December 22, 2006

\sasperiodofwork01/05/200630/11/2006

\sascommittee\Bagchi

\Vellekoop

\Kandhai

Incorporating a Volatility Smile into the Markov-Functional Model111This is the author’s thesis for the Master of Science in Applied Mathematics with specialization in Financial Engineering. The thesis was under the supervision of A. Bagchi, M.H. Vellekoop and D. Kandhai and was defended on 22 December 2006. The project was executed from May 2006 to November 2006 at the ABN AMRO Bank in Amsterdam.

Preface Acknowledgement

This thesis is a detailed report of my 7-month internship at the

Product Transaction Analysis group of ABN AMRO in Amsterdam.

I would like to take this opportunity to thank all the people who

have given help related to this project. First of all, I would like

to thank my university supervisors Prof. Bagchi and Michel Vellekoop

for giving comments on my work and all other contributions. Without

Prof. Bagchi’s initial effort, anything related to this project

would not have happened. I also want to thank Marije Elkenbracht and

Lukas Phaf from ABN AMRO for offering me such a nice internship.

Here I do owe a major acknowledgement to my company supervisor Drona

Kandhai, who took care of every aspect of the project in detail and

had the time lines well under control so that the project could be

finished without significant delays. Thanks also to Rutger Pijls,

Bert-Jan Nauta, Alex Zilber and Artem Tsvetkov for their useful

opinions on parts of my work, and other colleagues at ABN for

creating a harmonious atmosphere for work. Last but not least, I

would like to thank all the teachers of the MSc programme in

Financial Engineering of the University of Twente for educating me

in both math and finance.

Chapter 1 Introduction

Interest rate models evolved from short rate models, which model the

instantaneous rate implied from the yield curve, to market models

that are based on LIBOR/swap rates. A nice property of short rate

models is that they are based on low-dimensional Markov processes.

This allows for analytical valuation or the use of tree/PDE based

approaches. But on the other hand, it has the difficulty of

calibration to caps/floors or swaptions. Market models are more

intuitive as LIBOR/swap rates are something that exists in reality.

They can be also easily calibrated to market instruments. However,

due to the large dimensionality which is inherent to these models,

the only tractable approach is to apply Monte-Carlo simulation.

Markov-Functional (MF) models contain the nice properties from

both these two classes of models. Only a low-dimensional Markov

process is tracked such that the value of exotic derivatives

can be computed efficiently on a lattice. Meanwhile MF models can

still be calibrated to caps/floors or swaptions in a relatively easy

way.

The major question in MF models is how to go from ’s

stochasticity to the distributions of LIBOR/swap rates. The original

MF models map to the lognormal distribution of the underlying,

and thus volatility smile is not taken into account. A natural

extension of this model is a mapping to another distribution that is

consistent with volatility smile. The objective of this project is

to study the effect of volatility smile on the values and hedging

performance of co-terminal Bermudan swaptions in the

Markov-Functional model. We focus on Bermudan swaptions because they

are one of the most liquid American-style interest rate derivatives.

A convenient choice that can fit to the static volatility smile and

satisfy the arbitrage-free condition is the Uncertain Volatility

Displaced Diffusion (UVDD) model. This model can generate both

the effects of skew and smile, as has already been demonstrated in

Abouchoukr [1]. However, it is not clear whether

its hedging performance is good or not. The fact that different

models can calibrate to today’s smile but disagree on the hedging

performance has been discussed in the literature [8][11]. In this report, we present in detail the

performance of the Markov-Functional model with UVDD digital mapping

in terms of pricing and hedging of Bermudan swaptions.

The rest of this report is organized as follows. Chapter

2 focuses on explaining the original

Markov-Functional models in every aspect. Chapter

3 studies the effect of incorporating volatility

smile for pricing. Chapter 4 investigates the

future smile and smile dynamics of the extended MF model. Chapter

5 presents the calibration results of the

UVDD model. Chapter 6 reports the details of the

hedging simulations. Finally, Chapter 7

summarizes the main conclusions of this study and some suggestions

for future research.

Chapter 2 Markov-Functional Models

2.1 Quick Review of Interest Rate Models

The first generation of interest rate models was a family of short rate models whose governing SDE is specified under a martingale measure Q. These short rate models share the general form:

| (2.1) |

where ranges from 0 to 1 and is Brownian motion under . In practice only values of , and are typically used, which correspond to, for example, the Hull-White model, the Cox-Ingersoll-Ross model and the Black-Karasinski model. Specifying r as the solution of a SDE allows us to use Markov process theory, and thus we may work within a PDE framework. If the term structure 111 denotes the value at time of a discount bond maturing at . has the form

| (2.2) |

where and are deterministic functions, then the model is said to process an affine term structure (ATS) [3]. Hence the yield222The continuously compounded yield from to is defined as . from t to T has the form:

| (2.3) |

This makes it particularly convenient to obtain analytical formulas for the values of bonds and derivatives on bonds. However, the obviously very unrealistic fact that Equation 2.3 implies is that all yields are perfectly correlated, as short rate is the only source of risk, i.e.,

| (2.4) |

Instead of specifying a much more complicated short rate model, for example a two-factor or even multi-factor short rate model, Heath-Jarrow-Morton [10] chose to model the entire forward rate curve as their (infinite dimensional) state variable. The HJM approach to interest rate modelling is a general framework for analysis rather than a specific model, like, for example, the Hull-White model. In this framework, the forward rate can be specified directly under a martingale measure Q as

| (2.5) |

where is a d-dimensional row-vector and is a d-dimensional column-vector. By the choice of volatilities , the drift parameters are determined by the arbitrage-free principle333For proof, we refer to Chapter 23 of Bjork [3]..

| (2.6) |

where in the formula T denotes transpose. Then we implicitly observe today’s forward rate structure from the market so that we can integrate to get the whole spectrum of the forward rates.

| (2.7) |

Using the results obtained from Equation 2.7, we can

compute the prices of bonds and derivatives on bond444For

details, we refer to Bjork [3]..

Short rate and forward rate models are mimicking the modelling of

equity/currency derivatives, whose underlying dynamics has the

following form

| (2.8) |

where can function as either the spot or forward value of the underlying. However, the interest rate we observe in reality, like LIBOR or swap rate, always carries a tenor from overnight to years. Then it’s by intuition more suitable to model the interest rate dynamics by carrying a tenor parameter as well, i.e.,

| (2.9) |

where is the tenor length. Comparing Equation

2.8 and Equation 2.9, we see that

short/forward rate models are dealing with interest rates with an

infinitesimal tenor length.

Remark: From now on we will use the notation defined in

Appendix A.1.

A historic breakthrough came from Brace-Gatarek-Musiela [5] and Jamshidian [13], whose approach was to

directly model discrete market rates such as forward LIBOR rates in

the LIBOR market models or forward swap rates in the swap market

models. For LIBOR market models, let’s look at Equation

A.1. If we choose as the numeraire, it can

be proved that the LIBOR process is a martingale under

the forward measure .555For proof, we refer to

Chapter 25 of Bjork [3]. If we then further assume

the LIBOR rate to be lognormally distributed under its

forward measure, i.e.,

| (2.10) |

where is a d-dimensional row-vector and is a d-dimensional column-vector, we can transform all the LIBOR process to the terminal measure by application of Girsanov theorem,666For derivation of Equation 2.11, we refer to Chapter 25 of Bjork [3].

| (2.11) |

The valuation and risk management of interest rate derivatives by

means of LIBOR market models then resort to multi-dimensional

Monte-Carlo simulation. A similar line is followed by swap market

models, in which PVBP, , is chosen to be the numeraire.

Hence, the forward swap process is a martingale under the

forward measure .777For the definitions of

, and , please refer to Appendix

A.1. What’s worth mentioning is that the terminal

measure in swap market models, , coincides with that of

LIBOR market model as their numeraires just differ by a

constant . This can be further explained by the fact

that division by a certain numeraire determines a certain measure,

which is the rule of allocating probabilities. So division by an

extra constant won’t matter for the distributions of random

variables.

Market models are more intuitive than short rate models as

LIBOR/swap rates exist in reality. They can be also easily

calibrated to market instruments. However, due to the large

dimensionality which is inherent to these models, the only tractable

approach is to apply Monte-Carlo simulation. Hunt-Kennedy-Pelsser

[12] proposed a general class of Markov-Functional

interest rate models, which contain nice properties from both these

two classes of models. In Markov-Functional models, we would only

have to track a low-dimensional process which is Markovian in

some martingale measure, usually the terminal measure ,

| (2.12) |

where can be either a deterministic or a stochastic process as long as retains the Markov property888For details of the Markov property, please refer to Chapter 7 of Oksendal [15].. For each terminal time point , the random variable , which has no financial interpretation at all, is mapped to the terminal LIBOR rate or swap rate . The former leads to the LIBOR MF models and the latter leads to the swap MF models.999In this report, we focus on the swap MF models rather than the LIBOR MF models, both of which nevertheless work in the same fashion. Each of these state variables is originally modelled in market models by a stand-alone process or . In such a setting, we can avoid Monte-Carlo simulations, which reduces the computing time significantly in comparison with market models for the same task [20]. Because of the freedom to choose the functional forms of state variables, MF models retain the advantage of accurate calibration to relevant market prices. Besides, MF models are capable of controlling the state transition to some extent thanks to the freedom to choose the volatility process . We will discuss these aspects in more detail in the following sections.

2.2 Markov-Functional Interest Rate Models

This section explains the details of Markov-Functional models and is based on Hunt-Kennedy-Pelsser [12], Pelsser [19] and Regenmortel [23].

2.2.1 Assumptions of MF Model

-

•

Assumption 1 The state of the economy at time t is entirely described via some low-dimensional Markov process, which will be denoted by . A convenient and typical choice of the process has the following form

(2.13) where is a deterministic function. Thus this corresponds to a one-factor MF model. Actually, throughout this report, we stick to the one-dimensional MF model.

To be more concrete, we assume that the numeraire discount bond is a function of . This implies that is totally determined by . By applying the martingale property it can be shown that every discount bond , for all , is a function of :(2.14) Note , where is the information generated by on .

Conditional on the random variable follows, for , a normal probability distribution with mean and variance .101010For derivation, please refer to Appendix C.1. The probability density function of given is denoted by and can be expressed as(2.15) -

•

Assumption 2 The terminal swap rate , for all , is a strictly monotonically increasing function of .

2.2.2 What is Modelled in MF?

Remark: From now on we are applying the simplified notation

defined in Appendix A.2.

An interest rate model should be able to describe the distribution

of the future yield curve, whose fundamental quantities are discount

bonds. For pricing Bermudan swaptions, it is more convenient to use

a swap Markov-functional model that is calibrated to the underlying

European swaptions. Roughly speaking, by the relationship (see

Equation A.4 and A.2)

| (2.16) |

we should determine ’s functional form, shown in Figure 2.1, such that fits its market distribution. Actually we only need to determine the functional form of the numeraire discount bond , the shadowed state variables in Figure 2.1, as functional forms of all other discount bonds can be determined by Equation 2.14 and 2.15,

| (2.17) | |||||

where denotes the probability density function of

conditional on .

In conclusion, given a specified process, we determine the functional forms of such that the model is calibrated to the market prices of European swaptions.

2.2.3 Black-Scholes Digital Mapping

Let’s illustrate the mapping from to assuming

the terminal swap rate is lognormally distributed and

thus smile is not taken into account. We conduct the mapping via

Digital swaptions111111For details of Digital swaption, please

refer to Appendix A.1 for the sake of its relatively

simple payoff. This is why it’s called a ”Digital Mapping”.

Because of the lognormal assumption above, the digital mapping here

is call the ”Black-Scholes Digital Mapping”.

The functional form of the numeraire discount bond

() is determined by following a backward induction

process from to .

First the value at time 0 of a Digital Receiver Swaption with strike

and maturity , i.e., , is given

by121212For details, please refer to Appendix

A.1.

| (2.18) |

As explained in Appendix A.1 (see Equation

A.11), Digital swaption values across a continuum of

strikes imply the terminal density of the underlying swap rate. In

the Black-Scholes world, this is assumed to be a lognormal

distribution.131313Note this is the only place we should change

in the digital mapping if we want to calibrate the model to the

market smile. More concretely, we use another option pricing model’s

formula for Digital swaption to imply the market distribution.

On the other hand, the option’s value can be expressed under the

terminal measure as

| (2.19) |

By Assumption 2 in Section 2.2.1, we have that is a strictly monotonically increasing function of , which implies that we can invert the function to get a certain such that . Thus can be rewritten as

| (2.20) |

which we denote by a new symbol instead of the original symbol . Applying the martingale property to , we would get

| (2.21) | |||||

where denotes the probability density function of

conditional on and denotes the probability

density function of . Note the functional form of

can be determined by

Equation A.3. Therefore can

be evaluated at least numerically for different values of

which correspond to different values of K observed in the market.

Equating 2.18 and 2.21, we get

| (2.22) |

As is a certain value of , we generalize Equation 2.22 to get the functional form of .

| (2.23) |

Then the functional form of can be determined by rewriting Equation 2.16

| (2.24) |

where has already been calculated in Equation 2.21.

2.2.4 Numerical Solution

In practice, the MF model is solved on a lattice. For each floating reset date , we choose values of from to 141414 denotes the standard deviation of ., or equivalently to with step length , see Figure 2.2, where

An implementation of the MF model relies heavily on the evaluation of expectations using numerical integration routines. The numerical integration adopted was introduced by Pelsser [18], which is outlined as follows151515Detailed explanation of the method can be found in Appendix B.:

-

•

fit a polynomial to the payoff function defined on the grid by applying Neville’s algorithm161616For details of Neville’s algorithm, please refer to Section 3.1 of ”Numerical Recipes in C++” [21].;

-

•

calculate analytically the integral of the polynomial against the Gaussian distribution.

2.3 Volatility Function and Terminal Correlation

2.3.1 Volatility Function and Terminal Correlation

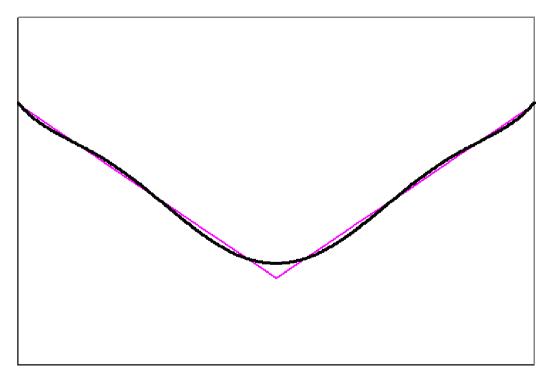

The prices of Bermudan swaptions depend strongly on the joint distribution or the terminal correlations of underlying swap rates .171717This section is based on Pelsser [16][19]. By applying a first order Taylor expansion to , we could get the following linear approximation. It it accurate enough for close to zero, where a majority of the probability mass concentrates181818You will see the validity check for this approximation in Section 3.2.3..

| (2.26) | |||||

Hence for we approximately have

| (2.27) |

The problem in turn transforms to finding the auto-correlation of the process . Pelsser [19] got inspired by the Hull-White model, whose short rate process follows

| (2.28) |

By some algebra, we derive the auto-correlation structure of the short rates depending on the mean-reversion parameter via the relationship191919For derivation, please refer to Appendix C.2.

| (2.29) |

for . If we set process’ volatility function in equation 2.13 to be

| (2.30) |

we would get an equivalent expression for the auto-correlation of the process 202020For derivation, please refer to Appendix C.2.

| (2.31) |

for . Thus, parameter can be interpreted as the mean-reversion parameter of the process . We can see from Equation 2.31 that increasing the mean-reversion parameter has the effect of reducing the auto-correlation between the values of for different floating reset dates . Thus increasing the mean-reversion parameter reduces the auto-correlation between terminal swap rates .

2.3.2 Estimation of the Mean-Reversion Parameter

Because of the ill-liquidity of other exotic interest rate derivatives that contain the information of terminal correlation of co-terminal swap rates, we are left with estimating the terminal correlations by historical data analysis.212121This section is based on Pelsser [16]. The correlation of and , for , is equivalent to the correlation of their log differences and . This is because and are known today, division by which is sort of a normalization. One approach is to estimate the correlation by analyzing the most recently historical time series222222Note we are using small letter to denote a time series of swap rates because they are market quotes. of and . However, this method turns out to give estimates with large standard deviation due to the long lags needed for the calculation of the difference (see [16]). Therefore we instead analyze the time series with shorter lags, i.e., and , where represents the lag size. If , we are virtually analyzing the time series with infinitesimal lags, i.e., and . If we stick to the lognormal assumption, i.e.,

| (2.32) |

by applying It’s lemma we would have

| (2.33) |

If we apply the Girsanov transformation232323For details of Girsanov Theorem, please refer to Chapter 11 of Bjork [3]., i.e., we set

| (2.34) |

where and denote Brownian motions under the new measure, we would have

| (2.35) |

Let’s denote the instantaneous correlation between and by , i.e.,

| (2.36) |

Then the correlation we are interested in can be expressed as

| (2.37) |

The problem thus transforms to a historical estimation242424The instantaneous correlation is the same under the real world measure and risk-neutral measure, because the dynamics under the two measures differ only by the drift term. of the instantaneous correlation . In practice, we could approximately estimate by choosing a smallest possible lag size , that is, one day. How valid this approach is depends on how valid the lognormal assumption is and how valid the approximation of instantaneous correlation by historically estimating the correlation on a daily basis is.

2.4 Bermudan Swaption Pricing under Markov-Functional

In this section, we first discuss the general backward induction method for valuing an American-style option, and then illustrate the pricing procedure under MF’s framework.

2.4.1 American-style Option Pricing in a Discrete Time Model

Let’s express everything in the swap/swaption context. Suppose we are under some risk-neutral measure Q with numeraire B(t) and the American swaption is allowed to exercise at any floating reset date . Then the value of the American swaption 252525An American option applied on a set of discrete time points is literally still a Bermudan option, so we adopt the notation here. at time can be computed backwardly as follows [24],

| (2.38) | |||||

where the payoff of a European swaption at maturity is

| (2.39) |

where is the swap value at time (see Section A.1 for notation).262626 is actually a Q-supermartingale, meaning

2.4.2 Bermudan Swaption Pricing with the MF Model

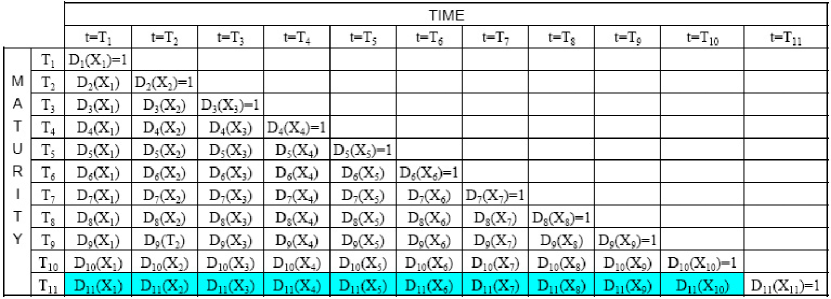

Assume N=4 and we have the LIBOR ”tree” after the digital

mapping,272727 is determined by Equation

A.1. shown in Figure 2.3, we can compute the

corresponding swap value ”tree” and option valuation ”tree”, shown

in Figure 2.4 and 2.5,

respectively. In other words, we ought to determine the functional

forms of and

so as to find out today’s option

value .282828It’s obviously more convenient to get the

functional forms of and

rather than and

.

The functional form of numeraire-discounted swap value can be determined by the backward induction:

| (2.40) | |||||

where is 1 for a payer swap and -1 for a receiver swap. Note there is no cash exchange at time .

The functional form of numeraire-discounted option value

can be determined backwards from

to :

If is not an exercise date, we have

| (2.41) |

If is an exercise date, we have

| (2.42) | |||||

where .

Now we can obtain today’s Bermudan swaption value .

| (2.43) |

Chapter 3 Integration of Volatility Smile

3.1 Incorporating Volatility Smile into the MF Model

In the MF model a smile can be incorporated quite naturally. What is required for this, is a model to obtain swaption prices across a continuum of strikes given a limited number of market quotes.

3.1.1 Interpolation of Implied Volatility

A first approach that might come into one’s mind is to keep the Black-Scholes mapping and interpolate/extrapolate the market quotes to obtain a continuum of implied volatilities as a function of the strike, i.e., . Then, provided that assumption 2 in Section 2.2.1 still holds, the only thing that we need to change in the mapping procedure described in Section 2.2.3, is to replace 111In the lognormal case is constant. in Equation 2.23 with . More precisely, we instead solve numerically the following equation for ,

| (3.1) |

3.1.2 Uncertain Volatility Displaced Diffusion Model

An alternative approach is to base the digital mapping on an option pricing model that includes smile. In other words, we use another distribution rather than the lognormal one to approximate the terminal density of the swap rate, which allows for a good fit to the volatility smile observed in the market. In this project, we will use the Uncertain Volatility Displaced Diffusion model (hereafter UVDD) proposed by Brigo-Mercurio-Rapisarda [6].

In the following, we will first describe the displaced diffusion model which is the simplest extension of the lognormal model that can include skew effects. The description of the UVDD model will follow afterwards.

Displaced Diffusion Model (hereafter DD)

We assume in this setting that the dynamics of the swap rate under the forward measure is as follows,

| (3.2) |

The parameter is called the displacement coefficient. Following the same reasoning from Equation A.6 to A.7, we can derive the closed form solution for the value of a Digital receiver swaption,

| (3.3) |

Similarly, the value of a European swaption is given by

| (3.4) | |||||

where is 1 for a payer European swaption and -1 for a

receiver one.

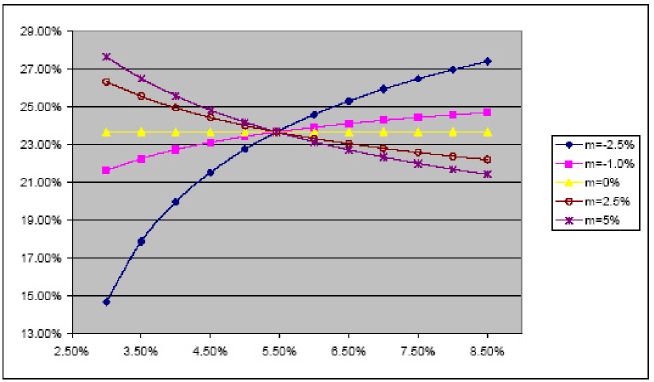

The displacement coefficient can be used to generate an implied volatilities’ skew shape. A positive value of the displacement coefficient generates a downward sloping skew, while a negative value generates an upward slopping skew. The latter is unrealistic and should not be used. We report in Figure 3.1 the implied skew for various values of the displacement coefficient. The case corresponds to the usual lognormal model. We have used the market data corresponding to Data Set I in Appendix E.1.1 and Trade I in Appendix E.2. The tested instrument was a European swaption expiring at the fifth floating reset date, i.e., , with at-the-money swap rate of . The parameter was adjusted such that the implied ATM volatility was the same for all cases. More precisely, we determine such that the UVDD ATM price equals the BS ATM price.

The DD model can only incorporate the volatility skew, but market data suggest that the volatility quotes of swaption is typically a smile shape [9]. Thus the DD model is insufficient for describing the market quotes.

UVDD Model

In the UVDD setup, is assumed to have the following dynamics

| (3.5) |

where is a constant and is a random variable that is independent of and can take the following values,

| (3.6) |

where . Denoting by the risk neutral probability under the forward measure , we have

| (3.7) |

Differentiating Equation 3.7 with respect to , we get the probability density function of ,

| (3.8) |

where is the density of a displaced lognormal variable with constant volatilities . The value of a Digital receiver swaption can be expressed under as follows,

| (3.9) | |||||

Now following once more the same line of reasoning from A.6 to A.7, we derive a closed form solution for the value of Digital receiver swaption,

| (3.10) |

Similarly, the value of a European swaption can be determined analytically by

| (3.11) | |||||

where is 1 for a payer European swaption and -1 for a

receiver one.

We have performed the tests reported in this chapter with two

components (). The model can be expressed in terms of the

following parameters , , ,

, . It can be also expressed in terms of

the parameters , , , with:

| (3.12) |

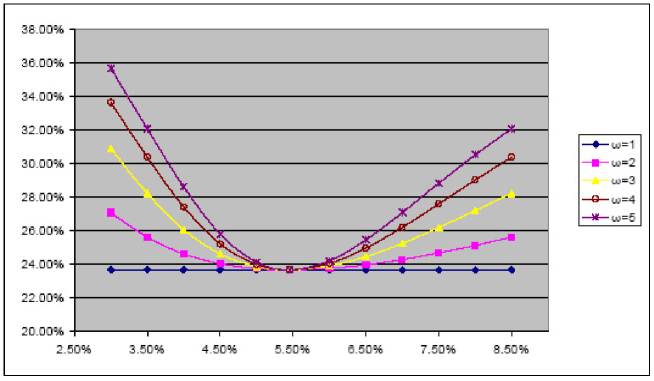

We first report in Figure 3.2 the shapes of the volatility smile obtained by setting to 0.75, to 0 and by varying from 1 to 5. The case reduces to the usual lognormal model. In this test and also the following one, we use the same data set and trade specification as was used in DD case described previously. We again adjust the parameter such that the implied Black volatility corresponding to the at-the-money strike is the same for all the cases. We see that a mixture of lognormal components without displacement produces a symmetric smile centered around the at-the-money strike. The smile shape is more pronounced for higher values of . This is because increasing the value of implies that there are fatter tails (both left side and right side) in the underlying distribution, and thus that away-from-the-money swaptions are more underpriced in a lognormal model.

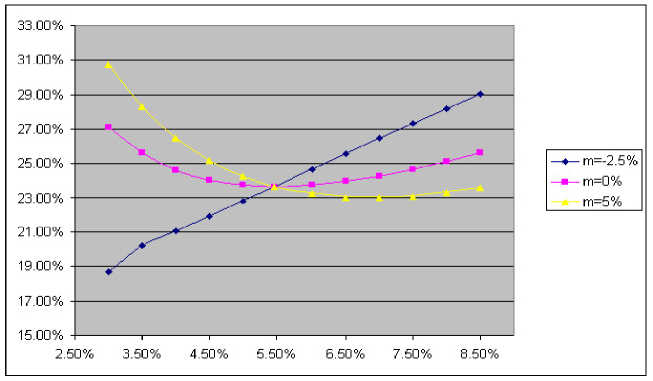

We report in Figure 3.3 the shape of the volatility smile obtained by setting to 0.75, to 2 and by varying from 1 to 5. When is set to zero, a symmetric smile is produced. Assigning a positive value to this parameter puts more weight on low strike and less weight on the high strike. The opposite happens when is set to a negative value. This is because a higher displacement implies a fatter left tail and a thinner right tail of the underlying distribution. Therefore, the UVDD approach allows for combining a symmetric shape of the smile with upward or downward sloping behavior.

3.1.3 UVDD Digital Mapping

We can perform the UVDD digital mapping by applying a small change in the original BS mapping. The BS mapping is explained in Section 2.2.3. In the UVDD digital mapping, the analytical formula for digital swaptions corresponding to the UVDD model (Equation 3.10) should be used instead of the Black digital formula. We get the functional form of by solving the following equation numerically with respect to ,

| (3.13) | |||||

3.2 Test Results of Different Digital Mappings

We have performed a number of tests based on the market data of Data Set I in Appendix E.1 and using the setting of Trade I in Appendix E.2. The tests were run for the following digital mappings:

-

•

case 1: a Black-Scholes mapping;

-

•

case 2: a Displaced Diffusion mapping with ;

-

•

case 3: a Displaced Diffusion mapping with ;

-

•

case 4: a Displaced Diffusion mapping with ;

-

•

case 5: a UVDD mapping with , and ;

-

•

case 6: a UVDD mapping with , and ;

-

•

case 7: a UVDD mapping with , and ;

-

•

case 8: a UVDD mapping with , and .

For cases 2 to 8 we adjust the parameter in order to recover the same ATM volatilities as for case 1. We first discuss the results obtained for some consistency checks. Next, some test results will be shown for the validity of the assumptions made in the MF model and the convergence of the Markov-Functional model with respect to the discretization parameters. Finally, we will discuss the effect of the smile on the value of Bermudan swaptions.

3.2.1 Consistency of European Swaption Prices

To demonstrate the correctness of the implementation, we first compare the European swaption values ( for n=1..10) obtained by the MF model with the analytical formula for each of the eight cases mentioned above. The strike (fixed coupon rate) is set to 5. The results are shown in Table 3.1 to Table 3.4. The first row refers to the 1 into 10 period swaption and the last row to the 10 into 1 period swaption. The results clearly show that the MF model reproduces the values of the underlying Europeans with high accuracy: the relative error is less than 1 bp.

| Analytical values | MF values |

|---|---|

| 0.00 | 0.00 |

| 109.10 | 109.10 |

| 194.40 | 194.40 |

| 241.31 | 241.31 |

| 246.96 | 246.96 |

| 241.18 | 241.18 |

| 208.48 | 208.48 |

| 171.98 | 171.98 |

| 119.22 | 119.22 |

| 64.15 | 64.15 |

| Case 2 | Case 3 | Case 4 | |||

|---|---|---|---|---|---|

| Analytical | MF values | Analytical | MF values | Analytical | MF values |

| 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| 107.86 | 107.86 | 107.25 | 107.25 | 113.05 | 113.05 |

| 194.79 | 194.79 | 194.98 | 194.98 | 193.26 | 193.26 |

| 243.10 | 243.10 | 244.01 | 244.01 | 236.28 | 236.28 |

| 249.43 | 249.43 | 250.70 | 250.70 | 240.23 | 240.23 |

| 244.12 | 244.12 | 245.67 | 245.67 | 233.35 | 233.35 |

| 211.25 | 211.25 | 212.72 | 212.72 | 201.21 | 201.20 |

| 174.52 | 174.52 | 175.88 | 175.88 | 165.46 | 165.46 |

| 121.07 | 121.07 | 122.05 | 122.05 | 114.54 | 114.54 |

| 65.21 | 65.21 | 65.79 | 65.79 | 61.52 | 61.52 |

| Case 5 | Case 6 | ||

|---|---|---|---|

| Analytical | MF values | Analytical | MF values |

| 0.01 | 0.01 | 0.35 | 0.35 |

| 109.55 | 109.55 | 111.91 | 111.91 |

| 194.42 | 194.42 | 194.53 | 194.53 |

| 241.63 | 241.63 | 243.31 | 243.31 |

| 247.51 | 247.51 | 250.35 | 250.34 |

| 241.90 | 241.90 | 245.61 | 245.60 |

| 209.14 | 209.13 | 212.49 | 212.48 |

| 172.62 | 172.62 | 175.89 | 175.88 |

| 119.68 | 119.68 | 122.00 | 122.00 |

| 64.45 | 64.45 | 65.95 | 65.95 |

| Case 7 | Case 8 | ||

|---|---|---|---|

| Analytical | MF values | Analytical | MF values |

| 0.01 | 0.01 | 0.06 | 0.06 |

| 108.31 | 108.31 | 109.06 | 109.06 |

| 194.81 | 194.81 | 194.84 | 194.84 |

| 243.42 | 243.42 | 243.95 | 243.95 |

| 249.97 | 249.97 | 250.87 | 250.87 |

| 244.84 | 244.84 | 246.03 | 246.03 |

| 211.91 | 211.91 | 212.99 | 212.98 |

| 175.17 | 175.17 | 176.22 | 176.22 |

| 121.53 | 121.53 | 122.28 | 122.28 |

| 65.52 | 65.52 | 66.01 | 66.01 |

3.2.2 Convergence of the Numerical Algorithm

The MF model is based on a lattice. In this section, we check the convergence of the numerical integration with respect to the discretization of the lattice. There are two parameters controlling the level of discretization, namely,

-

•

The range of values that can take expressed in units of its standard deviation, i.e. ”Number of Deviations”;

-

•

The number of discrete points per standard deviation, i.e. ”Steps per Deviation”.

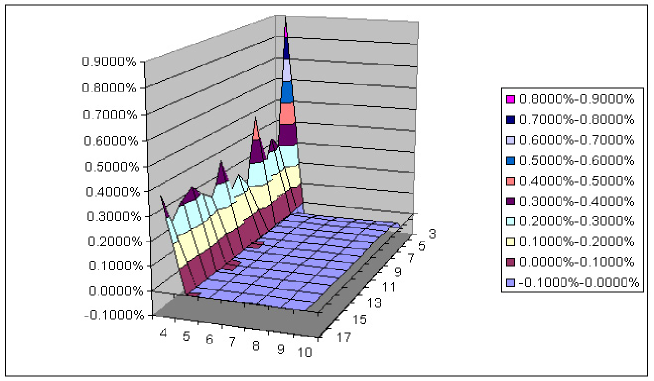

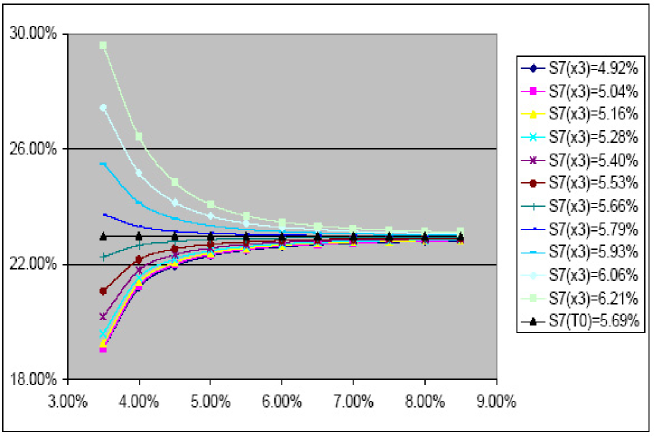

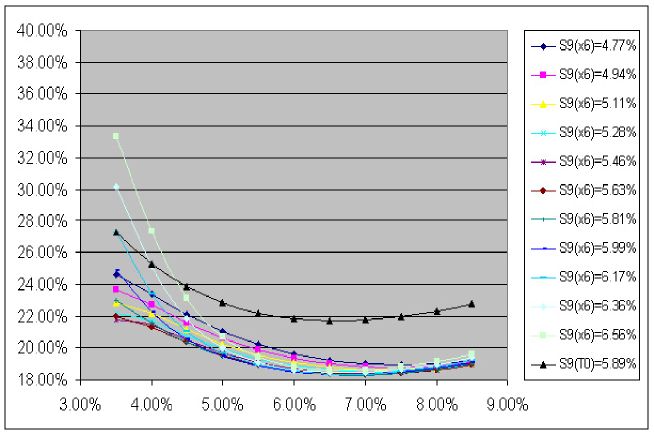

To access the convergence of the method, it is sufficient to look at the pricing of the European swaptions as this is basically exposed to the discretization error in the numerical integration. We consider the swaption which expires at and case 8 of Section 3.2.1. The analytical value of this European swaption is 212.986 bp. The relative error is shown in Figure 3.4, where the ”Steps per Deviation” ranges from 3 to 17 and the ”Number of Deviations” from 4 to 10. A very good convergence is obtained by using the following setting: ”Steps per Deviation” higher than 5 and ”Number of Deviations” higher than 4.

3.2.3 Assumption/Approximation Validity Check under UVDD Mapping

Before continuing further with pricing, we would like to check the validity of the assumptions made in Section 2.2.1. To summarize the following assumptions were made:

-

•

The numeraire discount bond is a function of ;

-

•

The terminal swap rate is a strictly monotonically increasing function of .

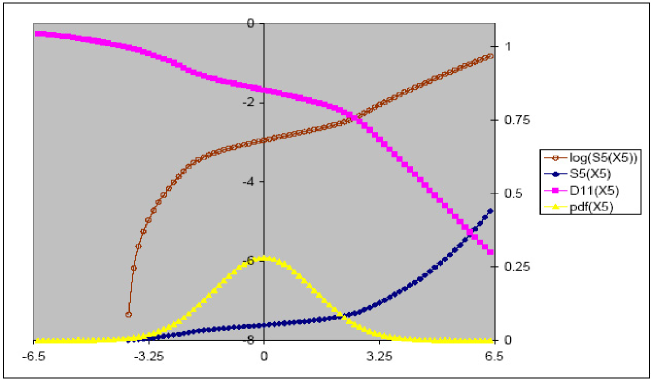

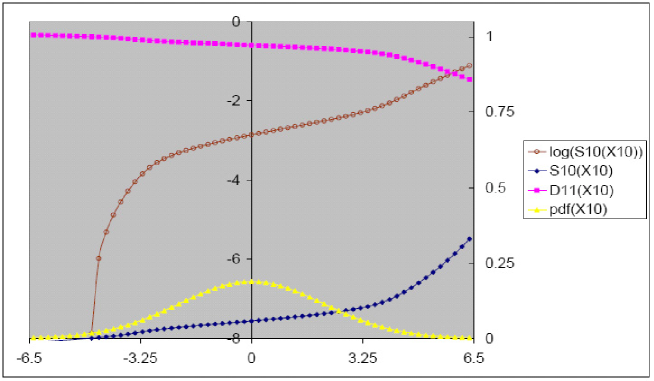

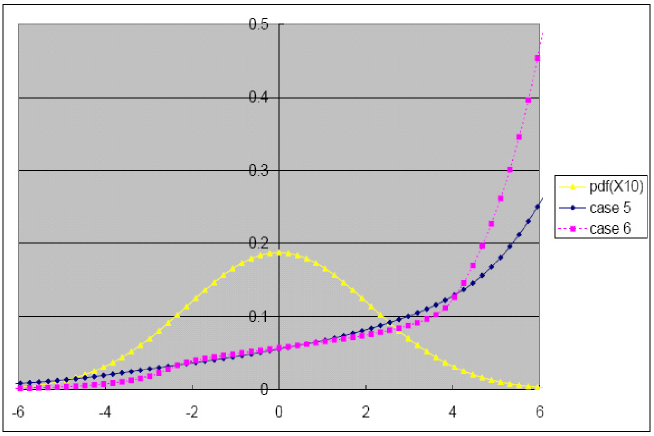

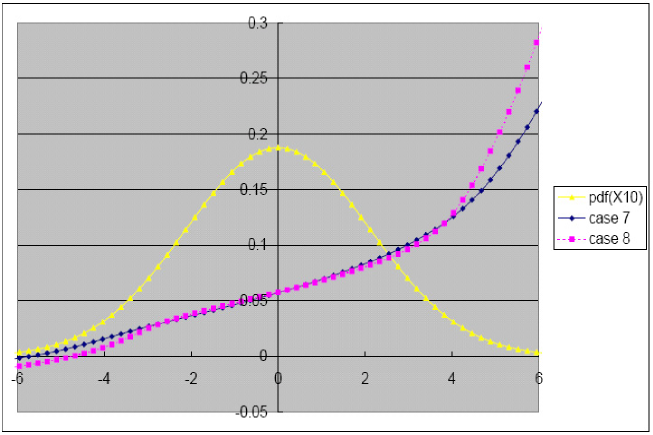

In Figures 3.5 and 3.6, we show the functional behavior of and , respectively, for and and corresponding to case 8. Also included in these figures is the probability density function of . The following can be observed from these plots:

-

•

The numeraire discount bond and are functions monotonically decreasing in and , respectively;

-

•

The swap rate and , respectively, are functions strictly monotonically increasing in and .

This demonstrates that the assumptions mentioned above are still

valid for the UVDD mapping.

We would also like to check the linear approximation made in

Equation 2.26 of Section 2.3.1. Here we

repeat that equation below,

We report in Figure 3.5 and 3.6333In these two figures only for is related to the first y-axis in the middle. the results for and , respectively, and using the setting corresponding to case 8. We see that are linear functions of and for and close to zero. It should be noted that the approximation is even valid for the range of X where the majority of the probability mass is concentrated. This demonstrates that in the UVDD mapping the linear approximation is still valid.

3.2.4 Effect on Bermudan Swaption Prices

To test the impact of the shape of the implied volatility smile on the value of Bermudan swaptions, we consider the following trades and settings:

-

•

A Bermudan swaption with the right to exercise at reset dates , , , , and ;

-

•

All the different cases (case 4 eliminated) with the strike set to , and , respectively;

-

•

Forward par swap rates , , , , and were set to , , , , and , respectively. The mean-reversion parameter was set to .444At this point we don’t calibrate the mean-reversion parameter using empirical data. can be seen as a benchmark mean-reversion level.

The results are reported in Table 3.5. Case 1 is

the standard lognormal case.

| Strike | 3.50% | 5.50% | 7.50% |

|---|---|---|---|

| case 1 | 541.00 | 228.45 | 90.11 |

| case 2 | 548.63 | 228.45 | 82.32 |

| case 3 | 552.71 | 228.48 | 78.23 |

| case 5 | 545.76 | 226.27 | 95.52 |

| case 6 | 567.78 | 223.78 | 126.56 |

| case 7 | 553.17 | 226.54 | 88.30 |

| case 8 | 560.57 | 223.97 | 99.17 |

For the displaced diffusion cases, i.e., cases 2-3,

increasing the displacement coefficient leads to an increase in the

implied volatilities corresponding to low strikes and to a decrease

in the implied volatilities corresponding to high strikes. This

results in a fatter left tail and a thinner right tail for the

underlying’s distribution. Thus we see an increase in the

displacement coefficient results in an increase in the value of a

deep ITM Bermudan and a decrease in the value of a deep OTM

Bermudan.

For the UVDD cases, i.e., cases 5-6 or 7-8, more pronounced

smiles result in a higher price for a deep ITM/OTM Bermudan

swaption. This can be explained in a similar way as above since a

more pronounced smile leads to fatter tails (both left side and

right side) in the distribution of the underlying. However, for the

near-the-money Bermudans, we see that more pronounced smiles result

in a lower price. This is counter-intuitive and is contrary to the

findings of Abouchoukr [1]. We emphasize that the

tests in that study were based on different market data and trade

specifications. It was found that more pronounced smiles result in a

higher near-the-money Bermudan price. To make sure that this result

is not due to numerical artifacts, we have increased the ”Steps per

Deviation” and ”Number of Deviations”555Please refer to

Appendix E.2 for the grid specification. to 100

and 20, respectively. The findings did not changed. A possible

explanation for this phenomenon is provided in Appendix

D. It is shown that this behavior is

plausible in the case of a simple example.

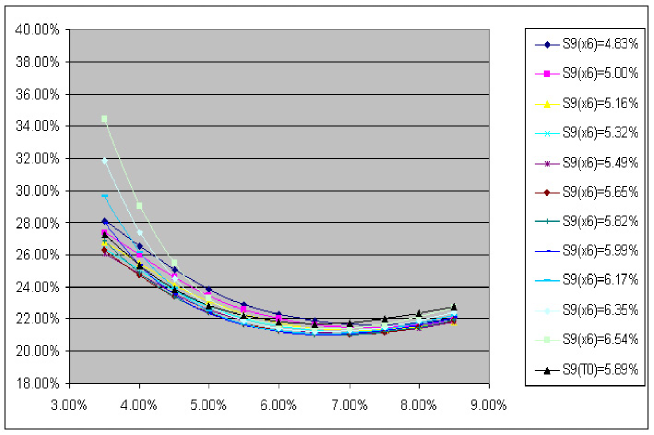

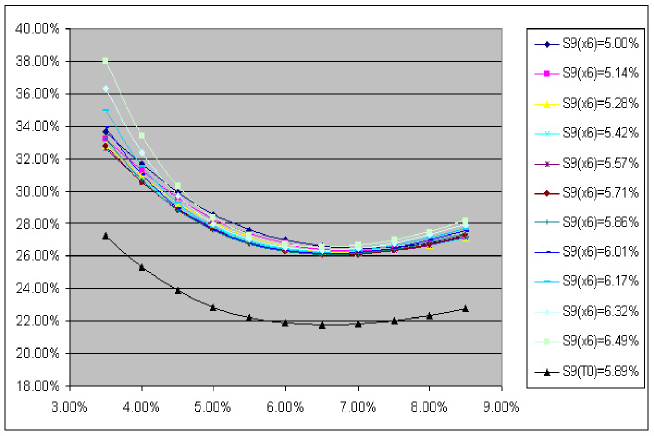

In order to analyze the impact of the mean-reversion parameter, we

valued the Bermudan swaption for case 1 and 8 for a wider range of

strikes and two different mean-reversion levels ( and ,

respectively). The results are shown in Table 3.6.

As expected, in both cases, the European value converges to the

underlying swap value as the strike gets lower. Moreover, in both

cases, the Bermudan swaption value converges to its European

counterpart as the strike gets lower. This is because for a payer

Bermudan it becomes more likely to exercise early as the strike gets

lower.

To summarize the following can be concluded from the results presented in Table 3.6:

-

•

Incorporating the volatility smile has a significant impact for the away-from-the-money Bermudan prices, while it has a relatively marginal impact for the near-the-money Bermudan prices. This is inline with the observation that the effect of smile on the Europeans is more pronounced as one moves away from the ATM level;

-

•

For payer Bermudans, increasing the mean-reversion level gives rise to an increase of the overall level of Bermudan prices. This can be roughly explained as follows. Increasing the mean-reversion level will reduce the terminal correlations of swap rates and for (see Section 2.3.1). In our case, if in the future state at , was below the strike, a higher mean-reversion level would increase the likelihood that the economy would transform to a state at a further future time for in which would be higher than the strike, and thus increasing the value of the Bermudan.

Finally, the increase is more pronounced for the near-the-money Bermudans compared to the away-from-the-money ones. This can be explained as follows. If the strike is much lower than the ATM level, the Bermudan will be less sensitive to the terminal correlations as the likelihood of early exercising at is quite high. If the strike gets much higher than the ATM strike level, this effect would become less pronounced too as the likelihood of postponing the exercise later in future will increase.

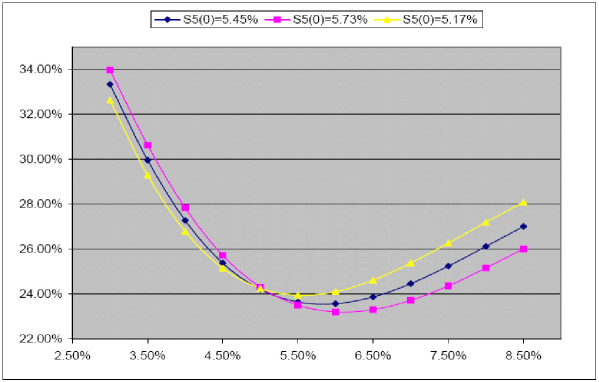

| Strike | 3.00% | 3.50% | 4.00% | 4.50% | 5.00% | 5.50% |

| Swap value | 639.98 | 509.63 | 379.28 | 248.93 | 118.58 | -11.77 |

| European (BS) | 645.22 | 526.08 | 418.22 | 324.74 | 246.96 | 184.52 |

| Bermudan MR=0% (BS) | 652.52 | 541.00 | 442.23 | 357.49 | 286.60 | 228.45 |

| Bermudan MR=10% (BS) | 656.70 | 547.48 | 450.62 | 367.07 | 296.63 | 238.30 |

| Bermudan MR=0% (UVDD) | 675.22 | 560.57 | 455.04 | 362.39 | 285.15 | 223.97 |

| Bermudan MR=10% (UVDD) | 679.24 | 565.75 | 461.58 | 370.09 | 293.51 | 232.50 |

| European (UVDD) | 663.95 | 546.10 | 435.07 | 335.24 | 250.87 | 184.29 |

| Strike | 6.00% | 6.50% | 7.00% | 7.50% | 8.00% | 8.50% |

| Swap value | -142.12 | -272.47 | -402.82 | -533.17 | -663.52 | -793.87 |

| European (BS) | 135.85 | 98.84 | 71.23 | 50.95 | 36.24 | 25.67 |

| Bermudan MR=0% (BS) | 181.41 | 143.75 | 113.81 | 90.11 | 71.40 | 56.65 |

| Bermudan MR=10% (BS) | 190.64 | 152.11 | 121.18 | 96.49 | 76.83 | 61.23 |

| Bermudan MR=0% (UVDD) | 177.84 | 143.48 | 118.04 | 99.17 | 84.85 | 73.67 |

| Bermudan MR=10% (UVDD) | 186.11 | 151.38 | 125.55 | 106.23 | 91.43 | 79.80 |

| European (UVDD) | 135.00 | 100.33 | 76.63 | 60.49 | 49.23 | 41.02 |

| MR denotes the mean-reversion level. | ||||||

Chapter 4 Future Smile and Smile Dynamics

4.1 Future Volatility Smile Implied by MF Models

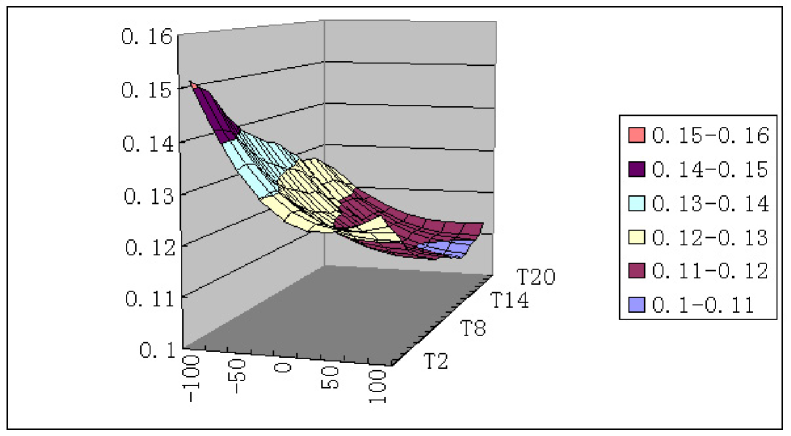

It is well-known that the value of a path dependent option is highly sensitive to the future volatility smile (see e.g. Ayache [2] and Rosien [22]). The future volatility smile is defined as follows. Today we observe market quotes for European swaptions expiring at . We calibrate our model to the vanilla options such that the terminal density of the underlying is consistent with the market. We now move to a future date which is still before expiry, and use our calibrated model to compute, at that time, values of the vanilla options across strikes. Conditional on the state of the future date, we can invert the option values to get the implied smile, i.e. the future volatility smile. It should be noted that in the MF model the state transition111For instance, the probability that goes to . is controlled by the mean-reversion parameter.

Let’s now explain in more detail how to obtain future smiles in the MF models. For ease of calculation, we choose the future date, denoted by , to be one of the floating reset dates, i.e., for . Suppose at time , . Conditional on this state, the value of the European swaption is determined as described in Section 2.4.2. In order to get the implied volatility from the price, we still need to determine and . This can be done by using the functional form of (k=n,..,N+1) which can be obtained through numerical integration on the calibrated lattice. For more details we refer to Section 2.2.2. Note that all these computations depend on the conditional expectation , for and , which is ultimately subject to the mean-reversion parameter value.

4.1.1 Future Volatility Smile Implied by the BS Mapping

We first investigate the future volatility smile implied by the Black-Scholes digital mapping, i.e., the future volatility smile implied by case 1 in Section 3.2. The test was run for a payer swaption expiring at the seventh floating reset date, i.e., . The at-the-money swap rate was around , and the mean-reversion parameter was set to zero. We calculated the future smiles standing at conditional on different future states 222 is the state variable in MF. We chose, by trial and error, different states from the lattice such that swap rates were in the desired range. such that the underlying swap rate ranges from to . The corresponding future smiles are reported in Figure 4.1. In the case of the Black-Scholes model we expect the future smile to be flat. We see that this is not the case in the MF model with the BS mapping. However, the future smiles obtained for the different strikes (low and high, respectively) are compensating each other. More precisely, the fat-tailed distributions implied for high swap rates compensate the thin-tailed distributions implied for low swap rates. Therefore, on an integrated level we still may obtain a flat smile.

4.1.2 Future Volatility Smile Implied by the UVDD Mapping

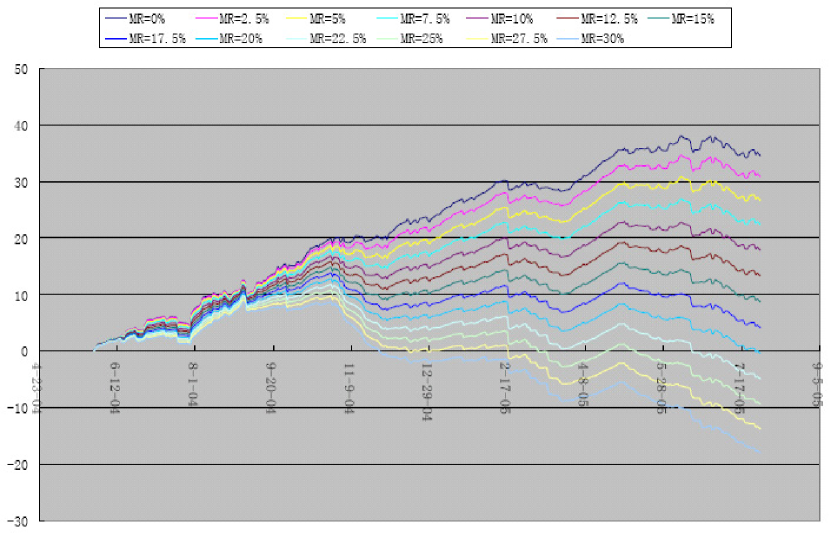

We will now investigate the future volatility smile implied by the UVDD digital mapping, more precisely, the future volatility smile implied by case 8 in Section 3.2. The test was run for a payer swaption expiring at the ninth floating reset date, i.e., . The at-the-money swap rate was . We calculated the future smiles standing at . We adjusted ’s value such that the underlying swap rate varies approximately from to . In order to study the effect of the mean-reversion parameter, we considered three MR levels, namely , , and 333A mean-reversion speed of 30% is very unrealistic. We set this exaggerated value just for illustrative purposes., respectively. The results of these three tests together with today’s smile are reported in Figure 4.2, 4.3 and 4.4, respectively. We see that increasing the mean-reversion level has the effect of increasing the overall level of the future smiles. This can be explained as follows. For close to zero444This is also the range where the majority of the probability mass is concentrated., , can be approximated as follows,

| (4.1) | |||||

The correlation between the future underlying level and the terminal underlying level is given by,

| (4.2) |

Here we use the analytical form of from

Section 2.3.1, and is the mean-reversion parameter.

Therefore, increasing the mean-reversion parameter has the

effect of reducing the correlation between the future underlying

level and the terminal underlying level

. This implies that the average volatility within the

time period increases, which is consistent with the

phenomenon we observe in Figure 4.2,

4.3 and 4.4.

In conclusion, by calibrating the mean-reversion parameter to the

relevant market information555For details, please refer back

to Section 2.3.2 for the relevant discussion.,

the MF model is able to control the future smiles to some extent.

4.2 Smile Dynamics Implied by the UVDD Model

Many previous studies [2][9][22][25] point out that the smile dynamics implied by an option pricing model indicates whether the model is able to produce good hedge ratios. Let’s take a look at an European option and a model . We define the implied volatility, , as the volatility that should be used in the Black model to match the value of this option obtained using model ,

| (4.3) |

where denotes the value of the European option as obtained by model . By Equation 4.3, we can obtain the implied Black volatility , which is a function of the underlying with parameters strike and maturity , from the prices implied by the model.

The delta hedge ratio of this model, , is given by,

| (4.4) | |||||

From Equation 4.4, we see that the validity of the delta ratio generated by model is subject to the sensitivity . This is what we mean by the smile dynamics of a model. In Ayache [2] and Rosien [22], they entitle a wider concept to smile dynamics, which also covers the structure of conditionals666We refer back to Section 4.1 for the relevant discussion. apart from this sensitivity. In our report, we stick to this definition of the smile dynamics777This definition is equivalent to the ”local smile dynamics” in Rosien [22]., i.e.,

| (4.5) |

The smile dynamics has been a point of discussion for many models. It is well-known that the stochastic volatility models show a sticky delta behavior888A stick delta smile dynamics means the implied volatility stays the same for every moneyness, which is defined as underlying’s level divided by strike. This equivalently means the volatility smile slides along the strike axis., while local volatilty models may predict the opposite smile dynamics [9]. To study the smile dynamics of the UVDD model, we have calculated the smile dynamics by the following cases:

-

•

We first considered a digital mapping corresponding to case 6 of Section 3.2, i.e., the model has no displacement but is a purely Uncertain Volatility (UV) model. Moreover, a swaption expiring at the fifth floating reset date, i.e., , with at-the-money swap rate of was considered. The first experiment was done by bumping up/down the yield curve by 50 bp999This is equivalent to bumping only the relevant part of the yield curve, i.e., from ’s yield to ’s yield. so that the underlying swap rate increases/decreases to , respectively. We use the calibrated UV model corresponding to the un-bumped case. The volatility smiles are shown in Figure 4.5. We observe a sticky delta smile dynamics. This is not surprising as the UV model falls into the category of stochastic volatility models, whose smile dynamics has typically a sticky delta effect [22];

-

•

Because bumping the yield curve also changes the PVBP, , (see Equation A.9), in the second experiment, we have bumped up/down only the discount factor 101010This is unrealistic in hedging simulations as in practice the interest rates risk is delta-hedged using swaps. by an amount of 100 bp so that only increases/dereases to while retains at the original level. The implied volatility smiles are reported in Figure 4.6. We observe the same sticky delta phenomenon as was obtained in the first experiment.

We repeated these two experiments for case 8 in Section 3.2, i.e., the UVDD model. The corresponding results are shown in Figure 4.7 and 4.8, respectively. In both figures, we see the ATM implied volatility is sloping down and the smile moves in the same direction as the underlying’s movement. This is qualitatively consistent with the market observation according to Hagan [9].

Chapter 5 Calibration of UVDD Model

In this section, we will first discuss the different choices that can be made in the calibration procedure, namely: minimization of the error in terms of option prices or in terms of implied volatilities. Next, we will discuss the results that have been obtained using different settings in the calibration procedure.

5.1 Calibration Methods

We may calibrate the UVDD model by minimizing the error in terms of option prices (OP) across strikes, that is,

| (5.1) |

where

| (5.2) |

Alternatively, we may instead minimize the error in terms of implied volatilities (IV), that is,

| (5.3) |

where

| (5.4) |

However, in practice, solving the first optimization problem does not mean that we have an optimal solution for the other, and vice versa. We will explain this below. Due to the relationship,

| (5.5) |

we can derive the following relation after some algebraic manipulations,

| (5.6) |

First note that stays in a relatively narrow

range across strikes, while and may

vary widely subject to the strike . If is

very big or is very small,

can still be large even for very

small values of . It will be the

other way around if is very small or

is very big. This means that in practice, it is very difficult to

satisfy both criteria simultaneously.

We choose to minimize the error in terms of option prices instead of

implied volatilities because of the following reasons:

-

•

We want to get a consistent terminal density of the underlying by the calibration procedure. The implied density is directly sensitive to the accuracy in terms of option prices (see Equation A.11). On the other hand, by Equation A.11, we may have

(5.7) Please note that is directly sensitive to the accuracy in terms of implied volatilities. This means that a small minimization error in terms of implied volatilities may lead to a large error in the value of because of a high vega level.

-

•

Computing is much faster compared to computing . This is because for the latter we have to include an extra step in the minimization procedure, in which the implied volatility is obtained from the option price.

In the calibration we use only two components for the UVDD model, i.e., , and thus we can alternatively use the parametric scheme described in Equation 3.12. We do this because of the following reasons:

-

•

If , every parameter plays a clear role: controls the level of the smile/skew; controls the implied volatilities’ skewness; and are responsible for the convexity, i.e., the shape of the smile. But if , the interpretation for each parameter is not that clear any more;

-

•

As we will see in the next section, a mixture of two lognormal distributions is rich enough for fitting the market prices.

Furthermore, in the calibration, we fix and thus have only

three free parameters (, and

). We may do this because and control similar

features of the implied volatilities.

Now the calibration problem reduces to

| (5.8) |

where

| (5.9) |

We set because the case of would generate an

unrealistic shape of implied volatilities111For details,

please refer to Section 3.1.2.

We are using the NL2SOL minimizer in the calibration222For

details of the NL2SOL algorithm, please refer to Dennis-Gay-Walsh

[7].. NL2SOL is an unconstrained minimizer. Thus we

need to transform our bounded model parameters to unbounded ones:

5.2 Calibration Results

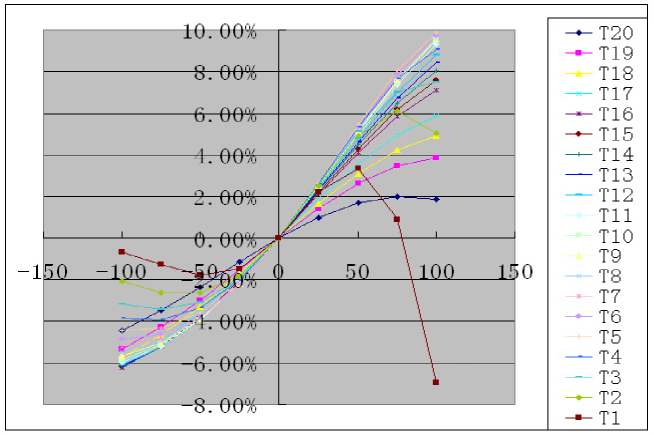

We run our tests based on the market data corresponding to Data Set II in Appendix E.1.2, which is for the EURO market, and used the setting of Trade II in Appendix E.2. We calibrate the following models to all co-terminal swaptions, for n=1,..,20:

-

•

case 1: a Black model, that is, we take the ATM quote as the flat volatility. This case serves as a benchmark for the relative error when smile is not taken into account;

-

•

case 2: a lognormal model, that is, a reduced Displaced Diffusion model with . In this case, we are not necessary fitting the ATM volatility;

-

•

case 3: a Displaced Diffusion model with ;

-

•

case 4: a UVDD model for and ;

-

•

case 5: the same model as in case 4, but the calibration is done in terms of implied volatilities instead of options prices;

-

•

case 6: a UVDD model for and .

For each option maturity , we calibrate the

model to market prices333Except for case 5, in which the

calibration is to implied volatilities. for strikes where the

offset relative to the ATM point varies from -100bp to 100bp, in

total 9 quotes444More precisely, there are quotes with offset

of -100bp, -75bp, -50bp, -25bp, 0, 25bp, 50bp, 75bp and 100bp. See

Data Set II in Appendix E.1.2.. These 20 input

volatility skews/smiles are shown in Figure

5.1. The relative error for the calibration

of the above models in terms of option prices555Except for

case 5, in which the relative error is in terms of implied

volatilities. is shown from Figure 5.2 to

5.7, respectively. The average absolute

error is also listed in the legend of each figure.

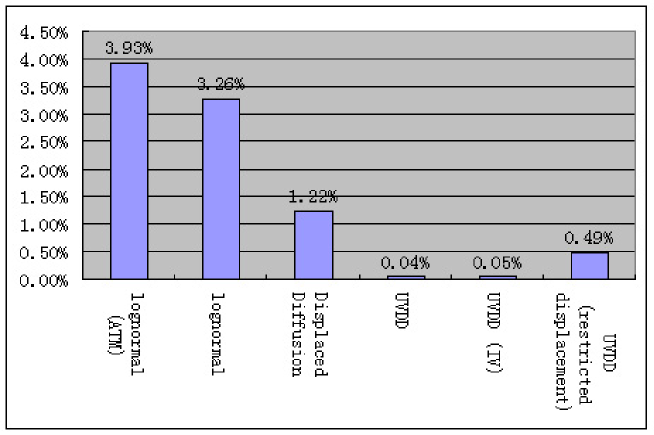

From Figure 5.2 to 5.4,

we see that the Displaced Diffusion model improves the fitting to

market prices significantly than the Black model. From Figure

5.4 and 5.5, we see that

the UVDD model further improves the fitting to market prices

significantly than the Displaced Diffusion model. In this test, we

don’t see from Figure 5.5 and

5.6 any difference between the

calibrations in terms of option prices and implied volatilities. A

comparison for the relative error in all the cases is shown in

Figure 5.8.

Sometimes, if we want to get a very good fit to the market, the

calibrated parameter can be extremely large666This

doesn’t happen in the test here., for instance, more than 100, and

in the same time the calibrated and can be

extremely small, for instance, less than 0.01bp. being 100

means that a negative swap rate very close to -10000% is allowed in

the model, which is obviously unrealistic. Therefore, we prefer a

local solution which leads to realistic parameters over a global

solution which may be unrealistic. This is why we have restricted

the displacement parameter in case 6. We see in Figure

5.7 that restricting within

still gives us a reasonably good fit.

![[Uncaptioned image]](/html/1404.6120/assets/x20.png)

5.3 Terminal Density Implied by the UVDD Model

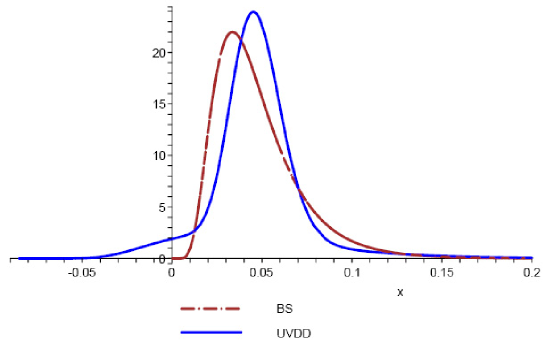

Another interesting quantity is the terminal density implied by the model for the underlying swap rate. We study this for the underlying rate with maturity at corresponding to case 4 of Section 5.2. The input implied volatility quotes are shown in Figure 5.9. The ATM strike level is . The probability density function is plotted in Figure 5.10, and the calibrated model parameters are listed below.

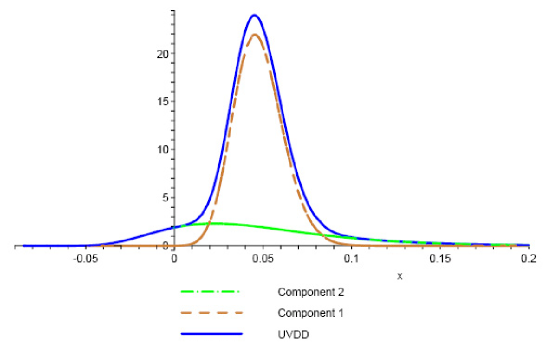

In Figure 5.10, the implied distribution by taking only the ATM volatility, i.e., the counterpart lognormal distribution, is plotted as well. We see that the UVDD model allows for negative swap rates (down to almost ) which is unrealistic. However the negative swap rates have small densities (). Such a small fraction of negative swap rates leads to a left-side fat tail, and thus helps the model to generate the skew effect. Figure 5.11 shows the two lognormal components of the implied distribution, each of them scaled by their weight factor.

Chapter 6 Hedging Simulations

6.1 Overview of the Hedging Simulations

We have performed our hedging simulations on a 10 year Bermudan swaption with the right to exercise at floating reset dates , for . The trade is running from May 28th 2004 to July 29th 2005 (in total 14 months). The trade specification is shown in Table E.6 of Appendix E.2. The market data for the hedge tests, part of which was created synthetically based on the available data111All the available market data is for the EURO market., is presented in Section 6.2. We have performed both delta and delta+vega hedgings to the smile and non-smile Bermudans222The smile Bermudan is the abbreviation for a Bermudan swaption which is valued by taking volatility smiles into account. The non-smile Bermudan is the abbreviation for a Bermudan swaption which is valued without taking volatility smiles into account.. The details of the hedging strategies will be explained in Section 6.3. The calculation of delta and vega ratios will be elaborated in Section 6.4. Below we summarize the most important conclusions from the conducted hedging simulations:

-

•

The smile model333The ”smile model” is an abbreviation for the MF model with UVDD digital mapping. outperforms the non-smile model444The ”non-smile model” is an abbreviation for the MF model with Black-Scholes digital mapping. in both delta hedging and delta+vega hedging simulations. In both the smile and non-smile cases, a delta hedging reduces the profitloss effect of the unhedged Bermudan trade significantly, and a delta+vega hedging further improves the delta hedging performance significantly. Besides, a delta+vega hedging reduces significantly the oscillation of the hedged NPV compared to the corresponding delta hedging, but doesn’t affect the drift level of the hedged NPV. The above conclusions will be drawn gradually from Section 6.5.1 to 6.5.3;

-

•

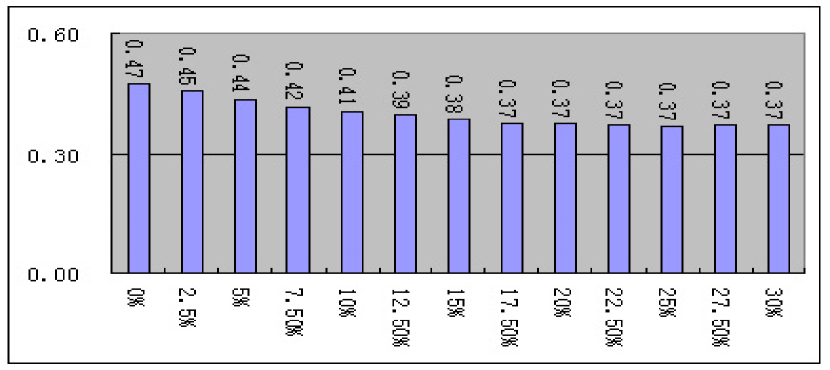

The change from rolling the vega positions from daily to monthly has little impact on the delta+vega hedged NPV. The relevant details can be found in Section 6.5.1;

-

•

Increasing the mean-reversion parameter reduces the drift of the hedged NPV, but doesn’t affect its oscillation. The relevant details are in Section 6.5.4.

6.2 Market and Synthetic Data

6.2.1 Available Market Data

Yield Curve Data

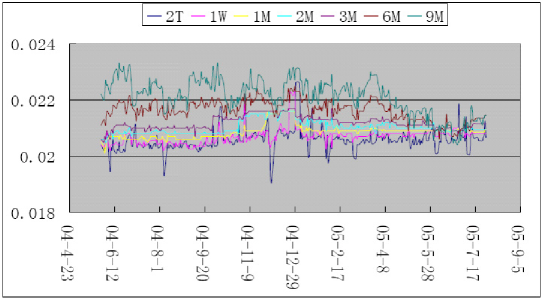

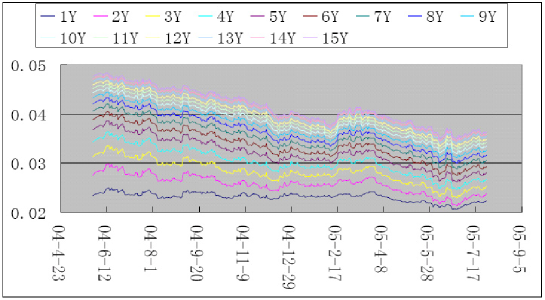

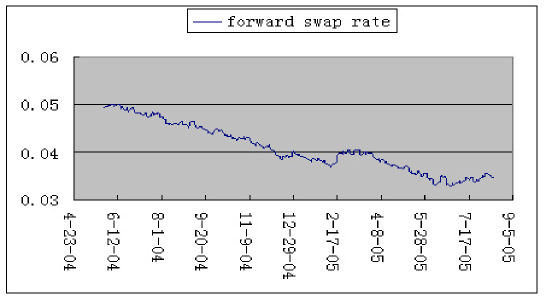

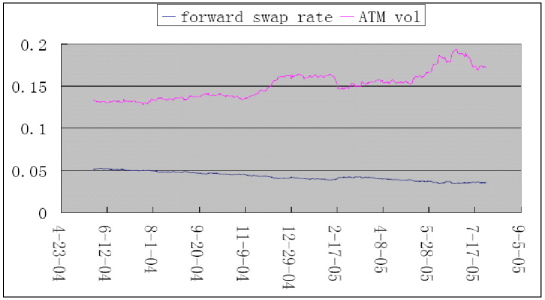

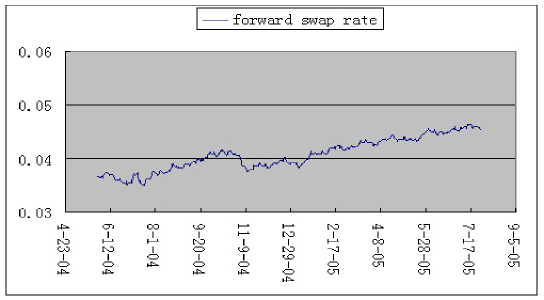

There are two kinds of yield curve related data. The first one is the deposit rates of 2 days, 1 week, 1 month, 2 months, 3 months, 6 months and 9 months, all shown in Figure 6.1. The second one is the spot-starting swap rates with tenors from 1 year to 15 years, shown in Figure 6.2. The deposit rates are used to construct the short-end of the yield curve. The spot-starting swap rates are used to construct the long-end of the yield curve. For every day in the 14 month hedge period, the yield curve is bootstrapped from these deposit rates and spot-starting swap rates.555The bootstrapping is done by using ABN AMRO’s Common Analytics Library. We use this library as a black box. From the constructed yield curves, we calculate the forward swap rates. For example, Figure 6.3 shows the time series of the forward swap rate corresponding to the underlying co-terminal swap which starts at .

Swaption Volatility Data

We have access to daily ATM implied volatilities of European swaptions. Each European swaption has two attributes, the expiry and tenor. The expiry can typically take the following 11 values: 1 month, 3 months, 6 months, 1 year, 2 years, 3 years, 4 years, 5 years, 7 years, 10 years and 15 years. The tenor takes one of the 10 values from 1 year to 10 years. Thus every day there are in total 110 ATM quotes available for the European swaptions. From these quotes, we get the ATM volatilities by applying a two-dimensional linear interpolation. For example, Figure 6.4 shows the time series of the ATM volatilities of the European swaption corresponding to underlying co-terminal swap which starts at . The time series of the corresponding forward swap rates is plotted in the figure as well.

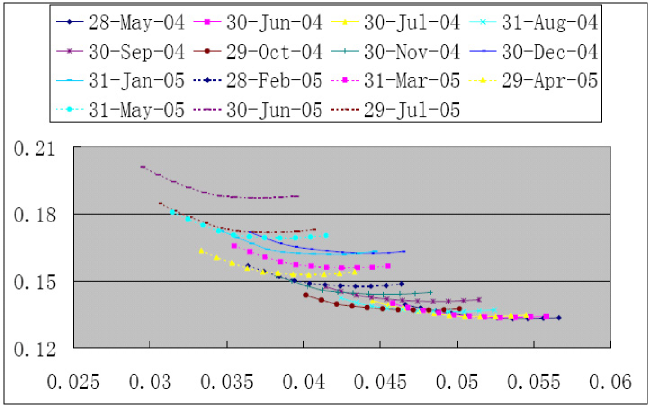

Besides we have only access to end-of-month smile quotes for each month of the period. Each European swaption has three attributes, namely, expiry, tenor and strike. Each attribute can take a value in a certain range. Similar to above, we get the required European swaptions’ smile quotes by applying a three-dimensional linear interpolation. Figure 6.5 shows the end-of-month smiles of the European swaption corresponding to the underlying co-terminal swap which starts at . Each of these smiles are composed of 11 quotes for strikes with the offset to the ATM point varying from -50bp to 50bp. More precisely, there are quotes for strikes with an offset to the ATM level of -50bp, -40bp, -30bp, -20bp, -10bp, 0, 10bp, 20bp, 30bp, 40bp and 50bp.

6.2.2 Creating Synthetic Smiles

For a hedging simulation based on a one-day time step, we need daily smile quotes even just for book-keeping of the value of the Bermudan. Thus we need to create smile data for non-end-of-month dates. This is achieved as follows:

-

•

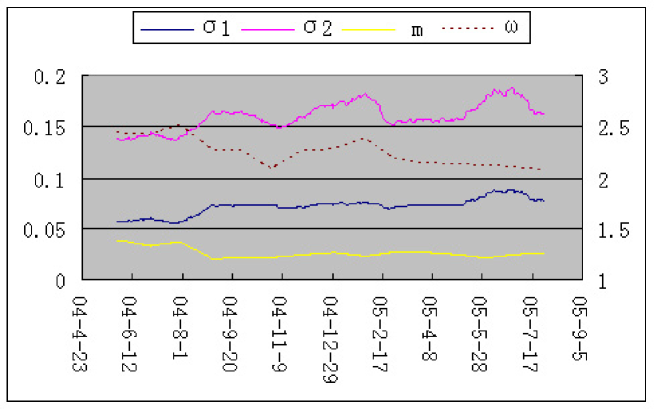

For each end-of-month date, we calibrate the swaptions’ prices to the UVDD model to get the model parameters , , and . In the calibration, we use exactly the same setting corresponding to case 6 in Section 5.2. That is, we have two log-normal components with , and is restricted within the range ;666For more details of the calibration, please refer back to Chapter 5.

-

•

For each of the other days, we get the values of and by linear interpolation of the parameters corresponding to the previous and next end-of-month dates. We do the interpolation in terms of these two parameters, because the former is an indicator of the smile shape and the latter of the skew effect.777For details, please refer back to Section 3.1.2. The parameter has been adjusted such that the implied (Black) ATM volatility equals the market quote.

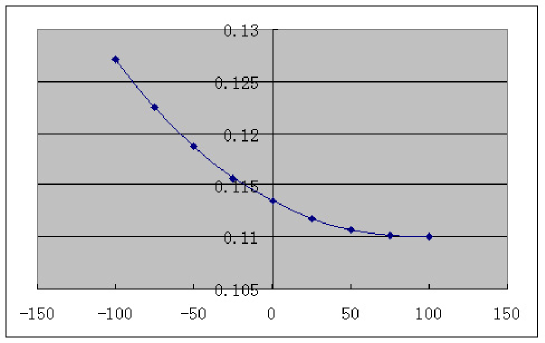

Now we have created the required smile data in terms of the UVDD model parameters for the complete 14 months period on a daily level. Figure 6.6 shows the time series of the UVDD model parameters. In Figure 6.6, the range in which varies is shown in the y-axis on the right.

6.3 Hedge Test Setup

We set up our hedge test as follows.

1. At the very beginning of the first day, we long a Bermudan

swaption by shorting money from our bank account. We keep the

Bermudan till the last day of the hedge period. We construct a hedge

portfolio containing all the hedging instruments. At the very

beginning of the first day, the hedge portfolio contains nothing.

2. Everyday we value the Bermudan and the hedge portfolio. The

hedged NPV888NPV denotes net present value. corresponding to

that day is given by

| (6.1) |

3. After that, we add the hedge portfolio’s value to our bank

account and liquidate the instruments in the hedge portfolio

(constructed in the previous day).

4. Next, we calculate the vega sensitivities of the Bermudan

and take positions of European swaptions to neutralize these vega

sensitivities. We deduct money from our bank account for setting up

these positions (vega hedging).

5. Then, we calculate the delta sensitivities of the Bermudan

and the hedge portfolio as a whole. We take positions in

spot-starting swaps and deposits to neutralize these delta

sensitivities. We again deduct money from our bank account for

setting up these positions (delta hedging).

6. Finally, at the end of the day, we add the accrued interest

for that day to our bank account.

7. We repeat steps 2. to 6. on a daily basis until

the last day of the hedge period.

The above procedure is for a delta+vega999How to calculate

the sensitivities will be elaborated in the next section. hedging

simulation. For only a delta hedging simulation, we have to skip the

4th step.

6.4 Sensitivity Calculation

In Pelsser [18], hedging simulations for non-smile Bermudans were conducted. When a vega hedging was set up, ATM European swaptions were used to neutralize the vega sensitivity of the Bermudan. The vega of an ATM European swaption is given by the following formula,

| (6.2) |

where

Of course, only ATM European swaptions are used to which the

Bermudan shows vega sensitivities. What’s important to mention is,

that even for European swaptions, it is assumed that the volatility

is flat across all strikes. This means that when we liquidate the

European positions on the next day, these are not

marked-to-market101010This is because today’s ATM option will

very probably become an ITM/OTM option tomorrow., but

marked-to-model. This was a fairly good approximation when those

hedging simulations were performed. Because at that time, the smile

effect of the swaption market was much less pronounced than

nowadays.

We conduct vega hedging against a smile Bermudan in terms of the

UVDD volatilities . For example, for our Bermudan trade,

we can calculate the sensitivity with respect to

, i.e., in total 10 vega

sensitivities. We can do this by using the following analytical

formula111111Equation 6.3 is achieved by

differentiating Equation 3.11 with respect to

.,

| (6.3) |

where

Then we need to take a certain amount of position for each European

to vega hedge against the smile Bermudan. The next day when we

liquidate the European positions, we mark the positions to

market.121212The mark-to-market in the smile case is a bit

tricky, since most of the days’ smile data are created by using the

UVDD model. For details, we refer back to Section

6.2.2.

The deposits and spot-starting swaps are the inputs for constructing

the yield curve. Thus the changes of the option value with respect

to the change of these instruments’ rates are defined as its

delta ratios. The way to calculate the delta ratios is the same for

both the smile and non-smile cases.

A relevant (payer) spot-starting swap, with the fixed coupon rate at

the par level, is used to neutralize the sensitivity to the

corresponding spot-starting swap rate. The ratio of the change of

the swap value to the change of the par swap rate is

| (6.4) | |||||

where denotes the par swap rate.

A relevant deposit is used to neutralize the sensitivity to the

corresponding deposit rate. The sensitivity of the value of the

deposit to the deposit rate is

| (6.5) | |||||

where denotes the accrued time associated with the

deposit.

Except for the sensitivities described in Equation 6.2,

6.3, 6.4 and 6.5,

all the other vega and delta sensitivities are computed numerically

by the ”bump and revalue” method. The ”bump and revalue” method is

just a simple finite-difference approach to approximate the first

derivative,

| (6.6) |

where is the value of an instrument which depends on the underlying factor , and is the bump size. In our test, the bump size is always set to 1bp, except for the vega of the non-smile Bermudan, which is calculated with a bump size of 10bp. This has been determined by experimenting with different settings. Note that increasing or decreasing the bump size by a factor 10 has little impact for the hedge results.

6.5 Results of Hedge Tests

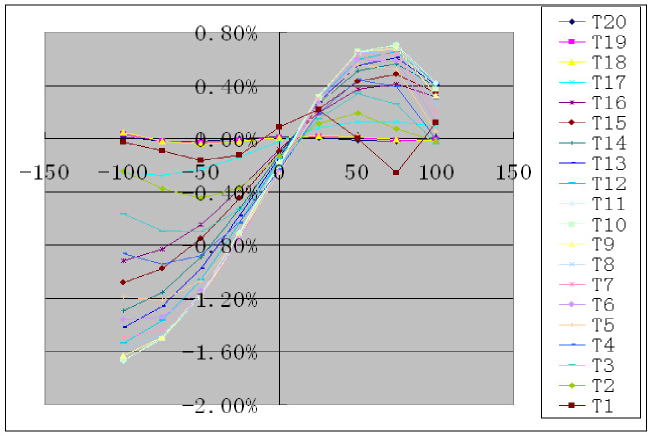

6.5.1 Comparison between Hedging against Smile Bermudan and the Original Hedging against Non-smile Bermudan

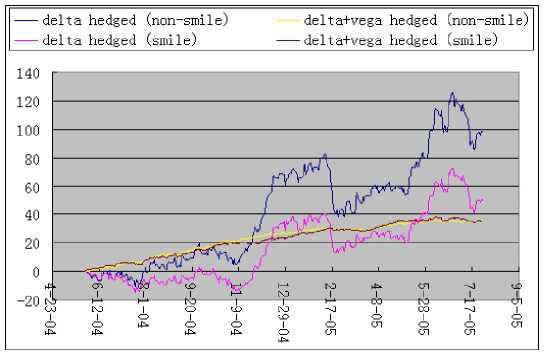

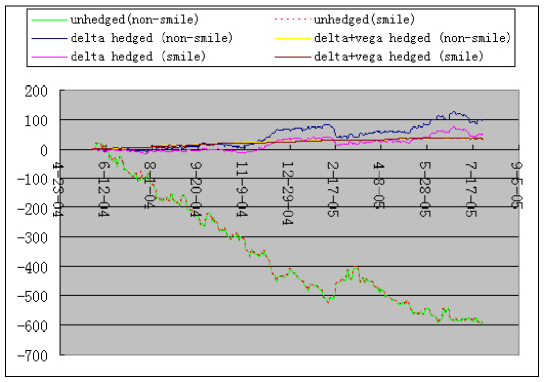

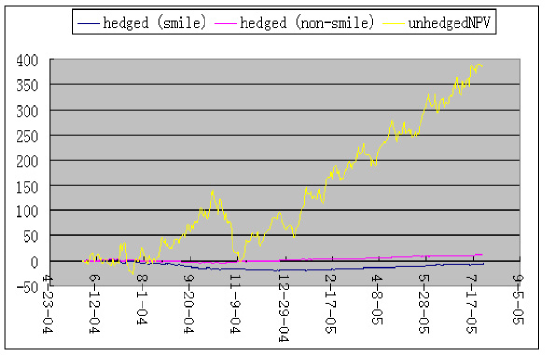

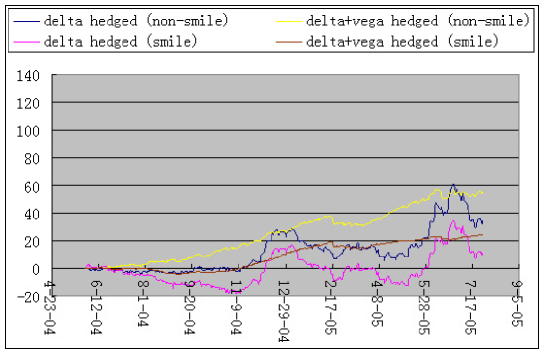

For hedging the non-smile Bermudans, we first stick to the approach used in Pelsser [18] as a benchmark. In Figure 6.7, we show the delta and delta+vega hedged NPV for hedging smile and non-smile Bermudans. The mean-reversion parameter is set to zero.131313Again we don’t quantify the mean-reversion parameter. can be seen as a benchmark mean-reversion level. In Section 6.5.4, we will discuss the impact of the mean-reversion level on the hedge performance. The strike of the Bermudan is set to . This is a near-the-money level, which has the maximal exposure to vega risk. If we check Figure 6.3, the Bermudan is running from a little in-the-money to a little out-of-the-money during the whole hedge period. We see from Figure 6.7 that the smile model has a better delta hedging performance than the non-smile model. But they have similar delta+vega hedging performances.141414Please note that this is not a fair comparison for delta+vega hedging because the Europeans in the non-smile case should be marked to market instead. If we put the unhedged NPV along with the hedged NPV, which is shown in Figure 6.8, any of the hedged NPVs has a much smaller order of magnitude.

Monthly Vega-hedging vs Daily Vega-hedging

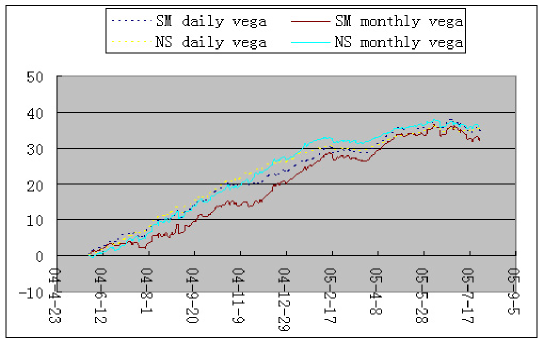

The transaction cost for trading European swaptions is fairly expensive. In practice, we can not do the vega hedging on a daily basis, but on a monthly basis. Figure 6.9 shows the delta+vega hedged NPV when the European positions are only rolled at the end of each month, together with the original daily delta+vega hedged NPV. We see that in both the smile and non-smile cases, the change from a daily rolling to monthly rolling for vega positions has little impact to the hedged NPV. The vega hedging in all the forth-coming tests is done on a daily basis.

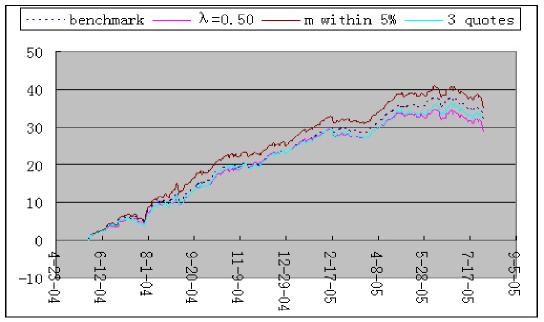

Experiments for Different Settings of the UVDD Model

We have also tested some other settings for the smile vega hedging. These tests are all related to adjustments of the calibration to the end-of-month smile data151515For relevant details, we refer back to Section 6.2.2.:

-

•

case 1: When we calibrate the UVDD model, we set the first components’ weight to instead of the original ;

-

•

case 2: When we calibrate the UVDD model, we restrict the displacement coefficient within instead of the original ;

-

•

case 3: We calibrate the UVDD model to only 3 quotes instead of the original 11 quotes. More precisely, there are quotes with relative strikes to the ATM level of -50bp, 0 and 50bp.

We show in Figure 6.10 the delta+vega hedged NPV for each of the three cases described above. The benchmark series is the original delta+vega hedged NPV in the smile case. We see that all these different settings have little impact to the hedged NPV.

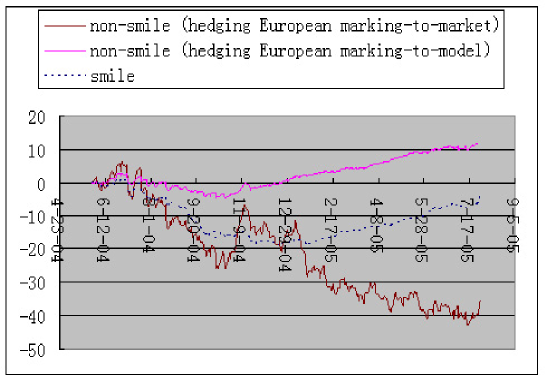

6.5.2 Marking the Vega-hedging to Market in case of Non-smile Bermudan

For the tests described in the previous section, for the non-smile

delta+vega hedging simulations, the hedging European swaptions are

not marked to market when they are being liquidated. However, for a

fair comparison of the hedge performance between the smile and

non-smile models, it is consistent to mark European swaptions in the

non-smile case to market instead of to the (Black) model. Figure

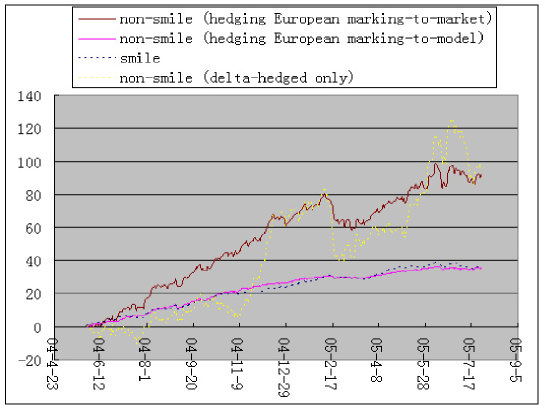

6.11 shows the new delta+vega hedged NPV in the

non-smile case according to the adjustment. For completeness, we

have also included in the figure the following data: the original

non-smile delta+vega hedged NPV, where the Europeans are marked to

model; the smile delta+vega hedged NPV; the non-smile delta hedged

NPV.

We see from Figure 6.11 that the

marking-to-market version of the non-smile delta+vega hedged NPV has

a larger (positive) drift than the marking-to-model one. This can be

explained as follows. From Figure 6.2,

6.3 and 6.4, we see that the

underlying co-terminal swap rates have an overall decreasing trend.

In our hedge test, we long a Bermudan and short161616In most

cases, a Bermudan has positive vegas. ATM (payer) Europeans to kill

the vega sensitivities. The next day, the Europeans are most likely

to be out of the money because of the decreasing trend of the

underlying. We see from Figure 6.5 that the

out-of-the-money, but close to ATM, volatility quote is always lower

than the ATM quote. This means that on the next day the Europeans

marked to market have lower values than those when marked to (Black)

model. Because of the short positions, the marking-to-market

version’s hedge portfolio has a higher value than the

marking-to-model one. This directly leads to a larger drift of the

hedged NPV for the former by Equation 6.1. This

phenomenon can also be explained in another way. In the original

non-smile case, although we take the correct prices for the (ATM)

European positions, we are generating the wrong hedge ratios. The

next day, if we still mark the Europeans to the wrong model, which

generates the wrong ratios, we would get a quite satisfactory hedge

result. But if we mark them to market, the hedge performance becomes

much worse.

If we reverse the historical data, we should expect the opposite drift effect in the non-smile case between the marking-to-market and marking-to-model versions. Figure 6.12 shows that the time series of the forward swap rate corresponding to the underlying co-terminal swap which starts at . Now the underlying has an increasing trend, starting a little out-of-the-money and ending a little in-the-money (strike ). Figure 6.13 is the counterpart figure to Figure 6.8 after reversing the historical data, but without the delta hedged NPV. As expected, we see that the unhedged NPV now has a large positive drift instead of the original very negative one. Figure 6.5 shows that the in-the-money volatility quote is always higher than the ATM quote. This means that on the next day the Europeans marked-to-market have lower values than those when marked to (Black) model. This leads to the opposite effect for the drift. Figure 6.14 is the counterpart figure to Figure 6.11 after reversing the historical data, but without the delta hedged NPV. We see from Figure 6.14 that the marking-to-market version of the non-smile delta+vega hedged NPV has a larger (negative) drift than the marking-to-model one. This is exactly the drift effect we expect for reversing the historical data.

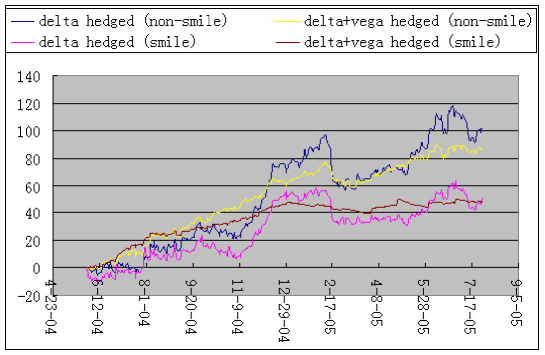

6.5.3 Hedge Tests for ITM/OTM Trades

In Section 6.5.1 and 6.5.2, we

only conducted hedge tests for the near-the-money strike (),

which is most sensitive to vega risk. In this section, we perform

the counterpart hedging simulations for the in-the-money (ITM)

strike () and the out-of-the-money (OTM) strike

().

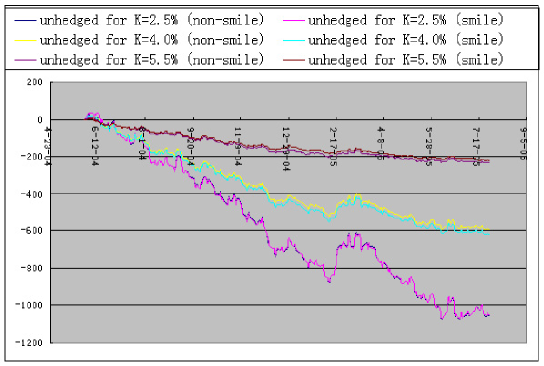

Let’s first get an impression of the magnitudes of the unhedged NPV.

Figure 6.15 shows the unhedged NPV for the

ITM/OTM trades, together with the previous near-the-money ones. We

see that the ITM unhedged NPV has the largest drift and OTM a fairly

small one. The near-the-money unhedged NPV fall in between.

In Figure 6.16 and 6.17, we

show the delta and delta+vega hedged NPV for hedging smile and

non-smile Bermudans with strike levels of and ,

respectively. Note that in the non-smile cases, the hedging

Europeans are marked to market when they are being

liquidated.171717This applies to this whole section. Similar to

the results of the near-the-money trade, the smile model outperforms

the non-smile model in both delta and delta+vega hedgings.

We also observe that in both smile and non-smile cases, a delta+vega

hedging reduces significantly the oscillation of the hedged NPV as

compared to the delta hedging. However, it doesn’t affect the drift

level of the hedged NPV. This phenomenon can be observed throughout

the trades across the three strikes (ITM/near-the-money/OTM). In

Figure 6.18, 6.19 and

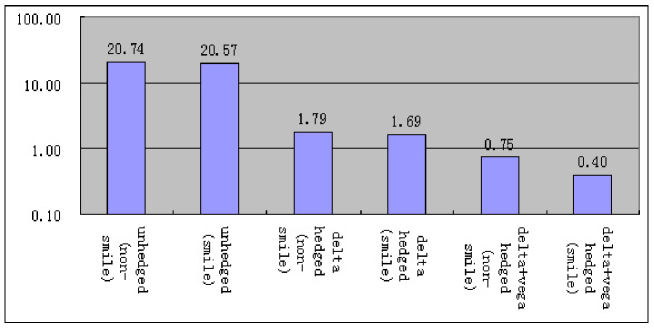

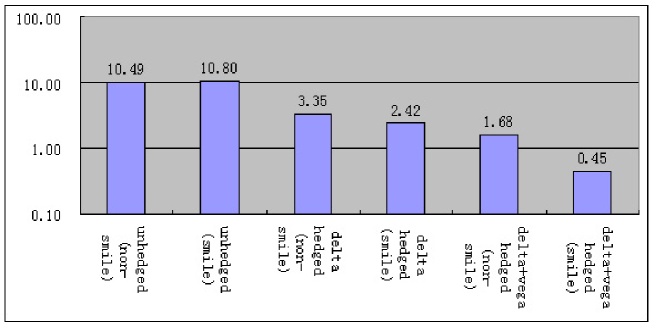

6.20, we show the standard deviations of the

unhedged and hedged daily profit and loss (PL) for each of the

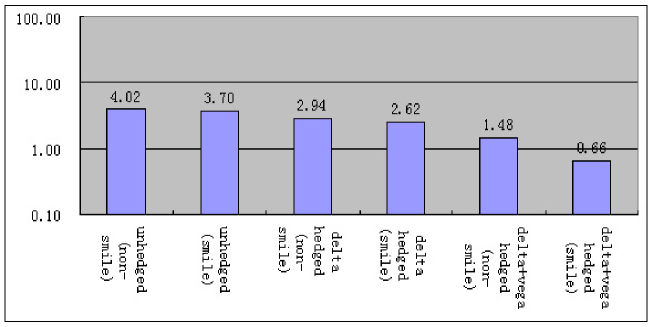

three strikes, respectively. The y-axes in these figures are all in

logarithmic scale. The main conclusions are:

-

•