An explicit Euler scheme with strong rate of convergence for financial SDEs with non-Lipschitz coefficients

Abstract

We consider the approximation of stochastic differential equations (SDEs) with non-Lipschitz drift or diffusion coefficients. We present a modified explicit Euler-Maruyama discretisation scheme that allows us to prove strong convergence, with a rate. Under some regularity and integrability conditions, we obtain the optimal strong error rate. We apply this scheme to SDEs widely used in the mathematical finance literature, including the Cox-Ingersoll-Ross (CIR), the and the Ait-Sahalia models, as well as a family of mean-reverting processes with locally smooth coefficients. We numerically illustrate the strong convergence of the scheme and demonstrate its efficiency in a multilevel Monte Carlo setting.

Acknowledgements

The authors would like to thank the anonymous referees for their suggestions, as well as Stefano de Marco and Lukasz Szpruch for valuable comments. Jean-François Chassagneux acknowledges financial support from the ANR grant Liquirisk ANR-11-JS01-0007. Antoine Jacquier acknowledges financial support from the EPSRC First Grant EP/M008436/1.

Key words: Stochastic differential equations, non-Lipschitz coefficients, explicit Euler-Maruyama scheme with projection, CIR model, Ait-Sahalia model, multilevel Monte Carlo.

MSC Classification (2000): 60H10, 65J15, 91G60.

1 Introduction

One of the main tasks in mathematical finance is to evaluate complex derivative products, where the underlying assets are modelled by multi-dimensional SDEs, which rarely admit closed-form solutions. Monte Carlo techniques are therefore needed to approximate these prices, and Glasserman’s book [19] has become the main reference for a comprehensive overview of such methods with applications to financial engineering.

Classical weak and strong convergence results for discretisation schemes of SDEs assume that the drift and the diffusion coefficients are globally Lipschitz continuous [32]; however many models used in the literature, such as the CIR, CEV, Ait-Sahalia models, violate this assumption. For pricing purposes, weak error is usually sufficient, but strong convergence rates are needed when using multilevel Monte Carlo methods (MLMC), in order to optimise the computational complexity [16, 17].

In traditional Euler-Maruyama discretisation schemes, the approximation can potentially escape the domain of the true solution of the SDE. In recent years, a lot of effort has focused on deriving schemes staying in restricted domains for SDEs with non-Lipschitz continuous coefficients [4, 5, 6, 24, 27, 34]. Several modifications have been introduced such as the drift-implicit [13] and the increment-tamed explicit Euler schemes [25, Theorem 3.15]; in the context of mathematical finance, a thorough overview of these can be found in [31].

A now classical trick is to apply a suitable Lamperti transform in order to obtain an SDE with constant diffusion coefficient, thereby translating all the non-smoothness to the drift. In the context of non-globally Lipschitz coefficients, this idea, introduced by Alfonsi [3], was further exploited in [4, 34] to obtain strong -convergence rates for implicit “Lamperti-Euler” schemes, in particular for the CIR and the Ait-Sahalia models, and for scalar SDEs with one-sided Lipschitz continuous drift and constant diffusion [34].

Under sufficient differentiability conditions, modified Itô-Taylor schemes [29] of order provide pathwise convergence results of order (for arbitrarily small ). This approach relies on a localisation argument similar to that in [20], with an auxiliary drift and a diffusion function chosen upon the discretised process exiting a sub-domain. For irregular coefficients, some strong rates of convergence have been obtained under more restrictive conditions in [20, 21, 39, 35].

Motivated by these different approaches, our main contribution is to provide an efficient numerical approximation of SDEs with non-globally Lipschitz coefficients. We first present an explicit Euler scheme with a projection for SDEs with locally Lipschitz and globally one-sided Lipschitz drift coefficient, which has a computational cost of the same order as the explicit Euler-Maruyama scheme. We prove strong rates of convergence for a wide family of SDEs, enlarging the range of parameters usually studied in explicit and implicit schemes. Under suitable assumptions, we are able to obtain fast convergence reaching the optimal rates of convergence. The scheme shares some of the features of the tamed-scheme family. Its analysis however does not require heavy technical tools. Having in mind applications to mathematical finance, the analysis is made for SDEs whose support is included in . Nevertheless, the techniques used here can be extended to the multi-dimensional case under some suitable assumptions. An important contribution is to relate the choice of the scheme with the rate of explosion of the drift function at the boundaries of the domain through a locally Lipschitz continuous condition. To the best of our knowledge, thus far in the literature of tamed schemes, only the exploding behaviour at one of the boundary of the domain has been considered to obtain convergence rates. Our scheme considers generically both boundaries at the same time.

We then turn our attention to SDEs with non-globally Lipschitz diffusion coefficients, as often encountered in finance. We apply a Lamperti transformation to the process in order to shift the non-Lipschitz behaviour from the diffusion to the drift function, before using the modified scheme. This allows us to prove rates of convergence for the original process in the -norm for ; in particular, the rate of convergence for can be used for MLMC applications, which we apply to the pricing of zero-coupon bonds and call spread options for correlated CIR processes. In particular, we are able to prove convergence results for CEV/CIR-like model with non-constant smooth coefficients, see Section 4.2. Importantly, we also obtain new convergence results for the -model, see Remark 4.2.

The remainder of the paper is structured as follows. In Section 2, the modified Euler-Maruyama scheme is introduced, and the convergence results are proved in Section 3. In Section 4, the scheme is applied to families of SDEs, such as the CIR, the and the Ait-Sahalia models, widely used in mathematical finance, and the Ginzburg-Landau equation. In Section 5, numerical results for the rates of convergence obtained are shown and discussed.

Notations: In the sequel, is the interval . We denote by the domain , and . Furthermore, we define the interval and , for . We denote by the space of twice differentiable functions with continuous derivatives on , and by the space of functions in with first and second bounded derivatives. We shall denote by the set of strictly positive integers. Given a probability space , we denote , for , the set of random variables such that . In the sequel, we will simply write when the probability space considered is clear from context. We denote by the conditional expectation given the filtration

2 Definitions and assumptions

Let be a filtered probability space, and a one-dimensional standard -adapted Brownian motion. Consider a one-dimensional stochastic differential equation of the form

| (2.1) |

Throughout this article, we shall assume the following:

: the SDE (2.1) admits a unique strong solution in ;

the drift is locally Lipschitz continuous and globally one-sided Lipschitz continuous on ,

namely there exist , , such that for all :

| (2.2) | ||||

| (2.3) |

furthermore, the diffusion function is K-Lipschitz continuous on for some : for all , the inequality holds.

Remark 2.1.

The function could as well be defined on . However, assuming the Lipschitz continuity of on would lead to a natural extension of on .

Remark 2.2.

In many models used in practice (in particular the Feller/CIR diffusion in mathematical finance, see Section 4.1, these assumptions are not met. A suitable change of variables, however, allows us to bypass this: consider an SDE of the form

| (2.4) |

where the process takes values in some domain . When is well defined and continuously differentiable on , the Lamperti transformation of is defined as , and Itô’s Lemma implies that the process defined pathwise by satisfies (2.1) with and is constant.

Let be a fixed positive integer and a fixed time horizon. Define the partition of the interval by , with .

For a closed interval , we define as the projection operator onto . For ease of notation, we let also , i.e. for ,

| (2.5) |

In the following, we denote by a positive constant that depends only on , , , , , but whose value may change from line to line. We denote it by if it depends on an extra parameter . We now introduce our explicit scheme for the discretisation process :

Definition 2.1.

Set and for ,

with , , and .

Remark 2.3.

-

(i)

For some applications, it may be interesting to force the scheme to take values in a domain, e.g. intervals , , or even . To this end, we introduce some extensions of the previous scheme. For all , we define , , and , for some to be determined later on, see Corollary 3.1 for details. In Proposition 3.3, we prove finite moments and finite inverse moments for these modifications.

-

(ii)

Observe that for , is the usual Euler-Maruyama scheme, up to a projection onto .

The following lemma shows how the properties of the initial drift translate into the new projected drift (proof in Appendix A):

Lemma 2.1.

For any , the composition is Lipschitz continuous with Lipschitz constant , and one-sided Lipschitz continuous with the same Lipschitz constant as that of .

Remark 2.4.

For any , since and are Lipschitz continuous, an easy induction shows that the scheme in Definition 2.1 satisfies . The bound is a priori non-uniform in , since the Lipschitz constant of depends on .

We now introduce the following assumption, which implies that , for all , and which relates the locally Lipschitz exponents and to the size of the truncated domain :

: the strictly positive constants , satisfy and .

We require additional assumptions to prove the strong convergence rate of our scheme: below imposes a condition on the moments of the process in terms of the locally Lipschitz exponents and , to obtain a minimal convergence rate. We shall further impose regularity conditions on and to obtain a better rate of convergence.

: holds and there exist and such that

: holds, the drift function is of class , and

| (2.6) |

3 Convergence results

In this section we prove strong rates of convergence for the scheme in Definition 2.1 under some of the assumptions stated above; this result follows from estimates for the regularity of the processes and , and the discretisation error of the scheme. Below, we give the results for the general case , but in the proof we restrict to the most complicated case .

3.1 Preliminary estimates

Our first two results concern the error due to projecting the true solution on .

Lemma 3.1.

Assume that and hold. Then, for any ,

where are given by .

Proof. For any , we can write

Set and , its conjugate exponent. Hölder’s inequality yields

Using and the set equality , Markov’s inequality implies

.

Likewise, since , Markov’s inequality yields

, and the lemma follows.

Lemma 3.2.

Assume that and hold. Then, for any ,

where are given by .

Proof. Using (2.2), we observe that

Set and . Hölder’s inequality then yields

and together with Markov’s inequality imply

.

Setting and

,

a similar computation gives

.

The following lemma provides a regularity result for the process and will be required for the main convergence result. For a given stochastic process on and the partition , we define its “regularity” by

| (3.1) |

Lemma 3.3.

Assume that and hold. The regularity of satisfies , where are given by .

Proof. For , since is -Lipschitz, implies

For , by Lemma 3.2, we now compute

Using and the inequality , which holds under , we obtain for , and the lemma follows from the upper bound

We now compute upper bounds for the regularity of .

Lemma 3.4.

Assume that and hold.

-

(i)

Then , where are given by .

-

(ii)

If moreover holds, then .

Proof. The inequality in (i) is a direct consequence of the following computation:

where we used Lemma 3.2. Let us now prove (ii). The drift function is of class by , and Itô’s Formula on the interval implies

Squaring and applying the Cauchy-Schwarz inequality the yields

and (ii) follows from (2.6), direct integration on and summation.

3.2 Convergence result

We consider here the discretisation error between the true process and the discretised process . Let us introduce the following notations:

| (3.2) |

The following key proposition provides a bound on the squared differences , which depends on both the partition size and the regularity (in the sense of (3.1)), and which will be refined further below in Theorem 3.1.

Proposition 3.1.

Assume that and hold, then

| (3.3) |

where are given by .

Proof. 1. We first show that the global error between the scheme and the solution is controlled by the sum of local truncation errors defined below. Indeed, observe that

for , where

The last equality comes from the fact that takes values in and , for all . Therefore, squaring the difference gives

| (3.4) | ||||

Using the simple identity and an application of Young’s inequality yields

since is one-sided Lipschitz continuous (Lemma 2.1), globally Lipschitz continuous with Lipschitz constant and is Lipschitz continuous. Under , and an iteration yields

| (3.5) | ||||

| (3.6) |

2. We now provide explicit errors for the global truncation. As is -Lipschitz, we have , and hence

| (3.7) |

We now compute an upper bound for . Since

| (3.8) |

The Cauchy-Schwarz inequality yields

and Lemma 3.2 implies and . Combining this with (3.6) and (3.7) concludes the proof.

Remark 3.1.

We have kept the above result general, without a priori assuming that the drift function belongs to . If we consider a constant diffusion and , we can recover a better upper bound using (3.5) instead of (3.6) in the first part of the previous proof and prove a first-order strong rate of convergence. This will be illustrated in Proposition 3.2 below.

We now state the main result of our paper, namely a strong rate for defined in (3.2).

Theorem 3.1.

Assume that holds, then the inequality

| (3.9) |

holds with under by setting and under by setting .

Proof. 1. Assume . Combining Lemma 3.3 and Lemma 3.4(i) with (3.3) yields

To balance the error terms, set and , observing that under , holds for this choice of parameters. Thus, we obtain , with , with .

2. Assume . Lemma 3.3 and Lemma 3.4(ii) with (3.3) imply

Setting , yields , where . Since implies , we observe that .

We now state the convergence results associated to the extensions of the scheme defined in Remark 2.3.

Corollary 3.1.

Assume that holds. Then the approximations and defined in Remark 2.3 satisfy

holds with under by setting and under by setting , where and .

Proof. The proof follows by computing upper bounds for each of the three quantities on the left-hand side. For all , since is -Lipschitz continuous, we can write

and the upper bound for follows from Theorem 3.1.

Set now . For ,

| (3.10) |

where the last inequality follows from Theorem 3.1. A straightforward adaptation of the proof of Lemma 3.1 yields , which gives the second bound.

Similarly, for , the equality holds, and an application of Hölder’s inequality gives . Choosing concludes the proof.

Remark 3.2.

For SDEs defined on the whole real line, strong convergence rates have been proved using tamed explicit schemes [27, 37]. The authors assumed that the drift satisfies (2.2) and (2.3) with locally Lipschitz exponents , , and that the diffusion is -Lipschitz. Under these assumptions, (2.1) has a unique strong solution [33]. Our modified scheme and a slight modification of the projection, namely, can be applied to cover this case.

We now show that, as for the classical Euler scheme, our modified scheme may have a first-order strong rate of convergence if the diffusion coefficient is constant. This can be observed in practice, as shown in Section 5.1. This also suggests that a similarly modified Milstein scheme, when the diffusion coefficient is not constant, will have a first-order strong rate of convergence.

Proposition 3.2.

Assume that for all , and that with and , and hold. Then,

where we set and in the definition of and .

Proof. The proof is similar to Step 2 in the proof of Proposition 3.1, but uses the sharper upper bound (3.5). Since the diffusion function is constant, is null, and using (3.8) and Lemma 3.2, we can write

| (3.11) | |||

Moreover, Itô’s Lemma implies

which we can rewrite as

Under , we then obtain easily, recalling (3.11), that

The proposition then follows by setting

and using the fact that and , from Lemma 3.2.

The statement for , , ,

follows from the same arguments as in Corollary 3.1.

3.3 Moment properties of the schemes

For later use, we show that our approximations have uniformly bounded second moments, which completes the result of Remark 2.4.

Lemma 3.5.

Assume that and hold. Then, for given by ,

with for , and for , , recall Remark 2.3, and with , under , and if moreover, , and , .

Proof. Since , and Theorem 3.1 imply that

holds for any , which proves the claim.

The statement for , and follows from Corollary 3.1

or Proposition 3.2.

We now consider the modifications and defined in Remark 2.3 and prove some finite moments or inverse moments for them, extending the previous result.

Proposition 3.3.

Assume that hold and let and , where and are given by .

-

(i)

if holds, then for all ;

-

(ii)

if holds with , then for all .

Proof. 1. We first prove (i). We remark that the result for follows directly from Lemma 3.5. We now assume that and we introduce the sets and , where . We then observe that

and deal which each terms in the right hand side separately.

Since by definition, we compute, for the first term,

| (3.12) |

For the second term, as on , we obtain

| (3.13) |

For the last term, we first observe that for non negative , and ,

| (3.14) |

Using the above equality for , and we compute that

Then since, we observe that

Applying Corollary 3.1, we thus obtain

| (3.15) |

The proof of the first statement is concluded by combining the previous inequality

with (3.12) and (3.13).

2. We now prove (ii). We assume that and that . We introduce

the set and , where .

We observe that

We are going to upper bound separately the expectation of each terms appearing in the right hand side of the above equality.

For the first term, since on , holds by definition, we get

For the second term, observing that , by we compute

since on , and . For the last term, we compute that

and using (3.14), we get

Using the Cauchy-Schwarz inequality and then applying Chebyshev’s inequality, we obtain

which concludes the proof for this step.

4 Applications

As a first illustration, we now apply our results to various stochastic differential equations widely used in the literature.

4.1 CIR model

We consider the Feller diffusion [14], defined as the unique strong solution to

| (4.1) |

where is a Brownian motion, and , , are strictly positive constant parameters. This process is widely used in mathematical finance, both for interest rate modelling [10] and for the instantaneous variance of a stock price process [22]. Under the Feller condition , remains strictly positive almost surely, and Itô’s Lemma implies that the Lamperti transform satisfies

| (4.2) |

where

| (4.3) |

furthermore, when the Feller condition holds. Since , proving a rate of convergence for a discretisation scheme for the process will allow us to obtain a rate of convergence for the process . In the following corollary, we apply Theorem 3.1 to provide bounds for and , where .

Corollary 4.1.

For , holds, where

| (4.4) |

Proof. Consider first the bound for . The drift of is one-sided Lipschitz continuous and locally Lipschitz continuous with exponents and , and the diffusion is constant, hence Lipschitz continuous. From [13, page 5], we know that for all , and therefore

| (4.5) |

In the case , we choose and fix , so that holds

(no condition on is required since )

and holds as well.

From Theorem 3.1 it follows that the convergence rate is given by . We compute easily, since , that

, depending on the choice of .

Consider now the case .

We compute that

hold.

Combining the previous inequality with (4.5), we obtain that holds.

If , fix and set , it follows that from Theorem 3.1.

The case follows directly from Proposition 3.2, since there exists a such that for all by (4.5).

We now prove the corollary for the difference . The Cauchy-Schwarz inequality and the result above imply

Define , where , recall Remark 2.3. We now consider a general -norm for convergence of the discretisation scheme of process .

Corollary 4.2.

Proof. For all , we have

From (4.5), we have that . Similarly, since , we obtain from Proposition 3.3(i), that . This moment bounds, combined with Corollary 3.1 (or Proposition 3.2, when ) and the above inequality, leads to .

Remark 4.1.

To the best of our knowledge, the best convergence result in term of range for the parameter are obtained using an implicit Euler scheme, in [28], see also the references therein. In this paper, belongs to whereas our results are valid for . The main advantage of our scheme is its explicit nature that allows to retrieve convergence results for non-constant coefficients as illustrated in the next section. Let us also mention in this regard the very recent paper [7] on the symmetrised Milstein scheme.

4.2 Locally smooth coefficients

We now consider a stochastic differential equation of the form (2.4), with drift function , where , and diffusion function , with and . This model encompasses the Feller diffusion (see Section 4.1) and the CEV model [11], both widely used in mathematical finance. For the special case , the diffusion function is -Lipschitz and our scheme applies directly to the process as long as (2.2) and (2.3) hold for the drift function .

We now focus on the case . The Lamperti transform reads , with inverse . The process is the solution to , with and

| (4.6) |

In order for the functions and to satisfy the required conditions, we assume:

: , and are bounded, belong to

and .

We distinguish between two cases for the parameter :

: and .

: and there exists such that for all .

We now prove a rate of convergence as a corollary of Theorem 3.1.

Proposition 4.1 (Locally smooth coefficients).

Assume that holds. Then,

with

-

1.

If holds, .

-

2.

If and hold, if , if and if .

In both cases, we set , with in the definition of , recall Remark 2.3.

Proof. In [12, Proposition 3.1], De Marco proves that under , there exists a unique strong solution to (2.4), which stays in almost surely. In addition, he shows that and further imply that , where is the first time the process reaches zero. We recall that once we perform the Lamperti transformation, the diffusion function is a constant.

We divide the proof in several parts: in (i) we show that the drift function is one-sided Lipschitz continuous; in (ii) we show that is locally Lipschitz continuous, and hence conclude that (2.2) and (2.3) hold. This is based on a direct study of the derivative of .

(i) From (4.6), it follows that, for all ,

| (4.7) |

where and for , we set , for all .

If , under and , we have that (since ) and as well (since and ).

If , under and , we deduce from the same arguments as previously that . In this case, we obtain

because .

(ii) We now show that is locally Lipschitz continuous. From and the boundedness assumptions on , , and , we obtain

Observing that for , , for all , we obtain that is locally Lipschitz continuous, with .

We now prove statements and in the corollary.

1) Assume . Since the locally Lipschitz exponents are , fix , so that holds. By [12], and are finite for all ; therefore is finite for all [12, Lemma 3.1]. We note that belongs to the class and holds, therefore from Proposition 3.2. The proof of the statement for follows from the same arguments as in the proof of Corollary 4.2.

2) Assume that holds and let . Here, an . Then, is finite for all [12, Lemma 3.1], and so is for all . Fix and set , so that and hold. From Theorem 3.1, holds.

Further assume that .

Note that the drift function belongs to the class .

Fix and , so that holds.

By the assumptions on the parameters it follows that is finite, and therefore holds.

From Theorem 3.1, .

Finally, in the case , we can apply Proposition 3.2, to conclude that .

The proof of the statement for follows from the same arguments as in the proof of Corollary 4.2.

In the CIR model, we obtain for , using finite inverse moments of the process from [13]. For the general case in Proposition 4.1, we assumed that for .

In the next corollary, we impose additional assumptions in order to recover the same parameter constraints as for the Feller diffusion in the previous section.

Proposition 4.2.

Assume and . Moreover, let be such that and for all . Then,

with if , and if .

We set , with in the definition of , recall Remark 2.3.

Proof. From the assumptions on and , there exists

such that the inequality holds

in the domain .

We define as the process with drift (instead of ),

and diffusion .

Therefore, by the Comparison Theorem (see [30, Section 5.2])

the inequality holds for all almost surely,

and hence is true for all .

Now, is clearly a Feller diffusion and, from the assumption on , it follows that

is finite.

The result then follows directly from the second part of Corollary 4.1.

The proof of the statement for follows from the same arguments as in the proof of Corollary 4.2.

4.3 model

The process [23] is the solution to

| (4.8) |

with . Introduce the quantity . The Feller diffusion and the process are related as follows: the map yields the Lamperti transformed CIR process , as in (4.2) and (4.3), with parameters, , and . Existence and uniqueness can be retrieved from the properties of the Feller diffusion, and is finite for all .

Corollary 4.3 ( model).

Let . Then, , with if , if and if .

Proof. In terms of the CIR coefficients, we have . We directly apply Corollary 4.1 to get the desired results.

We now establish a convergence result for the process , using the modification (recall Remark 2.3).

Proposition 4.3.

Let and fix . If , then

with for and for , where .

Proof. It follows that

where we used Young’s inequality to obtain the last inequality. We now compute

Since it follows that is bounded by a constant. Furthermore, for ( is such that ), it follows that , therefore , which together with and Corollary 3.1 (or Proposition 3.2, if ), conclude the result.

Remark 4.2.

The last corollary proves -bounds () for the model and improves the existing literature by yielding strong rates of convergence for . More specifically, in the -case, Neuenkirch and Szpruch [34, Proposition 3.2] shows a rate of convergence using a drift-implicit scheme when , and Sabanis [36, Theorem 2] gives a rate for . Corollary 4.3 improves these to an -rate of convergence also for .

Alternatively, we could indeed use Proposition 3.3 for a higher rate of convergence, however the parameter required is larger:

Corollary 4.4.

Let for some fixed . Then

4.4 Ait-Sahalia model

In the Ait-Sahalia interest rate model [2], is the solution to

| (4.9) |

where all constant parameters are non-negative, and . From [38], there exists a strong solution on , and the Lamperti transformation satisfies

| (4.10) |

with

Corollary 4.5.

If , then .

Proof. Straightforward differentiation yields

We have , hence is finite by continuity and therefore is one-sided Lipschitz continuous. In addition, for , so is locally Lipschitz continuous with and . The diffusion is constant, hence Lipschitz continuous. Using the locally Lipschitz continuous properties of the drift, fix and . We recall that if , then and are finite for all [38, Lemma 2.1] so that holds. Differentiation yields

Since belongs to and (2.6) is finite by [38, Lemma 2.3], then holds.

Fix and . Then, by Proposition 3.2, the statement is proved.

We now compute a strong rate of convergence for the Ait-Sahalia process . We need to control the behaviour of the approximation near and at . In order to do that, we introduce modification where , for and to be determined later on.

Corollary 4.6.

If , then for ,

with , and , .

Proof. A similar approach to Proposition 3.3 yields

where and . Since and , is finite. Observing that , and using Proposition 3.3, we get . Also, we compute

recalling that and are -Lipschitz. Using similar arguments as in the proof of Corollary 3.1, we then obtain and the result follows.

Remark 4.3.

In [34], the authors prove order one -rate of convergence for the same range of parameter but using an implicit scheme.

5 Numerical results

In this section, we numerically confirm the strong convergence rate of the modified Euler scheme for the CIR model, the one-dimensional stochastic Ginzburg-Landau equation with multiplicative noise, and the Ait-Sahalia model. For a process , denote by the modified Euler-Maruyama approximation at time and the closed-form solution (or reference solution), using the same Brownian motion path (the path). The empirical average absolute error is defined by

over sample paths, which we will set to . An equidistant time grid is used, with step sizes , for different values of . The strong error rates are computed by plotting against the number of discretisation steps on a log-log scale, and the strong rate of convergence is then retrieved using linear regression.

5.1 CIR model

The Lamperti-transformed drift-implicit square-root Euler method (see [13, 34]) has a unique strictly positive solution defined for by

with defined in (4.3). The CIR/Feller diffusion is recovered by setting for , and we compare the modified explicit Euler scheme with this implicit scheme used as a reference solution (with a large number of time steps).

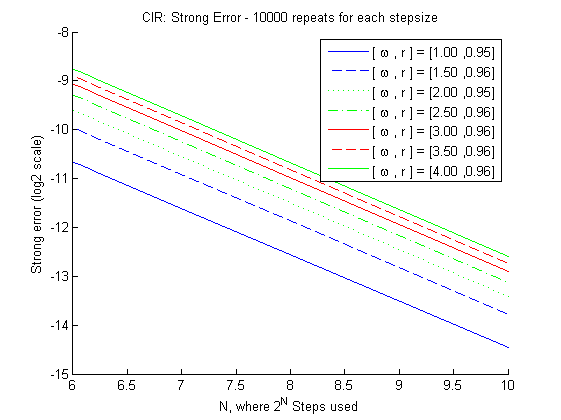

We compute the strong rates of convergence for the CIR process, where the implicit scheme is used as a reference solution. Set , such that . The cases are considered. The reference solution is computed using .

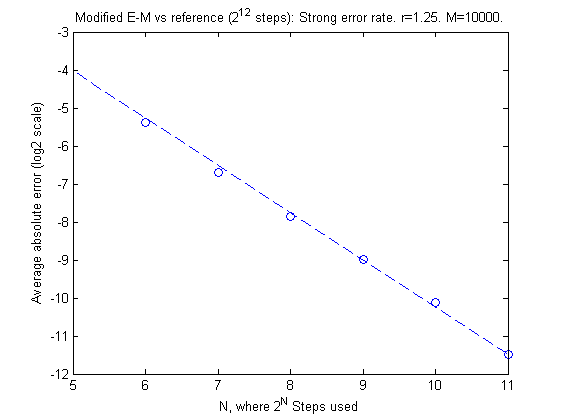

Figure 1 shows the rates of convergence achieved for the CIR process, where in the modified scheme, according to Corollary 4.1. In the corollary, we prove a strong rate of convergence of when , and for . The coefficient of determination , for the goodness of the fit of the straight line, is above for all . We observe that numerically order 1 is achieved by our scheme for , which is better than the bound we proved.

Remark 5.1.

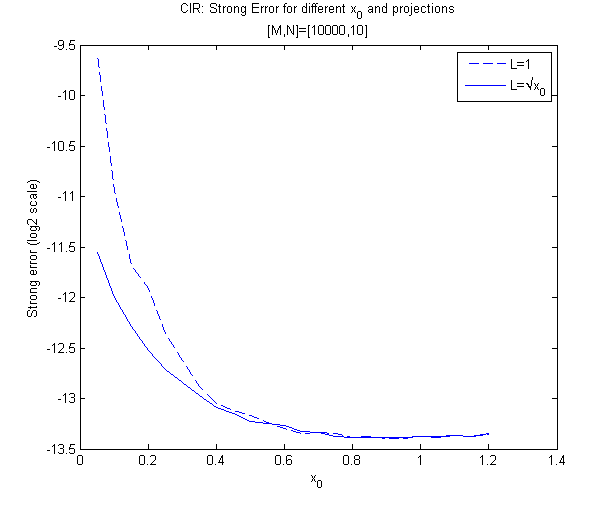

The projection introduced in Definition 2.1 can be modified to , with suitably chosen constant. This is beneficial if the process has extreme initial conditions or average state, and does not impact the convergence results.

For small , it is intuitive to use the projection in Remark 5.1 to achieve faster convergence (albeit without affecting the asymptotic behaviour). Set , such that . In Figure 2, we let vary between and in increments of . We compare the errors achieved for , using the projections and . By using the projection , smaller errors can be achieved for small .

5.2 Ginzburg-Landau equation

Consider the one-dimensional stochastic Ginzburg-Landau SDE [32, Chapter 4], where the process is the unique strong solution to

for , which admits the closed-form solution

| (5.1) |

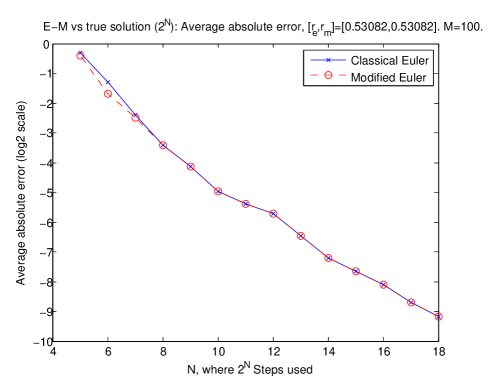

This SDE is a special case of the Ait-Sahalia process with . For this choice of parameters, , hence the moments and inverse moments of are finite for all , and the solution stays in almost surely. The drift function satisfies (2.2), with , e.g. set in the modified scheme. In addition, the drift is one-sided Lipschitz continuous and the diffusion is -Lipschitz. As a result, theoretical convergence for this example can be obtained with rate , recall also Remark 3.2.

Ginzburg-Landau strong convergence:

For this SDE, the closed-form solution is used in the definition of to compute the strong rate of convergence . Figure 3 shows the average absolute error using the modified scheme, for parameters . The empirical rate achieved of (same as the standard Euler scheme) which is lower than the predicted rate of . This can be explained since we are approximating the integral in (5.1) as a summation.

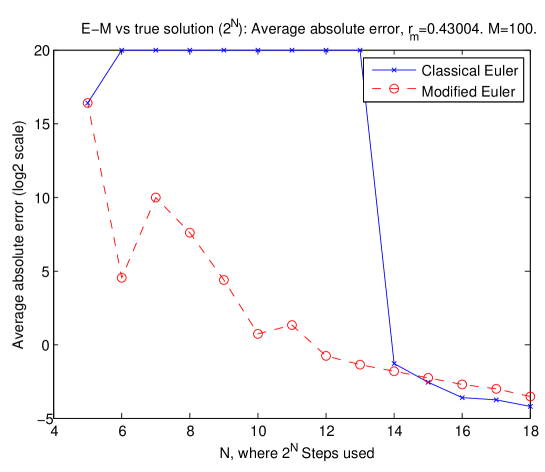

Ginzburg-Landau Euler-Maruyama divergence:

We consider an example of the Ginzburg-Landau SDE for which the standard Euler-Maruyama scheme diverges, and compare the results with the modified explicit scheme. Fix parameters as in [26], for which the authors prove moment explosion for the classical Euler-Maruyama scheme, see [26, Table 1].

Figure 4 shows the error for the classical and the modified schemes, for different . For the modified scheme, set . The modified Euler scheme converges with a rate . For a range of step sizes, the classical Euler scheme explodes, as proven in [26] (N.B. very large and values are set to in the figure, to illustrate the explosions for the classical scheme). The modified scheme appears to be more robust.

5.3 Ait-Sahalia model

The strong rate of convergence for the Ait-Sahalia model is computed using a reference solution with a large number of steps. Consider the parameters , and . From these parameters, note that and . Fix and , such that and , so that holds. Figure 5 shows against the number of steps (log-log plot), where steps are used for the reference solution. The Ait-Sahalia empirical rate of convergence could be justified by the fact that we used a reference solution instead of the true solution.

5.4 MLMC

We combine the modified Euler scheme and the multilevel Monte Carlo approach introduced by Giles [16, 18]. The original paper focused on approximating the expected value of Lipschitz continuous payoffs. The MLMC method has also been justified for digitals, lookback and barrier options [17]. Multischeme MLMC techniques use different discretisation schemes in order to further improve the computational efficiency [1]. The use of MLMC techniques has also been applied to compute Greeks [9].

We target a root mean squared error (RMSE) of for the option price. Using an Euler-Maruyama scheme, the MSE of an option price is , where is the number of Monte Carlo paths, and is the step size of the discretisation. By choosing , and , the total cost is .

The idea behind MLMC is to use different time steps, at different levels of the simulation. We increase the number of time steps at each level by a factor , where level uses steps of size . We define to be the numerical approximation of the payoff at level , for , where is the maximum number of levels. By linearity of the expectation operator we note that

| (5.2) |

where the difference in the payoff approximation on levels and is estimated using the same Brownian path, for both levels. The variance of the payoff difference, , decreases quickly with increasing levels, and it has been shown that for European options with Lipschitz continuous payoffs, converges to zero twice as fast as the strong convergence rate of the scheme. At each level , we simulate paths and estimate . The multilevel estimator has variance , and minimises the computational cost [16], to achieve a RMSE of . The strong convergence rate is required for the MLMC techniques, and the complexity theorem provides a general result for the computational cost of the MLMC method [16]. MLMC methods have been shown to improve the computational efficiency using an Euler-Maruyama discretisation to , and for a Milstein scheme [16, 15].

CIR model ZCB:

We consider the Cox-Ingersoll-Ross model (4.1) for the process ; the price of a zero-coupon bond (ZCB) with maturity , at time , reads

which admits a closed-form solution [10, 8]. This solution at time zero is , where and

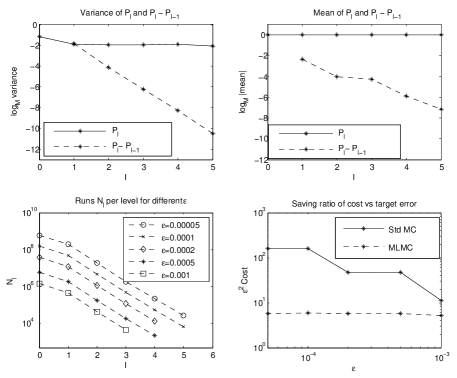

We consider a CIR model with parameters , , and RMSE thresholds .

In Figure 6, we compute the standard Monte Carlo, and MLMC approximations for the ZCB. The first plot demonstrates the average variance for the approximations and the differences . Observe that the variance of the differences decreased roughly twice as fast as the rate of weak convergence of an Euler scheme. Also, the variance of is asymptotically a constant. The second plot shows the mean of and the mean of . The third plot shows how decreasing the target requires more steps and increases the number of levels from 3 to 5. The fourth plot shows the ratio of savings between the standard Monte Carlo approach for approximating the bond price (Std MC), and the MLMC counterpart. The ratio of savings is a factor of 27 for between the standard Monte Carlo and the MLMC approach. We adapt code freely available from [16].

CIR model spread option:

We consider the CIR model for processes and , the solutions of the following stochastic differential equations:

| (5.3) |

where , are correlated Brownian motions with and are strictly positive constant parameters.

The payoff of a European call spread option at the terminal time for a given strike is defined as . Spread options are used for hedging and speculation purposes and are widely traded in the commodity markets. Their price is particularly sensitive to the correlation parameter; for increasing , the price of the spread option decreases.

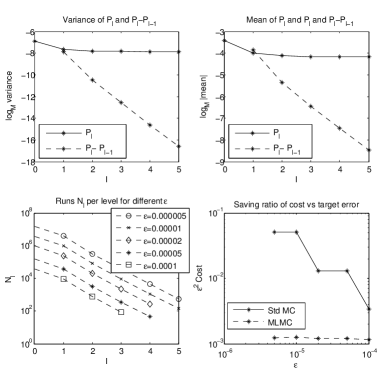

Example 5.1.

We set throughout, where is the multiple of the step-sizes for the MLMC. In Table 1, the RMSE and the target is shown. The savings column shows the speedup multiple of the MLMC computational cost compared to the standard Monte Carlo routine.

| RMSE | Target | Ratio | Savings |

|---|---|---|---|

| 0.000046 | 0.0001 | 0.456 | 2.97 |

| 0.000032 | 0.00005 | 0.637 | 10.61 |

| 0.000018 | 0.00002 | 0.921 | 10.67 |

| 0.000007 | 0.00001 | 0.671 | 40.90 |

| 0.000004 | 0.000005 | 0.855 | 40.97 |

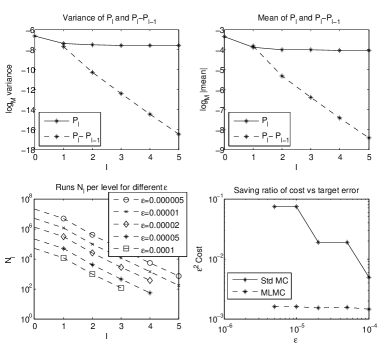

Example 5.2.

Suppose (5.3) with parameters , , . For this example, we compute the reference option price using the drift-implicit Euler scheme, using paths with time steps. The price and its confidence interval is .

For Example 5.2, the RMSE, ratio to target and savings factor over standard Monte Carlo are shown in Table 2.

| RMSE | Target | Ratio | Savings |

|---|---|---|---|

| 0.000075 | 0.0001 | 0.751 | 3.39 |

| 0.000037 | 0.00005 | 0.745 | 12.15 |

| 0.000019 | 0.00002 | 0.953 | 12.2 |

| 0.000007 | 0.00001 | 0.707 | 47.2 |

| 0.000004 | 0.000005 | 0.811 | 47.19 |

Remark 5.2.

For the above MLMC examples above, recall the constant from Remark 5.1, which for the CIR examples above is chosen at . The modified Euler scheme parameter is set to as seen before.

References

References

- [1] K. Abe, Pricing exotic options using MSL-MC, Quantitative Finance 11 (2011), no. 9, 1379–1392.

- [2] Y. Ait-Sahalia, Testing continuous-time models of the spot interest rate, Review of Financial studies 9 (1996), no. 2, 385–426.

- [3] A. Alfonsi, On the discretization schemes for the CIR (and Bessel squared) processes, Monte Carlo Methods and Applications 11 (2005), no. 4, 355–384.

- [4] , Strong order one convergence of a drift implicit Euler scheme: Application to the CIR process, Statistics & Probability Letters 83 (2013), no. 2, 602–607.

- [5] A. Berkaoui, M. Bossy, and A. Diop, Euler scheme for SDEs with non-Lipschitz diffusion coefficient: strong convergence, ESAIM: Probability and Statistics 12 (2008).

- [6] M. Bossy and A. Diop, An efficient discretization scheme for one dimensional SDEs with a diffusion coefficient of the form , , Tech. report, INRIA working paper, 2004.

- [7] M. Bossy and H.O. Quinteros, Strong convergence of the symmetrized Milstein scheme for some CEV-like SDEs, arXiv preprint arXiv:1508.04581 (2015).

- [8] D. Brigo and F. Mercurio, Interest rate models-theory and practice: with smile, inflation and credit, Springer Finance, 2007.

- [9] S. Burgos and M. Giles, Computing Greeks using multilevel path simulation, Monte Carlo and Quasi-Monte Carlo Methods 2010, Springer, 2012, pp. 281–296.

- [10] J. Cox, J. Ingersoll, and S. Ross, A Theory of the Term Structure of Interest Rates, Econometrica 53 (1985), no. 2, 385–407.

- [11] J. Cox and S. Ross, The Valuation of Options for Alternative Stochastic Processes, Journal of Financial Economics 3 (1976), 145–166.

- [12] S. De Marco, Smoothness and asymptotic estimates of densities for SDEs with locally smooth coefficients and applications to square root-type diffusions, The Annals of Applied Probability 21 (2011), 1282–1321.

- [13] S. Dereich, A. Neuenkirch, and L. Szpruch, An Euler-type method for the strong approximation of the Cox–Ingersoll–Ross process, Proceedings of the Royal Society A: Mathematical, Physical and Engineering Science 468 (2012), no. 2140, 1105–1115.

- [14] W. Feller, Diffusion Processes in One Dimension, Transactions of the American Mathematical Society 77 (1954), no. 1, pp. 1–31.

- [15] M. Giles, Improved multilevel Monte Carlo convergence using the Milstein scheme, Monte Carlo and quasi-Monte Carlo methods 2006, Springer, 2008, pp. 343–358.

- [16] , Multilevel Monte Carlo path simulation, Operations Research 56 (2008), no. 3, 607–617.

- [17] M. Giles, D. Higham, and X. Mao, Analysing Multi-Level Monte Carlo for options with non-globally Lipschitz payoff, Finance and Stochastics 13 (2009), no. 3, 403–413.

- [18] M. Giles and L. Szpruch, Multilevel Monte Carlo methods for applications in finance, Recent Advances in Computational Finance, World Scientific (2013).

- [19] P. Glasserman, Monte Carlo methods in Financial Engineering, vol. 53, Springer, 2003.

- [20] I. Gyöngy, A note on Euler’s approximations, Potential Analysis 8 (1998), no. 3, 205–216.

- [21] I. Gyöngy and M. Rásonyi, A note on Euler approximations for SDEs with Hölder continuous diffusion coefficients, Stochastic processes and their applications 121 (2011), no. 10, 2189–2200.

- [22] S. Heston, A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options, The Review of Financial Studies 6 (1993), no. 2, 327–343.

- [23] , A simple new formula for options with stochastic volatility, Course notes of Washington University in St. Louis, Missouri, 1997.

- [24] D. Higham, X. Mao, and A. Stuart, Strong convergence of Euler-type methods for nonlinear stochastic differential equations, SIAM Journal on Numerical Analysis 40 (2002), no. 3, 1041–1063.

- [25] M. Hutzenthaler and A. Jentzen, Numerical approximations of stochastic differential equations with non-globally lipschitz continuous coefficients, Mem. Amer. Math. Soc. 236 (2015), no. 1112.

- [26] M. Hutzenthaler, A. Jentzen, and P. Kloeden, Strong and weak divergence in finite time of Euler’s method for stochastic differential equations with non-globally Lipschitz continuous coefficients, Proceedings of the Royal Society A: Mathematical, Physical and Engineering Science 467 (2011), no. 2130, 1563–1576.

- [27] , Strong convergence of an explicit numerical method for SDEs with nonglobally Lipschitz continuous coefficients, The Annals of Applied Probability 22 (2012), no. 4, 1611–1641.

- [28] M. Hutzenthaler, A. Jentzen, and M. Noll, Strong convergence rates and temporal regularity for Cox-Ingersoll-Ross processes and Bessel processes with accessible boundaries, arXiv:1403.6385 (2014).

- [29] A. Jentzen, P. Kloeden, and A. Neuenkirch, Pathwise approximation of stochastic differential equations on domains: higher order convergence rates without global Lipschitz coefficients, Numerische Mathematik 112 (2009), no. 1, 41–64 (English).

- [30] I. Karatzas and S. Shreve, Brownian motion and stochastic calculus, Springer, 1991.

- [31] P. Kloeden and A. Neuenkirch, Convergence of numerical methods for stochastic differential equations in mathematical finance, arXiv:1204.6620 (2012).

- [32] P. Kloeden and E. Platen, Numerical solution of stochastic differential equations, vol. 23, Springer Verlag, 1992.

- [33] N. Krylov, A simple proof of the existence of a solution of Itô’s equation with monotone coefficients, Theory of Probability & Its Applications 35 (1990), 583–587.

- [34] A. Neuenkirch and L. Szpruch, First order strong approximations of scalar SDEs defined in a domain, Numerische Mathematik 128 (2014), no. 1, 103–136.

- [35] H. Ngo and D. Taguchi, Strong rate of convergence for the Euler-Maruyama approximation of stochastic differential equations with irregular coefficients, arXiv:1311.2725 (2013).

- [36] S. Sabanis, Euler approximations with varying coefficients: the case of superlinearly growing diffusion coefficients, arXiv:1308.1796 (2013).

- [37] , A note on tamed Euler approximations, Electronic Communications in Probability 18 (2013), 1–10.

- [38] L. Szpruch, X. Mao, D. Higham, and J. Pan, Numerical simulation of a strongly nonlinear Ait-Sahalia-type interest rate model, BIT Numerical Mathematics 51 (2011), no. 2, 405–425.

- [39] L. Yan, The Euler scheme with irregular coefficients, The Annals of Probability 30 (2002), no. 3, 1172–1194.

Appendix A Proof of Lemma 2.1

The fact that is -Lipschitz continuous is straightforward. We prove

the one-sided Lipschitz property in two steps below.

Step . Let such that . Assume that is . From (2.3), we have, for , ,

and letting , we retrieve that

.

This shows that , where is a non-increasing function and is -Lipschitz continuous,

setting e.g. and .

Since is non-decreasing and -Lipschitz on , we have , with non-increasing and

-Lipschitz continuous on . This shows that satisfies (2.3) as well on .

Step . We now deal with the general case using a smoothing argument.

Let , , such that for all .

We consider a sequence of mollifiers whose supports are included in and define

as the convolution of and .

We observe that, for all ,

where we used (2.3) and the fact that . Since is smooth, we can apply Step to obtain, for all ,

Letting go to infinity, we then obtain

for all , which concludes the proof.