Yash Deshpande

Department of Electrical Engineering, Stanford UniversityAndrea Montanari

Departments of Electrical Engineering and Statistics, Stanford University

Abstract

In sparse principal component analysis we are given noisy observations

of a low-rank matrix of dimension and seek to

reconstruct it under additional sparsity assumptions.

In particular, we assume here each of the principal components

has at most

non-zero entries. We are particularly interested in

the high dimensional regime wherein is comparable to, or even much larger

than .

In an influential paper, [JL04] introduced a simple

algorithm that estimates the support of the principal vectors

by the largest entries

in the diagonal of the empirical covariance.

This method can be shown to identify the correct support with high probability if

, and to fail with high probability if for two constants .

Despite a considerable amount of work over the last ten years, no

practical algorithm exists with provably better support recovery guarantees.

Here we analyze a covariance thresholding algorithm that was recently

proposed by [KNV13]. On the basis of numerical simulations (for the rank-one case),

these authors conjectured that covariance thresholding correctly recover the support with high probability for

(assuming of the same order as ).

We prove this conjecture, and in fact establish a more general guarantee including higher-rank

as well as much smaller than .

Recent lower bounds [BR13, MW15a] suggest that no polynomial time

algorithm can do significantly better.

The key technical component of our analysis develops new bounds on the norm of kernel

random matrices, in regimes that were not considered before. Using these, we also derive sharp bounds

for estimating the population covariance (in operator norm), and the principal component (in -norm).

1 Introduction

In the spiked covariance model proposed by [JL04], we are given data

with of the form111Throughout the paper, we follow the convention of denoting

scalars by lowercase, vectors by lowercase boldface, and

matrices by uppercase boldface letters.:

(1)

Here is a set of orthonormal vectors, that we want to

estimate, while and

are independent and identically distributed. The quantity is a measure of signal-to-noise ratio.

In the rest of this introduction, in order to simplify

the exposition, we will refer to the rank one case and drop the subscript .

Further, we will assume to be of the same order as .

Our results and proofs hold for a broad range of scalings of , , , and will be stated in general form.

The standard method of principal component analysis involves computing the

sample covariance matrix and estimates

by its principal eigenvector . It is a well-known

fact that, in the high dimensional regime, this yields an inconsistent estimate

(see [JL09]). Namely unless .

Even worse, [BBAP05] and [Pau07] demonstrate the

following phase transition

phenomenon. Assuming that , if the estimate is asymptotically

orthogonal to the signal, i.e. . On the other hand, for ,

remains bounded away from zero as .

This phase transition phenomenon has attracted considerable attention

recently within random matrix theory

[FP07, CDMF09, BGN11, KY13].

These inconsistency results motivated several efforts to exploit

additional structural information on the signal .

In two influential papers,

[JL04, JL09] considered the

case of a signal that is sparse in a suitable basis, e.g. in the

wavelet domain. Without loss of generality, we will assume here that

is sparse in the canonical basis , ….

In a nutshell, [JL09] propose the following:

1.

Order the diagonal entries of the Gram matrix

, and let

be the set of indices

corresponding to the largest entries.

2.

Set to zero all the entries of unless , and estimate with the principal eigenvector of the

resulting matrix.

Johnstone and Lu formalized the sparsity assumption by requiring that belongs to a weak -ball

with .

[AW09] studied

the more restricted case when every entry of has equal

magnitude of .

Within this restricted model, they proved

diagonal thresholding successfully recovers the support of

provided the sample size satisfies222Throughout the introduction, we write

as a shorthand of ‘ for a

some constant ’.

[AW09].

This result is a striking improvement over vanilla

PCA. While the latter requires a number of samples scaling with the

number of parameters , sparse PCA via diagonal thresholding achieves the

same objective with a number of samples that scales with the

number of non-zero parameters, .

At the same time, this result is not as strong as might have

been expected. By searching exhaustively over all possible supports

of size (a method that has complexity of order ) the correct

support can be identified with high probability as soon as . No method can succeed for much smaller

, because of information theoretic obstructions. We refer the reader

to [AW09] for more details.

Over the last ten years, a significant effort has been devoted to developing practical

algorithms that outperform diagonal thresholding, see e.g.

[MWA05, ZHT06, dEGJL07, dBG08, WTH09].

In particular, [dEGJL07] developed a

promising M-estimator based on a semidefinite programming (SDP)

relaxation. [AW09] also carried out an

analysis of this method and proved that, if333Throughout the paper,

we denote by constants that can depend on problem parameters

and . We denote by upper case (lower case ) generic absolute constants that

are bigger (resp. smaller) than 1, but which might change from line

to line.(i) , and (ii) the SDP solution has rank one, then the SDP

relaxation provides a

consistent estimator of the support of .

At first sight, this appears as a satisfactory solution of the

original problem.

No procedure can estimate the support of from less than samples, and the SDP relaxation succeeds in doing it from –at most– a constant

factor more samples.

This picture was upset by a recent, remarkable result by [KNV13] who showed that

the rank-one condition assumed by Amini and Wainwright

does not hold for . This

result is consistent with recent work of

[BR13] demonstrating that sparse PCA cannot be

performed in polynomial time in the regime , under

a certain computational complexity conjecture for the so-called

planted clique problem.

In summary, the sparse PCA problem demonstrates a fascinating

interplay between computational and statistical barriers.

From a statistical perspective,

and disregarding computational

considerations, the support of can be estimated consistently

if and only if . This can be done, for instance,

by exhaustive search over all the possible supports of

. We refer to [VL12, CMW+13] for a minimax analysis.

From a computational perspective,

the problem appears to be

much more difficult. There is rigorous evidence

[BR13, MW+15b, MW15a, WBS14]

that no polynomial

algorithm can reconstruct the support unless .

On the positive side, a very simple algorithm (Johnstone and Lu’s

diagonal thresholding) succeeds for .

Of course, several elements are still missing in this emerging

picture. In the present paper we address one of them, providing

an answer to the following question:

Is there a polynomial time algorithm that is guaranteed to solve

the sparse PCA problem with high probability for ?

We answer this question positively by analyzing a covariance

thresholding algorithm that proceeds, briefly, as follows.

(A precise, general definition, with some technical changes is given

in the next section.)

1.

Form the empirical covariance matrix and set to zero all its entries that

are in modulus smaller than , for a suitably

chosen constant.

2.

Compute the principal eigenvector of this thresholded

matrix.

3.

Estimate the support of by thresholding .

Such a covariance thresholding approach was proposed in

[KNV13], and is in turn related to earlier work by

[BL08b, CZZ+10]. The formulation

discussed in the next section presents some technical differences that

have been introduced to simplify the analysis. Notice that, to

simplify proofs, we assume to be known: this issue is discussed in

the next two sections.

The rest of the paper is organized as follows. In the next section we

provide a detailed description of the algorithm and state our main

results. The proof strategy for our results is explained in

Section 3. Our theoretical results assume full knowledge of problem

parameters for ease of proof. In light of this, in Section 4 we discuss a practical implementation

of the same idea that does not require prior knowledge of problem parameters, and is

data-driven. We also illustrate the method through simulations.

The complete proofs are in

Sections 5, 7 and 6 respectively.

A preliminary version of this paper appeared in [DM14].

This paper extends significantly the results in [DM14].

In particular, by following an analogous strategy, we improve greatly the

bounds obtained by [DM14]. This significantly improves the

regimes of on which we can obtain non-trivial results.

The proofs follow a similar strategy but are,

correspondingly, more careful.

2 Algorithm and main results

Algorithm 1 Covariance Thresholding

1:Input: Data , parameter

, ;

2:Compute the empirical covariance matrices ,

;

3:Compute (resp. );

4:Compute the matrix by soft-thresholding

the entries of :

5:Let be the first eigenvectors of ;

6:Output: .

We provide a detailed description of the covariance

thresholding algorithm for the general model (1) in Table 1.

For notational convenience, we shall assume that sample vectors are given (instead of ):

.

We start by splitting the data into two halves: and

and compute the respective sample covariance matrices and

respectively. Define to be the population covariance minus identity, i.e.

(2)

Throughout, we let and denote the support of and its size respectively,

for .

We further let and .

The matrix is used, in steps to to obtain a good estimate

for the low rank part of the population covariance .

The algorithm first computes , a centered version of the

empirical covariance as follows:

(3)

where is the sample covariance

matrix.

It then obtains the estimate

by soft thresholding each entry of at a threshold .

Explicitly:

(4)

Here is the soft thresholding function

(5)

In step of the algorithm, this estimate is used to construct good estimates of the

eigenvectors . Finally, in step , these estimates are combined with the (independent) second half of the data

to construct estimators for the support of the individual eigenvectors

. In the first two subsections we will focus on the estimation of

and the individual principal components. Our results on support recovery are provided

in the final subsection.

2.1 Estimating the population covariance

Our first result bounds the estimation error of the

soft thresholding procedure in operator norm.

Theorem 1.

There exist numerical constants such that the following happens.

Assume , and let . We

keep the thresholding level according to

(6)

. Then

with probability :

(7)

At this point,

it is useful to compare Theorem 1 with available results in the literature.

Classical denoising theory [DJ94, Joh15] provides upper bounds on the

estimation error of soft-thresholding. However, estimation error is measured by (element-wise) norm, while here we are interested

in operator norm.

[BL08a, BL08b, Kar08, CZZ+10, CL11] considered

the operator norm error of thresholding estimators for structured covariance matrices.

Specializing to our case of exact sparsity, the result of [BL08a] implies that, with high probability:

(8)

Here is the hard-thresholding function: , and the threshold is chosen to

be . Also, is the matrix obtained by thresholding the entries of .

In fact, [CZ+12] showed that the rate in (8) is minimax optimal over the class of sparse

population covariance matrices, with at most non-zero entries per row, under the

assumption .

Theorem 1 ensures consistency under

a weaker sparsity condition, viz.

is sufficient. Also, the resulting rate depends on instead of .

In other words, in order to achieve

for a fixed , it is sufficient as opposed to .

Crucially, in this regime for , Theorem 1 suggests a threshold of order

as opposed to which is used in

[BL08a, CZ+12].

As we will see in Section 3, this regime mathematically more challenging than the one of [BL08a, CZ+12]. By setting

for a large enough constant , all the entries of outside the support

of are set to . In contrast, a large part of our proof is devoted to control the operator norm of the noise part of

.

2.2 Estimating the principal components

We next turn to the question of estimating the principal components

. Of course, these are not identifiable if

there are degeneracies in the population

eigenvalues . We thus introduce the following identifiability condition.

A1

The spike strengths are all distinct.

We denote by and

.

Namely, is the largest signal strength and is the minimum gap.

We measure estimation error through the following loss, defined for

:

(9)

(10)

Notice the minimization over the sign . This is required because the principal components

are only identifiable up to a sign. Analogous results can obtained for alternate

loss functions such as the projection distance:

(11)

The theorem below is an immediate consequence of Theorem 1.

In particular, it uses the guarantee of Theorem 1 to

show that the corresponding principal components of

provide good estimates of the principal components .

Theorem 2.

There exists a numerical constant such that the following holds.

Suppose that Assumption A1 holds in addition to the conditions

, , and .

Set as according to Theorem 1, and

let denote the principal eigenvectors of .

Then, with probability

(12)

Proof.

Let .

By Davis-Kahn sin-theta theorem [DK70], we have, for ,

(13)

For , the claim follows by using Theorem 1.

If , the claim is obviously true since always.

∎

2.3 Support recovery

Finally, we consider the question of support recovery of the principal

components . The second phase of our algorithm aims at estimating union of the

supports from the estimated principal

components . Note that, although is

not even expected to be sparse, it is easy to see that

the largest entries of should have significant overlap

with . Step 6 of the algorithm exploit this

property to construct a consistent estimator

of the support of the spike .

We will require the following assumption to ensure support recovery.

A2

There exist constants such that the following holds.

The non-zero entries of the spikes satisfy for all . Further, for any

for every

. Without loss of generality, we will assume

.

Theorem 3.

Assume the spiked covariance model of Eq. (1) satisfying

assumptions A1 and A2, and further , , and

for a large enough numerical constant. Consider the Covariance

Thresholding algorithm of Table 1, with as in Theorem 1

.

Then there exists such that, if

(14)

then the algorithm recovers the union of supports of with probability

(i.e. we have ).

The proof in Section 7 also provides an explicit expression for

the constant .

Remark 2.1.

In Assumption A2, the requirement on the minimum size of is

standard in support recovery literature [Wai09, MB06]. Additionally, however, we require that when the supports of overlap, they

are of the same order, quantified by the parameter . Relaxing this condition

is a potential direction for future work.

Remark 2.2.

Recovering the signed supports and

, up to a sign flip, is possible using the same technique

as recovering the supports above, and poses no additional difficulty.

3 Algorithm intuition and proof strategy

For the purposes of exposition, throughout this section,

we will assume that and drop the corresponding subscript

.

Denoting by the matrix with rows ,

…, by the matrix with rows ,

…, and letting , the model

(1) can be rewritten as

(15)

Recall that .

For , the

principal eigenvector of , and hence of is positively

correlated with , i.e. is bounded away from zero.

However, for , the noise component in dominates

and the two vectors become asymptotically

orthogonal, i.e. for instance .

In order to reduce the noise level, we must exploit the sparsity of

the spike .

Now, letting , and , we can rewrite as

(16)

For a moment, let us neglect the cross terms . The ‘signal’ component is sparse

with entries of magnitude , which (in the regime of

interest ) is equivalent to . The ‘noise’ component

is dense with entries of order .

Assuming for some small constant , it should be possible to remove

most of the noise by thresholding the entries at level of order

. For technical reasons, we use the soft thresholding function

.

We will omit the second argument from wherever it is clear from context.

Consider again the decomposition (16).

Since the soft thresholding function is affine

when , we would expect that the following decomposition

holds approximately (for instance, in operator norm):

(17)

Since and each entry of has magnitude at

least , the first term is still approximately rank one, with

(18)

This is straightforward to see since soft thresholding introduces a maximum bias of per entry

of the matrix, while

the factor comes due to the support size of (see Proposition 6.2 below for a rigorous

argument).

The main technical challenge now is to control the operator norm of

the perturbation .

We know that has entries of

variance , for .

If entries were independent with mild tail conditions, this would imply –with high probability–

(19)

for some constant . Combining the bias bound from Eq. (18) and the

heuristic decomposition of Eq. (19) with the decomposition (17) results in the bound

(20)

Our analysis formalizes this argument and shows that such a

bound is essentially correct when . A modified bound is

proved for (see Theorem 4 for a general statement).

The matrix is a special

case of so-called inner-product kernel random matrices, which have

attracted

recent interest within probability theory

[EK10a, EK10b, CS13, FM15].

The basic object of study in this line of work is a matrix of the type:

(21)

In other words, is a kernel function and

is applied entry-wise to the matrix , with a matrix

with independent standard normal entries as above and are the columns

of .

The key technical challenge in our proof is the analysis of the

operator norm of such matrices, when is the

soft-thresholding function, with threshold of order .

Earlier results

are not general enough to cover this case.

[EK10a, EK10b] provide conditions under which the

spectrum of

is close to a rescaling of the spectrum of .

We are interested instead in a different regime in which the

spectrum of is very different from the one of

.

[CS13] consider -dependent kernels, but their results are

asymptotic and concern the weak limit of the empirical spectral distribution of .

This does not yield an upper bound on the spectral norm

of . Finally, [FM15] consider the spectral norm of kernel random

matrices for smooth kernels , only in the proportional regime .

Our approach to proving Theorem 1 follows instead the -net method: we develop

high probability bounds on the maximum Rayleigh quotient:

(22)

by discretizing , the unit sphere in dimensions.

For a fixed , the Rayleigh quotient is a (complicated)

function of the underlying Gaussian random variables . One might hope that it is Lipschitz

continuous with some Lipschitz constant , thereby implying, by Gaussian

isoperimetry [Led01], that it concentrates to the scale

around its expectation (i.e. 0). Then, by a standard union bound argument over a discretization

of the sphere, one would

obtain that the operator norm of is typically no more than

.

Unfortunately, this turns

out not to be true over the whole space of , i.e. the Rayleigh

quotient is not Lipschitz continuous in the underlying Gaussian variables .

Our approach, instead, shows that for

typical values of , we can control the gradient of

with respect to , and extract the required concentration only from such local information

of the function.

This is formalized in our concentration lemma 5.4,

which we apply extensively while proving Theorem 1. This lemma

is a significantly improved version of the analogous result in [DM14].

4 Practical aspects and empirical results

Specializing to the rank one case, Theorems 2 and 3 show that

Covariance Thresholding succeeds with high probability for a number of

samples , while Diagonal Thresholding requires . The reader might wonder whether eliminating the factor

has any practical relevance or is a purely conceptual improvement.

Figure 1 presents simulations on synthetic data under the

strictly sparse model, and the Covariance Thresholding algorithm of

Table 1, used in the proof of Theorem 3. The

objective is to check whether the factor has an impact at

moderate . We compare this with Diagonal Thresholding.

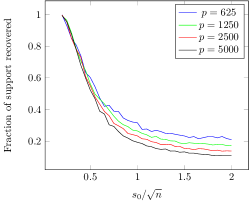

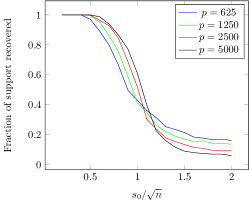

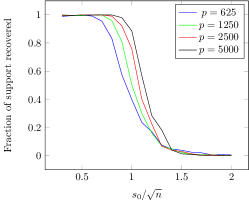

Figure 1: The support recovery phase transitions for Diagonal Thresholding (left) and

Covariance Thresholding (center) and the data-driven version

of Section 4 (right). For Covariance Thresholding, the

fraction of support recovered correctly increases monotonically with

, as long as with . Further, it

appears to converge to one throughout this region. For Diagonal

Thresholding, the fraction of support recovered correctly

decreases monotonically with for all of order

.

This confirms that Covariance Thresholding (with or without knowledge

of the support size ) succeeds with high

probability for , while Diagonal Thresholding

requires a significantly sparser principal component.

We plot the empirical

success probability as a function of for several values

of , with . The empirical success probability was computed by

using independent instances of the problem.

A few observations are of interest: Covariance

Thresholding appears to have a significantly larger success

probability in the ‘difficult’ regime where Diagonal Thresholding

starts to fail; The curves for Diagonal

Thresholding appear to decrease monotonically with indicating that

proportional to is not the right scaling for this

algorithm (as is

known from theory); In contrast, the curves for Covariance

Thresholding become steeper for larger , and, in particular, the

success probability increases with for . This

indicates a sharp

threshold for , as suggested by our theory.

In terms of practical applicability, our algorithm in Table 1

has the shortcomings of requiring knowledge of problem parameters

. Furthermore, the thresholds suggested by theory need

not be optimal. We next describe a

principled approach to estimating (where possible) the parameters

of interest and running the algorithm in a purely data-dependent manner.

Assume the following model, for

where is a fixed mean vector, have mean

and variance , and have mean and covariance .

Note that our focus in this section is not on rigorous analysis, but instead to demonstrate

a principled approach to applying covariance thresholding in practice.

We proceed as follows:

Estimating , :

We let be the empirical mean estimate

for . Further letting we

see that entries of are mean and variance .

We let

where denotes the median absolute

deviation of the entries of the matrix in the argument, and

is a constant scale factor. Guided by the

Gaussian case, we take .

Choosing :

Although in the statement of the theorem, our choice of depends on the SNR ,

it is reasonable to instead

threshold ‘at the noise level’, as follows. The noise component of

entry of the sample covariance (ignoring lower order

terms) is given by . By the central limit theorem,

. Consequently, , and we need to choose the (rescaled) threshold proportional

to . Using previous estimates, we let

for a constant . In simulations, a choice appears to work well.

Estimating :

We define and soft threshold it

to get using as above.

Our proof of Theorem 2 relies on the fact

that has eigenvalues that are separated from the

bulk of the spectrum. Hence, we estimate using : the number of

eigenvalues separated from the bulk in . The edge of the

spectrum can be computed numerically using the Stieltjes transform method as

in [CS13].

Estimating :

Let denote the

eigenvector of . Our theoretical analysis indicates that is

expected to be close to . In order to denoise , we assume

, where is additive random noise

(perhaps with some sparse corruptions).

We then threshold ‘at the

noise level’ to recover a better estimate of . To do this, we

estimate the standard deviation of the “noise” by

. Here we set –again guided by the Gaussian heuristic– . Since is sparse,

this procedure returns a good estimate for the size of the noise

deviation. We let denote the vector obtained by hard

thresholding : set

and

We then let and return

as our estimate for .

Note that –while different in several respects– this empirical approach

shares the same philosophy of the algorithm in Table

1.

On the other hand, the data-driven algorithm presented in this section is less

straightforward to analyze, a task that we defer to future work.

Figure 1 also shows results of a support recovery

experiment using the ‘data-driven’ version of this section. Covariance thresholding

in this form also appears to work for supports of size .

Figure 2 shows the performance of vanilla PCA, Diagonal Thresholding

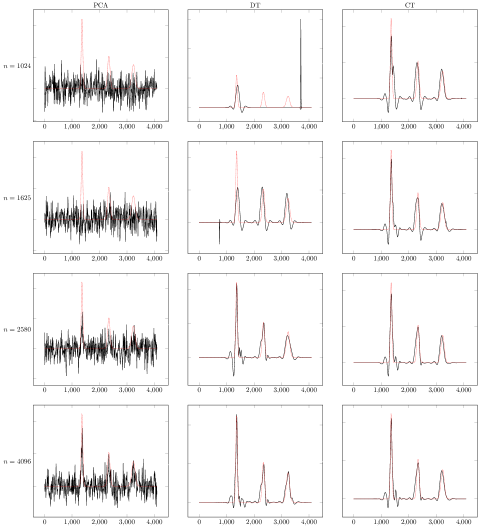

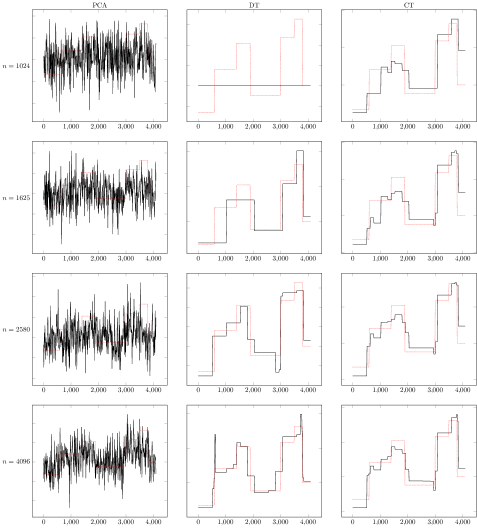

and Covariance Thresholding on the “Three Peak” example of [JL04].

This signal is sparse in the wavelet domain and the simulations employ the data-driven

version of covariance thresholding. A similar experiment with the “box” example of Johnstone

and Lu is provided in Figure 3. These experiments demonstrate that, while for large values of both Diagonal

Thresholding and Covariance Thresholding perform well, the latter

appears superior for smaller values of .

Figure 2: The results of Simple PCA, Diagonal Thresholding and Covariance Thresholding (respectively) for

the “Three Peak” example of [JL09] (see Figure 1

of the paper). The signal is sparse in the ‘Symmlet 8’ basis. We use , and the rows correspond to sample sizes

respectively. Parameters for Covariance Thresholding are chosen as in Section 4,

with . Parameters for Diagonal Thresholding are from [JL09]. On each curve,

we superpose the clean signal (dotted). Figure 3: The results of Simple PCA, Diagonal Thresholding and Covariance Thresholding (respectively) for

a synthetic block-constant function (which is sparse in the Haar wavelet basis).

We use , and the rows correspond to sample sizes

respectively. Parameters for Covariance Thresholding are chosen as in Section 4,

with . Parameters for Diagonal Thresholding are from [JL09]. On each curve,

we superpose the clean signal (dotted).

5 Proof preliminaries

In this section we review some notation and preliminary facts

that we will use throughout the paper.

5.1 Notation

We let denote the set of first integers.

We will represent vectors using boldface lower case letters,

e.g. . The entries of a vector will be

represented by .

Matrices are represented using boldface upper

case letters e.g. . The entries of a matrix are

represented by for .

Given a matrix , we generically let ,

denote its rows, and ,

its columns.

For , we define the projector operator

by letting

be the matrix with entries

(23)

For a matrix , and a set , we

define its column restriction to be the

matrix obtained by setting to columns outside :

Similarly is obtained from by setting to zero all

indices outside .

The operator norm of a matrix is denoted by (or

)

and its Frobenius norm by . We write for the standard

norm of a vector . Other vector norms such as or are

denoted with appropriate subscripts.

We let denotes the support of the

spike . Also, we denote the union of the supports of by .

The complement of a set is denoted by .

We write for the soft-thresholding function.

By we denote the derivative of with respect

to the first argument, which exists Lebesgue almost everywhere. To simplify the

notation, we omit

the second argument when it is understood from context.

For a random variable and a measurable set we write to denote ,

the expectation of constrained to the event .

In the statements of our results, consider the limit of large and large

with certain conditions on (as in Theorem 1). This limit will be referred to either as “ large enough”

or “ large enough” where the phrase “large enough” indicates dependence of (and

thereby ) on specific problem parameters.

The Gaussian distribution function will be denoted by .

5.2 Preliminary facts

Let denote the unit sphere in dimensions, i.e. .

We use the following definition [Ver12, Definition 5.2] of

the -net of a set :

Definition 5.1(Nets, Covering numbers).

A subset is called an -net of if every point in

may be approximated by one in with error at most . More precisely:

The minimum cardinality of an -net of , if finite, is called its covering number.

The following two facts are useful while using -nets to bound the

spectral norm of a matrix. For proofs, we refer the reader to [Ver12, Lemmas 5.2, 5.4].

Lemma 5.2.

Let be the unit sphere in dimensions. Then there exists an -net

of , satisfying:

Lemma 5.3.

Let be a symmetric matrix. Then, there exists such

that

(24)

Proof.

Firstly, we have . Let be the

maximizer (which exists as is compact and is continuous in ).

Choose so that . Then:

(25)

The lemma then follows as .

∎

Throughout the paper we will denote by an -net on the unit sphere

that satisfies Lemma 5.2. For a subset of indices we denote

by the natural isometric embedding of in .

We now state a general concentration lemma. This will be our basic tool to

establish Theorem 2, and thereby Theorem 3.

Lemma 5.4.

Let be vector of i.i.d. standard normal

variables. Suppose is a finite set and we have functions for

every . Assume is a Borel set such that for Lebesgue-almost every

:

(26)

Then, for any :

(27)

Here is an independent copy of .

Proof.

We use the Maurey-Pisier method along with symmetrization.

By centering, assume that for all . Further, by

including the functions in the set (at most doubling its size), it suffices to prove the

one-sided version of the inequality:

(28)

We first implement the symmetrization. Note that:

(29)

(30)

Furthermore, by centering, . Hence for any non-decreasing convex function

:

(31)

(32)

(33)

Here we use Jensen’s inequality with the monotonicity of to obtain and with

the convexity of to obtain .

Now we choose , for .

(34)

(35)

(36)

(37)

(38)

Here is Markov’s inequality, and is the symmetrization bound Eq. (33), where

we use the fact that is non-decreasing and convex in .

At this point, it is

easy to see that the lemma follows if we are able to control the first term in Eq. (38).

We establish this

via the Maurey-Pisier method. Define the path ,

the velocity .

(39)

(40)

(41)

where, in the last inequality we use the union bound followed by Markov’s inequality. To

control the exponential moment, note that

whence, using Jensen’s inequality:

(42)

(43)

Define the set . Then:

(44)

(45)

(46)

Here follows as . Equality follows from noting that

is measurable with respect to and, hence, first integrating with respect to , a Gaussian

random variable that is independent of . The final inequality follows by using the fact that on the

set .

Since this bound is uniform over , we can use it in (41):

(47)

(48)

We can now set , to obtain the exponent above as .

The prefactor is bounded by when . Therefore, as

required, we obtain:

(49)

Combining this with Eq. (38) and the fact that gives Eq. (28)

and, consequently, the lemma.

∎

By a simple application of Cauchy-Schwarz, this lemma implies the following.

The following two lemmas are well-known concentration of measure results.

The forms below can be found in [Ver12, Corollary 5.35], [LM00, Lemma 1]

respectively.

Lemma 5.6.

Let be a matrix with i.i.d. standard normal

entries, i.e. . Then, for every :

We let be the diagonal

entries not included in any support. (Recall that denote the

union of the supports.) Further let , ,

and , or, equivalently .

Since these are disjoint we have:

(54)

The first term corresponds to the ‘signal’ component, while

the last three terms correspond to the ‘noise’ component.

Theorem

1 is a direct consequence of the next five propositions.

The first demonstrates that, even for a low level

of thresholding, viz. ,

the term has small operator norm.

The second demonstrates that the soft thresholding operation preserves

the signal in the term . The next two propositions show that the

cross and diagonal terms and are negligible as well.

Finally, in the last proposition, we demonstrate that,

for the regime of thresholding far above the noise level, i.e. ,

the noise terms and vanish entirely.

Let denote the matrix corresponding to the third term

of Eq. (54):

Assuming the conditions of Proposition 6.1 and, additionally,

that , there exist constants such that with probability

(59)

Proposition 6.4.

Let denote the matrix corresponding to the third term

of Eq. (54):

With probability we have that .

Proposition 6.5.

For some absolute constant , we have for

that, with probability :

(60)

Therefore, and .

Remark 6.6.

At this point we remark that the probability can be made

quantitative, for e.g. of the form , for

every large enough. For simplicity of exposition we do not pursue this

in the paper.

We defer the proofs of Propositions 6.1,

6.2, 6.3, 6.4 and 6.5 to

Sections 6.1, 6.2,

6.3, 6.4 and 6.5

respectively.

By combining them for , we immediately obtain the following bound.

Theorem 4.

There exist numerical constants such that the following happens.

Assume , and . Then

with probability :

(61)

Proof.

The proof is obtained by adding the error terms from Propositions 6.1,

6.2, 6.3 and 6.4, and noting that is bounded.

∎

Using Propositions 6.1, 6.2, 6.3 and 6.4, together with a suitable choice of

, we obtain the proof of Theorem 1.

Note that in the case there is no thresholding and hence the result follows from the fact that

[Ver12, Remark 5.40].

We assume now that and the case that . In that case we set .

Below we will keep a large enough constant, and check that each of the error terms

in Propositions 6.1, 6.2, 6.3 and 6.4 is upper bounded by (a constant times) the right-hand side of

Eq. (7). Throughout will denote a generic constant that can be made as large as we want, and can change from line to line.

From Proposition 6.3, we get, using the same argument as in Eq. (65)

(68)

(69)

Finally, the term of Proposition 6.4 is also bounded as desired using

(dividing both sides by and using the fact that is increasing).

The case of is easier. In that case, we can keep

with large enough so that for of Proposition

6.5. Then, by Proposition 6.5,

we know that and . Therefore we only need consider the terms

and . For these terms we can use Propositions 6.2

and 6.4 respectively and, arguing

as in the earlier case , we obtain the desired

result.

∎

Since is a principal submatrix of , it suffices to prove the same bound for

. Our main tool in the proof will be the concentration lemma 5.4 which we

use on multiple occasions. With

a view to using the lemma, we let let denote an independent copy of , and it’s

column. The proof relies on two preliminary lemmas. For some (to be chosen later), we first state and

prove the following lemma that controls

the norm of any principal submatrix of of size at most .

Lemma 6.7.

Fix any . There exists an absolute constants such that:

(70)

Proof.

For any subset recall that denotes an -net of unit vectors in supported

on the subset . For simplicity let .

It suffices, by Lemma 5.3, to control on the

set . In particular:

(71)

Consider the good set given by:

(72)

To use Lemma 5.4, we need to compute and the gradient of

with respect to the underlying random variables . Since is an odd function

the expectation vanishes. To compute

the gradient, we let and ,

and consider as a function of the

. Taking the gradient with respect to a column for :

(73)

(74)

where

(75)

Since , we have that .

Summing over we obtain the gradient bound, holding on the good set :

(76)

(77)

which holds because of triangle inequality and the fact that

. We can now apply Lemma 5.4

to bound the RHS of Eq. (71) and get:

(78)

We can simplify the terms on the right-hand side to obtain the result of the lemma. With , Stirling’s

approximation and Lemma 5.2 we have:

(79)

We use a crude bound on the complement of the good set . It is easy to see that, for any unit vector ,

.

Cauchy-Schwarz then implies that

(80)

(81)

where the bound on follows from Lemma 5.6. This concludes the lemma.

∎

Note that Lemma 6.7, with , tells us that

is of order (uniformly in ) with high probability. Already this non-asymptotic

bound is non-trivial, since

the previous results of [CS13] and [FM15] do

not extend to this case. However, Proposition 6.1 is stronger,

and establishes a rate of decay with the thresholding level .

The second lemma we require controls the Rayleigh quotient

when the entries of are “spread out”.

Lemma 6.8.

Assume that . Given and a

unit vector , let and denote

the projections of onto supports respectively. We have:

(82)

for any where .

The same bound holds for .

Proof.

We first prove the claim for .

Firstly, we have . Consider the “good set” of pairs

satisfying the conditions:

(83)

(84)

(85)

(86)

Also, for any pair , for (and its columns

defined appropriately) we have:

(87)

(88)

Equation (87) follows by a simple application of triangle inequality and condition (83) defining

. For inequality (88), expanding the product :

(89)

whence, by triangle inequality and

(90)

The gradient of with respect to a column of is given by:

(91)

(92)

(93)

Therefore

(94)

(95)

(96)

(97)

Here follows from fact that the entries of are bounded by and the

definition of the soft thresholding function. Inequality follows

follows when we set and .

Therefore, summing over we obtain the following bound for the gradient of

(98)

We can use now Lemma 5.4, to get, for as defined above and any :

(99)

(100)

where the last line follows by Cauchy-Schwarz, as in the proof of Lemma 6.7,

and the fact that using the upper bound .

To obtain the thesis, we need to now bound . It suffices

to control the failure probability of conditions (83), (84), (85), (86)

of the good set

individually, and apply the union bound. For independent,

with probability at most by Lemma 5.6.

Now consider condition (84) with , without loss of generality. First, for any we have:

(101)

Lemma 5.7 guarantees that the second term is at most .

To control the first term, we note that, conditional on , are independent Gaussian

random variables with variance . Therefore, conditional on ,

are independent Bernoulli random variables with success probability , where is the

Gaussian cumulative distribution function.

It follows, by the Chernoff-Hoeffding bound for Bernoulli random variables that

(102)

where . Choosing , and

conditional on , for a constant , implying

that

A similar bound holds for and the other conditions (85) and (86),

whence we have by the union bound that . This completes

the proof of the claim (82).

The proof of the claim for is analogous, so we only sketch the points at which it differs from that

of Eq. (82). We use the same good set , as defined earlier. Computing the gradient as for

we obtain:

(106)

Here if and otherwise. Define the vector as

(107)

As before, we have that .

Therefore, summing over :

(108)

(109)

(110)

(111)

Under the condition of , the gradient also satisfies, when evaluated at :

(112)

The rest of the proof is then the same as before.

∎

Given these lemmas, we can now establish Proposition 6.1.

We use a variant of the -net argument of Lemma 6.7.

To bound the probability that is large, with Lemma

5.3, we obtain:

(113)

Let for some to be

chosen later. Then let denote

the projections of onto supports respectively. Since

by triangle inequality and union bound:

(114)

(115)

(116)

With , the first term is controlled by

Lemma 6.7 while the

final two are controlled by Lemma 6.8.

We choose in Eq. (116), and

(117)

for large enough so that, using the bounds of Lemmas 6.7 and 6.8, we have:

(118)

This probability bound is provided is not too large: we choose

which guarantees that the bound above is when for some large enough. This concludes the proposition.

∎

We decompose the empirical covariance matrix (6) as

(119)

(120)

(121)

Next notice that, for any ,

(122)

With a view to employing this inequality, we use

Eq. (119) and the triangle inequality:

(123)

(124)

(125)

where the last line follows by noticing that the first term is supported on

of size and then using bias bound Eq. (122) entry-wise.

We next bound each of the three terns on the right hand side.

For the first term in Eq (125), note that with a

change of basis to the orthonormal set

is equivalent to an matrix with entries , where . Denote by the diagonal

matrix with and

by , the matrix with columns ,….

Then, we have, with high probability

(126)

(127)

(128)

The last inequality follows from the Bai-Yin law on eigenvalues of Wishart matrices [Ver12, Corollary 5.35].

Consider the second term in Eq (125). By orthonormality of , the matrix is orthogonally

equivalent to , where we recall that denotes the submatrix of

formed by the columns in . Denoting by the orthogonal projector onto

the column space of , we then have, with high probability,

(129)

(130)

(131)

Here the penultimate inequality follows by Lemma 5.6 noting

that, by invariance under rotations (and since project onto a random subspace of dimensions

independent of ), is distributed as the norm of a matrix with i.i.d. standard normal

entries, with dimensions , .

Finally, for the third term of Eq. (125) we use the Bai-Yin law of

Wishart matrices [Ver12, Corollary 5.35] to obtain, with high probability:

(132)

(133)

Finally, substituting the above bounds in Eq. (125), we get

Note that where . It is therefore sufficient to

control , and then use triangle inequality.

The proof is similar to that of Proposition 6.1. We let denote the matrix with columns ,

,…, and introduce the set

(135)

We then have

(136)

Notice that, by the Bai-Yin law on eigenvalues of Wishart matrices [Ver12, Corollary 5.35],

(throughout for a small constant).

It is therefore sufficient to show for as in the statement of

the theorem.

In order to lighten the notation, we will write and bound the above probability uniformly over

. (In other words denotes expectation over with fixed).

We first control the norms of small submatrices of , following

which we control the full matrix.

Lemma 6.9.

Fix an , and let . Then, there exists an absolute constant such that, for any :

(137)

Proof.

Let, as before, denote the -net of unit vectors supported on of size at most and let

.

Then, by

Lemma 5.3, with :

(138)

It now suffices to control the right hand side via Lemma 5.4. We first compute

the gradients with respect to as before:

(139)

Therefore, arguing as in proof of Proposition 6.1 (see Lemma 6.7):

(140)

Let be the diagonal matrix with entries , and be the matrix with columns

. We then have , whence, recalling , and with small enough

(141)

(142)

Consider the good set of pairs satisfying:

(143)

(144)

For , and , define . Now

Using Eqs. (140) and (142, the gradient evaluated at

satisfies:

Let , observing that , we have the bound (using Lemma 5.2 and Stirling’s approximation):

(149)

for some absolute . Now, as in the proof of Proposition 6.1, .

From this it follows that for some . Finally

using Lemmas 5.6, 5.7 and the union bound.

Combining these bounds in Eq. (148) yields the lemma.

∎

Now we prove a similar lemma when has entries that are “spread out”.

Lemma 6.10.

Fix an , and a unit vector let ,

and denote the projection of on the set of indices . Then there exists a numerical constant such that,

assuming , we have

(150)

where .

Proof.

For simplicity of notation, it is convenient to introduce the vector . Throughout the proof, we will use that and

.

We compute the gradients as follows:

(151)

Therefore we have

(152)

(153)

where we used the fact that and that .

Similarly, for :

(154)

(155)

(156)

Combining the bounds in Eqs.(153), (156), we obtain

(157)

(158)

With , we define the good set of pairs

satisfying

(159)

(160)

(161)

(162)

(163)

Define with .

By Eq. (158) the gradient evaluated at is bounded by

(164)

(165)

where we bounded as in Eq. (142),

and used , which follows from Eq. (159) and triangle inequality.

Furthermore, as

, we have that:

(166)

(167)

Hence on the good set , we have:

(168)

Therefore the gradient satisfies, on the good set:

By Lemma 5.2, keeping we have that the first term is at most .

For the second term, we have . Since

,

we have that .

Also as , , implying that the

second term is bounded above by . Therefore:

(171)

It remains to control the probability of the

bad set . For this, we control the probability of violating

any one condition among (159), (160),

(161), (162) and (163) defining

and then use the union bound.

By Lemmas 5.6, condition (159) hold with probability

.

The argument controlling the probability for conditions (160),

(161), (162) and (163) to hold

are essentially the same, so we restrict ourselves to condition (160) keeping ,

without loss of generality.

Conditional on , for

are independent variables. Therefore, conditional on ,

are independent Bernoulli random variables

with success probability . Define to be the success probability, i.e.

.

Since we can enlarge to a large absolute constant.

Letting be the matrix with

columns , and the diagonal matrix with , we have,

with probability at least ,

(172)

where the last equality holds since and by tail bounds on chi-squared random variables.

Further

(173)

By the above argument, the first term is at most and

we turn to the second term. By the Chernoff bound

(174)

with when . Choosing implies that when

and, thereby,

that . Further since , . This implies that

(175)

Combining this with Eq. (173) we have that for some absolute .

Plugging this in Eq. (171) yields the lemma.

∎

We are now ready to prove Proposition 6.3. Indeed, as in Proposition 6.1, for any unit vector ,

let and denote the projections

on the indices in respectively.

(176)

(177)

As before, we will let .

The first term is controlled via Lemma 6.9, while the second is controlled

by Lemma 6.10. We keep where

(178)

so that, via the bounds of Lemmas 6.9, 6.10 and that :

(179)

We now set with for a suitable constant

and, since , we get that . Furthermore, it is straightforward to see that ,

and this implies that

(180)

With this setting of , we get the form of below, as required for the proposition.

This is a standard argument [BL08b, Lemma A.3] where

(following the dependence on ) it suffices to take for a sufficiently large absolute constant. We note here that the same can also

be proved via the conditioning technique applied in the

proofs of Propositions 6.1 and 6.3.

Throughout this section, to lighten notation, we drop the prime from

and while keeping in mind that these are independent from

. We further write , where

is the matrix with columns , is diagonal with and

has columns .

Define the event

(187)

By the Bai-Yin law on eigenvalues of Wishart matrices [Ver12],

. In the rest of the proof, we will therefore assume fixed,

and denote by the expectation conditional on . In other words,

denotes expectation with respect to .

Note that

(188)

We then have, for and ,

(189)

(190)

(191)

(192)

We next bound, with high probability, for .

Throughout we let .

Considering the first term, we have

(193)

(194)

where in the last inequality we used .

Consider next the second term. Since , it follows that

, for a Gaussian random variable with variance

(195)

(196)

(197)

(198)

By union bound over , we obtain

(199)

Finally, consider the last term. By rotational invariance of , the distribution of

only depends on the angle between and . Calling this angle ,

we have

(200)

(201)

Both of these terms have Bernstein-type tail bonds, whence

(202)

Using , and recalling that for a large constant, we

obtain . Hence by union bound

(203)

By putting together Eqs. (194), (199), (203),

and using assumption A2, we get

(204)

Let .

We claim that the above implies that, with high probability, for all .

On the other hand, By Theorem 2 and using the assumption (14),

we can guarantee

(207)

Hence for , and considering –to be definite– , we get

(208)

(209)

(210)

(211)

where, in the first inequality, we used .

This concludes the proof. Keeping track of the dependence on , , , ,

we get that the following conditions are sufficient for the theorem’s conclusion to hold (with a suitable

numerical constant):

(212)

(213)

(214)

(215)

All of these conditions are implied by the assumptions of Theorem 3, namely

Eq. (14). In particular, this is shown by using the fact that

for .

Acknowledgements

We are grateful to David Donoho for his feedback on this manuscript.

This work was

partially supported by the NSF CAREER award CCF-0743978, the NSF grant CCF-1319979, and

the grants AFOSR/DARPA FA9550-12-1-0411 and FA9550-13-1-0036.

References

[AW09]

Arash A Amini and Martin J Wainwright, High-dimensional analysis of

semidefinite relaxations for sparse principal components, The Annals of

Statistics 37 (2009), no. 5B, 2877–2921.

[BBAP05]

Jinho Baik, Gérard Ben Arous, and Sandrine Péché, Phase

transition of the largest eigenvalue for nonnull complex sample covariance

matrices, Annals of Probability (2005), 1643–1697.

[BGN11]

Florent Benaych-Georges and Raj Rao Nadakuditi, The eigenvalues and

eigenvectors of finite, low rank perturbations of large random matrices,

Advances in Mathematics 227 (2011), no. 1, 494–521.

[BL08a]

Peter J Bickel and Elizaveta Levina, Covariance regularization by

thresholding, The Annals of Statistics (2008), 2577–2604.

[BL08b]

, Regularized estimation of large covariance matrices, The Annals

of Statistics (2008), 199–227.

[BR13]

Quentin Berthet and Philippe Rigollet, Computational lower bounds for

sparse pca, arXiv preprint arXiv:1304.0828 (2013).

[CDMF09]

Mireille Capitaine, Catherine Donati-Martin, and Delphine Féral, The

largest eigenvalues of finite rank deformation of large wigner matrices:

convergence and nonuniversality of the fluctuations, The Annals of

Probability 37 (2009), no. 1, 1–47.

[CL11]

Tony Cai and Weidong Liu, Adaptive thresholding for sparse covariance

matrix estimation, Journal of the American Statistical Association

106 (2011), no. 494, 672–684.

[CMW+13]

T Tony Cai, Zongming Ma, Yihong Wu, et al., Sparse pca: Optimal rates and

adaptive estimation, The Annals of Statistics 41 (2013), no. 6,

3074–3110.

[CS13]

Xiuyuan Cheng and Amit Singer, The spectrum of random inner-product

kernel matrices, Random Matrices: Theory and Applications 2 (2013),

no. 04, 1350010.

[CZ+12]

T Tony Cai, Harrison H Zhou, et al., Optimal rates of convergence for

sparse covariance matrix estimation, The Annals of Statistics 40

(2012), no. 5, 2389–2420.

[CZZ+10]

T Tony Cai, Cun-Hui Zhang, Harrison H Zhou, et al., Optimal rates of

convergence for covariance matrix estimation, The Annals of Statistics

38 (2010), no. 4, 2118–2144.

[dBG08]

Alexandre d’Aspremont, Francis Bach, and Laurent El Ghaoui, Optimal

solutions for sparse principal component analysis, The Journal of Machine

Learning Research 9 (2008), 1269–1294.

[dEGJL07]

Alexandre d’Aspremont, Laurent El Ghaoui, Michael I Jordan, and Gert RG

Lanckriet, A direct formulation for sparse pca using semidefinite

programming, SIAM review 49 (2007), no. 3, 434–448.

[DJ94]

David L. Donoho and Iain M. Johnstone, Minimax risk over balls,

Prob. Th. and Rel. Fields 99 (1994), 277–303.

[DK70]

Chandler Davis and William Morton Kahan, The rotation of eigenvectors by

a perturbation. iii, SIAM Journal on Numerical Analysis 7 (1970),

no. 1, 1–46.

[DM14]

Yash Deshpande and Andrea Montanari, Sparse pca via covariance

thresholding, Advances in Neural Information Processing Systems, 2014,

pp. 334–342.

[EK10a]

Noureddine El Karoui, On information plus noise kernel random matrices,

The Annals of Statistics 38 (2010), no. 5, 3191–3216.

[EK10b]

, The spectrum of kernel random matrices, The Annals of

Statistics 38 (2010), no. 1, 1–50.

[FM15]

Zhou Fan and Andrea Montanari, The spectral norm of random inner-product

kernel matrices, arXiv:1507.05343 (2015).

[FP07]

Delphine Féral and Sandrine Péché, The largest eigenvalue of

rank one deformation of large wigner matrices, Communications in

mathematical physics 272 (2007), no. 1, 185–228.

[JL04]

Iain M Johnstone and Arthur Yu Lu, Sparse principal components analysis,

Unpublished manuscript (2004).

[JL09]

, On consistency and sparsity for principal components analysis in

high dimensions, Journal of the American Statistical Association

104 (2009), no. 486.

[Joh15]

Iain M. Johnstone, Function estimation and gaussian sequence models,

Unpublished manuscript (2015).

[Kar08]

Noureddine El Karoui, Operator norm consistent estimation of

large-dimensional sparse covariance matrices, The Annals of Statistics

(2008), 2717–2756.

[KNV13]

R. Krauthgamer, B. Nadler, and D. Vilenchik, Do semidefinite relaxations

really solve sparse pca?, CoRR abs/1306:3690 (2013).

[KY13]

Antti Knowles and Jun Yin, The isotropic semicircle law and deformation

of wigner matrices, Communications on Pure and Applied Mathematics (2013).

[Led01]

M. Ledoux, The concentration of measure phenomenon, Mathematical

Surveys and Monographs, vol. 89, American Mathematical Society, Providence,

RI, 2001.

[LM00]

Beatrice Laurent and Pascal Massart, Adaptive estimation of a quadratic

functional by model selection, Annals of Statistics (2000), 1302–1338.

[MB06]

Nicolai Meinshausen and Peter Bühlmann, High-dimensional graphs and

variable selection with the lasso, The Annals of Statistics (2006),

1436–1462.

[MW15a]

Tengyu Ma and Avi Wigderson, Sum-of-squares lower bounds for sparse pca,

Advances in Neural Information Processing Systems, 2015, pp. 1603–1611.

[MW+15b]

Zongming Ma, Yihong Wu, et al., Computational barriers in minimax

submatrix detection, The Annals of Statistics 43 (2015), no. 3,

1089–1116.

[MWA05]

Baback Moghaddam, Yair Weiss, and Shai Avidan, Spectral bounds for sparse

pca: Exact and greedy algorithms, Advances in neural information processing

systems, 2005, pp. 915–922.

[Pau07]

Debashis Paul, Asymptotics of sample eigenstructure for a large

dimensional spiked covariance model, Statistica Sinica 17 (2007),

no. 4, 1617.

[Ver12]

R. Vershynin, Introduction to the non-asymptotic analysis of random

matrices, Compressed Sensing: Theory and Applications (Y.C. Eldar and

G. Kutyniok, eds.), Cambridge University Press, 2012, pp. 210–268.

[VL12]

Vincent Q Vu and Jing Lei, Minimax rates of estimation for sparse pca in

high dimensions, Proceedings of the 15th International Conference on

Artificial Intelligence and Statistics (AISTATS) 2012, 2012.

[Wai09]

Martin J Wainwright, Sharp thresholds for high-dimensional and noisy

sparsity recovery using-constrained quadratic programming (lasso),

Information Theory, IEEE Transactions on 55 (2009), no. 5,

2183–2202.

[WBS14]

Tengyao Wang, Quentin Berthet, and Richard J Samworth, Statistical and

computational trade-offs in estimation of sparse principal components, arXiv

preprint arXiv:1408.5369 (2014).

[WTH09]

Daniela M Witten, Robert Tibshirani, and Trevor Hastie, A penalized

matrix decomposition, with applications to sparse principal components and

canonical correlation analysis, Biostatistics 10 (2009), no. 3,

515–534.

[ZHT06]

Hui Zou, Trevor Hastie, and Robert Tibshirani, Sparse principal component

analysis, Journal of computational and graphical statistics 15

(2006), no. 2, 265–286.