Numerical analysis for Spread option pricing model in illiquid underlying asset market: full feedback model

Abstract

This paper performs the numerical analysis and the computation of a Spread option in a market with imperfect liquidity. The number of shares traded in the stock market has a direct impact on the stock’s price. Thus, we consider a full-feedback model in which price impact is fully incorporated into the model. The price of a Spread option is characterize by a nonlinear partial differential equation. This is reduced to linear equations by asymptotic expansions. The Peaceman-Rachford scheme as an alternating direction implicit method is employed to solve the linear equations numerically. We discuss the stability and the convergence of the numerical scheme. Illustrative examples are included to demonstrate the validity and applicability of the presented method. Finally we provide a numerical analysis of the illiquidity effect in replicating an European Spread option; compared to the Black-Scholes case, a trader generally buys more stock to replicate this option.

a Faculty of Mathematics, Statistics and Computer Science , Semnan University, Tehran, Iran.

b Department of Mathematics and Statistics, McMaster University, Hamilton, Canada.

Keywords: Spread option pricing, Price impact, Illiquid markets, Nonlinear finance, Asymptotic analysis, Peaceman-Rachford scheme.

1 Introduction

Classical asset pricing theory assumes that traders act as price takers, that is,

they have no impact on the prices paid

or received. The relaxation of this assumption and its impact

on realized returns in asset pricing models is called liquidity risk. Consistent with this discussion, most of the option pricing models assume that an option trader cannot affect the price in trading the underlying asset to replicate the option payoff, regardless of her trading size. The papers of Black and Scholes [1], and much of the work undertaken in mathematical finance has been done under this underlying assumption (which is reasonable only in a perfectly liquid market).

In presence of a price impact, the replication of an option becomes more involved.

The first issues is whether or not the option is perfectly replicable. Second, one

has to find out how the presence of price impact affects the the replicating costs.

This encouraged researchers to develop a Black-Scholes model with price impact due to a large trader who is able to move the price by his/her actions.

An excellent survey of these research can be found in [2, 3, 4, 5].

Most of these research works discussed how the price impact affects the replication of an option written on a single stock.

The purpose of our paper is to investigate the effects of imperfect liquidity on the replication of an European Spread option by a typical option trader in a full-feedback model (any trade will impact the prices of the underlyings). Spread option is a simple example of multi-assets derivative, whose payoff is the difference between the prices of two or more assets; for instance let the prices of two underlying assets at time be and , then the payoff function of an European Spread option with maturity is (here is the strike of the option and the function is defined as ). Therefore the holder of an European Spread option has the right but not the obligation to buy the spread at the prespecified price and maturity . In general, there is no any analytical formula for the price of multi-assets options (even in models with perfect liquidity). The only exception is Margrabe formula for exchange options (Spread options with a strike of zero)[6]. Margrabe derived a Black and Scholes type solution for this class of options as follows

| (1.1) |

where is the standard normal cumulative distribution function and

| (1.2) |

Since that a linear combination of correlated lognormals is not lognormal, for non-zero strikes, there is no closed form Spread option valuation formula under the multivariate lognormal model. People rely on approximation formulas and numerical methods for Spreads valuation. Kirk[7] suggested the following analytical approximation for a Spread option with payoff

| (1.3) |

where

| (1.4) |

This formula provides a good approximation of Spread option prices when the strike is not far from zero. All these works on spread options assume a model with perfect liquidity.

Several Spread options are traded in the markets. Some popular Spread option products are : fixed Income Spread options and commodity Spread options (including Crush Spread options, Crack Spread options, Spark Spread options). In this work, we will focus our interest on Oil Markets and more specifically one of the most frequently quoted Spread options which are Crack Spreads. A Crack Spread represents the differential between the price of crude oil and petroleum products (gasoline or heating oil). The underlying indexes comprise futures prices of crude oil, heating oil and unleaded gasoline. Details of crack Spread options can be found in the New York Mercantile Exchange (NYMEX) Crack Spread Handbook [8]. In the oil markets with finite liquidity, trading does affect the underlying assets price. In our study, we are going to investigate the effects of impact price on Spread option pricing in oil markets, when trading affects only the crude oil price and not petroleum products .

This paper is organized as follows: Section2 discusses the general framework. In Section3 we apply an asymptotic expansion for the full nonlinear partial differential equation which characterizes the spread option price. In Section4, we propose a numerical method for the linearized equation. ( the Peaceman and Rachford numerical scheme [11] is employed). We discuss the stability and convergence of this scheme. In Section5, we carry out several numerical experiments and provide a numerical analysis of the model for European Spread calls. Section6 contains the concluding remarks.

2 Statement of the problem

In this section we describe the setup used for pricing Spread options. Our model of a financial market, based on a filtered probability space that satisfies the usual conditions, consists of two assets. Their prices are modeled by a two–dimensional diffusion process . All the stochastic processes in this work are assumed to be -adapted. Their dynamics are given by the following stochastic differential equations, in which is defined a two–dimensional standard correlated Brownian motion with correlation , and being its natural filtration augment by all -null sets:

| (2.1) |

Here and are the expected return and the volatility of stock in the absence of price impact. It is possible to add a forcing term, i.e.

| (2.2) |

( is the price impact function on the first stock). The term represents the price impact of the trading strategy We note that the classical Black-Scholes model is a special case of this model with . Our aim is to price a Spread option in this illiquid market model. The option’s payoff at maturity (a call at this case) is:

| (2.3) |

where is the strike price. The well-known generalized Black-Scholes equation (more details [12]) is used to characterize the spread option price within our full-feedback model for This leads to the nonlinear PDE

| (2.4) |

with the terminal condition in . Notice that the classical Black-Scholes model for Spread option is a special case of this model with .

3 Matched Asymptotic Expansions

In this section we use a matched asymptotic expansion technique to linearize (2.4). For this purpose we let so that (2.4) becomes

| (3.1) |

By replacing in the equation (3.1) with

| (3.2) |

we get

| (3.3) |

Using Maclaurin series expansion on some terms of above equation, we have:

| (3.4) |

Therefore we get the following linear equation for

| (3.5) |

and for

| (3.6) |

Here

| (3.7) |

In the following, we apply a numerical scheme for comupting and .

4 Numerical Solution of the Partial Differential Equations

4.1 The Alternating Direction Implicit

In this section, we present a numerical method for solving the partial differential equations:

| (4.1) |

and

| (4.2) |

Functions and are defined on . To simplify notations we write:

| (4.3) |

where

| (4.4) |

and . While symmetry considerations might speak for an , it is computationally simpler to use or , i.e., nclude the term fully in one of the two operators. Hence, we can write

| (4.5) |

where

| (4.6) |

In order to define a numerical solution for these equations, we need to truncate the spatial domain to a bounded area: . Let us introduce a grid of points in the time interval and in the truncated spatial domain:

| (4.7) |

For the simplicity assume that and . Functions and evaluated at a point on the grid are denoted as and . If we need to refer to the solution at a specific time point, we will use notation and . Furthermore, let symbols and denote second-order approximations to the operators and . Since the differential operator can be split as in (4.4) we can use Alternating Direction Implicit (ADI). The general idea is to split a time step into two and consider one operator or one space coordinate at a time. We implement the Peaceman-Rachford scheme. Let us begin by discretizing (4.1) in the time-direction:

| (4.8) |

Next Insert into (4.3), multiply by , and rearrange to obtain:

| (4.9) |

where denotes the identity operator. If we add on the left side and on the right side then we commit an error which is and therefore:

| (4.10) |

We now discretize in the space coordinates replacing by , by and by

| (4.11) |

This leads to the Peaceman-Rachford method [9]

| (4.12) |

where auxiliary function links above equations. We have introduced the values and to take into account the mix derivative term because it is not obvious how this term should be split. To align (4.12) with (4.11), we require that

| (4.13) |

where a discrepancy of order may be allowed with reference to a similar term in (4.10). One of the possible choices for and is

| (4.14) |

Finally, the Peaceman-Rachford scheme for in (4.1) is obtain as follows

| (4.15) |

In a first step we calculate using . This step is implicit in direction . In a second step, defined by equations (4.15), we use to calculate . This step is implicit in the direction of . The Peaceman-Rachford scheme for in (4.2) is obtained as follows:

| (4.16) |

where auxiliary function links above equations. To align (4.16) with (4.11) we require that

| (4.17) |

One of the possible choices for and is

| (4.18) |

The Peaceman-Rachford scheme for of (4.2) is obtained as follows:

| (4.19) |

In a first step calculate using . This step is implicit in direction . In ta second step, defined by equations (4.19), we use to calculate . This step is implicit in the

direction of .

Notice that due to the use of centered approximations of the derivatives, at , and , there appear external fictitious nodes , , and . The approximations in these nodes are obtained by using linear interpolation. Thus we have the following relations

| (4.20) |

Similarly, we can write the same relations in terms of . Now all values and are available. By repeating this procedure for we obtain and at all time points. The price of a Spread option at time can be approximated as :

| (4.21) |

4.2 Stability and Convergence of the Numerical Scheme

In this section, we discuss stability and convergence of the numerical schemes introduced in Section 4.1. First we analyze the stability of the Peaceman-Rachford. In this case, we can use the Von Neumann analysis to establish the conditions for stability. This approach was described in [9](Chapter 2.2). The Von Neumann analysis is based on calculating the amplification factor of a scheme (), and deriving conditions under which .

Theorem 4.1.

A one-step finite difference scheme (with constant coefficients) is stable in a stability region (any bounded nonempty region of the first octant of that has the origin as an accumulation point) if and only if there is a constant (independent of , , , and ) such that

| (4.22) |

Here is amplification factor of scheme with . If is independent of , and , the above stability condition can be replaced with the restricted stability condition

| (4.23) |

Proof.

See [9]. ∎

Remark 4.2.

This theorem shows that to determine the stability of a finite difference scheme with the constant coefficient, we only need to consider the amplification factor . This theorem does not apply directly to problems with variable coefficients. Nonetheless, the stability conditions obtained for constant coefficient schemes can be used to give stability conditions for the same scheme applied to equations with variable coefficients. The general procedure is that one considers each of the frozen coefficient problems arising from the scheme. The frozen coefficient problems are the constant coefficient problems obtained by fixing the coefficients at their values attained at each point in the domain of the computation. If each frozen coefficient problem is stable, then the variable coefficient problem is also stable. The interest reader can see the proof of this result in [13, 14].

For finding the amplification factor, a simpler and equivalent procedure is to replace and in the scheme

by for each value of and . Then, the resulting equation can be solved for the amplification factor.

Replacing and by and respectively, one gets

| (4.24) |

Here

| (4.25) |

Also, by replacing and by and respectively, we have that

| (4.26) |

According to ”Duhamel’s principle” we ignore the and terms in stability analysis (more details [9]). We obtain the amplification factor

| (4.27) |

where

| (4.28) |

By arranging, one gets

| (4.29) |

Thus

| (4.30) |

According to (4.25), we can write , where and are constants. Moreover so as , and , . Therefore by replacing in (4.30), one gets

| (4.31) |

It is enough to find conditions so that

| (4.32) |

Notice that

| (4.33) |

Thus , provided that . and also we have

| (4.34) |

Then , provided that . Therefore we should find conditions so that

| (4.35) |

or equivalently

| (4.36) |

Since , then for any , , and by , we have that

| (4.37) |

Thus (4.35) is satisfied if and if

| (4.38) |

Since and a sufficient condition for stability of the scheme is

| (4.39) |

Thus, the Peaceman-Rachford scheme is stable if the number of steps in the time interval, , and in the spatial domain, , satisfy inequality (4.39). This condition is a consequence of the cross-derivative terms. In the absence of these terms, the scheme would be unconditionally stable.

The remaining issue we need to address is the convergence of the numerical method to the true value of the problem. According to [9] , this scheme is first-order accurate in time and space and due to stability the scheme is convergent. Results of this convergence are summarized in the next section.

5 Numerical Results

Let us fix the values of the parameters of the marginal dynamical equations according to Table1. We also assume the following form for price impact

where is a constant price impact coefficient, is time to expiry, is a decay coefficient, and represent respectively, the lower and upper limit of the stock price within which there is a impact price.

We consider and for the subsequent numerical analysis. Choosing a different value for and will change the magnitude of the subsequent results, however, the main qualitative results remain valid.

| Asset 1 | 112 | 0.15 | 0 | 200 |

| Asset 2 | 104 | 0.10 | 0 | 200 |

Convergence of numerical results. As we mentioned in Section1, the exact option values for the option in illiquid market are unknown. Since leads to the standard Black-Scholes model, we compare the results obtained from the numerical method (with and strike ) with the Margrabe’s closed formula for exchange options (i.e. Spread Option with strike ). We fix the values of the parameters

| m | l | ||||||

|---|---|---|---|---|---|---|---|

| 50 | 100 | 8.1979 | 9.1570 | 10.0519 | 10.8369 | 11.8622 | |

| 100 | 100 | 8.2110 | 9.1892 | 10.0930 | 10.8757 | 11.9579 | |

| 200 | 200 | 8.2153 | 9.2373 | 10.1607 | 10.9727 | 12.0041 | |

| Margrabe | 8.2323 | 9.2462 | 10.1723 | 10.9892 | 12.0666 | ||

| 50 | 100 | 8.0088 | 8.5425 | 9.1276 | 9.6662 | 10.5095 | |

| 100 | 100 | 8.0591 | 8.5983 | 9.1961 | 9.7205 | 10.5405 | |

| 200 | 200 | 8.0687 | 8.6222 | 9.2209 | 9.7843 | 10.5636 | |

| Margrabe | 8.0692 | 8.6235 | 9.2294 | 9.7949 | 10.5648 | ||

| 50 | 100 | 7.9195 | 8.2199 | 8.6180 | 9.0019 | 9.5315 | |

| 100 | 210 | 7.9734 | 8.2509 | 8.6296 | 9.0929 | 9.6244 | |

| 200 | 200 | 7.9950 | 8.3023 | 8.7106 | 9.1035 | 9.6728 | |

| Margrabe | 8.0186 | 8.3128 | 8.7115 | 9.1110 | 9.6775 | ||

| 50 | 100 | 7.9252 | 7.9803 | 8.1740 | 8.3417 | 8.6412 | |

| 100 | 100 | 7.9310 | 7.9852 | 8.1894 | 8.3532 | 8.6498 | |

| 200 | 200 | 7.9938 | 8.0515 | 8.2032 | 8.3686 | 8.6571 | |

| Margrabe | 8.0005 | 8.0588 | 8.2015 | 8.3799 | 8.6675 |

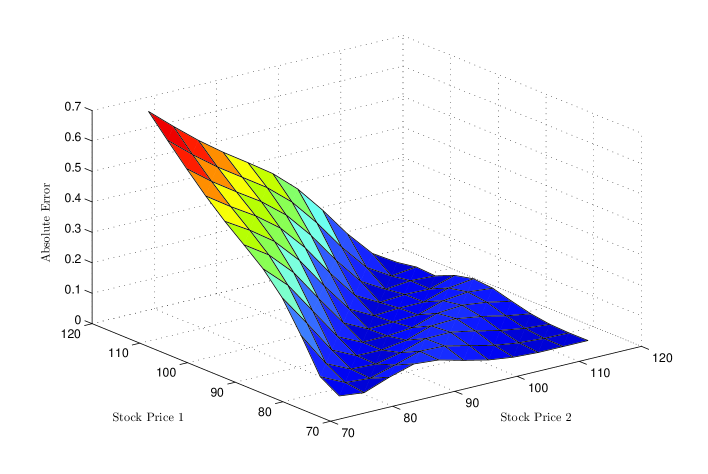

according to Table1, and vary the values of the correlation coefficient . Results of this convergence study are summarized in Table2. We can see from the table that the agreement is excellent. We plot the absolute error of our approximation (using strike and Margrabe’s closed formula as benchmark) against the stocks in Fig1. Results of the numerical method for Spread option in illiquid market are stated in Table3.

| k=20 | ||||||||

|---|---|---|---|---|---|---|---|---|

| 15.0929 | 7.1600 | 5.3275 | 4.2936 | 3.4027 | 2.3395 | 1.1267 | 0.1905 | |

| Excess price | 0.0001 | 0.0005 | 0.0005 | 0.0005 | 0.0005 | 0.0005 | 0.0003 | 0.00006 |

| 14.7992 | 6.2972 | 4.3645 | 3.3368 | 2.4486 | 1.4909 | 0.5435 | 0.0426 | |

| Excess price | 0.0001 | 0.0007 | 0.0009 | 0.0009 | 0.0009 | 0.0007 | 0.0003 | 0.00003 |

| 14.7085 | 5.7956 | 3.7731 | 2.7085 | 1.8642 | 0.9981 | 0.2593 | 0.0055 | |

| Excess price | 0.00006 | 0.0009 | 0.0013 | 0.0013 | 0.0012 | 0.0009 | 0.0004 | 0.00001 |

| 14.6833 | 5.2299 | 3.0523 | 1.9601 | 1.1531 | 0.4387 | 0.0088 | 0.0029 | |

| Excess price | 0.00003 | 0.0013 | 0.0020 | 0.0020 | 0.0018 | 0.0012 | 0.0003 | 0.00000 |

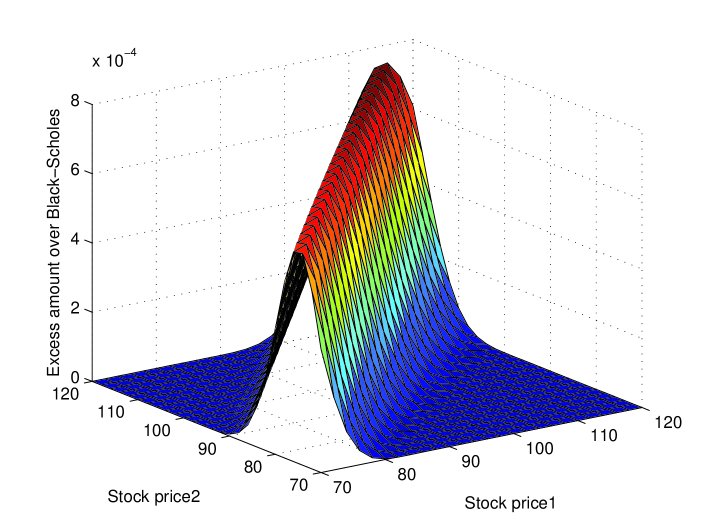

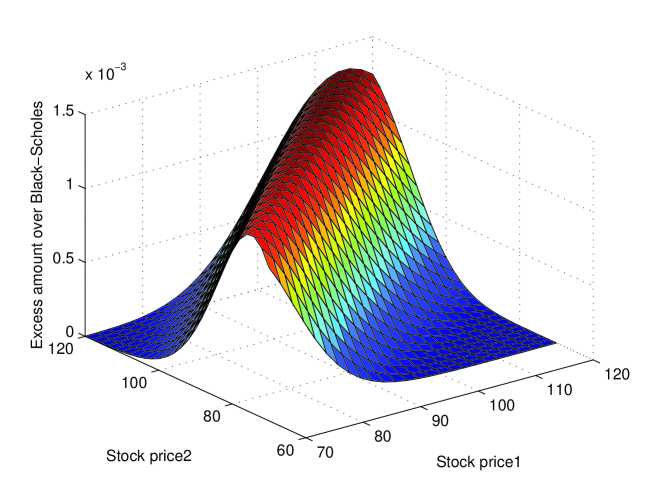

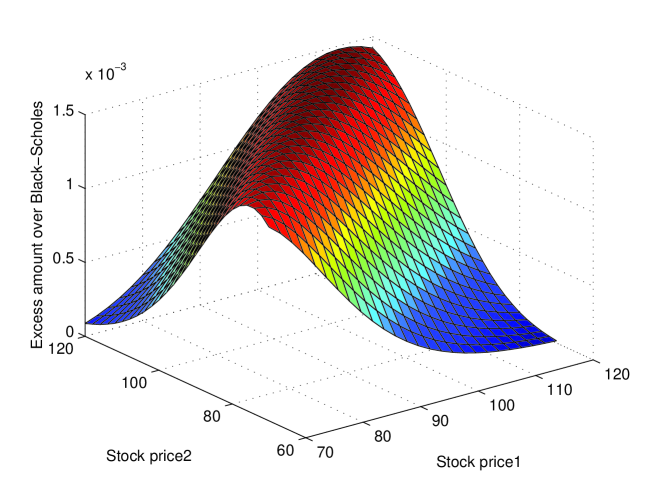

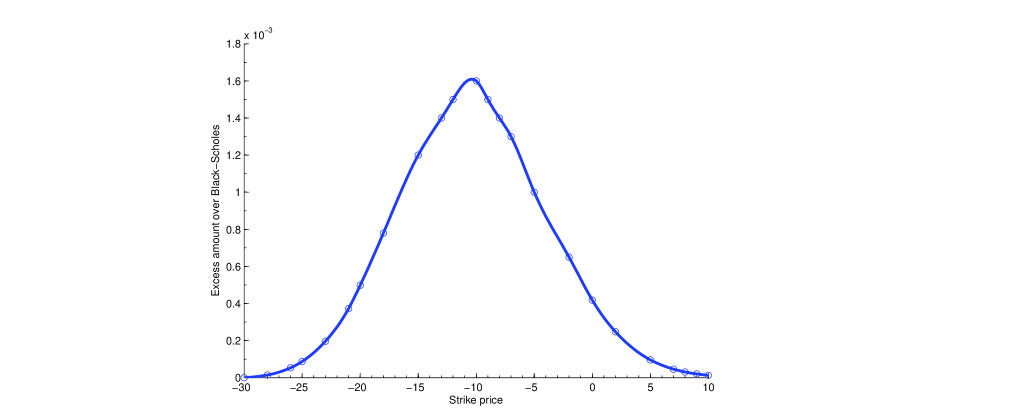

Replicating cost. Next investigate the effects of the price impact (full feedback model) on the replication cost of Spread option. We investigate the excess price which is the difference between the call price in the full feedback model and the corresponding Black-Scholes price.

These figures indicate that the Spread option price in the full feedback model is higher than the classical Spread option price.

As the option becomes more and more in the money and out of the money, the excess price converges monotonically to zero.

6 Conclusion

In this work, we have investigated a model which incorporates illiquidity of the underlying asset into the classical multi-asset Black-Scholes-Merton framework. We considered the full feedback model in which the hedger is assumed to be aware of the feedback effect and so would change the hedging strategy accordingly. Since there is no analytical formula for the price of an option within this model, we applied the Matched Asymptotic Expansions technique to linearize the partial differential equation characterizing the price. We applied a standard alternating direction implicit method (Peaceman-Rachford scheme) to solve the corresponding linear equations numerically. We also discussed the stability and the convergence of the numerical scheme. By running a numerical experiment, we investigated the effects of liquidity on the Spread option pricing in the full feedback model. Finally, we found out that the Spread option price in the market with finite liquidity (full feedback model), is more than the Spread option price in the classical Black-Scholes-Merton framework.

References

- [1] Black. F and Scholes. M, The pricing of options and corporate liabilities J. Political Economy 81 (1973), pp 637-654.

- [2] Frey, Perfect option replication for a large trader, Finance Stoch., 2 (1998), pp. 115-142.

- [3] J. Sch¨onbucher and P. Wilmott , The feedback effect of hedging in illiquid markets, SIAM J. Appl. Math., 61(2000), pp. 232-272.

- [4] Liu and J. Yong (2005), Option pricing with an illiquid underlying asset market, J. Econom. Dynam. Control, 29, pp. 2125-2156.

- [5] Kristoffer J. Glover, Peter W. Duck, David P. Newton. On Nonlinear Models of Markets with Finite Liquidity: Some Cautionary Notes. SIAM Journal on Applied Mathematics 70:8,(2010), 3252-3271.

- [6] Margrabe. W, The value of an option to exchange one asset for another, J. Finance 33 (1978 ) pp 177-86.

- [7] Kirk. E, Correlation in the energy markets, Managing Energy Price Risk 1st edn (Risk Publications) 1995, pp 71-8.

-

[8]

New York Mercantile Exchange, ”Crack Spread handbook.”

partners.futuresource.com/marketcenter/pdfs/crack.pdf, 2011. - [9] Strikwerda, J. C. Finite Difference Schemes and Partial Differential Equations, Chapman Hall, 1989.

- [10] Duffy, D. J, Finite Difference Methods in Financial Engineering, Wiley Finance 2006.

- [11] Peaceman, D. W. and H. H. Rachford, The Numerical Solution of Parabolic and Elliptic Differential Equations, Journal of the Society for Industrial and Applied Mathematics, Vol. 3, No. 1, 1955, 28-41.

- [12] Duffie, Dynamic Asset Pricing Theory, 2nd ed., Princeton University Press, Princeton,NJ. (1996).

- [13] Lax, P.D., and L. Nirenberg, On stability of difference schemes; a sharp form of Gdrding’s inequality, Cornm. Pure Appl. Math., 19 (1966), pp. 473-492.

- [14] Wade, B. A., Stability and Sharp Convergence Estimates for Symmetrizable Difference Operators, Ph.D. Thesis, University of Wisconsin-Madison, 1987.