Optimal stopping and control near boundaries

Abstract.

We will investigate the value and inactive region of optimal stopping and one-sided singular control problems by focusing on two fundamental ratios. We shall see that these ratios unambiguously characterize the solution, although usually only near boundaries. We will also study the well-known connection between these problems and find it to be a local property rather than a global one. The results are illustrated by a number of examples.

Key words and phrases:

Linear diffusion, Optimal stopping, Singular control2010 Mathematics Subject Classification:

62L15, 60G40, 60J60, 93E201. Introduction

We consider an optimal stopping problem

| (1) |

as well as a singular control problem

where and is an upper semicontinuous function and is understood as in [23]. Furthermore, the underlying process is a linear, time-homogeneous Itô diffusion on ; is a non-negative control process; and We will elaborate on these assumptions and notations in the sections to come.

1.1. Core of the study

We shall unambiguously determine the solution for these problems near the boundaries in quite a simple way. We will do this by focusing on two fundamental ratios. We use these ratios by embedding the Markovian methods and classical diffusion theory (see e.g. [35]) into the Beibel-Lerche method (see [8, 9]); for a similar approach, see also [9].

In the present study, the singular control case is especially interesting since one often has to solve control problems globally when applying the usual variational arguments (cf. [24]). However, we are able to find inactive regions and the value function locally, i.e. near the boundary, without having to consider the problem on the whole state space. Moreover, this is the first time, that the author is aware of, that the Beibel-Lerche -method is used in a singular control situation.

Another interesting finding concerns the renowned connection between one-sided singular control and optimal stopping problems (see e.g. [25, 26, 12]). We will construct the classical associated optimal stopping problem whose value is the derivative of the value of the given singular control problem. We will, however, show that this property only holds true locally, i.e. near the boundaries; as we operate on a level more general than is typical in the literature, this connection does not automatically hold on the whole space. We shall actually see an example where the value of a stopping problem can be the associated value for two different singular control problem on disjoint sets. Most interestingly, this means that we can interpret the renowned connection between the one-sided singular control and optimal stopping problem to be, in general, a local property rather than a global one. Moreover, we get an interesting necessary connection when this connection can hold on the whole state space.

1.2. Mathematical introduction

We are using the Markovian method utilising the classical diffusion theory. This technique is based on work [35], where it is applied for optimal stopping problems in a linear diffusion setting. Similar technique has been later applied in different situations e.g. in [3, 4, 30, 15]. We mix this Markovian method with the Beibel-Lerche method which is originally developed in [8, 9], and which is later refined e.g. in different problem settings in [31], and using jump processes in [6]. See also [19] for an analysis considering the relations between Beibel-Lerche and free boundary approaches. The power of the Beibel-Lerche method is in the fact that it can identify the continuation region with quite simple arguments in a general context.

Stopping problem

Consider the optimal stopping problem (1). Our study is strongly based on the ratios and , where and are the increasing and decreasing fundamental solutions of ODE , where is the infinitesimal generator of . The reason these ratios are used becomes clear after noticing that the stopping time , the first hitting time to a state , provides a value (see e.g. II.10 in [13])

The formulation above suggests that the ratios and could strongly dictate the behaviour of . Indeed, one aspect of the paper is to show that the global maximum points of these ratios allow us to write down explicitly the value function near the boundaries, the upper semicontinuity of being the only restricting requirement. The areas ”near the boundaries” that we are interested in are in fact the intervals and , where and are, respectively, the greatest and the smallest points that globally maximise and . In practice, this means that in every optimal stopping problem, as soon as one has found the global maximum points and , the problem is completely solved near the boundaries. We shall also prove that the two sets, where the ratio is increasing and where is decreasing belong to the continuation region. This is an observation that the author has not come across before.

Another aspect of the study is the following. From literature we know that under some weak assumptions , a hitting time to the set , is an optimal stopping time for (1) whenever a.s. (see e.g. Theorem 2.7 in [33]). Furthermore, we know (Theorem 2.4 in [33]) that for any stopping time that provides the value . However, there have not been too many examples where . In the present paper we offer such examples.

There are naturally also other studies concerning the fundamental ratios and , which is no surprise as they play central roles in solving (at least one-sided) optimal stopping problems. In [3] sufficient conditions are given under which the ratio has exactly one global maximum point, after which is decreasing, and it is shown that the value function is then unambiguously given everywhere. (The analogous result holds for the ratio .) Another direction is considered in [14], where it is shown that the points which maximise the ratio for some -excessive function are in the stopping region . This directly gives that the points that globally maximise and are in the stopping region . Furthermore, in an extensive study [29] on the optimal stopping of linear diffusions these ratios have also been inspected. In the aforementioned study (see also [17, 16]), the finiteness of the ratios and is linked to the finiteness of the value. Also, it is shown how these ratios agree on the boundaries to the ratios created by the value function. Additionally, in [17], and later in [16] in a more general setting, the optimal stopping time is characterised as a threshold rule relying on the ratios and on the boundaries.

Singular control problem and connection to stopping problem

Taking advantage of the close relations between optimal stopping and singular control problems we shall utilise similar techniques for singular control problems. We will show that the Beibel-Lerche based method also works in a (one-sided) singular control situation, where the ratios and dictate the value. Maintaining the harmony between a singular control and optimal stopping scene, we see that the solution to a singular control problem is unambiguously characterised on the intervals and , though we now need some additional assumptions on the underlying diffusion. Here and are, respectively, the greatest and the smallest point that globally maximises and .

It is a well known and greatly studied fact that a singular stochastic control problem has a close relationship with optimal stopping problems. The close connection between a one-sided singular control problem (i.e. either downward or upward control is allowed, but not both) and an optimal stopping problem was already present in the seminal paper by [5]. Later studies have shown it to hold in general (see [25, 26, 10]): For a one-sided singular control problem there exists an associated optimal stopping problem such that the derivative of the value of the one-sided singular control problem is the value of the associated optimal stopping problem.

This connection partially explains the -smooth fit condition for the value of a control problem (cf. e.g. [7]). Since the value of a stopping problem is often and is a derivative of the value of a control problem, we can interpret the -condition as an inherited condition from a smooth fit condition of a stopping problem.

This connection can also be generalised to concern two-sided singular control problems (i.e. both downward and upward controls are present). Interestingly, for a two-sided singular control problem there exists an associated Dynkin game, such that the derivative of the two-sided singular control problem constitutes the value of the associated Dynkin game (see [28] and [11]).

Also, a relation between a singular control problem and switching problem has been presented in [20, 21]. This connection states that the value of an singular control problem is also the value of an associated switching problem. Hence, interestingly, with sequential stopping the, somehow subordinate, derivative connection is converted to an equal connection. As a result, understandably, this connection has been identified as a ”missing link” between singular control problems and Dynkin games. In addition, there is a connection between Dynkin games and backward stochastic differential equations with two reflecting barriers (see [22]).

In our study we will link the two studied problems together by inspecting the well-known connection between the one-sided singular control problem and the optimal stopping problem on the intervals and . In the literature, one usually has sufficient assumptions to ensure that this connection holds everywhere. However, we find that operating on a general level, this connection does not necessarily hold on the whole space, only near the boundaries.

The contents of this study are as follows. In Section 2 we will present the definitions and the optimal stopping problem in detail. This is followed in Section 3 by our main results. These results are then illustrated by several short examples in Section 4. Sections 5 and 6 are devoted to the singular stochastic control and its relationship to optimal stopping problems.

2. Optimal stopping problem and definitions

Let be a regular linear diffusion defined on a filtered probability space , evolving on . The assumption that the state space is is done for reasons of convenience — It could be any interval on . We assume that is given as the solution of the Itô equation

| (2) |

where and are measurable mappings. We assume that for all there exists such that and satisfy the condition . This ensures that (2) has a unique weak solution (see e.g. Chapter V in [27]). We assume that the boundaries and are natural, exit, entrance, or killing (for a characterisation of boundaries, see e.g. Section II.1 in [13]). We understand that if the process hits an exit or a killing boundary, it is sent immediately to a cemetery state , where it stays for the rest of the time (cf. [18], Subsection 3.1). Consequently, boundaries cannot be used as stopping points for a diffusion in any circumstances.

We study an optimal stopping problem

| (3) |

where the supremum is taken over all -stopping times and is an upper semicontinuous reward function that attains positive values for some (if always, it is never optimal to stop). Notice that as and cannot be used as stopping points, is not necessarily defined on the boundaries and we further understand that . We denote by the continuation region and by the stopping region of the considered problem. Furthermore, we follow the notations of [33] and define optimal stopping time to be any stopping time at which the supremum (3) is attained.

Denote by and the increasing and decreasing fundamental solution to , where and is the infinitesimal generator of the diffusion. We will analyse the behaviour of the solution applying the functions and . To prepare this, we denote by

-

•

the set of global maximum points of and let be the maximal element of that set; and

-

•

the set of global maximum points of and let be the minimal element of that set.

For a boundary point we understand and , and we use analogous interpretation for . Especially we notice that with these interpretations , and that and can include and although is not necessarily defined on them. Moreover, by upper semicontinuity we have and . Further, also by upper semicontinuity, it is true that and for all and .

3. Optimal stopping near boundaries

The proofs for the results in this section are given only applying the ratio , as the proofs with the ratio are treated analogously with obvious changes.

3.1. Main results

Let us first show that there are possibly several stopping strategies that provide the values and .

Lemma 3.1.

-

(A)

Let , , and and let . Then the following stopping times yield the same value :

-

(i)

.

-

(ii)

.

-

(iii)

, for all .

-

(iv)

, where is any subset that contains .

-

(i)

-

(B)

Let , , and and let . Then the following stopping times yield the same value :

-

(i)

.

-

(ii)

.

-

(iii)

, for all .

-

(iv)

, where is any subset that contains .

-

(i)

Proof.

(A) (i), (ii) Since , we have for all

(iii) Let . Then the stopping rule gives a value (cf. Lemma 3.3 in [29])

Now we can calculate that

and thus

which is the same we got by using a stopping rule .

(iv) As a diffusion is continuous, we must have , where is the smallest point of such that , and is the greatest point of such that (if no such exist, then ). Consequently the claim follows from part (iii) (or (ii)) ∎

Let us state our main result, which is greatly inspired by Theorem 2 in [9].

Theorem 3.2.

-

(A)

For , the value function can be written as

(4) Moreover, is an optimal stopping time, where is any subset that contains . Lastly, , and .

-

(B)

For , the value function can be written as

(5) Moreover, is an optimal stopping time, where is any subset that contains . Lastly , and .

-

(C)

If , then there is no such that the admissible stopping time yields the value for all . Similarly if , then there is no such that the admissible stopping time yields the value for all .

Proof.

(A) Let . Then, for all a.s. finite stopping times , we have

By Lemma 3.1 this value is attained with a stopping rule , where is any subset containing , and thus the proposed is the value function.

Lastly, Theorem 2.1 in [14] says that a point is in the stopping set if and only if there exists a positive -harmonic function such that . This implies straightaway that .

(C) Let and suppose, contrary to our claim, that there exists such that is an optimal stopping time for . Then we have

for all . Since provides the maximum for , there exists such that , whence for all

which is contradicts the maximality of . ∎

Interestingly, if the set or contains more than one element, then by Theorem 3.2 there are several different optimal stopping times that provide the unique value function . Especially, the points of (and ) can now be interpreted as indifference points: For , the decision maker receives the same value irrespectively whether she uses stopping time , , , , or , where are any points for which . However, it is quite clear that is the smallest (a.s.) of all these stopping times (cf. Theorem 2.4 in [33]). In the sequel we wish to be unambiguous and thus we select to be our optimal stopping time on interval with a notion that there might also be others.

It should also be mentioned that the values and are crucial when investigating the optimality of a stopping time on the whole state space. This question has been treated quite comprehensively in [17, 16]. In addition, in Theorem 6.3(III) in [29] it is proven that provides the value function, where and are suitable chosen sequences such that , when . In our research this aspect is omitted, as the above mentioned analyses are quite exhaustive, and the present study does not bring any new insights to that subject.

3.2. Minor results

In short, Theorem 3.2 guarantees that if we can find the global maximum points of and , then the solution is unambiguously characterised near the boundaries. Usually the set contains only one element, but this is not always the case, as will be illustrated with examples in Section 4 below. The theorem also gives rise to a handful of corollaries, which shall be presented in this subsection (proofs are given in the Subsection 3.4). These corollaries are more or less straight consequences of Theorem 3.2 (and hence of Theorem 2 from [9]), but they have not been written out explicitly before.

Let us start with the ordering of and .

Corollary 3.3.

One has .

This means that the regions where the value is dictated by ratios and are always separated.

Let us then present an easy, but surprisingly powerful corollary.

Corollary 3.4.

The power of this corollary lies in the fact that if one can check somehow that , the value is immediately characterised near the boundary ; For example if or , then we know at once that . In this way Corollary 3.4 can be used to quicken the standard Beibel-Lerche method: If , we immediately know the solution without needing more closely inspection. This corollary is also related to corollaries 7.2 and 7.3 in [29], where it is shown how the value function looks like if we find out that and (and analogously for and ).

In the next two corollaries we will study more closely the situations that or include or .

Corollary 3.5.

If and , then one of the following is true.

-

(i)

It is optimal to stop immediately, i.e. and is -excessive.

-

(ii)

The optimal stopping rule is at least two-boundary rule (i.e. there are such that ).

-

(iii)

The optimal stopping time is not finite/admissible.

Corollary 3.6.

-

(A)

Let . Then for all , where . Especially, if , then .

-

(i)

If , then and there does not exist a finite stopping time that yields the value.

-

(ii)

If there is at least one other element in , then and, for all , the stopping time is optimal and admissible. For there does not exist an admissible stopping time that yields the value.

-

(i)

-

(B)

Let . Then , where . Especially, if , then .

-

(i)

If , then and there does not exist a finite stopping time that yields the value.

-

(ii)

If and there is at least one other element in , then and, for all , the stopping time is optimal. For there does not exist an admissible stopping time that yields the value.

-

(i)

We observe that the condition alone is not enough to guarantee that a stopping region is an empty set nor that a value cannot be attained with an admissible stopping time. Indeed, we will illustrate these cases below in Section 4. It is worth mentioning that the sufficient conditions in Corollary 3.6 for the value function to be infinite are known results (e.g. Theorem 1 in [9], Theorem 6.3(I) in [29], Proposition 5.10 in [17]).

Let us then show that if (or ) includes an interval, then must equal to a fundamental solution on it.

Lemma 3.7.

-

(A)

If an interval , then for all for some .

-

(B)

If an interval , then for all for some .

Proof.

(A) Since we know that for all . This in turns means that for some on . ∎

To end the subsection, we will show that using the ratios and we can also say something about the continuation region outside the set .

Lemma 3.8.

-

(A)

Denote by . Then .

-

(B)

Denote by . Then .

Proof.

(A) Let . Since is strictly increasing at , we can choose such that . Now, using a stopping time , we get

and so . ∎

Consider a reverse result: An interval is subset of , with , only if is increasing or is decreasing for some . If this would be true, then one could try to identify all the continuation regions using only ratios and . However, it is possible to construct an example where and and are decreasing and increasing, respectively, everywhere. In other words this reverse result is not true, and thus this approach cannot be used to get an alternative method for identifying continuation and stopping regions.

3.3. Extensions

3.3.1. Involving an integral

The problem setting can easily be extended to contain also an integral term. To that end, let be a measurable function such that , and let us consider a problem

Using a strong Markov property, this can be rewritten as (cf. (1.13) in [29])

where is the resolvent of , or a cumulative net present value of . We see at once that all the results above hold for this problem with obvious changes and with the sets and .

3.3.2. State dependent discounting

Another fairly straightforward extension can be made by introducing a discounting function: Instead of a constant , we can define to be a continuous function, which is bounded away from zero, whence is the cumulative discounting from now until a time . As the ODE has an increasing and a decreasing as its two independent solutions, we see that all the previous results hold in this case.

3.3.3. Other boundaries

Assume that the boundaries are either absorbing or reflecting and that is extended to be defined also on these boundaries.

For a reflecting boundary Lemma 3.1, Theorem 3.2(A),(B) and Corollary 3.6 can quite easily seen to hold as well as Lemmas 3.7 and 3.8. However, as the boundaries can now be used as stopping points, Theorem 3.2(C) is no longer valid (for an counterexample, see Example 7 in Section 4 below), nor are its corollaries.

The process is trapped in an absorbing boundary once it hits there, and so we have to take into account the positiveness of the reward function at the boundaries. If , it is not worthwhile to stop at the boundaries. Consequently, in this case, absorbing boundaries behaves as killing ones and all the preceding results are valid with absorbing boundaries.

However, if or is positive with absorbing boundaries, then the boundary points are always stopping points. This influences the analysis and consequently, of the introduced results, only Lemmas 3.7 and 3.8 hold true in the present formulation. (For a formulation of a value function near absorbing boundaries, see also Corollaries 7.2 and 7.3 in [29].)

3.4. Proofs to the corollaries

Proof of Corollary 3.3.

Suppose, contrary to our claim, that . Then for all , by Theorem 3.2, both and would give the value, i.e.

From this we get

But as is increasing and is decreasing, the ratio cannot be constant for all . ∎

Proof of Corollary 3.6.

(A) Since , we have . Clearly is an -excessive majorant of , and consequently a candidate for the value.

Let us create an increasing sequence such that , that the sequence is increasing, and that . Fix and let be such that for all . Then the sequence of values

is increasing for all . Moreover, for each there exists such that

Therefore is the limit of the increasing sequence of the values of the admissible stopping times , and thus it is the value.

(A) (i) The value reads as , but as cannot be used as a stopping point, this value cannot be reached by any finite stopping time.

(A) (ii) By Theorem 3.2, for all , provides the value. The rest follows from part (i). ∎

4. Examples

Let us illustrate the results with a geometric Brownian motion on . Now satisfies the stochastic differential equation

where and , and the boundaries are natural. The fundamental solutions are and , where is the positive root and the negative root of the characteristic equation

We shall demonstrate the results of Section 3 numerically by choosing , and , so that and .

Example 1.

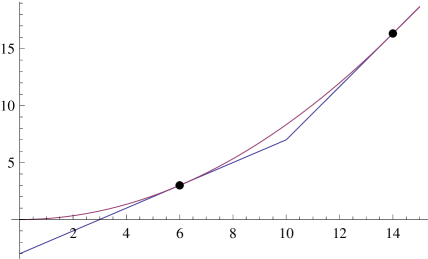

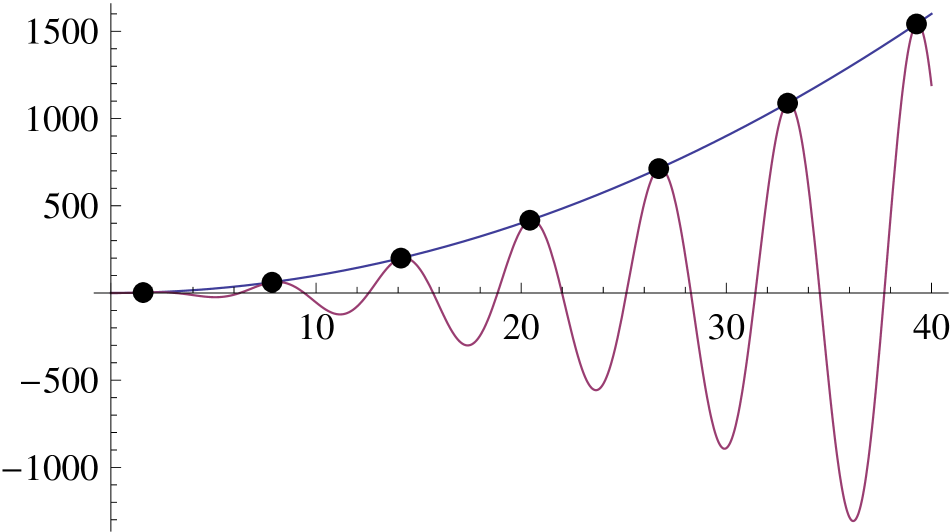

We will present a simple example, where have more than one point so that there are multiple different optimal stopping rules. By Theorem 3.2 this is true, if have at least two maximum points. To get such a function, choose

where and are chosen so that is continuous and that contains two points. With these choices , and for all (see Figure 1). For , the usually accepted optimal stopping time is , but also is optimal despite the fact that a.s.

Example 2.

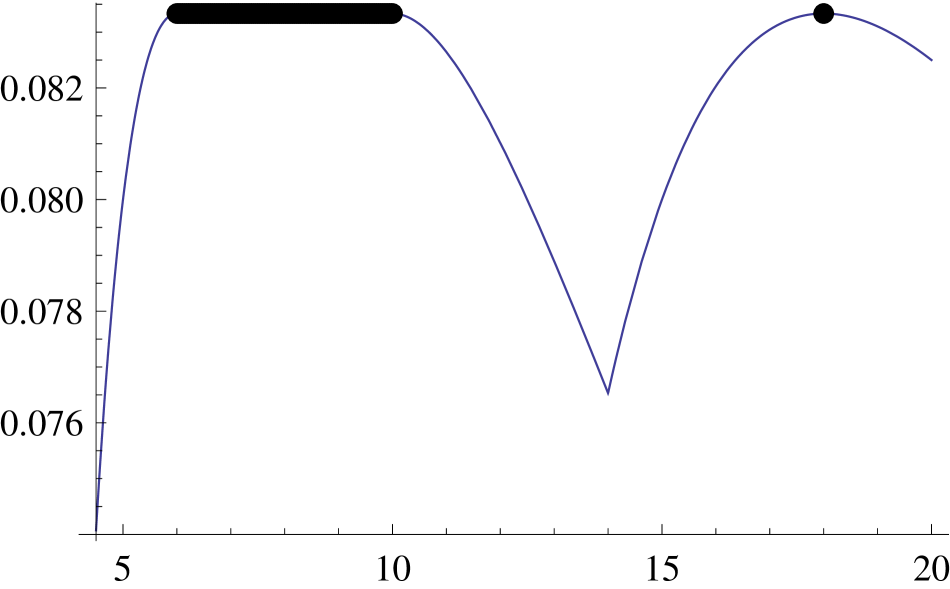

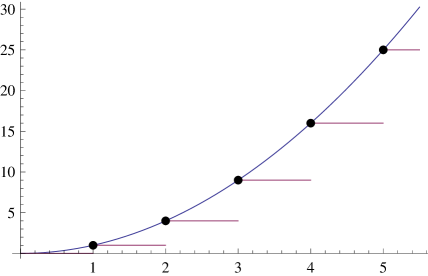

Extending the previous example, we now show that can be uncountable, so that there are uncountably many different optimal stopping rules. This is possible (by Theorem 3.2) if contains an interval, which by Lemma 3.7 means that for some on some interval. To that end, choose

With this choice, we can calculate that , and it is reached at the points , so that for all (see Figure 2). Further, by Theorem 3.2 for any stopping time , is optimal.

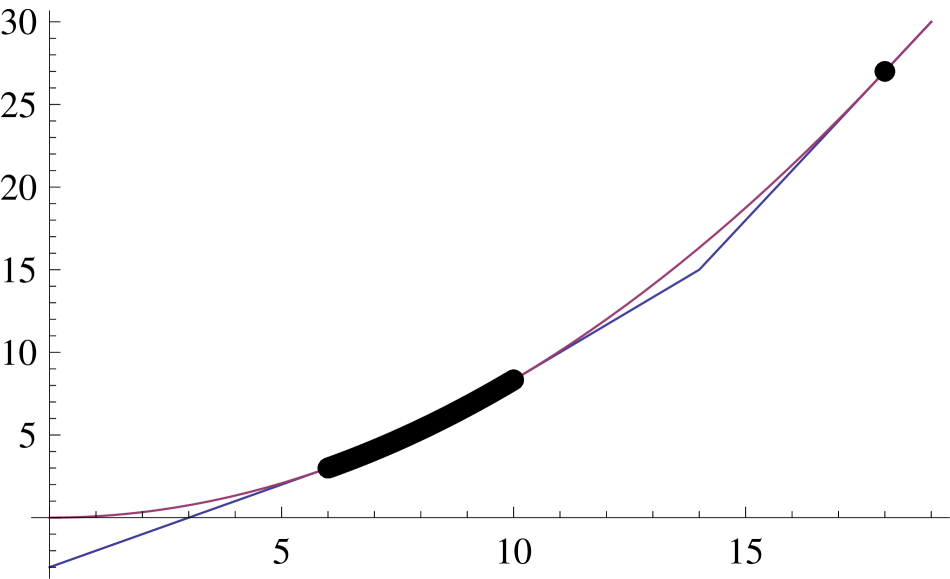

Example 3.

In this example we consider a case illustrating that can include , and that the value function is not attainable although the stopping set . Choose

where is chosen so that is continuous. Now we see that as , and so , and that the value function , for all , exists finitely. However, for there is no admissible stopping time that provides this value (see Figure 3(a)). Notice that for , is an optimal stopping time. Worth observing is that does not satisfy the integrability condition , a sufficient condition for the existence of a finite solution. For a similar example, see Example 8.2 in [29].

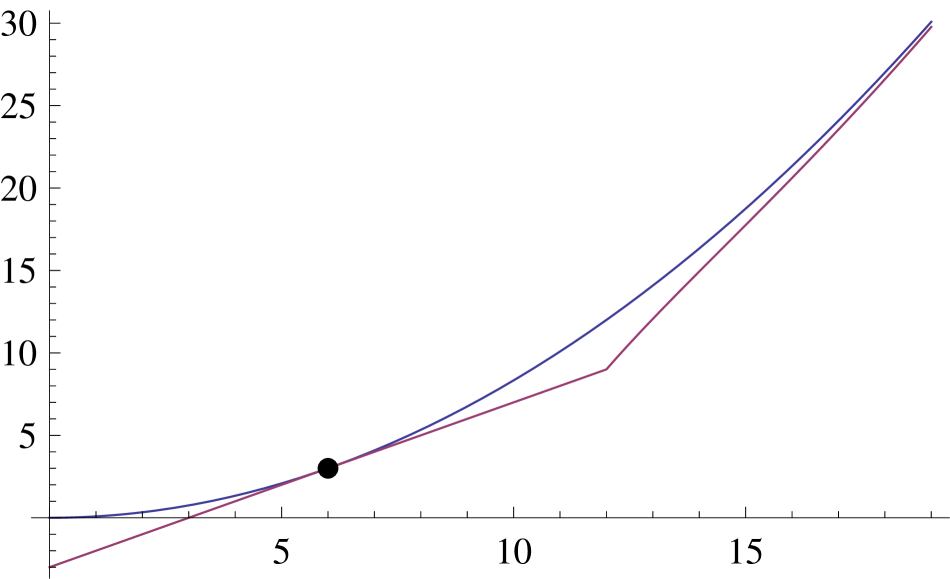

Example 4.

In this example we characterise a situation where and the value is nevertheless attained with a finite stopping time for all . To that end, let us choose

Now clearly , and thus , and . The value reads as for all and it is attained with a stopping time , which is finite a.s. (see Figure 3(b)). In fact, by Theorem 3.2, for each there are countably many finite stopping times that provide the value . Notice that the value is attainable, although, like in the previous example, the integrability condition does not hold in this one either.

Example 5.

From Corollary 3.3 we know that . Let us now illustrate that can equal to . For that end, let . Now , , , and consequently .

Example 6.

In this example we show that if a boundary point can be used as a stopping point, previous results do not necessarily hold. Let the state space be and let be a reflecting boundary. Let

Then is an upper semicontinuous function, , and . It can be easily seen that is an optimal stopping time. This differs from Theorem 3.2(C), which says that cannot provide optimal value for any for unattainable boundaries. Hence we see that as soon as a boundary can be used as a stopping point, Theorem 3.2(C) does not necessarily hold.

Example 7.

Here we will study more closely the subtle issue about a continuation region and an optimal stopping time. Assume that . Then by Theorem 3.2(C) we know that is not an optimal stopping time for any . From this one could wrongly conclude that for some . However, contrary to this belief, we will illustrate that for some we can actually have , in spite of the fact that is not an optimal stopping time.

Let

where we have chosen so that . It is easy to check that and implying that and . Then by Theorem 3.2(C) we know that is not an optimal stopping time for any . However, it can be proven that (cf. Theorem 6.3(III) and Corollary 7.2 in [29]), for say,

which is maximized with . Thus . In other words, for we have so that . Moreover, the time provides the value , but now is not an admissible stopping time.

We could have also used Lemma 3.8 to prove the point: Now is strictly decreasing on , meaning that .

Example 8.

In all the preceding examples we have had for all . Here we will show that actually we do not need smooth fit in order to apply Theorem 3.2. To that end, let us take

to be a step function, which is an upper semicontinuous function. In this case, , and . Moreover, now for all , but unlike in the preceding examples the smooth fit does not hold in this case. See Figure 4 for an illustration.

5. Singular control problem

In this section we shall show that the principles behind Beibel-Lerche -method can be used in a singular control situation resulting in conclusions similar to the ones in the previous sections. Moreover, this is the first time, that the author is aware of, that the Beibel-Lerche -method is used in a singular control situation.

5.1. Definitions

Let us now consider a controlled diffusion

on , where and are as previously and is non-negative, non-decreasing, right-continuous, and -adapted process. Consequently any admissible control has finite variation. An arbitrary control can be composed as , where is the continuous part and is the jump part of the control at time .

Let be as previously and let us study a singular control problem

| (6) |

Here we understand (in the spirit of e.g. [23])

If exits the state space at time , we understand for all . In this problem setting, we understand an optimal control to be any control that produces the value . We denote by and the inaction region and action region, respectively, of an optimal control. Furthermore, we denote by the set of global maximum points of and let be the maximal element of that set. Moreover, we denote by the control of reflecting downwards at the threshold . It is known that, for , the value applying can be written as (see e.g. discussion below Lemma 3.1 in [32]).

To end this introductory subsection, let us present an auxiliary lemma, which is a consequence of Itô’s Lemma (cf. Lemma 3.1 from [32]).

Lemma 5.1.

Let be a twice continuously differentiable function such that is bounded on for some . Let be an arbitrary admissible control such that is bounded. Then

Proof.

Let us apply (generalised) Itô’s lemma to a mapping to get

| (7) |

where is a local martingale (e.g. Theorem IV.30.7 in [34]). The boundedness of implies that also is bounded so that . Moreover, the boundedness of together with the fact that is bounded near , implies that . Therefore, the claim follows by taking expectation of both sides in (7) and letting . ∎

5.2. The main results

A use of a control results into a value , which clearly resembles the value of a one-sided optimal stopping problem, only now we have a ratio instead of . Hence it is no surprise that the analysis of a singular control problem follows more or less analogous path to that of an optimal stopping problem.

Lemma 5.2.

Assume that and let , , and and let . Then the following controls yield the same value :

-

(i)

Control .

-

(ii)

Control .

-

(iii)

If , wait until hits either or and then reflect downwards at a threshold it hits first. (I.e. wait time and then reflect downwards at a threshold .)

-

(iv)

Wait until enters the set , where where is any subset that contains , and use downward control with a reflecting threshold .

Proof.

(i), (ii) Since , we have, for ,

(iii) Let . The proposed control gives value

As , we see straight that the coefficient of vanishes, and further that the last term can be written as

(iv) As a diffusion is continuous, we must have , where be the smallest point of such that , and is the greatest point of such that (if no such exist, then ). Consequently the claim follows from item (iii) (or (ii)) ∎

Let us state our main result. This utilises Lemma 5.1, and hence we shall make the following assumption.

Assumption 5.3.

Assume that is bounded on for some and let us consider only controls such that is bounded from above.

Theorem 5.4.

- (A)

-

(B)

If , then there is no threshold such that a downwards reflecting control would yield the maximal value for .

Proof.

(A) Let and let be an arbitrary admissible control such that is bounded from above. Then we have

where the last equality follows from Lemma 5.1. For this value is attained by applying a reflecting control , and so the proposed is the value function. Furthermore, any control from Lemma 5.2 produces this maximal value.

(B) Let and suppose, contrary to our claim, that there exists such that, for , a singular control provides the maximal value, so that . Since is the maximum for , there exists such that , whence for all

contradicting the maximality of . ∎

The most noteworthy fact is that the Beibel-Lerche -approach allows us to construct a value for a control problem locally, whereas usually, applying variational inequalities, one needs global information in order to solve a problem.

Furthermore, we see that the optimal control is not uniquely determined if has at least two members. In fact we could use following kind of control: Choose to be an arbitrary sequence of subsets of that includes . In the first step wait time and then reflect downwards at until . In the second step wait time and then reflect downwards at until , etc. This control also leads to a value .

However, in the sequel we wish to be unambiguous, and consistent with the optimal stopping scene, and hence we select to be our optimal action region on interval with a notion that there might also be others.

5.3. Minor results

Similar to optimal stopping scheme, the main theorem gives handful of corollaries in singular control case .

If or , then and we can directly apply the following corollary.

Corollary 5.5.

Let Assumption 5.3 hold. If , then and the value reads as for .

Proof.

Straight consequence of Theorem 5.4. ∎

The special cases that or is contained in are handled in the following two corollaries.

Corollary 5.6.

Let .

-

(A)

One can never use control , i.e. one cannot reflect downwards at .

-

(B)

If , then one of the following is true.

-

(i)

It is optimal to drive the process instantaneously (i.e. infinitely fast) to the boundary , whence .

-

(ii)

There exists such that and .

-

(iii)

The optimal control is something else than an admissible reflecting control satisfying Assumption 5.3.

-

(i)

Proof.

(A) If is unattainable, it is never attained at a finite time and thus cannot be used as a control. If is attainable (i.e. exit or killing), then the process is terminated immediately at , before is activated, and thus cannot be used.

(B) Straight consequence of Theorem 5.4. ∎

Corollary 5.7.

Let Assumption 5.3 hold and assume that . Then for all , where . Especially, if , then . Moreover,

-

(i)

if , then and there is no admissible optimal control;

-

(ii)

if there is at least one other element in , then there exists an admissible optimal control for and no admissible optimal control for , and .

Proof.

Let . Using the arguments from the proof of Theorem 5.4, we known that for all admissible controls under Assumption 5.3 it is true that

Since , we can choose an increasing sequence , such that , is increasing, and . Then a sequence of controls gives an increasing sequence of values . As this converges to , it must be the maximal value.

(i) If is unattainable, then it is never reached and there is no control that provides the optimal value . If is attainable (i.e. exit or killing), then the process is terminated immediately at before a control is activated.

(ii) Straight consequence from Theorem 5.4 and part (i). ∎

Notice that by Corollary 5.7 the condition alone is not enough to guarantee that the value cannot be attained with an admissible control, while condition is enough.

Lemma 5.8.

If an interval , then for all for some .

Proof.

Since we know that for all . This in turns means that for some on . ∎

5.4. Differences to optimal stopping

The main difference to the optimal stopping case is the fact that in the singular control problem (6) only the ratio has meaning; the ratio leads to values that cannot be attained with downward control. It should be mentioned that this cannot be fixed easily by adding an upward control to the problem. This is because when both downward and upward controls are present, the solution can rarely be identified with a one-sided control, and as a consequence the analysis of the simple ratios and is not adequate.

We also notice that we found more corollaries in the optimal stopping scene. This can be seen due to a rather simple local characterisation of stopping regions/continuation regions in optimal stopping problems: is in the continuation region whenever . On the other hand, in control problems action regions/inaction regions are rarely found locally; More often than not, they are found globally applying variational inequalities. Most noticeably this is seen in the fact that in the control scene the set is not necessarily part of the inaction region, as we shall see in Example 10.

5.5. Extensions

We can easily extend the results from this section to concern also a running payoff case. To that end let be once continuously differentiable function for which , and let us study a problem

| (9) |

As the resolvent solves the ordinary differential equation , a straight consequence of Lemma 5.1 is that

Hence the problem (9) can be re-written as

provided that the conditions of Lemma 5.1 are satisfied.

It follows at once that all the results from this section hold for this problem with obvious changes and with the set .

5.6. Controlling upwards

Until now we have only controlled the diffusion downwards. Let us now introduce an upward control defining

on , where and are as previously and is a non-negative, non-decreasing, right-continuous, and -adapted. For a function , defined as previously, we define a singular control problem

| (10) |

It is known that, for , the value applying , i.e. a control that reflects upwards at a threshold , can be written as (see e.g. discussion below Lemma 3.1 in [32]). It is now quite clear that all the results from this section hold true for the problem (10) near the upper boundary with obvious changes; Instead of we have , instead of we have , instead of we have , etc.

5.7. Examples

Let be as in Section 4, i.e. is a geometric Brownian motion for which and .

Example 9.

Here we show that both an impulse control and a singular control can yield the maximal value. Let

so that is continuous, increasing, , and . Consequently, by Theorem 5.4, for , a control (with ) provides the solution and the value reads as .

On the other hand, taking to be the action region, we get a control that coincides with an impulse control with and . That is, every time we hit the state , we jump to the state . It can be easily calculated that, for , this impulse control also results into a value .

Example 10.

In this example we will see that does not necessarily belong to the inaction region. Take

Now , and . However, it can be shown (cf. Lemma 1 in [1] for a verification result) that the action region is and that the optimal control is . In other words, contrary to what Lemma 3.8 from optimal stopping scene would suggest, the region do not necessary belong to the inaction region in singular control problems.

6. Connection between singular control and optimal stopping

6.1. Introducing the associated optimal stopping problem

In most studies analysing the connection between singular control and optimal stopping there are some growth, convexity, or positiveness restrictions on the payoff , or there are some restrictions for the diffusion process. These restrictions guarantee the connection to hold everywhere on the state space which is exactly what one usually needs or wants. However, in some sense something has gone unnoticed because of these restrictions: the renowned connection is not a global phenomenon. Here we will show that when we let the setting to be very general, the connection does not necessarily hold on the whole state space (Proposition 6.2 and Example 11).

To introduce the connection in the present case, let us consider control problems (6) and (10) and let , , , , , , and be as in the previous section.

Let us define an associated diffusion

and let us consider an optimal stopping problem

| (11) |

(The infinitesimal generator can be seen as a derivative of the operator .)

In the sequel we need to utilise the fact that the Laplace transform of , the hitting time to a state , with respect to a diffusion can be written as

| (12) |

It is quite clear that if and are convex, then their derivatives and are the non-negative increasing and decreasing fundamental solutions to . This in turn ensures that in the convex case condition (12) holds.

In the following we state sufficient conditions guaranteeing that the fundamental solutions and are convex.

Lemma 6.1.

-

(A)

Assume that a transversality condition holds and that for all . Further assume that either is unattainable or . Then is convex.

-

(B)

Assume that one or the other of the following hold.

-

(i)

for all ; or

-

(ii)

a transversality condition holds, is unattainable and for all .

Then is convex.

-

(i)

6.2. The connection between singular control and optimal stopping

Assuming that the condition (12) holds, we can straightforwardly apply Theorem 3.2 to the associated stopping problem (11) with the sets and . On the other hand, at the same time we can apply Theorem 5.4 to the control problems (6) and (10) with the sets and .

These facts give the following proposition, which is the celebrated connection between a singular control problem and the associated optimal stopping problem in our case.

Proposition 6.2.

We see that the associated stopping problem carries, potentially, more information than a single singular control problem; Although played no role in a downward controlled singular control problem, it has a well defined meaning in the associated stopping problem. This is illustrated in Example 11 below. Moreover, the proposition reveals that there is no guarantee, a priori, that we can connect a one-sided singular control problem to its associated stopping problem on the whole state space. This observation gives us the following, quite interesting, necessary condition under which this connection can hold everywhere.

Corollary 6.3.

Proof.

(A) By Proposition 6.2 we have , for all . As the value cannot be reached by applying a downward control, we can have for all only if . Part (B) follows analogously. ∎

6.3. When fundamental solutions can be concave

Earlier we have seen that the Laplace transform of the hitting time in (12) holds if and were convex. Here we generalise this to a case where and are concave near the boundaries.

The following theorem (Theorem 1 in [3]) reveals that the fundamental solutions are concave near the boundaries, if there.

Theorem 6.4.

Assume that the transversality condition holds and that and are unattainable. Then for all

where .

The following sums up the Laplace transform of the hitting time in this concave case.

Lemma 6.5.

-

(A)

Assume that the transversality condition holds and that is unattainable for a diffusion . Further, assume that there exists such that for all (it may be negative also elsewhere). Let and . Then

where is the first hitting time to a state .

-

(B)

Assume that the transversality condition holds and that is unattainable for a diffusion . Further, assume that there exists such that for all (it may be negative also elsewhere). Let and . Then

where is the first hitting time to a state .

Proof.

The proof follows quite closely that of Theorem 9 in [2].

(A) Now , where is the scale derivative of the process . Because of this, we see that the ratio is increasing. Moreover, as and are two independent solutions to , any solution to it can be expressed as for some . It is now an easy exercise in linear algebra to demonstrate that if , then

| (13) |

where is the first exit time of from an open interval . Invoking the alleged boundary conditions of implies that

Consider now the first term on the right hand side of (13). We want to show that it convergences to as approaches . To that end, we firstly notice that it can be written as

where the inequality follows from the fact that is increasing and . Secondly, from Theorem 6.4 we see at once that is concave on , whence we can approximate

Letting and invoking again the alleged boundary conditions of we get

indicating that the first term on the right hand side of (13) tends to zero as tends to zero. Consequently

(B) Proof is analogous to the part(A). ∎

6.4. Examples

Again, let be a geometric Brownian motion for which and . Let us present perhaps the most striking example of the paper.

Example 11.

In this example we will illustrate that the associated stopping problem can be associated problem to a two different singular control problem at the same time. Let

It is quite straightforward to show that

Moreover, now and . Thus we can say that for we have and . (Actually, applying Theorem 1 from [1], we can say that is the optimal control on and that for .)

On the other hand, now we also have with , so that and for . (Again we can prove that, for , .)

It follows that the value of the associated optimal stopping problem is, in fact, the associated value function for two different singular control problems on separate regions and :

This means that the connection between the one-sided singular control and optimal stopping problem is in general a local property rather than global.

Acknowledgements.

The author is grateful to Professor L.H.R. Alvarez for helpful conversations and valuable comments during the research. The author would also like to thank Professor M. Zervos for pointing out Example 6. Lastly, S. Christensen is acknowledged for his helpful comments on the contents of the earlier draft of the paper.

References

- [1] L. H. R. Alvarez, Singular stochastic control in the presence of a state-dependent yield structure, Stochastic Process. Appl. 86 (2000), no. 2, 323–343.

- [2] by same author, Singular stochastic control, linear diffusions, and optimal stopping: A class of solvable problems, SIAM Journal on Control and Optimization 39 (2001), 1697–1710.

- [3] by same author, On the properties of -excessive mappings for a class of diffusions, The Annals of Applied Probability 13 (2003), 1517–1533.

- [4] L. H. R. Alvarez and T. A. Rakkolainen, On singular stochastic control and optimal stopping of spectrally negative jump diffusions, Stochastics 81 (2009), no. 1, 55–78.

- [5] J. A. Bather and H. Chernoff, Sequential decisions in the control of a spaceship, Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability 3 (1966), 181–207.

- [6] E. J. Baurdoux, Examples of optimal stopping via measure transformation for processes with one-sided jumps, Stochastics 79 (2007), no. 3-4, 303–307.

- [7] E. Bayraktar and M. Egami, An analysis of monotone follower problems for diffusion processes, Mathematics of Operations Research 33 (2008), 336–350.

- [8] M. Beibel and H. R. Lerche, A new look at warrant pricing and related optimal stopping problems. empirical bayes, sequential analysis and related topics in statics and probability, Statistica Sinica 7 (1997), 93–108.

- [9] by same author, A note on optimal stopping of regular diffusions under random discounting, Rossiĭskaya Akademiya Nauk. Teoriya Veroyatnosteĭ i ee Primeneniya 45 (2000), no. 4, 657–669.

- [10] F. E. Benth and K. Reikvam, A connection between singular stochastic control and optimal stopping, Appl. Math. Optim. 49 (2004), no. 1, 27–41.

- [11] F. Boetius, Bounded variation singular stochastic control and Dynkin game, SIAM Journal on Control and Optimization 44 (2005), no. 4, 1289–1321.

- [12] F. Boetius and M. Kohlmann, Connections between optimal stopping and singular stochastic control, Stochastic Processes and their Applications 77 (1998), no. 2, 253–281.

- [13] A. Borodin and P. Salminen, Handbook of brownian motion - facts and formulae, Birkhauser, Basel, 2002.

- [14] S. Christensen and A. Irle, A harmonic function technique for the optimal stopping of diffusions, Stochastics 83 (2011), no. 4-6, 347–363.

- [15] F. Crocce and E. Mordecki, Explicit solutions in one-sided optimal stopping problems for one-dimensional diffusions, Stochastics 86 (2014), no. 3, 491–509.

- [16] S. Dayanik, Optimal stopping of linear diffusions with random discounting, Mathematics of Operations Research 33 (2008), no. 3, 645–661.

- [17] S. Dayanik and I. Karatzas, On the optimal stopping problem for one-dimensional diffusions, Stochastic Processes and their Applications 107 (2003), 173–212.

- [18] E. B. Dynkin, Markov processes. Vols. I & II, Springer-Verlag, 1965.

- [19] P. V. Gapeev and H. R. Lerche, On the structure of discounted optimal stopping problems for one-dimensional diffusions, Stochastics 83 (2011), no. 4-6, 537–554.

- [20] X. Guo and P. Tomecek, A class of singular control problems and the smooth fit principle, SIAM Journal on Control and Optimization 47 (2008), 3076–3099.

- [21] by same author, Connections between singular control and optimal switching, SIAM Journal on Control and Optimization 47 (2008), 421–443.

- [22] S. Hamadène and M. Hassani, BSDEs with two reflecting barriers driven by a Brownian and a Poisson noise and related Dynkin game, Electronic Journal of Probability 11 (2006), no. 5, 121–145.

- [23] A. Jack, T. C. Johnson, and M. Zervos, A singular control model with application to the goodwill problem, Stochastic Processes and their Applications 118 (2008), no. 11, 2098–2124.

- [24] I. Karatzas, A class of singular stochastic control problems, Advances in Applied Probability 15 (1983), no. 2, 225–254.

- [25] I. Karatzas and S. E. Shreve, Connections between optimal stopping and singular stochastic control I. Monotone follower problems, SIAM Journal on Control and Optimization 22 (1984), no. 6, 856–877.

- [26] by same author, Connections between optimal stopping and singular stochastic control II. Reflected follower problems, SIAM Journal on Control and Optimization 23 (1985), no. 3, 433–451.

- [27] I. Karatzas and S. E. Shreve, Brownian motion and stochastic calculus, Springer-Verlag New York, 1988.

- [28] I. Karatzas and H. Wang, Connections between bounded-variation control and Dynkin games, Optimal Control and Partial Differential Equations; Volume in Honor of Professor Alain Bensoussan’s 60th Birthday (J. L. Menaldi, A. Sulem, and E. Rofman, eds.), IOS Press, Amsterdam, 2001, pp. 353–362.

- [29] D. Lamberton and M. Zervos, On the optimal stopping of a one-dimensional diffusion, Electronic Journal of Probability 18 (2013), 1–49.

- [30] J. Lempa, A note on optimal stopping of diffusions with a two-sided optimal rule, Operations Research Letters 38 (2010), 11–16.

- [31] H.R. Lerche and M. Urusov, Optimal stopping via measure transformation: the beibel-lerche approach, Stochastics 79 (2007), 275–291.

- [32] P. Matomäki, On solvability of a two-sided singular control problem, Mathematical Methods of Operations Research 76 (2012), no. 3, 239–271.

- [33] G. Peskir and A. Shiryaev, Optimal stopping and free-boundary problems, Lectures in Mathematics ETH Zürich, Birkhäuser Verlag, Basel, 2006.

- [34] L. C. G. Rogers and D. Williams, Diffusions, Markov processes, and martingales. Vol. 2, Cambridge Mathematical Library, Cambridge University Press, 2000.

- [35] P. Salminen, Optimal stopping of one-dimensional diffusions, Mathematische Nachrichten 124 (1985), 85–101.