Fact Sheet Research on Bayesian Decision Theory

Abstract.

In this fact sheet we give some preliminary research results on the Bayesian Decision Theory. This theory has been under construction for the past two years. But what started as an intuitive enough idea, now seems to have the makings of something more fundamental.

1. Introduction

It has been shown that the product and sum rules of both the Bayesian probability and the Bayesian information theories are derivable by way of consistency, [8, 30, 14, 41, 58]; the implication being that in our plausibility and relevancy judgments we humans have a preference for consistency, or, equivalently, rationality. Moreover, Knuth, a MaxEnt-Bayesian111MaxEnt-Bayesians are, as a rule, physicists that trace their statistical lineage from Jaynes, back to Jeffreys, back to Laplace., is now researching if the very laws of physics may be derived by way of consistency constraints on lattices of events, [43].

In light of these exciting new developments, in both the fields of inference and physics, where consistency arguments are taking the stage by storm, and the fact that these authors, after two years of continuous research, have reached the point that they have come to trust their Bayesian decision theory to almost the same extent as they have grown to trust the Bayesian probability and information theories222The former being their field of expertise, and the latter being the subject matter of the first author’s current thesis work., these authors have come to entertain the notion that maybe their Bayesian decision theory, which initially started as an intuitive enough Bayesian alternative for the paradigm of behavioral economics, might actually be Bayesian in the strictest sense of the word; that is, an inescapable consequence of the desideratum of consistency.

In this fact sheet we will present the case, as it currently stands, for the Bayesian decision theory, and which led us to this conjecture, together with the consistency proof of the Bernoulli utility function, also known as the Weber-Fechner law of sense perception.

2. The Bayesian Decision Theory

The Bayesian decision theory is very simple in structure. Its algorithmic steps are the following:

-

(1)

Use the product and sum rules of Bayesian probability theory to construct outcome probability distributions.

-

(2)

If our outcomes are monetary in nature, then by way of the Bernoulli utility function we may map utilities333Or, as Bernoulli called them, moral values, [6]. to the monetary outcomes of our outcome probability distributions.

-

(3)

Maximize the sum of the lower and upper bounds of the resulting utility probability distributions.

This, then, is the whole of the Bayesian decision theory.

3. Constructing Outcome Probability Distributions

In the Bayesian decision theory each problem of choice is understood to consist of a set of decisions from which we must choose. Each possible decision, when taken, has its own set of possible outcomes, and each outcome, for a given decision, has its own plausibility of occurring relative to the other outcomes under that same decision. So, each decision in our problem of choice admits its own outcome probability distribution.

We will demonstrate in this section how to construct outcome probability distributions using the rules of Bayesian probability theory444See also Appendix A.. In our hypothetical problem of choice, the possible decisions , for , under consideration are whether or not to wear seat belts:

The relevant events , for , when driving a car, as perceived by the decision maker, are

The perceived outcomes , for , are

For this particular case, the decisions taken do not modulate the probabilities of an event. So, we have that the probability for an event conditional on the decision taken is the same for both decisions, say:

| (3.1) |

for . However, the conditional probability distributions of the outcomes given an event are modulated by the decision taken.

We first consider the case where the decision maker is considering to wear seat belts, that is, . Say, we have the following conditional probabilities:

Then by way of the product rule, [30],

| (3.3) |

we may combine the probability of an event, (3.1), with the corresponding conditional probability distributions of some outcome given that event, (3), and obtain the probabilities of an event and an outcome given decision :

| (3.4) |

We may present all these probabilities (3.4) in a table and so get the corresponding bivariate probability distribution, Table 1.

| : | 0.9500 | 0.0 | 0.0 |

| : | 0.0370 | 0.0120 | 0.0 |

| : | 0.0002 | 0.0007 | 0.0001 |

Let be a set of mutually exclusive and exhaustive propositions, that is, one and only one of the is necessarily true. Let be another set of mutually exclusive and exhaustive propositions. Then, by way of the generalized sum rule, [30], we have

| (3.5) |

where . Using this generalized sum rule, we may ‘marginalize’ the event-outcome probabilities over the events , that is,

| (3.6) |

and so get the marginalized outcome probability distribution, Table 2.

| 0.9872 | 0.0127 | 0.0001 |

We now consider the case we the decision maker is considering not to wear seat belts, that is, . Say we have the following conditional probabilities:

Then, using (3.3), we may combine the probability of an event, (3.1), with the corresponding conditional probability distributions of some outcome given that event, (3), and so get the corresponding bivariate probability distribution, Table 3.

| : | 0.9500 | 0.0 | 0.0 |

| : | 0.0120 | 0.0370 | 0.0 |

| : | 0.0001 | 0.0003 | 0.0006 |

Marginalizing the event-outcome probabilities over the events , (3.5), we get the marginalized outcome probability distribution, Table 4.

| 0.9621 | 0.0373 | 0.0006 |

In its most abstract form, we have that each problem of choice consists of a set of potential decisions

Each decision we make may give rise to a set of possible events

These events are associated with the decisions by way of the conditional probabilities . Furthermore, each event allows for a set of potential outcomes

These outcomes are associated with the events by way of the conditional probabilities .

By way of the product rule, (3.3), we compute the bivariate probability distribution of an event and an outcome conditional on the decision taken:

| (3.8) |

The outcome probability distribution is then obtained by marginalizing, (3.5), over all the possible events

| (3.9) |

The outcome probability distributions (3.9), for , are the information carriers which represent our state of knowledge in regards to the consequences of our decisions.

At first sight the added event space in the abstract form given here may seem somewhat superfluous555As this event space hardly is used in this fact sheet.. But it was felt that further down the line, in decision theoretical problems more complex than the ones given in this fact sheet, this added space may help one in the construction of outcome probability distributions666If we want to collect all the possible outcomes in one probability distribution, under a given decision, then we may first gather the different events, which precede these outcomes, in a seperate probability distribution. We foresee that this factoring may greatly help in the construction of complex outcome probability distributions; cascading events, event trees, etc….

4. Translating Monetary Outcomes to Utilities

The Bernoulli utility function in the field of psycho-physics777Psycho-physics is the experimental field of psychology that studies sense perception. is called Weber-Fechner law. Seeing that we will use in this section the psycho-physical point of view of money increments as a stimulus, we will refer in what follows to the Bernoulli utility function as the Weber-Fechner law. But both names point to the same function888In the next section we will formally derive the Bernoulli utility function by way of a novel consistency argument. In Appendices B and C we, respectively, discuss the ubiquitousness of the Bernoulli utility function, which has been derived several times over by different arguments, and proceed to give its corollary, the negative Bernoulli utility function, which may be used to model the utility of debt..

The translation of monetary stimuli to utilities is analogous to the case where we are asked to translate loudness to a numerical value. According to Weber-Fechner law, postulated in the 19th century999Which is just Bernoulli’s utility function, postulated in the 18th century; see Appendix B. by the experimental psychologist Fechner, intuitive human sensations tend to be logarithmic functions of the difference in stimulus, [16]. So, we do not perceive stimuli in isolation, rather we perceive the relative change in stimuli, case in point being the decibel scale of sound.

Let and be two stimuli which are to be compared. Then the Weber-Fechner law tells us that the Relative Change (RC) is the difference of the logarithms of the stimuli:

| (4.1) |

where is some scaling factor and some base of the logarithm. From (4.1), we have that if stimuli and are indistinguishable, that is, of the same strength, then their RC is 0. If increases relative to , then . If decreases relative to , then .

The Weber-Fechner law allows for one degree of freedom. This can be seen as follows. Since

we can rewrite (4.1) as

| (4.2) |

where

| (4.3) |

Let be an increment, either positive or negative, in a monetary stimulus . Then we may define the utility of a monetary increment to be the perceived relative change in the initial wealth due to that increment , (4.2):

| (4.4) |

If , then (4.4) tells us that a loss of all one’s initial wealth would have a utility of minus infinity. This is clearly not realistic. So, in order to model such a loss, we must introduce the threshold of income which is still significant , [30], where . The threshold of income has the following interpretation.

Even for the homeless person there is some minimum amount of money that is still significant. This may be one dollar for a bag of potato chips, or three dollars for a packet of cigarettes. If the loss of money breaks through the limit of the minimum significant amount , the homeless person is left with an amount of money which, for all intents and purposes, is worthless. Using the concept of the threshold of income, we may modify (4.4) as

| (4.5) |

If we want to give a graphical representation of (4.5), then the scaling constant , also known as the Weber constant, must be set to some numerical value.

Say, we have a monthly expendable income of a thousand dollars, for groceries and the like, then introspection101010Introspection being the starting point of all psychological experimentation. would suggest that a loss or gain of an amount less than ten dollars would not move us that much.

So, constitutes a just noticeable difference, or, equivalently, 1 utile, for an initial wealth of , (4.5):

| (4.6) |

If we then solve for the unknown Weber constant , we find

| (4.7) |

Note that utiles represent the utility of the monetary outcomes, much like decibels represent the perceived intensity of sound111111Note that for the decibel scale the Weber constant has been determined to be ..

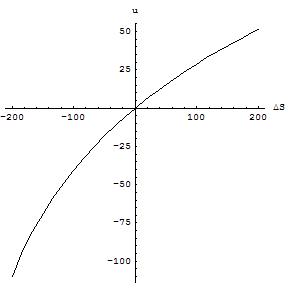

Suppose we have a student who has three hundred dollars per month to spend on groceries and the like and who stands to lose or to gain up to two hundred dollars. Then, by way of (4.5) and (4.7), we obtain the following mapping of monetary outcomes to utilities, Figure 1.

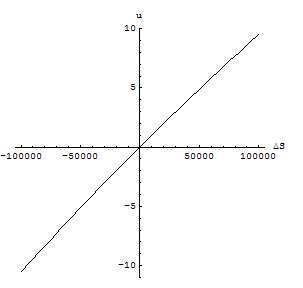

For the case of the rich man who has one million dollars to spend on groceries and the like and who stands stands to lose or to gain up to a hundred thousand dollars, we obtain the alternative mapping, Figure 2.

Loss aversion is the phenomenon that losses may loom larger than gains, [63]. Comparing Figures 1 and 2, we see that the Weber-Fechner law of experimental psychology, which is just Bernoulli’s utility function, captures both the loss aversion of the poor student, that is, asymmetry in gains and losses, as well as the linearity of the utility of relatively small gains and losses for the rich man.

5. A Consistency Proof of the Bernoulli Utility Function

We will derive the Bernoulli utility function, or, equivalently, the Weber-Fechner law, using the desiderata of invariance and consistency. In this we follow a venerable Bayesian tradition, [8, 30, 41].

5.1. Setting up the functional equations

Say, we have the positive quantities , , , of some stimulus or commodity of interest. These quantities, being numbers on the positive real and, consequently, transitive, admit an ordering. The quantities are assumed to be ordered as . We now want to find the function that quantifies the perceived decrease associated with going from, say, the quantity to the quantity .

The first functional equation is based on the observation that the unknown function should be invariant for a change in the unit of the quantity, that is,

| (5.1) |

where is some scaling factor.

For, example, if our quantities concern sums of money, then a perceived loss should be invariant for a change in the monetary unit. The perceived loss of going from ten dollars to one dollar should be the same perceived loss if we reformulate this scenario in dollar cents, that is, if we go from a thousand dollar cents to a hundred dollar cents.

Note that we also may interpret (5.1) in the following way. If person has an initial wealth of and person has a wealth of , where is some positive constant, then the perceived loss of person when going from to should be the same as the perceived loss of person when going from to . This alternative interpretation of (5.1) connects with Bernoulli’s original derivation of the utility function, in that it is a corollary of the reasoning that led him to his third and final consideration121212See Appendix B..

In order to give the second functional equation, we must introduce the function that enforces a change of context, [41]:

| (5.2) |

The functional equation (5.2) is a consistency equation that states that the perceived decrease in going from to , should be the same perceived decrease if we first go from to , and then from to .

5.2. Solving the functional equations

We first will look at the structure that the invariance equation (5.1) provides us in determining the form of . To do so, we take for (5.1) the derivative over :

| (5.5) |

which leaves with the partial differential equation

| (5.6) |

or, equivalently, if we let and ,

| (5.7) |

This partial differential equation has as its general solution:

| (5.8) |

were is some arbitrary function.

The consistency equation (5.2) may be solved as follows. First, by way of (5.2), we construct the associativity equation, [1, 41]:

| (5.9) |

The solution of this associativity equation, which is relatively well-known, is given as, [1, 41]:

| (5.10) |

where is some monotonic function.

If we substitute (5.8) into (5.10), we get:

| (5.11) |

Letting , we may rewrite (5.11) as:

| (5.12) |

Taking the derivative over (5.12), that is,

| (5.13) |

we obtain the ordinary differential equation:

| (5.14) |

or, equivalently,

| (5.15) |

If we let and , then we may rewrite (5.15) as

| (5.16) |

If we take the derivative of over (5.16), that is,

| (5.17) |

then we obtain the ordinary differential equation:

| (5.18) |

If we let , then we may rewrite (5.18) as

| (5.19) |

The general solution of is given as:

| (5.20) |

where and are arbitrary constants.

It then follows from (5.8) and (5.20) that the function , which adheres to the invariance desideratum (5.1) and the consistency desideratum (5.2), has as its general solution:

| (5.21) |

where and are arbitrary constants.

From the boundary conditions (5.3) and (5.4), it then follows, respectively, that and that , which leaves us with the specific solution:

| (5.22) |

which is the Bernoulli utility function, originally proposed by Bernoulli in 1738, [6].

It follows that the Bernoulli utility function is the only function that adheres to the desiderata of unit invariance and consistency, respectively, (5.1) and (5.2), and the boundary conditions that a zero change should lead to a zero perceived loss and that a perceived loss should be assigned a negative value, respectively, (5.3) and (5.4). Any other utility function will be in violation with these fundamental desiderata and boundary conditions.

The amazing thing here, at least to these authors’ mind, is that so much was gained for so little. As one need not mention monetary gains and losses or changes in offered sensory stimuli in order to derive the Bernoulli utility function, or, equivalently, the Weber-Fechner law.

We offer here the following observation, the functional equation (5.1) is, in its alternative interpretation, an invariance argument for two persons holding different amounts of initial wealth. Bernoulli, instead, uses variance arguments to arrive at his derivation. But both the variance and invariance arguments, as in the variance argument the wealth of person approaches the wealth of person 131313See Appendix B..

6. The Criterion Of Choice

In this section we will discuss the maximization of the sum of the lower and upper bounds, the third step in the Bayesian decision algorithm, as a criterion of choice. This criterion is highly non-intuitive, as it admits no interpretation. This is because it is a ‘corollary’, or, to be more precise, an algebraic reshuffling, of a criterion which is intuitive, but less succinct in its expression.

Let and be two decisions we have to choose from. Let , for , and , for , be the monetary outcomes associated with, respectively, decisions and .

In the Bayesian decision analysis, we first construct the two outcome distributions that correspond with these decisions:

| (6.1) |

where, if , the outcomes and may or not may be equal for .

We then proceed, by way of the Bernoulli utility function, or, equivalently, the Weber-Fechner law, to map utilities to the monetary outcomes and in (6.1). This leaves us with the utility probability distributions:

| (6.2) |

Our most primitive intuition regarding the utility probability distributions (6.2) is that the decision which corresponds with the utility probability distribution which lies more to the right will also be the decision that promises to be the most advantageous. So, when making a decision we compare the positions of the utility probability distribution on the utility axis. This utility axis goes from minus infinity to plus infinity. Hence, the more-to-the-right criterion of choice.

Now, the confidence bounds of (6.2), say:

| (6.3) |

may provide us with a numerical handle on the concept of more-to-the-right.

For example, if we have that both

| (6.4) |

Then we will have an unambiguous preference for decision over decision ; seeing that under both the still probable worst and best case we will be better if we opt for .

Likewise, if we have that either

| (6.5) |

or

| (6.6) |

Then, again, we will have an unambiguous preference for decision over decision . In the constellation (6.5), we stand, all other things being equal, to be better of under the still probable best case scenario; while in the constellation (6.6), we stand, all other things being equal, to be less worse of under the still probable worst case scenario.

However, things become more ambiguous when, say, under decision , we have to make a trade-off between either a gain in the upper bound and a loss in the lower bound

| (6.7) |

or a gain in the lower bound and a loss in the upper bound

| (6.8) |

We postulate here that a rational criterion of choice in the respective trade-off situations (6.7) and (6.8), would be to pick that decision whose gain in either the lower or upper bound exceeds the loss in the corresponding upper or lower bound.

So, if, say, under we stand to gain more in the still probable best case scenario than we stand to lose under the still probable worst case scenario, that is, (6.7):

| (6.9) |

then we will choose over . Likewise, if under we stand to gain more in the still probable worst case scenario than we stand to lose under the still probable best case scenario, that is, (6.8):

| (6.10) |

then again we will choose over .

Note that the gains and losses in this discussion pertain to gains and losses on the utility dimension, not on the monetary outcome dimension. On the utility dimension the phenomenon of loss aversion, that is, the phenomenon that monetary losses may weigh heavier than equal monetary qains, has already been accounted for. Stated differently, the utility scale is a linear loss-aversion corrected scale for the moral value of monies.

Now, if we look at the scenarios (6.7) and (6.8), and the corresponding postulated rational, because intuitive, criteria of choice (6.9) and (6.10), then we see that we will choose over whenever we have that

| (6.11) |

Moreover, this single criterion of choice is also consistent with the choosing of over in the scenarios (6.4), (6.5), and (6.6).

This, then, is the rationale behind the non-intuitive, because it admits no interpretation, criterion of choice that we should maximize the sum of the lower and upper bounds of the utility probability distributions, in order to come to the optimal decision141414Instead of the criterion (6.11), one may also use a lower bound maximization, that is, choose whenever A possible lower bound maximizer might be the regulator who is not that interested in a bank’s potential profit, but only has an eye for the potential catastrophic losses that, were they to materialize, could destabilize the entire financial system. Or,alternatively, one may use an upper bound maximization, that is, choose whenever where the upper bound maximizer is the banker that tries to maximize his yearly bonus..

Note that if the decision inequality (6.11) goes to an equality:

| (6.12) |

Then we have that we will be undecided when it comes to the decisions and .

Also note that for -sigma bounds (6.3) translates to

| (6.13) |

which, if substituted in (6.11), gives the inequality

| (6.14) |

which brings us right back to Bernoulli’s expected utility theory, as proposed in 1738, [6], in which it is stated that the expectation value of the utility probability distribution should be maximized.

Nonetheless, the criterion of choice, that the sum of the upper and lower bound should be maximized, as proposed here, will deviate from Bernoulli’s initial 1738 proposal when the -sigma intervals overshoots either its minimal or maximal value of the utility probability distribution.

Let and , respectively, be the minimal and maximal values of a given utility probability distribution. Then we may identify two additional symmetry breaking cases, relative to (6.14):

| (6.15) |

These two last symmetry breaking cases, where the -sigma intervals overshoot the minimal and maximal values of a given utility probability distribution are non-trivial, as they give rise to the specific -shape of the fair probabilities in certainty bets151515Certainty bets will be discussed in the section following the next one..

Another instance where we will deviate from Bernoulli’s proposal is when we put an explicit premium on either caution or opportunity. If we take as the lower and upper bounds, whose sum is to be maximized:

| (6.16) |

and

| (6.17) |

Then (6.16) and (6.17) sum to:

| (6.18) |

If in (6.18) we let , then we put a premium caution; if we set , then we put a premium on opportunity; and if we let , then we have an equal trade-off between caution and opportunity taking.

7. The Ellsberg Paradox

In this section we will demonstrate how to construct a non-trivial outcome distribution, by way of the product and sum rules, and how to map outcomes to their corresponding utilities by way of the product and sum rules.

Ellsberg found that the willingness to bet on an uncertain event depends not only on the degree of uncertainty but also on its source, [11]. He observed that people prefer to bet on an urn containing equal numbers of red and green balls, rather than on an urn that contains red and green balls in unknown proportions. Ellsberg called this observed phenomenon source dependence.

Tversky and Kahneman [63], state that source dependence constitutes one of the minimal challenges that must be met by any adequate descriptive theory of choice. As our theory of choice is Bayesian, we will proceed to give a Bayesian treatment of this phenomenon161616Note that we do not claim that decision makers will derive the Bayesian equations which will follow ad verbatim. Rather, we state that Bayesian inference is common sense amplified, having a much higher probability resolution than our human brains can ever hope to achieve. So, being common sense amplified, the results of the Bayesian analysis should be commensurate with our intuitions; rather than the analysis itself. See also Appendix D..

7.1. Constructing outcome probability distributions.

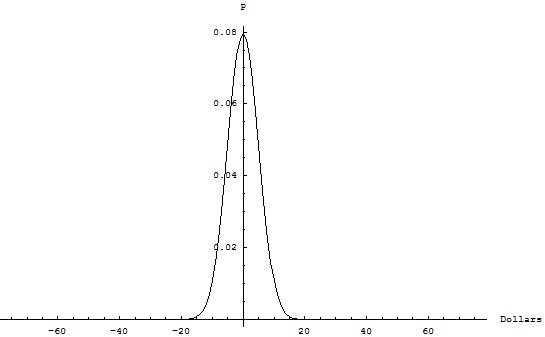

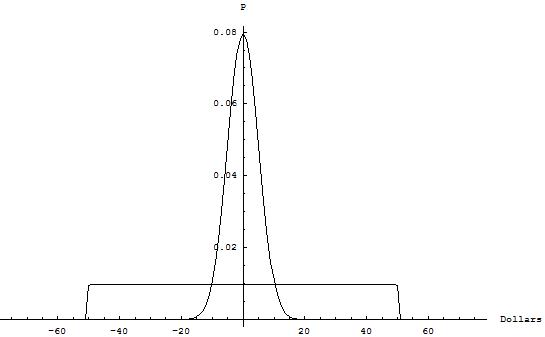

Say, we have a large urn consisting of 1000 balls of which 500 are red and 500 green. We tell our subject that of the balls are red and green, and that he is to draw a ball times. After each draw he will get a dollar if the ball is red and nothing if the ball is green, after which the ball is to be put back in the urn. The subject is also told that for the privilege to partake in this bet an entrance fee of 50 dollars is to be paid.

The probability of drawing red balls in the first bet may be modeled by way of a binomial distribution:

| (7.1) |

Now as the net return, say, is in dollars, having as its value number of red balls minus entrance fee, we have

| (7.2) |

where, as there are draws, . We then make a simple change of variable, using (7.2),

| (7.3) |

and substitute (7.3) into (7.1), so as to get the probability function of the net return

| (7.4) |

The probability distribution of the net return for bet , that is,

then can be plotted as, Figure 3:

This probability distribution has a mean and a standard deviation of, respectively,

| (7.5) |

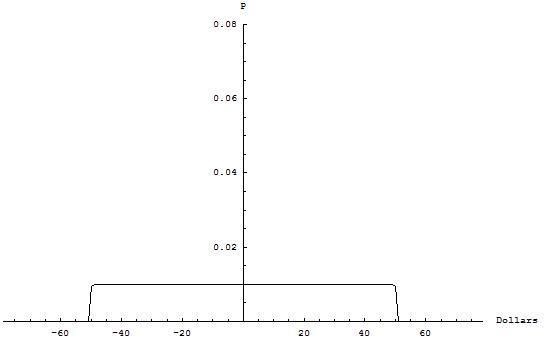

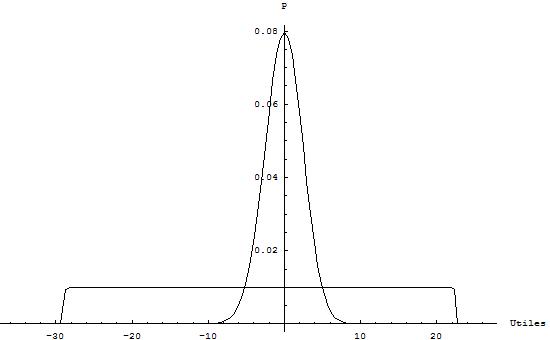

For the second bet, we tell our subject that the urn holds balls which are either red or green. Again, for every red ball drawn there will be a dollar payout. There will be draws and after each draw the ball is to be placed in the urn again. The entrance fee of the bet is 50 dollars. However, we are also told that the number of red balls is neither zero nor thousand171717We could let the range of the red balls be . But then the resulting outcome probability distribution would become unwieldy, because of this added structure., that is, , thus, precluding the certainty outcomes of and for, respectively, and .

As the subject does not know the actual number of red balls , the Bayesian thing to do is to weigh the probability of drawing red balls over all plausible values of , the total number red balls in the urn.

Based on the background information, we assign an uniform prior probability distribution to , the unknown number of red balls in the urn:

| (7.6) |

where . So, by way of the product and the generalized sum rules, (3.3) and (3.5), the probability of drawing red balls in the second bet translates to

| (7.7) |

Again making a change of variable from the number of red balls drawn to the net return , we substitute (7.1) and (7.6) into (7.7) and make a change of variable by way of (7.3). This results in the probability distribution of the net return :

| (7.8) |

The probability distribution of the net return for bet , that is,,

then can be plotted as, Figure 4:

This probability distribution has a mean and standard deviation of, respectively,

| (7.9) |

In Figure 5, we give both probability distributions, Figures 6.1 and 6.2, together.

7.2. Constructing utility probability distributions.

Let stand for the decision to choose the first Ellsberg bet and for the decision to choose the second Ellsberg bet. Then, by substituting, where appropriate, the values , , into (7.4) and (7.8), we may obtain the corresponding outcome probability distributions:

In order to map the outcomes in (7.2) to values on the utility dimension , we introduce the conditional probability distribution . Combining (7.2) with , by way of the product rule (3.3), and marginalizing over the possible outcomes , by way of the generalized sum rule (3.5), we may get the utility probability distribution of interest, that is,

| (7.11) |

Now, if we assign as our utility function the Bernoulli utility function, then the conditional utility probability distribution to be employed in the Ellsberg example is:

| (7.12) |

for , and where is our initial wealth and is the scaling constant of the Bernoulli utility function. This probability distribution takes us from the -dimension, which is the dimension of the monetary outcomes, to the -dimension, which is the dimension of the moral value of these monetary outcomes.

From (7.12), we see that every outcome admits only one utility value ; that is, (7.12) is of the Dirac delta form:

| (7.13) |

where is the Dirac delta function for which

| (7.14) |

Because of (7.14), we have that

| (7.15) |

Applying both (7.11) and the Dirac delta (7.13) to the outcome distributions (7.2), we obtain the utility probability distributions:

where in the probability distributions we only conditionalize on that which is not yet specified.

The th-order moments of the utility probability distributions (7.2) may be evaluated by way of the integrals:

| (7.17) |

7.3. Applying the criterion of choice.

If we assume a modest intial wealth, that is, monthly expendable income, of two-hundred dollars, that is, . Then the mean, standard deviation, and skewness of the utility probability distributions (7.2) are given as181818The first two cumulants of the utility probability distributions (7.2) may be computed by way of (7.17) and the identities, [23]:

| (7.18) |

and

| (7.19) |

The minimum and maximum values, respectively, and , of the utility probability distributions are given as, (4.5) and problem statement:

| (7.20) |

In the following, we will use 1-sigma intervals. Seeing that for these confidence intervals no overshoot occurs, we use for the sum of the lower and upper bounds of the utility probability distributions the first identity of (6.15). This gives for (7.18):

| (7.21) |

and for (7.19):

| (7.22) |

If we compare (7.21) and (7.22), then we find that decision is more advantageous than decision :

| (7.23) |

since

| (7.24) |

for any positive scaling constant .

As an aside the unknown scaling constant will always fall away in the decision theoretical inequalities. This is because the mean and standard deviations of the utility probability distributions are linear in . Stated differently, it may be checked that, for the stochastics and , and a positive constant , [45]:

| (7.25) |

So, unless we want to interpret our decisions in terms of net utility gain, as we do below, then we may, without any loss of generality, set the unknown scaling constant to one.

Now, if we are willing to commit ourselves to the scaling constant value of as the Weber constant for monetary stimuli, (4.7). Then we may, by way of (6.10), interpret (7.23) as follows.

Under decision , betting on an urn with an equal number of red and green balls, there is a gain of 13.34 utiles, in terms of loss mitigation, and a loss of 11.24 utiles, in terms of gain reduction, relative to decision , betting on an urn with an unknown proportion of red balls. This makes , with a net utility gain of 2.10 utiles, more attractive a choice than .

The setting of the scaling constant also allows us to plot the utility probability distributions under and , Figure 6.

We summarize, in a Bayesian decision theoretical analysis we first construct the outcome probability distributions on a monetary unit scale under the decisions and , Figure 5. We then construct, by way of the Bernoulli utility function, the corresponding utility probability distributions on an (un)scaled utile scale, Figure 6. We then compare, for a given decision, the gain/loss in the lower bound relative to the corresponding loss/gain in the upper bound; or, equivalently, in the algebraic sense of the word, we compare the sums of the upper and lower bounds under the decisions and .

The results of this Bayesian decision theoretical analysis is in correspondence with the Ellsberg finding that people prefer to bet on an urn containing equal numbers of red and green balls, rather than on an urn that contains red and green balls in unknown proportions, [11].

In closing, we may envisage decision problems in which we are uncertain regarding the actual utility of a given outcome . Such an occasion may arise when we do not know the initial wealth of the subject under investigation. In those cases we will want to assign probability distributions less dogmatic than the Dirac delta (7.13) to our utilities.

8. The Psychological Certainty Effect, Part I

Certainty bets admit the following structure. Let and , respectively, be the certainty and the uncertainty outcomes, where . The uncertainty outcome has a probability of of being realized. In the case that is not realized the outcome will be zero, and the probability corresponding with this outcome is . The certainty outcome is certain and, hence, has a probability of one.

So, the outcome probability distributions for certainty bets are

| (8.1) |

and

| (8.2) |

In what follows we will assume, initially, for simplicity’s sake, a linear utility for monetary outcomes. This assumption corresponds with an initial wealth that vastly exceeds any increment . This can be seen as follows. The logarithmic function admits the series expansion:

| (8.3) |

So, as tends to zero, we have that the Bernoulli utility function, or, equivalently, the Weber-Fechner law, (4.5) tends to, (8.3):

| (8.4) |

as can be seen in Figure 2.

Fairness is defined as the decision theoretical equality:

| (8.5) |

where and correspond with the choosing of, respectively, the uncertainty and certainty bets. Fairness finds its expression in the equality (8.5) because this equality guarantees that any loss/gain in the lower bound will be offset by a commensurate gain/loss in the upper bound191919See Section 6., for both and .

If, for a certainty bet having positive outcomes, we solve (8.5) for the fair probability , assuming a linear utility for money, and taking care to take into account any symmetry breaking conditions that may occur, (6.15), we find that the fair probability maps to the outcome intervals

| (8.6) |

which is intuitively fair for both the takers and the providers of decision , relative to the certainty offer of , and

| (8.7) |

which is intuitively fair for both the takers and providers of decision , relative to the certainty offer of .

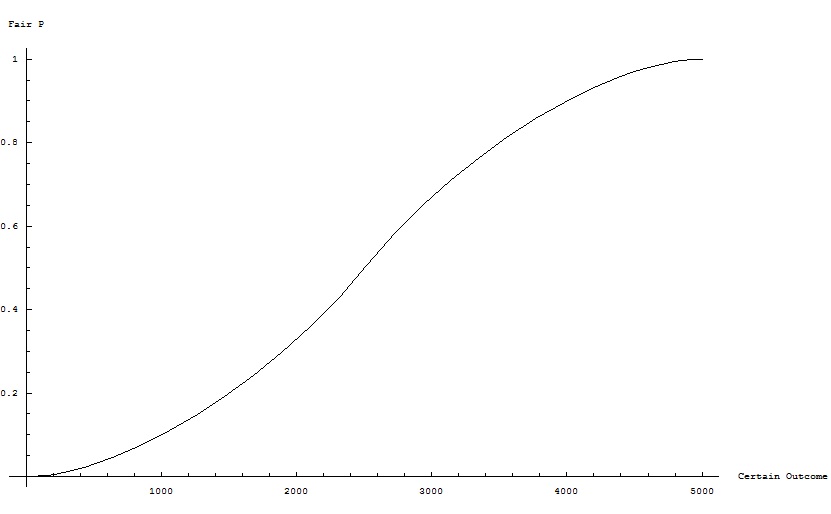

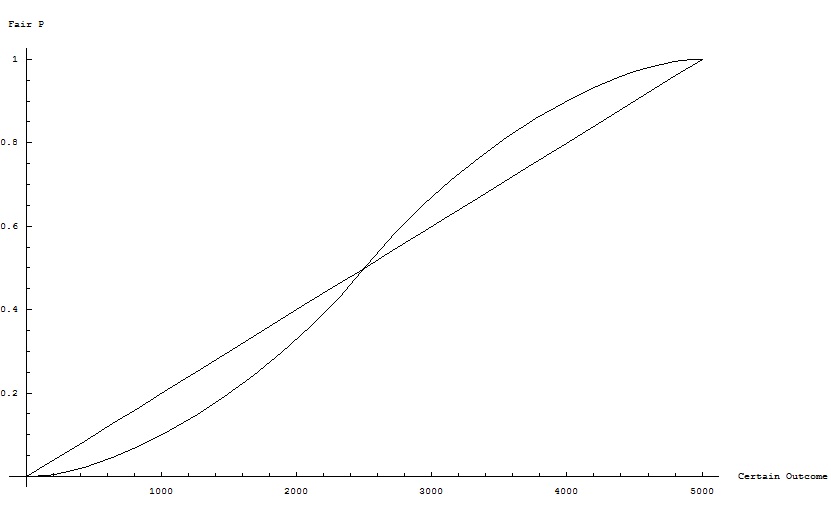

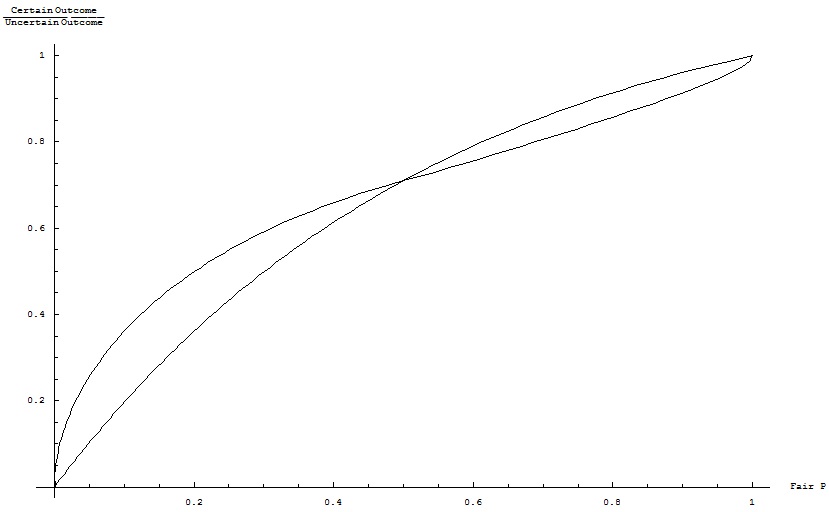

If for an uncertainty pay out of either or , we plot the solution of (8.5) for the fairness probability , assuming a linear utility for monetary outcomes, as a function of the certainty outcome , we obtain Figure 7:

If we again solve (8.5) for the fairness probability , as a function of the certainty outcome , assuming a linear utility for monetary outcomes, but now neglecting any symmetry breaking conditions, and add this expected utility theory solution to Figure 7, we obtain Figure 8:

If, for a certainty bet having negative outcomes, we solve (8.5) for the fair probability , assuming a linear utility for money, and taking care to take into account any symmetry breaking conditions that may occur, (6.15), we find that the fair probability maps to the outcome intervals

| (8.8) |

which is intuitively fair for both the takers and the providers of decision , relative to the certainty offer of , and

| (8.9) |

which is intuitively fair for both the takers and providers of decision , relative to the certainty offer of .

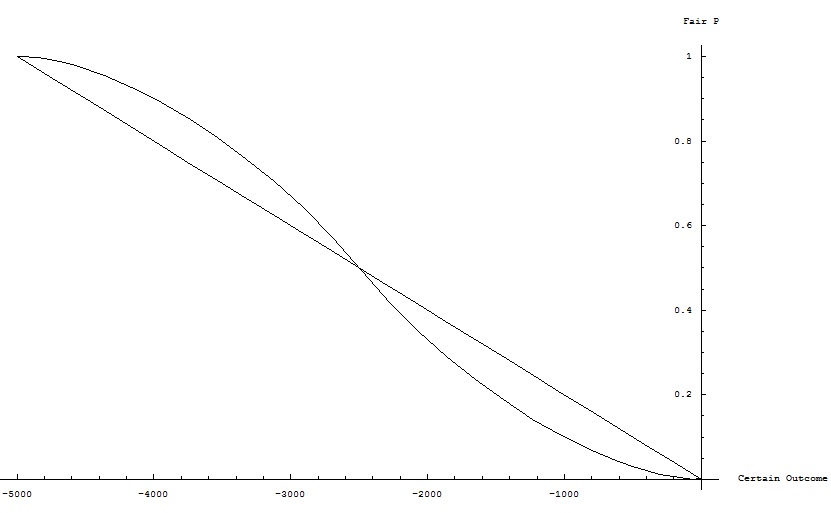

If for an uncertainty pay out of either or , we plot the solution of (8.5) for the fairness probability , assuming a linear utility for monetary outcomes, as a function of the negative certainty outcome , we obtain Figure 9:

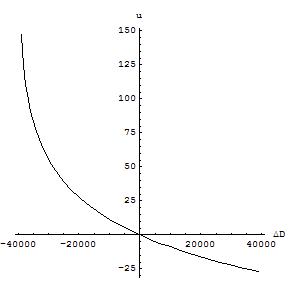

If we rescale the -axes of Figures 8 and 9 as the ratio , where , and reverse the axes, we obtain the alternative Figure 10:

Now, those readers who are familiar with the cumulative prospect theory may recognize in Figure 10, Kahneman and Tversky’s Figures 1, 2, and 3 of their [63].

But Kahneman and Tversky obtained their figures not from first principles, as is done here, but through experimentation, in which subjects where asked to decide on certainty bets of the type we discussed in the previous section. So, it would seem that Kahneman and Tversky, inadvertently, for they are outspoken anti-Bayesian202020See Appendix F., have provided the Bayesian decision theory with a very strong supporting contact.

Kahneman and Tversky see in the empirical observation of the typical -curve of Figure 10 another justification212121See Appendix G, for a discussion of the initial justification. for their probability weighing functions222222Note that Kahneman and Tversky’s and are not our and .,

| (8.10) |

and

| (8.11) |

which over weighs small probabilities and under weighs large probabilities. Moreover, Kahneman and Tversky offer up the implied under weighing of small probabilities, in order to explain the general popularity of lotteries and insurances.

We, on the other hand, see in the empirical observation of the typical -curve of Figure 10 a confirmation of the non-triviality of the proposed criterion of choice (6.15).

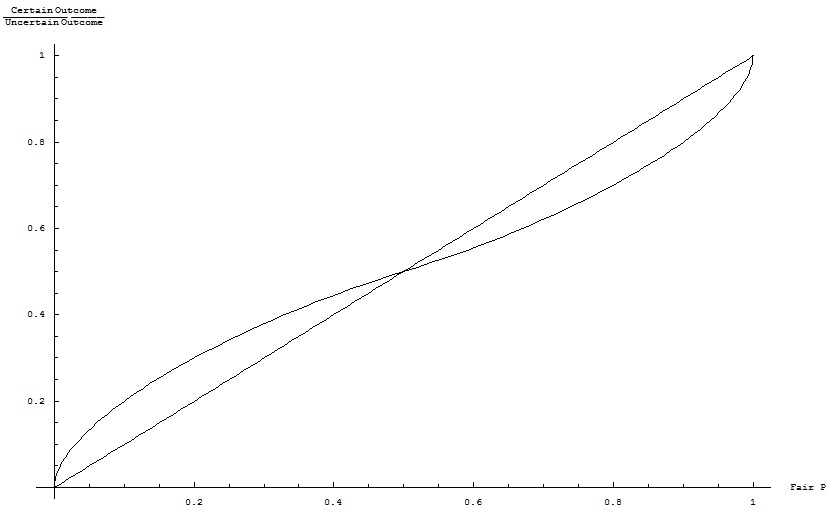

If we drop the assumption of a linear utility of monetary outcomes in the neighborhood of , and for initial wealths of and for certainty bets involving, respectively, positive and negative outcomes. Then we may assign, by way of the Bernoulli law, (4.5), utilities to the monetary outcomes. By doing so, we obtain the following fairness ratio outcomes for a given probability of the uncertain proposition, Figures 11 and 12:

and

Comparing Figures 11 and 10, we see that by taking into account the initial wealth , through the Bernoulli law, (4.5), the fair outcome ratios, as a function of the probability for the positive uncertainty outcome , are adjusted downward, relative to Figure 10. Furthermore, the fairness symmetry point has been adjusted downward in Figure 11.

If we have a small initial wealth, Figure 11, and we stand to gain more than we initially would have gained. Then, for given outcome ratios, we will be more inclined to accept the possibility of gaining nothing, relative to the case where we have a large initial wealth, Figure 10, as the pay-out, in terms of subjective consequences, is relatively higher under a small initial wealth.

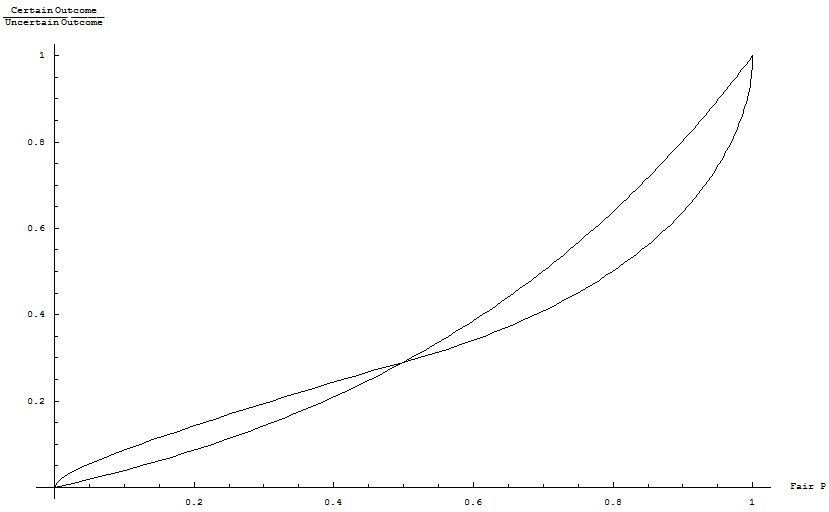

Comparing Figures 12 and 10, we see that by taking into account the initial wealth , through the Bernoulli law, (4.5), the fair outcome ratios, as a function of the probability for the negative uncertainty outcome , are adjusted upward, relative to Figure 10. Furthermore, the fairness symmetry point has been adjusted upward in Figure 12. These adjustments make nothing but sense.

If we have a small initial wealth, Figure 12, and we stand to lose more than we initially would have lost. Then, for given outcome ratios, we will be less inclined to accept the possibility of losing even more, relative to the case where we have a large initial wealth, Figure 10, as the penalty, in terms of subjective consequences, is relatively larger under a small initial wealth.

As our initial wealth tends to infinity, and our utility for money becomes linear, we will perceive both problems to be symmetric, as monetary losses are weighed the same as monetary gains, Figure 10.

9. The Psychological Certainty Effect, Part II

Risk seeking refers to a specific pattern in betting behavior. Uncertain larger gains are preferred over sure smaller gains and uncertain larger losses are preferred over sure smaller losses. The psychologists Kahneman and Tversky state that risk seeking constitutes one of the minimal challenges that must be met by any adequate descriptive theory of choice, [63].

The observation that large gains are preferred over sure much smaller gains is commensurate with the fact that we may prefer high-risk, high-yield investment opportunities over low-risk, low-yield ones. Likewise, the observation that uncertain larger losses are preferred over sure smaller, though still substantial, losses is in accordance with those instances in the past where traders incurred hundreds of millions in losses, in their attempts to make good on their previous losses232323As, for example, happened to Nicholas William Leeson, a trader for the Barrings Bank in the nineties. Though we believe that Leeson would have acted less recklessly had he been investing his own money, instead that of the deposit holders. That is, we expect that his Weber constant for his own money, say, , was markedly larger than his Weber constant for the deposit holders money, say, , where ..

If the signs of the outcomes in the risk seeking betting scenarios are reversed, then the preferences between the bets will also reverse. This is called the reflection effect, [34]. So, risk seeking in the positive domain is accompanied by risk aversion in the negative domain. Conversely, risk seeking in the negative domain is accompanied by risk aversion in the positive domain.

9.1. Risk Seeking I

We first give an example of risk seeking in the case of a small probability of winning a large prize, that is, risk seeking in the positive domain. This case of risk seeking represents our tendency to profit maximization and demonstrates that we will be willing to invest in a long shot if the pay-out is high enough.

The outcome probability distributions for the respective bets in our risk seeking example are

| (9.1) |

and

| (9.2) |

It is found that 72% of subjects prefer decision over , [34]. Even though both bets have the same expectation value of

We now interpret this finding in terms of the Bayesian decision theoretic framework.

Seeing that Kahneman and Tversky’s Figure 3 of their [63] is in close correspondence with Figure 10, we will assume here a linear utility for monetary outcomes242424This assumption is not that far-fetched, seeing that we have here imaginary increments in an imaginary inital wealth; stated differently, no money will be actually gained or lost, as a consequence of our decisions. See also Appendix H for a further discussion of the validity of hypothetical bets.. This assumption allows us to use either Figure 7 or Figure 8 to ‘read off’ the corresponding fair probability.

It is found that the fair probability for the certainty bets (9.1) and (9.2) is given as:

| (9.3) |

This fair probability may be checked to correspond with the fair interval, (8.6):

| (9.4) |

where the overshoot in the lower bound is re-set to zero252525See also (6.15)..

So, if the probability of the uncertain gain exceeds this fair probability, as it does, then, as our ‘expected’ utility moves away from the equilibrium situation to a greater expected gain, we will accept the uncertainty bet . As the gain in the utility upper bound under will dominate the gain in the utility lower bound under .

And indeed, it is found that 72% of subjects prefer decision over , [34], even though both bets have the same outcome expectation values. The phenomenon of utility upper bound dominance for gains constitutes risk seeking in the positive domain.

9.2. Risk Aversion I

The above analysis may also be performed for the case when there is a small probability of loosing a large sum of money. We then will see a reversal in the preference for bet over bet to a preference for bet over bet . Risk aversion in the negative domain represents our tendency to hedge against large and catastrophic losses.

The outcome probability distributions for the respective bets are262626Compare with (9.1) and (9.2).:

| (9.5) |

and

| (9.6) |

It is found that 83% of subjects preferred the bet over , [34].

We will again assume here a linear utility for monetary outcomes. This assumption allows us to use Figure 10 to ‘read off’ the corresponding fair probability.

It is found that the fair probability for the certainty bets (9.5) and (9.6) is given as:

| (9.7) |

This fair probability may be checked to correspond with the fair interval, (8.8):

| (9.8) |

where the overshoot in the upper bound is re-set to zero272727See also (6.15)..

So, if the probability of the uncertain loss exceeds this fair probability, as it does, then as our ‘expected’ utility moves away from the equilibrium situation to a greater expected loss, we will reject the uncertainty bet . As the gain in the utility lower bound under will dominate the gain in the utility upper bound under .

And indeed, it is found that 83% of subjects prefer decision over , [34], even though both bets have the same outcome expectation values. The phenomenon of utility lower bound dominance for losses constitutes risk aversion in the negative domain.

9.3. Risk Seeking II

We now give an example of risk seeking when people must choose between a sure loss and a substantial probability of a larger loss, that is, risk seeking in the negative domain. This case of risk seeking represents our tendency to try to evade large and catastrophic losses.

The outcome probability distributions for the respective bets in our risk seeking example are

| (9.9) |

and

| (9.10) |

It is found that 92% of subjects preferred the bet over , [34].

If we assume a linear utility for monetary outcomes, then we may use Figure 10 to ‘read off’ the corresponding fair probability. It is found that the fair probability for the certainty bets (9.9) and (9.10) is given as:

| (9.11) |

This fair probability may be checked to correspond with the fair interval, (8.9):

| (9.12) |

where the overshoot in the lower bound is re-set to minus four thousand282828See also (6.15)..

So, if the probability of the uncertain loss is less than the fair probability (9.11), as it is, then as our ‘expected’ utility moves away from the equilibrium situation to a lesser expected loss, we will accept the uncertainty bet . As the gain in the utility upper bound under will dominate the gain in the lower bound under .

And indeed, it is found that 92% of subjects prefer decision over , [34], even though has a slightly larger outcome expectation value than . The phenomenon of utility upper bound dominance for losses constitutes risk seeking in the negative domain.

9.4. Risk Aversion II

The previous analysis may also be performed for the opposite case of a sure gain and a substantial probability of a larger gain. We then will see a reversal in the preference for bet over bet to a preference for bet over bet . Risk aversion in the positive domain represents our tendency to secure our profits.

The outcome probability distributions for this problem of choice are292929Compare with (9.9) and (9.10).:

| (9.13) |

and

| (9.14) |

It is found that 80% of subjects preferred the bet over , [34].

If we assume a linear utility for monetary outcomes, then we may use either Figure 7 or Figure 8 to ‘read off’ the corresponding fair probability. It is found that the fair probability for the certainty bets (9.13) and (9.14) is given as:

| (9.15) |

This fair probability may be checked to correspond with the fair interval, (8.7):

| (9.16) |

where the overshoot in the upper bound is re-set to four thousand303030See also (6.15)..

So, if the probability of the uncertain loss is less than the fair probability (9.15), as it is, then as our ‘expected’ utility moves away from the equilibrium situation to a lesser expected gain, we will accept the certainty bet . As the gain in the utility lower bound under will dominate the gain in the upper bound under .

And indeed, it is found that 80% of subjects prefer decision over , [34], even though has a slightly larger outcome expectation value than . The phenomenon of utility lower bound dominance for gains constitutes risk aversion in the positive domain.

10. Discussion

In this fact sheet we have presented the case for the Bayesian decision theory. It may be read in Jaynes’ [30], that to the best of his knowledge, there are as of yet no formal principles at all for assigning numerical values to loss functions; not even when the criterion is purely economic, because the utility of money remains ill-defined. In the absence of these formal principles, Jaynes final verdict was that decision theory can not be fundamental. This situation may have changed.

The Bernoulli utility function, initially derived by Bernoulli, by way of common sense first principles313131See Appendix B., has now been derived by way of a consistency argument323232See Section 5.. This might explain why it is that Bernoulli’s utility function has proven to be so ubiquitous and successful the field of sensory perception research; simply because it is consistent.

The first two algorithmic steps of the Bayesian decision theory, respectively, the construction of outcome probability distributions by way of the Bayesian probability theory and the construction of utility probability distributions by way of the Bernoulli utility function, allow us no freedom. To construct our outcome and utility probability distributions otherwise, would be to invite inconsistency.

Our initial justification for the Bernoulli utility function had come from the observation that this function, in the guise of the Weber-Fechner and the Steven’s power law, had been demonstrated by psycho-physics to be an appropriate model for the way we humans perceive the increments in sensory stimuli, in terms of sensation strength. So, if monetary outcomes are considered to be a sensory stimuli, in the most abstract sense of the word, then it would follow the Bernoulli utility function would be the most appropriate model for the way we humans perceive the increments in monetary wealth.

As in the course of our research we came to trust the Bayesian decision algorithm to teach our intuition, in those instances where the intuitive ‘resolution’ is lacking to make clear and crisp choices333333Just like we have learned, having been Bayesians for the past ten years, to trust the Bayesian probability algorithm to teach our intuition, in those instances where the intuitive resolution is lacking to make clear and crisp plausibility assessments; that is, by analogy, Jaynes’ reasoning computer of Bayesian probability theory, [30], had become a decision making computer., the burden fell on us to provide a proof of the fundamentalness of the Bayesian decision theory.

The history of Bayesian probability theory has taught us that the usefulness of a theory, in terms of its practical and beautifully intuitive results, in the absence of a compelling axiomatic basis, provides no safeguard against attacks by those who choose to close their eyes to this usefulness343434Note that this historical fact explains why Bayesians have their axiomatic house in such good order. This process started with the work of Cox, [8], was expanded upon by Jaynes, [30], which was then further refined by the work of Knuth and Skilling, [41]. Moreover, the more general axiomatic framework of the latter has enabled them, amongst other things, [43], to bring some order to the field of quantum theory, by showing why this theory is forced to use a complex arithmetic, [22].. This is why we felt compelled to search for a consistency derivation of the Bernoulli utility function.

Especially so, since we had taken painstaking care to search out those ‘unyielding practical realities’, that would put our foundations to the test. And it had been found that all these practical realities fell nicely in line with the proposed foundations of the Bayesian decision theory, as may be witnessed in our treatment of the Ellsberg paradox and the Kahneman and Tversky data on the certainty effect353535The Allais paradox corresponds, more or less, with Risk Aversion II in Section9. But one may take, trivially, any of the proposed Allais paradoxes and solve them with the here proposed decision algorithm.

So, having presented a consistency proof for the Bernoulli utility function, the question now is: Is the Bayesian decision theory, just like the Bayesian probability and information theories, Bayesian in the strictest sense in the word, or, equivalently, an inescapable consequence of the desideratum of consistency? We will now try to answer this question.

There is one degree of freedom remaining in the Bayesian decision theory as a whole. This remaining degree of freedom is the criterion of choice which states that we should maximize the sum of the lower bound of the utility probability distribution363636See Section 6..

In any problem of choice we will endeavor to choose that decision which has a corresponding utility probability distribution that is lying most the right on the utility axis; that is, we will choose to maximize our utility probability distributions. In this there is little freedom. But we are free, in principle, to maximize the positions of our utility probability distributions any way we see fit. Nonetheless, we believe that it is always a good policy to take into account all the pertinent information we have.

For example, if we only maximizes the expected value of the utility probability distribution, then we will, by definition, neglect the information that the standard deviation of the utility probability distribution has to bear on our problem of choice, by way of the symmetry breaking in the case of an overshoot of one of the bounds. Likewise, we are free to only maximize one of the bounds of our utility probability distributions, while neglecting the other. But in doing so, we will neglect the possibility of either (catastrophic) losses in the lower bound or (astronomical) gains in the upper bound.

In the Bayesian probability theory we have an analogous situation of both constraint and freedom. The Bayesian probability theory states that the product and sum rules of probability theory are the only two consistent and, therefore, admissible operators to combine probabilities with. But it also states that in our assignment of our probabilities we are totally free to do as we see fit. There are no ‘wrong’ probability distributions, only better or worse informed ones. It’s all a matter of choice.

Acknowledgments: The research leading to these results has received partial funding from the European Commission’s Seventh Framework Program [FP7/2007-2013] under grant agreement no.265138.

References

- [1] Aczel, J.: Lectures on Functional Equations and Their Applications, Academic Press, New York, (1966).

- [2] Allais M.: L’Extension des Theories de l’Equilibre Economique General et du Rendement Social au Cas du Risque, Econometrica, 21, 269-290, (1953) .

- [3] Allais M.: Fondements d’une Theorie Positive des Choix Comportant un Risque et Critique des Postulates et Axiomes de l’Ecole Americaine, Colloque Internationalle du Centre National de la Recherche Scientifique, No. 36, (1952).

- [4] Allais M.: Le Comportement de l’Homme Rationel devant le Risque, Critique des Postulates et Axiomes de l’Ecole Americaine, Econometrica 21,503-546, (1953).

- [5] Allais M.: An Outline of My Main Contributions to Economic Science, Nobel Lecture, December 9, (1988).

- [6] Bernoulli D.: Exposition of a New Theory on the Measurement of Risk. Translated from Latin into English by Dr Louise Sommer from ‘Specimen Theoriae Novae de Mensura Sortis’, Commentarii Academiae Scientiarum Imperialis Petropolitanas, Tomus V, 175-192, (1738).

- [7] Bernstein W.: A Splendid Exchange; How Trade Shaped the World, Grove Atlantic Ltd., (2008).

- [8] Cox R.T.: Probability, Frequency and Reasonable Expectation, American Journal of Physics, 14, 1-13, (1946).

- [9] Cox R.T.: The Algebra of Probable Inference, John Hopkins University Press, Baltimore MD, (1961).

- [10] Edwards W.: The Theory of Decision Making, Psychological Bulletin, Vol 51., No. 4, (1954).

- [11] Ellsberg D.: Risk, Ambiguity, and the Savage Axioms, Quarterly Journal of Economics 75, 643-699, (1961).

- [12] Erp van H.R.N., Linger R.O., and Gelder van P.H.A.J.M.: Constructing Cartesian Splines. The Open Numerical Methods Journal, 3, 26-30, (2011). But we recommend to search for the unmutilated arXiv version of this article: arXiv:1409.5955 [math.NA], (2014).

- [13] Erp van H.R.N., Linger R.O., and Gelder van P.H.A.J.M.: Deriving Proper Uniform Priors for Regression Coefficients, Part II, arXiv:1308.1114 [stat.ME], (2013).

- [14] Erp van H.R.N.: Uncovering the Specific Product Rule for the Lattice of Questions, arXiv:1308.6303 [stat.ME], (2013).

- [15] Fancher R.E.: Pioneers of Psychology, W. W. Norton and Company, London, (1990).

- [16] Fechner G.J.: Elemente der Psychophysik, 2 vols.; Vol. 1 translated as Elements of Psychophysics, Boring, E.G. and Howes, D.H., eds. Holt, Rinehart and Winston, New York, (1966).

- [17] Finetti de B.: Theory of Probability, 2 vols., J. Wiley and Sons, Inc., New York, (1974).

- [18] Georgescu-Roegen N.: Utility, Expectations, Measurability, and Prediction, Paper read Econometric Soc., September (1953).

- [19] Go S.C.: Marine Insurance in the Netherlands 1600-1870: A Comparative Institutional Approach, Groningen, (2009).

- [20] Good, I.J.: Probability and the Weighing of Evidence, C. Griffin and Co., London, (1950).

- [21] Good, I.J.: The Contributions of Jeffreys to Bayesian Statistics, in Zellner, A. ed., Bayesian Analysis in Econometrics and Statistics, North-Holland Pub. Co., Amsterdam, (1980).

- [22] Goyal P., Knuth K. H., and Skilling J.: Origin of Complex Quantum Amplitudes and Feynman’s Rules, Phys Rev. A 81 (2010), 022109, arXiv:0907.090 [quant-ph].

- [23] Hall P.: The Bootstrap and Edgeworth Expansion, Springer-Verlag (1992).

- [24] Heath C. and Tversky A.: Preference and Belief: Ambiguity and Competence in Choice Under Uncertainty, Journal of Risk and Uncertainty 4, 5-28, (1991).

- [25] Hudson M.: The New Road to Serfdom; An Illustrated Guide to the Coming Real Estate Collapse, Harper’s Magazine, (May 2006).

- [26] Jaynes E.T.: Confidence Intervals vs Bayesian Intervals; Reply to Kempthorne’s Comments, W.L. Harper and C.A. Hooker, eds. Foundations of Probability Theory, Statistical Inference, and Statistical Theories of Science, Reidel Publishing Co., Dordrecht, Holland, (1976).

- [27] Jaynes E.T.: Where Do We Stand on Maximum Entropy?, in Levine R.D. and Tribus M., eds., The Maximum Entropy Formalism, M.I.T. Press, Cambridge MA, (1978).

- [28] Jaynes E.T.: Some Random Observations, Synthese 63 115-138, (1985).

- [29] Jaynes E.T.: A Backward Look into the Future, Jaynes’ retirement speech, on-line available.

- [30] Jaynes E.T.: Probability Theory; the Logic of Science. Cambridge University Press, (2003).

- [31] Jeffreys H.: Theory of Probability Theory, Clarendon Press, Oxford, (1939).

- [32] Kahneman D. and Tversky A.: Subjective Probability: a Judgment of Representativeness, Cognitive Psychology 3, 430-454, (1972).

- [33] Kahneman D. and Tversky A.: On the Psychology of Prediction, Psychological Review, Vol. 80, No. 4, (1973).

- [34] Kahneman D. and Tversky A.: Prospect Theory: an Analysis of Decision Under Risk, Econometrica, 47(2), 263-291, (1979).

- [35] Kahneman D: Maps of Bounded Rationality: A Perspective on Intuitive Judgement and Choice, Nobel Lecture, December 8, (2002).

- [36] Keynes J.M.: A Treatise on Probability, MacMillan, London, (1921); Reprinted by Harper and Row, New York (1962).

- [37] Knuth K.H.: Intelligent Machines in the Twenty-First Century: Foundations of Inference and Inquiry. Phil. Trans. R. Soc. Lond. A 361, 2859-2873, (2003).

- [38] Knuth K.H.: Lattice Duality: the Origin of Probability and Entropy. Neurocomputing 67;245-274, (2004).

- [39] Knuth K.H.: Information and Entropy, Power Point Presentation, on-line available, (2008).

- [40] Knuth K.H.: Measuring on Lattices, (2009).

- [41] Knuth K.H. and Skilling J.: Foundations of Inference, arXiv: 1008.4831v1 [math.PR], (2010).

- [42] Knuth K.H.: A Derivation of Special Relativity from Causal Sets, arXiv: 1005.4172v2 [math-ph], 29 Aug. (2010).

- [43] Knuth K.H.: Information-Based Physics: An Observer-Centric Foundation. Contemporary Physics, (Invited Submission). doi:10.1080/00107514.2013.853426. arXiv:1310.1667 [quant-ph]

- [44] Laplace P.S.: Essai Philosophique sur les Probabilites, Courcier Imprimeur, Paris, (1819).

- [45] Lindgren B.W.: Statistical Theory, Chapman & Hall, Inc., New York, (1993).

- [46] Linger R.O., Erp van H.R.N., and Gelder van P.H.A.J.M.: Constructing Explicit B-Spline Bases, arXiv:1409.3824, (2014).

- [47] McGlothlin W.H.: Stability of Choices among Uncertain Alternatives, American Journal of Psychology, 69, 604-615, (1956).

- [48] Mongin P.: Expected Utility Theory, Prepared for the Handbook of Economic Methodology (slightly longer version than the published one), Davis J., Hands W., and Maki U., eds., London, Edward Elgar, (1997).

- [49] Neumann von J. and Morgenstern O.: Theory of Games and Economic Behavior, Princeton, Princeton Univer. Press, (1944).

- [50] Phillips L.D. and von Winterfeldt D.: Reflections on the Contributions of Ward Edwards to Decision Analysis and Behavioral Research, Working Paper LSEOR 06.86, Operational Research Group, Department of Management London School of Economics and Political Science, (2006).

- [51] Polya G.: How to Solve It, Princeton University Press, (1945). Second paperbound edition by Doubleday Anchor Books, (1957).

- [52] Polya G.: Mathematics and Plausible Reasoning, 2 vols: Induction and Analogy in Mathematics, Patterns of Plausible Inference, Princeton Press, (1954).

- [53] MacKay D.J.C.: Information Theory, Inference, and Learning Algorithms, Cambridge University Press, Cambridge, (2003).

- [54] Masin S.C., Zudini V., and Antonelli M.: Early Alternative Derivations of Fechner’s Law, Journal of Behavioral Sciences, 45, 56-65, (2009).

- [55] Rosenkrantz R.D.: Inference, Method, and Decision: Towards a Bayesian Philosophy of Science, D. Reidel Publishing Co., Boston, (1977).

- [56] Skilling J.: Bayesics, Bayesian Inference and Maximum Entropy Methods in Science and Engineering- International Workshop, edited by K. Knuth, A.E. Abbas, R.D. Morris, and J.P. Castle, (2005).

- [57] Skilling J.: Nested Sampling for Bayesian Computations, Proc. Valencia, ISBA th World Meeting on Bayesian Statistics, (2006).

- [58] Skilling J.: The Canvas of Rationality, Bayesian Inference and Maximum Entropy Methods in Science and Engineering- International Workshop, edited by M. de Souza Lauretto, C.A. de Braganca Pereira, and J.M. Stern, (2008).

- [59] Slovic P., Finucane M.L., Peters E., and MacGregor D.G.: Risk as Analysis and Risk as Feelings: Some Thoughts About Affect, Reason, Risk and Rationality, Risk Analysis 24(2), (2004).

- [60] Stevens S.S.: To Honor Fechner and Repeal His Law, Science, New Series, Vol. 133, No. 3446, 80-86, (1961).

- [61] Tribus M.: Rational Descriptions, Decisions, and Designs, Pergamon Press, New York, (1969).

- [62] Tversky, A., and Kahneman, D.: Rational Choice and the Framing of Decisions. Journal of Business, 59, S251-S278, (1986).

- [63] Tversky A. and Kahneman D.: Advances in Prospect Theory: Cumulative Representation of Uncertainty, Journal of Risk and Uncertainty, 5: 297-323, (1992).

Appendix A Bayesian Probability Theory

The whole of Bayesian probability theory flows forth from two simple rules. The product rule,

| (A.1) |

and the sum rule

| (A.2) |

By way of the product and the sum rule, we may derive the generalized sum rule,

| (A.3) |

If we have that the propositions are exhaustive and mutually exclusive, that is, , we may derive, by way of (A.2), (A.3), and the fact that , the most primitive probability distribution:

| (A.4) |

This probability distribution then may be further generalized, by taken as it propositional elements the exhaustive and mutual exclusive conjunctions , to the bivariate probability distribution:

| (A.5) |

which allows us to ‘marginalize’ over the parameter, say, , which is of no direct interest:

| (A.6) |

where

| (A.7) |

We may let and , that is, the number of propositions and in (A.5), tend to infinity. By doing so, we go from discrete to continuous probability distributions. Furthermore, we may add propositions , , , etc…, and so get higher variate distributions.

Now, to a non-Bayesian it may seem to be somewhat surprising, that the whole of Bayesian probability theory flows forth from the product and rules. But the whole of Boolean logic373737We use the term ‘Boolean algebra’ in its meaning as referring to two-valued logic in which symbols like ‘A’ stand for propositions, [30]., on an operational level, is also captured by the AND- and NOT-operations. These operations correspond, respectively, with (A.1) and (A.2); as these operators combine, with the negation of a NAND-operation, in the OR-operation, which corresponds with (A.3).

Moreover, it may be shown that Boolean logic is just a special limit case of the more general Bayesian probability theory. The operators of Boolean logic combine in a like manner as the operators in Bayesian probability theory. But in Boolean logic propositions can have only the truth values true or false. Whereas in Bayesian probability theory propositions can have plausibility values in the interval , where and , respectively, correspond with false and true.

So Boolean logic is the language of deduction, whereas Bayesian probability theory is the language of both induction and deduction; the former being a limit case of the latter, in which we have absolute knowledge about the propositions in play.

Now, on the conceptual level Bayesian probability theory is very simple. However, on an implementation level, when doing an actual data-analysis, it may be quite challenging383838In close analogy, Boolean logic, which is a specific limit case of Bayesian probability theory, is simple on the conceptional level. However, on the implementation level it may be quite challenging, when, say, we use this Boolean logic to design logic circuits for computers.; which, as an aside, makes it fun to do Bayesian statistics. And we refer the interested reader to [56], for a first cursory overview on the considerations that come with a Bayesian data-analysis393939Though the absolute autority is [30]. But the reading of this 680-page tome would require a considerable time investment on the part of the reader. But then again, as Calculus is the royal highway to the exact sciences, so we have that Jaynes’ Probability Theory: The Logic of Science is the royal highway to Bayesian statistics..

Appendix B The Ubiquitous Bernoulli Utility Function

The utility of a given outcome is the perceived worth of that outcome. If we take the utilities that monetary outcomes hold for us to be an incentive for our decisions, then we may perceive money to be a stimulus.

For the rich man ten dollars is an insignificant amount of money. So, the prospect of gaining or losing ten dollars will fail to move the rich man, that is, an increment of ten dollars for him has an utility which tends to zero.

For the poor man ten dollars is two days worth of groceries and, thus, a significant amount of money. So, the prospect of gaining or losing ten dollars will most likely move the poor man to action. It follows that an increment of ten dollars for him has an utility significantly greater than zero.

We now will give the derivations of the Bernoulli, the Weber-Fechner, and Steven’s power laws. It will be seen all that these three laws are equivalent.

B.1. The Bernoulli utility function.

Consider persons and , with having a fortune of 100.000 full-ducats, and with a fortune of 100.000 semi-ducats, a semi-ducat being the half of a full-ducat. Let and be the moral value functions, defined on, respectively, the monetary full-ducat axis and the semi-ducat axis . Let and stand for the initial wealths of and , respectively; where and are points on the monetary axes and , respectively.

Bernoulli derived his law by way of three simple variance considerations for the moral functions and , [6, 54]:

-

(1)

For an arbitrary increment in wealth, the moral movement of this increment will be less for the rich man, than for the poor man; that is, if we make for the appropriate change of variable, from to , then we have that

From which it follows that effect of on a given decreases as the initial wealth increases.

-

(2)

It is proposed that the movement in a general moral value function , for a given positive increment , is proportional to the value of this increment; that is,

as this is the simplest function for which increases as a function of an increment in .

-

(3)

Furthermore, it is proposed that this movement in is inversely proportional to the value of the initial wealth ; that is,

where ‘’ is the proportionality sign.

Bernoulli arrived at his third consideration, using the following reasoning. The change in moral value of full-ducats for will be half the change in moral value of full-ducats for . Only if either sees his fortune increased to 200.000 semi-ducats, or, equivalently, 100.000 full-ducats, or if sees his fortune reduced to 50.000 full-ducats, or, equivalently, 100.000 semi-ducats, only then will have the same change in moral value as for full-ducats404040In these two limit cases the Bernoulli variance argument will tend to the invariance argument (5.1), which was used in Section 5.. So, if we make for the appropriate change of variable from to ,

| (B.1) |

where is the initial fortune of , translated from the semi-ducat -axis to the full-ducat -axis.

It follows from (B.1) that we have, in general, that the change in moral value is inversely proportional to the initial we hold, that is,

| (B.2) |

which is Bernoulli’s third consideration.

If we combine the second and the third consideration, we obtain the differential equation

| (B.3) |

which, if solved for the boundary condition that for a given person with an initial wealth of an increment of zero holds no utility, either negative or positive, gives

| (B.4) |

which may be rewritten as

| (B.5) |

B.2. The Weber-Fechner Law.

Let signify stimuli intensity and let signify sensation strength. Weber’s law states that the increment needed to elicit a judgment that is just noticeably different from is proportional to :

| (B.6) |

where is a positive constant dependent upon the specific type of sensory stimulus offered and is understood to be the stimulus increment corresponding with a just noticeable difference.

Fechner generalized the experimental Weber law by stating that all differences in sensational strength, and not only the ones that are just noticeable, are proportional to the relative change , that is,

| (B.7) |

where is a positive constant dependent upon the specific type of sensory stimulus offered and is now understood to be the stimulus increment corresponding with the increment in sensation strength .

Dividing both sides of (B.7) by gives

| (B.8) |

Fechner then makes the assumption that, just as a physically small quantity can be reduced without limit to the differential , so a small quantity of sensation can be reduced without limit to the differential . By way of this assumption, we may let (B.8) tend to the differential equation

| (B.9) |

The general solution of this differential equation is

| (B.10) |

where is some constant of integration.

Introducing an initial value condition for (B.9) that says that at stimulus value there is no sensation strength, that is, , leaves us with the Weber-Fechner law

| (B.11) |

or, equivalently,

| (B.12) |

The Weber-Fechner law, (B.12), is identical to the utility function which had been proposed a century earlier by Bernoulli, (B.5).

Fechner himself was aware of this equivalence. Nonetheless, he believed his derivation to be the more general. Fechner argued that Bernoulli’s derivation only applied to the special case of utility, whereas his law, though identical, applied to all sensations, as it invokes Weber’s law.

However, as pointed out in [54], Fechner failed to provide any compelling reason why the principles employed in Bernoulli’s derivation of the subjective value of objective monies should not be extendible to sensations in general. Nonetheless, we do believe that Fechner acted in good faith, in denying Bernoulli scientific primacy.

First of all, Fechner called the Weber-Fechner law, when he first published it, very modestly, the Weber law. Second of all, Fechner had a deep spiritual need for some kind of harmony between the physical and mental universes, and the Weber-Fechner law provided him with this harmony, for this law spoke of the basic oneness of the physical and mental universes, [15].

The Weber-Fechner law demonstrated that both universes adhered to seemingly mechanistic laws. It then followed that the freedom of the latter universe, in terms of free will and volition, implied, by way of analogy, a commensurate freedom of the former; thus, opening the way for the possibility of a besouled physical universe. Which had become Fechner’s only hope for spiritual salvation, [15].

We can imagine that Fechner might have felt that a law that assigned subjective values to objective monies was too arbitrary and sordid a foundation for the lofty purpose he wished it to serve. In contrast, the initial Weber law allowed Fechner to forgo of the money argument and derive a law, which though in form identical to Bernoulli’s, differed in that it applied to all human sensations.

B.3. Steven’s Power Law.

Steven’s power law is based on the observation, that it is the ratio , rather than the difference , that is proportional to , [60]. This observation leads to the equality

| (B.13) |

Letting the differences in and go to differentials, we may rewrite (B.13) as

| (B.14) |

This equation has its general solution

| (B.15) |

Taking the exponent of both sides of (B.15), we get the power law for stimulus perception

| (B.16) |

where .

Stevens found the power law to hold for several sensations; binaural and monaural loudness, brightness, lightness, smell, taste, temperature, vibration duration, repetition rate, finger span, pressure on palm, heaviness, force of hand grip, autophonic response, and electric shock, [60].

The power law is applied by letting subjects compare the sensation ratio of to for corresponding stimuli strengths and :

| (B.17) |

Let , where is some increment, then we may rewrite (B.17) as

| (B.18) |

For an increment of , the ratio of perception stimuli will be . Taking the log of the ratio (B.18) we may map the ratio of perceived stimuli to a corresponding utility scale where a zero increment corresponds with a zero utility:

| (B.19) |

But this is just the Weber-Fechner law, (B.13).

B.4. Summary.

The Weber-Fechner law gives us just noticeable differences on a log scale, (B.13). The power law gives us ratios of sensation strengths, (B.18). Taking the log of the ratio of sensation strengths, we may obtain the just noticeable differences again, (B.19). But the Weber-Fechner for just noticeable differences is just the Bernoulli utility function for utilities, (B.5).

We refer the reader to [54], for a discussion of Thurnstone’s derivation of the satisfaction law. This law, which takes as its input the increment in the number of items of commodity, is also of the form of Bernoulli’s utility function.

Appendix C The Negative Bernoulli utility function

In this appendix we present the negative Bernoulli utility function for debts, which is a corollary of the Bernoulli utility function for income. The negative Bernoulli utility function predicts that for the very poor, having a small initial wealth and large initial debts, a large loss of direct income will be more devastating, than an increase of, say, twice that loss in their long-term debt. This law also explains why, for these poor, having a small initial wealth and large initial debts, the temptation to take out loans, if offered the opportunity, will be quite great, [25].

Until now we have treated only the case were the maximal loss did not exceed the initial wealth . However, in real life we may lose more than we actually have, by way of debt. So, we now proceed to assign utilities to increments in debt.

According to the Weber-Fechner law we cannot lose more money than we initially had. Otherwise we may have that the ratio in the logarithm in the Weber-Fechner Law, (4.4),

| (C.1) |

may become negative, leading to a breakdown of the logarithm.

However, whenever we incur a debt we lose more money than we have. Furthermore, we can have a debt and an income, both at same time. So, we propose that there are two different monetary stimuli dimensions in play; the first dimension being an actual income dimension and the second dimension being a debt dimension.

We propose to model the debt utilities by way of the negative Weber-Fechner law:

| (C.2) |

where we let be the initial debt, the increment in debt, and the the Weber constant of a monetary debt.