Quality Sensitive Price Competition in Spectrum Oligopoly-Part 1

Abstract

We investigate a spectrum oligopoly market where each primary seeks to sell its idle channel to a secondary. Transmission rate of a channel evolves randomly. Each primary needs to select a price depending on the transmission rate of its channel. Each secondary selects a channel depending on the price and the transmission rate of the channel. We formulate the above problem as a non-cooperative game. We show that there exists a unique Nash Equilibrium (NE) and explicitly compute it. Under the NE strategy profile a primary prices its channel to render the channel which provides high transmission rate more preferable; this negates the perception that prices ought to be selected to render channels equally preferable to the secondary regardless of their transmission rates.We show the loss of revenue in the asymptotic limit due to the non co-operation of primaries. In the repeated version of the game, we characterize a subgame perfect NE where a primary can attain a payoff arbitrarily close to the payoff it would obtain when primaries co-operate.

I Introduction

To accommodate the ever increasing traffic in wireless spectrum, FCC has legalized the unlicensed access of a part of the licensed spectrum band- which is known as secondary access. However, secondary access will only proliferate when it is rendered profitable to license holders (primaries)111Primaries are unlikely to encourage “free ride” where secondaries (unlicensed users) can access idle channel without paying for them. If primaries are not compensated, they may therefore create artificial activity by transmitting some noise to deny secondaries.. We devise a framework to enable primaries to decide price they would charge unlicensed users (secondaries). The price will depend on the transmission rate which evolves randomly owing to usage of subscribers of primaries and fading. A secondary receives a payoff from a channel depending on the transmission rate offered by the channel and the price quoted by the primary. Secondaries buy those channels which give them the highest payoff, which leads to a competition among primaries.

Price selection in oligopolies has been extensively investigated in economics as a non co-operative Bertrand Game [23] and its modifications [26, 18]. Price competition among wireless service providers have also been explored to a great extent [10, 22, 21, 32, 24, 25, 36, 15, 31, 3, 35, 12, 34, 29, 16]. We divide this genre of works in two parts: i) Papers which model price competition as Auction ([29, 33]), and ii) Papers which model the price competition as a non co-operative game ([10, 22, 21, 32, 24, 25, 15, 12, 34, 31, 35, 19, 3, 16]). We now distinguish our work with respect to these papers. As compared to the genre of work in the first category our model is readily scalable and a central auctioneer is not required. Some papers in the second category [12, 34, 31, 35, 3, 16] considered the quality of primaries as a factor while selecting the price. But all of these papers mentioned above, ignore two important properties which distinguish spectrum oligopoly from standard oligopolies: First, a primary selects a price knowing only the transmission rate of its own channel; it is unaware of transmission rates offered by channels of its competitors. Thus, if a primary quotes a high price, it will earn a large profit if it sells its channel, but may not be able to sell at all; on the other hand a low price will enhance the probability of a sale but may also fetch lower profits in the event of a sale. Second, the same spectrum band can be utilized simultaneously at geographically dispersed locations without interference; but the same band can not be utilized simultaneously at interfering locations; this special feature, known as spatial reuse adds another dimension in the strategic interaction as now a primary has to cull a set of non-interfering locations which is denoted as an independent set; at which to offer its channel apart from selecting a price at every node of that set. We have accommodated both of the above the uncertainty of competition in this paper. Building on the results we obtain in this paper, we have accommodated both of the above characteristics in the sequel.

Some recent works ([13, 11, 17, 14]) that consider uncertainty of competition and the impact of spatial reuse ([36] and [14]) assume that the commodity on sale can be in one of two states: available or otherwise. This assumption does not capture different transmission rates offered by available channels. A primary may now need to employ different pricing strategies and different independent set selection strategies for different transmission rates, while in the former case a single pricing and independent set selection strategy will suffice as a price needs not be quoted for an unavailable commodity. Our investigation seeks to contribute in this space.

We have studied the price competition in spectrum oligopoly in a sequel of two papers. Overall a primary has to select an independent set and a pricing strategy in each location of the independent set. In this paper we focus only on the pricing strategy of primaries by studying the game for only one location. The results that we have characterized provide indispensable tools for studying the joint decision problem involving multiple locations. In the sequel to this paper, we provide a framework for solving the joint decision problem building on the single location pricing strategy. In addition, initially secondary market is likely to be introduced in geographically dispersed locations; which are unlikely to interfere with each other, thus, the price competition in each location reduces to a single location pricing problem which we solve in this paper. The reduced problem turns out to be of independent interest as it exhibits certain desirable properties which no longer hold when there are multiple locations.

We formulate the price selection as a game in which each primary selects a price depending on the transmission rate its channel provides. Since prices can take real values, the strategy space is uncountably infinite; which precludes the guarantee of the existence of an Nash Equilibrium (NE) strategy profile. Also standard algorithms for computing an NE strategy profile do not exist unlike when the strategy space is finite.

First, we consider that primaries interact only once (Section III). We consider that the preference of the secondaries can be captured by a penalty function which associates a penalty value to each channel that is available for sale depending on its transmission rate and the price quoted. We show that for a large class of penalty functions, there exists a unique NE strategy profile, which we explicitly compute (Section III-B). In the sequel to this paper, we show that this is no longer the case when a primary owns a channel over multiple locations.

We show that the unique NE strategy profile is symmetric i.e. price selection strategy of all primaries are statistically identical. Our analysis reveals that primaries select price in a manner such that the preference order of transmission rates is retained. This negates the intuition that prices ought to be selected so as to render all transmission rates equally preferable to a secondary. The analysis also reveals that the unique NE strategy profile consists of ”nice” cumulative distributions in that they are continuous and strictly increasing; the former rules out pure strategy NEs and the latter ensures that the support sets are contiguous.

Subsequently, utilizing the explicit computation algorithm for the symmetric NE strategies, we analytically investigate the reduction in expected profit suffered under the unique symmetric NE pricing strategies as compared to the maximum possible value allowing for collusion among primaries (Section IV).Finally, we extend our one shot game at single location, to a repeated game where primaries interact with each other multiple number of times (Section V) and compute a subgame perfect Nash equilibrium (SPNE) in which a primary attains a payoff which is arbitrarily close to the payoff that a primary would have obtained if primaries were select price jointly; thus, price competition does not lower payoff.

All proofs are relegated to Appendix.

II System Model

We consider a spectrum market with primaries. Each primary owns a channel. Different channels leased by primaries to secondaries constitute disjoint frequency bands. There are secondaries. We initially consider the case when primaries know , later generalize our results for random, apriori unknown (Section III-C). The channel of a primary provides a certain transmission rate to a secondary who is granted access. Transmission rate (i.e. Shanon Capacity) depends on 1) the number of subscribers of a primary that are using the channel222Shanon Capacity [2] for user at a channel is equal to where is the power with which user is transmitting, is the power of white noise, is the channel gain between transmitter and receiver which depends on the propagation condition. If a secondary is using the channel then of the numerator are the attributes associated with the secondary while are those of the subscribers of the primaries. In general, the power for subscriber of primaries is constant for subscriber of primary, but the number of subscribers vary randomly over time. The power with which a secondary will transmit may be a constant or may decrease with the number of subscribers of primaries in order to limit the interference caused to each subscriber. The above factors contributes to the random fluctuation in the capacity of a channel offered to a secondary. In our setting s are assumed to be the same across the secondaries for a channel which we justify later. However, these values can be different for different channels. and 2) the propagation condition of the radio signal. The transmission rate evolves randomly over time owing to the random fluctuations of the usage of subscribers of primaries and the propagation condition333Referring to footnote 2, and evolve randomly owing to the random scattering of the particles in the ionosphere and troposphere; this phenomenon is also known as fading.. We assume that at every time slot, the channel of a primary belongs to one of the states 444We discretize the available transmission rates into a fixed number of states . This is a standard approximation to discretize the continuous function[6, 20]. The corresponding inaccuracy becomes negligible with increase in .. State provides a lower transmission rate to a secondary than state if and state arises when the channel is not available for sale i.e. secondaries can not use the channel when it is in state 555Generally a minimum transmission rate is required to send data. State indicates that the transmission rate is below that threshold due to either the excessive usage of subscribers of primaries or the transmission condition.. A channel is in state w.p. and in state w.p. where , independent of the channel states of other primaries 666We have shown that at a given slot, the channel state differs across the primaries mainly because of the differences of i) the number of subscribers that are using the channel and ii) the propagation conditions. Since different primaries have different subscriber bases, thus, their usage behaviors are largely uncorrelated. Also, channels of different primaries operate on different frequency bands and have different noise levels, thus, the propagation conditions are also uncorrelated across the channels.. Thus, the state of the channel of each primary is independent and identically distributed. We do not make any assumption on the relationship between and or and .777 Since each primary sells its channel to only one secondary, thus, referring to footnotes 2 and 3 transmission rate (or ) at a channel does not depend on (secondary demand) in practice.. We assume

| (1) |

We assume that the transmission rate offered by the channel of a primary is the same to all secondaries. We justify the above assumption in the following. We consider the setting where the secondaries are one of the following types: i) Service provider who does not lease spectrum from the FCC and serves the end-users through secondary access, ii) end-users who directly buy a channel from primaries. In initial stages of deployment of the secondary market, secondaries will be of the first type. When the secondaries are of the first type, then a primary would not know the transmission rate to the end-users who are subscribers of the service provider. A primary measures the channel qualities across different positions in the locality (e.g. a cell) and considers the average as the channel quality that an end-user subscribed to a secondary service provider will get at the location (e.g. a cell). This average will be identical across different end-users subscribed to different secondary service providers and hence, the channel quality is identical across the secondaries.

If the secondaries are of the second type, then the primary may know the transmission rate that an end-user will attain which may be different at different positions. However, if a primary needs to select a price for each position of the location, then it needs to compute the transmission rate at each possible position at that location (e.g. a cell). Thus, the computation and storage requirement for the primary would be large. Such position based pricing scheme will also not be attractive to the end-users since they may perceive it discriminatory as the price changes when its position changes within a location (e.g. a cell). Thus, such a position based pricing scheme may not be practically implementable. Hence, a primary estimates the channel quality and decides the price for the estimated channel quality by considering that the channel quality will not significantly vary across the location. This is because end-users who are interested to buy the channel from a primary at a location most likely have similar propagation paths: for example, secondary users who buy the channels are most often present in buildings (e.g. shopping complex, an office or residential area). The distance from the base station of the primary to the end-users is also similar because the end-users are close to each other in a location. Thus, the path loss component will also similar. Hence, the channel quality is considered to be identical across the secondaries.

Though the quality of a channel is identical for secondaries, the quality can vary across the channels. A primary can get an estimate of the transmission rate by sending a pilot test signal at different positions with the location and then, applying some standard estimation techniques[1].

II-A Penalty functions of Secondaries and Strategy of Primaries

Each primary selects a price for its channel if it is available for sale. We formulate the decision problem of primaries as a non-cooperative game. A primary selects a price with the knowledge of the state of its channel, but without knowing the states of the other channels; a primary however knows .

Secondaries are passive entities. They select channels depending on the price and the transmission rate a channel offers. We assume that the preference of secondaries can be represented by a penalty function. If a primary selects a price at channel state , then the channel incurs a penalty for all secondaries. As the name suggests, a secondary prefers a channel with a lower penalty. Since lower prices should induce lower penalty, thus, we assume that each is strictly increasing; therefore, is invertible. A primary selects a price for its available channel, but, since there is an one-to-one relation between the price and penalty at each state, we can equivalently consider that primaries select penalties instead. For a given price, a channel of higher transmission rate must induce lower penalty, thus, if . We can also consider that desirability of a channel for a secondary is the negative of penalty. A secondary will not buy any channel whose desirability falls below a certain threshold, equivalently, whose penalty exceeds a certain threshold. We consider that such threshold is the same for each secondary and we denote it as i.e. no secondary will buy any channel whose penalty exceeds . Secondaries have the same penalty function and the same upper bound for penalty value (), thus, secondaries are statistically identical.

Primary chooses its penalty using an arbitrary probability distribution function (d.f.) 888Probability distribution refers cumulative distribution function (c.d.f.). C.d.f. of a random variable is the function [4]. when its channel is in state . If (i.e., the channel is unavailable), primary chooses a penalty of : this is equivalent to considering that such a channel is not offered for sale as no secondary buys a channel whose penalty exceeds .

Definition 1.

A strategy of a primary for state , provides the penalty distribution it uses at each node, when the channel state is . denotes the strategy of primary , and denotes the strategy profile of all primaries (players). denotes the strategy profile of primaries other than .

II-B Payoff of Primaries

We denote as the inverse of . Thus, denotes the price when the penalty is at channel state . We assume that is continuous, thus is continuous and strictly increasing. Also, for each and . Each primary incurs a transition cost when the primary leases its channel to a secondary, and therefore never selects a price lower than .

If primary selects a penalty when its channel state is , then its payoff is

Note that if is the number of channels offered for sale, for which the penalties are upper bounded by , then those with lowest penalties are sold since secondaries select channels in the increasing order of penalties. The ties among channels with identical penalties are broken randomly and symmetrically among the primaries.

Definition 2.

is the expected payoff when primary ’s channel is at state and selects strategy and other primaries use strategy .

II-C Nash Equilibrium

We use Nash Equilibrium (NE) as a solution concept which we define below

Definition 3.

[23] A Nash equilibrium is a strategy profile such that no primary can improve its expected profit by unilaterally deviating from its strategy. So, with , , is an NE if for each primary and channel state

| (2) |

An NE is a symmetric NE if for all

An NE is asymmetric if for some .

Note that if , then primaries select the highest penalty with probability . This is because, when , then, the channel of a primary will always be sold. Henceforth, we will consider that .

II-D A Class of Penalty Functions

Since is strictly increasing in and for , we focus on penalty functions of the form , where and are strictly increasing in their respective arguments. Note that may be considered as a utility that a secondary would get at channel state when the price is set at . Such utility functions are commonly assumed to be concave [30]; which is possible only if is convex in i.e. is convex. It is easy to show that when and is convex, satisfies the following property:

Assumption 1

| (3) |

Moreover, when , then, the inequality in (3) is satisfied for some certain convex functions like . In addition, there is also a large set of functions that satisfy (3), such as: where is continuous and strictly increasing. Moreover, are such that the inverses are of the form , where is any strictly increasing function, satisfy Assumption 1. Henceforth, we only consider penalty functions which satisfy (3).

III One Shot Game: Structure, Computation, Uniqueness and Existence of NE

First, we identify key structural properties of a NE (should it exist). Next we show that the above properties lead to a unique strategy profile which we explicitly compute - thus the symmetric NE is unique should it exist. We finally prove that the strategy profile resulting from the structural properties above is indeed a NE thereby establishing the existence.

III-A Structure of an NE

We provide some important properties that any NE (where ) must satisfy. First, we show that each primary must use the same strategy profile (Theorem 1). In the sequel to this paper, we show that this is no longer the case when there are multiple locations. In fact we show that there may be multiple asymmetric NEs when there are multiple locations. We show that under the NE strategy profile a primary selects lower values of the penalties when the channel quality is high (Theorem 3). We have also shown that are continuous and contiguous (Theorem 2 and 4).

Theorem 1.

Each primary must use the same strategy i.e. and .

Theorem 1 implies that an NE strategy profile can not be asymmetric. Since channel statistics are identical and payoff functions are identical to each primary, thus this game is symmetric. Given that the game is symmetric, apparently there should only be symmetric NE strategies. Although there are symmetric games where asymmetric NEs do exist [5], we are able to rule that out in our setting using the assumptions that naturally arise in practice namely those which are stated in Sections II.A. and II.B and Assumption 1 which is satisfied by a large class of functions that are likely to arise in practice (Section II.E). Thus, a significance of Theorem 1 is that Theorem 1 holds for a large class of penalty functions which are likely to arise in practice. However, we show that there may exist asymmetric NE in absence of Assumption 1 (Section VI-B).

Now, we point out another significance of the above theorem. In a symmetric game it is difficult to implement an asymmetric NE. For example, for two players if is an NE with , then is also an NE due to the symmetry of the game. The realization of such an NE is only possible when one player knows whether the other is using or . But, coordination among players is infeasible apriori as the game is non co-operative. Thus, Theorem 1 entails that we can avoid such complications in this game. We show that this game has a unique symmetric NE through Lemma 2 and Theorem 5. Thus, Theorem 1, Lemma 2 and Theorem 5 together entail that there exists a unique NE strategy profile.

Since every primary uses the same strategy, thus, we drop the indices corresponding to primaries and represent the strategy of any primary as , where denotes the strategy at channel state . Thus, we can represent a strategy profile in terms of only one primary.

Definition 4.

is the expected profit of a primary whose channel is in state and selects a penalty 999Note that depend on strategies of other primaries , to keep notational simplicity, we do not make it explicit.

Theorem 2.

is a continuous probability distribution. Function is continuous.

The above theorem implies that does not have any jump at any penalty value. i.e. no penalty value is chosen with positive probability. We now intuitively justify the property. There are uncountably infinite number of penalty values and thus, clearly can only have jump at some of those values. Intuitively, there is no inherent asymmetry amongst the penalty values within the interval i.e. at the penalty values except the end points of the interval . Thus, a primary does not prioritize any of those penalty values. Now, we intuitively explain why does not have jump at the end points. First, at penalty , a primary gets a payoff of when the channel state is ; but the payoff at any penalty value greater that is positive, thus does not prioritize the penalty value . On the other hand, intuitively if a primary selects penalty with positive probability, then the rest would select slightly lower penalty in order to enhance their sales and thus, the probability that the primary would sell its channel decreases. Thus, also does not have a jump at .

Note that in a deterministic N.E. strategy at channel state , then must have a jump from to at the above penalty value. Such is not continuous. Thus, the above theorem rules out any deterministic N.E. strategy. The fact that is continuous has an important technical consequence; this guarantees the existence of the best response penalty in Definition 6 stated in Section III-B.

Definition 5.

We denote the lower and upper endpoints of the support set101010The support set of a probability distribution is the smallest closed set such that the probability of its complement is [4] of as and respectively i.e.

We next show that primaries select higher penalty when the transmission rate is low. More specifically, we show that upper endpoint of the support set of is upper bounded by the lower endpoint of .

Theorem 3.

, if .

Theorem 3 is apparently counter intuitive. We prove it using the assumptions stated in Section II. In particular, we rely on Assumption 1 which is satisfied by a large class of penalty functions (Section II-D). Thus, the significance of Theorem 3 is that the counter intuitive structure holds for a large class of penalty functions. However, in Section VI-C we show that Theorem 3 needs not to hold in absence of Assumption 1.

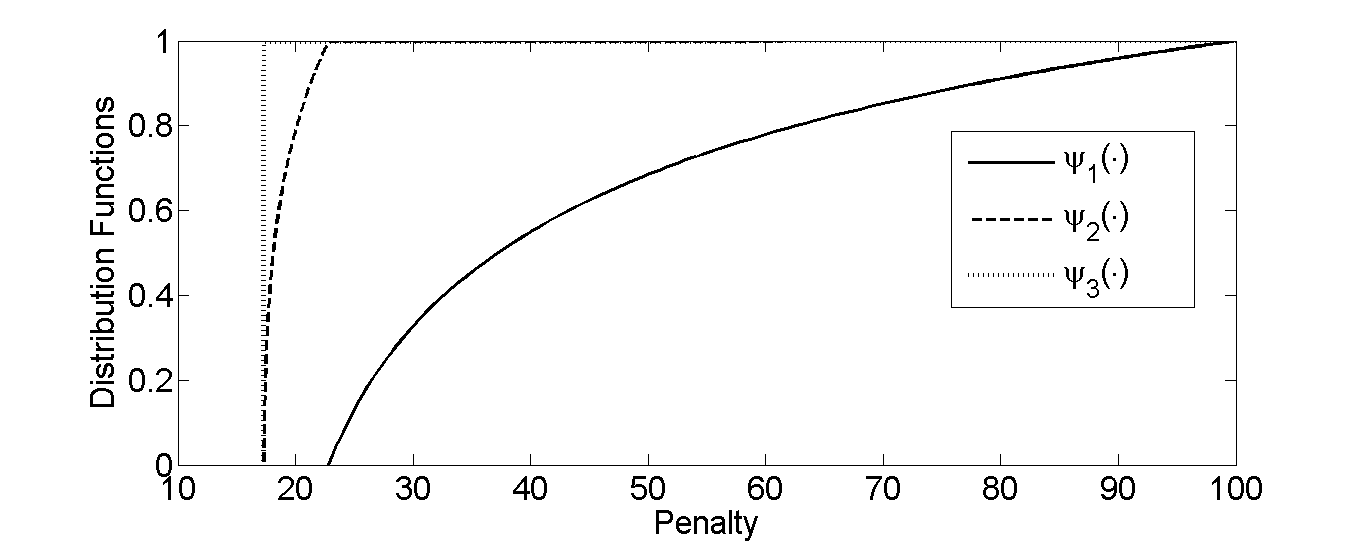

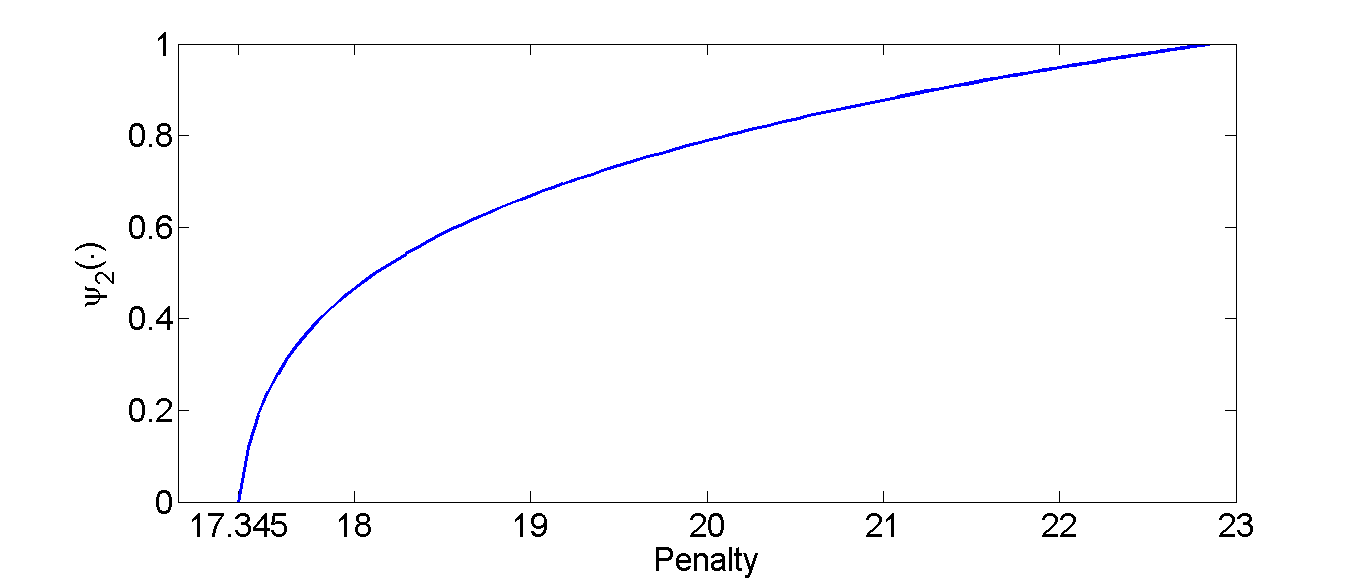

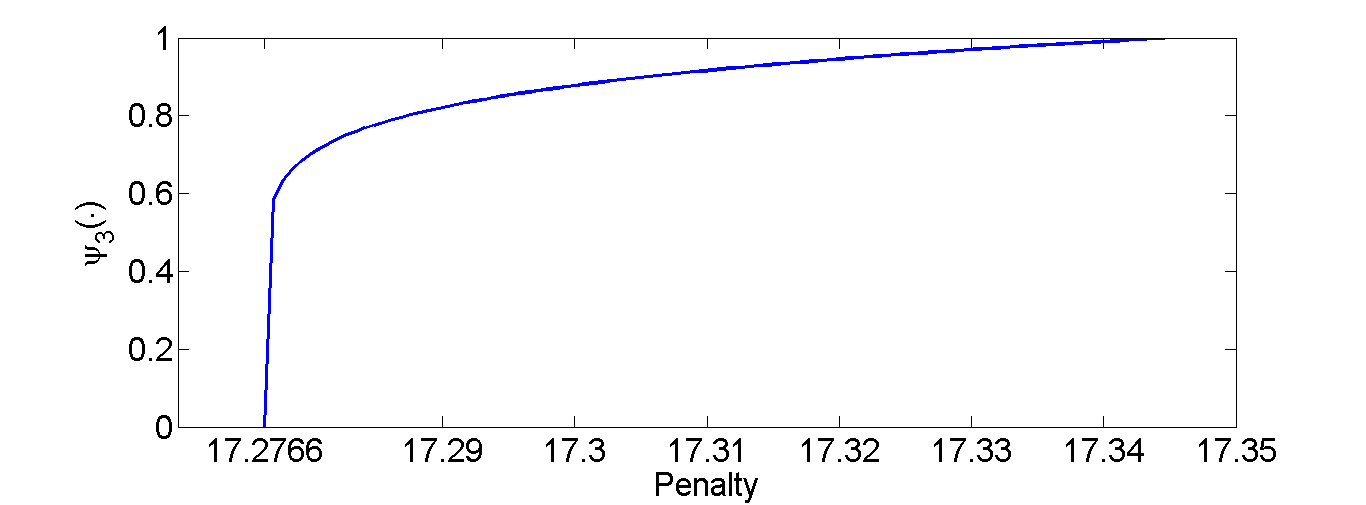

Fig. 1 illustrates s and s in an example scenario (The distribution in Fig. 1 is plotted using (2)).

In general, a continuous NE penalty selection distribution may not be contiguous i.e. support set may be a union of multiple number of disjoint closed intervals. Thus, the support set of may be of the following form with and . In this case, is strictly increasing in each of , but it is constant in the “gap” between the intervals i.e. is constant in the interval . We rule out the above possibility in the following theorem i.e. the support set of consists of only one closed interval which also establishes that is strictly increasing from to . In the following theorem we also rule out any “gap” between support sets for different , .

Theorem 4.

The support set of is and for , .

Theorem 3 states that . Theorem 4 further confirms that i.e. there is no “gap” between the support sets. Theorem 4 also implies that there is no “gap” within a support set. We now explain the intuition that leads to the reason. If there are and which are in the support sets such that the primaries do not select any penalty in the interval , then, a primary can get strictly a higher payoff at any penalty in the interval compared to penalty at or just below . Thus, a primary would select penalties at or just below with probability which implies that can not be in the support set of an NE strategy profile. We prove Theorem 4 using the above insights and Theorem 3.

Figure 1 illustrates d.f. for an example scenario.

III-B Computation, Uniqueness and Existence

We now show that the structural properties of an NE identified in Theorems 1-4 are satisfied by a unique strategy profile, which we explicitly compute (Lemma 2). This proves the uniqueness of a NE subject to the existence. We show that the strategy profile is indeed an NE in Theorem 5. We start with the following definitions.

Definition 6.

A best response penalty for a channel in state is if and only if

| (4) |

Let for a best response 111111Since is continuous by Theorem 2 and penalty must be selected within the interval , thus the maximum exists in (4). This maximum is equal to and is equal to for some . for state , i.e., is the maximum expected profit that a primary earns when its channel is in state , .

Remark 1.

In an NE strategy profile a primary only selects a best response penalty with a positive probability. Thus, a primary selects with positive probability at channel state , then expected payoff to the primary must be at .

Definition 7.

Let (, respectively) be the probability of at least successes out of independent Bernoulli trials, each of which occurs with probability (, respectively). Thus,

| (5) | |||||

| (6) |

The following lemma provides the explicit expression for the maximum expected payoff that a primary can get under an NE strategy profile.

Lemma 1.

For ,

| (7) | |||||

| (8) |

Remark 2.

Expected payoff obtained by a primary under an NE strategy profile at channel state is given by .

Remark 3.

We now obtain expressions for using expression of and . We use the fact that is strictly increasing and continuous in .

Lemma 2.

Remark 4.

The following lemma ensures that as defined in Lemma 2 is indeed a strategy profile.

Lemma 3.

as defined in Lemma 2 is a strictly increasing and continuous probability distribution function.

Fig. 1 illustrates continuous and strictly increasing for for an example setting.

Explicit computation in Lemma 2 shows that the NE strategy profile is unique, if it exists. There is a plethora of symmetric games [23] where NE strategy profile does not exist. However, we establish that any strategy profile of the form (2) is an NE.

Theorem 5.

Strategy profile as defined in Lemma 2 is an NE.

Hence, we have shown that

Theorem 6.

The strategy profile, in which each primary randomizes over the penalties in the range using the continuous probability distribution function (defined in Lemma 2) when the channel state is , is the unique NE strategy profile.

III-C Random Demand

Note that all our results readily generalize to allow for random number of secondaries (M) with probability mass functions (p.m.f.) . A primary does not have the exact realization of number of secondaries, but it knows the p.m.f. . We only have to redefine as-

and .

IV Performance Evaluations of NE Strategy Profile in Asymptotic Limit

In this section, we analyze the reduction in payoff under NE strategy profile due to the competition. First, we study the expected payoff that a primary obtains under the unique NE strategy profile in the asymptotic limit (Lemma 4). Subsequently, we compare the expected payoff of primaries under the NE strategy profile with the payoff that primaries get when they collude (Lemma 5). Subsequently, we investigate the asymptotic variation of strategy profiles of primaries with in an example setting (Fig. 4).

Recall from Remark 2 that expected payoff obtained by a primary under the unique NE strategy profile at channel state is given by . Next,

Definition 8.

Let denote the ex-ante expected profit of a primary at the Nash equilibrium. Then,

| (10) |

Note that denotes the total ex-ante expected payoff obtained by primaries at the NE strategy profile. We obtain

Lemma 4.

Let . When , then

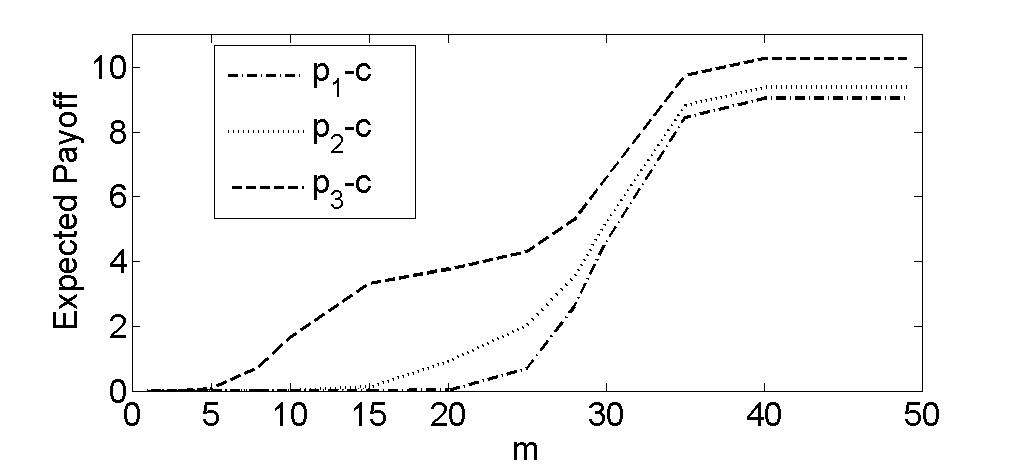

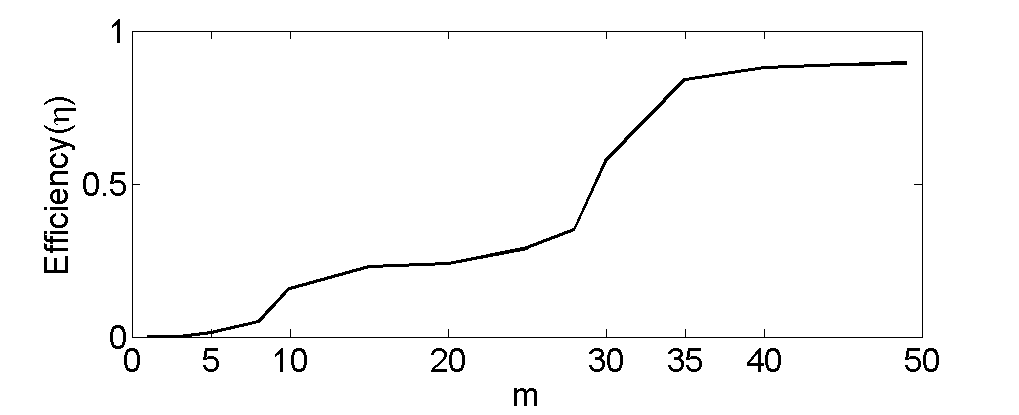

We illustrate Lemma 4 using an example in Figure 3. Intuitively, competition increases with the decrease in . Primaries choose prices progressively closer to the lower limit . Thus, the expected payoff decreases as decreases. The above lemma reveals that, as becomes smaller only those primaries whose channels provide higher transmission rate can have strictly positive payoff i.e. is positive (Fig. 3).

Corollary 1.

When , then,

Thus, asymptotically decreases as decreases (Fig. 3).

Definition 9.

Let be the maximum expected profit earned through collusive selection of prices by the primaries. Efficiency is defined as

Efficiency is a measure of the reduction in the expected profit owing to competition. The asymptotic behavior of is characterized by the following lemma.

Lemma 5.

When , then

We illustrate the variation of efficiency with using an example in Figure 3. Intuitively, the competition decreases with increase in ; thus primaries set their penalties close to the highest possible value for all states. This leads to high efficiency. On the other hand, competition becomes intense when decreases, thus, becomes very small as Corollary 1 reveals. But, if primaries collude, primaries can maximize the aggregate payoff by offering only the channels of highest possible states by selecting highest penalties. Thus, efficiency becomes very small when is very small (Fig. 3).

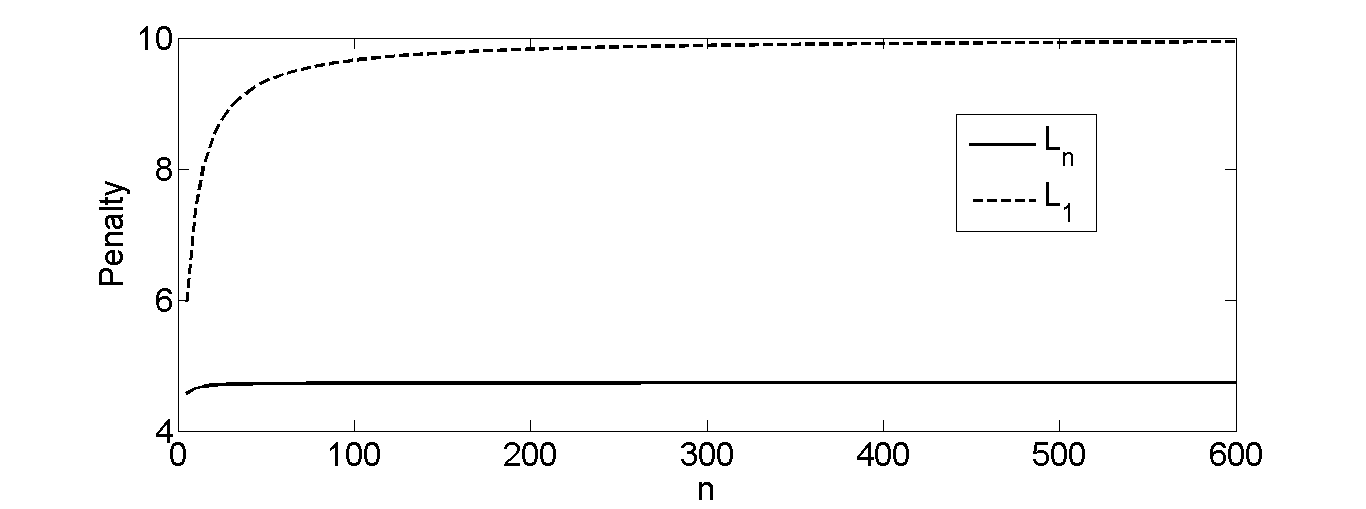

The transmission rates of an available channel constitute a continuum in practice. We have discretized the transmission rates of an available channel in multiple states for the ease of analysis. However, the theory allows us to investigate numerically how the penalty distribution strategies behave in the asymptotic limit (Fig. 4).

Fig. 4 reveals that increases with and eventually converges to a point which is strictly less than . On the other hand, converges to as becomes large (Fig. 4). Thus, the lower endpoints (and thus, the upper endpoints (since )) of penalty selection strategies converge at different points when becomes large.

V Repeated Game

We have so far considered the setting where primaries and secondaries interact only once. In practice, however, primaries and secondaries interact repeatedly. To analyze repeated interactions we consider a scenario where the one shot game is repeated an infinite number of times. We characterize the subgame perfect Nash Equilibrium where the expected payoff of primaries can be made arbitrarily close to the payoff that primaries would obtain if they would collude.

The one shot game is played at time slots . Let, denote the expected payoff at stage , when the channel state is . Hence, the payoff of a primary, when its channel state is , is given by

| (11) |

where, is the discount factor.

Since NE constitutes a weak notion in repeated game [23], we will focus on Subgame Perfect Nash Equilibrium (SPNE).

Definition 10.

[23] Strategy profile constitutes a SPNE if the strategy profile prescribes an NE at every subgame.

The one shot unique NE that we have characterized, is also a SPNE in repeated game. Total expected payoff that a primary can get, is (Definition 8) under one-shot game. We have already shown that this payoff is not always efficient (Lemma 5) i.e. . Here, we present an efficient SPNE (Theorem 7), provided that is sufficiently high.

Fix a sequence of such that

| (12) | |||

| (13) |

We provide a Nash Reversion Strategy such that a primary will get a payoff arbitrarily close to the payoff that it would obtain when all primaries collude.

Strategy Profile ():

Each primary selects penalty , (where satisfies (12) and (13)), when state of the channel is , at and also at time slot as long as all other primaries have chosen , , when their channel state is at all time slots . Otherwise, play the unique one shot game NE strategy (Lemma 2).

Remark 5.

Note that if everyone sticks to the strategy, then each primary selects a penalty of at every time slot, when the channel state is . Under the collusive setting, each primary selects penalty . Thus, for every , we can choose sufficiently small and sufficiently high such that the efficiency (definition 9) is at least .

Now we are ready to state the main result of this section.

Theorem 7.

Remark 6.

Thus, there exists a SPNE strategy profile (for sufficiently high ) where each primary obtains an expected payoff arbitrarily close to the payoff it would have obtained if all primaries collude.

VI Pending Question: What happens when Assumption 1 is relaxed?

We show that if penalty functions do not satisfy Assumption 1, then the system may have multiple NEs (section VI-A), asymmetric NE (section VI-B) and the strategy profile that we have characterized in (2) may not be an NE (section VI-C).

VI-A Multiple NEs

We first give a set of penalty functions which do not satisfy Assumption 1 and then we state a strategy profile which is an NE for this set of penalties along with the strategy profile that we have characterized in (2).

Let be such that

| (14) |

Examples of such kind of functions are .

It can be easily verified that strategy profile, described as in (2), is still an NE strategy profile under the above setting. We will provide another NE strategy profile.

First, we will introduce some notations which will be used throughout this section.

| (15) | |||

| (16) |

Now, we show that there exists a symmetric NE strategy profile where a primary selects the same strategy for its each state of the channel. This establishes that the the system has multiple NEs.

Let’s consider the following symmetric strategy profile where at channel state a primary’s strategy profile is for , where

| (17) |

First, we show that is a probability d.f.

Lemma 6.

as defined in (VI-A) is a probability distribution function.

Note that in this strategy profile each primary selects the same strategy irrespective of the channel state. Next, we show that strategy profile as described in (VI-A) is an NE strategy profile.

Theorem 8.

Consider the strategy profile where , for . This strategy profile constitute an NE.

VI-B Asymmetric NE

If Assumption 1 is not satisfied, then there may exist asymmetric NEs in contrast to the setting when Assumption 1 is satisfied. We again consider the penalty functions are of the type given in (14). We consider and . Here, we denote as the strategy profile for primary at channel state , . Let

| (18) |

Note from (18) that

| (19) |

Next

| (20) |

Again using (14) and the fact that we also obtain

| (21) |

Consider the following strategy profile

| (22) |

and

| (23) |

It is easy to discern that the above strategy profile is a continuous distribution function. Also note that and . Hence, the strategy profile is asymmetric. The following theorem confirms that the strategy profile that we have just described is indeed an NE.

The above theorem confirms that there may exist an asymmetric NE when the penalty functions are of the form (14).

VI-C Strategy Profile Described in (2) may not be an NE

We first describe a set of penalty functions that do not satisfy (3) and then we show that the strategy profile that we have characterized in (2) is not an NE. 121212Note that in theorem 5 we have shown that the strategy profile described in (2) is an NE when (3) is satisfied

Consider that ; penalty functions are as follow:

| (24) | |||

| (25) |

Now, as , hence

| (26) |

From (VI-C), it is clear that for , is strictly decreasing. Hence we have for

| (27) |

which contradicts (3).

Now, let and . Under this setting, we obtain

Theorem 10.

The strategy profile as defined in (2) is not an NE strategy profile.

Remark 7.

In the example constructed above, however, an NE strategy profile may still exist. Now, we show that in certain cases we can have a symmetric NE where . Thus, when channel state is and , a primary chooses penalty from the interval and respectively. (Note the difference; in the strategy profile described in lemma 2, we have ). Consider the following symmetric strategy profile where each primary selects strategy at channel state , -

| (28) |

with , .

and

| (29) |

When , ; we obtain .

It is easy to show that as defined in (VI-C) is distribution function with and . Note that under , a primary selects penalty from the interval and when the channel states are and respectively. So, it remains to show that it is an NE strategy profile. The following theorem shows that it is indeed an NE strategy profile.

Theorem 11.

Strategy profile as described in (VI-C) is an NE .

VII Conclusion and Future Work

We have analyzed a spectrum oligopoly market with primaries and secondaries where secondaries select a channel depending on the price quoted by a primary and the transmission rate a channel offers. We have shown that in the one-shot game there exists a unique NE strategy profile which we have explicitly computed. We have analyzed the expected payoff under the NE strategy profile in the asymptotic limit and compared it with the payoff that primaries would obtain when they collude. We have shown that under a repeated version of the game there exists a subgame perfect NE strategy profile where each primary obtains a payoff arbitrarily close to the payoff that it would have obtained if all primaries collude.

The characterization of an NE strategy profile under the setting i) when secondaries have different penalty functions and ii) when demand of secondaries vary depending on the pricing strategy remains an open problem. The analytical tools and results that we have provided may provide the basis for developing a framework to solve those problems.

References

- [1] S.E. Bensley and B. Aazhang. Subspace-based channel estimation for code division multiple access communication systems. Communications, IEEE Transactions on, 44(8):1009–1020, Aug 1996.

- [2] Thomas M. Cover and Joy A. Thomas. Elements of Information Theory. Wiley, 2nd edition, 2006.

- [3] Lingjie Duan, Jianwei Huang, and Biying Shou. Competition with dynamic spectrum leasing. In New Frontiers in Dynamic Spectrum, 2010 IEEE Symposium on, pages 1–11, April 2010.

- [4] B.S. Everitt. The Cambridge Dictionary of Statistics. 3rd Edition, Cambridge University Press, 2006.

- [5] Mark Fey. Symmetric games with only asymmetric equilibria. Games and Economic Behavior, 75(1):424 – 427, 2012.

- [6] R.F.H. Fischer and J.B. Huber. A new loading algorithm for discrete multitone transmission. In Global Telecommunications Conference, 1996. GLOBECOM ’96., volume 1, pages 724–728 vol.1, Nov 1996.

- [7] A. Ghosh and S. Sarkar. Quality sensitive price competition in spectrum oligopoly. In Proceedings of IEEE International Symposium on Information Theory (ISIT), pages 2770–2774, 2013 (Proofs are available at http://arxiv.org/abs/1305.3351).

- [8] Arnob Ghosh and Saswati Sarkar. Quality sensitive price competition in spectrum oligopoly: Part 1. CoRR, abs/1404.2514, 2014.

- [9] W. Hoeffding. Probability inequalities for sums of bounded random variables. Journal of the American Statistical Institute, 58, 1963.

- [10] O. Ileri, D. Samardzija, T. Sizer, and N. B. Mandayam. Demand Responsive Pricing and Competitive Spectrum Allocation via a Spectrum Policy Server. In IEEE Proceedings of DySpan, pages 194–202, 2005.

- [11] M. Janssen and E. Rasmusen. Bertrand Competition Under Uncertainty. Journal of Industrial Economics, 50(1):11–21, March 2002.

- [12] Juncheng Jia and Qian Zhang. Bandwidth and price competitions of wireless service providers in two-stage spectrum market. In Communications, 2008. ICC ’08. IEEE International Conference on, pages 4953–4957, May 2008.

- [13] G.S. Kasbekar and S. Sarkar. Spectrum Pricing Game with arbitrary Bandwidth Availability Probabilities. In Proceeding of IEEE International Symposium on Information Theory (ISIT), pages 2711–2715, 2011.

- [14] G.S. Kasbekar and S. Sarkar. Spectrum Pricing Game with Bandwidth Uncertainty and Spatial Reuse in Cognitive Radio Network. IEEE Journal on Special Areas in Communication, 30(1):153–164, 2012.

- [15] Alanyali M. Kavurmacioglu, E. and D. Starobinski. Competition in secondary spectrum markets: Price war or market sharing? In IEEE Proceedings of DYSPAN.

- [16] Hyoil Kim, Jaehyuk Choi, and K.G. Shin. Wi-fi 2.0: Price and quality competitions of duopoly cognitive radio wireless service providers with time-varying spectrum availability. In INFOCOM, 2011 Proceedings IEEE, pages 2453–2461, April 2011.

- [17] S. Kimmel. Bertrand Competition Without Completely Certain Productions. Economic Analysis Group Discussion Paper, Antitrust Division, U.S. Department of Justice, 2002.

- [18] D.M. Kreps and J.A. Scheinkman. Quantity Precommitment and Bertrand Competition yield Cournot Outcomes. Bell Journal of Economics, 14:326–337, Autumn, 1983.

- [19] Peng Lin, Juncheng Jia, Qian Zhang, and M. Hamdi. Dynamic spectrum sharing with multiple primary and secondary users. Vehicular Technology, IEEE Transactions on, 60(4):1756–1765, May 2011.

- [20] Zhi-Quan Luo and Shuzhong Zhang. Dynamic spectrum management: Complexity and duality. Selected Topics in Signal Processing, IEEE Journal of, 2(1):57–73, Feb 2008.

- [21] P. Maille and B. Tuffin. Analysis Of Price Competition in a Slotted Resource Allocation Game. In Proceeding of 27th IEEE INFOCOM, pages 888–896, 2008.

- [22] P. Maille and B. Tuffin. Price War with Partial Spectrum Sharing for Competitive Wireless Service Provider. In Proceeding Of IEEE GLOBECOM, pages 1–6, 2009.

- [23] A. Mas Colell, M. Whinston, and J. Green. Microeconomic Theory. Oxford University Press, 1995.

- [24] D. Niyato and E. Hossain. Competitive Pricing for Spectrum Sharing in Cognitive Radio Network: Dynamic Games, Inefficiency of Nash Equilibrium, and Collusion. IEEE Journal on Special Areas in Communication, 26(1):192–202, 2008.

- [25] D. Niyato, E. Hossain, and Z. Han. Dynamics of Multiple Seller and Multiple Buyer Spectrum Trading in Cognitive Radio Network: A Game theoretic Modeling approach. IEEE Transaction on Mobile Computing, 8(8):1009–1022, 2009.

- [26] M.J. Osborne and C. Pitchik. Price Competition in a Capacity Constrained Duopoly. Journal On Economic Theory, 38(2):238–260, 1986.

- [27] Sheldon Ross. A First Course in Probability. 8th Edition, Prentice Hall, 2009.

- [28] W. Rudin. Principles Of Mathematical Analysis. Third Edition, Mc-Graw Hill, 1976.

- [29] S. Sengupta and M. Chatterjee. An economic framework for dynamic spectrum access and service pricing. Networking, IEEE/ACM Transactions on, 17(4):1200–1213, Aug 2009.

- [30] G. Song and Ye Li. Utility-based resource allocation and scheduling in ofdm-based wireless broadband networks. Communications Magazine, IEEE, 43(12):127–134, Dec 2005.

- [31] Yi Tan, S. Sengupta, and K.P. Subbalakshmi. Competitive spectrum trading in dynamic spectrum access markets: A price war. In Global Telecommunications Conference (GLOBECOM 2010), 2010 IEEE, pages 1–5, Dec 2010.

- [32] Y. Xing, R. Chandramouli, and C. Cordeiro. Price Dynamics in Competitive Agile Spectrum Access Markets. IEEE Journal on Special Areas in Communication, 25(3):613–621, 2008.

- [33] Hong Xu, Jin Jin, and Baochun Li. A secondary market for spectrum. In INFOCOM, 2010 Proceedings IEEE, March 2010.

- [34] Lei Yang, Hongseok Kim, Junshan Zhang, Mung Chiang, and Chee wei Tan. Pricing-based spectrum access control in cognitive radio networks with random access. In INFOCOM, 2011 Proceedings IEEE, pages 2228–2236, April 2011.

- [35] Feng Zhang and Wenyi Zhang. Competition between wireless service providers: Pricing, equilibrium and efficiency. In Modeling Optimization in Mobile, Ad Hoc Wireless Networks (WiOpt), 2013 11th International Symposium on, pages 208–215, May 2013.

- [36] X. Zhou and H. Zheng. TRUST: A General Framework for Truthful Double Spectrum Auctions. In In the Proceedings of Infocom, April 2009.

-A Proof of the results of Section III-A

We first state Lemma 7, 8 and 9 in order to prove Theorem 1. Theorem 2 readily follows from Lemma 7. After that we show Corollary 3 which we use to prove theorems 3 and 4.

Now, we introduce some notations which we use throughout this section.

Definition 11.

Let denote the probability of winning of primary when it selects penalty .

Let denote the probability of at least success out of (except ) independent Bernouli event with event has success probability of .

Note that does not depend on the state of the channel since secondaries select the channels based only on the penalties. Since secondaries prefer channels which induce lower penalty thus is non-increasing function. Note that is strictly increasing in each component. Note also that

| (30) |

If primary selects penalty at channel state , then its expected payoff is

| (31) |

Definition 12.

A Best response penalty for primary at channel state is

Let denote the maximum expected payoff under NE strategy profile for primary at channel state i.e. is equal to the payoff at at channel state if is a best response for primary at channel state .

A primary only selects penalty with positive probability at channel state , if is a best penalty response at . We state an observation that we will use throughout:

Observation 1.

Any penalty can not be a best response (definition 6) for channel state .

Proof.

Note that the profit of a primary is non-positive if the selected penalty is upper bounded by . On the other hand when a primary selects penalty where , it can sell its channel at least in the event when the total number of available channels are less than . Since by (1), thus the event occurs with non-zero probability, hence the profit is strictly positive when . Hence, the result follows. ∎

We denote throughout this section for a function . Now we are ready to show Lemma 7.

Lemma 7.

is continuous at all points, except possibly at . Also, at most one primary can have a jump at .

Proof.

Let has a jump at where and . Thus, is a best response for primary at channel state . Next, we show that no player other than player will select penalty in the interval with positive probability for small enough .

Fix a player and channel state .

First, note that if , then a player can not select penalty in the interval with positive probability where since a primary gets a payoff of at least at penalty . Note that , thus . We need to consider states such that .

The payoff that player will get at a channel state at a is

| (32) |

For any , expected payoff for player at at channel state is lower bounded by

| (33) |

Since has a jump at , thus . Hence, by continuity of there exists a and small enough such that for every we have

Thus, player has strictly higher payoff at compared to at penalty .

Hence, no player apart from selects penalty in the interval with positive probability where .

Since no player apart from player select penalty in the interval , thus player will have a strictly higher payoff at instead of which contradicts the fact that is a best penalty response for player .

If player selects with positive probability, then player will have strictly higher payoff by selecting a penalty just below . Hence, player will select with probability. Hence, the result follows. ∎

We introduce some notations which we use throughout this section:

Definition 13.

Let be the th lowest penalty selected by primaries except .

Note that if primary selects penalty , then it will not be able to sell its channel if . Now we show some results which directly follow from Lemma 7. We use these results to prove Theorem 1.

Observation 2.

If does not have jump at apart from ( may or may not have jump at ), then

| (34) |

Proof.

Note that

| (35) |

where is the probability that primary will be selected by secondaries when . If does not have any jump at , then,

| (36) |

On the other hand note that the probability of the event that primary selects penalty less than or equal to is given by , hence, is given by

| (37) |

where . Thus, if does not have jump at for all and , then (2) follows from (35), (36) and (37). ∎

By Lemma 7 no primary has a jump at . Thus, is exactly given by (2) when . By Lemma 7, only one player can have a jump at . Thus, if player have a jump at , then by Observation 2, . Hence, the following corollary is a direct consequence of (2).

Corollary 2.

iff and iff for and for if no primary has a jump at . If primary has a jump at , then .

Definition 14.

Let

| (38) | |||

| (39) |

are respectively the lowest and upper endpoint of support set of .

Lemma 8.

i ) is a best response for primary at channel state .

ii) is a best response for primary at channel state , if one of the followings is true:

a) .

b) and no primary has a jump at .

c) and only primary has a jump at .

Proof.

We prove part (i). The proof of part (ii) is similar and hence we omit.

We prove part (i) by considering the following two scenarios:

Case i: : Note that . Thus, by (38), has a jump at ; thus, is a best response to primary at channel state .

Case ii: : By Lemma 7, no primary has a jump at and thus is continuous at . Thus, by (38), primary selects a penalty just above with positive probability when the channel state is i.e. for every there exists such that is a best response to primary at channel state . Then, we must have a sequence such that each is a best response for primary at channel state and . But profit to primary at channel state is . Now from continuity of and at we obtain

| (40) |

Since each is a best response, thus, is also a best response. ∎

Lemma 9.

if

Proof.

Fix a primary . We first show that for any such that , if is a best response when the state of the channel is , then can not be a best response when the state of the channel is where . If not, consider such that are the best responses when channel states are respectively . Since is a best response at channel state , thus by Observation 1. On the other hand, since is a best response at channel state , thus, by Observation 1. Since , thus . Also,

| (41) |

Expected payoff to primary at channel state at is . Thus, from (41)

| (42) |

Since is a best response to primary at channel state , thus

Expected payoff of primary at channel state at penalty is

| (43) |

Using (42) and (43), we obtain-

| (44) |

which contradicts Definition 12.

We also obtain from the argument in the above paragraph, if is a best response then .

If is not a best response then by Lemma 8, and there exists a primary other than which has a jump at . Thus, by Lemma 7, primary does not have a jump at . Thus, is continuous and thus, by the definition of (39) for every , there exists such that is a best response for primary at channel state . Hence, if , then there exists a such that is a best response for primary for state . But, we have already shown that it is not possible. Hence, the result follows. ∎

Proof of Theorem 1: Suppose the statement is not true. Thus, we must have which do not have identical strategy. Let, be the largest index in such that and differs. Thus, we must have

If , then since for any . Hence, we must have .

Note that by definition of , . Since , thus and are continuous at by Lemma 7, thus, . Hence, for all . By definition of , and can not differ at a penalty less than and thus . Thus and , hence by Lemma 9. Since for all and are exactly the same for each primary, thus, by Corollary 2

| (45) |

By definition of , for every , there is a such that and . Without loss of generality, we assume that for every in for some . Thus, for every . We consider the following two possible scenarios:

Case i: for every .

Hence, there is a , such that , is a best response for primary at channel state and . Since and for every ; and no primary has a jump at , thus, is also a best response for primary and primary at channel state . But, expected payoff to primary at at channel state is

| (46) |

Since is a best response for primary at channel state , thus,

| (47) |

Since and (since ) by Lemma 9 for all , thus, . Thus, from Corollary 2 . Thus, expected payoff at is

| (48) |

Since and are best response to primary at channel state , thus expected payoff to primary at channel state at and must be equal. But, this leads to a contradiction from (-A) and (46).

Case ii: for some :

Let . Note that . We consider two possible scenarios:

Case ii a: :

Since no primary has a jump at by Lemma 7, thus, by definition of , it is a best response for primary at channel state . But expected payoff to primary at channel state at is given by

| (49) |

Since , thus, , thus, by Lemma 9. Since for every , thus, , hence . Since , thus, for all . If for some , then differs from (since for all ) at least at , but this is against the definition of . Hence, . Since and for all ,thus, . Thus, by Corollary 2, . Since is a best response for player at channel state , thus

| (50) |

Hence,

which contradicts the fact that is a best response for player when the channel state is .

case ii b: :

Since must be and . Hence, must have a jump at and thus is a best response to primary when the channel state is . Thus, by Corollary 2, . Thus, by the continuity of , penalties close to is also a best response for primary at channel state i.e.

| (51) |

Since by the definition of , thus, similar to argument in case ii a, we obtain for , i.e. there exists an , but (by (51)). Thus, there exists an , such that

| (52) |

Note that the right hand side is the expression for the expected payoff of primary at channel state at penalty . Since is a best response to primary at channel state , thus,

which contradicts that is a best response for primary at channel state . Hence, . Hence, this case does not arise.

Thus from case i, case ii.a, and case ii.b we obtain the desired result. ∎

Henceforth, we denote and as and respectively by dropping the index corresponding to primary . Note from Definition 4 that

| (53) |

Also note that and for all . Since strategy profiles of primaries are identical, thus, we can consider strategy profile in terms of only one primary (say, primary ).

Proof of Theorem 2: By Lemma 7 does not have a jump at . If a primary has a jump at , then by symmetric property other primaries also have a jump at , which is not possible by Lemma 7 since . Thus, does not have a jump for any .

Now, we show that is continuous. Now, we provide a closed form expression for using (53). Since , thus, from Observation 2, (30) and Theorem 2 the expected payoff for primary at at channel state is given by

The continuity follows from the equation due to the continuity of (Definition 7) and . ∎

We obtain

| (54) |

Now, we show a corollary which is a direct consequence of Theorem 2. We use this result to prove Theorems 3 and 4.

Corollary 3.

Every element in the support set of is a best response131313Note that in general every element of a support set need not be a best response. To illustrate the fact consider a 3 player non co-operative game and the following NE strategy profile: players 1 and 2 have identical strategy profile which is a uniform distribution from and player 3 selects with probability . Since the support set is closed, thus is in the support set for players and . But, players and will attain strictly higher payoff at just below compared to at . Thus, is not a best penalty response for players and. We show that this is not the case here because of the continuity of strategy profile. Specifically, a primary attains the highest possible expected payoff at every penalty in the support set in our setting.; thus, so are .

Proof.

Suppose that there exists a point in the support set of , which is not a best response. Therefore, primary 1 plays at with probability when the channel state is .

Now, one of the following two cases must arise.

Case I: a neighborhood [28] of radius around , such that no point in this neighborhood is a best response. Neighborhood of radius of is an open set (Theorem 2.19 of [28]). Hence, we can eliminate that neighborhood and can attain a smaller closed set, such that its complement has probability zero under , which contradicts the fact that is in the support set of .

Case II: For every , , such that is a best response. Then, we must have a sequence such that each is a best response, and [28]. But profit to primary 1 for channel state at each of is by (54). Thus, we can show that is also a best response from the continuity of ad . We can conclude the result by noting that (Definition 5) are in the support set of .

∎

Remark 8.

By corollary 3, at any channel state , a primary attains the same expected payoff () at every point in the support set.

Proof Of Theorem 4: Suppose the statement is not true. But, it follows that there exists an interval , such that no primary offers penalty in the interval with positive probability. So, we must have such that

By definition of , is a best response for at least one state . But, as no primary offers penalty in the range , so from (54), for each . This is because and . Thus, can not be a best response for state i.∎

-B Proof of Results of Section III-B

Proof of Lemma 1: We first outline a recursive computation strategy that leads to the expressions in (7) and (8).

Using Theorem 4, we have and thus is a best response at channel state (Corollary 3). If a primary chooses penalty then it sells only when , this allows us to compute . By Theorem 4, primaries with channel states choose penalty below and primaries with channel state select penalty greater than with probability . This allows us to calculate the payoff at which must be equal to . The above equality allows us to compute the expression for .

Since (Theorem 4) and is a best response at channel state , which enables us to obtain the expression for . By Theorem 4 primaries with channel states choose penalty below and primaries with channel state and select penalty greater than with probability . This allows us to calculate the payoff at which must be equal to . The above equality allows us to compute the expression for . Using recursion, we can get the values of , . The detailed argument follows:

From theorem 4, ’s support set is for and for Thus, is a best response for channel state 1 (by Corollary 3), hence

Thus, (7) holds for with . Let, (7) be true for . We have to show that (7) is satisfied for assuming that it is true for . Thus,by induction hypothesis,

| (55) |

Now, is a best response for state , and thus,

Now, as is also a best response for state by Corollary 3, thus

Thus, and it satisfies (7). Thus, (7) follows from mathematical induction.

(8) follows since and is the inverse of ∎

Proof of Lemma 2: By Theorem 4, are respectively the lower end-point and the upper end-point of the support set of . We should have for , and for ,. From Corollary 3, every point is a best response for state , and hence,

Thus, the expression for follows. We conclude the proof by noting that the domain and range of is , and for : so is defined at . ∎

Proof of Lemma 3: Note that

is continuous, strictly increasing on compact set , so is also continuous (theorem 4.17 in [28]). Also, is continuous for as , so is continuous as it is a composition of two continuous functions. Again, is strictly increasing (as is strictly increasing), is strictly increasing (as is strictly increasing), so is strictly increasing on ( as it is a composition of two strictly increasing functions (Theorem 4.7 in [28]))∎.

First, note that as , thus, . Hence, from (8) it is evident that

| (56) |

Observation 3.

For

| (57) |

Proof.

Proof of Theorem 5: Fix a state . First, we show that if a primary follows its strategy profile then it would attain a payoff of at channel state . Next, we will show that if a primary unilaterally deviates from its strategy profile, then it would obtain a payoff of at most of (Case i and Case ii) when the channel state is .

If the state of the channel of primary 1 is and it selects penalty , then its expected profit is-

| (60) |

First, suppose . From (-B) and (2), we obtain

| (61) |

Since , we have

| (62) |

From (62) expected payoff to a primary at state at is . At any expected payoff to a primary at state will be strictly less than . Hence, it suffices to show that for , profit to primary 1 is at most , when the channel state is .

Now, let . From (-B) and (2), expected payoff at

| (63) |

We will show that is non-positive. As, , so only the following two cases are possible.

Case i: :

From (3), (56) and for , we have-

| (64) |

From Observation 3 we obtain-

Using (64) the above expression becomes

| (65) |

Hence, from (-B) and (-B), we obtain-

| (66) |

Since , and (by (56)); hence, from (-B) and Assumption 1, we have-

| (67) |

Case ii: : If then a primary gets a non-positive payoff at channel state , which is strictly below . Hence we consider the case when . Since thus . Now, if and , we have from (3) and (56)-

| (68) |

Since , thus

| (69) |

Now, from Observation 3 we obtain-

| (70) |

Thus, from (-B) and (-B), we obtain-

| (71) |

Hence, from (-B), (67), and (-B), every is a best response to primary 1 when channel state is . Since is arbitrary, it is true for any and thus (2) constitutes a Nash Equilibrium strategy profile.∎

-C Proof of results of Section IV

Proof of Lemma 4: We divide the proof in three parts:

-

•

First, we prove that when for some , then as (Part I).

-

•

Next we show that if for some , then if and if (Part II).

-

•

Finally, we show if for some , then as for any (Part III).

Part I: Suppose for some .

Since , thus, from (7)-

| (72) |

When primary 1 selects penalty at channel state , then its expected profit is . Now, from Theorem 6 under the NE strategy profile,

| (73) |

Let be Bernoulli trials with success probabilities and ; so is equal to by (6). Since for some and , by weak law of large numbers [27], as . Hence, as by (72) and (73).Thus, the result follows.∎.

Part II:

We show the result by evaluating the expressions for in the asymptotic limit. Towards this end, we first evaluate the expressions for and in the asymptotic limit. We obtain the expression for when we combine those two values.

Suppose for some . Since is the probability of at least successes out of independent Bernoulli trials, each of which occurs with probability (by (6)). Hence from the weak law of large numbers [27]

| (74) |

Since , for any (from (6)), we have from (74) for

| (75) |

Again, as , so, from weak law of large numbers[27], for every , , such that , whenever . Hence,

| (76) |

Thus, it is evident from (7) and (-C) that if , then

| (77) |

Thus, from (8), (75), and (77)

| (78) |

We obtain for from (7) and (75)

| (79) |

Again, using (8) and (75), we obtain for

| (80) |

is strictly increasing, thus from (79) and (80), (for ). Hence, for ,

| (81) |

Thus, from (-C), and (80), we obtain for any

| (82) |

Thus, from (77) as if . From (82) we obtain as if . Hence, the result follows.∎

Part III: Suppose that , for some . Let, be the Bernoulli trials with success probabilities and , . Hence,

| (83) | |||||

Note that (if ), . Hence, it can be readily seen from (7) that

| (84) |

Thus, for , , from (83) and (85), we obtain.

| (86) |

where . We will use this bound in proving Lemma 5.

From, the definition of , it should be clear that

| (87) |

Now, we show Lemma 5

Proof of Lemma 5: We divide the proof in the following two parts

-

•

First, we show that if for some , then as (Part I).

-

•

Next, we show that if , for some , then as (Part II).

Part I: First suppose that for some .

From, definition of , it is obvious that

| (88) |

Part II: Now, suppose that , for some . We prove that as .

We prove the result by showing that decreases at fast rate to compared to when .

Let, be the number of primaries, whose channel is in state . Hence,

| (89) |

Note that , .

We introduce a new random variable as follows-

So,

| (90) |

Hence, from (86), (-C) and (-C), we obtain-

Thus, tends to zero for ,as tends to infinity (as ).∎

-D Proof of Results of Section VI

First, we prove Lemma 6. Subsequently, we state and prove Observation 4 which we use to show Theorem 8. The proof of Theorem 9 is similar and hence we omit it. Finally, we show Theorems 10 and 11.

Proof of Lemma 6: First , it is evident from (15) and (16)

Hence, is defined at . Note that

Note that

We already know that is continuous and strictly increasing. Since is strictly increasing and continuous for . Hence, is continuous and strictly increasing on . ∎.

Observation 4.

| (91) |

Proof.

Proof of Theorem 8: We show that for any , a primary attains a payoff of at channel state . Then, we will show that if a primary selects a penalty outside the interval a primary’s payoff is strictly less than at channel state .

Suppose, . Now, fix any channel state . If primary 1 selects penalty at channels state , then its expected payoff is

| (92) |

Now, at any , expected payoff will be strictly less than . But, from Observation 4, .

Thus, from (-D), when channel state is , every point in the interval is a best response to primary 1. Hence, the result follows.∎

Proof of Theorem 10: By simple calculation, we obtain the following values

Now, consider the following unilateral deviation for primary 1: primary 1 will choose a penalty with probability 1, when the channel state is . Since, no primary selects penalty lower than under the strategy profile (2), thus expected payoff that primary 1 will obtain is , which is strictly larger than (since ), the expected payoff that primary 1 gets by Theorem 6 when it selects strategy according to (2). Thus, the strategy profile as defined in (2) is not an NE.∎

Proof of Theorem 11:

We show that when the channel state is a primary does not have any profitable unilateral deviation from the strategy profile. The proof for is similar and thus we omit it.

First, we show that under the strategy profile a primary attains a payoff of at channel state . Next, we show that if a primary deviates at channel state , then its expected payoff is upper bounded by .

Note that when channel state is and primary chooses penalty , expected payoff to primary 1 is-

| (93) |

Now, suppose . From (-D), expected payoff to a primary when it selects penalty at channel state , is-

| (94) |

Note that at , . Hence, the expected payoff to a primary when it selects penalty at channel state is given by . From (-D) we obtain , hence any penalty will induce payoff of strictly lower than when channel state is . Hence, the result follows.∎

-E Proof of Results of Section V

First, we evaluate the total expected payoff that a primary will get under the strategy profile (). Note that the strategy is symmetric, thus, the expected payoff of primaries would be identical and thus, we only evaluate the expected payoff of primary .

Now we introduce some notations which we use throughout this section:

Definition 15.

Let be the th smallest offered penalty offered by primaries .

Let, denote the event that at a time slot, primary 1’s channel will be bought, when its channel state is and selects penalty and primary selects penalty , when its channel state is , . Let’s recall the definition of (definition 15). From the law of total probability,

| (95) |

Now, note that if and if .

Note from (12) that

| (96) |

Thus, the first term of right hand side (r.h.s.) of(-E) is . We will denote the second term of the r.h.s. of (-E) as . Since the third term of the r.h.s. of (-E) is zero, hence,

| (97) |

Thus, if primary follows the strategy profile as described, then its total expected payoff at any stage of the game will be

| (98) |

Next observation will be used in proving Theorem 7.

Observation 5.

If a primary selects a penalty which is strictly greater than , then the probability of winning is .

Proof.

Now, we are ready to prove Theorem 7.

proof of Theorem 7:

Fix any state . We prove the theorem in two part. In Part 1, we show that when the game is at a stage where other primaries select penalty at channel state , then primary 1 does not have any unilateral deviation by selecting penalty different from for sufficiently high . In part 2, we show that if the game is in a stage where all the other primaries play the unique NE strategy profile, then primary 1 also does not have any profitable unilateral deviation. This will ensure that is a subgame perfect NE.

Proof of Part 1: First, we show that, deviating to lower penalty compared to is not profitable (case 1) and then we show that deviating to a higher penalty compared to , is also not profitable (case 2) when other primaries select penalty at channel state .

Case 1: First, suppose that primary 1 offers penalty, which is strictly less than .

A primary can attain at most a payoff of at this stage. After this deviation, all the primaries play the unique N.E. strategy. The payoff is given by . Now,

| (102) |

If a primary deviates at stage , then its expected payoff starting from stage would be at most

| (103) |

If a primary would not have deviated, then its expected payoff would have been

| (104) |

Hence, from (-E) and (-E), the following condition must be satisfied for sub game perfect equilibrium

| (105) |

From (98) and (-E), it is enough to satisfy the following inequality in order to satisfy inequality (-E)

| (106) |

By simple algebraic manipulation in (-E), we obtain

| (107) |

The proof is complete by observing that the right hand side of (107) is strictly less than 1. Hence, if is greater than the following expression

then, a primary will not have any profitable one shot deviation.

Case 2: Now, suppose that primary 1 offers penalty which is strictly greater than .

Since primary 1 offers penalty strictly greater than and , thus, from observation 5, primary 1 can at most attain a payoff of by offering penalty higher than . After the deviation, all the primaries play the one-shot NE strategy profile. If a primary deviates at stage , then its expected payoff starting from stage would be

| (108) |

If a primary would not have deviated, then its expected payoff would be

| (109) |

Hence, from (-E) and (-E), the following condition must be satisfied for sub game perfect equilibrium

| (110) |

Hence, from (98) satisfying the following condition will be enough for the strategy profile to be a SPNE.

| (111) |

But, from (13)

Hence, it is enough to satisfy the following inequality in order to satisfy inequality (-E)

| (112) |

which is exactly similar to (-E). Hence, the rest of the proof will be similar to case 1.

proof of part 2: If other primaries play the unique one-shot NE strategy, selecting the unique one-shot NE strategy is a best response for a primary. Hence, no primary has any profitable unilateral deviation.