Portfolio Optimization in R

Abstract

We consider the problem of finding the efficient frontier associated with the risk-return portfolio optimization model. We derive the analytical expression of the efficient frontier for a portfolio of risky assets, and for the case when a risk-free asset is added to the model. Also, we provide an R implementation, and we discuss in detail a numerical example of a portfolio of several risky common stocks.

portfolio optimization, efficient frontier, R.

1 Introduction

Portfolio optimization is a challenging problem in economic analysis and risk management, which dates back to the seminal work of Markowitz [1]. The main assumption is that the return of any financial asset is described by a random variable, whose expected mean and variance are assumed to be reliably estimated from historical data. The expected mean and variance are interpreted as the reward, and respectively the risk of the investment. The portfolio optimization problem can be formulated as following: given a set of financial assets, characterized by their expected mean and their covariances, find the optimal weight of each asset, such that the overall portfolio provides the smallest risk for a given overall return [1-5]. Therefore, the problem reduces to finding the "efficient frontier", which is the set of all achievable portfolios that offer the highest rate of return for a given level of risk. Using the quadratic optimization mathematical framework it can be shown that for each level of risk there is exactly one achievable portfolio offering the highest rate of return. Here, we consider the standard risk-return portfolio optimization model, when both long buying and short selling of a relatively large number of assets is allowed. We derive the analytical expression of the efficient frontier for a portfolio of risky assets, and for the case when a risk-free asset is added to the model. Also, we provide an R implementation for both cases, and we discuss in detail a numerical example of a portfolio of several risky common stocks.

2 Assets and portfolios

A portfolio is an investment made in assets , with the returns , , using some amount of wealth . Let denote the amount invested in the -th asset. Negative values of can be interpreted as short selling. Since the total wealth is we have:

| (1) |

It is convenient to describe the investments in terms of relative values such that:

| (2) |

and

| (3) |

To characterize the portfolio we consider the expected return:

| (4) |

where is the expected return of each asset, . Also, we use the covariance matrix of the portfolio:

| (5) |

where

| (6) |

in order to quantify the deviation from the expected return, and to capture the risk of the investment. The variance of the portfolio is then given by:

| (7) |

where is the vector of weights.

3 N risky assets

A portfolio is optimal if for a given expected return , the portfolio has the least variance . Finding such a portfolio requires the solution of the following constrained quadratic optimization problem [6]:

| (8) |

subject to:

-

•

the constant invested wealth constraint (equivalent to Eq. 2)

| (9) |

-

•

the expected return constraint (equivalent to Eq. 4):

| (10) |

where and .

This problem can be solved using the method of Lagrange multipliers. Let us define the Lagrangian:

| (11) |

where and are the Lagrange multipliers. The critical point of the Lagrangian can be obtained by solving the system of equations:

| (12) |

| (13) |

| (14) |

From the first equation we have:

| (15) |

and from the next two equations we have:

| (16) |

| (17) |

Taking into account that:

| (18) |

we can write:

| (19) |

where:

| (20) |

This system has a solution if:

| (21) |

Since is a positive definite matrix, the inverse is also positive definite, which means that for any vector . Obviously we have and , and:

| (22) |

and therefore we also have . The Lagrange multipliers are then given by:

| (23) |

and the weights of the optimal portfolio are:

| (24) |

where:

| (25) |

| (26) |

The portfolio which minimizes the variance for a specified expected return is called a "frontier portfolio". It follows that all frontier portfolios are a linear combination of the two portfolios and .

The variance of the frontier portfolio is:

| (27) |

which can be further simplified as:

| (28) |

This equation represents the "efficient frontier", and it represents a hyperbola in the -plane. From here we obtain the weights of the minimum variance portfolio:

| (29) |

and the corresponding risk-return values:

| (30) |

| (31) |

An important investment preference on the "efficient frontier" is the portfolio with the maximum Sharpe ratio [1-3]:

| (32) |

The Sharpe ratio represents the expected return per unit of risk. Therefore, the portfolio with maximum Sharpe ratio gives the highest expected return per unit of risk, and therefore is the most "risk-efficient" portfolio. Geometrically, the portfolio with maximum Sharpe ratio is the point where a line through the origin is tangent to the efficient frontier, and therefore it is also called the "tangency portfolio".

In order to find the tangency point we observe that the slope of the tangency line:

| (33) |

should be equal with the derivative of the "efficient frontier" at that point:

| (34) |

Thus, we easily obtain the risk-return pair for the "tangency-portfolio":

| (35) |

| (36) |

Also, the allocation of the assets for the "tangency portfolio" are therefore given by:

| (37) |

4 Eigen-portfolios

The covariance matrix is positive definite, and the correlation matrix is given by:

| (38) |

where

| (39) |

Obviously, the correlation matrix has positive eigenvalues:

| (40) |

and associated orthogonal eigenvectors:

| (41) |

| (42) |

such that:

| (43) |

where:

| (44) |

In order to define the eigen-portfolios [7] we divide each eigenvector of the correlation matrix by the volatility of the corresponding asset:

| (45) |

and we normalize by imposing a constant invested wealth, such that:

| (46) |

where , . For each eigen-portfolio, the weight of a given asset is inversely proportional to its volatility. Also, the eigen-portfolios are pairwise orthogonal, and therefore completely decorrelated, since:

| (47) |

Thus, any portfolio can be represented as a linear combination of the eigen-portfolios, since they are orthogonal and form a basis in the asset space.

It is also important to emphasize that the first eigen-portfolio, corresponding to the largest eigenvalue, typically has positive weights, corresponding to long-only positions. This is a consequence of the classical Perron-Frobenius theorem, which states that a sufficient condition for the existence of a dominant eigen-portfolio with positive entries is that all the pairwise correlations are positive. One can always get a dominant eigen-portfolio with positive weights using a shrinkage estimate [8-9], which is a convex combination of the covariance matrix and a shrinkage target matrix :

| (48) |

where the shrinkage matrix is a diagonal matrix:

| (49) |

In this case, there exists a such that the shrinkage estimator has a Dominant Eigen-Portfolio (DEP) with all weights positive. This portfolio is of interest since it provides a long-only investment solution, which may be desirable for investors who would like to avoid short positions and high risk.

5 N risky assets and a risk-free asset

Let us now assume that one can also invest in a risk-free asset. A risk-free asset is an asset with a low return , but with no risk at all, i.e. zero variance . The risk-free asset is also uncorrelated with the risky assets, such that for all risky assets . The investor can both lend and borrow at the risk-free rate. Lending means a positive amount is invested in the risk-free asset, borrowing implies that a negative amount is invested in the risk-free asset. In this case, we consider the following quadratic optimization problem [1-3]:

| (50) |

subject to:

| (51) |

The Lagrangian of the problem is given by:

| (52) |

The critical point of the Lagrangian is the solution of the system of equations:

| (53) |

| (54) |

From the first equation we have:

| (55) |

Therefore, the second equation becomes:

| (56) |

and from here we obtain:

| (57) |

where

| (58) |

The weights of the risky assets are therefore given by:

| (59) |

and the corresponding amount that is invested in the risk-free asset is:

| (60) |

Also, the standard deviation of the risky assets is:

| (61) |

or equivalently:

| (62) |

This is the efficient frontier when the risk-free asset is added, or the Capital Market Line (CML), and it is a straight line in the return-risk () space. Obviously, CML intersects the return axis for , at , which is the return when the whole capital is invested in the risk-free asset.

The tangency point of intersection between the efficient frontier and the CML corresponds to the "market portfolio". This is the portfolio on the CML where nothing is invested in the risk-free asset. If the investor goes on the left side of the market portfolio, then he invests a proportion in the risk-free asset. If he chooses the right side of the market portfolio, he borrows at the risk-free rate.

The market portfolio can be easily calculated from the equality condition:

| (63) |

The solution of the above equation provides the coordinates of the market portfolio:

| (64) |

| (65) |

and the weights of the market portfolio are then given by:

| (66) |

# number of risky assets (given)

# expected returns (given)

# number of portfolios computed on the frontier

; maximum value of risk considered

# return values on the frontier

# risk values on the frontier

for( to ){

}

# portfolio weights

for( to ){

}

# risk of MVP

# return of MVP

# weights of MVP

# risk of TGP

# return of TGP

# weights of TGP

6 R implementation

The code for portfolio optimization was written in R, which is a free software environment for statistical computing and graphics [10]. To exemplify the above analytical results, we consider a portfolio of common stocks. The raw data can be downloaded from Yahoo finance [11], and contains historical prices of each stock. The list of stocks to be extracted is given in a text file, as a comma delimited list. The raw data corresponding to each stock is downloaded and saved in a local "data" directory, using the "data.r" script (Appendix A), which has one input argument: the file containing stock symbols.

Once the raw data is downloaded the correct daily closing prices for each stock are extracted, and saved in another file, which is the main data input for the optimization program. The extraction is performed using the "price.r" script (Appendix B), which has three input arguments: the file containing stock symbols included in the portfolio, the number of trading days used in the model, the output file of the stock prices.

The pseudo-code for the case with N risky assets is presented in Algorithm 1. Also, the R script performing the optimization and visualization for the N risky assets case is "optimization1.r" (Appendix C). The script has three input arguments: the name of the data file, the number of portfolios on the efficient frontier to be calculated, and the maximum return considered on the "efficient frontier" (this should be several (5-10) times higher than the maximum return of the individual assets).

The pseudo-code for the case with N risky assets and a risk-free asset is presented in Algorithm 2, and the R script performing the optimization and visualization for the N risky assets case is "optimization2.r" (Appendix D). The script has four input arguments: the name of the data file, the number of portfolios on the CML to be calculated, the daily return of the risk free asset, and the maximum return considered on the "efficient frontier".

# number of risky assets

# expected returns

; # return of the risk free asset

# number of portfolios to be computed on the CML

; maximum value of risk considered

# return values on the CML

# risk values on the CML

for( to ){

}

# portfolio weights on CML

# risk free asset weights on CML

for( to ){

}

# risk of MP

# return of MP

# weights of MP

In order to exectute the code, on Unix/Linux platforms one can simply run the following script:

On Windows platforms one can use a simple batch file, like the following ones:

In these examples: "stocks.txt" is a file containing the symbols of some common stocks to be downloaded; "portfolio.txt" is the file where all the relevant stock prices are extracted for the current analysis.

7 Numerical examples

In order to illustrate the above results, we consider the case of a portfolio consisting of common stocks from IT industry. The content of the "stocks.txt" file is:

| (67) |

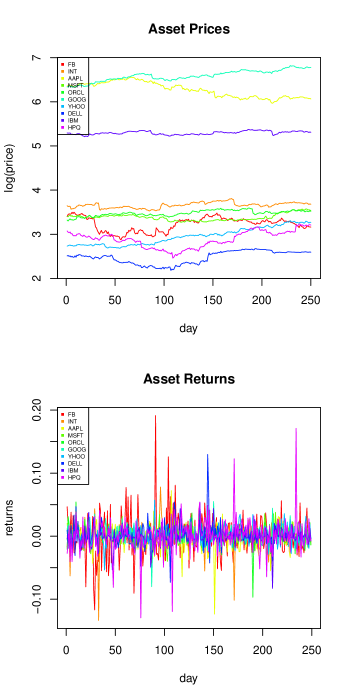

A historical record of daily prices of these stocks for the last trading days was used to estimate the mean return and the covariance matrix. The maximum return considered in computation is 0.01.

The daily returns of the assets are calculated as:

| (68) |

where is the day index, and is the price of asset at the closing day . The estimate average returns and covariances are:

| (69) |

| (70) |

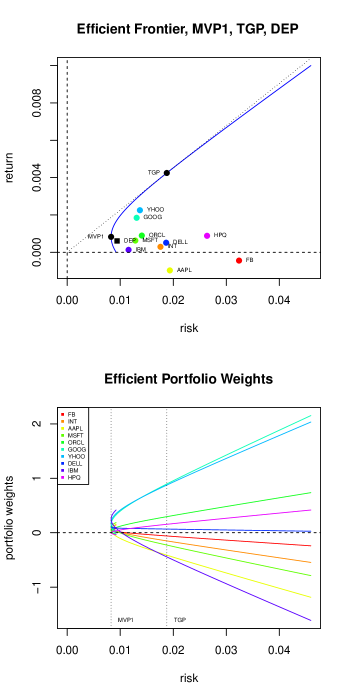

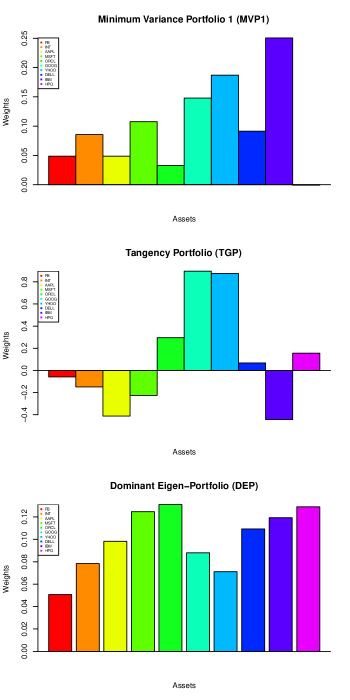

The asset prices and their expected returns for the considered time period are given in Figure 1. The resulted efficient frontier is given in Figure 2. The figure shows also the risk-return values of each stock considered, the minimum variance portfolio MVP1, the tangency portfolio TGP, and the weights of the efficient frontier portfolios as a function of risk. Figure 3 provides the weights of the MVP1, TGP and DEP portfolios.

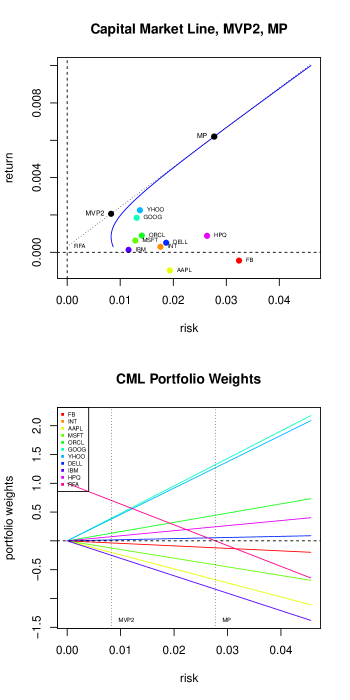

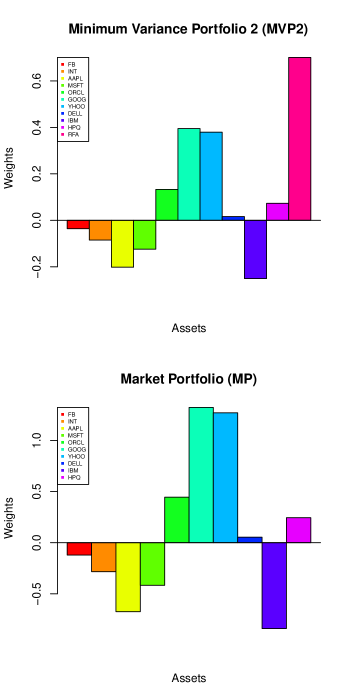

In order to illustrate the effect of the risk free asset (RFA), we consider that the investor can invest at a daily rate of return of . The capital market line, together with the frontier line and the position of the new minimum variance portfolio MVP2 and of the market portfolio MP are given in Figure 4. In this figure we also the risk dependence of the optimal portfolios from the capital market line, and we emphasize the MVP2 and MP portfolios. The weights of MVP2 and MP are plotted in Figure 5.

8 Conclusion

We have considered the standard risk-return portfolio optimization model, when both long buying and short selling, i.e. positive and negative weights, of a relatively large number of assets is allowed. We have derived the analytical expression of the efficient frontier for a portfolio of risky assets, and of the capital market line when a risk-free asset is added to the model. Also, we have provided an R implementation for both cases, and we have discussed in detail a numerical example of a portfolio of several risky common stocks.

9

10

11

12

References

- [1] H. Markovitz, Portfolio selection: Efficient Diversification of Investments, Wiley, New York, 1959.

- [2] J.-P. Bouchaud, M. Potters, Theory of Financial Risk, Alea-Saclay, Eyrolles, Paris, 1997.

- [3] E.J. Elton, M.J. Gruber, S.J. Brown, W.N. Goetzmann, Modern Portfolio Theory and Investment Analysis, 8th ed., Wiley, New York, 2010.

- [4] T. Hasuike and H. Ishii, “Robust Portfolio Selection Problems Including Uncertainty Factors,” IAENG International Journal of Applied Mathematics, 38:3, IJAM_38_3_09, 2008.

- [5] S. K. Mishra, G. Panda, B. Majhi, R. Majhi, “Improved Portfolio Optimization Combining Multiobjective Evolutionary Computing Algorithm and Prediction Strategy,” Proceedings of the World Congress on Engineering 2012 Vol I, WCE 2012, July 4 - 6, 2012, London, U.K..

- [6] G. Cornuejols, R. Tutuncu, Optimization Methods in Finance, Cambridge University Press, Cambridge, 2007.

- [7] M. H. Partovi and M. Caputo, “Principal Portfolios: Recasting the efficient frontier,” Economics Bulletin, vol. 7, pp. 1-10, 2004.

- [8] O. Ledoit and M. Wolf, “Improved Estimation of the Covariance Matrix of Stock Returns with an Application to Portfolio Selection,” Journal of Empirical Finance, vol. 10, pp. 603-621, 2003.

- [9] O. Ledoit and M. Wolf, “Honey, I Shrunk the Sample Covariance Matrix,” The Journal of Portfolio Management, vol. 30, no. 4, pp. 110-119, 2004.

- [10] http://www.r-project.org

- [11] http://finance.yahoo.com