A lack-of-fit test for quantile regression models with high-dimensional covariates

Abstract

We propose a new lack-of-fit test for quantile regression models that is suitable even with high-dimensional covariates. The test is based on the cumulative sum of residuals with respect to unidimensional linear projections of the covariates. The test adapts concepts proposed by Escanciano (Econometric Theory, 22, 2006) to cope with many covariates to the test proposed by He and Zhu (Journal of the American Statistical Association, 98, 2003). To approximate the critical values of the test, a wild bootstrap mechanism is used, similar to that proposed by Feng et al. (Biometrika, 98, 2011). An extensive simulation study was undertaken that shows the good performance of the new test, particularly when the dimension of the covariate is high. The test can also be applied and performs well under heteroscedastic regression models. The test is illustrated with real data about the economic growth of 161 countries.

Keywords: quantile regression, lack-of-fit testing, high-dimensional covariates.

1 Introduction

Let us consider a regression setting where a quantile of the response variable of interest, , is expressed as a function of a vector of explanatory variables, . The resulting regression model can then be denoted by

where represents the quantile regression function; and the error, , has a conditional -quantile equal to zero, for almost all .

Quantile regression models have been receiving increased attention in the literature, due to their flexibility for general error distributions and because they provide a more detailed description of the conditional distribution of the response, compared to classical mean regression. Koenker and Bassett (1978) can be considered as the seminal work on the estimation of linear quantile regression models. The main concept is to exploit that the -quantile, , of a variable minimizes the expectation,

where , and denotes the indicator function of an event. Estimation of quantile models is obtained by minimizing the sum of penalized residuals, similarly to the sum of squares in the case of mean regression. That is, given a sample of independent observations, , the coefficients of a linear model, ( denotes the transpose of ), are estimated as the minimizers of

The same criterion can be applied to estimate general parametric models, where the regression function is of the type and is a parameter to be estimated, and even to nonparametric estimation of the quantile regression function. See Koenker (2005) for a complete review on quantile regression methods.

We focus on the problem of testing a parametric model of quantile regression. That is, a test of the null hypothesis

versus a nonparametric alternative.

This problem was addressed by He and Zhu (2003), who based their test on the process

where is the derivative of , , and is an estimator of . This is an extension to the quantile regression setting of the cumsum process considered by Stute (1997) in the mean regression setting. Zheng (1998) proposed a U-statistic of the quantities with smoothing kernel weights, thereby extending the test of Zheng (1996) to quantile models. Other specification tests for quantile regression models can be found in Horowitz and Spokoiny (2002), Whang (2006), Otsu (2008), Escanciano and Velasco (2010), and Escanciano and Goh (2014), among others.

It is well-known that a high (or even moderate) dimension of the covariate can affect the performance of the specification tests. This problem has been addressed by several authors in the mean regression setting, where modified tests have been proposed with better properties for multiple covariates. In particular, Escanciano (2006) applied a cumsum test to one-dimensional projections of the covariates, Lavergne and Patilea (2008) considered similar one-dimensional projections for a Zheng type test, and Stute et al. (2008) based their test on the residual empirical process marked by proper functions of the regressors.

Little can be found in the literature for lack-of-fit testing adapted to multidimensional covariates in the framework of quantile regression. Wilcox (2008) used a He and Zhu type test and defined some ranks over the covariate. This proposal has the virtue of simplicity but does not provide an omnibus test, i.e., it is not consistent for all alternatives.

We propose and study a lack-of-fit test for parametric models of quantile regression, with good properties for multidimensional covariates and consistent for all alternatives. In Section 2 we present the new He and Zhu type test calculated on one-dimensional projections of the covariates. A bootstrap method is also proposed to approximate the critical values of the test. Section 3 contains a simulation study where the performance of the test is studied under homo- and heteroscedastic models, with different error distributions and with increasing dimension of the covariate. We compare the proposed test with a He and Zhu test. In Section 4 the test is applied to real data, and we provide some concluding remarks and extensions in Section 5.

2 The proposed method

2.1 The test

The strategy to improve the performance of the test with multiple covariates consists of applying a lack-of-fit test to one-dimensional projections of the covariates. This is motivated by a fundamental result, that states that the null hypothesis, , holds if and only if, for some , and for any with ,

almost surely. This is an immediate extension of Lemma 1 in Escanciano (2006) to the quantile regression setting.

If the true parameter was known, the test could be based on the process

Otherwise, an estimator is substituted, yielding the process useful for lack-of-fit testing of the parametric model

The test statistic is then defined as

| ((1)) |

where , is the unit sphere on , and is the empirical distribution of the projected covariates .

The process is similar to that proposed by Escanciano (2006), with two differences: the loss function is now the quantile loss function, and the gradient vector is introduced following the suggestion of He and Zhu (2003).

The limit distribution of under the simple null hypothesis, with known, can be expressed as

where is a Gaussian process with mean zero and covariance given by

where and . This result can be obtained similarly to Escanciano (2006), where the tightness comes from the fact that the family of functions in the definition of is a VC-class of functions.

Under the composite null hypothesis of a parametric model, , and under certain regularity conditions, the following representation can be obtained:

uniformly in , where , are the errors, denotes the conditional density of the error at zero, and the matrices and are defined by

The proof and the subsequent consequences are a combination of arguments given in He and Zhu (2003) and Escanciano (2006). The representation itself is different from that of He and Zhu (2003), because we do not assume homoscedasticity. From this representation, the limit distribution of the test statistic, , under the null hypothesis can be derived.

Under the alternative, the representation is similar to the previous case, but a new term appears which will be crucial to prove the consistency of the test. Let us assume that the data come from

where are independent errors with conditional quantile equal to zero. The errors are not assumed to be identically distributed. In particular, their density at zero may depend on . With this type of data drawn from the alternative hypothesis, the process allows the following representation:

uniformly in . The second and third summands of the right-hand side are constants reflecting the deviation from the null hypothesis. If the data come from

where is a sequence of real numbers converging to infinity (at any rate), then the test statistic, , will converge to infinity and the power of the test will converge to one. To obtain this consistency, it is assumed that the sequence does not coincide with any element of the parametric model, , and that for any .

2.2 Bootstrap approximation

The approximation of critical values is a crucial issue in lack-of-fit testing. One possible solution would be to use the limit distribution. However, this would require an estimate of the limit variance which involves the estimation of complicated unknown quantities. Furthermore, the convergence to the limit distribution could be slow. Another possibility could be to use the representations as given above. Then, a bootstrap method based on multipliers can be considered (see He and Zhu (2003)). The approximation by a multipliers bootstrap is generally better than the limit distribution, but still requires estimating many unknown quantities. He and Zhu (2003) assume homoscedasticity, so the conditional density of the error at zero, , does not have to be estimated. On the other hand, Escanciano and Goh (2014) allow for heteroscedasticity and use a multipliers bootstrap, which requires an estimate of the conditional density by a smoothing method.

We propose a bootstrap approximation based on drawing new bootstrap samples,

, where

is the parameter estimate obtained from the original sample, and , where are the residuals from the original sample. The multipliers, , are independently generated from a common distribution with -quantile equal to zero. Following the proposal by Feng et al. (2011), the absolute values of the residuals are used to construct the bootstrap errors, which is a convenient modification of wild bootstrap for quantile regression. Regarding the multipliers distribution, we adopt the two-point distribution with probabilities and at and , respectively, that was proposed by Feng et al. (2011) to satisfy their Conditions 3, 4 and 5. Note that other common multipliers distributions for mean regression, generally with the only condition that the variance is one and occasionally with the condition that the third moment is one (see Mammen (1993) for a two-point multipliers distribution in the mean regression), do not satisfy Conditions 4 and 5 required by Feng et al. (2011) to establish consistency of the bootstrap for quantile regression.

The advantage of the proposed bootstrap approximation for the lack-of-fit test, in comparison to existing methods such as those proposed by He and Zhu (2003) and Escanciano and Goh (2014), is that it allows consideration of heteroscedastic regression models of any type without needing to estimate complicated quantities in the representations, and in particular without estimating the conditional density by smoothing methods.

Once the bootstrap sample is generated, the test statistic is computed in the same way as for the original sample, obtaining . If a number, , of bootstrap samples are generated, then represents the bootstrap values of the test statistic. The p-value of the test may be approximated by the proportion of bootstrap values not smaller than the original test statistic, i.e., .

The validity of this bootstrap mechanism comes from the representation of the process under the null hypothesis, in terms of the true errors plus the parameters estimation,

uniformly in . A similar representation can be derived for the bootstrap process conditionally on the original sample, where the convergence of the bootstrap version of the estimation error, , was established in Theorem 1 of Feng et al. (2011).

2.3 Computational aspects

Tests that face the curse of dimension usually require additional algorithms over other more common model checks. In particular, Escanciano (2006) and Stute et al. (2008) are based on Stute (1997)’s test and require additional computations over this original method. Similarly, Lavergne and Patilea (2008) is a test for high-dimensional covariates that is based on Zheng (1996)’s test, and requires an optimization algorithm over a set of Zheng-type statistics. The proposed method here is an adaptation of He and Zhu (2003)’s test to high-dimensional covariates with a procedure similar to that given by Escanciano (2006). One important virtue of this procedure is the ease of computation and that the amount of computations does not grow dramatically with the dimension of the covariate. To illustrate this, recall that our test statistic, , was defined in (1) as the largest eigenvalue of a Cramer-von-Mises norm of the process . Following Escanciano (2006), one can show that can be expressed as

where is given by

where is the complementary angle between the vectors and measured in radians, is the gamma function, and is the dimension of the covariate, . Thus, the total number of computations required to obtain the test statistic depends on the dimension, , only at a linear rate, which is the same rate required by He and Zhu (2003)’s test, and much less than the optimization in dimensions required by other methods in the literature. Note also that the matrix , which is the most expensive in computation time, does not need to be computed for each bootstrap sample. All these computational properties are particularly useful in the case of high-dimensional or functional covariates, see García-Portugués et al. (2013) for an illustration in the mean regression functional context.

Table 1 shows the mean of the times required by original samples with bootstrap replications, in units of seconds per original sample. The data are drawn from Model 8, whose details are given in the next section, and the sample size is . The dimension of the covariate is . As expected, the new test requires more computations than He and Zhu (2003)’s test, but the differences are quite small, and the amount of computations does not dramatically grow with the dimension, even for very large dimensions. The gain of power from the new test, shown in the next section, justifies the small increase in the computation time.

| Proposed test | 2.76 | 2.84 | 2.85 | 2.91 | 2.91 | 3.10 | 3.20 | 3.38 |

|---|---|---|---|---|---|---|---|---|

| HZ test | 2.71 | 2.51 | 2.81 | 2.56 | 2.92 | 2.83 | 2.85 | 2.77 |

3 Simulation study

We study the performance of our proposed method under the null and the alternative hypotheses using a Monte Carlo simulation. In all experiments, the number of simulated original samples was , the number of bootstrap replications , and the multipliers for the bootstrap approximation followed the two-point distribution given in Section 2.2.

We first focus on the behavior under the null hypothesis, to check the adjustment of the significance level. We simulate values for the following quantile regression models with :

where for , and they are mutually independent; and and is the unknown error, which is drawn independently of the covariates. In Models 1 and 3 the null hypothesis is the linear model in and versus an alternative that includes any dependence of on and . In Model 2 the null hypothesis is the linear model in the five explanatory variables versus any dependence on them. Model 1 represents a common homoscedastic model with small dimension of the covariate. Model 2 is intended to show the possible effect of a larger dimension on the level. Model 3 is useful to show the possible effect of heteroscedasticity on the level.

Table 2 shows the proportions of rejections associated with different sample sizes, , and for different nominal significance levels, . The proposed test works well in a homoscedastic context (Models 1 and 2) as well as in a heteroscedastic context (Model 3) even for small sample sizes. Comparing Models 1 and 2, the increase of the dimension of the explanatory variables does not have a negative impact on the adjustment of the significance level of the test. These are important, because our bootstrap mechanism was designed to work under heteroscedastic models and the aim of the test itself was to be applied for larger dimensions of the covariate.

| Model 1 | Model 2 | Model 3 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| n=25 | 0.096 | 0.049 | 0.002 | 0.119 | 0.066 | 0.017 | 0.107 | 0.061 | 0.014 |

| n=50 | 0.112 | 0.047 | 0.008 | 0.112 | 0.053 | 0.014 | 0.099 | 0.045 | 0.005 |

| n=100 | 0.102 | 0.058 | 0.016 | 0.094 | 0.047 | 0.011 | 0.107 | 0.049 | 0.010 |

| n=150 | 0.089 | 0.048 | 0.007 | 0.104 | 0.056 | 0.014 | 0.096 | 0.055 | 0.015 |

| n=200 | 0.100 | 0.048 | 0.010 | 0.106 | 0.049 | 0.010 | 0.100 | 0.054 | 0.015 |

Table 3 provides the same proportions of rejections for different error distributions and quantiles, restricted to Model 1 and nominal level . The error distributions are centered standard normal, centered log-normal, and centered exponential with expectation one. That is, , where follows a standard normal, log-normal, and exponential with expectation one, respectively, and is the -quantile of the -distribution. The nominal level is respected under the null hypothesis for all the error distributions considered and orders of the quantile.

| Centered Standard Normal | 0.048 | 0.061 | 0.047 | 0.063 | 0.043 | |

|---|---|---|---|---|---|---|

| 0.052 | 0.053 | 0.048 | 0.057 | 0.051 | ||

| Centered Log-Normal | 0.057 | 0.053 | 0.042 | 0.055 | 0.057 | |

| 0.041 | 0.053 | 0.052 | 0.051 | 0.057 | ||

| Centered Exponential | 0.058 | 0.054 | 0.048 | 0.057 | 0.053 | |

| 0.060 | 0.056 | 0.059 | 0.049 | 0.046 | ||

We now study the performance of the new test under the alternative. To this end, the new test will be compared with that of He and Zhu (2003). Before doing so, we must remember that He and Zhu (2003) suggested a bootstrap calibration of their test based on an asymptotic representation of the empirical process in a homoscedastic scene. We will verify if this manner of calibrating the test allows a good fit to the significance level for heteroscedastic models. We simulate values of the following regression model with under the null hypothesis of linearity:

where , , , and and are independent.

The proportions of rejections associated with the test proposed by He and Zhu (2003) are shown in Table 4 for different sample sizes and nominal significance levels. The bootstrap method proposed by He and Zhu (2003) does not work well in a heteroscedastic context. This is due to their representation being only valid under homoscedasticity. However, the proposed bootstrap (Section 2.2) works well for their test also under heteroscedasticity. Therefore, with the aim to make a fair comparison between our proposal and He and Zhu (2003)’s test, subsequently we use a wild bootstrap as given in Section 2.2 to calibrate both lack-of-fit tests.

| Wild bootstrap | Bootstrap proposed | |||||

|---|---|---|---|---|---|---|

| of Section 2.2 | in He and Zhu (2003) | |||||

| 0.103 | 0.057 | 0.014 | 0.441 | 0.305 | 0.142 | |

| 0.116 | 0.064 | 0.015 | 0.263 | 0.164 | 0.067 | |

| 0.094 | 0.051 | 0.013 | 0.167 | 0.092 | 0.033 | |

| 0.104 | 0.051 | 0.010 | 0.155 | 0.085 | 0.025 | |

| 0.103 | 0.051 | 0.014 | 0.136 | 0.080 | 0.026 | |

Once the adjustment of the level of both lack-of-fit tests has been studied, we analyze their performance under the alternative hypothesis. Consider the following regression model associated with quantiles of different orders, :

where and they are independent, and , where is the -quantile of the variable . is drawn independently of and . Three possibilities are considered for the distribution of : standard normal, uniform on the interval , and chi-squared with four degrees of freedom.

Table 5 shows the proportions of rejections for several quantiles and the three error distributions, when the tests are applied to check the no-effect model, i.e., to check the null hypothesis that the quantile regression function is a constant not depending on the covariates. The sample size is fixed to . We consider a relatively simple hypothesis and a simple deviation under the alternative, to facilitate the comparison between quantiles of different orders, and to evaluate the effect of the error distribution.

The proposed test is more powerful than He and Zhu (2003)’s test for any of the quantiles and for the three error distributions. The power of the proposed test is symmetric with respect to the order of the quantile around for the symmetric error distributions, which are the standard normal and the uniform in Table 5. For the standard normal error distribution, the proposed test is more powerful for the central quantiles (around ), which can be explained by the higher density at these quantiles. For the uniform error distribution, the density is constant with respect to the quantile, while the factor appearing in the asymptotic distribution of the proposed test makes the test more powerful for the external quantiles (with orders close to or ). For the chi-squared error distribution, the proposed test is more powerful for the quantiles with smaller order, since the error distribution is asymmetric with higher density at these quantiles.

| Proposed test | HZ test | ||||||

|---|---|---|---|---|---|---|---|

| 0.346 | 0.229 | 0.092 | 0.183 | 0.094 | 0.023 | ||

| 0.498 | 0.362 | 0.180 | 0.210 | 0.121 | 0.030 | ||

| 0.575 | 0.444 | 0.231 | 0.208 | 0.110 | 0.032 | ||

| 0.487 | 0.377 | 0.200 | 0.191 | 0.096 | 0.016 | ||

| 0.357 | 0.245 | 0.102 | 0.128 | 0.052 | 0.007 | ||

| 0.930 | 0.885 | 0.707 | 0.524 | 0.335 | 0.112 | ||

| 0.866 | 0.789 | 0.593 | 0.397 | 0.242 | 0.066 | ||

| 0.809 | 0.691 | 0.475 | 0.325 | 0.186 | 0.056 | ||

| 0.877 | 0.795 | 0.587 | 0.381 | 0.229 | 0.054 | ||

| 0.945 | 0.872 | 0.693 | 0.382 | 0.193 | 0.027 | ||

| 0.315 | 0.207 | 0.076 | 0.144 | 0.078 | 0.018 | ||

| 0.245 | 0.144 | 0.045 | 0.124 | 0.056 | 0.015 | ||

| 0.208 | 0.124 | 0.041 | 0.112 | 0.058 | 0.012 | ||

| 0.141 | 0.070 | 0.022 | 0.115 | 0.058 | 0.017 | ||

| 0.137 | 0.077 | 0.028 | 0.120 | 0.064 | 0.015 | ||

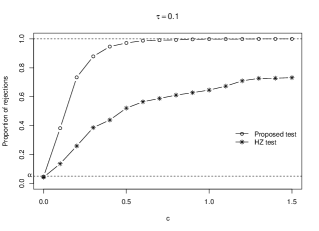

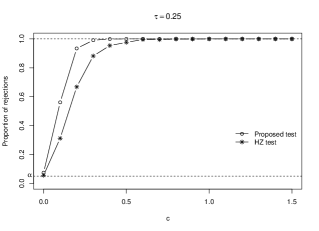

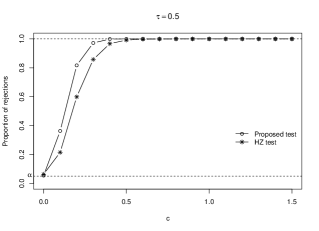

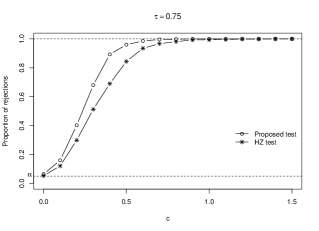

We now consider a linear model under the null hypothesis and a quadratic deviation under the alternative. The deviation is multiplied by a value , to evaluate the effect of the deviation on the power of the test.

where , ; and is a log-normal distribution centered to the quantile , i.e., , where and are the -quantile of the variable ; and , and are drawn independently.

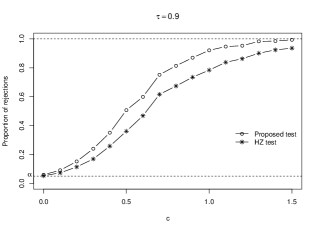

Figure 1 shows the powers of the proposed test and He and Zhu (2003)’s test as functions of the value of , and with five orders of the quantile: , , , , and . The nominal level is and the sample size is fixed to . As expected, the power increases with . The new test is more powerful than He and Zhu (2003)’s test for any value of and for any of the considered quantiles. Both tests are more powerful for central quantiles (orders close to ). Symmetry around is not strictly satisfied, since the error distribution is not symmetric around the median, and the deviation from the null hypothesis is more complex than that given in Model 5.

We consider different deviations from the linear null hypothesis and error distributions, as Model 7.

where , ; and , with being the -quantile of the variable ; and , , and are drawn independently. For the deviation , a quadratic function including interaction is considered, as well as a sinus, exponential, and logarithm function of the linear transformation (see Table 6). For the distribution of , the log-normal, chi-squared with two degrees of freedom, exponential with expectation one, and a mixture of normal distributions are considered. The mixture is obtained as a standard normal with probability and a normal distribution with mean and standard deviation with probability .

The proposed test and He and Zhu (2003)’s test are applied to check the null hypothesis of linearity on and with nominal level . Results for the proportions of rejections are given in Table 6. For each deviation and each error distribution, the proposed test is more powerful than He and Zhu (2003)’s.

| Proposed | HZ | Proposed | HZ | Proposed | HZ | Proposed | HZ | |||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.373 | 0.162 | 0.199 | 0.097 | 0.448 | 0.184 | 0.135 | 0.083 | |||

| 0.577 | 0.364 | 0.345 | 0.208 | 0.696 | 0.435 | 0.287 | 0.175 | |||

| 0.309 | 0.217 | 0.200 | 0.150 | 0.490 | 0.365 | 0.074 | 0.068 | |||

| 0.994 | 0.910 | 0.934 | 0.705 | 1.000 | 0.962 | 0.702 | 0.386 | |||

| 0.981 | 0.899 | 0.849 | 0.619 | 0.999 | 0.976 | 0.829 | 0.617 | |||

| 0.773 | 0.579 | 0.516 | 0.361 | 0.952 | 0.831 | 0.138 | 0.112 | |||

| 0.443 | 0.409 | 0.425 | 0.414 | 0.461 | 0.429 | 0.381 | 0.356 | |||

| 0.562 | 0.321 | 0.458 | 0.270 | 0.607 | 0.353 | 0.390 | 0.238 | |||

| 0.124 | 0.066 | 0.106 | 0.061 | 0.157 | 0.081 | 0.103 | 0.053 | |||

| 1.000 | 0.996 | 1.000 | 0.990 | 1.000 | 0.999 | 0.998 | 0.985 | |||

| 1.000 | 0.997 | 1.000 | 0.998 | 1.000 | 1.000 | 1.000 | 0.957 | |||

| 0.865 | 0.419 | 0.811 | 0.380 | 0.982 | 0.637 | 0.586 | 0.228 | |||

| 0.190 | 0.113 | 0.154 | 0.112 | 0.169 | 0.135 | 0.133 | 0.109 | |||

| 0.411 | 0.251 | 0.254 | 0.167 | 0.483 | 0.268 | 0.225 | 0.161 | |||

| 0.244 | 0.145 | 0.164 | 0.097 | 0.382 | 0.251 | 0.102 | 0.089 | |||

| 0.917 | 0.498 | 0.788 | 0.378 | 0.963 | 0.577 | 0.533 | 0.281 | |||

| 0.980 | 0.747 | 0.797 | 0.455 | 0.998 | 0.868 | 0.759 | 0.458 | |||

| 0.700 | 0.450 | 0.493 | 0.325 | 0.955 | 0.744 | 0.216 | 0.137 | |||

| 0.820 | 0.627 | 0.736 | 0.570 | 0.874 | 0.678 | 0.622 | 0.483 | |||

| 0.396 | 0.306 | 0.291 | 0.200 | 0.561 | 0.398 | 0.227 | 0.183 | |||

| 0.090 | 0.094 | 0.098 | 0.086 | 0.122 | 0.104 | 0.068 | 0.074 | |||

| 1.000 | 0.998 | 0.999 | 0.987 | 1.000 | 1.000 | 0.997 | 0.973 | |||

| 0.897 | 0.757 | 0.751 | 0.558 | 0.971 | 0.875 | 0.660 | 0.471 | |||

| 0.166 | 0.171 | 0.167 | 0.166 | 0.297 | 0.196 | 0.112 | 0.138 | |||

Our main purpose in proposing a new lack-of-fit test was to overcome the curse of dimensionality. Thus, the new test should show an acceptable power for increasing dimensionality of the covariate. To check this, we simulate values of the following median regression model:

where our goal is to realize the following lack-of-fit test:

where if is odd, and if is even; the error is drawn from the centered log-normal distribution, i.e., where ; is any smooth (nonparametric) function of the covariates; and represents the number of additional covariates in the alternative, and so is the additional dimension where the test is looking for deviations from the null. It would be expected that increased value of implies decreased power of the test.

Table 7 shows the proportions of rejections associated with the new test and He and Zhu (2003)’s test, for different values of the additional dimension, . Both tests suffer a loss of power due to the increase of the dimension, as expected. Nonetheless, the loss of power is more pronounced for the test proposed by He and Zhu (2003). For example, from dimension the proportion of rejections associated with their test is near to the significance level, whereas our proposed test preserves noticeable power, even for very high dimensions.

Note that, for very high dimensions, He and Zhu (2003)’s test statistic is almost degenerate, because for any observation of the covariate, , the indicators , involved in the computation of their test process at , will be zero for most of the other observations , when the dimension of the covariates and is large. Thus, the test is unable to make a reasonable number of evaluations to check the model, and its power is consequently destroyed, as observed in Table 7 for . On the other hand, our proposed method is able to make comparisons even for large dimensions of the covariate, because the indicators are calculated with unidimensional projections of the covariate. We conclude that the proposed method constitutes a necessary modification of He and Zhu (2003) when the dimension of the covariate is large.

| Proposed test | HZ test | ||||||

|---|---|---|---|---|---|---|---|

| 0.252 | 0.154 | 0.057 | 0.225 | 0.135 | 0.035 | ||

| 0.675 | 0.564 | 0.361 | 0.487 | 0.357 | 0.163 | ||

| 0.961 | 0.918 | 0.776 | 0.822 | 0.725 | 0.460 | ||

| 0.993 | 0.983 | 0.943 | 0.949 | 0.903 | 0.751 | ||

| 0.999 | 0.998 | 0.990 | 0.982 | 0.965 | 0.897 | ||

| 0.177 | 0.100 | 0.029 | 0.143 | 0.080 | 0.021 | ||

| 0.507 | 0.391 | 0.186 | 0.215 | 0.117 | 0.040 | ||

| 0.868 | 0.813 | 0.638 | 0.349 | 0.228 | 0.077 | ||

| 0.978 | 0.957 | 0.869 | 0.506 | 0.355 | 0.163 | ||

| 0.997 | 0.993 | 0.975 | 0.636 | 0.498 | 0.263 | ||

| 0.133 | 0.055 | 0.010 | 0.054 | 0.018 | 0.004 | ||

| 0.345 | 0.244 | 0.097 | 0.098 | 0.051 | 0.010 | ||

| 0.797 | 0.696 | 0.501 | 0.097 | 0.056 | 0.021 | ||

| 0.935 | 0.901 | 0.768 | 0.151 | 0.083 | 0.027 | ||

| 0.992 | 0.978 | 0.929 | 0.177 | 0.089 | 0.029 | ||

| 0.120 | 0.057 | 0.011 | 0.066 | 0.018 | 0.005 | ||

| 0.267 | 0.161 | 0.056 | 0.043 | 0.028 | 0.004 | ||

| 0.659 | 0.562 | 0.366 | 0.052 | 0.025 | 0.003 | ||

| 0.884 | 0.830 | 0.672 | 0.071 | 0.036 | 0.006 | ||

| 0.966 | 0.946 | 0.887 | 0.085 | 0.040 | 0.008 | ||

| 0.094 | 0.042 | 0.010 | 0.065 | 0.023 | 0.010 | ||

| 0.174 | 0.098 | 0.019 | 0.055 | 0.024 | 0.007 | ||

| 0.520 | 0.398 | 0.235 | 0.054 | 0.028 | 0.005 | ||

| 0.800 | 0.707 | 0.525 | 0.000 | 0.004 | 0.003 | ||

| 0.918 | 0.876 | 0.748 | 0.050 | 0.033 | 0.008 | ||

| 0.074 | 0.044 | 0.005 | 0.050 | 0.026 | 0.007 | ||

| 0.111 | 0.059 | 0.014 | 0.074 | 0.036 | 0.009 | ||

| 0.237 | 0.149 | 0.041 | 0.068 | 0.034 | 0.007 | ||

| 0.492 | 0.374 | 0.188 | 0.001 | 0.005 | 0.005 | ||

| 0.686 | 0.600 | 0.438 | 0.063 | 0.024 | 0.009 | ||

4 Application to real data

The proposed method is applied to real data from the evolution of the Gross Domestic Product (GDP) in several countries. GDP is an economic indicator that reflects the monetary value of the goods and final services produced by an economy in a certain period and it is used as a measure of the material well-being of a society. Different median regression models have been proposed to explain the annual growth rate of the Per Capita GDP in terms of a number of explanatory variables, including the initial Per Capita GDP and diverse economic and social indicators.

We focus on the model of Koenker and Machado (1999), based on the available information included in Barro and Lee (1994). A complete study of this economic model is given by Barro and Sala-i-Martin (1995). The aim of Koenker and Machado (1999) was to check the combined effect of the different explanatory variables on the response in a quantile regression model. Here we test the specification of the quantile regression model itself.

The dataset we use is available in the R package quantreg, barro (http://cran.at.r-project.org/web/packages/quantreg/). This data set contains measurements associated with 71 countries during the period 1965-1975 and 90 countries during the period 1975-1985, yielding a total sample size of countries.

The explanatory variables used to explain the median of the annual growth of the Per Capita GDP (the response variable, ) can be split in two groups as given below. More details about these variables and their role in the model for GDP can be found in Barro and Sala-i-Martin (1995).

- State variables:

-

These variables reflect characteristics of the different countries that cannot be directly decided by political or social agents. They are measures of the steady-state position of the country, such as human capital, education or health. Koenker and Machado (1999) consider the following variables in this group:

log(Initial Per Capita GDP)

Male Secondary Education

Female Secondary Education

Female Higher Education

Male Higher Education

Life Expectancy

Human Capital - Control and environmental variables:

-

These variables are direct consequences of decisions made by government or private agents. The variables included in this group are

Education/GDP

Investment/GDP

Public Consumption/GDP

Black Market Premium

Political Instability

Growth Rate Terms Trade

We apply the AIC criterion proposed by Hurvich and Tsai (1990) to variable selection among the thirteen explanatory variables for the quantile regression model. We will consider only those variables that show as relevant for the response. Based on this criterion, we propose a model that includes the variables with .

We apply the proposed lack-of-fit test in four different testing problems:

where (state variables). Problem 1 is a lack-of-fit test of the linear model versus a nonparametric alternative, including all the thirteen explanatory variables under both the null and alternative hypotheses. Problem 2 is a lack-of-fit test of the linear model versus a nonparametric alternative, including only the nine variables in the set . Problem 3 is the same test as Problem 2, but with an alternative in the thirteen original variables. Problem 4 is a lack-of-fit test of a linear model that only includes the state variables.

Table 8 contains the -values obtained from the application of the proposed lack-of-fit test to each of the testing problems. The number of bootstrap replications was . We would accept the null hypothesis in Problems 1, 2 and 3. In Problem 3, the model under the null is the simplest, while the model under the alternative is the most complex. Despite this, the -value is quite large, so we can conclude that the simple model with the nine explanatory variables in the set is correct, and there is no significant deviation from this model arising from any (smooth) function of the thirteen possible explanatory variables.

On the other hand, the null hypothesis is rejected for Problem 4. Thus, a model that only includes the state variables is insufficient to explain the evolution of the GDP, that is, some of the control or environmental variables are necessary.

In summary, our proposed test confirms the validity of the model proposed by Koenker and Machado (1999). In addition, from the outcome for Problem 3, it would be sufficient to consider a model with nine explanatory variables to explain the growth rate of the Per Capita GDP.

| Problem 1 | Problem 2 | Problem 3 | Problem 4 | |

| -values | 0.194 | 0.458 | 0.440 | 0.002 |

5 Concluding remarks and extensions

We proposed a new lack-of-fit test for quantile regression models, together with a bootstrap mechanism to approximate the critical values. The bootstrap approximation does not need to estimate the conditional sparsity, and was shown to work well in homoscedastic and heteroscedastic error distributions and with high-dimensional covariates.

The proposed test is generally more powerful than its natural competitors, and particularly more powerful in the case of a high-dimensional covariate.

The proposed test was applied to a real data situation, where it was useful to validate well-known models in the economic literature, that describe the evolution of the GDP in terms of a number of explanatory variables.

The proposed method can be generalized to test models involving quantiles of different orders. The most treated model in the literature is the multiple quantile linear model, where it is assumed that the quantile regression function is linear for a subset of orders ,

with coefficients depending on the order, , of the quantile. The coefficients allow consideration of a different effect of the covariates depending on the order of the quantile. See Escanciano and Goh (2014) for a lack-of-fit test of multiple quantile linear models, or Escanciano and Velasco (2010) for a test of multiple quantile models with time series. Our proposed method can be generalized to test multiple quantile models in a general framework of parametric (possibly nonlinear) quantile regression with heteroscedasticity and without estimating unknown quantities. To this end, one would consider a process depending on , as well as on . We restricted to the case of testing a single quantile to focus on the performance of the test for high-dimensional covariates and other important features of the testing problem. Extension to multiple quantile testing was left to future research. Similarly, extensions of the proposed method to time series are possible using the results in Escanciano and Velasco (2010). These possible extensions show that the concept of projecting the covariate, given by Escanciano (2006) to overcome the curse of dimensionality, combined with the bootstrap methodology introduced by Feng et al. (2011), provide a promising strategy for checking quantile regression models.

Acknowledgements

The authors are grateful for constructive comments from the associate editor and three reviewers which helped to improve the paper. They also acknowledge the support of Project MTM2008-03010, from the Spanish Ministry of Science and Innovation and IAP network StUDyS, from Belgian Science Policy. Work of M. Conde-Amboage has been supported by FPU grant AP2012-5047 from the Spanish Ministry of Education.

References

References

- Barro and Lee (1994) Barro, R.J. and Lee, J.W. (1994). Data set for a panel of 138 countries, discussion paper, NBER, http://www.nber.org/pub/barro.lee.

- Barro and Sala-i-Martin (1995) Barro, R.J. and Sala-i-Martin, X. (1995). Economic Growth. McGraw-Hill, New York.

- Escanciano (2006) Escanciano, J.C. (2006). A consistent diagnostic test for regression models using projections. Econometric Theory, 22, 1030-1051.

- Escanciano and Goh (2014) Escanciano, J.C. and Goh, S.C. (2014). Specification analysis of linear quantile models. Journal of Econometrics, 178, 495-507.

- Escanciano and Velasco (2010) Escanciano, J.C. and Velasco, C. (2010). Specification tests of parametric dynamic conditional quantiles. Journal of Econometrics, 159, 209-221.

- Feng et al. (2011) Feng, X., He, X. and Hu, J. (2011). Wild bootstrap for quantile regression. Biometrika, 98, 995-999.

- He and Zhu (2003) He, X. and Zhu, L.-X. (2003). A lack-of-fit test for quantile regression. Journal of the American Statistical Association, 98, 1013-1022.

- Horowitz and Spokoiny (2002) Horowitz, J.L. and Spokoiny, V.G. (2002). An adaptive, rate-optimal test of linearity for median regression models. Journal of the American Statistical Association, 97, 822-835.

- Hurvich and Tsai (1990) Hurvich, C.M. and Tsai, C.L. (1990). Model selection for least absolute deviations regression in small samples. Statistics & Probability Letters, 9, 259-265.

- García-Portugués et al. (2013) García-Portugués, E., González-Manteiga, W. and Febrero-Bande, M. (2013). A goodness-of-fit test for the functional linear model with scalar response. Journal of Computational and Graphical Statistics, 23, 761-778.

- Koenker (2005) Koenker, R. (2005). Quantile Regression. Cambridge University Press, Cambridge.

- Koenker and Bassett (1978) Koenker, R. and Bassett, G. (1978). Regression quantiles, 46, 33-50.

- Koenker and Machado (1999) Koenker, R. and Machado, J.A.F. (1999). Goodness of fit and related inference processes for quantile regression. Journal of the American Statistical Association, 94, 1296-1310.

- Lavergne and Patilea (2008) Lavergne, P. and Patilea, V. (2008). Breaking the curse of dimensionality in nonparametric testing. Journal of Econometrics, 143, 103-122.

- Mammen (1993) Mammen, E. (1993). Bootstrap and wild bootstrap for high dimensional linear models. The Annals of Statistics, 21, 255-285.

- Otsu (2008) Otsu, T. (2008). Conditional empirical likelihood estimation and inference for quantile regression models. Journal of Econometrics, 142, 508-538.

- Stute (1997) Stute, W. (1997). Nonparametric model checks for regression. The Annals of Statistics, 25, 613-641.

- Stute et al. (2008) Stute, W., Xu, W.L. and Zhu, L.X. (2008). Model diagnosis for parametric regression in high-dimensional spaces. Biometrika, 95, 451-467.

- Whang (2006) Whang, Y.-J. (2006). Smoothed empirical likelihood methods for quantile regression models. Econometric Theory, 22, 173-205.

- Wilcox (2008) Wilcox, R. R. (2008). Quantile regression: A simplified approach to a goodness-of-fit test. Journal of Data Science, 6, 547-556.

- Zheng (1996) Zheng, J. X. (1996). A consistent test of functional form via nonparametric estimation techniques. Journal of Econometrics, 75, 263-289.

- Zheng (1998) Zheng, J. X. (1998). A consistent nonparametric test of parametric regression models under conditional quantile restrictions. Econometric Theory, 14, 123-138.