Adaptive, Anisotropic and Hierarchical

cones of Discrete Convex functions††thanks:

This work was partly supported by ANR grant NS-LBR ANR-13-JS01-0003-01.

Abstract

We introduce a new class of adaptive methods for optimization problems posed on the cone of convex functions. Among the various mathematical problems which posses such a formulation, the Monopolist problem [24, 10] arising in economics is our main motivation.

Consider a two dimensional domain , sampled on a grid of points. We show that the cone of restrictions to of convex functions on is typically characterized by linear inequalities; a direct computational use of this description therefore has a prohibitive complexity. We thus introduce a hierarchy of sub-cones of , associated to stencils which can be adaptively, locally, and anisotropically refined. We show, using the arithmetic structure of the grid, that the trace of any convex function on is contained in a cone defined by only linear constraints, in average over grid orientations.

Numerical experiments for the Monopolist problem, based on adaptive stencil refinement strategies, show that the proposed method offers an unrivaled accuracy/complexity trade-off in comparison with existing methods. We also obtain, as a side product of our theory, a new average complexity result on edge flipping based mesh generation.

A number of mathematical problems can be formulated as the optimization of a convex functional over the cone of convex functions on a domain (here compact and two dimensional):

This includes optimal transport, as well as various geometrical conjectures such as Newton’s problem [16, 18]. We choose for concreteness to emphasize an economic application: the Monopolist (or Principal Agent) problem [24], in which the objective is to design an optimal product line, and an optimal pricing catalog, so as to maximize profit in a captive market. The following minimal instance is numerically studied in [1, 10, 21] and on Figure 1. With

| (1) |

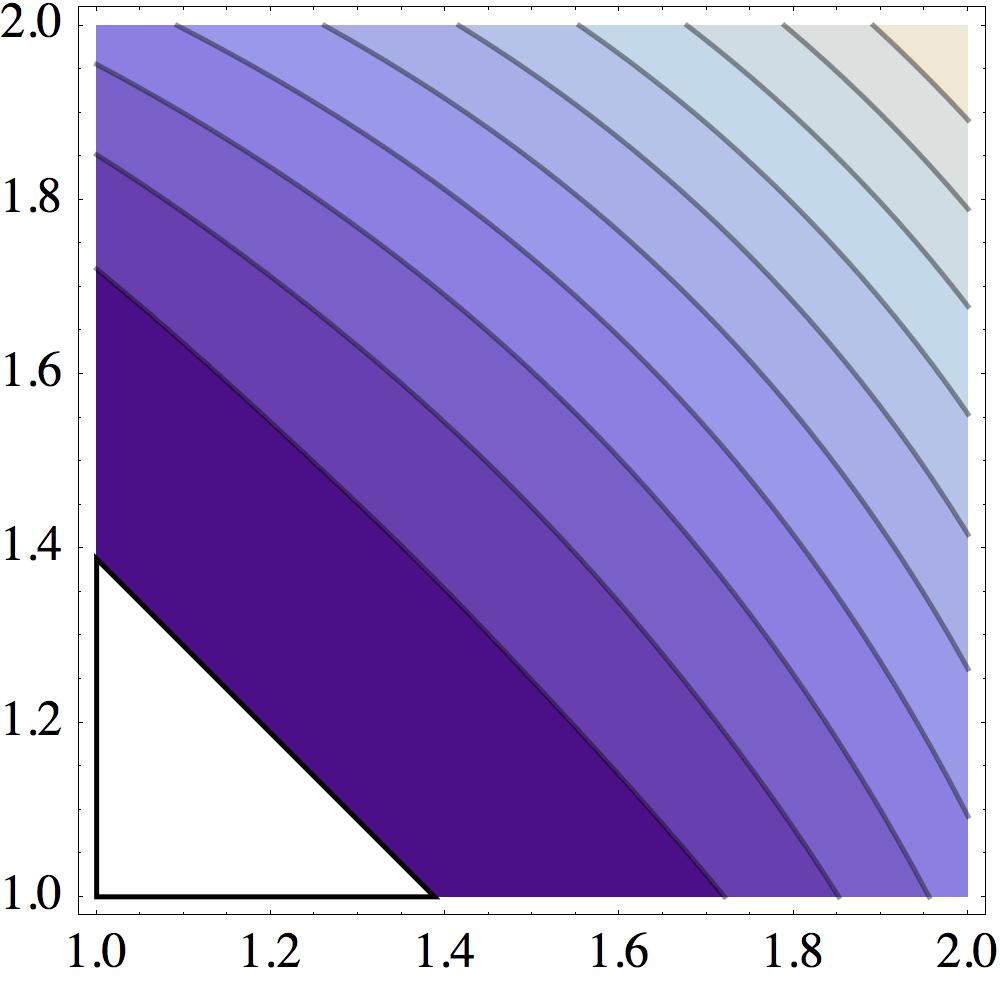

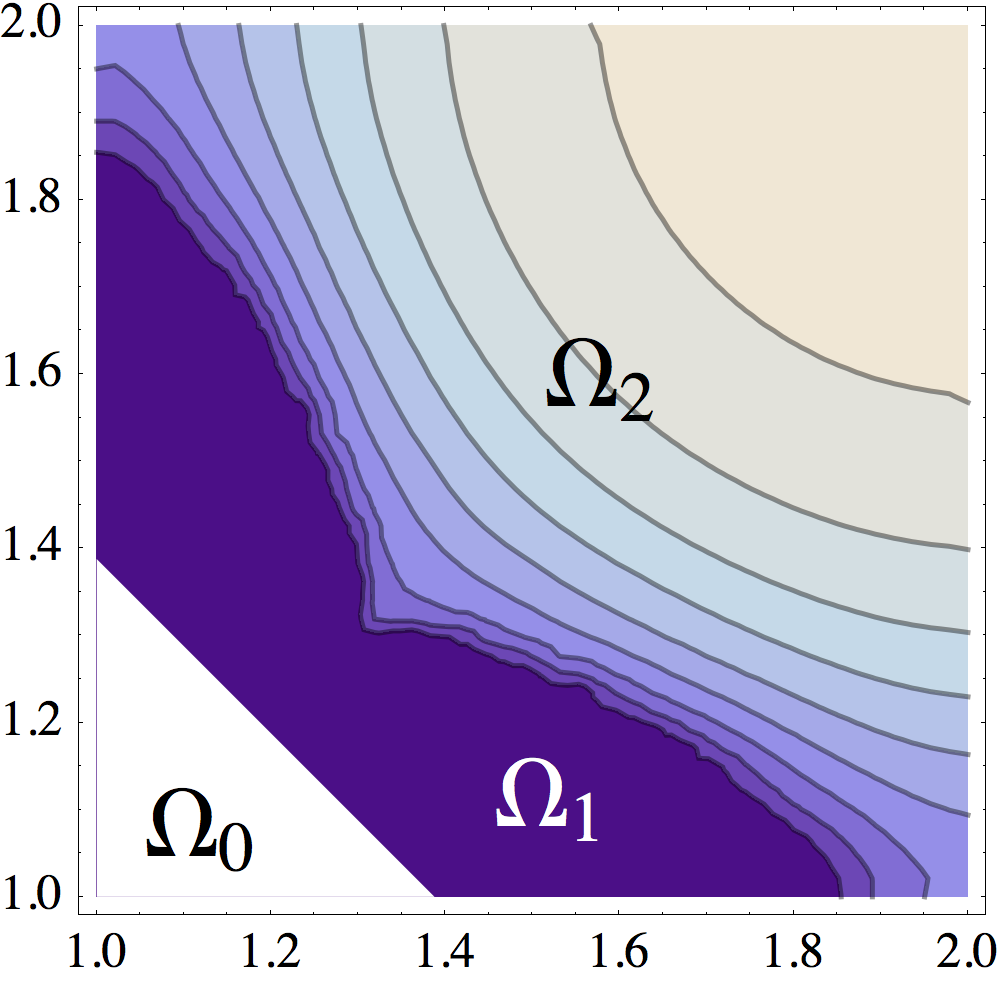

We refer to the numerical section §6, and to [24] for the economic model details; let us only say here that the Monopolist’s optimal product line is , and that the optimal prices are given by the Legendre-Fenchel dual of . Consider the following three regions, defined for (implicitly excluding points close to which is not smooth)

| (2) |

Strong empirical evidence suggests that these three regions have a non-empty interior, although no qualitative mathematical theory has yet been developed for these problems. The optimal product line observed numerically, Figure 1, confirms a qualitative (and conjectural) prediction of the economic model [24] called “bunching”: low-end products are less diverse than high-end ones, down to the topological sense. (The monopolist willingly limits the variety of cheap products, because they may compete with the more expensive ones, on which he has a higher margin.)

We aim to address numerically optimization problems posed on the cone of convex functions, through numerical schemes which preserve the rich qualitative properties of their solutions, and have a moderate computational cost. In order to put in light the specificity of our approach, we review the existing numerical methods for these problems, which fall in the following categories. We denote by a grid sampling of the domain , and by the cone of discrete (restrictions of) convex functions

| (3) |

-

•

(Interior finite element methods) For any triangulation of , consider the cone

A natural but invalid numerical method for (1) is to fix a-priori a family of regular triangulations of , where denotes mesh scale, and to optimize the functional of interest over the associated cones. Indeed, the union of the cones is not dense in , see [7]. Let us also mention that for a given generic , there exists only one triangulation of such that , see §1.3.

-

•

(Global constraints methods) The functional of interest, suitably discretized, is minimized over the cone of discrete convex functions [5], or alternatively [10] on the augmented cone

(4) in which we refer by to arbitrary elements of the subgradient of the convex map .

Both and are characterized by a family of long range linear inequalities, with domain wide supports, and of cardinality growing quadratically with , see §1.1 and [10]. Despite rather general convergence results, these two methods are impractical due to their expensive numerical cost, in terms of both computation time and memory.

-

•

(Local constraints methods) Another cone is introduced, usually satisfying neither nor , but typically characterized by relatively few constraints, with short range supports. Obermann et al. [22, 21] use linear constraints, with . Merigot et al. [18] use slightly more linear constraints, but provide an efficient optimization algorithm based on proximal operators. Aguilera et al. [1] consider constraints of semi-definite type.

-

•

(Geometric methods) A polygonal convex set can be described as the convex hull of a finite set of points, or as an intersection of half-spaces. Geometric methods approximate a convex function by representing its epigraph under one of these forms. Energy minimization is done by adjusting the points position, or the coefficients of the affine forms defining the half-spaces, see [26, 16].

The main drawback of these methods lies in the optimization procedure, which is quite non-standard. Indeed the discretized functional is generally non-convex, and the polygonal structure of the represented convex set changes topology during the optimization.

We propose an implementation of the constraint of convexity via a limited (typically quasi-linear) number of linear inequalities, featuring both short range and domain wide supports, which are selected locally and anisotropically in an adaptation loop using a-posteriori analysis of solutions to intermediate problems. Our approach combines the accuracy of global constraint methods, with the limited cost of local constraint ones, see §6.3. It is based on a family of sub-cones

each defined by some linear inequalities associated to a family of stencils, see Definition 1.7. These stencils are the data of a collection of offsets pointing to selected neighbors of any point , and satisfying minor structure requirements, see Definition 1.6. The cones satisfy the hierarchy property , see Theorem 1.8. Most elements of belong to a cone defined by only linear inequalities, in a sense made precise by Theorem 1.11. Regarding both stencils and triangulations as directed graphs on , we show in Theorem 1.13 (under a minor technical condition) that the cone is the union of the cones associated to triangulations included in . Our hierarchy of cones has similarities, but also striking differences as discussed in conclusion, with the other multiscale constructions (wavelets, adaptive finite elements) used in numerical analysis.

The minimizer of a given convex energy can be obtained without ever listing the inequalities defining (which would often not fit into computer memory for the problem sizes of interest), but only solving a small sequence of optimization problems over sub-cones associated to stencils , designed through adaptive refinement strategies. Our numerical experiments give, we believe, unprecedented numerical insight on the qualitative behavior of the monopolist problem and its variants. Thanks to the adaptivity of our scheme, this accuracy is not at the expense of computation time or memory usage. See §6.

1 Main results

The constructions and results developed in this paper apply to an arbitrary convex and compact domain , discretized on an orthogonal grid of the form:

| (5) |

where is a scale parameter, is the rotation of angle , and is an offset. The latter two parameters are used in our main approximation result Theorem 1.11, heuristically to eliminate by averaging the influence of rare unfavorable cases in which the approximated convex function hessian is degenerate in a direction close to the grid axes. For simplicity, and up to a linear change of coordinates, we assume unless otherwise mentionned that these parameters take their canonical values:

The choice of a grid discretization provides arithmetic tools that would not be available for an unstructured point set.

Definition 1.1.

-

1.

An element is called irreducible iff .

-

2.

A basis of is a pair such that . A basis of is direct iff , and acute iff .

Considering special (non-canonical) bases of is relevant when discretizing anisotropic partial differential equations on grids, such as anisotropic diffusion [11], or anisotropic eikonal equations [19]. In this paper, and in particular in the next proposition, we rely on a specific two dimensional structure called the Stern-Brocot tree [13], also used in numerical analysis for anisotropic diffusion [2], and eikonal equations of Finsler type [20].

Proposition 1.2.

The application defines a bijection between direct acute bases of , and irreducible elements such that . The elements are called the parents of . (Unit vectors have no parents.)

Proof.

Existence, for a given irreducible with , of the direct acute basis such that . We assume without loss of generality that has non-negative coordinates. Since and we obtain that and . Classical results on the Stern-Brocot tree [13] state that the irreducible positive fraction can be written as the mediant of two irreducible fractions , (possibly equal to or ), with and . Setting and concludes the proof.

Uniqueness. Assume that , where , are direct acute bases of . One has , and likewise . Hence , and therefore for some scalar , which is an integer since is irreducible. Subtracting we obtain , and therefore

This expression is negative unless the integer is zero, hence , and . ∎

1.1 Characterization of discrete convexity by linear inequalities

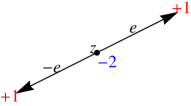

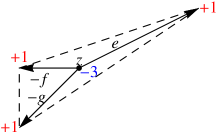

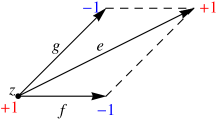

We introduce some linear forms on the vector space , which non-negativity characterizes restrictions of convex maps. The convex hulls of their respective supports have respectively the shape of a segment, a triangle, and a parallelogram, see Figure 2.

Definition 1.3.

For each , consider the following linear forms of .

-

1.

(Segments) For any irreducible :

-

2.

(Triangles) For any irreducible , with , of parents :

-

3.

(Parallelograms) For any irreducible , with , of parents :

A linear form among the above can be regarded as a finite weighted sum of Dirac masses. In this sense we define the support , . The linear form is also defined on whenever .

If , then by an immediate convexity argument one obtains and , whenever these linear forms are supported on . As shown in the next result, this provides a minimal characterization of by means of linear inequalities. The linear forms will on the other hand be used to define strict sub-cones of . The following result corrects222Precisely, the constraints were omitted in [5] for . Corollary 4 in [5].

Theorem 1.4.

-

•

The cone is characterized by the non-negativity of the linear forms and , introduced in Definition 1.3, which are supported in .

-

•

If one keeps only one representative among the identical linear forms and , then the above characterization of by linear inequalities is minimal.

For any given , the number of linear inequalities (resp. ) appearing in the characterization of is bounded by the number of irreducible elements such that . Hence the -dimensional cone is characterized by at most linear inequalities, where .

If all the elements of are aligned, this turns out to be an over estimate: one easily checks that exactly inequalities of type remain, and no inequalities of type . This favorable situation does not extend to the two dimensional case however, because irreducible elements arise frequently in , with positive density [14]:

If the domain has a non-empty interior, then one easily checks from this point that the minimal description of given in Theorem 1.4 involves no less than linear constraints333This number of constraints is empirically (and slightly erroneously) estimated to in [5]. , where the constant depends on the domain shape but not on its scale (or equivalently, not on the grid scale in (5)). This quadratic number of constraints, announced in the description of global constraint methods in the introduction, is a strong drawback for practical applications, which motivates the construction of adaptive sub-cones of in the next subsection.

Remark 1.5 (Directional convexity).

Several works addressing optimization problems posed on the cone of convex functions [5, 22], have in the past omitted all or part of the linear constraints , , irreducible with . We consider in Appendix A this weaker notion of discrete convexity, introducing the cone of directionally convex functions, defined by the non-negativity of only , , irreducible.

We show that elements of cannot in general be extended into globally convex functions, but that one can extend their restriction to a grid coarsened by a factor . We also introduce a hierarchy of sub-cones of , similar to the one presented in the next subsection.

1.2 Hierarchical cones of discrete convex functions

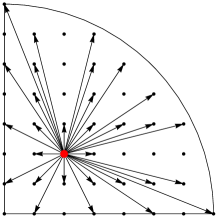

We introduce in this section the notion of stencils on , and discuss the properties (hierarchy, complexity) of cones attached to them. The following family of sets is referred to as the “maximal stencils”: for all

| (6) |

The convex cone generated by a subset of a vector space is denoted by , with the convention .

Definition 1.6.

A family of stencils on (or just: “Stencils on ”) is the data, for each of a collection (the stencil at ) of irreducible elements of , satisfying the following properties:

-

•

(Stability) Any parent , of any , satisfies .

-

•

(Visibility) One has .

The set of candidates for refinement consists of all elements which two parents belong to .

In other words, a stencil at a point contains the parents of its members whenever possible (Stability), and covers all possible directions (Visibility). By construction, these properties are still satisfied by the refined stencil , for any candidate for refinement . The collection is easily recovered from , see Proposition 3.8.

Definition 1.7.

We attach to a family of stencils on the cone , characterized by the non-negativity of the following linear forms: for all

-

1.

, for all such that .

-

2.

for all , with , such that .

-

3.

for all (by construction ).

When discussing unions, intersections, and cardinalities, we (abusively) identify a family of stencils on with a subset of :

| (7) |

Note that the cone is defined by at most linear inequalities. The sets are clearly stencils on , which are maximal for inclusion, and by Theorem 1.4 we have . The cone always contains the quadratic function , for any family of stencils. Indeed, the inequalities , , , and , , hold by convexity of . In addition for all , of parents , one has

since the basis of is acute by definition, see Proposition 1.2.

Theorem 1.8 (Hierarchy).

The union , and the intersection of two families of stencils are also families of stencils on . In addition

| (8) | ||||

| (9) |

As a result, if two families of stencils satisfy , then

The left inclusion follows from (8), and the right inclusion from (9) applied to and . The intersection rule (8) also implies the existence of stencils minimal for inclusion, which are illustrated on Figure 3 and characterized in Proposition 5.1.

Remark 1.9 (Optimization strategy).

For any , there exists by (8) a unique smallest (for inclusion) family of stencils such that . If is the minimizer of an energy on , then it can be recovered by minimizing on the smaller cone , defined by linear constraints. Algorithm 1 in §6, attempts to find these smallest stencils (or slightly larger ones), starting from and performing successive adaptive refinements.

In the rest of this subsection, we fix a grid scale and consider for all , and all , the grid

| (10) |

The notions of stencils and related cones trivially extend to this setting, see §5 for details. We denote by the domain area, and by its diameter. We also introduce rescaled variants, defined for by

For any parameters , one has denoting (with underlying constants depending only on the shape of )

| (11) |

Proposition 1.10.

Let , for some grid position parameters , , and let . Let , and let be the minimal stencils on such that . Then , for some universal constant (i.e. independent of ).

Combining this result with (11) we see that an optimization strategy as described in Remark 1.9 should heuristically not require solving optimization problems subject to more than linear constraints. This is already a significant improvement over the linear constraints defining . The typical situation is however even more favorable: in average over randomized grid orientations and offsets , the restriction to of a convex map (e.g. the global continuous solution of the problem (1) of interest) belongs to a cone defined by a quasi-linear number of linear inequalities.

Theorem 1.11.

Let , and let be the minimal stencils on such that , for all , . Assuming , one has for some universal constant (i.e. independent of ):

| (12) |

1.3 Stencils and triangulations

We discuss the connections between stencils and triangulations, which provides in Theorem 1.13 a new insight on the hierarchy of cones , and yields in Theorem 1.15 a new result of algorithmic geometry as a side product of our theory. We assume in this subsection and §4 that the discrete domain convex hull, denoted by , has a non-empty interior. All triangulations considered in this paper are implicitly assumed to cover and to have as collection of vertices.

Definition 1.12.

Let be a triangulation, and let be a family of stencils on . We write iff the directed graph associated to is included in the one associated to . In other words iff for any edge of , one has .

The next result provides a new interpretation to our approach to optimization problems posed on the cone of convex functions, as a relaxation of the naïve (and flawed without this modification) method via interior finite elements.

Theorem 1.13.

Let be a family of stencils on . If has a non-empty interior, then

| (13) |

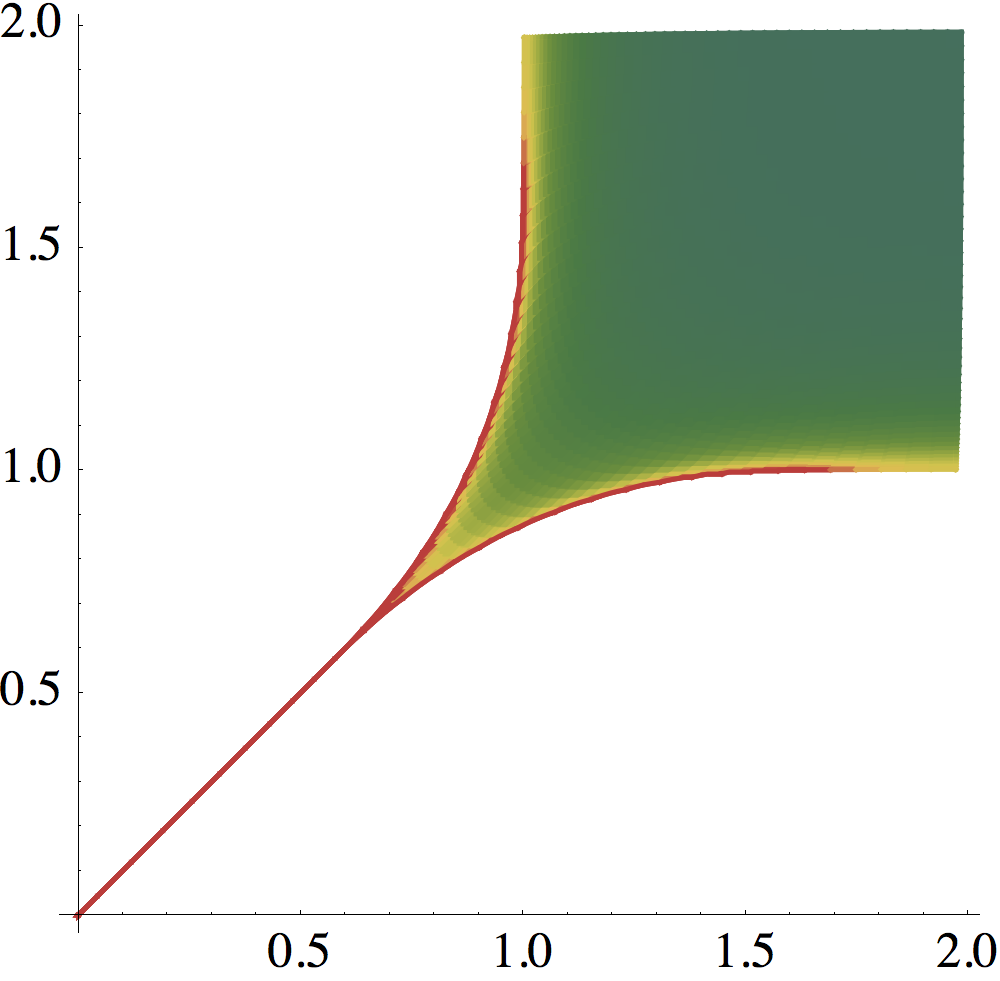

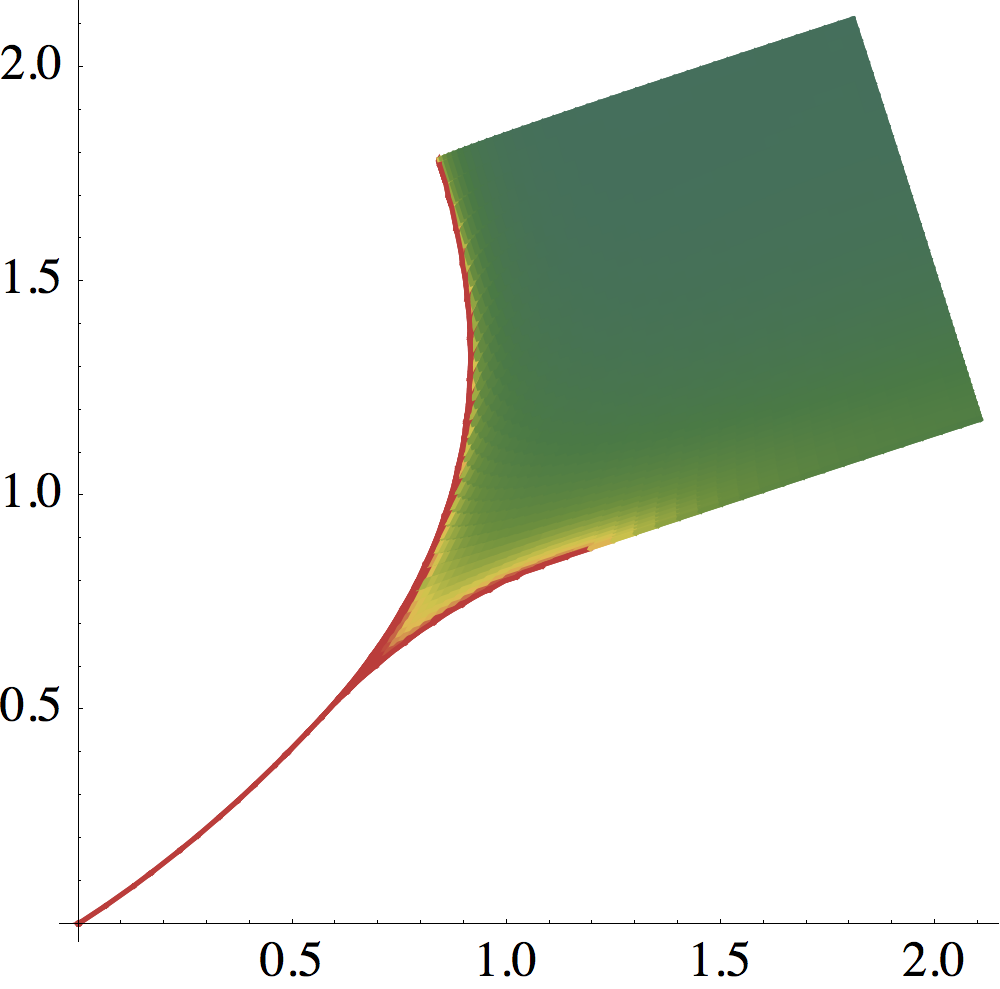

Delaunay triangulations are a fundamental concept in discrete geometry [9]. We consider in this paper a slight generalization in which the lifting map needs not be the usual paraboloid, but can be an arbitrary convex function, see Definition 1.14. Within this paper Delaunay triangulations are simultaneously (i) a theoretical tool for proving results, notably Proposition 1.10 and Theorem 1.13, (ii) an object of study, since in Theorem 1.15 we derive new results on the cost of their construction, and (iii) a numerical post-processing tool providing global convex extensions of elements of , see Figure 4 and Remark 6.3.

Definition 1.14.

We say that is an -Delaunay triangulation iff ; equivalently the piecewise linear interpolation is convex. We refer to as the lifting map.

A -Delaunay triangulation, with , is simply called a Delaunay triangulation.

Two dimensional Delaunay triangulations, and three dimensional convex hulls, have well known links [9]. Indeed is an -Delaunay triangulation iff the map spans the bottom part of the convex envelope of lifted set . As a result of this interpretation, we find that (i) any element admits an -Delaunay triangulation, and (ii) generic elements of admit exactly one -Delaunay triangulation (whenever all the faces of are triangular). In particular, the union (13) is disjoint up to a set of Hausdorff dimension .

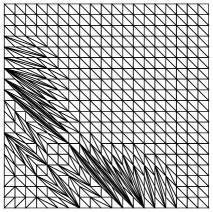

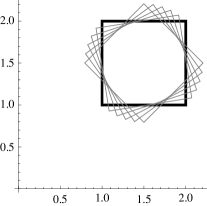

Any two triangulations of can be transformed in one another through a sequence of elementary modifications called edge flips, see Figure 4. The minimal number of such operations is called the edge flipping distance between and . Edge flipping is a simple, robust and flexible procedure, which is used in numerous applications ranging from fluid dynamics simulation [8] to GPU accelerated image vectorization [23]. Sustained research has been devoted to estimating edge flipping distances within families of triangulations of interest [15], although flipping distance bounds are usually quadratic in the number of vertices.

Theorem 1.15.

Let be a family of stencils on , and let . Then any standard Delaunay triangulation of can be transformed into an -Delaunay triangulation via a sequence of edge flips. The constant is universal (in particular it is independent of ).

Combining this result with Theorem 1.11, we obtain that only edge flips are required to construct an -Delaunay triangulation of , with , for any convex function , in an average sense over grid orientations. Note that (more complex and specialized) convex hull algorithms [6] could also be used to produce an -Delaunay triangulation, at the slightly lower cost . Theorem 1.15 should be understood as a first step in understanding the typical behavior of edge flipping.

1.4 Outline

We prove in §2 the characterization of discrete convexity by linear constraints of Theorem 1.4. The hierarchy properties of Theorem 1.8 are established in §3. Triangulation related arguments are used in §4 to show Proposition 1.10 and Theorems 1.13 and 1.15. The average cardinality estimate of Theorem 1.11 is proved in §5. Numerical experiments, and algorithmic details, are presented in §6. Finally, the weaker notion of directional convexity is discussed in Appendix A.

2 Characterization of convexity via linear constraints

This section is devoted to the proof of Theorem 1.4, which characterizes discrete convex functions via linear inequalities. The key ingredient is its generalization, in [5], to arbitrary unstructured finite point sets (in contrast with the grid structure of ).

Theorem 2.1 (Carlier, Lachand-Robert, Maury).

Let be a convex domain, and let be an arbitrary finite set. The cone , of all restrictions to of convex functions on , is characterized by the following inequalities, none of which can be removed:

-

•

For all , all , , such that and :

(14) -

•

For all , all with , such that , the points are not aligned and :

(15)

In the following, we establish Theorem 1.4 by specializing Theorem 2.1 to the grid , and identifying (14) and (15) with the constraints and respectively, in Propositions 2.2 and 2.5 respectively. Note that the cases (14) and (15) are unified in [5], although we separated them in the above formulation for clarity. For , we denote

Proposition 2.2.

Let , , , be such that and . Then and there exists an irreducible such that , . (Thus .)

Proof.

We define , and assume for contradiction that is not irreducible: , for some integer and some . Then , which is a contradiction. Thus is irreducible, and likewise is irreducible. Observing that is negatively proportional to , namely , we obtain that , which concludes the proof. ∎

The next lemma, used in Proposition 2.5 to identify the constraints (15), provides an alternative characterization of the parents of an irreducible vector, see Proposition 1.2.

Lemma 2.3.

Let be such that , , and . Then are the parents of .

Proof.

Since , the vector is irreducible. In addition, , since otherwise would be three pairwise linearly independent unit vectors in . Let be the parents of . Observing that , we obtain that for some scalar , which must be an integer since is irreducible. If then which is a contradiction (recall that ). If , then observing that we obtain likewise a contradiction. Hence and are the parents of , which concludes the proof. ∎

Corollary 2.4.

Let be a basis of which is not acute. If , then is a parent of , and otherwise it is a parent ot .

Proof.

Up to exchanging the roles of , we may assume that . Denoting , we have by Lemma 2.3 three possibilities: (i) , and are the parents of , (ii) , and are the parents of , (iii) , and are the parents of . Excluding (i), since is not an acute basis, we conclude the proof. ∎

Proposition 2.5.

Let , , with , be such that , the points are not aligned, and . Then and, up to permuting , there exists an irreducible with , of parents , such that , , and . (Thus .)

Proof.

Let , , . Up to permuting , we may assume that and . Note that and are not collinear since lies in the interior of . We claim that is a basis of . Indeed, otherwise, the triangle would contain an element of distinct from its vertices. Since is convex, this implies , which is a contradiction.

Thus , and likewise and , are bases of , and therefore

| (16) |

Injecting in the above equation the identity , we obtain that and . Thus since these coefficients are positive and sum to one. Finally, we have , , and is a direct basis. Using Lemma 2.3 we conclude as announced that are the parents of . ∎

3 Hierarchy of the cones

This section is devoted to the proof of Theorem 1.8, which is split into two parts: the proof that an intersection (or union) of stencils is still a stencil, and the hierarchy properties (8) and (9).

3.1 An intersection of stencils is still a stencil

Let be families of stencils on . Property (Stability) of stencils immediately holds for the intersection and union, , while property (Visibility) is also clear for the union . In order to establish property (Visibility) for the intersection , we identify in Proposition 3.7 a family of stencils which included in any other. From and we obtain , so that (Visibility) for implies the same property for .

Definition 3.1.

The cyclic strict trigonometric order on is denoted by .

In other words iff there exists , such that and for all , with . The following lemma, and Corollary 3.5, discuss the combination of the cyclic ordering with the notions of parents (and children) of an irreducible vector.

Definition 3.2 (Collection of ancestors of a vector).

For any irreducible , let be the smallest set containing and the parents of any element such that .

Lemma 3.3.

Let , let be a direct basis of such that , and let us consider the triangle . Then (i) . If in addition is irreducible, and (ii.a) or (ii.b) , then the parents of also belong to .

Proof.

Point (i). By construction, we have for some positive integers . One easily checks that . This expression of as a weighted barycenter of the points establishes (i).

Points (ii.a) and (ii.b). We fix and show these points by decreasing induction on the integer . Initialization: Assume that . Then , which is a contradiction. No basis satisfies simultaneously and . The statement is vacuous, hence true.

Case . If , then are the parents of , and the result follows. Otherwise, we have either or . Since and , we may apply our induction hypothesis to the bases and which satisfy (ii.a). Thus the parents of belong to or . Finally, Point (i) implies that , thus which concludes the proof of this case.

Case . Assumption (ii.b) must hold, since (ii.a) contradicts this case. By corollary 2.4, is a parent of or of . Hence and . We apply our induction hypothesis to the bases and which satisfy (ii.b), and conclude the proof similarly to the case . ∎

Lemma 3.4.

Consider an irreducible , , and let be its parents. The children of (i.e. the vectors of which is a parent) have the form and , .

Proof.

Let be a children of , and let , be its parents. Without loss of generality, we assume that . Then , thus for some . Since is irreducible, one has . Since , one has . The result follows. ∎

Corollary 3.5.

Let , let be a direct acute basis of such that . Then any child of (i.e. is a parent of ) satisfies .

Proof.

Lemma 3.6 (Consecutive elements of a stencil).

Let be a family of stencils on , let , and let be two trigonometrically consecutive elements of . Then either (i) form a direct acute basis, or (ii) no element satisfies .

Proof.

We distinguish three cases, depending on the value of . In case , property Visibility of stencils implies (ii).

Case . Assuming that (i) does not hold, Corollary 2.4 implies that is a parent of or of . Assuming that (ii) does not hold, we have for some by Lemma 3.3 (i), thus by convexity of , thus by (Stability), which contradicts our assumption are trigonometrically consecutive in .

Case . We assume without loss of generality that , hence . Let be the parents of , so that for some . We obtain . If or , then is not irreducible, which is a contradiction. If and have the same sign, then , which again is a contradiction. Hence have opposite signs, and since we obtain . Finally we have , thus , and therefore . By convexity , by (Stability) , which contradicts our assumption that are trigonometrically consecutive in . This concludes the proof. ∎

Proposition 3.7 (Characterization of the smallest stencils).

For all , define as the collection of all which have none or just one parent in (this includes all unit vectors in ). Then is a family of stencils, which is contained in any other family of stencils.

Proof.

Property (Stability) of stencils. Consider and . Assume for contradiction that has one parent which is not an element of . Hence has two parents . By Corollary 3.5 we have , thus by Lemma 3.3 (ii.a) the two parents of belong to the triangle , hence also to by convexity of . This contradicts our assumption that .

Property (Visibility). We consider , and prove by induction on the norm that . If or if none of just one parent of belongs to , then . If both parents of belong to , then by induction , and by additivity , which concludes the proof.

Minimality for inclusion of . Let be a family of stencils, let , , and let us assume for contradiction that . By property (Visibility) of stencils, the vector belongs to the cone generated by two elements , which can be chosen trigonometrically consecutive in . By lemma 3.6, is a direct acute basis of . By Lemma 3.3 (ii.a) the parents of belong to the triangle , hence to by convexity of , which contradicts the definition of . ∎

Proposition 3.8 (Structure of candidates for refinement).

Let be a family of stencils on , and let . Then the parents , of any candidate for refinement , are consecutive elements of in trigonometric order.

3.2 Combining and intersecting constraints

The following characterization of the cones implies the announced hierarchy properties.

Proposition 3.9.

For any family of stencils on one has

| (17) |

Before turning to the proof of this proposition, we use it to conclude the proof of Theorem 1.8. The sub-cone , of , is characterized by the non-negativity of a family of linear forms indexed by , with the convention (7). Observing that

we find that is characterized, as a subset of , by the intersection of the families of constraints defining and , while is defined by their union. Hence we conclude as announced

Proof of Proposition 3.9.

We proceed by decreasing induction on the cardinality .

Initialization. If , then , and therefore and . The result follows.

Induction. Assume that , thus . Let and be such that is minimal. Since , the two parents of belong to . Since , and by minimality of the norm of , we have . Hence is a candidate for refinement: .

Consider the extended stencils defined by , and for all . Let and be the collections of linear forms enumerated in Definition 1.7, which non-negativity respectively defines the cones and as subsets of . Let also . Since we have . Using Proposition 3.8 we obtain , hence is the union of and of those of the following constraints which are supported on :

| (18) |

We next show that , by expressing the linear forms (18) in terms of the elements of .

-

•

If is supported on , then . Assuming that , we obtain . On the other hand, assuming that , we obtain by Proposition 3.7, since otherwise . Therefore are supported on , hence they belong to . By minimality of the norm of , we have , hence and therefore . As a result .

-

•

If is supported on , then . Therefore are supported on , hence they belong to . As a result .

-

•

If is supported on , then , thus and therefore by minimality of . The linear form belongs to , since it has support . Observing that the parents of are and , we find that . The case of is similar.

Denoting by the dual cone of a cone , we obtain

Applying the induction hypothesis to , we conclude the proof. ∎

4 Stencils and triangulations

Using the interplay between stencils and triangulations , we prove Proposition 1.10 and Theorems 1.13, 1.15. By convention, all stencils are on , and all triangulations have as vertices and cover .

4.1 Minimal stencils containing a triangulation

We characterize in Proposition 4.4 the minimal stencils containing a triangulation, in the sense of Definition 1.12, and we estimate their cardinality, proving Proposition 1.10. In the way, we establish in Proposition 4.3 “half” (one inclusion) of the decomposition of announced in Theorem 1.13.

Lemma 4.1.

Let be a triangulation, and let . Let . Assume that is an edge of , and that . Then

Proof.

The interpolating function is convex on , and linear on the edge . Introducing the edge midpoint we obtain , as announced. ∎

The inequalities identified in the previous lemma are closely tied with the linear constraints , since is a parallelogram, and as shown in the next lemma. The set of ancestors of an irreducible vector was introduced Definition 3.2.

Lemma 4.2.

Let be irreducible, with , and let be a direct basis such that and . Let be such that . If satisfies , then .

Proof.

Without loss of generality, up to adding a global affine map to , we may assume that . Denoting by the parents of , we have by Lemma 3.3 (ii.b) , hence by convexity . Our hypothesis implies , therefore . ∎

Proposition 4.3.

If a triangulation , and stencils , satisfy , then .

Proof.

The inequalities , and , for , , hold by convexity of . We thus consider an arbitrary refinement candidate , , and establish below that .

Proposition 4.4.

Let be a triangulation, and for all let be the collection of all such that is an edge of . The minimal family of stencils satisfying is given by

Proof.

The family of sets satisfies the (Stability) property by construction. Since the triangulation covers , the sets satisfy the (Visibility) property, hence also the larger sets .

Minimality. Consider arbitrary stencils such that . Let also , , , and let us assume for contradiction that . By property (Visibility) there exists , trigonometrically consecutive elements of , such that (where refers to the cyclic trigonometric order, see Definition 3.1). By Lemma 3.6, is a direct acute basis of . By Corollary 3.5, and an immediate induction argument, we have , hence , which contradicts our assumption that . ∎

Given a triangulation , our next objective is to estimate the cardinality of the minimal stencils such that . We begin by counting the ancestors of an irreducible vector.

Lemma 4.5.

-

1.

Let be an acute basis of . Then either (i) is a parent of , (ii) is a parent of , or (iii) .

-

2.

For any irreducible one has , where .

Proof.

Point 1. If , then applying Corollary 2.4 to the non-acute basis we find that either (i) are the parents of , or (ii) are the parents of . On the other hand if , then , hence (iii) .

Before proving Point 2, we introduce the cone generated by , so that for any . If irreducible belongs to the interior of , then its parents , and we have .

Point 2 is proved by induction on . It is immediate if , hence we may assume that , and denote its parents by . We have , since without loss of generality we may assume that . Applying Point 1 we find that either (i) , (ii) , or (iii) , so that , a case which we have excluded. Thus , which implies the announced result by induction. ∎

Proposition 4.6.

Let be a triangulation, and let be the minimal family of stencils such that . Then , with . A sharper estimate holds for (standard) Delaunay triangulations: ,

Proof.

Let be respectively the number of edges and faces of , where faces refer to both triangles and the infinite exterior face. By Euler’s theorem, . Since each edge is shared by two faces, and each face has at least three edges, one gets , hence , and therefore, with the notation of Proposition 4.4,

| (19) |

Combining lemma 4.5, Proposition 4.4, and observing that any edge of satisfies , we obtain , which in combination with (19) implies the first estimate on .

In the case of a Delaunay triangulation, we claim that . Indeed, consider an edge of , and a parent of . Since covers , it contains a triangle with and on the same side of the edge . Thus the determinants and have the same sign, and therefore the same value since their magnitude is . As a result , for some integer . Since is Delaunay, the point is outside of the circumcircle of . This property is equivalent to the non-positivity of the following determinant, called the in-circle predicate: assuming without loss of generality that so that the vertices are in trigonometric order

| (26) | ||||

| (27) |

where we denoted , . Observing that , we find that (27) is non-positive only for . Thus , hence , and therefore as announced. Finally, the announced estimate of immediately follows from (19). ∎

4.2 Decomposition of the cone , and edge-flipping distances

We conclude in this section the proof of Theorem 1.13, and establish the complexity result Theorem 1.15 on the edge-flipping generation of -Delaunay triangulations.

Definition 4.7.

We say (abusively) that a discrete map is generic iff, for all and all such that the linear form is supported on , one has .

Generic elements are dense in , since this set is convex, has non-empty interior, and since non-generic elements lie on a union of hyperplanes. The quadratic function is not generic however, since choosing one gets .

Lemma 4.8.

Consider stencils , a generic , and an -Delaunay triangulation . Then .

Proof.

We established in Proposition 4.3 that . The next corollary, stating the reverse inclusion, concludes the proof of Theorem 1.13.

Corollary 4.9.

If has a non-empty interior, then .

Proof.

The set contains all generic elements of , by Lemma 4.8. Observing that is closed, and recalling that generic elements are dense in , we obtain the announced inclusion. ∎

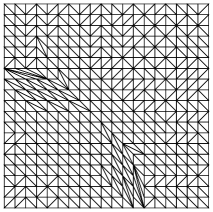

The next lemma characterizes the obstructions to the convexity of the piecewise linear interpolant of a convex function on a triangulation . See also Figure 4 (right).

Lemma 4.10.

Consider , and a triangulation which is not -Delaunay. Then there exists , and a direct basis of , such that the triangles and belong to , and satisfy .

Proof.

Since convexity is a local property, there exists two triangles , sharing an edge, such that the interpolant is not convex on (i.e. convexity fails on the edge by and ). Up to a translation of the domain, we may assume that and , for some . The pair is a basis of because the triangle contains no point of except its vertices; up to exchanging and we may assume that it is a direct basis. Up to adding an affine function to , we may assume that vanishes at the vertices of .

If lies in the triangle , then since , and recalling that , we obtain . This implies that is convex on , which contradicts our assumption. Likewise , thus and therefore and . We next observe that

The four members of this equation are integers, the two left being equal to , and the two right being positive. Hence , and therefore as announced. From this point, the inequality is easily checked to be equivalent to the non-convexity of on . ∎

Proposition 4.11.

Consider stencils , a triangulation , and . Define a sequence of triangulations as follows: if is -Delaunay, then the sequence ends, otherwise is obtained by flipping an arbitrary edge of satisfying Lemma 4.10. Then the sequence is finite, contains at most elements, and for all .

Proof.

Proof that , by induction on . Initialization: by assumption. Induction: adopting the notations of Lemma 4.10, the “flipped” edge of is replaced with in , with . We only need to check that , and for that purpose we distinguish two cases. If the basis is acute, then are the parents of , and we have by Lemma 4.10. This implies by Proposition 3.9. On the other hand, if the basis is not acute, then by Corollary 2.4 the vector is a parent of either or , thus by property (Stability) of stencils.

Bound on the number of edge flips. For all one has on , and this inequality is strict at the common midpoint of the flipped edges and , with the above conventions. Hence the edge appears in the triangulation but not in any of the , for all . It follows that is injective, and since this implies . ∎

We finally prove Theorem 1.15. Consider a Delaunay triangulation , and the minimal stencils such that . Let also , and let be the minimal stencils such that . Then, by Proposition 4.11, can be transformed into an -Delaunay triangulation via edge flips. Furthermore by Proposition 4.6 and , as follows e.g. from property (Visibility) of stencils. Thus , and the result follows.

5 Average case estimate of the cardinality of minimal stencils

The minimal stencils , such that the cone contains a given discrete convex map, admit a simple characterization described in the following proposition.

Proposition 5.1.

Let , and let be the minimal stencils on such that . For any , and any irreducible with , one has:

( is not supported on , or ).

Proof.

The rest of this section is devoted to the proof of Theorem 1.11, and for that purpose we consider the rotated and translated grids , defined in (10). For simplicity, but without loss of generality, we assume a unit grid scale . For each rotation angle , and each offset , we introduce an affine transform : for all

For any set , and any affine transform , we denote . For instance, the displaced grids (10) are given by .

The maximal stencils on the grid are defined by: for all

A family of stencils on is a collection of sets , which satisfies the usual (Stability) and (Visibility) properties of Definition 1.6 (replacing, obviously, instances of with ). For , and we consider the linear forms , and likewise , , which are used to define cones . In a nutshell, when embedding a stencil element , where , into the physical domain (e.g. considering ), one should never forget to apply the rotation .

Consistently with the notations of Theorem 1.11, we consider a fixed convex map , and study the smallest stencils on such that the restriction of to belongs to . The midpoints of “stencil edges” , , , play a central role in our proof.

Definition 5.2.

For any , and any irreducible , let

We introduce offsetted grids, of points with half-integer coordinates

For any with irreducible, the midpoint of the segment belongs to the disjoint union .

Lemma 5.3.

For any and any , one has .

Proof.

Let , and , be such that . Observing that the coordinates of are not both even, since is irreducible, we obtain . Adding to yields as announced a point . ∎

For any point , and any angle , there exists exactly one offset such that ; and likewise for , . Hence the set contains redundant information, which motivates the following definition: for any , and any irreducible

| (28) |

and similarly we define , , by replacing with , respectively in (28). By convention, for non irreducible vectors . The following lemma accounts in analytical terms for a simple combinatorial identity: one can count stencil edges by looking at their endpoints or their midpoints.

Lemma 5.4.

The following integrals are equal:

| (29) |

where denotes the Lebesgue measure of a Borel set .

Proof.

Consider , , and . Then there exists a unique such that . This uniquely determines the point such that . Likewise for , . Conversely, the data of , , and uniquely determines , and also by Lemma 5.3 a unique set among , , containing . As a result the left and right hand side of (29) are just two different expressions of the measure of

where , , and . Implicitly, we equipped and with the counting measure, and and with the Lebesgue measure (which in the latter case is preserved by the rotations ). ∎

In order to estimate (29), we bound in the next lemma the size of the sets , , .

Lemma 5.5.

Let be irreducible, with , of parents . Let also . Then for any , one has . Likewise for , .

Proof.

Without loss of generality, we may assume that is the origin of . Let be the parallelogram of vertices ; note that . A point belongs to iff

| (30) |

Indeed , since by construction. We assume without loss of generality that . Introducing we observe that , and compute

In the second line, we used the identity , where denotes the angle between and , and . Combining these two estimates with (30), and assuming for contradiction that , we obtain that . By symmetry, , and likewise .

In the following, we denote , , , , where the signs for and are chosen so that . Denoting by (resp. ) the barycentric coordinates of (resp. ) in this triangle, convexity implies

| (31) | ||||

| (32) |

Let be such that . Then , , and (recall that we fixed ). Using the characterization of minimal stencils of Proposition 5.1, we obtain

| (33) |

provided this linear form is supported on . Note that , that , and that for some . Since this confirms that (33) is supported on . Inserting in (33) the values of , and proceeding likewise for and , we obtain

| (34) | ||||

| (35) |

Up to adding an affine map to , we may assume that , and . From (34) we obtain . Hence also using (31), and therefore using (32). Likewise , which contradicts (35) and concludes the proof. ∎

Lemma 5.6.

For any , with : (likewise for , )

| (36) |

Proof.

Note that for any , and that if the is not irreducible, or if . For any two vectors , we write iff is a parent of (which implies that are irreducible, and that ). Isolating the contributions to (36) of the four unit vectors, and applying Lemma 5.5 to other vectors, we thus obtain

| (37) |

where we used the concavity bound for all (and slightly abused notations for arguments of larger than ).

Consider a fixed irreducible , and denote by its parents if , or the two orthogonal unit vectors if , so that . If is such that , then ; assuming (resp. ) we obtain that (resp. ) for some scalar which must be (i) an integer since is irreducible, (ii) non-negative since , and (iii) positive since . Assuming , we obtain in addition , thus and . As a result

| (38) |

Inserting (38) into (37) yields the product of the two following sums, which are easily bounded via comparisons with integrals: isolating the terms for , and for all

Noticing that we obtain (36) as announced. ∎

6 Numerical experiments

Our numerical experiments cover the classical formulation [24] of the monopolist problem, as well as several variants, including lotteries [17, 25], or the pricing of risky assets [4]. We choose to emphasize this application in view of its appealing economical interpretation, and the often surprising qualitative behavior. Our algorithm can also be applied in a straightforward manner to the computation of projections onto the cone of convex functions defined on some square domain, with respect to various norms as considered in [5, 18, 22, 21] (this amounts to denoising under a convexity prior). It may however not be perfectly adequate for the investigation of geometric conjectures [16, 26, 18], due to the use of a grid discretization.

The hierarchical cones of discrete convex functions introduced in this paper are combined with a simple yet adaptive and anisotropic stencil refinement strategy, described in §6.1. The monopolist model is introduced in §6.2, and illustrated with numerous experiments. We compare in §6.3 our implementation of the constraint of convexity, with alternative methods proposed in the literature, in terms of computation time, memory usage, and solution quality.

6.1 Stencil refinement strategy

We introduce two algorithms which purpose is to minimize a given lower semi-continuous proper convex functional , on the -dimensional cone , , without ever listing the linear constraints which characterize this cone. They both generate an increasing sequence of stencils on , and minimizers of on cones defined by linear constraints. The subscript refers to the loop iteration count in Algorithms 1 and 2, and the loop ends when the stencils are detected to stabilize: . The final map is guaranteed to be the global minimum of on .

Our first algorithm is based on an increasing sequence of sub-cones of . If constraints of type , , are active for the minimizer of on (i.e. the corresponding Lagrange multipliers are positive), then refined stencils are adaptively generated from ; otherwise is the global minimizer of on , and the method ends. Note that the optimization of on can be hot-started from the previous minimizer .

Start with the minimal stencils: . (See Proposition 3.7)

Until the stencils stabilize

Find a minimizer of the energy on ,

and extract the Lagrange multipliers associated to the constraints , , .

Set , for all .

Definition 6.1.

For any family of stencils on , we denote by the cone defined by the non-negativity of: for all , and all , the linear forms and if , provided they are supported on . Note that .

Algorithm 2 is based on a decreasing sequence of super-cones of . The minimizer of on may not belong to , even less to , and in particular some of the values , , , may be negative. In that case, refined stencils are adaptively generated from ; otherwise, is the global minimizer of on , and the method ends.

Start with the minimal stencils .

Until the stencils stabilize

Find a minimizer of the energy on .

Set , for all .

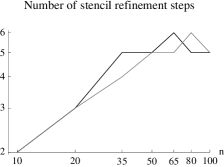

Algorithms 1 and 2 are provided “as is”, without any complexity guarantee. Our numerical experiments are based on algorithm 2, because the numerical test “” turned out to be more robust than “”. In order to limit the number of stencil refinement steps, we use a slightly extended set of candidates for refinement, with , see Definition 6.2 below (note that ). With this modification, remained below 10 in all our experiments. The constructed stencils were generally sparse, highly anisotropic, and almost minimal for the discrete problem solution eventually found, see Figure 5. Observation of Figure 9 suggests that grows logarithmically with the problem dimension , and that the final stencils cardinality depends quasi-linearly on , as could be expected in view of Remark 1.9 and Theorem 1.11. However, we could not mathematically establish such complexity estimates.

Definition 6.2 (Extended candidates).

Let be a family of stencils, let , and let . A vector , of parents , belongs to the extended candidates iff there exists trigonometrically consecutive such that and .

6.2 The monopolist problem

A monopolist has the ability to produce goods, which have two characteristics and may thus be represented by a point . The manufacturing cost is known and fixed a-priori. Infinite costs account for products which are “meaningless”, or impossible to build. The selling price is fixed unilaterally by the monopolist except for the “null” product , which must be available for free (). The characteristics of the consumers are also represented by a point , and the utility of product to consumer is modeled by the scalar product between their characteristics

| (39) |

More general utility pairings are considered in [12], yet the numerical implementation of the resulting optimization problems remains out of reach, see [18] for a discussion. All consumers are rational, “screen” the proposed price catalog , and choose the product of maximal net utility (i.e. raw utility minus price). Introducing the Legendre-Fenchel dual of the prices : for all

we observe that the optimal product444Strictly speaking, the optimal product is an element of the subgradient , which (Lebesgue-)almost surely is a singleton . Hence we may write (41) in terms of , provided the density of customers is absolutely continuous with respect to the Lebesgue measure. for consumer is , which is sold at the price

| (40) |

The net utility function is convex and non-negative by construction, and uniquely determines the products bought and their prices. Conversely, any convex non-negative defines prices satisfying the admissibility condition , and such that . The distribution of the characteristics of the potential customers is known to the monopolist, under the form of a bounded measure on . He aims to maximize his total profit: the integrated difference (sales margin) between the selling price (40), and the production cost

| (41) |

If production costs are convex, then this amounts to maximizing a concave functional of under convex constraints; see [3] for precise existence results. If maximizes (41), then an optimal catalog of prices is given by . Quantities of particular economic interest are the monopolist margin, and the distribution of product sales:

| (42) |

where denotes the push forward operator on measures. The regions defined by and are also important, as they correspond to different categories of customers, see below. We present numerical results for three instances of the monopolist problem, associated to different product costs. These three models are clearly simplistic idealizations of real economy. Their interest lies in their, striking, qualitative properties, which are stable and are expected to transfer to more complex models.

For implementation purposes, we observe that the maximum profit (41) is unchanged if one considers only defined on a convex set , and imposes the additional constraint for all . The chosen discrete domain is a square grid , such that . This density is represented by non-negative weights , set to zero outside . The integral appearing in (41) is discretized using finite differences, see [5] for convergence results. The resulting convex program is solved by combining Mosek software’s interior point (for linear problems) or conic (for quadratic555Following the indications of Mosek’s user manual, quadratic functionals are implemented under the form of linear functionals involving auxiliary variables subject to conic constraints. problems) optimizer, with the stencil refinement strategy of Algorithm 2, §6.1.

Classical model.

The produced goods are cars (for concreteness), which characteristics are non-negative and account for the engine horsepower and the upholstery quality . Production cost is quadratic: for all , and otherwise (cars with negative characteristics are unfeasible). Consumer characteristics are their appetite for car performance, and for comfort, consistently with (39). The qualitative properties of this model are the following [24]: denoting by a solution of (41), and ignoring regularity issues in this heuristic discussion

-

•

(Desirability of exclusion) The optimal monopolist strategy often involves neglecting a positive proportion of potential customers - which “buy” the null product at price . In other words, the solution of (41) satisfies on an open subset of , hence also . The economical interpretation is that introducing (low end) products attractive to this population would reduce overall profit, because other customers currently buying expensive, high margin products, would change their minds and buy these instead.

-

•

(Bunching) “Wealthy” customers generally buy products which are specifically designed for them, in the sense that is a local diffeomorphism close to . “Poor” potential customers are excluded from the trade: close to , see the previous point. There also exists an intermediate category of customers characterized by close to , so that the same product is bought by a one dimensional “bunch” of customers . The image of this category of customers, by , is one dimensional product line. From an economic point of view, the optimal strategy limits the variety of intermediate range products in order, again, to avoid competing with high margin sales.

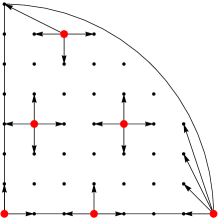

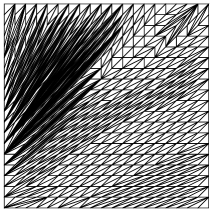

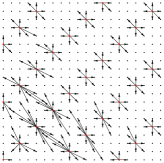

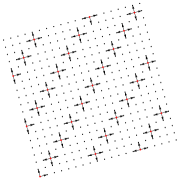

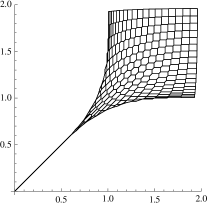

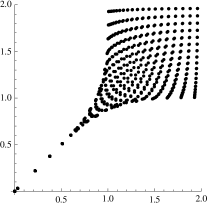

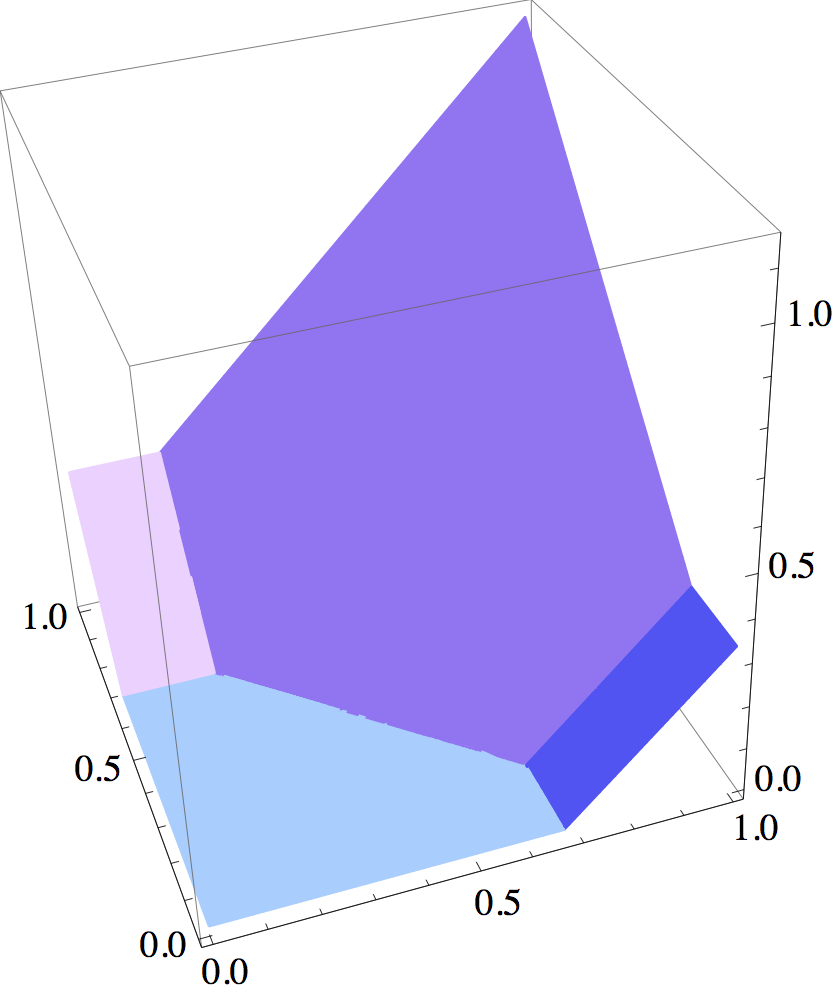

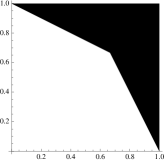

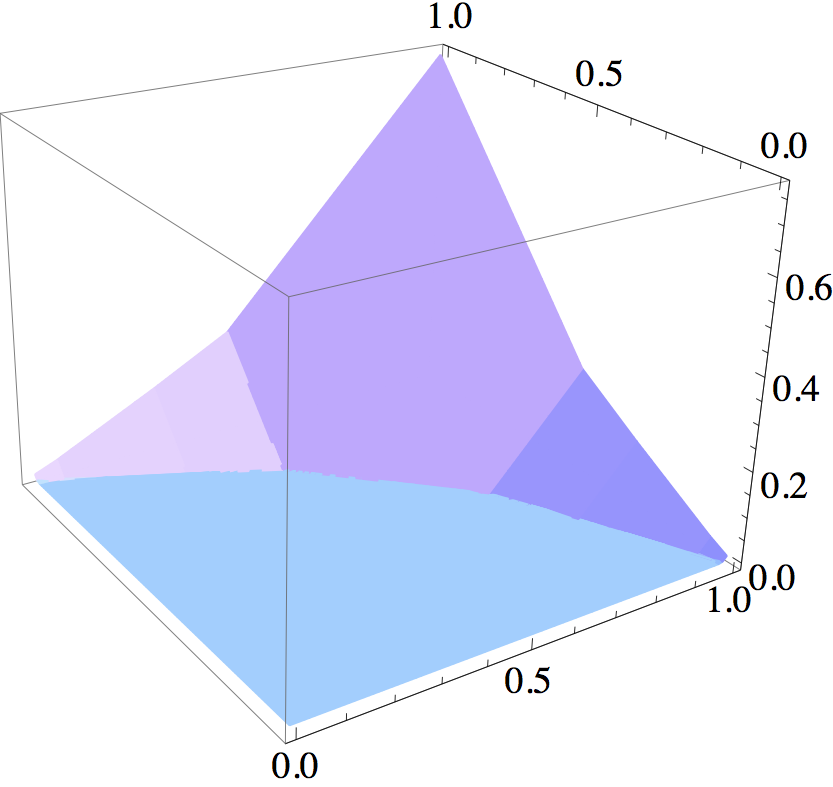

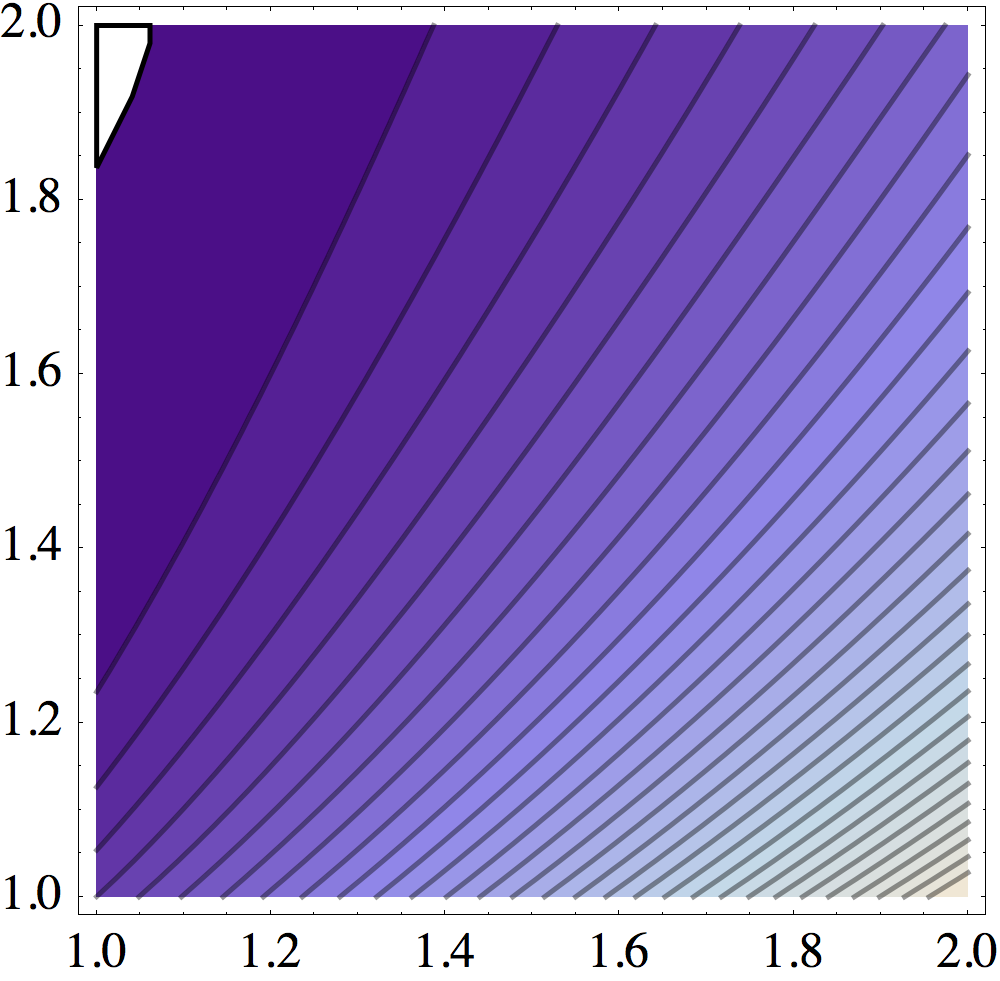

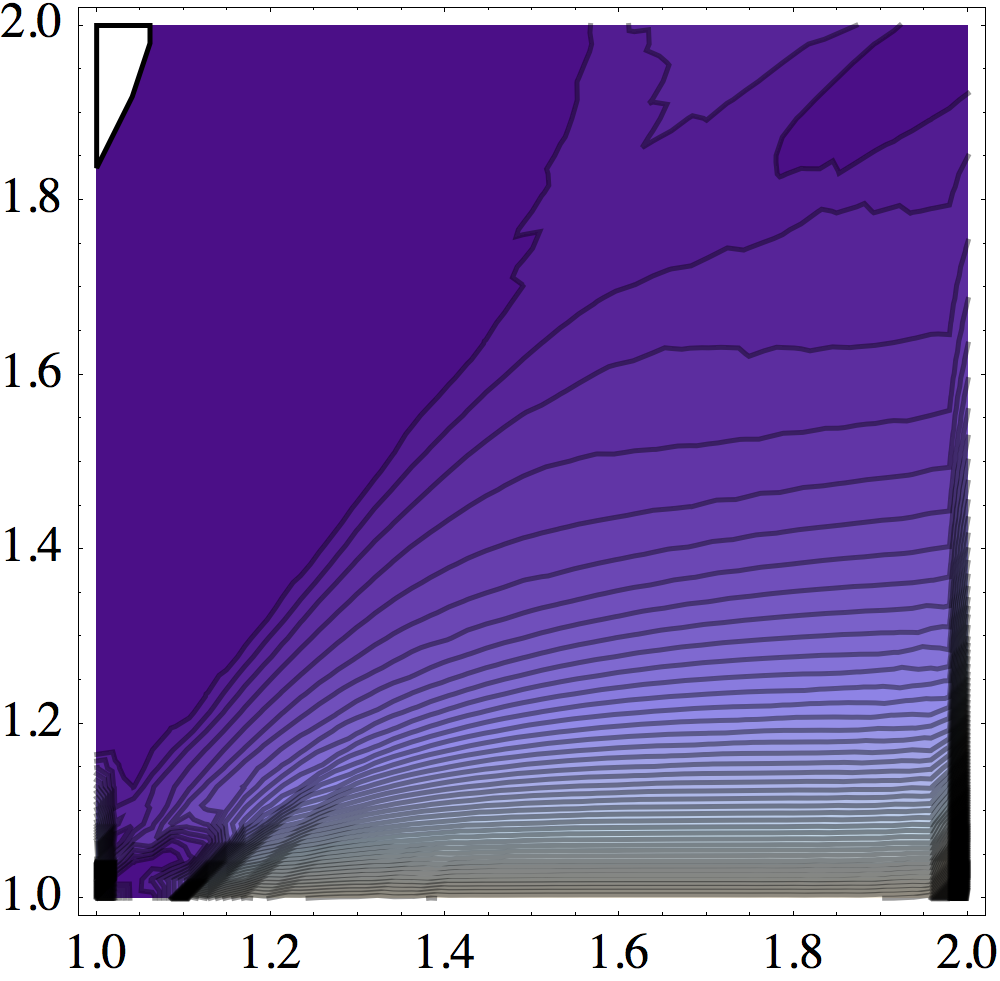

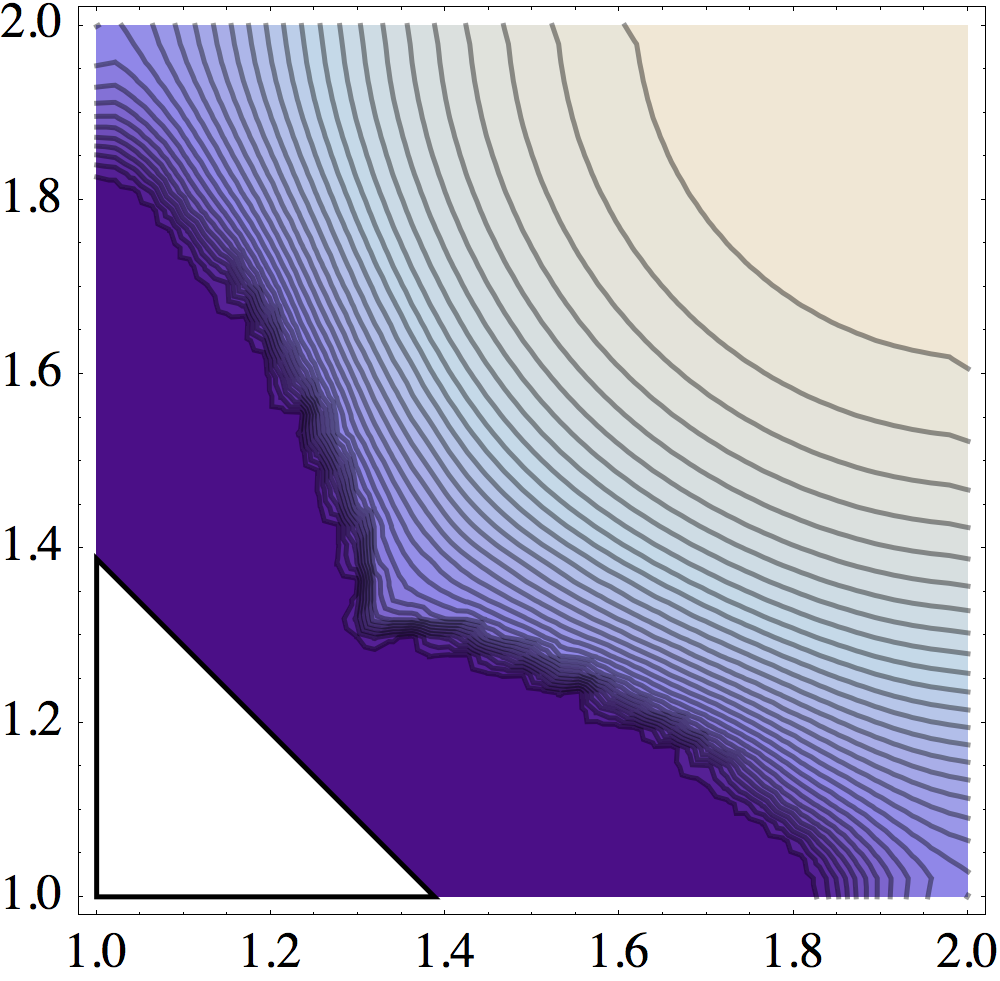

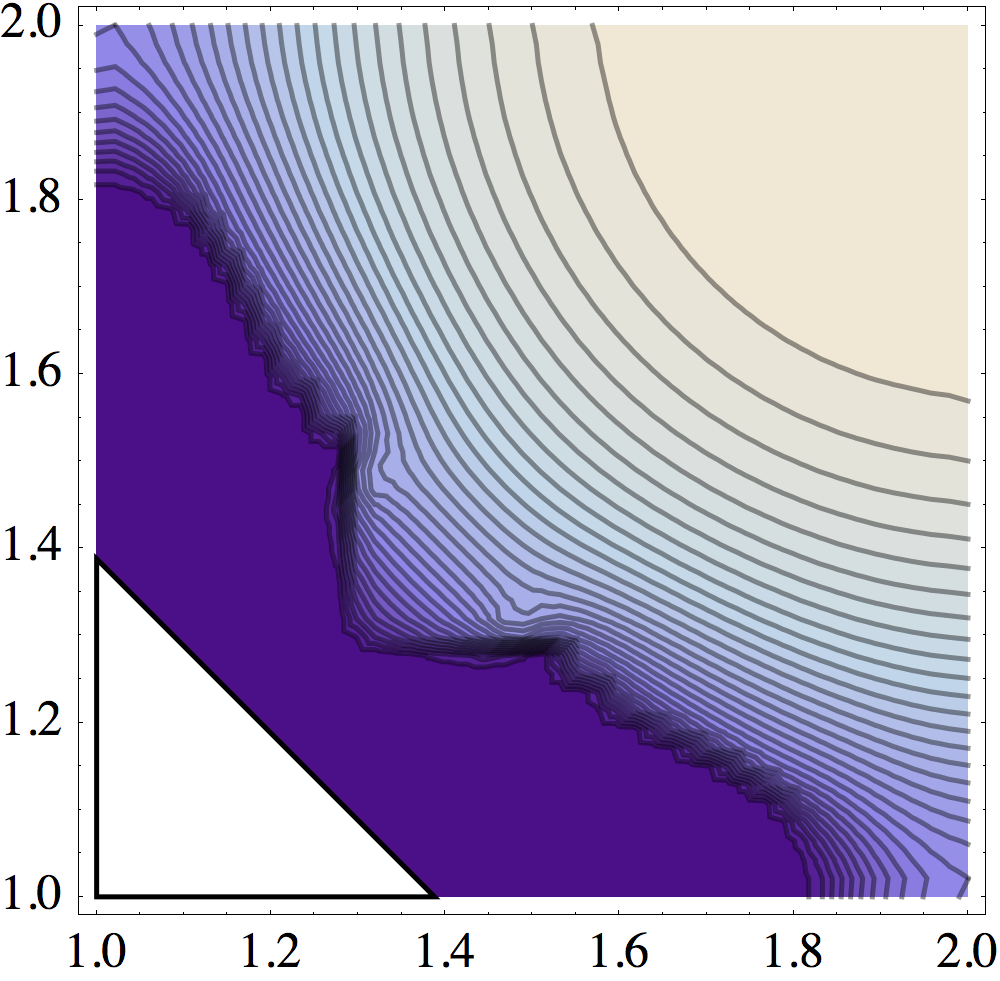

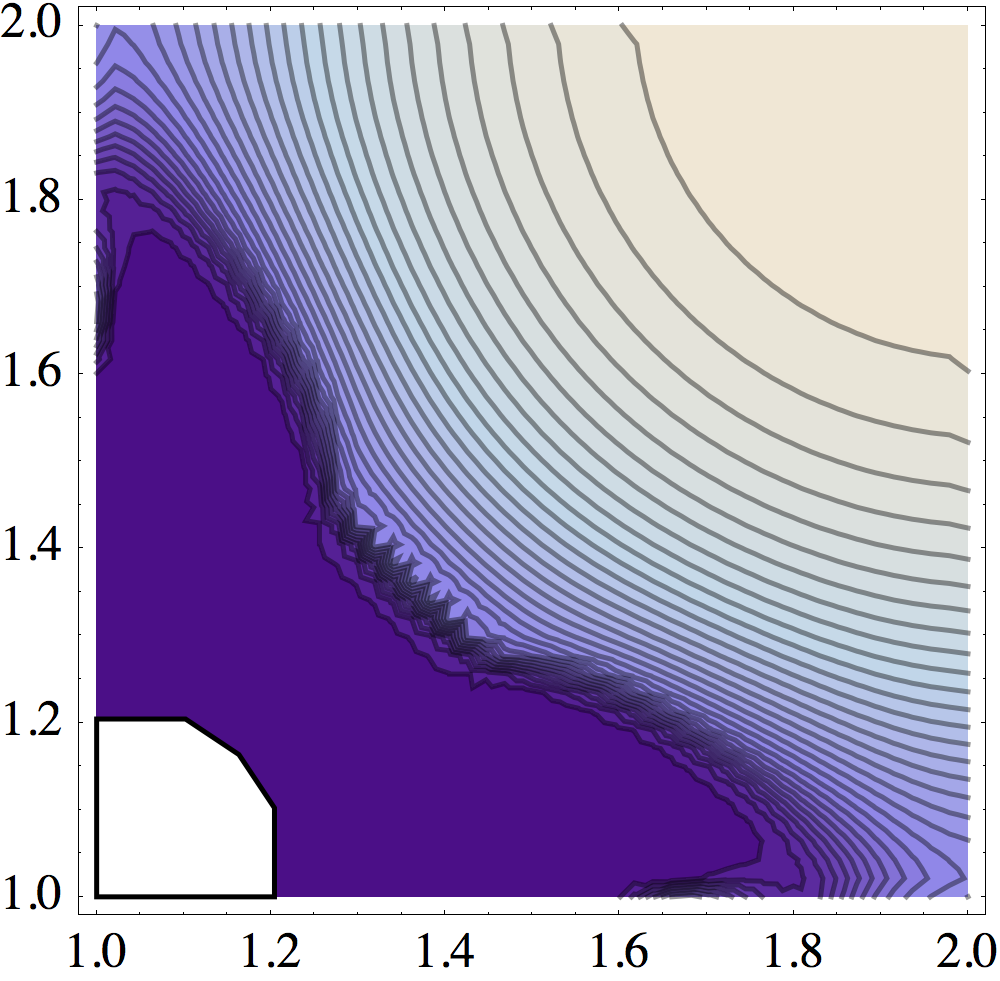

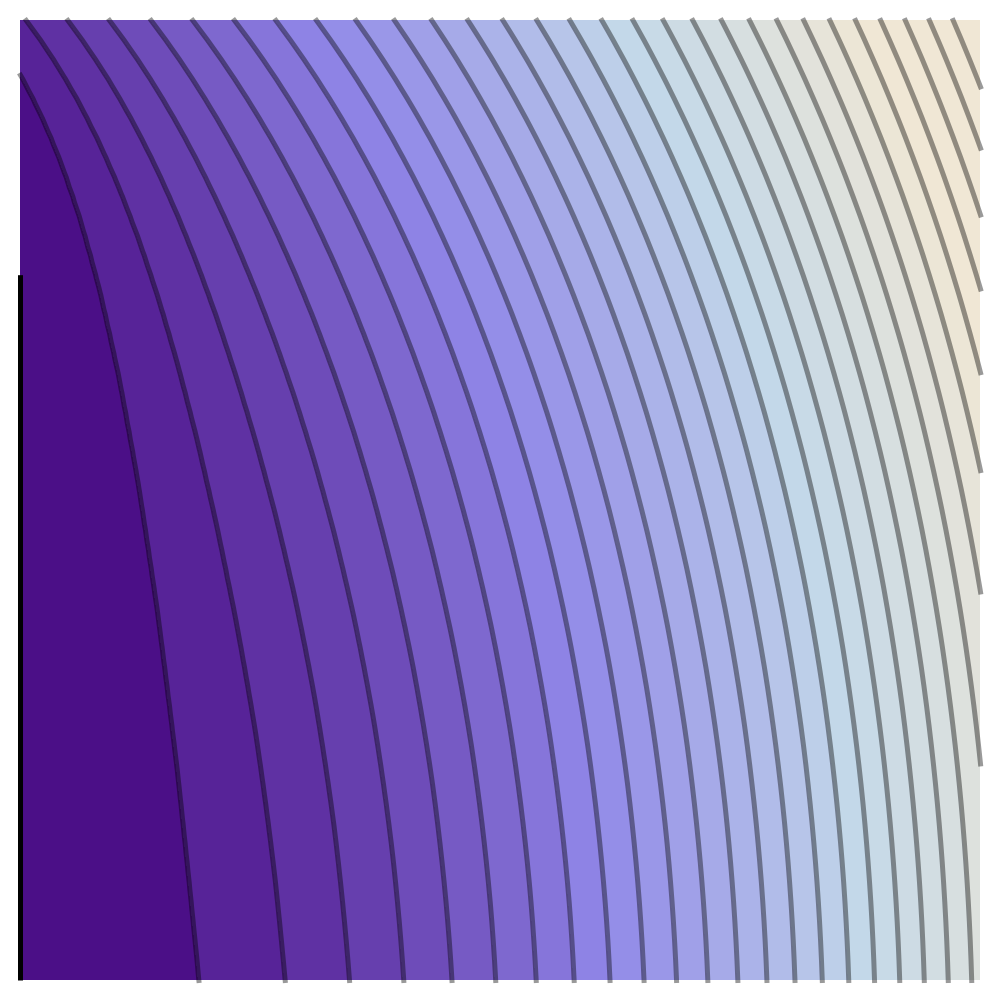

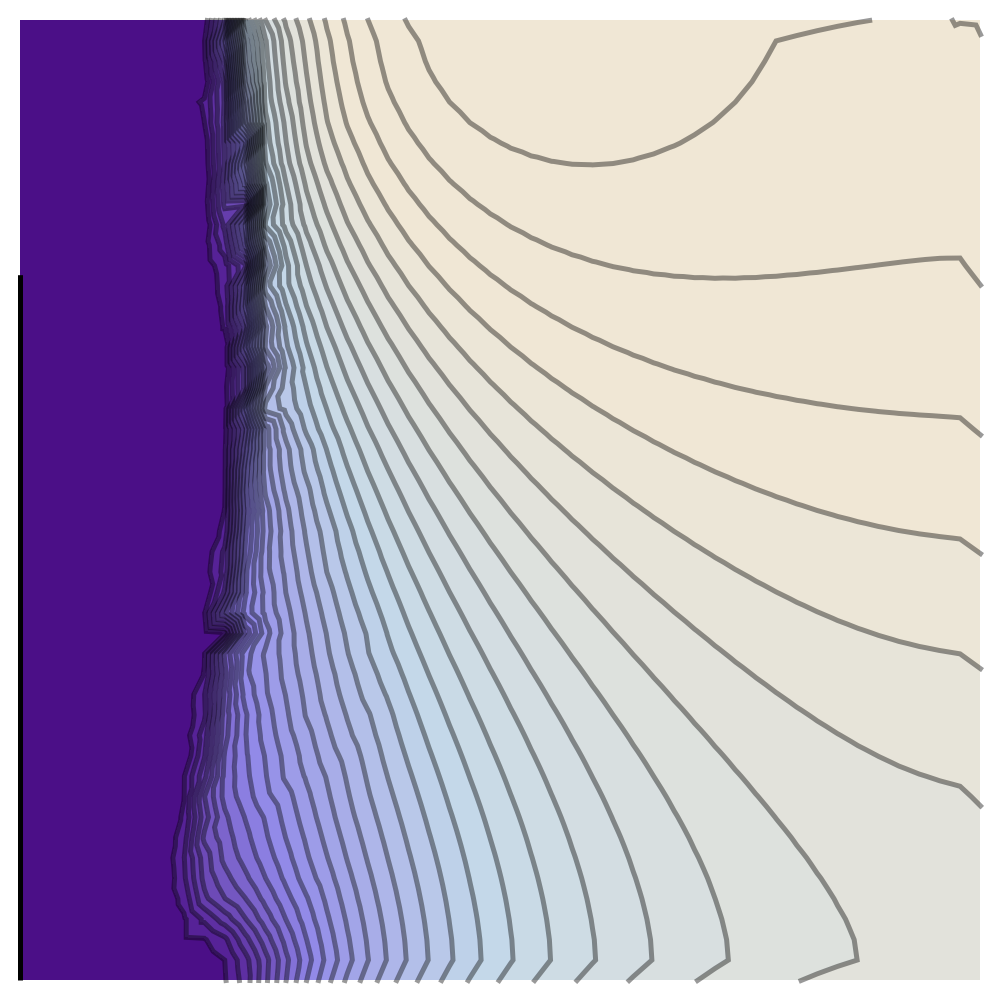

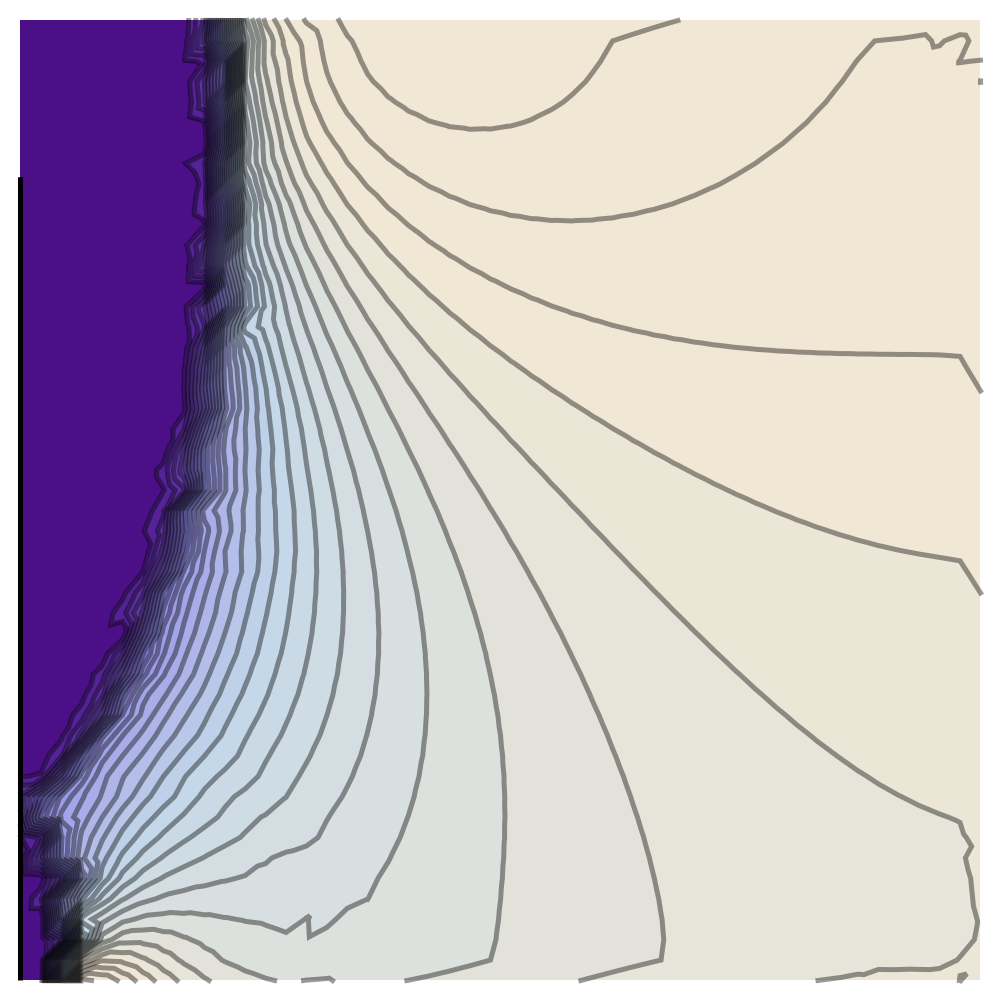

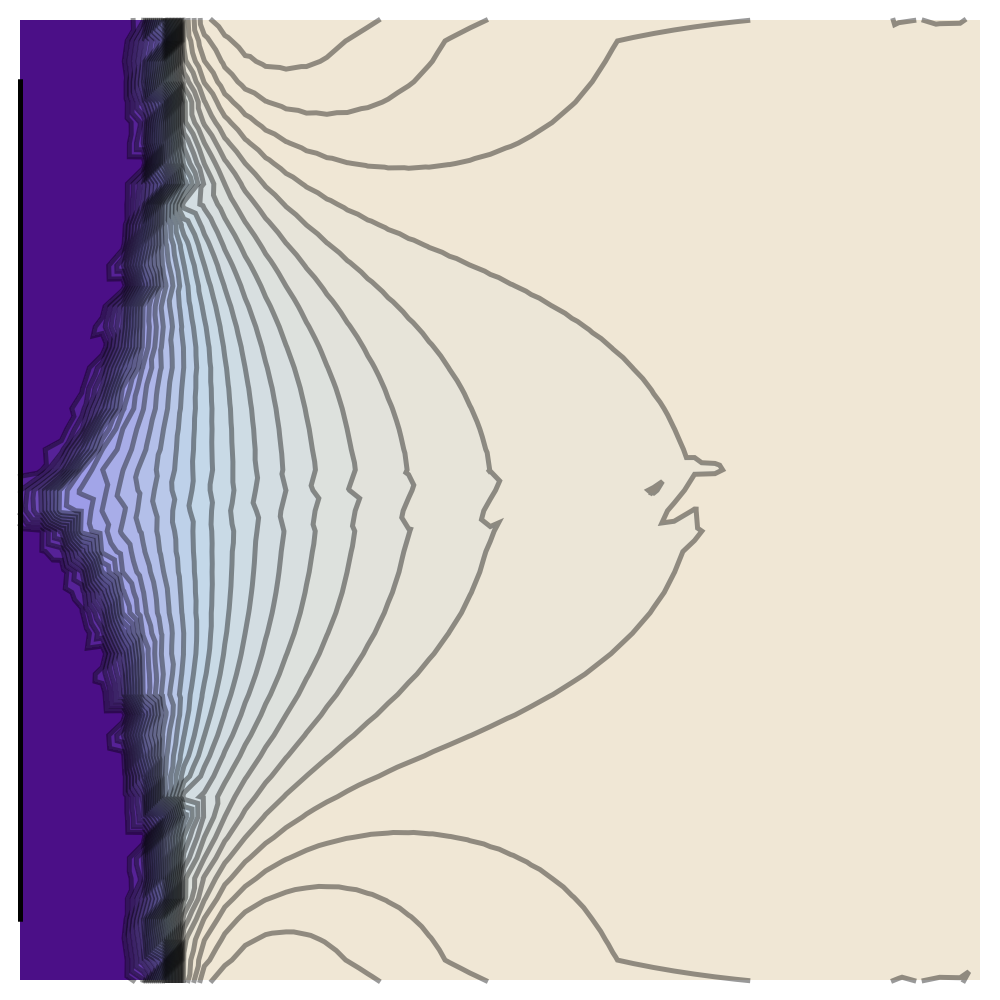

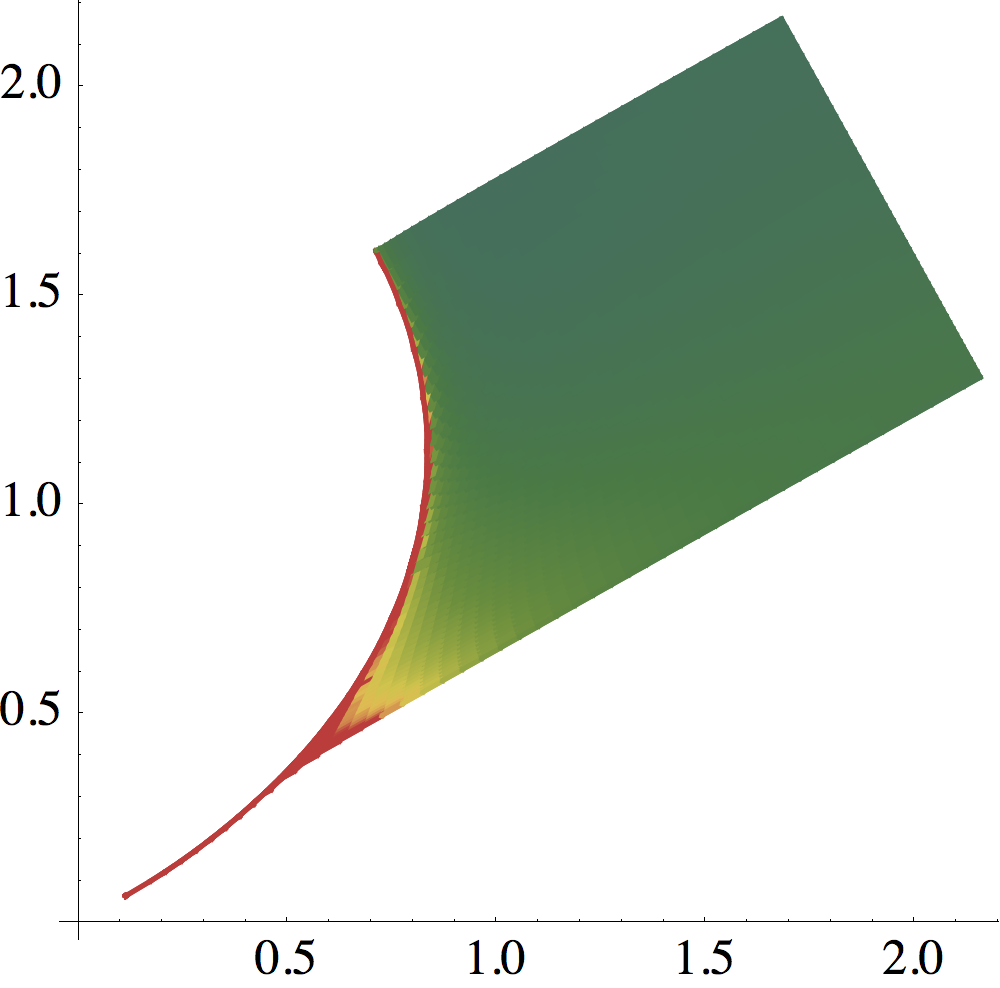

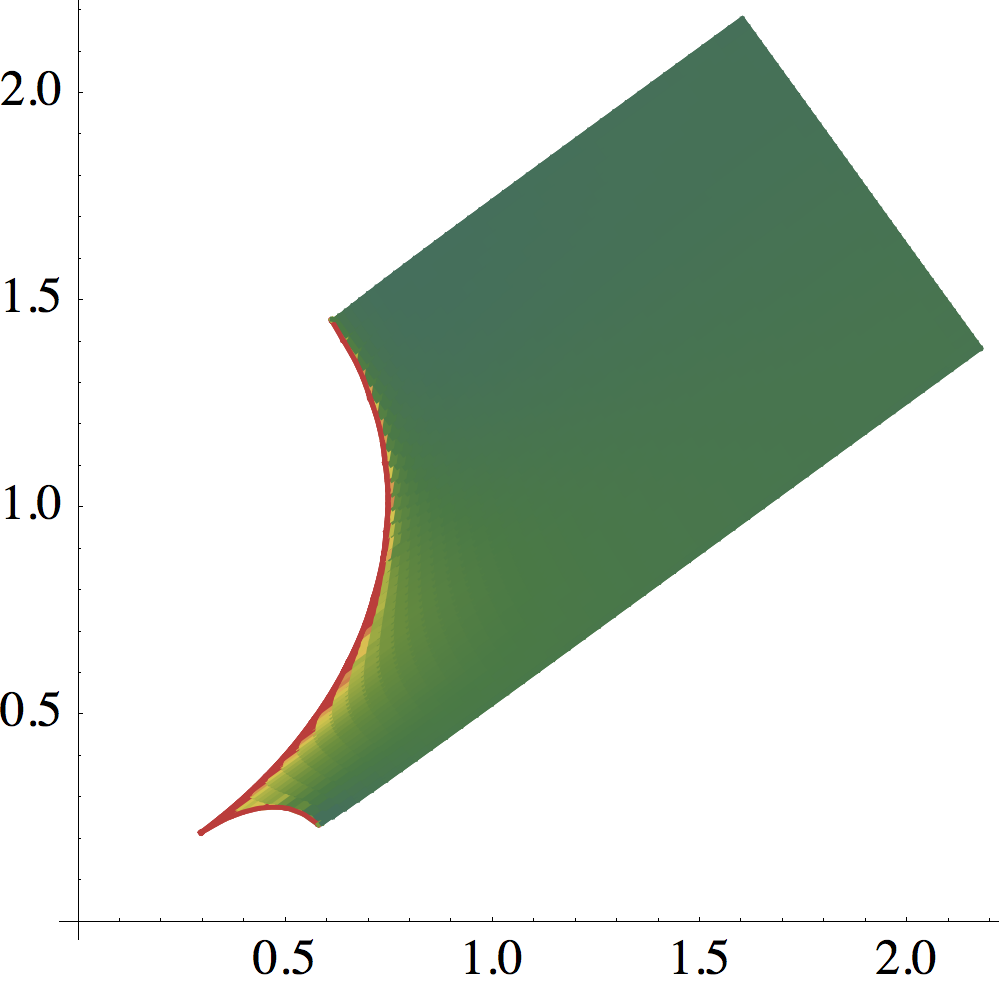

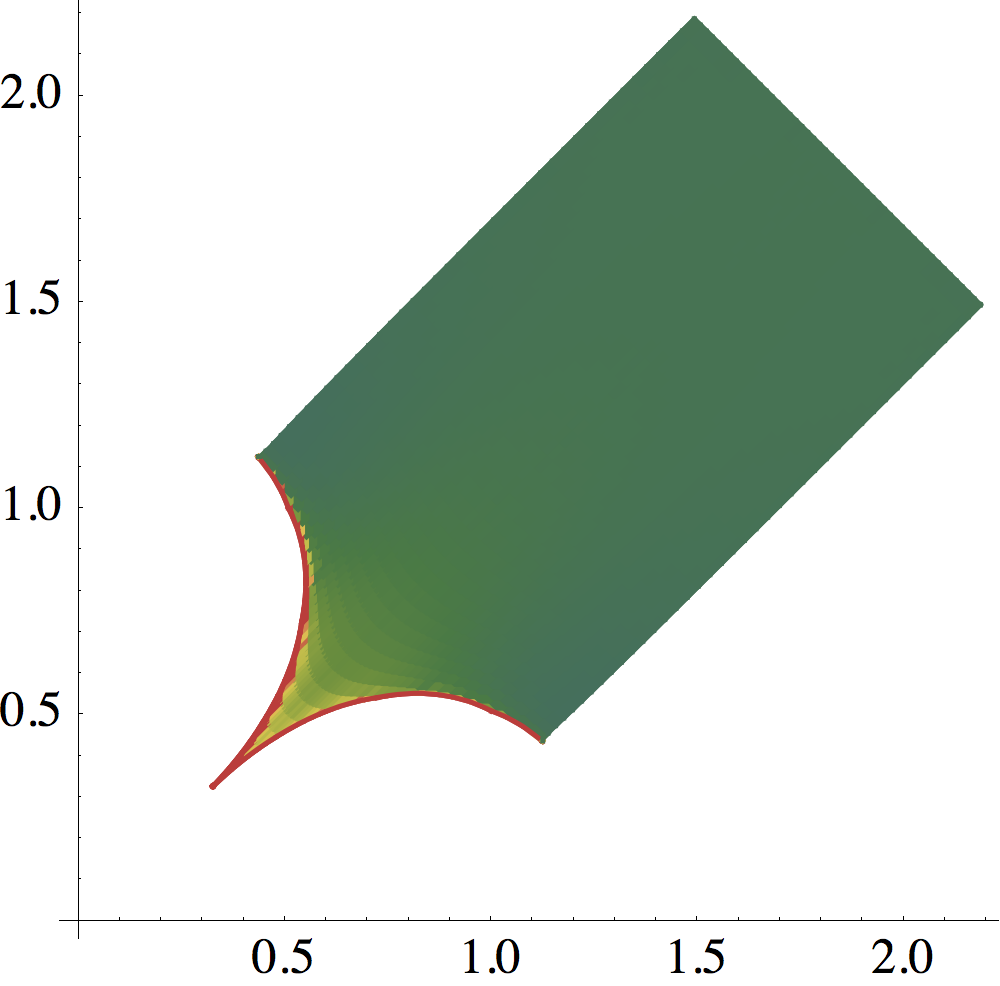

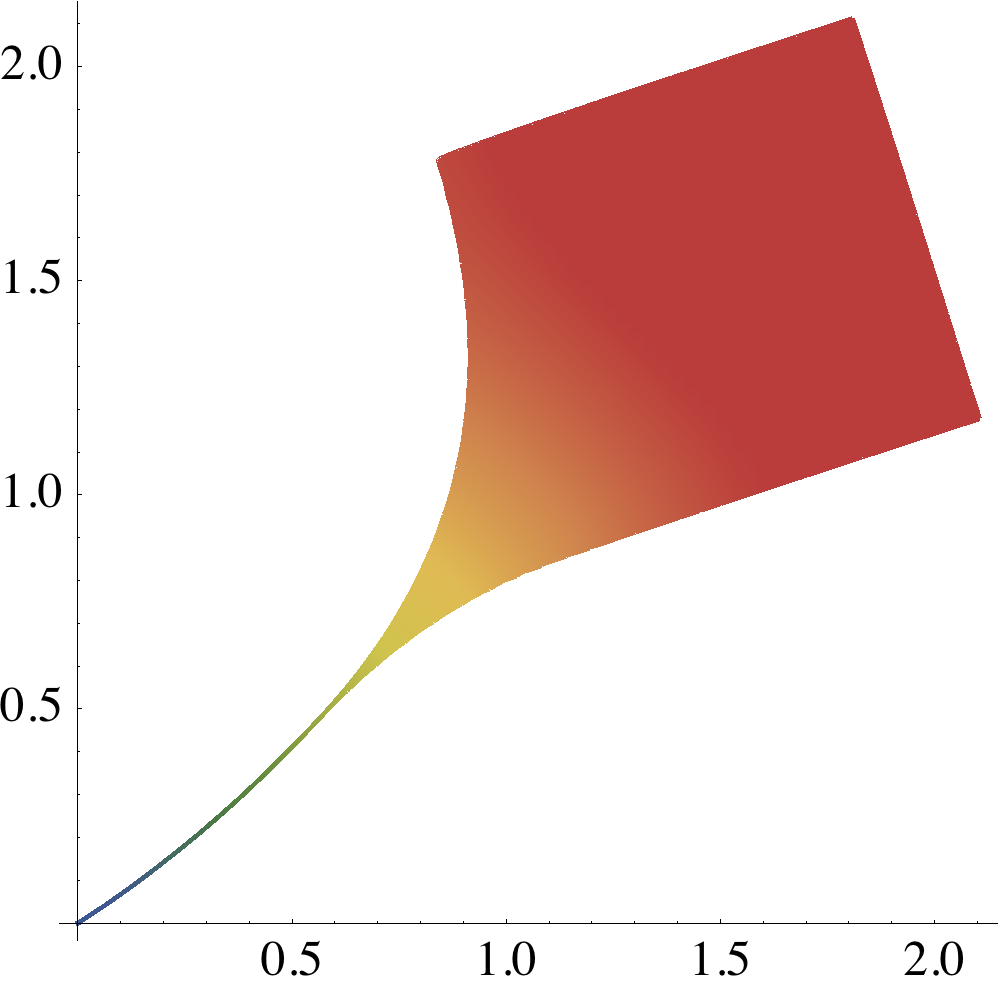

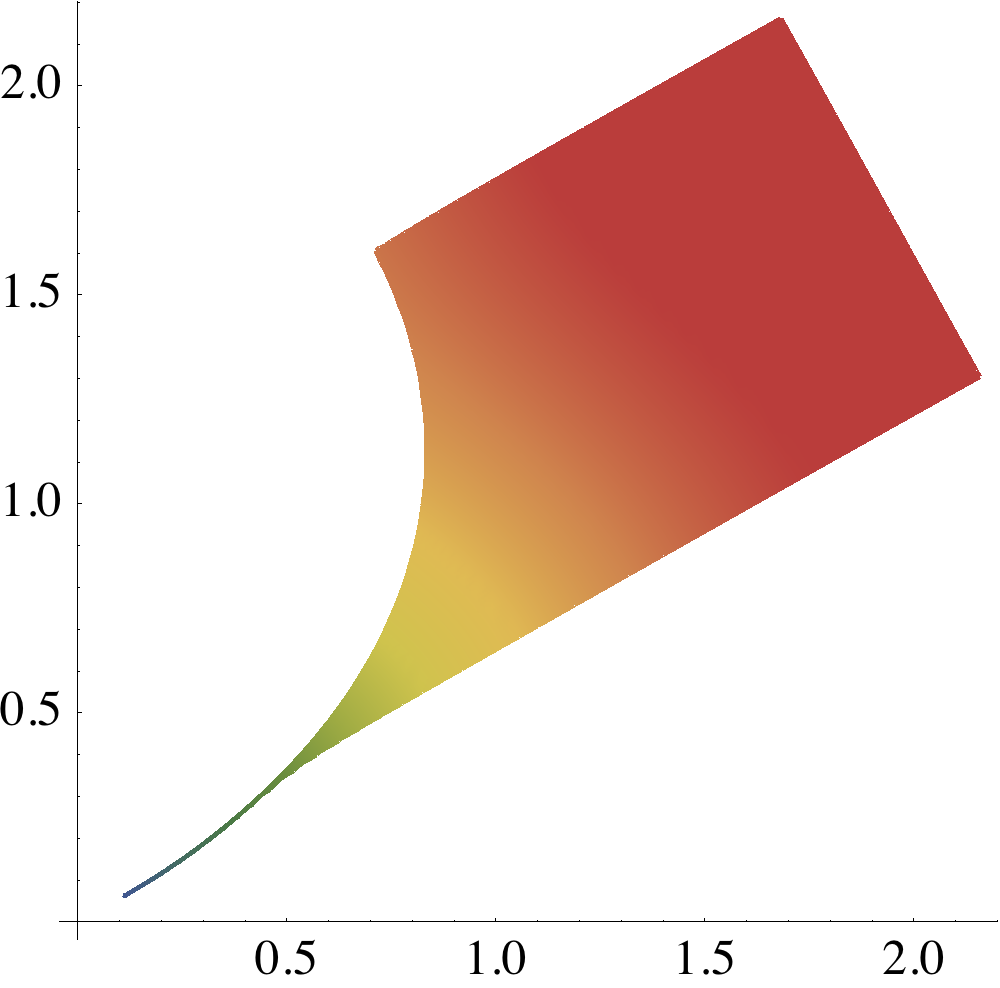

Considering, as in [24, 18], a uniform density of customers on the square , we illustrate666With this customer density, [24] expected the bunching region to be triangular, and the image to be the union of the segment and of the square . After discussion with the author, and in view of the numerical experiments, we believe that these predictions are erroneous. on Figure 1 the estimated solution (left), (center left), the sales distribution (center right) and the monopolist margin (right), see (42). The phenomena of exclusion and of bunching are visible (center left subfigure) as a white triangle and as the darkest level set of respectively. The image by of customers subject to bunching appears (center right subfigure) as a one dimensional red structure in the product sales distribution.

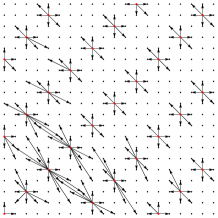

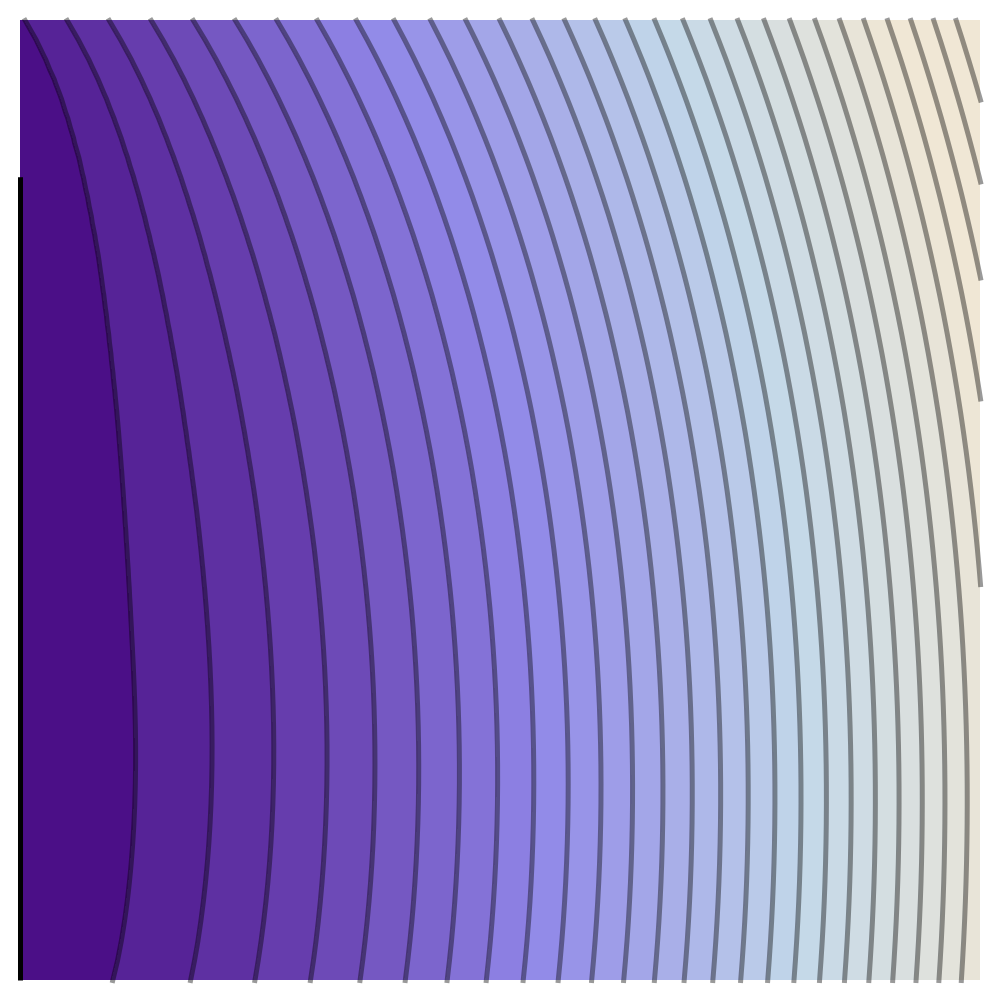

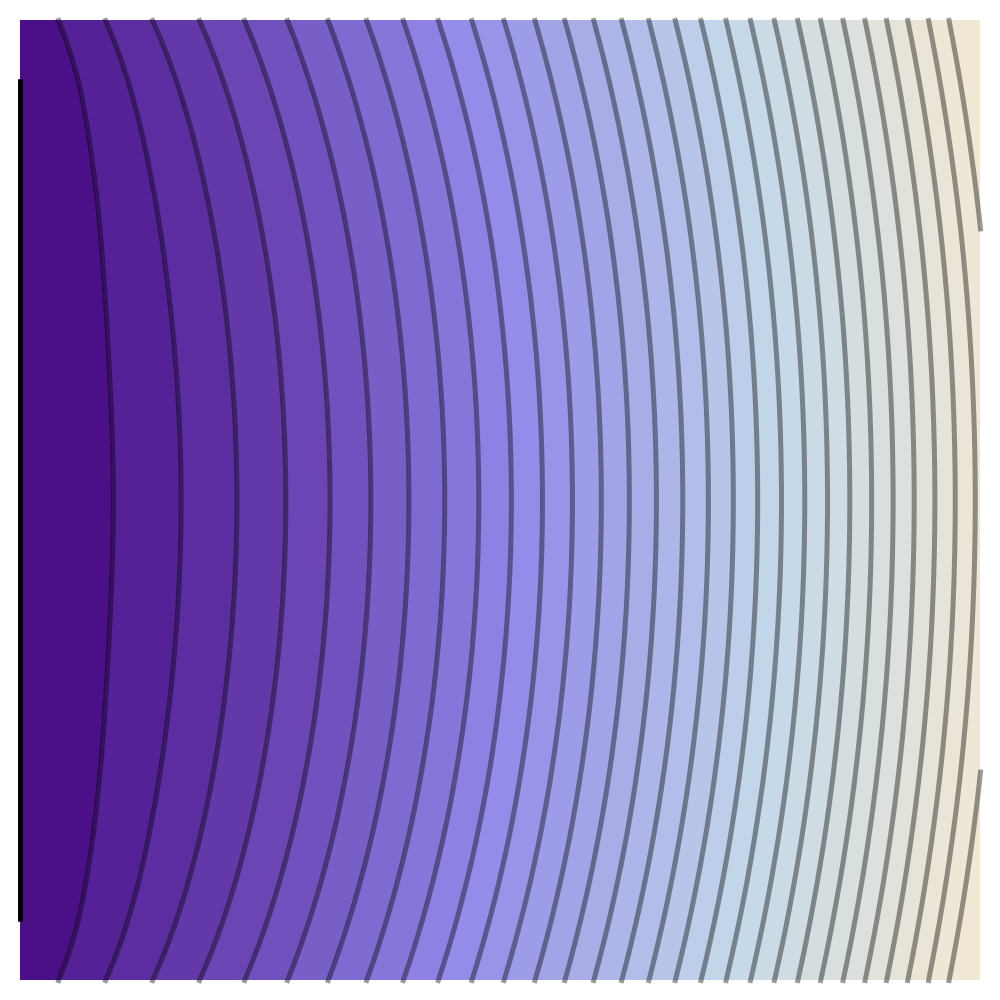

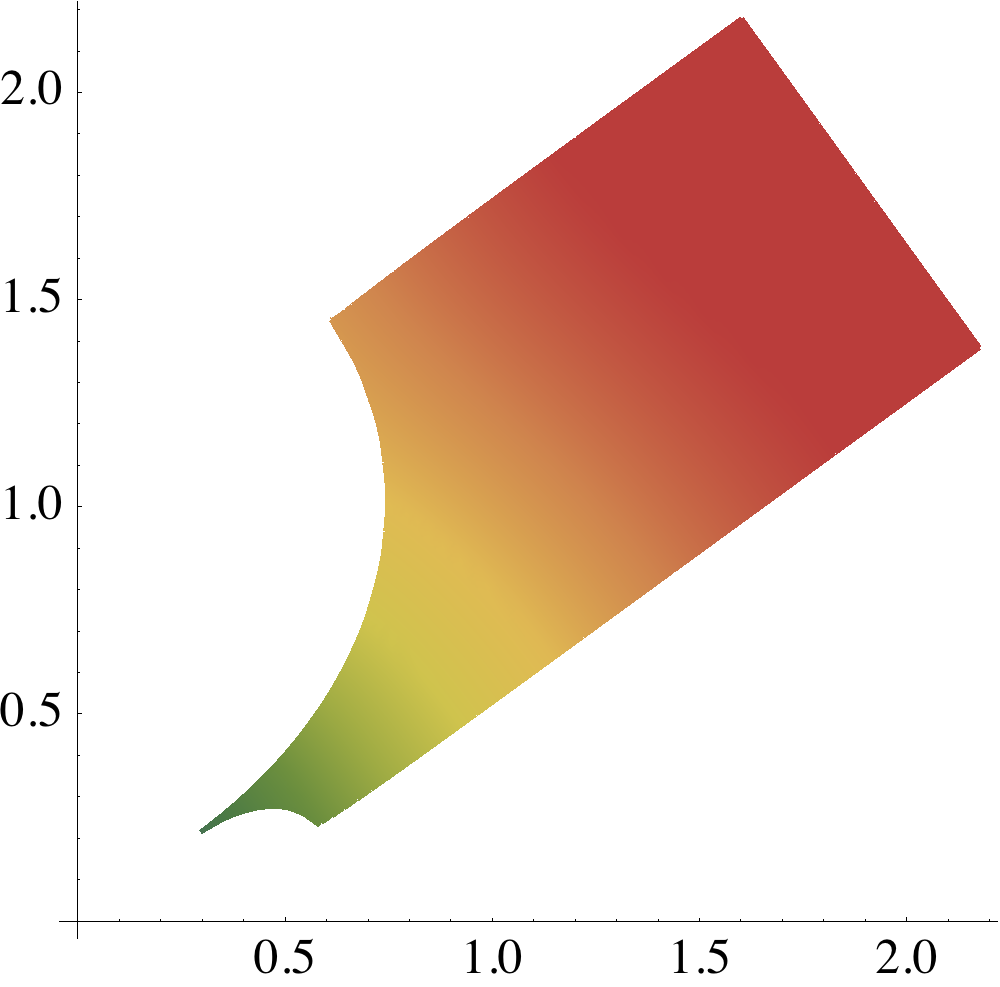

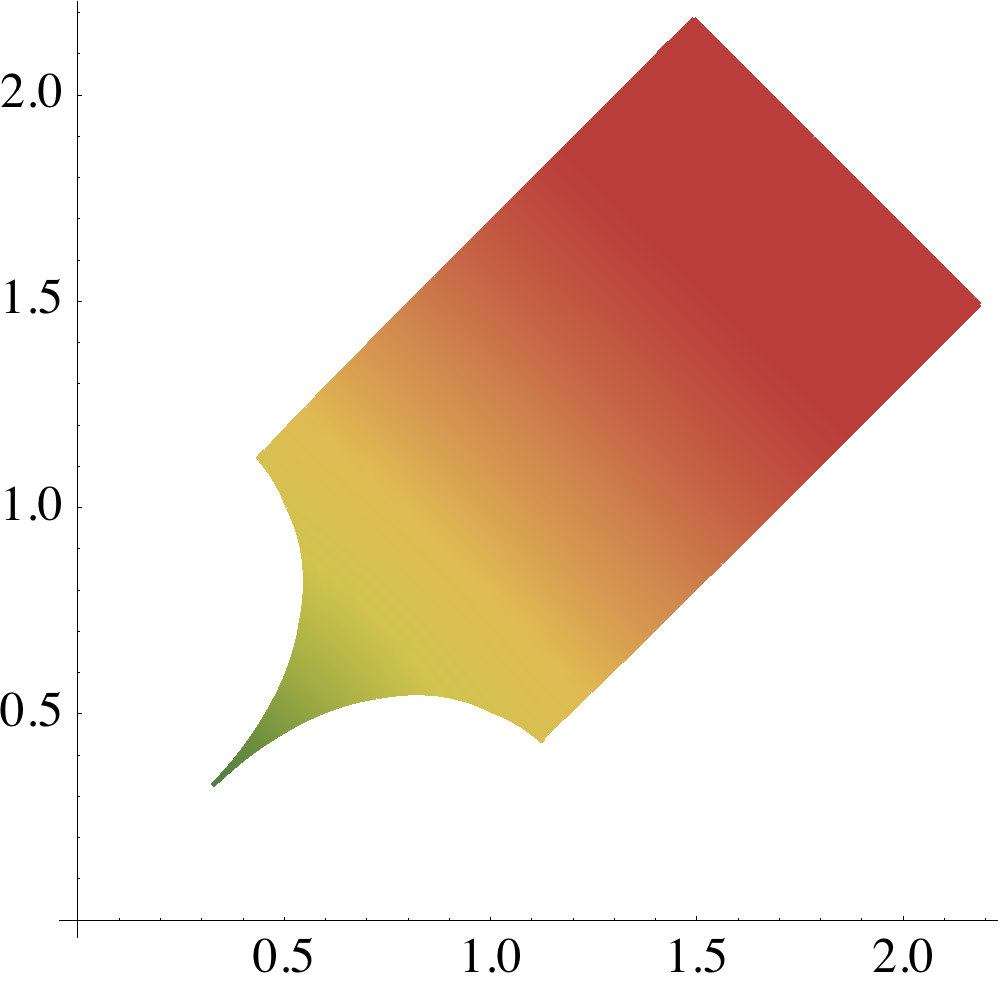

We also consider variants where the density of customers is uniform on the square rotated by an angle around its center, see Figures 6 (left) and 11. Our experiments suggest that exclusion occurs iff , with rad. Bunching is always present, yet two regimes can be distinguished: the one dimensional product line, associated to the bunching phenomenon, is included in the boundary of the two dimensional one iff , with rad. Proving mathematically this qualitative behavior is an open problem.

Remark 6.3 (Subgradient measure).

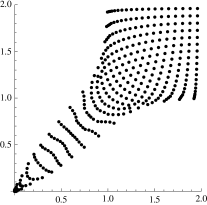

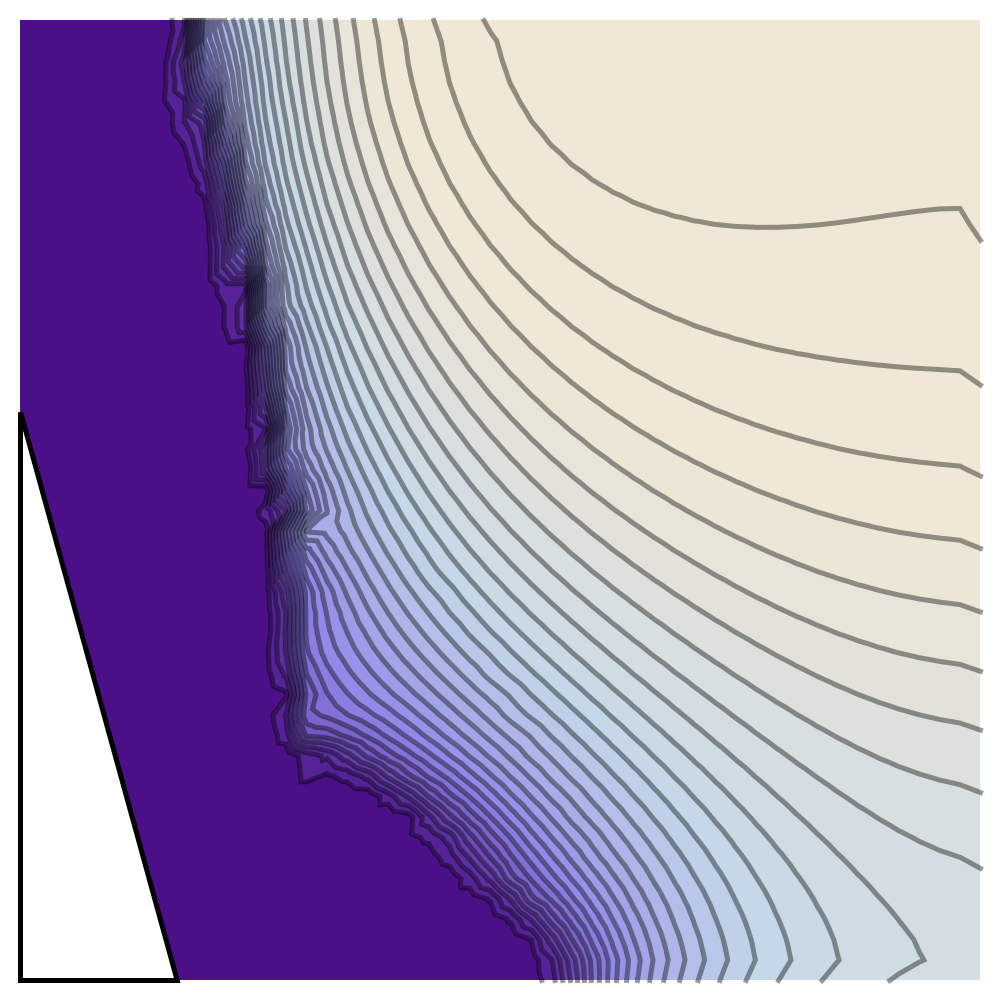

Studying the “bunching” phenomenon requires to estimate the hessian determinant of the solution of (41), and to visualize the degenerate region . The hessian determinant also appears in the density of product sales (42). These features need to be extracted from a minimizer of a finite differences discretization of (41), which is a delicate problem since (i) the hessian determinant is a “high order” quantity, and (ii) equality to zero is a numerically unstable test. Naïvely computing a discrete hessian via second order finite differences, we obtain an oscillating, non-positive and overall imprecise approximation , see Figure 10 (right).

The following approach gave better results, see Figure 10 (left): compute the largest convex such that on (if , then for any -Delaunay triangulation). Then for all

where denotes the sub-gradient, set-valued operator on convex functions, and the two dimensional Lebesgue measure. The sub-gradient sets are illustrated on Figure 6.

Product bundles and lottery tickets.

Two types of products , are considered, which the consumer of characteristics respectively values and . The two products are indivisible, and consumers are not interested in buying more than one of each. The monopolist sells them in bundles which characteristics are the presence () of product , or its absence (), for . In order to maximize profit, the monopolist also considers probabilistic bundles, or lottery tickets, for which the product has the probability of being present. This is consistent with (39), provided consumers are risk neutral. Production costs are neglected, so that if and otherwise. Three different customer densities were considered, see below. The qualitative property of interest is the presence, or not, of probabilistic bundles in the monopolist’s optimal strategy.

-

•

Uniform customer density on . We recover the known exact minimizer [17]:

up to numerical accuracy, see Figure 7 (left). This optimal strategy does not involve lottery tickets: , wherever this gradient is defined. The uselessness of lottery tickets is known for similar 1D problems and was thought to extend to higher dimension, until the following two counter-examples were independently found [17, 25].

-

•

Uniform customer density on the triangle . The monopolist strategy associated to

(43) which involves the lottery ticket , yields better profits that any strategy restricted to deterministic bundles [17]. The triangle , and the numerical best , are illustrated on Figure 7 (center). These experiments suggest that (43) is a777Optimal solutions of (41) are not uniquely determined outside the customer density support . globally optimal solution.

-

•

Uniform customer density on the kite shaped domain , see Figure 7 (right). The optimal monopolist strategy is proved in [25] to involve probabilistic bundles, but it is not identified. Our numerical experiments suggest that it has the form

which involves the lottery tickets and . Under this assumption, the optimal value is easily computed.

Numerous qualitative questions remain open. Is there a distribution of customers for which the optimal strategy involves a continuum of distinct lottery tickets ?

|

|

|

|

|

Pricing of risky assets.

A more complex economic model is considered in [4], where financial products, characterized by their expectancy of gain and their variability, are sold to agents characterized by their risk aversion and their initial risk exposure. We do not give the details of this model here, but simply point out that it fits in the general framework of (41) with the cost function , if , and otherwise, where and are parameters, see Example 3.2 in [4]. Observing that, for

we easily obtain that this cost is convex888This property was not noticed in the original work [4].. The lack of smoothness of the square-root appearing in the cost function is a potential issue for numerical implementation, hence the problem (41) is reformulated using an additional variable subject to a (optimizer friendly) conic constraint

| (44) |

A numerical solution, presented Figure 8, displays the same qualitative properties (Desirability of exclusion, Bunching) as the classical monopolist problem with quadratic cost.

6.3 Comparison with alternative methods

We compare our implementation of the constraint of convexity with alternative methods that have been proposed in the literature. The compared algorithms are the following:

- •

-

•

(Local constraints) The approach of Aguilera and Morin (AM, [1]) based on semi-definite programming. A method of Oberman and Friedlander (OF2, OF3, [22]), where OFk refers to minimization over the cone associated to the fixed stencil . A modification of OF3 by Oberman (Ob3, [21]), with additional constraints ensuring that the output is truly convex.

-

•

(Global constraints) Direct minimization over the full cone , as proposed by Carlier, Lachand-Robert and Maury (CLRM, [5]). Minimization over , see (4), following999We use the description of by linear constraints given in [10], but (for simplicity) not their energy discretization, nor their method for globally extending elements . Ekeland and Moreno (EM, [10]).

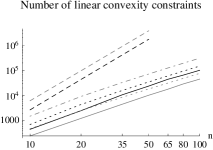

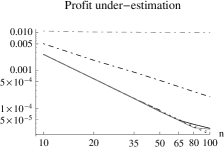

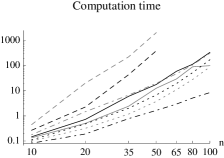

The numerical test chosen is the classical model of the monopolist problem, with quadratic cost, on the domain , see Figure 1 and §6.2. This numerical test case is classical and also considered in [10, 18, 22]. It is discretized on a grid, for different values of ranging from to ( to for global constraint methods due to memory limitations).

The number of linear constraints of the optimization problems assembled by the methods is shown on Figure 9 (center left). For adaptive strategies, this number corresponds to the final iteration. The semi-definite approach AM is obviously excluded from this comparison. Two groups are clearly separated: Adaptive and Local methods on one side, with quasi-linear growth, and Global methods on the other side, with quadratic growth. Let us emphasize that, despite the similar cardinalities, many constraints of the adaptive methods are not local, see Figure 5. The method generally uses the least number of constraints, followed by OF2 and then .

Definition 6.4.

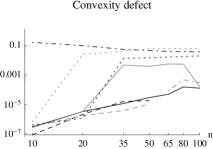

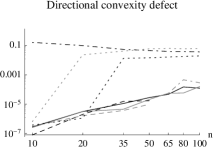

The convexity defect of a discrete map , is the smallest such that . The directional convexity defect of is the smallest such that , see Appendix A.

Figure 9 displays the convexity defect of the discrete solutions produced by the different algorithms, at several resolutions. This quantity stabilizes at a positive value for the methods OF2 and OF3, which betrays their non-convergence as . We expect the convexity defect of the method AM to tend to zero, as the resolution increases, since this method benefits from a convergence guarantee [1]; for practical resolutions, it remains rather high however. Other methods, except , have a convexity defect several orders of magnitude smaller, and which only reflects the numerical precision of the optimizer (some of the prescribed linear constraints are slightly violated by the optimizer’s output). Finally, the method has a special status since it often exhibits a large convexity defect, but its directional convexity defect vanishes (up to numerical precision).

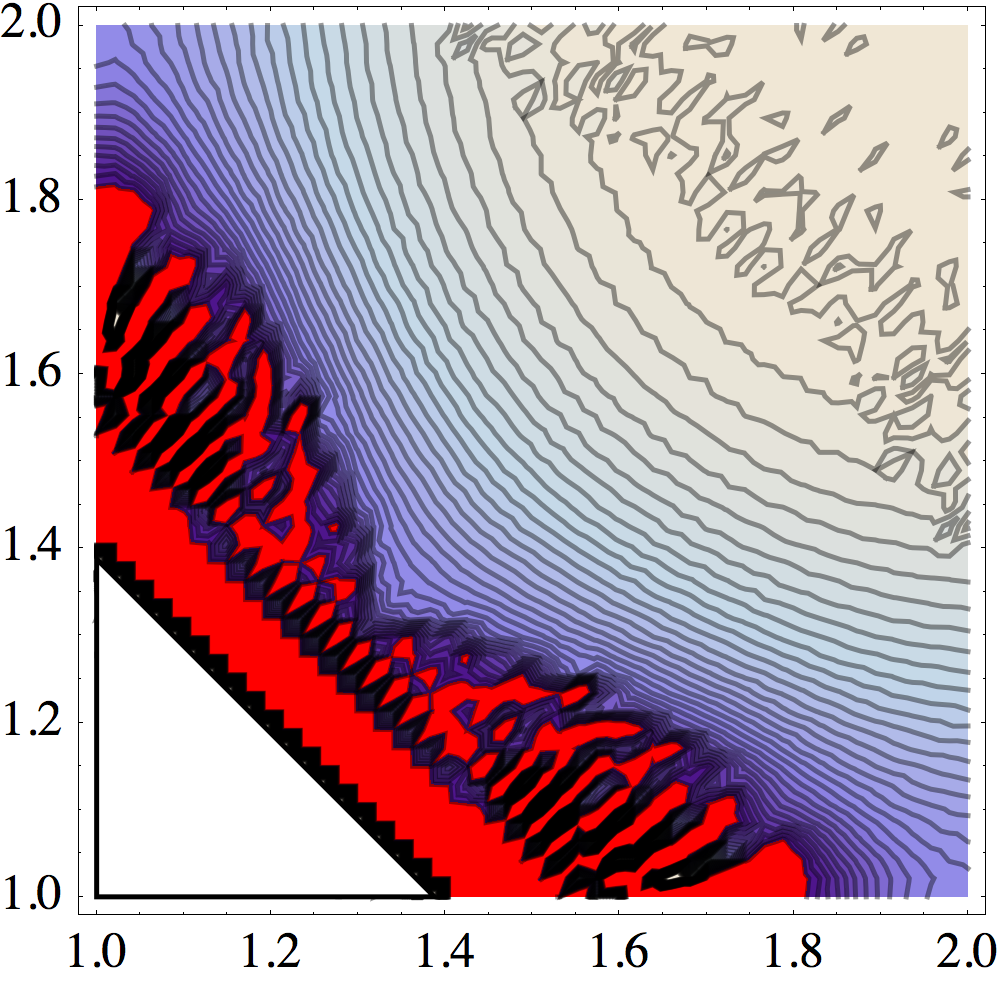

We attempt on figure 10 to extract, with the different numerical methods, the regions of economical interest: potential customers excluded from the trade , and of customers subject to bunching . While the features extracted from the method are (hopefully) convincing, the coordinate bias of the method OF2 is apparent, whereas the method AM does not recover the predicted triangular shape of the set of excluded customers [24]. The other methods , CLRM, EM, (not shown) perform similarly to ; the method OF3 (not shown) works slightly better than OF2, but still suffers from coordinate bias. The method Ob3 (not shown) seems severely inaccurate101010The methods (Obk)k≥1 are closely related to our approach since they produce outputs with zero convexity defect (up to numerical precision), and the number of linear constraints only grows linearly with the domain cardinality: , with . We suspect that better results could be obtained with these methods by selecting adaptively and locally the integer . : indeed the hessian matrix condition number with Obk, , cannot drop below , see [21], which is incompatible with the bunching phenomenon, see the solution gradients on Figure 6.

For each method we compute exactly the monopolist profit (41), associated with the largest global map satisfying on , where is the method’s discrete output. It is compared on Figure 9 with the best possible profit (which is not known, but was extrapolated from the numerical results). Convergence rate is numerically estimated to for all methods111111The (presumed) non-convergence of the methods OF2 and OF3 is not visible in this graph. except (i) the semi-definite approach AM for which we find , and (ii) the method Ob3, for which energy does not seem to decrease.

In terms of computation time121212Experiments conducted on a 2.7 GHz Core i7 (quad-core) laptop, equipped with 16 GB of RAM. , three groups of methods can be distinguished. Global methods suffer from a huge memory cost in addition to their long run times. Methods using a (quasi)-linear number of constraints have comparable run times, thanks to the limited number of stencil refinement steps of the adaptive ones (their computation time might be further reduced by the use of appropriate hot starts for the consecutive subproblems). Finally, the semi-definite programming based method AM is surprisingly fast131313The method AM, implemented with Mosek’s conic optimizer, takes only 2.5s to solve the product bundles variant of the monopolist problem on a grid, with a uniform density of consumers on . This contrasts with the figure, 751s, reported in [1] in the same setting but with a different optimizer. , although this is at the expense of accuracy, see above. For , the method CLRM would use linear constraints, which with our equipment simply do not fit in memory. The proposed method selects in refinement steps a subset containing of these constraints (), and which is by construction guaranteed to include all the active ones; it completes in minutes on a standard laptop.

In summary, adaptive methods combine the accuracy and convergence guarantees of methods based on global constraints, with the speed and low memory usage of those based on local constraints.

Conclusion and perspectives

We in this paper introduced a new hierarchy of discrete spaces, used to adaptively solve optimization problems posed on the cone of convex functions. The comparison with existing hierarchies of spaces, such as wavelets or finite element spaces on adaptively refined triangulations, is striking by its similarities as much as by its differences. The cones (resp. adaptive wavelet or finite element spaces) are defined through linear inequalities (resp. bases), which become increasingly global (resp. local) as the adaptation loop proceeds. Future directions of research include improving the algorithmic guarantees, developing more applications of the method such as optimal transport, and generalizing the constructed cones of discrete convex functions to unstructured or three dimensional point sets.

Acknowledgement.

The author thanks Pr Ekeland and Pr Rochet for introducing him to the monopolist problem, and the Mosek team for their free release policy for public research.

| Method | AM | OF2 | OF3 | Ob3 | CLRM | EM | ||

|---|---|---|---|---|---|---|---|---|

| Constraints | 24 | 10 | NA | 18 | 35 | 72 | 1738 | 3803 |

| Defect | 0.03 | 3.8 | 46 | 59 | 14 | 0 | 0.02 | 0.01 |

| Profit under estimation | 0.11 | 0.11 | 0.57 | 0.11 | 0.11 | 10 | 0.12 | 0.11 |

| Computation time | 18s | 13s | 1.7s | 3.8s | 6.8s | 20s | 391s | 2070s |

References

- [1] N. E. Aguilera and P. Morin. Approximating optimization problems over convex functions. Numerische Mathematik, 2008.

- [2] J. F. Bonnans, E. Ottenwaelter, and H. Zidani. A fast algorithm for the two dimensional HJB equation of stochastic control. Technical report, 2004.

- [3] G. Carlier. A general existence result for the principal-agent problem with adverse selection. Journal of Mathematical Economics, 2001.

- [4] G. Carlier, I. Ekeland, and N. Touzi. Optimal derivatives design for mean–variance agents under adverse selection. Mathematics and Financial Economics, 2007.

- [5] G. Carlier, T. Lachand-Robert, and B. Maury. A numerical approach to variational problems subject to convexity constraint. Numerische Mathematik, 2001.

- [6] B. Chazelle. An optimal convex hull algorithm in any fixed dimension. Discrete and Computational Geometry, 1993.

- [7] P. Choné and H. V. J. Le Meur. Non-Convergence result for conformal approximation of variational problems subject to a convexity constraint. Numerical Functional Analysis and Optimization, 2001.

- [8] C. Dobrzynski and P. Frey. Anisotropic Delaunay Mesh Adaptation for Unsteady Simulations. In Proceedings of the 17th international Meshing Roundtable. 2008.

- [9] H. Edelsbrunner and R. Seidel. Voronoi diagrams and arrangements. Discrete and Computational Geometry, 1986.

- [10] I. Ekeland and S. Moreno-Bromberg. An algorithm for computing solutions of variational problems with global convexity constraints. Numerische Mathematik, 2010.

- [11] J. Fehrenbach and J.-M. Mirebeau. Sparse Non-negative Stencils for Anisotropic Diffusion. Journal of Mathematical Imaging and Vision, 2013.

- [12] A. Figalli, Y. H. Kim, and R. J. McCann. When is multidimensional screening a convex program? Journal of Economic Theory, 2011.

- [13] R. L. Graham, D. E. Knuth, and O. Patashnik. Concrete mathematics : a foundation for computer science, 2nd ed 1994 GRAHAM Ronald L., KNUTH Donald E., PATASHNIK Oren: Librairie Lavoisier. Addison & Wesley, 1994.

- [14] G. Hardy and E. M. Wright. An Introduction to the Theory of Numbers. Oxford Science Publications, 1979.

- [15] F. Hurtado, M. Noy, and J. Urrutia. Flipping Edges in Triangulations. Discrete and Computational Geometry, 1999.

- [16] T. Lachand-Robert and E. Oudet. Minimizing within Convex Bodies Using a Convex Hull Method. SIAM Journal on Optimization, 2005.

- [17] A. M. Manelli and D. R. Vincent. Bundling as an optimal selling mechanism for a multiple-good monopolist. Journal of Economic Theory, 2006.

- [18] Q. Merigot and E. Oudet. Handling convexity-like constraints in variational problems (Preprint). www-ljk.imag.fr.

- [19] J.-M. Mirebeau. Anisotropic Fast-Marching on cartesian grids using Lattice Basis Reduction (Preprint). arXiv.org, 2012.

- [20] J.-M. Mirebeau. Efficient fast marching with Finsler metrics. Numerische Mathematik, 2013.

- [21] A. M. Oberman. A Numerical Method for Variational Problems with Convexity Constraints. SIAM Journal on Scientific Computing, 2013.

- [22] A. M. Oberman and M. P. Friedlander. A numerical method for variational problems over the cone of convex functions (Preprint). arXiv.org, 2011.

- [23] M. Qi, T.-T. Cao, and T.-S. Tan. Computing 2D constrained Delaunay triangulation using the GPU. In the ACM SIGGRAPH Symposium, 2012.

- [24] J. C. Rochet and P. Choné. Ironing, Seeping, and Multidimensional Screening. Econometrica, 1998.

- [25] J. Thanassoulis. Haggling over substitutes. Journal of Economic Theory, 2004.

- [26] G. Wachsmuth. The Numerical Solution of Newton’s Problem of Least Resistance (Preprint). 2013.

Appendix A Directional convexity

We introduce and discuss a weak notion of discrete convexity, which involves slightly fewer linear constraints than (3) and seems sufficient to obtain convincing numerical results, see §6.3.

Definition A.1.

We denote by the collection of elements in on which all the linear forms , , irreducible, supported on , take non-negative values.

Some elements of cannot be extended into global convex maps on . Their existence follows from the second point of Theorem 1.4 (minimality of the collection of constraints , ), but for completeness we give (without proof) a concrete example.

Proposition A.2.

Let be defined by , , and for other . Then for all , and all irreducible , one has , and if , with the exception .

Elements of are nevertheless “almost” convex, in the sense that their restriction to a coarsened grid is convex.

Proposition A.3.

If , then , with .

Proof.

Let , and let , , be irreducible and of parents . Assuming that , and observing that by convexity, we obtain

Likewise . ∎

The cone of directionally convex functions admits, just like , a hierarchy of sub-cones associated to stencils.

Definition A.4.

Let be a family of stencils on , and let . The cone is defined by the non-negativity of the following linear forms: for all

-

•

For all , the linear form , if supported on .

-

•

For all , the linear form , if supported on .

Proposition A.5.

-

•

For any stencils , one has , , and .

-

•

For any stencils , one has

(45)

Proof.

As observed in §3.2, the second point of this proposition implies the first one. We denote by the identity (45), and prove it by decreasing induction over . Since clearly holds, we consider stencils .

Let , , be such that is minimal. Similarly to Proposition 3.9 we find that belongs to the set of candidates for refinement at , and define stencils by , and for . The cones and are defined by a common collection of constraints, with the addition respectively of for , and , , for . Expressing the latter linear forms as combinations of those defining

and observing that holds by induction, we conclude the proof of . ∎