A General Framework for Updating Belief Distributions

Abstract

We propose a framework for general Bayesian inference. We argue that a valid update of a prior belief distribution to a posterior can be made for parameters which are connected to observations through a loss function rather than the traditional likelihood function, which is recovered under the special case of using self information loss.

Modern application areas make it is increasingly challenging for Bayesians to attempt to model the true data generating mechanism. Moreover, when the object of interest is low dimensional, such as a mean or median, it is cumbersome to have to achieve this via a complete model for the whole data distribution. More importantly, there are settings where the parameter of interest does not directly index a family of density functions and thus the Bayesian approach to learning about such parameters is currently regarded as problematic.

Our proposed framework uses loss-functions to connect information in the data to functionals of interest. The updating of beliefs then follows from a decision theoretic approach involving cumulative loss functions. Importantly, the procedure coincides with Bayesian updating when a true likelihood is known, yet provides coherent subjective inference in much more general settings. Connections to other inference frameworks are highlighted.

Keywords: Bayesian updating; PAC-Bayes, Decision theory; Generalized estimating equations; Gibbs posteriors; Information; Loss function; Maximum entropy; Self–information loss function.

1. Introduction. Data sets are increasing in size and modelling environments are becoming more complex. This presents opportunities for Bayesian statistics but also major challenges, perhaps the greatest of which is the requirement to define the true sampling distribution, or likelihood, for the data generator , regardless of the study objective. Even if the task is inference for a low-dimensional statistic of the population, Bayesian analysis is required to model the complete data distribution and, moreover, assume that the model is “true”.

In this paper we present a coherent procedure for general Bayesian inference which is based on the updating of a prior belief distribution to a posterior when the parameter of interest is connected to observations via a loss function. Briefly here, and in the simplest scenario, suppose interest is in the minimizing the expected loss

| (1) |

for some loss function , e.g. for estimating a median, where is the unknown distribution function from which i.i.d. observations arise. If represents prior beliefs about this , and is observed from , then we argue that a valid and coherent update of is to the posterior , where

| (2) |

The argument for this is given later in the paper, and to some extent relies on the idea that such an update must exist. For we have a well defined parameter of interest , an initial belief distribution about the location of the parameter, , and gain further information about via coming from . Updating beliefs is mandatory and it is obvious for some function we must have

That the form for is (2) is detailed later and a coherence property plays a key role:

| (3) |

This ensures we end up with as the same object whether we update with together or one after the other.

A special case is when it is known that for some parametric family of distributions , with corresponding density function , and . For minimizing here yields and the update (2) is the usual Bayesian update. It is important to note that our general update using loss functions should not to be seen as an approximation to anything; rather, it is targeting the parameter of interest, employing the necessary loss function with a valid update of beliefs.

Classical inference based on the likelihood function can be regarded as using the “negative log likelihood function” as a loss function; for example, in the case of independent and identically distributed observations, we can regard

as a loss function connecting data with a parameter indexing the family of density functions . And in this setting, one does not even need to assume the correctness of the model; one is merely expressing interest in the parameter minimizing

which is the parameter minimizing the Kullback-Leibler divergence between the unknown and the family .

1.1 The idea. Here we provide further elaboration on the outline of the idea given previously. Let denote a parameter or functional of interest, for example the mean or median of a population , and let denote an observation from , with unknown. We are interested in a formal way to update prior beliefs to posterior beliefs given .

Bayesian inference proceeds through knowledge of a complete, true, model for . This is often parameterised via a sampling distribution and a prior , and define the marginal likelihood

Then, see for example Bernardo and Smith (1994), inference for occurs via Bayes theorem

However, the statement “inference for ” is meaningless unless the true parametric family is known. In this case, following the Savage axioms (Savage, 1954), the Bayesian update can be shown to be the rational way to proceed. However, may be unknown, and even if is correct, might be ultra high dimensional mainly made up of nuisance parameters relative to a low dimensional subset of the parameters of interest. Taken all together, these points can make the Bayesian approach cumbersome.

We are interested in the rational updating of beliefs under more general and less stringent conditions. To do so we make use of loss functions to connect information in data to parameters of interest. Informally for now, we write such loss functions as , and we will discuss specific types later in the paper. We shall consider the reporting of subjective beliefs, , as an action made under uncertainty and use decision theory to guide the optimal action. See, for example, Hirshleifer and Riley (1992).

To outline the theory, let denote a probability measure on the space of . We shall construct a loss function to select an optimal posterior distribution 222We use to denote optimality rather than an approximation or estimate given a prior and data . To achieve this we construct a loss-function on the space of probability measures on space, and then present

as the representation of beliefs about the unknown value of given the prior information, represented via the belief distribution , and data . As it is widely assumed data is an independent piece of information to that which gave rise to the prior, it is appropriate to consider an additive, or cumulative, loss function of the form

| (4) |

where and are themselves loss functions on probability measures, representing fidelity-to-data and fidelity-to-prior, respectively. See, for example, Berger (1993) for more about ideas on uses of loss functions within decision theory.

The question is whether we can claim a probability measure selected as the solution to a decision problem; i.e. minimizing a loss function, can be viewed as representing beliefs about a parameter. To answer this, given the aim (1), we would clearly prefer probability measure to as representing beliefs if

| (5) |

Indeed, it would be incoherent to select rather than when (5) holds. Thus the answer is affirmative. Though we are not minimizing or comparing (5), since we do not have , we can substitute the expression

| (6) |

with the Bayesian finite sample expression of the form (4). We now discuss the choices of and which give (4) as a Bayesian finite sample version of (6).

Under this approach the analyst needs to specify and in such a way that they proceed in an optimal, rational, and coherent manner. Somewhat remarkably, as proved in the Supplementary Material, for coherent inference (3), must be the Kullback–Leibler divergence, Kullback and Leibler (1951), and given by

Regarding , since is a probability measure representing beliefs about , the only choice here is to take the loss-to-data on the probability measure as the expected loss (see von Neumann and Morgenstern, 1944) of ; that is

with the particular types of the loss-function on the parameter on interest to be discussed later.

Substituting in and , the cumulative loss function is then given by

| (7) |

This then; i.e. (7), is our finite sample version of (6), and note that (7) becomes (6) as . The solution to (7) provides the which the statistician believes best minimizes (6). This is, according to our approach, done by using the empirical distribution function as a substitute for and using a penalty term which prevents the answer from being too far from the prior in a Kullback-Leibler sense; the Kullback-Leibler appearing here for the necessary coherence property of the answer. Of interest, as discussed later on, is the PAC Bayes solution to the problem (Langford, 2005) that finds an approximation which minimizes an upper bound for (6).

Surprisingly, but quite easy to show, the minimizer of is given by

| (8) | |||||

This can be seen by observing that

So (8) has the form of a Bayesian update. As is usual in decision problems involving the use of loss functions, it is incumbent on the decision maker to ensure solutions exist. So needs to be constructed such that

Whereas the Bayesian approach requires the construction of a probability model for all possible outcomes conditional on all unknown states of nature, the approach here requires the construction of loss functions given the outcomes for only the parameter of interest. This allows the decision maker to concentrate on modeling only those quantities that are important to the task at hand.

1.2 Connections with related work. There is a large literature on procedures for robustly estimating a parameter of interest by minimizing the cumulative loss

| (9) |

This is clearly the finite sample version of

Our claim is that (7) is the Bayesian version of (9), where interest is on probability measues on space rather than single states .

Hüber (2009) provides examples of (9), where we note that the primary aim is not modeling the data but rather estimating a statistic. This is an advantage when a probability model for the data is too hard to formulate. We are presenting a Bayesian extension of this idea. Since we are interested in a belief distribution for given data, and have further information provided by , we claim the appropriate Bayesian version is given by (8).

Some of the ideas presented in the paper have been considered in a less general setting by Zhang (2006a, 2006b) and Jiang and Tanner (2008). In Zhang (2006a) an estimation procedure, named Information Risk Minimization, also known as a Gibbs posterior, which has the same form as (8), is described in Section IV of his paper. This is our procedure when data is regarded as stochastic. Zhang then concentrates on the properties of the Gibbs posterior.

Further theoretical work is done in Zhang (2006b). In Jiang and Tanner (2008) a Gibbs posterior is studied in comparison with a true Bayesian posterior where the model is assumed to be misspecified. The claim is that posterior performance of a Bayesian model can be unreliable when misspecified, whereas a Gibbs posterior which targets points of interest can have better performance. The comparison involves variable selection for high-dimensional classification problems involving a logit model.

We build on the work of Zhang (2006a, 2006b) and Jiang and Tanner (2008) in a number of important directions. The first is that we show that the Gibbs posterior is the only coherent, decision theoretic approach for inference and statistical applications under misspecification. We provide a principled approach to scale the relative information in the data to information in the prior (see Section 3); that is left as an arbitrary free parameter in Zhang (2006a, 2006b) and Jiang and Tanner (2008).

Bissiri and Walker (2010) use (7) with Bernoulli observations and find sufficient conditions on for the sequence of posteriors, based on (8), to be consistent. This result for consistency is extended to more general i.i.d. observations in Bissiri and Walker (2012a). In Bissiri and Walker (2012b) it is shown that starting from the class of -divergences, for a coherent sequence of updates, which will be explained later in the paper, we need the Kullback-Leibler divergence as the loss between prior and . In this paper, the Theorem presented in the Appendix, we provide a simpler and more intuitive proof to this result by assuming a straightforward and realisitic assumption about the class of -divergences.

A similar construct to is provided by Zellner (1988), who presents what is essentially a loss function for the posterior distribution using ideas of information processing from prior to posterior. The motivation is different and relies on notions of information present in log probabilities and log likelihoods, which may not be compatible as noted by J.M. Bernardo in the discussion of Zellner’s paper. Furthermore, our derivation of the loss function allows a broader interpretation of the elements, which does not require the existence of a probability distribution for the observation.

Concerns that the specification of a complete model for the data generating distribution is unachievable date back to de Finetti (1937) and the notion of “prevision”. In his work de Finetti considers conditional expectation as the fundamental primitive, or statistic, of interest on which prior beliefs are expressed and updated. Recently other researchers have further developed this approach under the field of Bayesian linear statistics, see Goldstein and Wooff (2007).

There has been increasing awareness of the restrictive assumptions that formal Bayesian analysis entails. Royall and Tsou (2003) describe procedures for adjusting likelihood functions when the model is misspecified. More recently, Doucet and Shepherd (2012), and Muller (2012) consider formal approaches to pseudo-Bayesian methods using sandwich estimators to update subjective beliefs, motivated by robustness to model misspecification, see also Hoff and Wakefield (2013). Ribatet et al. (2009) consider pseudo-Bayesian approaches with composite likelihoods. More generally there is increasing recognition that formal Bayesian analysis can be restrictive for example through computational issues, such as arise in the area of Approximate Bayesian Computation (see for example Marin et al (2012)).

Several authors have considered issues with Bayesian updating by using proxy models, , for example, see Key et al. (1999), when is known not to arise from for any value of . That is, there is no conditional on which is from . This is referred to as the M–open case in Bernardo and Smith (1994). One suggested solution is to use methods based on approximations and Key et al. (1999) describe one such idea using a cross–validation approach. While this may be a pragmatic it does have some shortcomings. Most serious is that there is little back–up theory and this has repercussions in that the update suffers from a lack of coherence

Another approach is to ignore the problem. That is, assume the observations are coming from even though it is known they are not. According to Goldstein (1981), “there is no obvious meaning for Bayesian analysis in this case”. The disaster of making horribly wrong inference can be protected to some extent by model selection; that is, postulating a number of models for , say , with corresponding priors , and model probabilities , for . But as Key et al. (1999) point out, how does one construct and when one knows none of the postulated models are correct. So the Bayesian update breaks down in that nothing has any interpretation.

Finally, and we acknowledge the contribution of the reviewers for pointing this out, we discuss connections with PAC Bayes; see, for example, Shawe-Taylor and Williamson (1997), Langford (2005), Alquier (2008), McAllester (1998), and also the approach in Cesa-Bianchi and Lugosi (2006). PAC Bayes is an interesting emerging field in machine learning concerned with techniques for bounding the generalisation error (empirical risk) of a Bayesian model. The motivation behind PAC Bayes is to find an upper bound for the empirical risk of a probability measure on a model in (6), termed generalisation error in the PAC Bayes literature. Given observation and prior , the upper bound will be written as ; i.e., for all it is that

See Catoni (2003) where the form of is provided. Then it can be shown that an upper bound is provided by (8). The PAC Bayes approach is complementary to our work. The motivation and construction is very different. We are interested in a framework for the rational updating of beliefs, rather than seeking bounds on the empirical risk of a probability measure on models. The minimizer of an upper bound is interesting but does not justify using as an update of a belief distribution for Bayesian style inference, and hence whether form a coherent sequence of belief distributions is not discussed in the PAC Bayes formulation of . Whereas the requirement of coherence is central to our formulation. Moreover the scaling of the loss-to-data to the loss-to-prior enters as a constant in the margin of the error bound in PAC Bayes whereas here it has explicit meaning in the relative weight of information provided by the two sources, prior and data (see Section 3).

This said, there are clear synergies and the operational characteristics of PAC Bayes are similar, they must be since we gather the same answer. However, the motivation is different and we sincerely believe our derivation is providing full support for the use of the posterior. Moreover, as we will see later, this derivation provides insights into the necessary calibration of loss functions and .

1.3 Layout of paper. The layout of the remainder of the paper is as follows. In Section 2 we discuss types of loss function. When the self-information loss function is used then the update is the traditional Bayes update. With other loss functions there is a calibration issue between the two styles of loss function used, i.e. the loss to the data and the loss to the prior. This calibration problem is discussed and resolved in a number of ways in Section 3. In Section 4 we discuss forms of information other than the usual data arising from some unknown distribution function. This includes non-stochastic information and also partial information. Section 5 provides some numerical illustrations including inference based on partial information and a clustering problem. Section 6 concludes with a discussion on a number of points.

2. Types of loss function. In this section we will consider the form of in (4) that connects information in the data to the value of the unknown . We shall consider three broad situations. First, when the analyst believes they know the complete family of distributions from which the arose, the so called M–closed scenario. Second, when is unknown but where a complete likelihood is being used as a proxy model. Finally, when there is no sampling distribution or proxy model for and the parameter of interest is connected to via a loss function .

2.1 M–closed and self-information loss. When the analyst knows the family from which arose, the so-called M–closed view, then the Bayesian approach to learning is fully justified, well known and widely used as a statistical approach to inference; the book of Bernardo and Smith (1994) is comprehensive. To see how Bayes arises in our framework, we would need to construct a loss function for with the knowledge that came from . It is well known that the appropriate and sole loss function in this case is the self–information, or logarithmic loss function, given by

Indeed, the cumulative loss version of this is the log-likelihood function.

See Bernardo (1979) and Merhav and Feder (1998) for more on the self information loss function. This amounts to the use of proper scoring rules to ensure that the analyst remains honest in expressing subjective beliefs when the parametric family is known, under which our approach coincides with the Bayesian updating rule.

2.2 M–open and the use of proxy models. Issues with the Bayesian rule arise when the form of is not known, for example, see Key et al. (1999). Equivalently, there is no conditional on which is from ; more bluntly, there is no connection between any and any via . This is referred to as the M–open case in Bernardo and Smith (1994). In many situations, the correct sampling density, , is unknown or unavailable or too complex to work with.

One way to proceed is by considering , the value of that minimizes the the Kullback–Leibler divergence between a proxy model and the true density function ; i.e. minimizes

Then prior beliefs, , will be expressed on this unknown value. We show in Appendix B that it is then possible to learn about this since an infinite collection of yields . Then we would wish the sequence of to accumulate about . The appropriate loss function in this case is still . For the standardized cumulative loss based on a sequence of observations is given by

which is minimized by .

So while the Bayesian approach has foundational issues to deal with whether the M–open or M–closed view hold, for the approach here it is irrelevant. If one adopts as the parameter value taking the family closest to then one does not need to worry if one is M–open or M–closed, since if is the true family then obviously reverts to the true parameter value. This point is crucial, since for the Bayesian being in M–open or M–closed forces one to adopt different inference approaches, see Bernardo and Smith (1994).

Moreover our approach supports the use of the relevant partial information in the data for updating beliefs on the parameter of interest, such as in the proportional hazards model. This can be especially important when the data is high dimensional. Such updates have no formal justification from a Bayesian perspective.

2.3 Paremeter minimizing a loss function. In the most general scenario the parameter of interest minimizes a loss function of the type (1). In the classical literature, this type of estimation problem is in the area of Robust Statistics and specific loss functions can be found in the literature, pertaining to -estimation and estimating equations. See, for example, Hüber (2009).

An important class of loss functions is provided by the estimators for a location parameter, Hüber (1964). So rather than using the loss function , a is used in an attempt to obtain robust estimation, rather than the traditional maximum likelihood estimator, which can be suspect if the model is incorrect. This idea has been generalized to the class of estimating equations, whereby the estimate of is obtained by minimizing

Our approach, which mirrors this classical robust procedure, would use the loss function

with solution provided by

The of interest is implicitly assumed to be the limit of the sequence of minimizers of the cumulative losses. This would be the minimizer of and hence the prior beliefs are being expressed about this unknown value. Then the loss function is ensuring the updates are indeed “moving towards” . To complete the picture, it would have been that the decision maker would be happy to make a decision given the minimizer of .

3. Calibration of relative losses. This section deals with the important aspect of specifying the relative information in the data to the information in the prior in general settings. In the M–closed and M–open settings the use of the self-information loss results in a fully specified form for (8). However, in the setting of Section 2.3 there is an issue about the scale of the loss function which is a consequence of the apparent arbitrariness in the weight of relative to , in that we are free to multiply either by an arbitrary factor. So, equivalently, we are interested in the loss function for some . The question is how to select , noting that controls the relative weight of loss-to-data to loss-to-prior. Of course, such an issue does not arise in the classical literature on estimation using such loss functions since there is no combining with different styles of loss functions. However, the calibration of different types of loss function is not a unique problem. It arises in many applied contexts; possibly the most well known be in health economics where losses pertaining to costs need to be balanced against losses pertaining to health benefits.

The most common ideas for assigning in Gibbs posteriors and PAC Bayes typically involve cross validation and subjective choices. As mentioned above, in PAC Bayes the weighting is a constant that enters into the margin of the error bound. Here we discuss some more ideas intended to help the analyst. We do not claim to be exhaustive in the approaches, or to be prescriptive in advocating one approach over an other. Our intention is to provide tools for elicitation of the relative loss-to-data to loss-to-prior.

3.1 Annealing. In the literature on Gibbs posteriors, the weighting parameter is labelled as a “temperature” and selected subjectively. There are clear connections here with the use of “power priors” (Ibrahim & Chen, 2000) where

Such an idea has also been discussed in Walker and Hjort (2001). It is evident what achieves; if then the loss-to-prior is given more prominence than in the Bayesian update and the data will be less influential. In the extreme case when we retain the prior throughout. On the other hand, when the loss is given more prominence than in the Bayesian update and in the extreme case when is very large the is accumulating about the maximum likelihood estimator for the model; that is

where maximizes .

3.2 Unit information loss. Here we discuss a procedure for default subjective assignment based on a prior evaluation of the expected value of . The idea originates from work in the specification of reference priors and “objective Bayes”, see for example Kass and Wasserman (1996).

To aid in the calibration of the loss functions and the selection of we can consider the following. To begin we need to ensure that both losses are non-negative for all . Hence we write the loss function with an additional term , which is a constant, and where maximizes , so that the cumulative loss becomes

and we would additionally standardise such that for any . If this is not the case then we replace by where now minimizes . Hence, we can regard

as a loss function for with information provided by and . So, assuming that , we want to calibrate the two loss functions given by

These are two loss functions for and to adhere with the notion that before we have any data, there is a single piece of information, we can calibrate the two losses by making the expected losses, taken over and , to match. That is, whether someone takes a and is penalized by the loss

or takes a and is penalized by the loss , at the outset, the expected losses should match. They are confronted by two choices of loss with one piece of information and thus the losses can be calibrated by ensuring their expected losses coincide. The connection between expected information and expected loss can be found in Bernardo (1979).

Thus can be set by ensuring

Here is with respect to a joint belief in and ; say , the marginal for of which is . So

This requires specifying a sampling distribution for , which we’ve said is problematic, so an empirical choice is then given by

where denotes the empirical distribution function.

Let us consider an example, where with with being any density with mean and variance . Then we can evaluate

and

so Hence, this calibration idea yields the “correct” value of in this case. This construction requires the user specification of a joint density which in some circumstances may prove difficult. One further suggestion is to replace the prior evaluation of the expected datum-loss with the observed unit information loss given ,

| (10) |

where

is the data-loss estimate of and is the dimension of . For instance, in the above example this leads to, where

It is interesting to note in the above that if it is thought the appropriate choice for is flat, possible if the space is bounded, then clearly . Thus, to be coherent, we would equally believe does not depend on , where is a belief distribution for given . This is a condition which would be hard to justify, as it would then be also for the uniform prior for . If one is used, then we only recommend the value of is not assigned in the above way.

3.3 Hierarchical loss. Another way to proceed is to extend the loss function to include as an unknown parameter. Standard ideas here would suggest we take

for some . We would appear to be making no progress since we now have a to assign. However, this is akin to the hierarchical Bayesian model where uncertainty is propagated via hyper-prior distributions to robustify the ultimate prior choice at some level. Hence, the allocation of a would not be as crucial as the assignment of a .

For example, as is a scale parameter on loss-to-data, taking the solution is given by

and given that can be absorbed in to the prior it is reasonable to assess subjectively. That is, it seems unreasonable to accept that can be chosen subjectively but that can not.

3.4 Operational characteristics and subjective calibration The idea here is to set so that the posterior quantiles are calibrated at some level of error to frequentist confidence intervals based on the estimation of via minimizing the loss

So, if is the % level confidence interval for , then we could select the such that the posterior distribution of , with parameter , is such that

See, for example, the review article by Datta and Sweeting (2005) for references to probability matching priors and posteriors, and Ribatet et al. (2009) for ideas in pseudo-Bayesian approaches with composite likelihoods.

More generally we can consider the subjective setting of where knowledge of the frequentist sampling statistic of can assist. To begin note that is explicitly related to the Bayes Factor quantifying the posterior to prior odds,

where measures the update in beliefs in favour of from on observing . Clearly the larger the difference the greater the relative evidence in favour of , with determining the scale for unit change. It is interesting to note that should the Bayes Factor be known for any three points in the joint parameter sample space, , then would be fixed. The idea here is that the analyst is free to contemplate any specific values for which the distribution of the statistic may be known, and use this knowledge in turn to help elicit a Bayes Factor therefore setting . A concrete example will help:

Suppose denotes the unknown mean of a population with prior and loss . Consider the design points so that the statistic, , is then

the difference in the sum of squares to the sum of squares around the mean, and log Bayes factor

The analyst is free to contemplate any value of and any to help in the elicitation. Let be chosen large and contemplate such that the confidence interval for the unknown mean touches . In this case, for large , we know , where denotes the F distribution. If the analyst is prepared to say how their prior beliefs would be updated on observing in knowledge of this symmetric CI for then the can be set via

We give a concrete illustration of this approach in Section 5.

3.5 Conjugate loss prior. If prior beliefs about can be expressed in the form

for given parameters , then the posterior has a conjugate type property; that is

Thus the prior has interpretation of prior observation with precision . Thus and would be standard objects for a Bayesian to specify. If the prior can then be established as the equivalent of observations, then we obtain via .

If the prior is thought not to be able to be specified in such a way, then a good approximation to any prior can be found with choices of such that

If we now write

where , then we see that now .

Thus there is an apparent new concept here in that the experimenter is required to think about how much information, in the form of the number of prior observations, there is available. However, not completely new, since in some conjugate problems there are parameters which do have the interpretation of a prior sample size; the exponential family, for example.

4. General forms of information. In this section we discuss more general forms of information rather than assume it arises from some unknown . The argument is that provided has been specified then an update of a belief distribution about is available. Clearly this does not rely on any assumption about where came from or indeed how it became known.

In particular, we provide a definition of conditional probability when non–stochastic information is available. This allows for posteriors to be applied in much more general settings than Bayesian models, which require a stochastic .

4.1 Conditional probability distributions and non-stochastic data. The theory of conditional probability distributions is a well-established mathematical theory which provides a procedure to update probabilities taking into account new information. Such a procedure is available only if the information which is used to update the probability concerns stochastic events; that is, events to which a probability is pre-assigned. In other words, such information needs to be already included into the probability model. In this section, we shall show how the updating approach can be used to define conditional probability distributions based on non–stochastic information.

Information about may arrive in the form of non–stochastic data; such as if an expert declares

| (11) |

This type of information has been discussed by a number of authors and is known to be problematic for the Bayesian especially when such information arises after or during the arrival of stochastic observations . We cite the paper by Diaconis and Zabell (1982) and in particular refer the reader to example in Section 1.1 of their paper.

We denote by a piece of information for which no probability model for each is assigned, in other words it is not and can not be determined to be stochastic in any way. To undestand expressions such as this it is worthwhile to recall the type of information we envisage of the type (11).

While a probability model can not connect (11) and , they can be connected via a loss function without much difficulty. For example, for some could be deemed appropriate. Note here we use to denote information now, replacing the stochastic . The update based on and can then be considered as a means of defining an operational conditional probability distribution in the presence of non-stochastic information, given by

So, the general Bayesian approach introduced in Section 2 provides a general definition of conditional distributions based on non-stochastic information.

For literature on paradoxes related to forcing non-stochastic events into a probability model with a determination of all the alternatives to we refer the reader to Freund (1965), Gardener (1959), Bar-Hillel and Falk (1982), and Hutchison (1999, 2008).

4.2 Partial information.

As noted in Section 2, while the parameter of interest is , the information collected may be more informative. That is, there is within information which does not assist with the learning about , for which it is possible to identify which provides all the information about . One is therefore interested in constructing the loss function , leading to

| (12) |

The partial likelihood, or partial self-information loss, used in proportional hazards model is one such example. While Bayesian practitioners may have adopted such a procedure in the past it would be regarded as lacking motivation. On the other hand, our point is that (12) represents a valid update of beliefs. We illustrate this approach in Section 5.

5. Illustrations. In this section we discuss the application of our approach to important inferential problems. The first problem is one from survival analysis where we have a well motivated proxy likelihood based on partial information. The second example is from model-free clustering where we have a general loss function so that calibration of is important. A third example, to be found in the Supplementary Material, is for joint inference on a set of quantiles. In all cases we claim that the choice of loss function is well founded (and unique) and that there is no traditional Bayesian interpretation of the updates we are implementing. Yet the updates we employ do allow us to learn about the specified parameters of interest. All of the models used to generate results are available as open source code in R or Matlab.

5.1 Colon cancer genetic survival analysis. Colon cancer is a major worldwide disease with increasing prevalence particularly within western societies. Exploring the genetic contribution to variation in survival times following incidence of the cancer may shed light into the disease eitiology and underlying disease heterogeneity. To this aim collaborators at the Wellcome Trust Centre for Human Genetics, University of Oxford, obtained survival times on 918 cancer patients with germline genotype data at 100,000’s of markers genome-wide. For demonstration purposes we only consider one chromosomal previously identified as holding a potential association signal containing 15,608 genotype measurements. The data table then has rows and columns, where denotes the genotype of the ’th individual at the ’th marker. Alongside this we have the corresponding response table of survival times with a column of event-times, and a column of indicator variables , denoting whether the event is observed or right-censored at .

To explore association between genetic variation and time-to-event we employ a loss function derived under proportional hazards, treating the loss to the baseline hazard as a nuisance parameter. This is based on the Cox proportional hazard (PH) model, one of the most widely used methods in survival analysis since its introduction in Cox (1972). In this log-linear model the hazard rate at time for an individual with covariate is defined as,

where is a baseline hazard function. In the seminal work of Cox (1972), is treated as a nuisance parameter (or process) that does not enter into the partial-likelihood for estimating the parameters of interest .

On the other hand, a Bayesian approach to the Cox model necessarily involves the baseline hazard function. There is a limiting argument for the use of the partial likelihood but this is rarely, if at all, used. Most common is the finite partitioning of the time axis and using a piecewise constant baseline hazard function. Though typically regarded as a nuisance parameter, the Bayesian must specify a full probability model for it. See Ibrahim et al. (2001), Chapter 3, for details, where they note that the proportional hazards model is obtained under a limiting improper prior on the baseline, but it is not known what affect this has on marginal quantities of interest such as marginal model choice probabilities.

Using our construction we can consider only the order of events as partial-information relevant to the regression coefficients, , via the cumulative loss function,

| (13) |

where denotes the risk set, those individuals not censored or at time , and in this way obtain a conditional distribution . We assume, and set for our study, reflecting beliefs that associated coefficients will be modest; although we note that one advantage of our approach is that subjective prior information can be integrated into the analysis.

For evidence of effects; i.e. , we can calculate the general Bayes Factor of association at the th marker as,

which involves a one-dimensional integral that we calculate via importance sampling.

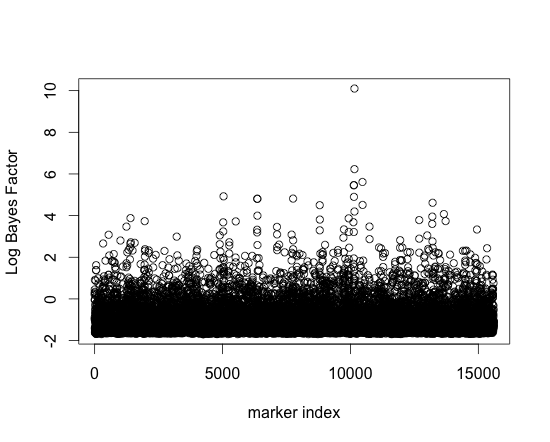

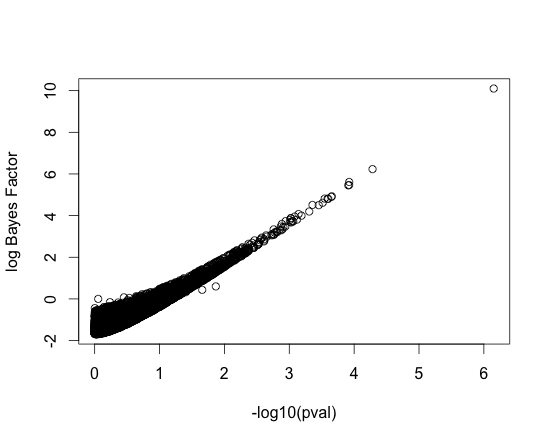

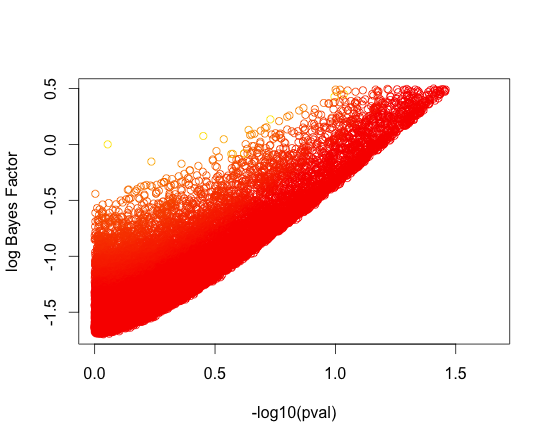

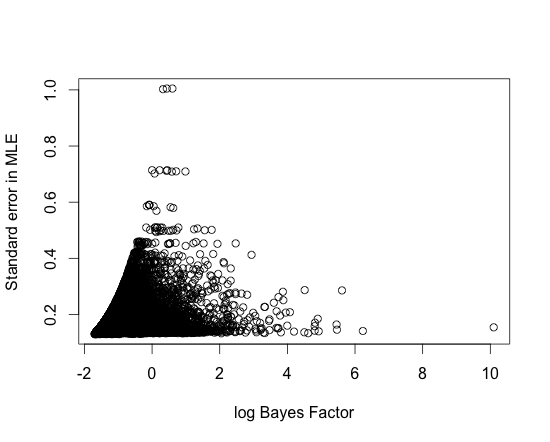

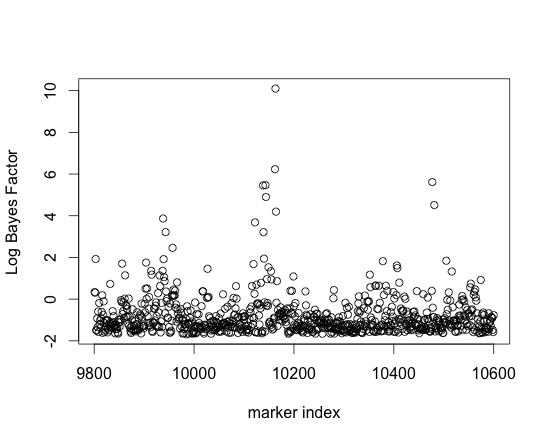

We calculated the general Bayes Factors for each marker and in Fig (1) we plot the log Bayes Factors over the chromosome. While there is considerable variation we observe strong evidence of association around marker 10,000. It is interesting to compare the evidence of association provided by the Bayes Factor Fig (1) in comparison to that obtained using a conventional Cox PH partial-likelihood based test. In Fig (2) we plot the log Bayes Factors versus p-values obtained from a likelihood ratio test. We can see general agreement especially at the markers with strongest association as one would expect for a large sample size. Interestingly there appears to be greater dispersion at markers of weaker association. In Fig (3) we highlight the region of weaker association and colour the points by the standard error of the maximum likelihood estimate. We can see a tendency for markers with less information, greater standard error, to get attenuated towards a logBF of 0 under the general Bayesian approach. This is further highlighted in Fig (4) where we plot the standard error against log Bayes Factors. Markers with high standard error relate to genotypes of rarer alleles and the attenuation reflects a greater degree of uncertainty for association at these markers that contain less information.

Returning to the “hit region” showing strongest association around marker 10,000, in Fig (5) we see the portion of the graph from Fig (1) containing 800 makers around the marker of strongest association. Due to high colinearity between markers it is not clear whether the signal of association arises from a single effect correlated with others, or from multiple independent association signals. In order to investigate this we developed multiple marker methods.

We consider a model using potentially all 800 makers in the region and phrase the problem as a variable selection task under a partial-likelihood (loss), in which the user suspects that some of the recorded covariates (13) may not be relevant to variation in survival times.

In the non-Bayesian paradigm, variable selection can proceed by defining a cost function, such as AIC or BIC, that adjusts fit to the data by the number of covariates in the model. Inference proceeds using an optimization algorithm, such as forward or stepwise selection, to find a model that minimises the cost. More recently, penalized-likelihood methods have proved popular (Tibshirani, 1997; Fan and Li, 2002) where the partial-likelihood is maximised subject to some constraint on the norm of the regression coefficients defined by some appropriate sparsity inducing metric.

Despite the enormous impact of Cox PH models and the importance of variable selection, the Bayesian literature in this area is limited. This is because of the lack of a theoretical foundation to treat as a nuisance parameter, leading to either ad hoc methods or the full specification of a joint probability model. For instance, Faraggi and Simon (1998) and Volinsky et al. (1997) adopt pseudo-Bayesian approaches. The paper of Volinsky et al. (1997) take the BIC as an approximation to the marginal likelihood and they use a branch and bound algorithm to find a set of models with differing sets of covariates with high BIC scores. The difficulty here is that, while the methods are important and well motivated, they are ultimately ad hoc. Moreover, prior information on does not enter into the calculation of the BIC, meaning that an important aspect of the Bayesian approach is lost.

In contrast, Ibrahim et al. (1999) consider variable selection within a full joint model using a prior specification of a gamma process for the baseline hazard (see also Ibrahim et al. (2001)). This provides a formal Bayesian solution but inference is then conditional on, and sensitive to, the specification of the prior on , something the partial-likelihood model explicitly avoids.

Here we use the partial-information relevant to the regression coefficients via the cumulative loss function (13). We assume proper priors, on the regression coefficient,

where is an indicator variable on covariate relevance with, and we now treat as a vector in a joint model. In this way the posterior quantifies beliefs about which variables are important to the regression. We use Markov chain Monte Carlo (MCMC) to draw samples approximately from from which the marginal distribution on can be examined. In particular we make use of an efficient joint updating proposal, , within the MCMC as where proposes a local move to add, remove, or swap one variable per MCMC iteration in or out of the current model indexed by , and is a joint independence Metropolis update proposal, where are the MAP and approximate Information Matrix obtained from the combination of log-partial-loss and normal prior. The joint proposal is then accepted with probability,

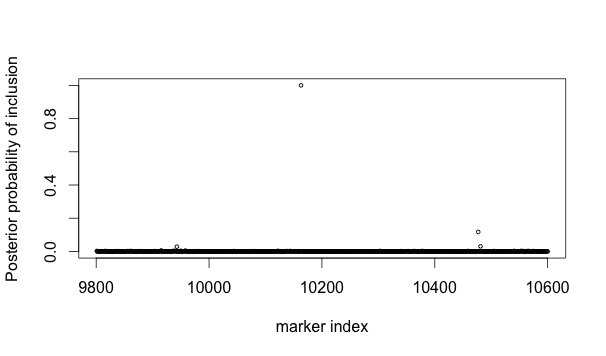

We ran our MCMC algorithm for 100,000 iterations with prior parameter settings, , for all , equivalent to a prior assumption of a single associated marker. In Fig (6) we show the marginal inclusion probability, after discarding 10,000 samples as a burn in. The algorithm showed an overall acceptance rate of 8% for proposed moves. The model suggest overwhelming evidence for a single marker in the region of index 10200 but also weaker evidence of independent signal in a couple of other regions. R code to perform the reversible jump MCMC multiple variable sampling for the Cox PH partial-likelihood with normal priors is available on request.

5.2 Bayesian model-free clustering. Cluster analysis is one of the most widely used and important areas of modern statistics (Hastie et al 2009). In cluster analysis a primary objective is to identify self-similar groups within data, such that observations within a group are deemed more closely related to one another than observations between groups. -means clustering being arguably the most popular clustering method in use today.

The clustering problem is interesting from a formal Bayesian perspective as it raises a number of challenges. The object of interest is the cluster partition mapping, , that allocates observations to clusters. However the partition as it stands is not a generative model (sampling distribution for observables). To implement clustering the Bayesian analyst is forced to define a sampling distribution for observations within a cluster, , where denotes parameters associated with the th cluster, with an associated prior probability of cluster membership . This leads to the well known marginal mixture representation,

the canonical example being with Gaussian mixture components, , which necessitates a further layer of hierarchical priors . The mixture model representation to accomplish inference on has significant consequences. First, cluster membership can be sensitive to the choice of sampling distribution. Secondly Bayesian mixture models suffer from the well known label switching problem (Jasra et al 2005).

This is a good illustration of where conventional Bayesian updating is restrictive. In cluster analysis the object of interest is typically the partition structure, , yet the Bayesian analyst is forced to introduce an additional level of complexity, specifying mixture components with nuisance parameters and priors on nuisance parameters, , which are of no interest, yet affect the analysis, and define a likelihood which exhibits symmetry to permutation of the labels.

On the other hand, non-Bayesian model-free segmentation methods have a distant advantage in allowing the analyst to concentrate on the object of interest, namely the clustering , typically defined through the specification of a pairwise dissimilarity score between observations . An optimisation algorithm is then used to find the optimal partition that minimises the score over pairs within and/or between clusters. However, in this approach there is no natural method333Note, we are not referring to the stability of the optimisation routine to find the global minima but rather that there maybe many competing segmentations of the data with near equivalent scores. to explore uncertainty, sensitivity or stability in the reporting of . Conventional methods of frequentist uncertainty characterisation, via the bootstrap or sub-sampling, cannot be routinely applied to model-free cluster analysis as dissimilarity scores are typically defined over pairs of observations and we only have one realisation of the data. Some methods propose to subsample the data and look at stability of global statistics, such as the choice of the number of groups, but there is generally a lack of theoretical understanding and justification for stability methods in clustering, and moreover such approaches cannot answer the important question of pairwise cluster uncertainty on the joint allocation .

In Seldin and Tishby (2001), the authors use PAC Bayesian ideas to consider latent cluster structure to obtain a predictor distribution for outcome given based on a clustering of the . For example, could be a set of movies, or a set of individuals, or a vector combination of both. The loss function to be minimized is given by

where

and

for some probability measure . Here would denote a clustering of the and the are the observed data. This minimization is non-trivial and the setting of the coefficient scaling the information in the data can be hard to determine, though the authors suggest a cross-validation approach.

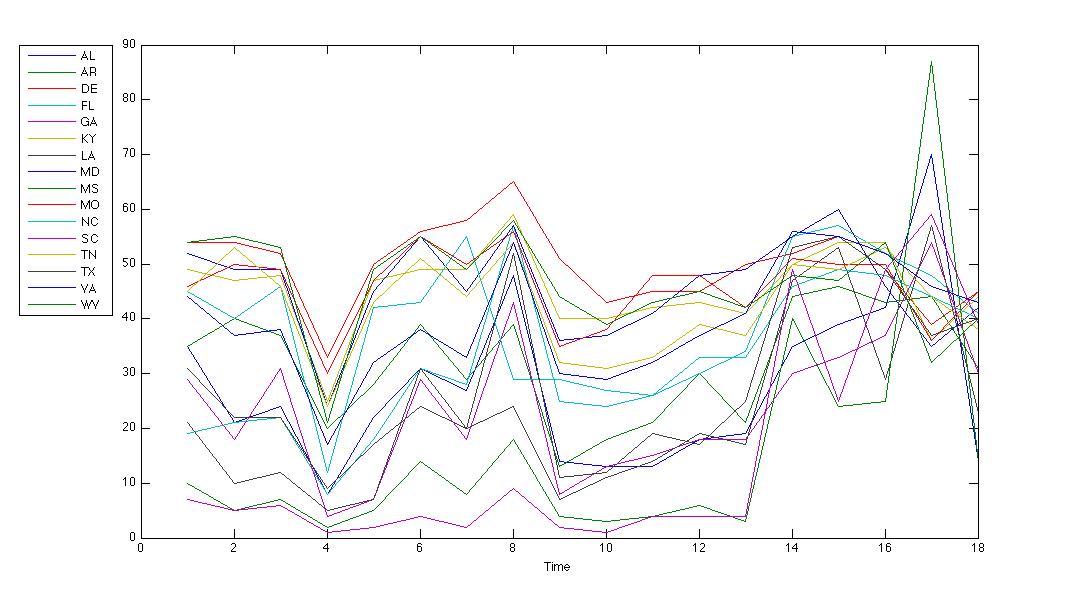

Our setting is slightly different since we only observe and wish to make inference on the underlying clustering of observations into groups. Hence we define a prior distribution directly on the partition, , and a loss function and use general Bayesian updating. To illustrate this we consider uncertainty analysis of a classic data set considered in Hartigan (1972), illustrated in Figure 7, in his highly influential paper that introduced biclustering. Biclustering refers to the simultaneous clustering of observations and covariates (rows and columns) of a data matrix. It having proved extremely useful in modern application areas, particularly in genomics (Cheng & Church (2000), Tanay et al (2002), Heard et al (2005)).

Hartigan’s paper considered the percentage Republican presidential vote of sixteen southern States in the US over 18 elections covering the years 1900–1968. Hartigan treated the time series as independent covariates in his co-clustering approach. Here, for simple illustration, we maintain the time series ordering, so that the co-clustering is akin to clustering multiple change-point time series with common but unknown change points. We assume the cluster memberships are constant over time, but the time series change at specific breakpoints. Our loss function is defined as in Hartigan (1972) using a sum of squares decomposition,

where denotes a grouping of States over a particular time period and denotes the mean vote of the States and elections assigned to the ’th cluster, and posterior distribution The setting of the loss parameter is a crucial part of the model specification. Following the procedures discussed in Section 3, it’s difficult to consider a conjugate specification or a unit information prior on the discrete structures. We instead propose to use a frequentist calibration approach in the following manner. Recall that under a flat prior on we can set via a subjective assessment of the posterior ratio at a reference point,

and where we can solve for if all the other elements are given. In elicitation of we propose to make use of classical results from ANOVA. We take as our first reference point the null partition using a single global cluster, so that the loss is simply the sum of squares around the mean. Then consider a randomised data partition that allocates the data uniformly at random to clusters. Under this allocation scheme we expect,

where denotes the distribution. We can then use the F-distribution to help in the calibration. For example, if we consider a point in the tails of such that, with , and specify then represents the value of loss such that a randomised allocation has probability of producing a smaller loss. Equivalently, with probability a random allocation would lead to a reduction in loss as high as relative to the single cluster. When is large we can be confident that a partition achieving a loss of represents a significant clustering. The analyst can then calibrate in the following way:

-

•

Define a reference value for under a uniform prior, setting small, say .

-

•

Define a p-value value, , such that should a partition achieve a relative reduction in loss of , relative to the global partition , then you would assign relative posterior beliefs of .

-

•

Set

For the election data we found is quite stable to the calibration choice of , e.g with we find , and for . We choose and ran an MCMC algorithm for 100,000 iterations using a burn in of 50,000. The iteration numbers were chosen after experimentation to deliver stable results over multiple runs. The MCMC algorithm was re-run for differing numbers of partitions of States and differing number of time series change points. Table 1 presents the results of the average loss achieved over each run alongside the estimate of the posterior probability for each configuration shown in brackets using a Poisson(3) prior on the number of groups and a Poisson(2) prior on the number of time groupings ( in the table), which is the number of change-points +1. Note that the first column in Table 1 equates to standard clustering of the States with zero change points, whereas the first row represents a multivariate change point model. We can see from Table 1 that there is strong evidence for clustering in both time and across States. The maximum posterior probability favours the model with 3 groups of States and 3 time groupings.

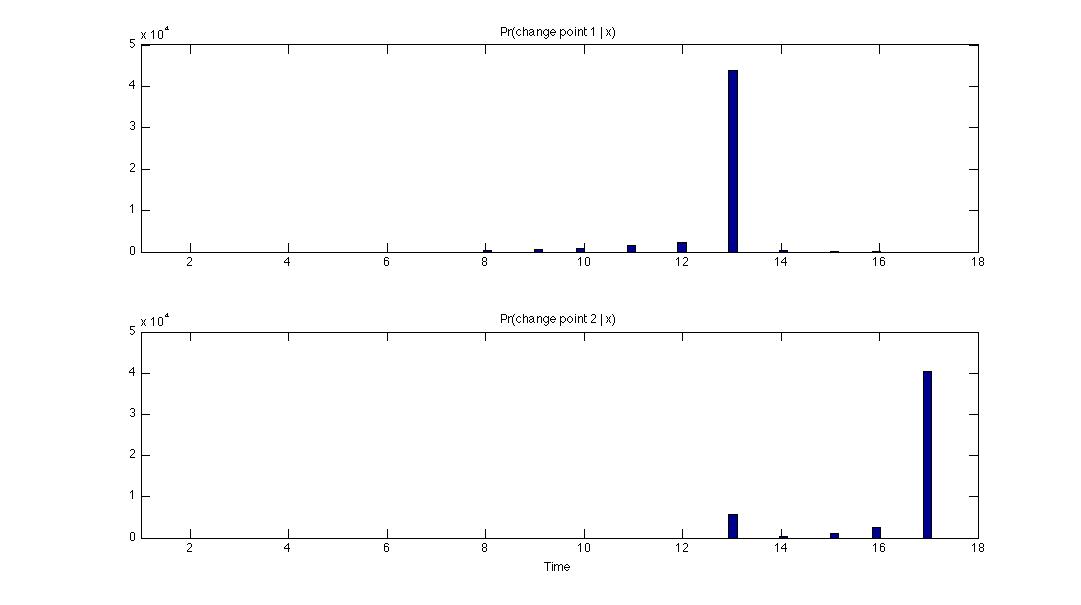

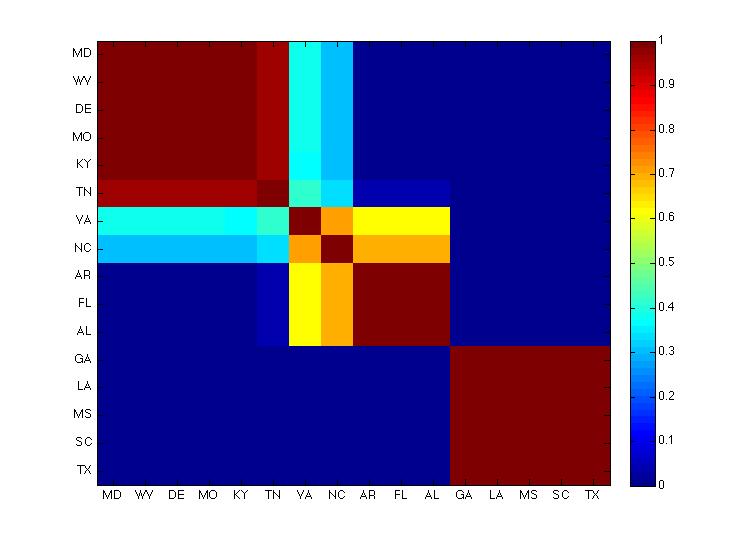

We can investigate uncertainty in the partitions and in the cluster allocation of the maximal posterior model. To illustrate this we plot in Figure 8 the distribution of the location of time-series change points for the model. We can see strong evidence that the change points occur late in the series, which is visually supported by the data in Figure 7. The pairwise co-clustering probabilities of this model are shown in Figure 9, where each element represents the pairwise probability events , where is the cluster index for the ’th State. The cluster blocks show strong concordance with the single co-cluster reported by Hartigan, see Figure 6a in Hartigan (1972). However our method highlights considerable uncertainty in the pairing of Virginia and North Carolina, something we’re able to quantify using our general Bayesian approach.

6. Discussion. We have provided a basis for general learning and the updating of information using belief probability distributions. Loss functions constructed on spaces of probability measures allow for coherent updating. Specifically, information is connected to the parameter of interest via a loss function and this is the fundamental concept, replacing the restrictive connection based on probability models. We can recover precisely the traditional updating rules such as the Bayes rule when we select the self–information loss function, when it is appropriate to do so.

The assumptions we make are minimal. That information can be connected to unknown parameters via loss functions and that individuals then act rationally by minimizing their expected loss. If information is assumed to come from some probability model then we can accommodate this within our framework by appealing to the self–information loss function equivalent to the negative log-likelihood and so we can argue that loss functions are sufficient for learning mechanisms currently in use.

More generally, we can use loss functions currently employed in a classical context for robust estimation; for example, generalized estimating equations. We can also deal appropriately with partial information where it is only a part of some observed information is useful or relevant for learning about the decision making process based on a particular relevant parameter of interest.

We have developed a rigorous approach to updating beliefs where we are required only to think about which is the best parameter from a chosen model needed to make a decision rather than have to think about a non–existent true model parameter which coincides with the true data generating mechanism.

We believe it is more fundamental to identify parameters of interest through loss functions. The alternative route through a probability model is, we argue, highly restrictive and leads to narrow types of Bayesian updating. The necessary supporting theory for us is minimal, the construction and minimization of loss functions, whereas for the use of probability models is more intricate and restrictive.

Acknowledgements. The authors are grateful for the detailed comments of two anonymous reviewers and an Associate Editor on a previous version of the paper.

References.

-

Ali, S.M. and Silvey, S.D. (1966). A general class of coefficients of divergence of one distribution from another. Journal of the Royal Statistical Society, Series B 28, 131–142.

-

Alquier, P. (2008). PAC-Bayesian bounds for randomized empirical risk minimizers. Mathematical Methods of Statistics, 17(4), 279-304.

-

Bar-Hillel, M. and Falk, R. (1982). Some teasers concerning conditional probabilities. Cognition, 11:109–122, 1982.

The consistency of posterior distributions in nonparametric problems Annals of Statistics 27, 536–561.

-

Berger, J.O. (1993). Statistical Decision Theory and Bayesian Analysis. Springer Series in Statistics.

-

Bernardo, J.M. (1979). Expected information as expected utility. Annals of Statistics 7 686–690.

-

Bernardo, J.M. and Smith, A.F.M. (1994). Bayesian Theory. Wiley.

-

Bissiri, P.G. and Walker, S.G. (2010). On Bayesian learning from Bernoulli observations. Journal of Statistical Planning and Inference 140, 3520-3530.

-

Bissiri, P.G. and Walker, S.G. (2012a). On Bayesian learning from loss functions. Journal of Statistical Planning and Inference 142, 3167-3173.

-

Bissiri, P.G. and Walker, S.G. (2012b). Converting information into probability measures via the Kullback–Leibler divergence. Annals of the Institute of Statistical Mathematics 64, 1139-1160.

-

Catoni, O. (2003). A PAC Bayesian approach to adaptive classification. Preprint Laborataire de Probabilités et Modèles Aléatoires, no. 840.

-

Cesa-Bianchi, N., and Lugosi, G. (2006). Prediction, learning, and games. Cambridge University Press.

-

Cox, D. R. (1972). Regression models and life tables (with discussion). Journal of the Royal Statistical Society, Series B 34, 187-220.

-

Cheng, Y. and Church, G. M. (2000). Biclustering of expression data. ISMB 8, pp. 93-103.

-

Datta, G. S., and Sweeting, T. J. (2005). Probability matching priors. Handbook of statistics, 25, 91-114.

-

Diaconis, P. and Zabell, S.L. (1982). Updating subjective probability. Journal of the American Statistical Association 77, 822–830.

-

Doucet, A., and Shephard, N. (2012). Robust inference on parameters via particle filters and sandwich covariance matrices. University of Oxford, Department of Economics. No. 606.

-

de Finetti, B. (1937). La prévision: ses lois logiques, ses sources subjectives. Annales de l’Institute Henri Poincaré 7, 1–68.

-

Fan, J and Li, R. (2002). Variable Selection for Cox’s proportional Hazards Model and Frailty Model. Ann. Statist. 30, 1, 74-99.

-

Faraggi, D. and Simon R. (1998). Bayesian variable selection method for censored survival data. Biometrics 54, 1475-1485.

-

Freund., J. E. (1965) Puzzle or paradox? Am. Stat., 19 (4): 29–44, 1965.

-

Gardner, M. (1959). The Scientific American Book of Mathematical Puzzles and Diversions. Simon and Schuster, New York, 1959.

-

Ghosh, J.K. and Ramamoorthi, R.V. (2003). Bayesian Nonparametrics Berlin: Springer–Verlag.

-

Goldstein, M. (1981). Revising previsions: A geometric interpretation. Journal of the Royal Statistical Society, Series B 43, 105–130.

-

Goldstein, M., and Wooff, D. (2007). Bayes Linear Statistics, Theory & Methods. 716. Wiley.

-

Hastie, T., Tibshirani, R. and Friedman, J. (2009). Elements of Statistical Learning. Springer.

-

Heard, N. A., Holmes, C. C., Stephens, D. A., Hand, D. J., and Dimopoulos, G. (2005). Bayesian coclustering of Anopheles gene expression time series: study of immune defense response to multiple experimental challenges. PNAS 102(47), 16939–16944.

-

Hirshleifer, J. and Riley, J.G. (1992). The Analytics of Uncertainty and Information. Cambridge University Press.

-

Hoff, P. and Wakefield, J.C. (2013). Bayesian sandwich posteriors for pseudo-true parameters. Journal of Statistical Planning and Inference 143, 1638-1642.

-

Hüber, P. (1964). Robust estimation of a location parameter. Annals of Mathematical Statistics 35, 73-101.

-

Hüber, P. (2009). Robust Statistics (2nd ed.). Hoboken, NJ: John Wiley & Sons Inc.

-

Hutchison, K. (1999). What are conditional probabilities conditional upon? Brit. J. Phi. Sci., 50:665–695, 1999.

-

Hutchison,K. (2008). Resolving some puzzles of conditional probability. Adv. Sci. Lett., 1:212–221, 2008.

-

Ibrahim, J.G. and Chen, M.H. (2000). Power prior distributions for regression models. Statistical Science 15, 46–60.

-

Ibrahim, J.G., Chen, M.H. and MacEachern, S.N. (1999). Bayesian variable selection for proportional hazards models. The Canadian Journal of Statistics. 27, 701-171.

-

Ibrahim, J.G., Chen, M.H. and Sinha, D. (2001). Bayesian Survival Analysis, Springer Series in Statistics.

-

Jasra, A., Holmes, C. C., and Stephens, D. A. (2005). Markov chain Monte Carlo methods and the label switching problem in Bayesian mixture modeling. Statistical Science, 50-67.

-

Jiang, W. and Tanner, M.A. (2008). Gibbs posterior for variable selection in high-dimensional classification and data mining. Ann. Statist. 36, 2207-2231

-

Kass, R.E. and Wasserman, L.A. (1996). The selection of prior distributions by formal rules. Journal of the American Statistical Association 91, 1343–1370.

-

Key, J.T., Pericchi, L.R. and Smith, A.F.M. (1999) Bayesian model choice: What and why? (with discussion). In Bayesian Statistics 6, Bernardo, J.M., Berger, J.O., Dawid, A.P. and Smith, A.F.M. (Eds). Oxford University Press, 343–370.

-

Kullback, S. and Leibler, R.A. (1951). On information and sufficiency. Annals of Mathematical Statistics 22, 79–86.

-

Liang, K.Y. and Zeger, S.L. (1986). Longitudinal data analysis using generalized linear models. Biometrika 73, 13–22.

-

Marin, J. M., Pudlo, P., Robert, C. P., and Ryder, R. J. (2012). Approximate Bayesian computational methods. Statistics and Computing, 22(6), 1167-1180.

-

McAllester, D. (1998). Some PAC Bayes theorems. In Proceedings of the 11th Annual Conference on Computational Learning Theory, ACM, pp. 164–170.

-

Merhav, N. and Feder, M. (1998). Universal prediction. IEEE Transactions on Information Theory 44, 2124–2147.

-

Muller, U. (2012). Risk of Bayesian inference in misspecified models, and the sandwich covariance matrix. Department of Economics, Princeton University.

-

Ribatet, M., Cooley, D. and Davison, A. C. (2009). Bayesian inference from composite likelihoods, with an application to spatial extremes. arXiv preprint :0911.5357.

-

Royall, R., and Tsou, T. S. (2003). Interpreting statistical evidence by using imperfect models: robust adjusted likelihood functions. Journal of the Royal Statistical Society: Series B 65, 391–404.

-

Savage, L.J. (1954). The Foundations of Statistics. New York. Wiley.

-

Seldin, Y. and Tishby, N. (2010). PAC Bayesian analysis of co-clustering and beyond. Journal of Machine Learning Research 11, 3595-3646.

-

Shawe-Taylor, J. and Williamson, R. (1997). A PAC analysis of a Bayesian estimator. In Proceedings of the 10th Annual Conference on Computational Learning Theory, ACM, pp. 2–9.

-

Tanay, A., Sharan, R., and Shamir, R. (2002). Discovering statistically significant biclusters in gene expression data. Bioinformatics, 18 (1), 136–144.

-

Tibshirani, R. J. (1997). The lasso method for variable selection in the Cox model. Statistics in Medicine 16, 385-395.

-

Volinsky, C.T., Madigan, D., Raftery, A. E. and Kronmal, A. (1997). Bayesian Model Averaging in Proportional Hazard Models: Assessing the Risk of a Stroke. Journal of the Royal Statistical Society, Series C. 46, 4, 433–448.

-

von Neumann, J. and Morgenstern, O. (1944). Theory of Games and Economic Behaviour. Princeton University Press.

-

Walker, S.G. and Hjort, N.L. (2001). On Bayesian consistency. Journal of the Royal Statistical Society, Series B

-

Zellner, A. (1988). Optimal information processing and Bayes’s theorem. The American Statistician 42, 278–284.

-

Zhang, T. (2006a). From -entropy to KL-entropy: Analysis of minimum information complexity density estimation. Ann. Statist. 34, 2180-2210.

-

Zhang, T. (2006b). Information theoretical upper and lower bounds for statistical estimation. IEEE Trans. Inform. Theory 52, 1307-1321.

| No. change points in time | |||

|---|---|---|---|

| No. State clusters | |||

| 7.98 (-14.49) | 6.82 (-14.34) | 6.72 (-14.73) | |

| 5.36 (-13.69) | 5.13 (-13.65) | 3.19 (-13.58) | |

| 5.09 (-13.64) | 3.92 (-13.38) | 2.36 (-13.28) | |

| 4.99 (-13.91) | 3.32 (-13.50) | 2.02 (-13.41) |