A model of financial contagion with variable asset returns may be replaced with a simple threshold model of cascades

Abstract

I show the equivalence between a model of financial contagion and the threshold model of global cascades proposed by Watts (2002). The model financial network comprises banks that hold risky external assets as well as interbank assets. It is shown that a simple threshold model can replicate the size and the frequency of financial contagion without using information about individual balance sheets.

Keywords: financial network, cascades, financial contagion, systemic risk.

JEL codes: G01, G18.

1 Introduction

Bank default is contagious. The failure of a single bank can spread through financial networks, generating default cascades. Over the past few years, many researchers in various fields of natural and social sciences, such as physicists, ecologists and economists, have been addressing the question of how to prevent financial contagion (e.g., Nier et al., 2007, Soramaki et al., 2007, Gai and Kapadia, 2010, Gai et al., 2011, Lenzu and Tedeschi, 2012, Kobayashi, 2013, Kobayashi and Hasui, 2014).

However, there is no wide agreement among researchers about how to construct a model of financial contagion. Different research groups use different models, which makes it difficult to establish a consensus about policy implications.111See Lorenz et al. (2009) and Upper (2011) for a survey of the literature.

In this letter, I show the equivalence between a model of financial contagion and the widely-used threshold model of global cascades proposed by Watts (2002).222See, for example, Dodds and Watts (2004), Gleeson and Cahalane (2007), Watts and Dodds (2007) and Gleeson (2013). Basically, financial network models require researchers to construct bank balance sheets. The influence of a bank failure is then examined by sequentially undermining the interbank assets of the lenders. Second-round defaults occur if the number of defaulted borrowers among total borrowers exceeds a certain threshold.

This mechanism is closely related to that of the Watts model of cascades. I show that there is no need to construct bank balance sheets as long as the “shadow” threshold of default is appropriately defined in accordance with the volatility of assets.

2 The models

2.1 A model of financial contagion

The model of financial contagion used in this paper is an extended version of Gai and Kapadia (2010). The essential difference is that I take into account stochastic fluctuations in the value of external assets.

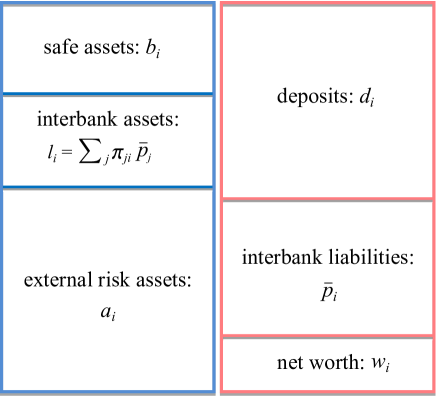

A typical bank’s balance sheet is illustrated in Figure 1. There are banks in the financial market. Bank holds risky external assets, , interbank assets, , and riskless assets, . On the liability side, there are deposits, , interbank liabilities, , and net worth, . The balance-sheet condition implies that .

Banks are connected to each other by lending and borrowing. The existence of a lending-borrowing relationship is expressed as a link or an edge. In network theory, the number of outgoing links is called out-degree, while the number of incoming links is called in-degree. The direction of links represents the flow of funds at the time of initial lending.

The amount of bank ’s borrowings from bank is expressed as , where denotes the relative weight of bank ’s borrowings from , and thereby . The amount of bank ’s total interbank assets is given by .

Bank will default if

| (1) |

where and stand for the ex-post values of external assets and interbank liabilities, respectively. It should be pointed out that deposits, , are reserved because they are senior to interbank assets.

Provided that there is no loss in interbank assets, a bank will default with probability due to a loss of external assets. indicates the probability of fundamental defaults, which is assumed to be common across banks.

If bank fails, then bank ’s creditors lose all of the credits they extended to bank . Some of these creditors may fail due to the loss of their interbank assets. Accordingly, the creditors of the creditors of bank may fail as well, because they in turn lose the credits they extended to the failed banks.

Given the size of each interbank asset, the total sizes of interbank assets and liabilities are determined by the structure of the interbank network. To ensure that the probability of fundamental defaults is the same across banks, the relative size of external assets to net worth is fixed. If bank has so many incoming links that its liability side is bigger than its tentative total assets, , where denotes the tentatively assigned riskless assets, then riskless assets are added to adjust the asset side. Otherwise, deposits are imposed to adjust the liability side.333Notice that this adjustment does not affect the probability of fundamental default. After such adjustments, the capital ratio, , may differ across banks while the tentative capital ratio, , is common. The tentative ratio of total interbank assets to total assets, , is allowed to vary across banks.

2.2 The Watts model of global cascades

Let us summarize the Watts’ (2002) threshold model of cascades. In this model, each node in the network takes one of two states: “flipped” or “not flipped”. The network is undirected.

Let and denote node ’s degree and the number of its flipped neighbors, respectively. The algorithm of cascading behavior in the Watts model is that

where is the threshold of flipping for node . This means that the threshold number of flipped neighbors above which node will flip is , where denotes the floor function that returns the maximum integer smaller than .

3 Equivalence between a financial network model and a threshold model

Here, I show the equivalence between the financial network model and a modified version of the threshold model. Recall that the ex-post value of external assets, , is determined stochastically. Let be the return of external assets.

Let us suppose that the amount of individual interbank lending is common. Then, if , bank will fail if the fraction of its defaulted borrowers exceeds . Note that there is no possibility of contagious default if , as long as there is no loss in external assets.

If , on the other hand, the threshold for the fraction of defaulted borrowers depends on the realization of asset returns. If a bank earns positive (negative) returns from its external assets, it becomes more resilient against (susceptible to) contagious default.

Let be the “shadow” threshold of default for bank . It follows that

| (2) | |||||

Here, is treated as a parameter. Thus, if asset returns, , follow a distribution of mean zero and variance , then the shadow threshold follows a distribution of mean and variance . More generally, the of , defined as , is given by

| (3) |

where is the p.d.f. of .

Let us assume that asset returns follow a normal distribution with mean zero. Let , where is the inverse of the standard normal distribution. The standard deviation of asset returns, , such that the probability of fundamental default becomes is given as

| (4) | |||||

It follows from Eqs. (2) and (4) that the shadow threshold follows a normal distribution with mean and standard deviation .444Recall that takes a negative value.

In this way, the balance sheet-based model of financial contagion shown above can be expressed as a simple threshold model. Intuitively, the shadow threshold will become smaller as the returns of external assets take a lower value, meaning that the bank becomes more susceptible to default contagion. Those banks that have a negative value of will fail at the beginning, which corresponds to the case of fundamental defaults in the model of financial contagion.555Note that = = = , where is a random variable from the standard normal distribution.

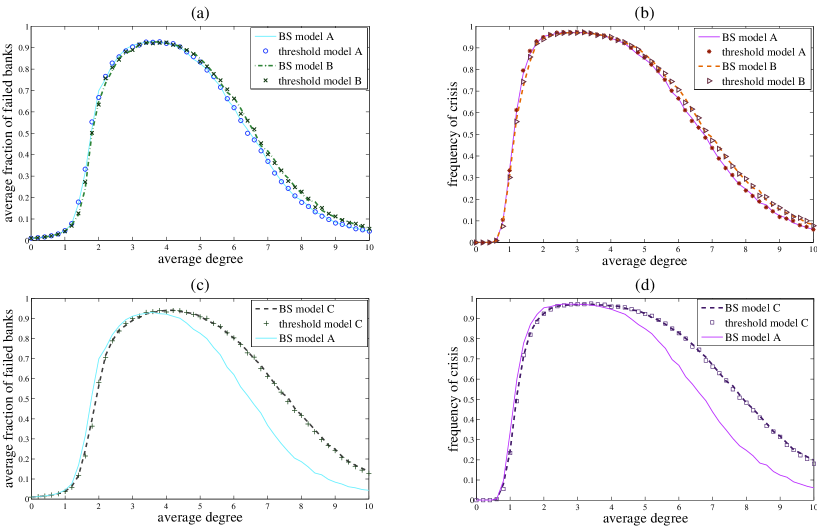

I consider three variants of the model: Cases A, B and C. In Case A, or the baseline model, the size of individual interbank assets is fixed at unity, and for In Case B, is assumed to be uniformly distributed on [.2, .4]. In Case 3, the size of individual interbank asset is uniformly distributed on [.2, 1.8].

In Figure 2, a balance sheet-based contagion model, called “BS model”, is compared with the corresponding threshold model. With respect to BS model C, the corresponding threshold model is modified as follows:

where is the sum of the flipped neighbors’ weights. It should be pointed out that is not necessarily equal to unless identical weights are given to all the neighbors.

Given the average degree, Erds-Rényi (directed) random networks are created 20 times, and asset returns and shadow thresholds are independently generated 1000 times for each network structure. Other parameters are as follows: , and .

Figure 2 reveals that in all cases, an appropriately defined threshold model can replicate the size and frequency of financial contagion created by the BS model.

4 Conclusion and discussion

The methods shown in this letter will enable us to analyze financial contagion without detailed information about every single balance sheet. What is needed is the distribution of balance-sheet components among banks. Fluctuations in asst returns and cross-sectional differences in various balance-sheet parameters can be incorporated into the threshold model.

Acknowledgments

I thank Kohei Hasui for his excellent research assistance. Financial support from KAKENHI 25780203 and 24243044 is gratefully acknowledged.

References

- 1 Dodds, P.S., Watts, D. J., 2004. Universal behavior in a generalized model of contagion. Phys. Rev. Lett. 92, 218701.

- 2 Gai, P., Kapadia, S., 2010. Contagion in financial networks. Proc. Roy. Soc. A. 466, 2401-2423.

- 3 Gai, P., Haldane, A., Kapadia, S., 2011. Complexity, concentration and contagion. J. Monetary. Econ. 58(5), 453-470.

- 4 Gleeson, J.P., 2013. Binary-state dynamics on complex networks: pair approximation and beyond. Phys. Rev. X. 3, 021004.

- 5 Gleeson, J.P., Cahalane, D.J., 2007. Seed size strongly affects cascades on random networks. Phys. Rev. E. 75, 056103.

- 6 Kobayashi, T., 2013. Network versus portfolio structure in financial systems. Eur. Phys. J. B. 86:434.

- 7 Kobayashi, T., Hasui, K., 2014. Efficient immunization strategies to prevent financial contagion. Sci. Rep. 4, 3834.

- 8 Lenzu, S., Tedeschi, G., 2012. Systemic risk on different interbank network topologies. Physica A. 391(18), 4331-4341.

- 9 Lorenz, J., Battiston, S., Shweitzer, F., 2009. Systemic risk in a unifying framework for cascading processes on networks. Eur. Phys. J. B. 71(4), 441-460.

- 10 Nier, E., Yang, J., Yorulmazer, T., Alentorn, A., 2007. Network models and financial stability. J. Econ. Dyn. Cont. 31(6), 2033-2060.

- 11 Soramäki, K., Bech, M.L., Arnold, J., Glass, R.J., Beyeler, W.E., 2007. The topology of interbank payment flows. Physica A. 379(1), 317-333.

- 12 Upper, C., 2011. Simulation methods to assess the danger of contagion in interbank markets. J. Financ. Stability. 7(3), 111-125.

- 13 Watts, D.J., 2002. A simple model of global cascades on random networks. Proc. Natl. Acad. Sci. USA. 99(9), 5766-5771.

- 14 Watts, D. J., Dodds, P. S., 2007. Influentials, networks, and public opinion formation. J. Consumer. Res. 34(4), 441-458.