Vector Quantile Regression: An Optimal Transport Approach

Abstract

We propose a notion of conditional vector quantile function and a vector quantile regression. A conditional vector quantile function (CVQF) of a random vector , taking values in given covariates , taking values in , is a map , which is monotone, in the sense of being a gradient of a convex function, and such that given that vector follows a reference non-atomic distribution , for instance uniform distribution on a unit cube in , the random vector has the distribution of conditional on . Moreover, we have a strong representation, almost surely, for some version of . The vector quantile regression (VQR) is a linear model for CVQF of given . Under correct specification, the notion produces strong representation, , for denoting a known set of transformations of , where is a monotone map, the gradient of a convex function, and the quantile regression coefficients have the interpretations analogous to that of the standard scalar quantile regression. As becomes a richer class of transformations of , the model becomes nonparametric, as in series modelling. A key property of VQR is the embedding of the classical Monge-Kantorovich’s optimal transportation problem at its core as a special case. In the classical case, where is scalar, VQR reduces to a version of the classical QR, and CVQF reduces to the scalar conditional quantile function. An application to multiple Engel curve estimation is considered.

keywords:

[class=MSC]keywords:

arXiv:1406.4643 \startlocaldefs \endlocaldefs

T1First ArXiv submission: June, 2014. Carlier is partially supported by INRIA and the ANR for partial support through the Projects ISOTACE (ANR-12-MONU-0013) and OPTIFORM (ANR-12-BS01-0007). Chernozhukov is partially supported by an NSF grant. Galichon is partially supported by the European Research Council under the European Union’s Seventh Framework Programme (FP7/2007-2013) / ERC grant agreement 313699.

, and

1 Introduction

Quantile regression provides a very convenient and powerful tool for studying dependence between random variables. The main object of modelling is the conditional quantile function (CQF) , which describes the -quantile of the random scalar conditional on a -dimensional vector of regressors taking a value . Conditional quantile function naturally leads to a strong representation via relation:

where is the latent unobservable variable, normalized to have a uniform reference distribution, and is independent of regressors . The mapping is monotone, namely non-decreasing, almost surely.

Quantile regression (QR) is a means of modelling the conditional quantile function. A leading approach is linear in parameters, namely, it assumes that there exists a known -valued vector , containing transformations of , and a ( vector-valued) map of regression coefficients such that

for all in the support of and for all quantile indices in . This representation highlights the vital ability of QR to capture differentiated effects of the explanatory variable on various conditional quantiles of the dependent variable (e.g., impact of prenatal smoking on infant birthweights). QR has found a large number of applications; see references in Koenker ([18])’s monograph. The model is flexible in the sense that, even if the model is not correctly specified, by using more and more suitable terms we can approximate the true CQF arbitrarily well. Moreover, coefficients can be estimated via tractable linear programming method ([20]).

The principal contribution of this paper is to extend these ideas to the cases of vector-valued , taking values in . Specifically, a vector conditional quantile function (CVQF) of a random vector , taking values in given the covariates , taking values in , is a map , which is monotone with respect to , in the sense of being a gradient of a convex function, which implies that

| (1.1) |

and such that the following strong representation holds with probability 1:

| (1.2) |

where is latent random vector uniformly distributed on . We can also use other non-atomic reference distributions on , for example, the standard normal distribution instead of uniform distribution (as we can in the canonical, scalar quantile regression case). We show that this map exists and is unique under mild conditions, as a consequence of Brenier’s polar factorization theorem. This notion relies on a particular, yet very important, notion of monotonicity (1.1) for maps , which we adopt here.

We define vector quantile regression (VQR) as a model of CVQF, particularly a linear model. Specifically, under correct specification, our linear model takes the form:

where is a monotone map, in the sense of being a gradient of convex function; and is a map of regression coefficients from to the set of matrices with real entries. This model is a natural analog of the classical QR for the scalar case. In particular, under correct specification, we have the strong representation

| (1.3) |

where is uniformly distributed on conditional on . (Other reference distributions could also be easily permitted.)

We provide a linear program for computing in population and finite samples. We shall stress that this formulation offers a number of useful properties. In particular, the linear programming problem admits a general formulation that embeds the optimal transportation problem of Monge-Kantorovich-Brenier, establishing a useful conceptual link to an important area of optimization and functional analysis (see, e.g. [34], [35]).

Our paper also connects to a number of interesting proposals for performing multivariate quantile regressions, which focus on inheriting certain (though not all) features of univariate quantile regression– for example, minimizing an asymmetric loss, ordering ideas, monotonicity, equivariance or other related properties, see, for example, some key proposals (including some for the non-regression case) in [6], [23], [32], [16], [24], [2], which are contrasted to our proposal in more details below. Note that it is not possible to reproduce all ”desirable properties” of scalar quantile regression in higher dimensions, so various proposals focus on achieving different sets of properties. Our proposal is quite different from all of the excellent aforementioned proposals in that it targets to simultaneously reproduce two fundamentally different properties of quantile regression in higher dimensions – namely the deterministic coupling property (1.3) and the monotonicity property (1.1). This is the reason we deliberately don’t use adjective “multivariate” in naming our method. By using a different name we emphasize the major differences of our method’s goals from those of the other proposals. This also makes it clear that our work is complementary to other works in this direction. We discuss other connections as we present our main results.

1.1 Plan of the paper

We organize the rest of the paper as follows. In Section 2, we introduce and develop the properties of CVQF. In Section 3, we introduce and develop the properties of VQR as well its linear programming implementation. In Section 4, we provide computational details of the discretized form of the linear programming formulation, which is useful for practice and computation of VQR with finite samples. In Section 5, we implement VQR in an empirical example, providing the testing ground for these new concepts. We provide proofs of all formal results of the paper in the Appendix.

2 Conditional Vector Quantile Function

2.1 Conditional Vector Quantiles as Gradients of Convex Functions

We consider a random vector defined on a complete probability space . The random vector takes values in . The random vector is a vector covariate, taking values in . Denote by the joint distribution function of , by the (regular) conditional distribution function of given , and by the distribution function . We also consider random vectors defined on a complete probability space , which are required to have a fixed reference distribution function . Let be the a suitably enriched complete probability space that can carry all vectors and with distributions and , respectively, as well as the independent (from all other variables) standard uniform random variable on the unit interval. Formally, this product space takes the form , where is the canonical probability space, consisting of the unit segment of the real line equipped with Borel sets and the Lebesgue measure. The symbols , , , , denote the support of , , , , , and denotes the support of . We denote by the Euclidian norm of .

We assume that the following condition holds:

-

(N)

has a density with respect to the Lebesgue measure on with a convex support set .

The distribution describes a reference distribution for a vector of latent variables , taking values in , that we would like to link to via a strong representation of the form mentioned in the introduction. This vector will be one of many random vectors having a distribution function , but there will only be one , in the sense specified below, that will provide the required strong representation. The leading cases for the reference distribution include:

-

•

the standard uniform distribution on the unit -dimensional cube, ,

-

•

the standard normal distribution over , or

-

•

any other reference distribution on , e.g., uniform on a ball.

Our goal here is to create a deterministic mapping that transforms a random vector with distribution into such that conditional on has the conditional distribution . Such a map that pushes forward a probability distribution of interest onto another one is called a transport between these distributions. That is, we want to have a strong representation property like (1.2) that we stated in the introduction. Moreover, we would like this transform to have a monotonicity property, as in the scalar case. Specifically, in the vector case we require this transform to be a gradient of a convex function, which is a plausible generalization of monotonicity from the scalar case. Indeed, in the scalar case the requirement that the transform is the gradient of a convex map reduces to the requirement that the transform is non-decreasing. We shall refer to the resulting transform as the conditional vector quantile function (CVQF). The following theorem shows that such map exists and is uniquely determined by the stated requirements.

Theorem 2.1 (CVQF as Conditional Brenier Maps).

Suppose condition (N) holds.

(i) There exists a measurable map from to , such that for each in , the map is the unique (-almost everywhere) gradient of convex function such that, whenever , the random vector has the distribution function , that is,

| (2.1) |

(ii) Moreover, there exists a random variable such that -almost surely

| (2.2) |

The theorem is our first main result that we announced in the introduction. It should be noted that the theorem does not require to have an absolutely continuous distribution, it holds for discrete and mixed outcome variables; only the reference distribution for the latent variable is assumed to be absolutely continuous. It is also noteworthy that in the classical case of and being scalars we recover the classical conditional quantile function as well as the strong representation formula based on this function ([29], [18]). Regarding the proof, the first assertion of the theorem is a consequence of fundamental results due to McCann ([25]) (as, e.g, stated in [34], Theorem 2.32) who in turn refined the fundamental results of [3]. These results were obtained in the case without conditioning. The second assertion is a consequence of Dudley-Philipp ([12]) result on abstract couplings in Polish spaces.

Remark 2.1 (Monotonicity).

The transform has the following monotonicity property:

| (2.3) |

Remark 2.2 (Uniqueness).

In part (i) of the theorem, is equal to a gradient of some convex function for -almost every value of and it is unique in the sense that any other map with the same properties will agree with it -almost everywhere. In general, the gradient exists -almost everywhere, and the set of points where it does not is negligible. Hence the map is still definable at each from the gradient values on , by defining it at each as a smallest-norm element of .

Let us assume further that the following condition holds:

-

(C)

For each , the distribution admits a density with respect to the Lebesgue measure on .

Under this condition we can recover uniquely in the following sense:

Theorem 2.2 ( Conditional Inverse Vector Quantiles or Conditional Vector Ranks).

Suppose conditions (N) and (C) holds.

Then there exists a measurable map , mapping to , such that for each in , the map is the inverse of in the sense that:

for almost all under . Furthermore, we can construct in (2.2) as follows,

| (2.4) |

Remark 2.3 (Conditional Vector Rank Function).

The mapping , which maps to , is the conditional rank function. When , it coincides with the conditional distribution function, but when it does not. The ranking interpretation stems from the fact that when we set , vector measures the centrality of observation for each of the dimensions, conditional on .

It is also of interest to state a further implication, which occurs under (N) and (C), on the link between the transportation map and its derivatives on one side, and the densities and on the other side. This link is a nonlinear second order partial differential equation called a (conditional) Monge-Ampère equation.

Corollary 2.1 (Conditional Monge-Ampère Equations).

Assume that conditions (N) and (C) hold and, further, that the map is continuously differentiable and injective for each . Under this condition, the following conditional forward Monge-Ampère equation holds for all :

| (2.5) |

where is the Dirac delta function in and . Reversing the roles of and , we also have the following conditional backward Monge-Ampère equation holds for all :

| (2.6) |

The latter expression is useful for linking the conditional density function to the conditional vector quantile function. Equations (2.5) and (2.6) are partial differential equations of the Monge-Ampère type, carrying an additional index . These equations could be used directly to solve for conditional vector quantiles given conditional densities. We can also use them to set up maximum likelihood method for recovering conditional vector quantiles. In the next section we describe a variational approach to recovering conditional vector quantiles.

2.2 Conditional Vector Quantiles as Optimal Transport

Under additional moment assumptions, the CVQF can be characterized and even defined as solutions to a regression version of the Monge-Kantorovich-Brenier’s optimal transportation problem or, equivalently, a conditional correlation maximization problem.

We assume that the following conditions hold:

-

(M)

The second moment of and the second moment of are finite:

We consider the following optimal transportation problem with conditional independence constraints:

| (2.7) |

where the minimum is taken over all random vectors defined on the probability space . Note that the value of objective is the Wasserstein distance between and subject to . Under condition (M) we will see that a solution exists and is given by constructed in the previous section.

The problem (2.7) is the conditional version of the classical Monge - Kantorovich problem with Brenier’s quadratic costs, which was solved by Brenier in considerable generality in the unconditional case. In the unconditional case, the canonical Monge problem is to transport a pile of coal with mass distributed across production locations from into a pile of coal with mass distributed across consumption locations from , and it can be rewritten in terms of random variables and . We are seeking to match with a version of that is closest in mean squared sense subject to having a prescribed distribution. Our conditional version above (2.7) imposes the additional conditional independence constraint .

The problem above is equivalent to covariance maximization problem subject to the prescribed conditional independence and distribution constraints:

| (2.8) |

where the maximum is taken over all random vectors defined on the probability space . This type of problem will be convenient for us, as it most directly connects to convex analysis and leads to a convenient dual program. This form also connects to unconditional multivariate quantile maps defined in [13], who employed them for purposes of risk analysis; our definition given in the previous section is more satisfactory, because it does not require any moment conditions, as follows from the results of [25].

The dual program to (2.8) can be stated as:

| (2.9) |

where is any vector such that , and minimization is performed over Borel maps from to and from to , where and are lower-semicontinuous for each value .

Theorem 2.3 (Conditional Vector Quantiles as Optimal Transport).

Suppose conditions (N), (C), and (M) hold.

(i) There exists a pair of maps and , each mapping from to , that solve the problem (2.9). For each , the maps and are convex and are Legendre transforms of each other:

for all and .

(iii) We can take the gradient of as the conditional vector quantile function, namely, for each , for almost every value under .

(iv) We can take the gradient of as the conditional inverse vector quantile function or conditional vector rank function, namely, for each , for almost every value under .

(v) The vector is a solution to the primal problem (2.8) and is unique in the sense that any other solution obeys almost surely under . The primal (2.8) and dual (2.9) have the same value.

(vi) The maps and are inverses of each other: for each , and for almost every under and almost every under

Remark 2.4.

There are many maps such that if , then . Any of these maps define a transport from to . Our choice is to take the optimal transport, in the sense that it minimizes the Wasserstein distance among such maps. This has several benefits: (i) the optimal transport is unique as soon as is absolutely continuous, as noted in Remark 2.2 and (ii) this object is easily computable through a linear programming problem. Note that the classical, scalar quantile map is the optimal transport from to in this sense, so oue notion indeed extends the classical notion of a quantile.

Remark 2.5.

Unlike in the scalar case, we cannot compute at a given point without computing the whole map . This highlights the fact that CVQF is not a local concept with respect to values of the rank .

Theorem 2.3 provides a number of analytical properties, formalizing the variational interpretation of conditional vector quantiles, providing the potential functions and , which are mutual Legendre transforms, and whose gradients are the conditional vector quantile functions and its inverse, the conditional vector rank function. This problem is a conditional generalization of the fundamental results by Brenier as presented in [34], Theorem 2.12.

Example 2.1 (Conditional Normal Vector Quantiles).

Here we consider the normal conditional vector quantiles. Consider the case where

Here is the conditional mean function and is a conditional variance function such that (in the sense of positive definite matrices) for each with . The reference distribution is given by . Then we have the following conditional vector quantile model:

Here we have the following conditional potential functions

and the following conditional vector quantile and rank functions:

It follows from Theorem 2.3 that solves the covariance maximization problem (2.8). This example is special in the sense that the conditional vector quantile and rank functions are linear in and , respectively.

2.3 Interpretations of vector rank

We can provide the following interpretations of :

1) As multivariate rank. An interesting interpretation of is as

a multivariate rank. In the univariate case, [18], Ch. 1.3 and

3.5, interprets as a continuous notion of rank in the setting of

quantile regression. The rank has a reference distribution , which is

typically chosen to be uniform on , but other reference distributions

could be used as well. The concept of vector quantile allows us to assign a

continuous rank to each of the dimensions, and the vector quantile mapping

is monotone with respect to the rank in the sense of being the gradient of a

convex function. As a result, can be interpreted as a multivariate

rank for , as we are trying to map the distribution of to a

prescribed distribution at minimal distortion, as seen in (2.7).

2) As a reference outcome for defining quantile treatment effects. Another motivation is related to the classical definition of quantile treatment effects introduced by [27], and further developed by [10], [18], and others. Suppose we define as an outcome for an untreated population; for this we simply set the reference distribution to the distribution of outcome in the untreated population. Suppose is the indicator of the receiving a treatment ( means no treatment). Then we can represent outcome as the multivariate health outcome conditional on . If , then the outcome is distributed as . If , then the outcome is distributed as . The corresponding notion of vector quantile treatment effects is

3) As nonlinear latent factors. As it is apparent in the variational formulation (2.7), the entries of can also be thought as latent factors, independent of each other and explanatory variables and having a prescribed marginal distribution , and that best explain the variation in . Therefore, the conditional vector quantile model (2.2) provides a non-linear latent factor model for with factors solving the matching problem (2.7). This interpretation suggests that this model may be useful in applications which require measurement of multidimensional unobserved factors, for example, cognitive ability, persistence, and various other latent propensities; see, for example, [8].

2.4 Overview of Other Notions of Multivariate Quantile

We briefly review other notions of multivariate quantiles in the statistical literature. We highlight the main contrasts with the notion we are using, based on optimal transport. For the sake of clarity of exposition, we discuss the unconditional case; albeit the comparisons extend naturally to the regression case.

In [6], the following definition of multivariate quantile function is suggested: for , let

which coincides with the classical notion when . See also [32]. More generally, [23] offers the following definition based on M-estimators, still for ,

for a choice of kernel assumed to be convex with respect to its first argument. Like our proposal, these notions of quantile maps are gradients of convex potentials. However, unlike our proposal, these notions do not provide a transport from a fixed distribution over values of to the distribution of as soon as .

In [36], a notion of quantile based on the Rosenblatt map is investigated. In the case , this quantile is defined for as

where and are the univariate and the conditional univariate quantile map. This map is a transport of the distribution of ; however, in this definition, and play sharply assymetric roles, as the second dimension is defined conditional on the first one. Unlike ours, this quantile map is not a gradient of convex function.

In [16], the authors specify a vector of latent indices the unit ball of . For , they define multivariate quantiles as

where and minimize subject to constraint . In contrast to ours, their notion of quantile is a set-valued. A closely related construction is provided by [24] who define the directional quantile associated to the index via:

where is the univariate quantile function of the random variable . We can provide a transport interpretation to this notion of quantiles, but unlike our proposal this map is not a gradient of convex function.

A notion of quantile based on a partial order on is proposed in [2]. For an index , these authors define

where is the set of elements that can be ordered by relative to the point . Unlike our proposal, the index is scalar and the quantile is set-valued.

3 Vector Quantile Regression

3.1 Linear Formulation

Here we let denote a vector of regressors formed as transformations of , such that the first component of is 1 (intercept term in the model) and such that conditioning on is equivalent to conditioning on . The dimension of is denoted by and we shall denote with .

In practice, would often consist of a constant and some polynomial or spline transformations of as well as their interactions. Note that conditioning on is equivalent to conditioning on if, for example, a component of contains a one-to-one transform of .

Denote by the distribution function of and . Let denote the support of and the support of . We define linear vector quantile regression model (VQRM) as the following linear model of CVQF.

-

(L)

The following linearity condition holds:

where is a map from to the set of matrices such that is a monotone, smooth map, in the sense of being a gradient of a convex function:

where is map from to , and is a strictly convex map from to .

The parameter is indexed by the quantile index and is a matrix of quantile regression coefficients. Of course in the scalar case, when , this matrix reduces to a vector of quantile regression coefficients. This model is a natural analog of the classical QR for scalar where the similar regression representation holds. One example where condition (L) holds is Example 2.1, describing the conditional normal vector regression. It is of interest to specify other examples where condition (L) holds or provides a plausible approximation.

Example 3.1 (Saturated Specification).

The regressors with are saturated with respect to , if, for any , we have . In this case the linear functional form (L) is not a restriction. For this can occur if and only if takes on a finite set of values , in which case we can write:

Here the problem is equivalent to considering unconditional vector quantiles in populations corresponding to .

The rationale for using linear forms is two-fold – one is convenience of estimation and representation of functions and another one is approximation property. We can approximate a smooth convex potential by a smooth linear potential, as the following example illustrates for a particular approximation method.

Example 3.2 (Linear Approximation).

Let be of class with on the support . Consider a trigonometric tensor product basis of functions in . Then there exists a vector such that the linear map:

where and , provides uniformly consistent approximation of the potential and its derivative:

The approximation property via the sieve-type approach provides a rationale for the linear (in parameters) specification (1.3). Another approach, based on local polynomial approximations over a collection of (increasingly smaller) neighborhoods, also provides a useful rationale for the linear (in parameters) specification, e.g., similarly in spirit to [37]. If the linear specification does not hold exactly we say that the model is misspecified. If the model is flexible enough, by using a suitable basis or localization, then the approximation error is small, and we effectively ignore the error when assuming (1.3). However, when constructing a sensible estimator we must allow the possibility that the model is misspecified, which means we can’t really force (1.3) onto data. Our proposal for estimation presented next does not force (1.3) onto data, but if (1.3) is true in population, then as a result, the true conditional vector quantile function would be recovered perfectly in population.

3.2 Linear Program for VQR

Our approach to multivariate quantile regression is based on the multivariate extension of the covariance maximization problem with a mean independence constraint:

| (3.1) |

Note that the constraint condition is a relaxed form of the previous independence condition.

Remark 3.1.

The new condition is weaker than , but the two conditions coincide if is saturated relative to , as in Example 3.1, in which case for every . More generally, this example suggests that the richer is, the closer the mean independence condition becomes to the conditional independence.

The relaxed condition is sufficient to guarantee that the solution exists not only when (L) holds, but more generally when the following quasi-linear assumption holds.

-

(QL)

We have a quasi-linear representation a.s.

where is a map from to the set of matrices such that is a gradient of convex function for each and a.e. :

where is map from to , and is a strictly convex map from to .

This condition allows for a degree of misspecification, which allows for a latent factor representation where the latent factor obeys the relaxed independence constraints.

Theorem 3.1.

Suppose conditions (M), (N) , (C), and (QL) hold.

(i) The random vector entering the quasi-linear representation (QL) solves (3.1).

(ii) The quasi-linear representation is unique a.s. that is if we also have with , is a gradient of a strictly convex function in a.s., then and a.s.

(iii) Under condition (L) and assuming that has full rank, a.s. and solves (3.1). Moreover, a.s.

The last assertion is important – it says that if (L) holds, then the linear program (3.1), where the independence constraint has been relaxed into a mean independence constraint, will find the true linear vector quantile regression in the population.

3.3 Dual Program for Linear VQR

As explained in details in the appendix, Program (3.1) is an infinite-dimensional linear programming problem whose dual program is:

| (3.2) |

where , where the infimum is taken over all continuous functions , mapping to and mapping to , such that and are finite.

Since for fixed , the smallest which satisfies the pointwise constraint in (3.2) is given by

one may equivalently rewrite (3.2) as the minimization over continuous of

By standard arguments ([34], section 1.1.7), the infimum over continuous functions coincides with the one over smooth or simply integrable functions.

Theorem 3.2.

Under (M) and (QL), we have that the optimal solution to the dual is given by functions:

This result can be recognized as a consequence of strong duality of the linear programming (e.g. [34]).

3.4 Connecting to Scalar Quantile Regression

We now consider the connection to the canonical, scalar quantile regression primal problem, where is scalar and for each probability index , the linear functional form is used. [20] define linear quantile regression as with solving the minimization problem

| (3.3) |

where , with and denoting the negative and positive parts of . The above formulation makes sense and is unique under the following simplified conditions:

-

(QR)

and , is bounded and uniformly continuous, and is of full rank.

We note that (3.3) can be conveniently rewritten as

| (3.4) |

[20] showed that this convex program admits as dual formulation:

| (3.5) |

An optimal for (3.4) and an optimal rank-score variable in (3.5) may be taken to be

| (3.6) |

and thus the constraint reads:

| (3.7) |

which simply is the first-order optimality condition for (3.4).

We say that the specification of quantile regression is quasi-linear if

| (3.8) |

Define the rank variable , then under (3.8) we have that

and the first-order condition (3.7) implies that for each

The first property implies that and the second property can be easily shown to imply the mean-independence condition:

Thus quantile regression naturally leads to the mean-independence condition and the quasi-linear latent factor model. This is the reason we used mean-independence condition as a starting point in formulating the vector quantile regression. Moreover, in both vector and scalar cases, we have that, when the conditional quantile function is linear (not just quasi-linear), the quasi-linear representation coincides with the linear representation and becomes fully independent of .

The following result summarizes the connection more formally.

Theorem 3.3 (Connection to Scalar QR).

Suppose that (QR) holds.

(i) If (3.8) holds, then for we have the quasi-linear model holding

| a.s., and . |

Moreover, solves the problem of correlation maximization problem with a mean independence constraint:

| (3.9) |

(ii) The quasi-linear representation above is unique almost surely. That is, if we also have with , is increasing in a.s., then and a.s.

(iii) Consequently, if the conditional quantile function is linear, namely , so that , then the latent factors in the quasi-linear and linear specifications coincide, namely , and so do the model coefficients, namely .

4 Implementation of Vector Quantile Regression

In order to implement VQR in practice, we employ discretization of the problem, namely we approximate the distribution of the outcome-regressor vector and of the vector rank by discrete distributions and , respectively. For example, for estimation purposes we can approximate by an empirical distribution of the sample, and the distribution of by a finite grid.

Let denote values of outcomes and of regressors for ; we assume the first component of is . For estimation purposes, we assume these values are obtained as a random sample from distribution , and so each observation receives a point mass . When we perform computation for theoretical purposes, we can think of these values as grid points, which are not necessarily obtained as a random sample, and so each observation receives a point mass which does not have to be . We also set up a collection of grid points , for , for values of the vector rank , and assign the probability mass to each of the point. For example, if and we generate values as a random sample or via a uniformly spaced grid of points, then .

Thus, let be the matrix with row vectors and the matrix of row vectors ; the first column of this matrix is a vector of ones. Let be a matrix such that is the probability attached to a value , so that and . Let be the number of points in the support of . Let be a matrix, where the th row denoted by . Let be a matrix such that is the probability weight of (hence and ).

We are looking to find an matrix such that is the probability mass attached to which maximizes

subject to constraint , where is a vector of ones, and subject to constraints and .

Hence, the discretized VQR program is given in its primal form by

| (4.1) |

where the square brackets show the associated Lagrange multipliers, and in its dual form by

| (4.2) |

where is a vector, and is a matrix.

Problems (4.1) and (4.2) are two linear programming problems dual to each other. However, in order to implement them on standard numerical analysis software such as R or Matlab coupled with a linear programming software such as Gurobi, we need to convert matrices into vectors. This is done using the vec operation, which is such that if is a matrix, is a column vector of size such that . The use of the Kronecker product is also helpful. Recall that if is a matrix and is a matrix, then the Kronecker product is the matrix such that for all relevant choices of indices , The fundamental property linking Kronecker products and the vec operator is

Introduce , the optimization variable of the “vectorized problem”. Note that the variable is a -vector. Then we rewrite the objective function, ; as for the constraints, is a vector; and is a -vector. Thus we can rewrite the program (4.1) as:

| (4.3) |

which is a LP problem with variables and constraints. The constraints and are very sparse, which can be taken advantage of from a computational point of view.

5 Empirical Illustration

We demonstrate the use of the approach on a classical application of Quantile Regression since [21]: Engel’s ([15]) data on household expenditures, including 199 Belgian working-class households surveyed by Ducpetiaux ([11]), and 36 observations from all over Europe surveyed by Le Play ([28]). Due to the univariate nature of classical QR, [21] limited their focus on the regression of food expenditure over total income. But in fact, Engel’s dataset is richer and classifies household expenses in nine broad categories: 1. Food; 2. Clothing; 3. Housing; 4. Heating and lighting; 5. Tools; 6. Education; 7. Safety; 8. Medical care; and 9. Services. This allows us to have a multivariate dependent variable. While we could in principle have , we focus for illustrative purposes on a two-dimensional dependent variable (), and we choose to take as food expenditure ( category #1) and as housing and domestic fuel expenditure (category #2 plus category #4). We take with and the total expenditure (income) as an explanatory variable.

5.1 One-dimensional VQR

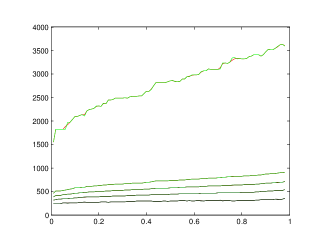

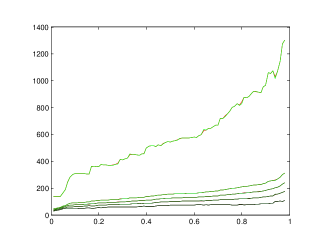

To begin with, we run a pair of one dimensional VQRs, where we regress on , and on . We plot the results in Figure 1; the curves drawn here are for five percentiles of the income (0%, 25%, 50%, 75%, 100%), and the corresponding probabilistic representations are

| (5.1) |

with and . Here, is interpreted as a propensity to consume food, while is interpreted as a propensity to consume the housing good. Note that in general, and are not independent; in other words, the distribution of differs from . In fact, the distribution of is called the copula associated to the conditional distribution of conditional on .

As explained above, when , VQR is very closely connected to classical quantile regression. Hence, in Figure 1, we also draw the classical quantile regression (in red). In each case, the curves exhibit very little difference between classical quantile regression and vector quantile regression. Small differences occur, since vector quantile regression in the scalar case can be shown to impose the fact that map in (3.5) is nonincreasing, which is not necessarily the case with classical quantile regression under misspecification in population, or even under specification in sample. As can be seen in Figure 1, the difference, however, is minimal.

From the plots in Figure 1, it is also apparent that one-dimensional VQR can also suffer from the “crossing problem,” namely the fact that may not be monotone with respect to . Indeed, the fact that is nonincreasing fails to imply the fact that is nondecreasing. There exist procedures to repair the crossing problem, see [7]. However, we see that the crossing problem is modest in the current example.

Running a pair of one-dimensional Quantile Regressions is interesting, but it does not immediately convey the information about the joint conditional dependence in and (given ). In other words, representations (5.1) are not informative about the joint propensity to consume food and income. One could also wonder whether food and housing are locally complements (respectively locally substitute), in the sense that, conditional on income, an increase in the food consumption is likely to be associated with an increase (respectively a decrease) in the consumption of the housing good. All these questions can be immediately answered with higher-dimensional VQR.

5.2 Two dimensional VQR

In contrast, the two-dimensional vector quantile regression with as a dependent variable yields a representation

where . Let us make a series of remarks.

First, and have an interesting interpretation: is a propensity for food expenditure, while is a propensity for domestic (housing and heating) expenditure. Let us explain this denomination. If VQR is correctly specified, then is convex with respect to , and , which implies in particular that

Hence an increase in keeping constant leads to an increase in . Similarly, an increase in keeping constant leads to an increase in .

Second, the quantity is a measure of joint propensity of expenditure conditional on . This is a way of rescaling the conditional distribution of conditional on into the uniform distribution on . If VQR is correctly specified, then is independent from , so that . In this case, can be used to detect “nontypical” values of .

Third, representation (5.2) may also be used to determine if and are local complements or substitutes. Indeed, if VQR is correctly specified and are independent conditional on , then , so that the cross derivative . In this case, (5.2) becomes and , which is equivalent to two single-dimensional quantile regressions. In this case, conditional on , an increase in is not associated to an increase or a decrease in . On the contrary, when are no longer independent conditional on , then the term is no longer zero. Assume it is positive. In this case, an increase in the propensity to consume food not only increases the food consumption , but also the housing consumption , which we interpret by saying that food and housing are local complements.

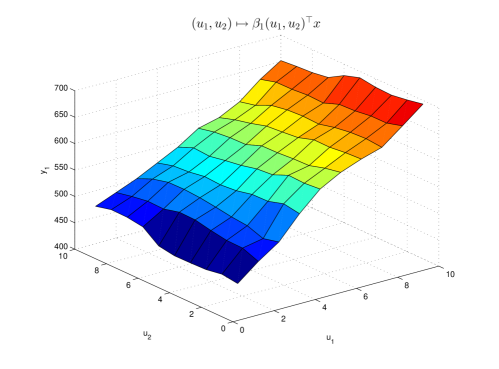

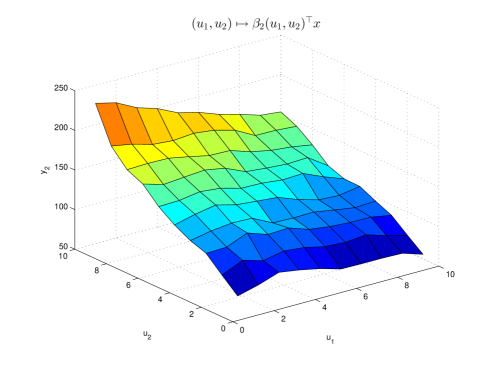

Going back to Engel’s data, in Figure 2, we set , where is the median value of the total expenditure , and we are able to draw the two-dimensional representations.

The top pane expresses as a function of and , while the bottom pane expresses as a function of and . The insights of the two-dimensional representation become apparent. One sees that while covaries strongly with and covaries strongly with , there is a significant and negative cross-covariation: covaries negatively with respect to , while covaries negatively with . The interpretation is that, for a median level of income, the food and housing goods are local substitutes. This makes intuitive sense, given that food and housing goods account for a large share of the surveyed households’ expenditures.

Appendix A Proofs for Section 2

A.1 Proof of Theorem 2.1

The first assertion of the theorem is a consequence of the refined version of Brenier’s theorem given by [25] (as, e.g, stated in [34], Theorem 2.32), which we apply for each . In particular, this implies that for each , the map is Borel-measurable. The Borel measurability of follows from the measurability of conditional probabilities and standard measurable selection arguments [14]; for details, we refer to Appendix D.

Next we are going to show that the probability law of is the same as that of . Indeed, for any rectangle ,

where the first equality relies on the regularity of the conditional distribution function, and the penultimate equality follows from the previous paragraph. Since probability measure defined over rectangles uniquely pins down the probability measure on all Borel sets via Caratheodory’s extension theorem, the claim follows.

To show the second assertion we invoke Dudley-Phillip’s ([12]) coupling result given in their Lemma 2.11.

Lemma A.1 (Dudley-Phillip’s coupling).

Let and be Polish spaces and a law on , with marginal law on . Let be a probability space and a random variable on with values in and . Assume there is a random variable on , independent of , with values in a Polish space and law on having no atoms. Then there exists a random variable on with values in such that .

First we recall that our probability space has the form:

where is the canonical probability space, consisting of the unit segment of the real line equipped with Borel sets and the Lebesgue measure. We use this canonical space to carry , which is independent of any other random variables appearing below, and which has the uniform distribution on . The space is Polish and the distribution of has no atoms.

Next we apply the lemma to to show existence of , where both and live on the probability space and that obeys the second assertion of the theorem. The variable takes values in the Polish space , and the variable takes values in the Polish space .

Next we describe a law on by defining a triple that lives on a suitable probability space. We consider a random vector with distribution , a random vector , independently distributed of , and uniquely determined by the pair , which completely characterizes the law of . In particular, the triple obeys , and . Moreover, the set is assigned probability mass 1 under .

By the lemma quoted above, given , there exists an , such that , but this implies that and that with probability 1 under .

A.2 Proof of Theorem 2.2

We condition on . By reversing the roles of and , we can apply Theorem 2.1 to claim that there exists a map with the properties stated in the theorem such that has distribution function , conditional on . Hence for any test function such that we have

This implies that for -almost every , we have Hence -almost surely, Thus we can set -almost surely in Theorem 2.1.

A.3 Proof of Theorem 2.3

The result follows from [34], Theorem 2.12.

Appendix B Proofs for Section 3

B.1 Proof of Theorem 3.1

We first establish part(i). We have a.s.

For any such that , and , we have by the mean independence

where depends only on . We have by Young’s inequality

but a.s. implies that a.s.

so taking expectations gives

which yields the desired conclusion.

We next establish part(ii). We can argue similarly as above to show that for some convex potential , and that for we have a.s.

Using the fact that and the fact that mean-independence gives , we have

where we used Young’s inequality again. Reversing the role of and and using the same reasoning, we also conclude that , and hence then

so that, thanks to the Young’s inequality again,

we have

which means that a.s., which by strict concavity admits as the unique solution a.s. This proves that a.s. and thus we have a.s.

The part (iii) is a consequence of part (i). Note that by part (ii) we have that a.s. and a.s. Since and are independent, we have that, for denoting vectors of the canonical basis in , and each :

Since has full rank this implies that for each , which implies the rest of the claim.

B.2 Proof of Theorem 3.2

We have that any feasible pair obeys the constraint

Let be the solution to the primal program. Then for any feasible pair we have:

The last inequality holds as equality if

| (B.1) |

since this is a feasible pair by (QL) and since

as shown the proof of the previous theorem. It follows that is the optimal value and it is attained by the pair (B.1).

B.3 Proof of Theorem 3.3

Obviously . Hence and which proves that is uniformly distributed and coincides with a.s. We thus have , with standard approximation argument we deduce that for every , which means that .

As already observed implies that in particular for , letting and using the a.e. continuity of we get . The converse inequality is obtained similarly by remaking that implies that .

Let us now prove that solves (3.9). Take uniformly distributed and mean-independent from and set , we then have , but since solves (3.5) we have . Observing that and integrating the previous inequality with respect to gives so that solves (3.9).

Next we show part(ii). Let us define for every Let us also define for in :

thanks to monotonicity condition, the maximization program in the display above is strictly concave in for every and each . We then note that

exactly is the first-order condition for the above maximization problem when . In other words, we have

| (B.2) |

with an equality holding a.s. for , i.e.

| (B.3) |

Using the fact that and the fact that the mean independence gives , we have

but reversing the role of and , we also have and then

so that, thanks to inequality (B.2)

which means that solves which, by strict concavity admits as unique solution.

Part (iii) is a consequence of Part (ii) and independence of and . Note that by part (ii) we have that a.s. and that a.s. Since and are independent, we have that

Since has full rank this implies that , which implies the rest of the claim.

Appendix C Additional Results for Section 2 and Section 3

This section provides a rigorous Proof of Duality for Conditional Vector Quantiles and Linear Vector Quantile Regression.

We claimed in the main text we stated two dual problems for CVQF and VQR without the proof. In this sections we prove that these assertions were rigorous. Here for simplicity of notation we assume that , which entails no loss of generality under our assumption that conditioning on and is equivalent.

We shall write , where denotes the non-constant component of vector . Let denote the joint density of with support , and the distribution of with support set . Assume without loss of generality that

C.1 Duality for Conditional Vector Quantiles

Let and be two integers, be a compact subset of and and be compact subsets of . Let have support , and we may decompose where denotes the first marginal of . We also assume that is centered i.e.

Finally, let have support . We are interested here in rigorous derivation for dual formulations for covariance maximization under an independence and then a mean-independence constraint.

Duality for the independence constraint

First consider the case of an independence constraint:

| (C.1) |

where consists of the probability measures on such that and , namely that

and

As already noticed, given a random such that , (C.1) is related to the problem of finding independent of and having law which is maximally correlated to . It is clear that is a nonempty (take ) convex and weakly compact set so that (C.1) admits solutions. Let us consider now:

| (C.2) |

subject to the constraint

| (C.3) |

Then we have

Theorem C.1.

Proof.

Let us rewrite (C.2) in standard convex programming form as :

where , is the linear continuous map from to defined by

and is defined for by:

It is easy to check that the Fenchel-Rockafellar theorem (see Ekeland and Temam [14]) applies here so that the infimum in (C.2) coincides with

| (C.4) |

Direct computations give that

that and

This shows that the maximization problem (C.4) is the same as (C.1). Therefore the infimum in (C.2) coincides with the maximum in (C.1). When one relaxes (C.2) to functions, we obtain a problem whose value is less than that of (C.2) (because minimization is performed over a larger set) and larger than the supremum in (C.1) (direct integration of the inequality constraint), the common value of (C.1) and (C.2)-(C.3) therefore also coincides with the value of the relaxation of (C.2)-(C.3).

C.2 Duality for Linear Vector Quantile Regression

Here we use the notation where we partition

with mapping to , corresponding to the coefficient in front of the constant. Let denote the interior of .

Let us denote by the mean of :

Let us now consider the mean-independent correlation maximization problem:

| (C.5) |

where consists of the probability measures on such that , and according to , is mean independent of i.e.

| (C.6) |

Again the constraints are linear so that is a nonempty convex and weak compact set so that the infimum in (C.1) is attained. In probabilistic terms, given distributed according to , the problem above consists in finding with law , mean-independent of (i.e. such that ) and maximally correlated to .

We claim that (C.5) is dual to

| (C.7) |

subject to

| (C.8) |

Then we have the following duality result

Theorem C.2.

Appendix D Proof of the measurability claim in Theorem 2.1

Let us denote by the probability law (absolutely continuous with respect to the Lebesgue measure on and having a convex support with nonempty interior) of and by the conditional probability law of given .

Let us also assume first that both and have finite second moments. Denoting by the Wasserstein space of probability measures on having finite second moments endowed with the -Wasserstein distance , we recall that it is a separable metric space (see [34]). Now consider the set-valued map

where is the set of having and as marginals. It then follows from standard measurable selection arguments (see [5] or chapter VIII of [14]) that admits a Borel (with respect to the Wasserstein metric) selection which we denote . Note in particular that is measurable and the optimality of is characterized by the fact that its support is included in the subdifferential of a convex function that we denote . The measurability claim in Theorem 2.1, amounts to proving that one can select a in a jointly measurable way (note that since is absolutely continuous with respect to the Lebesgue measure, is single valued on a set of full measure for but which depends on ). Let us first define as the conditional expectation of given , then is measurable separately in the variables and . We know that is a selection of the subgradient of a convex function which we may reconstruct by integration on the segment (there is no loss of generality in assuming here that lies in the interior of the support of and that for every ) as , from which it is easy to see that is convex in and measurable in . Now we regularize by Yosida regularization i.e. set for every

for each , has a Lipschitz gradient with respect to and depends in a measurable way on , hence is Lipschitz in its first argument and measurable in its second one, it thus follows form Proposition 1.1 in chapter VIII of [14] that is jointly measurable in . It is well known that converges pointwise to the element of minimal norm of so that is measurable.

Finally, in the case where one drops the finiteness of the second moments assumption, one cannot use optimal transport and as above. Instead, one has to proceed by approximation as was done in the seminal work of McCann [25]. First one has to suitably extend to the case of an arbitrary probability measure and again select a Borel (with respect to the narrow topology) selection of , which can be done since the narrow topology is metrizable and separable on the set of Borel probability measures. The remainder of the argument is the same as above.

Acknowledgements

We thank the editor Rungzhe Li, an associate editor, two anonymous referees, Denis Chetverikov, Xuming He, Roger Koenker, Steve Portnoy, and workshop participants at Oberwolfach 2013, Université Libre de Bruxelles, UCL, Columbia University, University of Iowa, MIT, and CORE for helpful comments. Jinxin He, Jérôme Santoul, and Simon Weber provided excellent research assistance.

References

- [1] Barlow, R. E., D. J. Bartholomew, J. M. Bremner, and H. D. Brunk (1972). Statistical inference under order restrictions. The theory and application of isotonic regression. John Wiley & Sons.

- [2] Belloni, A. and R.L. Winkler (2011). “On Multivariate Quantiles Under Partial Orders”. The Annals of Statistics, Vol. 39 No. 2, pp. 1125–1179

- [3] Brenier, Y (1991). “Polar factorization and monotone rearrangement of vector-valued functions ”. Comm. Pure Appl. Math. 44 4, pp. 375–417.

- [4] Carlier, G., Galichon, A., Santambrogio, F. (2010). “From Knothe’s transport to Brenier’s map”. SIAM Journal on Mathematical Analysis 41, Issue 6, pp. 2554-2576.

- [5] C. Castaing, M. Valadier, Convex analysis and measurable multifunctions, Lecture Notes in Mathematics, Vol. 580. Springer-Verlag, Berlin-New York, (1977).

- [6] Chaudhuri P. (1996). “On a geometric notion of quantiles for multivariate data,”. Journal of the American Statistical Association 91, pp. 862–872.

- [7] Chernozhukov, V., Fernandez-Val, I., and A. Galichon (2010). “Quantile and Probability Curves without Crossing”. Econometrica 78(3), pp. 1093–1125.

- [8] Cunha, F., Heckman, J. and Schennach, S. (2010). “Estimating the technology of cognitive and noncognitive skill formation”. Econometrica 78(3), pp. 883–931.

- [9] Dette, H., Neumeyer, N., and K. Pilz (2006). “A simple Nonparametric Estimator of a Strictly Monotone Regression Function”. Bernoulli, 12, no. 3, pp. 469–490.

- [10] Doksum, K. (1974). “Empirical probability plots and statistical inference for nonlinear models in the twosample case”. Annals of Statistics 2, pp. 267–-277.

- [11] Ducpetiaux, E. (1855). Budgets économiques des classes ouvrières en Belgique, Bruxelles.

- [12] Dudley, R. M., and Philipp, W. (1983). “Invariance principles for sums of Banach space valued random elements and empirical processes”. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete 62 (4), pp. 509–552.

- [13] Ekeland, I., Galichon, A., and Henry, M. (2012). “Comonotonic measures of multivariate risks”. Mathematical Finance, 22 (1), pp. 109–132.

- [14] I. Ekeland, R. Temam, Convex Analysis and Variational Problems, Classics in Mathematics, Society for Industrial and Applied Mathematics, Philadelphia, (1999).

- [15] Engel, E. (1857). “Die Produktions und Konsumptionsverhältnisse des Königreichs Sachsen”. Zeitschrift des Statistischen Bureaus des Königlich Sächsischen Misisteriums des Innerm, 8, pp. 1–54.

- [16] Hallin, M., Paindaveine, D., and Šiman, M. (2010). “Multivariate quantiles and multiple-output regression quantiles: From L1 optimization to halfspace depth”. Annals of Statistics 38 (2), pp. 635–669.

- [17] He, X. (1997). “Quantile Curves Without Crossing”. American Statistician, 51, pp. 186–192.

- [18] Koenker, R. (2005), Quantile Regression. Econometric Society Monograph Series 38, Cambridge University Press.

-

[19]

Koenker, R. (2007). quantreg: Quantile

Regression. R package version 4.10.

http://www.r-project.org. - [20] Koenker, R. and G. Bassett (1978). “Regression quantiles,” Econometrica 46, 33–50.

- [21] Koenker, R. and Bassett, G. (1982). “Robust Tests of Heteroscedasticity based on Regression Quantiles,” Econometrica 50, pp. 43–61.

- [22] Koenker, R. and P. Ng (2005), “Inequality constrained quantile regression.” Sankhyā 67, no. 2, pp. 418–440.

- [23] Koltchinskii, V. (1997). “M-Estimation, Convexity and Quantiles”. Annals of Statistics 25, No. 2, pp. 435–477.

- [24] Kong, L. and Mizera, I. (2012). “Quantile tomography: using quantiles with multivariate data.” Statistica Sinica 22, pp. 1589–1610.

- [25] McCann, R.J. (1995). “Existence and uniqueness of monotone measure-preserving maps”. Duke Mathematical Journal 80 (2), pp. 309–324.

- [26] Laine, B. (2001). “Depth contours as multivariate quantiles: a directional approach.” Master’s thesis, Université Libre de Bruxelles.

- [27] Lehmann, E. (1974). “Nonparametrics: statistical methods based on ranks. ”Holden-Day Inc., San Francisco, Calif.

- [28] Le Play, F. (1855). Les Ouvriers Européens. Etudes sur les travaux, la vie domestique et la condition morale des populations ouvrières de l’Europe. Paris.

- [29] Matzkin, R. (2003). “Nonparametric estimation of nonadditive random functions,” Econometrica 71, pp. 1339–1375.

-

[30]

R Development Core Team (2007): R: A language

and environment for statistical computing. R Foundation for Statistical

Computing, Vienna, Austria. ISBN 3-900051-07-0, URL

http://www.R-project.org. - [31] Ryff, J.V. (1970). “Measure preserving Transformations and Rearrangements.” J. Math. Anal. and Applications 31, pp. 449–458.

- [32] Serfling, R. (2004). “Nonparametric multivariate descriptive measures based on spatial quantiles”. Journal of Statistical Planning and Inference 123, pp. 259–278.

- [33] Tukey, J. (1975). Mathematics and the picturing of data. In Proc. 1975 International Congress of Mathematicians, Vancouver pp. 523–531. Montreal: Canadian Mathematical Congress.

- [34] Villani, C. (2003). Topics in Optimal Transportation. Providence: American Mathematical Society.

- [35] Villani, C. (2009). Optimal transport: Old and New. Grundlehren der mathematischen Wissenschaften, Springer-Verlag, Heidelberg, 2009.

- [36] Wei, Y. (2008). “An Approach to Multivariate Covariate-Dependent Quantile Contours With Application to Bivariate Conditional Growth Charts”. Journal of the American Statistical Association, 103 (481), pp. 397–409.

- [37] Yu, K., and Jones, M.C. (1998), “Local Linear Quantile Regression”. Journal of the American Statistical Association, 93 (441), pp. 228–237.