Branching ratio approximation for the self-exciting Hawkes process

Abstract

We introduce a model-independent approximation for the branching ratio of Hawkes self-exciting point processes. Our estimator requires knowing only the mean and variance of the event count in a sufficiently large time window, statistics that are readily obtained from empirical data. The method we propose greatly simplifies the estimation of the Hawkes branching ratio, recently proposed as a proxy for market endogeneity and formerly estimated using numerical likelihood maximisation. We employ our new method to support recent theoretical and experimental results indicating that the best fitting Hawkes model to describe S&P futures price changes is in fact critical (now and in the recent past) in light of the long memory of financial market activity.

I The self-exciting Hawkes Process

The Hawkes model hawkes ; hawkes2 is a simple and powerful framework for simulating or modelling the arrival of events which cluster in time (e.g. earthquake shocks and aftershocks, neural spike trains and transactions on financial markets). In one dimension, the model is a counting process with an intensity (the expected number of events per unit time) given by a constant term and a ‘self-exciting’ term which is a function of the event history.

| (1) |

This self-exciting term gives rise to event clustering through an endogenous feedback: past events contribute to the rate of future events. is the “influence kernel” which decides the weight to attribute to events which occurred at a lag in the past. The base intensity and the kernel shape are parameters to be varied. A popular choice for the kernel is the exponential function filimonov ; ozaki but in general the kernel to be used should depend on the application or the dynamics of the data to be modelled. Note that for the model reduces to a Poisson process with constant intensity .

By taking the expectation of both sides of Eq. (1) and assuming stationarity (i.e. a finite average event rate ), we can express the average event rate of the process as where . One can create a direct mapping between the Hawkes process and the well known branching process harris in which exogenous “mother” events occur with an intensity and may give rise to additional endogenous “daughter” events, where is drawn from a Poisson distribution with mean . These in turn may themselves give birth to more “daughter” events, etc.

The value , which corresponds with the integral of the Hawkes kernel is the branching ratio, determines the behaviour of the model. If , meaning that each event typically triggers at least one extra event, then the process is non-stationary and may explode in finite time commodityreflexivity . However, for , the process is stationary and has proven useful in modelling the clustered arrival of events in a wide variety of applications including neurobiology neurobiology , social dynamics social ; crime and geophysics earthquakes1 ; earthquakes2 . The Hawkes model has also seen many recent applications to finance bauwens ; hawkesvolatility ; bormetti , especially as a means of modelling the very high-frequency events affecting the limit-order book of financial exchanges bacry ; hawkesmicrostructure ; bacrypricetrades ; toke ; dafonseca .

One novel application of the Hawkes framework to finance is as a means of measuring market endogeneity or ‘reflexivity’ in financial markets filimonov ; commodityreflexivity . In filimonov , the authors consider mid-price changes in the E-mini S&P Futures contract between 1998 and 2010 and observe that the branching ratio of the best-fitting exponential kernel model has been increasing steadily over this period, from in 1998 to in 2010 (see our Fig. 6 below). They argue that this observation implies that the market has become more reflexive in recent years with the rise of high frequency and algorithmic trading and is therefore more prone to market instability and so-called “flash crashes”.

In criticalreflexivity , however, we have argued that due to the presence of long-range dependence in the event rate of mid-price changes (detectable in both 1998 and 2011) as one extends the window of observation, the best fitting stationary Hawkes model must in fact be critical, i.e. have a branching ratio . This is backed up by theoretical arguments and empirical measurements on market data.

Let us however insist that this conclusion only holds if one believes that Hawkes processes provide an exact representation of the reality of markets. It is very plausible that the dynamics of markets is more complicated (and involves, for example, non-linearities absent from the Hawkes process defined by Eq. (1)), but that the best way to represent this dynamics within the framework of Hawkes processes is to choose with a long-ranged influence kernel.

In this article we introduce a simple approximation for the branching ratio of the Hawkes process which allows us to faithfully reproduce the results of filimonov which proposes the statistic as a measure of market instability and as a crash prediction metric. The interest of our approximation lies in its great simplicity: one need only estimate the mean and variance of the event count in a sufficiently large time window. The approximation also avoids a number of pitfalls apparentcriticality inherent to the significantly more complex approach ozaki employed in filimonov .

The estimator accepts one parameter, a time window size, , during which we measure the mean and variance of the event count. We note that when we employ our estimator to mid-price changes in the S&P electronic futures market with a fixed window size then the branching ratio estimate obtained increases over time as reported in filimonov . If, however, we allow the window size to scale appropriately (halving in size every 18 months) to adapt to the decreasing latency of interactions on the market we recover a constant branching ratio estimate as proposed in criticalreflexivity . This result reiterates the need for a scale-invariant, or at least scale-sensitive means of measuring the ‘reflexivity’ of financial market events.

II Maximum likelihood estimation

Given observed events (e.g. mid-price changes) at times in an interval one can fit the Hawkes model by maximising the log-likelihood rubin ; ozaki over the set of parameters .

| (2) |

In the case of the exponential kernel . In practice, the model parameters which maximise this log-likelihood are obtained with numerical techniques due to the lack of a closed form solution 111Note that the method above is not the only method proposed to fit the parameters of the Hawkes process for financial applications, indeed a recent publication dafonseca proposes a fast albeit still parametric method for fitting the multivariate exponential Hawkes process.. The branching ratio estimate is then .

However, there are a number of pitfalls to using this procedure as a means of estimating the Hawkes branching ratio apparentcriticality . Arguably the most important of which is that any estimate of made in this manner will be heavily dependent on the choice of kernel model (e.g. exponential, power-law, etc.) It may be that the chosen model cannot satisfactorily describe the observed events, hence the meaning of the branching ratio extracted from the maximum likelihood method is questionable.

Care must also be taken when employing this method in the presence of imperfect event data as illustrated in apparentcriticality . In one of their figures, the authors present a (negative) log-likelihood surface which features two minima (one local, and one global). The global log-likelihood minimum does in fact little more than describe packet clustering inside the millisecond which arises from the manner in which events arriving at the exchange at different times are bundled and recorded with the same timestamp. Subsequent randomisation of the timestamps inside a short time interval (in this case, one millisecond) creates a spurious high frequency correlation, that makes the global minimum irrelevant. The local log-likelihood minimum, which is in fact a better fit to the ‘true’ lower frequency dynamics, does a poor job at explaining the spurious high frequency clustering and is punished with a lower log-likelihood. Indeed, when the authors of apparentcriticality choose to fit this local minimum they corroborate results presented in criticalreflexivity .

We believe it is therefore essential to have additional checks (such as non-parametric methods bacry ) at one’s disposal to support results obtained from likelihood maximisation. To address the pitfalls in branching ratio estimation that arise from the model choice we propose a simple model-independent tool for branching ratio approximation, in the next section, which accurately reproduces previous results of filimonov and also indicates the criticality of the relevant Hawkes process which describes the market.

III A mean-variance estimator for the branching ratio

We begin with a general expression relating the Fourier transform of the kernel function to the Fourier transform of the auto-covariance of the event rate. (see hawkes ; bacry for a derivation).

| (3) |

Setting we obtain a relation between the branching ratio, the average event rate and the integral of the auto-covariance (in the stationary case )

| (4) |

Therefore, to deduce the branching ratio of the stationary Hawkes process, we need only find the value of and . Estimating is trivial, it is given by the empirical average number of events per unit time. To estimate , we consider the variance of the total event count in a window of length . Theoretically, this is given by:

| (5) | |||||

We then note that provided:

-

1.

for

-

2.

such that for all

then

| (6) |

and we find, using Eq. (4):

| (7) |

where is the average number of events falling in a window of size . The above expression has a very intuitive interpretation. When the variance is equal to the event rate, the process is obeying Poisson statistics and . Any increase in the variance above the event rate indicates some positive correlations and, within a Hawkes framework, a positive branching ratio.

Note from Eq. (5) that is a biased estimator for and for a general will fall short of its theoretical value. This means that Eq. (7) will generally under-estimate the branching ratio and only become exact in the limit .

In practice, to estimate the branching ratio of an empirical sample of total length we substitute the mean and variance term in Eq. (7) by their sample estimates:

| (8) | |||

| (9) |

An estimate obtained in this fashion is asymptotically convergent for large , i.e. . For a fixed window size we can always ensure that our estimate of the variance of is within a desired maximum error with a desired minimum probability by increasing and therefore the number of observations of . Furthermore, we can make Eq. (6) exact by allowing to be arbitrarily large.

Note, however, that for any finite , the average of over all possible realisations of the process is in fact ! This is because a value is always possible with a non zero probability. For this reason we choose to present the median of our estimates.

IV Numerical simulations & Implementation notes

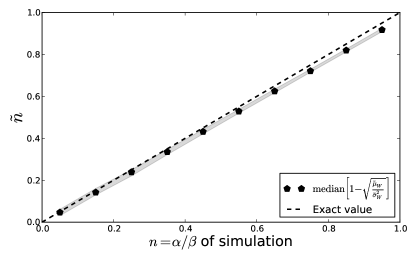

In Fig. 1, we test the estimation procedure described in the previous section on a number of simulated exponential Hawkes processes with a variety of branching ratios. To do this we fix but vary in the range . We choose a base intensity such that each process has the same average event rate . We simulate the process for a time using simulation Algorithm 1 described in moller2005perfect . This procedure is prone to edge effects so we disregard the initial period of size to ensure the process is close to stationarity in the period studied.

We estimate the branching ratio with a window size significantly larger than the time-scale of correlation of our process . However, the window size chosen is also sufficiently small that we have a significant number of independent observations with which to make a reliable estimate of the variance of . We see very good agreement between our branching ratio estimates and the input branching ratio of the simulation, see Fig. 1.

Note however, that our approximation systematically underestimates the branching ratio since our finite window size does not completely cover the region of support of the autocorrelation function. This is particularly visible in Fig. 1 for large . We now investigate the effect of window size on the estimate obtained.

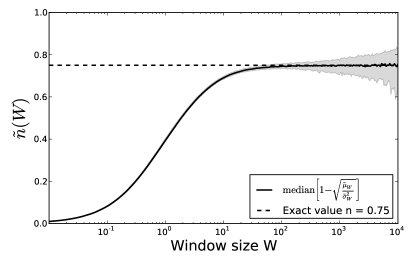

IV.1 Choice of window size W

For Eq. (6) to be accurate, we must choose a large . However for a finite sample size, large implies small and therefore less statistical power with which to estimate the variance of the event count . This compromise is illustrated in Fig. 2 for which we simulate an ensemble of exponential Hawkes processes with parameters , and . We note that for increasing window size , the confidence bands of our estimate converge on the expected value of .

However when we make the window size too large, we suffer significant error coming from the estimation of the variance. For the practical implementation of this procedure to empirical data we recommend a choice of window size sufficiently large to capture the bulk of autocorrelation present in the event rate, but sufficiently small that one can expect to obtain reliable estimates of the variance of the event count in that window.

One can approximate upper and lower confidence intervals on the branching ratio estimate from a single realisation of a time series by bootstrap re-sampling. Indeed the simple variance estimator of Eq. (9) is not optimal and can be improved with the use of over-lapping windows or, for example, a Monte Carlo sampling scheme which selects random windows with replacement.

IV.2 Power-law kernel

Finally we test the estimation procedure on a (near) critical power-law Hawkes process, a type suggested in some recent publications as a good fit to financial event data bacry ; criticalreflexivity . Specifically, we consider a kernel with an Omori law form:

In the critical case of with this process will exhibit long-range dependence, with an autocorrelation function decaying asymptotically as a power law: bremaud ; criticalreflexivity . The integral of the autocorrelation function is therefore divergent for large ’s and the variance of the event count in a window of size grows with as . The term in Eq. 7 will in this case not converge to a finite constant for large but rather shrink to zero, leading to .

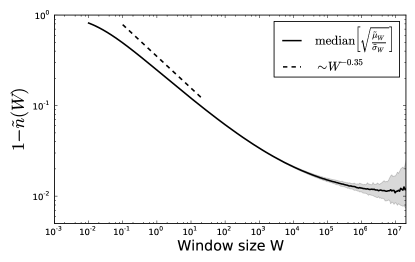

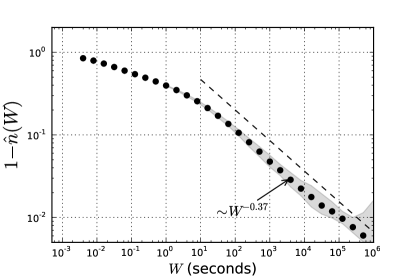

We have simulated such a process with exponent and cut-off parameter . To allow our simulation to attain a stationary state with an average event rate , we make our process very near critical by choosing and . We simulate for a very long period and discard the first to ensure the process is close to stationarity ( at ). In Fig. 3 we present the results of branching ratio estimation using Eq. (7) with a variety of window sizes .

We note that the branching ratio estimate we obtain is very much dependent on the choice of window size used. To capture all the correlation present in the process and obtain estimates close to the the true input value we must probe the correlation on very large scales, by choosing a very large value for . The branching ratio obtained indeed varies with window size according to the law , in a similar way to the integral of the kernel , see Fig. 3.

V Empirical applications

V.1 Flash-crash revisited

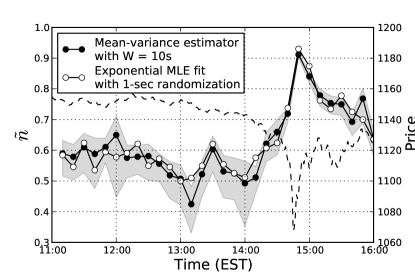

To demonstrate the effectiveness of this simple estimator we have repeated the flash-crash day branching ratio analysis of Filimonov & Sornette filimonov . We consider non-overlapping periods of 10 minutes in the hours of trading before and just after the flash-crash. For each 10-minute period, we calculate the sample mean and variance of the number of mid-price changes in the 60 windows of length contained. The resulting values are plugged into Eq. (7) to obtain an approximation of the branching ratio for each period. The results are presented in Fig. 4.

Note that this simple estimator is biased, and for a general , will typically underestimate the value of and therefore the branching ratio. Since we consider a window size we have systematically underestimated in Figure 4 as measurements of on this data have support outside the interval — there is still significant autocorrelation in the event rate at scales longer than .

However, we have identified that a window size of the order of approximately 10 to 30 seconds produces estimates of the branching ratio on our data in line with those obtained by ML fitting to the exponential model after intra-second randomisation (the method applied in filimonov .) Note that we do not fix in our ML fit but let it settle naturally at the value which maximises the log-likelihood. We observe that this value is very much dependent on the period of randomisation222To address the limited precision of the event data in filimonov , the authors randomise timestamps uniformly inside the second that they are reported. of the timestamps. When we randomise timestamps inside each millisecond we obtain for periods in 2010 but randomisation at larger intervals (e.g. the intra-second randomisation of Filimonov & Sornette) prevents from exceeding values of the order of magnitude of the scale of randomisation.

Note that since our results with correspond well with those obtained using the methods of Filimonov & Sornette filimonov , their procedure must also underestimate the branching ratio. To converge on the true in expectation, we must take Eq. (7) in the limit of . We do just this in Fig. 5 for mid-price changes of the E-mini S&P Futures contract in 2010. One notes that as the window size increases, the branching ratio converges to in a non-trivial way. As reported in criticalreflexivity for the structure of the kernel at short and long time-scales, two regimes are detectable with a transition around five minutes. The branching ratio asymptotically tends towards with a scaling exponent compatible with the value of estimated in criticalreflexivity for a 14-year period. Note that in taking the limit we consider variation in the event rate at significant time-scales to be explained by the stationary Hawkes model.

V.2 Reflexivity : 1998 - 2013

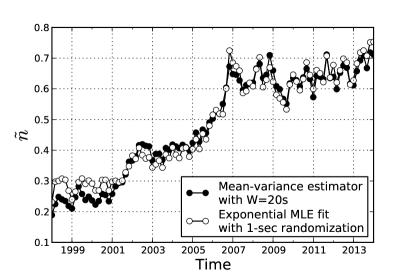

Using the mean-variance estimator, we can also easily reproduce the result of filimonov that claims to demonstrate that reflexivity has been increasing in the S&P futures market since 1998. To do this we set our only parameter and estimate the branching ratio in periods of 15-minutes. In Fig. 6 we present the 2-month medians of these estimates beside the median of the branching ratio estimate obtained using the exponential maximum likelihood approach after intra-second randomisation.

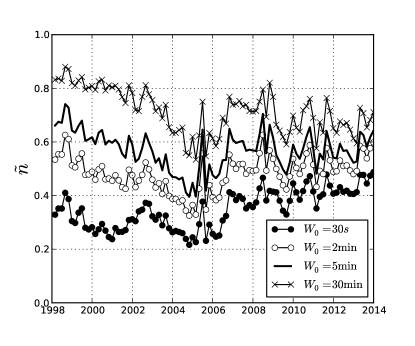

Since we expect the minimum time-scale of correlation in the data to have decreased over the past decades (due to decreasing latency with advancing technology) we now re-perform the experiment but with a window size that follows Moore’s law in such a way to keep the average number of events in roughly constant. More precisely the window size halves every 18 months; this describes well the increase in the high frequency activity of markets, see criticalreflexivity . The results of this experiment are presented in Fig. 7 and confirm that the kernel integral is approximately invariant over time provided that the measurement window is appropriately rescaled to account for the changing speed of interactions in the market. We find this quite remarkable, as this suggests that the amount of self-reflexivity in financial markets is scale invariant, and has not significantly increased due to high-frequency trading.

VI Summary

We have introduced a simple estimator for the branching ratio of Hawkes self-exciting point-process. The method is straight-forward to apply to empirical event data since it requires only a rudimentary calculation on the mean and variance of the event rate. The estimator does not suffer from the bias inherent to the contentious question of the choice of kernel in the likelihood maximisation approach, and furthermore it avoids the need for complicated numerical minimisation techniques.

Despite its simplicity, our estimator can accurately reproduce results obtained for the branching ratio using this prior method. The estimator presented is indeed a biased estimator, but it can be made asymptotically unbiased in the limit of large and , for which we observe that the branching ratio for empirical mid-price changes of the E-mini S&P futures contract approaches unity in line with previous theoretical and empirical results criticalreflexivity .

Furthermore we demonstrate that if the window size is allowed to scale with Moore’s law and adapt to the changing speed of interaction in the market over the past fifteen years, then the branching ratio approximation recovered is constant supporting prior observations of the invariance of the Hawkes kernel and branching ratio over time in criticalreflexivity .

Finally, let us reiterate the caveat made above: the Hawkes analysis of the activity in financial markets leads to the conclusion that the process must be critical. However, it might well be that the dynamics of markets is more complicated and requires non-linearities absent from the Hawkes process defined by Eq. (1)). More work on this issue would be highly interesting, and is in progress in our group.

Acknowledgements

We thank V. Filimonov for many productive discussions about this topic. We are also indebted to N. Bercot, J. Kockelkoren, M. Potters, I. Mastromatteo, P. Blanc and J. Donier for interesting and useful comments.

References

- (1) A. G. Hawkes, “Spectra of some mutually exciting point processes,” Biometrika 58 (1970) 83.

- (2) A. G. Hawkes, “Point spectra of some mutually exciting point processes,” Journal of the Royal Statistical Society, Series B 33 no. 3, (1971) 438–443.

- (3) V. Filimonov and D. Sornette, “Quantifying reflexivity in financial markets: Toward a prediction of flash crashes,” Physical Review E 85 (2012) 056108.

- (4) T. Ozaki, “Maximum likelihood estimation of Hawkes self-exciting point process,” Annals of the Institute of Statistical Mathematics 31 (1979) 145–155. Part B.

- (5) T. E. Harris, The Theory of Branching Processes. Dover Publications, 2002.

- (6) V. Filimonov, D. Bicchetti, N. Maystre, and D. Sornette, “Quantification of the high level of endogeneity and of structural regime shifts in commodity markets.,” Journal of International Money and Finance 42 (April, 2013) 174–192.

- (7) V. Pernice, B. Staude, S. Cardanobile, and S. Rotter, “How structure determines correlations in neuronal networks,” PLOS Computational Biology 7 (2011) e1002059.

- (8) R. Crane and D. Sornette, “Robust dynamic classes revealed by measuring the response function of a social system,” Journal of the American Statistical Association 105 no. 41, (September, 2008) 15649–15653.

- (9) G. O. Mohler, M. B. Short, P. J. Brantingham, F. P. Schoenberg, and G. E. Tita, “Self-exciting point process modeling of crime,” Journal of the American Statistical Association 106 (2011) 100–108.

- (10) Y. Ogata, “Seismicity analysis through point-process modeling: A review,” Pure and Applied Geopysics 155 no. 2-4, (1999) 471–507.

- (11) A. Helmstetter and D. Sornette, “Subcritical and supercritical regimes in epidemic models of earthquake aftershocks,” Journal of Geophysical Research: Solid Earth 107 no. B10, (2002) ESE 10–1–ESE 10–21.

- (12) G. Bormetti, L. M. Calcagnile, M. Treccani, F. Corsi, S. Marmi, and F. Lillo, “Modelling systemic cojumps with Hawkes factor models,” arXiv:1301.6141 [q-fin.ST].

- (13) L. Bauwens and N. Hautsch, “Modelling financial high frequency data using point processes,” in Handbook of Financial Time Series, T. Mikosch, J.-P. Kreiss, R. A. Davis, and T. G. Andersen, eds. Springer Berlin Heidelberg, 2009.

- (14) P. Embrechts, T. Liniger, and L. Lin, “Multivariate Hawkes processes: an application to financial data,” Journal of Applied Probability 48A (August, 2011) 367–378.

- (15) E. Bacry, K. Dayri, and J.-F. Muzy, “Non-parametric kernel estimation for symmetric Hawkes processes. application to high frequency financial data,” European Physics Journal B 85 no. 5, (2012) 157.

- (16) E. Bacry and J.-F. Muzy, “Hawkes model for price and trades high-frequency dynamics,” Quantitative Finance 14 (2014) 1147–1166.

- (17) I. M. Toke and F. Pomponio, “Modelling trades-through in a limit order book using Hawkes processes,” Economics: The Open-Access, Open-Assessment E-Journal 6 (2012) .

- (18) J. D. Fonseca and R. Zaatour, “Hawkes process: Fast calibration, application to trade clustering, and diffusive limit,” Journal of Futures Markets (2013) .

- (19) E. Bacry, S. Delattre, M. Hoffmann, and J.-F. Muzy, “Modeling microstructure noise with mutually exciting point processes,” Quantitative Finance 13 (2012) 65–77.

- (20) S. J. Hardiman, N. Bercot, and J.-P. Bouchaud, “Critical reflexivity in financial markets: a Hawkes process analysis,” The European Physical Journal B 86 no. 10, (2013) 1–9.

- (21) V. Filimonov and D. Sornette, “Apparent criticality and calibration issues in the Hawkes self-excited point process model: application to high-frequency financial data,” arXiv:1308.6756 [q-fin.ST].

- (22) I. Rubin, “Regular point processes and their detection,” IEEE Transactions on Information Theory IT-18 (September, 1972) 547–557.

- (23) J. Møller and J. G. Rasmussen, “Perfect simulation of hawkes processes,” Advances in Applied Probability (2005) 629–646.

- (24) P. Brémaud and L. Massoulié, “Hawkes branching point processes without ancestors,” Journal of Applied Probabability 38 no. 1, (2001) 122–135.