Supplementary Appendix for “Inference on Treatment Effects After Selection Amongst High-Dimensional Controls”

Abstract.

In this supplementary appendix we provide additional results, omitted proofs and extensive simulations that complement the analysis of the main text (arXiv:1201.0224).

1. Intuition for the Importance of Double Selection

To build intuition, we discuss the case where there is only one control; that is, . This scenario provides the simplest possible setting where variable selection might be interesting. In this case, Lasso-type methods act like conservative -tests which allows the properties of selection methods to be explained easily.

With , the model is

| (1.1) | |||

| (1.2) |

For simplicity, all errors and controls are taken as normal,

| (1.7) |

where the variance of is normalized to be 1. The underlying probability space is equipped with probability measure (referred to as “dgp” throughout the paper). Let denote the collection of all dgps where (1.1)-(1.7) hold with non-singular covariance matrices in (1.7). Suppose that we have an i.i.d. sample from the dgp . The subscript signifies that the dgp and all true parameter values may change with to better model finite-sample phenomena such coefficients being “close to zero”. As in the rest of the paper, we keep the dependence of the true parameter values on implicit. Under the stated assumption, and are jointly normal with variances and and correlation .

The standard post-single-selection method for inference proceeds by applying model selection methods – ranging from standard -tests to Lasso-type selectors – to the first equation only, followed by applying OLS to the selected model. In the model selection stage, standard selection methods would necessarily omit wp if

| (1.8) |

where is a slowly varying sequence depending only on P. On the other hand, these methods would necessarily include wp , if

| (1.9) |

where is another slowly varying sequence in depending only on P. In most standard model selection devices with sensible tuning choices, we shall have and with constants and depending only on P. In the case of Lasso methods, we prove this in Section 5. This is also true in the case of the conservative -test, which omits if the -statistic , where is the OLS estimator, and is the corresponding standard error. In this case, we have so the test will have power approaching 1 for alternatives of the form (1.9) with and power approaching 0 for alternatives of the form (1.9) with . 111 This assumes that the canonical estimator of the standard error is used.

A standard selection procedure would work with the first equation. Under “good” sequences of models such that (1.9) holds, is included wp , and the estimator becomes the standard OLS estimator with the standard large sample asymptotics under

where . On the other hand, when or and is bounded away from 1, we have that

where . The variance is smaller than the variance from estimation with included if . The potential reduction in variance is often used as a “motivation” for the standard selection procedure. The estimator is super-efficient, achieving a variance smaller than the semi-parametric efficiency bound under homoscedasticity. That is, the estimator is “too good.”

The “too good” behavior of the procedure that looks solely at the first equaiton has its price. There are plausible sequences of dgps where , the coefficient on is not zero but is close too zero,222Such sequences are very relevant in that they are designed to generate approximations that better capture the fact that one cannot distinguish an estimated coefficient from 0 arbitrarily well in any given finite sample. in which the control is dropped wp and

| (1.10) |

That is, the standard post-selection estimator is not asymptotically normal and even fails to be uniformly consistent at the rate of . This poor behavior occurs because the omitted variable bias created by dropping may be large even when the magnitude of the regression coefficient, , in the confounding equation (1.2) is small but is not exactly zero. To see this, note

The term has standard behavior; namely . The term generates the omitted variable bias, and it may be arbitrarily large, since wp ,

if .333Recall that , so as long as assuming that is bounded away from 0 and . This yields the conclusion (1.10) by the triangle inequality.

In contrast to the standard approach, our post-double-selection method for inference proceeds by applying model selection methods, such as standard -tests or Lasso-type selectors, to both equations and taking the selected controls as the union of controls selected from each equation. This selection is than followed by applying OLS to the selected controls. Thus, our approach drops only if the omitted variable bias term is small. To see this, note that the double-selection-methods include wp if its coefficient in either (1.1) or (1.2) is not very small. Mathematically, is included if

| (1.11) |

where is a slowly varying sequence in . As already noted, would be standard for Lasso-type methods as well as for using simple t-tests to do model selection. Considering t-tests and using these rates, we would omit if both and where and denote the OLS estimator from each equation and s.e. denotes the corresponding estimated standard errors. Note that the critical value used in the t-tests above is conservative in the sense that the false rejection probability is tending to zero because We note that Lasso-type methods operate similarly.

Given the discussion in the preceding paragraph, it is immediate that the post-double selection estimator satisfies

| (1.12) |

under any sequence of . We get this approximating distribution whether or not is omitted. That this is the approximate distribution when is included follows as in the single-selection case. To see that we get the same approximation when is omitted, note that we drop only if

| (1.13) |

i.e. coefficients in front of in both equations are small. In this case,

Once again, the term is due to omitted variable bias, and it obeys wp under (1.13)

since . Moreover, we can show under such sequences, so the first order asymptotics of is the same whether is included or excluded.

To summarize, the post-single-selection estimator may not be root- consistent in sensible models which translates into bad finite-sample properties. The potential poor finite-sample performance may be clearly seen in Monte-Carlo experiments. The estimator is thus non-regular: its first-order asymptotic properties depend on the model sequence in a strong way. In contrast, the post-double selection estimator guards against omitted variables bias which reduces the dependence of the first-order behavior on . This good behavior under sequences translates into uniform with respect to asymptotic normality.

We should note, of course, that the post-double-selection estimator is first-order equivalent to the long-regression in this model.444This equivalence may be a reason double-selection was previously overlooked. There are higher-order differences between the long regression estimator and our estimator. In particular, our estimator has variance that is smaller than the variance of the long regression estimator by a factor that is proportional to if ; and when , there is a small reduction in variance that is traded against a small increase in bias. This equivalence disappears under approximating sequences with number of controls proportional to the sample size, , or greater than the sample size, . It is these scenarios that motivate the use of selection as a means of regularization. In these more complicated settings the intuition from this simple example carries through, and the post-single selection method has a highly non-regular behavior while the post-double selection method continues to be regular.

It is also informative to consider semi-parametric efficiency in this simple example. The post-single-selection estimator is super-efficient when and . The super-efficiency in this case is apparent upon noting that the estimator is root-n consistent and normal with asymptotic variance . This asymptotic variance is generally smaller than the semi-parametric efficiency bound . The price of this efficiency gain is the fact that the post-single-selection estimator breaks down when may be small but non-zero. The corresponding confidence intervals therefore also break down. In contrast, the post-double-selection estimator remains well-behaved in any case, and confidence intervals based on the double-selection-estimator and are uniformly valid for this reason.

2. Extensions: Other Problems and Heterogeneous Treatment Effects

2.1. Other Problems

In order to discuss extensions in a very simple manner, we assume i.i.d sampling as well as assume away approximation errors, namely and , where parameters and are high-dimensional and that as before. In this paper we considered a moment condition:

| (2.14) |

where and are measurable functions of , and the target parameter is . We selected the instrument such that the equation is first-order insensitive to the parameter at :

| (2.15) |

Note that and implement this condition. If (2.15) holds, the estimator of gets “immunized” against nonregular estimation of , for example, via a post-selection procedure or other regularized estimators. Such immunization ideas are in fact behind the classical Frisch-Waugh-Robinson partialling out technique in the linear setting and the \citeasnounNeyman1979’s test in the nonlinear setting. Our contribution here is to recognize the importance of this immunization in the context of post-selection inference,555To the best of our knowledge, all prior theoretical and empirical work uses the standard post-selection approach based on the outcome equation alone, which is highly non-robust way of conducting inference, as shown in extensive monte-carlo, in Section 2.4, and in a sequence of fundamental critiques by Leeb and Potscher, see \citeasnounleeb:potscher:review . to develop a robust post-selection approach to inference on the target parameter, and characterize the uniformity regions of this procedure. Our approach uses modern selection methods to estimate and the function defining the intstrument . In an ongoing work, we explore other regularization methods, such as the ridge method or combination of ridge method with Lasso methods, and characterize uniformity regions of the resulting procedures. Also, generalizations to nonlinear models, where is non-linear and can correspond to a likelihood score or quantile check function are given in \citeasnounBCK-LAD and \citeasnounBCY-honest; in these generalizations achieving (2.15) is also critical.

Within the context of this paper, a potentially important extension is to consider a general treatment effect model, where is interacted with transformations of . As long as the interest lies in a particular regression coefficient, the current framework covers this implicitly since could contain interactions of with transformations of controls . In the case a fixed number of such regression coefficients is of interest, we can estimate each of the coefficients by re-labeling the corresponding regressor as and other regressors as and then applying our procedure the fixed number of times. Such component-wise procedure is valid as long as our regularity conditions hold for each of the resulting regression models in this manner.

A related research direction being pursued is the study of estimation of average treatment effects when treatment effects are fully heterogeneous. When the treatment variable is binary (or discrete more generally) our approach is readily amenable to this problem. In this case the parameter of interest is the average treatment effect

where . We can write, assuming again no approximation errors for simplicity, Suppose that the propensity score is , where is a link such as logit or linear, then we can use the moment equations of \citeasnounhahn-pp:

| (2.16) |

where It is straightforward to check that for each :

| (2.17) |

when (i.e., evaluated at the true values). Therefore, by using \citeasnounhahn-pp’s equation we obtain immunization against the crude estimation of either or , just like we do in the partially linear case. Hence we can use the selection approach to regularization and estimate the parameter of interest . Note that in this case the resulting procedure is a double selection method, where terms explaining propensity score and the regression function are selected. Here too we can use the “union” approach in fitting each regression function involved, as it gives the best finite-sample performance in extensive computational experiments. Using the results of this paper, it is not difficult to show for the case that that under the sparsity assumption imposed on both and , and additional assumptions needed to guarantee consistency of post-Lasso estimators and in the uniform norm, that the post-double-selection estimator that solves has the following large sample behavior:

| (2.18) |

where the latter is the semiparametric efficiency bound of \citeasnounhahn-pp. Formal result is proven and stated below, and other formal results along these lines are given in an ongoing work that studies this as well as other types of effects.

2.2. Theoretical Results on ATE with Heterogeneity

Consider i.i.d. sample on the probability space , where we call the data-generating process. Consider the case where treatment variable is binary , and the outcome and propensity equations, as before,

| (2.19) | |||||

| (2.20) |

The first target parameter is the average treatment effect: defined above, which is implicitly indexed by , like other parameters. In this model is not additively separable. The purpose of this section is to show that our analysis easily extends to this case, using our techniques.

The confounding factors affect the policy variable via the propensity score and the outcome variable via the function . Both of these functions are unknown and potentially complicated. As in the main text, we use linear combinations of control terms to approximate and , writing (2.19) and (2.20) as

| (2.21) | |||

| (2.22) |

where and are the approximation errors, and

| (2.23) |

where , , and are approximations to , , and , and for the case of linear link and for the case of the logistic link. In order to allow for a flexible specification and incorporation of pertinent confounding factors, the vector of controls, , we can have a dimension which can be large relative to the sample size.

The efficient moment condition, derived by \citeasnounhahn-pp, for parameter is as follows:

| (2.24) |

where

The post-double-selection estimator that solves

| (2.25) |

where and are post-Lasso estimators of functions and based upon equations (2.21)-(2.22). In case of the logistic link , Lasso for logistic regression is as defined in \citeasnounvdGeer and \citeasnounBach2010, and the associated post-Lasso estimators are as those defined in \citeasnounBCY-honest.

In what follows, we use to denote the norm of a random variable with law determined by , and we to denote the empirical norm of a random variable with law determined by the emprical measure , i.e., .

Consider fixed positive sequences and and constants

, which will not vary with .

Condition HTE () . Heterogeneous Treatment Effects. Consider i.i.d.

sample on the probability space ,

where we shall call the data-generating process, such that equations (2.21)-(2.22)

holds, with . (i) Approximation errors satisfy , , and , . (ii)

With -probability no less than , estimation errors satisfy

, , , ,

estimators and approximations are sparse, namely , ,

and ,

and the empirical and populations norms are equivalent on sparse subsets, namely . (iii) The following boundedness conditions hold: for each , , , , and . (iv) The sparsity index obeys the following growth condition, .

These conditions are simple high-level conditions, which encode both the approximate sparsity of the models as well as impose some reasonable behavior on the post-selection estimators of and (or other sparse estimators). These conditions are implied by other more primitive conditions in the literature. Sufficient conditions for the equivalence between population and empirical sparse eigenvalues are given in \citeasnounRudelsonZhou2011 and \citeasnounRudelsonVershynin2008. The boundedness conditions are made to simplify arguments, and they could be dealt away with more complicated proofs, under more stringent side conditions.

Theorem 1 (Uniform Post-Double Selection Inference on ATE).

Consider the set of data generating processes such that equations (2.19)-(2.20) and Condition ATE (P) holds. (1) Then under any sequence ,

| (2.26) |

(2) The result continues to hold with replaced by . (3) Moreover, the confidence regions based upon post-double selection estimator have the uniform asumptotic validity,

The next target parameter is the average treatment effect on the treated:

The efficient moment condition, derived by \citeasnounhahn-pp, for parameter is as follows:

| (2.27) |

where , and

In this case the post-double-selection estimator that solves

| (2.28) |

where and are post-Lasso estimators (or other sparse estimators obeying the regularity conditions posed in HTE) of functions and based upon equations (2.21)-(2.22), and . As mentioned before, in case of the logistic link , the post-Lasso estimators are as those defined in \citeasnounBCY-honest.

Theorem 2 (Uniform Post-Double Selection Inference on ATT).

Consider the set of data generating processes such that equations (2.19)-(2.20) and Condition HTE (P) holds. (1) Then under any sequence ,

| (2.29) |

(2) The result continues to hold with replaced by . (3) Moreover, the confidence regions based upon post-double selection estimator have the uniform asumptotic validity,

2.3. Proof of Theorems 1 and 2.

The two results have identical structure and have nearly the same proof, and so we present the proof of the Proof of Theorems 1 only.

In the proof means that , where the constant depends on the constants in Condition HT only, but not on once , and not on . For the proof of claims (1) and (2) we consider a sequence in , but for simplicity, we write throughout the proof, omitting the index . Since the argument is asymptotic, we can just assume that in what follows.

Step 1. In this step we establish claim (1).

(a) We begin with a preliminary observation. Define, for ,

The derivatives of this function with respect to obey for all ,

| (2.30) |

where depends only on and , and

(b). Let

We observe that with probability no less than ,

To see this note, that under assumption HT (), under condition (i)-(ii), under the event occurring under condition (ii) of that assumption: for :

for , with evaluation after computing the norms, and noting that for any

under condition (iii). Furthermore, for :

for , with evaluation after computing the norms.

Hence with probability at least ,

(c) We have that

so that

with evaluated at . By Liapunov central limit theorem,

(d) Note that for ,

(with evaluated at ). By the law of iterated expectations and because

we have that

Moreover, uniformly for any we have that

Since with probability , we have that once ,

(e). Furthermore, we have that

The class of functions for is a union of at most VC-subgraph classes of functions with VC indices bounded by . The class of functions is a union of at most VC-subgraph classes of functions with VC indices bounded by (monotone transformation preserve the VC-subgraph property). These classes are uniformly bounded and their entropies therefore satisfy

Finally, the class is a Lipschitz transform of with bounded Lipschitz coefficients and with a constant envelope. Therefore, we have that

We shall invoke the following lemma derived in \citeasnounBelloni:Chern.

Lemma 1 (A Self-Normalized Maximal inequality).

Let be a measurable function class on a sample space. Let , and suppose that there exist some constants and , such hat

Then for every we have

with probability at least for some constant that .

Then by Lemma 1 together and some simple calculations, we have that

The last conclusion follows because by definition of the norm, and

where the last conclusion follows from the same argument as in step (b) but in a reverse order, switching from empirical norms to population norms, using equivalence of norms over sparse sets imposed in condition (ii) , and also using an application of Markov inequality to argue that

Step 2. Claim (2) follows from consistency: , which follows from being a Lipschitz transform of with respect to , once and the consistency of for under .

Step 3. Claim (3) is immediate from claims (2) and (3) by the way of contradiction. ∎

3. Deferred Proofs: Proof of Lemma 1

We establish the result for Lasso (the proof for other feasible Lasso estimators is similar).

By Lemma 7 in \citeasnounBellChenChernHans:nonGauss, under our choice of penalty level and loadings, we have that the condition holds with probability . Thus, the conclusion of Lemma 11 of \citeasnounBellChenChernHans:nonGauss holds with probability , namely for

| (3.31) |

where ,

By Condition SE, with probability for sufficiently large we have so that with the same probability

| (3.32) |

Moreover, by condition RF we have with probability that

| (3.33) |

Finally, since we have

| (3.34) |

since by condition ASM and Chebyshev inequality.

Therefore, for some constant , we have , so that for sufficiently large with probability by Condition SE. In turn combining this bound with (3.32), (3.33) and (3.34) into (3.31) we have that holds with probability which is the first statement of (i).

To show the second statement in (i), note that

where is the Lasso estimator. Again by Lemma 7 in \citeasnounBellChenChernHans:nonGauss we have that the assumptions of Lemma 6 in \citeasnounBellChenChernHans:nonGauss hold with probability . Using Condition SE to bound from below and Condition RF to bound from above with probability as before, and , it follows from Lemma 6 in \citeasnounBellChenChernHans:nonGauss that with probability that

The results regarding Post-Lasso in (ii) follow similarly by invoking Lemma 8 in \citeasnounBellChenChernHans:nonGauss.

4. Split-Sample Estimation and Inference

In this section we discuss a variant of the double selection estimator based on sample splitting. The motivation for the split-sample estimator is that its use allows us to relax the requirement that is assumed in the full-sample counterpart to the milder condition

To define the estimator, divide the sample randomly into (approximately) equal parts and with sizes and . We use superscripts and for variables in the first and second subsample respectively. We let the index refer to one of the subsamples and let refer to the other.

For each subsample , the model is selected based on the subsample independently from the subsample . In what follows the model is used to fit the subsample . A constructive way to obtain and is to apply the double selection method for each subsample to select the sets of controls and .

Then we form estimates in the two subsamples

For an index in the subsample , we define the residuals

| (4.35) | ||||

| (4.36) | ||||

| (4.37) |

where and .

Finally, we combine the estimates into the split-sample estimator based on and is defined as

| (4.38) |

where .

We state below sufficient conditions for the analysis of the split-sample method.

Condition ASTESS (). (i) are i.n.i.d. vectors on that obey the model (2.2)-(2.3), and the vector is a dictionary of transformations of , which may depend on but not on . (ii) The true parameter value , which may depend on , is bounded, . (iii) Functions and admit an approximately sparse form. Namely there exists and and , which depend on and , such that

| (4.39) | |||

| (4.40) |

(iv) The sparsity index obeys . (v) For each subsample , the model satisfies condition HLMS. (vi) We have for some and .

The Conditions ASTESS(i)-(iii) agree with the corresponding conditions in ASTE. The remaining conditions ASTESS(iv)-(v) are implied by Condition ASTE. We note that Condition ASTESS(vi) is needed only for obtaining consistent estimates of the asymptotic variance. Such conditions are mild since they do not require uniform estimation of the functions and .

The next result establishes that the split-sample estimator has similar large sample properties to the full-sample double-selection estimator under weaker growth condition.

Theorem 3 (Inference on Treatment Effects, Split Sample).

Let be a sequence of data-generating processes. Assume conditions ASTESS()(i-v), SM(), and SE() hold for for each and each subsample. The split sample estimator based on and obeys,

Moreover, if Condition ASTESS()(vi) also holds, the result continues to apply if and are replaced by and for and defined in (4.37) and (4.36).

Proof.

We use the same notation as in the proof of Theorem 1 with the addition of sub/superscripts indicating the appropriate subsample , where .

Step 0.(Combining) In this step we combine both subsample estimators. Letting , for , so that we have

where we are also using the fact that

which follows similarly to the proofs given in Step 5.

For , define

where are i.n.i.d. with mean zero. We have that for some small enough

by Condition SM(ii).

This condition verifies the Lyapunov condition and thus implies that .

Step 1.(Main) For the subsample write so that

By Steps 2 and 3, and . Next note that by Chebyshev, and we have that and are bounded from above and away from zero by assumption.

Step 2. (Behavior of .) Decompose

First, note that by Condition ASTESS we have

Second, by the split sample construction, we have that is independent from , and by assumption of the model is also independent of . Thus by Chebyshev inequality

where the last relation follows by ASTESS.

Third, using similar independence arguments, by Chebyshev and Condition ASTESS, conclude

Fourth, using that by ASTESS so that by condition SE, we have that

by Chebyshev since because of the independence of the two subsamples and .

Step 3.(Behavior of .) Since , decompose

Then by Condition ASTESS, by reasoning similar to deriving the bound for , and by reasoning similar to deriving the bound for .

Step 4.(Auxiliary Bounds.) Note that

By condition ASTESS and by condition SM(ii) we have , and by Step 1 we have . Moreover,

We have by condition SE, and by condition SM(ii), the independence between the selected components and since they are based on different subsamples, and applying Chebyshev inequality.

Finally, collecting terms we have

Similarly, we have .

Step 5.(Variance Estimation.) Since , , so we can use as the denominator. Recall the definitions , and if belongs to subsample where . For notational convenience let . Since , , and , we have . Hence consider

by Step 3 and for some by condition SM(ii).

By Condition ASTESS(vi), for each subsample , we have by Vonbahr-Esseen’s inequality in \citeasnounvonbahr:esseen since is uniformly bounded for . Thus it suffices to show that . By the triangular inequality

since by Step 6. Then,

As a consequence of Condition SM(ii) we have , , , thus by Markov inequality we have .

We have the following relations:

since , by Step 4, , and by Step 1.

Similarly, .

Finally, since , we have

Step 6.(Controlling large terms) By definition of the event we have

Since , and , we have

Therefore,

Finally note that

since , , and by ASTESS. Also, by construction, we have .

∎

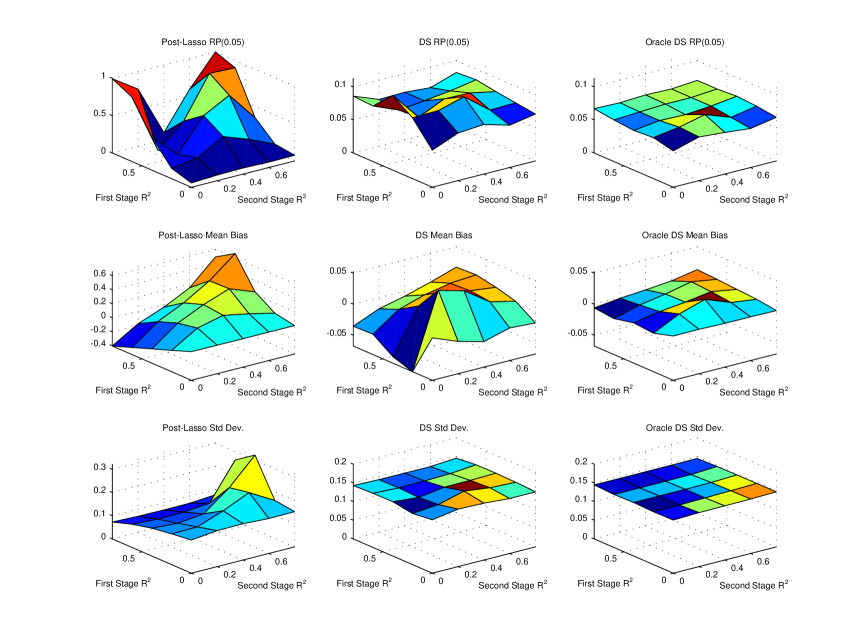

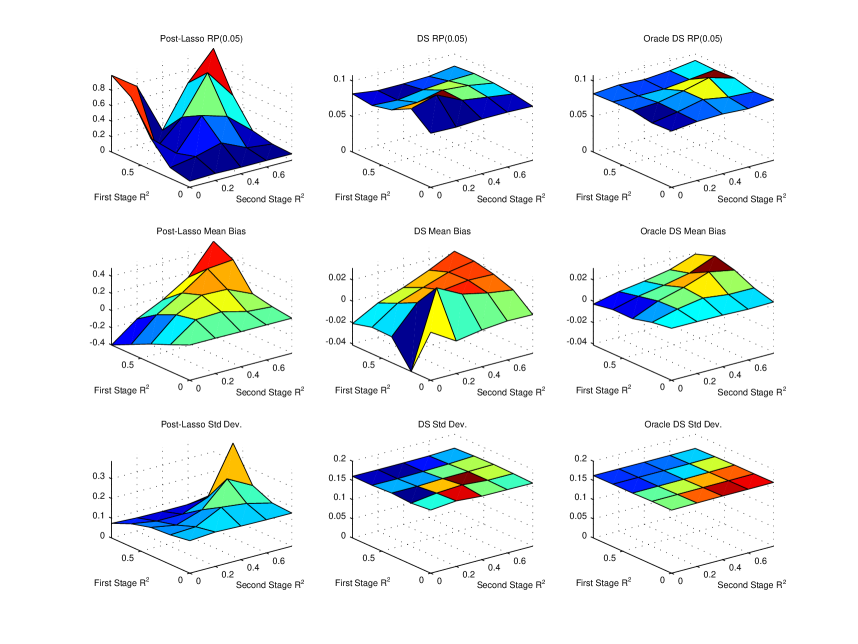

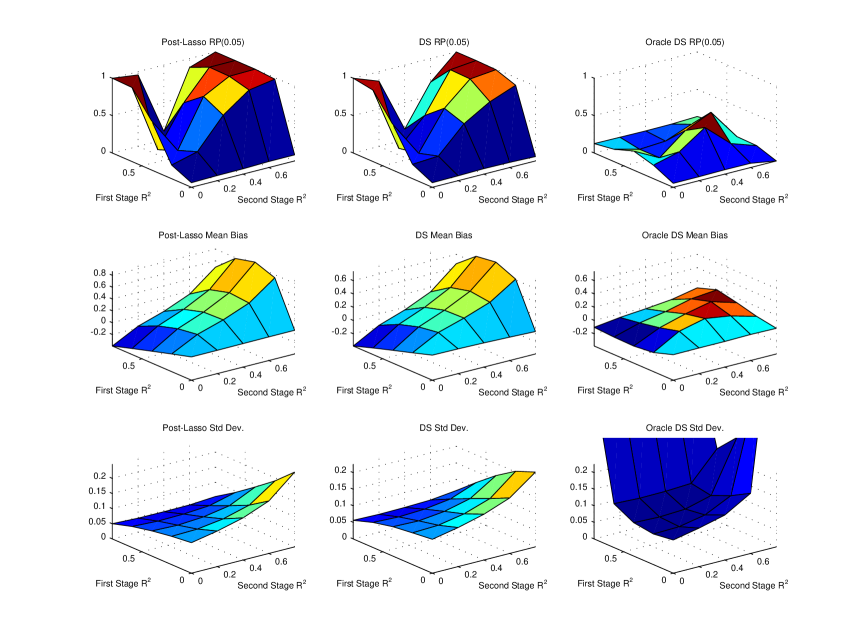

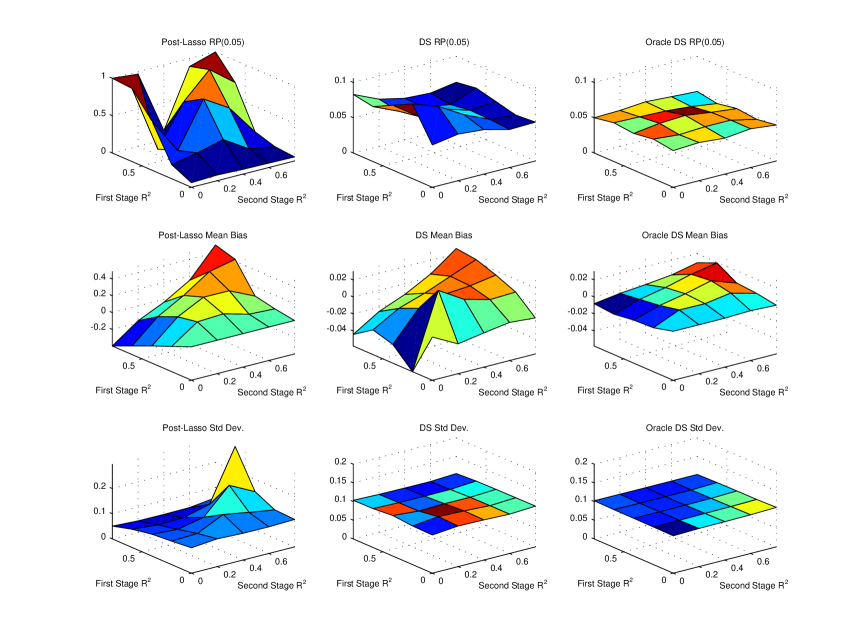

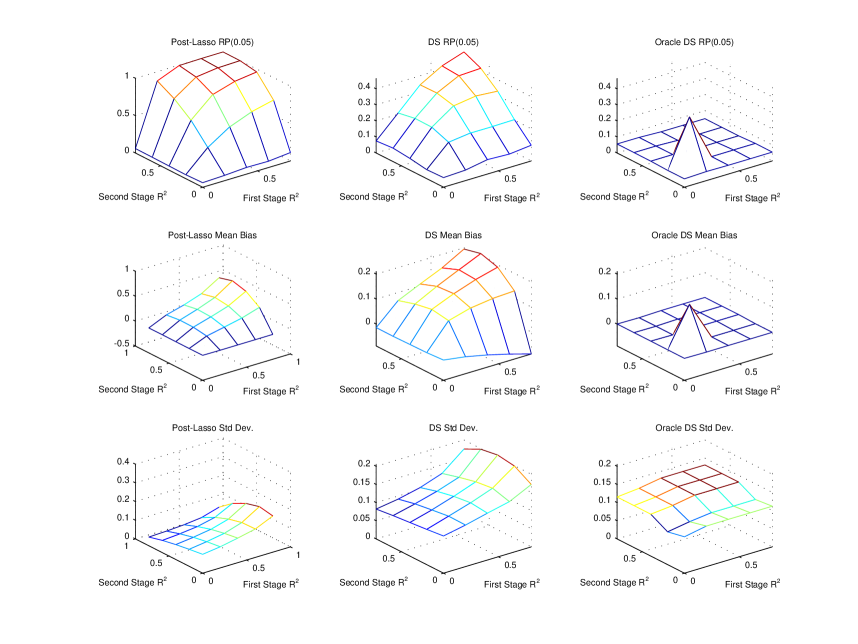

5. Additional Simulation Results

In this section, we present additional simulation results. All of the simulation results are based on the structural model

| (5.41) |

where , the covariates with , , and the sample size is set to . In each design, we generate

| (5.42) |

with E[. Inference results for all designs are based on conventional t-tests with standard errors calculated using the heteroscedasticity consistent jackknife variance estimator discussed in \citeasnounmackinnon:white. We set according to the algorithm outlined in Appendix A with . We draw new ’s, ’s and ’s at every replication and draw new ’s and ’s at every replication in the random coefficient designs.

In the first thirteen designs, . We set the constants and to generate desired population values for the reduced form ’s, i.e. the ’s for equations (5.41) and (5.42). Let be the desired for the regression of on and be the desired from the regression of on . For each equation, we choose and to generate and . In the heteroscedastic and binary designs discussed below, we choose and based on as if (5.41) held with and and were homoscedastic with variance equal to the average variance and label the results by as in the other cases. In the homoscedastic cases, we set ; and in the heteroscedastic cases, the average of and the average of are both one. We set

-

•

Design 1. , , .

-

•

Design 2. , , .

-

•

Design 22. , , .

-

•

Design 3. , , , .

-

•

Design 4. , , , .

-

•

Design 44. , , , .

-

•

Design 5. , , .

-

•

Design 6. , , .

-

•

Design 7. , , , .

-

•

Design 72. , , , .

-

•

Design 722. , , , .

-

•

Design 8. , , , , ,

-

•

Design 1001. , , .

In the last thirteen designs, we set the constants and according to

for and and and .

-

•

Design 1a. , , , .

-

•

Design 2a. , , , .

-

•

Design 22a. , , , .

-

•

Design 3a. , , , , .

-

•

Design 4a. , , , , .

-

•

Design 44a. , , , , .

-

•

Design 5a. , , , .

-

•

Design 6a. , , , E, .

-

•

Design 7a. , , , , , , , E, .

-

•

Design 72a. , , , , , , , E, .

-

•

Design 722a. , , , , , , , E, .

-

•

Design 8a. , , , , , , , ,

-

•

Design 1001a. , , , .

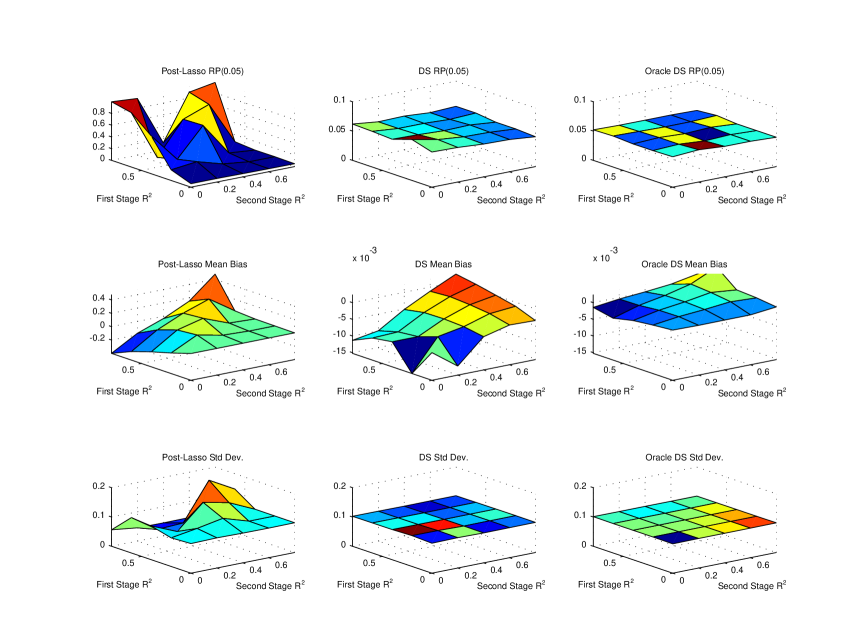

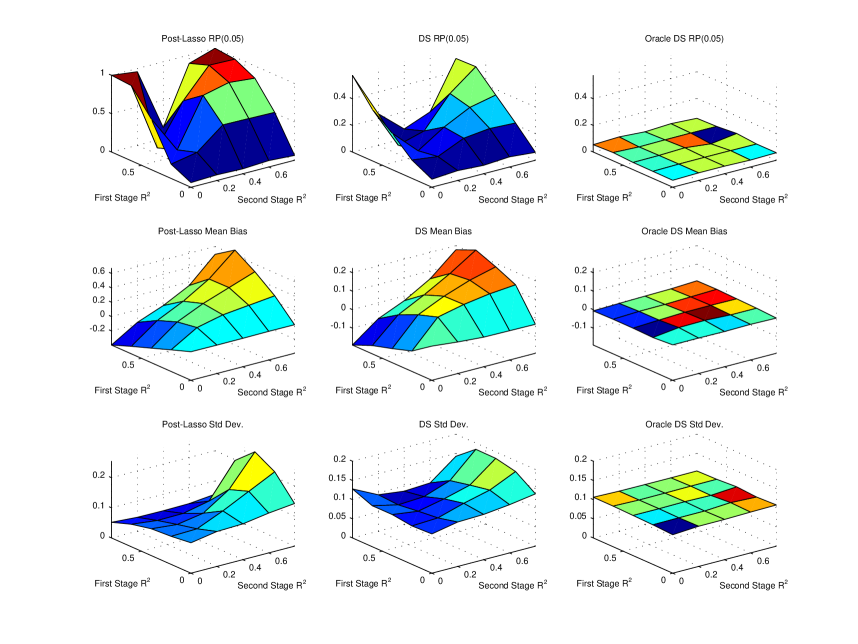

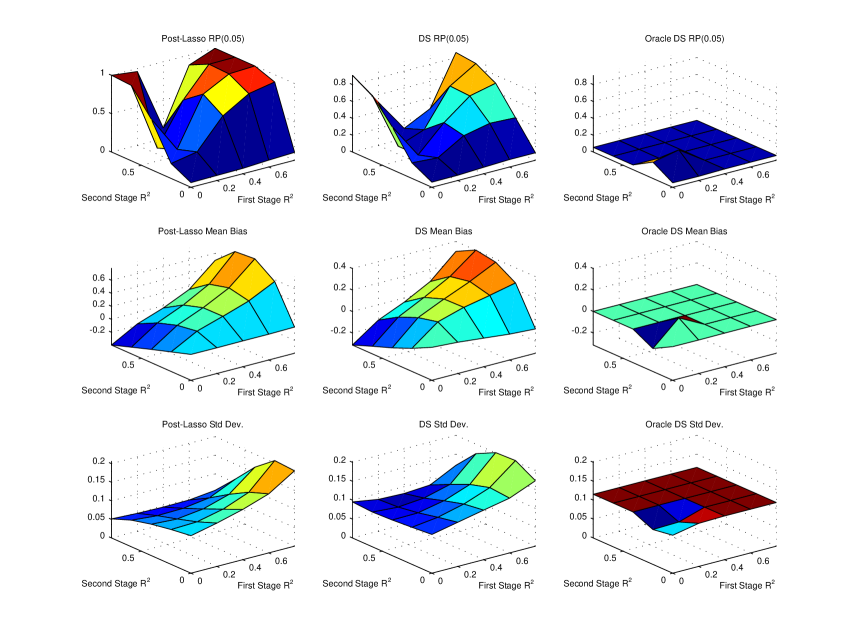

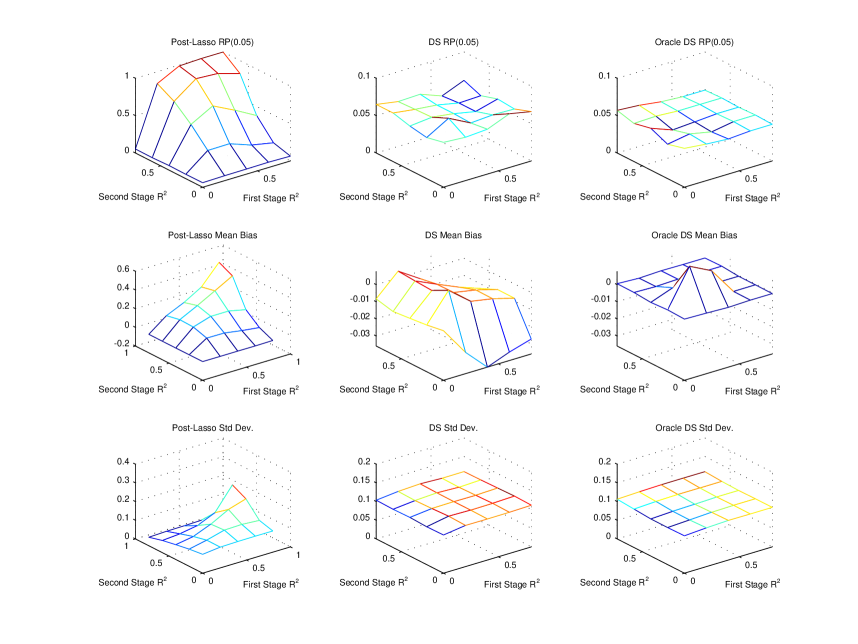

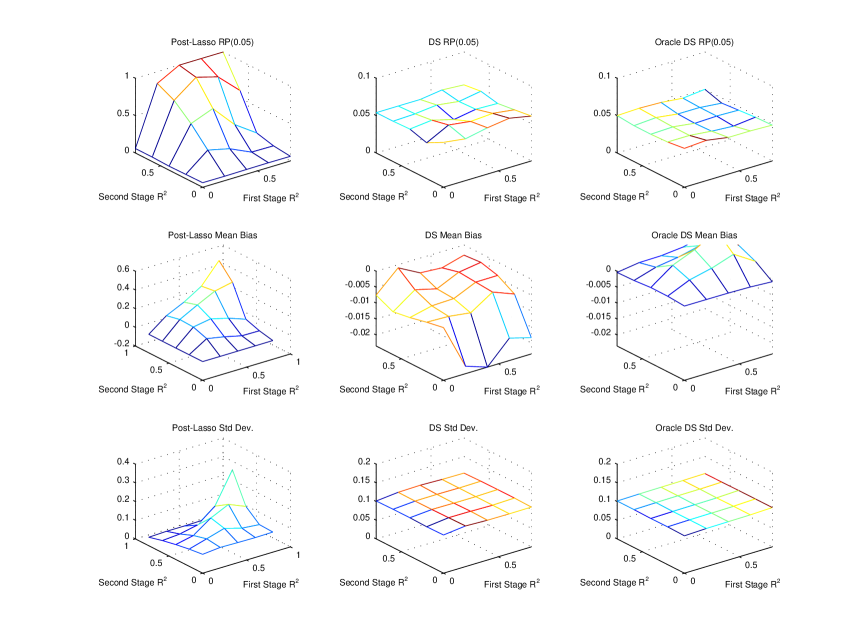

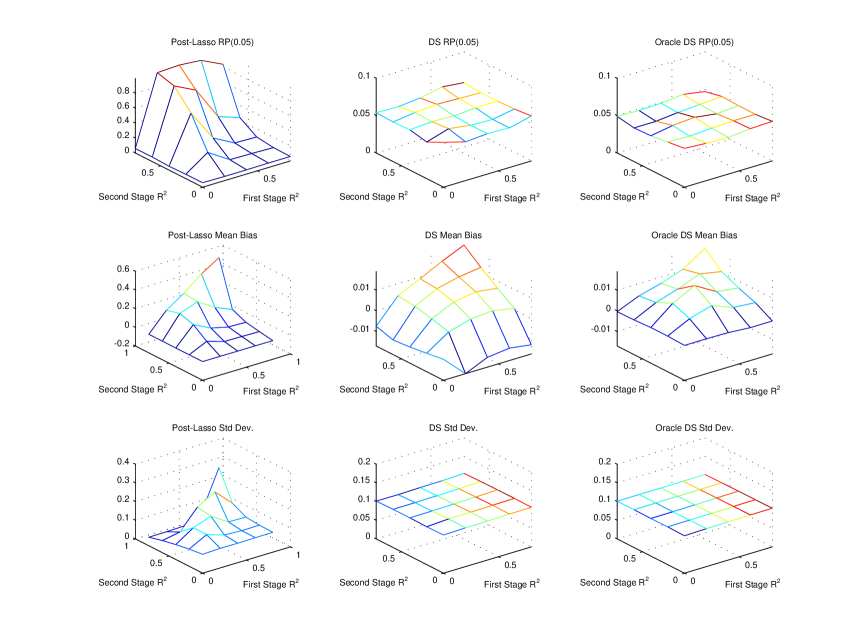

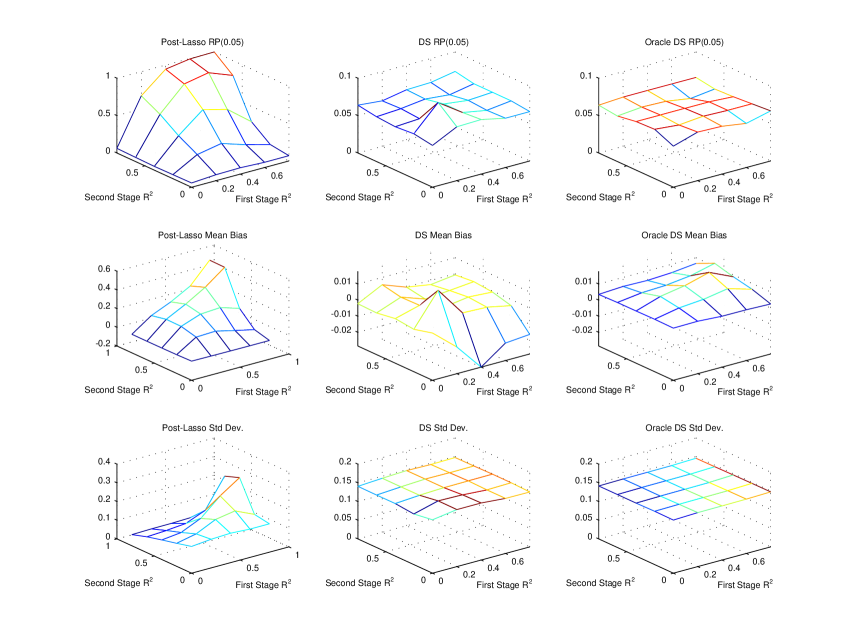

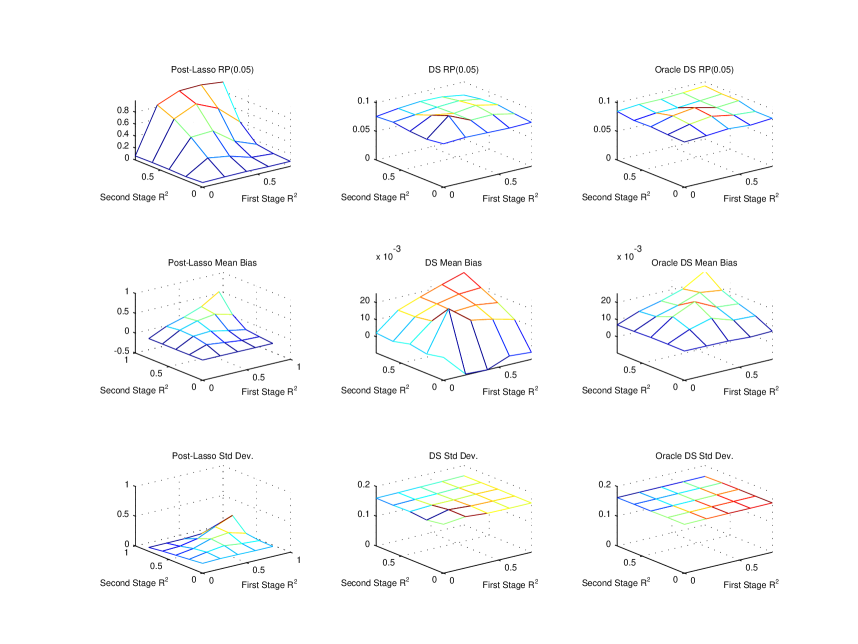

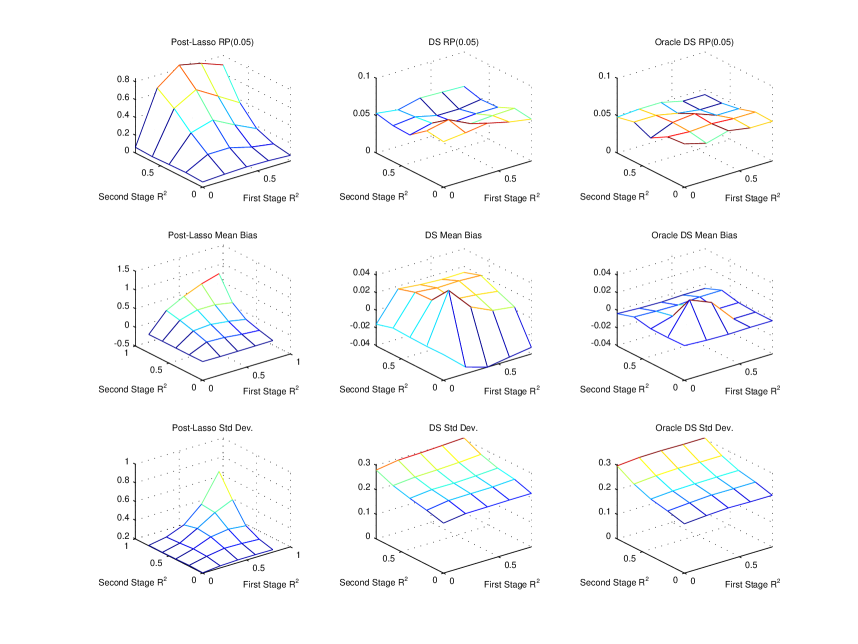

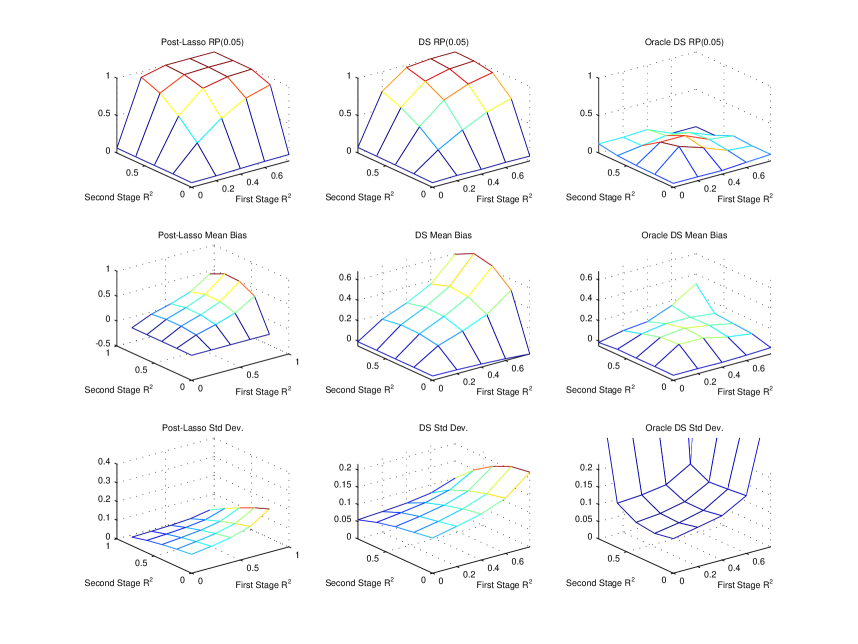

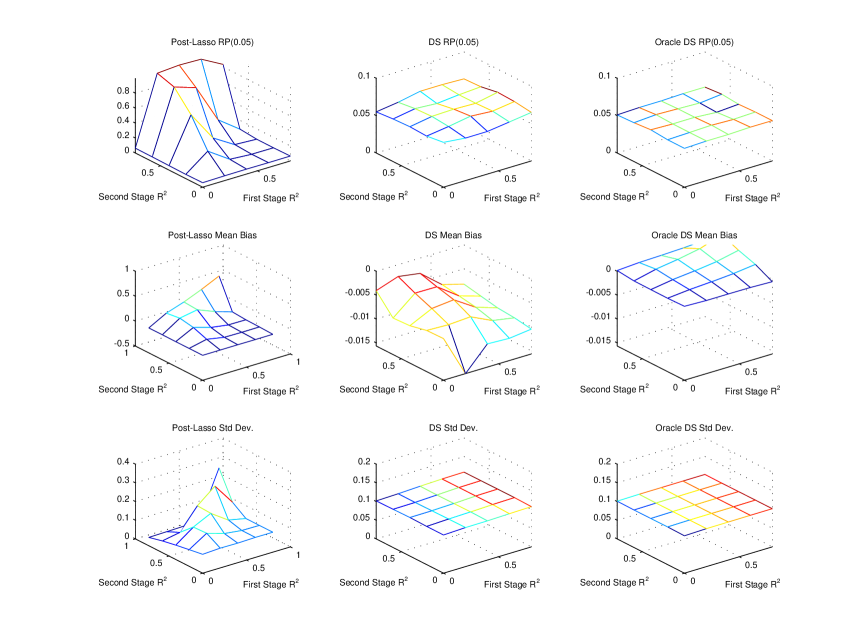

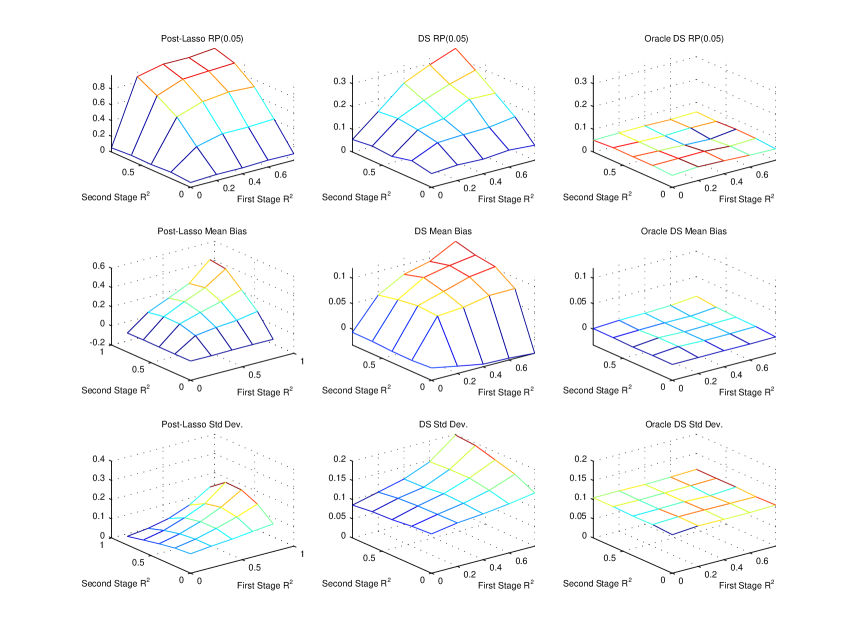

Results are summarized in figures and tables below. In the tables, we report results for the four estimators considered in the main text (Oracle, Double-Selection Oracle, Post-Lasso, and Double-Selection). We also report results for regular Lasso (Lasso), the union of the Double-Selection interval with the Post-Lasso interval (Double-Selection Union ADS), using the union of the set of variables selected by Double-Selection and the set of variables selected by running Lasso of on and without penalizing (Double-Selection + I3), and the split-sample procedure discussed in the text (Split-Sample). For Double-Selection Union ADS, the point estimate is taken as the midpoint of the union of the intervals.

![[Uncaptioned image]](/html/1305.6099/assets/x1.png)

![[Uncaptioned image]](/html/1305.6099/assets/x2.png)

![[Uncaptioned image]](/html/1305.6099/assets/x3.png)

![[Uncaptioned image]](/html/1305.6099/assets/x4.png)

![[Uncaptioned image]](/html/1305.6099/assets/x5.png)

![[Uncaptioned image]](/html/1305.6099/assets/x6.png)

References

- [1] \harvarditem[Bach]Bach2010Bach2010 Bach, F. (2010): “Self-concordant analysis for logistic regression,” Electronic Journal of Statistics, 4, 384–414.

- [2] \harvarditem[Belloni, Chen, Chernozhukov, and Hansen]Belloni, Chen, Chernozhukov, and Hansen2012BellChenChernHans:nonGauss Belloni, A., D. Chen, V. Chernozhukov, and C. Hansen (2012): “Sparse Models and Methods for Optimal Instruments with an Application to Eminent Domain,” Econometrica, 80, 2369–2429.

- [3] \harvarditem[Belloni and Chernozhukov]Belloni and Chernozhukov2011Belloni:Chern Belloni, A., and V. Chernozhukov (2011): “-penalized quantile regression in high-dimensional sparse models,” Ann. Statist., 39(1), 82–130.

- [4] \harvarditem[Belloni, Chernozhukov, and Kato]Belloni, Chernozhukov, and Kato2013BCK-LAD Belloni, A., V. Chernozhukov, and K. Kato (2013): “Uniform Post Selection Inference for LAD Regression Models,” arXiv preprint arXiv:1304.0282.

- [5] \harvarditem[Belloni, Chernozhukov, and Wei]Belloni, Chernozhukov, and Wei2013BCY-honest Belloni, A., V. Chernozhukov, and Y. Wei (2013): “Honest Confidence Regions for Logistic Regression with a Large Number of Controls,” arXiv preprint arXiv:1304.3969.

- [6] \harvarditem[Hahn]Hahn1998hahn-pp Hahn, J. (1998): “On the role of the propensity score in efficient semiparametric estimation of average treatment effects,” Econometrica, pp. 315–331.

- [7] \harvarditem[Leeb and Pötscher]Leeb and Pötscher2008leeb:potscher:review Leeb, H., and B. M. Pötscher (2008): “Recent developments in model selection and related areas,” Econometric Theory, 24(2), 319–322.

- [8] \harvarditem[MacKinnon and White]MacKinnon and White1985mackinnon:white MacKinnon, J. G., and H. White (1985): “Some heteroskedasticity consistent covariance matrix estimators with improved finite sample properties,” Journal of Econometrics, 29, 305–325.

- [9] \harvarditem[Neyman]Neyman1979Neyman1979 Neyman, J. (1979): “ tests and their use,” Sankhya, 41, 1–21.

- [10] \harvarditem[Rudelson and Vershynin]Rudelson and Vershynin2008RudelsonVershynin2008 Rudelson, M., and R. Vershynin (2008): “On sparse reconstruction from Fourier and Gaussian measurements,” Communications on Pure and Applied Mathematics, 61, 1025 1045.

- [11] \harvarditem[Rudelson and Zhou]Rudelson and Zhou2011RudelsonZhou2011 Rudelson, M., and S. Zhou (2011): “Reconstruction from anisotropic random measurements,” ArXiv:1106.1151.

- [12] \harvarditem[van de Geer]van de Geer2008vdGeer van de Geer, S. A. (2008): “High-dimensional generalized linear models and the lasso,” Annals of Statistics, 36(2), 614–645.

- [13] \harvarditem[von Bahr and Esseen]von Bahr and Esseen1965vonbahr:esseen von Bahr, B., and C.-G. Esseen (1965): “Inequalities for the th absolute moment of a sum of random variables, ,” Ann. Math. Statist, 36, 299–303.

- [14]