Optimal Investment with Transaction Costs and Stochastic Volatility

Abstract

Two major financial market complexities are transaction costs and uncertain volatility, and we analyze their joint impact on the problem of portfolio optimization. When volatility is constant, the transaction costs optimal investment problem has a long history, especially in the use of asymptotic approximations when the cost is small. Under stochastic volatility, but with no transaction costs, the Merton problem under general utility functions can also be analyzed with asymptotic methods. Here, we look at the long-run growth rate problem when both complexities are present, using separation of time scales approximations. This leads to perturbation analysis of an eigenvalue problem. We find the first term in the asymptotic expansion in the time scale parameter, of the optimal long-term growth rate, and of the optimal strategy, for fixed small transaction costs.

AMS subject classification 91G80, 60H30.

JEL subject classification G11.

Keywords Transaction costs, optimal investment, asymptotic analysis, utility maximization, stochastic volatility.

1 Introduction

The portfolio optimization problem, first analyzed within a continuous time model in Merton (1969), ignores two key features that are important for investment decisions, namely transaction costs and uncertain volatility. Both these issues complicate the analysis of the expected utility maximization stochastic control problem, and obtaining closed-form optimal policies, or even numerical approximations, is challenging due to the increase in dimension by incorporating a stochastic volatility variable, and the singular control problem that arises by considering proportional transaction costs. Here, we develop asymptotic approximations for a particular long-run investment goal in a model with transaction costs and stochastic volatility.

The typical problem has an investor who can invest in a market with one riskless asset (a money market account), and one risky asset (a stock), and who has to pay a transaction cost for selling the stock. The costs are proportional to the dollar amount of the sale, with proportionality constant . The investment goal is to maximize the long-term growth rate. The original works all assumed stocks with constant volatility. Transaction costs were first introduced into the Merton portfolio problem by Magill and Constantinides (1976) and later further investigated by Dumas and Luciano (1991). Their analysis of the infinite time horizon investment and consumption problem gives an insight into the optimal strategy and the existence of a “no-trade” (NT) region. Under certain assumptions, Davis and Norman (1990) provided the first rigorous analysis of the same infinite time horizon problem. These assumptions were weakened by Shreve and Soner (1994), who used viscosity solutions to also show the smoothness of the value function.

When , and the volatility is constant, the optimal policy is to trade as soon as the position is sufficiently far away from the Merton proportion. More specifically, the agent’s optimal policy is to maintain her position inside a NT region. If the investor’s position is initially outside the NT region, she should immediately sell or buy stock in order to move to its boundary. She will trade only when her position is on the boundary of the NT region, and only as much as necessary to keep it from exiting the NT region, while no trading occurs in the interior of the region; see Davis et al. (1993).

There is a trade-off between the amount of transaction costs paid due to portfolio rebalancing and the width of the NT region. A smaller NT region generally increases the amount spent paying transaction costs in maintaining the optimal portfolio. Not surprisingly, the same behavior persists when volatility is stochastic, but in this case, the boundaries of NT region in general will no longer be straight lines as before. Hence, the approach of this paper, is to find a simple strategy that will be asymptoticaly optimal in both the volatility scaling and transaction costs parameters.

Small transaction cost asymptotic expansions (in powers of ) were used in Janecek and Shreve (2004) for an infinite horizon investment and consumption problem. This approach allows them to find approximations to the optimal policy and the optimal long-term growth rate, and is also used in Bichuch (2012) for a finite horizon optimal investment problem. The survey article Guasoni and Muhle-Karbe (2013) describes recent results using so-called shadow price to obtain small transaction cost asymptotics for the optimal investment policy, its implied welfare, liquidity premium, and trading volume. All of the above mentioned literature on transaction costs assumes constant volatility. Some recents exceptions are Kallsen and Muhle-Karbe (2013a, b), where the stock is a general Itô diffusion, and Soner and Touzi (2013) where the stock is described by a complete (local volatility) model. We summarize some of this literature and the individual optimization problems and models that they study in Table 1.

| Paper | Model | Utility | Objective | Solution |

|---|---|---|---|---|

| Dumas and Luciano (1991) | B-S | Power | LTGR | Explicit |

| Davis and Norman (1990) | B-S | Power | -consumption | Numerical |

| Shreve and Soner (1994) | B-S | Power | -consumption | Viscosity |

| Davis et al. (1993) | B-S | Exponential | Option pricing | Viscosity |

| Whalley and Wilmott (1997) | B-S | Exponential | Option pricing | -expansion |

| Janecek and Shreve (2004) | B-S | Power | -consumption | -expansion |

| Bichuch (2012) | B-S | Power | -expansion | |

| Dai et al. (2009) | B-S | Power | ODEs Free-Bdy | |

| Gerhold et al. (2014) | B-S | Power | LTGR | -expansion |

| Goodman and Ostrov (2010) | B-S | General | -expansion | |

| Choi et al. (2013) | B-S | Power | -consumption | ODEs Free-Bdy |

| Kallsen and Muhle-Karbe (2013a) | Itô | General | , consumption | -expansion |

| Kallsen and Muhle-Karbe (2013b) | Itô | Exponential | Option pricing | -expansion |

| Soner and Touzi (2013) | Local Vol | General on | -expansion | |

| Caflisch et al. (2012) | Stoch vol | Exponential | Option pricing | -SV expansion |

| This paper | Stoch vol | Power | LTGR | SV expansion |

Our approach exploits the fast mean-reversion of volatility (particularly when viewed over a long investment horizon) leading to a singular perturbation analysis of an impulse control problem. We treat the case, when the volatility is slow mean reverting separately. This complements multiscale approximations developed for derivatives pricing problems described in Fouque et al. (2011) and for optimal hedging and investment problems in Jonsson and Sircar (2002) and Fouque et al. (2013) respectively. Recently, Caflisch et al. (2012) study indifference pricing of European options with exponential utility, fast mean-reverting stochastic volatility and small transaction costs which scale with the volatility time scale. The current transaction cost problem can be characterized as a free-boundary problem. The fast mean-reversion asymptotics for the finite horizon free boundary problem arising from American options pricing was developed in Fouque et al. (2001), and recently there has been interest in similar analysis for perpetual (infinitely-lived) American options (used as part of a real options model) in Ting et al. (2013), and for a structural credit risk model in McQuade (2013). Here, we also have an infinite horizon free-boundary problem, but it is, in addition, an eigenvalue problem.

In Section 2 of this paper, we introduce our model and objective function and give the associated Hamilton-Jacobi-Bellman (HJB) equation. In Section 3 we perform the asymptotic analysis. We first consider the fast-scale stochastic volatility in Section 4, where we find the first correction term in the power expansion of the value function, and as a result also find the corresponding term in the power expansion of the optimal boundary. We perform similar analysis in the case of slow-scale stochastic volatility in Section 5. In Section 6 we show numerical calculations based on our results, and give an alternative intuitive explanation to the findings. We summarize the results obtained in the paper in Section 7, and leave some technical computations to the Appendix.

2 A Class of Stochastic Volatility Models with Transaction Costs

An investor can allocate capital between two assets – a risk-free money market account with constant rate of interest , and risky stock that evolves according to the following stochastic volatility model:

where and are Brownian motions, defined on a filtered probability space , with constant correlation coefficient : . We assume that is a smooth, bounded and strictly positive function, and that the stochastic volatility factor is a fast mean-reverting process, meaning that the parameter is small, and that is an ergodic process with a unique invariant distribution that is independent of . We refer to (Fouque et al., 2011, Chapter 3) for further technical details and discussion. Additionally are positive constants, and are smooth functions: examples will be specified later for computations.

2.1 Investment Problem

The investor must choose a policy consisting of two adapted processes and that are nondecreasing and right-continuous with left limits, and . The control represents the cumulative dollar value of stock purchased up to time , while is the cumulative dollar value of stock sold. Then, the wealth invested in the money market account and the wealth invested in the stock follow

The constant represents the proportional transaction costs for selling the stock.

Next, we define the solvency region

| (2.1) |

which is the set of all positions, such that if the investor were forced to liquidate immediately, she would not be bankrupt. This leads to a definition that a policy is admissible for the initial position and starting at time , if is in the closure of solvency region, , for all . (Since the investor may choose to immediately rebalance his position, we have denoted the initial time ). Let the set of all such policies. Clearly, if then we can always liquidate the position, and then hold the resulting cash position in the risk-free money market account. It is easy to adapt the proof in Shreve and Soner (1994) (for the constant volatility case) to show that if and only if

We work with CRRA or power utility functions defined on :

where is the constant relative risk aversion parameter. We are interested in maximizing:

where This is a problem in optimizing long term growth. To see the economic interpretation note that the quantity is the certainty equivalent of the terminal wealth . Hence if we can match this certainty equivalent with – the investor’s initial capital compounded at some rate , then For a survey and literature on this choice of objective function we refer to Guasoni and Muhle-Karbe (2013). This choice of optimization problem ensures the simplest HJB equation, which in this case turns out to be linear and time independent.

2.2 HJB Equation

Consider first the value function for utility maximization at a finite time horizon :

From Itô’s formula it follows that

Since must be a supemartingale, the and terms must not be positive. It follows that and . Alternatively,

| (2.2) |

We will define the no-trade () region, associated with , to be the region where both of these inequalities are strict. Moreover, for the optimal strategy, is a martingale, and so the term above must be zero inside the region. Thus it will then satisfy the HJB equation

| (2.3) |

where

| (2.4) | ||||

| (2.5) |

The fact that is a viscosity solution of (2.3) is standard, and a similar proof can be found for example in Shreve and Soner (1994), and thus will be omitted here. We will furthermore assume that the viscosity solution of (2.3) is in fact a classical solution, that is we will assume that it is sufficiently smooth. It can be shown that is smooth inside each of three regions: the , and the regions where and . The assumption that it is also smooth on the boundary of the is the smooth fit assumption, which is very common; see, for instance, Goodman and Ostrov (2010).

Next, we look for a solution of the HJB equation (2.3) of the form

| (2.6) |

where is a constant, and the function is to be found. However, we will not impose the final time condition on . For now, we will only assume that it is smooth and is bounded away from zero. We will define the NT region (associated with ) as the region where Additionally, we will assume that for any point in the NT region, the ratio is bounded. We note that is not equivalent to the value function , since we have not imposed the final time condition In fact there is no reason to believe that the final time condition can be satisfied if is given by (2.6).

However, if we find a constant such that , then it would follow that is the optimal growth rate and the NT region for the long-term optimal growth problem can be defined as the region where In other words,

We will now show that there exists a constant such that . Indeed, note that the utility function is homogeneous of degree , that is , it follows that

By our assumption, is bounded, being inside the NT region. Hence, there exists a constant such that

| (2.7) |

Since both and solve the HJB equation (2.3), it follows by a comparison theorem that everywhere. For the reader convenience, we have sketched the proof of it in Appendix A.

2.3 Free Boundary Formulation & Eigenvalue Problem

We will look for a solution to the variational inequality (2.8) in the following free-boundary form. The NT region is defined by (2.2), but for the function . Using the transformation (2.6), this translates to

for . Similar to the case with constant volatility, we assume that there exists a no-trade region, within which with boundaries and . We write this region as

where and are free boundaries to be found. In typical parameter regimes, we will have , so we can think of them as lower and upper boundaries respectively, with being the buy boundary, and the sell boundary. (The other two possibilities are that with being the buy boundary, and the sell boundary, or that with being the sell boundary, and the buy boundary. Under a constant volatility model these cases can be categorized explicitly in term of the model parameters: see Remark 1).

Inside this region we have from the HJB equation (2.8) that

| (2.14) |

The free boundaries and are determined by continuity of the first and second derivatives of with respect to , that is looking for a solution. In the buy region,

| (2.15) |

and so the smooth pasting conditions at the lower boundary are

| (2.16) | ||||

| (2.17) |

In the sell region, the transaction cost enters and we have:

| (2.18) |

Therefore the sell boundary conditions are:

| (2.19) | ||||

| (2.20) |

We note that (2.14), (2.15) and (2.18) are homogeneous equations with homogeneous boundary conditions (2.16), (2.17), (2.19) and (2.20), and so zero is a solution. However the constant is also to be determined, and in fact it is an eigenvalue found to exclude the trivial solution and give the optimal long-term growth rate. In the next section, we construct an asymptotic expansion in for this eigenvalue problem using these equations.

3 Fast-scale Asymptotic Analysis

We look for an expansion for the value function

| (3.1) |

as well as for the free boundaries

| (3.2) |

and the optimal long-term growth rate

| (3.3) |

which are asymptotic as .

Crucial to this analysis is the Fredholm alternative (or centering condition) as detailed in Fouque et al. (2011). In preparation, we will use the notation to denote the expectation with respect to the invariant distribution of the process , namely

| (3.4) |

The Fredholm alternative tells us that a Poisson equation of the form

has a solution only if the solvability condition is satisfied, and we refer for instance to (Fouque et al., 2011, Section 3.2) for technical details.

It is also convenient to introduce the differential operators

| (3.5) |

in terms of which the operators and in (2.9) are

In the following, a key role will be played by the squared-averaged volatility defined by

| (3.6) |

The principal terms in the expansions will be related to the constant volatility transaction costs problem, and we define the operator that acts in the no trade region by

| (3.7) |

and it is written as a function of the parameters and .

The zero-order terms in each of the asymptotic expansions (3.1), (3.2) and (3.3) are known and will be re-derived in Section 4. In the rest of this section, we calculate the next terms in the above asymptotic expansion in the case of fast-scale stochastic volatility.

3.1 Power expansion inside the NT region

In this subsection we will concentrate on constructing the expansion inside the NT region , where (2.8) holds. We now insert the expansion (3.1) and match powers of .

The terms of order lead to . Since the operator takes derivatives in , we seek a solution of the form , independent of .

At order , we have . But since takes a derivative in , , and so . Again, we seek a solution of the form that is independent of .

The terms of order one give

Since we have that takes derivatives in , and is independent of , we have that

| (3.8) |

This is a Poisson equation for with as the solvability condition. We observe that

where is the square-averaged volatility defined in (3.6), and is the constant volatility no trade operator defined in (3.7). Then we have

| (3.9) |

which, along with boundary conditions we will find in the next subsection, will determine .

3.2 Boundary Conditions

So far we have concentrated on the PDE (2.8) in the NT region. We now insert the expansions (3.1) and (3.2) into the boundary conditions (2.16)–(2.20). The terms of order one from (2.16) and (2.17) give

| (3.15) |

while the terms of order one from (2.16) and (2.17) give

| (3.16) |

Since is independent of , these equations imply that and are also independent of (they are constants).

Taking the order terms in (2.16) gives

Using the fact that , we see the terms in cancel, and we obtain

| (3.17) |

which is a mixed-type boundary condition for at the boundary .

From the order terms in (2.17), we obtain

| (3.18) |

and so, as does not depend on , is also a constant (independent of ) given by

| (3.19) |

3.3 Determination of

The next term in the asymptotic expansion solves the ODE (3.14), with boundary conditions (3.17) and (3.20), but we also need to find which appears in the equation. In fact, the Fredholm solvability condition for this equation determines , and so we look for the solution of the homogeneous adjoint problem.

To do that we first multiply both sides of (3.14) by and integrate from to :

| (3.22) |

Integration by parts gives

| (3.23) |

where is the adjoint operator to :

| (3.24) |

We set to satisfy

| (3.25) |

and, to cancel the boundary terms in (3.23), the boundary conditions

| (3.26) |

where we define the constants

| (3.27) |

Lemma 3.1.

Proof.

Now the left hand side of (3.22) is zero, and so we find that is given by

| (3.29) |

Note that is well defined, as the undetermined multiplicative constant of cancels in the ratio.

3.4 Summary of the Asymptotics

To summarize, we have sought the zeroth and first order terms in the expansions (3.1), (3.2) and (3.3) for . The principal terms are found from the eigenvalue problem described by ODE (3.9), with boundary and free boundary conditions (3.15)-(3.16):

The next term in the asymptotic expansion of the boundaries of the NT region, and of the optimal long-term growth rate and respectively, are given by (3.19), (3.21) and (3.29), and solves the ODE (3.14), with boundary conditions (3.17) and (3.20):

We describe the essentially-explicit solutions to these problems in the next section.

4 Building the Solution

In the previous section we have established that solve the constant volatility optimal growth rate with transaction costs problem, which is described in Dumas and Luciano (1991), but using the averaged volatility , where . In this section, we review how to find , and then use them to build the stochastic volatility corrections .

4.1 Building and

We denote by the solution to the constant volatility problem with volatility parameter and corresponding eigenvalue , and so

| (4.1) |

Assumption 4.1.

Without loss of generality assume that . The case can be handled similarly to the current case. The case is not interesting, as in this case one would not hold the risky stock at all. We also assume that the optimal proportion of wealth invested into the risky stock in case of constant volatility and zero transaction costs is less than 1:

| (4.2) |

We will refer to as the Merton proportion.

Remark 1.

It turns out that under the assumption (4.2), we will have . The other two cases when and when can be handled similarly. If , we would have , with being the buy boundary, and the sell boundary. If we had , then and is the sell boundary, and the buy boundary. For small enough, the same is true for and . The final case when is not interesting either, since in this case, all wealth will be invested into stock, and no trading will be necessary, except possibly at the initial time. Also, note that under these assumptions, we are assured that the NT region is non-degenerate.

In preparation, we define the following quantities. Given , we define

| (4.3) |

and let

| (4.4) |

where in both cases, we will suppress the dependency on . Additionally, let

where we have again suppressed the dependency on , and we also define

| (4.5) |

Proposition 4.2.

The function is given by

where, given , there are two cases:

- Real Case:

-

The eigenvalue is a real root of the algebraic equation

(4.6) and in (4.3) are real and distinct. Then

- Complex Case:

-

Otherwise, is the real root of the transcendental equation

(4.7) where the real and the imaginary parts of . Then

(4.8)

Proof.

We have that solves the ODE in the NT region:

| (4.9) |

with boundary conditions

| (4.10) | ||||

| (4.11) |

at the lower boundary and analogous conditions

| (4.12) | ||||

| (4.13) |

at the upper boundary . This is a free-boundary problem with two undetermined boundaries and two conditions on each boundary. We note that is a solution of (4.9) and the boundary conditions (4.10)–(4.13), but that the long-term growth rate also has to be found. In fact it will be determined as an eigenvalue that eliminates the trivial solution.

First, substituting from (4.10) and (4.11) into (4.9) at , we have

| (4.14) |

Then for a non-trivial , equation (4.14) becomes the quadratic equation

| (4.15) |

By substituting (4.12) and (4.13) into (4.9) at , we obtain the same equation

| (4.16) |

That is, are the two roots of the same quadratic (4.4).

Next, let and be the two independent solutions of the second-order ODE (4.9), so that the general solution is

| (4.17) |

for some constants . Inserting this form into the boundary conditions (4.10) and (4.12), and using the definitions in (4.5) gives the linear system

| (4.18) |

Then, for a non-trivial solution, we require the determinant of to be zero, which leads to

| (4.19) | |||

| (4.20) |

Note that (4.20) is an algebraic equation for the optimal long-term growth rate constant , where each term in the expression depends on through (4.9), (4.15) and (4.16).

As will only be determined up to a multiplicative constant, we can choose

| (4.21) |

The solutions of (4.9) can be written as powers: with defined in (4.3). If at the eigenvalue , the roots are real and distinct, then the transcendental equation (4.20) can be written as (4.6).

If the roots are complex at the eigenvalue , then the real-valued solutions of (4.9) are those given in (4.8), where are the real and imaginary parts of . Then, after some algebra, (4.20) transforms to (4.7). It cannot happen that the two roots are real and equal, , since this will contradict our conclusion in Remark 1 that the NT region is non-degenerate. ∎

In the zero transaction cost case , the no-trade region collapses and , which implies from (4.15) and (4.16) that , the Merton ratio, and that

| (4.22) |

For and small enough, we expect to be close (and smaller than) , and so in (4.4) are real. Moreover, we can expect whether we are in the real or complex case to be determined by the discriminant of the quadratic equation (4.3) for , namely

| (4.23) |

This reveals the following cases, as described in (Guasoni and Muhle-Karbe, 2013, Lemma 3.1):

- Case I:

-

If , then and , and we will be in the case of real for small enough.

- Case II:

-

If , then and and so we will be in the complex case if , and in the real case if is outside that interval.

Remark 2.

Additionally, it is shown in Gerhold et al. (2014) that the gap function defined by has the following asymptotic approximation as :

| (4.24) |

However, even though the asymptotic approximation (4.24) is very accurate for small transaction costs , we have used the numerical solution of (4.6) or (4.7) in both cases that the roots are real and complex respectively.

4.2 Finding and

In the previous section, we detailed the solution to the constant volatility problem, from which are found by formulas (4.1) using the averaged volatility . In the next proposition we give expressions for and . In preparation, we define the following constants which will be used in the formulas for the complex case:

| (4.25) | |||

| (4.26) |

Proposition 4.3.

If are real then

| (4.27) |

where , and

Moreover, is determined up to an additive multiple of by

| (4.28) |

for any , where and are given by

| (4.29) | ||||

| (4.30) |

The proof is given in Appendix B.

5 Slow-scale Asymptotics

We now consider another stochastic volatility approximation, but this time with slow-scale stochastic volatility:

| (5.1) | ||||

| (5.2) |

where the Brownian motions have correlation structure . As described in Fouque et al. (2011), there is empirical evidence for both a fast and slow scale in market volatility. Here we treat the optimal investment with transaction costs problem separately under each scenario for simplicity of exposition. The two approaches can be considered as different approximations for understanding the joint effects of stochastic volatility and costs of trading.

Then the analog of the HJB equation (2.8) is

| (5.3) |

where

and the operators were defined in (3.5). The definitions of the buy and sell operators stay the same as in (2.10)-(2.11). Similarly, we will work with the free-boundary eigenvalue formulation in Section 2.3, so that the analog of (2.14) in the no trade region is

| (5.4) |

We look for an expansion for the value function

| (5.5) |

as well as for the free boundaries

and the optimal excess growth rate which are asymptotic as .

5.1 Power expansion inside the NT region

We proceed similarly to Section 3.1 and analyze (5.4) inside the NT region. The terms of order one in (5.4) are

| (5.6) |

The operators in the boundary conditions (2.16)–(2.20) do not depend on and so the expansions in Section 3.2 are the same in the slow case as in the fast. Therefore, for the zeroth order problem, we have (3.15) and (3.16). This is the constant volatility problem with volatility , that is frozen at today’s level. Therefore we have

| (5.7) |

where are the solution described in Section 4.1. To simplify notation, we will typically cease to write the argument , and simply write .

5.2 Computation of

As in Section 4.2, we set to be the solution of the adjoint equation (3.25) with boundary conditions (3.26), but with replaced by . As before, Lemma 3.1 carries through with the new notation and we recall with similar to (3.27). Multiplying both sides of (5.9) by and integrating from to we get

where , and are the constant volatility solution, and we define

| (5.10) |

We observe that we need to compute , which depends on the eigenvalue , and so we will need the derivative . Computing the “Vega” of the constant volatility “value function” is difficult to perform analytically because appears in numerous places in the solution constructed in Section 4.1: the transcendental equation (4.6) or (4.7) for , the quadratic equations (4.3) and (4.15) for and and consequently in and . Numerically, computing a finite difference approximation is simple, but we will need to do so at many values of for use in certain integrals in the asymptotic correction in the next section. Therefore it is of interest to relate it to derivatives (or Greeks) of in the variable, in particular the Gamma , which we have found to be amenable to computation in the fast asymptotics.

First we give an expression for which avoids numerical differentiation of the eigenvalue problem.

Lemma 5.1.

The derivative is given by the following ratio of integrals:

| (5.11) |

Proof.

In the NT region and at the boundaries, we have

| (5.12) | ||||

| (5.13) | ||||

| (5.14) | ||||

| (5.15) | ||||

| (5.16) |

where . Differentiating the ODE (5.12) with respect to , we find that in the NT region, satisfies

| (5.17) |

We also have by differentiating (5.13) with respect to and using the smooth pasting condition (5.14) for that satisfies the usual homogeneous Neumann boundary condition at :

Similarly, differentiating (5.15) with respect to and using (5.16) gives:

We note that since is well-defined, so is by differentiation: we are just using equations it must satisfy to try and shortcut its computation. Then a Fredholm solvability condition for (5.17) determines . Multiplying equation (5.17) by the adjoint function , integrating by parts and using the boundary conditions satisfied by the vega yields (5.11). ∎

The expression for the Vega is given in Appendix C in the case of real . The formula in the complex case is very long and we omit it in this presentation. Writing the Vega in terms of spatial derivatives is related to the classical Vega-Gamma relationship for European option prices (see, for instance the discussion in (Fouque et al., 2011, Section 1.3.5)), which can be used to show that portfolios that are long Gamma (convex) and long volatility (positive Vega). In the context of the classical Merton portfolio optimization problem with no transaction costs, an analogous relationship between the derivative of the value function with respect to the Sharpe ratio and the negative of the second derivative with respect to the wealth variable is found in (Fouque et al., 2013, Lemma 3.1). For infinite horizon problems, as here, it is not so direct because there is no time derivative that allows for a simple explicit solution of equation (5.17) and its boundary conditions that would give in terms of , but nonetheless, a useful expression (C.1) can be found.

5.3 Computation of

We proceed, as in Section 4.2 to use the variation of parameters (B.2) to solve the inhomogeneous equation (5.9) with boundary conditions (3.17) and (3.20). We recall that the principal solution is given by formulas (4.17) and (4.21), where are the independent solutions of the the ODE (in ) (4.9) with the volatility . Then we have where solve the same system of equations (B.3) and (B.4),

| (5.18) | |||

| (5.19) |

and ′ denotes the derivative with respect to . The only change is that in this case,

| (5.20) |

The solution of the system (5.18)–(5.19) is given by

| (5.21) |

This determines . In the Proposition 5.2 that follows, we show how these can be explicitly computed in the case of real .

5.4 Explicit Computations of in the real case

For the rest this section we will show the computations of and , in the case when the roots of quadratic (4.3) (with ) are real. The complex case can also be calculated analytically, but we did not find the formulas to be enlightening, so we choose to omit the presentation of this calculation.

Proposition 5.2.

The proof is given in Appendix D.

6 Analysis of the results

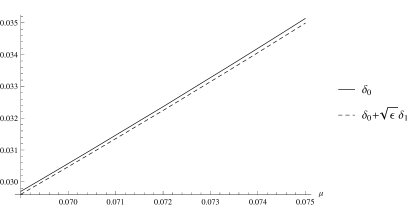

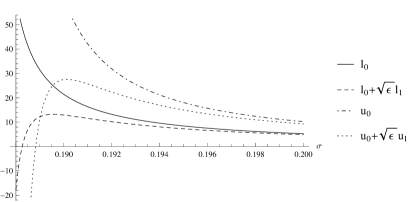

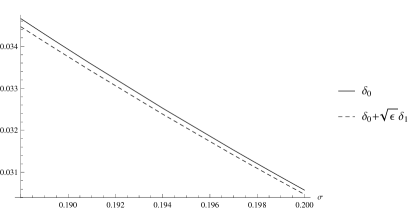

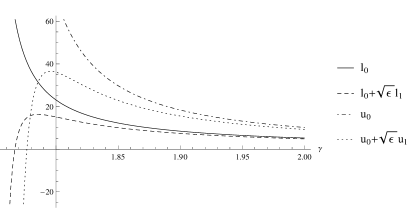

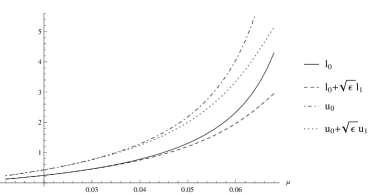

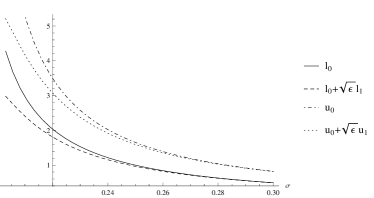

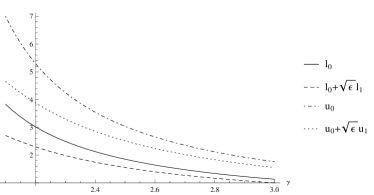

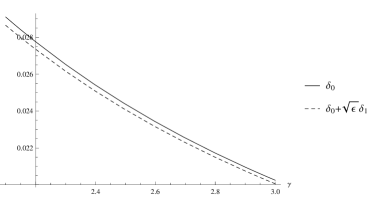

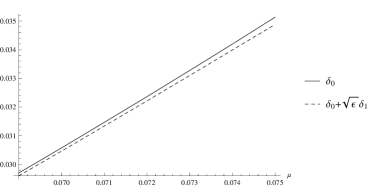

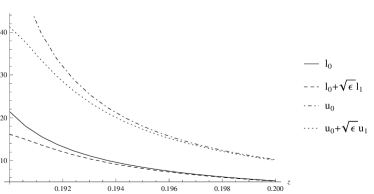

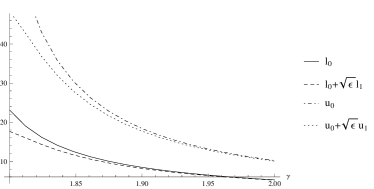

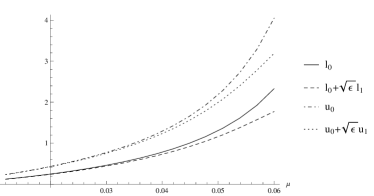

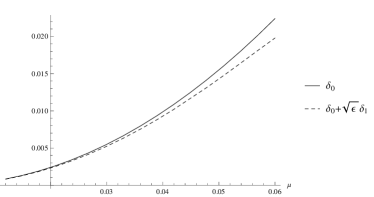

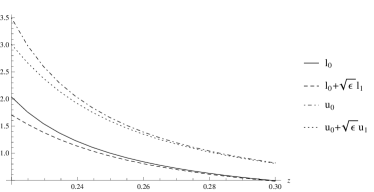

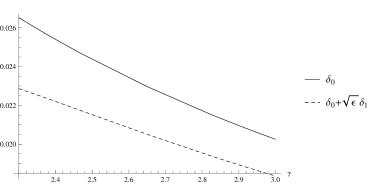

The following are graphs of the buy and the sell boundaries and and the long-term growth rate with constant volatility and the first order approximation to the buy and the sell boundaries with stochastic volatility and to the long-term growth rate . We have four separate cases: slow-scale and fast-scale stochastic volatility, and in each cases, two different sets of graphs that illustrate two additional cases: when the roots of equation (4.3) are real, and when they are complex.

The values used to obtain these graphs are for the case are real, and for the imaginary roots . Additionally, we have used in case of fast-scale real roots, in case of fast-scale complex, in case of slow-scale real roots, and in case of the complex roots. The reason for such vastly different in all the cases, is the desire to have the approximation to be close to the original boundaries.

We observe that the effect of stochastic volatility is to shift both the buy and the sell boundaries down. Interestingly, in case of fast-scale stochastic volatility, the shifts to the boundaries and do not depend on the current level of stochastic volatility factor. The intuitive explanation of this observation is the following: we emphasize that this is only approximation to the boundary. As such, even if the current position is away from the boundary, then in the time it takes the wealth ratio to reach the boundary, the volatility factor will have changed by . Hence, even at such close proximity to the boundary, the current volatility factor level is not important. What important is the average of the variance . Hence, in case of fast-scale stochastic volatility, only the average level plays a role. The situation is, of course, not analogous in the slow-scale case, where the current level is extremely important. As intuitively, we can use the same level of volatility factor, for a significant amount of time, with insignificant measurement error.

Intuitively, the effect of stochastic volatility should reduce (or at least not increase) the long-term growth rate , at least for small correlation , the intuition coming from Jensen’s inequality. Indeed,

| (6.1) | ||||

| (6.2) |

The right hand side, for , is approximately the total wealth using the average volatility , in case of fast-scale volatility, and the the total wealth using the initial volatility level in the slow-scale volatility. Hence, we expect in those cases.

It turns out however that the first order effect in case is zero. This is clear from the calculations, specifically (3.13), (3.29), (B.1), (B.6), that , and and thus so are and from (3.19) and (3.21), since all the terms are proportional to . This effect has been observed by Fouque et al. (2013).

Additionally, if , as is typically observed in the equity markets, the effect should be tighter NT region, and lower boundaries, than in case of constant volatility. The intuition here being that if the stock price goes up, the current volatility should be lower, while keeping the average volatility unchanged. This will cause the investor to start selling earlier. Similarly, when stock price goes down, the current volatility will tend to decrease, this will cause the investor to start buying later. Additionally, since the volatility will be quick to return to it’s average value, these changes would not be symmetric, and the width of the NT region will decrease. These changes can be observed in the following graphs too, especially in graphs of the boundaries as a function of in the the upper left of the graphs in Figures 1, 2, 3, 4.

We observe, that in all the cases the approximation does not differ much, from the original boundaries, as long as we’re sufficiently away from the case when Merton’s proportion In this case, it is known that the NT region degenerates, as it is optimal to trade only once, and invest all the wealth into the risky stock. In this cases, because the boundaries are positive, and increase to as the Merton’s optimal proportion approaches one. Additionally, both , and are negative, and they converge to as the Merton’s optimal proportion approaches one. Finally, it appears that the speed of the convergence of , and is faster than that of and . Hence, overall the approximation and the original boundaries cross each other before diverging. Even though, for any fixed the approximation would be very close to the original boundary, if is taken to be small enough. This is another reason why we have used different between the cases in the fast-scale and the slow-scale stochastic volatility. As the behaviors of the graphs is very different in the slow- and fast-scale cases and in the real and imaginary , as the Merton’s proportion approaches one.

The change to the equivalent safe rate from to exhibit more stability. In fact, it is almost a parallel shift down, in case of fast-scale stochastic volatility. However, in certain cases, specifically in fast-scale stochastic volatility, with complex roots we see that the approximation can be greater, then the original equivalent safe rate . This seems to be the case, because the shift is almost, but not entirely parallel, and with approximation term changes signs. For small drift and for large it is positive, whereas it’s negative in other cases. In case of slow-scale stochastic volatility factor, this shift is more pronounced, especially for low initial volatility factor and for high .

7 Conclusion

We have analyzed the Merton problem of optimal investment in the presence of transaction costs and stochastic volatility. This is tractable, when the problem is to maximize the long-term growth rate. This leads us to a perturbation analysis of an eigenvalue problem, and shows that the asymptotic method can be used to capture the principle effect of trading fees and volatility uncertainty. In particular we identify that the appropriate averaging, when volatility is fast mean reverting, is given by root-mean-square ergodic average . These techniques can also be adapted to the finite time horizon Merton problem, indifference pricing of options and other utility functions, on a case by case basis.

Appendix A Comparison Theorem

In this appendix, we will sketch a proof of the comparison theorem specifically adapted for our case, that shows that . We note, that a standard comparisons theorem for viscosity solutions can be easily adapted for the case such as the one in Bichuch and Shreve (2013). However, as far as we are aware, this proof is limited to the case as it requires the finite values on the boundary of the solvency region from (2.1). To circumvent these problems and provide a proof for all cases, we adapt the proof from Janecek and Shreve (2004). To streamline the proof, we will assume that all local martingales in the following argument are true martingales.

We remind the reader that we have made the assumption that are both smooth functions, namely, Additionally, we will also assume that there exists optimal strategies and for , and respectively. So that for we have that

In other words the no-trade region for is when the ratio of wealths is within . Similar, equations hold for with the no-trade region given by .

Sketch of the proof: We want to show that , for some fixed If , this follows from the terminal condition, and in case it can be shown by adapting the proof in Shreve and Soner (1994) that the optimal strategy is to liquidate the stock position, resulting in zero total wealth, in which case, , and . Hence, we proceed with the assumption that and and consider the strategy starting from at time that keeps, inside . For which we have that It follows that

| (A.1) | ||||

| (A.2) | ||||

| (A.3) |

Using the fact that the terms in (A.1) are zero by the optimality of the strategy we conclude that

| (A.4) | ||||

| (A.5) |

Taking the expectation, we conclude that

Writing an equation for similar to (A.1), and using the same strategy , we conclude that

| (A.6) | ||||

| (A.7) |

where we have used the fact that also solves the HJB equation (2.3). Again, taking the expectation, and recalling the final time condition (2.7), we conclude that

The other inequality can be proved similarly, by reversing the roles of and .

Appendix B Proof of Proposition 4.3

To find , we use the method of variation of parameters to solve the inhomogeneous equation (3.12), whose source (right-hand side) term after dividing by the coefficient of the 2nd derivative is

| (B.1) |

Specifically, we write

| (B.2) |

Then we need that solve the system of equations

| (B.3) | |||

| (B.4) |

Indeed, using (B.3), (B.4), and the fact that , we see that

| (B.5) |

The solution of the system (B.3)-(B.4) is

| (B.6) |

where the constants will be determined by the boundary conditions (3.17) and (3.20).

We divide the proof into two cases: the case when the roots of equation (4.3) are real, and the case when they are complex. These are presented in Sections B.1 and B.2 respectively.

B.1 Real

When the roots of the quadratic in (4.3) with volatility and at the eigenvalue are real, we have that

where were given in (4.21). We compute , where were defined in Proposition 4.3, and so the calculations for from the formula (3.29) leading to (4.27) are straightforward.

Next, we compute that

and so where are given in (4.29). Then, from (B.6), we have

and, from (B.2), we have

| (B.7) |

where we have absorbed some constants into and retained the same label as they have yet to be determined.

Inserting (B.7) into the boundary conditions (3.17) and (3.20) and dividing by , we obtain:

| (B.10) |

where the matrix from (4.18) evaluates in this case to

| (B.13) |

and the vector is

| (B.16) | ||||

| (B.19) |

and were defined in (4.5) and we insert the replacements .

We recall that is a singular matrix, as we have required that its determinant is zero by choice of in (4.20). The Fredholm alternative solvability condition for is satisfied by choice of in (3.29). Thus, we get a particular solution by taking and as given by (4.30). This determines as given in (4.28) up to the addition of a multiple of .

B.2 Complex

When the roots of the quadratic in (4.3) at the eigenvalue are complex, we have

where using the notation for defined in (3.27), and c± were chosen in (4.21).

We first compute . From (3.29), we have , where are the integrals in the numerator and denominator respectively to be computed. Using the change of variable , we have

where we define and as was defined in (4.25). Differentiating the formula in (4.8) amounts to multiplying the coefficients of the and terms by the matrix . Then reduces to

where were given in (4.26). Similarly, we have

where was also given in (4.26). These lead to the expression (4.31) for .

Next, we compute in (B.6) where was defined in (B.1). Again in the variable , we have

where denotes in co-ordinates, and the Wronskian simplifies to . We find that with was defined in (4.26). Then we obtain

The constants are determined by the boundary conditions (3.17) and (3.20). As before, we can take . Therefore, from (B.2), we have is given by (4.32) using definitions of and in (4.33)–(4.34).

Appendix C Explicit Calculation of the Vega in the Real Case

Appendix D Proof of Proposition 5.2

In the case when the roots are real, we have

| (D.1) |

It follows that

where we have used that together with the definitions of and in (5.27). A calculation shows that

Therefore, from (B.2), we have

| (D.2) | ||||

where we have absorbed some constants into and retained the same label as they have yet to be determined.

As before, we obtain a system of equation similar to (B.10) for , with the same matrix defined as before in (B.13), but with different right hand side vector , given by

| (D.3) | ||||

| (D.4) |

where . The second component is given by the same formula with replaced by . We recall that is a singular matrix, as we have required that its determinant is zero by choice of in (4.20). The Fredholm alternative solvability condition for is satisfied by choice of in (3.29). Thus, we get that a particular solution by taking and as defined in (5.28) This determines up to an addition of a multiple of as in (5.25) for any .

References

- Bichuch [2012] M. Bichuch. Asymptotic analysis for optimal investment in finite time with transaction costs. SIAM J. Financial Math., 3:433–458, 2012.

- Bichuch and Shreve [2013] M. Bichuch and S. Shreve. Utility maximization trading two futures with transaction costs. SIAM J. Financial Math., 4(1):26–85, 2013.

- Caflisch et al. [2012] R. E. Caflisch, G. Gambino, M. Sammartino, and C. Sgarra. European option pricing with transaction costs and stochastic volatility: an asymptotic analysis. 2012. Preprint.

- Choi et al. [2013] J. Choi, M. Sirbu, and G. Zitkovic. Shadow prices and well-posedness in the problem of optimal investment and consumption with transaction costs. SIAM J. Control Optim., 51(6):4414–4449, 2013.

- Dai et al. [2009] M. Dai, L. Jiang, P. Li, and F. Yi. Finite horizon optimal investment and consumption with transaction costs. SIAM J. Control Optim., 48(2):1134–1154, 2009.

- Davis and Norman [1990] M. Davis and A. Norman. Portfolio selection with transaction costs. Math. Oper. Res., 15(4):676–713, 1990.

- Davis et al. [1993] M. Davis, V. Panas, and T. Zariphopoulou. European option pricing with transaction costs. SIAM J. Control Optim., 31(2):470–493, 1993.

- Dumas and Luciano [1991] B. Dumas and E. Luciano. An exact solution to a dynamic portfolio choice problem under transaction costs. J. Finance, XLVI(2):577–595, 1991.

- Fouque et al. [2001] J.-P. Fouque, G. Papanicolaou, and R. Sircar. From the implied volatility skew to a robust correction to Black-Scholes American option prices. International Journal of Theoretical & Applied Finance, 4(4):651–675, 2001.

- Fouque et al. [2011] J.-P. Fouque, G. Papanicolaou, R. Sircar, and K. Sølna. Multiscale Stochastic Volatility for Equity, Interest-Rate and Credit Derivatives. Cambridge University Press, 2011.

- Fouque et al. [2013] J.-P. Fouque, R. Sircar, and T. Zariphopoulou. Portfolio optimization & stochastic volatility asymptotics. 2013. Submitted.

- Gerhold et al. [2014] S. Gerhold, P. Guasoni, J. Muhle-Karbe, and W.Schachermayer. Transaction costs, trading volume, and the liquidity premium. Finance and Stochastics, 18(1):1–37, 2014.

- Goodman and Ostrov [2010] J. Goodman and D. Ostrov. Balancing small transaction costs with loss of optimal allocation in dynamic stock trading strategies. Siam journal on applied mathematics, 70(6):1977–1998, 2010.

- Guasoni and Muhle-Karbe [2013] P. Guasoni and J. Muhle-Karbe. Portfolio choice with transaction costs: a user’s guide. In V. Henderson and R. Sircar, editors, Paris-Princeton Lectures on Mathematical Finance 2013. Springer, 2013.

- Janecek and Shreve [2004] K. Janecek and S. Shreve. Asymptotic analysis for optimal investment and consumption with transaction costs. Finance Stoch., 8(2):181–206, 2004.

- Jonsson and Sircar [2002] M. Jonsson and R. Sircar. Partial hedging in a stochastic volatility environment. Mathematical Finance, 12(4):375–409, October 2002.

- Kallsen and Muhle-Karbe [2013a] J. Kallsen and J. Muhle-Karbe. The general structure of optimal investment and consumption with small transaction costs. 2013a. URL http://arxiv.org/abs/1303.3148.

- Kallsen and Muhle-Karbe [2013b] J. Kallsen and J. Muhle-Karbe. Option pricing and hedging with small transaction costs. Mathematical Finance, 2013b.

- Magill and Constantinides [1976] M. Magill and G. Constantinides. Portfolio selection with transactions costs. J. Econom. Theory, 13(2):245–263, 1976.

- McQuade [2013] T. McQuade. Stochastic volatility and asset pricing puzzles. Technical report, 2013.

- Merton [1969] R. C. Merton. Lifetime portfolio selection under uncertainty: the continous-time case. Rev. Econom. Statist., 51:247–257, 1969.

- Shreve and Soner [1994] S. Shreve and H.M. Soner. Optimal investment and consumption with transaction costs. Ann. Appl. Prob., 4:609–692, 1994.

- Soner and Touzi [2013] H.M. Soner and N. Touzi. Homogenization and asymptotics for small transaction costs. SIAM J. Control Optim., 51(4):2893–2921, 2013.

- Ting et al. [2013] S. Ting, C.-O. Ewald, and W.-K. Wang. On the investment-–uncertainty relationship in a real option model with stochastic volatility. Mathematical Social Sciences, 2013. In press.

- Whalley and Wilmott [1997] A.E. Whalley and P. Wilmott. An asymptotic analysis of an optimal hedging model for option pricing with transaction costs. Mathematical Finance, 7(3):307–324, 1997.