Prices of Options as Opinion Dynamics of the Market Players with Limited Social Influence

Abstract

The dynamics of market prices is described as the evolution of opinions in the trading community regarding future market behavior. The price then is a function of the voting process of the market players in favor to raise or reduce the value of a stock. The model presented in this paper is suited for pricing of options and was verified against real market data. The model allows deriving the parameters of market players from available real market data, especially maximum possible correlation (herding) and anti-correlation between the players’ opinions. The deviations of market prices from those predicted by the Black-Scholes model, such as smile and skew implied volatilities, are interpreted as the current values and limits of social influence of the market players, respectively. To the best of our knowledge, this is the first work that discriminates skew and smile phenomena. Our approach unifies and develops a further connection between trading, voters’ model, and statistical physics analogies of opinion dynamics.

I Introduction

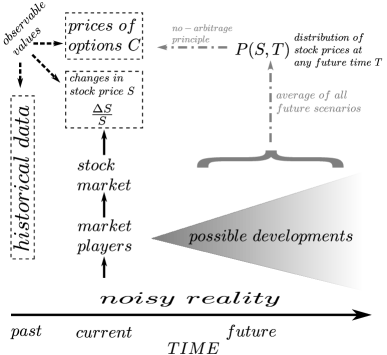

The world of finance provides a challenge to the modeling of stock price dynamics as a function of the most important market characteristics. The prices of financial markets depend on the state of the economy, recent news, stock trading regulations, and especially the mood of the market players. To describe stock price dynamics, one should develop a united analytic framework for behavior of market players and for market mechanisms that translate this behavior into actual prices of a stock and its options (i.e., future contracts with a profit that depends on the specific behavior of the stock price in the future). Consequently, the modeling of stock markets is part of a more general problem of community opinion dynamics Castellano et al. (2009)Feigenbaum (2003).

The current prices of options are affected by demand and supply of the market players according to their beliefs regarding the future evolution of the prices. The future distribution of prices imagined by the market players might be revealed by the prices of the optionsBlack and Scholes (1973)Merton (1973). For instance, the greater expected change of the price of a stock, the greater the change in the price of the corresponding options that benefit from the raising market. Financial markets supply a huge amount of historical prices of stocks and their options to analyze, including phenomena such as nationwide financial crises.

An analysis of historical market prices clearly demonstrates abrupt changes that result in greater probabilities than in Gaussian (normal) distributions for large price steps. The Gaussian distribution is used as a reference because it is a cumulative result of many random independent contributions and it is widespread. Deviations from the normal distribution are known as fat-tail distributionMandelbrot (1963). Moreover, the distribution of future prices imagined by the market players according to the options’ prices possesses the same fat-tail distribution. Non-Gaussian behavior of option prices is called volatility smile or skewDerman and Kani (1994). It is notable that the volatility smile developed significantly after the financial crisis of 1987Rubinstein (1994).

The abrupt changes of the prices indicate complex phenomena among the market players such as communicationEguiluz and Zimmermann (2000), herdingBanerjee (1992)Cont and Bouchaud (2000), or crashophobiaRubinstein (1994). These phenomena result in a collective response of the market players that might explain abrupt (non-Gaussian) changes of the pricesStanley et al. (2008)Schinckus (2013)Chakraborti et al. (2011). Their connection to markets makes these phenomena of great practical importance.

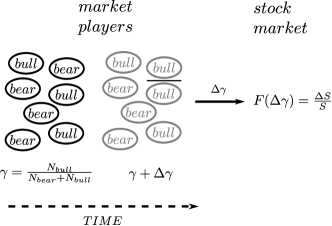

Stock players are historically separated into bulls and bears that act in favor of growing or reducing the market, respectively. This analogy unites the problem of the market players with the models of opinion dynamicsSznajd-Weron and Weron (2002)Cont and Bouchaud (2000). Collective behavior such as herding emerges due to the social influence between the playersBanerjee (1992)Vespignani (2012)Kocsis and Kun (2011)Eguiluz and Zimmermann (2000)Feigel (2008).

To test different models of voting or opinion dynamics against real data of the market prices, one should link the price of a stock with the amount of bulls and bears in the market players’ community. Previous attempts assumed a mere linear dependence of the price or change of the price on disbalance between the bulls and the bears in the communitySznajd-Weron and Weron (2002)Cont and Bouchaud (2000)Farmer and Joshi (2002)Feng et al. (2012). These assumptions generate prices with a fat-tail distribution in the case of herding of the market players. A comparison with real data and an explanation of the real phenomenon of volatility smile, however, require further clarification of the correct dependence between the stock price and the parameters of the market players, such as herding and social influence.

This Article presents a general description of stock and options’ price formation as an opinion dynamics of the market players to be either bulls or bears. The model shows a good fit to real data of option prices, both of stocks and indices. According to our results, the non-Gaussian distribution of prices depends on social influence between the market players and the initial collective memory on distribution of bears and bulls. Moreover, social influence and collective memory discriminate two different patterns, skew and smile, of the option prices. The model describes both Gaussian and non-Gaussian distributions, allowing a discussion of how the latter might appear as it happened during the 1987 financial crisis. We argue that a vote to price connection may be independent of exact market mechanisms.

We demonstrate market modeling using the seminal Black-Scholes model for pricing optionsBlack and Scholes (1973)Merton (1973). This model relies on two major assumptions. The first is that the relative change in the price of a stock in a time step is the sum of the deterministic change in monetary value and a Gaussian stochastic process that describes contribution of the market players:

| (1) |

where is a prime rate, is a Wigner process ( is a random variable of normal distribution with mean and standard deviation ). The parameter is called volatility.

The volatility of the Black-Scholes model solely describes the result of the decision making and trades of the market players. The stochastic process (1) corresponds to diffusion in space and, therefore, leads to a log normal distribution of the prices:

| (2) |

High values of volatility , therefore, correspond to greater changes of the stock prices at a given period of time.

The second assumption of the Black-Scholes model is the non-arbitrage principle, also called an assumption of the effective market, which allows one to link the dynamics of the stock prices with the price of future contracts, for instance put or call options. Consider a plain vanilla call option, which is the right to buy a stock at some strike price after some maturity time . The value of a call option with strike price as a function of the corresponding stock price at the maturity day is:

| (3) |

This expression describes the possibility to buy stock at price and immediately sell it at price . The value of the option is its average return multiplied by the expected change in monetary value until the maturity time:

| (4) |

where is the expected distribution of stock value at maturity time . The distribution of stock value is unequivocally linked to the dynamics of the stock price. Any deviation from (4) leads to arbitrage possibilities between investments in stock and its options.

The Black-Scholes model describes the future distribution of stock prices together with corresponding prices of the options as the functions of the single free parameter, volatility , see eq. (4). One might, therefore, calibrate volatility against current prices of options using eq. (4). This calibration is essential to use for pricing exotic or non-tradable options and to get unobservable parameters such as for hedging. However, the calibration of the Black-Scholes model demonstrates that single parameter volatility does not suffice to describe the dynamics of the observed market prices.

The real prices of options are presented by the implied volatility surface , which describes the deviation of the reality from the Black-Scholes modelGatheral and Taleb (2006). Implied volatility is defined for each strike price and maturity time as the volatility of the Black-Scholes model that corresponds to the current price of option :

| (5) |

where the Black-Scholes value of options is defined by eq. (4). The volatility surface is flat in case of a Black-Scholes market since eq. (4 has the same solution for all values of and . In reality, the volatility surface is far from being flat, indicating a non-Gaussian behavior of the stock price.

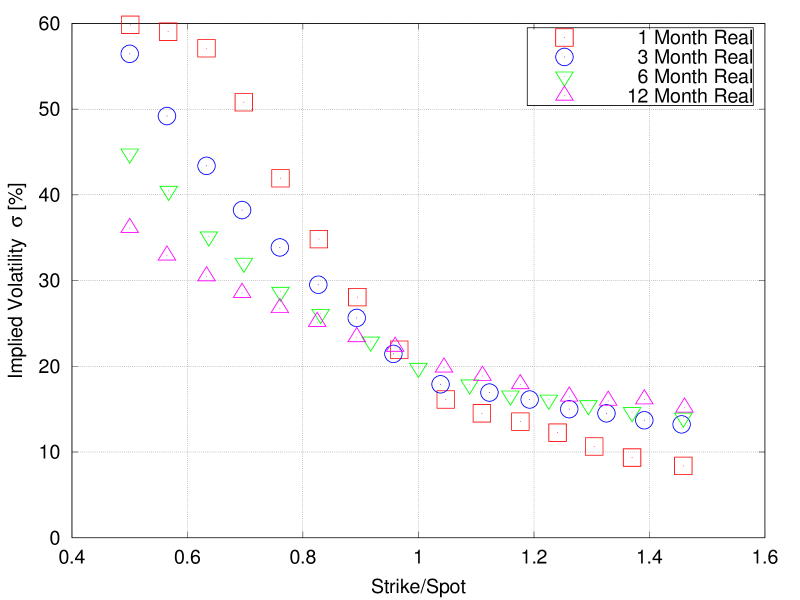

After the financial crisis of 1987, implied volatility as a function of strike price for a given maturity time generally demonstrates smile or skew behavior (see Fig. 1). This deviation from flat Black-Scholes volatility indicates that stock price dynamics is not Gaussian. Skew is more present in indices that are averages of many stocks, and smile is more common for stocks.

To describe the volatility smile phenomenon, one should correct the stochastic process (1) to include non-Gaussian dynamics. The main corrections include stochasticHull and White (1987), local volatilityDupire (1994)Derman and Kani (1994), and additional stochastic processes such as jumps or non-Gaussian behavior due to correlated behavior of the players (opinion aggregation)Gatheral and Taleb (2006). The stochastic volatility approach assumes volatility to be a stochastic process. Local volatility is the assumption that is a function of stock price and maturity time. These two corrections possess high practical value. However, they lack reasonable justification and cannot explain the nature of the volatility smile phenomenon. Human parameters such as crashofobia or herding are difficult to quantify and to compare with real data. That leads to arguments regarding the true nature of the volatility smile and the corresponding dynamic of market players.

Market micromodeling using agent simulations is an alternative approach for deriving the stochastic process of a stockBak et al. (1997)Samanidou et al. (2007)Wellman et al. (2004)Farmer and Joshi (2002)Muchnik and Solomon (2003). A market player is modeled to the level of its strategy to buy and sell available assets. Market mechanisms then translate the actions of many players into changes of the prices. An advantage of this approach is a clear understanding of all processes on all levels. A disadvantage is the great number of parameters and the difficulty to define completely human trading as the actions of an agent in simulation.

This work presents price dynamics as a function of the limited number of parameters with special emphasis on social influence (herding) between the market playersSznajd-Weron and Weron (2002)Cont and Bouchaud (2000). We present an alternative way to network topology to define social responsivity that is better integrated in classic modeling of market prices by stochastic processesBlack and Scholes (1973). The advantages of our method include both positive and negative social influence, boundaries, and dynamics. We achieve a good fit of the model with real market data and answer some-long standing questions, such as the origin and especially the difference between smile and skew in implied volatility surfaces.

When social influence is zero, our model converges to the Black-Scholes model result. This is due to the assumption that players without mutual effect compose a Gaussian Black-Scholes market.

The model is suitable for parallel Monte Carlo simulations. A Graphical Processing Unit (GPU) was used to calibrate the model’s parameters to fit real data. The model may be optimized further for practical needs.

Next, we describe the model in detail, present the results of fitting real volatility surfaces, and discuss the basic assumptions, implications, and relations of our model to other works.

| A | B |

|---|---|

|

|

II The Model

We model a market assuming the following general characteristics (see Fig 2). The market players collect available information and define their strategies to profit either from increasing or decreasing prices; the players that expect neutral market are neglected at this point. The players, according their choice, are called either bulls or bears. To decide their strategy, the players might observe historic and current prices of stocks together with the corresponding options. The market mechanisms translate the players’ decisions into real prices. The option prices depend on the non-observable distribution of future prices of the corresponding stock through non-arbitrage principle (4).

There are two steps to defining the stochastic dynamics of the stocks as a function of the parameters of the market players. First, we describe trading as a voting process with two choices to be either bear or bull. Second, we derive the price change of a stock as a function of the outcome of the voting process. We argue that under general circumstances this function is unique, disregarding the exact market mechanisms.

We can then derive option prices as a function of the parameters of the market players’ community. The distribution of the future stock prices is obtained by averaging stochastic stock price dynamics. It allows calculating the corresponding options prices and calibrating the model parameters against real market data.

II.1 Market of non-interacting players and Black-Scholes (Gaussian) prices

According to this model, the market players are separated into bulls that push the prices up and bears that try to move the market down. The ratio between bulls and all market players is:

| (6) |

where and are the total numbers of bulls and bears, respectively, and is the total number of players. The ratio changes with time since the players change their state occasionally (see Fig. 3). The trade advances by discrete steps in time.

To derive the stochastic process for the ratio of bulls to the total number of market players during a single trading step, we make two assumptions. First, the number of transactions is proportional to the number of possible interactions between bulls and bears . Thus, changes either by a positive or by a negative step:

| (7) |

Second, in the absence of communication, the probability of a player to change its state (from bear to bull or vice versa) is assumed equal for all players. Consequently, the probabilities of positive and negative steps are:

| (8) | |||

, respectively, because is the ratio of bulls in the community (6).

Following (7) and (8), the stochastic dynamics of bull ratio as a generalized Wigner process:

| (9) |

taking into account that and , is:

| (10) |

where is an arbitrary constant and . The main properties of (10) are the limited range of and zero drift term in the case of neutral population . The latter is a direct consequence of the second assumption, i.e., an unbiased population (equal probability for all players). In general, biased population equilibrium occurs at different values , because the step probabilities become and .

Having a stochastic process for (10), we are now searching for a market function that translates the voting process into stock price dynamics of the Black-Scholes type:

| (11) |

To find this function, we use Ito’s lemma, describing the differential of a time-dependent function of a stochastic process (9):

| (12) |

The requirement (11) means that coefficients of both terms in (12) are constant, similar to Eq. (11).

Following (11) and (12), the market function that translates the voting process (10) into Black-Scholes stock price dynamics is:

| (13) |

where is a numeric coefficient. Substituting (13) in (12), we get:

| (14) |

The change in the price of a stock as a function of is:

| (15) |

Integration of (15) gives:

| (16) |

It follows from analogy between (14) and (11) if:

| (17) | |||

and assuming that:

| (18) |

the noise of a stock is the noise of the voting process and the market is deterministic in the sense that it does not contribute with additional noise.

The stochastic process for the ratio of bulls to the total number of the market players (Eq. 10) should be modified to include the deviation of stock price dynamics from the Gaussian process (eq. 11). We argue that the expression Eq. 15 holds for any modification of Eq. 10. It is true if the market is described by a function of the vote outcome and is independent of how it was obtained.

II.2 Market players with social influence

To extend the model to include stock price dynamics that is different from the Black-Scholes model (11), we introduce the social influence between the market players. Social influence means that the state of a player depends on the state of the other players rather than being bull or bear with probabilities and independent of the environment.

We describe the interaction between market player and any other randomly selected player as follows: The probability per contact of player to be bear () depends on the state of player . This conditional probability is given by:

| (19) |

where is the state of player ( for bull state and for bear state) and parameter and is the probability per contact of player being bear given player is bear or bull correspondingly, regardless of the state of player prior to the interaction with player .

In the mean field approximation, players exposed equally to the state of all other players (), Eq. 19 become

| (20) |

Using the definition for , we get

| (21) |

Therefore, we can derive an expression for in terms of the conditional probabilities and

| (22) |

because in steady state the ratio of bull players to the total number of the players equals to the probability of players to be bull (see Fig. 4).

To calculate social influenceOster et al. (2015), let us estimate the response of the homogeneous community to the injection of a group of relative size and unconditional average state . An unconditional response is independent of other players. The mean field eq. (21) in this case becomes:

because a player possesses probabilities and to interact with a responsive and an unconditional player, respectively. Eq. (II.2) can be rewritten as:

| (24) |

where and, therefore, indicates the strength of the injection.

The responsivity of average ratio of bulls to the total number of market players to the injection of the unconditional group of strength , following (24), is:

| (25) |

For small perturbations one gets:

| (26) |

where and are the average ratios of bulls prior and after the perturbation occurs. Social responsivity vanishes if because in this case the players possess probabilities to be bear independent of the state of the other players. Responsivity diverges at . At this point, a single individual’s change of state causes a phase-like transition of the state of the entire community.

Social responsivity (25) depends on the single herding parameter:

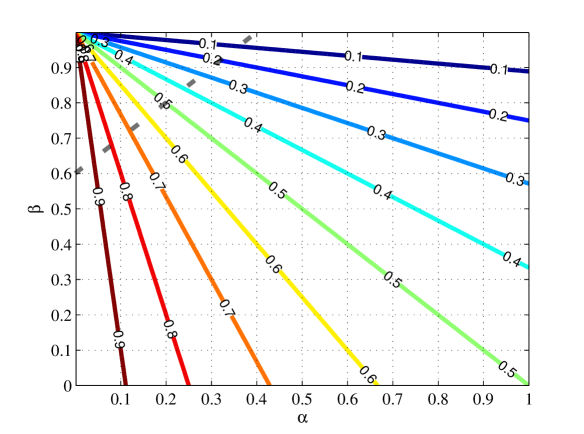

| (27) |

with range . It might be called herding because the contribution of unconditional group to of responsive players is proportional to ; see (24). Thus, it indicates how much the responsive players are affected by a single member of the injected unconditional group. For comparison, the herding parameter is defined in Cont and Bouchaud (2000) using community graph topology as a ratio of the community that are connected to a single member and form a cluster of correlated behavior. The main advantage of is that it describes both positive and negative social influence.

The absolute value of the herding parameter might be limited in real communities because high social responsivity assumes a high level of direct or indirect information exchange in community. A high level of information flow is limited because of the stochastic nature of market news, the topology of communication channels, and the tendency to hide individual strategies.

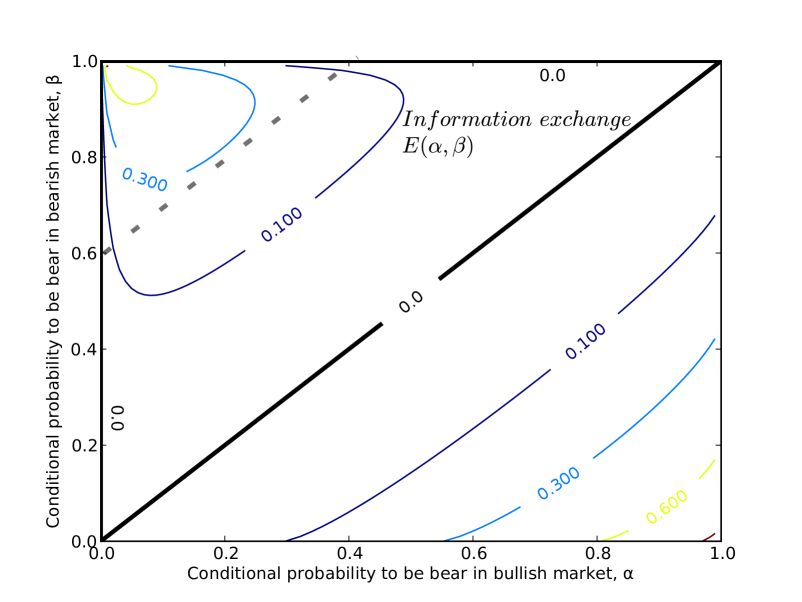

The mutual information of the players can be a measure of information exchange in the trading community. Mutual information between market players and is the amount of known information about state of if state of is known for certain. Greater mutual information indicates either direct or indirect information flow. The direct information flow assumes communication, while the indirect information flow assumes synchronization by common external signal. Mutual information makes possible to separate markets with completely random and highly correlated choices of the players, corresponding to the lack of social influences and developed social influences, respectively.

Mutual information in a community of homogeneous players , see Fig. 5, is defined by probabilities , , and for four possible interactions in the community:

These probabilities are:

| (29) |

following the definition of conditional probabilities and . Substituting (29) in (LABEL:SMmutinfo1) we get:

The relationship between herding parameter , ratio of bulls (22), and mutual information (LABEL:mutinfo2) is presented in Figs. 4 and 5. Communities with the same herding might possesses arbitrary values of . The specific value of herding, however, constraints the possible maximum value of mutual information in the community and, vice versa, the specific value of mutual information limits the possible herding. For instance, the mutual information in community is:

| (31) |

These constraints are valid for social influence (25), making impossible to achieve the maximum value at ( point).

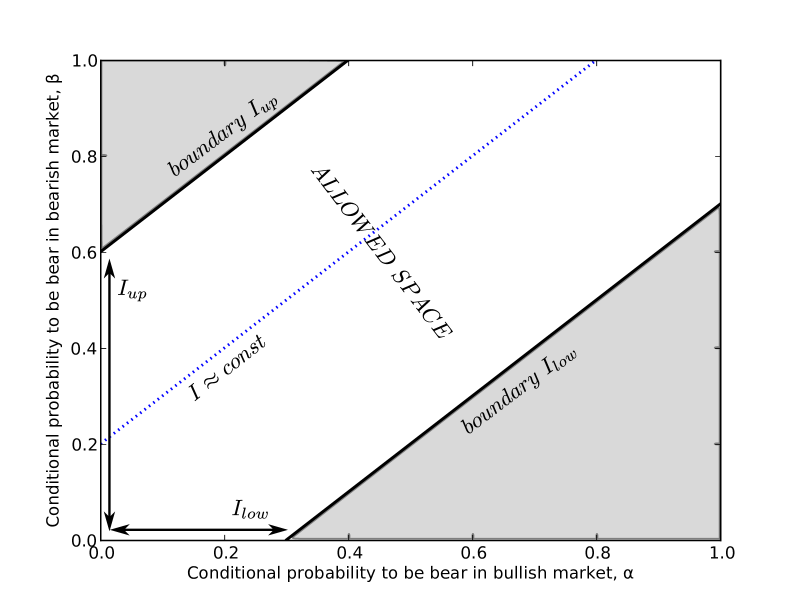

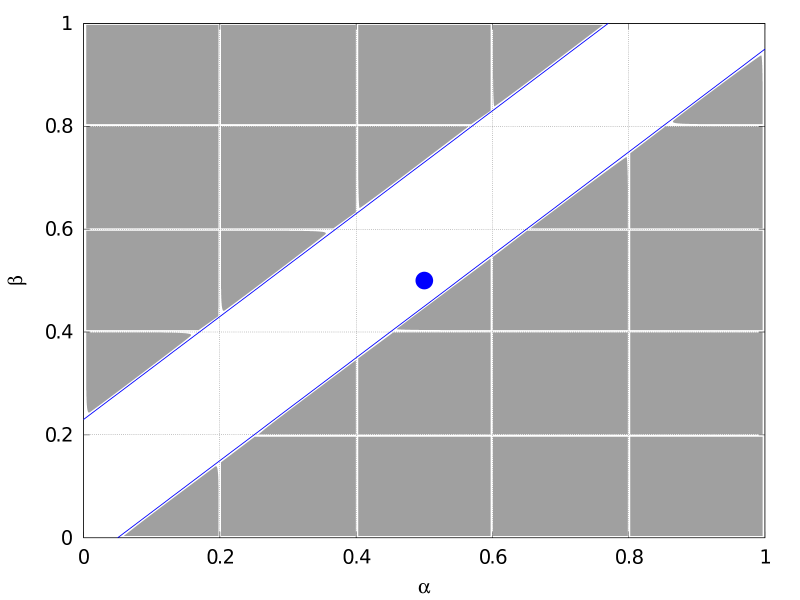

II.3 General Market Model

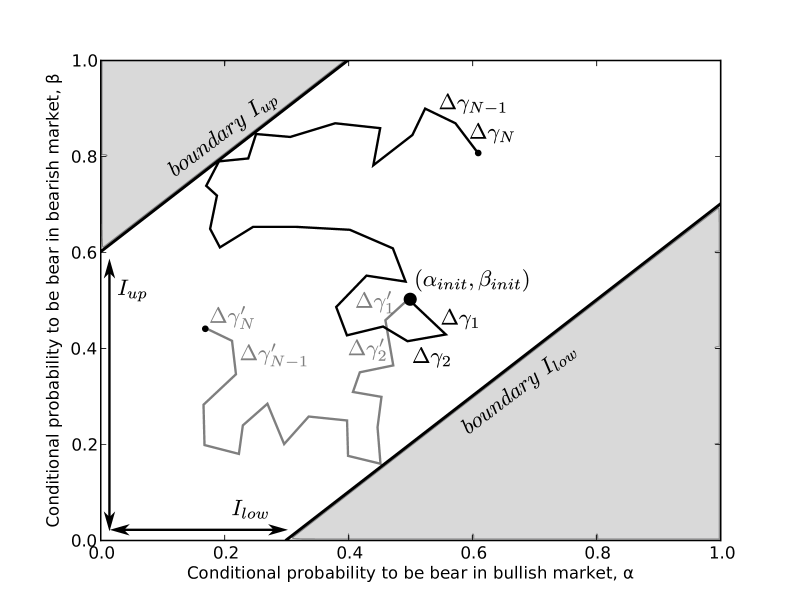

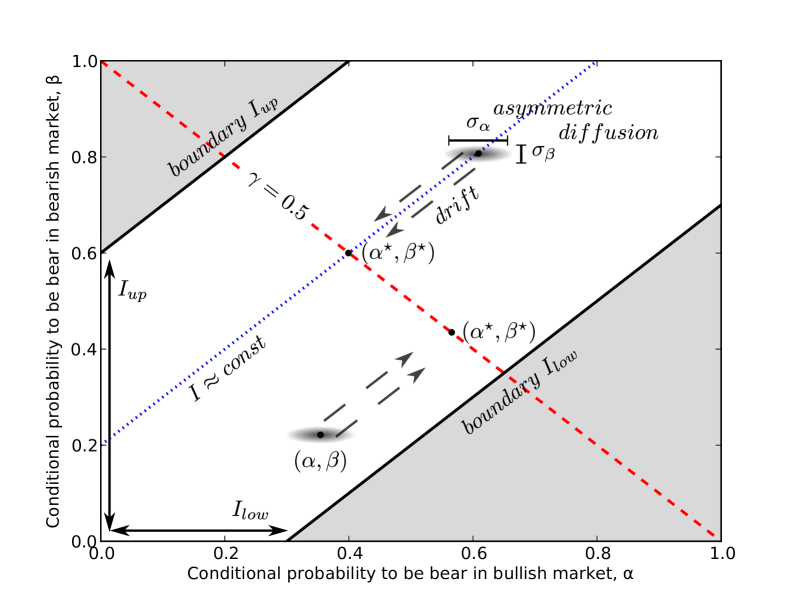

The community of the market players is considered as a point in the space of conditional probabilities , see Fig. 6. The dynamics is limited to a subspace that is bounded by two mutual influence limits, namely . On the mutual influence boundaries, we have reflecting boundary conditions.

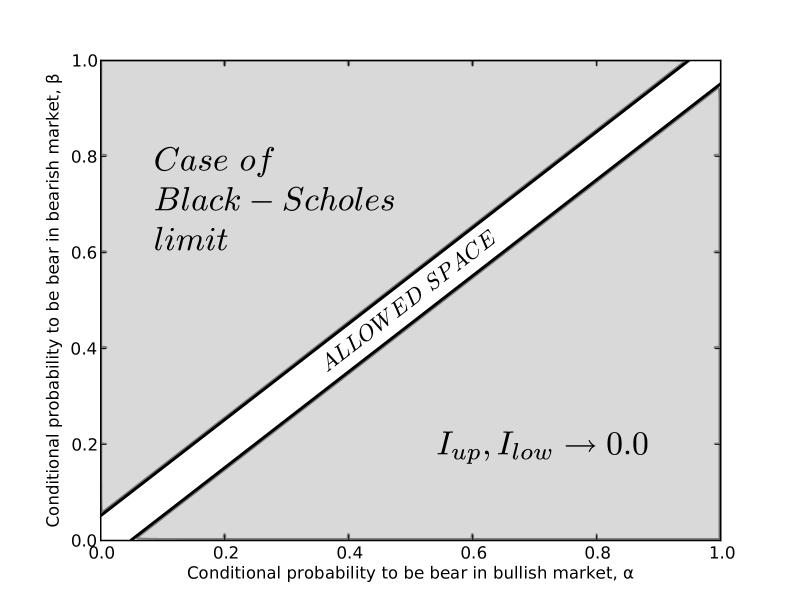

If then , there is no mutual influence and the players’ state is independent of other players. In this case, the model converges to the Black-Scholes result, since the dynamics is described by asymmetric random walk (Eq. 10) and the stocks’ price exhibit a log-normal behavior (definition of ).

In the general case , the community propagates by the stochastic process:

| (32) | |||||

starting from some initial point . It is derived assuming that, if the market is fixed to either bullish or bearish state, the ratio of bears ( and , respectively) behaves analogous with (Eq. 10). Moreover, in the case of random responses , the process (Eq. II.3) should exactly converge to (Eq. 10) taking into account (Eq. 22).

The parameters and in (II.3) indicate equilibrium values of and in case noise term vanishes. The choice of is ambiguous. In this work, we assume that this point corresponds to neutral population and possesses the same herding coefficient as the current state of the trading community:

| (33) | |||||

The sensitivity to specific values of on our results is low; it was checked by assuming .

The stock price is updated at each time step of the process. The initial value is set to . The simulation proceeds by steps in time of arbitrary small value . At each step, the next coordinates are calculated:

| (34) | |||||

| (35) | |||||

where and are defined by (33). New coordinates lead to a new value of :

| (36) |

following Eq. 22. The new stock price is calculated using Eq. (15):

| (37) |

Then, call option prices are calculated for different strike prices

| (38) |

where is an average over different runs for a set of times and strike prices.

Finally, implied volatility is calculated solving Eq. 5 by iterations. The prime value is used only while calculating implied volatility. The prime is neglected in the voting process itself. This volatility value is reduced by constant

| (39) |

This new parameter essential to fit the real values of volatility. It can be interpreted as a reduction of volatility by market regulations.

| A | B |

|

|

| C | D |

|

|

The model’s parameters are summarized as follows:

-

•

- volatility-like parameters for market players’ vote in conditional probability to be bear in a bullish market.

-

•

- volatility-like parameters for market players’ vote in conditional probability to be bear in a bearish market.

-

•

- lower boundary of propagation in space and

-

•

- upper boundary of propagation in space

-

•

- prime is known though it can be treated as a free parameter

-

•

- lowering of implied volatility of the market players by market regulations. This parameter is not fitted but calculated at each run.

-

•

- initial coordinate of the population

-

•

- initial coordinate of the population

-

•

- coefficient between votes and stock prices’ change

These parameters define the simulation and corresponding implied volatility surface . The implied volatility surface for specific parameters’ values is derived via a Monte Carlo simulation enforced by GPU processingWang et al. (1995). The resulting volatility surface is compared with the actual surface and multiple runs are made to adjust the parameters using a simplex optimization methodNelder and Mead (1965) fro GNU Scientific LibraryGough (2009).

III Results

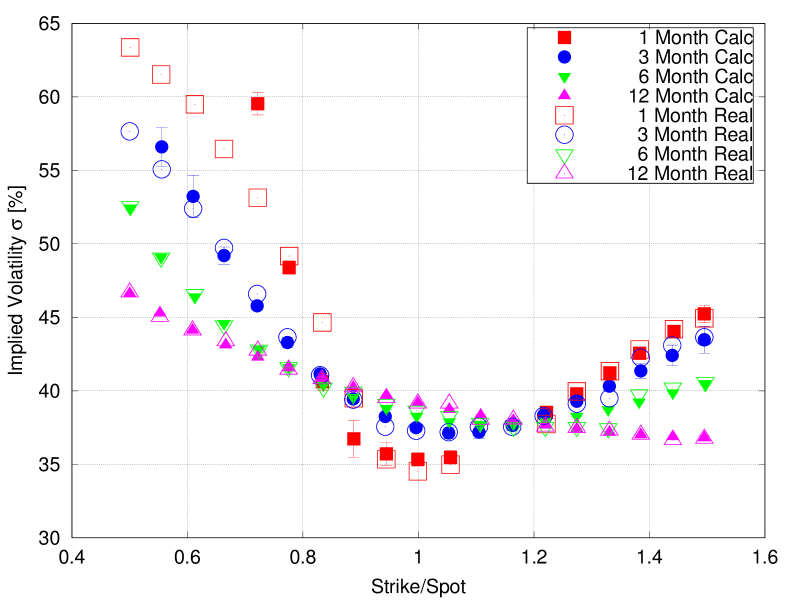

The results include sets of the model parameters together with the corresponding calculated volatility surfaces that provide the best match of the real implied volatility surfaces either of skew or smile types. Calibrating the model’s parameters against real market data accomplishes two main tasks. First, it demonstrates the model’s ability to describe a wide range of the real volatility surfaces for practical trading or hedging. Second, it identifies the main parameters of the model responsible for skew or smile volatility for better understanding of these phenomena.

Calibration is done either by using a single set of parameters’ values for the entire implied volatility surface or by using different parameters’ values for implied volatilities with different maturity times. The latter is done because we cannot fit all surface by a single set of parameters. Consequently, the parameters may be functions of maturity time, similar to the definition of implied volatility.

The model’s parameters were calibrated against real implied volatility surfaces corresponding to the S & P index (SPX) at different times and Vodafone Company (VOD) stock:

-

•

SPX index at 12/26/01 with maturities of 1,3,6, and 12 months

-

•

VOD stock at 12/27/01 with maturities of 1,3,6, and 12 months

-

•

SPX index at 09/15/05 with maturities of 1 day together with 1,3,6,15 months

These cases include implied volatilities with both smile and skew at different strengths.

The index is an average of many stocks; therefore, it represents well the average properties of the market. On the contrary, a single stock such as VOD can deviate from average market behavior and from general assumptions of the model.

The skew pattern of SPX was successfully fitted by a single set of parameters that are independent of time and price value. On the contrary, the smile pattern of VOD and early SPX cannot be fitted be a single set of parameters; therefore, it was fitted separately for each maturity time.

III.1 SPX 12/26/01

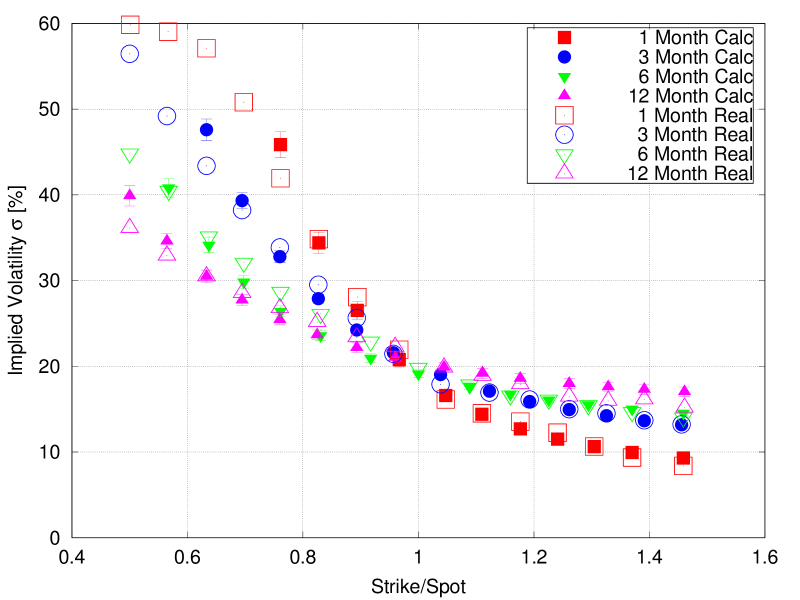

The implied volatility surface of the SPX index from 12/26/01 demonstrates clear skew behavior at maturity times 1,3,6, and 12 months. First, we fit the surface with the entire set of model’s parameters (see Fig. 7 and Table 1). The results include both mean and standard deviation values obtained over many calibration runs.

Small standard deviations (see Table 1) of the calibrated herding limits, volatilities and , initial position of the community , and market volatility correction indicate the important role of these parameters. The real value of prime at 12/26/01 is within the error range of the result. Interestingly, the initial position of the population is almost neutral and coefficient .

| Parameter | Optimized value |

|---|---|

| 0.24 0.009 | |

| -0.03 0.006 | |

| 1.37 0.04 | |

| 0.74 0.016 | |

| 0.069 0.026 | |

| 0.50 0.004 | |

| 0.51 0.005 | |

| 1.09 0.03 | |

| 0.99 0.04 |

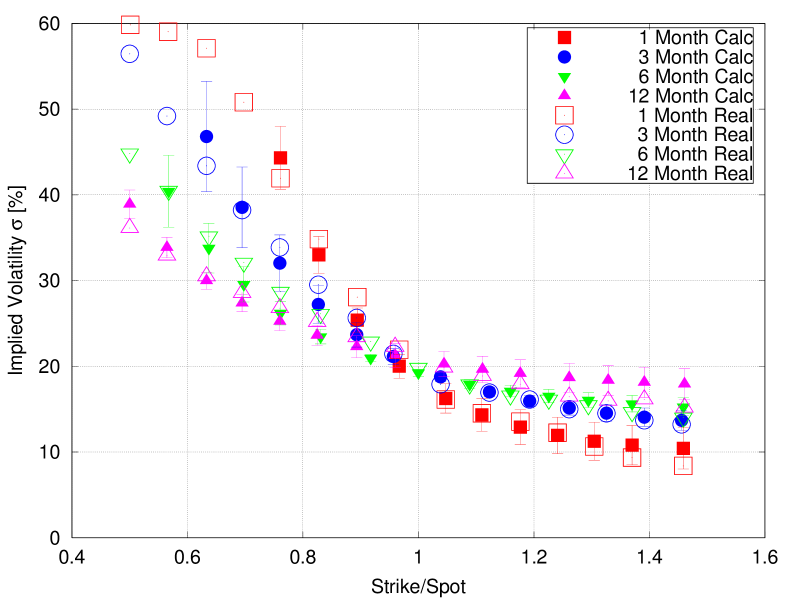

To highlight the most important parameters and to reduce the calibration time, some parameters where fixed with predefined values. Based on the previous results using the complete set of optimized parameters, the initial position is chosen to be and . The value of prime corresponds to its real value at that time (12/26/01). This reduction barely affects the quality of the fit (see Fig. 8 and Table 2).

| Parameter | Optimized value |

|---|---|

| 0.23 0.03 | |

| -0.05 0.03 | |

| 1.38 0.13 | |

| 0.74 0.07 | |

| 0.88 0.05 |

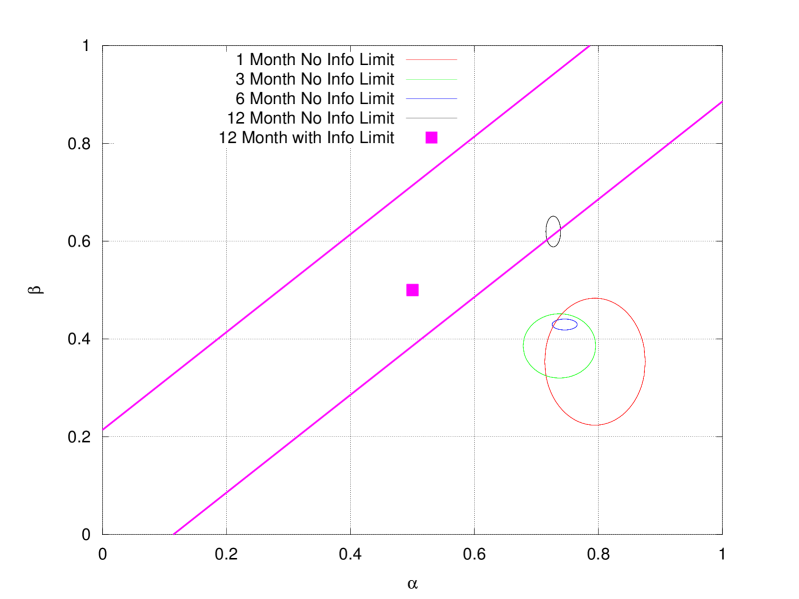

The derived herding limits indicate that the decisions of the market players to be either bull or bear tend to correlate with market behavior. The allowed space for diffusion is shifted toward region that includes state of the maximum correlation (see Figs. 9 and 6). On the other hand, there is no possibility of exact correlations with the market due to social influence limits.

III.2 VOD 12/27/01

The implied volatility of the Vodafone Company (VOD) demonstrates clear smile behavior at maturity times of 1,3, and 6 months. The smile effect, however, reduces with greater maturity time. The implied volatility with maturity 1 year is of the skew type. As in the SPX case, the results are obtained over many calibration runs and include both the mean and the standard deviation value for optimized parameters.

We found it impossible to fit the entire implied volatility surface of VOD with a single set of model parameters. Each maturity time then was fitted separately (see Table 3). For maturity times of 6 and 12 months, additional solutions were found (see Table 4). Convergence depends on the initial choice of parameters.

The fit of strong smile pattern of single maturity time depends more on the initial position of the population, while moderate smiles and skew can be fitted both by initial condition and by herding limits (see Fig. 10). The initial position may indicate a starting value of herding of the market players together with an excess of demand (disbalance between bears and bulls in the players’ community).

| Parameter | 1 Month | 3 Month | 6 Month | 1 Year |

|---|---|---|---|---|

| 1.74 0.2 | 1.90 0.25 | 1.31 0.04 | 1.01 0.06 | |

| 0.64 0.25 | 0.83 0.084 | 0.85 0.03 | 0.91 0.01 | |

| 0.79 0.08 | 0.74 0.06 | 0.74 0.02 | 0.72 0.01 | |

| 0.35 0.13 | 0.38 0.06 | 0.43 0.01 | 0.62 0.03 | |

| 1.00 0.26 | 1.06 0.26 | 1.05 0.08 | 1.13 0.20 | |

| 0.17 0.22 | 0.44 0.1 | 0.21 0.06 | 0.29 0.10 |

| Parameter | 6 Month | 1 Year |

|---|---|---|

| 0.29 0.06 | 0.21 0.03 | |

| -0.11 0.08 | -0.11 0.02 | |

| 1.28 0.06 | 1.33 0.05 | |

| 0.91 0.04 | 1.07 0.03 | |

| 7.6e-03 5.1e-04 | 2.3e-03 5.8e-04 |

There are multiple fit solutions for maturity times 6 and 12 months. A mild smile and an individual skew might be fitted either by herding limits or by initial position of the players’ community. The values of are closer to each other in Table 3 than in the initial position. This, together with SPX results and general reduction of social influence-like phenomena with time, favors the assumption of the herding limits solution for skew patterns.

The smile of implied volatility corresponds to a high value of the initial anti-herding between the market players, see 10.

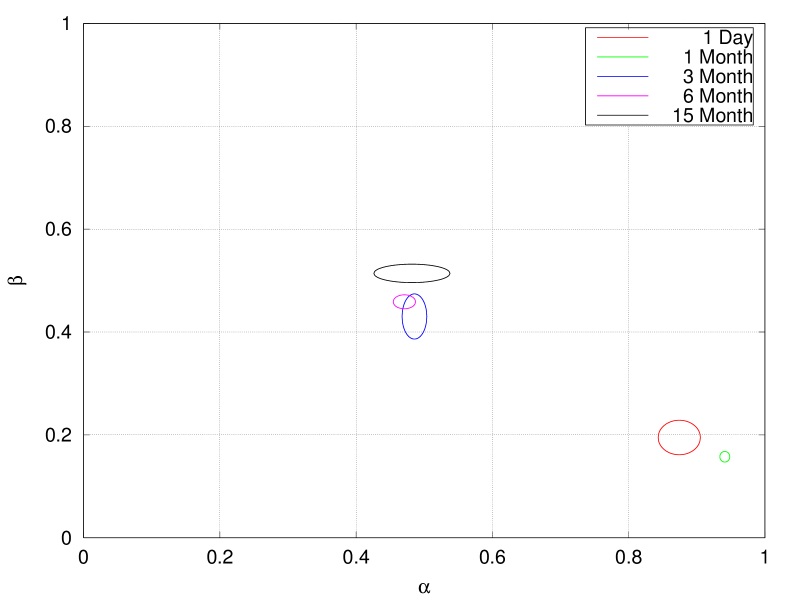

III.3 SPX 09/15/05

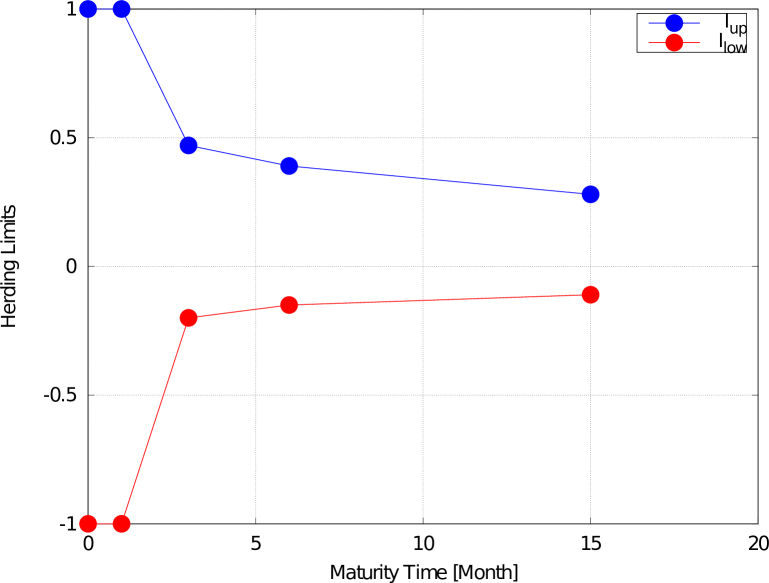

The SPX index 09/15/05 possesses a smile type of implied volatility for maturity times of 1 day and 1 month, together with a skew type for later maturity timesGatheral and Taleb (2006). The results of parameter calibration are presented in Table 5. The calibration of skew was done with initial conditions to favor the influence of herding limits (see Fig. 9).

| Parameter | 1 Day | 1 Month | 3 Month | 6 Month | 15 Month |

|---|---|---|---|---|---|

| 1 | 1 | 0.47 0.06 | 0.39 0.04 | 0.28 0.02 | |

| -1 | -1 | -0.20 0.05 | -0.15 0.01 | -0.11 0.01 | |

| 24.0 0.08 | 5.6 0.01 | 1.54 0.09 | 1.46 0.04 | 1.45 0.04 | |

| 0.97 0.039 | 0.62 0.02 | 0.61 0.08 | 0.80 0.04 | 0.87 0.03 | |

| 0.87 0.030 | 0.94 0.007 | 0.48 0.018 | 0.47 0.02 | 0.48 0.05 | |

| 0.19 0.033 | 0.16 0.01 | 0.43 0.04 | 0.46 0.01 | 0.51 0.02 | |

| 0.005 0.016 | 0.79 0.052 | 1.19 0.08 | 1.11 0.02 | 1.09 0.07 | |

| -0.007 0.036 | 0.40 0.02 | 1.30 0.07 | 1.33 0.06 | 1.33 0.07 |

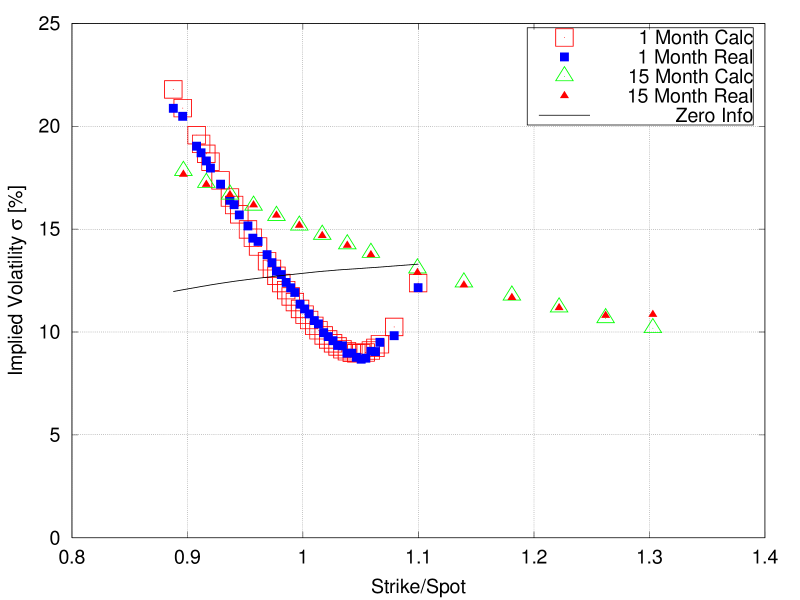

The fit of implied volatilities with 1 month and 15 month maturity times is presented in Fig. 11. The fit of the smile mainly depends on the initial position of the market players. The skew depends more on imposed herding limits. A stronger limit can bring implied volatility to almost flat Black-Scholes form.

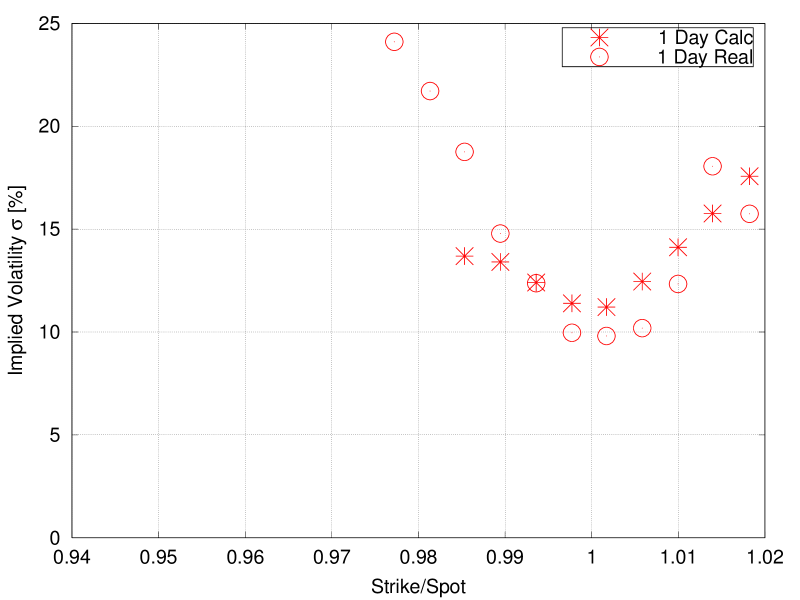

The strong smile at 1 day maturity can be fitted (see Fig. 12), though it requires extreme values of volatility relative to other maturity times (see Table 5. The initial position indicates that the market players anti-correlated with the market.

Following results 5, the initial position of the community converges to the region of small social influence with maturity time (Fig. 13). It is clearly separated into two groups of early and later maturity times.

Herding limits as a function of time according to Table 5 are shown in Fig. 14. The limits converge to with time and bring the market players’ community closer to the Black-Scholes limit. The lower absolute value of than at later maturity times indicates a positive correlation between the market behavior and players’ predictions.

Market players’ dynamics, following the results for SPX indices and VOD stock, at early maturity times, may possess a high value of social influence. This is reasonable, since information about the current state of the community is preserved for a short time into the future. Longer maturity times are characterized by strong herding limits. The initial position of the population lacks almost any social influence value. Indeed, no memory is preserved for a long time and, consequently, the market envisioned by its players converges to the Black-Scholes limit with maturity time.

IV Discussion

To corroborate the basic assumptions of the model, let us compare the implied volatility surfaces of the SPX index, the VOD stock, and the results of this work. The model, after appropriate calibration of its parameters, successfully fits real implied volatility surfaces of both smile and skew types. The model’s parameters describe the community of the market players together with the market that transforms the players’ action into observable prices. The obtained description of the market, together with players’ community, is analyzed in light of the model assumptions and common sense.

The assumption of the Black-Scholes (log normal) price dynamics in the case of random (zero social influence) acts of the market players is supported both by properties of real implied volatility surfaces and the results of this work. The properties of market players for the purpose of evaluation options with greater maturity times are less correlated with their current values. Indeed, implied volatilities converge to the Black-Scholes “flat” form with maturity time. The same happens for calibrated herding limits that converge to their Black-Scholes limit with maturity time (see Figure 14).

The assumptions of market mechanism in the form of deterministic function (without a stochastic term) are supported by the ability to fit real implied volatility surfaces. Each parameter of the model is justified and essential. Moreover, the model requires an additional heuristic parameter to match reality. This parameter, however, is justified as market’s reduction of market players’ volatility by regulations for stability and crisis prevention.

The distinctive explanations for skew and smile phenomena as limits and initial values of herding, respectively, agree with previous association of skew and smile implied volatility surfaces with indices and stocks. The index is an average price of multiple stocks and, therefore, better presents the average properties of the market. Consequently, in the case of indices, the limits on herding should be stronger and the dependence on initial value of herding is low. Contrary, individual stock might possess broader limits on herding and its value for short maturity times.

Upper and lower limits on herding correspond to the maximum of the correlation and anti-correlation of market players’ opinions, respectively. The greater the greater the possibility of collective phenomena of the players.

The definition of market player strategies using conditional probabilities stems from similar techniques of the game theoryNowak and Sigmund (2004). The question of optimal strategy and its evolutionary stability remains under discussionPress and Dyson (2012). An analysis of the market may contribute to this discussion due to the huge amount of available data. On the other hand, there is also an interesting discussion whether evolution is relevant for the market playersFarmer (2002)da Cruz and Lind (2013)Gao et al. (2013)Shi et al. (2013)Durrett et al. (2012)Zhu et al. (2011)Dong (2007).

The model’s limitations and drawbacks are the following: the transaction costs and other players’ states but bull or bear were not taken into account; equal financial weight of the players was assumed; and the prime interest rate was omitted in the voting process of the market players and considered only as monetary value change during calculating implied volatility. The prime converges close to its real value, however, if assumed to be a free parameter. In addition, we did not take into account near neighbors’ topological constraint. A single market player may affect any other player with a limit on the total amount of social influence it generates. The excessive communication abilities of the present time and a good match of the model results with real prices justify this approach.

This work predicts the stochastic process for price dynamics that depends on a small number of well-justified parameters. It is an advantage over approaches of localDerman and Kani (1994) and stochastic volatilitiesHull and White (1987). The latter together with completely heuristic descriptions of implied volatility may be advantageous for practical needs by their speed. Our model, however, can be accelerated by further massive parallelization and, in general, is comparable to any Monte-Carlo based trading tools.

The results of this work are potentially relevant for any agent-based simulationFeng et al. (2012)Bertella et al. (2014)Kim and Kim (2014)Liu et al. (2014)Chen et al. (2014)Wei et al. (2013)Schmitt et al. (2012)Chakraborti et al. (2011) because the model’s major assumptions are independent of the market microstructure. Moreover, the model is impervious to modifications. The need for a function that transforms the voting process to log normal requires the terms and to depend on each other and prevents their arbitrary modifications. Moreover, neglecting (10) and writing the process in the form leads to unrealistic bounded expression for the price–vote relation instead of (13).

The results of this work support the relation of information technologies (IT) contribution to the financial crisis of 1987. The implied volatilities of the SPX index acquired significant skew during this crisisRubinstein (1994). According to our model, it indicates the growth of possible social influence of the market players. The latter might be a consequence of extensive IT technology modification of the markets and trading at that time. It corroborates that information-like phenomena are the cause rather than the consequence of the crisis.

The herding of the market players might be a new tradable parameter, similar to the volatility index (VIX)Brenner and Galai (1989), which describes the past values of market’s volatility. On the contrary, in this work, herding describes possible future developments of the market players’ community. It may be an important market indicator for crisis analysisSornette (2003). Moreover, herding can be estimated by other means from internet responses and artificial market experiments for comparison with the market, or even for predicting the market behavior.

V Conclusion

We presented a framework for modeling the market prices’ dynamics based on opinion dynamics and herding in the trading community. This framework uses the social influence and mutual information between the players as a quantitative measure of the herding effect and corresponding deviation of the prices from the Black-Scholes model. The derived relation between opinion dynamics and price formation is general and argued to be independent of exact market mechanism. The calculated option prices fit real market data and can be useful for trading and hedging. In addition, the estimated herding from market data can be compared with herding from other sources such as artificial markets, news, or social networks.

References

- Castellano et al. (2009) C. Castellano, S. Fortunato, and V. Loreto, Rev. of Mod. Phys. 81, 591 (2009).

- Feigenbaum (2003) J. Feigenbaum, Rep. on Prog. in Phys. 66, 1611 (2003).

- Black and Scholes (1973) F. Black and M. Scholes, J. of Pol. Econ. 81, 637 (1973).

- Merton (1973) R. Merton, Bell J. of Econ. 4, 141 (1973).

- Mandelbrot (1963) B. Mandelbrot, J. of Business 36, 394 (1963).

- Derman and Kani (1994) E. Derman and I. Kani, Tech. Rep., Goldman Sachs (1994).

- Rubinstein (1994) M. Rubinstein, The J. of Finance 49, pp. 771 (1994).

- Eguiluz and Zimmermann (2000) V. Eguiluz and M. Zimmermann, Phys. Rev. Lett. 85, 5659 (2000).

- Banerjee (1992) A. Banerjee, Quant. J. of Econ. 107, 797 (1992).

- Cont and Bouchaud (2000) R. Cont and J. Bouchaud, MacroEcon. Dyn. 4, 170 (2000).

- Stanley et al. (2008) H. E. Stanley, V. Plerou, and X. Gabaix, Physica A: Stat. Mech. 387, 3967 (2008).

- Schinckus (2013) C. Schinckus, Cont. Phys. 54, 17 (2013).

- Chakraborti et al. (2011) A. Chakraborti, I. M. Toke, M. Patriarca, and F. Abergel, Quant. Finance 11, 991 (2011).

- Sznajd-Weron and Weron (2002) K. Sznajd-Weron and R. Weron, Int. J. of Mod. Phys. C 13, 115 (2002).

- Vespignani (2012) A. Vespignani, Nature Phys. 8, 32 (2012).

- Kocsis and Kun (2011) G. Kocsis and F. Kun, Phys. Rev. E 84 (2011).

- Feigel (2008) A. Feigel, J. of Theor. Biol. 254, 768 (2008).

- Farmer and Joshi (2002) J. D. Farmer and S. Joshi, J. of Econ. Behav. & Org. 49, 149 (2002).

- Feng et al. (2012) L. Feng, B. Li, B. Podobnik, T. Preis, and H. E. Stanley, Proc. of Nat. Acad. of Sci. 109, 8388 (2012).

- Gatheral and Taleb (2006) J. Gatheral and N. Taleb, The Volatility Surface: A Practitioner’s Guide, Wiley Finance (Wiley, 2006), ISBN 9780470068250.

- Hull and White (1987) J. Hull and A. White, The J. of Finance 42, 281 (1987).

- Dupire (1994) B. Dupire, Risk Mag. pp. 18–20 (1994).

- Bak et al. (1997) P. Bak, M. Paczuski, and M. Shubik, Physica A: Stat. Mech. 246, 430 (1997).

- Samanidou et al. (2007) E. Samanidou, E. Zschischang, D. Stauffer, and T. Lux, Rep. on Prog. in Phys. 70, 409 (2007).

- Wellman et al. (2004) M. Wellman, D. Reeves, K. Lochner, and Y. Vorobeychik, J. of Art. Intell. Res. 21, 19 (2004).

- Muchnik and Solomon (2003) L. Muchnik and S. Solomon, Physica Scripta 2003, 41 (2003).

- Oster et al. (2015) E. Oster, E. Gilad, and A. Feigel, submitted (2015).

- Wang et al. (1995) L. Wang, S. L. Jacques, and L. Zheng, Comp. Meth. and Prog. in Biomed. 47, 131 (1995).

- Nelder and Mead (1965) J. A. Nelder and R. Mead, The Comp. J. 7, 308 (1965).

- Gough (2009) B. Gough, Gnu Scientific Library Reference Manual (Network Theory Ltd., 2009).

- Nowak and Sigmund (2004) M. A. Nowak and K. Sigmund, Science 303, 793 (2004).

- Press and Dyson (2012) W. H. Press and F. J. Dyson, Proc. of Nat. Acad. of Sci, 109, 10409 (2012).

- Farmer (2002) J. D. Farmer, Ind.l and Corp. Change 11, 895 (2002).

- da Cruz and Lind (2013) J. P. da Cruz and P. G. Lind, Phys. Lett. A 377, 189 (2013).

- Gao et al. (2013) Y.-C. Gao, S.-M. Cai, L. Lu, and B.-H. Wang, Physica A: Stat. Mech. 392, 3385 (2013).

- Shi et al. (2013) F. Shi, P. J. Mucha, and R. Durrett, Phys. Rev. E 88 (2013).

- Durrett et al. (2012) R. Durrett, J. P. Gleeson, A. L. Lloyd, P. J. Mucha, F. Shi, D. Sivakoff, J. E. S. Socolar, and C. Varghese, Proc. of Nat. Acad. of Science 109, 3682 (2012).

- Zhu et al. (2011) C.-P. Zhu, H. Kong, L. Li, Z.-M. Gu, and S.-J. Xiong, Phys. Lett. A 375, 1378 (2011).

- Dong (2007) L. Dong, Physica A: Stat. Mech. 376, 573 (2007).

- Bertella et al. (2014) M. A. Bertella, F. R. Pires, L. Feng, and H. E. Stanley, Plos One 9 (2014).

- Kim and Kim (2014) M. Kim and M. Kim, Plos One 9 (2014).

- Liu et al. (2014) Y.-F. Liu, W. Zhang, and H.-C. Xu, Econ. Mod. 39, 232 (2014).

- Chen et al. (2014) S. Chen, H. Hu, J. Chen, and Z. Chen, Int. J. of Mod. Phys. C 25 (2014).

- Wei et al. (2013) J. R. Wei, J. P. Huang, and P. M. Hui, Physica A: Stat. Mec. 392, 2728 (2013).

- Schmitt et al. (2012) T. A. Schmitt, R. Schaefer, M. C. Muennix, and T. Guhr, Europ. phys. Lett. 100 (2012).

- Brenner and Galai (1989) M. Brenner and D. Galai, Fin. Anal. J. 45, 61 (1989).

- Sornette (2003) D. Sornette, Phys. Reports 378, 1 (2003).