single captive market has an essentially unique equilibrium which is described explicitly and polynomially computable from the network structure.

Our analysis is explicit about what “essentially unique” means, completely characterizing the degrees of freedom. In particular, the utilities of each seller are the same over all equilibria. This theorem has two significant limitations: being a tree and having a single captive market. We provide examples showing that both restrictions are necessary and relaxing either one of them results in multiple equilibria with multiple possible utilities for a seller. We are able to fully analyze and prove uniqueness of equilibria for an additional case: a “Star” where each seller may have a captive market and every peripheral seller shares a market with the center and all shared markets have the same size.

For general graphs, while equilibria are not necessarily unique, nor are we in general able to characterize them, we do prove various structural results as well as quantitative estimates on prices and utilities in every possible equilibria. We are able to bound the amount of utility that ”flows” from sellers with captive markets to sellers that are “decoupled” from them in each of two senses: (1) distance (2) cut:

Theorem 1.5.

(Informal) In every non-trivial network and in any equilibrium:

-

1.

The utility of every seller is bounded from below by an expression that decreases exponentially in his distance from any captive market.

-

2.

The utility of every seller is bounded from above by a linear expression in the size of the shared markets in an edge-cut that separates him from all captive markets.

-

3.

For every seller, as the sizes of all shared markets in an edge-cut that separates him from all captive markets increase to infinity, his utility decreases to 0.

Note that our “line of sellers” example above shows that the decrease in utility in part 1 of the theorem may indeed be exponential. Part 3 of the theorem may be surprising, with the intuitive explanation being that the largeness of the markets in the cut causes the sellers in these markets to “focus” on them, not letting indirect competition “spread” over the cut.

Structure of the paper

We start by describing our model in section 2, and before diving into the body of our analysis, present a few simple examples in section 3. Our general analysis of the existence, robustness, and properties of equilibria are given in section 4 that also proves theorems 1.1 and 1.2. Section 5 reduces the problem to analysis only at the boundary points, proving theorem 1.3. Section 6 analyzes trees with a single captive market and proves theorem 1.4 and section 7 analyzes the star network. Finally, section 8 analyzes utilities in general networks, proving a formal version of theorem 1.5. Many open problems remain, and we sketch some of them in our concluding section 9.

2 Model

In a general network economy (network for short) there are sellers and a collection of disjoint buyer populations which we call markets. All sellers sell the same type of good, and each seller is associated with a supply curve which specifies how many units the seller can sell at any given price. Each market has access to some of the sellers, possibly not to all of them. Each market is associated with a demand curve, specifying how many units the population would buy at a given price.

We will focus on the following subclass of networks. First, we assume that all buyers in a market are willing to pay up to per unit but no more. Also, we assume that each seller has a marginal cost of for producing the good and is able to supply any quantity. Each buyer will purchase a full unit of the good from whichever accessible seller has the lowest price. Finally, we assume that each market has access to at most two sellers.

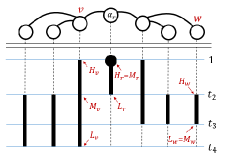

As each market has access to at most two sellers, it is natural to represent a network by a graph as follows. Each seller is represented by a node in the graph. If a market has access to only a single seller, we say that this market is captive. We write for the size of the captive market of seller , where if seller has no captive market. Note that we assume without loss of generality that each seller has at most one captive market, since having two or more is equivalent to having one with the combined size. We write . If a market has access to two sellers and , we represent that market by an edge from node to node , and use to denote the size of that market. We use to denote the set of sellers that share a market with seller , and write . See Figure 2 for an illustration.

A network defines the following pricing game between the sellers. Each seller needs to offer a price per unit of the good. Each edge (market) buys from the incident node (seller) that offers the lowest price. A captive market always buys from its associated node. Formally one needs to specify a tie breaking rule for the case of a tie, but we will later show that ties never occur in equilibrium (see Section 4), so from that point on will usually omit tie-breaking considerations from our discussion and notation. Note that each seller offers the same price to all available (i.e. incident) markets (edges). Sellers offer prices simultaneously, and can use randomization to determine prices. We assume that all sellers are risk neutral.

Consider the case that each seller offers price , the utility of seller with price in this case is

Here is an indicator taking value if , and otherwise; formally, this models loosing in case of a tie. As mentioned above, changing the tie breaking rule will result in exactly the same equilibria.

A mixed strategy of seller can be represented by a CDF with support . The support of is (w.l.o.g) contained in (as buyers are not willing to pay more than 1 per item). We use to denote the probability that puts strictly below . If we say that has an atom at and is its size. We denote the probability that places on at least by . A point is a boundary (transition) point for seller if every open interval containing intersects but is not contained in . Note that if is a collection of intervals, then the set of boundary points is precisely the set of endpoints of these intervals. We use and to denote the supremum and infimum of .

We can now define , the utility of (risk-neutral) seller when declaring price , when the other sellers price according to :

| (1) |

As mentioned, in Section 4 we show that ties do not matter and that no two neighboring sellers can both have an atom at . From that point on, when considering an equilibrium, it would be notationally convenient to slightly deviate from the formula above that corresponds to loosing the tie with as we formally defined. Instead, for a seller that has a neighbor with an atom at 1 we will replace the above by the formula that corresponds to winning the tie at 1 against and define:

This is notationally convenient as it maintains so in many arguments this avoids the extra notation of taking limits as approaches . In particular, this notation is useful as it allows us to think of every price in the support as being optimal for . This is trivially true for every point in which the utility of is continuous. As atoms only happen at , the price of is the only possible point of discontinuity. With this definition of the utility of seller with supremum price of is also optimal at . We use to denote the equilibrium utility of seller . Additionally, when is clear from context we will abuse notation and write .

A network consists of a graph and market sizes. We say that a network is non-trivial if it is connected, has at least two sellers, and has at least one captive market. For most of the paper we will focus on non-trivial networks.777Indeed, for disconnected graphs our results will hold for each component separately, and the degenerate case of no captive markets is solved in Theorem 4.5 and thus is irrelevant to any later parts of the paper.

3 Simple Examples

We begin by building some intuition for our pricing game by describing a few simple examples. This intuition will be helpful when describing general properties of equilibria in Section 4 and the structure of equilibria in Section 5.

The simplest network is a single seller that is a monopolist over a single market. In this case he will price the item at 1 and extract all surplus. Another simple network is the case of two sellers with no captive markets who share a single market; this is precisely a Bertrand competition (with marginal cost of 0). In this example the unique equilibrium is for both sellers to price the item at (regardless of the size of the shared market), and all surplus goes to the buyers.

We now consider two more interesting examples with non-trivial networks.

|

|

| (a) | (b) |

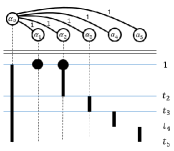

Example 3.1 (General case of Sellers).

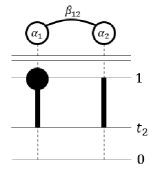

Consider two sellers that share a market, where additionally each seller has his own captive market. The captive markets have sizes and the shared market has size . Theorem 4.6 will imply that, in the unique equilibrium, the support of each seller’s strategy is some interval where , and moreover seller has no atom at . See Figure 2(a). It holds that and . If seller sets price , he will sell only to his captive market and lose the shared market to seller with probability . On the other hand, if he sets price , he will win the shared market with probability . Since prices and are both in the support of , it must therefore hold that , and thus . Applying similar reasoning to seller , we have , thus the size of the atom of seller at is . Note that seller has no atom if and only if the sellers are symmetric ().

We can now explicitly find the CDFs, using the fact that sellers must be indifferent within their supports. For every it holds that , and thus . It also holds that , and thus . Note that the seller with the larger captive market gains nothing from the shared market (his utility is ), while the other seller gains more than when the sellers are asymmetric.

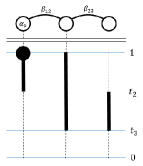

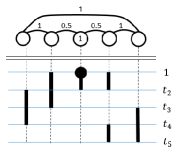

Example 3.2 ( Sellers in a line with captive market).

In this example, seller has a captive market of size and shares a market of size with seller . Seller shares a market of size with seller . Neither seller nor has a captive market. As we prove in Section 6.4, the unique equilibrium has the following form. Seller has an atom of size at . For some , the support of seller is , the support of seller 2 is , and the support of seller is . See Figure 2(b) for a “sketch” of this equilibrium structure.

Given the form of the equilibrium, it is possible to solve for the values of and and in a method similar to Example 3.1. This turns out to give , , and . We now have the values of for all and , and, similarly to Example 3.1 we can deduce the full form of the CDFs that will be the piece-wise linear in functions that agree with these values. The general methodology of finding the equilibrium from the “sketch” is described in section 5 with the details for general line networks in Section 6.4.

4 Equilibrium Analysis

In this section we study the existence and properties of equilibria in pricing networks. We first establish that ties occur with probability in any equilibrium. We then show that the non-occurence of ties implies that an equilibrium always exists. Finally, we describe some general properties of every equilibrium.

4.1 Tie Breaking

We first show that any valid tie breaking rule results in the same set of equilibrium. Moreover, in any equilibrium, the utility of each seller is independent of the tie-breaking rule.

A valid tie breaking rule specifies for every two sellers and that share a market, and every price vector with , the fraction of the market that buys from and respectively: and that and respectively (where ). To determine the impact of tie-breaking, let us revisit the definition of seller utilities in case of a tie. Consider the case that each seller offers price . The utility of seller is then

where is the fraction of the market shared by and for which sells. That fraction is if , and is if .

We would like to compute the utility when seller uses price and the others sample according to . Define As sellers are risk neutral, the utility obtained by seller when selecting price , assuming others set prices according to , is

We can now show that tie breaking has no impact on the equilibria of the game.

Theorem 4.1.

Fix any network. If a profile of strategies is an equilibrium with some valid tie breaking rule, then that profile is an equilibrium for any other valid tie breaking rule. Moreover, in each such equilibrium, the utility of each seller is independent of the tie breaking rule.

Proof.

As ties at price do not influence seller utilities, it is enough to show that ties at positive prices have measure zero in any equilibrium. To prove this it is enough to prove the following lemma.

Lemma 4.2.

Fix any valid tie breaking rule. In any network and any equilibrium, no two sellers who share a market both have an atom at the same positive price.

Proof.

The lemma follows from the fact that for one seller , a slight decrease in the price will allow to win over the atom for sure (instead of just a fraction of the time due to tie breaking) and increase his utility. We next formalize this claim.

Assume that and share a market and both have an atom at . We assume without loss of generality that (otherwise replace and . Note that ).

Note that is an optimal price for seller . Assume that a seller that shares a market with and has an atom of size . We show that there is a price with , contradicting the assumption that is optimal for . Indeed, for

thus

where the strict inequality follows from the existence of a seller that is a neighbor of for which it holds that has an atom at () and . ∎

This concludes the proof of the theorem. ∎

We note that Lemma 4.2 implies that the utility of every seller at every point smaller than is continuous in his price. Thus any price in , including the boundary of , is optimal for the seller.

4.2 Existence of equilibrium

We show that a mixed equilibrium is guaranteed to exist for any network. This is a non-trivial claim, since the strategy space is infinite and utilities are discontinuous.

Theorem 4.3.

In any network there exists a mixed equilibrium.

Proof.

The existence of a mixed equilibria in our game follows from the general results of [11]. They consider general games where the strategy sets are compact metric spaces and the utility functions are only defined to be continuous on a dense subset of the space of strategy profiles. Their main motivation is scenarios where the utilities are continuous everywhere except at sparse “tie points” in which some discontinuity occurs. This is exactly the case we have in our setting where the strategy set of a seller is the interval and the utility of every seller is continuous (linear in his own price) everywhere except at points where his price equals that of another seller, in which case a discontinuous jump in utility occurs. To place our setting into their formalism we simply consider the subspace of strategy profiles that have no ties, which is a dense subset, and over this subset the utilities in our game are continuous.

The main result of [11] is that as long as we allow our equilibrium to endogenously choose “tie-breaking” utilities for the strategy profiles that lie outside the dense subset then a mixed Nash equilibrium exists. Specifically, the endogenously chosen profile of utilities lies in the convex hull of the closure of the graph of utilities in the dense subset over which the utility function was exogenously defined and continuous. In our setting, at a point with a tie between sellers and and the endogenously chosen utilities for and will be some convex combination of the utility when wins the market in case of tie and when does so. That corresponds to each of the two sellers winning some fraction of the market in a tie, with the sum of the fractions being exactly 1.

At this point we can invoke the fact that, for our games, the tie breaking rule does not matter as discussed in Section 4.1: for the endogenously-chosen tie breaking rule, a mixed Nash equilibrium exists by the results of [11]. This tie breaking rule certainly falls into the family of tie-breaking rules considered in Section 4.1. Therefore, for any other tie-breaking rule in this family, the same profile of mixed strategies is still a mixed-Nash equilibrium. ∎

Theorem 4.3 shows that an equilibrium exists, but is it unique? In the example presented in Section 7.2 we show that there may exist multiple equilibria. Moreover, these equilibria are truly distinct from the perspective of the sellers, in the sense that they are not utility-equivalent (i.e. some sellers’ utilities differ between the equilibria).

Is it possible that a pure equilibrium exists? We observe that when at least one seller has a captive market, a pure equilibrium never exists. Recall that a non-trivial network is connected, has at least two sellers, and has at least one captive market.

Observation 4.4.

If a network is non-trivial then there does not exist a pure equilibrium (that is, in any equilibrium at least one seller uses a mixed strategy).

Proof.

Assume that a pure equilibrium exists. Note that not all sellers can choose price , as a seller with a captive market would generate positive utility by selecting a positive price. We further claim that no seller can choose price . Indeed, if some seller chooses price , then there exists a seller that chooses price and that has a neighbor that chooses positive price . In this case, this seller with price receives utility , but would receive positive utility (from the market shared with ) if he chose price . This contradicts the equilibrium assumption, and hence no seller chooses price .

Let be a seller with minimal price . By Lemma 4.2 none of his neighbors price at . As has finitely many neighbors and they all price using a pure strategy, there is an such that if increases his price by he sells to exactly the same set of buyers for a higher price, increasing his utility. This contradicts the equilibrium assumption. ∎

Observation 4.4 does not consider networks in which no seller has a captive market. For networks with no captive markets we show that the unique equilibrium is a pure equilibrium in which every seller selects price .

Theorem 4.5.

Consider any connected network with at least two sellers. If no seller has a captive market then the unique equilibrium is for all sellers to price the good at ( for all ). In this equilibrium every seller has zero utility.

Proof.

Consider any equilibrium (either pure or randomized) and assume that not all sellers always price the good at . This means that for some seller it holds that and that . This implies that any seller that is neighbor of has positive utility, and thus positive infimum price. By Observation 4.7 every seller has a positive infimum price and positive utility in equilibrium. Consider a seller with maximal supremum price, breaking ties in favor of a seller that has an atom at that price. This means that if does not have an atom at , none of his neighbors has an atom. Moreover, if has an atom at it is still true that none of his neighbors has an atom at this price due to Lemma 4.2. In any case is in the support of and when pricing at seller make no sell in any of his non-captive markets. That seller has no captive market and thus he never sells and has zero utility, a contradiction. ∎

Motivated by Theorem 4.5, we consider only non-trivial networks in later sections.

4.3 Properties of Equilibria of Non-Trivial Networks

We next present some properties that every equilibrium in a non-trivial network must satisfy.

Theorem 4.6.

Fix any non-trivial network and equilibrium. The following holds:

-

1.

There exists some positive (independent of the equilibrium) such that the support of prices of every seller is contained in . Moreover, every seller has positive utility, and his utility is at least .

-

2.

If seller has an atom, that atom must be at , and it must be the case that has a captive market. None of the neighbors of has any atoms.

-

3.

If seller has no captive market and none of his neighboring sellers has an atom at , then seller ’s supremum price is strictly less than .

-

4.

For any seller the support excluding the point is contained in the union of the supports of the neighbors of .

-

5.

If the supremum of the support of seller is at least the supremum of the support of all his neighboring sellers then the supremum of his support is .

-

6.

There is at least one seller with utility . That seller has a captive market () and . Any seller with no captive market has no atoms.

The proof of the theorem follows from the following sequence of claims and observations. Our first observation holds for any network.

Observation 4.7.

Fix any network and any equilibrium. If there is at least one seller with support that has a positive infimum (), then there exists some positive such that in any equilibrium the support of prices of every seller is contained in . Moreover, in any equilibrium every seller has positive utility, and the utility is at least .

Proof.

We show that any seller that has a neighbor with positive infimum price, also have positive infimum price. Indeed, assume that has and consider a seller that shares a market of size with . for small enough , by pricing at seller can unsure utility of at least , thus any price in the support of must be at least .

The above claim implies the existence of such that in any equilibrium the support of prices of every seller is contained in . This implies that every seller has positive utility in equilibrium, as the utility must be at least as high as the utility achieved by pricing at , which is least .

Finally, observe that in any equilibrium the utility of is at least , as by pricing the good at seller gets utility of at least (for any strategies of the others). ∎

Corollary 4.8.

Fix any non-trivial network (connected with at least one captive market). There exists some positive such that in any equilibrium the support of prices of every seller is contained in . Moreover, in any equilibrium every seller has positive utility, and the utility is at least .

Proof.

Consider some seller with a captive market of size . If prices at , his utility is at most (recall that is the total size of all non-captive markets of ), thus any price in the support of must be at least . The claim now follows from Observation 4.7. ∎

Note that this in particular says that the profile in which all sellers post a price of is not an equilibrium when there is a captive market.

Observation 4.9.

Fix any non-trivial network and any equilibrium. If price is in the support of seller then there exists a neighbor of such that for any it holds that .

Proof.

By Corollary 4.8 seller has positive utility and thus wins with positive probability with the price of . There must exist a neighbor of seller such that for any it holds that , as otherwise a small enough increase in the price by will result with higher utility for him (he still wins the same buyers with the same positive probability, but for a higher price). ∎

Observation 4.10.

Fix any non-trivial network and any equilibrium. If seller has an atom, that atom must be at , and it must be the case that has a captive market. None of the neighbors of has any atoms.

Proof.

Assume in contradiction that in some equilibrium there is a seller with an atom at some , which means that is in the support. By Corollary 4.8 seller ’s support has positive infimum (), and thus has no atom at , so we can assume that . By Observation 4.9 there exists a neighbor of such that for any it holds that . This means that has optimal prices arbitrarily close to (above ). By Corollary 4.8 wins with positive probability with any price in his support. Now, seller can increase his utility by pricing at that is large enough, as he now also wins over the atom of but losses arbitrarily small in price (the formal argument is similar to the one presented in Lemma 4.2 and is omitted).

Finally, if a seller has an atom at this means that his utility is (as none of his neighbors has an atom at 1 by Lemma 4.2). If he has no captive market this means that his utility is zero, in contradiction to Corollary 4.8.

None of the neighbors of has any atoms as any such atom must be at , but that is impossible by Lemma 4.2. ∎

Observation 4.11.

Fix any non-trivial network. Consider any seller that has no captive market and assume that in some equilibrium none of his neighboring sellers has an atom at . Then seller ’s supremum price in that equilibrium is strictly less than 1.

Proof.

Seller has no captive market. Assume that . As none of his neighbors has an atom at , his utility is continuous at and is eqaul to which is as he has no captive market. But, if has a captive market then he has positive utility by Corollary 4.8. A Contradiction. ∎

Observation 4.12.

Fix any non-trivial network and any equilibrium. For any seller the support excluding the point is contained in the union of the supports of the neighbors of .

Proof.

By Observation 4.10 no seller has any atom, except possibly at .

Assume that the claim is not true, then for some seller and some prices in the support of it holds that for every neighbor of . It is easy to see that in this case the utility of by price is strictly larger then his utility by price , contradiction the assumption that is optimal for (any point in the support that is not is optimal). ∎

The next corollary shows that any local minimum of the infima must be shared by at least two sellers.

Corollary 4.13.

Fix any non-trivial network and any equilibrium. If the infimum of the support of seller is at most the infimum of the support of all his neighboring sellers then there is some neighboring seller with the same support infimum.

The next observation shows that any local maximum of the suprema is a global maximum. It implies Theorem 4.6 (5).

Observation 4.14.

Fix any non-trivial network and any equilibrium. If the supremum of the support of seller is at least the supremum of the support of all his neighboring sellers then the supremum of his support is .

Proof.

Corollary 4.15.

Fix any non-trivial network and any equilibrium. There is at least one seller with utility , that seller has a captive market ().

Proof.

Consider seller with the maximum supremum price, breaking ties in favor of a seller with an atom. By Observation4.14 it holds that . None of ’s neighbors has an atom at by Lemma 4.2. When seller prices arbitrarily close to he only wins his captive market, thus his utility is . It must be the case that , as every seller has positive utility, by Corollary 4.8. ∎

5 Supports and Equilibrium

In general, the definition of a mixed Nash equilibrium requires checking a continuum of equations and inequalities. In this section we show that the space of potential equilibria – and the conditions to check – can be simplified immensely. An equilibrium sketch (defined formally below) describes each seller’s support and the set of players that have an atom at . We will show that once the sketch of an equilibrium is known, the full specification of an equilibrium with that support can be determined. Moreover, one can efficiently decide whether a given sketch corresponds to an equilibrium: it suffices to check the equilibrium conditions at the boundary points of the players’ supports. We also provide conditions under which a sketch uniquely determines an equilibrium.

Assume that we are given the support of each CDF for every seller . Let be the set of boundary points for the support , and let be the union of all these sets, we call it the set of boundary points of . Let be the set of points in . That is, is the set of boundary points that are in the support of seller .

We say that support has finite boundary if is finite. Suppose all sellers have supports with finite boundary. Then is finite; write . We can then write , where . Note that if the CDFs form an equilibrium then and (by Theorem 4.6, items 1 and 6). It will sometimes be convenient to think of the list of points that also includes the point , so we denote . Additionally, for we denote by the set of sellers with support that contains the interval . Note that is empty when , as happens in any equilibrium. Finally, specifies the set of sellers that have an atom at .

Definition 5.1.

A sketch (of an equilibrium) specifies for every seller the support of , where all supports have finite boundary. Additionally, the sketch specifies a set of sellers that should have atoms at . An equilibrium satisfies the sketch if its supports and atoms match those of the sketch.

A sketch solution is a sketch augmented with partial information about a Nash equilibrium, concerning behavior at boundary points. Recall that for seller and point , we denote . Since no seller has an atom at in equilibrium, we have for . Also, is the size of the atom of at .

Definition 5.2.

A sketch solution (of an equilibrium) specifies a sketch and, additionally, it defines values for every seller and point in the set of boundary points of the sketch. These values must satisfy the following linear program (LP1) in the variables , (observe that the values of are not variables).

| (2) |

| (3) |

| (4) |

| (5) |

| (6) |

| (7) |

| (8) |

An equilibrium satisfies the sketch solution if it satisfies the sketch and, moreover, for every and the value of equals the corresponding value in the sketch solution.

We next explain the constraints of the linear program. Constraints (2) state that each seller has the same utility from every boundary point in his support. Constraints (3) state that each seller has weakly lower utility for boundary points that are not in his support. Constraints (4) state that, for each , the CDF for has value at the lowest boundary point. Constraints (5) states that sellers not in have no atom, while constraints (6) state that sellers in have an atom. Note that for the size of the atom of at is exactly . Finally, constraints (7) state that sellers do not price outside their support, while constraints (8) state that they do price inside their support. Observe that as all these constraints must be satisfied in equilibrium. If the linear program cannot be satisfied then an equilibrium satisfying the sketch does not exist.

Since the linear program can be solved in polynomial time, it follows that we can efficiently find a sketch solution for a given sketch.

Observation 5.3.

There exists a polynomial time algorithm that, when given as input a nontrivial network and a sketch, it outputs a sketch solution that satisfies the sketch, if such a solution exists.

We next point out that, generically, there will only be a unique sketch solution that satisfies a given sketch.

Definition 5.4.

Fix a network and a sketch. We say that a network has full rank with respect to the sketch if, for every , the sized matrix with entries for has full rank.888Note that this notion does not depend on .

Note that this condition ensures that if we look at the constraints (2) as linear equations in the variables for every , the system will have a unique solution. This in turn will imply that there is at most one sketch solution that satisfies the sketch (depending on whether the unique solution to constraints (2) satisfy the remaining constraints).

We will say that a statement holds for generic values of certain parameters if the Lebesgue measure of the parameter values for which the statement holds is 1. As any minor of a generic matrix has full rank the following observation is immediate.

Observation 5.5.

Fix a nontrivial network. Then, for every sketch, there exists at most one sketch solution that satisfies the sketch, generically over the shared market sizes .

We next show that a sketch solution suffices for recovering the full information about a corresponding equilibrium (which will be generically unique). Specifically, each CDF can be described by a list of linear functions in .

Lemma 5.6.

Fix a nontrivial network and assume that we are given a sketch solution. There is a polynomial time algorithm that outputs an equilibrium that satisfies the sketch solution, where each is a piece-wise linear functions of the inverse of its input. Moreover, if the network has full rank with respect to the sketch, then this is the unique equilibrium that satisfies the sketch solution.

Proof.

A solution to the linear program specifies for any seller and . We use the solution to define for any seller and , that coincides with the solution on . Together with for every , this will completely define a CDF for each seller. Once we specify the CDFs we check that they indeed form an equilibrium.

For any seller and any we define to be a linear function in on the interval , that is, is of the form . We fix the linear function to the unique linear function that coincides with the solution at the boundaries, that is and .

Given a solution to the linear program above, for seller and define

| (9) |

The next lemma would be useful.

Lemma 5.7.

For the CDFs as defined above, for any seller , and any , the utility is a linear function on the interval , moreover, it is the unique linear function that pass through the points and

Proof.

Consider any point in the interval .

| (10) |

This is clearly a linear function, and clearly it go through the two specified points by the way is defined at these boundary points for every seller . ∎

This lemma shows that for the defined CDFs it is indeed the case that each is indifferent between all the prices in the interval , and that for any interval such that , cannot gain by deviating and pricing on that interval. This prove that the specified CDFs indeed forms an equilibrium.

Finally, we observe that if the network has full rank with respect to the sketch then that equilibrium is the unique one that respects the solution to the LP. Indeed, consider any in the interval . The solution to LP1 specifies utility for every seller . For any , consider the equation for as specified in Equation (10). This is a set of linear equations in the variables for every . As the network has full rank with respect to the sketch this set specifies a matrix of full rank, thus there is at must one solution to the set. ∎

The following theorem (which is a re-statement of theorem 3 from the introduction) follows by combining Lemma 5.6 with observations 5.3 and 5.5.

Theorem 5.8.

There is a polynomial time algorithm that gets a sketch as input and has the following properties. If there exists an equilibrium satisfying the sketch then it will compute such an equilibrium (a list of CDFs each linear in ), and if such an equilibrium does not exist then it will provide a proof of that claim. Moreover, generically in the shared market sizes, the provided equilibrium is unique.

6 Trees with a Single Captive Market

We now turn our attention to a particular type of network: a tree with exactly one captive market. Such a network may have multiple equilibria, but we will show that all equilibria have a particular form and that every equilibrium is utility-equivalent for each seller. Moreover, when the tree is a line with the captive market at one endpoint, there is a unique equilibrium.

Fix an arbitrary tree as our network, and suppose seller is the unique seller with . We will think of the tree as being rooted at . In this rooted tree, we write for the parent of seller (with ), and for the set of children of seller . We say is a leaf if . We will also write , the set of grandchildren of .

Before characterizing the equilibria of our network, it will be helpful to describe a particular type of sketch. In this sketch, the support of each seller is an interval, say . Moreover, for each seller there is a “midpoint” value such that and for each . That is, the “top” portion of a seller’s range is shared with his parent, and the “bottom” portion is shared with each of his children. The root has and each leaf has . Note that if sellers and are siblings then they must have . See Figure 3. We say that such a profile of intervals is staggered.

|

|

| (a) | (b) |

Informally speaking, we will show that there is an equilibrium whose sketch corresponds to a profile of staggered intervals, where only the root has an atom at . In general this equilibrium will not be unique. However, we will show that there is a unique profile of staggered intervals such that, for every equilibrium, for each seller . Our main theorem for this section, which is a more detailed statement of Theorem 1.4 from the introduction, is as follows.

Theorem 6.1.

Fix a rooted tree with single captive market, as described above. Then there exists a profile of staggered intervals such that, for any equilibrium of the network and every seller ,

-

1.

,

-

2.

, and

-

3.

and for all .

This profile of intervals (and an equilibrium) can be computed from the network structure in polynomial time, and every equilibrium is utility-equivalent for each seller.

We prove Theorem 6.1 in two parts. In Section 6.1 we prove that, for any given equilibrium, there is a corresponding profile of staggered intervals satisfying the conditions of Theorem 6.1. In Section 6.2 we complete the proof of Theorem 6.1 by showing that the profile of staggered intervals corresponding to a given equilibrium can be fully described and computed as a function of the network weights only. This will imply that there is a single interval profile that satisfies the conditions of Theorem 6.1 for all equilibria. In Section 6.3 we explore some comparative statics implied by our equilibrium characterization. In Section 6.4 we focus on the special case of a line network, where we show that there is a unique equilibrium. We will defer some proof details to Appendix A.

6.1 The Form of an Equilibrium

Fix a tree network as above. In this section we prove of the following lemma.

Lemma 6.2.

For any equilibrium , there is a profile of staggered intervals such that, for every seller , and . Moreover, and for all .

Lemma 6.2 asserts the existence of an interval profile for each equilibrium, whereas Theorem 6.1 makes the stronger claim that a single profile applies to all equilibria. Fix equilibrium F. We observe that the sellers’ suprema must be decreasing with depth.

Claim 6.3.

We have and for all . Also, for each seller , with equality only if .

We can now define a profile of staggered intervals corresponding to equilibrium . We begin with the lower bounds of the intervals. For each with , define . For with but , let . Finally, for each leaf , . For the upper bounds, set for each , and for each . Let and for each . Claim 6.3 implies that for each , with only if is a leaf and only if . Thus is, in fact, a profile of staggered intervals.

The main technical step in the proof of Lemma 6.2 is to show that for each . Roughly speaking, we show that if some seller bids below , then we can find a certain pair of prices and such that , a child of , and a grandchild of all maximize utility at both and . We then show that such a circumstance leads to a contradiction, due to the relationship between these prices and the supports of the neighbors of the three nodes.

Proposition 6.4.

For each seller , . Moreover, for each that is not a leaf, there exists with .

Proposition 6.5.

For each seller , .

Proposition 6.6.

for each seller .

Combining the results in this section completes the proof of Lemma 6.2.

6.2 Uniqueness of Intervals

In Section 6.1 we defined a profile of staggered intervals for equilibrium . In Appendix A.1 we show that these intervals are uniquely determined by (and can be efficiently computed from) the network, completing the proof of Theorem 6.1.

Lemma 6.7.

There exists a profile of staggered intervals such that for every and every equilibrium it holds that .

A corollary of our analysis is that there exists an equilibrium in which for each , and in particular this equilibrium can be computed efficiently. Another corollary is that that every equilibrium is utility-equivalent for each seller.

Corollary 6.8.

All equilibria are utility-equivalent for all sellers.

Proof.

Let be the profile of interval midpoints corresponding to our tree network, from Theorem 6.1. Then, for each seller , we have in every equilibrium. Also, in every equilibrium. The seller utilities are therefore equilibrium-invariant, as required. ∎

6.3 Utilities and Captive Market Size

One implication of our equilibrium analysis is that, in every equilibrium, each seller’s utility increases as increases.

Proposition 6.9.

For fixed shared market sizes , the value of is strictly increasing as increases, for every seller .

Our analysis in Section 8.2 allows us to relate the size of a shared market to the utilities of the descendents of . Write to mean is a strict descendent of .

Proposition 6.10.

Fix shared market sizes and captive market size . Choose node . If we take , then for all . Alternatively, as , we again have for all .

6.4 Special Case: A Line with a Single Captive Market

Consider now the special case that our network is a line with a single captive market belonging to one of the endpoints, . Label the sellers , with and for all . A corollary of Theorem 6.1 is that there is a unique equilibrium. See Figure 3(a) for an illustration of the sketch of this equilibrium.

Claim 6.11.

For the line network with a single captive market belonging to a seller at one endpoint, there is a unique equilibrium. Moreover, this equilibrium has a sketch of the following form: , only seller has an atom at , and for each (where we define and for notational convenience).

Example 6.12.

As an illustration of our equilibrium for the line, consider the case in which and for all . By Claim 6.11, the unique equilibrium has a sketch with boundary points , for all , and an atom at for seller .

Considering the utility of seller at declarations and , we have

Moreover, considering the utility of each seller at points and , we have

where we used Claim A.5 in the last equality to infer that . A simple recursion then implies that for each , where denotes the th Fibonacci number, indexed so that . Since we know , we can solve for to conclude that for each .

Since for each , we conclude for each seller . In particular, the utilities of sellers decay exponentially with the distance to the captive market, with the rate of decay converging to the golden ratio as grows large.

6.5 Non-uniqueness for Cycles with a Single Captive Market

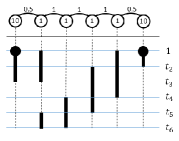

We now show that Theorem 6.1 does not extend to networks with cycles. Our example is a network of sellers in a cycle, where only one seller has a captive market. The network will be symmetric with respect to reflection about seller . We will exhibit a non-symmetric equilibrium for this network. Symmetry will then imply the existence of two different equilibria, in which some sellers achieve different utilities. The example is graphically depicted in figure 4(a). The details are postponed to the appendix and give and .

7 Trees with Multiple Captive Markets

We now consider extending our analysis of trees to allow for multiple captive markets. As we will show, the results of Theorem 6.1 do not extend beyond a single captive market; we present an example with multiple equilibria that are not utility-equivalent. However, we are able to fully characterize the (generically unique) equilibrium for the star network with equal-sized shared markets but generic captive markets.

7.1 Star Networks

In this section we study star networks with all edges having the same market size, and generic sizes of the captive markets. There is a central seller that shares a market of size with each of additional peripheral sellers. The central seller is labelled and the sellers are labelled . Seller has a captive market of size . We assume without loss of generality that . All claims in this section will be made for a generic .

|

|

| (a) | (b) |

We will show that for a star network there exists a unique equilibrium, generically with respect to . In Appendix B.1 we discuss the sellers’ equilibrium utilities.

Theorem 7.1.

A star network has a unique equilibrium, generically over .

We outline the proof; for the complete proof see Appendix B. We first show that for any equilibrium, a sketch that satisfies the equilibrium must have the following form. The support of the center seller is a non-trivial interval with supremum . The support of each peripheral seller is an interval (possibly degenerate, containing only point ). The interiors of the peripheral sellers’ intervals do not overlap. Moreover, the intervals of the peripheral sellers are “ordered” by : if , then lies (weakly) above . More precisely, for some such that , it holds that and each peripheral seller has support . Next, we show that for a star network with generic , there is a unique sketch (set of sellers with atoms at , and setting of ) that can be satisfied in equilibrium. For any sketch with these supports, the network has full rank with respect to the given sketch. Equilibrium uniqueness then follows from Lemma 5.6.

7.2 Non-uniqueness of Equilibrium: Lines with Captive Markets

We now show that tree networks can exhibit multiple, non-utility-equivalent equilibria when there is more than one captive market. Our example network will consist of sellers in a line. This network will be symmetric, but we will exhibit a non-symmetric equilibrium. Symmetry will then imply the existence of two different equilibria, and we will show that some sellers achieve different utilities in these equilibria. The example is graphically depicted in figure 4(b), the details are postponed to the appendix and show and

8 Quantitative Estimates of Utility

This section provides bounds on utility in general networks. We study how utility ”flows” from sellers with captive markets to sellers that are “far away” from captive markets. We study two notions of being “far away:” (1) large distance in the graph to any captive market, and (2) small cut separating from all captive markets.

Theorem 8.1.

Take a non trivial network with sellers and let be the size of the largest captive market. Then there exist constants that depend only on the maximum degree of the network as well as on the maximum ratio between sizes of markets in the network such that, for every seller , the following are true.

-

1.

In every equilibrium, where is the distance of from the seller with captive market .

-

2.

Let be an edge cut that separates from all captive markets and does not contain edges adjacent to , and change all market sizes in to be of size then in every equilibrium of the modified network we have that and .

An implication of item 2 is that ’s utility goes to 0 if the cut size goes to 0 or infinity.

Subsection 8.1 proves (a more explicit version of) part 1 of this theorem and subsection 8.2 proves a more explicit and more general version of part two of this theorem. We will use the following parameters in our estimates:

-

1.

The diameter of the graph denoted by .

-

2.

The “Effective degree” of a seller : . When all market sizes ( and ) faced by are the same then this is exactly the degree of the seller plus . When the market sizes are not identical, this parameter is increased by the imbalance. The effective degree of the entire graph is .

-

3.

.

8.1 Utilities and Distance

The following lemmas provide bounds on seller utilities with respect to the network topology. The first bounds the possible gaps between utilities of neighbors, and the second applies this bound along a path to a captive market.

Lemma 8.2.

In any network and any equilibrium, for any two sellers , we have that .

Proof.

Clearly can never price below since even winning all his markets at a lower price would lead to lower utility than . It follows that if prices at he would certainly win his whole shared market with , getting utility at least which is a lower bound to . ∎

Lemma 8.3.

In any network and any equilibrium, for every seller we have that .

Proof.

For the lower bound on take the seller with and apply lemma 8.2 repeatedly along the shortest path between and . For the upper bound on take the seller for which Theorem 4.6 (6) ensures and again apply lemma 8.2 repeatedly along the shortest path between and , but this time using it to provide upper bounds. ∎

The following examples show that both a dependence in and an exponential dependence in are needed.

Example 8.4.

Consider a line of length , with a single captive market at one end, and all markets of equal sizes. Formally, , and for all . Thus we have and . While per Theorem 4.6 (6), our analysis in Section 6.4 shows that , where is the golden ratio. Thus we see that utilities may indeed decrease exponentially in the distance.

Example 8.5.

Consider a line of three sellers with , , and for some large (so in particular ). While per Theorem 4.6 (6), our analysis of Example 3.2 shows that . Thus we see three interesting and perhaps non-intuitive effects: first, the utility of a seller with no captive market may be larger than that of any seller with a captive market, and the gap may be unbounded. Second, a small captive market may increase the utility of sellers by more than its size, again with the gap being unbounded. Third, these gaps may indeed increase with the effective degree even when the graph size is fixed.

We still do not know though whether the upper bound on may be improved, e.g. to .

8.2 Utilities Across Cuts

Take a network and consider “part” of the network which is “rather separated” from captive markets (perhaps except from tiny ones). We would expect that seller utilities in this part of the market be indeed quite low. In this section we justify this intuition for two different notions of “separate”, one of them quite natural and the second more surprising.

More specifically, consider an edge-cut separating from the rest of the network. It would seem that if the sizes of all markets on this cut are very small then the influence of the captive markets outside of cannot be too large on . This is indeed justified by the following lemma:

Lemma 8.6.

Let be a subset of sellers in the network such that for every , . Denote by and by the diameter of the largest connected component of . Then for every we have that .

Proof.

We will prove it for every connected component of separately. Take the seller with highest supremum price in a component, and as in the proof of Theorem 4.6 (6), we can assume without loss of generality that none of his neighbors in has an atom at 1. When pricing arbitrarily close to his supremum, he will not win any markets that are shared within and thus his utility will be at most . At this point we proceed like in lemmas 8.2 and 8.3, only staying inside the connected component of and thus we get the same upper bound as in lemma 8.3 but with and replaced by and . ∎

In particular this shows a phenomena that can be expected: take an edge-cut that separates a subset of sellers from any captive market, and let the size of all markets in this cut approach zero, then the utilities of all sellers in will approach zero.

The following phenomena may be more surprising: if instead of letting all market sizes in the cut approach zero, we let them approach infinity, then it turns out that the utilities of all sellers in will also go down to zero, possibly except those who are direct neighbors of one of these cut markets that approach infinity. The following theorem looks at a situation where a graph has two different scales of market size: “regular” ones and “big” ones, where the big markets separate a subset of sellers from all captive markets. We show that in this case too, the sellers in get low utility.

Consider a network where all captive markets satisfy and all joint market sizes are either similarly small or much larger (for some ), and denote by the set of large edges and by the sellers that share some large market. For the following lemma we denote and where and are the maximum diameter of a connected component and the effective degree in the sub-network that only contains the large edges within and similarly and in the sub-network that only contains the small edges within .

Lemma 8.7.

If separates a subset of the sellers from all captive markets then for all we have that .

The point is that as is taken to infinity the utilities go to zero.

Proof.

Let us first look at the sub-network on and try to apply lemma 8.6 to it. Notice that after scaling all market sizes down by a factor of , we have an instance where all markets that go out of have weight of at most , and so we can apply lemma 8.6 to it with (where is the total number of sellers in the graph). This would give us a bound of , where we need to emphasize that only takes into account the large edges in and does not depend on . (To be slightly more precise, in case that there are small edges between some the sellers in , we need to apply a variant of lemma 8.6 that defines using only the big edges – as we did – but allows additional small edges as long as their total weight is also summed up as part of the markets whose weight is bounded by . The proof of this variant is identical to the proof of lemma 8.6. If we now scale back up all market weights by a factor of , the strategies of all sellers remain exactly the same, but the utilities scale up by a factor of too, giving for all . This implies that for any and any possible price level we have that since otherwise the that shares a large market with could price at and obtain more than utility just from this market.

Now consider a connected component of and take the seller in it with highest supremum price. When he prices at his supremum he can only get win markets that are shared with some (since separates him from ). Now we can estimate his utility from above by noting that a price of can only win the shared market with probability bounded by giving utility of at most from this market an a total utility bounded by . For the rest of the sellers in ’s connected component we apply lemma 8.3 on obtaining the lemma. ∎

9 Conclusions and Open Problems

We have studied price competition between sellers that have access to different sets of buyers, focusing on the case that at most two sellers can access each of the buyers’ populations. Our work leaves an ample supply of open problems. Is it possible to compute an equilibrium in any graph? We have reduced the problem of equilibrium computation to the problem of finding the supports and the set of sellers with an atom at 1, but it is not clear how to compute these in polynomial time in a general network. Another interesting question concerns the structure of the sellers’ supports in equilibrium: is the support of the equilibrium distributions necessarily finite for a generic instance? Finally, one might like to consider the more general case of hyper-graphs instead of graphs, and relax our assumptions about the forms of the supply and demand curves.

References

- [1] Moshe Babaioff, Noam Nisan, and Elan Pavlov. Mechanisms for a spatially distributed market. Games and Economic Behavior (GEB), 66(2):660–684, 2009.

- [2] Larry Blume, David Easley, Jon Kleinberg, and Eva Tardos. Trading networks with price-setting agents. In Proceedings of the 8th ACM conference on Electronic commerce, EC ’07, pages 143–151, New York, NY, USA, 2007. ACM.

- [3] Shuchi Chawla and Feng Niu. The price of anarchy in bertrand games. In ACM Conference on Electronic Commerce, pages 305–314, 2009.

- [4] Shuchi Chawla and Tim Roughgarden. Bertrand competition in networks. In SAGT, pages 70–82, 2008.

- [5] Margarida Corominas-Bosch. Bargaining in a network of buyers and sellers. Journal of Economic Theory, 115(1):35 – 77, 2004.

- [6] Carlos Lever Guzman. Price competition on network. Working Papers 2011-04, Banco de Mexico, July 2011.

- [7] Ken Hendricks, Michele Piccione, and Guofu Tan. Equilibria in networks. Econometrica, 67(6):1407–1434, November 1999.

- [8] Sham M. Kakade, Michael Kearns, and Luis E. Ortiz. Graphical economics. In In Proceedings of the 17th Annual Conference on Learning Theory (COLT), pages 17–32, 2004.

- [9] Michael J. Kearns, Michael L. Littman, and Satinder P. Singh. Graphical models for game theory. In Proceedings of the 17th Conference in Uncertainty in Artificial Intelligence, UAI ’01, pages 253–260, 2001.

- [10] Rachel E. Kranton and Deborah F. Minehart. A theory of buyer-seller networks. American Economic Review, 91(3):485–508, June 2001.

- [11] Leo K Simon and William R Zame. Discontinuous games and endogenous sharing rules. Econometrica, 58(4):861–72, July 1990.

Appendix A Trees with a Single Captive Market: Details

We now provide the details of proofs from Section 6.

Claim A.1 (Restatement of Claim 6.3).

We have and for all . Also, for each seller , with equality only if .

Proof.

Proposition A.2 (Restatement of Proposition 6.4).

For each seller , . Moreover, for each that is not a leaf, there exists with .

Proof.

Note that the definition of implies that for all , so to show it suffices to show that .

If is a leaf, then and hence Observation 4.12 implies as required. In the case that but is not a leaf, we have by definition. We are left with the case that that has at least one grandchild: .

Suppose for contradiction that there exists and such that . Let , and choose such that this value of is maximized (over all with ), breaking ties in favor of closer to the root.

We claim that there exists such that and either or . If then this follows immediately from the fact that . Otherwise, if for all , then we conclude that , contradicting our choice of . We therefore have as claimed.

If , we have

and

Since , we can write and conclude

| (11) |

where . If we also have (11) with , so (11) holds for any choice of .

Our strategy for the remainder of the proof of Proposition 6.4 is to show that for each . This plus the fact that will contradict (11), leading to the desired contradiction.

From the definition of , there must exist and with , and in particular for all . Since , we then have for all , where

and

so, in particular, for all .

Choose and first suppose that is a leaf. Then for all . We conclude that , and in particular , so as required.

Suppose is not a leaf. From the definition of , for all . We claim that there exists with (this will establish the second claim of Proposition 6.4). Let , and suppose for contradiction that . We must then have , since Claim 6.3 implies that is the only neighbor of who can price at , for each . But then , a contradiction.

We conclude that there exists with , and hence for this . Since all children of have suprema strictly less than by Claim 6.3, we then have

and hence as required. ∎

Proposition A.3 (Restatement of Proposition 6.5).

For each seller , .

Proof.

Proposition A.4 (Restatement of Proposition 6.6).

for each seller .

Proof.

We first claim that . If then by definition. Otherwise, there exists some and with by Proposition 6.4. We must therefore have by Observation 4.12, and hence by Proposition 6.5.

Let . Since we know . Suppose for contradiction that . Then there exists some range such that but for each . However, since , we then conclude that

a contradiction. Thus , so as required. ∎

A.1 Uniqueness of Intervals

In this section we prove Lemma 6.7, which is that there exists a profile of staggered intervals such that for every equilibrium .

Choose an equilibrium and consider the corresponding profile of staggered intervals (and values ). Write to mean that is a (strict) ancestor of . We now show that each is determined by the values of for the ancestors of .

Claim A.5.

Proof.

If then as required. Otherwise, let . By Proposition 6.5 there exists some with . For this seller , we have , which implies

Since from the definition of a staggered interval profile, we then have . The result then follows by structural induction on the tree, with base case . ∎

Claim A.6.

For each seller , is positive and uniquely determined by the network weights. Moreover, is independent of for each .

Proof.

We proceed by structural induction on the tree network. For the base case, suppose is a leaf; then . Next suppose that and . By Lemma 6.2 we have that and hence . Choose and note that by Claim A.5. We conclude that

which implies

| (12) |

Since each is uniquely determined by the network weights by induction, we conclude that is as well. Finally, for , a similar analysis yields

| (13) |

and hence our induction implies is positive and uniquely determined by the network weights, as required. ∎

A.2 Utilities and Captive Market Size

In this section we prove Proposition 6.9, which states that for fixed edge weights , the value of is strictly increasing as increases, for every seller .

Observation A.7.

For every seller , there exist positive independent of such that

A.3 Special Case: A Line with a Single Captive Market

Claim A.8 (Restatement of Claim 6.11).

For the line network with a single captive market belonging to a seller at one endpoint, there is a unique equilibrium. Moreover, this equilibrium has a sketch of the following form: , only seller has an atom at , and for each (where we define and for notational convenience).

Proof.

By Theorem 6.1, there is a staggered profile of intervals such that , and moreover . Since for all , we have , and hence for each . Since and , we conclude that for each . We therefore have for each seller .

We can now describe the sketch of our equilibrium. We have a set of boundary points with for each . Our supports are of the form for each .

A.4 Non-uniqueness for Cycles with a Single Captive Market

Here are the details of the example depicted in figure 4(a). The set of sellers is . We will have and for . The shared market weights are . Note that this market is symmetric in terms of reflection around seller .

We now describe a sketch for this network. Our set of boundary points will be . Seller is the only one with an atom at . The sellers’ supports are , , , , and .

Thinking of program (LP1) from Section 5 as a quadratic program in which the boundary points are treated as variables, we can solve to find a sketch solution. The boundary points of this solution are (approximately)

and the relevant values of are given by

At this equilibrium, and .

By symmetry of the network, there exists a second equilibrium in which the cycle is reflected about seller ; that is, with the roles of sellers and reversed, and the roles of sellers and reversed. In this equilibrium, and . These two equilibria are therefore not utility-equivalent for the sellers, as required.

Appendix B Star: Proof of Theorem 7.1

We restate and prove Theorem 7.1.

Theorem B.1.

For a star network with generic , there exists a unique equilibrium.

We first outline the proof. To prove the claim we first show that for any equilibrium, a sketch that satisfies the equilibrium must has the following form. The center price on a non-trivial interval with supremum , and the peripheral sellers each price on an interval (possibly degenerated to the point ), the interior of these intervals do not overlap. Moreover, the interval of a peripheral seller is above the intervals of any other peripheral seller with a smaller captive market. Formally, for some such that it holds that the support of the center is the interval . Additionally, Each peripheral seller has support . Next, in Lemma B.7 we show that for a star network with generic , there is a unique sketch (set of sellers with atoms at , and setting of ) that can be satisfied in equilibrium. For any sketch with these supports, the network has full rank with respect to the given sketch. Equilibrium uniqueness follows from Lemma 5.6.

Consider any equilibrium in this market. For any seller and any point , recall that . As each peripheral node has only one neighbor (the center), and its support (except possibly an atom at 1) must be contained in the center’s support (Observation 4.12), the center cannot be pricing at with probability . Additionally the same observation implies that there is at least one peripheral seller that is not always pricing at .

Observation B.2.

For a star network with in any equilibrium the intersection of the supports of any two peripheral sellers includes at most one point.

Proof.

Consider two peripheral sellers and assume that both and are in the support of both sellers, and optimal for them. That is,

and

Thus

a contradiction to for every . ∎

Observation B.3.

For a star network, in any equilibrium the support of the center is an interval with supremum of , and this interval is exactly the union of the supports of the peripheral sellers.

Observation B.4.

For a star network, in any equilibrium, for any peripheral sellers with it holds that , with strict inequality if .

Proof.

For any

The utility of is at least his utility by pricing at some thus

when the right inequality follows since and is strict if (since means , by Corollary 4.8). ∎

Observation B.5.

Fix any star network and any equilibrium. For any pair of peripheral sellers with it holds that any price in the support of is at least as high as any price in the support of . That is for any and it holds that .

Proof.

Assume in contradiction that for and . We will show that seller can increase his utility by pricing at instead of . As it holds that

Thus,

Combining with being optimal for (as ), it holds that

we conclude that

Simplifying this shows that this is equivalent to , a contradiction. ∎

Corollary B.6.

For a star network with , any equilibrium must have the following form. For some such that it holds that the support of the center is the interval . Additionally, Each peripheral seller has support .

Note that in particular, there is no equilibrium with infinite-boundary for any of the CDFs.

Lemma B.7.

For a star network with generic , any equilibrium has finite boundary. Moreover, there is a unique sketch that can be satisfied in equilibrium.

Proof.

We continue by presenting additional properties that must hold in any equilibrium. The support of the center is the interval . For every with , is in the support of the center, thus . We conclude that

| (14) |

This means that if then . Thus, once we fix some such that and we fix every .

We next compute for every such that , starting from and decreasing by one at every step. For every peripheral seller with and every it holds that . This holds in particular at .

alternatively

Thus

| (15) |

Equation (15) gives a recurrence for computing given , starting with , this recurrence must hold in any equilibrium. For generic it holds that for every . In equilibrium it must be the case that .

Case 1: If it means that the center must have an atom at . This means that no other seller has any atom. This implies that , which means that for every , . Thus for this case we have a unique sketch that can be satisfied in equilibrium.

We remark that for this case to happen it is necessary that is quite large since for every it must hold that which implies that and thus .

Case 2: If by using the recurrence of Equation (15) we get , then let be the maximum (i.e. first) value for which (15) yields (thus for a generic ). It must hold that has an atom at and while . This imply that and thus every seller always price at (has an atom at of size ) and no other seller has any atom. Additionally, for any this allows us to fix every using the recursion . Thus for this case we have a unique sketch that can be satisfied in equilibrium. ∎

B.1 Equilibrium Utilities