Sudden Trust Collapse in Networked Societies

Abstract

Trust is a collective, self-fulfilling phenomenon that suggests analogies with phase transitions. We introduce a stylized model for the build-up and collapse of trust in networks, which generically displays a first order transition. The basic assumption of our model is that whereas trustworthiness begets trustworthiness, panic also begets panic, in the sense that a small decrease in trustworthiness may be amplified and ultimately lead to a sudden and catastrophic drop of collective trust. We show, using both numerical simulations and mean-field analytic arguments, that there are extended regions of the parameter space where two equilibrium states coexist: a well-connected network where global confidence is high, and a poorly connected network where global confidence is low. In these coexistence regions, spontaneous jumps from the well-connected state to the poorly connected state can occur, corresponding to a sudden collapse of trust that is not caused by any major external catastrophe. In large systems, spontaneous crises are replaced by history dependence: whether the system is found in one state or in the other essentially depends on initial conditions. Finally, we document a new phase, in which agents are well connected yet distrustful.

I Introduction

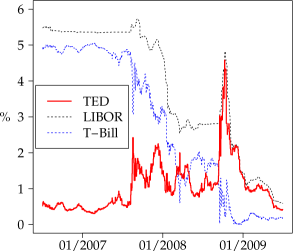

In the wake of the 2008 crisis, President Barack Obama declared: Our workers are no less productive than when this crisis began. Our minds are no less inventive, our goods and services no less needed than they were last week, or last month, or last year Obama (2009). So what had happened that made the world so different from a few months before? No war or physical catastrophe had occurred that would have destroyed tangible assets, infrastructures or knowledge. As implied by President Obama’s comment, the damage seems to have been, at least partially, self-inflicted by a sudden collapse of trust that led to a “freeze” of the interbank lending network (evidenced by soaring interbank rates, see Fig. 1) and, nearly immediately afterwards, to a collapse of confidence of all economic actors – investors, firms, households interrupted projects and reduced consumption, driving the economy to a grinding halt111Those who were in New York at the end of Sept. 2008 will remember the sight of completely empty retail stores and the stories of people emptying their bank accounts and going home with cash in plastic bags.. The bewildering aspect of such a crisis (as well as many previous ones) is the speed at which financial markets, or the economy as a whole, can shift from a relatively efficient state to a completely dysfunctional one. Whereas most “real” economic factors (technology, workforce, R&D) usually change relatively slowly, trust or subjective expectations seem to have no inertia, no anchor to their past values, and can swing from high to low in a matter of days, hours or even minutes.

Trust is critical in determining the prosperity of human societies and to secure a well-functioning economy and orderly financial markets. Moreover, trust is a collective asset that allows efficient coordination and cooperation, and tremendously accelerates business. It allows for the emergence of genuinely collective figments, such as money and other social conventions. Fiat money is a perfect example: a piece of paper can only be valuable if everybody believes that it will not be worthless tomorrow, and if everybody does, bank notes indeed become valuable.

The fact that trust is (as we view it) a collective, self-fulfilling phenomenon suggests analogies with phase transition phenomena, where collective properties emerge that cannot exist at the individual level, like magnetism, superfluidity, etc. Magnets, for example, arise because the spin of each atom acquires a favoured orientation, imposed by the favoured orientation of neighbouring atoms. This occurs when the interaction between spins becomes strong enough. Clearly, trust emergence is similar, and follows from positive feedback loops such as I trust you because he trusts you because I trust you. The most important aspect of the analogy with phase transition is the possible coexistence of very different equilibrium states, which leads to dis-equilibrium phenomena like history dependence or “hysteresis”, when the system is trapped in one equilibrium while another is more favourable, and discontinuities, when the system jumps from one state to the other. This is an interesting scenario as it opens a path to explain the sudden swings of trust that seem to underpin many economic, financial or political crises.

Several models for trust collapse have been studied along these lines in the past few years, see e.g. Anand et al. (2010, 2013); Cont and Wagalath (2014); Amini et al. (2013); Caballero and Simsek (2009); Heise and Kühn (2012); Battiston et al. (2012); Harmon et al. (2010); Sieczka et al. (2011); Peixoto and Bornholdt (2012); Bouchaud (2013); Gai and Kapadia (2010); Gai et al. (2011); Caccioli et al. (2012); Contreras and Fagiolo (2014); Bianconi and Marsili (2004) and references therein. The common crucial feature is the coexistence of two (or more) equilibrium states in a region of the parameter space, and therefore the possibility of a sudden jump between a favourable, high-confidence state to an unfavourable, low-confidence state. In these models, the jump is not induced by a major catastrophe (that would replace the favourable equilibrium by an unfavourable one) but rather by some anecdotal random fluctuation, which can induce a transition toward an already pre-existing low-confidence equilibrium.

Here, we introduce and study a highly stylized model for the build-up and collapse of collective trust in a dynamically evolving network, which generically displays a first order transition with possible coexistence of different equilibria. The nodes of the network can represent individuals, firms, banks, etc. Each node is assigned a real number that measures its (perceived) trustworthiness.

The presence of an undirected link between two nodes indicates an established relationship of some kind (business, loan, collaboration, etc.) resulting from some common rational benefit, but only possible if the perceived trustworthiness of the partner is high enough. Links are thus created or destroyed depending on the trustworthiness of the nodes and their dynamics; conversely, the trustworthiness of a node depends on that of its neighbours. The network and the trustworthiness therefore co-evolve and, depending on the precise specification of the model (see below), this leads to a rich dynamics with crises where the network disintegrates and the collective trust collapses. We solve our model within a mean-field approximation and find, as anticipated, that there is a region of parameters where different equilibria indeed coexist.

Our model and results are in several ways similar to those obtained by M. Marsili and associates in two very inspiring papers Marsili et al. (2004); Ehrhardt et al. (2006). They also study the coupled dynamics of links and nodes and find generic phase coexistence and hysteresis. One new aspect of our work is to consider that the speed of change of trustworthiness is itself a piece of information which agents strongly react to, in particular when it is negative – in a “panic feeds panic” spirit. Our mean-field analysis describes the phenomena induced by this effect and predicts phases which had not been considered before, such as a connected yet distrustful phase. In a sense, our model is a stylized version of Anand et al. (2010, 2013) that removes all the specifics of the interbank lending network, and a generalized version of Ehrhardt et al. (2006), where some ingredients specific to the dynamics of trustworthiness are introduced, leading to new effects. The possible coexistence of different states has also been noted in the context of epidemic propagation on networks which may be rewired so as to avoid infected nodes. In this case, infected network situations may indeed coexist with healthy networks Pastor-Satorras et al. (2014). This is similar to our model, where agents/firms/banks tend to cut their links with degraded nodes.

II The model

II.1 Trustworthiness of the nodes

The nodes in the network are agents which can represent individuals, companies, banks or other institutions. We make the strong assumption that the perceived trustworthiness of a node , which determines its propensity to link with other nodes, can be summarized by the value of a real number . That real number may depend on a variety of factors, which can be deemed either objective or subjective depending on their underlying nature. The balance sheet of a bank or the health of a business are examples of objective or “intrinsic” factors. Subjective factors come into play, for instance, when one needs to assess how trustworthy the counterparties or business partners of are. Clearly, if the debtors of are close to bankruptcy, they endanger the balance sheet of itself – this mechanism is at the core of many recent models of bankruptcy cascades such as Corsi et al. (2013); Sieczka et al. (2011); Contreras and Fagiolo (2014); Gai and Kapadia (2010); Caccioli et al. (2012); Lorenz et al. (2009); Battiston et al. (2012). But one can imagine different, less mechanical channels of propagation. A good example for our purpose is reputation risk. In fact, if node is caught up in a scandal while making business with , other partners of might become wary that is also involved and decide to end their business with , unless reacts immediately and severs its own link with .

Another important factor is the speed of variation of the trustworthiness itself. Imagine a highly respected bank or institution that rapidly loses many of its partners. This will be interpreted as worrying news by the remaining partners who, as a precautionary measure, will be tempted to cut their relation as well, even if the trustworthiness of is still high. This “bank run” or “panic” type of feedback loop can be amplified by the existence of a CDS (Credit Default Swap) market, which is supposed to price the default probability of firms and banks (and countries) and thus a proxy for . The very fact that the price of the CDS increases (and thus the perceived default probability) can trigger a crash-type dynamics. These avalanches of sell-offs when the perceived risk increases are often observed in financial markets as a consequence of a highly conservative management of “Black Swan” events – that, ironically, may result from these risk management policies!

Mathematically, we therefore write the trustworthiness of each node as the sum of three terms:

| (1) |

where are positive constants, is the degree of node , is the average trustworthiness of the nodes that are connected to (with if ), and is the variation of over the last time step.

The first term is the intrinsic trustworthiness of node , assumed here to be time-independent, IID random variables with mean and variance . More specifically we will choose to be uniformly distributed in the interval , corresponding to a positive mean and .

The second term describes how much of the trustworthiness of the peers of is bequeathed to . When is much smaller than a characteristic value , expanding for small arguments gives the following contribution:

| (2) |

which means that a fraction of the total trustworthiness of the business partners of is transferred to itself. The function imposes a saturation: for large average trustworthiness, node only receives a quantity that grows with the number of neighbours but not with the value of .

Finally, the third term accounts for the dependence of the current trustworthiness on its speed of change. In particular, increases with the difference between the current and previous trustworthiness values, while the minimum operator implies that only negative recent changes are considered. Therefore, the coefficient tunes the amplification of negative events and introduces an asymmetry between positive and negative trustworthiness variations. In a sense, it measures the susceptibility of a population to panic. For simplicity, we shall refer to as “panic factor”. The exact definition of can be found in appendix A or da Gama Batista (2015).

How real is our notion of perceived trustworthiness ? How could it be measured, for example? As mentioned above, one clear example are the CDSs of companies, which directly price the default probability as seen by market participants. Another possibility is to gauge the trustworthiness of individuals and firms through surveys, as discussed in Glaeser et al. (2000), echoing a concern expressed by Putnam Putnam (1995): since trust is so central to the theory of social capital, it would be desirable to have strong behavioural indicators of trends in social trust or misanthropy. I have discovered no such behavioural measures. Even if there is still a lot to be done in order to devise faithful, quantitative indicators of trustworthiness in general, it is highly plausible that the final answer will not be a single real variable as we assume, but a more complex, higher dimensional object. Nevertheless, we believe that the results obtained below, in particular those pertaining to the co-existence of different equilibria where collective trust is present or absent, will survive in more elaborate models of trustworthiness.

II.2 Network dynamics

We now specify how links in the network are created or broken depending on the trustworthiness of the nodes. Since the latter depends itself on the degree of the nodes and on its dynamics, we end up with a model of coupled trustworthiness/network dynamics which shows interesting properties, much as in Ehrhardt et al. (2006).

At each time step, we choose a pair of nodes at random, say , characterized by their trustworthiness and . The total number of nodes is constant in time and equal to . The global average (over all nodes) of , which characterizes the overall confidence level in the network, is denoted by .

II.2.1 Link creation

If there are no links between and , the probability that they decide to do business together is

| (3) |

where is the a priori propensity to enter into a business relation (the factor is discussed below) and is a modulating factor that depends on the trustworthiness and as follows:

| (4) |

where are two positive parameters. Therefore, a small value of implies a small probability of link formation. The term attempts to capture the idea that a trustful society eases the creation of new collaborations or business relations, i.e. that a rising tide lifts all boats. This is the essential virtue of trust that we discussed in the introduction: it acts as a catalyst to exchange and activity, an effect that we attempt to model through . It is quite clear that together with Eq. (1) above, this term can lead to a virtuous circle – more confidence leads to a more connected society which in turn leads to more confidence.

The second term decreases and is consequently detrimental to link creation. This attempts to account for “homophily”, i.e. the intuitive fact that two entities with very similar credit level are more likely to conduct business together than less comparable peers Ehrhardt et al. (2009); McPherson et al. (2001); Marsden (1988); Coleman (1958); Pin et al. (2008).

Instead of coupling to the overall confidence level , one could have imagined to use only the “local” trustworthiness . We have in fact investigated a generalized model in which

| (5) |

where the term captures deviations from the global average. We have found numerically that the new term does not change much the phenomenology of the model. This will be confirmed by the mean-field approximation below. We will thus set henceforth .

II.2.2 Link destruction

If there is a link between the chosen pair , it is destroyed with probability

| (6) |

which tends to unity when , i.e. when average confidence is very negative, or when homophily is strong (), both being detrimental to maintaining relationships. The specific choice for , and the factor in front of , can be understood by calculating the probability that the link between and exists in the stationary state. Assuming to be time independent, is the solution of

| (7) |

Therefore, when are both of order unity, the probability that a link exists is of order and the typical degree of a node is itself of order . This is the scaling needed in order to have a non trivial dynamics in the limit .

III Numerical results

We have numerically investigated this model in detail for various values of its six parameters: for trustworthiness and for link creation/destruction. Some initial conditions for the ’s and for the state of the network also need to be specified to run the dynamics. It turns out that as soon as is somewhat large (i.e. ), and for some regions in parameter space, the dynamics of the model becomes history dependent, in the sense that starting from an empty network (no links at all) or a full network (all links are present) leads to completely different stationary states – at least over time scales that can be reached in simulations and hence in reality as well (if our model captures anything of reality).

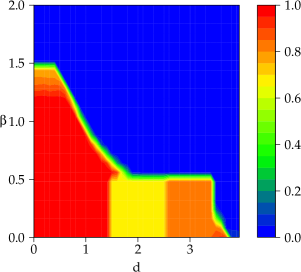

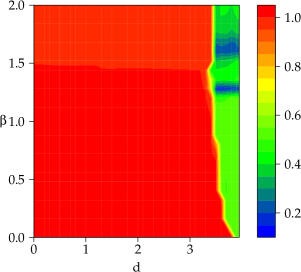

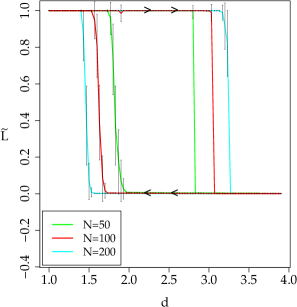

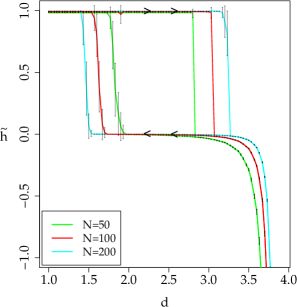

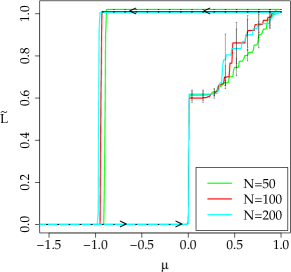

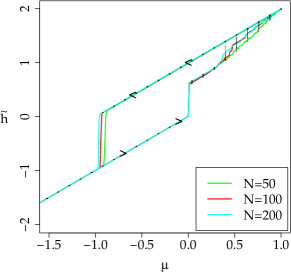

The most important parameters of our model appear to be the homophily parameter and the panic factor . This will be justified within our mean-field approximation below: as long as the confidence parameter is not vanishingly small and is large enough, the phenomenology of the model is mostly determined by and . We have therefore plotted the phase diagram of the model in the plane, and the results are shown in Fig. 2. We represent the average density of links of the network in a color code, starting from an empty network at (Fig. 2a) or from a densely connected network (Fig. 2b). Similar patterns appear when one represents the average confidence instead. One observes a clear boundary line separating two distinct phases: one in which the network is sparse in the stationary state, corresponding to a low average confidence , and another in which the network is dense, corresponding to a high average confidence . However, this boundary line shifts to significantly higher values when one starts from an already dense network. In other words, there is a large crescent region in phase space where the two outcomes (sparse or dense) are possible, and where the initial condition determines the fate of the network. Another way to illustrate this is to show the evolution of the density of links and of the average trustworthiness as a function of as one cycles along the line as in Fig. 3a and Fig. 3b.

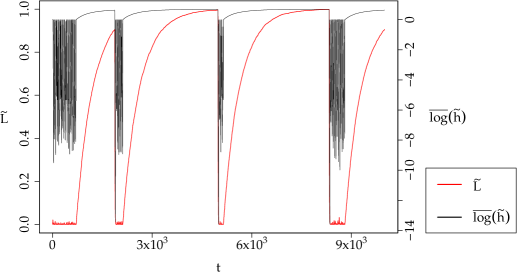

For small (but still large enough to be of practical interest, say ) the system can in fact alternate between these two states, leading to interesting endogenous crises – i.e. large swings between high confidence and low confidence that are not due to any particular event, but are the result of the noisy evolution of a system for which two very different equilibrium states coexist – see Fig. 5. As grows larger and larger, the probability to jump from one state to another becomes exponentially small, a typical behaviour of physical systems undergoing a first order phase transition (see below for a discussion of this point within a mean-field approximation). However, interesting dynamics will follow from the time-variation of parameters. A suggestive numerical experiment is to let the average value of the intrinsic trustworthiness slowly evolve with time, in order to model a progressive shift of the objective state of the economy. When the system is in the coexistence region, one observes a succession of booms and crises, corresponding to jumps between the two underlying equilibrium states – see Fig. 4a and Fig. 4b.

An analytic description of the dynamics of crisis and recovery can be performed, in particular when and close to the complete instability limit , which is derived in appendix B. The interested reader is referred to da Gama Batista (2015) for further details. We now turn to a mean-field approximation that accounts relatively well for our numerical observations.

IV A mean-field analysis

IV.1 Warm-up: Erdös-Rényi

Let us start by adopting a kinetic view of the standard Erdös-Rényi network with nodes. At each time step , a link is randomly chosen among the possible links. Following the same notation as before, the probability to create a link is , where, for the time being, and are constants. If the link is already present, the probability that it is destroyed is . We introduce the time-dependent degree distribution , i.e. the probability that a randomly chosen node has exactly outgoing links at time . The probability that this node changes from in the next time step is

| (8) |

while the probability to change from in the next time step is

| (9) |

Making time a continuous variable leads to the following Master equation for :

| (10) |

By inspection, one finds that is a stationary solution of Eq. (10), as it should be, provided

| (11) |

The average degree and the corresponding variance are then given by:

| (12) | |||||

| (13) |

The following sections extend the above calculation to the case where self-consistently depends on the trustworthiness of the nodes.

IV.2 Coupling with the average trustworthiness

We now consider the baseline case where , with and the average trustworthiness of the population. For the time being, we discard all homophily effects or feedback loops (i.e. ).

We first assume that the average intrinsic trustworthiness has a zero mean, . This is an interesting situation since it does not break the symmetry, i.e. collective trust or distrust are a priori equally probable outcomes. Averaging Eq. (1) over all nodes and using a mean field argument, i.e neglecting all fluctuations making all different, we find

| (14) |

This approximation is certainly justified in the dense limit , but breaks down for small , in particular when . In this latter case the network does not percolate and, in the absence of a giant component, no collective behaviour is possible. In this case, the only solution to Eq. (14) is .

Suppose for simplicity that is somewhat larger than unity (say or more), then and Eq. (14) has two possible solutions: 222For but not so large, the qualitative discussion below remains valid, up to prefactors of order unity.. Now we can plug these solutions in Eq. (12), which yields a second self-consistent equation:

| (15) |

IV.2.1 The positive trust self-consistent solutions

Let us focus first on the case where a positive average trustworthiness appears, corresponding to the minus sign in the exponential in Eq. (15). Assume first that . Then, the second term in the denominator is completely negligible and , which obeys the above hypothesis provided , which we will assume in the following. This corresponds to a self-sustained “euphoric state” where the network is full and confidence at its peak. This solution always exists unless is vanishingly small: in the absence of the detrimental effects studied below, a dense network should appear due to the positive feedback term that favours link formation when confidence rises.

A second, sparse but percolating (i.e. with a giant component) solution can also exist. To see that this is the case, assume now that . Then, Eq. (15) leads to , where

| (16) |

This self-consistent equation depends on the product :

-

•

When , there is no solution to this equation. Only the dense network solution described above exists.

-

•

When , on the other hand, there are 2 solutions and , one stable corresponding to a sparse, but trustful network, and a dynamically unstable one, which is nevertheless interesting since the associated value for is the critical value above which a sparse network is unstable and flows towards the fully connected solution above. Said differently, if the spontaneous fluctuations around the stable solution are not strong enough to reach with appreciable probability, the sparse network will appear dynamically stable. This is indeed the case when is small enough.

IV.2.2 A negative trust self-consistent solution

An important question at this point is whether this model also allows for the existence of sustained negative average trustworthiness values , i.e. a connected, but suspicious society. This would correspond to the positive sign in the exponential in Eq. (15). In this case, the solution for large is:

| (17) |

When , the solution of Eq. (17) is , therefore when the solution with negative is indeed self-consistent. Hence a self-sustained state of distrust in a sparse network (but with a giant component) is possible when a) is small enough (i.e. distrust is not too detrimental to link formation) and b) sufficiently large (i.e. agents meet often enough so that links are created even if the two parties are mutually suspicious). This corresponds, pictorially, to a “wary” society in which distrustful relationships are the norm.

On the other hand, if , we have

| (18) |

Equation (18) shows that as grows, decreases until the giant component disappears (when ) and the solution with is no longer viable. For large , this occurs for a certain value . We have checked numerically that this “wary society” phase indeed exists in our model and is not an artifact of the mean-field approximation.

IV.2.3 Summary

Summarizing, for and there are three viable solutions, one corresponding to very dense networks and positive self-sustained collective trust, and the two other to sparse networks (but still percolating, ), one with positive and one with negative self-sustained trust. These latter two solutions however disappear as increases, beyond for the former and for the latter.

The above analysis assumed that the average intrinsic trustworthiness is . When , the self consistent equation becomes:

| (19) |

Clearly, this equation now selects the dense, positive confidence solution as soon as is not vanishingly small. This is the situation we have considered in simulations.

IV.3 Coupling with speed of trust degradation

We now study the influence of the panic parameter on the trustworthiness in Eq. (1), i.e. the positive feedback effect that may trigger a link breaking avalanche when an increase of perceived risk takes place. We set the homophily term to zero for the time being and look into the general case in the next section.

As a warm-up exercise, let us compute the evolution of from Eq. (10). Multiplying by and summing over yields

| (20) |

At equilibrium, with , we trivially recover the result in Eq. (12):

For small deviations from equilibrium, is described by an Ornstein-Uhlenbeck process that can be fully characterized from the knowledge of the variance of .

Now, in our model with feedback we assume that all events contributing to lowering the degree of the nodes will lead to a decrease of trustworthiness. Restricted to events lowering the degree, this contribution can be written as

| (21) |

After time steps, which is the average time it takes to attempt to change the status of each link once, the total contribution to degree decrease is

| (22) |

Again in a mean-field spirit, the resulting expression for is

| (23) |

meaning that the stronger the activity that decreases connectivity, the smaller the value of and hence the larger the probability of breaking further links. There is also a second contribution to arising from the time fluctuations of itself, but it is much smaller in the equilibrium region we are focusing on.

Hence, we find a set of self-consistent equations valid when and :

| (24) | |||||

| (25) |

Let us study the possible solutions to Eq. (24) and Eq. (25). Suppose first that . In this case, we have from Eq. (25) that . The self-consistent Eq. (24) then leads to

which is indeed such that provided that . This solution corresponds to such dense a network that the downwards degree fluctuations cannot destabilize it, at least locally.

However, there might coexist a second solution, even for values of where it would not exist for . Suppose now that and , which we assume to be larger than to allow for non-zero collective trust to exist and be locally stable. The self-consistent equation now reads

| (26) |

It is clear that there is no solution to Eq. (26) when is small and . However, there is a critical value of , denoted by , above which Eq. (26) has two solutions: , which is stable at least for not too large, and , which is unstable. This is illustrated in Fig. 6. As increases further, becomes smaller and smaller and at one point becomes itself unstable, leading to limit cycle dynamics. This small solution however corresponds to a completely disconnected network.

The existence of a second, sparse solution for large enough corresponds well to our numerical observations: the network attempts to connect but trustworthiness is small and cannot grow because it is killed by spontaneous negative fluctuations.

The intermediate, unstable solution is also interesting as it again characterizes the critical transition path from the dense solution towards the sparse solution (and vice versa). For large , one finds , corresponding to a characteristic average degree . When is much smaller than , the dense solution has an exponentially small (in ) probability of spontaneous destabilisation. However, as increases towards , fluctuation induced crash events become more and more frequent, as shown in Fig. 5.

IV.4 Homophily

We finally turn to the influence of homophily, i.e. the term in the definition of in Eq. (4). Here we assume, as in Ehrhardt et al. (2006), that the network is at all times an Erdös-Rényi network with a time dependent density of links . We also assume, as above, that the network is well-formed, with somewhat larger than unity so that one can assume that for most nodes, the following approximation holds:

| (27) |

Again, two cases should be considered. One corresponds to dense networks, such that . In this case, fluctuations of node degree are at most of order . In fact, the homophily term leads to cliques of connected nodes with a relatively homogeneous degree, so we expect these fluctuations to be much smaller than . Therefore, one can estimate as

| (28) |

which shows that unless is very small, the highly connected phase is not destabilized by homophily.

In the case of sparse but percolating networks with , the dispersion of trustworthiness that prevents links from forming has two distinct origins. One is the intrinsic heterogeneity of the nodes, measured by the root mean square of the fields . The second is the degree heterogeneity which, for an Erdös-Rényi network with , is given by . Using , valid in the sparse phase, one finally ends up with the following schematic estimate of the homophily term:

| (29) |

where are numerical constants of order unity. This leads to a new self-consistent equation for the link activity in the sparse phase:

| (30) |

It is graphically clear that this equation behaves much in the same way as Eq. (26): for small and , no solution exists except for dense networks. But as increases, two non-trivial solutions, and appear, corresponding to a sparse solution that is not able to connect because of the strong repulsion between different nodes. This corresponds to the sparse phase observed in the phase diagram of the model for large , see Fig. 2.

V Conclusion

We have introduced, in the spirit of Marsili et al. (2004); Ehrhardt et al. (2006), a highly stylized model for the asymmetric build-up and collapse of collective trust in a network where the links and the trustworthiness of the nodes dynamically co-evolve. The basic assumption of our model is that whereas trustworthiness begets trustworthiness (meaning that a higher level of trustworthiness is more favourable to link formation), trustworthiness heterogeneities, both across nodes and in time, are detrimental to the network. In particular, panic also begets panic, in the sense that sudden drops of trust may lead to link breaking (or “sell-offs” in the context of financial markets) that further decreases trustworthiness. We have shown, using both numerical simulations and mean-field analytic arguments, that there are extended regions of parameter space where two equilibrium states coexist: one corresponds to a favourable, well connected network with a high level of confidence prevails, and the second is an unfavourable, poorly connected and low-confidence state. In these coexistence regions, sudden spontaneous jumps between the two states can occur. These transitions are not induced by any major catastrophe that would replace a favourable equilibrium by an unfavourable one, but rather by random fluctuations that trigger the switch between two already existing equilibria. When the system becomes large, however, these jumps become less and less frequent, unless an external parameter is changed – corresponding, for example, to a measure of the overall economic activity that sets the average trustworthiness level. For large systems, the phenomenon of spontaneous crises is replaced by the notion of strong history dependence: whether the system is found in one state or in the other essentially depends on initial conditions: ergodicity is dynamically broken.

Our stylized model only aims at this stage to provide a generic (but certainly oversimplified) conceptual framework to understand how financial markets, or the economy as a whole, can shift so rapidly from a relatively efficient state to chaos, when nothing “material” has changed at all, when our minds are no less inventive, our goods and services no less needed than they were last week, as noted by President Obama. Our model illustrates Keynes remark: a conventional valuation which is established as the outcome of the mass psychology of a large number of ignorant individuals is liable to change violently as the result of a sudden fluctuation of opinion due to factors which do not really make much difference Keynes (2006). A theoretical challenge is of course to take our framework seriously and think about how such a model could be calibrated against data, for example using interbank loan networks (see e.g. Battiston et al. (2012)), CDS data or survey results as in Glaeser et al. (2000). An obvious goal would be to obtain early warning signals for potential trust collapse and crises Squartini et al. (2013) that could, in some cases, look like precursor avalanches or “crackling noise” (see Sethna et al. (2001), and for a recent review on this theme, Bouchaud (2013)).

VI Acknowledgements

This work was partially financed by the EU “CRISIS” project (grant number: FP7-ICT-2011-7-288501-CRISIS) and Fundação para a Ciência e Tecnologia.

Appendix A Model specifications

The adjacency matrix at time is denoted by , while the trustworthiness of node at time is given by . is the total number of nodes in the network and is the degree of node at time , i.e., .

At each time step , the links between nodes are updated first. Then, the new trustworthiness of each node is computed.

Therefore, the evolution of the system at each time step happens in two distinct steps as follows.

-

1.

Create, destroy, or leave , links untouched:

(31) (32) where

(33)

-

2.

Update the trustworthiness values :

(34) where:

-

,

-

,

-

,

-

and .

-

Regarding the first step, it is worth remarking that , which implies that the number of new links per node remains finite even for large . is a measure of the propensity of nodes and to link or remain linked at time , which we assume to increase with and . On the other hand, we consider that is bigger if is smaller, i.e., that the likelihood of node linking with node increases with the similarity of their perceived trustworthiness in the community (homophily).

The term , with its intrinsic asymmetry, is a proxy for the panic sentiment mentioned in the main text. Besides, is the tentative cumulative trustworthiness of the peers of node at time , while is the actual value.

We can view the parameter as a mere refresh rate in the algorithm but we can also interpret it as a measure of overall communication intensity between nodes.

Appendix B Panic factor and stability

Let us consider the case where node ends up without any links at time . Moreover, let us assume that is small enough for us to neglect new links involving node as per Eq. (31). For the sake of simplicity, let us define . In this notation, node has at least one link at and becomes disconnected from the rest of the network at . Moreover, let us define and .

Then, we have from Eq. (34) that

| (35) |

In this scenario, Eq. (35) defines the fate of node , as it determines whether its trustworthiness enters an infinite downfall or not.

After some computations, Eq. (36) becomes

| (44) | |||||

| (45) |

where .

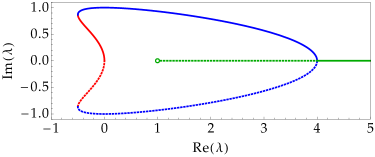

where and , with are the eigenvalues of in Eq. (36).

Therefore, under the assumptions we made in the beginning of this section, there are the following possibilities regarding the fate of node :

-

1.

If , and . Thus, the system is unstable and will tend to infinitely large negative values after node becomes disconnected from the network. Consequently, the probability of a new link involving node tends to exponentially quickly. Moreover, and .

-

2.

If , . Therefore and . Thus, the system is stable and will eventually return to values close to , which allow for the creation of links between node and the rest of the network.

-

3.

If , the evolution of would be unstable and unbounded for in the absence of the asymmetry in the panic factor defined in Eq. (34). However, this asymmetry condition gives rise to a situation in which eventually returns to a point close to , where link formation is possible. This happens when becomes non-negative, which implies .

The eigenvalues and corresponding to the cases above are represented in Fig. 7. The interested reader is referred to da Gama Batista (2015) for further details.

References

- Obama (2009) Barack Obama, “Address by Barack Obama,” Fifty-Sixth Inaugural Ceremonies (2009), Speech.

- Note (1) Those who were in New York at the end of Sept. 2008 will remember the sight of completely empty retail stores and the stories of people emptying their bank accounts and going home with cash in plastic bags.

- Anand et al. (2010) Kartik Anand, Prasanna Gai, and Matteo Marsili, “The rise and fall of trust networks,” Progress in Artificial Economics 645, 77–88 (2010).

- Anand et al. (2013) Kartik Anand, Alan Kirman, and Matteo Marsili, “Epidemics of rules, rational negligence and market crashes,” The European Journal of Finance 19, 438–447 (2013).

- Cont and Wagalath (2014) Rama Cont and Lakshithe Wagalath, “Fire sales forensics: Measuring endogenous risk,” Mathematical Finance (2014), 10.1111/mafi.12071.

- Amini et al. (2013) Hamed Amini, Rama Cont, and Andreea Minca, “Resilience to contagion in financial networks,” Mathematical Finance (2013), 10.1111/mafi.12051.

- Caballero and Simsek (2009) Ricardo Caballero and Alp Simsek, “Complexity and financial panics,” Working Paper Series (2009), 10.3386/w14997.

- Heise and Kühn (2012) Sebastian Heise and Reimer Kühn, “Derivatives and credit contagion in interconnected networks,” The European Physical Journal B 85, 115 (2012).

- Battiston et al. (2012) Stefano Battiston, Michelangelo Puliga, Rahul Kaushik, Paolo Tasca, and Guido Caldarelli, “Debtrank: too central to fail? financial networks, the fed and systemic risk.” Scientific reports 2, 541 (2012).

- Harmon et al. (2010) Dion Harmon, Blake Stacey, Yavni Bar-Yam, and Yaneer Bar-Yam, “Networks of economic market interdependence and systemic risk,” arXiv preprint , 9 (2010), arXiv:1011.3707 .

- Sieczka et al. (2011) Pawel Sieczka, Didier Sornette, and Janusz Holyst, “The Lehman Brothers effect and bankruptcy cascades,” The European Physical Journal B 82, 257–269 (2011).

- Peixoto and Bornholdt (2012) Tiago P. Peixoto and Stefan Bornholdt, “No need for conspiracy: Self-organized cartel formation in a modified trust game,” Physical Review Letters 108, 218702 (2012).

- Bouchaud (2013) Jean-Philippe Bouchaud, “Crises and collective socio-economic phenomena: Simple models and challenges,” Journal of Statistical Physics 151, 567–606 (2013).

- Gai and Kapadia (2010) Prasanna Gai and Sujit Kapadia, “Contagion in financial networks,” Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences 466, 2401–2423 (2010).

- Gai et al. (2011) Prasanna Gai, Andrew Haldane, and Sujit Kapadia, “Complexity, concentration and contagion,” Journal of Monetary Economics 58, 453–470 (2011).

- Caccioli et al. (2012) Fabio Caccioli, Munik Shrestha, Cristopher Moore, and J. Doyne Farmer, “Stability analysis of financial contagion due to overlapping portfolios,” Journal of Banking & Finance 46, 25 (2012), arXiv:1210.5987 .

- Contreras and Fagiolo (2014) Martha Contreras and Giorgio Fagiolo, “Propagation of economic shocks in input-output networks: A cross-country analysis,” Phys. Rev. E 90, 062812 (2014).

- Bianconi and Marsili (2004) Ginestra Bianconi and Matteo Marsili, “Clogging and self-organized criticality in complex networks,” Physical Review E 70, 35105 (2004).

- Marsili et al. (2004) Matteo Marsili, Fernando Vega-Redondo, and Frantisek Slanina, “The rise and fall of a networked society: a formal model.” Proceedings of the National Academy of Sciences of the United States of America 101, 1439–1442 (2004).

- Ehrhardt et al. (2006) George Ehrhardt, Matteo Marsili, and Fernando Vega-Redondo, “Phenomenological models of socioeconomic network dynamics,” Physical Review E 74, 036106 (2006).

- Pastor-Satorras et al. (2014) Romualdo Pastor-Satorras, Claudio Castellano, Piet Van Mieghem, and Alessandro Vespignani, “Epidemic processes in complex networks,” , 61 (2014), arXiv:1408.2701 .

- Corsi et al. (2013) Fulvio Corsi, Stefano Marmi, and Fabrizio Lillo, “When micro prudence increases macro risk: The destabilizing effects of financial innovation, leverage, and diversification,” SSRN Electronic Journal (2013), 10.2139/ssrn.2278298.

- Lorenz et al. (2009) Jan Lorenz, Stefano Battiston, and Frank Schweitzer, “Systemic risk in a unifying framework for cascading processes on networks,” The European Physical Journal B 71, 441–460 (2009).

- da Gama Batista (2015) Joao da Gama Batista, Dynamics of Trust in Networks and Systemic Risk, Ph.D. thesis, École Centrale Paris (2015).

- Glaeser et al. (2000) Edward L. Glaeser, David I. Laibson, Jose A. Scheinkman, and Christine L. Soutter, “Measuring trust,” Quarterly Journal of Economics 115, 811–846 (2000).

- Putnam (1995) Robert Putnam, The case of missing social capital, Tech. Rep. (Harvard University working paper, 1995).

- Ehrhardt et al. (2009) George Ehrhardt, Matteo Marsili, and Fernando Vega-Redondo, “Homophily, conformity, and noise in the (co-)evolution of complex social networks,” Complexity and Spatial Networks, Advances in Spatial Science, 105–115 (2009).

- McPherson et al. (2001) Miller McPherson, Lynn Smith-Lovin, and James M Cook, “Birds of a feather: Homophily in social networks,” Annual Review of Sociology 27, 415–444 (2001).

- Marsden (1988) Peter Marsden, “Homogeneity in confiding relations,” Social Networks 10, 57–76 (1988).

- Coleman (1958) James Coleman, “Relational analysis: the study of social organizations with survey methods,” Human Organization (1958).

- Pin et al. (2008) Paolo Pin, Silvio Franz, and Matteo Marsili, “Opportunity and choice in social networks,” Fondazione Eni Enrico Mattei Working Papers (2008).

- Note (2) For but not so large, the qualitative discussion below remains valid, up to prefactors of order unity.

- Keynes (2006) John Maynard Keynes, General Theory Of Employment , Interest And Money (Atlantic Publishers & Dist, 2006) p. 400.

- Squartini et al. (2013) Tiziano Squartini, Iman van Lelyveld, and Diego Garlaschelli, “Early-warning signals of topological collapse in interbank networks,” Scientific reports 3 (2013).

- Sethna et al. (2001) James Sethna, Karin Dahmen, and Cristopher Myers, “Crackling noise.” Nature 410, 242–50 (2001).