An Identity of Hitting Times and Its Application to the Valuation of Guaranteed Minimum Withdrawal Benefit

Abstract

In this paper we explore an identity in distribution of hitting times of a finite variation process (Yor’s process) and a diffusion process (geometric Brownian motion with affine drift), which arise from various applications in financial mathematics. As a result, we provide analytical solutions to the fair charge of variable annuity guaranteed minimum withdrawal benefit(GMWB) from a policyholder’s point of view, which was only previously obtained in the literature by numerical methods. We also use complex inversion methods to derive analytical solutions to the fair charge of the GMWB from an insurer’s point of view, which is used in the market practice, however, based on Monte Carlo simulations. Despite of their seemingly different formulations, we can prove under certain assumptions the two pricing approaches are equivalent.

Key Words. Geometric Brownian motion with affine drift, Yor’s process.

1 Introduction

There are two sets of stochastic processes that are of particular interests for financial and actuarial applications. One of them is the time-integral of a geometric Brownian motion, defined by

where is a standard Brownian motion. It is also known as Yor’s process in computational finance literature and arises from the pricing of continuously monitoring Asian (average price) options. Detailed accounts of the laws of the geometric Brownian motion and its time-integral as well as their applications in mathematical finance can be found in Yor, (1992), Geman and Yor, (1993), Yor, 2001a , Carr and Schröder, (2003), etc.

The other one is a set of diffusion processes, known as geometric Brownian motions with affine drift, which are defined as solutions to stochastic differential equations for

| (1.1) | |||||

| (1.2) |

It follows immediately from Itô’s formula that for

| (1.3) |

From time to time, we also use the notation and to indicate the parameter used in their definitions in comparison with the process . The process was introduced for financial applications in Lewis, (1998) for the pricing of European-style options on dividend paying stocks. It is also well-known using a duality lemma of Lévy process (c.f. (Kyprianou,, 2006, Lemma 3.4)) that for and each fixed ,

| (1.4) |

where means “equals in distribution” throughout the note. This identity in distribution is exploited extensively in many papers for alternative methods for the pricing of Asian options, such as Donati-Martin et al., (2001), Linetsky, (2004), etc. There appears to be little discussion about the process in the existing literature.

In this paper, we investigate the first passage times of the processes and . Let

We shall also write and for short when the parameter is known from the context. It is immediately clear from (1.3) that

| (1.5) |

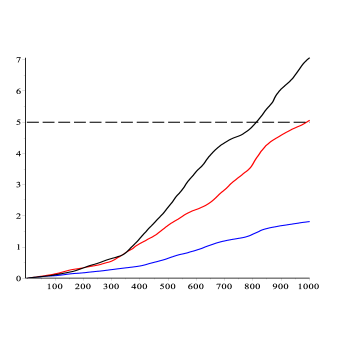

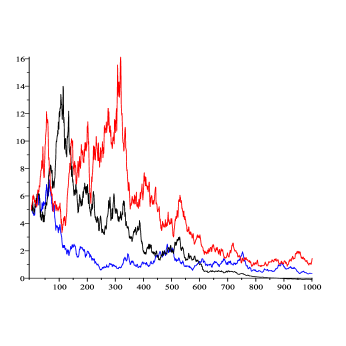

This appears to be a rather peculiar identity, which roughly means that for every sample path of the process starting off at and ascending to , there is a sample path of the process starting off at that takes just as much time descending (not monotonically) to . Although the two processes are intricately connected by the hitting times, they have drastically different sample path properties as evident from Figure 1. For instance, the process is a process of finite variation whereas the process has infinite variation; the process is an almost surely increasing process while no such monotonicity can be said of the diffusion process .

In Sections 2 and 3, we analyze the two types of hitting times seperately using their distinct analytic properties. As an application of the identity in distribution (1.5) in Section 4, we develop closed-form solutions to various quantities required for the valuation of the guaranteed minimum withdrawal benefit (GMWB).

2 Hitting time of Yor’s process

The distribution of was one of many computational issues raised but not directly addressed in (Yor, 2001b, , Section 8.2) regarding the exponential functionals of Brownian motion in connection with Asian options. In this section, we derive two equivalent expressions for the distribution of . Since we rely on a key result from Yor, (1992) as well as the transition density function of Bessel process with positive index, it is assumed throughout this section that .

Proposition 2.1.

For , the Laplace transform of is given by

| (2.1) |

where and is the Kummer’s function of the first kind.

Proof.

It is shown in Yor, (1992) that for

The known density of the Bessel process is, for

Therefore, we can find the Laplace transform of by

| (2.2) | |||||

It follows from (Watson,, 1944, page 383) that

∎

Proposition 2.2.

(First Representation) For , the probability density of is given by

| (2.3) |

where

| (2.4) |

and is a parabolic cylinder function related to Kummer’s function of second kind by

Proof.

It is known from Yor(1992) that

where

Therefore,

Due to the one-to-one correspondence of Laplace transform and a continuous density function, we must have the density function of the hitting time

Denote the integrand by . On one hand, note that there exists some such that

Using the asymptotics of (Olver et al.,, 2010, p.153,(6.12.1)), we know that for some as .

Similarly, using (Olver et al.,, 2010, p.151,(6.6.2)), we know that for some as ,

which approaches zero by (Olver et al.,, 2010, p.107,(4.4.14)). Thus By Fubini’s theorem, we exchange the integrals and obtain

where

According to (Olver,, 1974, page 208), the following formula holds

Assuming and substituting we obtain

We choose and and obtain (2.4). ∎

Proposition 2.3.

(Second Representation) For , the probability density of is given by

| (2.5) |

where is the Whittaker function of the second kind.

Proof.

The distribution function of with is obtained in (Feng and Volkmer,, 2013, (3.26)). Using the indentity in distribution (1.4), we can obtain the distribution of by letting and in (Feng and Volkmer,, 2013, (3.26)),

| (2.6) |

We note that

| (2.7) |

Therefore, differentiating (2.6) w.r.t. and taking the opposite sign yields the density (2.5). ∎

Remark 2.1.

We can demonstrate directly that the two representations of the hitting time density are indeed equivalent. Let be the Laplace transform of in (2.5) and be the Laplace transform of the distribution function of w.r.t. . We can find by setting and letting in (Feng and Volkmer,, 2013, (4.6)) that

where Using (Olver et al.,, 2010, (13.14.2)),

we obtain

It follows from (2.7) that Thus,

This agrees with the Laplace transform (2.1) of the second representation (2.3), since and

We are also interested in the “increments” of hitting times. For example, the time it takes for Yor’s process to reach level after attaining level ,

Proposition 2.4.

For ,

where is a Bessel process with index independent of on the right-hand side.

Proof.

Note that

Letting in (2.2) yields that for all . Thus it follows immediately from Theorem 6.16 of (Karatzas and Shreve,, 1991, page 86) that is a drifted Brownian motion independent of . Therefore,

where is a Yor’s process independent of Recall Lamperti’s identity (c.f. (Yor,, 1992, (2.a)))

where is a Bessel process with index (starting from ). Therefore, it follows immediately that

Note that in this case is independent of . ∎

Corollary 2.1.

The Laplace transform of for is given by

| (2.8) | |||||

3 Hitting time of diffusion process

In the theory of interest, annuity-certain is a type of financial arrangement in which payments of fixed amount are made periodically. If the investor starts with dollars and makes continuous payments into a savings account at the rate of one dollar per time unit and the accounts earns interest at the rate of per time unit, then the accumulated value at time of the account is

| (3.1) |

or equivalently by the ODE

In generalization, if the accumulation of deposits is linked to an equity index driven by a geometric Brownian motion

Then the accumulated value at time of one dollar deposited at should be proportional to the financial return of buying one share of the equity index over the period , i.e. With analogy to (3.1), the accumulated value at of incoming annuity payments should be

| (3.2) |

Similarly, with an initial deposit of dollars at time , the outstanding balance at time of outgoing annuity payments would be

| (3.3) |

A simple application of Itô’s formula shows that they are in fact the geometric Brownian motions with affine drift. We may write and to indicate their dependency on parameters.

One can also introduce annuity payments at any arbitrary constant number ( replaced by any constant). However, the SDEs of such form achieve no more generality than (1.1) and (1.2), as one can convert one to another by changing the time scale. The relations (1.4) and (1.5) continue to hold except for a change in time parameter. For example, for and each fixed ,

| (3.4) |

We can use the connections of these hitting times to find analytical solutions to their densities.

Proposition 3.1.

The Laplace transform of for is given by

| (3.5) |

where

Proof.

Denote the Laplace transform by According to Proposition 50.3 of Rogers and Williams, (2000) the solution is given by

where is a decreasing solution to the ODE

| (3.6) |

We obtain two real-valued fundamental solutions to

and

where and are Kummer’s functions of first and second kind respectively. It can be verified that is a decreasing solution whereas is an increasing solution. According to Andrews, (1985), we have the following asymptotics

Hence, as ,

Therefore, the solution to is given by (3.5). ∎

Remark 3.1.

When matching the parameters by letting then and . It follows immediately that the two expressions (3.5) and (2.1) agree, which confirms the identity in distribution of two hitting times (3.4). One should note, however, the result in Proposition 3.1 is more general than that in Proposition 2.1, as we do not require , the equivalent of .

Remark 3.2.

One immediate use of the identity in distribution is that we could provide an explicit expression of the density function of , which is usually a very difficult task by other means. Since with . Thus, if , we obtain the density of the hitting time given by

For the convenience of applications in Section 4.1, we present here the density of , even though similar results can be easily obtained for as shown in Remark 3.2.

Proposition 3.2.

For , the density of is given by

| (3.7) |

The probability of eventual passage below zero is given by

| (3.10) |

where is the lower incomplete Gamma function.

Proof.

It is known in (Linetsky,, 2004, p863,(63)) that for , the density of is given by

Let us now consider the distribution function The integral part can be integrated using the method in Feng and Volkmer, (2012). We shall use the following identity derived from (Prudnikov et al.,, 1986, p.463, (2.19.3.5)) for the summation part. For

Making a simple change of variables gives

Note that the first term in the summation has a simpler form

Thus, using a change of variables yields

In summary, the distribution of is given by

| (3.11) |

where we used the fact that Kummer function is the same as the hypergeometric function . Since we differentiate the above expression w.r.t. and obtain the density function (3.7).

We can also explore a “symmetry” between the processes and . It is clear from (3.2) and (3.3) that for any ,

Introduce the hitting time of

Then it follows that for any

| (3.13) |

Proposition 3.3.

The Laplace transform of is given by

Proof.

We first consider . It is clear from the proof of Proposition 3.1 that as are the decreasing and increasing solutions respectively for . Thus,

the first of which yields the expression for and the second of which produces the expression for by exchanging and . When , we obtain two real-valued fundamental solutions to (3.6)

In this case, is the decreasing function whereas is the increasing function. Thus for ,

and for and ,

which yield the desired expressions. ∎

Corollary 3.1.

The Laplace transform of is given by

Proof.

Remark 3.3.

Passing to the limit as , we obtain for ,

4 Guaranteed Minimum Withdrawal Benefit

The variable annuity guarantee product is arguably the most complex investment-combined insurance policy available to individual investors. Without any investment guarantees, they are almost the same as mutual funds except that all purchase payments are tax-deferred. In order to compete with mutual funds, variable annuity writers have introduced a variety of investment guarantees, among which the most recent market innovation is the guaranteed minimum withdrawal benefit (GMWB). Milevsky and Salisbury, (2006) was among the first to provide a mathematical model for the valuation of the GMWB, followed by various optimization problems based on withdrawal strategies in Dai et al., (2008), Chen and Forsyth, (2008), Forsyth and Vetzal, (2012), all of which are based on numerical PDE solutions. In this work, we attempt to show that in the plain vanilla case, the fair charge of the GMWB rider can in fact be determined by analytical solutions.

The GMWB typically is sold as a rider to variable annuity contracts. The policyholder is allowed to withdraw up to a fixed amount per year out of the investment fund without penalty. On the liability side, the GMWB rider guarantees the return of total purchase payment regardless of the performance of the underlying investment funds. For example, a contract starts with an initial purchase payment of $100 and the policyholder elects to withdraw the maximum amount of purchase payment without penalty each year. Due to the poor performance of the funds in which the policyholder invests, the account value is depleted at the end of five years. By this time, the policyholder would have only withdrawn in total. Then the guarantee kicks in to sustain the annual withdrawal until the entire purchase payment is return, which means it pays until the maturity at the end of years. On the revenue side, the guarantee is funded by daily charges of a fixed percentage of fees from the investment funds.

4.1 Policyholder’s perspective

Viewed as an investment vehicle, the GMWB rider is priced under the no-arbitrage assumptions from the investor’s perspective in Milevsky and Salisbury, (2006). Let be the initial deposit and be the guaranteed rate of withdrawal per time unit. Thus the GMWB rider provides safeguards to the continuous withdrawal until the initial deposit is completely refunded, i.e. the GMWB matures at time . Let be the risk-free force of interest. Thus the present value of guaranteed income is

In addition, if the equity fund performed well and the fund is not exhausted at maturity, then the policyholder is entitled to the then-current fund balance. We assume that the equity-index is driven under the physical measure by a geometric Brownian motion

As with mutual funds, the policyholder’s investment fund is linked to the equity index so that its value fluctuates in proportion to the equity index. Let be the rate per time unit of total fees charged by the insurer as a fixed percentage of the fund. Then the fund value is driven by

Throughout the section, we shall denote and reserve for the process whenever is clear from the context. Thus the policyholder receives at maturity

We determine the fair value of fees so that the arbitrage-free price of policyholder’s asset at maturity plus guaranteed income is equal to the initial purchase payment, i.e. to find such that

| (4.1) |

where is the risk-neutral measure. Under the risk neutral measure, the dynamics of the investment fund is driven by

where is the corresponding Brownian motion under the risk neutral measure. Note that where is an independent Brownian motion. We let

Then the process satisfies (1.2) with Thus and

where

| (4.2) |

Here we use to indicate the risk-neutral measure under which .

Proposition 4.1.

Let If , then

| (4.3) | |||||

If , then

| (4.4) |

where is the exponential integral.

Proof.

Recall that Hence Thus, it suffices to find an expression for Observe that using the strong Markov property

First consider . It is easy to show that the mean of the process is

Thus, we want to compute the integral

Once is known, we can obtain To simplify the double integral in , we rewrite in the form

We now distinguish the cases and .

When ,

The first integral is determined by the lower case of (3.10). We show in Lemma A.1 that the Laplace transform can be extended to even if , as . Thus,

| (4.5) |

where It is also clear from the proof of Lemma A.1 that the integrand of is absolutely integrable over for . We can exchange the order of integration for the third integral by Fubini’s Theorem. Piecing all together, we get

When ,

Similarly, the first integral is determined by the top case of (3.10). The second integral is given by (4.5) due to (3.12). We use Fubini’s theorem to obtain the expression for the third integral.

Then consider . Note that . Thus,

We denote the three terms by respectively. Note that

where we used known from (3.11).

We observe that when the expression (3.12) reduces to

Using the identities (Olver et al.,, 2010, p.251, (10.29.1)) and (Olver et al.,, 2010, p.254,(10.38.6))

where is the generalized exponential integral, we can show that

Using Fubini’s theorem, we can show that

Combining all terms we arrive at (4.4) after simplifications. ∎

Remark 4.1.

In the case that , can be further simplified to

| (4.6) |

This result can be obtained from the spectral method used in Feng and Volkmer, (2013) to determine risk measures (Section 3.2).

4.2 Insurer’s perspective

We can also price the GMWB from an insurer’s point of view so that the insurer’s revenue covers its liability. The outgoing cash flow for the insurer is the guaranteed payments after the investment fund is exhausted prematurely,

and the incoming cash flow for the insurer is determined by the GMWB rider charges

where is the rate per time unit of fees allocated to fund the GMWB. Note that in general as part of fees and charges are used to cover overheads and other expenses. Assuming both cash flows can be securitized as tradable assets, we can also use the no-arbitrage arguments to determine the fair fees by

| (4.7) |

Observe that the first term can be computed from

where is known from (3.12). The second term involves

The third term can be written as

In the rest of this subsection, we derive explicit expressions for each of the three unknown quantities.

Proposition 4.2.

Proof.

It follows that where is given in (3.7). ∎

Proposition 4.3.

Proof.

It follows immediately from which can be obtained from (3.11). ∎

Proposition 4.4.

Let and . If , then

| (4.8) |

If , then and

| (4.9) |

Proof.

We take a Laplace transform to remove the finite time . Define

Observe that

Let for the moment. It is not difficult to show that satisfies the ODE

with the boundary condition Let and for short . The ODE has the following general solution

where and are to be determined. Note that . We observe that

| (4.10) | |||||

Note that as ,

Then as ,

It is easy to show the fact that implies that , which means this term would not be bounded by (4.10). Hence Second, we can use the boundary condition to determine the coefficient . Note that as ,

Thus, as ,

Since , we must have

In summary,

and hence,

The three terms shall be denoted by respectively. Note that if we take the principal value (value with positive real part), then the square root function is analytic on The Kummer function is entire in and and meromorphic in with poles at . (Olver et al.,, 2010, p.322) Therefore, the Kummer function in is analytic on . The gamma function is meromorphic with no zeros, and with simple poles of residue at . (Olver et al.,, 2010, p.136) All in all, the function is meromorphic on with poles at and poles where i.e. let ,

First consider the case where . We deform the path of integration towards the negative -axis (Doetsch,, 1974, Sections 25 and 26) to obtain the Bromwich integral

Here is the path coming from following the lower boundary of the cut until and then returning to along the upper boundary of the cut. Since is conjugate to , then it simplifes to the second expression.

Note that if we let , then

Note that and are real-valued. Using the identity

where is the Whittaker function of the first kind, we rewrite as

It can be shown that

Let and . Using the fact that any real analytic function satisfies and that , we obtain

| (4.11) |

Thus,

Then we use to obtain

Note, however, since is meromorphic, finite many poles are placed on . Then we use the method of residues to identify the remaining contribution to the inverse Laplace transform.

We compute the residues arising from the gamma function.

One can simplify the formula slightly by using the identity

The rest of resides from are given by

Thus we collect all the residues and the inversion integral to obtain the expression for (4.8).

Last, we consider the case where . Note that becomes a pole of degree 2. We rewrite as

where is the modified Bessel function of the first kind with the order of . In order to calculate the residue of at , we evaluate

In a manner similar to the case of in the proof of Proposition 4.1, we can show that

Also note that Thus,

The rest of contributions to the Bromwich integral are the same as calculated in the case with , which are given by

Collecting all above terms, we obtain the expression of (4.9). ∎

4.3 Equivalency

We can summarize the cash flows for the buyer (policyholder) and the seller (insurer) of the GMWB. From a buyer’s standpoint, the present value of the profit (the payoff less the cost) is given by

From an insurer’s standpoint, the present value of the profit (the payoff less the cost) is given by

Note that on the insurer’s income side, there is an extra parameter which does not appear in the policyholder’s cash flows. To make the two viewpoints comparable, we first consider no expenses other than the pure cost of the GMWB, i.e. , which implies all charges are used to fund the guarantee. Observe that, unlike most financial derivatives seen in the literature, the buyer’s profit from the GMWB does not exactly offset the seller’s profit, which appears to be an asymmetric structure. Nevertheless, no-arbitrage theory dictates that the fair charge from a policyholder’s standpoint should agree with the fair charge from an insurer’s standpoint in this Black-Schole model, which otherwise would lead to an arbitrage bidding on their discrepancy.

Here we give a probabilistic proof of the equivalance of the pricing equations (4.1) and (4.7). Note that (4.1) can be rewritten as

| (4.12) |

and (4.7) can be rewritten as

| (4.13) |

We subtract (4.13) from (4.12) to obtain

| (4.14) |

It is easy to see that (4.1) and (4.7) are equivalent if and only if (4.14) holds true for all . Consider the bivariate process and its infinitesimal generator is then given by

Recall Dynkin’s formula (Øksendal,, 2003, p.124) that for any stopping time such that ,

We let and and obtain

which yields (4.14) after rearrangement. Therefore, (4.1) and (4.7) are equivalent and the implied fair charges must be the same.

4.4 Numerical illustration

We provide the first numerical example to show the fair charge level determined by both points of view, which are proven to be equivalent when . For the purpose of comparison, we use the same valuation basis as in (Milevsky and Salisbury,, 2006, p.31, Table 4). The risk-free interest rate is set at and volatility coefficient is taken at two levels, . A bisection method is used to determine the fair charge levels as solutions to the pricing equations. The search algorithm is programmed to reach accuracy up to 5 decimal places and then the fair charge levels, presented in Table 1, are rounded up to the nearest basis point (). In all immediate steps, we keep 10 significant digits. Each value takes about less than a minute to compute. We used both the pricing equations (4.1) and (4.7) to numerically confirm the accuracy of the explicit formulas.

| 0.05 | 29 | 77 |

|---|---|---|

| 0.06 | 41 | 104 |

| 0.07 | 54 | 132 |

| 0.08 | 68 | 162 |

| 0.09 | 82 | 192 |

Although within a close proximity, we found that the fair charges determined in Milevsky and Salisbury, (2006) from the policyholder’s perspective are generally overestimated, which appears to show some limitations of the numerical PDE methods introduced in the paper. The calculations based on Monte Carlo simultions would be very difficult, due to numerous recursions required to determine solutions to the pricing equations and the subsequent accumulation of estimation errors.

One should be reminded, however, that in practice only a certain percentage of the total fees is used to fund the GMWB rider, i.e. . The rest of the fees and charges are used to cover overhead expenses, commisions and costs of other benefits. We explore this practical situation in a second example where differs from . In each of the following cases, the GMWB charge is set at of total charges, i.e. Then we calculate the fair charges from the insurer’s point of view based on (4.7). The values of and are rounded to the nearest basis point in Table 2. A comparison of Table 1 and Table 2 also shows that the total charges with are more than than those with . A likely explanation is that higher fees lower the value of investment account, thereby increasing the chance of early exhaustion and consequently increasing the costs of guaranteed payments from the insurer.

| 0.05 | 37 | 29 | 101 | 81 |

|---|---|---|---|---|

| 0.06 | 53 | 42 | 139 | 111 |

| 0.07 | 71 | 56 | 179 | 143 |

| 0.08 | 90 | 72 | 222 | 178 |

| 0.09 | 110 | 88 | 267 | 213 |

Appendix A Appendix

Lemma A.1.

Proof.

It follows from (4.11) that

It is known in (Buchholz,, 1953, p.95,(10)) that

| (A.1) |

We also known from (Olver et al.,, 2010, (5.11.9)) that for fixed ,

| (A.2) |

Using (A.1) and (A.2), we obtain that as ,

where is a positive constant. Arguing as in the proof of Watson’s lemma (c.f. Olver, (1974)), it follows that

| (A.3) |

The positive constant may depend on and but is independent of (large) . We conclude from (A.3) that the Laplace transform

is analytic for and continuous for (since is integrable at .) Let be the expression for the Laplace transform of determined for in (3.12). Recall that the principle value of the square root function is analytic for and the Kummer function is analytic in and except for . Thus is analytic for . Since and agree on the positive real axis, they must agree for all The expression of holds for due to the continuity of . ∎

References

- Andrews, (1985) Andrews, L. C. (1985). Special functions for engineers and applied mathematicians. Macmillan Co., New York.

- Buchholz, (1953) Buchholz, H. (1953). Die konfluente hypergeometrische Funktion mit besonderer Berücksichtigung ihrer Anwendungen. Ergebnisse der angewandten Mathematik. Bd. 2. Springer-Verlag, Berlin.

- Carr and Schröder, (2003) Carr, P. and Schröder, M. (2003). Bessel processes, the integral of geometric Brownian motion, and Asian options. Teor. Veroyatnost. i Primenen., 48(3):503–533.

- Chen and Forsyth, (2008) Chen, Z. and Forsyth, P. A. (2008). A numerical scheme for the impulse control formulation for pricing variable annuities with a guaranteed minimum withdrawal benefit (GMWB). Numer. Math., 109(4):535–569.

- Dai et al., (2008) Dai, M., Kwok, Y. K., and Zong, J. (2008). Guaranteed minimum withdrawal benefit in variable annuities. Math. Finance, 18(4):595–611.

- Doetsch, (1974) Doetsch, G. (1974). Introduction to the theory and application of the Laplace transformation. Springer-Verlag, New York.

- Donati-Martin et al., (2001) Donati-Martin, C., Ghomrasni, R., and Yor, M. (2001). On certain Markov processes attached to exponential functionals of Brownian motion; application to Asian options. Rev. Mat. Iberoamericana, 17(1):179–193.

- Feng and Volkmer, (2012) Feng, R. and Volkmer, H. (2012). Analytical calculation of risk measures for variable annuity guaranteed benefits. Insurance Math. Econom., 51(3):636–648.

- Feng and Volkmer, (2013) Feng, R. and Volkmer, H. (2013). Spectral methods for the calculation of risk measures for variable annuity guaranteed benefits. Preprint.

- Forsyth and Vetzal, (2012) Forsyth, P. A. and Vetzal, K. R. (2012). Numerical methods for nonlinear PDEs in finance. In Handbook of computational finance, Springer Handb. Comput. Stat., pages 503–528. Springer, Heidelberg.

- Geman and Yor, (1993) Geman, H. and Yor, M. (1993). Bessel processes, asian options, and perpetuities. Math. Finance, 3(4):349–375.

- Karatzas and Shreve, (1991) Karatzas, I. and Shreve, S. E. (1991). Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition.

- Kyprianou, (2006) Kyprianou, A. E. (2006). Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin.

- Lewis, (1998) Lewis, A. L. (1998). Applications of eigenfunction expansions in continuous-time finance. Math. Finance, 8(4):349–383.

- Linetsky, (2004) Linetsky, V. (2004). Spectral expansions for Asian (average price) options. Oper. Res., 52(6):856–867.

- Milevsky and Salisbury, (2006) Milevsky, M. A. and Salisbury, T. S. (2006). Financial valuation of guaranteed minimum withdrawal benefits. Insurance Math. Econom., 38(1):21–38.

- Øksendal, (2003) Øksendal, B. (2003). Stochastic differential equations. Universitext. Springer-Verlag, Berlin, sixth edition. An introduction with applications.

- Olver, (1974) Olver, F. W. (1974). Asymptotics and Special Functions. Academic Press, New York.

- Olver et al., (2010) Olver, F. W. J., Lozier, D. W., Boisvert, R. F., and Clark, C. W., editors (2010). NIST handbook of mathematical functions. U.S. Department of Commerce National Institute of Standards and Technology, Washington, DC.

- Prudnikov et al., (1986) Prudnikov, A. P., Brychkov, Y. A., and Marichev, O. I. (1986). Integrals and series. Vol. 2. Gordon & Breach Science Publishers, New York. Special functions, Translated from the Russian by N. M. Queen.

- Rogers and Williams, (2000) Rogers, L. C. G. and Williams, D. (2000). Diffusions, Markov processes, and martingales. Vol. 2. Cambridge Mathematical Library. Cambridge University Press, Cambridge. Itô calculus, Reprint of the second (1994) edition.

- Watson, (1944) Watson, G. N. (1944). A Treatise on the Theory of Bessel Functions. Cambridge University Press, Cambridge, England.

- Yor, (1992) Yor, M. (1992). On some exponential functionals of Brownian motion. Adv. in Appl. Probab., 24(3):509–531.

- (24) Yor, M. (2001a). Exponential Functionals of Brownian Motion and Related Processes. Springer-Verlag, Berlin.

- (25) Yor, M. (2001b). Further results on exponential functionals of brownian motion. In Yor, M., editor, Exponential Functionals of Brownian motion and related processes. Springer, Berlin.