Optimal switching for pairs trading rule:

a viscosity solutions approach

Minh-Man NGO

John von Neumann (JVN) Institute

Vietnam National University

Ho-Chi-Minh City,

man.ngo at jvn.edu.vn

Huyên PHAM

Laboratoire de Probabilités et

Modèles Aléatoires, CNRS UMR 7599

Université Paris 7 Diderot,

CREST-ENSAE,

and JVN Institute

pham at math.univ-paris-diderot.fr

Abstract

This paper studies the problem of determining the optimal cut-off for pairs trading rules. We consider two correlated assets whose spread is modelled by a mean-reverting process with stochastic volatility, and

the optimal pair trading rule is formulated as an optimal switching problem between three regimes: flat position (no holding stocks), long one short the other and short one long the other. A fixed

commission cost is charged with each transaction. We use a viscosity solutions approach to prove the existence and the explicit characterization of cut-off points via the resolution of quasi-algebraic equations. We illustrate our results by numerical simulations.

Pairs trading consists of taking simultaneously a long position in one of the assets and , and

a short position in the other, in order to eliminate the market beta risk, and be exposed only to relative market movements determined by the spread. A brief history and discussion of pairs trading can be found in Ehrman [7], Vidyamurthy [18] and Elliott, Van der Hoek and Malcom [9]. The main aim of this paper is to rationale mathematically these rules and find optimal cutoffs, by means of a stochastic control approach.

Pairs trading problem has been studied by stochastic control approach in the recent years. Mudchanatongsuk, Primbs and Wong [13] consider self-financing portfolio strategy for pairs trading,

model the log-relationship between a pair of stock prices by an Ornstein-Uhlenbeck process and use this to formulate a portfolio optimization and obtain the optimal solution to this control problem in closed

form via the corresponding Hamilton-Jacobi-Bellman (HJB) equation. They only allow positions that are short one stock and long the other, in equal dollar amounts. Tourin and Yan [17] study the same problem, but allow strategies with arbitrary amounts in each stock. On the other hand, instead of using self-financing strategies, one can focus on determining the optimal cut-offs, i.e. the boundaries of the trading regions in which one should trade when the spread lies in. Such problem is closely related to optimal buy-sell rule in trading mean reverting asset. Zhang and Zhang [19] studied optimal buy-sell rule, where they model the underlying asset price by an Ornstein-Uhlenbeck process and consider an optimal trading rule determined by two regimes: buy and sell. These regimes are defined by two threshold levels, and a fixed commission cost is charged with each transaction.

They use classical verification approach to find the value function as solution to the associated HJB equations (quasi-variational inequalities), and the optimal thresholds are obtained by smooth-fit technique. The same problem is studied in Kong’s PhD thesis [10], but he considers trading rules with three aspects: buying, selling and shorting. Song and Zhang [16] use the same approach for determining optimal pairs trading thresholds, where they model the difference of the stock prices and by an Ornstein-Uhlenbeck process and consider an optimal pairs trading rule determined by two regimes: long short and flat position (no holding stocks).

Leung and Li [11] studied the optimal timing to open or close the position subject to transaction costs, and the effect of Stop-loss level under the Ornstein-Uhlenbeck (OU) model. They directly construct the

value functions instead of using variational inequalities approach, by characterizing the value functions as the smallest concave majorant of reward function.

In this paper, we consider a pairs trading problem as in Song and Zhang [16], but differ in our model setting and resolution method. We consider two correlated assets whose spread is modelled by a more general mean-reverting process with stochastic volatility, and the optimal pairs trading rule is based on optimal switching between three regimes: flat position (no holding stocks), long one short the other and vice-versa. A fixed commission cost is charged with each transaction. We use a viscosity solutions approach to solve our optimal switching problem. Actually, by combining viscosity solutions approach, smooth fit properties and uniqueness result for viscosity solutions proved in Pham, Ly Vath and Zhou [15], we are able to derive directly the structure of the switching regions, and thus the form of our value functions.

This contrasts with the classical verification approach where the structure of the solution should be guessed ad-hoc, and one has to check that it satisfies indeed the corresponding HJB equation, which is not trivial in this context of optimal switching with more than two regimes.

The paper is organized as follows. We formulate in Section 2 the pairs trading as an optimal switching problem with three regimes.

In Section 3, we state the system of variational inequalities satisfied by the value functions in the viscosity sense and the definition of pairs trading regimes.

In Section 4, we state some useful properties on the switching regions, derive the form of value functions, and obtain optimal cutoff points by relying on the smooth-fit properties of value functions. In Section 5, we illustrate our results by numerical examples.

2 Pair trading problem

Let us consider the spread between two correlated assets, say and modelled by a mean-reverting process with boundaries , and :

(2.1)

where is a standard Brownian motion on , and are positive constants, is a Lipschitz function on , satisfying

the nondegeneracy condition . The SDE (2.1) admits then a unique strong solution, given an initial condition , denoted .

We assume that is a natural boundary, is a natural boundary, and is non attainable.

The main examples are the Ornstein-Uhlenbeck (OU in short) process or the inhomogenous geometric Brownian motion (IGBM), as studied in detail in the next sections.

Suppose that the investor starts with a flat position in both assets. When the spread widens far from the equilibrium point, she naturally opens her trade by

buying the underpriced asset, and selling the overpriced one. Next, if the spread narrows, she closes her trades, thus generating a profit.

Such trading rules are quite popular in practice among hedge funds managers with cutoff values determined empirically by descriptive statistics.

The main aim of this paper is to rationale mathematically these rules and find optimal cutoffs, by means of a stochastic control approach. More precisely, we

formulate the pairs trading problem as an optimal switching problem with three regimes. Let be the set of regimes where

corresponds to a flat position (no stock holding), denotes a long position in the spread corresponding to a purchase of and a sale of , while

is a short position in (i.e. sell and buy ). At any time, the investor can decide to open her trade by switching from regime to (open to sell) or (open to buy). Moreover, when the investor is in a long ( ) or short position ( ), she can decide to close her position by switching to regime .

We also assume that it is not possible for the investor to switch directly from regime to , and vice-versa, without first closing

her position.

The trading strategies of the investor are modelled by a switching control where is a nondecreasing sequence of stopping times representing the trading times, with a.s. when goes to infinity, and valued in , -measurable, represents the position regime decided at until the next trading time. By misuse of notations, we denote by the value of the regime at any time :

which also represents the inventory value in the spread at any time.

We denote by the trading gain when switching from a position to , , , for a spread value . The switching gain functions are given by:

where is a fixed transaction fee paid at each trading time. Notice that we do not consider the functions and since it is not possible to switch

from regime to and vice-versa. By misuse of notations, we also set .

Given an initial spread value , the expected reward over an infinite horizon associated to a switching trading strategy

is given by the gain functional:

The first (discrete sum) term corresponds to the (discounted with discount factor ) cumulated gain of the investor by using pairs trading strategies, while the last integral term reduces the inventory risk, by penalizing with a factor ,

the holding of assets during the trading time interval.

For , let denote the value functions with initial positions when maximizing over switching trading strategies the gain functional, that is

where denotes the set of switching controls with initial position , i.e.

, . The impossibility of switching directly from regime to is formalized by restricting the strategy of position :

if or then for ensuring that the investor has to close first her position before opening a new one.

3 PDE characterization

Throughout the paper, we denote by the infinitesimal generator of the diffusion process , i.e.

The ordinary differential equation of second order

(3.1)

has two linearly independent positive solutions. These solutions are uniquely determined (up to a multiplication), if we require one of them to be strictly

increasing, and the other to be strictly decreasing. We shall denote by the increasing solution, and by the decreasing solution. They are called fundamental solutions of (3.1), and any other solution can be expressed as their linear combination.

Since is a natural boundary, and is either a natural or non attainable boundary, we have:

(3.2)

We shall also assume that

(3.3)

Canonical examples Our two basic examples in finance for satisfying the above assumptions are

•

Ornstein-Uhlenbeck (OU) process:

(3.4)

with , positive constants. In this case, , are natural boundaries, the two fundamental solutions to (3.1) are given by

and it is easily checked that condition (3.3) is satisfied.

•

Inhomogeneous Geometric Brownian Motion (IGBM):

(3.5)

where , and are positive constants. In this case, is a natural boundary, is a non attainable boundary, and the two fundamental solutions to (3.1) are given by

(3.6)

where

(3.7)

and and are the confluent hypergeometric functions of the first and second kind. Moreover, by the asymptotic property of the confluent hypergeometric functions (see [1]),

the fundamental solutions and satisfy condition (3.3), and

(3.8)

In this section, we state some general PDE characterization of the value functions by means of the dynamic programming approach.

We first state a linear growth property and Lipschitz continuity of the value functions.

Lemma 3.1

There exists some positive constant (depending on ) such that for a discount factor , the value functions are finite on . In this case, we have

and

for some positive constant .

Proof. The lower bound for and are trivial by considering the strategies of doing nothing.

Let us focus on the upper bound. First, by standard arguments using Itô’s formula and Gronwall lemma, we have the following estimate on the diffusion : there exists some positive constant , depending on

the Lipschitz constant of , such that

(3.9)

(3.10)

for some positive constant depending on , and .

Next, for two successive trading times and

corresponding to a buy-and-sell or sell-and-buy strategy, we have:

where the second inequality follows from Itô’s formula. When investor is staying in flat position , in the first trading time investor can move to state or , and in the second trading time she has to back to state . So that, the strategy when we stay in state can be expressed by the combination of infinite couples: buy-and-sell, sell-and-buy, for example: states it means: buy-and-sell, sell-and-buy, sell-and-buy, buy-and-sell,….

We deduce from (3) that for any ,

Recalling that, when investor starts with a long or short position ( ) she has to close first her position before opening a new one, so that

for or ,

which proves the upper bound for by using the estimate (3.9).

By the same argument, for two successive trading times and

corresponding to a buy-and-sell or sell-and-buy strategy, we have:

where the second inequality follows from Itô’s formula. We deduce that

which proves the Lipschitz property for by using the estimate (3.10).

In the sequel, we fix a discount factor so that the value functions are well-defined and finite, and satisfy the linear growth and Lipschitz estimates of Lemma 3.1.

The dynamic programming equations satisfied by the value functions are thus given by a system of variational inequalities:

(3.12)

(3.13)

(3.14)

Indeed, the equation for means that in regime , the investor has the choice to stay in the flat position, or to open by a long or short position in the spread, while the equation for , , means that in the regime ,

she has first the obligation to close her position hence to switch to regime before opening a new position.

By the same argument as in [14], we know that the value functions are viscosity solutions to the system

(3.12)-(3.13)-(3.14), and satisfied the smooth-fit condition.

Let us introduce the switching regions:

•

Open-to-trade region from the flat position :

where is the open-to-buy region, and is the open-to-sell region:

•

Sell-to-close region from the long position :

•

Buy-to-close region from the short position :

and the continuation regions, defined as the complement sets of the switching regions:

4 Solution

In this section, we focus on the existence and structure of switching regions, and then we use the results on smooth fit property, uniqueness result for viscosity solutions of the value functions to derive the form of value functions in which the optimal cut-off points can be obtained by solving smooth-fit condition equations.

Lemma 4.1

where

Proof.

Let , so that . By writing that is a viscosity supersolution to:

, we then get

(4.1)

Now, since , this implies that , so that

. Since satisfies the equation on , we then have from (4.1)

Recalling the expressions of and , we thus obtain:

, which proves the inclusion result for .

Similar arguments show that if then

which proves the inclusion result for after direct calculation.

Similarly, if then or : if , we obviously have the inclusion result for . On the other hand, if , using the viscosity supersolution property of , we have:

which yields the inclusion result for . By the same method, we shows the inclusion result for .

We next examine some sufficient conditions under which the switching regions are not empty.

Lemma 4.2

(1) The switching regions and are always not empty.

(2)

(i)

If , then is not empty

(ii)

If , and , then .

(3) If , then is not empty.

Proof. (1) We argue by contradiction, and first assume that . This means that once we are in the long position, it would be never optimal to close our position. In other words, the value function would be equal to given by

Since , this would imply , for all , which obviously contradicts the nonnegativity of the value function .

Suppose now that . Then, from the inclusion results for in Lemma 4.1, this implies that the continuation region would contain at least the interval

. In other words, we should have:

on , and so should be in the form:

for some constants and . In view of the linear growth condition on and condition (3.3) when goes to ,

we must have .

On the other hand, since , and recalling the lower bound on in Lemma 3.1, this would imply:

By sending to , and from (3.2), we get the contradiction.

(2) Suppose that . Then, a similar argument as in the case , would imply that , for all

. This immediately leads to a contradiction when by sending to . When , and under the condition that ,

we also get a contradiction to the non negativity of .

(3) Consider the case when , and let us argue by contradiction by assuming that . Then, from the inclusion results for in Lemma 4.1, this implies that the continuation region would contain at least the interval . In other words, we should have:

on , and so should be in the form:

for some constants and . In view of the linear growth condition on and condition (3.3) when goes to ,

we must have . On the other hand, since , recalling the lower bound on in Lemma 3.1, this would imply:

By sending to , and from (3.2), we get the contradiction.

Remark 4.1

Lemma 4.2 shows that is non empty. Furthermore, notice that in the case where , can be equal to

the whole domain , i.e. it is never optimal to stay in the long position regime. Actually, from Lemma 4.1, such extreme case may occur only if

, in which case, we would also get , and thus . In that case, we are reduced to a

problem with only two regimes and .

The above Lemma 4.2 left open the question whether is empty when and , and whether

is empty or not when .

We examine this last issue in the next Lemma and the following remarks.

Lemma 4.3

Let be governed by the Inhomogeneous Geometric Brownian motion in (3.5), and set

where , and are defined in (• ‣ 3). If there exists (resp ) such that

(resp. ) , then (resp. ) is not empty.

Proof. Suppose that . Then, from the inclusion results for in Lemma 4.1, this implies that the continuation region

would contain at least the interval . In other words, we should have:

on , and so should be in the form:

for some constants and . From the bounds on in Lemma 3.1, and (3.2), we must have .

Next, for , let us consider the first passage time of the inhomogeneous Geometric Brownian motion. We know from [20] that

(4.2)

We denote by the gain functional obtained from the strategy consisting in changing position from initial state and regime

, to the regime at the first time hits (), and then following optimal decisions once in regime :

By sending to zero, and recalling (3.6) and (3.8), this yields

Therefore, under the condition that there exists such that

, we would get:

which is in contradiction with the fact that we have: , and so: .

Suppose that , in this case .

By the same argument as the above case, we have

by (4.2).

By sending to zero, and recalling (3.6) and (3.8), we thus have

(4.3)

Therefore, under the condition that there exists such that

, we would get:

which is in contradiction with the fact that we have: , and so: .

Remark 4.2

The above Lemma 4.3 gives a sufficient condition in terms of the function and , which ensures that and are not empty. Let us discuss how it is satisfied. From the asymptotic property of the confluent hypergeometric functions, we have: . Then by sending to infinity (recall that ), and from the expression of and in Lemma 4.3, we have:

This implies that for large enough, one can choose so that . Notice also that

is nondecreasing with as a consequence of the fact that . In practice, one can check by numerical method the condition for .

For example, with , , , , , and , we have

, and .

Similarly, for large enough, one can find such that ensuring that is not empty.

We are now able to describe the complete structure of the switching regions.

Proposition 4.1

1) There exist finite cutoff levels , , , such that

and satisfying , ,

, .

Moreover, , i.e. and , i.e.

.

2) We have , and i.e. the following inclusions hold:

Proof. 1) (i) We focus on the structure of the sets and , and consider first the case where they are not empty.

Let us then set , which is finite

since is not empty, and is included in by Lemma

4.1. Moreover, since is included in , it does not intersect with , and so

for , i.e. . From (3.12), we deduce that is a viscosity solution to

(4.4)

Let us now prove that . To this end, we consider the function on . Let us check that

is a viscosity supersolution to

(4.5)

For this, take some point , and some smooth test function such that is a local minimum of . Then, is a local minimum

of by definition of . By writing the viscosity supersolution property of to: , at with the test function

, we get:

since . This proves the viscosity supersolution property (4.5), and actually, by recalling that

,

is a viscosity solution to

(4.6)

Moreover, since lies in the closed set , we have . By uniqueness

of viscosity solutions to (4.4), we deduce that on , i.e. .

In the case where is empty, which may arise only when (recall Lemma 4.2), then it can still be written in the above form

by choosing .

By similar arguments, we show that when is not empty, it should be in the form: ,

for some , while when it is empty, which may arise only when (recall Lemma 4.2), it can be written also in this form by choosing .

(ii) We derive similarly the structure of and which are already known to be non empty (recall Lemma 4.2):

we set , which lies in since is included in

by Lemma 4.1. Then, we observe that is a viscosity solution to

(4.7)

By considering the function , we show by the same arguments as in (4.6) that is also a viscosity solution to (4.7) with

boundary condition . We conclude by uniqueness that on , i.e.

. The same arguments show that is in the form stated in the Proposition.

2) We only consider the case where , since the inclusion result in this proposition is obviously obtained when

from the above forms of the switching regions.

Let us introduce the function on . On , we see that and are smooth , and satisfy:

which combined with the viscosity supersolution property of , gives

At we have and so that , which means . By the same way, at we also have , which means

. By the comparison principle, we deduce that

Let us assume on the contrary that . We have and , so that , leading to a contradiction. By the same argument, it is impossible to have , which ends the proof.

Remark 4.3

Consider the situation where . We distinguish the following cases:

(i)

. Then, we know from Lemma 4.2 that . Moreover, for small enough, namely

, we see from Proposition 4.1 that and thus .

(ii)

. Then , and for small enough namely,

, we see from Proposition 4.1 that , and thus and .

The next result shows a symmetry property on the switching regions and value functions.

Proposition 4.2

(Symmetry property)

In the case , and if is an even function and , then , and

Proof. Consider the process , which follows the dynamics:

where is still a Brownian motion on the same probability measure and filtration of , and we can see that .

We consider the same optimal problem, but we use instead of , we denote

For , let denote the value functions with initial positions when maximizing over switching trading strategies the gain functional, that is

For any , we see that , and so . Thus, , and since is arbitrary in ,

we get: . By the same argument, we have , and so ,

. Moreover, recalling that , we have:

In particular, we , so that

. Moreover, since , we notice that for all , . Thus,

, for all , which means that

. Recalling that , this shows that . By the same argument, we have .

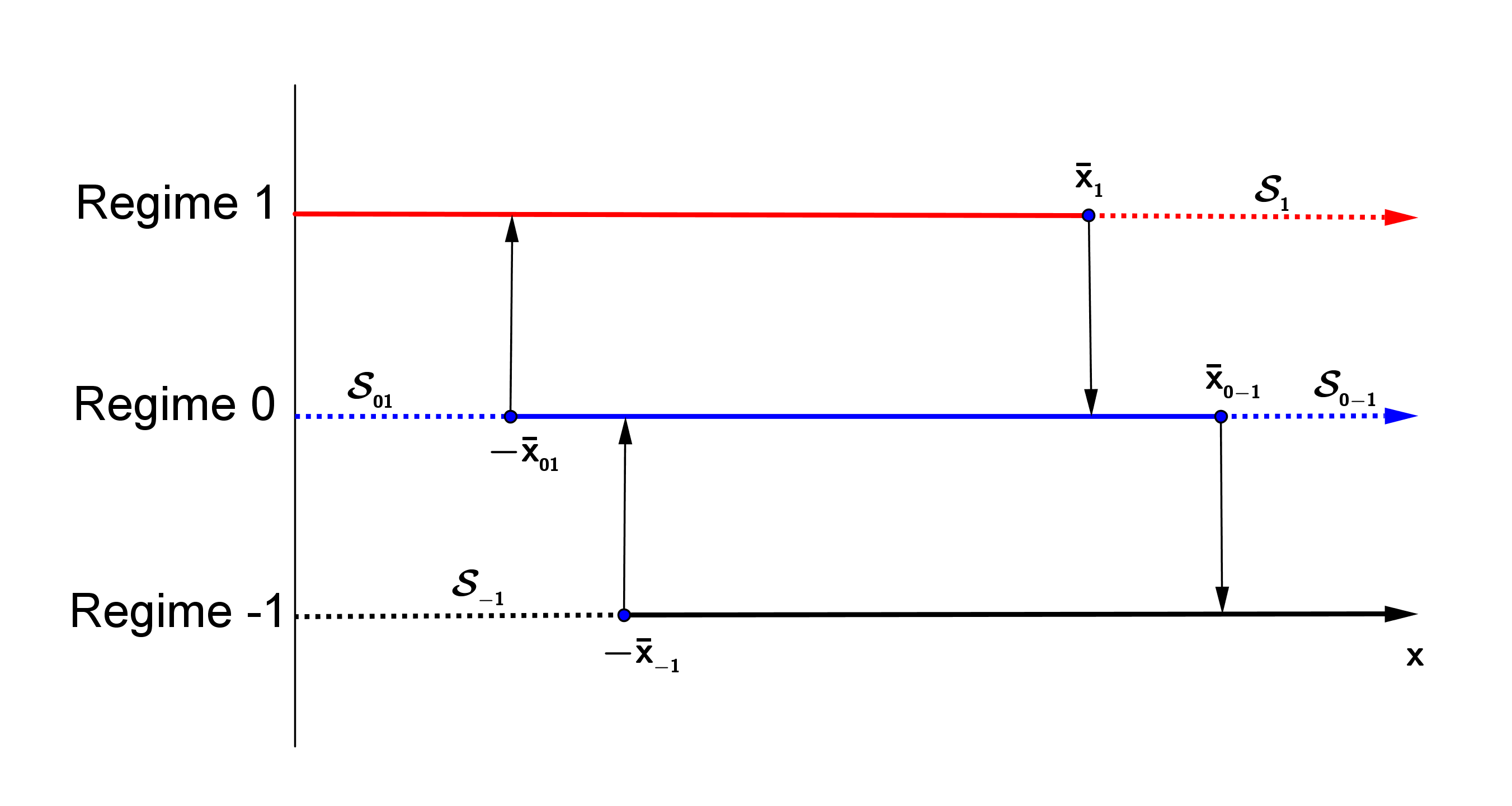

To sum up the above results, we have the following possible cases for the structure of the switching regions:

(1)

. In this case, the four switching regions , , and are not empty in the form

and are plotted in Figure 1. Moreover, when and is an even function, and .

(2)

. In this case, the switching regions and are not empty, in the form

for some , and by Proposition 4.1. However, and may be empty or not. More precisely, we have the three following possibilities:

(i)

and are not empty in the form:

for some by Proposition 4.1.

Such cases arises for example when is the IGBM (3.5) and for large enough, as showed in Lemma 4.3 and

Remark 4.2. The visualization of this case is the same as Figure 1.

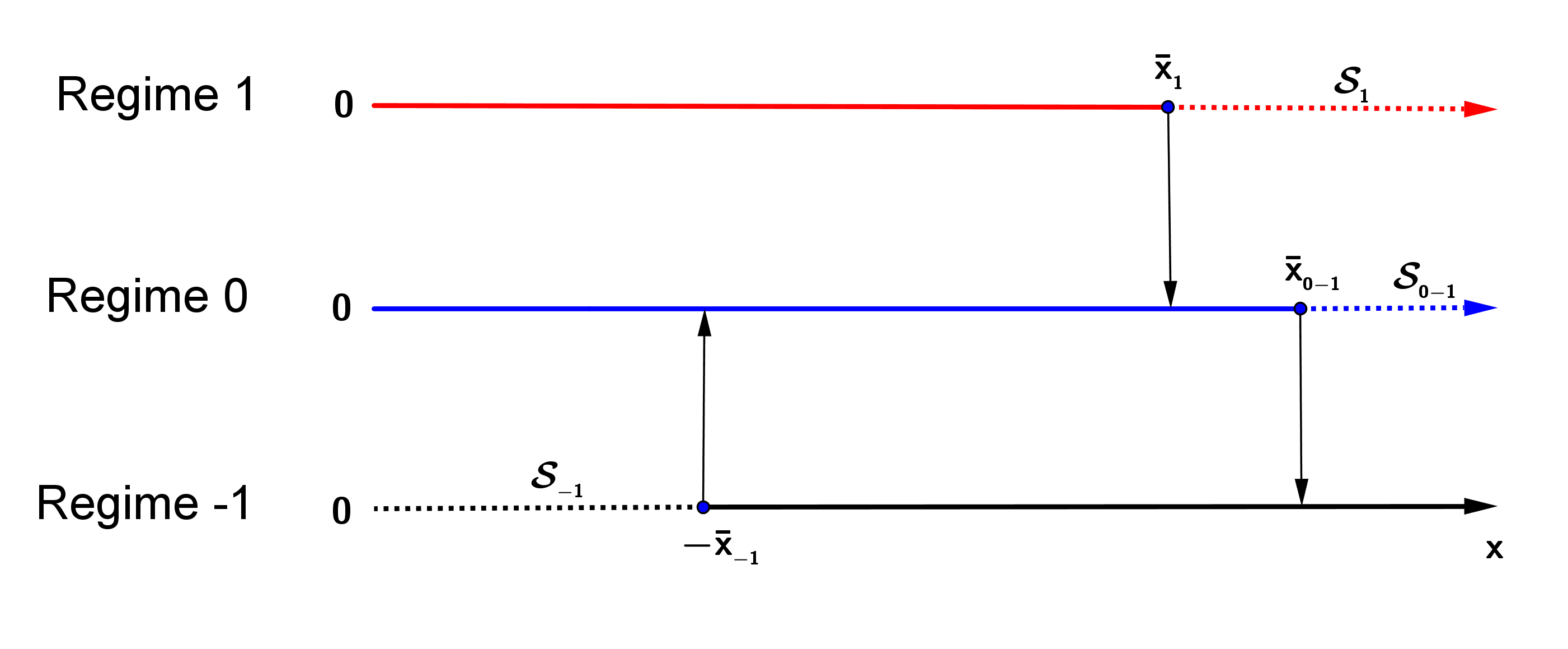

(ii)

is not empty in the form: for some by Proposition 4.1,

and . Such case arises when , and for , see Remark 4.3(i).

This is plotted in Figure 2.

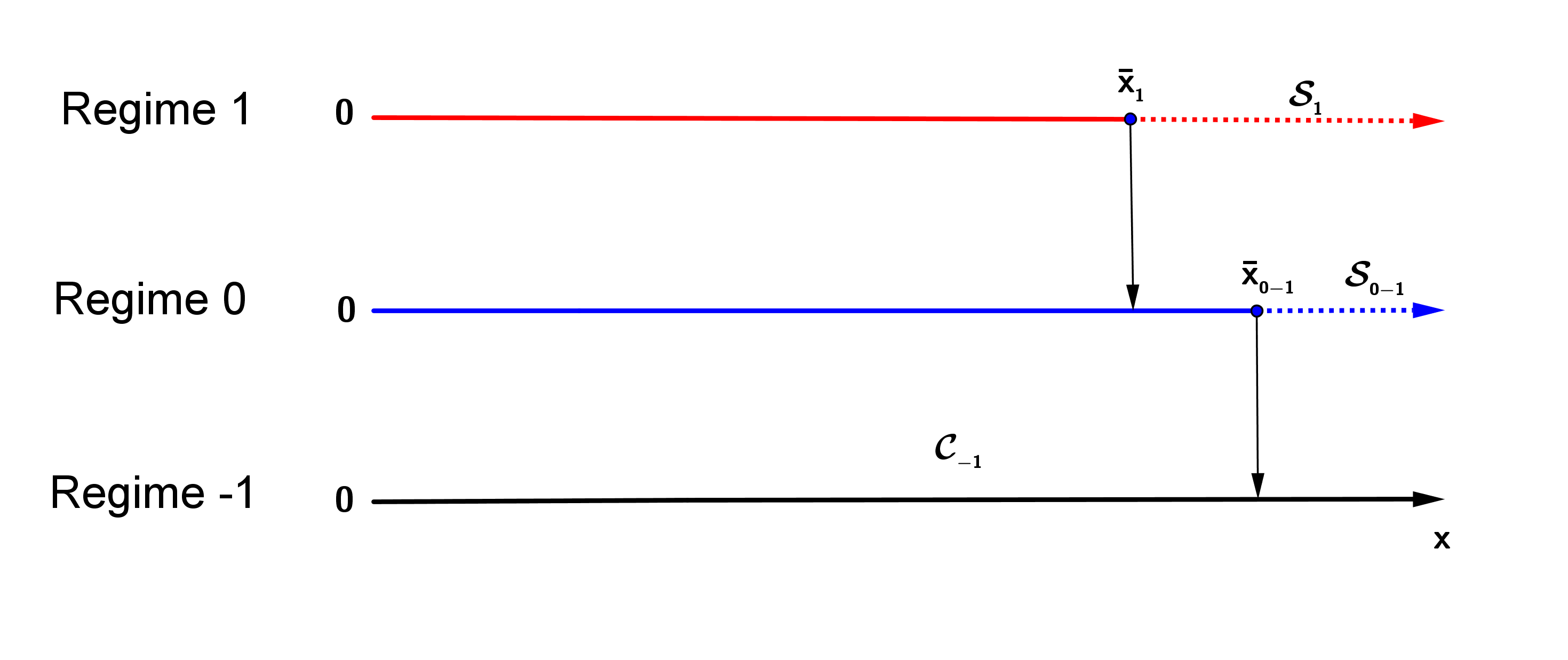

(iii)

Both and are empty. Such case arises

when , and for , see Remark 4.3(ii). This is plotted in Figure 3.

Moreover, notice that in such case, we must have by Lemma 4.2(2)(ii), and so by Proposition 4.1,

, i.e. .

Figure 1: Regimes switching regions in cases (1) and (2)(i).

Figure 2: Regimes switching regions in case (2)(ii).

Figure 3: Regimes switching regions in case (2)(iii).

The next result provides the explicit solution to the optimal switching problem.

Theorem 4.1

Case (1): . The value functions are given by

and the constants , , , , , ,

, are determined by the smooth-fit conditions:

Case (2)(i): , and both and are not empty. The value functions have the same form as Case (1) with the state space

domain .

Case (2)(ii): , is not empty, and .

The value functions are given by

and the constants , , , ,

, are determined by the smooth-fit conditions:

Case (2)(iii): , and .

The value functions are given by

and the constants , , , , are determined by the smooth-fit conditions:

Proof. We consider only case (1) and (2)(i) since the other cases are dealt with by similar arguments. We have

, which means that on . Moreover, is solution to

on , which combined with the bound in the Lemma 3.1, shows that should be in the form: on . Since , we deduce that

has the form expressed as: on . In the same way, should have the form expressed as on and has the form expressed as on .

We know that is solution to on so that should be in the form:

on . We have , which means that

on and , which means that on

.

From Proposition 4.1 we know that , and and by the smooth-fit property of value function we obtain the above smooth-fit condition equations in which we can compute the cut-off points by solving these quasi-algebraic equations.

Remark 4.4

1. In Case (1) and Case(2)(i) of Theorem 4.1, the smooth-fit conditions system is written as:

(4.28)

and

(4.42)

Denote by and the matrices:

Once and are nonsingular,

straightforward computations from (4.28) and (4.42) lead to the following equation satisfied by , ,

, :

This system can be separated into two independent systems:

(4.50)

(4.55)

and

(4.60)

(4.65)

We then obtain thresholds , , , by solving two quasi-algebraic system equations (4.50) and (4.60). Notice that for the examples of OU or IGBM process, the matrices

and are nonsingular so that their inverses are well-defined. Indeed, we have: and . This property is trivial for the case of OU process, while for the case of IGBM:

Thus, is strictly increasing since is strictly decreasing, and so . Moreover, we have:

Recalling that and (see Proposition 4.1), and since

is a strictly increasing and positive function, while

is a strictly decreasing positive function, we have: and , which implies the non singularity of the matrix

. On the other hand, we have:

Since is a strictly increasing positive function and is a strictly increasing function, with , we get:

and , which implies the non singularity of the matrix

.

2. In Case (2)(ii) of Theorem 4.1, we obtain the thresholds , from the smooth-fit conditions which lead to

the quasi-algebraic system:

(4.72)

(4.77)

The non singularity of the matrix above is checked similarly as in case (1) and (2)(i) for the examples of the OU or IGBM process. Note that , are independent from , which is obtained from the equation:

(4.78)

When , this means that .

3. In Case (2)(iii) of Theorem 4.1, the threshold is obtained from the equation (4.78), while the threshold

is derived from the smooth-fit condition leading to the quasi-algebraic equation:

(4.79)

5 Numerical examples

In this part, we consider OU process and IGBM as examples.

1.

We first consider the example of the Ornstein-Uhlenbeck process:

with , positive constants. In this case, the two fundamental solutions to (3.1) are given by

and satisfy assumption (3.3). We consider a numerical example with

the following specifications: :

, , , , , .

Remark 5.1

We can reduce the case of non zero long run mean of the OU process to the case of by considering process as spread process, because in this case is constant. Finally, we can see that, cutoff points translate along , as illustrated in figure 6.

We recall some notations:

is the open-to-buy region,

is the open-to-sell region,

is Sell-to-close region from the long position ,

is Buy-to-close region from the short position .

We solve the two systems (4.50) and (4.60) which give

and confirm the symmetry property in Proposition 4.2.

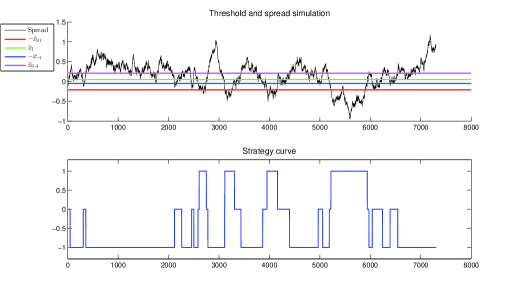

Figure 4: Simulation of trading strategies

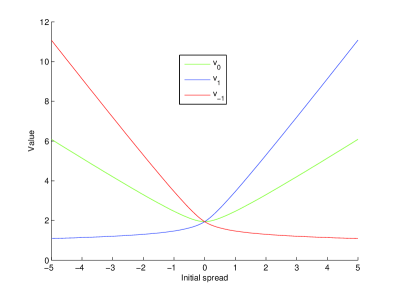

Figure 5: Value functions

In figure 5, we see the symmetry property of value functions as showed in Proposition 4.2.

Moreover, we can see that is a non decreasing function while is non increasing.

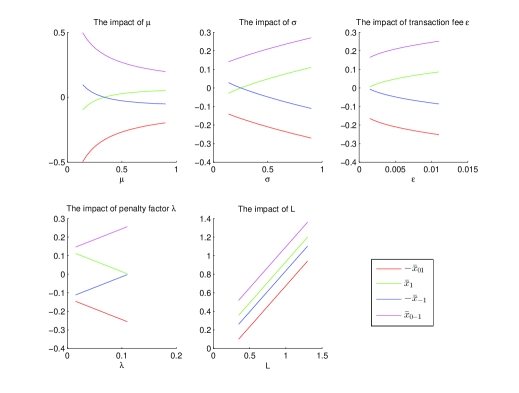

The next figure shows the dependence of cut-off point on parameters

Figure 6: The dependence of cut-off point on parameters

In figure 6, measures the speed of mean reversion and we see that the length of intervals , increases and the length of intervals

, decreases as gets bigger. The length of intervals , , , and decreases as volatility gets bigger. is the long run mean , to which the process tends to revert, and we see that the cutoff points translate along . We now look at the parameters that does not affect on the dynamic of spread: the length of intervals , , , and decreases as the transaction fee gets bigger. Finally, the length of intervals , decreases and the length of intervals

, increases as the penalty factor gets larger, which means that the holding time in flat position is longer and the opportunity to enter the flat position from the other position is bigger as the penalty factor is increasing.

2.

We now consider the example of Inhomogeneous Geometric Brownian Motions which has stochastic volatility, see more details in Zhao [20] :

where , and are positive constants. Recall that in this case, the two fundamental solutions to (3.1) are given by

where

and are the confluent hypergeometric functions of the first and second kind. We can easily check that is a monotone decreasing function, while

so that is a monotone increasing function. Moreover, by the asymptotic property of the confluent hypergeometric functions (cf.[1]), the fundamental solutions and satisfy the condition (3.3).

Case (2)(i): Both and are not empty.

Let us consider a numerical example with the following specifications: :

, , , , , and we set . Note that, in this case the condition in Lemma 4.3 is satisfied,

and we solve the two systems (4.50) and (4.60) which give

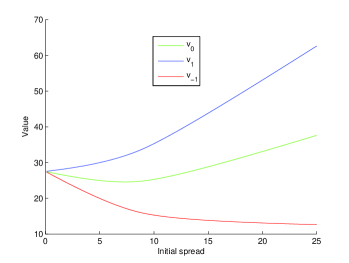

Figure 7: Value functions

In the figure 7, we can see that is non decreasing while is non increasing. Moreover, is always larger than , and .

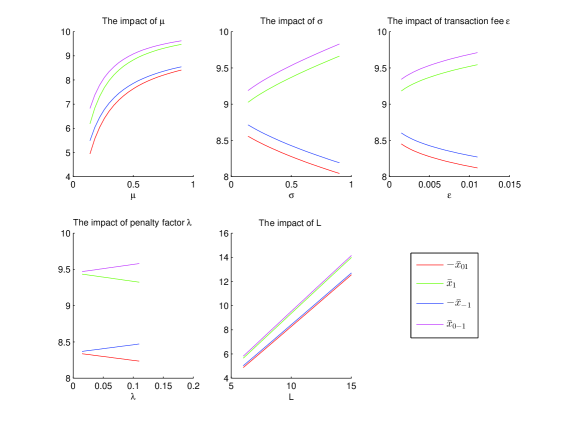

The next figure 8 shows the dependence of cut-off points on parameters (Note that the condition in Lemma 4.3 is satisfied for all parameters in this figure).

Figure 8: The dependence of cut-off point on parameters

We can make the same comments as in the case of the OU process, except for the dependence with respect to the long run mean .

Actually, we see that when increases, the moving of cutoff points is no more translational due to the non constant volatility.

Case (2)(ii): is empty.

Let us consider a numerical example with the following specifications: :

, , , , , and . We solve the two systems (4.72) and (4.78) which give

Case (2)(iii): Both and are empty.

Let us consider a numerical example with the following specifications: :

, , , , , and . The two equations (4.79) and (4.78) give

References

[1]

Abramowitz, M. and I. Stegun (1972): Handbook of mathematical functions: with formulas, graphs, and mathematical tables, Courier Dover Publications.

[2] Avellaneda, M. and J-H. Lee (2010): “Statistical arbitrage in the US equities market”, Quantitative Finance, 10, 761-782.

[3]

Bock, M. and R. Mestel (2009): “A regime-switching relative value arbitrage rule”, Operations Research Proceedings, 9-14, Springer.

[4]

Borodin, A. and P. Salminen (2002): Handbook of Brownian motion: facts and formulae, Springer.

[5]

Chen, Huafeng, Chen, Shaojun Jenny and F. Li (2012): “Empirical investigation of an equity pairs trading strategy”, preprint.

[6]

Do, B. and R. Faff (2010): “Does simple pairs trading still work?”, Financial Analysts Journal, 83-95.

[7]

Ehrman, D. (2006): The handbook of pairs trading: Strategies using equities, options, and futures, vol 240, John Wiley and Sons.

[8]

Ekstr m, E., Lindberg C. and J. Tysk (2011): “Optimal liquidation of a pairs trade”, Advanced mathematical methods for finance, Springer.

[9]

Elliott, R., Van der Hoek J. and W. Malcom (2005): “Pairs trading”, Quantitative Finance, vol 5, 271-276.

[10]

Kong, H. T. (2010): “Stochastic control and optimization of assets trading”, PhD thesis, University of Georgia.

[11]

Leung, T. and X. Li (2013): “Optimal Mean Reversion Trading with Transaction Costs and Stop-Loss Exit”, Social Science Research Network Working Paper Series.

[12]

Ly Vath, V. and H. Pham (2007): “Explicit solution to an optimal switching problem in the two-regime case”, SIAM Journal on Control and Optimization, vol 46, 395-426.

[13]

Mudchanatongsuk, S., Primbs J. and W. Wong (2008): “Optimal pairs trading: A stochastic control approach”, American Control Conference, IEEE, 2008.

[14]

Pham H. (2007): “On the smooth-fit property for one-dimensional optimal switching problem”, Séminaire de Probabilités XL, 187-199, Springer.

[15]

Pham, H., Ly Vath, V. and X.Y. Zhou (2009): “Optimal switching over multiple regimes”, SIAM Journal on Control and Optimization, vol 48, 2217-2253.

[17]

Tourin A. and R. Yan (2013): “Dynamic pairs trading using the stochastic control approach”, Journal of Economic Dynamics and Control, vol 37, 1972-1981.

[18]

Vidyamurthy, G. (2004): Pairs Trading: quantitative methods and analysis, John Wiley and Sons.

[19]

Zhang, H. and Q. Zhang (2008): “Trading a mean-reverting asset: Buy low and sell high”, Automatica, vol 44, 1511-1518.

[20]

Zhao B. (2009): “Inhomogeneous geometric Brownian motions”, Available at SSRN 1429449.