\pkgBiips: Software for Bayesian Inference with Interacting Particle Systems

A. Todeschini, F. Caron, M. Fuentes, P. Legrand, P. Del Moral \PlaintitleBiips: a Software for Bayesian Inference with Interacting Particle Systems \Shorttitle\pkgBiips \Abstract

\pkgBiips is a software platform for automatic Bayesian inference with interacting particle systems. \pkgBiips allows users to define their statistical model in the probabilistic programming \proglangBUGS language, as well as to add custom functions or samplers within this language. Then it runs sequential Monte Carlo based algorithms (particle filters, particle independent Metropolis-Hastings, particle marginal Metropolis-Hastings) in a black-box manner so that to approximate the posterior distribution of interest as well as the marginal likelihood. The software is developed in \proglangC++ with interfaces with the softwares \proglangR, \proglangMATLAB and \proglangOctave.

\Keywordssequential Monte Carlo, particle filters, Markov chain Monte Carlo, particle MCMC, graphical models, \proglangBUGS, \proglangC++, \proglangR, \proglangMATLAB, probabilistic programming, \proglangOctave

\Plainkeywordsprobabilistic programming, sequential Monte Carlo, particle filters, Markov chain Monte Carlo, particle MCMC, graphical models, BUGS, C++, R, Matlab, Octave \Address

Adrien Todeschini

INRIA Bordeaux Sud-Ouest

200 avenue de la vieille tour

33405 Talence Cedex, France

E-mail:

URL: https://sites.google.com/site/adrientodeschini/François Caron

Department of Statistics

University of Oxford

1 South Parks Road

OX13TG, Oxford, United Kingdom

E-Mail:

URL: http://www.stats.ox.ac.uk/~caron/

1 Introduction

Bayesian inference aims at approximating the conditional probability law of an unknown parameter given some observations . Several problems such as signal filtering, object tracking or clustering can be cast into this framework. This conditional probability law is in general not analytically tractable. Markov chain Monte Carlo (MCMC) methods (Gilks et al., 1995; Robert and Casella, 2004), and in particular Gibbs samplers, have been extensively used over the past 20 years in order to provide samples asymptotically distributed from the conditional distribution of interest. As stated by Cappé and Robert (2000)

“The main factor in the success of MCMC algorithms is that they can be implemented with little effort in a large variety of settings. This is obviously true of the Gibbs sampler, which, provided some conditional distributions are available, simply runs by generating from these conditions, as shown by the BUGS software.”

The \proglangBUGS (which stands for Bayesian Inference Using Gibbs Sampling) software has actually greatly contributed to the development of Bayesian and MCMC techniques among applied fields (Lunn et al., 2012). \proglangBUGS allows the user to define statistical models in a natural language, the \proglangBUGS language (Gilks et al., 1994), then approximates the posterior distribution of the parameter given the data using MCMC methods and provides some summary statistics. It is easy to use even for people not aware of MCMC methods and works as a black box. Various softwares have been developed based on or inspired by the ‘classic’ \proglangBUGS software, such as \pkgWinBUGS, \pkgOpenBUGS, \pkgJAGS or \pkgStan.

A new generation of algorithms, based on interacting particle systems, has generated a growing interest over the last 20 years. Those methods are known under the names of interacting MCMC, particle filtering, sequential Monte Carlo methods (SMC)111Because of its widespread use in the Bayesian community, we will use the latter term in the remaining of this article.. For some problems, those methods have shown to be more appropriate than MCMC methods, in particular for time series or highly correlated variables (Doucet et al., 2000, 2001; Liu, 2001; Del Moral, 2004; Douc et al., 2014). Contrary to MCMC methods, SMC do not require the convergence of the algorithm to some equilibrium and are particularly suited to dynamical estimation problems such as signal filtering or object tracking. Moreover, they provide unbiased estimates of the marginal likelihood at no additional computational cost. They have found numerous applications in signal filtering and robotics (Thrun et al., 2001; Gustafsson et al., 2002; Vermaak et al., 2002; Vo et al., 2003; Ristic et al., 2004; Caron et al., 2007), systems biology (Golightly and Wilkinson, 2006, 2011; Bouchard-Côté et al., 2012), economics and macro-economics (Pitt and Shephard, 1999; Fernández-Villaverde and Rubio-Ramírez, 2007; Flury and Shephard, 2011; Del Moral et al., 2012), epidemiology (Cauchemez et al., 2008; Dureau et al., 2013), ecology (Buckland et al., 2007; Peters et al., 2010) or pharmacology (Donnet and Samson, 2011). The introduction of the monograph of Del Moral (2013) provides early references on this class of algorithms and an extensive list of application domains.

Traditionally, SMC methods have been restricted to the class of state-space models or hidden Markov chain models for which those models are particularly suited (Cappé et al., 2005). However, SMC are far from been restricted to this class of models and have been used more broadly, either alone or as part of a MCMC algorithm (Fearnhead, 2004; Fearnhead and Liu, 2007; Caron et al., 2008; Andrieu et al., 2010; Caron et al., 2012; Naesseth et al., 2014).

The \pkgBiips software222http://alea.bordeaux.inria.fr/biips, which stands for Bayesian Inference with Interacting Particle Systems, has the following features:

-

•

\proglang

BUGS compatibility: Similarly to the softwares \pkgWinBUGS, \pkgOpenBUGS and \pkgJAGS, it allows users to describe complex statistical models in the \proglangBUGS probabilistic language.

-

•

Extensibility: \proglangR/\proglangMATLAB custom functions or samplers can be added to the \proglangBUGS library.

-

•

Black-box SMC inference: It runs sequential Monte Carlo based algorithms (forward SMC, forward-backward SMC, particle independent Metropolis-Hastings, particle marginal Metropolis-Hastings) to provide approximations of the posterior distribution and of the marginal likelihood.

-

•

Post-processing: The software provides some tools for extracting summary statistics (mean, variance, quantiles, etc.) on the variables of interest from the output of the SMC-based algorithms.

-

•

\proglang

R/\proglangMATLAB/\proglangOctave interfaces: The software is developed in \proglangC++ with interfaces with the softwares \proglangR, \proglangMATLAB and \proglangOctave.

This article is organized as follows. Section 2 describes the representation of the statistical model as a graphical model and the \proglangBUGS language. Section 3 provides the basics of SMC and particle MCMC algorithms. The main features of the \pkgBiips software and its interfaces to \proglangR and \proglangMATLAB/\proglangOctave are given in Section 4. Sections 5 and 6 provide illustrations of the use of the software for Bayesian inference in stochastic volatility and stochastic kinetic models. In Section 7 we discuss the relative merits and limits of \pkgBiips compared to alternatives, and we conclude in Section 8.

2 Graphical models and \proglangBUGS language

2.1 Graphical models

A Bayesian statistical model is represented by a joint distribution over the parameters and the observations . The joint distribution decomposes as where the two terms of the right-hand side are respectively named likelihood and prior. As stated in the introduction, the objective of Bayesian inference is to approximate the posterior distribution after having observed some data .

A convenient way of representing a statistical model is through a directed acyclic graph (Lauritzen, 1996; Green et al., 2003; Jordan, 2004). Such a graph provides at a glance the conditional independencies between variables and displays the decomposition of the joint distribution. As an example, consider the following switching stochastic volatility model (1).

Example (Switching stochastic volatility).

Let be the response variable (log-return) and the unobserved log-volatility of . The stochastic volatility model is defined as follows for

| (1a) | ||||

| (1b) | ||||

| where ‘’ means ‘statistically distributed from’, denotes the normal distribution of mean and variance , and . The regime variables follow a two-state Markov process with transition probabilities | ||||

| (1c) | ||||

| for with and . | ||||

The graphical representation of the switching volatility model as a directed acyclic graph is given in Figure 1.

2.2 \proglangBUGS language

The \proglangBUGS language is a probabilistic programming language that allows to define a complex stochastic model by decomposing the model into simpler conditional distributions (Gilks et al., 1994). We refer the reader to the \pkgJAGS user manual (Plummer, 2012) for details on the \proglangBUGS language. The transcription of the switching stochastic volatility model (1) in \proglangBUGS language is given in Listing 1333We truncated the Gaussian transition on to lie in the interval in order to prevent the measurement precision to be numerically approximated to zero, which would produce an error..

3 Sequential Monte Carlo methods

3.1 Ordering and arrangement of the nodes in the graphical model

In order to apply sequential Monte Carlo methods in an efficient manner, \pkgBiips proceeds to a rearrangement of the nodes of the graphical model as follows:

-

1.

Sort the nodes of the graphical model according to a topological order (parents nodes before children), by giving priority to measurement nodes compared to state nodes (note that the sort is not unique);

-

2.

Group together successive measurement or state nodes;

-

3.

We then obtain an ordering where correspond to groups of unknown variables, and to groups of observations.

Figure 2 gives an example of rearrangement of a graphical model.

3.2 Sequential Monte Carlo algorithm

Assume that we have variables which are sorted as described in Section 3.1, where and respectively correspond to unobserved and observed variables, for . By convention, let , . Also, let and for where . The statistical model decomposes as

| (2) |

where pa denotes the set of parents of variable in the decomposition described in Section 3.1.

Sequential Monte Carlo methods (Doucet et al., 2001; Del Moral, 2004; Doucet and Johansen, 2011) proceed by sequentially approximating conditional distributions

| (3) |

for , by a weighted set of particles that evolve according to two mechanisms:

-

•

Mutation/Exploration: Each particle is randomly extended with

-

•

Selection: Each particle is associated a weight depending on its fit to the data. Particles with high weights are duplicated while particles with low weights are deleted.

The vanilla sequential Monte Carlo algorithm is given in Algorithm 1.

For

For , sample and let

For , set

For , set

Duplicate particles of high weight and delete particles of low weight using some resampling strategy. Let , be the resulting set of particles with weights .

Outputs:

Weighted particles for

Estimate of the marginal likelihood

The output of the algorithm is a sequence of weighted particles providing approximations of the successive conditional distributions . In particular, provides a particle approximation of the full conditional distribution of the unknown variables given the observations. Point estimates of the parameters can then be obtained. For any function

| (4) |

For example, by taking one obtains posterior mean estimates

The algorithm also provides an unbiased estimate of the marginal likelihood

| (5) |

is the proposal/importance density function and is used for exploration. This proposal may be a function of pa and/or . The simplest is to use the conditional distribution , which is directly given by the statistical model, as a proposal distribution. A better choice is to use the distribution , or any approximation of this distribution.

3.3 Limitations of SMC algorithms and diagnostic

Due to the successive resampling, the quality of the particle approximation of decreases as increases, a problem referred as sample degeneracy or impoverishment, see e.g. Doucet and Johansen (2011). \pkgBiips uses a simple criteria to provide a diagnostic on the output of the SMC algorithm.

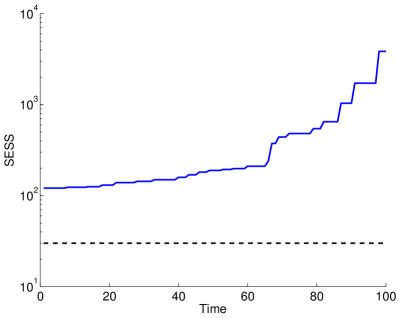

Let child be set of indices of the children of particle at time . Note that if a particle is deleted at time , then child. Similarly, let anc be the index of the first-generation ancestor of particle at time . We therefore have . By extension, we write anc for the index of the second-generation ancestor of particle at times . Let be the set of unique values in (anc. Due to the successive resampling, the number of unique ancestors of the particles at time decreases as increases. A measure of the quality of the approximation of the marginal posterior distributions , for , is given by the smoothing effective sample size ():

| (6) |

with . Figure 3 provides an illustration on a simple example. Larger values of the SESS indicate better approximation. As explained earlier, this value is likely to decrease with the number due to the successive resamplings. For a given value of , one can increase the number of particles in order to obtain an acceptable SESS. In a simple importance sampling framework, the ESS corresponds to the number of perfect samples from the posterior needed to obtain an estimator with similar variance (Doucet and Johansen, 2011); as a rule of thumb, the minimal value is set to .

Nonetheless, in cases where is very large, or when a given unobserved node is the parent of a large number of other unobserved nodes (sometimes referred as parameter estimation problem in sequential Monte Carlo), this degeneracy may be too severe in order to achieve acceptable results. To address such limitations, Andrieu et al. (2010) have recently proposed a set of techniques for mitigating SMC algorithms with MCMC methods by using the former as a proposal distribution. We present such algorithms in the next section.

3.4 Particle MCMC

One of the pitfalls of sequential Monte Carlo is that they suffer from degeneracy due to the successive resamplings. For large graphical models, or for graphical models where some variables have many children nodes, the particle approximation of the full posterior will be poor. Recently, algorithms have been developed that propose to use SMC algorithms within a MCMC algorithm (Andrieu et al., 2010). The particle independent Metropolis-Hastings (PIMH) algorithm 2 provides MCMC samples asymptotically distributed from the posterior distribution, using a SMC algorithm as proposal distribution in an independent Metropolis-Hastings (MH) algorithm.

Set

For

Run a sequential Monte Carlo algorithm to approximate .

Let and be respectively the set of weighted particles and the estimate of the marginal likelihood.

With probability

set and , where

otherwise, set and

Output:

MCMC samples

The particle marginal Metropolis-Hastings (PMMH) algorithm splits the variables in the graphical model into two sets: one set of variables that will be sampled using a SMC algorithm, and a set sampled with a MH proposal. It outputs MCMC samples asymptotically distributed from the posterior distribution. Algorithm 3 provides a description of the PMMH algorithm.

Set and initialize

For

Sample

Run a sequential Monte Carlo algorithm to approximate . Let and be respectively the set of weighted particles and the estimate of the marginal likelihood.

With probability

set , and , where

otherwise, set , and

Output:

MCMC samples

4 Biips software

The \pkgBiips code consists of three libraries written in \proglangC++ whose architecture is adapted from \pkgJAGS and two user interfaces. Figure 4 summarizes the main components from the bottom to the top level.

\pkgBiips \proglangC++ libraries

-

•

The Core library contains the bottom level classes to represent a graphical model and run SMC algorithms.

-

•

The Base library is an extensible collection of distributions, functions and samplers.

-

•

The Compiler library allows to describe the model in \proglangBUGS language and provides a controller for higher level interfaces.

\pkgBiips user interfaces

At the top level, we provide two user interfaces to the \pkgBiips \proglangC++ classes:

-

•

\pkg

Matbiips interface for \proglangMATLAB/\proglangOctave.

-

•

\pkg

Rbiips interface for \proglangR.

These interfaces for scientific programming languages make use of specific libraries that allow binding \proglangC++ code with their respective environment. \pkgMatbiips uses the \proglangMATLAB MEX library or its \proglangOctave analog. \pkgRbiips uses the \pkgRcpp library (Eddelbuettel and François, 2011; Eddelbuettel, 2013).

In addition, the interfaces provide user-friendly functions to facilitate the workflow for doing inference with \pkgBiips. The typical workflow is the following:

-

1.

Define the model and data.

-

2.

Compile the model.

-

3.

Run inference algorithms.

-

4.

Diagnose and analyze the output.

The main functions in \pkgMatbiips and \pkgRbiips are described in Table 1. Both interfaces use the same set of functions, with similar inputs/outputs; the interface is also similar to the \pkgrjags (Plummer, 2014) interface to \pkgJAGS. The \pkgMatbiips interface does not use object-oriented programming due to compatibility issues with \proglangOctave, whereas \pkgRbiips uses S3 classes. The prefix \codebiips_ is used for function names in order to avoid potential conflicts with other packages.

| Construction of the model | |

|---|---|

| \codebiips_model | Instantiates a BUGS-language stochastic model |

| \codebiips_add_function | Adds a custom function |

| \codebiips_add_distribution | Adds a custom sampler |

| Inference algorithms | |

| \codebiips_smc_samples | Runs a SMC algorithm |

| \codebiips_smc_sensitivity | Estimates the marginal likelihood for a set of parameter values |

| \codebiips_pimh_init | Initializes the PIMH |

| \codebiips_pimh_update | Runs the PIMH (burn-in) |

| \codebiips_pimh_samples | Runs the PIMH and returns samples |

| \codebiips_pmmh_init | Initializes the PMMH |

| \codebiips_pmmh_update | Runs the PMMH (adaptation and burn-in) |

| \codebiips_pmmh_samples | Runs the PMMH and returns samples |

| Diagnosis and summary | |

| \codebiips_diagnosis | Performs a diagnosis of the SMC algorithm |

| \codebiips_density | Returns kernel density estimates of the posterior (continuous) |

| \codebiips_table | Returns probability mass estimates of the posterior (discrete) |

| \codebiips_summary | Returns summary statistics of the posterior |

Extensions of the \proglangBUGS language with custom functions

In addition to the user interfaces, we provide a simple way of extending the \proglangBUGS language by adding custom distributions and functions. This is done by calling \proglangMATLAB/\proglangOctave or \proglangR functions from the \proglangC++ layer using the \proglangC \pkgMEX library in \proglangMATLAB/\proglangOctave and the \pkgRcpp package in \proglangR.

5 Example: Switching stochastic volatility model

5.1 Bayesian inference with SMC

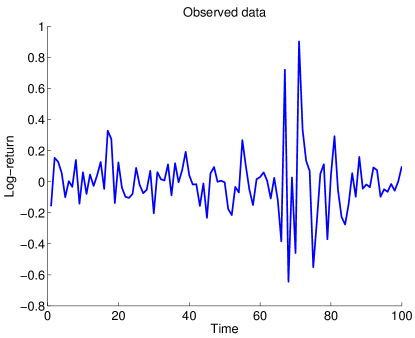

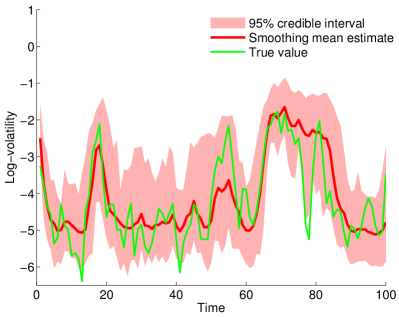

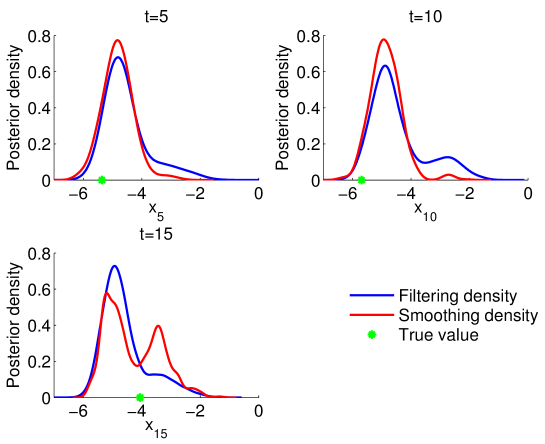

We consider the switching stochastic volatility model (1). Our objective is to approximate the filtering distributions and smoothing distributions , for and obtain some point estimates, such as the posterior means or posterior quantiles. The function \codebiips_model parses and compiles the \proglangBUGS model, and sample the data if \codesample_data is set to true. The data are represented in Figure 5.

One can then run a sequential Monte Carlo algorithm with the function \codebiips_smc_samples to provide a particle approximation of the posterior distribution. The particle filter can be run in filtering, smoothing and/or backward smoothing modes, see (Doucet and Johansen, 2011) for more details. By default, \pkgBiips also automatically chooses the proposal distribution .

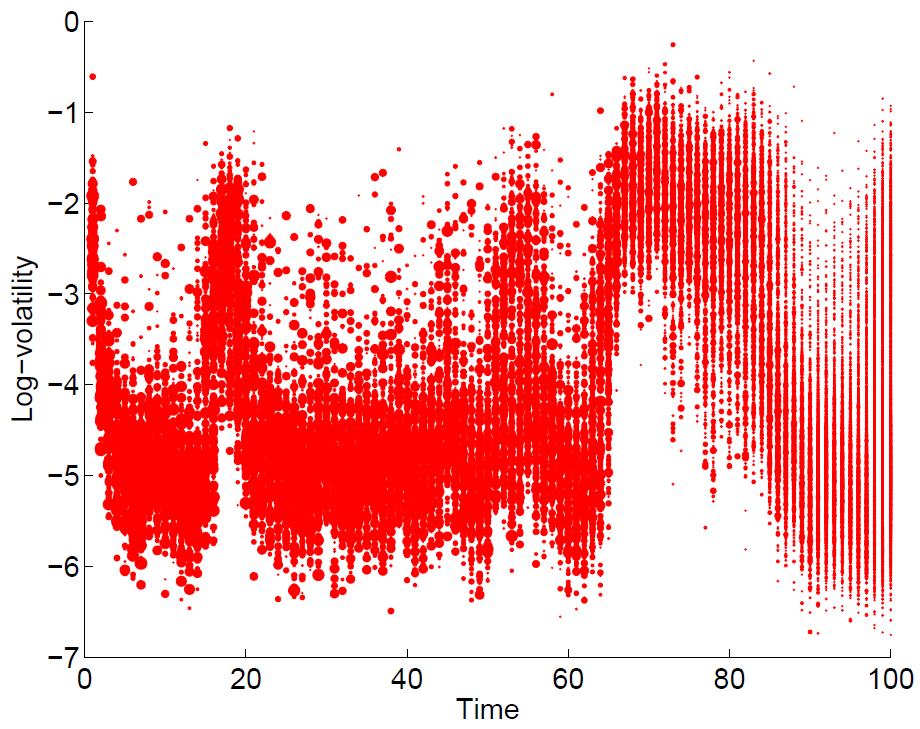

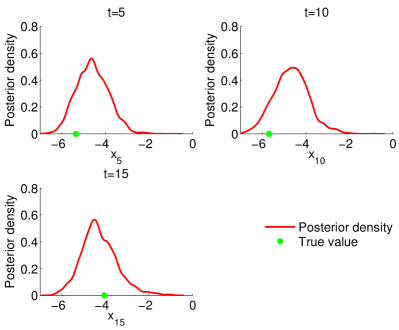

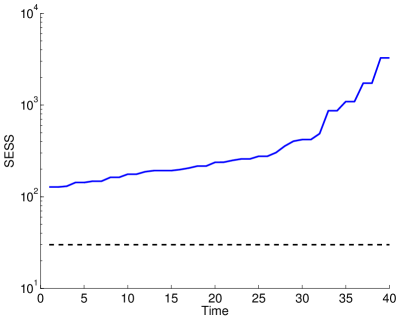

out_smc is an object containing the values of the particles and their weights for each of the monitored variables (the variable in the example). An illustration of the weighted particles is given in Figure 6(a). Figure 6(b) shows the value of the SESS with respect to time. If the minimum is below the threshold of 30, \codebiips_diagnosis recommends to increase the number of particles.

The function \codebiips_summary provides some summary statistics on the marginal distributions (mean, quantiles, etc.), and \codebiips_density returns kernel density estimates of the marginal posterior distributions.

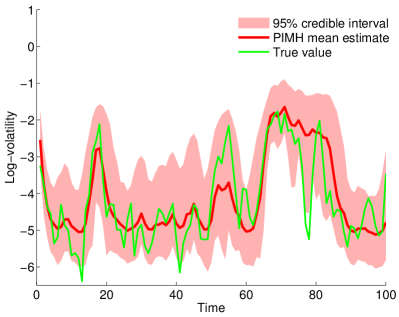

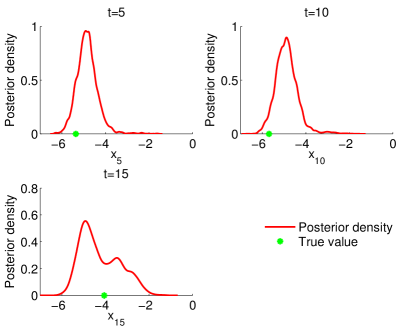

5.2 Bayesian inference with particle independent Metropolis-Hastings

The SMC algorithm can also be used as a proposal distribution within an MCMC algorithm to provide MCMC samples from the posterior distribution, as described in Section 3.4. This can be done with \pkgBiips with the functions \codebiips_pimh_init, \codebiips_pimh_update and \codebiips_pimh_samples. The first function creates a PIMH object; The second one runs burn-in iterations; The third one runs PIMH iterations and returns samples.

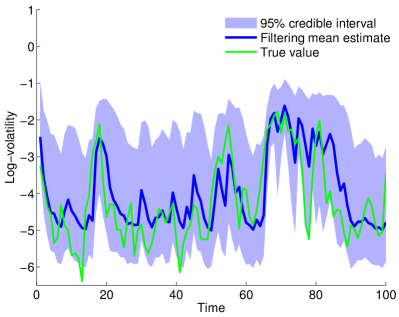

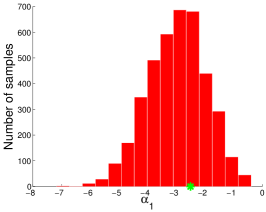

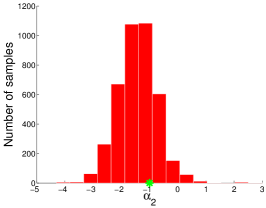

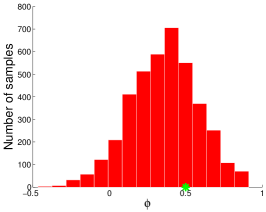

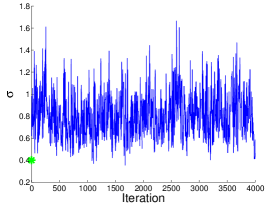

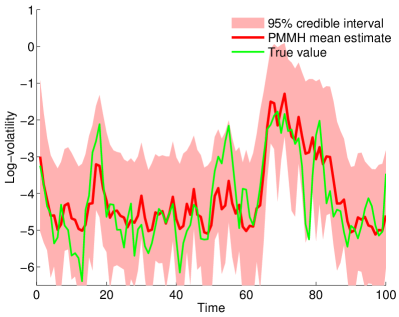

Posterior means, credible intervals and some marginal posteriors are reported in Figure 9.

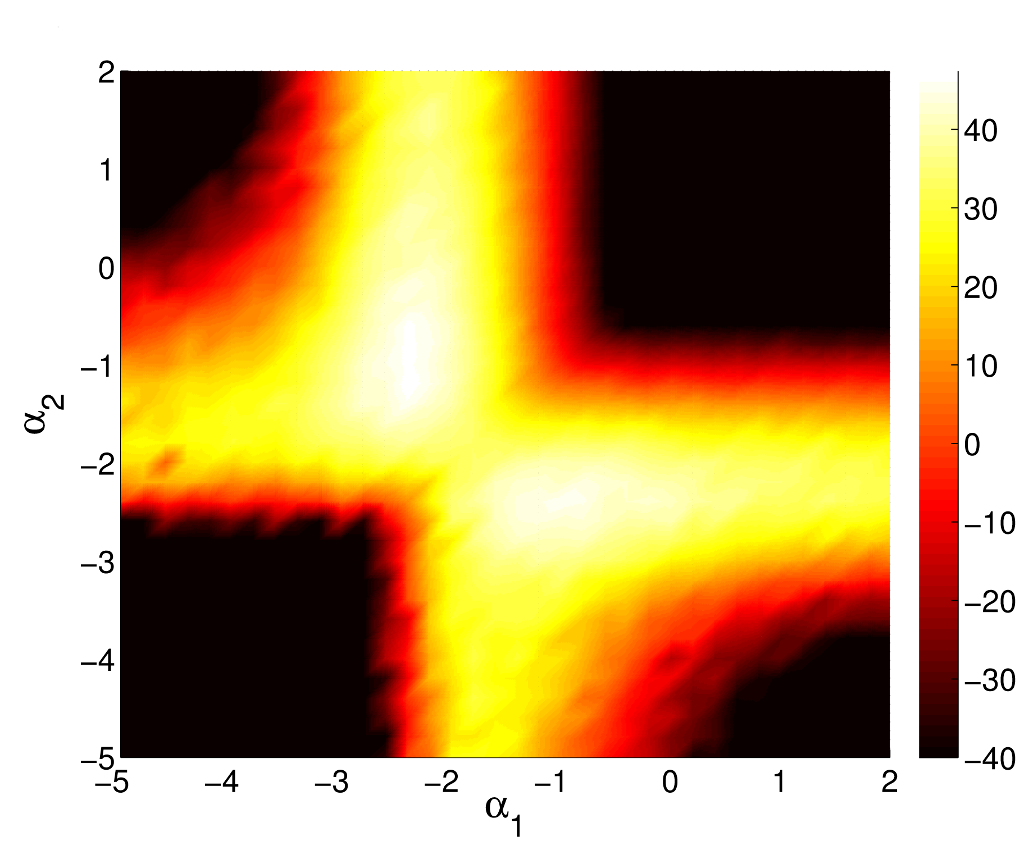

5.3 Sensitivity analysis with SMC

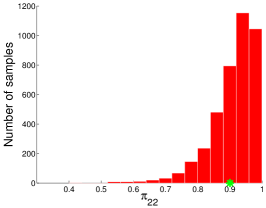

We now consider evaluating the sensitivity of the model with respect to the model parameters and . For a grid of values of those parameters, we report the estimated logarithm of the marginal likelihood using a sequential Monte Carlo algorithm.

The results are reported in Figure 10.

5.4 Bayesian inference with unknown parameters with the particle marginal Metropolis-Hastings

So far, we have assumed that the parameters , , and were fixed and known. We now consider that these variables have to be estimated as well. We consider the following prior on the parameters (Carvalho and Lopes, 2007):

| (7) |

where is the standard Gamma distribution of scale and rate , is the truncated normal distribution of mean and variance with support , and is the standard beta distribution with parameters and . Note that the prior on is essentially uniform. Figure 11 shows the representation of the full statistical model as a directed acyclic graph.

The Listing 2 provides the transcription of the statistical model defined by Equations (1) and (7) in \proglangBUGS language.

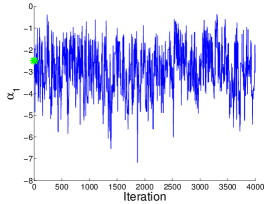

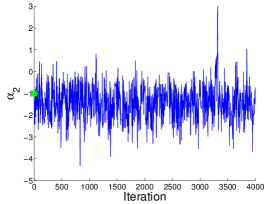

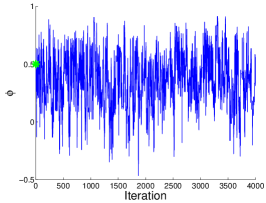

The user can then load the model and run a PMMH sampler to approximate the joint distribution of and given the data . The function \codebiips_pmmh_init creates a PMMH object. The input \codeparam_names contains the names of the variables to be updated using a Metropolis-Hastings proposal, here . Other variables are updated using a SMC algorithm. The input \codelatent_names specifies the other variables for which we want to obtain posterior samples. The function \codebiips_pmmh_update runs a PMMH with adaptation and burn-in iterations. During the adaptation phase, it learns the parameters of the proposal distribution in Algorithm 3.

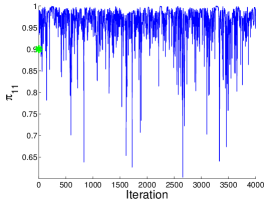

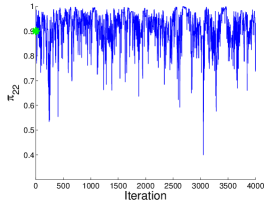

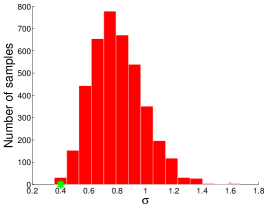

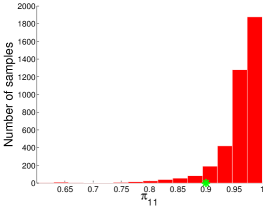

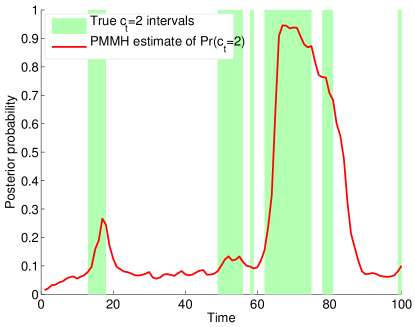

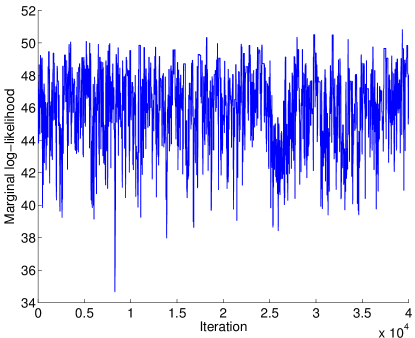

Posterior sample traces and histograms of the parameters are given in Figure 12. Posterior means and marginal posteriors for the variables and are given in Figures 13 and 14. The PMMH also returns an estimate of the logarithm of the marginal likelihood at each iteration. The algorithm can therefore also be used as a stochastic search algorithm for finding the marginal MAP of the parameters. The log-marginal likelihood is shown on Figure 15.

6 Example: Stochastic kinetic Lotka-Volterra model

We consider now Bayesian inference in the Lotka-Volterra model (Boys et al., 2008). This continuous-time Markov jump process describes the evolution of two species (prey) and at time , evolving according to the three reaction equations:

|

(8) |

where , and are the rate at which some reaction occur. Let be an infinitesimal interval. More precisely, the process evolves as

| (9a) | ||||

| (9b) | ||||

| (9c) | ||||

Forward simulation from the model (9) can be done using the Gillespie algorithm (Gillespie, 1977; Golightly and Gillespie, 2013). We additionally assume that we observe at some time the number of preys with some additive noise

| (10) |

The objective is to approximate the posterior distribution on the number of preys and predators at given the data . Listing 3 gives the transcription of the model defined by Equations (9) and (10) in the \proglangBUGS language.

The Gillespie sampler to sample from (9) is not part of the \proglangBUGS library of samplers. Nonetheless, \pkgBiips allows the user to add two sorts of external functions:

-

1.

Deterministic functions, with \codebiips_add_function. Such an external function is called after the symbol \code<- in \proglangBUGS, e.g. \codey <- f_ext_det(x)

-

2.

Sampling distributions, with the function \codebiips_add_distribution. Such an external sampler is called after the symbol \code in \proglangBUGS, e.g. \codez f_ext_samp(x)444Note that in the current version of \pkgBiips the variable \codez needs to be unobserved in order to use a custom distribution.

The function \code‘LV’ used in the Listing 3 is an additional sampler calling a \proglangMATLAB/\proglangR custom function to sample from the Lotka-Volterra model using the Gillepsie algorithm.

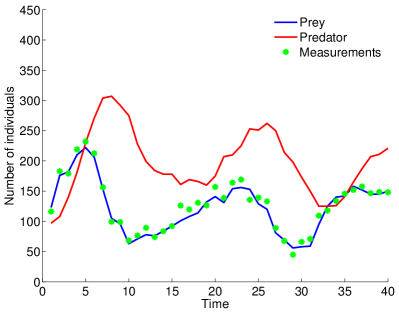

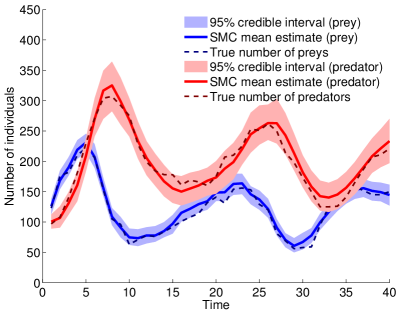

One can add the custom function \code‘LV’ to \pkgBiips, and run a SMC algorithm on the stochastic kinetic model in order to estimate the number of preys and predators. Estimates, together with the true numbers of prey and predators, are reported in Figure 16.

7 Discussion of related software

7.1 Related software for Bayesian inference using MCMC

Biips belongs to the \proglangBUGS language software family of \pkgWinBUGS, \pkgOpenBUGS (Lunn et al., 2000, 2012) and \pkgJAGS software (Plummer, 2003). All these probabilistic programming software use \proglangBUGS as a language for describing the statistical model.

In particular, \pkgBiips is written in \proglangC++ like \pkgJAGS but unlike \pkgWin/\pkgOpenBUGS which is written in \proglangComponent Pascal. This was a good reason for adapting \pkgJAGS implementation of the \proglangBUGS language which might slightly differ from the \pkgWin/\pkgOpenBUGS original one.

Like the above software, \pkgBiips compiles the model at runtime, by dynamically allocating instances of node classes. The resulting graphical model might have a substantial memory size. \pkgStan (Stan Development Team, 2013) is a similar software which uses another strategy. It translates the model description into \proglangC++ code that is transformed into an executable at compile-time. This might result in lower memory occupancy and faster execution, at the cost of a longer compilation. In addition, \pkgStan implements its own language for model definition. In particular, \pkgStan language is imperative as opposed to the declarative nature of \proglangBUGS.

The main difference between \pkgBiips and the aforementioned software is that \pkgBiips uses SMC instead of MCMC as inference algorithm.

7.2 Related software for Bayesian inference using SMC

SMCTC (Johansen, 2009) is a \proglangC++ template class library offering a generic framework for implementing SMC methods. It does not come with many features though and might require a lot of coding and understanding of SMC from the user. The development of \pkgBiips has started by adapting this library and providing it with more user-friendly features. This template is extended in \pkgvSMC (Zhou, 2013) to directly support parallelisation. \pkgRCppSMC (Eddelbuettel and Johansen, 2014) provides an \proglangR interface to \pkgSMCTC.

LibBi (Murray, 2013) is another similar software that implements SMC methods and is suited to parallel and distributed computer hardware such as multi-core CPUs, GPUs and clusters. \pkgLibBi comes with its own modeling language although restricting to the state-space model framework. Like \pkgStan, \pkgLibBi transforms the model definition into an executable at compile-time, resulting in high computing performances.

Other software such as \pkgVenture (Mansinghka et al., 2014) or \pkgAnglican (Wood et al., 2014) also propose particle MCMC inference engines for posterior inference, with a different probabilistic language, that allows for more expressiveness; in particular, it can deal with models of changing dimensions, complex control flow or stochastic recursion.

7.3 Related software for stochastic optimization

Although the focus of \pkgBiips is automatic Bayesian inference, interacting particle methods have long been successfully used for stochastic optimization. These algorithms use similar exploration/selection steps and are usually known under the names of evolutionary algorithms, genetic algorithms or meta-heuristics. Several softwares have been developed over the past few years, such as \pkgEASEA (Collet et al., 2000), \pkgEvolver555http://www.palisade.com/evolver/ or \pkgParadisEO (Cahon et al., 2004).

8 Conclusion

The \pkgBiips software is a \proglangBUGS compatible, black-box inference engine using sequential Monte Carlo methods. Due to its use of the \proglangBUGS language, and the ability to define custom functions/distributions, it allows a lot of flexibility in the development of statistical models. By using particle methods, the software can return estimates of the marginal likelihood at no additional cost, and can use custom conditional distributions, possibly with an intractable expression. Although particle methods are particularly suited to posterior inference on the two examples discussed in this paper, \pkgBiips running times are still higher than those of a more mature software with a MCMC inference engine such as \pkgJAGS. Nonetheless, there is room for improvement and optimization of \pkgBiips; in particular, particle algorithms are particularly suited to parallelization (Lee et al., 2010; Vergé et al., 2013; Murray, 2013), and we plan in future releases of the software to provide a parallel implementation of \pkgBiips.

Acknowledgement.

The authors thank Arnaud Doucet, Pierre Jacob, Adam Johansen and Frank Wood for useful feedback on earlier versions of the paper. François Caron acknowledges the support of the European Commission under the Marie Curie Intra-European Fellowship Programme.

References

- Andrieu et al. (2010) Andrieu C, Doucet A, Holenstein R (2010). “Particle Markov Chain Monte Carlo Methods.” Journal of the Royal Statistical Society B, 72, 269–342.

- Bouchard-Côté et al. (2012) Bouchard-Côté A, Sankararaman S, Jordan MI (2012). “Phylogenetic inference via sequential Monte Carlo.” Systematic biology, 61(4), 579–593.

- Boys et al. (2008) Boys RJ, Wilkinson DJ, Kirkwood TBL (2008). “Bayesian Inference for a Discretely Observed Stochastic Kinetic Model.” Statistics and Computing, 18(2), 125–135.

- Buckland et al. (2007) Buckland ST, Newman KB, Fernandez C, Thomas L, Harwood J (2007). “Embedding population dynamics models in inference.” Statistical Science, pp. 44–58.

- Cahon et al. (2004) Cahon S, Melab N, Talbi EG (2004). “\pkgParadisEO: A Framework for the Reusable Design of Parallel and Distributed Metaheuristics.” Journal of Heuristics, 10(3), 357–380.

- Cappé et al. (2005) Cappé O, Moulines E, Ryden T (2005). Inference in Hidden Markov Models. Springer.

- Cappé and Robert (2000) Cappé O, Robert C (2000). “Markov Chain Monte Carlo: 10 years and Still Running!” Journal of the American Statistical Association, 95, 1282–1286.

- Caron et al. (2008) Caron F, Davy M, Doucet A, Duflos E, Vanheeghe P (2008). “Bayesian Inference for Linear Dynamic Models with Dirichlet Process Mixtures.” IEEE Transactions on Signal Processing, 56(1), 71–84.

- Caron et al. (2007) Caron F, Davy M, Duflos E, Vanheeghe P (2007). “Particle filtering for multisensor data fusion with switching observation models: Application to land vehicle positioning.” IEEE Transactions on Signal Processing, 55(6), 2703–2719.

- Caron et al. (2012) Caron F, Doucet A, Gottardo R (2012). “On-line Changepoint Detection and Parameter Estimation with Application to Genomic Data.” Statistics and Computing, 22(2), 579–595.

- Carvalho and Lopes (2007) Carvalho CM, Lopes HF (2007). “Simulation-based Sequential Analysis of Markov Switching Stochastic Volatility Models.” Computational Statistics & Data Analysis, 51(9), 4526–4542.

- Cauchemez et al. (2008) Cauchemez S, Valleron AJ, Boelle P, Flahault, Ferguson NM (2008). “Estimating the impact of school closure on influenza transmission from Sentinel data.” Nature, 452(7188), 750–754.

- Collet et al. (2000) Collet P, Lutton E, Schoenauer M, Louchet J (2000). “Take it \pkgEASEA.” In Parallel Problem Solving from Nature PPSN VI, pp. 891–901. Springer.

- Del Moral (2004) Del Moral P (2004). Feynman-Kac Formulae. Genealogical and Interacting Particle Systems with Application. Springer.

- Del Moral (2013) Del Moral P (2013). Mean Field Simulation for Monte Carlo Integration. Chapman and Hall/CRC.

- Del Moral et al. (2012) Del Moral P, Peters GW, Vergé C (2012). “An introduction to particle integration methods: with applications to risk and insurance.” In Monte Carlo and Quasi-Monte Carlo Methods. Springer-Verlag.

- Donnet and Samson (2011) Donnet S, Samson A (2011). “EM algorithm coupled with particle filter for maximum likelihood parameter estimation of stochastic differential mixed-effects models.” Technical report.

- Douc et al. (2014) Douc R, Moulines E, Stoffer DS (2014). Nonlinear Time Series. CRC Press.

- Doucet et al. (2001) Doucet A, de Freitas N, Gordon N (eds.) (2001). Sequential Monte Carlo Methods in Practice. Springer-Verlag.

- Doucet et al. (2000) Doucet A, Godsill S, Andrieu C (2000). “On Sequential Monte Carlo Sampling Methods for Bayesian Filtering.” Statistics and Computing, 10(3), 197–208.

- Doucet and Johansen (2011) Doucet A, Johansen A (2011). “A Tutorial on Particle Filtering and Smoothing: Fifteen Years Later.” In D Crisan, B Rozovsky (eds.), Oxford Handbook of Nonlinear Filtering. Oxford University Press.

- Dureau et al. (2013) Dureau J, Kalogeropoulos K, Baguelin M (2013). “Capturing the time-varying drivers of an epidemic using stochastic dynamical systems.” Biostatistics, p. kxs052.

- Eddelbuettel (2013) Eddelbuettel D (2013). Seamless \proglangR and \proglangC++ Integration with \pkgRcpp. Springer, New York. ISBN 978-1-4614-6867-7.

- Eddelbuettel and François (2011) Eddelbuettel D, François R (2011). “\pkgRcpp: Seamless \proglangR and \proglangC++ Integration.” Journal of Statistical Software, 40(8), 1–18. URL http://www.jstatsoft.org/v40/i08/.

- Eddelbuettel and Johansen (2014) Eddelbuettel D, Johansen AM (2014). \pkgRcppSMC: \pkgRcpp bindings for Sequential Monte Carlo. \proglangR package version 0.1.4.

- Fearnhead (2004) Fearnhead P (2004). “Particle Filters for Mixture Models with an Unknown Number of Components.” Statistics and Computing, 14(1), 11–21.

- Fearnhead and Liu (2007) Fearnhead P, Liu Z (2007). “On-line Inference for Multiple Changepoint Problems.” Journal of the Royal Statistical Society B, 69(4), 589–605.

- Fernández-Villaverde and Rubio-Ramírez (2007) Fernández-Villaverde J, Rubio-Ramírez JF (2007). “Estimating macroeconomic models: A likelihood approach.” The Review of Economic Studies, 74(4), 1059–1087.

- Flury and Shephard (2011) Flury T, Shephard N (2011). “Bayesian inference based only on simulated likelihood: particle filter analysis of dynamic economic models.” Econometric Theory, 27(05), 933–956.

- Gilks et al. (1995) Gilks W, Richardson S, Spiegelhalter D (eds.) (1995). Markov Chain Monte Carlo in Practice. Chapman & Hall/CRC.

- Gilks et al. (1994) Gilks W, Thomas A, Spiegelhalter D (1994). “A Language and Program for Complex Bayesian Modelling.” The Statistician, 43, 169–177.

- Gillespie (1977) Gillespie DT (1977). “Exact Stochastic Simulation of Coupled Chemical Reactions.” The journal of physical chemistry, 81(25), 2340–2361.

- Golightly and Gillespie (2013) Golightly A, Gillespie CS (2013). “Simulation of Stochastic Kinetic Models.” In In Silico Systems Biology, pp. 169–187. Springer.

- Golightly and Wilkinson (2006) Golightly A, Wilkinson D (2006). “Bayesian sequential inference for stochastic kinetic biochemical network models.” Journal of Computational Biology, 13(3), 838–851.

- Golightly and Wilkinson (2011) Golightly A, Wilkinson D (2011). “Bayesian parameter inference for stochastic biochemical network models using particle Markov chain Monte Carlo.” Interface Focus, p. rsfs20110047.

- Green et al. (2003) Green PJ, Hjort NL, Richardson S (eds.) (2003). Highly Structured Stochastic Systems. Oxford University Press.

- Gustafsson et al. (2002) Gustafsson F, Gunnarsson F, Bergman N, Forssell U, Jansson J, Karlsson R, Nordlund PJ (2002). “Particle filters for positioning, navigation, and tracking.” IEEE Transactions on Signal Processing, 50(2), 425–437.

- Johansen (2009) Johansen A (2009). “\pkgSMCTC: Sequential Monte Carlo in \proglangC++.” Journal of Statistical Software, 30, 1–41.

- Jordan (2004) Jordan MI (2004). “Graphical Models.” Statistical Science, 19, 140–155.

- Lauritzen (1996) Lauritzen S (1996). Graphical Models. Oxford Science Publications.

- Lee et al. (2010) Lee A, Yau C, Giles MB, Doucet A, Holmes CC (2010). “On the Utility of Graphics Cards to Perform Massively Parallel Simulation of Advanced Monte Carlo Methods.” Journal of Computational and Graphical Statistics, 19(4), 769–789.

- Liu (2001) Liu J (2001). Monte Carlo Strategies in Scientific Computing. Springer.

- Lunn et al. (2012) Lunn D, Jackson C, Best N, Thomas A, Spiegelhalter D (2012). The \pkgBUGS Book: A Practical Introduction to Bayesian Analysis. CRC Press/ Chapman and Hall.

- Lunn et al. (2000) Lunn D, Thomas A, Best N, Spiegelhalter D (2000). “\pkgWinBUGS - a Bayesian Modelling Framework: Concepts, Structure and Extensibility.” Statistics and Computing, 10, 325–337.

- Mansinghka et al. (2014) Mansinghka VK, Selsam D, Perov YN (2014). “\pkgVenture: A Higher-order Probabilistic Programming Platform with Programmable Inference.” Technical report, arXiv:1404.0099.

- Murray (2013) Murray L (2013). “Bayesian State-Space Modelling on High-Performance Hardware Using \pkgLibBi.” Technical report, CSIRO. Arxiv:1306.3277.

- Naesseth et al. (2014) Naesseth CA, Lindsten F, Schön TB (2014). “Sequential Monte Carlo for Graphical Models.” In Advances in Neural Information Processing Systems (NIPS).

- Peters et al. (2010) Peters GW, Hosack GR, Hayes KR (2010). “Ecological non-linear state space model selection via adaptive particle Markov chain Monte Carlo (AdPMCMC).” arXiv preprint arXiv:1005.2238.

- Pitt and Shephard (1999) Pitt M, Shephard N (1999). “Filtering via simulation: Auxiliary particle filters.” Journal of the American statistical association, 94(446), 590–599.

- Plummer (2003) Plummer M (2003). “\pkgJAGS: A Program for Analysis of Bayesian Graphical Models using Gibbs Sampling.” In Proceedings of the 3rd International Workshop on Distributed Statistical Computing.

- Plummer (2012) Plummer M (2012). \pkgJAGS Version 3.3.0 user manual.

- Plummer (2014) Plummer M (2014). \pkgrjags: Bayesian graphical models using MCMC. \proglangR package version 3-13, URL http://CRAN.R-project.org/package=rjags.

- Ristic et al. (2004) Ristic B, Arulampalam S, Gordon N (2004). Beyond the Kalman filter: Particle filters for tracking applications, volume 685. Artech house Boston.

- Robert and Casella (2004) Robert C, Casella G (2004). Monte Carlo Statistical Methods. Springer.

- Stan Development Team (2013) Stan Development Team (2013). “\pkgStan: A \proglangC++ Library for Probability and Sampling, Version 2.1.” URL http://mc-stan.org/.

- Thrun et al. (2001) Thrun S, Fox D, Burgard W, Dellaert F (2001). “Robust Monte Carlo localization for mobile robots.” Artificial intelligence, 128(1), 99–141.

- Vergé et al. (2013) Vergé C, Dubarry C, Del Moral P, Moulines E (2013). “On Parallel Implementation of Sequential Monte Carlo Methods: The Island Particle Model.” Statistics and Computing, to appear.

- Vermaak et al. (2002) Vermaak J, Andrieu C, Doucet A, Godsill SJ (2002). “Particle methods for Bayesian modeling and enhancement of speech signals.” IEEE Transactions on Speech and Audio Processing, 10(3), 173–185.

- Vo et al. (2003) Vo BN, Singh S, Doucet A (2003). “Sequential Monte Carlo implementation of the PHD filter for multi-target tracking.” In Proc. International Conference on Information Fusion, pp. 792–799.

- Wood et al. (2014) Wood F, van de Meent JW, Mansinghka V (2014). “A New Approach to Probabilistic Programming Inference.” In Proceedings of the 17th International conference on Artificial Intelligence and Statistics.

- Zhou (2013) Zhou Y (2013). “\pkgvSMC: Parallel Sequential Monte Carlo in \proglangC++.” Technical report, University of Warwick. ArXiv:1306.5583.