Games of singular control and stopping driven by spectrally one-sided LÉVY processes

Abstract.

We study a zero-sum game where the evolution of a spectrally one-sided Lévy process is modified by a singular controller and is terminated by the stopper. The singular controller minimizes the expected values of running, controlling and terminal costs while the stopper maximizes them. Using fluctuation theory and scale functions, we derive a saddle point and the value function of the game. Numerical examples under phase-type Lévy processes are also given.

Keywords: controller-and-stopper games; Lévy processes; scale functions; continuous and smooth fit

Mathematics Subject Classification (2010): 91A15, 60G40, 60G51, 93E20

1. Introduction

We study the Lévy model of the zero-sum game between a singular controller and a stopper in the framework of Hernández-Hernández et al. [19]. Based on the information provided by a given Lévy process , the controller modifies the evolution of while the stopper decides to terminate the game. More precisely, the former chooses a nondecreasing control process so as to minimize the expected costs that depend on the path of the controlled process while the latter chooses a stopping time to maximize them. The costs consist of the running cost , the controlling cost as well as the terminal cost . The objective is to identify a pair of strategies that constitute a saddle point (Nash equilibrium).

Games of singular control and stopping arise in problems where both players are interested in maintaining the state of the system in some region. Applications of the problem studied here include the following example adapted from the monotone follower problems (see, e.g., [20]): if the process represents a random demand of some specific good, the controller wants to prevent the lack of the product, while the stopper wants to prevent excess of inventory. Here, the process can represent the amount of accumulated capital needed to meet the demand. Other applications in the field of finance and insurance can be found in, among others, [22] and [9].

Another potential application lies in robust control, where the decision maker wants to optimize the worst case expectation when there is an ambiguity in the model specification. One way to model this is to include a “malevolent second agent”, who acts adversely to the decision maker (see the introduction of Hansen et al. [18]). This reduces to solving the two-player zero-sum game. In the light of our problem, it can be seen as a robust optimization of a singular controller when there is an ambiguity in the time-horizon; this can also be seen as a robust optimal stopping problem in the existence of misspecification of the underlying process. Regarding this matter, we refer the readers to, among others, [17, 18] for the robust control problems written in terms of games.

The version of the controller-stopper problem this paper is focusing on was first studied by [19] where they focus on a one-dimensional diffusion model. They derived a set of variational inequalities that fully characterize the saddle point and the associated value function. They also gave examples that admit explicit solutions. Although the variational inequalities and relevant theories of singular control and optimal stopping problems are well studied, when their games are considered, existing results are rather limited and there are very few cases that are known to be solved explicitly. For different formulations of the game between a controller and a stopper, we refer the reader to [29] and [21], and references therein. In the former they studied controller-stopper games in discrete time, while the latter considers the problem of optimally modifying the drift and diffusion coefficients of a Brownian motion using absolutely continuous controls. See also [13] for the solution of a singular optimal control problem with an arbitrary stopping time.

In this paper, we consider the aforementioned problem focusing on the case when is a spectrally one-sided (spectrally negative or positive) Lévy process. Without the continuity of paths, the problem naturally tends to be more challenging because one needs to take into account the overshoots when the process up-crosses or down-crosses a given barrier. Nonetheless, by taking advantage of the recent advances in the theory of Lévy processes, this can be handled for spectrally one-sided Lévy processes using so-called scale functions. We show, under appropriate conditions on the functions and , that a saddle point and the associated value function can be identified.

In order to achieve our goals, we take the following steps:

-

(1)

We first conjecture that the optimal strategies are of barrier-type; namely, the controlled process and the stopping time at equilibrium are a reflected Lévy process and a first up/down-crossing time of a certain level, respectively. By focusing on the set of these strategies, the associated expected cost functional is written in terms of the scale function.

-

(2)

We then identify the reflection-trigger level as well as the stopping-trigger level by using the continuous/smooth fit principle. Namely, the values of are chosen so that the corresponding expected cost functional is continuous (and/or smooth) at and simultaneously. The smoothness of the resulting value functions differ according to the path variation of and whether a spectrally negative or positive Lévy process is considered.

-

(3)

We finally verify the optimality of the candidate value function by showing that it satisfies the variational inequality and that it is indeed a sufficient condition for optimality.

These steps in the above solution methods are motivated by recent papers on optimal stopping/control problems for spectrally one-sided Lévy processes. In these papers, the scale function is commonly used as a proxy to the underlying process so as to write efficiently the expected cost corresponding to a barrier strategy. The optimal barrier is then determined by the continuous/smooth fit condition together with the known continuity/smoothness property of the scale function that differs according to the path variation of the process. The verification of optimality is carried out by the martingale (harmonic) property of the scale function. These methods avoid the use of techniques of integro partial differential equations (IPDEs) to prove existence and smoothness of the solution of the associated HJB equation; this tends to be hard to solve except for special cases (e.g. when the process has i.i.d. exponential jumps). For papers regarding spectrally one-sided Lévy processes and their applications, we refer the reader to, among others, [2, 4, 27] for optimal stopping problems in finance, [5, 8, 25, 28] for singular control problems in insurance, and [6, 7, 14] for optimal stopping games. To our best knowledge, this paper is the first attempt to solve the game between a controller and a stopper for spectrally one-sided Lévy processes.

We take advantage of the fluctuation theory and scale function for spectrally negative and spectrally positive Lévy cases. However these two cases are analyzed separately in different sections because the behavior of these processes is indeed significantly different. We require different assumptions and in addition the smoothness of the derived value function is different. There also is an interesting difference that while can happen for the spectrally positive Lévy case, it cannot happen for the spectrally negative Lévy case. This is caused due to the fact that while the lower boundary of an open set is regular (see Definition 6.4 of [24]) for a spectrally negative Lévy process, it is not so for the case of a spectrally positive Lévy process when it has paths of bounded variation; we discuss more in detail in Remark 5.3 below. It should be remarked that there also is a similarity, for example, in that for both cases the value function becomes convex.

The derived saddle point and the associated value function are expressed in terms of the scale function for both the spectrally negative and positive cases. Hence, computing these values reduce to computing the scale function. In general, this cannot be done explicitly, but there are numerical procedures that allow one to approximate them, for example, by Laplace inversion [23, 32] or by phase-type fitting [16]. In this paper, we use the latter and illustrate how the values of and the value function can be computed. We also show the impact of the parameters that describe the functions and on the value function.

The rest of the paper is organized as follows. In Section 2, we give a mathematical formulation of the game. In Section 3, we review the spectrally one-sided Lévy process and its scale function. In Sections 4 and 5, respectively, using the method described above, the spectrally negative and positive formulation is solved. In Section 6, we give numerical results for both the spectrally negative and positive cases. Throughout the paper, superscripts and are used to indicate the right and left limits, respectively. The subscripts and are used to indicate positive and negative parts.

2. Model and problem formulation

Let be a probability space hosting a Lévy process . Let be the conditional probability under which (also let ), and let be the filtration generated by . We denote by the completed filtration of with the -null sets of .

The games analyzed in this paper consist of two players. The controller chooses a process , where denotes the set of nondecreasing and right-continuous -adapted processes with , while the stopper chooses the time among the set of -stopping times . The controller minimizes and the stopper maximizes the common performance criterion:

where is a right-continuous controlled process defined by

The problem is to show the existence of a saddle point, or equivalently a Nash equilibrium , such that is the best response given while at the same time is the best response given .

More precisely, we shall show under a suitable condition that a saddle point is given by a pair of barrier strategies for some , where we define

| (2.1) | ||||

In this case, the controlled process is a reflected Lévy process, whose fluctuation theory has been studied in, for example, [5, 30]; see Figures 1 and 2 below for its sample paths when is a spectrally one-sided Lévy process. The corresponding performance criterion reduces to

| (2.2) |

The objective is to show, upon appropriate choices of and ,

| (2.3) |

for any and for any , where we define .

Intuitively, for such strategies to be a saddle point, it is suggested that decreases while increases, or more generally decreases faster than decreases. See Assumptions 4.1 and 5.2 below for the assumptions we make for the spectrally negative and positive case, respectively.

In addition, we need to choose the slope of carefully in view of the controlling cost derived by as well. Throughout the paper we assume that is affine and its slope is larger than due to the reason described below.

Assumption 2.1.

We assume that , , for some and .

Our formulation considers the case the controller has the first move advantage in that the stopper can stop only after the controller modifies the process at any time . As is studied in [19], we can also consider a version where the stopper has the first move advantage, and in general these two formulations are not equivalent. Under Assumption 2.1, however, these are equivalent in our case. Indeed, at when the controller modifies the process by units, the difference of payoffs between stopping immediately after and stopping immediately before is

which is greater than zero by Assumption 2.1.

For the rest of the paper, we assume that has a finite first moment, so that the problem is well defined and nontrivial.

Assumption 2.2.

We assume that , where we define

| (2.4) |

3. Spectrally one-sided Lévy processes and scale functions

In this section, we review the spectrally negative Lévy process and its scale function, which will be used to express fluctuation identities for Section 4. The spectrally positive Lévy process is its dual and hence the scale function is again used analogously for our discussion in Section 5.

Let be a spectrally negative Lévy process whose Laplace exponent is given by

| (3.1) |

where is a Lévy measure with the support that satisfies the integrability condition . It has paths of bounded variation if and only if and ; in this case, we write (3.1) as

with . We exclude the case in which is a subordinator (i.e., has monotone paths a.s.). This assumption implies that when is of bounded variation. The first moment of in (2.4) is , which is assumed to be finite by Assumption 2.2.

3.1. Scale functions

Fix , as the discount factor in the definition of . For any spectrally negative Lévy process, there exists a function called the q-scale function

which is zero on , continuous and strictly increasing on , and is characterized by the Laplace transform:

where

Here, the Laplace exponent in (3.1) is known to be zero at the origin and convex on ; therefore is well defined and is strictly positive as . We also define, for ,

In particular, because is zero on the negative half line, we have

| (3.2) |

Let us define the first down- and up-crossing times, respectively, of by

| (3.3) |

Then, for any and ,

| (3.4) | ||||

Fix and define as the Laplace exponent of under with the change of measure

see page 213 of [24]. The process remains to be a spectrally negative Lévy process under this measure. Suppose and are the scale functions associated with under (or equivalently with ). Then, by Lemma 8.4 of [24], , , which is well defined even for as in Lemmas 8.3 and 8.5 of [24]. In particular, we define

which is increasing as it is the scale function of under .

Important properties of the functions defined above are summarized next, in terms of the path variation of the process .

Remark 3.1.

-

(1)

If either is of unbounded variation or the Lévy measure is atomless, it is known that is ; see, e.g., [12]. Hence,

-

(a)

is and for the bounded variation case, while it is and for the unbounded variation case, and

-

(b)

is and for the bounded variation case, while it is and for the unbounded variation case.

-

(a)

- (2)

- (3)

4. Spectrally negative Lévy case

In this section, we assume that is a spectrally negative Lévy process as defined in the last section, and obtain a saddle point (2.3). In addition to Assumptions 2.1 and 2.2 above, we require additional conditions on the running cost function , which are imposed solely in this section. We define

| (4.1) |

where is the discount factor we use in the performance criterion .

Assumption 4.1.

We assume that (and ) are continuously differentiable with absolutely continuous first derivatives and

-

(1)

for all ;

-

(2)

on for some and ;

-

(3)

on for some and .

The monotonicity of is justified in various settings. For example, in the inventory example discussed in the introduction, the controller and the stopper try to avoid shortage and excess, respectively, and hence the running reward function needs to be decreasing. When robust control is considered, there are many applications where the higher value of a controlled process is more desirable. Examples include, in addition to the classical inventory models, the equity to debt ratio the company needs to control (so as to meet the capital adequacy requirements). Similar monotone running reward function appears in insurance dividend problem with capital injection when a random independent exponential time horizon is introduced (see [1]).

Notice that Assumption 4.1(1) is slightly stronger than the condition that is decreasing, but the value of is typically a small number. This tilted version (4.1) of the running reward function is commonly used in singular/impulse control problems; see, e.g., [10, 11, 33]. Assumption 4.1(2,3), which require that it is strictly decreasing in the tail, are assumed for technical reasons where we take limits in the arguments below.

|

|

4.1. Write using scale functions

Recall the set of strategies defined as in (2.1). Our aim is to show that a saddle point is given in this form for appropriate choice of and .

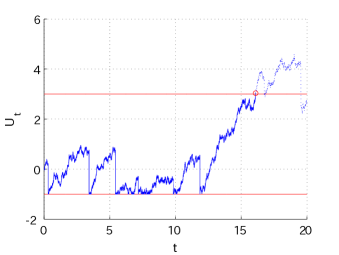

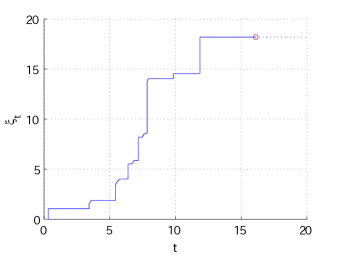

As an illustration, Figure 1 shows a sample path of the controlled process and its corresponding control process when is a spectrally negative Lévy process. In the figure, the controlled process is reflected at the lower boundary and is stopped at the first time it reaches the upper boundary . Due to the lack of positive jumps, the process necessarily creeps upward at (assuming it starts at a point lower than ). The process increases whenever the process touches or goes below the level . Due to the negative jumps, it can increase both continuously and discontinuously.

Our first task is to write the performance criterion as in (2.2) using scale functions. Because the controlled process is a reflected Lévy process, we can use its fluctuation theories developed by Pistorius [30] and Avram et al. [5]. Define, for any measurable function ,

| (4.2) |

Here for any because is zero on . We also define

Lemma 4.1.

For any ,

| (4.3) | ||||

For , we have , while for the equality holds.

4.2. Smooth fit

Now we shall choose the values of and so that the function is smooth. We will see that such desired pair satisfies some conditions that are characterized efficiently by the two functions:

| (4.4) | ||||

and its derivative with respect to the second argument,

| (4.5) |

Here we used that

| (4.6) |

which holds because by integration by parts.

Proposition 4.1.

Suppose are such that . Then

-

(1)

is differentiable (resp. twice-differentiable) at when is of bounded (resp. unbounded) variation;

-

(2)

is differentiable at for all cases.

We shall prove this proposition by a straightforward differentiation and the asymptotic property of the scale function near zero as in Remark 3.1(2).

First, taking derivatives in (4.3), for ,

| (4.7) | ||||

where we assume is of unbounded variation for the latter. Here and can be written, respectively, by (4.6) and

On the other hand,

Sending in (4.8),

In addition, for the unbounded variation case, by (4.9),

By Remark 3.1(2), if are such that , then is differentiable (resp. twice-differentiable) at when is of bounded (resp. unbounded) variation.

Now consider the smoothness at . By sending in (4.3),

and hence it is clearly continuous for any choice of . On the other hand, by taking in (4.8) and subtracting on both sides,

We therefore see that if we can find such that , we can attain a smooth function that satisfies (1) and (2) of Proposition 4.1.

4.3. Existence of

We show the existence of such that , or equivalently such that the function touches and also is tangent to the -axis at .

By (4.4), the function starts at

| (4.10) |

Because this is monotonically increasing in from to (by Assumptions 2.1 and 4.1), we can define to be the zero of . Then, if and only if .

Proposition 4.2.

There exist such that and

-

(1)

,

-

(2)

for and for ,

-

(3)

for all .

We shall prove Proposition 4.2 for the rest of this subsection. We first rewrite and in terms of as in (4.1). Integration by parts gives

Using this and (4.6),

| (4.11) | ||||

We can also write (4.5) as

| (4.12) |

Differentiating this further,

| (4.13) |

where the last inequality holds by Assumption 4.1 and because the scale function is increasing and nonnegative.

We show the following lemma to show the existence of a local maximizer of over .

Lemma 4.2.

For any fixed , and .

Proof.

Note that (4.5) and Assumption 2.1 imply

| (4.14) |

By (4.13), (4.14) and Lemma 4.2, for any choice of , is a concave function that first increases and then decreases to in the limit. This shows that there exists a unique global/local maximizer:

| (4.15) |

Moreover, because differentiation of (4.12) with respect to the first argument and Assumption 4.1 yield

| (4.16) |

we see that is increasing in . We shall show that there exists such that .

We first start at that makes (4.10) vanish. By (4.14) and (4.15), . We now gradually decrease its value to attain such that . Differentiating (4.11) and Assumption 4.1(1) give

| (4.17) |

This suggests that decreases monotonically as . Indeed, for any (here we know by (4.14)), we have by (4.17) and the definition of as in (4.15). Because is continuous, it is now sufficient to show that for sufficiently small, becomes negative.

4.4. Value function

Using as obtained in Proposition 4.2, equation (4.4) gives

Substituting this in (4.3),

| (4.19) | ||||

which holds for any . For , we have . By (4.4), we can also write

| (4.20) |

Proposition 4.3.

The function is convex such that and for .

Proof.

We are now ready to state the main theorem of this section; we shall prove this in the next subsection.

Theorem 4.1.

Let and be as in Proposition 4.2, and define as the value of the functional associated with the strategies , , and . Then, we have

-

(1)

for any ;

-

(2)

for any .

In other words, the pair is a saddle point and is the value function of the game.

4.5. Verification of optimality

In order to prove Theorem 4.1, we first present some preliminary results.

Let be the infinitesimal generator associated with the process applied to a sufficiently smooth function

By Remark 3.1(1) and Proposition 4.1, the function is when is of bounded variation while it is and when is of unbounded variation. Moreover, by Assumption 2.2 and Proposition 4.3, the integral part of is finite. Hence, makes sense at least anywhere on .

Proposition 4.4.

The following relations are satisfied.

-

(1)

for ,

-

(2)

for .

Proof.

On the right hand side of the continuation region we have the next result.

Lemma 4.3.

We have for .

Proof.

We first prove . By the smooth fit at , this holds for . For , we have by differentiating (4.21) further and by (4.13),

Hence by the smooth fit at and Proposition 4.4(1),

Now it remains to show is decreasing on . For any , by Assumptions 2.1 and 4.1,

In order to show that the right-hand side is nonpositive, let us define

Because is a constant, we have . Now because is decreasing on by Proposition 4.3 and is zero on , we have

which is nonpositive because is nonnegative and decreasing. This proves the claim.

∎

Lemma 4.4.

Let be the running minimum process of . We have .

Proof.

Under , with an independent exponential random variable with parameter , duality and the Wiener-Hopf factorization imply (see, e.g., (3.8) of [5])

This together with gives

On the other hand, we can also write , and

Hence,

This implies that , for all , from which we conclude the proof. ∎

We are now ready to prove Theorem 4.1.

Proof of Theorem 4.1.

We present the proof when is of unbounded variation. The proof for the bounded variation case is similar; while the smoothness of the function at is different, the following arguments in terms of the Meyer-Itô formula clearly hold.

Let be arbitrary such that and hence

| (4.23) |

Observe that when and the statement of the theorem holds, since ; when and , by Assumption 2.1. Hence we assume that .

Recall that is and with bounded second derivatives near . Hence, using the Meyer-Itô formula as in Theorem 4.71 of [31],

| (4.24) |

Further, if we denote as the continuous part of , we can write

| (4.25) |

From the Itô decomposition theorem (e.g., Theorem 2.1 of [24]), we know that

where is a standard Brownian motion and is a Poisson random measure in the measure space . The last term is a square integrable martingale, to which the limit converges uniformly on any compact .

Using this decomposition, we can write (4.25) as

Defining , , we have , and hence we can write the last term in (4.24) as

Putting together the above expressions in (4.24), we obtain

Using integration by parts (see e.g. Corollary II.2 of [31]) in and the above expressions, it follows that

| (4.26) | ||||

with

and

Since for , observe that for .

For each , define the stopping time as

and the martingale , with . Then, since for by Proposition 4.4 and since for by Proposition 4.3, taking expectation in (4.26) gives by optional sampling that

We shall take limits first as and then as on the right-hand side. Because is decreasing and for , we have . Hence we can apply the monotone convergence theorem and dominated convergence theorem, respectively, to the expectation of the positive and negative part of . For , monotone convergence theorem applies because is nondecreasing. Hence

On the other hand,

| (4.27) | ||||

Because for , we have a bound

Hence, noting ,

| (4.28) | ||||

which has a finite moment for any fixed . This together with (4.23) and (4.27) shows by Fatou’s lemma that

In order to take , observe that

| (4.29) |

As in (4.28),

Hence by Lemma 4.4 and , the limit of vanishes as ; together with (4.23) and (4.29),

Putting altogether the results above, we conclude .

For the second part of the theorem, let be as in the statement of the theorem. When , the controller acts immediately, returning the process to the set , i.e. . Hence, we assume that the initial condition . Fix an arbitrary stopping time such that and hence

| (4.30) |

For each define the stopping time as

From (4.26), Proposition 4.4(1), Lemma 4.3 and because (where is the continuous part of ) and whenever , the above localization argument gives

Similarly to the derivation above,

For the case , note that is bounded from below and hence Fatou’s lemma implies

where the second inequality holds because is bounded from below on for the case and the third inequality holds since .

Recall , and hence

Now,

| (4.31) | ||||

Because the right-hand side has a finite moment, Fatou’s lemma implies .

On the other hand, we have , which has a finite moment by (4.30). Hence,

Putting altogether, we have , as desired.

∎

5. Spectrally positive Lévy case

We now consider the spectrally positive Lévy process for . We assume throughout this section that its dual process is a spectrally negative Lévy process with a Laplace exponent (3.1). This is to say

where is a Lévy measure with the support that satisfies the integrability condition . For the case of bounded variation, we can define . The first moment of in (2.4) is , which is assumed to be finite by Assumption 2.2.

The scale function used in this section is associated with the spectrally negative Lévy process . Throughout this section, we assume the differentiability of the scale function on ; this is satisfied if is of unbounded variation or the Lévy measure has no atoms (see Remark 3.1(1)).

Assumption 5.1.

We assume that is differentiable on .

Remark 5.1.

Lemma 4.4 also holds for the spectrally positive Lévy process . Indeed, it is known that is exponentially distributed with parameter and hence .

Recall Assumption 2.1 again about our definition of the terminal cost . Regarding the running cost function , we focus on the case it is linear:

| (5.1) |

for some constants that satisfy the following.

Assumption 5.2.

The function

is decreasing. In other words,

While we are assuming here that the running cost function is linear, Assumption 5.2 is requiring a weaker condition on the slope in comparison to Assumption 4.1 that was assumed for the spectrally negative Lévy case. Indeed, Assumption 5.2 accommodates the case . In fact, we will see in this case that the controller’s optimal strategy becomes trivial (i.e. ). This is intuitively clear because, for small sufficiently far from the stopper’s exercise region, moving the process units upward costs the controller while its reduction of the future running cost is approximately , which is less than or equal to when ; hence the controller has no motivation to get involved.

|

|

5.1. Write using scale functions

Similarly to the spectrally negative Lévy case, we shall show the optimality of a set of strategies defined as in (2.1) for an appropriate choice of and .

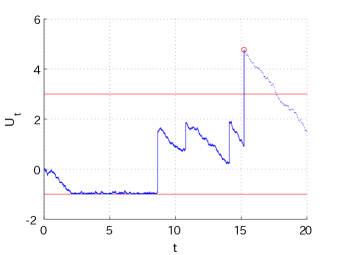

Figure 2 shows sample paths of the controlled process and its corresponding control process when is a spectrally positive Lévy process. The controlled process is reflected at the lower boundary and is stopped at the first time it reaches or exceeds the upper boundary . Due to the lack of negative jumps, the process necessarily creeps downward at (assuming it starts at a higher point); hence increases only continuously. On the other hand, due to the positive jumps, the process can jump over at the stopping time .

As in the spectrally negative Lévy case (see Section 4.1), as in (2.2) can be rewritten in terms of the scale function, using again the results by [30] and [5]. Define

| (5.2) | ||||

In particular, if , . Because and

we have

Lemma 5.1.

Fix any . For every ,

| (5.3) | ||||

Proof.

Fix . First, by Theorem 1(ii) of [30],

Second, as in Proposition 1 of [5],

Finally, by Proposition 2(ii) of [30],

and, by Proposition 2 of [5],

Summing up these terms and using the particular form of ,

For , we have . For , , as desired. ∎

Remark 5.2.

Integration by parts gives

Hence

| (5.4) | ||||

5.2. Continuous/smooth fit

Similarly to the spectrally negative Lévy case, we choose and so that the function is continuous and smooth. Define the derivative of with respect to the first argument,

| (5.5) |

where the second equality holds by (5.4). This subsection shows the following.

Proposition 5.1.

-

(1)

If are such that , then is continuous (resp. differentiable) at when is of bounded (resp. unbounded) variation.

-

(2)

If in addition and , then is twice-differentiable at .

Here we write this condition as a division respect to (instead of simply writing ) to cope with the case ; we will see below that with the choice defined below, converges as to a finite constant and hence .

The proof of Proposition 5.1 is again achieved by straightforward differentiation and asymptotic behavior of the scale function near zero. Taking derivatives in (5.3),

| (5.6) | ||||

Sending in (5.3) and the first identity of (5.6),

| (5.7) | ||||

Here we have that by (5.4)

| (5.8) |

which is if and only if is of unbounded variation or by Remark 3.1(2). Therefore, if , then is continuous (resp. differentiable) at when is of bounded (resp. unbounded) variation.

5.3. Existence of

We shall pursue such that ; we obtain such that and . Contrary to the spectrally negative Lévy case, we shall see that or can happen and in this case .

First, Assumption 5.2 implies and , and hence guarantees the existence and uniqueness of such that

| (5.10) | |||

| (5.11) |

With and as critical points, we shall prove the following.

Proposition 5.2.

-

(1)

When , by setting and , we have and and on .

-

(2)

Suppose and is of unbounded variation. Then, there exist such that and .

-

(3)

Suppose and is of bounded variation. Let be the unique value such that

(5.12) which exists by Assumption 5.2.

(i) If (including the case ), there exist such that and .

(ii) Otherwise, if we set , then and and on .

Remark 5.3.

Recall that it was necessarily that when is spectrally negative. In view of this and the spectrally positive Lévy case as obtained in Proposition 5.2(3), we see that the criterion for whether or is closely linked to how much the process moves (or fluctuates) upward in an infinitesimal time. Indeed, for the case of spectrally negative Lévy process and spectrally positive Lévy process of unbounded variation, the process at any point immediately enters the set . Otherwise, holds if the frequency of jumps is sufficiently large.

Intuitively speaking, is close to if the controller wants to terminate the game immediately. However, when the process fluctuates upward in an infinitesimal time by itself, the controller would not have to push it completely to the stopping region (recall that the controller also wants to minimize the controlling cost). On the other hand, for other cases as in (ii) of Proposition 5.2(3), the process can tend to move away from the stopping region without entering it, no matter how close it is to the stopping region; to avoid this, can happen for these cases.

We now prove Proposition 5.2. With satisfying (5.10), we first consider the function defined on . By (5.8) and Assumption 2.1,

This implies that is uniformly bounded from below by and hence never touches nor goes below zero.

Now consider increasing the value of starting from . Dividing both sides of (5.5) by ,

| (5.13) |

Lemma 5.2.

For any fixed , there exists such that is decreasing (resp. increasing) in on (resp. on ). Equivalently, is negative (resp. positive) for (resp. ).

Proof.

Because (5.13) is monotonically increasing in (given ), we can define by Remark 3.1(2,3),

Recall the definition of that satisfies (5.11). By (3.12), if or equivalently , . On the other hand, if or equivalently , . At the critical point (which is larger than ) at which , it is clear from the monotonicity of (5.13) in that for any and hence decreases monotonically as . In fact, the limit can be obtained explicitly as follows.

Lemma 5.3.

We have . Hence, if and only if .

Proof.

If , we already have a desired pair of defined by ; this concludes the proof of Proposition 5.2(1). We shall see in our later discussion that this corresponds to the case the controller never exercises.

Now suppose for the rest of this subsection that and hence . By the continuity of , we can choose such that . This together with the fact that shows that we can define the smallest value of such that first touches the -axis, i.e.,

and let . For any , because as discussed above, we have , and hence we must have that . Now there are two scenarios: or .

We first consider the case is of unbounded variation. In this case, we must have and hence . This necessarily means that attains a local minimum at and hence . These calculations conclude the proof of Proposition 5.2(2).

Now we assume that is of bounded variation. Unlike the unbounded variation case, now depends on and can attain negative values for large . Recall our definition of that satisfies (5.12). Note that by Remark 3.1(2), we can also write equivalently . Because as in (5.8) decreases to , we have and

| (5.14) |

First suppose . For fixed , again (5.13) is increasing in by Remark 3.1(3) and hence there exists, by Remark 3.1(2),

| (5.15) |

which is monotonically increasing in on . Note that if and only if uniformly on if and only if is monotonically decreasing on .

Case 1: Suppose . In this case, the monotonicity of implies for ; in other words, is monotonically decreasing on for any . Moreover, (5.14) implies that for . Hence, is the smallest value of such that touches the -axis; we must have . Notice here that and and on . See Figure 5(iii) below for the shape of and for this particular case.

Case 2: Suppose . Because is monotone and continuous, there exists such that . For , is monotonically decreasing. Moreover, because , . Hence we must have and hence or , which shows . We also see that by and the definition of .

We now show that Cases 1 and 2 correspond to (ii) and (i), respectively, in Proposition 5.2(3). By substituting (5.12) in (5.15),

Hence for the case of bounded variation with ,

which is confirmed to be mutually exclusive with , which is a necessary and sufficient condition for (here because otherwise the process becomes a subordinator).

This result can be extended to the case . Indeed, we have for any , and hence due to the same reason as in Case 2 above. Summarizing the results, Proposition 5.2(3) holds.

5.4. Verification of optimality

With as in Proposition 5.2(2,3), substituting in (5.3) gives

| (5.16) |

For , . Also, for ,

| (5.17) | ||||

As in Proposition 5.2(1), the same results hold for the case with . It can be easily shown that this corresponds to the value under the controller’s strategy for all and .

Proposition 5.3.

The function is convex. Hence, and for all .

Proof.

(i) The proof is immediate for because in this case it is continuous by Proposition 5.1 and on while on .

We now state the main theorem for the spectrally positive Lévy case.

Theorem 5.1.

Let and be as in Proposition 5.2, and define as the value of the functional associated with the strategies , , and . Then, the pair is a saddle point and is the value function of the game.

We shall show this by verifying the variational inequalities for the rest of this section. First, the generator of is given by

By Proposition 5.3 and Assumption 2.2, the integral part of is finite. Hence, by the smoothness by Proposition 5.1 and (5.9), is well defined everywhere on .

Proposition 5.4.

(1) Suppose . For , .

(2) We have for .

Proof.

(1) The result holds immediately in view of (5.16) as in the spectrally negative Lévy case.

(2) Because is spectrally positive,

and hence . The result holds immediately by and because is decreasing. ∎

By differentiating (5.4),

| (5.18) |

which is positive (resp. negative) whenever (resp. ). Namely, for fixed , increases (resp. decreases) monotonically in on (resp. ). Hence there exists .

Lemma 5.4.

For all , .

By (5.18) and Lemma 5.4, for each (which ensures even for the bounded variation case because ), there exists a unique such that .

Lemma 5.5.

Suppose . (i) If , then and (ii) if , for all .

Proof.

Suppose . We first prove that . Assume for contradiction that and hold simultaneously. By (5.18) and , we have , which is a contradiction because is decreasing on (by Lemma 5.2 and because for the case and by Proposition 5.2(3) for the case ) and . Hence whenever we must have .

This also shows (and hence (ii)) by Lemma 5.2. Indeed, if , this means by Lemma 5.2 that on and hence . However, this contradicts with , which is larger than by and (5.18).

Now suppose and assume for contradiction that to complete the proof for (i). By (5.18) we have , which is a contradiction because is decreasing on (due to (ii)) and . ∎

Lemma 5.6.

Suppose . Fix . We have for .

Proof.

Proposition 5.5.

Suppose . For , .

Proof.

It is sufficient to prove

| (5.19) |

Indeed if both (5.19) and hold simultaneously,

which leads to a contradiction because for that holds similarly to Proposition 5.4(1). Notice that the function admits the same form as (5.16) because .

By (5.6), for ,

| (5.20) |

The dominated convergence theorem gives

By the smooth fit of at as in (5.9) and and as , this is simplified to

| (5.21) | ||||

By taking limits in (5.20) and by Lemma 5.5(ii),

In order to prove the positivity of the integral part of (5.21), we shall prove that

| (5.22) |

Notice from (5.7) that both and are continuous on . Recall also that by Lemma 5.5(i).

(i) For , by Lemma 5.6, .

Propositions 5.3, 5.4 and 5.5 show the variational inequality, and we can modify slightly the proof of Theorem 4.1 to show that this is a sufficient condition for optimality. The proof is very similar, and we do not include it so as to avoid unnecessary repetitions. The only differences worthy of remark are (1) the smoothness of the value function in view of the difference between Propositions 4.1 and 5.1 and (2) the estimation of the running minimum process (obtained in Lemma 4.4 for the spectrally negative Lévy case), which is used to interchange limits over expectations. However, these do not cause any problems. For (1), the candidate value function fails to be differentiable at (although continuous) for the case of bounded variation, but the Meyer-Itô formula (Theorem 4.71 of [31]) applies and the local-time term vanishes due to paths of bounded variation. For (2), as it is pointed out in Remark 5.1, it also holds for the spectrally positive Lévy case. Hence Theorem 5.1 holds.

6. Numerical Examples

In this section, we confirm the results numerically using the case is given by (5.1). For , we use the spectrally negative process with i.i.d. phase-type distributed jumps [3] of the form

for some and , and also the spectrally positive Lévy process defined as its dual. Here is a standard Brownian motion, is a Poisson process with arrival rate , and is an i.i.d. sequence of phase-type-distributed random variables with representation ; see [3]. These processes are assumed mutually independent. The Laplace exponent (3.1) is then

which can be extended to except at the negative of eigenvalues of . Suppose is the set of the roots of the equality with negative real parts, and if these are assumed distinct, then the scale function can be written

where

see [16]. Here and are possibly complex-valued.

In our example, we assume and

which give an approximation of the log-normal distribution with density function

obtained using the EM-algorithm; see [16] regarding the approximation performance of the corresponding scale function. Throughout this section, we let and . We consider both the bounded and unbounded variation cases with and .

|

|

| Unbounded variation case with | |

|

|

| Bounded variation case with | |

|

|

|

|

6.1. Spectrally negative Lévy case

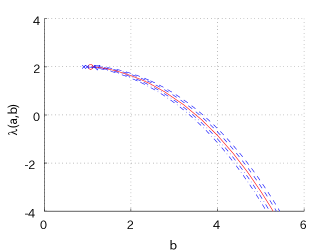

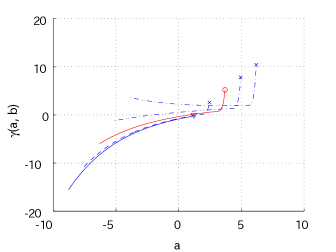

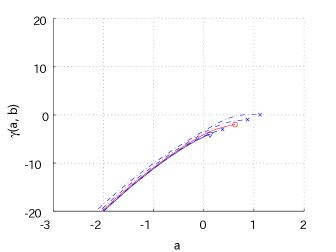

We first consider the spectrally negative Lévy case as studied in Section 4. Recall that the values of and are such that . Figure 3 shows, for both the unbounded and bounded variation cases, and for fixed . Regarding the computation of the pair , we observe, by (4.13) and (4.14), that the function for each fixed starts at a positive value and monotonically decreasing in to and hence its zero (see (4.15)) can be computed via bisection method. Recalling that is increasing in , we then apply another bisection method to to compute . Once these are obtained, the value function is computed by (4.19).

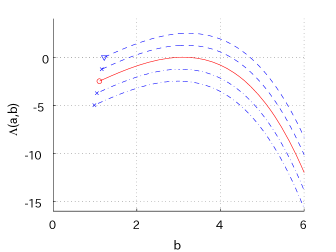

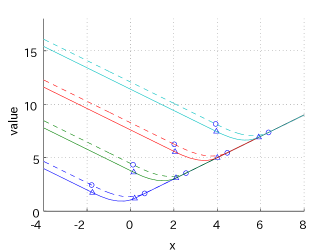

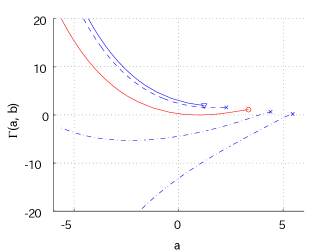

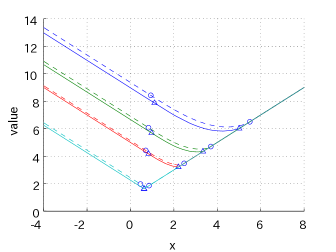

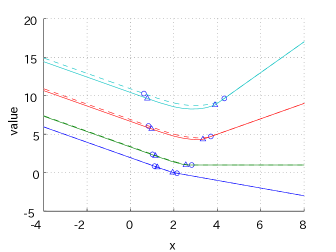

In Figure 4, we show how the value functions change in each of the parameters and . The parameters we use are unless otherwise specified. In each figure, the bounded variation case () is plotted in solid while the unbounded variation case () is in dotted. The circles (resp. triangles) indicate the values at and for the case of unbounded (resp. bounded) variation. We can confirm the results in Proposition 4.1 that the value functions are smooth in all cases. In addition, the value of the game is monotone in each parameter. Finally, the value function is indeed convex for both the bounded and unbounded variation cases; this is consistent with Proposition 4.3.

6.2. Spectrally positive Lévy case

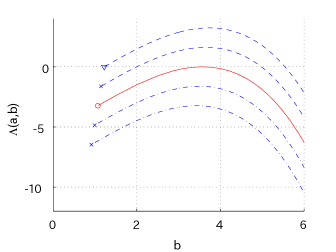

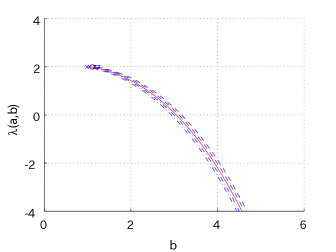

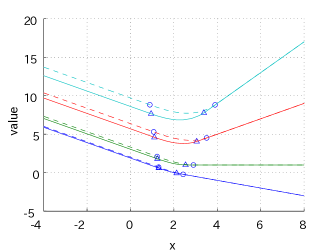

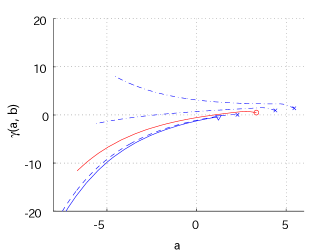

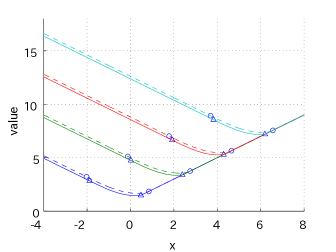

We now move onto the spectrally positive Lévy case as studied in Section 5. Recall that the values of and such that and are first attained when we increase the value of starting from . When is of unbounded variation or , we always have with ; otherwise with . In both cases, because has at most one local minimum (in other words, has at most one zero), the values of can be obtained by bisection methods similarly to the spectrally negative Lévy case as obtained above.

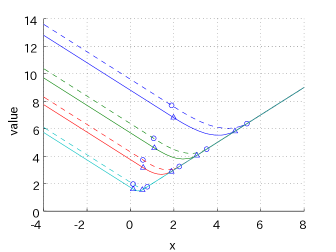

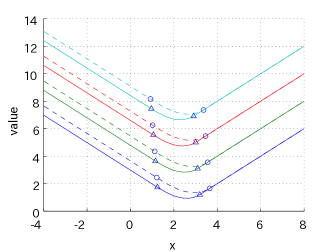

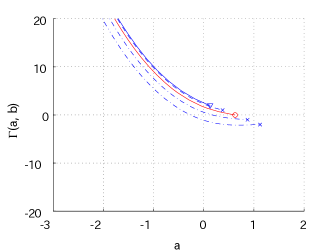

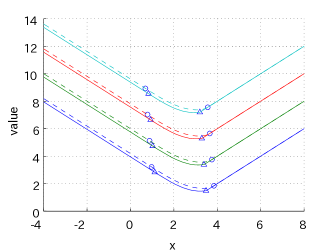

In Figure 5, we show and for fixed for (i) and , (ii) and and (iii) and . We choose these values of so that in (i) and (ii) while in (iii). In Figure 6, we show the value functions in the same fashion as in Figure 4. From our choice of such that , in all the results . Here, for the bounded variation case with in the top left plot, ; in other cases we have . The results are consistent with Proposition 5.1 that the value function is twice differentiable at (unless ), and at it is continuous (resp. differentiable) when is of bounded (resp. unbounded) variation. We also confirm the convexity of the value function as in Proposition 5.3.

|

|

| (i) and | |

|

|

| (ii) and | |

|

|

| (iii) and | |

|

|

|

|

Acknowledgements

The authors thank the two anonymous referees for their thorough reviews and insightful comments that help improve the presentation of the paper. The first author is indebted to V. Rivero for helpful discussions; the support received from Conacyt through the Laboratory LEMME is also greatly appreciated. The second author thanks M. Fukushima and H. Nagai for valuable comments and is supported by MEXT KAKENHI grant numbers 22710143 and 26800092, JSPS KAKENHI grant number 23310103, the Inamori foundation research grant, and the Kansai University subsidy for supporting young scholars 2014.

References

- [1] H. Albrecher and S. Thonhauser. On optimal dividend strategies in insurance with a random time horizon. Stochastic processes, finance and control, pages 157–180, 2012.

- [2] L. Alili and A. E. Kyprianou. Some remarks on first passage of Lévy processes, the American put and pasting principles. Ann. Appl. Probab., 15(3):2062–2080, 2005.

- [3] S. Asmussen, F. Avram, and M. R. Pistorius. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl., 109(1):79–111, 2004.

- [4] F. Avram, A. E. Kyprianou, and M. R. Pistorius. Exit problems for spectrally negative Lévy processes and applications to (Canadized) Russian options. Ann. Appl. Probab., 14(1):215–238, 2004.

- [5] F. Avram, Z. Palmowski, and M. R. Pistorius. On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl. Probab., 17(1):156–180, 2007.

- [6] E. Baurdoux, A. Kyprianou, and J. Pardo. The Gapeev-Kühn stochastic game driven by a spectrally positive Lévy process. Stochastic Process. Appl., 121(6):1266–1289, 2011.

- [7] E. Baurdoux and A. E. Kyprianou. The McKean stochastic game driven by a spectrally negative Lévy process. Electron. J. Probab., 13:no. 8, 173–197, 2008.

- [8] E. Bayraktar, A. E. Kyprianou, and K. Yamazaki. On optimal dividends in the dual model. ASTIN Bulletin, 43(3).

- [9] E. Bayraktar and V. R. Young. Proving regularity of the minimal probability of ruin via a game of stopping and control. Finance Stoch., 15:785–818, 2011.

- [10] L. Benkherouf and A. Bensoussan. Optimality of an policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach. SIAM J. Control Optim., 48(2):756–762, 2009.

- [11] A. Bensoussan, R. H. Liu, and S. P. Sethi. Optimality of an policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach. SIAM J. Control Optim., 44(5):1650–1676 (electronic), 2005.

- [12] T. Chan, A. E. Kyprianou, and M. Savov. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Fields, 150:691–708, 2011.

- [13] M. H. A. Davis and M. Zervos. A problem of singular stochastic control with discretionary stopping. Ann. of Appl. Probab., 4:226–240, 1994.

- [14] E. Egami, T. Leung, and K. Yamazaki. Default swap games driven by spectrally negative Lévy processes. Stochastic Process. Appl., 123(2):347–384, 2013.

- [15] M. Egami and K. Yamazaki. Precautional measures for credit risk management in jump models. Stochastics, 85(1):111–143, 2013.

- [16] M. Egami and K. Yamazaki. Phase-type fitting of scale functions for spectrally negative Lévy processes. J. Comput. Appl. Math., 264:1–22, 2014.

- [17] L. Hansen and T. Sargent. Robust control and model uncertainty. Am. Econ. Rev., 91(2):60–66, 2001.

- [18] L. Hansen, T. Sargent, G. Turmuhambetova, and N. Williams. Robust control and model misspecification. J. Econ. Theory, 128:45–90, 2006.

- [19] D. Hernández-Hernández, R. S. Simon, and M. Zervos. A zero-sum game between a singular stochastic controller and a discretionary stopper. Ann. Appl. Probab., forthcoming.

- [20] I. Karatzas and S. Shreve. Connections between optimal stopping and singular stochastic control i. monotone follower problems. SIAM J. Control Optim., 22(6):856–877, 1984.

- [21] I. Karatzas and W. Sudderth. The controller-and-stopper game for a linear diffusion. Ann. Probab., 29:1111–1127, 2001.

- [22] I. Karatzas and H. Wang. A barrier option of american type. Appl. Math. Optim., 42:259–279, 2000.

- [23] A. Kuznetsov, A. Kyprianou, and V. Rivero. The theory of scale functions for spectrally negative Lévy processes. Springer Lecture Notes in Mathematics, 2061:97–186, 2013.

- [24] A. E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin, 2006.

- [25] A. E. Kyprianou and Z. Palmowski. Distributional study of de Finetti’s dividend problem for a general Lévy insurance risk process. J. Appl. Probab., 44(2):428–443, 2007.

- [26] A. E. Kyprianou and B. A. Surya. Principles of smooth and continuous fit in the determination of endogenous bankruptcy levels. Finance Stoch., 11(1):131–152, 2007.

- [27] T. Leung and K. Yamazaki. American step-up and step-down default swaps under Lévy models. Quant. Finance, 13(1):137–157, 2013.

- [28] R. L. Loeffen. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Ann. Appl. Probab., 18(5):1669–1680, 2008.

- [29] A. Maitra and W. D. Sudderth. The gambler and the stopper. In Statistics, Probability and Game Theory: Papers in Honor of David Blackwell, volume 30. T. S. Ferguson, L. S. Shapley and J. B. MacQueen (eds), IMS Lecture Notes Monograph Series IMS, Hayward, CA., 1996.

- [30] M. R. Pistorius. On exit and ergodicity of the spectrally one-sided Lévy process reflected at its infimum. J. Theoret. Probab., 17(1):183–220, 2004.

- [31] P. E. Protter. Stochastic integration and differential equations, volume 21 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2005. Second edition. Version 2.1, Corrected third printing.

- [32] B. A. Surya. Evaluating scale functions of spectrally negative Lévy processes. J. Appl. Probab., 45(1):135–149, 2008.

- [33] K. Yamazaki. Inventory control for spectrally positive Lévy demand processes. arXiv:1303.5163, 2013.