Asymptotics for -dimensional Lévy-type processes

Abstract

We consider a general -dimensional Lévy-type process with killing. Combining the classical Dyson series approach with a novel polynomial expansion of the generator of the Lévy-type process, we derive a family of asymptotic approximations for transition densities and European-style options prices. Examples of stochastic volatility models with jumps are provided in order to illustrate the numerical accuracy of our approach. The methods described in this paper extend the results from Corielli et al. (2010), Pagliarani and Pascucci (2013) and Lorig et al. (2013a) for Markov diffusions to Markov processes with jumps.

Keywords: multi-dimensional Lévy-type process with killing, asymptotic approximation, integro-differential equation

1 Introduction

In a multi-dimensional Markovian setting, the time evolution of a market model is usually described by the solution of a Lévy-Itô stochastic differential equation (SDE). Such a model allows for features commonly seen in markets, such as stochastic volatility, jumps, default, co-integration and correlation. Many quantities of interest (e.g., option prices, net present values) can be expressed as expectations of the form . Under mild conditions, the function is the unique classical solution of a partial integro-differential equation (PIDE). Unfortunately, closed form and even semi-closed form solutions of these PIDEs are available only in rare cases. As such, it is important to develop general methods for finding analytical approximations for the solutions of these PIDEs.

Within the mathematical finance literature, a number of different approaches have been taken for finding approximate transition densities and option prices for markets described by Markov processes. Most of these techniques involve expansions that exploit a small parameter or a limiting case. For example, Benhamou et al. (2009) develop analytical approximations for models with local volatility and Gaussian jumps in the small diffusion and small jump frequency/size limits (see also the recent review paper by Bompis and Gobet (2013)). Deuschel et al. (2014) obtain densities for diffusion processes in a small noise limit. Fouque et al. (2011) find option prices for Black-Scholes-like multiscale models where volatility is driven by two factors, one running on a fast scale, one running on a slow scale. Lorig (2012); Lorig and Lozano-Carbassé (2013) extend these multiscale techniques to more general diffusions and to the exponential Lévy setting.

Recently, Pagliarani and Pascucci (2012) introduce a method for finding asymptotic solutions of parabolic PDEs. The approach, called the adjoint expansion method, is extended by Pagliarani et al. (2013); Lorig et al. (2014a) to models with jumps and it was further generalized by Lorig et al. (2013a) to a family of asymptotic expansions for a -dimensional market described by an Itô SDE (i.e., a Markov market with no jumps). The method consists of expanding the pricing PDE in polynomial basis functions, which results in a nested sequence of Cauchy problems, and deriving analytical solutions for these nested Cauchy problems. In this paper, we extend the results of Pagliarani et al. (2013); Lorig et al. (2014a, 2013a) to the PIDEs that arise when markets are described by a -dimensional Lévy-Itô SDE. Results presented here also simplify results from Pagliarani et al. (2013); Lorig et al. (2014a, 2013a).

The rest of this paper proceeds as follows. In Section 2 we present a general -dimensional market model. We also describe the kinds of derivative-assets we wish to price, and we relate the price of such derivative-assets to the solution of a parabolic PIDE. In Section 3 we introduce the idea of polynomial expansions of the pricing PIDE and in Section 4, we derive a family of analytical price approximations – one for each polynomial expansion of the pricing PIDE. Lastly, in Section 5 we provide a numerical example, illustrating the versatility and accuracy of our methods.

2 Market model

We take, as given, an equivalent martingale measure defined on a complete filtered probability space . All stochastic processes defined below live on this probability space and all expectations are taken with respect to . The risk-neutral dynamics of our market are described by the following -dimensional Markov Lévy-type process

| (2.1) |

Here is a standard -dimensional Brownian motion, and , given by

| (2.2) |

is a family of compensated Poisson measures on . The drift vector and volatility matrix map and , respectively. We assume the Lévy kernel satisfies

| (2.3) |

which is rather standard for Lévy-type models. The components of could represent a number of things such as e.g., economic factors, asset prices, indices, or functions of these quantities. We assume a risk-free interest rate of the form where . We also introduce a random time , which is given by

| (2.4) |

with exponentially distributed and independent of . The random time could represent the default time of an asset, the arrival of an economic shock, etc..

Denote by the no-arbitrage price of a European derivative expiring at time with payoff

| (2.5) |

It is well known (see, for instance, Jeanblanc et al. (2009)) that

| (2.6) | ||||||

| (2.7) | ||||||

Thus, to value a European-style option, one must compute functions of the form

| (2.8) |

Under mild assumptions (see, for instance, Pascucci (2011)), the function , defined by (2.8), satisfies the Kolmogorov backward equation

| (2.9) |

where the operator is given explicitly by

| (2.10) |

with

| (2.11) |

The formal representation of the shift operator is motivated by the fact that its Taylor expansion applied to the function gives the Taylor expansion of about the point . As in (Øksendal and Sulem, 2005, Chapter 1), we regard the domain of to be all functions such that exists and is finite for all .

3 General expansion basis

Let us start by rewriting the differential operator (2.10) in the more compact form

| (3.1) |

where by standard notations

| (3.2) |

In this section we introduce a family of expansion schemes for , which we shall use to construct closed-form approximate solutions (one for each family) of (2.9).

Definition 3.1.

For and , let and be such that the following hold:

-

(i)

For any , are polynomial functions with , and for any the functions belong to .

-

ii)

For any , , we have

(3.3) where each satisfies condition (2.3). Moreover, , and

(3.4) for some positive .

Then we say that , defined by

| (3.5) | ||||

| (3.6) |

is an th order polynomial expansion of .

Definition 3.1 allows for very general polynomial specifications. The idea is to choose an expansion that closely approximates . The precise sense of this approximation will depend on the application. Below, we present three polynomial expansions. The first two expansion schemes provide an accurate approximation in a pointwise local sense, under the assumption of smooth coefficients. The last expansion scheme approximates in a global sense and can be applied even in the case of discontinuous coefficients.

Example 3.2.

(Taylor polynomial expansion)

Assume the coefficients and that the compensator

takes the form

where with , and is a Lévy measure. Then, for any fixed and , we define and as the th order term of the Taylor expansions of and respectively in the spatial variables around the point . That is, we set

| (3.7) | ||||||

| (3.8) | ||||||

where as usual and . The expansion proposed in Lorig et al. (2013b) and Lorig et al. (2014c) is the particular case when , whereas the expansion proposed in Lorig et al. (2014a) and Lorig et al. (2014b) is a particular case when .

Example 3.3.

(Time-dependent Taylor polynomial expansion)

Under the assumptions of Example 3.2,

fix a trajectory .

We then define and as the th order term of the Taylor expansions of and respectively around . More precisely, we set

| (3.9) | ||||||

| (3.10) | ||||||

This expansion for the coefficients allows the expansion point of the Taylor series to evolve in time according to the evolution of the underlying process . For instance, one could choose . In Lorig et al. (2013b) this choice results in a highly accurate approximation for option prices and implied volatility in the Heston (1993) model.

Example 3.4.

(Hermite polynomial expansion)

Hermite expansions can be useful when the diffusion coefficients are discontinuous. A remarkable

example in financial mathematics is given by the Dupire’s local volatility formula for models with

jumps (see Friz

et al. (2013)). In some cases, e.g., the well-known Variance-Gamma model, the

fundamental solution (i.e., the transition density of the underlying stochastic model) has

singularities. In such cases, it is natural to approximate it in some norm rather than in

the pointwise sense. For the Hermite expansion centered at , one sets

| (3.11) | ||||||

| (3.12) | ||||||

where the inner product is an integral over with a Gaussian weighting centered at and the functions where is the -th one-dimensional Hermite polynomial (properly normalized so that with being the Kronecker’s delta function).

4 Formal solution via Dyson series

In this section we present a heuristic argument to pass from an expansion of the operator in (2.10) to an expansion for , the solution of problem (2.9). The following argument is not intended to be rigorous. Rather, the computations that follow provide motivation for the price expansion given in Definition 4.1. Throughout this section, we will generally omit -dependence, except where it is needed for clarity. To begin, we presume that the operator can be formally written as

| (4.1) |

We insert expansion (4.1) for into Cauchy problem (2.9) and find

| (4.2) |

Note that, by construction, is the generator of an additive process. Therefore, by Duhamel’s principle, we have

| (4.3) |

where is the semigroup of operators generated by . Inserting expression (4.3) for into the right-hand side of (4.3) and iterating we obtain

| (4.4) | ||||

| (4.5) | ||||

| (4.6) | ||||

| (4.7) | ||||

| (4.8) | ||||

| (4.9) | ||||

| (4.10) | ||||

| (4.11) |

The second-to-last equality (4.8) is known as the Dyson series expansion of (see, for instance, Section 5.7 of Sakurai and Tuan (1994) or Chapter IX.2.6 of Kato (1995)). To obtain (4.10) from (4.8) we have used (4.1) to replace by the infinite sum , and we have partitioned on the sum of the subscripts of the . Expansion (4.10) motivates the following definition.

Definition 4.1.

4.1 Expression for

In what follows, it will be helpful to recall the definition of the Fourier and inverse Fourier transforms. For any function in the Schwartz class, we define

| Fourier transform: | (4.16) | ||||

| Inverse transform: | (4.17) |

Recall that by construction (cf. Definition 3.1) and therefore the operator has time-dependent coefficients which are independent of . Then the action of the semigroup of operators of is well-known:

| (4.18) |

where

| (4.19) |

with

| (4.20) |

and

| (4.21) |

Remark 4.2.

We introduce and , the characteristic function and oscillating exponential, respectively

| (4.22) |

where is short-hand for . From (2.8) we observe that is obtained as the special case . We note that in (4.19) represents the th order approximation of . More generally, we denote by the th order approximation of , obtained by setting in (4.15).

4.2 Expression for

Remarkably, as the following proposition shows, every can be expressed as a pseudo-differential operator acting on .

Proposition 4.3.

Assume that belongs to the Schwartz class, and that in (4.20) is a smooth function of the variable . Then the function defined in (4.15) is given explicitly by

| (4.23) |

where is given by (4.18) and

| (4.24) |

with as defined in (4.11) and

| (4.25) | ||||

| (4.26) | ||||

| (4.27) | ||||

| (4.28) | ||||

| (4.29) |

Moreover, the components of commute. Therefore the operators , which are polynomials in by construction, are well defined.

Proof.

The proof consists in showing that the operator in (4.26) satisfies

| (4.30) |

Assuming (4.30) holds, we can use the fact that is a semigroup

| (4.31) |

and we can re-write (4.15) as

| (4.32) |

from which (4.23)-(4.24) follows directly. Thus, we only need to show that satisfies (4.30). It is sufficient to investigate how the operator acts on the oscillating exponential in (4.22). First, we note that

| (4.33) |

where , as given in (4.20), is a smooth function by condition (3.4). Next, we observe that the operator in (4.27) can be written

| (4.34) |

Denote by and the th component of and respectively. Then, using (4.34) we have

| (4.35) | ||||

| (4.36) | ||||

| (4.37) | ||||

| (4.38) |

More generally for any multi-index we have

| (4.39) |

From (4.38) we deduce that operators and commute when applied to , because so do and . Consequently, and also commute when applied to or any function that admits a representation as a Fourier transform. To see this observe that

| (4.40) |

Therefore, since acts on and not we have

| (4.41) |

Finally, we compute

| (4.42) | |||||

| (by (3.6)) | (4.43) | ||||

| (4.44) | |||||

| (4.45) | |||||

| (4.46) | |||||

| (4.47) | |||||

| (4.48) | |||||

| (by (4.33)) | (4.49) | ||||

| (4.50) | |||||

| (by (4.39)) | (4.51) | ||||

| (4.52) | |||||

| (4.53) | |||||

| (4.54) | |||||

| (by (4.33)) | (4.55) | ||||

| (by (4.26)) | (4.56) | ||||

which concludes the proof. ∎

4.3 Fourier representation for

Using (4.18), (4.19) and (4.23) we have

| (4.57) |

The term in parenthesis can be computed explicitly. However, is, in general, an integro-differential operator (when is a diffusion is simply a differential operator). Thus, for models with jumps, computing is a challenge. Remarkably, we will show that there exists a first order differential operator such that

| (4.58) |

where, for clarity, we have explicitly indicated using superscripts that acts on and acts on . With a slight abuse of terminology, we call the symbol111The operator is not a function as in the classical theory of pseudo-differential calculus. However is the symbol of . of the operator in (4.24).

Let us consider the operator in (4.27) and denote by its th component. The symbol of is defined analogously to (4.58), that is

| (4.59) |

Explicitly, we have

| (4.60) |

where the function is defined as

| (4.61) |

We note that, while is a first order integro-differential operator, its symbol is a first order differential operator. For this reason, it is more convenient to use the symbol instead of the operator . Note also that

| (4.62) |

Since and commute when applied to a function that admits a Fourier representation, then and also commute when applied to such functions. In particular, the operator , for , is well defined and we have

| (4.63) |

From identity (4.63) we obtain directly the expression of the symbol of in (4.26). Indeed, recalling the expression (3.3) of we have

| (4.64) |

Thus we have proved the following lemma

Lemma 4.5.

The following theorem extends the Fourier pricing formula (4.18) to higher order approximations.

Theorem 4.6.

Proof.

We first note that, since the approximating operator acts in the variables, then it commutes222This was one of the main points of the adjoint expansion method proposed by Pagliarani et al. (2013). with the Fourier pricing operator (4.18). Thus, by (4.23) combined with (4.18), we get

| (4.68) | ||||

| (4.69) |

and the thesis follows from (4.58). ∎

Remark 4.7.

Computing the term in parenthesis above is a straightforward exercise since the symbol , given in (4.65), is a differential operator.

Remark 4.8.

In case of non-integrable payoffs (e.g. Call and Put options), the Fourier representation (4.66) can be easily extended by considering the Fourier transform on the imaginary line . For instance, since the Call option payoff is not integrable, its Fourier transform must be computed in a generalized sense by fixing an imaginary component of the Fourier variable .

Remark 4.9.

Observe that the th order approximation (4.12)-(4.66) requires only a single Fourier inversion

| (4.70) |

Moreover, when evaluating the inverse transform, the number of dimensions over which one must integrate numerically is equal to the number of components of that appear in the option payoff . This is due to the fact that the Fourier transform of a constant is a Dirac delta function. In particular, let with , for some . Then we have with , and thus

| (4.71) |

5 Example: Heston model with stochastic jump-intensity

Consider the following model for an asset , written under the pricing measure assuming zero interest rates

| (5.1) | ||||

| (5.2) |

Note that, just as in the Heston model, the instantaneous volatility of is given by , where is a CIR process. Likewise, the instantaneous arrival rate of jumps of size is given by , where is a Lévy measure satisfying all of the usual integrability conditions. The generator of the process is given by

| (5.3) | ||||

| (5.4) |

The characteristic function is obtained in Carr and Wu (2004) by expressing the process as a time-changed Lévy process. One can also obtain the characteristic function by solving for the Fourier transform of the fundamental solution corresponding to the operator . We have

| (5.5) | ||||

| (5.6) | ||||

| (5.7) | ||||

| (5.8) | ||||

| (5.9) | ||||

| (5.10) |

With an explicit expression for available, the price of a European call option can be computed using standard Fourier methods

| (5.11) |

Note that, since the call option payoff is not in , its Fourier transform must be computed in a generalized sense by fixing an imaginary component of the Fourier variable .

Also of interest are sensitivities of option prices or Greeks. In particular, consider the and the , which are defined as

| (5.12) | ||||

| (5.13) |

where we have used . When computing terms of the form , observe that the differential operator acts only on the characteristic function appearing in (5.11) and not on the Fourier transform of the payoff . Likewise, when using Theorem 4.6 to compute the differential operator acts only on in (4.66).

Now, we specialize to the case where jumps are normally distributed

| (5.14) |

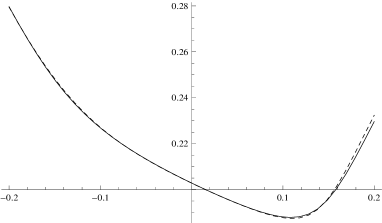

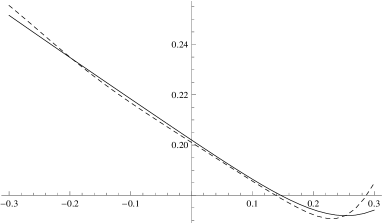

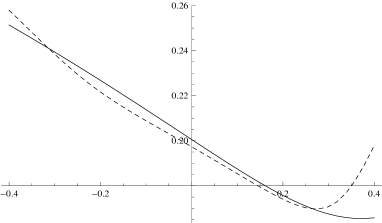

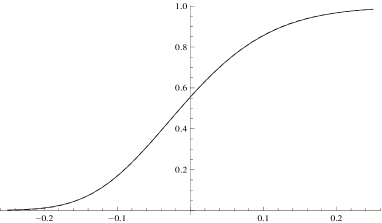

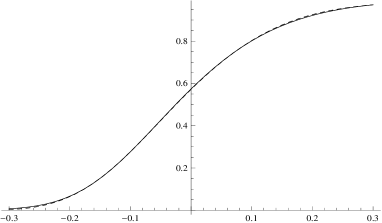

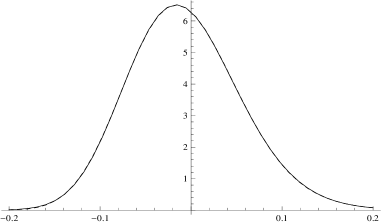

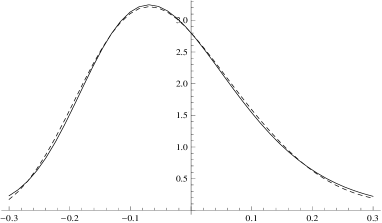

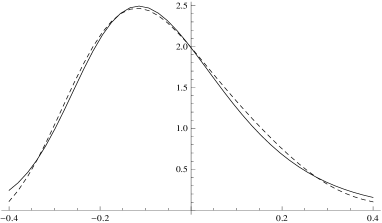

In Figure 1 we plot the implied volatility corresponding to the exact price as well as the implied volatility corresponding to our second order approximation . To compute we first compute option prices using (5.11); we then invert the Black-Scholes equation numerically in order to obtain the implied volatility . To compute our second order approximation of implied volatility we first compute our second order approximation for prices using Theorem 4.6; we then invert the Black-Scholes equation numerically in order to obtain . Values from Figure 1 can be found in Table 1. In Figure 2 we plot the exact as well as our second order approximation . In Figure 3 we plot the exact as well as our second order approximation . Values from Figures 2 and 3 are given in Tables 2 and 3 respectively. Exact Greeks are computed by combining (5.11), (5.12) and (5.13). Approximate Greeks are computed by combining Theorem 4.6 and equations (5.12) and (5.13).

6 Conclusion

In this paper we derive a family of asymptotic expansions for European option prices when the underlying is modeled as a -dimensional time inhomogeneous Lévy-type process. By combining the classical Dyson series expansion with a novel polynomial expansion of the generator, we obtain two equivalent representations for approximate option price: (i) as an integro-differential operator acting on the order zero price, and (ii) as a Fourier transform. We implement our pricing approximation on a Heston-like model which allows for both stochastic volatility and stochastic jump intensity. We find that our second order expansion provides and excellent approximation for prices (as seen through corresponding implied volatilities), as well as for the Greeks and .

References

- Benhamou et al. (2009) Benhamou, E., E. Gobet, and M. Miri (2009). Smart expansion and fast calibration for jump diffusions. Finance and Stochastics 13(4), 563–589.

- Bompis and Gobet (2013) Bompis, R. and E. Gobet (2013). Asymptotic and non asymptotic approximations for option valuation. In Recent developments in computational finance. Foundations, algorithms and applications., pp. 159–241. Hackensack, NJ: World Scientific.

- Carr and Wu (2004) Carr, P. and L. Wu (2004). Time-changed Lévy processes and option pricing. Journal of Financial Economics 71(1), 113–141.

- Corielli et al. (2010) Corielli, F., P. Foschi, and A. Pascucci (2010). Parametrix approximation of diffusion transition densities. SIAM J. Financial Math. 1, 833–867.

- Deuschel et al. (2014) Deuschel, J.-D., P. Friz, A. Jacquier, and S. Violante (2014). Marginal density expansions for diffusions and stochastic volatility, part i: Theoretical foundations. Communications on Pure and Applied Mathematics 67(1), 40–82.

- Fouque et al. (2011) Fouque, J.-P., G. Papanicolaou, R. Sircar, and K. Solna (2011). Multiscale stochastic volatility for equity, interest rate, and credit derivatives. Cambridge: Cambridge University Press.

- Friz et al. (2013) Friz, P. K., S. Gerhold, and M. Yor (2013). How to make Dupire’s local volatility work with jumps. arXiv preprint1302.5548.

- Heston (1993) Heston, S. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6(2), 327–343.

- Jeanblanc et al. (2009) Jeanblanc, M., M. Yor, and M. Chesney (2009). Mathematical methods for financial markets. Springer Verlag.

- Kato (1995) Kato, T. (1995). Perturbation theory for linear operators. Classics in Mathematics. Springer-Verlag, Berlin. Reprint of the 1980 edition.

- Lorig (2012) Lorig, M. (2012, November). Pricing derivatives on multiscale diffusions: An eigenfunction expansion approach. Mathematical Finance.

- Lorig and Lozano-Carbassé (2013) Lorig, M. and O. Lozano-Carbassé (2013). Exponential Lévy models with stochastic volatility and stochastic jump-intensity. ArXiv preprint arXiv:1205.2398.

- Lorig et al. (2013a) Lorig, M., S. Pagliarani, and A. Pascucci (2013a). Analytical expansions for parabolic equations. ArXiv preprint arXiv:1312.3314.

- Lorig et al. (2013b) Lorig, M., S. Pagliarani, and A. Pascucci (2013b). Implied vol for any local-stochastic vol model. ArXiv preprint arXiv:1306.5447.

- Lorig et al. (2014a) Lorig, M., S. Pagliarani, and A. Pascucci (2014a). A family of density expansions for Lévy-type processes with default. To appear in: Annals of Applied Probability.

- Lorig et al. (2014b) Lorig, M., S. Pagliarani, and A. Pascucci (2014b). Pricing approximations and error estimates for local Lévy-type models with default. ArXiv preprint arXiv:1304.1849.

- Lorig et al. (2014c) Lorig, M., S. Pagliarani, and A. Pascucci (2014c). A Taylor series approach to pricing and implied vol for LSV models. ArXiv preprint arXiv:1308.5019, to appear in Journal of Risk.

- Øksendal and Sulem (2005) Øksendal, B. and A. Sulem (2005). Applied stochastic control of jump diffusions. Springer Verlag.

- Pagliarani and Pascucci (2012) Pagliarani, S. and A. Pascucci (2012). Analytical approximation of the transition density in a local volatility model. Cent. Eur. J. Math. 10(1), 250–270.

- Pagliarani and Pascucci (2013) Pagliarani, S. and A. Pascucci (2013). Local stochastic volatility with jumps: analytical approximations. Int. J. Theor. Appl. Finance 16 (8), 1–35.

- Pagliarani et al. (2013) Pagliarani, S., A. Pascucci, and C. Riga (2013). Adjoint expansions in local Lévy models. SIAM J. Financial Math. 4, 265–296.

- Pascucci (2011) Pascucci, A. (2011). PDE and martingale methods in option pricing, Volume 2 of Bocconi & Springer Series. Milan: Springer.

- Sakurai and Tuan (1994) Sakurai, J. J. and S. F. Tuan (1994). Modern quantum mechanics, Volume 104. Addison-Wesley Reading (Mass.).

|

|

|

|

| (6.1) |

| -0.2 | -0.15 | -0.1 | -0.05 | 0.00 | 0.05 | 0.1 | 0.15 | 0.2 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.2797 | 0.2478 | 0.2269 | 0.2133 | 0.2028 | 0.1940 | 0.1881 | 0.1960 | 0.2296 | ||

| t=0.10 | 0.2795 | 0.2483 | 0.2271 | 0.2132 | 0.2028 | 0.1939 | 0.1877 | 0.1963 | 0.2324 | |

| rel. err. | 0.0006 | 0.0018 | 0.0009 | 0.0003 | 0.0002 | 0.0001 | 0.0020 | 0.0018 | 0.0120 | |

| 0.2441 | 0.2323 | 0.2217 | 0.2120 | 0.2028 | 0.1941 | 0.1863 | 0.1805 | 0.1803 | ||

| t=0.25 | 0.2456 | 0.2328 | 0.2215 | 0.2116 | 0.2025 | 0.1939 | 0.1859 | 0.1793 | 0.1799 | |

| rel. err. | 0.0059 | 0.0018 | 0.0013 | 0.0020 | 0.0013 | 0.0009 | 0.0021 | 0.0067 | 0.0027 | |

| 0.2348 | 0.2266 | 0.2183 | 0.2101 | 0.202 | 0.1940. | 0.1864 | 0.1796 | 0.1743 | ||

| t=0.50 | 0.2350 | 0.2254 | 0.2168 | 0.2088 | 0.201 | 0.1933 | 0.1856 | 0.1783 | 0.1723 | |

| rel. err. | 0.0005 | 0.0049 | 0.0069 | 0.0063 | 0.004 | 0.0037 | 0.0040 | 0.0070 | 0.0116 | |

| 0.2268 | 0.2204 | 0.2138 | 0.2072 | 0.2005 | 0.1939 | 0.1875 | 0.1813 | 0.1757 | ||

| t=1.00 | 0.2217 | 0.2149 | 0.2089 | 0.2031 | 0.1973 | 0.1914 | 0.1854 | 0.1794 | 0.1740 | |

| rel. err. | 0.0227 | 0.0246 | 0.0230 | 0.0197 | 0.0160 | 0.0130 | 0.0111 | 0.0103 | 0.0096 |

|

|

|

|

| -0.2 | -0.15 | -0.1 | -0.05 | 0.00 | 0.05 | 0.1 | 0.15 | 0.2 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.0008 | 0.00516 | 0.05084 | 0.2312 | 0.5370 | 0.8024 | 0.9385 | 0.9845 | 0.9959 | ||

| t=0.10 | 0.0009 | 0.00478 | 0.05081 | 0.2313 | 0.5368 | 0.8026 | 0.9387 | 0.9843 | 0.9958 | |

| rel. err. | 0.1309 | 0.07358 | 0.00048 | 0.0006 | 0.0003 | 0.0002 | 0.0002 | 0.0002 | 0.0000 | |

| 0.01311 | 0.05708 | 0.1690 | 0.3503 | 0.5559 | 0.7329 | 0.8563 | 0.9293 | 0.9672 | ||

| t=0.25 | 0.0114 | 0.05674 | 0.1696 | 0.3502 | 0.5552 | 0.7330 | 0.8576 | 0.9306 | 0.9673 | |

| rel. err. | 0.1305 | 0.00585 | 0.0035 | 0.0004 | 0.0012 | 0.0000 | 0.0014 | 0.0014 | 0.0000 | |

| 0.06608 | 0.1506 | 0.2767 | 0.4260 | 0.5739 | 0.7018 | 0.8014 | 0.8731 | 0.9215 | ||

| t=0.50 | 0.06425 | 0.1508 | 0.2766 | 0.4246 | 0.5719 | 0.7007 | 0.8027 | 0.8766 | 0.9256 | |

| rel. err. | 0.02773 | 0.0014 | 0.0003 | 0.0032 | 0.0034 | 0.0015 | 0.0015 | 0.0040 | 0.0044 | |

| 0.1708 | 0.2667 | 0.3760 | 0.4878 | 0.5927 | 0.6849 | 0.7618 | 0.8234 | 0.8713 | ||

| t=1.00 | 0.1662 | 0.2627 | 0.3710 | 0.4814 | 0.5857 | 0.6791 | 0.7595 | 0.8262 | 0.8789 | |

| rel. err. | 0.0268 | 0.01496 | 0.0131 | 0.0130 | 0.0117 | 0.0084 | 0.0030 | 0.0033 | 0.0088 |

|

|

|

|

| -0.2 | -0.15 | -0.1 | -0.05 | 0.00 | 0.05 | 0.1 | 0.15 | 0.2 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.01828 | 0.2978 | 2.159 | 5.539 | 6.288 | 3.831 | 1.446 | 0.3779 | 0.0780 | ||

| t=0.10 | 0.01197 | 0.2897 | 2.1760 | 5.5300 | 6.288 | 3.841 | 1.437 | 0.3748 | 0.0821 | |

| rel. err. | 0.3452 | 0.0273 | 0.0077 | 0.0015 | 0.0001 | 0.0025 | 0.0061 | 0.0082 | 0.0518 | |

| 0.5185 | 1.705 | 3.337 | 4.275 | 3.967 | 2.884 | 1.738 | 0.906 | 0.4229 | ||

| t=0.25 | 0.5267 | 1.747 | 3.334 | 4.255 | 3.969 | 2.907 | 1.754 | 0.8925 | 0.4016 | |

| rel. err. | 0.0157 | 0.024 | 0.0009 | 0.0046 | 0.0003 | 0.0079 | 0.0094 | 0.0149 | 0.0503 | |

| 1.514 | 2.488 | 3.135 | 3.206 | 2.802 | 2.174 | 1.54 | 1.017 | 0.635 | ||

| t=0.50 | 1.585 | 2.508 | 3.109 | 3.182 | 2.804 | 2.208 | 1.588 | 1.045 | 0.6244 | |

| rel. err. | 0.0468 | 0.0079 | 0.0081 | 0.0076 | 0.0007 | 0.015 | 0.0309 | 0.0279 | 0.0167 | |

| 2.095 | 2.425 | 2.483 | 2.306 | 1.985 | 1.612 | 1.251 | 0.9364 | 0.6814 | ||

| t=1.00 | 2.134 | 2.418 | 2.452 | 2.280 | 1.988 | 1.656 | 1.331 | 1.028 | 0.7511 | |

| rel. err. | 0.0183 | 0.0032 | 0.0124 | 0.0110 | 0.0015 | 0.0276 | 0.0644 | 0.097 | 0.1023 |