Limiting distributions

for explosive PAR(1) time series

with strongly mixing innovation

Dominique Dehay

111D. Dehay

Institut de Recherche Mathématique de Rennes, CNRS umr 6625,

Université de Rennes, France

e-mail :

dominique.dehay@uhb.fr

Abstract : This work deals with the limiting distribution of the least squares estimators of the coefficients of an explosive periodic autoregressive of order 1 (PAR(1)) time series when the innovation is strongly mixing. More precisely is a periodic sequence of real numbers with period and such that . The time series is periodically distributed with the same period and satisfies the strong mixing property, so the random variables can be correlated.

Keywords: Parameter estimation; Explosive autoregressive time series; Periodic models; Strong mixing.

M.S.C 2010: 62M10, 62M09.

1 Introduction

Many man-made signals and data, even natural ones, exhibit periodicities. The non-stationary and seasonal behavior is quite common for many random phenomena as rotating machinery in mechanics (see Antoni 2009), seasonal data in econometrics and climatology, but also signals in communication theory, biology to name a few (see e.g. Bloomfield et al. 1994; Chaari et al. 2014; Collet and Martinez 2008; Dragan et al. 1982; Franses and Paap 2004; Gardner et al. 2006; Serpedin et al. 2005; and references therein). Periodic autoregressive (PAR) models are one of the simplest linear models with a periodic structure. After more than fifty years of study these models and their generalizations (periodic ARMA (PARMA), etc.) remain a subject of investigations of great interest as they can be applied in modeling periodic phenomena for which seasonal ARIMA models do not fit adequatly (see e.g. Adams and Goodwin 1995; Bittanti and Colaneri 2009; Francq et al. 2011; Osborn et al. 1988).

It is well known that such linear models can be represented as vectorial autoregressive (VAR) models. However the general results known for VAR models do not take into account the whole periodic structure of the PARMA models (Basawa and Lund 2001; Tia and Grupe 1980) in particular the fact that the innovation can be periodically distributed. Thus specific methods have been developped for PAR and PARMA models.

There is a large amount of publications on the estimation problem for the coefficients of PARMA models essentially whenever the model is stable, that is periodic stationary also called cyclostationary (see e.g. Adams and Goodwin 1995; Aknouche and Bibi 2009; Basawa and Lund 2001; Francq et al. 2011; Pagano 1978; Tiao and Grupe 1980; Troutman 1979; Vecchia 1985). The unstable case has been also studied when some autoregressive coefficients are in the boundary of the periodic stationary domain (see e.g. Aknouche 2012a, 2012b; Aknouche and Al-Eid 2012; Boswijk and Franses 1995, 1996; Ghyshels and Osborn 2001 and references therein).

There are few results concerning explosive PAR model. Aknouche (2013) studies the case of explosive PAR models driven by a periodically distributed independent innovation. However the independence of the innovation is too stringent in practice (see e.g. Aknouche and Bibi 2009; Francq et al. 2011 and references therein).

In this work we relax the independence condition, and for simplicity of presentation, we consider periodic autoregressive of order 1 time series that is PAR(1) models. To state the convergence in distribution of the estimators (Theorems 1 and 2) we impose that the periodically distributed innovation is strongly mixing (see e.g. Bradley 2005). Thus it can be correlated and it satisfies some asymptotic independence between its past and its future (see condition (M) in Section 4). However there is no condition on the rate of the asymptotic independence. This is similar to what Phillips (1987) showed for the autoregressive time series with a unit root and constant coefficients.

Here we study the least squares estimators (LSE) of the PAR(1) coefficients, and the limiting distributions stated in Theorem 1 below generalize the results obtained by Monsour and Mikulski (1998) for explosive AR models with independent Gaussian innovation (see also Anderson 1959; Stigum 1974) and by Aknouche (2013) for explosive PAR models with independent innovation. The rate of convergence of the estimators depends on the product of the periodic PAR(1) coefficients of the PAR(1) model (Theorem 1). Actually this product determines whether the model is stable, unstable or explosive. Thus it is subject of great interest and we takle the problem of its estimation. For this purpose we consider two estimators : the product of the LSE of the PAR(1) coefficients (see (Aknouche 2013) for independent innovation), and a least squares estimator (Theorem 2). By simulation we detect no specific distinction between these estimators for the explosive PAR(1) models. The theoretical comparison of the limiting distributions of the two estimators is out of the scope of the paper and will be subject to another work.

The paper is organized as follows. In Section 2 the model under study is defined as well as the notations. Then the asymptotic behaviour as of the scaled vector-valued time series is stated in Section 3 where is the product of the periodic coefficients of the explosive PAR(1) model, thus . The period is . Section 4 deals with the consistency of the least squares estimators of the PAR coefficients , , as well as the limiting distributions of the scaled errors , as . Next in Section 5 we consider the problem of estimation of the product . The asymptotic behaviour of the estimators introduced in this paper are illustrated by simulation in Section 6. For an easier reading and understanding of the statements of the paper, the proofs of the results are presented in Appendix.

2 Background : PAR(1) time series

Consider the following PAR(1) model

| (1) |

where is a periodic sequence of real numbers and is a real-valued periodically distributed sequence of centered random variables defined on some underlying probability space . We assume that the periods of and of have the same value . Thus and for all integers and . To be short, in the sequel the sequence is called innovation of the model although it is not necessarily uncorrelated. Denote

and let . Since is periodic with period , we have and we obtain the decomposition

| (2) |

where

and for

Note that the sequence is strictly stationary (stationarily distributed).

If , the model is stable and converges in distribution to some random variable as . If , the model is unstable : its behaviour is similar to a random walk; indeed for each , the time series is a random walk when the innovation is independent with respect to the random variable .

Henceforth we assume that the time series satisfies the PAR(1) equation (1) with . We also assume that the initial random variable is square integrable. Moreover the innovation is centered periodically distributed with second order moments. Thus is periodically correlated (see Hurd et al. 2002) and we have as well as

for all integers , , and . Denote and .

3 Explosive asymptotic behaviour of the model

In the forthcoming proposition we study the asymptotic behaviour of the time series . Recall that we assume that .

Proposition 1

For any

where

Moreover

Remarks

1) Assume that , then conditionally that , the sequence converges to infinity almost surely as . Thus conditionally that , the paths of the time series are explosive.

2) When almost surely, the time series which follows the PAR(1) model with , is periodically distributed and satisfies the following stable PAR(1) equation

where is some periodically distributed time series. More precisely

The estimation problem of the coefficients of such a PAR equation is now well-known, see e.g. (Acknouche and Bibi 2009; Basawa and Lund 2001; Francq et al. 2011 and references therein).

3) To state the convergence in quadratic mean in Proposition 1 we can easily replace the assumption that the innovation is periodically distributed by the less stringent one that the innovation is periodically correlated.

4) When the innovation is uncorrelated and periodically distributed we obtain that

with .

4 Least squares estimation of the coefficients

Now we deal with the estimation problem of the coefficients , from the observation , , as . For that purpose we determine the periodic sequence that minimizes the sum of the squared errors

Since , for , and , the least squares estimator (LSE) of is defined by

where from expression (2) we can write

| (3) |

and

| (4) |

Here .

Note that under Gaussian and independence assumptions on the periodically distributed innovation , the LSE coincides with the maximum likelihood estimator of .

To prove the convergence in distribution of the scaled errors in the following results we use the next strong mixing condition. The notion of strong mixing, also called -mixing, was introduced by Rosenblatt (1956) and it is largely used for modeling the asymptotic independence in time series. The condition could be weakened using the notion of weak dependence, but this is out of the scope of the paper. For more information about mixing time series and weak dependence see e.g. (Bradley 2005; Dedeker et al. 2007; Doukhan 1994 and references therein).

(M) where the supremum being taken over all and all sets , and . Here the -fields and are defined by and .

Furthermore, in the following we assume that the underlying probability space is sufficiently large so that there is a sequence of real valued random variables which is independent with respect to and the innovation , and such that for any integer . This is always possible at least by enlarging the probability space.

Now we state the strong consistency of the LSE of , as well as the asymptotic limiting distribution of the scaled error for the explosive PAR(1) model (1).

Theorem 1

Conditionally that , the least squares estimator converges to almost surely as , for . Furthermore assume that and the mixing condition (M) is fulfilled, then the random vector of the scaled errors converges in distribution to

as . The random variable is defined in Proposition 1, the random vector is independent with respect to , and its distribution is defined by

where the sequence is independent with respect to and , and such that for any integer .

Note that in general the limiting distribution of is not parameter free, that is, it depends on the parameters we are estimating. Under Gaussian assumption on the periodically distributed innovation , the random variables and are Gaussian and independent, so the distribution of ratio is a Cauchy distribution (see also Aknouche 2013). In fact, the limiting distributions in Theorem 1 have heavy tails.

5 Estimation of

To estimate , the product of the coefficients , , we can consider the product of the estimators :

Then from Theorem 1, the estimator converges almost surely to conditionally that . Thanks to the Delta-method (Theorem 3.1, Van der Vaart 1998) we readily deduce the asymptotic law of the normalized error .

when we assume that and the mixing condition (M) is fulfilled. See (Aknouche 2013) for independent innovation.

Besides, we can define a least squares estimator of . For that purpose, note that from relation (1) and the periodicity of the coefficients, we obtain for all and , that where

Since the innovation is periodically distributed with the same period , the sequence is strictly stationary (stationarily distributed). Then minimizing the sum of the squared errors

we define the least squares estimator as

where

Then following the same arguments as for the LSE , we can state the forthcoming result.

Theorem 2

Conditionally that , the least squares estimator converges to almost surely. Assume that and the mixing condition (M) is fulfilled, then the scaled error converges in distribution

| (5) |

conditionally that , as . Here is a random variable independent with respect to and . The distribution of coincides with the distribution of

In the next section we see by simulation that the distributions of and of seem to be similar when . The theoretical comparison of these distributions is out of the scope of the paper.

6 Simulation

Here we present the simulations of some explosive PAR(1) time series, and we illustrate the behaviour of the LSE , and of for different values of the coefficients , and for different types of innovation. For that purpose we consider the PAR(1) model (1) with period . The periodic coefficients s are given in Table 1.

| family 1 | 0.8 | 1.2 | 1 | 1.5 | 1.1 | 0.9 | 1.4256 |

|---|---|---|---|---|---|---|---|

| family 2 | 0.8 | 1.1 | 1 | 1.5 | 1.1 | 0.7 | 1.0164 |

| family 3 | 0.5 | 1 | 1 | 2.5 | 1.6 | 0.5 | 1 |

| family 4 | 0.5 | 1 | 1.5 | 1.62 | 1.6 | 0.5 | 0.972 |

Thus we simulate the cases , close to 1, and . The innovation is defined by

the random variables , , are independent and identically distributed, and . When , we have , , and the random variables are periodically distributed and independent. When , the random variables are periodically distributed and correlated. Actually they are -dependent, thus strongly mixing. We consider two distributions for the s : the standard normal distribution , and the uniform distribution . Hence in the last case the distribution of the s is spread out.

To sum up, for each family of coefficients, we obtain four PAR(1) time series that we simulate with different lengths . In each case we perform 100 replications. The algorithm of the simulation is implemented in ’R’ software code. Below we present some of the tables and histograms that we obtain to compare the results.

| parameter | 0.8 | 1.2 | 1 | 1.5 | 1.1 | 0.9 | 1.4256 | |

|---|---|---|---|---|---|---|---|---|

| estimate | ||||||||

| mean | 0.8001 | 1.1999 | 0.9999 | 1.4999 | 1.0999 | 0.9000 | 1.4257 | 1.4256 |

| median | 0.8000 | 1.1999 | 1.0000 | 1.4999 | 1.0999 | 0.9000 | 1.4256 | 1.4255 |

| error | ||||||||

| mean | 2e-04 | -4e-05 | -2e-06 | -8e-05 | -1e-05 | 7e-06 | 2e-04 | 9e-05 |

| sigma | 2e-03 | 4e-04 | 8e-06 | 8e-04 | 9e-05 | 9e-05 | 3e-03 | 2e-03 |

| boxplot | ||||||||

| u. whisker | 8e-04 | 2e-04 | 8e-07 | 4e-04 | 6e-05 | 6e-05 | 9e-04 | 8e-04 |

| u. hinge | 3e-04 | 5e-05 | 3e-07 | 9e-05 | 2e-05 | 2e-05 | 3e-04 | 3e-14 |

| l. hinge | -2e-04 | -7e-05 | -4e-07 | -2e-04 | -2e-05 | -2e-05 | -2e-04 | -2e-04 |

| l. whisker | 8e-04 | -2e-04 | -9e-07 | -5e-04 | -6e-05 | -5e-05 | -7e-04 | -8e-04 |

| percentile | ||||||||

| abs 0.95 | 4e-03 | 1e-03 | 7e-06 | 2e-03 | 3e-04 | 3e-04 | 4e-03 | 4e-03 |

| parameter | 0.8 | 1.1 | 1 | 1.5 | 1.1 | 0.7 | 1.0164 | |

|---|---|---|---|---|---|---|---|---|

| estimate | ||||||||

| mean | 0.7965 | 1.0996 | 0.9999 | 1.4986 | 1.0999 | 0.7000 | 1.0131 | 1.0107 |

| median | 0.7994 | 1.0999 | 1.0000 | 1.4999 | 1.1000 | 0.6999 | 1.0158 | 1.0154 |

| error | ||||||||

| mean | -4e-03 | -4e-04 | -3e-05 | -2e-03 | -4e-05 | 4e-05 | -4e-03 | -6e-03 |

| sigma | 1e-02 | 2e-03 | 2e-04 | 7e-03 | 5e-04 | 1e-03 | 9e-03 | 3e-02 |

| boxplot | ||||||||

| u. whisker | 4e-03 | 4e-04 | 2e-05 | 2e-03 | 3e-04 | 9e-04 | 4e-03 | 3e-03 |

| u. hinge | 2e-04 | 5e-05 | 5e-06 | 4e-04 | 8e-05 | 3e-04 | 2e-04 | -5e-05 |

| l. hinge | -3e-03 | -3e-04 | -4e-06 | -1e-03 | -9e-05 | -3e-04 | -3e-03 | -2e-03 |

| l. whisker | -5e-03 | -6e-04 | -2e-05 | -3e-03 | -4e-04 | -8e-04 | -5e-04 | -7e-03 |

| percentile | ||||||||

| abs 0.95 | 3e-02 | 3e-03 | 4e-04 | 9e-03 | 7e-04 | 2e-03 | 3e-02 | 5e-02 |

| parameter | 0.8 | 1.1 | 1 | 1.5 | 1.1 | 0.7 | 1.0164 | |

|---|---|---|---|---|---|---|---|---|

| estimate | ||||||||

| mean | 0.7999 | 1.1000 | 1.0000 | 1.5000 | 1.1000 | 0.6999 | 1.0163 | 1.0163 |

| median | 0.8000 | 1.0999 | 1.0000 | 1.4999 | 1.0999 | 0.7000 | 1.0164 | 1.0164 |

| error | ||||||||

| mean | -8e-05 | 4e-07 | 4e-07 | 5e-06 | 2e-06 | -8e-06 | -7e-05 | -1e-04 |

| sigma | 7e-04 | 5e-05 | 3e-06 | 3e-04 | 4e-05 | 1e-04 | 7e-04 | 9e-04 |

| boxplot | ||||||||

| u. whisker | 2e-04 | 2e-05 | 2e-08 | 8e-05 | 2e-05 | 3e-05 | 2e-04 | 2e-04 |

| u. hinge | 5e-05 | 3e-06 | 5e-09 | 2e-05 | 2e-06 | 2e-05 | 5e-05 | 5e-05 |

| l. hinge | -4e-05 | -8e-06 | -6e-09 | -4e-05 | -4e-06 | -6e-06 | -4e-05 | -5e-05 |

| l. whisker | -2e-04 | -2e-05 | -2e-08 | -7e-05 | -2e-05 | -3e-05 | -2e-04 | -2e-04 |

| percentile | ||||||||

| abs 0.95 | 7e-04 | 8e-05 | 2e-06 | 4e-04 | 5e-05 | 2e-04 | 7e-04 | 8e-04 |

| parameter | 0.8 | 1.1 | 1 | 1.5 | 1.1 | 0.7 | 1.0164 | |

|---|---|---|---|---|---|---|---|---|

| estimate | ||||||||

| mean | 0.7999 | 1.1000 | 1.0000 | 1.5000 | 1.1000 | 0.6999 | 1.0163 | 1.0163 |

| median | 0.7999 | 1.1000 | 1.0000 | 1.5000 | 1.1000 | 0.6999 | 1.0163 | 1.0163 |

| error | ||||||||

| mean | -8e-05 | 9e-06 | -3e-10 | 5e-05 | 6e-06 | -2e-05 | -8e-05 | -8e-05 |

| sigma | 7e-04 | 9e-05 | 2e-09 | 4e-04 | 5e-05 | 2e-04 | 7e-04 | 7e-04 |

| boxplot | ||||||||

| u. whisker | 2e-04 | 3e-05 | 5e-12 | 2e-04 | 2e-05 | 5e-05 | 2e-04 | 2e-04 |

| u. hinge | 5e-05 | 9e-06 | -2e-12 | 4e-05 | 6e-06 | 2e-05 | 5e-05 | 5e-05 |

| l. hinge | -7e-05 | -7e-06 | -2e-11 | -3e-05 | -4e-06 | -2e-05 | -7e-05 | -7e-05 |

| l. whisker | -2e-04 | -3e-05 | -4e-11 | -2e-04 | -2e-05 | -5e-05 | -3e-04 | -3e-04 |

| percentile | ||||||||

| abs 0.95 | 9e-04 | 2e-04 | 5e-10 | 5e-04 | 7e-05 | 2e-04 | 9e-04 | 9e-04 |

| parameter | 0.8 | 1.1 | 1 | 1.5 | 1.1 | 0.7 | 1.0164 | |

|---|---|---|---|---|---|---|---|---|

| estimate | ||||||||

| mean | 0.7991 | 1.0998 | 1.0000 | 1.4996 | 1.0999 | 0.7000 | 1.0156 | 1.0150 |

| median | 0.7999 | 1.1000 | 1.0000 | 1.5000 | 1.1000 | 0.7000 | 1.0163 | 1.0163 |

| error | ||||||||

| mean | -9e-04 | -2e-04 | 1e-06 | -4e-04 | -2e-05 | 2e-05 | -8e-04 | -2e-03 |

| sigma | 6e-03 | 8e-04 | 2e-05 | 3e-03 | 1e-04 | 2e-04 | 6e-03 | 1e-02 |

| boxplot | ||||||||

| u. whisker | 2e-04 | 3e-05 | 4e-08 | 2e-04 | 2e-05 | 4e-05 | 2e-04 | 2e-04 |

| u. hinge | 4e-05 | 8e-06 | 1e-08 | 4e-05 | 5e-06 | 9e-06 | 4e-05 | 4e-05 |

| l. hinge | -8e-05 | -6e-06 | -4e-10 | -3e-05 | -4e-06 | -2e-05 | -8e-05 | -8e-05 |

| l. whisker | -3e-04 | -3e-05 | -4e-05 | -2e-04 | -2e-05 | -4e-05 | -3e-04 | -3e-04 |

| percentile | ||||||||

| abs 0.95 | 6e-04 | 1e-04 | 7e-06 | 4e-04 | 6e-05 | 2e-04 | 6e-04 | 7e-04 |

| parameter | 0.5 | 1 | 1 | 2.5 | 1.6 | 0.5 | 1 | |

|---|---|---|---|---|---|---|---|---|

| estimate | ||||||||

| mean | 0.4948 | 1.0000 | 1.0000 | 2.4372 | 1.5972 | 0.5004 | 0.9944 | 0.9644 |

| median | 0.4973 | 1.0000 | 1.0000 | 2.4566 | 1.5978 | 0.5002 | 0.9972 | 0.9765 |

| error | ||||||||

| mean | -5e-03 | -2e-06 | 1e-05 | -6e-02 | -2e-03 | 4e-03 | -6e-03 | 4e-02 |

| sigma | 9e-03 | 2e-04 | 4e-04 | 6e-02 | 3e-03 | 6e-04 | 9e-03 | 4e-02 |

| boxplot | ||||||||

| u. whisker | 4e-03 | 8e-05 | 4e-04 | -8e-03 | -4e-04 | 2e-03 | 5e-03 | 2e-03 |

| u. hinge | -4e-04 | 2e-05 | 8e-05 | -3e-02 | -2e-03 | 8e-04 | -5e-04 | -2e-02 |

| l. hinge | -9e-03 | -2e-05 | -9e-05 | -8e-02 | -4e-03 | 4e-05 | -1e-02 | -5e-02 |

| l. whisker | -2e-02 | -8e-05 | -4e-04 | -2e-01 | -7e-03 | -1e-03 | -3e-02 | -1e-01 |

| percentile | ||||||||

| abs 0.95 | 3e-03 | 5e-04 | 9e-04 | 3e-01 | 8e-03 | 2e-03 | 3e-02 | 2e-01 |

| parameter | 0.5 | 1 | 1.5 | 1.62 | 1.6 | 0.5 | 0.972 | |

|---|---|---|---|---|---|---|---|---|

| estimate | ||||||||

| mean | 0.4938 | 1.0000 | 1.3983 | 1.5579 | 1.5765 | 0.5071 | 0.9662 | 0.8612 |

| median | 0.4971 | 1.0000 | 1.4055 | 1.5624 | 1.5777 | 0.5072 | 0.9693 | 0.8745 |

| error | ||||||||

| mean | -7e-03 | 5e-06 | -2e-01 | -7e-02 | -3e-02 | 8e-03 | -6e-03 | -2e-01 |

| sigma | 2e-02 | 5e-04 | 3e-02 | 2e-02 | 4e-03 | 1e-03 | 2e-02 | 6e-02 |

| boxplot | ||||||||

| u. whisker | 2e-02 | 5e-04 | -6e-02 | -4e-02 | -2e-02 | 9e-03 | 2e-02 | -3e-02 |

| u. hinge | 3e-03 | 2e-04 | -9e-02 | -6e-02 | -3e-02 | 8e-03 | 4e-03 | -8e-02 |

| l. hinge | -2e-02 | -2e-04 | -2e-01 | -8e-02 | -3e-02 | 7e-03 | -2e-02 | -2e-01 |

| l. whisker | -4e-02 | -5e-04 | -2e-01 | -1e-01 | -4e-02 | 7e-03 | -3e-02 | -2e-01 |

| percentile | ||||||||

| abs 0.95 | 3e-02 | 2e-03 | 2e-01 | 1e-01 | 4e-02 | 9e-03 | 3e-02 | 2e-01 |

In each table we write down the mean and the median of the values of each estimator that we have obtained from the 100 replications, as well as some box-plot characteristics of the errors : extrem of upper whishers, upper hinge (3rd quarter), lower hinge (1rt quarter) and extrem of the lower whishers. We also give the 95% percentiles of the absolute values of the errors.

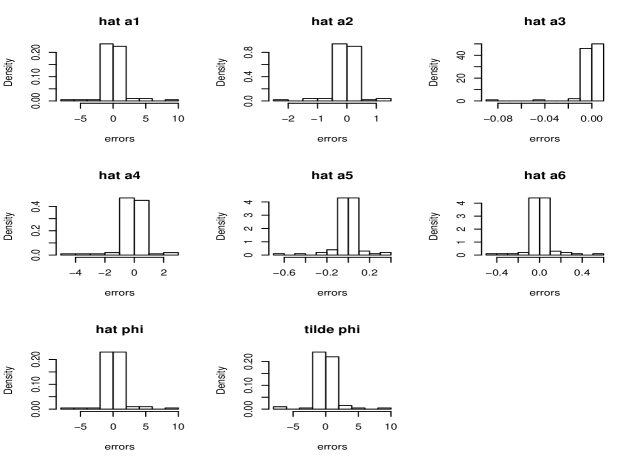

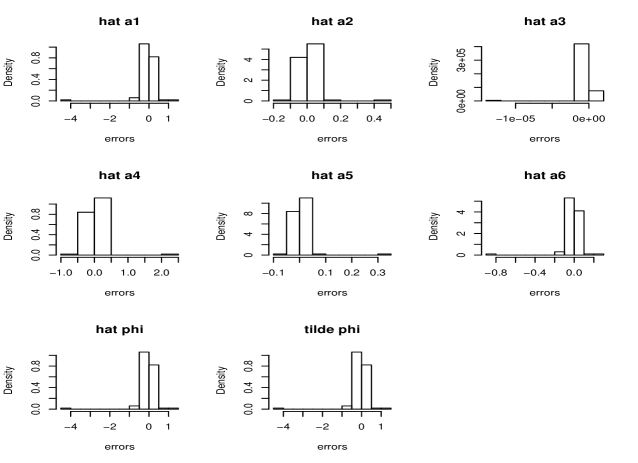

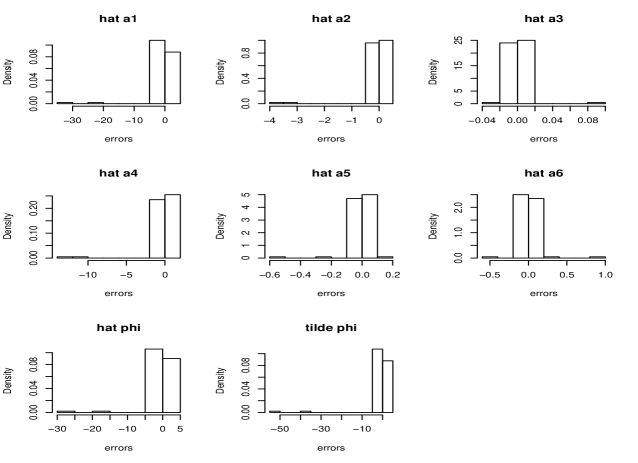

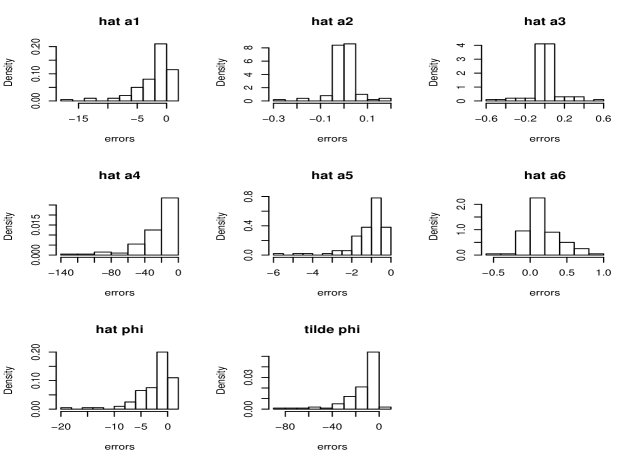

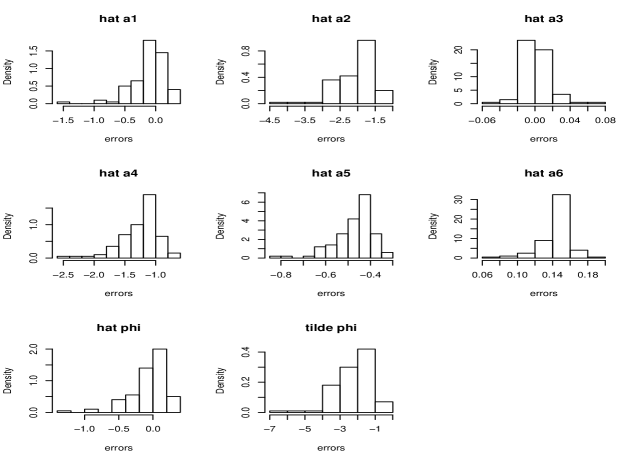

First we not that the rates of convergence of the estimates decrease with (see Tables 2, 3, 4, 7 and 8). Actually, from the theoretical point of view, the rate of convergence is when (Theorems 1 and 2 above). It is when (Boswijk and Franses 1995) and when (Basawa and Lund 2001). Thus we produce the histograms of scaled errors, the scale factor being when , when and when .

We observe when and when in Figures 1, 2, 3, 4 and 5, that the histograms of the scaled errors have long tails. In Tables 2, 3, 4, 5 and 6, we note that the ratios of the hinges (upper hinge, lower hinge) to the sigmas of the errors are of order of magnitude or less. It is the same for the ratios of the hinges to the whiskers. These phenomena correspond to the fact that the limiting distributions have heavy tails. See (Aknouche 2013) for independent innovation.

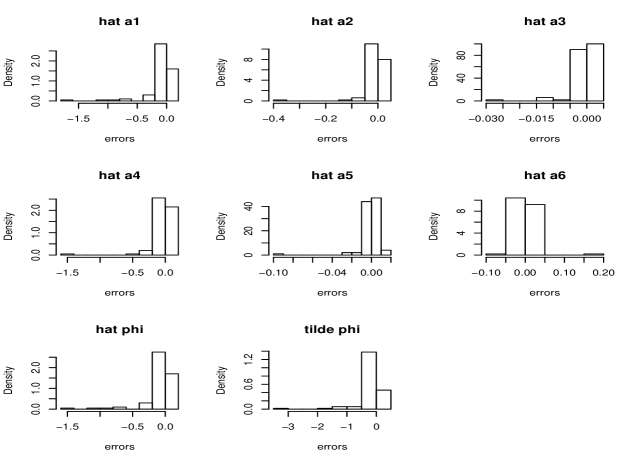

When , in Figure 6 and in Table 7 we observe the distributions for some estimates (, , , ) have also relatively long tails. But the phenomenon is very less apparent than previously. See (Phillips 1987) for the autoregressive model with a unit root.

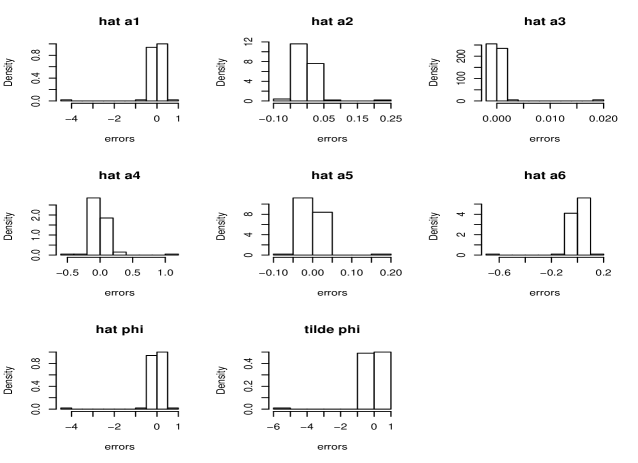

When , in Figure 7 the tails of the histograms are shorter than for the others values of . In Table 8 the hinges and the whishers are often with the same order of magnitude or larger than the sigmas. This fits to the theoretical result, the limiting distribution being Gaussian (Basawa and Lund 2001).

When the innovation is correlated with for , in Table 5 we observe few change in the performances of the estimates with respect to the case when the innovation is independent (Table 4). The confidence intervals are smaller for , and larger for . However in Figure 4 with and , the tails of the histograms are farther from 0 than in Figure 3 when .

Finally, comparing the statistics of the errors of the two estimates and in each table, we find out that they have globally the same order of magnitude whenever and the histograms are quite similar. However when it seems that gives better results than . The comparison of these two estimators need more investigation to determine whether one of them is better than the other.

Conclusion

In this paper we have studied the least squares estimators of the coefficients of explosive PAR(1) time series under relatively weak dependence assumptions. It is quite interesting to see how heavy tailed distributions enter in this context. We have also constructed two estimators of the product of these coefficients, which characterizes the explosive behaviour of the model. It would be worth to investigate the comparison of these estimators and also to consider more general PAR and PARMA models.

Appendix

Proof of Proposition 1

Let be fixed. We know that Since the sequence is stationary with finite second order moments and , we can readily establish that

Now we show that converges almost surely and in quadratique mean.

First we have

| (6) |

Then the sequence is a Cauchy sequence in the Hilbert space , thus this sequence converges to some random variable in quadratic mean. Moreover

From the exponential decreasing to 0 of the right hand side of the last inequality, we can readily deduce the convergence almost sure following the usual method applying Borel Cantelli lemma.

As for the second part of the proposition, note that

and

Since the sequence of random vectors is stationarily distributed, we deduce that

Then from the definition of , we readily achieve the proof of Proposition 1 .

Proof of Theorem 1

First in the two following lemmas we study the asymptotic behaviours of and .

Lemma 1

Proof We have seen that that converges to almost surely and in quadratic mean. Then Toeplitz lemma on series convergence gives the result.

Lemma 2

for any . Moreover, under the mixing hypothesis (M) we have

Proof To prove the lemma we study the left hand side of equality (4).

1) For the last term of equality (4), Cauchy Schwarz inequality entails

As the sequences and are stationary, we have

Thus

Furthermore, thanks to the exponential decreasing rate of convergence to 0 in , applying Borel Cantelli lemma, we easily establish the almost sure convergence

2) To study the first term of left hand side of equality (4) the idea is first to isolate the sums of and of . Then define blocks that separate the first and the last terms of the time series in order to be able to use the asymptotic independence which is given by the strong mixing condition on the innovation. Thus assume without lost of generality that is a multiple of 4 and let , and . Then we can write

| (7) |

(i) Thanks to inequality (6) we have

Hence

Using Borel Cantelli lemma, the exponential decreasing rate of convergence permits to prove the almost sure convergence.

(ii) Besides, the second term of the right hand side of equality (7) can be estimated as follows

Thus

As in part (i), we obtain the almost sure convergence.

(iii) It remains to study the asymptotic behaviour of where

| (8) |

We know that converges to almost surely and in quadratic mean. (Proposition 1). Since

converges to 0 in quadratic mean and also almost surely. Hence converges to 0 in and almost surely.

(iv) Now we establish the convergence in distribution of . Note that can be expressed with while can be expressed with . Hence, as , the mixing property entails that

for all Borel subsets and of , where is the strong mixing coefficient. The mixing hypothesis entails that tends to 0 as goes to , thus

for all Borel subsets and . So and are asymptotically independent. We know that converges in quadratic mean so in distribution to (Proposition 1). Now it remains to study the behaviour of .

(v) Since the time series is periodically distributed, the time series is also periodically distributed. Denoting

we have , and the sequence converges almost surely and in quadratic mean to some random variable . Then converge in distribution to as . Consequently converges in distribution to where and are independent random variables. Furthermore from definition (8), we easily deduce the distribution of the s.

Following the same lines with Cramér device we can establish the multidimensional convergence.

Proof of Theorem 1. The almost sure convergence is a direct consequence of Lemmas 1 and 2. To prove the convergence in distribution, we first apply Cramér device to prove the convergence in distribution of . For this purpose, let and establish the convergence in distribution of

Following the same method as in the proof of Lemma 2 we define blocks to separate the terms and , as well as to apply the asymptotic independence given by the strong mixing condition. Denote . Then can be decomposed as

Thanks to Lemma 1, converges to 0 almost surely. Moreover thanks to the parts 1, 2(i) and 2(ii) of the proof of Lemma 2, it remains to study

Then from the strong mixing condition, is asymptotically independent with respect to , and following the same lines as in the part 2(v) of the proof of Lemma 2 we deduce the convergence in distribution of as .

Finally the application of the continuous mapping theorem for convergence in distribution completes the proof of the theorem.

Proof of Theorem 2

Theorem 2 is a direct consequence of the following lemma about the asymptotic behaviours of and .

Lemma 3

| (9) |

and

| (10) |

Proof 1) First note that can be expressed as follows

Then thanks to Lemma 1

Using the fact that , we deduce limit (9).

2) The convergence almost sure and in of to 0, can be easily obtained following the lines of the proof of the convergence almost sure and in of in Lemma 2. Thus the proof is left to the reader.

3) From its definition, can be expressed by

| (11) |

(i) Thanks to the stationarity of the sequences and , the second term of expression (11) is of order of magnitude in probability. Indeed

(ii) Following the same lines as in the proof of Lemma 2, and using the stationarity of we can readily prove that

where and

| (12) |

The mixing hypothesis (M) entails that and are asymptotically independent. Besides the distribution of

coincides with the distribution of where

and the sequence is defined in part 2(v) of the proof of Lemma 2. The sequence is independent with respect to and , thus the sequence is also independent with respect to and . Since the sequence is centered periodically distributed with second order moments, the sequence converges almost surely and in quadratic mean to some random variable . Thanks to the definition (12) of and the periodicity of the distribution of the innovation , we deduce the distribution of . Then limit (10) is proved.

References

- [1] Adams G.J., Goodwin G.C. (1995) Parameter estimation for periodic ARMA models. J. Time Ser. Anal. 16(2): 127–147.

- [2] Aknouche A. (2012a) Implication of instability on econometric and financial time series modeling. In Econometrics : New Research (editors : Mendez S.A., Vega A.M.). Nova Publishers, New York.

- [3] Aknouche A. (2012b) Multi-stage weighted least squares estimation of ARCH processes in the stable and unstable cases. Statist. Inference Stochast. Process. 15: 241–256.

- [4] Aknouche A. (2013) Knife edge effect in strong periodic autoregressions. Preprint.

- [5] Aknouche A, Al-Eid E. (2012) Asymptotic inference of unstable periodic ARCH processes. Statist. Inference Stochast. Process. 15: 61–79.

- [6] Aknouche A, Bibi A (2009) Quasi-maximum likelihood estimation of periodic GARCH and periodic ARMA-GARCH processes. J. Time Ser. Anal. 30: 19–46.

- [7] Anderson T.W. (1959) On asymptotic distributions of estimates of parameters of stochastic difference equations. Ann. Math. Statist. 30: 676–687.

- [8] Antoni J. (2009) Cyclostationarity by Examples. Mechan. System. Signal Process. 23: 987–1036.

- [9] Basawa, I.V., Lund R. (2001) Large sample properties of parameter estimates for periodic ARMA models. J. Time Ser. Anal. 22 (6): 651–663.

- [10] Bittanti S., Colaneri P. (2009) Periodic Systems: Filtering and Control. Springer-Verlag, New York.

- [11] Bloomfield P., Hurd H.L., Lund R.B. (1994) Periodic correlation in Stratospheric ozonz data. J. Time Series Anal. 15(2): 127–150.

- [12] Boswijk H.P., Franses P.H. (1995) Testing for periodic integration. Economics Letters 48: 241–248.

- [13] Boswijk H.P., Franses P.H. (1996) Unit roots for periodic integration. J. Time Ser. Anal. 17: 221–245.

- [14] Bradley R.C. (2005) Basic properties of strong mixing conditions. A survey and some open questions. Probability Surveys 2 : 107-144.

- [15] Chaari F., Leśkow J., Napolitano A., Sanchez-Ramirez A. (editors) (2014) Cyclostationarity : Theory and Methods. Lecture Notes in Mechanical Engineering. Springer-Verlag, Cham (Switzerland).

- [16] Collet P., Martinez S. (2008) Asymptotic velocity of one dimensional diffusions with periodic drift. J. Math. Biol. 56: 765–792.

- [17] Dedecker J., Doukhan P., Lang G., León R. J.R., Louhichi S., Prieur C. (2007) Weak Dependence : with Examples ans Applications. Lecture notes in Statistics 190. Springer-Verlag, New York.

- [18] Doukhan P. (1994) Mixing : Properties and Examples. Lecture Notes in Statistics 85. Springer-Verlag, New York.

- [19] Dragan Ya., Javors´kyj I. (1982) Rhythmics of Sea Waving and Underwater Acoustic Signals. Naukova dumka, Kiev (Kijev) (in Russian).

- [20] Francq C., Roy R., Saidi A. (2011) Asymptotic properties of weighted least squares estimation in weak PARMA models. J. Time Ser. Anal. 32, 699–723.

- [21] Franses P., Paap R. (2004) Periodic Time Series. Oxford University Press, Oxford.

- [22] Gardner W.A., Napolitano A. Paura, L. (2006) Cyclostationarity : half a century of research. Signal Processing 86: 639–697.

- [23] Ghysels E., Hall A., Lee H.S. (1996) On periodic structures and testing for seasonal unit root. J. Amer. Statist. Associat. 91: 1551–1559.

- [24] Hurd H.L., Makagon A., Miamee A.G. (2002) On AR(1) models with periodic and almost periodic coefficients. Stochastic Process. Appl. 100: 167–185.

- [25] Monsour J.M., Mikulski P.W. (1998) On Limiting Distributions in Explosive Autoregressive Processess. Statistics & Probability Letters 37: 141–147.

- [26] Osborn D.R, Chui A.P.L., Smith J.P., Birchenhall C.R. (1988) Seasonality and the order of integration for consumption. Oxford Bull. Econom. Statist. 50: 361–377.

- [27] Pagano M. (1978) On periodic and multiple autoregression. Ann. Statist. 6: 1310–1317.

- [28] Phillips P.C.B. (1987) Time series regression with a unit root. Econometrica 55 (2): 277–301.

- [29] Serpedin E., Pandura F., Sari I., Giannakis G.B. (2005) Bibliography on Cyclostationarity. Signal Processing 85: 2233–2303.

- [30] Rosenblatt M. (1956) A central limit theorem and a strong mixing condition. Proc. Nat. Acad. Sci. USA 27 : 832–837.

- [31] Stigum B.P. (1974) Asymptotic properties of dynamic stochastic parameter estimates (III). J. Multivariate Anal. 4: 351–381.

- [32] Tiao G.C., Grupe M.R. (1980) Hidden periodic autoregressive-moving average models in time series data. Biometrika 67: 365–373.

- [33] Troutman B.M. (1979) Some results in periodic autoregressions. Biometrika 66: 219–228.

- [34] Vecchia A. (1985) Maximum likelihood estimation for periodic autoregressive moving average models. Technometrics 27: 375–384.

- [35] Van der Vaart A.W. (1998) Asymptotic Statistics Cambridge University Press, Cambridge.