Spin Glasses and Nonlinear Constraints in Portfolio Optimization

Abstract

We discuss the portfolio optimization problem with the obligatory deposits constraint. Recently it has been shown that as a consequence of this nonlinear constraint, the solution consists of an exponentially large number of optimal portfolios, completely different from each other, and extremely sensitive to any changes in the input parameters of the problem, making the concept of rational decision making questionable. Here we reformulate the problem using a quadratic obligatory deposits constraint, and we show that from the physics point of view, finding an optimal portfolio amounts to calculating the mean-field magnetizations of a random Ising model with the constraint of a constant magnetization norm. We show that the model reduces to an eigenproblem, with solutions, where is the number of assets defining the portfolio. Also, in order to illustrate our results, we present a detailed numerical example of a portfolio of several risky common stocks traded on the Nasdaq Market.

Unlimited Analytics Inc.

Calgary, AB, Canada

mircea.andrecut@gmail.com

1 Introduction

Portfolio optimization is an important problem in economic analysis and risk management [1, 2], and under certain nonlinear constraints maps exactly into the problem of finding the ground states of a long-range spin glass [3, 4, 5]. The main assumption is that the return of any financial asset is described by a random variable, whose expected mean and variance are interpreted as the reward, and respectively the risk of the investment. The problem can be formulated as following: given a set of financial assets, characterized by their expected mean and their covariances, find the optimal weight of each asset, such that the overall portfolio provides the smallest risk for a given overall return. The standard mean-variance optimization problem has an unique solution describing the so called “efficient frontier” in the -plane [6]. The expected return is a monotonically increasing function of the standard deviation (risk), and for accepting a larger risk the investor is rewarded with a higher expected return. Recently it has been shown that the portfolio optimization problem containing short sales with obligatory deposits (margin accounts) is equivalent to the problem of finding the ground states of a long-range Ising spin glass, where the coupling constants are related to the covariance matrix of the assets defining the portfolio [3, 4, 5]. As a consequence of this nonlinear constraint, the solution consists of an exponentially large number of optimal portfolios, completely different from each other, and extremely sensitive to any changes in the input parameters of the problem. Therefore, under such constraints, the concept of rational decision making becomes questionable, since the investor has an exponential number of “options” to choose from. Here, we discuss the portfolio optimization problem using a quadratic formulation of the nonlinear obligatory deposits constraint. From the physics point of view, finding an optimal portfolio amounts to calculating the mean-field magnetizations of a random Ising model with the constraint of a constant magnetization norm. We show that the proposed model reduces to an eigenproblem, with solutions, where is the number of assets defining the portfolio. In support to our results, we also work out a detailed numerical example of a portfolio of several risky common stocks traded on the Nasdaq Market.

2 Nonlinear optimization model

A portfolio is an investment made in assets , with the expected returns , and covariances , . Let denote the relative amount invested in the -th asset. Negative values of can be interpreted as short selling. The variance of the portfolio captures the risk of the investment, and it is given by:

| (1) |

where is the vector of weights, and is the covariance matrix. Also, another characteristic of the portfolio is the expected return:

| (2) |

where is the vector of asset returns. The standard portfolio selection problem consists in finding the solution of the following multi-objective optimization problem [1,2,6]:

| (3) |

| (4) |

subject to the invested wealth constraint:

| (5) |

As mentioned in the introduction, this problem has an unique solution, which can be obtained using the method of Lagrange multipliers [1, 2, 6].

Recently it has been shown that by replacing the invested wealth constraint (5) with an obligatory deposits constraint the problem cannot be solved analytically anymore [3-5]. The constraint consists in imposing the requirement to leave a certain deposit (margin) proportional to the value of the underlying asset, and it has the form:

| (6) |

where is the fraction defining the margin requirement, and is the total wealth invested. As a direct consequence of the constraint’s nonlinearity, the problem has an exponentially large number of solutions:

| (7) |

where is a positive number depending on the portfolio return [3, 4, 5]. The solutions are also completely different from each other, and extremely sensitive to any changes in the input parameters of the problem. Thus, finding the global optimum becomes prohibitive (NP-problem) for a larger .

Let us now to reformulate this constraint using a quadratic function:

| (8) |

Thus, we impose the requirement to leave a certain deposit proportional to the quadratic value of the asset. This is equivalent to a constant norm . Also, we combine the multi-objective optimization problem into a single Lagrangian objective function as following:

| (9) |

where is the risk aversion parameter, and is the Lagrange parameter.

If then the solution corresponds to the portfolio with maximum return, without considering the risk. In this case the optimal solution will be formed only by the asset with the greatest expected return. The case with corresponds to the portfolio with minimum risk, regardless the value of the expected return. In this case the problem becomes:

| (10) |

with the solutions given by the equation:

| (11) |

This is a standard eigenproblem:

| (12) |

where is a symmetric matrix with real eigenvalues, and real eigenvectors. The eigenvector corresponding to the largest eigenvalue will provide the global optimum, since it will have the lowest risk.

Any value represents a tradeoff between the risk and return. In this case the solution corresponds to the critical point of the Lagrangian, which is also the solution of the following system of equations:

| (13) |

| (14) |

One can see that the Lagrangian objective function is equivalent to the free energy of an Ising model with random couplings and a random magnetic field . From the physics point of view, finding an optimal portfolio amounts to calculating the mean-field magnetizations of this random Ising model with the constraint of a constant magnetization norm. In the following we show that solving this system of equations reduces to an inhomogeneous eigenproblem.

From the first equation we have:

| (15) |

Introducing this result into the second equation we obtain:

| (16) |

The left-hand side of this equation is the Schur complement of the matrix:

| (17) |

Since this matrix must be singular (the Schur complement is zero), we have:

| (18) |

which reduces to:

| (19) |

Obviously, there is a vector such that:

| (20) |

This is an inhomogeneous eigenproblem [7], and it can be reduced further to a standard eigenproblem by introducing the following quantity:

| (21) |

such that we have:

| (22) |

By combining the last two equations into a matrix representation we obtain:

| (23) |

where

| (24) |

and

| (25) |

and , are the zero, and respectively identity matrices. This eigenproblem obviously has eigenvalues , that may be real or complex.

If is a real optimal portfolio, associated to a real eigenvalue, then the corresponding risk and return are given by:

| (26) |

In the above equation we have defined the return as the absolute value of the scalar product. This is a consequence of the fact that the eigenvectors can be determined only up to the sign value, i.e. both and are eigen-vectors corresponding to the same eigenvalue . This means that if the return is negative, we can simply change the sign , such that the return becomes positive.

The real and imaginary parts of the complex portfolios are also valid investment portfolios, however they are sub-optimal and may be discarded. Assuming that , where and , the risk and return of the real and respectively imaginary parts can be determined as following:

| (27) |

| (28) |

3 Numerical example

In order to illustrate the above results, we consider the case of a portfolio consisting of common stocks from IT industry:

| (29) |

A historical record of daily prices of these stocks for the last trading days was used to estimate the mean return and the covariance matrix.

The daily returns of the assets are calculated as:

| (30) |

where is the day index, and is the price of asset at the closing day . The estimate average returns and covariances are:

| (31) |

| (32) |

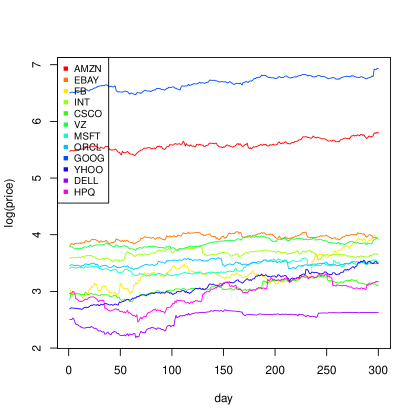

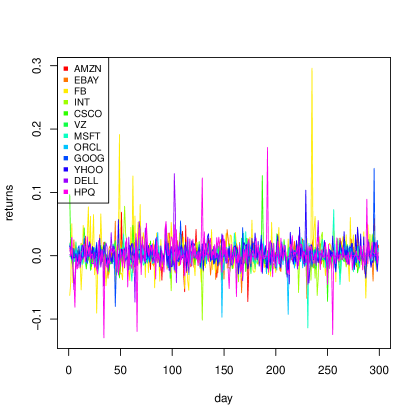

The time series of the asset prices for the considered time period are given in Figure 1. In Figure 2 we give also the expected daily returns of the assets.

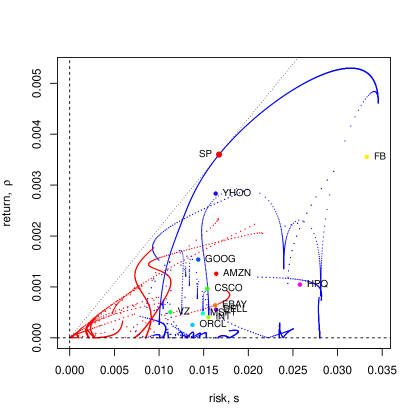

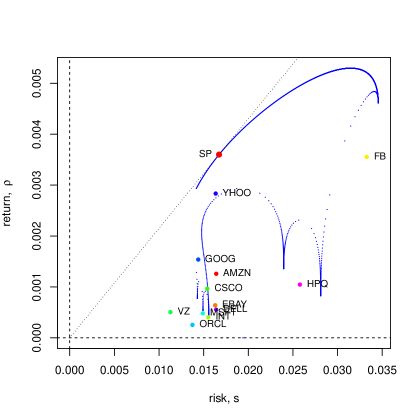

The risk aversion parameter was discretized as , , where . Also, the fraction defining the margin requirement was set to . Thus by solving the eigenproblem for each value of , one obtains eigenvalues and eigenvectors containing the weights of the portfolios. The risk-return, , representation of these complex solutions is shown in Figure 3, which also shows the risk-return values of the stocks included in the portfolio. The real contributions are shown in blue, while the imaginary contributions are shown in red. The pure real solutions, corresponding to the real eigenvalues are extracted in Figure 4. Here we also show the portfolio with the maximum Sharpe ratio , The Sharpe ratio represents the expected return per unit of risk [1,2]. The portfolio with maximum Sharpe ratio gives the highest expected return per unit of risk, and therefore is the most "risk-efficient" portfolio.

4 Conclusion

We have considered the portfolio optimization problem with the obligatory deposits constraint, when both long buying and short selling of a relatively large number of assets is allowed. Recently it has been shown that as a consequence of this nonlinear constraint, the solution consists of an exponentially large number of optimal portfolios, completely different from each other, and extremely sensitive to any changes in the input parameters of the problem, making the concept of rational decision making questionable. Here we have reformulated the problem using a quadratic obligatory deposits constraint, and we have shown that from the physics point of view, finding an optimal portfolio amounts to calculating the mean-field magnetizations of a random Ising model with the constraint of a constant magnetization norm. We have shown that the model reduces to an eigenproblem, with solutions, where is the number of assets defining the portfolio. Also, in order to illustrate our results, we have presented a detailed numerical example of a portfolio of several risky common stocks traded on the Nasdaq Market.

References

- [1] H. Markovitz, Portfolio selection: Efficient Diversification of Investments, Wiley, New York, 1959.

- [2] E.J. Elton, M.J. Gruber, S.J. Brown, W.N. Goetzmann, Modern Portfolio Theory and Investment Analysis, 8th ed., Wiley, New York, 2010.

- [3] S. Galluccio, J.-P. Bouchaud, M. Potters, Rational decisions, random matrices and spin glasses, Physica A 259, 449-456 (1998).

- [4] A. Gabor, I. Kondor, Portfolios with nonlinear constraints and spin glasses, Physica A 274, 222-228 (1999).

- [5] L. Bongini, M. Degli Esposti, C. Giardin, A. Schianchi, Portfolio optimization with short-selling and spin-glass, European Physics Journal B 27, 263–272 (2002).

- [6] G. Cornuejols, R. Tutuncu, Optimization Methods in Finance, Cambridge University Press, Cambridge, 2007.

- [7] R.M.M. Mattheij, G. Soderlind, On inhomogeneous eigenvalue problems. I, Linear Algebra and its Applications 88-89, 507-531 (1987).