Yumiharu Nakano111

This study is partially supported by JSPS KAKENHI Grant Number 26800079.

Graduate School of Innovation Management

Tokyo Institute of Technology

2-12-1 W9-117 Ookayama 152-8552, Tokyo, Japan

Abstract

We propose numerical integration methods for Choquet integrals where

the capacities are given by distortion functions of an underlying probability measure.

It relies on the explicit representation of the integrals for step functions and

can be seen as quasi-Monte Carlo methods in this framework.

We give bounds on the approximation errors in terms of the modulus of continuity of

the integrand and the star discrepancy.

Key words: Choquet integrals, quasi-Monte Carlo methods,

risk measures.

AMS MSC 2010:

65D30, 28A25, 65C05.

In this paper, we are concerned with numerical integration for Choquet integrals

(1)

for continuous functions on ,

where is a -valued and uniformly distributed random variable on an

atomless probability space , the function

is increasing and concave such that

, , and

is the submodular set function defined by

, .

We refer to Denneberg [2] for the theory of Choquet integrals.

The capacities of the form as above

appear in financial risk management. In particular,

the case , for some ,

corresponds to the risk measure known as the average-value-at-risk,

which is also called as the conditional value-at-risk or the expected shortfall in practice.

We refer to Artzner et al. [1],

McNeil et al. [4],

and Föllmer and Schied [3] for details.

As for numerical integration, several techniques that are analogous to those for

the linear integral have been studied in the literature.

See, e.g., [4] for Monte Carlo methods,

and Nakano [5] for optimal quantization methods.

However, to the best of our knowledge, quasi-Monte Carlo methods have not been

examined to Choquet integrals despite of its popularity.

To find a suitable quasi-Monte Carlo method for (1),

let is a point set in and consider

the simple random variable defined by

where is a partition of such that

, .

Note that such ’s exist since

is assumed to be atomless.

If is uniformly distributed, then we expect

Next, recall that the Choquet integral has the

comonotonicity, i.e., for any random variables and

that are integrable with respect to , we have

whenever

(2)

for all except for a

set of probability zero.

Two random variables and are said to be comonotone if

they satisfy (2).

Now observe that for ,

the two indicator functions

and are comonotone if .

Thus, for and ,

, we have

(3)

provided that and ,

.

Let be such that

.

Then we have the representation of given by

To obtain an error bound, we use the star discrepancy

defined by

for a point set ,

where stands for the Lebesgue measure on .

We refer to Niederreiter [6] for the relation between the discrepancy and

numerical integration.

Further, let be the modulus of continuity of a function defined by

where denotes the max norm of a vector .

Also, notice that by the concavity of , the limit

exists for any and decreasing with respect to .

Then we have the following:

Theorem 1.

Under the assumptions and notations above,

if , we have

Moreover, if , then

Remark 2.

Since we have assumed that and are continuous with ,

the quantity and so the approximation

error converge to zero, provided that as .

In particular, if , the function is Lipschitz on ,

and is a low-discrepancy point set, i.e., it satisfies

for some positive constant ,

then the theorem implies

where is the Lipschitz constant of .

Remark 3.

In case , we have

.

Remark 4.

If then the constant in the statement of the theorem is replaced by .

This can be verified from the proof below and Theorem 2.10 in [6].

Proof of Theorem 1.

By Lemma 4.63 in [3] we define the Borel probability measure

on by the identity

Then, from Lemma 4.46 and Theorem 4.64 in [3] it follows that

(4)

for any bounded random variable , where

for .

Moreover, for each , the infimum of the integrand in (4) is attained by

Since , ,

the first term in the equality just above is at most

.

By Fubini’s theorem, the second term is equal to

(5)

where

By Theorem 1 in Proinov [7],

the quantity (5) is bounded by .

Furthermore, it is straightforward to see that

.

Summarizing the above arguments, we deduce that

A similar argument shows that

is bounded by the right-hand side in

the inequality just above.

Thus,

(6)

Now, if , then we set in (6) to

obtain the second assertion of the theorem.

Otherwise, we use an argument from the proof of Lemma 4.63 in [3] to

obtain . Therefore, by the choice

the right-hand side in (6) is estimated as

Thus the first assertion of the theorem follows.

∎

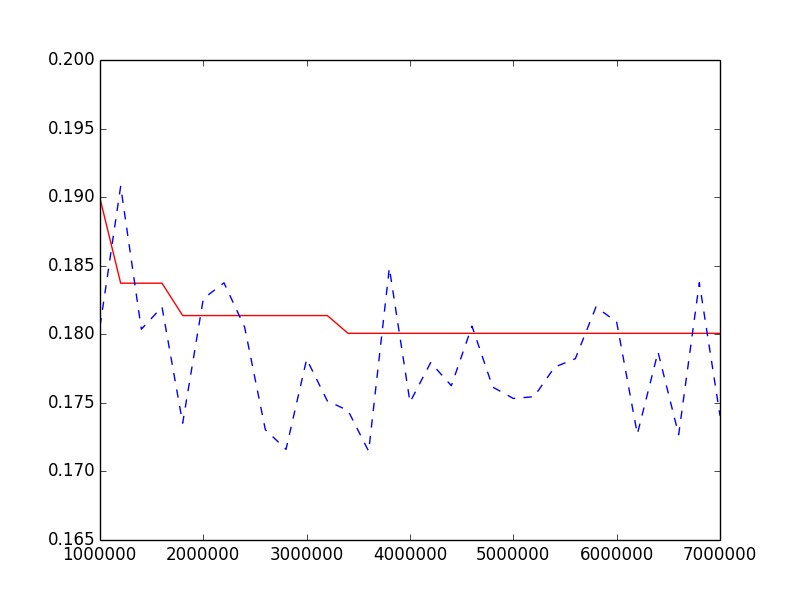

Example 5.

Here, we present a numerical result in the case of

, , and

We use the Halton sequence to compute .

As a comparison, we take the Monte Carlo method, which is described by

where is an IID sequence with uniform distribution on

and is such that

.

Figure 1 plots values of and for

from to with step .

We can see that steadily approaches to a true value as increases,

whereas the behavior of is still volatile even for

larger than .

Figure 1: Nurimerical integrations of with quasi-Monte Carlo (solid)

and Monte Carlo (dashed) methods for from to .

References

[1]

P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath.

Coherent measurement of risk.

Math. Finance, 9:203–228, 1999.

[2]

D. Denneberg.

Non-additive measure and integral.

Kluwer Academic Publishers, Dordrecht, 1994.

[3]

H. Föllmer and A. Schied.

Stochastic Finance: An Introduction in Discrete Time.

Walter de Gruyter, Berlin, 2nd edition, 2004.

[4]

A. J. McNeil, R. Frey, and P. Embrechts.

Quantitative risk management: concepts, techniques and tools.

Princeton University Press, Princeton, 2005.

[5]

Y. Nakano.

On approximating law-invariant comonotonic coherent risk measures.

Astin Bulletin, 42:343–353, 2012.

[6]

H. Niederreiter.

Random number generation and quasi-Monte Carlo methods.

Society for Industrial and Applied Mathematics, Philadelphia, 1992.

[7]

P. D. Proinov.

Discrepancy and integration of continuous functions.

J. Approx. Theory, 52:121–131, 1988.