=15pt

![[Uncaptioned image]](/html/1309.5073/assets/x1.png)

ECOLE CENTRALE

DES ARTS ET MANUFACTURES

T H E S E

présentée par

Rémy Chicheportiche

pour l’obtention du

grade de Docteur

Specialité :

Mathématiques appliquées

Laboratoire :

Mathématiques Appliquées aux Systèmes (MAS) — EA 4037

Sujet :

Dépendances non linéaires en finance

soutenue le 27 juin 2013 devant un jury composé de:

Directeurs :

Frédéric Abergel -

Ecole Centrale Paris

Anirban Chakraborti -

Ecole Centrale Paris

Rapporteurs :

Yannick Malevergne -

Ecole de Management de Lyon

Grégory Schehr -

Université de Paris-Sud

Examinateurs :

Jean-Philippe Bouchaud -

Capital Fund Management

Jean-David Fermanian -

CREST

![[Uncaptioned image]](/html/1309.5073/assets/x2.png)

ECOLE CENTRALE

DES ARTS ET MANUFACTURES

PARIS

P H D T H E S I S

to obtain the title of

PhD of Science

Specialty : Applied Mathematics

Non-linear Dependences in Finance

Defended by

Rémy Chicheportiche

on June 27 2013

Advisors : Frédéric Abergel - Ecole Centrale Paris Anirban Chakraborti - Ecole Centrale Paris Reviewers : Yannick Malevergne - Ecole de Management de Lyon Grégory Schehr - Université de Paris-Sud Examinators : Jean-Philippe Bouchaud - Capital Fund Management Jean-David Fermanian - CREST

\dominitoc

Dépendances non-linéaires en finance

Résumé:

La thèse est composée de trois parties.

La partie I introduit les outils mathématiques et statistiques appropriés pour l’étude des dépendances,

ainsi que des tests statistiques d’adéquation pour des distributions de probabilité empiriques.

Je propose deux extensions des tests usuels lorsque de la dépendance est présente dans les données,

et lorsque la distribution des observations a des queues larges.

Le contenu financier de la thèse commence à la partie II.

J’y présente mes travaux concernant les dépendances transversales entre les séries chronologiques

de rendements journaliers d’actions, c’est à dire les forces instantanées qui relient plusieurs actions entre elles

et les fait se comporter collectivement plutôt qu’individuellement.

Une calibration d’un nouveau modèle à facteurs est présentée ici,

avec une comparaison à des mesures sur des données réelles.

Finalement, la partie III étudie les dépendances temporelles dans des séries chronologiques individuelles,

en utilisant les mêmes outils et mesures de corrélations.

Nous proposons ici deux contributions à l’étude du “volatility clustering”, de son origine et de sa description:

l’une est une généralisation du mécanisme de rétro-action ARCH dans lequel les rendements sont auto-excitants,

et l’autre est une description plus originale des auto-dépendances en termes de copule.

Cette dernière peut être formulée sans modèle et n’est pas spécifique aux données financières.

En fait, je montre ici aussi comment les concepts de récurrences, records, répliques et temps d’attente,

qui caractérisent la dynamique dans les séries chronologiques, peuvent être écrits dans la cadre unifié des copules.

Mots-clés:

dépendances statistiques, copules, tests d’adéquation, processus stochastiques, séries temporelles, models financiers, volatility clustering

Non-linear dependences in finance

Abstract:

The thesis is composed of three parts.

Part I introduces the mathematical and statistical tools that are relevant for the study of dependences,

as well as statistical tests of Goodness-of-fit for empirical probability distributions.

I propose two extensions of usual tests when dependence is present in the sample data

and when observations have a fat-tailed distribution.

The financial content of the thesis starts in Part II.

I present there my studies regarding the “cross-sectional” dependences among the time series of daily stock returns,

i.e. the instantaneous forces that link several stocks together and

make them behave somewhat collectively rather than purely independently.

A calibration of a new factor model is presented here, together with a comparison to measurements on real data.

Finally, Part III investigates the temporal dependences of single time series,

using the same tools and measures of correlation.

I propose two contributions to the study of the origin and description of “volatility clustering”:

one is a generalization of the ARCH-like feedback construction where the returns are self-exciting,

and the other one is a more original description of self-dependences in terms of copulas.

The latter can be formulated model-free and is not specific to financial time series.

In fact, I also show here how concepts like recurrences, records, aftershocks and waiting times,

that characterize the dynamics in a time series can be written in the unifying framework of the copula.

Keywords:

statistical dependences, copulas, goodness-of-fit tests, stochastic processes, time series, financial modeling, volatility clustering

Remerciements / Acknowledgments

Mes premiers remerciements vont évidemment à Jean-Philippe Bouchaud, qui m’a offert l’opportunité de m’engager sur la voie du doctorat à un moment où j’en avais abandonné l’idée. Je lui suis infiniment reconnaissant pour ses encouragements répétés, la profonde confiance qu’il m’a accordée et pour son invraisemblable disponibilité.

Je remercie Frédéric Abergel, directeur de la Chaire de finance quantitative de l’École Centrale, pour avoir accepté la supervision académique de mon doctorat, et mis à ma disposition un environnement intellectuel et matériel favorable. Merci à Anirban Chakraborti pour sa co-supervision et son enthousiasme à me proposer de nouveaux projets.

J’adresse un remerciement particulier à mon jury de thèse: à Yannick Maleverge et Grégory Schehr pour avoir immédiatement accepté la tâche de relecteur, et à Jean-David Fermanian qui a porté un intérêt à mon travail.

Je veux aussi exprimer ma gratitude aux dirigeants de Capital Fund Management pour s’être impliqués dans une convention CIFRE et m’avoir procuré des conditions de travail des plus confortables, ainsi qu’à tous les collaborateurs avec qui j’ai eu la chance d’interagir. Je garderai longtemps le souvenir de la “salle des stagiaires” et de ses occupants plus ou moins éphémères, à commencer par Romain Allez et Bence Tóth qui y ont séjourné avec moi le plus longtemps.

Mes passages à l’École ont été l’occasion d’échanges (scientifiques ou non) avec les membres de la chaire et du laboratoire MAS, en particulier avec Damien Challet et les autres doctorants: Alexandre Richard, Aymen Jedidi, Ban Zheng, Fabrizio Pomponio, Nicolas Huth, avec qui j’ai le plus interagi. Qu’ils soient ici cordialement salués, de même que mes anciens camarades Michael Kastoryano, Nicolas Cantale, Liliana Foletti, Stefanie Stantcheva et David Salfati.

Je n’aurais sans doute pas d’autre occasion d’exprimer ma gratitude à toutes les figures qui ont marqué mon éducation. Qu’il me soit donc permis de rendre ici un hommage tardif à Mesdames Nelly Piguet, Regula Krattenmacher et Larissa Shargorodsky, Messieurs Didier Deshusses, Christian Charvin, Frederic Hermann, Elie Prigent et Bernard Delez, Monsieur Paco Carbonell, Maîtres Raymond Hyvernaud, Georges Léger, Jean-Marc Cagnet et Yanaki Altanov.

Je dédicace cette thèse à ma grande famille, proche et lointaine, qu’il est superflu de remercier.

Paris, juin 2013

List of publications and submitted articles

Published articles:

-

?

?

-

?

?

-

?

?

Pre-prints and submitted articles:

-

?

?

-

?

?

-

?

?

-

?

?

Work in progress, working papers and collaborations:

-

?

?

-

?

?

-

?

?

-

?

?

-

?

?

Chapter 0 Introduction

1 Introduction en français

1 Les marchés financiers comme systèmes complexes

L’économie présente des traits caractéristiques des systèmes complexes: un grand nombre de variables (individus, entreprises, contrats, maturités, etc.), des agents hétérogènes (d’où une difficulté à isoler des groupes), de l’information partielle et de l’aléa, de l’auto-organisation et des phénomènes spontanés (interactions fortes, non-perturbativité), une dynamique de réseau (entres banques, pays, contreparties, entreprises, etc.) et des interactions à longue portée, un quasi-continuum d’échelles de temps, de la non-stationnarité, des trajectoires avec mémoire et de l’exposition à des forces extérieures (régulations, catastrophes, etc.).

Cette réalité contraste fortement avec les hypothèses des théories économique et financière classiques, comme l’homogénéité (l’existence d’un agent représentatif), une rationalité parfaite, une capacité de prévision à horizon infini, un monde à l’équilibre dont les perturbations sont instantanément ajustées, l’absence de mémoire (toute l’information passée est reflétée dans l’état actuel du monde), …

Pour traiter ces enjeux sous un angle plus empirique, des communautés de chercheurs avec des points de vue différents ont progressivement investi le champ des sciences économiques et sociales. Parmi elles, on trouve des sociologues quantitatifs, des éconophysiciens, des statisticiens (physiciens statistiques ou biostatisticiens), des mathématiciens appliqués. En effet, beaucoup des traits listés ci-dessus ont déjà été étudiés en divers champs des sciences naturelles, où des méthodes ont été mises au point pour prendre en compte l’aléa, les interactions de réseaux, les comportements collectifs, la persistance et la réversion, etc. ????????

Parmi tous les champs de l’activité socio-économique, la finance de marché pourrait bien être le plus proche de ce que l’on peut raisonnablement étudier comme un système physique: du point de vue théorique, le nombre de degrés de liberté est quelque peu réduit par les règles des places de marché (mécanismes d’actions, carnets d’ordres, régulations, contrats standards, divulgation de l’information) alors que le nombre d’acteurs et d’actions reste assez large pour autoriser des moyennages dans des ensembles statistiques; et du point de vue empirique, la finance de marché génère des quantités astronomiques de données rendant possible la “répétition d’expériences” sous hypothèses, et le traitement des mesures avec des outils de statistique appropriés. En fait, il est établi que certaines propriétés des marchés financiers ressemblent à celles de systèmes étudiés en physique statistique: intermittence dans les écoulements turbulents, bruit de craquement de matériaux en réponse à un changement de conditions extérieures, lignes de fracture dans les solides, interactions à longue portée ou de champ moyen dans les systèmes de spins sur réseau, transitions de phases et criticalité spontanée, pour en citer quelques-unes.

2 Champ d’application de cette thèse

Cette thèse étudie les dépendances statistiques au sens général, aussi bien “transversalement” (entre variables aléatoires) que temporellement (réalisations successives d’une variable). Tous les résultats théoriques s’appliquent donc en principe à tout champ où plusieurs variables interagissent, ou où des processus stationnaires ont de la mémoire. Plus spécifiquement, l’étude est restreinte à des processus discrets avec des intervalles de temps équidistants, ce qui signifie que les séries chronologiques correspondantes sont échantillonnées et n’ont pas besoin d’être “marquées” temporellement.

En ce qui concerne le contenu appliqué, le focus est sur les données financières, plus précisément les séries chronologiques de prix (ou rendements) d’actions à la fréquence relativement basse du jour. Il s’agit principalement des prix des actions les plus liquides négociées sur les marchés états-uniens, et dont les historiques peuvent être téléchargés librement de plusieurs sources.

Propriétés statistiques, dépendances et dynamique

Les caractéristiques statistiques d’un ensemble de variables aléatoires sont de plusieurs ordres: propriétés distributionnelles, corrélations, et dynamique.

En certains endroits de cette thèse, les propriétés distributionnelles sont à l’étude: la distribution de probabilité empirique de mesures répétées est typiquement la première chose qu’un modèle doit reproduire. Concrètement, les quatre premiers moments d’une distribution sont très informatifs quant au phénomène à l’œuvre, mais une perspective d’ensemble précise n’est atteignable que si des outils puissants sont disponibles pour comparer les fonctions de répartition. Développer de tels outils est un des buts de ce travail de doctorat.

Les corrélations et la dynamique peuvent être étudiées comme deux faces d’une même pièce, comme des dépendances spatiales et temporelles. Elles peuvent être vues respectivement comme une manifestation de propagation horizontale d’information, ou d’incorporation de l’information passée dans les réalisations présentes. Ces dépendances sont le sujet principal de cette thèse, avec des applications en finance qui pourraient avoir d’importantes conséquences en gestion du risque.

Non-linéarités

Pour des raisons historiques et de commodité mathématique, les corrélations linéaires sont souvent considérées par les professionnels (et quelques fois aussi dans le monde académique et l’enseignement) comme l’alpha et l’oméga des dépendances. Cette description est satisfaisante tant que l’on se trouve dans un régime où de petites perturbations ont de petites conséquences, mais l’expérience enseigne que ce n’est pas toujours le cas. Souvent, des effets de seuil, de la latence et de la mémoire (hystérèse), des effects collectifs (avalanches), du chaos (sensibilité extrême aux conditions initiales), etc. peuvent générer des comportements anormaux, et il est alors nécessaire de faire attention aux non-linéarités dans les dépendances, en étudiant par exemple les probabilités d’évènements de queue joints, les corrélations conditionnelles, corrélations quadratiques, etc. Dans des situations extrêmes, les corrélations linéaires peuvent même être trompeuses pour la compréhension des interactions sous-jacentes, et comme l’a écrit D. Helbing, “un modèle non-linéaire simple peut être capable d’expliquer des phénomènes, que même des modèles linéaires compliqués peuvent échouer à reproduire. Les modèles non-linéaires pourraient apporter un éclairage nouveau sur les phénomènes sociaux. Ils pourraient même conduire à un changement de paradigme dans la manière dont nous interprétons la société.” ?

3 Plan général de la thèse, et principales contributions originales

La thèse est composée de trois parties. La partie 1 introduit les outils mathématiques et statistiques appropriés pour l’étude des dépendances. La plupart de ce qui y est présenté est connu, mais je passe en revue les définitions et propriétés principales. C’est aussi dans cette partie que j’introduis les notations que j’ai essayé de maintenir cohérentes tout au long de la thèse. J’ai passé beaucoup de temps à travailler sur des tests statistiques d’adéquation (“Goodness of Fit”, en anglais) pour des distributions de probabilité empiriques. Cela était originellement motivé par le besoin de tester les modèles bivariés finaux contre des hypothèses nulles. Ce “side project” initial s’est avéré être lié à un problème non-résolu et connu pour être difficile. Je n’apporte pas de solution définitive, mais discute en annexe de possibles directions pour des travaux futurs, qui ont émergé au cours de sessions de remue-méninges avec Jean-Philippe Bouchaud et Alexandre Richard. Pour autant, le sujet est fascinant, étant à la frontière de la théorie des probabilités (processus stochastiques) et la physique (particules quantiques dans des potentiels), et j’ai été intéressé de travailler sur d’autres extensions des tests d’adéquation usuels. Ce qui était censé n’être que le développement d’une boîte à outils pour un usage immédiat a finalement donné lieu à de très intéressants projets théoriques qui se sont concrétisés par la publication de deux articles et d’un chapitre de livre.

Le contenu financier de la thèse commence à la partie 2. J’y présente mes travaux concernant les dépendances transversales entre les séries chronologiques de rendements journaliers d’actions, c’est à dire les forces instantanées qui relient plusieurs actions entre elles et les fait se comporter collectivement plutôt qu’individuellement. Ce vaste sujet avait déjà été approché dans mon travail de master ?, où j’ai effectué une étude empirique des dépendances non-linéaires, et ai décrit une construction hiérarchique pour les modéliser. Une partie de ce travail a été publiée avec des développements consécutifs dans un journal de finance, et a servi de prémisse pour le modèle à facteur sur lequel j’ai finalement abouti au cours du doctorat. Une calibration de ce modèle est présentée ici, avec une comparaison aux données réelles.

Finalement, la partie 3 étudie les dépendances temporelles dans des séries chronologiques individuelles, en utilisant les mêmes outils et mesures de corrélations. Il est bien connu que les rendements d’actions ont une très faible auto-corrélation linéaire, ce qui se manifeste dans les alternances aléatoires de signes (rendements positifs ou négatifs), mais leurs amplitudes ont une longue mémoire. L’effet résultant de “volatility clustering” est une des plus anciennes énigmes en finance, et nous proposons ici deux contributions à l’étude de son origine et de sa description: l’une est une généralisation du mécanisme de rétro-action ARCH dans lequel les rendements sont auto-excitants, et l’autre est une description plus originale des auto-dépendances en termes de copule. Cette dernière peut être formulée sans modèle et n’est pas spécifique aux données financières. En fait, je montre ici aussi, après une longue collaboration avec Anirban Chakraborti, comment les concepts de récurrences, records, répliques et temps d’attente, qui caractérisent la dynamique dans les séries chronologiques, peuvent être écrits dans la cadre unifié des copules.

La thèse est rédigée au pluriel, car la plupart de son contenu est le fruit de collaborations (à tout le moins avec mes directeurs), et parce que j’y inclus beaucoup de matériel publié. Je renvoie aux articles listés en page List of publications and submitted articles et aux remerciements qu’ils contiennent pour l’identité de mes co-auteurs et collaborateurs sur chaque sujet.

2 Introduction in English

1 The financial markets as complex systems

The economy presents features that are characteristic of complex systems: a large number of variables (agents, firms, contracts, maturities, etc.), heterogeneous agents (difficulty to isolate groups), partial information and randomness, self-organization and emergent phenomena (strong interactions, non-perturbativity), network dynamics (among banks, countries, counter-parties, companies, etc.) and long-ranged interactions, quasi-continuum of time scales, non-stationarity, history dependence and sensitivity to external forces (regulations, catastrophes, etc.).

This reality is in sharp contrast with the hypotheses of classical economic and financial theory, like homogeneity (representative agent), perfect rationality, infinite horizon forecasting capabilities, steady-state world where perturbations of the equilibrium are instantaneously adjusted, absence of memory (all past information is reflected in the current state of the world), …

To address these issues with a more empirical perspective, different communities with diverse point of views have progressively invested the social and economic sciences. These include quantitative sociologists, econophysicists, statisticians (statistical physicists, biostatisticians), applied mathematicians and others. Indeed, many of the features listed above have already been encountered in various areas of natural sciences, where methods have been designed to account for randomness, network interactions, collective behaviors, persistence and reversion, etc. ????????

Among all the fields of socio-economic activity, market finance may however be the closest to what can be reasonably studied like a physical system: on the theoretical side, the number of degrees of freedom is somewhat reduced by the rules of the exchanges (auctions, order books, regulations, standard contracts, information disclosure) while the number of “players” and “actions” is still very large allowing for averaging in statistical ensembles; and on the empirical side, it produces huge amounts of data making it possible to “repeat experiments” under assumptions, and treat the measurements with appropriate statistical tools. In fact there are evidences that some properties of financial markets resemble those of systems studied in statistical physics: intermittency in turbulent flows, crackling noise of materials responding to changing external conditions, lines of fractures in solids, long-ranged or mean-field interactions in Ising spins systems, phase transitions and self-organized criticality, to name a few.

2 Field covered in the thesis

This thesis studies statistical dependences in a general sense, both cross-sectionally (between random variables) and temporally (successive realizations of one variable). All theoretical results thus apply in principle to any field where many variables are interacting or where stationary processes have memory. More specifically, the study is restricted to discrete processes with equidistant intervals, meaning that the corresponding series are sampled and need not be “time-stamped”.

As of the applied content, the focus is on financial data, more precisely time series of stock prices (or returns) at the rather low frequency of the day. Mainly, the prices of the most liquid stocks traded in US markets are used, whose histories can be downloaded freely from different sources.

Statistical properties, dependences and dynamics

The statistical characteristics of a set of random variables are of many kinds: distributional properties, correlations and dynamics.

In some places of this thesis, distributional properties are under the spotlights. As a matter of principle, the empirical probability distribution function of repeated measurement of a variable is the first thing a model should reproduce. Concretely, the first four moments of a distribution are much informative about the underlying phenomenon, but a precise global picture is only achieved if powerful tools are available to compare distribution functions. Developing such tools is one of the goals of this PhD work.

Correlations and dynamics can be studied as two faces of the same coin: they are spatial (or “cross-sectional”) dependences and temporal dependences, and can be regarded as a manifestation of horizontal information propagation, or incorporation of past information into current realizations, respectively. These dependences are the main subject of the present thesis, with applications in finance that could have important consequences in risk management.

Non-linearities

For historical reasons and mathematical convenience, linear correlations are often seen by practitioners (and sometimes also in academia and teaching) as the “be-all and end-all” of dependences. This works fine as long as small perturbations have small effects, but experience teaches that this is not always the case. Often, threshold effects, latency and memory (hysteresis), collective effects (avalanches), chaos (sensitivity to initial conditions) generate abnormal behavior, and it is necessary to care for non-linearities in dependences by studying, for example, tail joint probabilities, conditional correlations, quadratic correlations, etc. In extreme situations, linear correlations may even be misleading the understanding of the underlying interactions, and, as D. Helbing wrote, “a simple nonlinear model may explain phenomena, which even complicated linear models may fail to reproduce. Nonlinear models are expected to shed new light on […] social phenomena. They may even lead to a paradigm shift in the way we interpret society.” ?

3 Detailed outline of the thesis and main original contributions

The thesis is composed of three parts. Part 1 introduces the mathematical and statistical tools that are relevant for the study of dependences. Most of what is presented there is common knowledge, but I review the main definitions and properties for completeness and later usage. It is also the place where I introduce the notations, which I tried (but probably not succeeded completely) to keep coherent along the thesis. I have spent quite some time working on statistical tests of Goodness-of-fit for empirical probability distributions. This was originally motivated by the need to test the final multivariate models, or at least the bivariate marginals, against null hypotheses. This initial “side project” turned out to be a tough one and no definite solution is provided here — I still give in appendix an account of the literature and of some possible directions for future endeavor, that came out during brainstorming sessions with Jean-Philippe Bouchaud and Alexandre Richard. Yet the subject was fascinating, being at the frontier of probability theory (stochastic processes) and plain physics (quantum particles in potentials), and I was interested in working on other extensions of the usual GoF tests. What was supposed to be only the development of a toolkit for immediate use gave rise to very interesting theoretical projects and in fact led to the publication of two articles and a textbook chapter.

The financial content of the thesis starts in Part 2. I present there my studies regarding the “cross-sectional” dependences among the time series of daily stock returns, i.e. the instantaneous forces that link several stocks together and make them behave somewhat collectively rather than purely independently. Some work was already done in my Master’s thesis ?, where I performed an empirical study of non-linear dependences, and described a hierarchical construction to model them. Part of that work was published with subsequent developments in a financial journal, and served as a premise for the final factor model that I have come with. A calibration of this model is presented here, together with a comparison to measurements on real data.

Finally, Part 3 investigates the temporal dependences of single time series, using the same tools and measures of correlation. As is well known, stock returns have a vanishing linear autocorrelation that manifests itself in random sign alternations, but their magnitudes have a long memory. The resulting “volatility clustering” effect is one of the oldest puzzles in finance, and we propose here two contributions to the study of its origin and description: one is a generalization of the ARCH-like feedback construction where the returns are self-exciting, and the other one is a more original description of self-dependences in terms of copulas. The latter can be formulated model-free and is not specific to financial time series. In fact, I also show here, after a longstanding collaboration with Anirban Chakraborti and undergrad students at Ecole Centrale, how concepts like recurrences, records, aftershocks and waiting times, that characterize the dynamics in a time series can be written in the unifying framework of the copula.

After this brief non-technical overview of the landscape, I give below a more detailed outline with an abstract of each chapter. I quit now the first person and switch to the ‘we’ as most of what follows is the result of collaborations (at the very least with my advisors), and because I include much material of published work. I refer to the articles listed in page List of publications and submitted articles and acknowledgments therein for the identity of my co-authors on each topic.

Part I

-

I.2.

There exist many measures of dependence between random variables, some related to joint amplitudes, others related to joint occurrence probabilities. We recall the definition and properties of some of them, and introduce the unifying framework of the copula, an object that embeds all the linear and non-linear dependences that are invariant under a rescaling of the marginals, i.e. those that count joint occurrences. We then rewrite the important measures of dependences in terms of the copula, and suggest ways to efficiently visualize and compare them. An interesting point of comparison is the elliptical copula, that includes the Gaussian and Student cases. We define this class of multivariate distributions, and summarize its main features.

The content of this chapter needs not be read straight from the beginning, but can be accessed “on demand” when referred to, later in the text. The original material is limited to one theorem characterizing the asymptotic tail dependence coefficient of a Student pair.

-

I.3.

Usual goodness-of-fit (GoF) tests are designed for independent samples, and are not suited to investigate tail regions, because of the universal limit properties of the cumulative distribution functions. We extend the range of applicability of the GoF tests to these two cases. Section 1: Accurate tests for the extreme tails of empirical distributions is a very important issue, relevant in many contexts, including geophysics, insurance, and finance. We have derived exact asymptotic results for a generalization of the large-sample Kolmogorov-Smirnov test, well suited to testing a distribution with constant weight at any point of the domain, and in particular provide an improved resolution in the tail regions. In passing, we have rederived and made more precise the approximate limit solutions found originally in unrelated fields. Section 2: We revisit the Kolmogorov-Smirnov and Cramér-von Mises goodness-of-fit tests and propose a generalization to identically distributed, but dependent univariate random variables. We show that the dependence leads to a reduction of the “effective” number of independent observations. The generalized GoF tests are not distribution-free but rather depend on all the lagged bivariate copulas. Hence, a precise formulation of the test must rely on a modeled or estimated copula.

Part II

-

II.4.

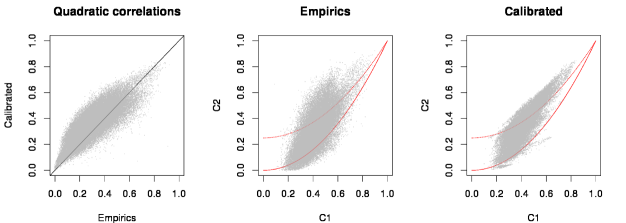

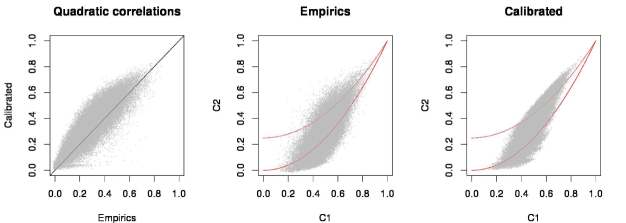

Using a large set of daily US and Japanese stock returns, we test in detail the relevance of Student models, and of more general elliptical models, for describing the joint distribution of returns. We find that while Student copulas provide a good approximation for strongly correlated pairs of stocks, systematic discrepancies appear as the linear correlation between stocks decreases, that rule out all elliptical models. Intuitively, the failure of elliptical models can be traced to the inadequacy of the assumption of a single volatility mode for all stocks. We suggest several ideas of methodological interest to efficiently visualize and compare different copulas. We identify the rescaled difference with the Gaussian copula and the central value of the copula as strongly discriminating observables. We insist on the need to shun away from formal choices of copulas with no financial interpretation.

-

II.5.

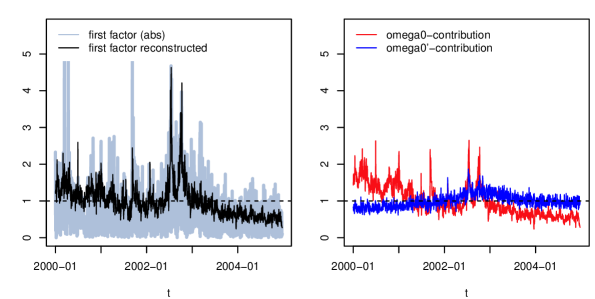

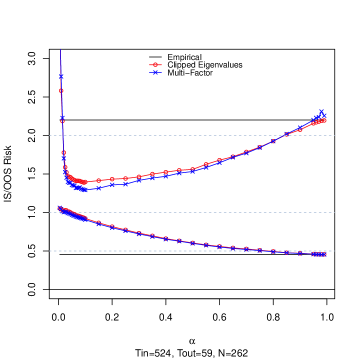

We propose a non-hierarchical multi-factor model for the joint description of daily stock returns. The model intends to better reproduce linear and non-linear dependences of empirical time series. The non-Gaussianity of the factors is an important ingredient of the model, that allows for the empirically observed anomalous copula at the medial point and other stylized facts (quadratic covariances, copula diagonals). A spectral analysis of the factor series suggests that a structure is present in the volatilities, with a dominant mode clearly affecting all linear factors and residuals. The model embedding this feature is calibrated on US stocks over several periods, and reproduces qualitatively all the non-trivial empirical observations. A systematic out-of-sample prediction over a long period confirms quantitatively the power of the model and of the proposed estimation methodology, both for linear and non-linear properties.

Part III

-

III.7.

We attempt to unveil the fine structure of volatility feedback effects in the context of general quadratic autoregressive (QARCH) models, which assume that today’s volatility can be expressed as a general quadratic form of the past daily returns. The standard ARCH or GARCH framework is recovered when the quadratic kernel is diagonal. The calibration of these models on US stock returns reveals several unexpected features. The off-diagonal (non ARCH) coefficients of the quadratic kernel are found to be highly significant both In-Sample and Out-of-Sample, but all these coefficients turn out to be one order of magnitude smaller than the diagonal elements. This confirms that daily returns play a special role in the volatility feedback mechanism, as postulated by ARCH models. The feedback kernel exhibits a surprisingly complex structure, incompatible with models proposed so far in the literature. Its spectral properties suggest the existence of volatility-neutral patterns of past returns. The diagonal part of the quadratic kernel is found to decay as a power-law of the lag, in line with the long-memory of volatility. Finally, QARCH models suggest some violations of Time Reversal Symmetry in financial time series, which are indeed observed empirically, although of much smaller amplitude than predicted. We speculate that a faithful volatility model should include both ARCH feedback effects and a stochastic component.

-

III.8.

A discrete time series is a collection of successive realizations of a random variable, every realization being conditional on the previous state. Seen collectively and ex ante, it can also be seen as one realization of a random vector with (directed) dependence. We show how the copula introduced in Part 1 in the context of cross-sectional dependences can also describe appropriately the non-linear temporal dependences in time series: in this context, we call them “self-copulas”.

-

III.9.

We introduce a specific, log-normal model for these self-copulas, for which a number of analytical results are derived. An application to financial time series is provided. As is well known, the dependence is to be long-ranged in this case, a finding that we confirm using self-copulas. As a consequence, the acceptance rates for GoF tests are substantially higher than if the returns were iid random variables.

Appendices

-

A.

Empirical counterparts of the copula (estimated together with the marginals on a sample of size ) have good properties only on discrete values in : for finite , the naive copula estimates are biased. We provide an approximate bias-correction mechanism.

-

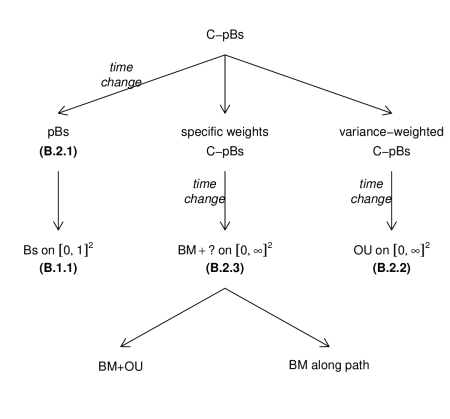

B.

Gaussian sheets (the generalization of Gaussian process indexed by two “times”) arise as limits of empirical multivariate cumulative distribution functions, when the sample size tends to infinity. Some properties of such sheets are of importance for distribution testing, since the Kolmogorov-Smirnov test statistic is related to the law of the supremum of their absolute value. We study some time changes and discretization schemes that may allow to reach a better knowledge of this law.

-

C.

Two contributions of methodological interest are made for models with a single common linear factor. In 11.A the estimator of optimal weights is found perturbatively in the limit of large dimension. In 11.B we reverse-engineer the constitution of the common factor, and embed the one-factor model in a hierarchical nested structure.

-

D.

We provide here technical details for the perturbative expansion of the pseudo-elliptical copula with log-normal scale around the independence copula, when all dependence parameters are small.

-

E.

Two appendices related to the continuous-time limit of the QARCH construction studied in Chapter 3.5. In 13.A we compute the exact spectrum of the Borland-Bouchaud model of Ref. ?, for three different kernel functions. In 13.B we relate the power-law behavior in the volatility correlation function, to the coefficient of the power-law decay in the kernel function of the FIGARCH model.

Part 1 Mathematical and statistical tools

Chapter 1 Characterizing the statistical dependence

1 Bivariate measures of dependence

In this first section, we recall several bivariate measures of statistical dependence between two random variables. Of course, as we discuss in the next section, many-points dependences among variables do not reduce to the pairwise dependences in the general case. But in the perspective of empirically measuring the dependences on a dataset, at least four issues motivate the present restriction to 2-points coefficients: (i) the number of triplets, quadruplets, etc. that should be considered when measuring coefficients of dependence involving 3-points, 4-points, etc. gets rapidly huge when considering even as few as some dozens of variables, whereas the number of undirected 2-points dependence coefficients is “only” ; (ii) error estimates on many-points coefficients are typically larger than on 2-points measures; (iii) in some classes of usual multivariate probability distributions, some information about the full structure can be inferred (or excluded) from the knowledge of the bivariate marginals; (iv) collective behavior and “effective” many-points dependences can be uncovered by collecting 2-points coefficients into a matrix or tensor and performing algebraic and spectral analysis.

Let be a random vector with joint probability distribution function (pdf) and joint cumulative distribution function (cdf) . Each component is a random variable with marginal pdf and cdf . Throughout the text (unless otherwise stated), we assume is continuous and are well-defined inverse marginal cdfs.

As the coefficients defined in this section are all measures of pairwise dependence, we define the pair . Similarly, all the transformations of defined later in the text can be restricted to the 2-dimensional space describing the pair.

1 Usual correlation coefficients

Bravais-Pearson’s correlation coefficient

The Bravais-Pearson’s correlation coefficient of is the usual normalized linear covariance

| (1) |

Often in what follows, it will be simply denoted . This correlation measure involves the probabilities and amplitudes of the possible realizations of . It can also be understood as a measure of asymmetry between the sum and the difference of the normalized variables:

| (1′) |

(the expression at the denominator is just an explicit way of writing the number ).

Spearman’s rho

Let be distributed like the -th marginal and independent of .Then the vector has independent components with the same marginals as . The difference is centered and has symmetric univariate marginals by construction. It allows to characterize the dependence in by counting how often both components of are simultaneously below the realizations of the independent couple with same marginals. Spearman’s rho is defined as

| (2) |

and thus involves only the signs of :

| (2′) |

Kendall’s tau

Let be a random vector with same joint distribution as : compared to the previous case, has not only the same univariate marginals as , but also its dependence structure. Then is the difference between two independent and identically distributed random vectors. It is centered and symmetric by construction. Kendall’s tau is defined as

| (3) |

and it measures concordances between realizations of identically distributed couples.

Blomqvist’s beta

Denote now . Blomqvist’s beta coefficient of dependence is defined as

| (4) |

If all ’s are centered around their median value (in particular if symmetric), then Blomqvist’s beta is equal to the Pearson’s correlation of the signs:

2 Non-linear correlation coefficients

Beyond the standard correlation coefficient, one can characterize the dependence structure through the correlation between functions of the random variables. In particular, we define the following coefficients:

| (5) | ||||

| (6) |

provided the variances in the denominators are finite. The case corresponds to the usual linear correlation coefficient, for which we will use the standard notation , whereas is the correlation of the squared returns, that would appear in the Gamma-risk of a -hedged option portfolio. However, high values of are expected to be very noisy in the presence of power-law tails (as is the case for financial returns) and one should seek for lower order moments, such as which also captures the correlation between the amplitudes (or the volatility) of price moves, or even that measures the correlation of the signs. Note that when , one recovers Spearman’s rho:

| (7) |

Proof of Eq. (7).

The LHS is decomposed onto four contributions:

Define then ; since , the RHS is

The result follows, noting that

and . ∎

Although the motivation of the definition (2) is quite intuitive (compare dependent and independent couples with same distributions), the definition of Spearman’s rho as Pearson’s correlation of the ranks makes it clear that it is invariant under any continuous stretching or shrinking of the axis, and that it involves the dependence structure regardless of the marginals.

3 Tail dependence

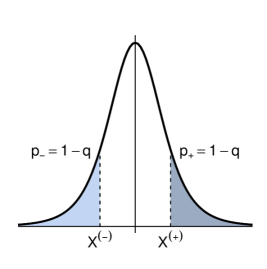

Another characterization of dependence, of great importance for risk management purposes, is the so-called coefficient of tail dependence which measures the joint probability of extreme events. More precisely, the upper tail dependence is defined as ??:

| (8) |

where is the cumulative distribution function (cdf) of , and a certain probability level. In spite of its seemingly asymmetric definition, it is easy to show that is in fact symmetric in . When , measures the probability that takes a very large positive value knowing that is also very large, and defines the asymptotic tail dependence. Random variables can be strongly dependent from the point of view of linear correlations, while being nearly independent in the extremes. For example, bivariate Gaussian variables are such that for any value of . The lower tail dependence is defined similarly:

| (9) |

and is equal to for symmetric bivariate distributions. One can also define mixed tail dependences:

with obvious interpretations.

2 Copulas

1 Definition and properties

A copula is a -variate cdf on the hypercube , with uniform univariate marginals.

Theorem (?).

A unique copula can be associated with any multivariate cdf by uniformizing its marginals:

According to this view, the copula of a random vector is the joint cdf of the marginal ranks . It hence encodes all the dependence between the individual random variables that is invariant under increasing transformations. Since the marginals of are uniform by construction, the copula only captures their degree of “entanglement”.

Of course, the converse of Sklar’s theorem is not true: infinitely many multivariate distributions can have the same copula ! In fact, it is in principle possible to build joint distributions with given copula and any univariate (continuous) marginals, for example a bivariate Gaussian copula with chi-2 marginals. Of course one sees that although possible, such exotic constructions barely make sense, as one would intuitively expect that random variables with positive support do not have a copula with the reversal symmetry .

Construction

A copula can be constructed in three manners: where (the generator function) is times continuously differentiable, and such that and is decreasing convex (more on this is Sect. 4, page 4).

Applying Sklar’s theorem to usual classes of parametric multivariate distributions. Examples include the Gaussian copula

where is a symmetric positive definite matrix. And the more general Elliptically Contoured copulas, that we introduce in the coming Sect. 4. 3. Implicitly defined as the dependence function of a random vector described through a structural model. Example: factor models.

Fréchet-Hoeffding bounds

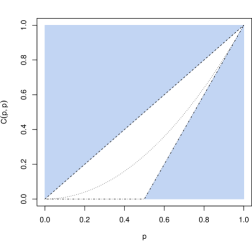

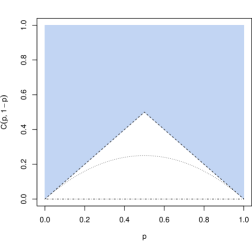

Copulas are multivariate cumulative distribution functions, and hence take values between 0 and 1, but there are in fact stronger constraints accounting for the properties of probability distributions. It is obvious that a univariate cdf tends to 0 at the extreme low values of its domain, and to 1 at the extreme high values, reflecting roughly the facts that the probability of an empty set is 0 and the probability of the whole universe is 1. Much in this spirit, the extreme values of the copulas are “pinned” to and . More precisely, if any component is 0, then the copula is 0, too. Furthermore, by reduction to the univariate marginals, if all but one components are 1, then the copula takes the value of the remaining component. Beyond these properties related to the marginals, the copula is subject to bounds imposed by the dependence structure: in short, a random pair cannot be more positively correlated than if it was built of twice the same variable, and similarly it cannot be more negatively correlated than if it was composed of a variable and its own opposite. This is more precisely stated by the following inequalities, for a copula of arbitrary dimension:

| (10) |

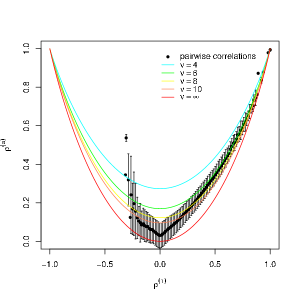

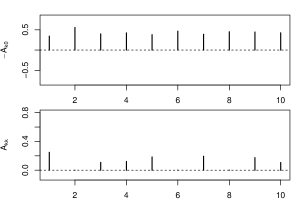

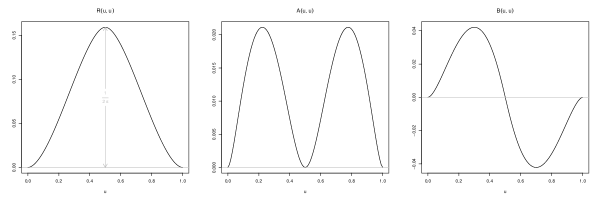

where the definitions of the upper and lower bounds were given in the previous page. We show in Fig. 1 how these bounds look like on the diagonal and anti-diagonal of a bivariate copula.

2 Dependence coefficients and the copula

The copula can be restricted to subsets of the studied random vector. For example, the bivariate copula of any random pair is

| (11) |

It is then natural to ask if and how all the coefficients of bivariate dependence introduced earlier are related to the description in terms of copula. It turns out that, whereas the ’s and ’s depend on the marginal distributions, Spearman’s rho, Kendall’s tau and Blomqvist’s beta can be expressed in terms of the copula only:

Similarly, the tail dependence coefficients can be expressed, for , as:

| (12a) | ||||||

| (12b) | ||||||

3 Visual representations

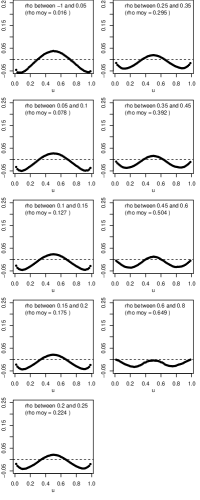

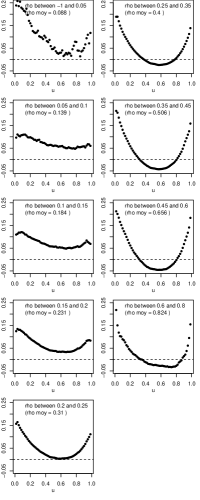

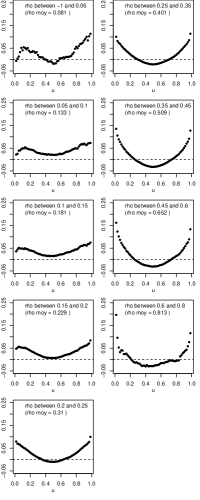

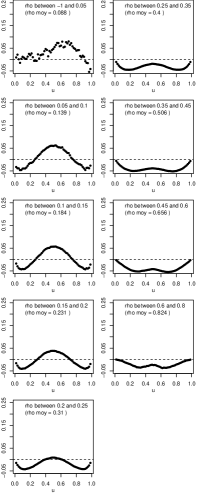

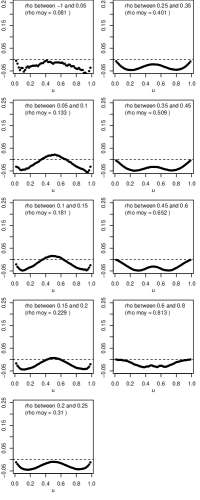

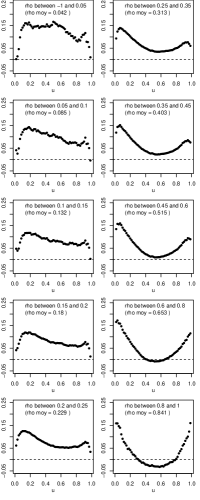

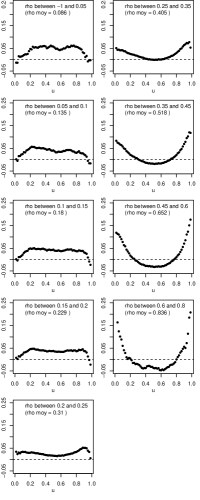

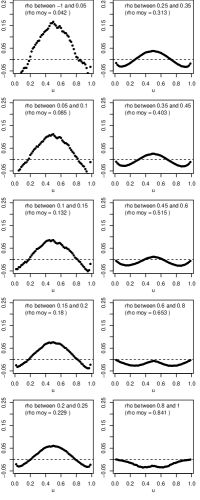

Copulas are not easy to visualize, first because they need to be represented as 3D plots of a surface in two dimensions and second because the bounds (10), within which is constrained to live, compress the difference between two arbitrary copulas — the situation is even worse in higher dimensions. Estimating copula densities, on the other hand, is even more difficult than estimating univariate densities, especially in the tails. We therefore propose to focus on the diagonal of the copula, and the anti-diagonal, , that capture part of the information contained in the full copula, and can be represented as 1-dimensional plots. Furthermore, in order to emphasize the difference with the case of independent variables, it is expedient to consider the following quantities:

| (13a) | ||||

| (13b) | ||||

where the normalization is chosen such that the tail correlations appear naturally. Another important reference point is the Gaussian copula , and we will consider below the normalized differences along the diagonal and the anti-diagonal:

| (14) |

The incentive to focus on the diagonals of the copula is motivated in the first place by the above argument that the whole copula is a particularly complex object that is hard to manipulate, estimate and visualize, and that some means have to be found in order to investigate its subtleties while reducing the number of parameters. But it also has a profound meaning in terms of physical observables that can be empirically measured. In particular, the diagonal quantity (13a) tends to the asymptotic tail dependence coefficients when ( when ). Similarly, the anti-diagonal quantity (13b) tends to as and to as . This still holds for the alternative definition in Eq. (14): tend to the asymptotic tail dependence coefficients in the limits and , owing to the fact that these coefficients are all zero in the Gaussian case. As we show in Chapter 3.6, the diagonal copula plays also an important role in the characterization of temporal dependences in time series: observables such as recurrence times, sequences lengths, waiting times, etc. are fundamentally many-points objects, and their statistics are characterized by the diagonal -points copulas.

The center-point of the copula, , is particularly interesting: it is the probability that both variables are simultaneously below their respective median. For bivariate Gaussian variables, one can show that:

| (15) |

where is the sign correlation coefficient defined on page 2. The trivial but remarkable fact is that the above expression holds for any elliptical models, that we define and discuss in the next section. This will provide a powerful test to discriminate between empirical data and a large class of copulas that have been proposed in the literature.

Generalized Blomqvist’s beta

We report for completeness a possible multivariate generalization of the bivariate Blomqvist’s beta, proposed in Ref. ?:

| (16) |

where is the survival copula defined similarly to Eq. (Theorem) as

has an immediate interpretation as a normalized distance between and : it measures the effective global departure from independence normalized by the maximum departure from independence. When and the copula is symmetric, it also nicely interpolates between several of the coefficients defined above, for example

4 A word on Archimedean copulas

In the universe of all possible copulas, a particular family has become increasingly popular in finance: that of “Archimedean copulas”. These copulas are defined as follows ?:

| (17) |

where is a function such that and is decreasing and completely monotone. For example, Frank copulas are such that where is a real parameter, or Gumbel copulas, such that , . The asymptotic coefficient of tail dependence are all zero for Frank copulas, whereas (and all other zero) for the Gumbel copulas. The case of general multivariate copulas is obtained as natural generalization of the above definition.

One can of course attempt to fit empirical copulas with a specific Archimedean copula. By playing enough with the function , it is obvious that one will eventually reach a reasonable quality of fit. What we take issue with is the complete lack of intuitive interpretation or plausible mechanisms to justify why the returns of two correlated assets should be described with Archimedean copulas. This is particularly clear after recalling how two Archimedean random variables are generated: first, take two random variables . Set with . Now, set:

| (18) |

and finally write and to obtain the two Archimedean returns with the required marginals and ??. Unless one finds a natural economic or micro-structural interpretation for such a labyrinthine construction, we content that such models should be discarded a priori, for lack of plausibility. In the same spirit, one should really wonder why the financial industry has put so much faith in Gaussian copulas models to describe correlation between positive default times, that were then used to price CDO’s and other credit derivatives. We strongly advocate the need to build models bottom-up: mechanisms should come before any mathematical representation (see also ? and references therein for a critical view on the use of copulas).

3 Assessing temporal dependences

In the context of discrete time series, where is a time index and (, say), the realization of the random variable occurs after that of . Nevertheless, before is realized, the a priori probability distribution of is not conditional but joint to that of , and it is possible to use all the measures of dependence defined above in this context.

For example, is the coefficient of linear auto-correlation at lag : it says in essence “how much of is expected to be reproduced, time steps later, in the realization of ”. When positive, it indicates persistence, while reversion is revealed by negative autocorrelation.

Blomqvist’s beta (defined in Eq. (4), page 4) is somehow more intuitive, as it quantifies directly the difference in probability that the signs will persist or alternate.

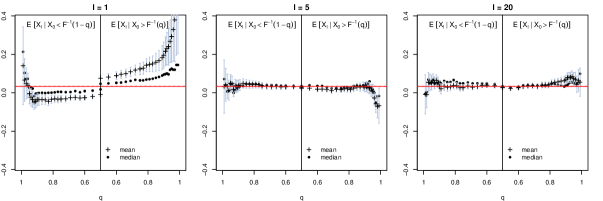

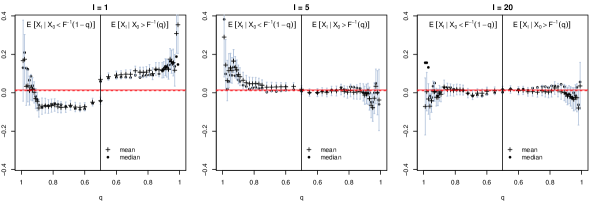

When one wants to be more specific in the characterization of temporal dependences and study for example the persistence and reversion probabilities of one realization of arbitrary magnitude, one needs to resort to the copula. Typically, persistence of extreme events (-th quantile, where is close to 1) separated by a time lag is measured by the tail dependence coefficients and , while reversion of extreme events is measured by and . We will elaborate on the topic of copulas in time series in Chapter 6 of Part 3.

All these coefficients will typically be of decreasing amplitude as gets larger, reflecting the loss of memory as time goes on and randomness comes in. There nevertheless exist systems where the -dependence is not monotonous but rather exhibits oscillations due to periodic activity (see for example the rising interest in electroencephalogram data analysis).

4 Review of elliptical models

1 General elliptical models

An elliptical distribution is characterized by a location parameter , a positive definite dispersion matrix and a function with positive support: let us denote this class by . Ellipticity of a random variable is a property of its characteristic function, as explicited in the following definition.

Definition.

| (19) |

The quadratic form in the argument of means that the points of constant characteristic function draw an ellipsoid in the Fourier space, whence the name (see ? for the construction and properties of elliptically contoured multivariate distributions). This definition in Fourier space is neither very convenient to build such variables, nor comfortable for its interpretation. The following theorem decomposes the elliptical random vector in terms of a uniformly distributed -dimensional sphere and a random radial scale.

Theorem (?).

If is a matrix with , and , then

| (20a) | |||

| The converse holds true and calls, for a positive definite of rank , | |||

| (20b) | |||

The class of elliptical distributions comprises the Gaussian and Student distributions:

-

1.

The Gaussian distribution: If the scaling variable has a chi-2 distribution with degrees of freedom, i.e. then the resulting is normally distributed:

-

2.

The Student distribution: As is well known, the quotient of a Gaussian variable over a chi-2 variable is Student-distributed. Hence,

As a consequence of the theorem above and the of the example 1, all elliptical random variables can be simply generated by multiplying standardized Gaussian random variables with a common random (strictly positive) factor , drawn independently from the ’s from an arbitrary distribution: ?

| (21) |

where is a location parameter, and .

Property (stability).

Let and be independent random vectors. Their sum is elliptical, too:

As an example, consider the difference of two independent and elliptical random vectors: Remark that the stability also holds whenever the random vectors and are dependent only through their radial part , see ?.

Property (bivariate marginals).

Let . Then, for all pair ,

In words, the bivariate marginals of a multivariate elliptical random variable are also elliptical, and inherit the parameters of the joint distribution.

This is clear from either representations (20) or (21). This property has an important converse: if the bivariate marginals are not elliptical with the same radial characteristic function, then the joint probability density is not elliptical. We will make use of this corollary in our empirical study of multivariate distribution for stock returns in Chapter 3 of Part 2.

2 Predicted dependence coefficients

The measures of dependence defined in Section 1 can be explicitly computed for elliptical models. Let and . Then

| (24a) | ||||

| (24b) | ||||

| (24c) | ||||

| (24d) | ||||

| (24e) | ||||

where and . Some remarks regarding these equations are of importance:

-

•

, and do not depend on (i.e. on ): they are invariant in the class of elliptical distributions with continuous marginals and given dispersion matrix .

-

•

No such invariance exists for Spearman’s rho (?) and for and !

- •

-

•

Relations (24e) and (24d) can be used to define alternative ways of measuring the correlation matrix elements . Indeed,

provide very low-moments (though slightly negatively biased) estimators — see ? for a study of . Said differently, it is always possible to define the effective correlation which, according to Eq. (15) and the subsequent discussion on page 15, can also be written as

(25) Now Eq. (24d) states together with Eq. (24a) that for all elliptical models, this effective correlation is just equal to the usual linear correlation ! This property provides a very convenient and simple testable prediction to check whether a given copula is compatible with an elliptical model or not, and will be at the heart of our empirical study in Chapters 3 and 4 of part 2.

-

•

is related to the kurtosis of the ’s through the relation .

The calculation of the tail correlation coefficients depends on the specific form of the function or, said differently, on the distribution of in Eq. (21), for which several choices are possible. We will focus in the following on two of them, corresponding to the Student model and the log-normal model.

The Gaussian ensemble

In the case of bivariate Gaussian variables of variance , i.e. when

all and all the coefficients of dependence depend on only ! For example, the quadratic correlation is given by:

| (26) |

whereas the correlation of absolute values is given by:

| (27) |

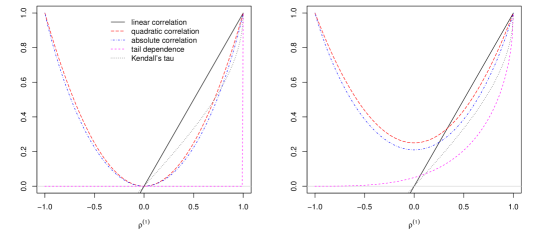

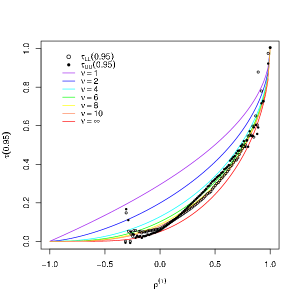

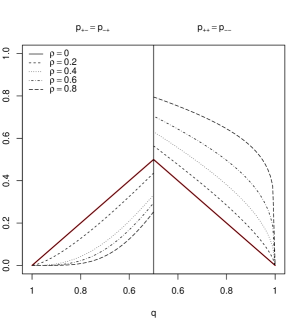

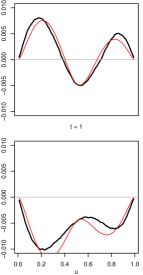

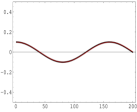

For some other classes of distributions, the higher-order coefficients and are explicit functions of the coefficient of linear correlation. This is for example the case of Student variables (see Fig. 2) and more generally for all elliptical distributions.

The Student ensemble

When the distribution of the square volatility is inverse Gamma, i.e. when

the joint pdf of the returns turns out to have an explicit form ???:

| (28) |

This is the multivariate Student distribution with degrees of freedom for random variables with dispersion matrix . Clearly, the marginal distribution of is itself a Student distribution with a tail exponent equal to , which is well known to describe satisfactorily the univariate pdf of high-frequency returns (from a few minutes to a day or so), with an exponent in the range (see e.g. Refs. ????). The multivariate Student model is therefore a rather natural choice; its corresponding copula defines the Student copula. For , it is entirely parameterized by and the correlation coefficient ().

The moments of are easily computed and lead to the following expressions for the coefficients :

| (29a) | ||||||

when (resp. ). Note that in the limit at fixed , the multivariate Student distribution boils down to a multivariate Gaussian. The shape of and for is given in Fig. 2.

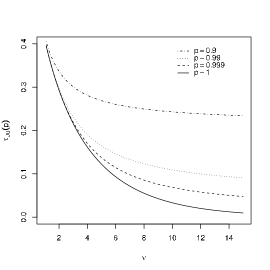

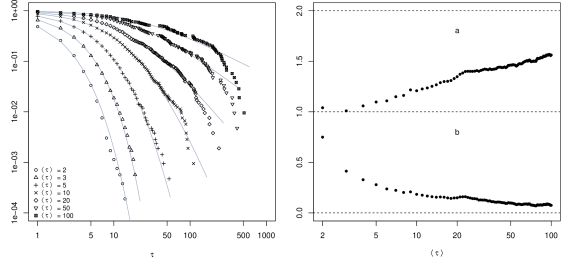

One can explicitly compute the coefficient of tail dependence for Student variables, which only depends on and on the linear correlation coefficient . By symmetry, one has . When with , the result is given by the following theorem:111 This result was simultaneously found by Manner and Segers ? (in a somewhat more general context). We still sketch our proof because it follows a different route (uses the copula), and the final expression looks quite different, although of course numerically identical.

Theorem (?).

Let follow a bivariate student distribution with degrees of freedom and correlation , and denote by the univariate Student cdf with degrees of freedom. The pre-asymptotic behavior of its tail dependence when is approximated by the following expansion in (rational) powers of :

| (30) |

with

where and .

The following Lemma, is needed for the proof of the Theorem:

Lemma.

Let and be like in the Theorem above, and . Define

Then,

| (31) |

Proof of the Lemma.

The proof proceeds straightforwardly by showing that when . The particular result for the limit case is stated in ?. ∎

Proof of the Theorem.

Recall from Eq. (12) that

| (32) |

One easily shows that

where the second equality holds in virtue of the aforementioned lemma.

Now, for close to , , and

But since the Student distribution behaves as a power-law precisely in the region , we write and immediately get . The result follows by collecting all the terms and performing the integration in (32). ∎

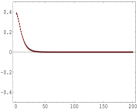

The notable features of the above results are:

-

•

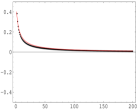

For large , the exponent is almost zero and the correction term is of order , and the expansion ceases to hold. This is particularly true for the Gaussian distribution () for which the behavior is radically different at the limit (where there’s strictly no tail correlation) and at where a dependence subsists, see Fig. 3(a).

-

•

The asymptotic tail dependence is strictly positive for all and finite , and tends to zero in the Gaussian limit (see Fig. 3(a)). The intuitive interpretation is quite clear: large events are caused by large occasional bursts in volatility. Since the volatility is common to all assets, the fact that one return is positive extremely large is enough to infer that the volatility is itself large. Therefore that there is a non-zero probability that another asset also has a large positive return (except if since in that case the return can only be large and negative!). It is useful to note that the value of does not depend on the explicit shape of provided the asymptotic tail of decays as , where is a slow function.

-

•

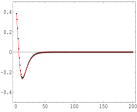

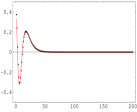

The coefficient is also positive, indicating that estimates of based on measures of at finite quantiles (e.g. ) are biased upwards. Note that the correction term is rapidly large because is raised to the power . For example, when and , and one expects a first-order correction for . This is illustrated in Figs. 3(a), 3(b). The form of the correction term (in ) is again valid as soon as decays asymptotically as .

-

•

Not only is the correction large, but the accuracy of the first order expansion is very bad, since the ratio of the neglected term to the first correction is itself . The region where the first term is accurate is therefore exponentially small in — see Fig. 3(b).

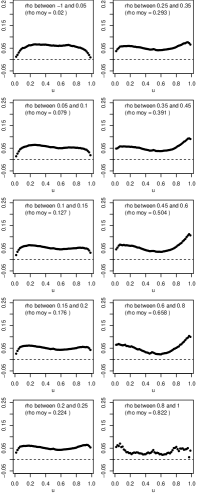

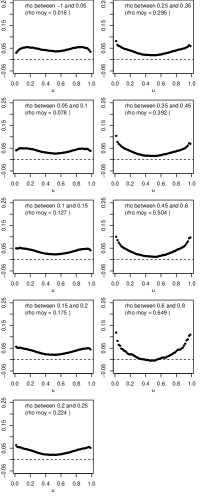

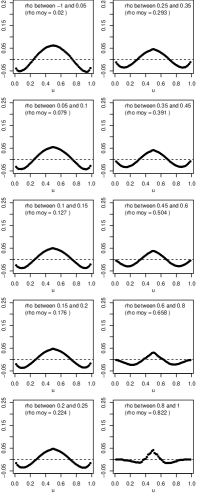

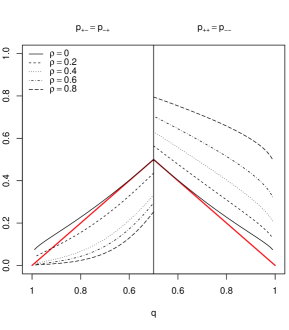

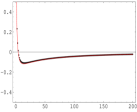

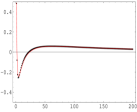

Finally, we plot in Fig. 4 the rescaled difference between the Student copula and the Gaussian copula both on the diagonal and on the anti-diagonal, for several values of the linear correlation coefficient and for . One notices that the difference is zero for , as expected from the expression of for general elliptical models. Away from on the diagonal, the rescaled difference has a positive convexity and non-zero limits when and , corresponding to and .

The log-normal ensemble

If we now choose with , the resulting multivariate model defines the log-normal ensemble and the log-normal copula. The factors are immediately found to be: with no restrictions on . The Gaussian case now corresponds to the limit .

Although the inverse Gamma and the log-normal distributions are very different, it is well known that the tail region of the log-normal is in practice very hard to distinguish from a power-law. In fact, one may rewrite the pdf of the log-normal distribution as:

| (33) |

where we have introduced . The above equation means that for large a log-normal is like a power-law with a slowly varying exponent. If the tail region corresponds to (say), the effective exponent lies in the range . Another way to obtain an approximate dictionary between the Student model and the log-normal model is to fix such that the coefficient (say) of the two models coincide. Numerically, this leads to , leading to for . In any case, our main point here is that from an empirical point of view, one does not expect striking differences between a Student model and a log-normal model — even though from a strict mathematical point of view, the models are very different. In particular, the asymptotic tail dependence coefficients or are always zero for the log-normal model (but or converge exceedingly slowly towards zero as ).

3 Pseudo-elliptical generalization

In the previous elliptical description of the returns, all stocks are subject to the exact same stochastic volatility, what leads to non-linear dependences like tail effects and residual higher-order correlations even for (see Fig. 2). In order to be able to fine-tune somewhat this dependence due to the common volatility, a simple generalization is to let each stock be influenced by an idiosyncratic volatility, thus allowing for a more subtle structure of dependence. More specifically, we write222 In vectorial form, we collect the individual (yet dependent) stochastic volatilities on the diagonal of a matrix , and can be decomposed as where is a random vector uniformly distributed on the unit hypersphere, the radial component is a chi-2 random variable independent of with degrees of freedom, and is a matrix with appropriate dimensions such that . This description can be contrasted with the one proposed in Ref. ? under the term “Multi-tail Generalized Elliptical Distribution”: with now depending on the unit vector . In other words, the description in provides a different radial amplitude for each component, whereas ? characterizes a direction-dependent radial part identical for every component. The latter allows for a richer phenomenology than the former, but lacks financial intuition.:

| (34) |

where the Gaussian residuals have the same joint distribution as before (in particular with linear correlations ), and are independent of the , but we now generalize the definition of the ratios . The random vector has a non trivial dependence structure which is partly described by the mixed -moments

| (35) |

When the ’s are dependent but identically distributed, the diagonal elements do not depend on . Within this setting, the generalization of coefficients (24b) can be straightforwardly calculated:

| (36a) | ||||

| (36b) | ||||

| (36c) | ||||

Importantly, Kendall’s tau and Blomqvist’s beta remain invariant in this class of Pseudo-elliptical distributions !

As an explicit example, we consider the natural generalization of the log-normal model and write , with333A further generalization that allows for stock dependent “vol of vol” is also possible. , and some correlation structure of the ’s: . One then finds:

| (37) |

Using the generic notation for the correlation of the log-volatilities, and for the correlation of the residuals (now different from ) we find:

| (38a) | ||||

| (38b) | ||||

| (38c) | ||||

When is fixed (e.g. for the elliptical case ), and are proportional, and all measures of non-linear dependences can be expressed as a function of . But this ceases to be true as soon as there exists some non trivial structure in the volatilities. In that case, and are “hidden” underlying variables, that can only be reconstructed from the knowledge of , , , assuming of course that the model is accurate.

Notice that the result on is totally independent of the structure of the volatilities444 This property holds even when depends on the sign of , which might be useful to model the leverage effect that leads to some asymmetry between positive and negative tails, as the data suggests.. Indeed, what is relevant for the copula at the central point is not the amplitude of the returns, but rather the number of events, which is unaffected by any multiplicative scale factor as long as the median of the univariate marginals is nil. An important consequence of this result is that for all elliptical or pseudo-elliptical model, implies that .

5 Conclusion

We have suggested several ideas of methodological interest to efficiently visualize and compare different copulas. We recommend in particular the rescaled difference with the Gaussian copula along the diagonal and the central value of the copula as strongly discriminating observables. We have studied the dependence of these quantities, as well as other non-linear correlation coefficients like the higher-order correlations , with the linear correlation coefficient .

The case of elliptical copulas is emphasized, with the lognormal and Student models as examples. We provide an original characterization of the pre-asymptotic tail dependence coefficient when as a development in rational powers of .

Chapter 2 Goodness-of-fit testing

The problem of testing whether a null-hypothesis theoretical probability distribution is compatible with the empirical probability distribution of a sample of observations is known as goodness-of-fit (GoF) testing and is ubiquitous in all fields of science and engineering. Goodness-of-Fit tests are designed to assess quantitatively whether a sample of observations can statistically be seen as a collection of realizations of a given probability law, or whether two such samples are drawn from the same hypothetical distribution.

The best known theoretical result is due to Kolmogorov and Smirnov (KS) ??, and has led to the eponymous statistical test for an univariate sample of independent draws. The major strength of this test lies in the fact that the asymptotic distribution of its test statistic is completely independent of the null-hypothesis cdf.

Several specific extensions have been studied (and/or are still under scrutiny), including: different choices of distance measures ?, multivariate samples ????, investigation of different parts of the distribution domain ????, dependence in the successive draws ?, etc.

This class of problems has a particular appeal for physicists since the works of Doob ? and Khmaladze ?, who showed how GoF testing is related to stochastic processes. Finding the law of a test amounts to computing a survival probability in a dissipative system. In a Markovian setting, this is often achieved by treating a Fokker-Planck problem, which in turn maps into a Schrödinger equation for a particle in a certain potential confined by walls.

1 Empirical cumulative distribution and its fluctuations

Let be a random vector of independent and identically distributed variables, with marginal cumulative distribution function (cdf) . One realization of consists of a time series that exhibits no persistence (see Sect. 2 when some non trivial dependence is present). The empirical cumulative distribution function

| (1) |

converges to the true CDF as the sample size tends to infinity. For finite , the expected value and fluctuations of are

The rescaled empirical CDF

| (2) |

measures, for a given , the difference between the empirically determined cdf of the ’s and the theoretical one, evaluated at the -th quantile. It does not shrink to zero as , and is therefore the quantity on which any statistic for GoF testing is built.

Limit properties

One now defines the process as the limit of when . According to the Central Limit Theorem (CLT), it is Gaussian and its covariance function is given by:

| (3) |

which characterizes the so-called Brownian bridge, i.e. a Brownian motion such that .

Interestingly, does not appear in Eq. (3) anymore, so the law of any functional of the limit process is independent of the law of the underlying finite size sample. This property is important for the design of universal GoF tests.

Norms over processes

In order to measure a limit distance between distributions, a norm over the space of continuous bridges needs to be chosen. Typical such norms are the norm-2 (or ‘Cramér-von Mises’ distance)

as the bridge is always integrable, or the norm-sup (also called the Kolmogorov distance)

as the bridge always reaches an extremal value.

Unfortunately, both these norms mechanically overweight the core values and disfavor the tails : since the variance of is zero at both extremes and maximal in the central value, the major contribution to indeed comes from the central region. To alleviate this effect, in particular when the GoF test is intended to investigate a specific region of the domain, it is preferable to introduce additional weights and study rather than itself. Anderson and Darling show in Ref. ? that the solution to the problem with the Cramér-von Mises norm and arbitrary weights is obtained by spectral decomposition of the covariance kernel, and use of Mercer’s theorem. They design an eponymous test ? with the specific choice of weights equal to the inverse variance, which equi-weights all quantiles of the distribution to be tested. We analyze here the case of the same weights, but with the Kolmogorov distance.

1 Weighted Kolmogorov-Smirnov tests

So again is a Brownian bridge, i.e. a centered Gaussian process on with covariance function given in Eq. (3). In particular, with probability equal to 1, no matter how distant is from the sample cdf around the core values. In order to put more emphasis on specific regions of the domain, we weight the Brownian bridge as follows: for given and , we define

| (6) |

We will characterize the law of the supremum :

1 The equi-weighted Brownian bridge: Kolmogorov-Smirnov

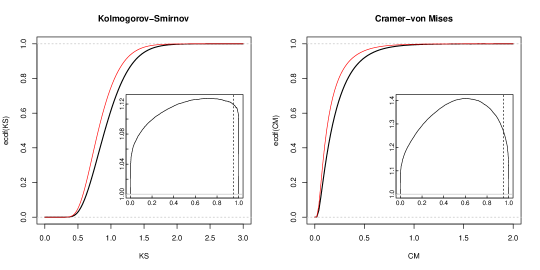

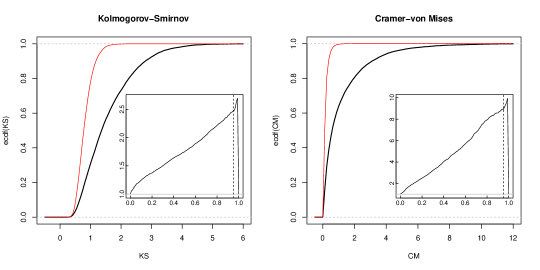

In the case of a constant weight, corresponding to the classical KS test, the probability is well defined and has the well known KS form ?:

| (7) |

which, as expected, grows from to as increases, see Fig. 5(a) on page 5(a). The value such that this probability is is ?. This can be interpreted as follows: if, for a data set of size , the maximum value of is larger than , then the hypothesis that the proposed distribution is a “good fit” can be rejected with confidence.

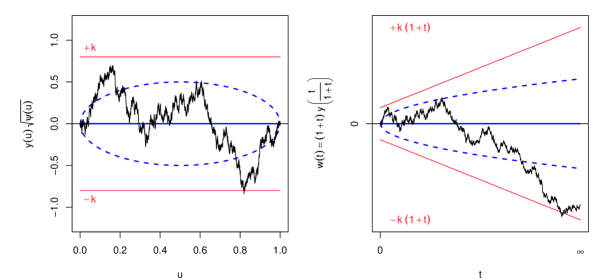

Diffusion in a cage with fixed walls

The Brownian bridge is nothing else than a Brownian motion with imposed terminal condition, and can be written as where is a Brownian motion. The test law is in fact the survival probability of in a cage with absorbing walls, and can be determined by counting the number of Brownian paths that go from 0 to 0 without ever hitting the barriers. More precisely, the survival probability of the Brownian bridge in the stripe can be computed as , where is the transition kernel of the Brownian motion within the allowed region, and it satisfies the simple Fokker-Planck equation

By spectral decomposition of the Laplace operator, the solution is found to be

and the free propagator in the limit is the usual

so that the survival probability of the constrained Brownian bridge is

| (10) |

Although it looks different from the historical solution Eq. (7), the two expressions can be shown to be exactly identical. First write the summand in Eq. (10) as the Fourier transform of . Then, adding a small imaginary part to allows to perform the summation of the series over , what makes poles appear in the integrand. Finally use Cauchy’s residue theorem to perform the integral, obtaining a sum over all residues evaluated at integer values of .

The computation of Kolmogorov’s distribution performed above is way easier than the canonical ones ?.

Diffusion in a cage with moving walls

An appropriate change of variable and time

leads to the problem of a Brownian diffusion inside a box with walls moving at constant velocity. Since the walls expand as faster than the diffusive particle can move (), the survival probability converges to a positive value, which turns out to be given by the usual Kolmogorov distribution (7) ?.

A way of addressing this problem of a diffusing particle in an expanding cage was suggested in Refs. ??. The time-dependent boundary conditions of the usual (forward) Fokker-Planck equation make it difficult to solve as such, and a nice way out is to consider instead the backward Fokker-Planck equation for the transition density, with the initial position of the absorbing wall as an additional independent variable ! This eliminates the time dependence in the boundary condition at the cost of introducing the initial wall parameter.

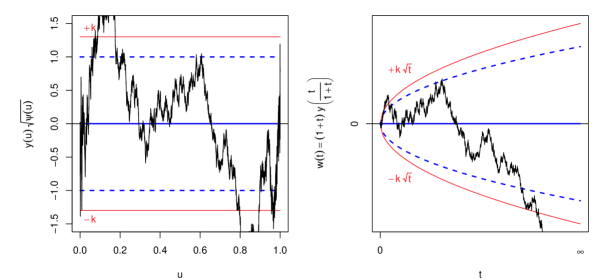

2 The variance-weighted Brownian bridge: accounting for the tails

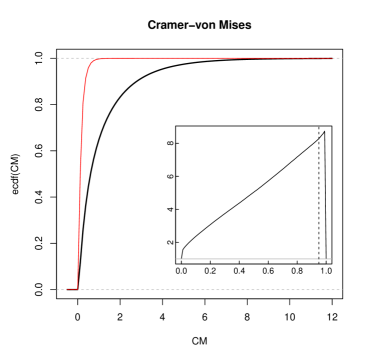

The classical KS test suffers from an important flaw: the test is only weakly sensitive to the quality of the fit in the tails of the tested distribution ??, when it is often these tail events (corresponding to centennial floods, devastating earthquakes, financial crashes, etc.) that one is most concerned with (see, e.g., Ref. ?).

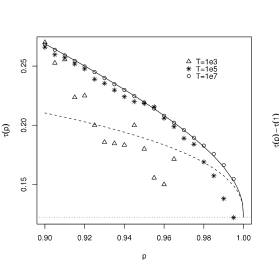

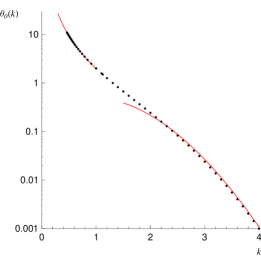

A simple and elegant GoF test for the tails only can be designed starting with digital weights in the form or for upper and lower tail, respectively. The corresponding test laws can be read off Eq. (5.9) in Ref. ?.111The quantity appearing there is the volume under the normal bivariate surface between specific bounds, and it takes a very convenient form in the unilateral cases and . Mind the missing exponentiating the alternating factor. Investigation of both tails is attained with (where ).

Here we rather focus on a GoF test for a univariate sample of size , with the Kolmogorov distance but equi-weighted quantiles, which is equally sensitive to all regions of the distribution.222Other choices of generally result in much harder problems. We unify two earlier attempts at finding asymptotic solutions, one by Anderson and Darling in 1952 ? and a more recent, seemingly unrelated one that deals with “life and death of a particle in an expanding cage” by Krapivsky and Redner ??. We present here the exact asymptotic solution of the corresponding stochastic problem, and deduce from it the precise formulation of the GoF test, which is of a fundamentally different nature than the KS test.

So in order to zoom on the tiny differences in the tails of the Brownian bridge, we weight it as explained in the introduction, with its variance