Pricing of Basket Options Using Polynomial Approximations

Abstract.

In this paper we use Bernstein and Chebyshev polynomials to approximate the price of some basket options under a bivariate Black-Scholes model. The method consists in expanding the price of a univariate related contract after conditioning on the remaining underlying assets and calculating the mixed exponential-power moments of a Gaussian distribution that arise as a consequence of such approximation. Our numerical implementation on spreads contracts shows the method is as accurate as a standard Monte Carlo approach at considerable lesser computational effort.

Key words and phrases:

Bernstein, Chebyshev, Taylor, basket options, spread options.1. Introduction

The objective of the paper is the study of basket options under a standard multivariate Black-Scholes model using different polynomial approximations of a related conditional contract on one of the underlying assets.

By conditioning on some of the asset prices we reduce the problem to computing the expected value of the Black-Scholes formula with a random strike price. Under suitable polynomial approximations this expected value can be obtained from the corresponding one dimensional price at selected points together with the truncated exponential-power moments of a joint Gaussian distribution. It allows to compute prices with a precision comparable to a Monte Carlo approach and considerable less computational effort.

An alternative point of view using Taylor polynomials is followed in Li, Deng and Zhou (2008, 2010) or Alvarez and Olivares (2014). Although a Taylor approximation produces fairly estimates in terms of a simple closed-formula based on the derivatives of the conditional price, it is quite sensible to the point around the expansion is done. Moreover, as this expansion is local at a particular value of the parametric set, it may introduce significant errors, albeit infrequent, at values far from the point where the expansion is considered.

In order to overcome this potential problem we study developments in terms of Bernstein and Chebyshev polynomial approximations, which offer a uniform convergence of the conditional price on a given closed interval. For the seek of simplicity we focus on bidimensional spread contracts and a Black-Scholes model, but the method can be extended to more complex models or other European derivatives. See for example Olivares (2014) for applications to the case of jump-diffusion and switching jump-diffusion models. Interesting approximations in terms of Fourier series can be found in Meng and Ding(2013) and in Fang and Oosterlee(2009).

Basket options are a multivariate extensions of univariate European calls or puts. A basket option takes the weighted average of a group of stocks (the basket) as the underlying, and produces a payoff equal to the maximum of zero and the difference between the weighted average and the strike (or the opposite difference for the case of a put). Index options, whose value depend on the movement of an equity or other financial index such as the S&P 500 and real options based on the difference between gas and oil prices are examples of such contracts.

In the particular case of spread options, several approximations have been previously considered in the works of Kirk(1995), Carmona and Durrleman(2003), Li, Deng and Zhou(2008, 2010) and Venkatramanan and Alexander (2011), where different ad-hoc approaches are studied.

The organization of the paper is the following, in section 2 we introduce the model, main notations and derive Bernstein approximation for spread options. In section 3 we study the case of a Chebyshev approximation and the sensitivity with respect to the spot prices. In section 4 we discuss the numerical implementation and results. Finally in section 5 we conclude.

2. An Approximation Based on Bernstein Polynomials

We first introduce some notations and our main model.

Let be a filtered probability space and define the filtration as the -algebra generated by the random variables completed in the usual way. Denote by the risk neutral measure and the expectation under .

The quantities and represent respectively the truncated moment and the generating moment function (g.m.f.) on , while the function is the cumulative distribution function (c.d.f.) of a standard normal distribution.

The matrix represents the transpose of matrix , while is, depending on the context, a diagonal matrix with components in the main diagonal or a column vector with components from the diagonal of the matrix . On the other hand denotes a matrix such that . The d-dimensional column vector of ones is described by .

The process of spot prices is denoted by while defines the asset log-return process at time , related as

| (1) |

We analyze European basket options whose payoff, at maturity time and strike price , is given by:

where are some deterministic weights and .

Probably the most studied of these contracts are spread options whose payoff is

We will focus on the case assuming a bidimensional Black-Scholes dynamics, that under the risk neutral probability is given by:

| (2) |

where is a two dimensional vector of Brownian motions such that and is a positive definite symmetric matrix defined by:

Here is the (constant) interest rate.

Equivalently, after applying Ito formula:

| (3) |

The price of a basket contact with maturity at and payoff , denoted by , is given by:

| (4) | |||||

where:

| (5) |

represents the price of a one dimensional European contract with underlying and payoff when .

We start writing the price in terms of a conditional price via the following elementary lemma.

Lemma 1.

The price of a European basket contract with payoff under the model given by equation (2) is

| (6) |

where:

is the Black-Scholes price of a Call Option written on the underlying asset price with strike price , maturity at , volatility , spot price and strike price given by:

with:

Proof.

From equation (3) we have:

where:

Moreover, it is well known that the conditional distribution of given is also normal. See for example Tong(1989). Thus we can write

| (7) |

where:

and , independent of .

Next, from equation (4) we have:

where .

Substituting equation (7) into (LABEL:eq:pgral) we have:

where:

Equation (6) follows immediately. ∎

For any and we consider the n-th expansion of the function in terms of Bernstein polynomials on the interval . Denoted as it is defined by:

| (10) |

where for , the functions

are the Bernstein polynomials of order on and

Consequently the Bernstein approximation of n-th order truncated on for the price of a basket option with payoff is defined as:

| (11) |

The next theorem provides an expression for the approximation defined above.

Theorem 2.

The Bernstein approximation of n-th order for the price of a spread contract with payoff under the model (2) is given by:

| (14) | |||||

where:

and

is the Black-Scholes price of a Call Option written on the underlying asset price with strike price , maturity at , volatility , spot price and strike price:

| (19) |

with:

| (20) | |||||

and

Proof.

By Lemma 1 we replace equation (10) into equation (11) to have:

Now:

| (26) | |||||

Moreover we have:

| (30) | |||||

Next, notice that:

| (37) | |||||

| (38) | |||||

Finally substituting equation (38), evaluated at , into equation (LABEL:eq:mgf2), then equation (LABEL:eq:mgf2) into equation (LABEL:eq:expinter) we get equation (LABEL:eq:approxgen ). ∎

Remark 3.

Notice that the approximation depends only on the values of a Black-Scholes option price on a partition of the interval and the truncated mixed exponential-power moments of a Gaussian multivariate distribution.

3. Approximation by Chebyshev Polynomials

We study an alternative approximation of the price via Chebyshev polynomials. For definition and their basic properties see for example Mason and Handscomb (2003).

Denoting by the sequence of Chebyshev polynomials of first type on we consider the n-th approximation of the function on the interval described by equation in terms of Chebyshev polynomials the one given by:

| (39) |

where is the sequence of Chebyshev polynomials of first type on defined by:

and the values are estimators of the corresponding coefficients in the Chebyshev expansion.

Chebyshev polynomials on are orthogonal with respect to the scalar product defined as:

with weight function .

Notice that

Then for the coefficients in the expansion can be calculated as:

after changes of variables and .

Also:

From the trapezoidal rule to approximate Riemnan integrals the coefficients can be estimated by an equidistant partition of points on :

where:

Chebyshev polynomials of first type can be written in terms of powers of the variable. From Amparo et al.(2007):

| (40) |

where:

In a similar way to the Bernstein polynomial approach we define the n-th order Chebyshev approximation for the spread price as:

The next theorem provides the Chebyshev approximation for the price of a Basket option:

Theorem 4.

The n-th order Chebyshev’s approximation of the price of a European basket option under the model given by equation (2) with payoff is given by:

where:

for ,

Proof.

3.1. Sensitivities with respect to the parameters

Sensitivities with respect to the parameters in the model and contract can be analyzed with the help of the approximations above. It is worth noticing that the lack of a closed-form formula of the spread price makes impossible to directly differentiate it to obtain the corresponding Greek. On the other hand a Monte Carlo approach to compute derivatives of the price with a reasonable error, in practice, requires a considerable extra amount of computational effort. Here we focus on the deltas of the spread contract, i.e. the sensitivities with respect to the spot prices given by a Chebyshev approximation. Other sensitivities follows in a similar way.

To this end we slightly change the notations, explicitly stating the dependence on the initial prices and . Thus, we write instead of in equation (5) and for .

The conditional price can be written now:

where:

Then by elementary differentiation:

where and are respectively the density and cumulative distribution functions of a standard normal random variable.

Taking into account equation (39) a natural estimator of is:

Notice that is continuously differentiable with respect to

and , then derivative and integral can be interchanged. Therefore we have:

for .

The coefficients in the development are estimated by:

where:

Finally we estimate by:

4. Numerical results

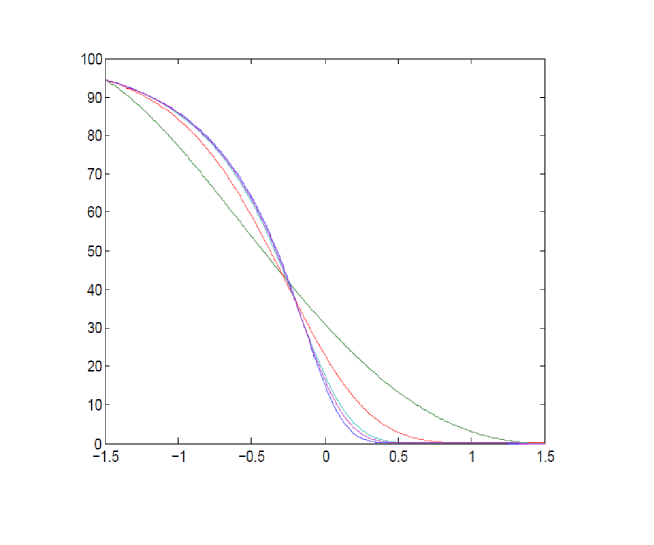

As benchmark setting we consider initial prices of and dollars, strike price of , maturity at year and an annual interest rate of under a bivariate Black-Scholes model, with a negative correlation and respective volatilities equal to and . In Figure 1 different approximations of the conditional price based on Bernstein polynomials are shown. The blue line represents the actual conditional price, the green line describes the corresponding expansion of order , while the red line is the approximation for .

In order to achieve an accurate approximation polynomials with high orders, e.g. or even , are required. This limits the applicability of the method. Moreover, numerical instabilities appear in the computation of large factorials, even when an asymptotic Stirling formula is used in their computation.

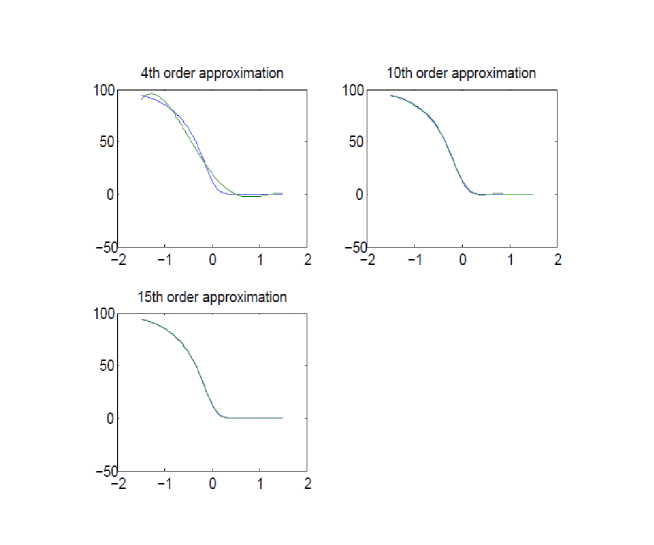

A more promising result is obtained when an approximation of the conditional price is done via Chebyshev polynomials. Figure 2 represents, clockwise from top left, approximations of 4th, 10th and 15th order respectively. Expansions of order 10th and 15th are practically indistinguishable from the original function. Coefficients in the expansion are calculated following a trapezoidal rule with points on the interval .

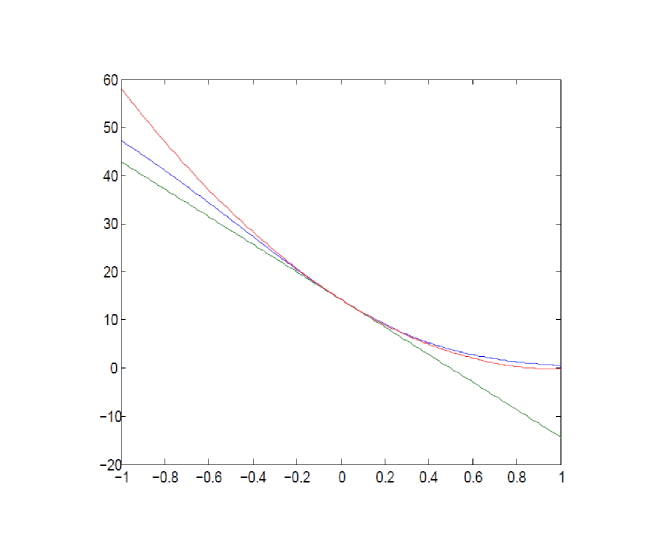

For comparison in Figure 3 we show the conditional price function on for the benchmark setting (blue line), together with the first and second Taylor expansions around the mean value of , i.e. (lines green and red respectively). While the second order approximation offers a reasonable local fit, significant errors may be found for values far from the mean, which in turns may impact in the price given by its conditional expected value under the risk neutral probability when, for example volatilities are high. See Alvarez and Olivares (2014) for details.

In Table 1 we show prices of spread contracts obtained under the benchmark parameter set, the correlation between the two assets varies. Prices are computed by a Monte Carlo approach based on 10 millions simulations of the asset prices with correlated Brownian motions (column 2). In addition we implement a second order Taylor expansion and an approximation by mean of Chebyshev polynomials of order . We consider positive and negative correlations, large moderated and weak correlations. In all cases the Chebyshev approximation shows a notable agreement with Monte Carlo prices at less computational cost.

| Correlation | Monte Carlo | Taylor Second approx. | Chebyshev, |

|---|---|---|---|

| 14.292128 | 13.87090 | 14.29060779 | |

| 13.56278 | 14.78882 | 13.5649 | |

| 14.9734 | 15.0065 | 14.96293 | |

| 12.8085 | 12.7901 | 12.790289 | |

| 15.6273 | 15.9238 | 15.63157 | |

| 11.9525 | 11.9646 | 11.9566 | |

| 16.2421 | 17.5217 | 16.25209 | |

| 11.03146 | 11.194724 | 11.05286 |

In the range of parameters considered pricing Chebyshev approximation works about seven times faster when compared with a standard Monte Carlo approach. Taylor has a even a lesser computational time, but for large correlations it is not as accurate as the former.

Due to the steepness of the function the Chebyshev approximation is sensible to the truncation interval . In our numerical computations we have used and . Within the range of parameter considered most values of lie on the selected interval , hence truncation does not affect the mixed exponential-power function by much. Otherwise outside the interval the truncation to zero can be replaced by if or if , as the conditional price remains flat outside a convenient interval.

The method is stable for the number of points considered in the trapezoid rule. Also approximation gets close to the actual price after a fairly moderate number of polynomials. For the method shows a good approximation within an error in the order of a penny. For and the approximation improves even more. For approximations of larger orders the gain in precision does not compensate the increase in computational time.

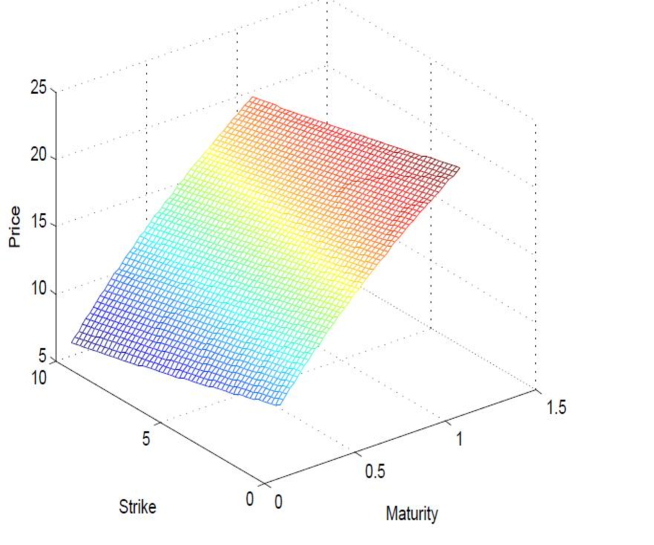

Figure 4 shows prices of a spread contract based on a Chebyshev approximation of order . Maturity times ranges from one month to one year, while strike prices go from zero (exchange option) to 10 dollars. Results are consistent with a linear increase in the contract prices with higher maturity and their decrease with the increase of the strike price.

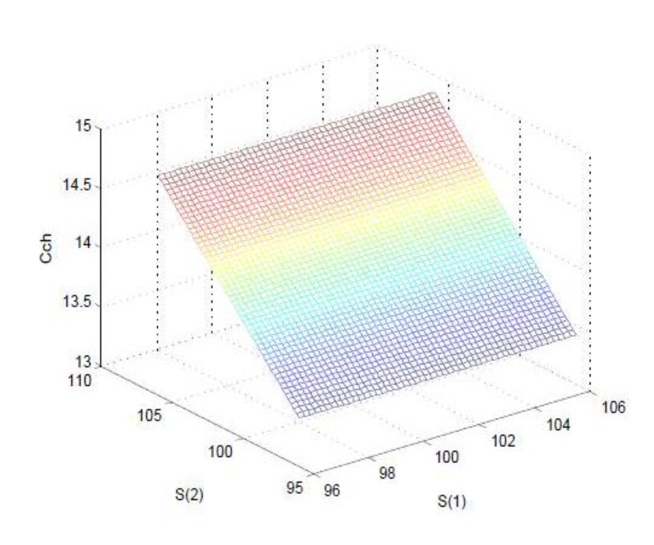

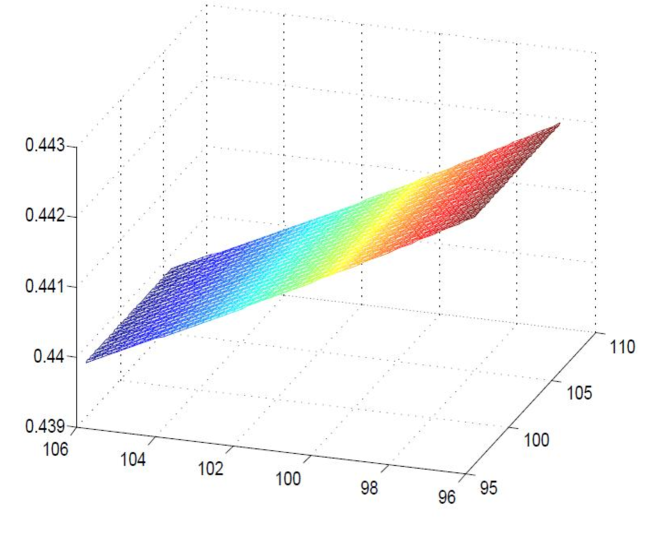

Figure 5 shows the price as function of both prices while Figure 6 provides the delta of the spread contract with respect to the second underlying and a range of values of initial prices going from 96 to 106 dollars. Delta values are calculated according to equation (LABEL:eq:chebdelta).

5. Conclusions

We compare three methods to price spreads options under a bivariate Black-Scholes model with correlated Brownian motions versus a standard Monte Carlo approach. Our results show that Bernstein approximation requires a large number of terms to achieve a good precision, while Taylor approximation does not offer a uniform convergence, hence a poor result when values are far from the point around the expansion is taken. For some values of the parameter set it may affect the corresponding expected value.

The approximation based on Chebyshev polynomials seems to be appropriate in terms of the balance offered between accuracy and computational cost. Moreover, the method is suitable to be implemented in more general models provided the conditional distribution is available.

References

- [1] Alvarez, A., Olivares,P. (2014). A Note on the Pricing of Basket Options Using Taylor Approximations, working paper.

- [2] Fang, F., and Oosterlee, C. W.(2009) A novel pricing method for European options based on Fourier-cosine series expansions,SIAM J. Sci. Comput. 31, 2 (2008/09), 826 848.

- [3] Gil, A., Segura, J. and Temme, N. (2007) Numerical Methods for Special Functions. Society for Industrial and Applied Mathematics. Philadelphia, PA, USA.

- [4] Carmona, R. and Durrleman, V.(2003) Pricing and Hedging Spread Options. SIAM Review, 45:4, 627-685.

- [5] Li, M., Deng, S. and Zhou, J. (2008) Closed-form Approximations for Spread Options Prices and Greeks. Journal of Derivatives, 15:3, 58-80.

- [6] Li, M., Zhou, J., Deng, S. J. (2010). Multi-asset spread option pricing and hedging. Quantitative Finance, 10(3), 305-324.

- [7] Kirk, E.(1995) Correlation in the Energy Markets, in managing energy price risk. Risk Publications and Enron, London, 71-78.

- [8] Mason, J.C. and Handscomb, D.C. (2003) Chebyshev Polynomials, CRC Press Company, Florida.

- [9] Meng, Q. J., Ding, D. (2013). An efficient pricing method for rainbow options based on two-dimensional modified sine sine series expansions. International Journal of Computer Mathematics, 90(5), 1096-1113.

- [10] Olivares, P.(2014) Basket Option Pricing Approximations Under Jump-Diffusion and Switching Models. Working paper.

- [11] Tong, Y. L. (1989) The Multivariate Normal Distribution, Springer, Berlin.