Orbits in a stochastic Goodwin-Lotka-Volterra model

Abstract

This paper examines the cycling behavior of a deterministic and a stochastic version of the economic interpretation of the Lotka-Volterra model, the Goodwin model. We provide a characterization of orbits in the deterministic highly non-linear model. We then study the cycling behavior for a stochastic version, where a Brownian noise is introduced via an heterogeneous productivity factor. Sufficient conditions for existence of the system are provided. We prove that the system produces cycles around an equilibrium point in finite time for general volatility levels, using stochastic Lyapunov techniques for recurent domains. Numerical insights are provided.

Keywords: Lotka-Volterra model; Goodwin model; Brownian motion; Random perturbation; Business cycles; Stochastic Lyapunov techniques.

1 Introduction

The Lotka-Volterra equation is at the heart of population dynamics, but also possesses a famous economic interpretation. Introduced by Richard Goodwin [10] in 1967, the model in its modern form [6] reduces to the planar oscillator on a subset of :

| (1) |

where denotes the wage share of the working population and the employment rate, and are constant, and the following assumption is made on and .

Assumption 1.

Consider system (1).

-

(i)

, , for all , and .

-

(ii)

, for all , and .

Lemma 1 below asserts that Assumption 1 is sufficient to have for any if . This property preserves the above interpretation for and : the employment rate cannot exceed one for obvious reasons, but the wage share can, depending on the chosen economic assumptions, see [11]. This distinctive feature of the economic version (1) on its biological counterpart follows from a construction based on assumptions describing a closed capitalist economy. It can be done in three steps:

-

(I)

Assume a Leontief production function with full utilization of capital, i.e., . Here, is the yearly output, the invested capital, a capital-to-output ratio, is the average productivity of workers and is the size of the labor class.

-

(II)

The capital depreciates and receives investment, i.e., , where is the depreciation rate and the investment function. Goodwin [10] originally invokes Say’s law, i.e., .

-

(III)

Assume a reserve army effect for wage negotiation of the form where represents the real wage of the total working population, and is the Phillips curve.

Defining allows to retrieve (1) for . The class-struggle model (1) has been extensively studied because it allows to generate endogenous real business cycles affecting the production level , e.g. [8, 9, 11, 15, 28, 29]. On this matter, Goodwin himself conceded that the model is “starkly schematized and hence quite unrealistic” [10]. It hardly connects with irregular observed trajectories, see [13, 22].

The objective of this paper is thus to study the following perturbed version of (1) by a standard Brownian motion on a stochastic basis :

| (2) |

where is a positive function of bounded by , and the filtration is generated by paths of . The form of is discussed in Remark 2 after. A stronger condition, Assumption 3, is assumed later on the behavior of to ensure that solutions of (2) remain in . The example of Section 5 will also illustrate how such condition can hold. We modify the economic development (I), (II) and (III) by introducing the perturbation on one assumption, namely we assume that for ,

| (3) |

instead of . Using Itô formula with (3) in the previous reasoning retrieves (2). Productivity is one of the few exogenous parameters of the model, and one of those that were significantly invoked as influencial over business cycles, e.g. [7, 12]. Without arguing for the pertinence of that particular assumption, we simply suggest here that a standard continuous perturbation in this crucial parameter seems a good starting point.

To our knowledge, this is the first attempt to consider random noise in Goodwin interpretation of the famous prey-predator model. To stay in the spirit of the economic application, the present paper studies the cyclical behavior of the deterministic system (1) and the stochastic version (2). Namely, our contribution are as follows, developed in the present order:

- •

-

•

In Section 3, we provide existence conditions for regular solutions of (2). We use the entropy of (1) to estimate the deviation induced by (3). We provide a definition of stochastic orbits for (2). The proof that solutions of (2) draw stochastic orbits in finite time around a unique point is given in Section 4.

Our contribution has to be put in contrast with numerous studies of random perturbations of the Lotka-Volterra system. Apart from the obviously different origin of perturbations in the model, attention was mainly given to systems like (2) for its asymptotic behavior (e.g., [18, 21, 24]), regularity, persistence and extinction of species (e.g., [4, 20, 24, 25]), and the addition of regimes, jumps or delay (e.g., [2, 19, 31]). Here, we attempt to provide a relevant description of trajectories and indirectly , namely a cyclical behavior. This is done using stochastic Lyapunov techniques for recurrent domains as described in [17, 27]. By conveniently dividing the domain , we obtain that almost every trajectory “cycles” around a point in finite time. The -boundedness is out of reach with our method, but numerical simulations are presented in Section 5, not only to provide expectation of cycles, but also allow to conjecture a limit cycle phenomenon for the expectation of . It is somewhat unclear how Assumption 1 and late Assumption 3 on , and , are relevant in these results. We show below thatthey are sufficient to obtain existence of regular solutions to (2). This actually emphasizes the role played by the entropy of the deterministic system in the well-posedness of the stochastic system and as a natural measure for perturbation.

2 Deterministic orbits

According to Assumption 1, there exists only one non-hyperbolic equilibrium point to (1) in given by . On the boundary of , there exists also an additional equilibrium which is eluded along the paper.

Definition 1.

Let and be three functions defined by and

Lemma 1.

Proof.

It is well-known [11] that is a Lyapunov function and a constant of motion for system (1): and take non-negative values with , and . Additionally, under Assumption 1.(i)-(ii),

| (4) |

so that for any , and the solution stays in .

∎

The value of characterizing an orbit, it is in bijection with its period. The following generalizes [14].

Theorem 1.

Let be a solution to (1) satisfying Assumption 1, with . Let , and the two solutions to equation . Define three functions by

Then for defined by

| (5) |

Proof.

Let , and a solution to (1) starting at . According to Lemma 1, implies . Then . Homogeneity of (1) allows to set without loss of generality. Let . For , , with such that . Let for . Then (1) rewrites , and we get

Let and define , to rewrite again

| (6) |

Since and for , separation of variables in (6) provides two quantities and :

| (7) |

The function verifies , is increasing on and decreasing on with so that . Coming back to we get

implying that for . We can write where and are the two restrictions of on and respectively. Notice that if , then . Thus, is a strictly increasing function of taking its values in . Getting back to for , we have for

Since we have , while minimums are given by . This sums up with , so we can write on this interval which finally gives

We apply the same method for the other half orbit, taking and , to reach the other half of expression (5), i.e., . ∎

Remark 1.

A first order approximation of (1) at provides a linear homogeneous system, which solution is trivially given by a linear combination of sines and cosines of . It follows that

3 Stochastic Goodwin model

We study a specific case of (2) where the deterministic part cancels at a unique point in defined by where comes from the following.

Assumption 2.

There is a unique such that

For a stochastic differential equation to have a unique global solution for any given initial value, functions and are generally required to satisfy linear growth and local Lipschitz conditions, see [17]. We can however consider the following Theorem of Khasminskii [17], which is a reformulation of Theorem 3.4, Theorem 3.5 and Corollary 3.1 of [17] to our context.

Theorem 2.

Consider the following stochastic differential equation for taking values in :

| (8) |

Let be an increasing sequence of open sets, and a sequence of constants, verifying

-

(a)

for all ,

-

(b)

.

-

(c)

For any , functions and are Lipschitz on and verify for any .

Let and be such that, denoting the generator associated with (8),

-

(d)

on the set ,

-

(e)

for any .

Then for any , there exists a regular adapted solution to (8), unique up to null sets, with the Markov property and verifying for all almost surely.

To satisfy conditions (a) to (e), we study (2) under the additional sufficient growth conditions.

Assumption 3.

There exist two positive constants such that

-

(i)

for all ,

-

(ii)

for all .

Remark 2.

Assumption 3.(i) involves both and to ensure that for all almost surely. Assumption 3.(ii) holds for polynomial growth of , suiting the classical conditions of existence on for . The dependence of could be generalized to in full generality, implying a stronger condition than (ii). We refrain from doing this easy extension, emphasizing the unavoidable dependence in .

For , we recall the diffusion operator associated with (2) by

| (9) |

Theorem 3.

Proof.

Let us show that conditions (a) to (e) of Theorem 2 are fulfilled. Consider the sequence of sets defined by . For any , is open and . (a) and (b) are satisfied with the limit . According to Assumption 1, one can always find big enough such that for any , and ensures the local Lipschitz condition (c).

Since and ,

| (10) |

Assumption 3 implies for two positive constants , checking condition (d). From Definition 1,

which implies that , the latter going to infinity with , recall (4). Similarly, goes to infinity as goes to or . Condition (e) is then satisfied, which allows to apply Theorem 2.

∎

Remark 3.

Notice that and thus . Following Assumption 1, (10) at provides . It is straightforward that (2) has no equilibrium point in , nor on its boundary . If the point cancels (2), we highlight that and by continuity, it holds on a small region . Recalling (4) implies that will diverge from almost surely if .

A solution to (2) can be pictured as a trajectory continuously jumping from an orbit of (1) to another. Along this idea, provides an estimate on trajectories, and can be related via Theorem 1 to the period .

Theorem 4.

Let , , and be a regular solution to (2). We first introduce a constant , the set and the stopping time . We then introduce two finite constants

and

Then for all

| (11) |

Proof.

Fix . Now we define the -measurable set where is a martingale defined by for and for by

The process is not right-continuous at but still verifies for all . The property holds by replacing by its càdlàg representation. Doob’s martingale inequality can then be applied: . At last, using Itô’s formula, we have from (10):

so that on almost surely. Also, on that set. Put in another way, on . According to Bayes rule,

∎

We now introduce the main result of the paper. We provide the following tailor-made definition for the cycling behavior of (2).

Definition 2.

Let and . Let be a stochastic process starting at staying in almost surely. We then introduce the angle between and . Let be a stopping time (a stochastic period). Then, the process is said to orbit stochastically around in if almost surely.

Theorem 5.

Let and a solution to (2) starting at . Then orbits stochastically around in .

4 Proof of Theorem 5

4.1 Preliminary definitions and results

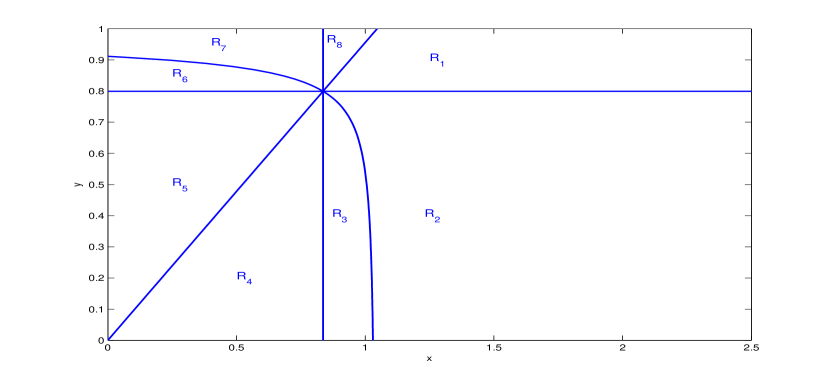

Recall that the probability space is given by with the filtration generated only by is completed with null sets. Our proof, although unwieldy, allows us to describe precisely the possible trajectories of solutions of (2). it consists in defining subregions of the domain , see Definition 4 below illustrated by Fig. 1, and prove that the process exits from them in finite time by the appropriate frontier. According to Theorem 3 any regular solution of (2) is a Markov process. We then repeatedly change the initial condition of the system, as equivalent of a time translation and use Definition 5 herefater. We obtain recurrence properties via Theorem 3.9 in [17]. Since it is repeatedly used hereafter, we provide here a version suited to our context.

Theorem 6.

Let be a regular solution of (2) in , starting at , for some . Let verifying for all and where and . Then leaves the region in finite time almost surely.

Definition 3.

Let be defined by as a concave decreasing function. For a solution to (2), we define the finite variation process verifying . Additionally, let .

Definition 4.

We define eight sets such that and , by

Definition 5.

Let be a solution to (2) starting at . For any , we define the stopping times .

Remark 4.

To ease the reading of the proof of Theorem 5 which follows from the following Propositions 1 to 10, we divide it in four quadrants around . We first prove that the process cycles, even in infinite time, for some particular starting points.

Proposition 1.

If , then . If , then .

Proof.

This is a direct consequence of the absence of Brownian motion in . Take . Then on , the process is non increasing almost surely, meaning that cannot be reached without first crossing region . The other side is identical. ∎

Remark 5.

Proposition 1 holds even if , for any involved. It also implies that if , then almost surely for .

4.2 Eastern quadrant

We ought to prove that for , the process reaches in finite time almost surely.

Proposition 2.

If then .

Proof.

Let . Then for any such that . Moreover,

Theorem 6 stipulates that leaves in finite time almost surely which is only possible via according to Proposition 1. Reaching the boundary is prevented by Theorem 3.

∎

Proposition 3.

If then .

Proposition 4.

If then .

Proof.

Step 1. Let be a sequence of stopping times defined by and

By construction if for some , then for all . Following Propositions 1, 2 and 3, for all almost surely, and . We prove in step 2 that this implies

| (12) |

Providing that (12) holds we immediately get .

Step 2. If , then for all , and according to Proposition 3, does not converge to the set . Since is a positive decreasing process for , Doob’s martingale convergence theorem implies that converges pathwise in . Assume now that does not converge to with on . Then for any , and for almost every

| (13) |

If the integral (13) explodes to for some on some non null subset , then for almost every ,

and for almost every , implying that converges to on , a contradiction with , so that (13) holds on . We then consider the random time , being the first time such that

| (14) |

and the smallest index such that . Note that is not a -stopping time and is not -adapted since they depend on which is -measurable. (14) implies that there exists a random time such that , otherwise we would have a contradiction of (13) on a subset of :

This implies that for almost every , and being a continuous process

This is impossible for small enough since is strictly decreasing and thus is a null set. (12) holds. ∎

4.3 Southern quadrant

We show that starting from , reaches in finite time almost surely.

Proposition 5.

If then .

Proof.

Step 1. We consider with , and aim to prove that the process with is a supermartingale on , for . Notice that it is bounded in . Applying Itô to first gives

Then, noticing that , we obtain

It is clear that for all . Now notice that for , we have so that

Now on , implies that , so that

Denoting , we conclude that is a supermartingale for . Using optional sampling theorem, assisted by Proposition 3, almost surely and

Since then

Step 2. According to Proposition 3, almost surely for any , and according to Proposition 4, for all . Taking , we define the sequence with and

We then have for any . The sequence is decreasing in the sense of inclusion, so that

| (15) |

Using Baye’s rule,

Using step 1 of the present proof and the Markov property of ,

Plugging this inequality into (15) concludes the proof. ∎

Remark 6.

Notice that by choosing properly in the above proof, it is possible to be arbitrarily close to in finite time. The device is used later in Proposition 9.

Proposition 6.

If then .

Proof.

Step 1. We claim that almost surely. Consider the function . The process is a positive supermartingale on :

| (16) |

According to Doob’s martingale convergence theorem, converges point-wise with . Let and define . Then on , and similarly to Proposition 3, we use Theorem 6 to assert that leaves in finite time almost surely. This being true for any , for almost every . In , this is only possible if also, implying that on this set. This being improbable, almost surely.

Step 2. By denoting , we then define the sequence by

If , then, according to Proposition 5, the process reaches back in finite time. Using step 1, we have that . By construction and Proposition 5, for

| (17) |

Therefore, and the sequence of sets

is decreasing in the sense of inclusion. Altogether we get

| (18) |

Now using Bayes formula and (17), we finally obtain for every

| (20) |

Step 3. Let . According to (16) the process is a supermartingale on . Fixing and applying optional sampling theorem, we obtain

Since almost surely, we apply Fatou’s lemma and obtain

| (21) |

Since and for all , (21) implies

leading to

| (22) |

If then and by continuity , implying

| (23) |

Markov inequality then leads to the following convergence for any :

Now Bayes rules with (23) provides

which leads for any to . From step 2, . Therefore on this set, the continuous mapping theorem asserts that at consecutive stopping times converge in probability. By continuity, this implies and for . By the Markov property of , for almost every We conclude that . ∎

4.4 Western Quadrant

Proposition 7.

If then .

Proof.

Step 1. Consider for arbitrarily fixed . Assume that . Denoting with and recalling Definition 3, for very . Theorem 6 then states that exits in finite time almost surely. Since that is non-decreasing on this set, and recalling Theorem 2, it is only possible via and . This holds for any .

Step 2. Assume now that . According to step 1, and thus . Because is non decreasing and according to Doob’s martingale convergence theorem, converges to on . This implies that converges with to on . Since , this convergence is improbable. ∎

4.5 Northern quadrant

Finally we prove that if , then the process reaches in finite time almost surely. One can notice that proofs are very similar to those of Subsections 4.2 and 4.3.

Proposition 8.

If then .

Proof.

Define the sequence of regions through where is sufficiently small to have . Applying Itô to we find that for all

while in . Doob’s supermartingale convergence theorem implies the existence of the pointwise limit almost surely, where we use the notation . In addition, Theorem 6 guarantees that every set is exited in finite time almost surely. Consequently if , we have that either or , a contradiction in either way. ∎

Proposition 9.

If then .

Proof.

The proof is identical to the one of Proposition 5, with small modifications. Here with and . The process is a supermartingale on if we chose where are two positive constants given by and The justification is the following. The domain contains the area of interest . Using Proposition 5, we can prove that is a supermartingale on . On ,

Proposition 10.

If then .

Proof.

We follow Proposition 6 with the minor following modifications.

1 We consider the exit time of . The process with verifies

for some . Indeed and is null only if , whereas only if . Applying Theorem 6 to , almost surely.

Step 2. If , then the process reaches in finite time almost surely according to Proposition 9. We define the sequence with and

Proceeding as in step 2 Proposition 6, we obtain that implies that

| (24) |

Step 3. Define , which is strictly positive according to step 1. Consider the new process with . It is a positive submartingale on , and similarly to step 3 of Proposition 6, we can obtain

Assuming (24), we have

We then proceed exactly as in step 3 of Proposition 6 to finish the proof. ∎

5 Example

In this section we assume that investment follows Say’s law and Philips curve is provided by [11, 15].

Assumption 4.

We let and .

Assumption 1 holds under Assumption 4. The unique non-hyperbolic equlibrium point in is given by Functions of Definition 1 are given by with

| (25) |

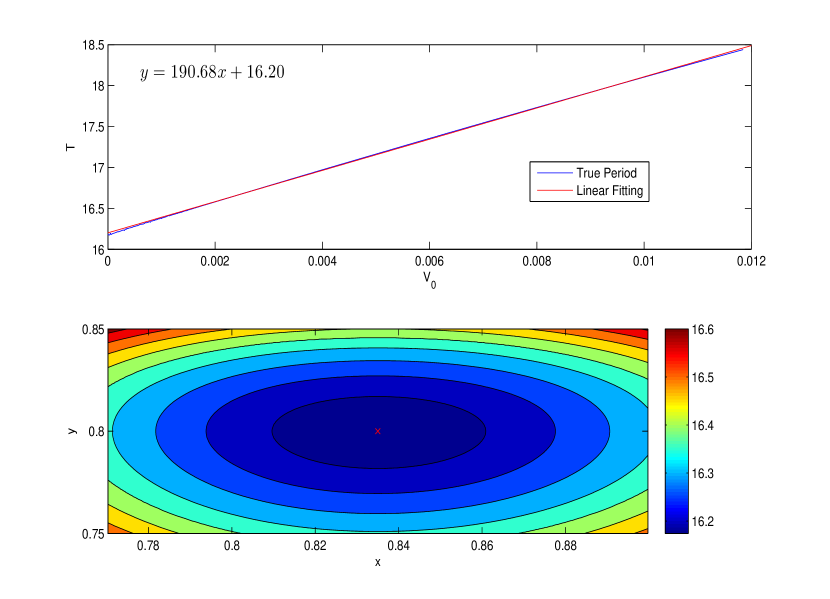

Although period given by Theorem 1 is not explicit here, numerical computations allow to approximate it with a linear function of , see first part of Fig. 2. Following Remark 1, does not converge to with solutions of (1) concentrating to . A local phase portrait with values of is provided in second part of Fig. 2.

Assumption 5.

Let with .

If we implicitly assume that the perturbation of the average growth rate of the productivity is due to the flow of workers coming in and out of the fraction employed at time , Assumption 5 conveniently expresses that this perturbation decreases with the employment rate since higher employment implies lower perturbation on the constant average rate . Other models can of course be considered.

Assumption 5 together with Assumption 4, and comparing with (25), satisfy Assumption 3. Indeed for all ,

| (26) |

and along with the sub-linearity of the log function,

| (27) |

In line with Assumptions 1 and 3 the vertical asymptote at implies that for some . Under Assumption 3 and following (26) and (27), and .

Assumption 5 also implies that is the root of a quadratic polynomial The latter shall have a unique root in to satisfy Assumption 6. The following example of condition is sufficient.

Assumption 6.

We assume and .

We are now able to claim the existence of such that , where is defined in Proposition 4. A direct application provides

Using (27), this estimate becomes where and is an explicitly calculable constant. Following the same procedure with (26), with the same and . Now choosing for some , so that , Proposition 4 provides

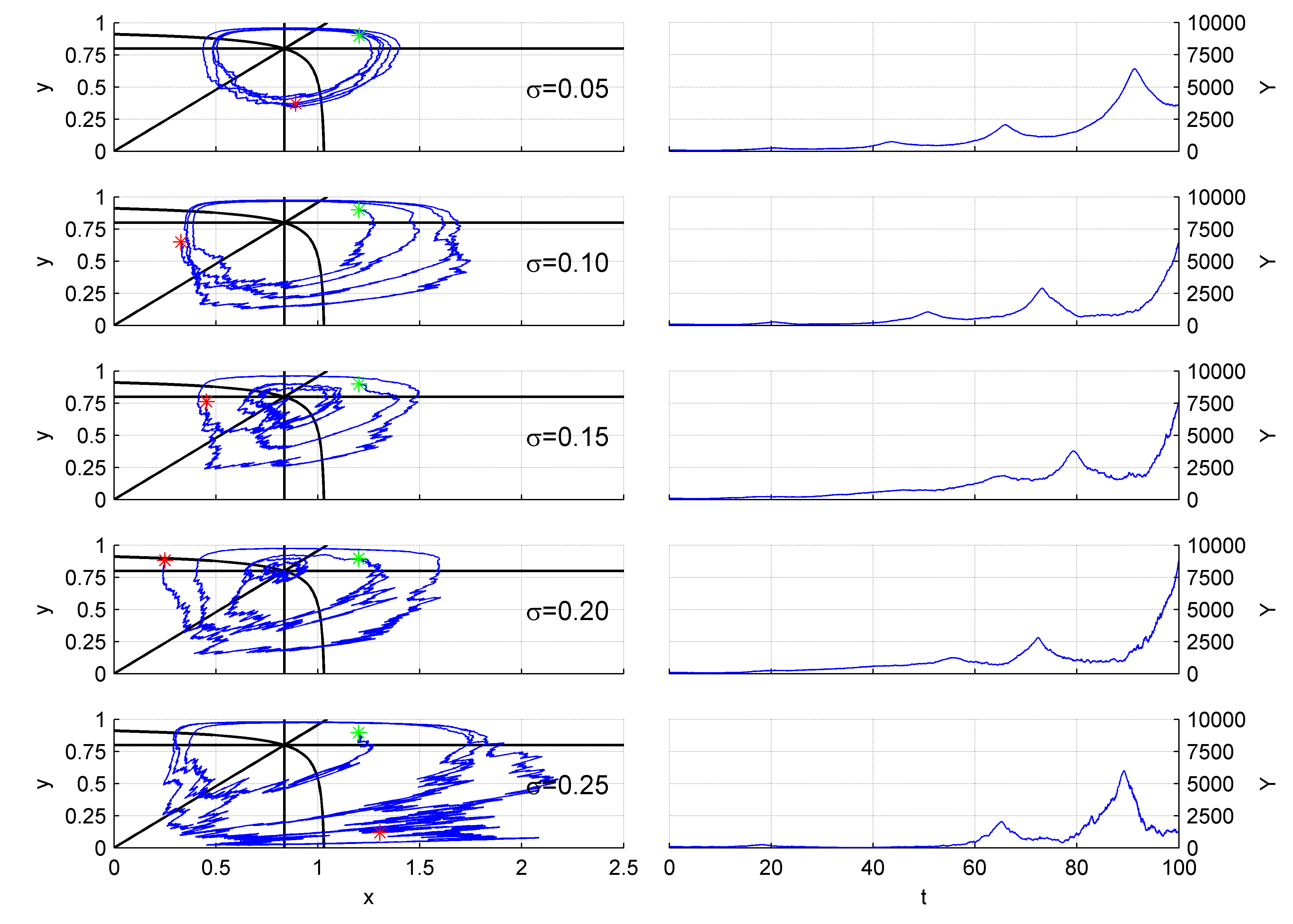

Theorem 5 is a straightly observable phenomenon with simulations, see Fig. 3. Under the assumptions of this section, the system has been simulated using XPPAUT with a fourth order Runge-Kutta scheme for the deterministic part, and an Euler scheme for the Brownian part. Fig. 3 illustrates the effect of the volatility level on trajectories of the system, as for the economic quantity .

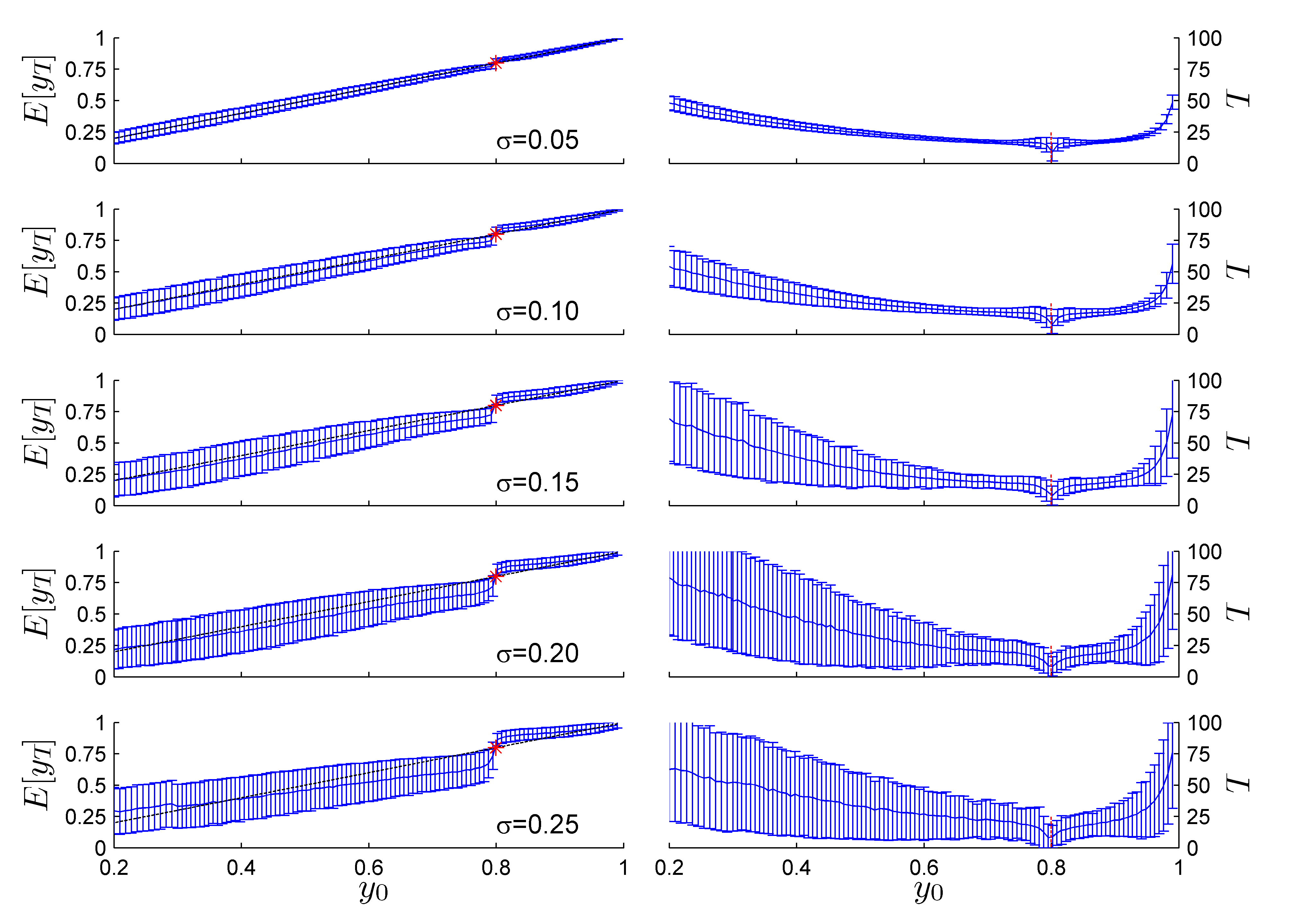

Apart from specific subregions of as or where Corollary 3.2 in [17] can provide an estimate for the expectation of the exit time, a bound for the expected period seems out of reach. Numerical simulations have nevertheless always provide reasonnable finite periods of stochastic orbits of (2). We thus expect that is finite for a wide range of values of . Let us start with and reformulate of Definition 2 as the time the process crosses the line for the second time. This is equivalent to take . Resorting to numerical methods, we have simulated the system times for different starting points in and recorded the position at the time when this line is crossed the second time, that is the positions after a full loop. Fig. 4 contains such examination for an array of values of . The expected time to complete a full-loop is also illustrated. As observed, there seems to be a stable attractive fixed point to for sufficiently large values of . If the starting point is picked too close to , the expected crossing value after one loop is further away from it. On the other hand, if the one starts extremely far away from , say with , then the expected value after on loop is higher. This implies that after many loops, the expectation converges, and so does with the number of loops around . Assuming that for enough initial points, Theorem 6 can be used with at points and to prove the following conjecture.

Conjecture 1.

6 Concluding remarks

This contribution attempts to draw the attention of dynamical system analysis onto macroeconomic models. Before looking into complex models of finance and crises, e.g. [5, 11, 15], we focus here on a Brownian perturbation added into a non-linear version of the Lotka-Volterra system used in Economics, the Goodwin model. To begin with, we recall the usual results for the deterministic planar oscillator: we provide the constant Entropy function and describe the period of the closed orbits drawned by the system. We then provide sufficient conditions for the stochastically perturbed system to stay in the meaningful domain which is a a bounded subset of for the -component. The entropy function is actually of great use for the last result, additionally to prior estimates on variations of the system.

We finally prove what seems a fundamental and staightforward property of the system, namely that a solution rotates with perturbations around a unique point . The definition of stochastic orbits provided here conventienly suits the intuition of how the deterministic concept can be extended. However it has clearly not the ambition to be a definitive concept and further investigations might confirm its usefulness or its precarity. The proof exploits the concept of reccurent domains in an intensive manner.

Acknowledgment

Both authors want to thank Matheus Grasselli for leading ideas and presentation suggestion. Remaining errors are authors responsibility.

References

- [1] M. Arató, A famous nonlinear stochastic equation (Lotka-Volterra model with diffusion), Mathematical and Computer Modelling, 38.7 (2003), 709–726.

- [2] A. Bahar and X. Mao, Stochastic delay Lotka–Volterra model, Journal of Mathematical Analysis and Applications, 292.2 (2004), 364–380.

- [3] S.M. Bartlett, On theoretical models for competitive and predatory biological systems, Biometrika, 44.1 (1957), 27–42.

- [4] G.Q. Cai and Y. K. Lin. Stochastic analysis of the Lotka-Volterra model for ecosystems, Physical Review E, 70.4 (2004), 041910.

- [5] B. Costa-Lima, M. R. Grasselli, X. S. Wangb and J. Wub, Destabilizing a stable crisis: employment persistence and government intervention in macroeconomics, to appear in Structural Change and Economic Dynamics, 2014.

- [6] M. Desai, B. Henry, A. Mosley and M. Pemberton, A clarification of the Goodwin model of the growth cycle, Journal of Economic Dynamics and Control, 30.12 (2006), 2661–2670.

- [7] C.L. Evans, (1992). Productivity shocks and real business cycles, Journal of Monetary Economics, 29.2 (1992), 191–208.

- [8] P. Flaschel, Some stability properties of Goodwin’s growth cycle a critical elaboration, Journal of Economics, 44.1 (1984), 63–69.

- [9] J. Glombowski and M. Krüger, Generalizations of Goodwin’s growth cycle model, Univ., FB Sozialwiss., 1986.

- [10] R.M. Goodwin, A growth cycle, Socialism, capitalism and economic growth (1967), 54–58.

- [11] M.R. Grasselli and B. Costa Lima, An analysis of the Keen model for credit expansion, asset price bubbles and financial fragility, Mathematics and Financial Economics, 6.3 (2012), 191–210.

- [12] G. D. Hansen, Indivisible labor and the business cycle, Journal of monetary Economics, 16.3 (1985), 309–327.

- [13] D. Harvie, Testing Goodwin: growth cycles in ten OECD countries, Cambridge Journal of Economics, 24.3 (2000), 349–376.

- [14] S.B. Hsu, A remark on the period of the periodic solution in the Lotka-Volterra system, Journal of Mathematical Analysis and Applications, 95.2 (1983), 428–436.

- [15] S. Keen, Finance and economic breakdown: modeling Minsky’s financial instability hypothesis, Journal of Post Keynesian Economics, 17.4 (1995), 607–635.

- [16] E. Kiernan and D.B. Madan, Stochastic stability in macro models, Economica (1989), 97–108.

- [17] R.Z. Khasminskii, Stochastic stability of differential equations, 2nd Ed. (Springerverlag Berlin Heidelberg), 2012.

- [18] R.Z. Khasminskii and F.C. Klebaner, Long term behavior of solutions of the Lotka-Volterra system under small random perturbations, The Annals of Applied Probability, 11.3 (2001), 952–963.

- [19] M. Liu and K. Wang, Stochastic Lotka–Volterra systems with Lévy noise, Journal of Mathematical Analysis and Applications, 410.2 (2014), 750–763.

- [20] X. Mao, G. Marion G. and E. Renshaw, Environmental Brownian noise suppresses explosions in population dynamics, Stochastic Processes and Their Applications, 97.1 (2002), 95–110.

- [21] X. Mao, S. Sabanis and E. Renshaw, Asymptotic behaviour of the stochastic Lotka-Volterra model, Journal of Mathematical Analysis and Applications, 287.1 (2003), 141–156.

- [22] S. Mohun and R. Veneziani, Goodwin cycles and the US economy, 1948-2004, 2006.

- [23] M. Neamtu, G. Mircea, M. Pirtea and D. Opris, The study of some stochastic macroeconomic models, Proceedings of the 11th WSEAS international conference on Applied Computer and Applied Computational Science (2012), 172–177.

- [24] D. Nguyen Huu and S. Vu Hai, Dynamics of a stochastic Lotka-Volterra model perturbed by white noise, Journal of mathematical analysis and applications, 324.1 (2006), 82–97.

- [25] T. Reichenbach, M. Mobilia, and E. Frey, Coexistence versus extinction in the stochastic cyclic Lotka-Volterra model, Physical Review E, 74.5 (2006), 051907.

- [26] J.G. Simmonds, J.G. A first look at perturbation theory, Courier Dover Publications, 1998.

- [27] U.H. Thygesen, U. H. (1997). A survey of Lyapunov techniques for stochastic differential equations, IMM, Department of Mathematical Modeling, Technical University of Denmark, working paper, 1997. Available at http://www.imm.dtu.dk

- [28] K. Velupillai, Some stability properties of Goodwin’s growth cycle, Journal of Economics, 39.3 (1979), 245–257.

- [29] R. Veneziani and S. Mohun, Structural stability and Goodwin’s growth cycle, Structural Change and Economic Dynamics, 17.4 (2006), 437–451.

- [30] C. Zhu and G. Yin, On competitive Lotka-Volterra model in random environments, Journal of Mathematical Analysis and Applications, 357.1 (2009), 154–170.

- [31] C. Zhu and G. Yin, On hybrid competitive Lotka-Volterra ecosystems, Nonlinear Analysis: Theory, Methods & Applications, 71.12 (2009), e1370–e1379.