Parametric Transformed Fay-Herriot Model for Small Area Estimation

Shonosuke Sugasawa and Tatsuya Kubokawa

University of TokyoGraduate School of Economics, University of Tokyo, E-Mail: shonosuke622@gmail.comFaculty of Economics, University of Tokyo, E-Mail: tatsuya@e.u-tokyo.ac.jp

Abstract

In this paper, we consider parametric transformed Fay-Herriot models, and clarify conditions on transformations under which the estimator of the transformation is consistent.

It is shown that the dual power transformation satisfies the conditions.

Based on asymptotic properties for estimators of parameters, we derive a second-order approximation of the prediction error of the empirical best linear unbiased predictors (EBLUP) and obtain a second-order unbiased estimator of the prediction error.

Finally, performances of the proposed procedures are investigated through simulation and empirical studies.

Key words and phrases:

Asymptotically unbiased estimator, Box-Cox transformation, dual power transformation, Fay-Herriot model, linear mixed model, mean squared error, parametric bootstrap, small area estimation.

1 Introduction

The linear mixed models (LMM) with both random and fixed effects have been extensively and actively studied from both theoretical and applied aspects in the literature.

As specific normal linear mixed models, the Fay-Herriot model (Fay and Herriot, 1979) and the nested error regression models (Battese, Harter and Fuller, 1988) have been used in small-area estimation (SAE), where direct estimates such as sample means for small areas have unacceptable estimation errors because sample sizes of small areas are small.

Then the model-based shrinkage methods such as the empirical best linear unbiased predictor (EBLUP) have been utilized for providing reliable estimates for small-areas with higher precisions by borrowing data in the surrounding areas.

For a good survey on SAE, see Ghosh and Rao (1994), Rao (2003) and Pfeffermann (2013).

Also, see Hall and Maiti (2006a,b), Chamber, et al.(2014), Chaudhuri and Ghosh (2011) and Opsomer, et al.(2008) for recent articles on parametric and nonparametric approaches to SAE.

This paper is concerned with flexible modeling for analyzing positive data in SAE.

A standard transformation of positive is the logarithmic transformation , and Slud and Maiti (2006) used this method in the Fay-Herriot model.

This approach may be reasonable when the distribution of positive observations is positively skewed.

However, the log-transformation is not always appropriate.

An alternative conventional method is the Box-Cox power transformation (Box and Cox, 1964) given by

However, it should be noted that is truncated as for and for .

Thus, the Box-Cox transformation is not necessarily compatible with the normality assumption.

Another drawback of the Box-Cox transformation is that the maximum likelihood (ML) estimator of the transformation parameter is not consistent.

This negative property discourages us from using the Box-Cox transformation in SAE, because EBLUP which plugs in the ML estimator of does not converge to the best predictor or the Bayes estimator.

In Section 2, we consider the parametric transformations and the corresponding transformed Fay-Herriot models which apply the transformed observations to the standard Fay-Herriot model.

In Section 3, we derive sufficient conditions which guarantee consistency of estimators for the three unknown parameters of the transformation parameter, regression coefficients and variance of a random effect.

It is shown that the conditions for consistency are satisfied by the dual power transformation described in Section 2, while the Box-Cox transformation does not satisfy the conditions.

The EBLUP which plugs in the consistent estimators is suggested.

The EEBLUP is a reasonable procedure, since it converges to the BLUP or the Bayes estimator.

Measuring uncertainty of the EBLUP is important in the context of SAE, and two approaches to this issue are known: One is to evaluate the EBLUP in terms of the mean squared error (MSE) (see Das et al., 2004, Datta et al., 2005 and Prasad and Rao, 1990), and the other is to construct the confidence interval based on the EBLUP (see Chatterjee et al., 2008, Diao et al., 2014 and Yoshimori and Lahiri, 2014b).

In Section 4, we derive a second-order approximation of the MSE of the EBLUP.

A second-order unbiased estimator of the MSE is also provided via the parametric bootstrap method.

In Section 5, we investigate finite-sample performances of the suggested procedures by simulation.

The suggested procedures are also examined through analysis of the data in the Survey of Family Income and Expenditure (SFIE) in Japan.

All the technical proofs are given in Appendix.

2 Parametric Transformed Fay-Herriot Models

Let be a monotone transformation from to for positive , where and denote the sets of real numbers and positive real numbers, respectively.

It is noted that the transformation involves unknown parameter .

It is assumed that positive data are available, where is an area-level data like a sample mean for the -th small area.

For , assume that the transformed observation has a linear mixed model suggested by Fay and Herriot (1979), given by

(1)

where is a -dimensional known vector, is a -dimensional unknown vector of regression coefficients, is a random effect associated with the area and is an error term.

It is assumed that , , , are mutually independently distributed as and , where is an unknown common variance and are known variances of the error terms.

When we use the Fay-Herriot model for analyzing real data, we need to estimate before applying the model.

Fay and Herriot (1979) employed generalized variance function methods that use some external information in the survey.

For more explanation, see Hawala and Lahiri (2010).

In our analysis given in Section 5.3, we estimate using data in the past ten years, where we need to incorporate the estimation of the transformation parameter in (1).

The method for estimating in (1) is given in Section 5.3.

Thus, it should be noted that all the theory described in the paper are correct under the conditional model given the value .

In this paper, we want to consider a class of the transformations so that the ML estimator of is consistent.

To this end, we begin by describing the conditions on .

For notational convenience, let for be the partial derivative of .

Assumption 1.

The following are assumed for the transformation :

(A.1)

is an monotone function of () and its range is .

(A.2)

The partial derivatives and

exist and they are continuous.

(A.3)

Transformation function satisfies the integrability conditions given by

where is normally distributed.

Assumption (A.1) means that the transformation is a one-to-one and onto function from to .

Clearly, (A.1) is not satisfied by the Box-Cox transformation, but by .

Assumptions (A.2) and (A.3) will be used to show consistency of estimators of and to evaluate asymptotically MSE of the EBLUP.

A useful transformation satisfying Assumption 1 is the dual power transformation suggested by Yang (2006), given by

(2)

This transformation will be used in simulation and empirical studies in Section 5.

It is noted that for , the inverse transformation is expressed as

for , and for .

It can be verified that satisfies Assumption 1, where the proof will be given in Appendix.

Proposition 1.

The dual power transformation (2) satisfies Assumption 1.

3 Consistent Estimators of Parameters

In this section, we derive consistent estimators of the parameters , and in model (1).

We first provide estimators and of and , respectively, when is fixed.

We next derive an estimator by solving an equation for estimating , and then we get estimators and by plugging in the estimator .

3.1 Estimation of and A given

We begin by estimating and when is given.

In this case, the conventional procedures given in the literature for the Fay-Herriot model can be inherited to the transformed model.

Thus, for given and , the maximum likelihood (ML) or generalized least square (GLS) estimator of is given by

(3)

Concerning estimation of given , we consider a class of estimators satisfying the following assumption:

Assumption 2.

The following are assumed for the estimator of :

(A.4)

,

(A.5)

,

(A.6)

.

Assumption (A.4) implies that the estimator is consistent.

Assumptions (A.5) and (A.6) will be used for approximating prediction errors of EBLUP.

Let us define by

which is provided by substituting into in (3).

Asymptotic properties of can be investigated under the following standard conditions on and .

Assumption 3.

The following are assumed for and :

(A.7)

converges to a positive definite matrix as .

(A.8)

There exist constants and such that for , and and are positive constants independent of .

Since , it is clear that is consistent and under Assumption 3.

Asymptotic properties on are given in the following lemma which will be proved in Appendix.

This lemma will be used in Lemma 2 to show that some estimators of satisfy condition (A.6).

Lemma 1.

Assume the conditions (A.4) and (A.5) in Assumption 2 and Assumption 3.

Then it holds that and

We here demonstrate that several estimators of suggested in the literature satisfy Assumption 2 for fixed .

A simple moment estimator of due to Prasad and Rao (1990) is given by

(4)

where , and is the ordinary least squares (OLS) estimator

Another moment estimator due to Fay and Herriot (1979), denoted by , is given as a solution of the equation

(5)

The maximum likelihood estimator (ML) of , denoted by , is obtained as a solution of the equation

(6)

The restricted maximum likelihood estimator (REML) of , denoted by , is given as a solution of the equation

(7)

Then, it can be verified that the above four estimators satisfy Assumption 2.

The proof will be given in Appendix.

Lemma 2.

Under Assumption 3, the estimators , , and satisfy Assumption 2.

3.2 Estimation of transformation parameter

We provide a consistent estimator of the transformation parameter .

For estimating , we use the log-likelihood function, which is expressed as

(8)

The derivative with respect to is written as

Thus, we suggest estimator as a solution of the equation:

(9)

where is an estimator of satisfying Assumption 2.

Then, it is shown in the following lemma that the estimator derived from (9) is consistent.

The proof will be given in Appendix.

Lemma 3.

Let be the solution of .

Then, and under Assumptions 1, 2 and 3.

4 EBLUP and Evaluation of the Prediction Error

We now provide the empirical best linear unbiased predictor (EBLUP) for small-area estimation and evaluate asymptotically the prediction error of EBLUP.

Since EBLUP includes the estimator of the transformation parameter in the transformed Fay-Herriot model, it is harder to evaluate the prediction error than in the non-transformed Fay-Herriot model.

To this end, the asymptotic results derived in the previous section are heavily used.

4.1 EBLUP

Consider the problem of predicting , which is the conditional mean of the transformed data given , namely, .

The best predictor of is given by

(10)

Since , and are unknown, we use the estimators suggested in Section 3.

Substituting , given in (3), into yields the estimator

which is the best linear unbiased predictor (BLUP) as a function of , .

For the parameters and , we use the estimators and suggested in Section 3.

Substituting those estimators into the BLUP, we get the empirical best linear unbiased predictor (EBLUP)

(11)

4.2 Second-order approximation of the prediction error

The prediction error of EBLUP is evaluated in terms of the mean squared error (MSE) of given by

for .

It is seen that the MSE can be decomposed as

(12)

where

It is noted that the first two terms in the r.h.s. of (12) are affected by estimation error of , but the last two terms are not affected, namely, and do not depend on randomness of .

Thus, it follows from the well-known result in small area estimation (Datta, Rao and Smith, 2005) that under Assumption 3,

(13)

where , and .

Thus, we need to evaluate the first two terms.

Since given in Lemma 3, the first term can be approximated as

To estimate this term, the following lemma is helpful.

Lemma 4.

Under Assumptions 1, 2 and 3, the derivative of is approximated as

For specific estimators of , we can calculate values of .

For and , the values of are given by

where corresponds to , and corresponds to and .

For , the value of is given by

For the second term, note that , and .

Then it follows from Lemma 4 that

(15)

where

for

It is noted that and are of order and that and generally cannot be expressed explicitly.

Combining the above calculations gives the following theorem.

Theorem 1.

Under Assumptions 1, 2 and 3, the prediction error of EBLUP given in is approximated as

where , are defined in , and .

4.3 Second-order unbiased estimator of the prediction error

For practical applications, we need to estimate the mean squared error of EBLUP.

Although and are not expressed explicitly, we can provide their estimators using the parametric bootstrap method.

Corresponding to model (1), random variable can be generated as

for , where ’s and ’s are mutually independently distributed random errors such that and for .

The estimators , and can be obtained from ’s by using the same manners as used in , and .

Since , it is seen that is a second order unbiased estimator of , namely .

For estimation of , has a second-order bias, since .

Thus, we need to correct the bias up to second order.

By the Taylor series expansion of ,

and that

Then it follows from Assumption 2 and Lemma 3 that , which implies that

where is a bias with order .

Hence, based on the parametric bootstrap, we get a second-order unbiased estimator of given by

(16)

In fact, it can be verified that , since .

For and , their estimators based on the parametric bootstrap are given by

where

Combining the above estimators yields the estimator of given by

(17)

Theorem 2.

Under Assumptions 1, 2 and 3, is a second order unbiased estimator of MSEi, that is

5 Simulation and Empirical Studies

In this section, we investigate finite-sample performances of estimators of the parameters, MSE of EBLUP and estimators of MSE through simulation experiments.

We also apply the suggested procedures to the data in the Survey of Family Income and Expenditure (SFIE) in Japan.

5.1 Finite sample behaviors of estimators

We first investigate finite sample performances of the proposed estimators in the model

We generate covariates from , and fix them through the simulation runs.

Let , , , and .

In the simulation experiments, we generate 10,000 data sets of for to investigate performances of the estimators.

The random effect is generated from with , and the sampling error is generated from .

For ’s, we treat the three patterns:

There are five groups and six small areas in each group.

The error variance is common in the same group.

For estimation of , we use four methods of the maximum likelihood estimator (ML), restricted maximum likelihood estimator (REML), Prasad–Rao estimator (PR) and Fay–Herriot estimator (FH).

We also apply the log-transformed model for the simulated data, which corresponds to the case of in the dual power transformation.

For estimation , and in the log-transformed model, we use the maximum likelihood method.

The average values of estimates and standard errors of , , and are reported in Table 1.

It is observed that the estimates of in the logarithmic transformed case tend to underestimate and their performances are not as good as those in the parametric transformed case.

Comparing the estimating method for , we can see that the REML method gives the estimates closer to the true value of than the other methods.

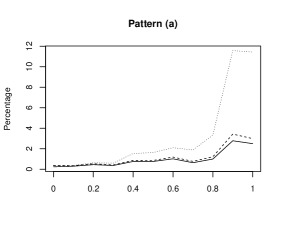

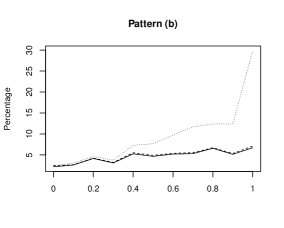

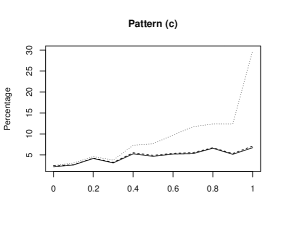

Recently, Li and Lahiri (2010) and Yoshimori and Lahiri (2014a) pointed out that zero estimates for in the Fay-Heriot model is not preferable since zero estimates for mean that resulting EBLUP estimates are over-shrunk to the regression estimator.

Then, we calculated the percentage of zero estimates of based on simulation runs for various values of .

The result is given in Figure 1 for pattern (a), (b) and (c).

It is observed that the percentage in the log-transformation increases as increases, so that it is better to use the parametric transformation for avoiding zero estimates for .

Finally, we investigate robustness of the proposed estimators.

Following Lahiri and Rao (1995), we considered two different distributions for the ’s, namely double exponential and location exponential, which have mean zero and variance .

The sampling error, , was generated from for specified by patterns (a)–(c).

Since the simulation results of and are not very different from the result given in Table 1, we report average values and standard errors of estimators of and for patterns (a) and (c) in Table 2.

Comparing these values with the corresponding average values given in Table 1, we note that the estimates of both and in the double-exponential case perform as well as in the normal case.

However, in the location-exponential case, the estimates of and are more biased than both normal and double-exponential cases.

This may come from skewness of underlying distributions, since the location exponential is a skewed distribution, but the normal and the double-exponential are symmetric distributions.

Table 1: Average Values of Estimators of and for , , , , -patterns (a), (b) and (c). (The standard erros are given in parentheses.)

Pattern (a)

Pattern (b)

Estimator of

ML

0.65

0.46

0.53

1.06

0.68

0.46

0.53

1.09

(0.25)

(0.36)

(0.18)

(0.21)

(0.22)

(0.37)

(0.19)

(0.29)

REML

0.63

0.39

0.52

1.05

0.67

0.41

0.53

1.07

(0.24)

(0.28)

(0.18)

(0.21)

(0.27)

(0.33)

(0.20)

(0.29)

FH

0.67

0.47

0.53

1.08

0.66

0.44

0.53

1.08

(0.28)

(0.37)

(0.18)

(0.24)

(0.22)

(0.39)

(0.20)

(0.26)

PR

0.67

0.50

0.54

1.07

0.66

0.55

0.53

1.08

(0.23)

(0.35)

(0.19)

(0.23)

(0.21)

(0.48)

(0.20)

(0.24)

log

—

0.16

0.42

0.84

—

0.19

0.43

0.82

—

(0.10)

(0.12)

(0.09)

—

(0.12)

(0.15)

(0.17)

Pattern (c)

Estimator of

ML

0.65

0.47

0.53

1.06

(0.21)

(0.49)

(0.22)

(0.23)

REML

0.66

0.39

0.53

1.05

(0.22)

(0.34)

(0.20)

(0.24)

FH

0.65

0.44

0.53

1.06

(0.21)

(0.46)

(0.21)

(0.24)

PR

0.62

0.52

0.52

1.04

(0.26)

(0.51)

(0.21)

(0.29)

log

—

0.11

0.41

0.82

—

(0.10)

(0.14)

(0.09)

Figure 1: Percentage of Zero Estimates of A in Pattern (a) and (c). (The horizontal axis indicates values of . The solid line corresponds to ML method, the dashed line to REML method and the dotted line to log-transformed model.)

Table 2: Average Values and Standard Errors of Estimators of and for , , , , -patterns (a), (b) and (c), and for Double-exponential and Location-exponential Random Effects Distributions. (The standard erros are given in parentheses.)

Double-exponential

Pattern (a)

Pattern (b)

Pattern (c)

Estimator of

ML

0.60

0.41

0.63

0.40

0.64

0.41

(0.32)

(0.34)

(0.26)

(0.36)

(0.21)

(0.41)

REML

0.56

0.36

0.61

0.36

0.63

0.36

(0.32)

(0.29)

(0.25)

(0.31)

(0.20)

(0.36)

Location-exponential

Pattern (a)

Pattern (b)

Pattern (c)

Estimator of

ML

0.45

0.27

0.56

0.32

0.57

0.30

(0.33)

(0.22)

(0.27)

(0.29)

(0.22)

(0.31)

REML

0.42

0.24

0.55

0.29

0.55

0.27

(0.32)

(0.19)

(0.26)

(0.26)

(0.21)

(0.27)

5.2 Numerical properties of MSE and the estimators

We next investigate MSE of EBLUP and performances of estimators of MSE.

The simulation experiments are implemented in the similar framework as treated in Datta (2005).

Since MSE is location invariant, we consider the model (1) without covariates namely , where the transformation function is the dual power transformation.

Let and .

Let be simulated data in the -th replication for , .

Let be EBLUP and let be the best predictor for the -th replication.

Also let be the direct predictor for the -th replication.

Then the true values of MSE of EBLUP and the direct predictor can be numerically obtained by

and their averages over six small areas within group are denoted by and for .

The true values of and the percentage relative gain in MSE defined by are reported in Table 3, where values of the percentage relative gain in MSE are given in parentheses.

It is noted that EBLUP is a shrinkage predictor and is the non-shrinkage direct predictor.

Thus, large values of the relative gain in MSE mean that the improvements of EBLUP over the direct predictor are large.

Table 3 reveals that for all groups, the prediction error of EBLUP is smaller than that of the direct predictor.

Especially, the improvement of EBLUP seems significant in , and .

This implies that EBLUP works well still in the transformed Fay-Herriot model.

The averages of estimates of MSE are obtained based on 5,000 simulated datasets with 1,000 replication for bootstrap, where the estimator of MSE is given in (17).

Then the relative bias of the MSE estimator are reported in Table 4.

From this table, it seems that the MSE estimator gives good estimates for MSE of EBLUP.

Table 3: True values of MSE of EBLUP multiplied by 100 and percentage relative gain in MSE for , , and -patterns (a), (b) and (c) (values of percentage relative gain in MSE are given in parentheses).

Pattern (a)

Pattern (b)

Pattern (c)

0.2

0.6

1.0

0.2

0.6

1.0

0.2

0.6

1.0

12.9

14.3

16.1

12.8

14.3

15.6

12.7

14.1

15.5

(13.8)

(9.5)

(6.0)

(12.9)

(7.6)

(10.1)

(12.7)

(8.3)

(6.9)

21.2

23.0

25.0

28.6

31.2

32.9

35.2

37.7

40.0

(20.8)

(16.3)

(13.5)

(25.5)

(19.5)

(19.2)

(28.7)

(24.5)

(22.9)

28.4

30.6

32.7

40.3

43.4

45.7

50.0

53.0

55.8

(26.4)

(20.5)

(17.8)

(34.5)

(29.1)

(27.4)

(40.2)

(36.7)

(33.3)

34.6

36.9

39.3

53.2

56.5

59.0

62.9

66.3

68.9

(31.1)

(26.0)

(22.9)

(44.8)

(39.6)

(37.8)

(51.4)

(48.2)

(45.8)

39.9

42.4

45.0

59.5

63.3

65.4

71.4

74.7

77.2

(35.4)

(29.4)

(27.5)

(50.1)

(44.8)

(43.5)

(59.0)

(55.7)

(54.0)

Table 4: Average of estimates of MSE multiplied by 100 and their relative biases for , , and -patterns (a), (b) and (c) (percentage relative biases of MSE estimators are given in parentheses).

Pattern (a)

Pattern (b)

Pattern (c)

0.2

0.6

1.0

0.2

0.6

1.0

0.2

0.6

1.0

17.2

16.0

16.4

18.2

16.1

20.4

15.8

15.5

22.0

11.9

10.1

11.8

9.9

7.2

8.9

6.7

5.6

7.8

9.9

7.4

8.8

8.5

5.4

5.7

5.4

3.9

5.3

8.8

6.7

6.9

7.4

4.5

4.3

5.1

3.4

4.9

8.2

5.8

5.8

7.4

3.8

3.6

5.2

3.5

5.2

5.3 Application to the survey data

We now apply the suggested procedures to the data in the Survey of Family Income and Expenditure (SFIE) in Japan.

In this study, we use the data of the spending item ’Education’ in the survey in November 2011.

The average spending (scaled by 10,000 Yen) at each capital city of 47 prefectures in Japan is obtained by for .

Although the average spendings in SFIE are reported every month, the sample size are around 100 for most prefectures, and data of the item ’Education’ have high variability.

On the other hand, we have data in the National Survey of Family Income and Expenditure (NSFIE) for 47 prefectures.

Since NSFIE is based on much larger sample than SFIE, the average spendings in NSFIE are more reliable, but this survey has been implemented every five years.

In this study, we use the data of the item ’Education’ of NSFIE in 2009, which is denoted by for .

Thus, we apply the dual power transformed Fay-Herriot model (1), that is

where .

In model (1), the variances are assumed to be known.

In practice, however, we need to estimate before applying the above model.

In our analysis, we use the data of the spending ’Education’ at the same city every November in the past ten years.

In the usual Fay-Herriot model, we can estimate with the sample variance, but is the variance of the transformed variables in our model.

Then, we propose an iterative method for calculating ’s.

First we calculate the sample variance ’s of the log-transformed data, and we get estimates of using ’s.

Next, we recalculate the sample variance ’s based on the dual power transformed data with parameter .

We continue the procedure until the values of ’s converge.

In our analysis, we get the values of ’s with 5 numbers of iterations.

We used the REML estimators for estimation of since it performs well in simulation studies, and their estimates are and .

The GLS estimates of and are and , so that the regression coefficient on is positive, namely there is a positive correlation between and .

Note that the estimate of is 1.44, which is far away from .

This means that the logarithmic transformation does not seem appropriate for analyzing the data treated here since the treated data is not so right-skewed compared to income data.

For model diagnostics, we calculated a correlation matrix based on the transformed data of past ten years with estimate .

The absolute values of each element are around , which indicates that i.i.d assumptions of is not unrealistic.

The values of EBLUP in seven prefectures around Tokyo are reported in Table 5 with the estimates of their MSEs based on .

It is interesting to investigate what happens when one uses the log-transformed model for the same data.

When the REML estimator is used for estimation of and , their estimates are given by , and .

Note that the estimate of in the log-transformed model is smaller than that in the dual power transformed model, which corresponds to the simulation result.

Remember that determines the rate of shrinkage of toward , namely, the rate increases as the value of increases.

Thus, in the log-transformed model are not shrunken as much as in the dual power transformed model.

Since the dual power transformation includes the log-transformation, we can analyze positive data more flexibly with using the parametric transformed Fay-Herriot model.

Table 5: Values of EBLUP and their estimated MSE.

prefecture

Ibaraki

0.112

-0.215

-0.161

-0.188

0.075

Tochigi

0.444

0.002

-0.158

-0.125

0.111

Gunma

0.110

-0.752

-0.092

-0.429

0.073

Saitama

0.056

0.213

0.461

0.294

0.058

Chiba

0.536

1.681

0.187

0.451

0.120

Tokyo

0.026

0.464

0.315

0.437

0.030

Kanagawa

0.188

1.068

0.235

0.551

0.097

Acknowledgments.

Research of the second author was supported in part by Grant-in-Aid for Scientific Research (21540114, 23243039 and 26330036) from Japan Society for the Promotion of Science.

Appendix

A.1 Proof of Proposition 1 We note that the derivatives of related to Assumption (A.2) are written as

We here check whether the dual power transformation satisfies the integrability conditions in (A.3).

Let be a random variable normally distributed with mean and variance . Then,

and

These evaluations show that the dual power transformation satisfies (A.3).

A.2 Proof of Lemma 1 Since it can be easily seen that , we here give the proof of the second part. We use as abbreviation of when there is no confusion.

Straightforward calculation shows that

(18)

where

(19)

Since , it is seen that

Thus from Assumption 2, the expectation of the first term in (18) is .

For the second term in (18), we have

where the order of the leading term of the last formula is . Then,

(20)

Therefore we obtain

(21)

Since from (A.5) in Assumption 2, the first term in (21) has .

For the second term in (21), from the central limit theorem, we have

which, together with Assumption 3, implies that the second term in (21) is of order .

Therefore we can conclude that .

A.3 Proof of Lemma 2 It is clear that condition (A.4) is satisfied for the estimators of from the results given in the literature, so that we shall verify conditions (A.5) and (A.6) in Assumption 2.

by the law of large numbers.

Since , we have , which shows (A.5).

For (A.6), note that

(22)

Then, it is observed that

where

(23)

Since it is clear that , , and are independent, by the central limit theorem, we have

which shows (A.6), and Assumption 2 is satisfied for .

FH, ML and REML estimators

We next show Lemma 2 for and .

For the proofs, we begin by showing that and satisfy condition (A.5).

Then we can use Lemma 1, which is guaranteed under (A.4), (A.5) and Assumption 3.

Using Lemma 1, we next show condition (A.6) for the estimators.

Since and are defined as the solutions of the equations (5), (6) and (7), it follows from the implicit function theorem that

(24)

where is an equation which determines an estimator of , and

For , and , the function is written as

(25)

where

which is under Assumptions 2 and 3. Note that the case of corresponds to , and the case of corresponds to and .

Using the expression of (24), we show that , which is sufficient to verify that and .

For this purpose, the following facts are useful:

(26)

(27)

(28)

(29)

where .

These facts can be verified by noting that , and using the law of large numbers and the central limit theorem under Assumptions 1 and 3.

If we assume that (this is actually proved for each estimators in the end of the proof), it is immediate from (26)(29) that

and we obtain .

Hence, it has been shown that condition (A.5) is satisfied by , and .

We next show that condition (A.6) is satisfied by , and .

Since (A.4) and (A.5) are satisfied, we can use Lemma 1.

Then,

From (26)(29) and Lemma 1, we can evaluate (25) as

since .

Here we assume that

(30)

where is a constant depending on with order .

This will be proved for each estimator in the end of this proof.

Then we have

(31)

Therefore we have

where is given in (23), and by the central limit theorem, we have

Consequently, we have proved for and .

It remains to show that for and .

For , from (5), we have

where

where is given in (19). Note that and from the law of large numbers, we have

Thus we have

Since , by the law of large numbers, we have

(32)

where the order of the leading term is , corresponding to .

Similarly, for and given in (6) and (7), straight calculation (almost the same as in the case of ) shows that

(33)

where the order of the leading term is , corresponding to .

A.4 Proof of Lemma 3 We begin by showing that .

By the Taylor series expansion of equation (9), we have

where

where is satisfying .

For , from Assumption 1, we have

for .

Since are mutually independent, by the law of large numbers, we have

where is the density function of observation in (1).

By the central limit theorem, we have

Therefore we have

and we conclude that .

We next show that .

From the first part of Lemma 3, we have .

Then expanding (9) shows that

Thus, it is sufficient to show that the expectation of the first term is .

It is observed that

Since and , it is noted that

which is of order .

Hence,

Since

it is cocluded that .

A.5 Proof of Lemma 4 By the Taylor series expansion of , we have

where is an intermediate value of and and is an intermediate vector of and . Differentiating the both sides by , we have

from Lemmas 1 and 2.

Also from Lemmas 1 and 2, we already know that

(34)

and

(35)

where corresponds to and corresponds to and .

The formula (34) comes from (20), and the formula (35) is obtained by combining (30), (32) and (33).

For , from (22),

which completes the proof.

References

[1]Box, G.E.P, and Cox, D.R. (1964).

An analysis of transformation (with discussion).

J. R. Stat. Soc. Ser. B Stat. Methodol., 26, 211-252.

[2]

[3]Battese, G.E., Harter, R.M. and Fuller, W.A. (1988). An error-components model for prediction of county crop areas using survey and satellite data. J. Amer. Statist. Assoc., 28-36.

[4]

[5]Chatterjee, S., Lahiri, P. and Li, H. (2008). Parametric bootstrap approximation to the distribution of EBLUP and related predictions intervals in linear mixed models. Ann. Statist., 36, 1221-1245.

[6]

[7]Chambers, R. L., Chandra, H., Salvati, N. and Tzavidis, N. (2014). Outlier robust small area estimation, J. R. Stat. Soc. Ser. B Stat. Methodol., 76, 47-69.

[8]

[9]Chaudhuri, S. and Ghosh, M. (2011). Empirical likelihood for

small area estimation. Biometrika, 98, 473–480.

[10]

[11]Datta, G.S., Rao, J.N.K. and Smith, D.D. (2005).

On measuring the variability of small area estimators under a basic area level model.

Biometrika, 92, 183-196.

[12]

[13]Das, K., Jiang, J. and Rao, J. N. K. (2004). Mean squared error

of empirical predictor. Ann. Statist.,32, 818–840.

[14]

[15]Diao, L., Smith, D. D., Datta, G. S., Maiti, T. and Opsomer, J. D. (2014). Accurate confidence interval estimation of small area parameters under the Fay–Herriot model. Scand. J. Statist., 41, 497–515.

[16]

[17]Fay, R. and Herriot, R. (1979).

Estimators of income for small area places: an application of James–Stein procedures to census.

J. Amer. Statist. Assoc., 74, 341-353.

[18]

[19]Ghosh, M. and Rao, J.N.K. (1994).

Small area estimation: An appraisal.

Statist. Science, 9, 55-93.

[20]

[21]Hall, P. and Maiti, T. (2006a). On parametric bootstrap methods for small area prediction. J. R. Stat. Soc. Ser. B Stat. Methodol., 68, 221-238.

[22]

[23]Hall, P. and Maiti, T. (2006b). Nonparametric estimation of mean-squared prediction error in nested-error regression models, Ann. Statist., 34, 1733–1750.

[24]

[25]Hawala, S. and Lahiri, P. (2010). Variance modeling in the U.S. small area income and poverty estimates program for the American community survey.

Proceedings of the American Statistical Association, Section on Bayesian Statistical Science, Section on Survey Research Methods, Alexandria, VA: American Statistical Association.

[26]

[27]Lahiri, P. and Rao, J. N. K. (1995). Robust estimation of mean squared error of small area estimators, J. Amer. Statist. Assoc., 90, 758–766.

[28]

[29]Li, H. and Lahiri, P. (2010). An adjusted maximum likelihood method for solving small area estimation problems.J. Multivariate Anal., 101, 882-892.

[30]

[31]Opsomer, J. D., Claeskens, G., Ranalli, M. G., Kauermann, G. and Breidt, F. J. (2008). Non-parametric small area estimation using penalized spline regression. J. R. Stat. Soc. Ser. B Stat. Methodol., 70, 265–286.

[32]

[33]Pfeffermann, D. (2013) New Important Developments in Small

Area Estimation. Statist. Sinica, 28, 40-68

[34]

[35]Prasad, N. and Rao, J. N. K. (1990).

The estimation of mean-squared errors of small-area estimators.

J. Amer. Statist. Assoc., 90, 758-766.

[36]

[37]Rao, J.N.K. (2003).

Small Area Estimation. Wiley.

[38]

[39]Slud, E.V. and Maiti, T. (2006).

Mean-squared error estimation in transformed Fay-Herriot models.

J. R. Stat. Soc. Ser. B Stat. Methodol., 68, 239-257.

[40]

[41]Yang, Z. L. (2006).

A modified family of power transformations.

Econ. Letters, 92, 14-19.

[42]

[43]Yoshimori, M. and Lahiri, P. (2014a). A New Adjusted Maximum Likelihood Method for the Fay-Herriot Small Area Model. J. Multivariate Anal., 124, 281-294.

[44]

[45]Yoshimori, M. and Lahiri, P. (2014b). A second-order efficient empirical Bayes confidence interval. Ann. Statist., 42, 1233-1261