U.S. stock market interaction network as learned by the Boltzmann Machine

Abstract

We study historical dynamics of joint equilibrium distribution of stock returns in the U.S. stock market using the Boltzmann distribution model being parametrized by external fields and pairwise couplings. Within Boltzmann learning framework for statistical inference, we analyze historical behavior of the parameters inferred using exact and approximate learning algorithms. Since the model and inference methods require use of binary variables, effect of this mapping of continuous returns to the discrete domain is studied. The presented analysis shows that binarization preserves market correlation structure. Properties of distributions of external fields and couplings as well as industry sector clustering structure are studied for different historical dates and moving window sizes. We found that a heavy positive tail in the distribution of couplings is responsible for the sparse market clustering structure. We also show that discrepancies between the model parameters might be used as a precursor of financial instabilities.

pacs:

89.65.Gh, 02.50.Tt, 64.70.kjI Introduction

Price formation on a financial market is a complex problem: It reflects opinion of investors about true value of the asset in question, policies of the producers, external regulation and many other factors. Given the big number of factors influencing price, many of which unknown to us, describing price formation essentially requires probabilistic approaches. In the last decades, synergy of methods from various scientific areas has opened new horizons in understanding the mechanisms that underlie related problems. One of the popular approaches is to consider a financial market as a complex system, where not only a great number of constituents plays crucial role but also non-trivial interaction properties between them Johnson et al. (2003); Sornette (2009). For example, related interdisciplinary studies of complex financial systems have revealed their enhanced sensitivity to fluctuations and external factors near critical events Albert and Barabási (2002); Kacperski and Hołyst (1999); Kiyono et al. (2006); Barabási and Albert (1999) with overall change of internal structure Dorogovtsev and Mendes (2003); Bornholdt and Schuster (2003). This can be complemented by the research devoted to equilibrium Gai and Kapadia (2010); Newman (2003); Fronczak et al. (2007); Strogatz (2001) and non-equilibrium Holme and Newman (2006); Klemm et al. (2003) phase transitions.

In general, statistical modeling of the state space of a complex system requires writing down the probability distribution over this space using real data. In a simple version of modeling, the probability of an observable configuration (state of a system) described by a vector of variables can be given in the exponential form

| (1) |

where is the Hamiltonian of a system, is inverse temperature (further is assumed) and is a statistical sum. Physical meaning of the model’s components depends on the context and, for instance, in the case of financial systems, can represent a vector of stock returns and can be interpreted as the inverse utility function Bury (2013a). Generally, has parameters defined by its series expansion in . Basing on the maximum entropy principle Jaynes (1957a, b), expansion up to the quadratic terms is usually used, leading to the pairwise interaction models. In the equilibrium case, the Hamiltonian has form

| (2) |

where is a vector of size of external fields and is a symmetric matrix of couplings ( denotes transpose). The model may also involve hidden states (nodes), which are not directly observable, but here we restrict ourselves to considering the visible nodes case only.

The energy-based models represented by Eq. (1) play essential role not only in statistical physics but also in neuroscience (models of neural networks Schneidman et al. (2006); Roudi et al. (2009)) and machine learning (also known as Boltzmann machines LeCun et al. (2007)). Recently, applications of the pairwise interaction models to financial markets have been also explored Bury (2013a); Maskawa (2002); Bury (2013b); Zeng et al. (2014). Given topological similarities between neural and financial networks Vértes et al. (2011), these systems can be considered as examples of complex adaptive systems Hommes (2001), which are characterized by the adaptation ability to changing environment, trying to stay in equilibrium with it. From this point of view, market structural properties, e.g. clustering and networks Mantegna (1999); Onnela et al. (2003); Bonanno et al. (2004), play important role for modeling of stock prices. Adaptation (or learning) in these systems implies change of the parameters of as financial and economic systems evolve. Using statistical inference for the model’s parameters, the main goal is to have a model capable of reproducing statistical observables based on time series for a particular historical period. In the pairwise case, the objective is

| (3) |

where and angular brackets denote statistical averaging over time.

Having specified general mathematical model, one can also discuss similarities between financial and infinite-range magnetic systems in terms of phenomena related, e.g. extensivity, order parameters and phase transitions, etc. These features can be captured even in the simplified case, when is a binary variable taking only two discrete values. Effect of the mapping to a binarized system, when the values and correspond to profit and loss respectively, is also studied in the paper. In this case, diagonal elements of the coupling matrix, , are zero because terms do not contribute to the Hamiltonian. It is worth stressing that the current investigation develops ideas outlined in the previous studies Bury (2013a, b); Zeng et al. (2014); Maskawa (2002) in a way that the effect of binarization, comparison of learning algorithms, evolution and scaling properties of the parameters distributions are studied in a more systematic fashion.

The paper is organized as follows. In Section II, basic statistical definitions and inference methods for and are presented. In Section III, effect of binarization of stock returns and historical evolution of the model parameters are discussed. Finally, the main findings of our investigation are summarized in Section IV.

II Data and methods

We study historical dynamics of the U.S. stock market using stock prices time series yah from the Standard & Poor’s 500 index (hereafter S&P 500) listed in Table 1. We analyze discrete daily closing prices, , starting from 1990 till 2013 (5828 trading days), which are converted to logarithmic returns, .

II.1 Basic statistical analysis of financial time series

The top panel in Fig. 1(a) shows historical data for the average stock return. In order to extract long-term trends from the time series, we employ a simple moving window (or simple moving average, SMA) approach. It acts like a low-pass filter, averaging out high frequency components, which are usually related to noise.

Within the SMA approach, data is divided into chunks (or windows) of size , assuming the time series to be stationary on this scale. In this case, th chunk corresponds to equally weighted previous values of daily log-returns (including the current one). For each set of chunks, one can calculate different statistical characteristics, such as average

| (4) |

and covariance matrix, (), with the elements

| (5) |

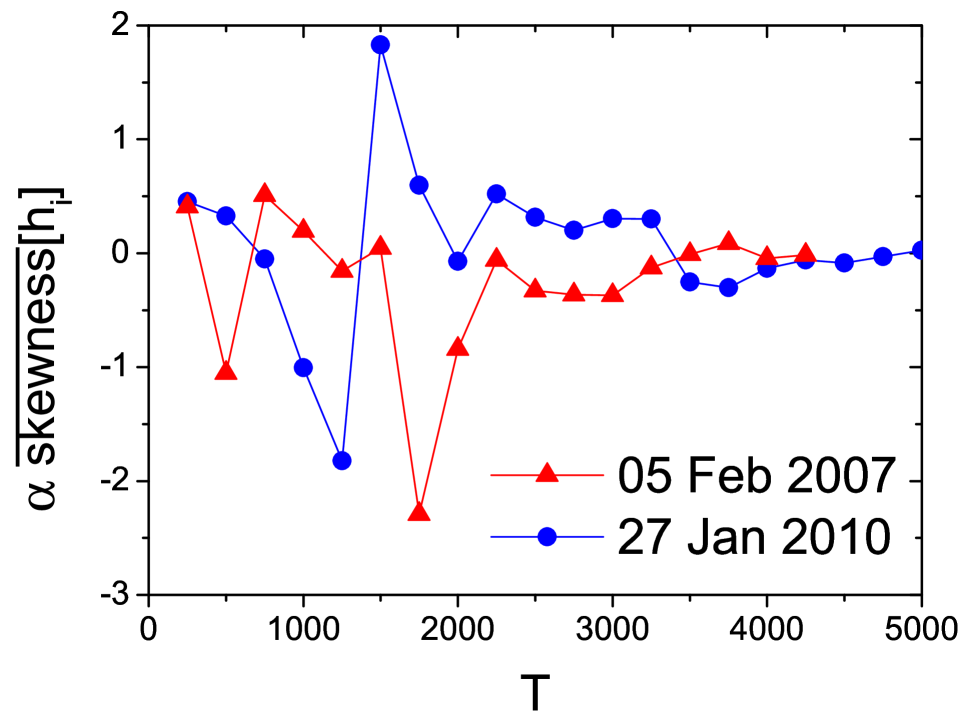

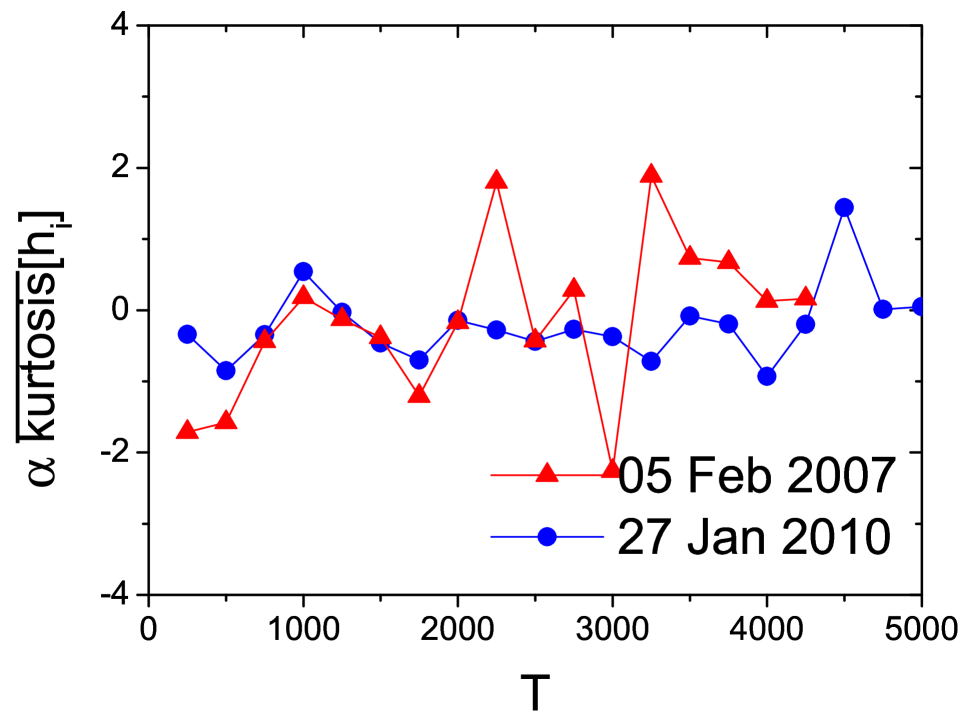

where is assumed for the covariance matrix to be positive definite. Hereinafter, angular brackets denote averaging over time (historical values), while bar denotes averaging over index (vector or matrix elements). It is also possible to investigate nonlinear dependence between time series using more sophisticated statistical concepts Lee et al. (2013) or nonlinear data transformations, however only the simplest linear case is considered in the current paper. Series variance is autocovariance, , where denotes standard deviation or volatility in finance. Usually, SMA volatility serves as the simplest risk measure quantifying stability of returns. In order to quantify deviation from the normal distribution, it is also useful to define higher-order moments, such as skewness

| (6) |

and kurtosis (also known as excess kurtosis)

| (7) |

which both equal zero in the Gaussian case. Indeed, SMA filter allows one to extract long-term trends in the market and, for a large value of , various moments of the distribution of returns can be used to identify market crashes (Figs. 2 and 3). Henceforth, we will call the considered portfolio “market” as it represents a big number of the top companies from S&P500 index. Also, we provide corresponding confidence intervals for these moments using basic bootstrapping algorithm (sampling with replacement) which are depicted in Figs. 2 and 3. However, a more comprehensive discussion on the moments estimates for the non-stationary time series, besides moving window and correlated variable effects Pindyck and Rubinfeld (1998), would also require considering nontrivial long-term memory effects and intraday correlations Utsugi et al. (2004); Podobnik et al. (2010) inherent to financial time series, what goes beyond the scope of the current investigation.

As mentioned in the Introduction, to reduce the amount of data required for our inference, we focus on a binarized version of the returns and not on the raw data. We thus define the binarized version of the returns as

| (8) |

This procedure also mitigates the scaling problem of multiple series since it assigns the same value of stock return independently of its absolute value. Another common technique to deal with this problem is standardization

| (9) |

In this case, correlation matrix, (), is a normalized covariance matrix with the elements

| (10) |

Standardization procedure is known to preserve market behavior and widely used for the statistical analysis of the financial time series Fenn et al. (2011). Effects of these transformations defined by Eqs. (8)–(10) are shown in Figs. 1–3 and will be discussed further in Section III where some simple statistical properties of the binarized return versus the raw and standardized returns are compared. Before this, however, we briefly describe the inference procedure.

II.2 Equilibrium Boltzmann learning methods

We harness inference methods based on maximizing of the model’s likelihood . In the equilibrium case, exact learning of the Hamiltonian [Eq. (2)] parameters implies solving Eq. (3) in a self-consistent way, where corrections and on each learning step can be calculated as

| (11) |

Here, and are learning rates, are empirical (observed) moments and are the moments sampled from the model using Monte Carlo (MC) methods. The exact learning algorithm always yields optimal values for and if there are no hidden nodes in the system Amari et al. (1992).

Being in general slow, the exact learning algorithm might be substituted by the approximate inference methods Tanaka (1998) which are based on expansion of the free energy of a system for small fluctuations around its mean value. The first-order (naïve) approximation within the mean field theory (nMF) gives

| (12) |

where and is the Kronecker delta. Here, taking into account the diagonal element (which is usually discarded) for the calculation of corresponding improves accuracy of the approximation, being known as the diagonal-weight trick Tanaka (1998). The second-order correction to the nMF approximation requires solving Thouless-Anderson-Palmer (TAP) equations

| (13) |

where Eq. (12) should be used instead for the calculation of the external fields if the diagonal-weight trick is used.

Another class of approximations can be derived using expansion of the free energy in pairwise correlations. The simplest independent-pair (IP) approximation assumes independence of every stock pair from the rest of the system. In this case, couplings and external fields can be found as Roudi et al. (2009)

| (14) |

where . Sessak and Monasson (SM) derived higher-order corrections to the IP approximation in a closed form using other terms in the perturbative correlation expansion Sessak and Monasson (2009)

| (15) |

It is also worth noting that there have been developed a few other approximate inference schemes tailored for different system regimes, such as a pseudo-maximum likelihood inference using all data Aurell and Ekeberg (2012), minimum probability flow Sohl-Dickstein et al. (2011) or mean field approximations for low temperatures Nguyen and Berg (2012). For example, pseudo-maximum likelihood inference Aurell and Ekeberg (2012), being more suitable for sparse connections, can be studied in a context of the correlation clustering structures described in Subsection III.4.

III Results and discussion

III.1 Effect of binarization

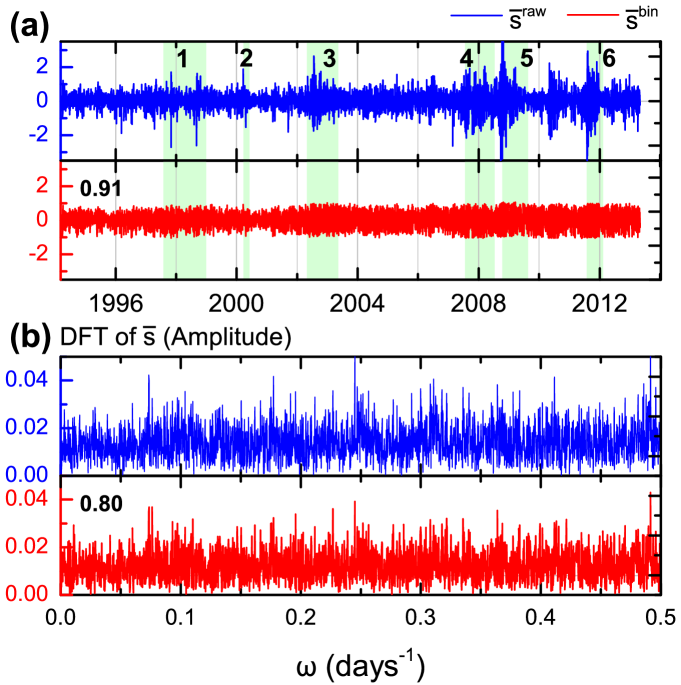

The mapping defined by Eq. (8) obviously affects information contained in the time series. In order to estimate this effect, we compare time series for the average raw and binary returns first. As Fig. 1 shows, correlation coefficient between historical values of and is very high (). Moreover, correlation between amplitudes of their Fourier transforms is also high (), suggesting that signatures of economic cycles and frequency of market crashes are preserved in the binarized time series. However, maximum magnitude of binary returns is obviously bounded by the definition.

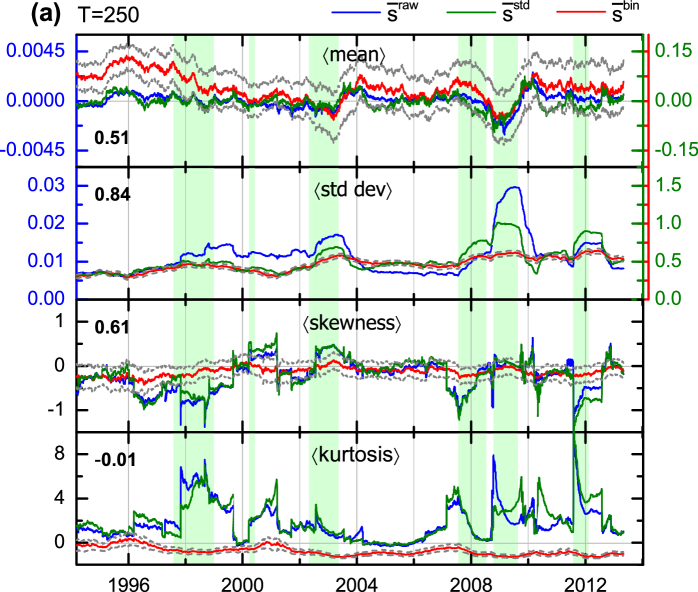

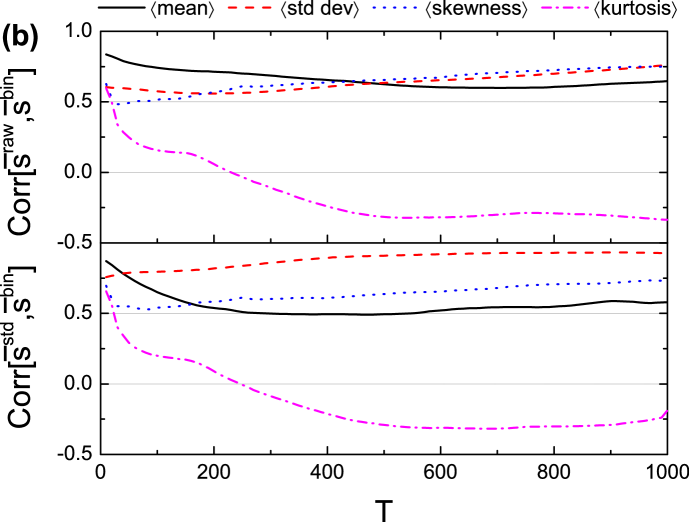

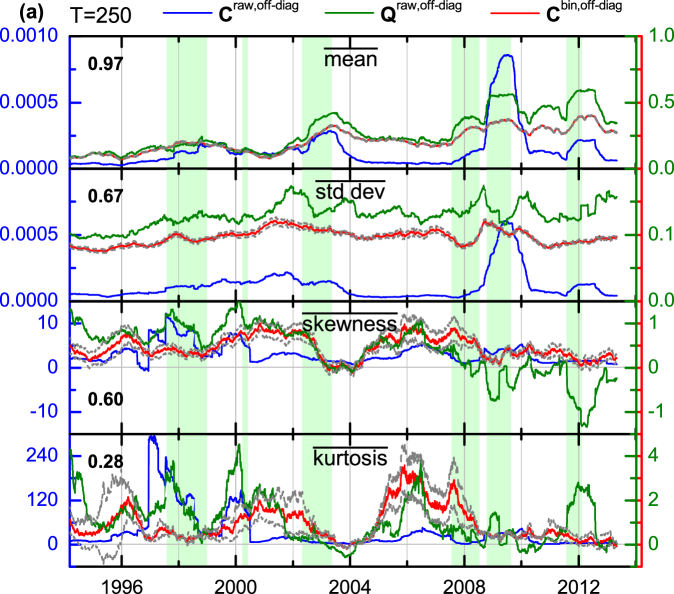

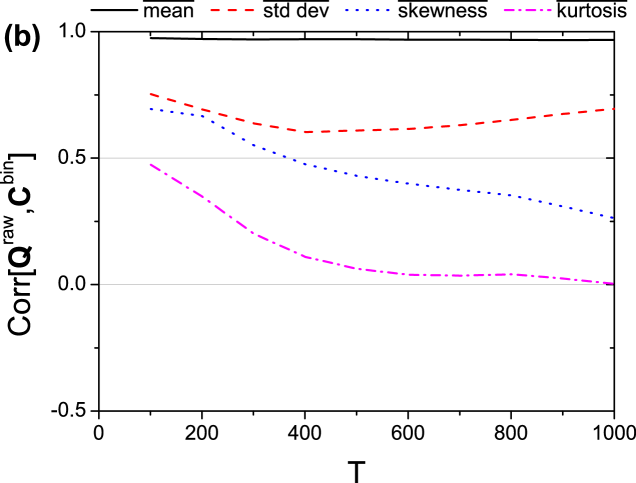

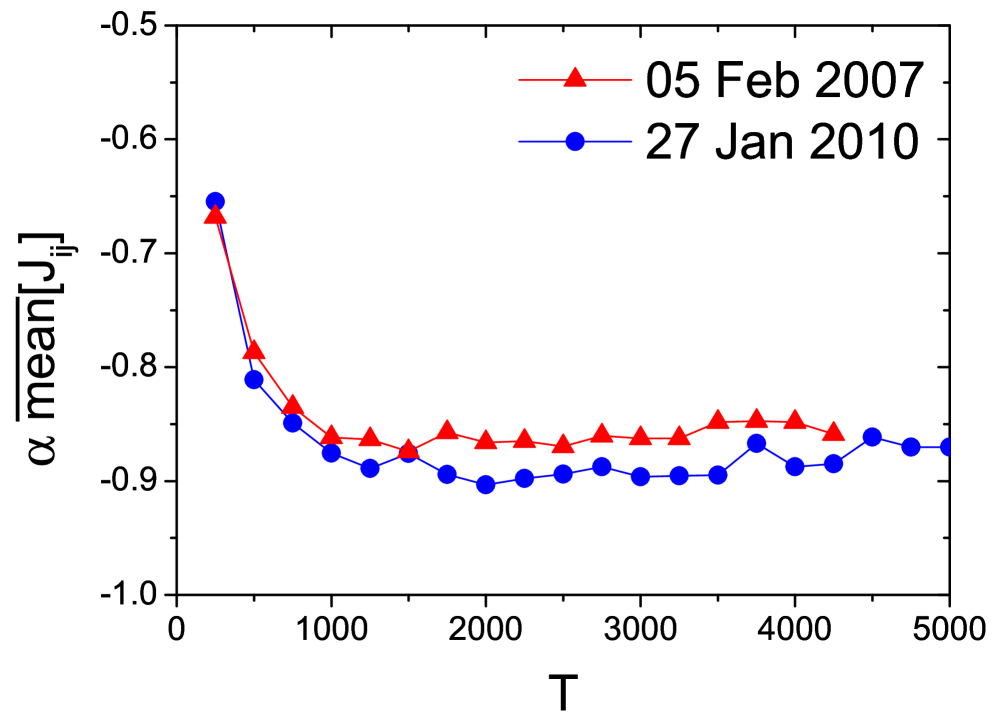

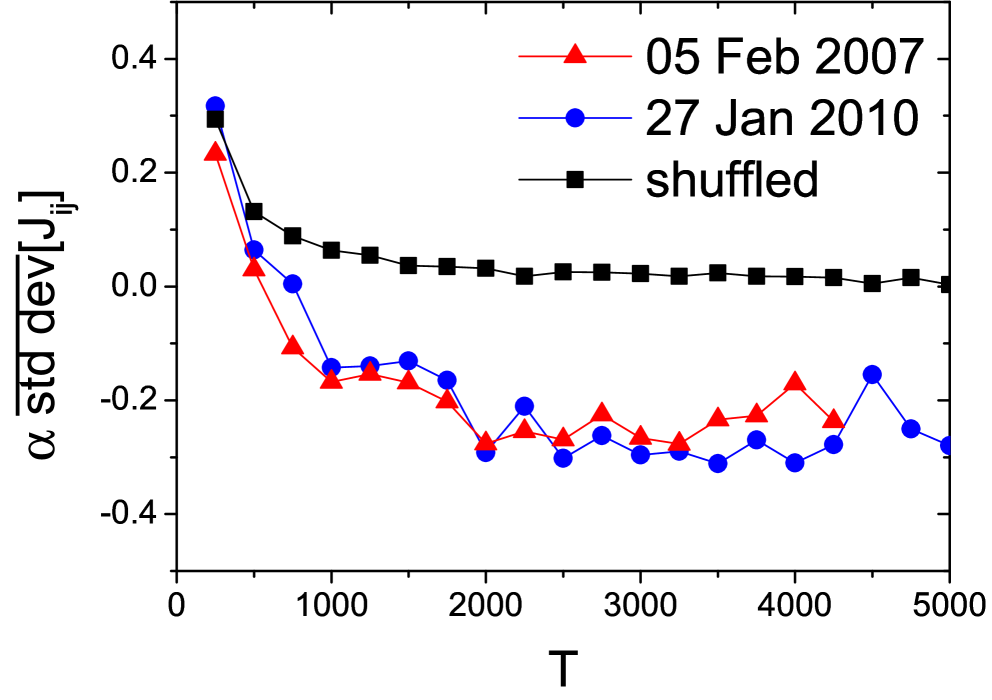

Comparison of the filtered time series using SMA also suggests the idea that the information about the market trends is preserved in the binarized time series. With this aim, we compare historical evolution of the first four moments of the distribution of average binarized versus raw and standardized returns. The results presented in Fig. 2 indicate that the binary returns behave similarly to the raw and standardized returns, preserving dynamics of the first two moments and less so about the third moment, while information about kurtosis is lost for all [Fig. 2(b)]. Regarding the pairwise correlations, Figure 3 shows that the covariance matrix of the binarized returns becomes similar to the correlation matrix of the raw returns. Indeed, their off-diagonal elements follow similar distributions with very high correlation between means. For higher-order moments, correlation decreases with [Fig. 3(b)].

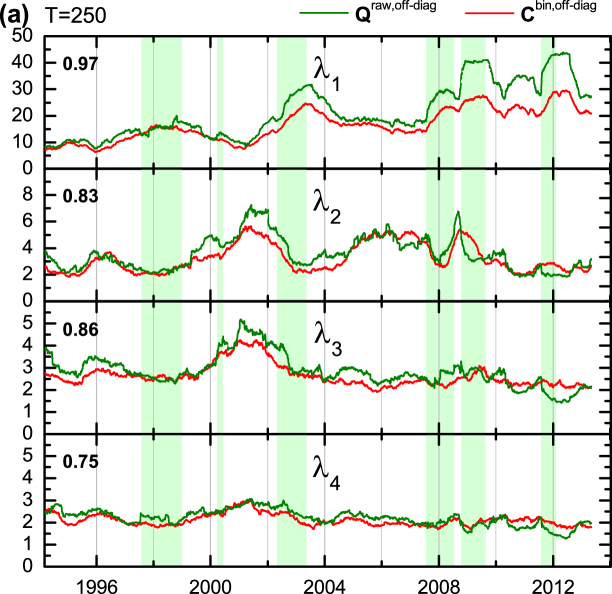

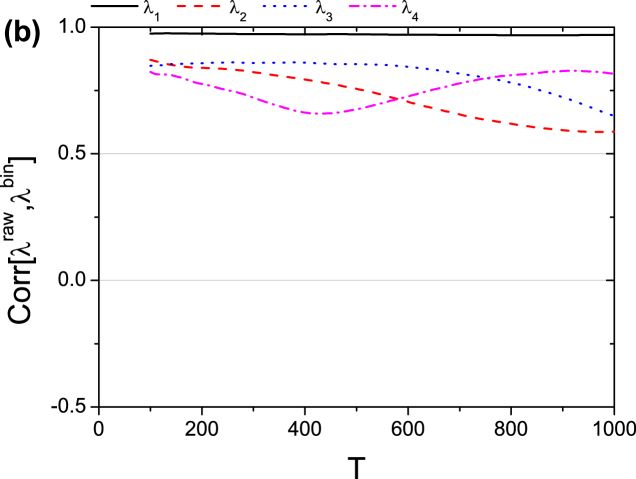

Another way to explore effects of the binarization procedure is to study eigenvalue distribution of correlation matrices for the original and transformed time series, since it is known to be different from the distribution of a random correlation matrix Laloux et al. (1999). With this aim, we compare historical dynamic of the four biggest eigenvalues, which do not match the Wigner law. As Fig. 4 shows, all four values are well preserved and the biggest one corresponding to the “market mode” is in remarkable agreement after binarization independently of moving window size.

Having validated that binary returns indeed capture market historical behavior similarly to standardized returns, we proceed to the Boltzmann model inference and evolution of its parameters.

III.2 Comparison of approximate and exact learning methods

Following the SMA approach with trading days (approximately one trading year), we study historical evolution of the external fields and couplings inferred for each chunk of the binarized time series. We employ four approximate (nMF, TAP, IP and SM) learning methods described in the previous section and compare them with the exact learning, where MC sampling is used for the latter.

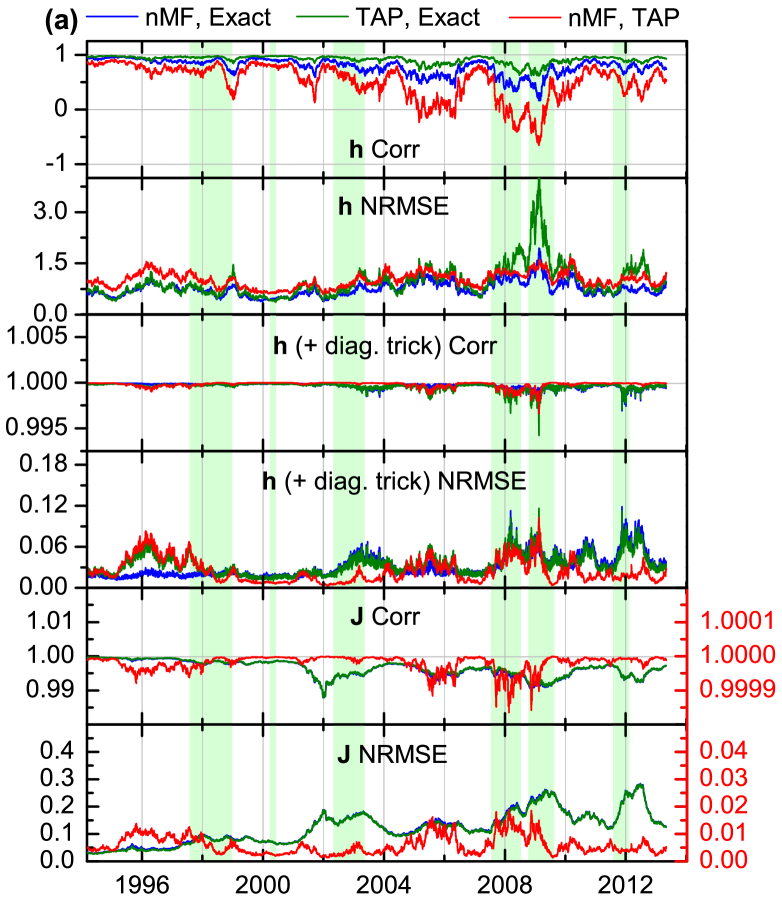

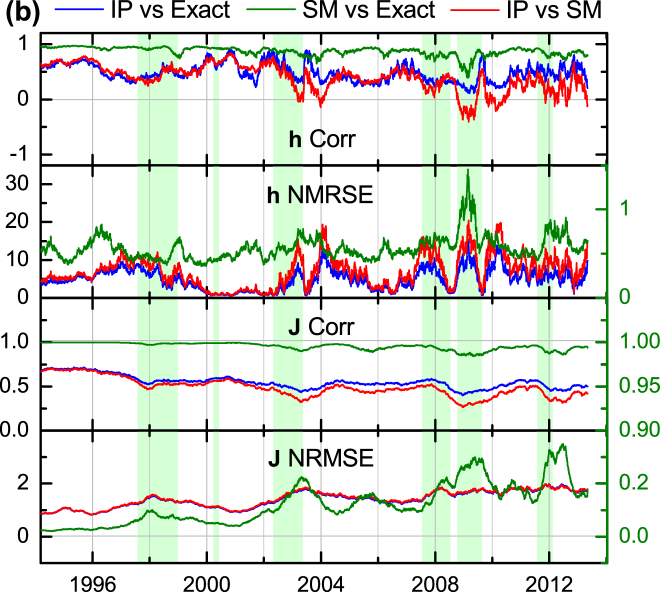

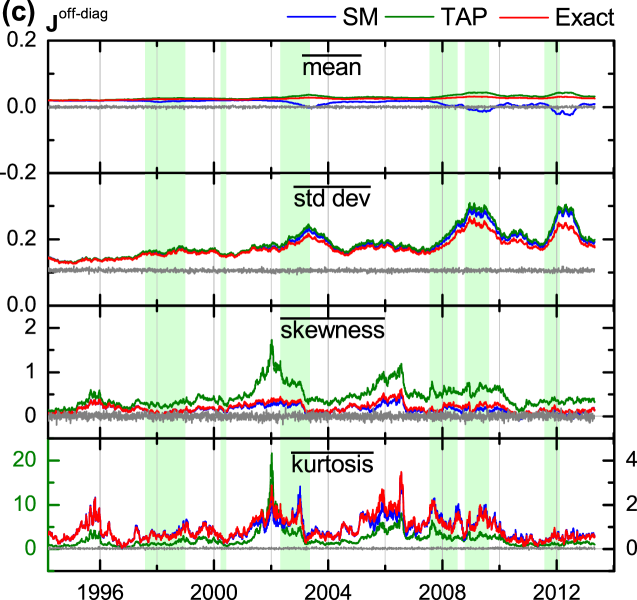

Figure 5 shows comparison of the inferred parameters for four different historical dates. Without use of the diagonal-weight trick, inference of external fields in the nMF case works better when the dates far from market crashes are considered (top row in the two leftmost columns, corresponding to 22 Dec 1997 and 09 Jan 2002). TAP correction slightly improves the inference accuracy however producing overestimated values in comparison with the exact learning algorithm (second row). Both MF approximations perform worse for the data near market crashes (two top rows in the two rightmost columns, corresponding to 09 Oct 2008 and 13 March 2012), while the diagonal-weight trick allows to achieve almost perfect accuracy in both cases (red triangles in the first two rows), justifying the need of high-order corrections. The IP algorithm (third row) shows much worse performance for the all dates except 09 Jan 2002. Although higher-order SM corrections (third row) considerably improve accuracy of the IP external fields, it is still lower than in the MF cases. Couplings inferred using both MF approximations show the same trend, being more/less accurate far from/near crashes (fourth row). Although the bulk of the MF couplings is in an excellent agreement with the exact couplings even near crashes, positive outliers are overestimated. The couplings estimated using the IP algorithm are in a very poor agreement with the exact couplings for the all dates considered (bottom row), while the use of the SM correction yields considerable improvement (bottom row). Moreover, it correctly captures the biggest outliers, outperforming the MF algorithms.

Historical dynamics of the inference quality for approximate methods is depicted in Fig. 6, where normalized root mean square error

| (16) |

and correlation between the model parameters inferred using different methods are presented. It confirms that the diagonal-weight trick considerably improves inference quality of the MF external fields, while couplings are systematically overestimated. Within the small correlation approximation, IP algorithm does not perform well for all historical dates, while quality of the SM couplings is comparable to the MF cases (however being still lower in general) and decreases for the periods where higher correlations are observed. Thus, the observed behavior indeed justifies use of TAP as a reliable approximation of true couplings and external fields (making use if the diagonal trick), which has been extensively used in the previous studies Bury (2013a, b); Zeng et al. (2014); Maskawa (2002). However, special care should be taken about overestimated positive outliers, where SM algorithm can be helpful.

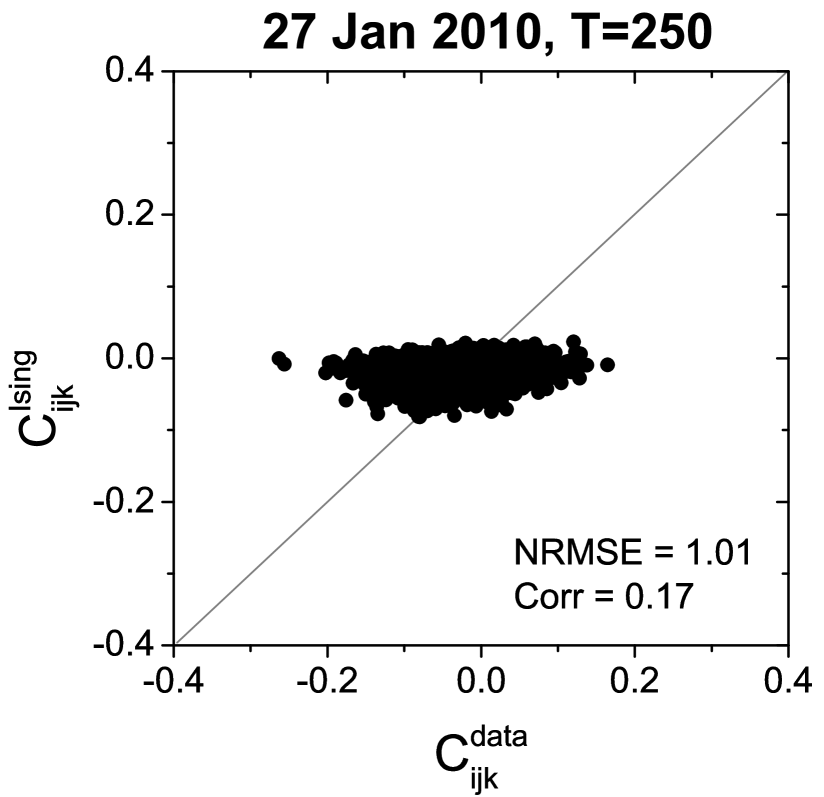

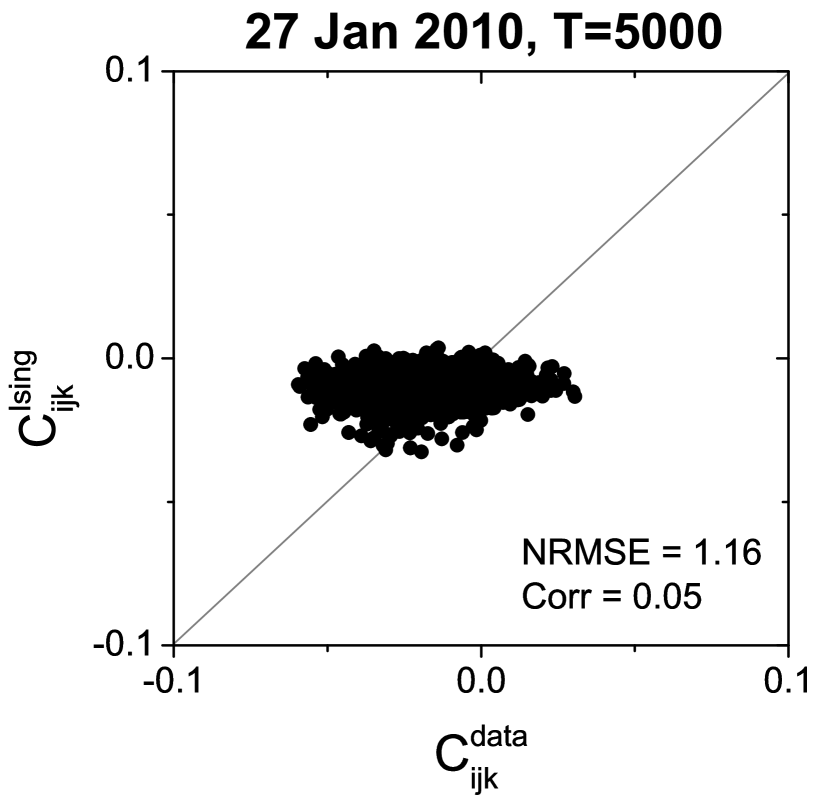

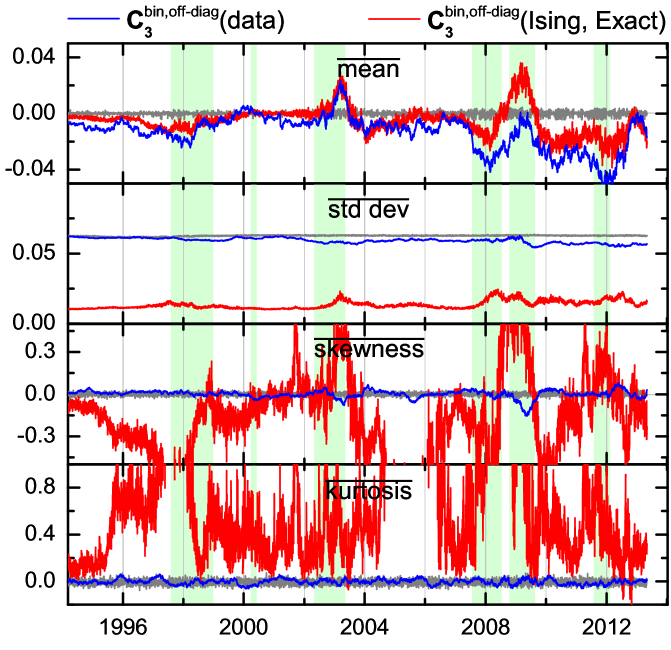

To validate results obtained by the exact learning algorithm, we sampled stock returns from the model using MC sampling. The single and pairwise empirical moments are nicely recovered from the exact model (figures are not shown), while the third-order covariances, , are almost not captured by the model (Fig. 7). Although the inability to capture third-order correlations could be due to the lack of data for estimating the real third-order covariances, this is unlikely to be the case as the degree of mismatch between the third-order covariances of the Ising model and the data is the same even when somehow bigger amounts of data are used for their estimation. Nevertheless, in spite of the fact that individual third-order covariances are not captured well, historical dynamics of their mean can be recovered from the model (Fig. 8).

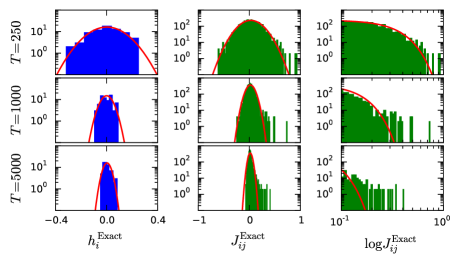

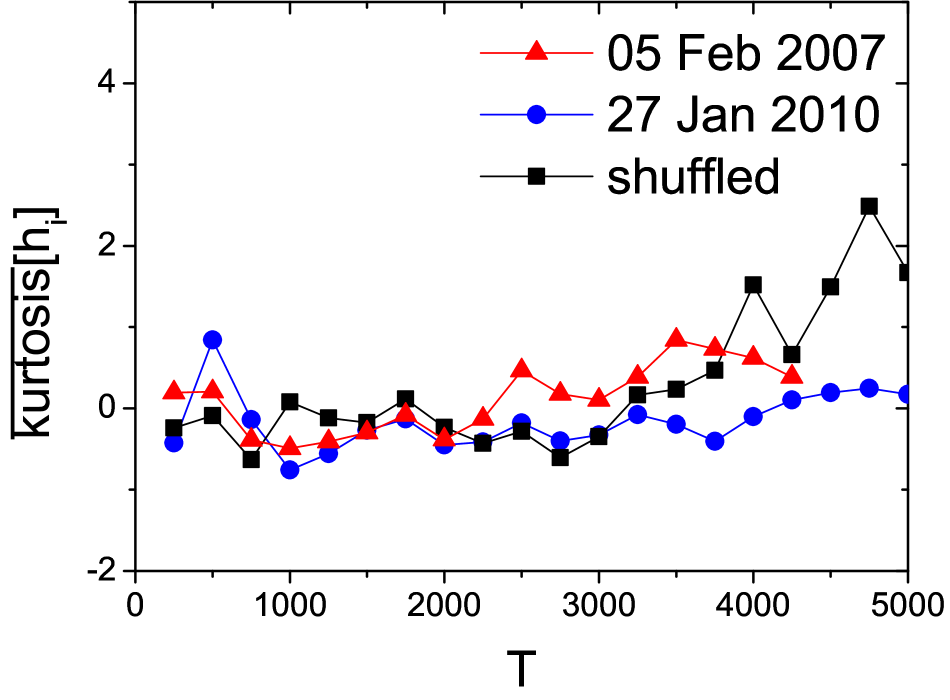

III.3 Distribution of inferred parameters

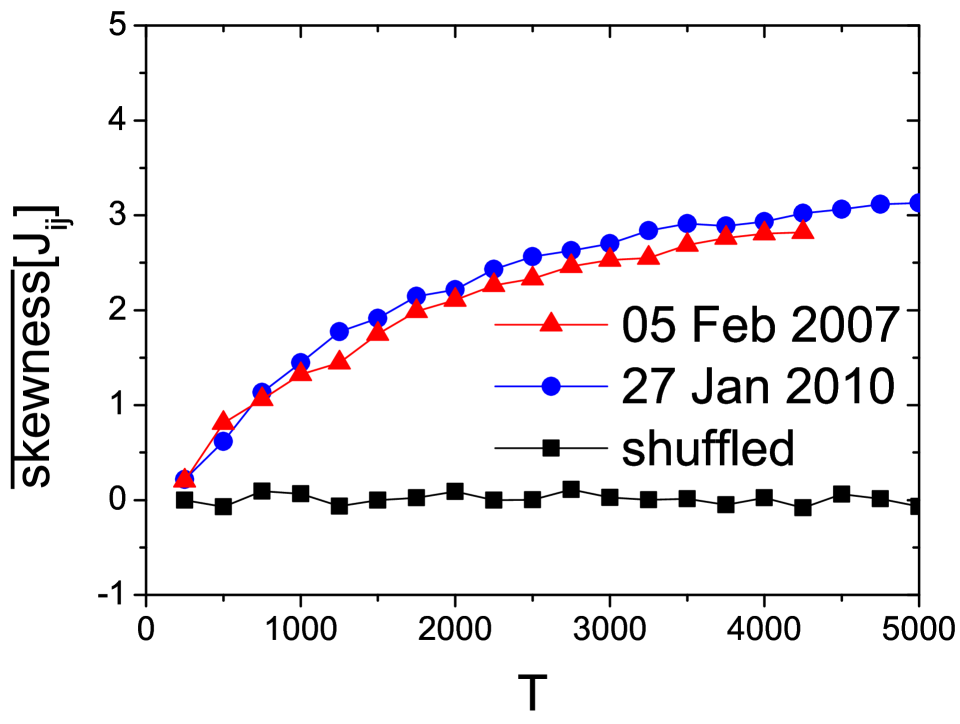

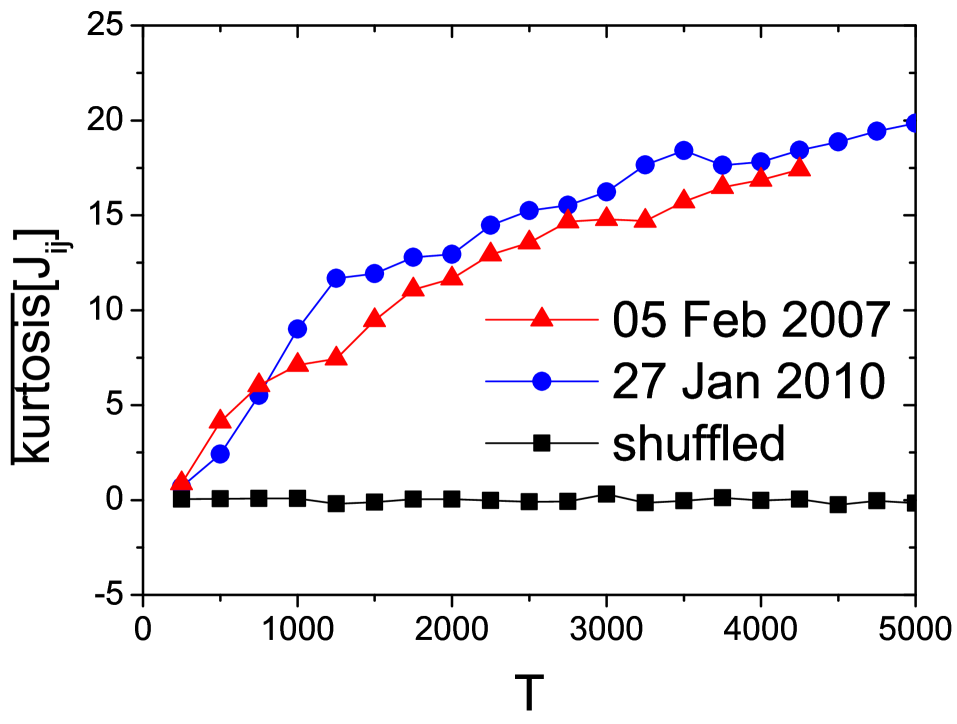

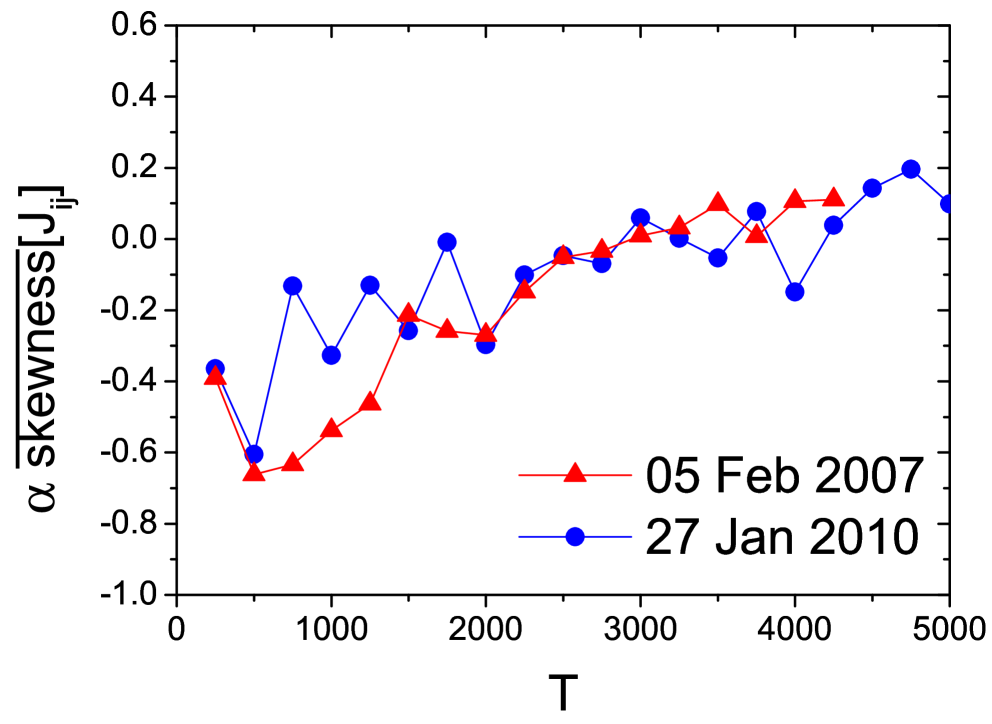

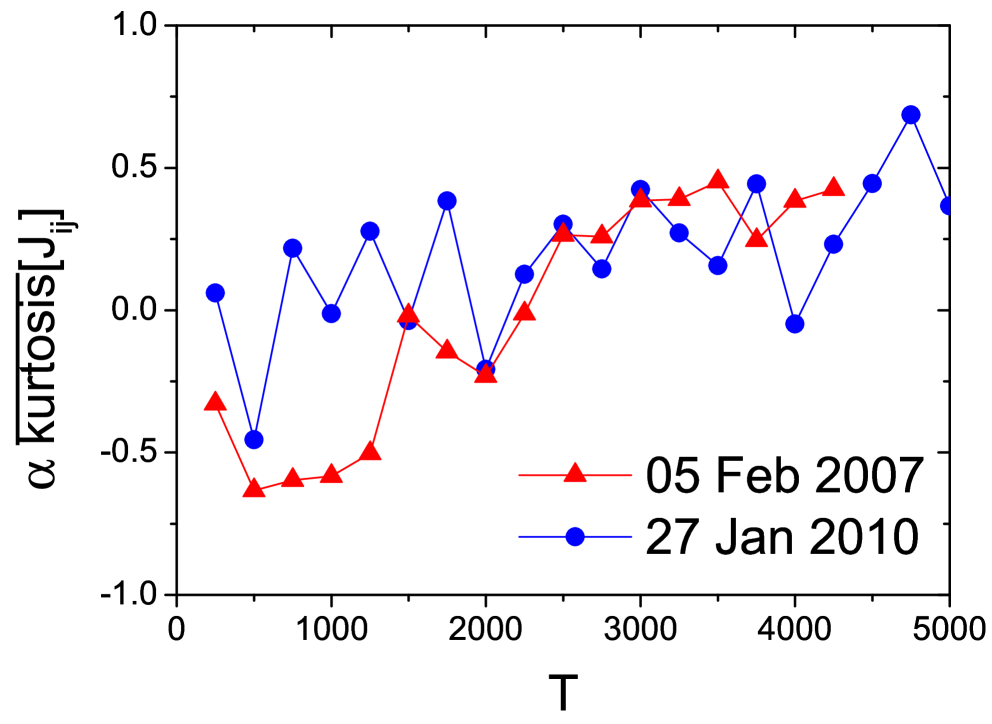

Figure 9 shows histograms of the external fields and couplings inferred using the exact learning algorithm for three different window sizes: and trading days. The distribution of external fields is close to the Gaussian and does not possess outliers independently of . The bulk of the couplings is also distributed normally, however a heavy positive tail is present. For bigger window sizes, the Gaussian bulk component of the inferred couplings becomes less prominent and the tail starts to dominate. Although this behavior has been previously reported in Ref. Bury (2013b), a role of the tail has remained unclear. We will address this question in the next subsection.

In fact, as shown in Fig. 10, all moments of the distribution of scale with . On the contrary, there is no obvious dependence for , which behavior is close to the external fields inferred on randomly shuffled time series (where each element is swapped with other randomly picked element using uniform distribution within the moving window chunk). Higher value of inferred on randomly shuffled time series can be explained by the fact that it compensates positive (ferromagnetic) contribution to the mean return stemming from the positive mean of the inferred couplings: In the shuffled case, becomes zero while all remain unaffected, therefore this effect should be compensated by the external fields.

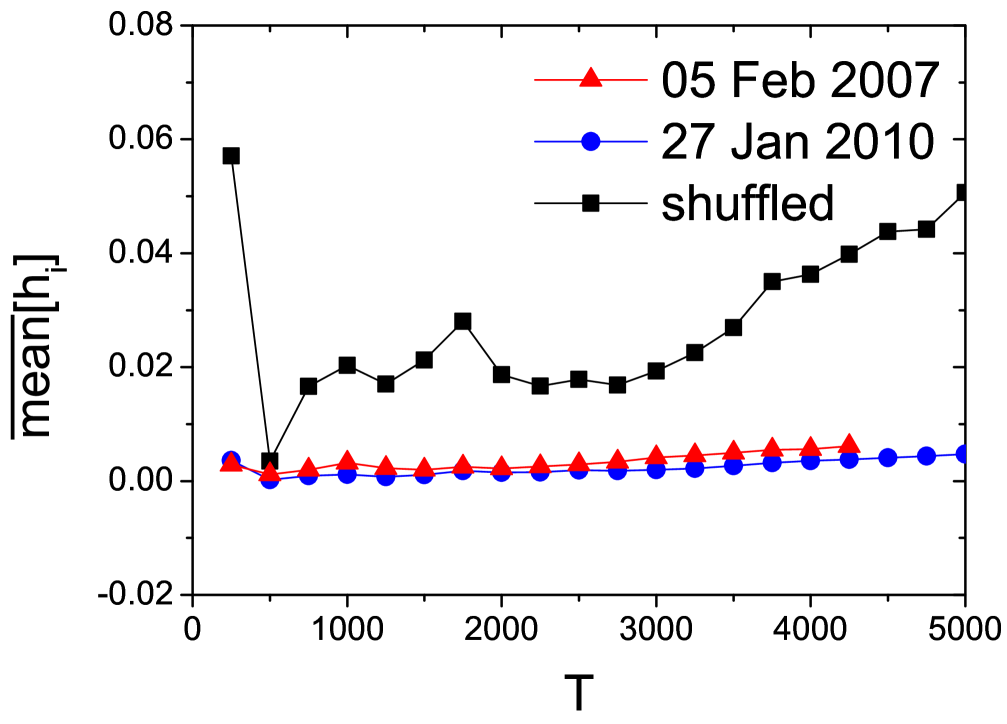

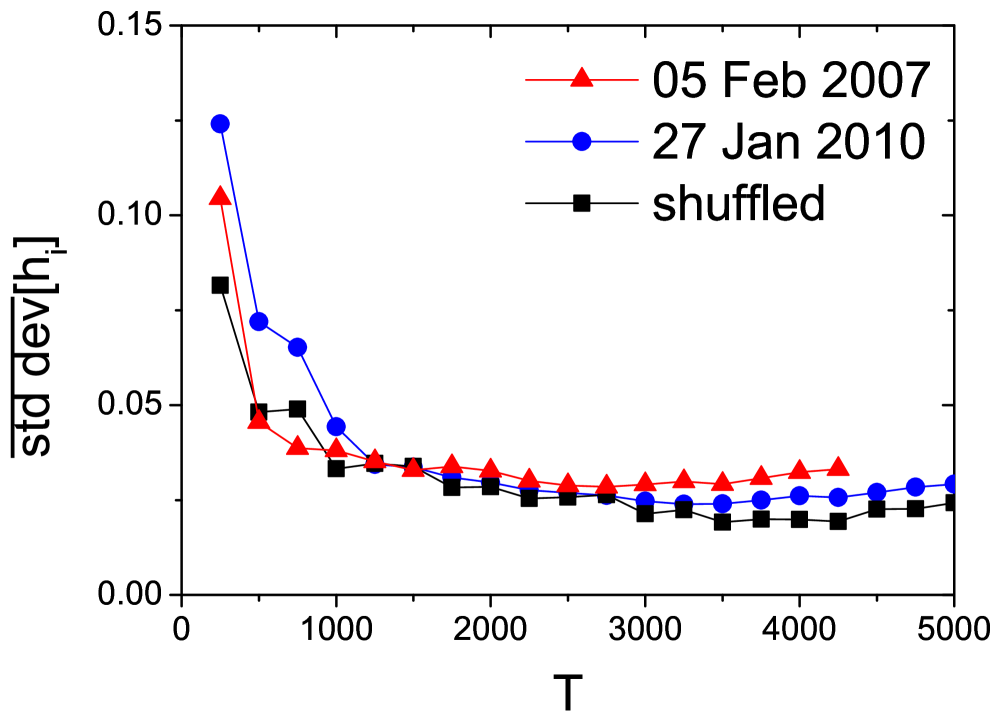

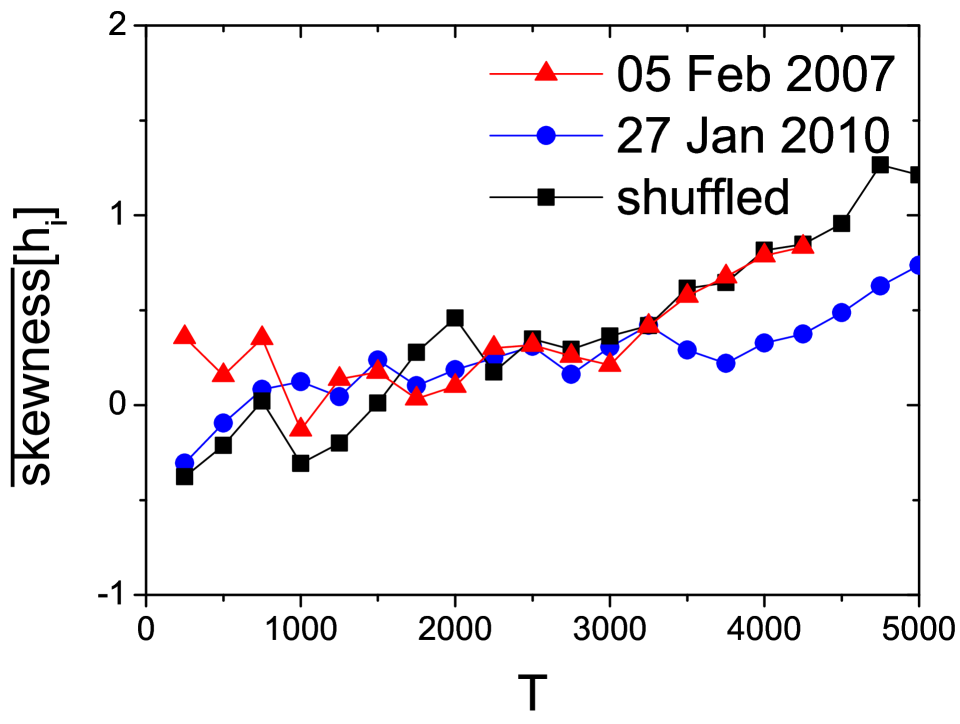

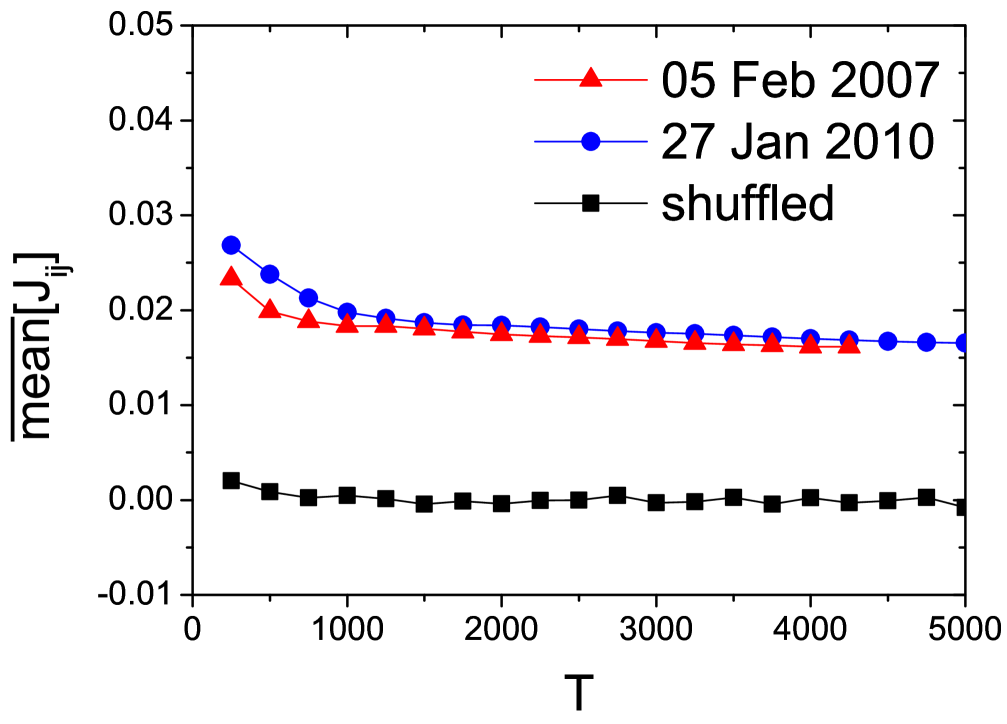

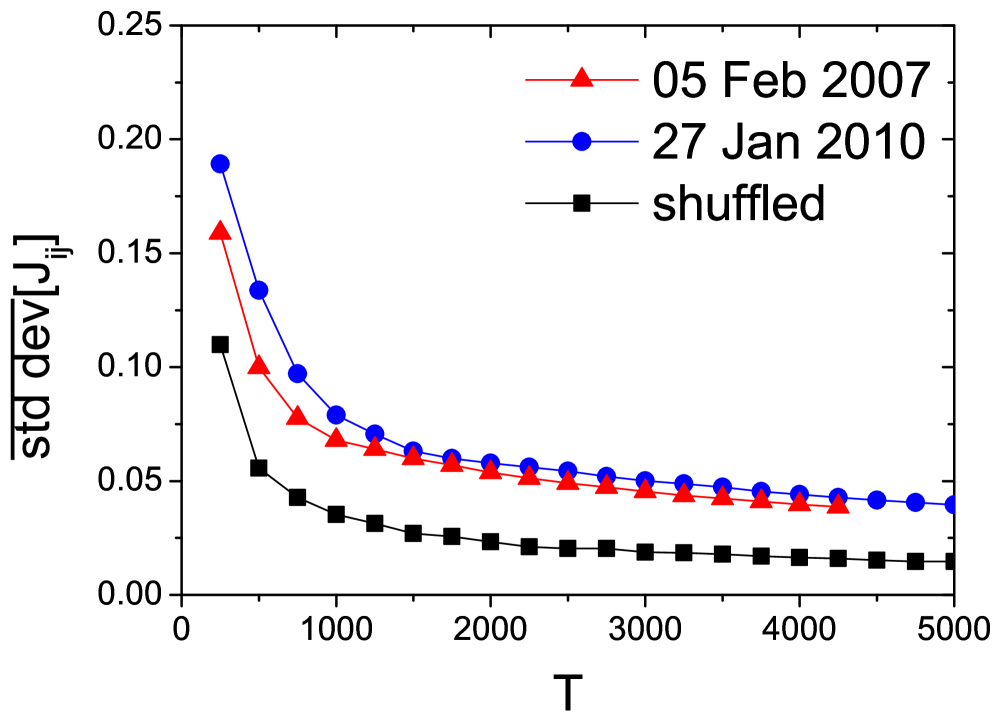

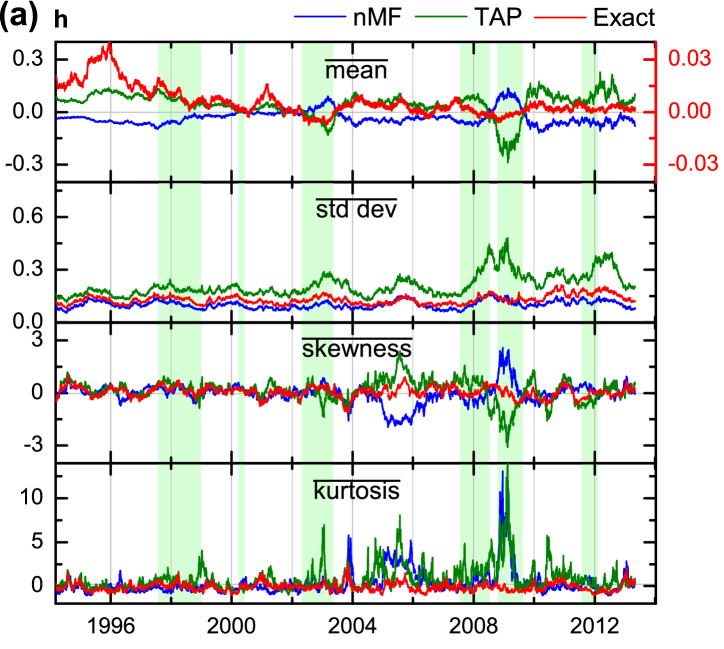

Historical dynamics of the moments of the distributions shown in Fig. 11 indicates that the average external field is strongly correlated with the mean return (), while higher moments, being almost stable over the historical period considered, seem not to convey any particular information about market behavior. Without use of the diagonal-weight trick, is completely inconsistent with [Fig. 11(a)]. Although behave more similar to , they are significantly overestimated. External fields inferred using the IP and SM algorithms show similar dynamics to and respectively, however being even more greatly overestimated (figures are not shown). At the same time, the diagonal-weight trick allows to achieve almost perfect accuracy in both MF cases [Fig. 11(b)]. Distribution of couplings has stable small positive mean corresponding to ferromagnetic interaction, however with almost half of couplings being negative, i.e. the system is likely to exhibit frustrated configurations. The SM algorithm in general performs better than TAP for couplings estimation except for their mean value , which becomes inconsistent with for the historical periods with highly correlated market [Fig. 11(c), top panel].

It is also interesting to note that the standard deviation of couplings far from the crashes almost linearly increases over the whole period considered from in 1996 to in 2013 [the second panel in Fig. 11(c)]. This observation gains more meaning when we note that the standard deviation of the couplings in 1996 equals approximately to the standard deviation of the couplings inferred on randomly shuffled returns, while its value is almost twice bigger than one for the shuffled time series in 2013. Also, during the biggest market crashes, standard deviation of couplings has jumps because interconnections on the market become tighter as a result of the herding behavior during a financial turmoil: Until system is not adapted to a new economic reality, prices tend to move collectively with overall market performance as a benchmark Borysov and Balatsky (2014). The heavy positive tail, which can be characterized by higher order moments, increases for some historical periods. A reason for it is unknown at the moment.

III.4 Industry-related clustering structure

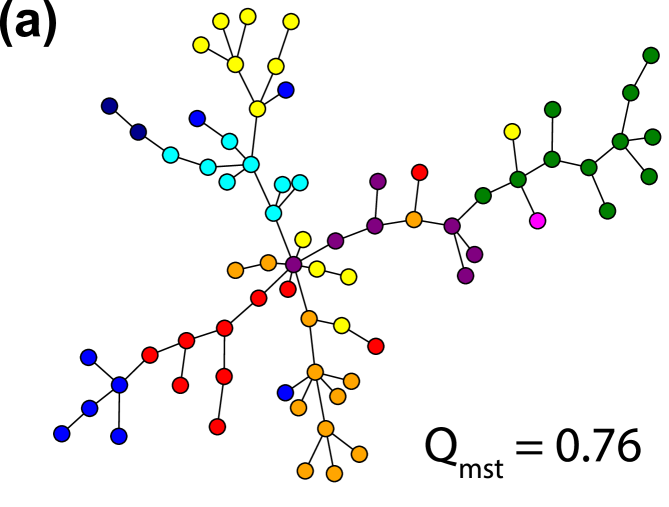

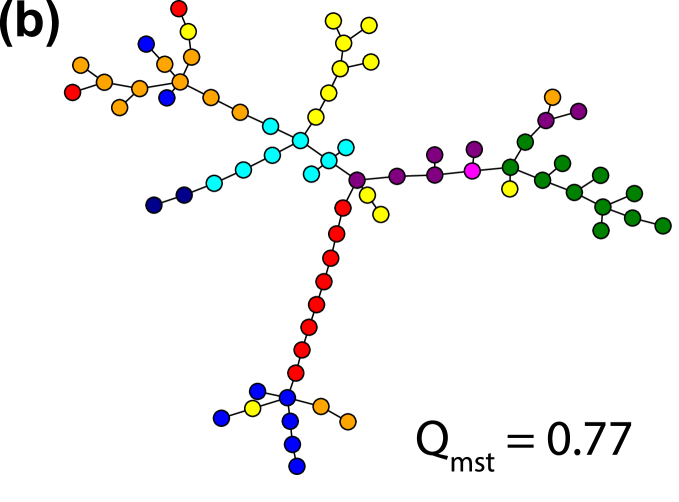

It is well known that a stock market possesses a hierarchical clustering structure which can be detected using correlations Mantegna (1999); Coelho et al. (2007) or couplings between stock prices Bury (2013a) or trading volumes Zeng et al. (2014). One of the most popular techniques employed to find related structures is based on the minimum spanning tree (MST) algorithm. For instance, Prim’s algorithm—a basic MST construction algorithm—consists of the three following steps:

-

1.

Initialize a tree with a single stock, chosen arbitrarily from the all stocks.

-

2.

Find the stock not yet in the tree which has the strongest coupling (biggest value of or ) to a stock in the tree and include it to the tree.

-

3.

Repeat step 2 until all stocks are in the tree.

Figure 12 shows examples of the MST constructed using covariance and coupling matrices of binary stock returns, which are similar to the previously reported in Refs. Bury (2013a) and Zeng et al. (2014). The remarkable feature of these structures is a manifestation of industry sector clustering. Here, we define an industry sector cluster as a connected subset of the tree where all stocks belong to the same industry sector, i.e. each cluster member interacts to the other members only through the stocks from the same sector. Further, we denote cluster size as , where is a sector index ( is the total number of sectors listed in Table 1) and is an index of the cluster ( is a number of such clusters for the sector ).

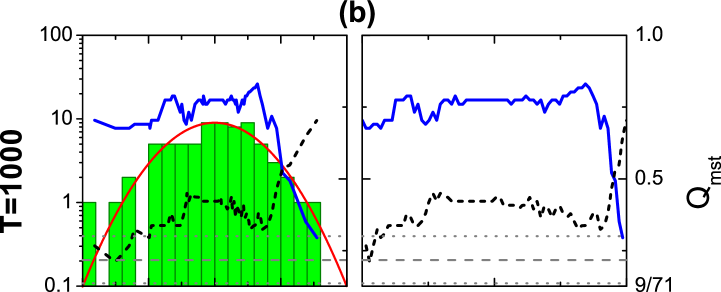

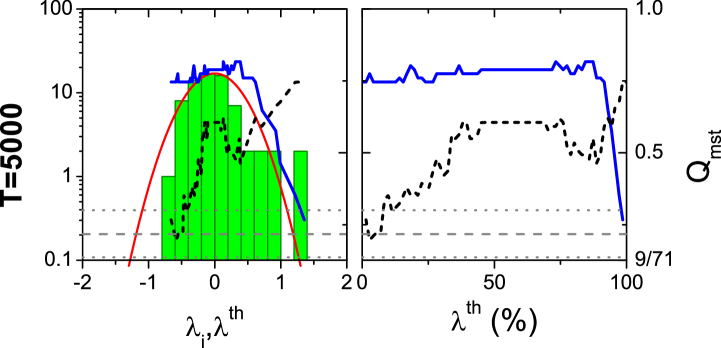

As mentioned above, there can be many clusters for each industry sector. In order to estimate overall industry clustering degree of the market, let us introduce a simple metric based on finding clusters of the maximum size

| (17) |

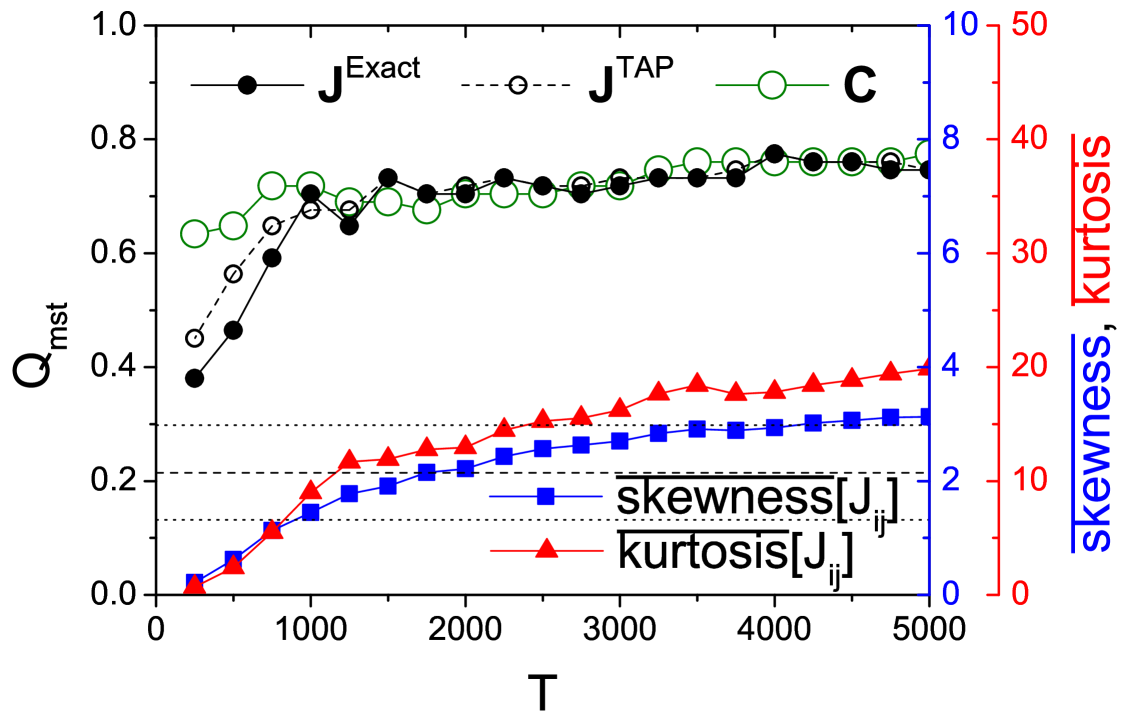

Intuitively speaking, a small value of corresponds to the case where stocks do not group with each other based on which industry sector they belong to. Its minimum value, , is defined by the situation where the biggest cluster for each sector has only one stock, i.e. equals to the total number of stocks in the sector . The maximum value of is 1, which corresponds to the perfect industry clustering structure when there is only one cluster for each industry sector (). This clustering measure shows interesting dependence on the size of moving window (Fig. 13), suggesting an increasing degree of sectoral connectedness of the stock market for bigger time windows as inferred by the Ising model. Also, the degree of connectedness increases with deviation of the distribution from the Gaussian measured by skewness and kurtosis.

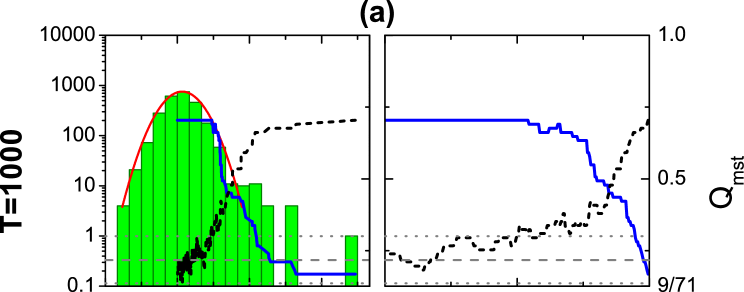

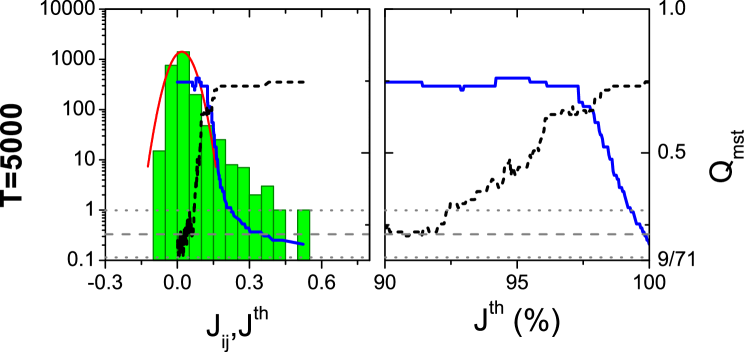

To further investigate the network structure and clustering degree of , we perform the clustering analysis based on two different filtering procedures, namely, considering only a subset of (i) couplings and (ii) eigenmodes of corresponding to different eigenvalues . With this aim, we choose thresholds and and construct MST only using values and respectively. Figure 14(a) shows that the biggest drop/increase of occurs only when the a small percent of the strongest couplings is excluded/included for MST construction. In a similar way, it is also sensitive to discarding the biggest eigenvalues [Fig. 14(b)]. Thus, one might conclude that distribution of couplings indeed can be viewed as a mixture of the Gaussian bulk and heavy positive tail which contains all information about market clustering structure. From this perspective, use of sparse regularization methods for couplings inference, for example, -regularization discussed in Ref. Ravikumar et al. (2010), would be of practical interest.

Finally, it is also worth noting that intraday internal structure of couplings is neither stable (quenched) nor completely random (annealed), somehow preserving a clustering structure with the diameter however being smaller near market crashes (figures are not shown, see for example Ref. Coelho et al. (2007)). These non-trivial features of a coupling matrix will be studied in more detail in the future works.

III.5 Scaling of inferred parameters

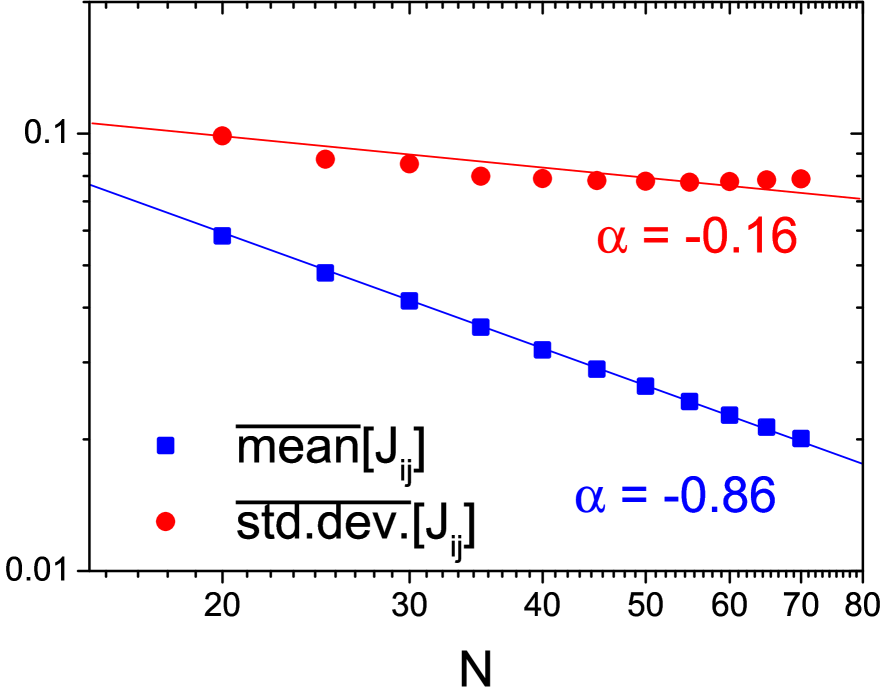

In order to study extensive properties of the system, we investigate scaling properties of the parameter distributions with number of stocks, which are usually characterized by the scaling exponent . We estimate its average value for each distribution moment over scaling exponents for randomly selected subsets of stocks of different size.

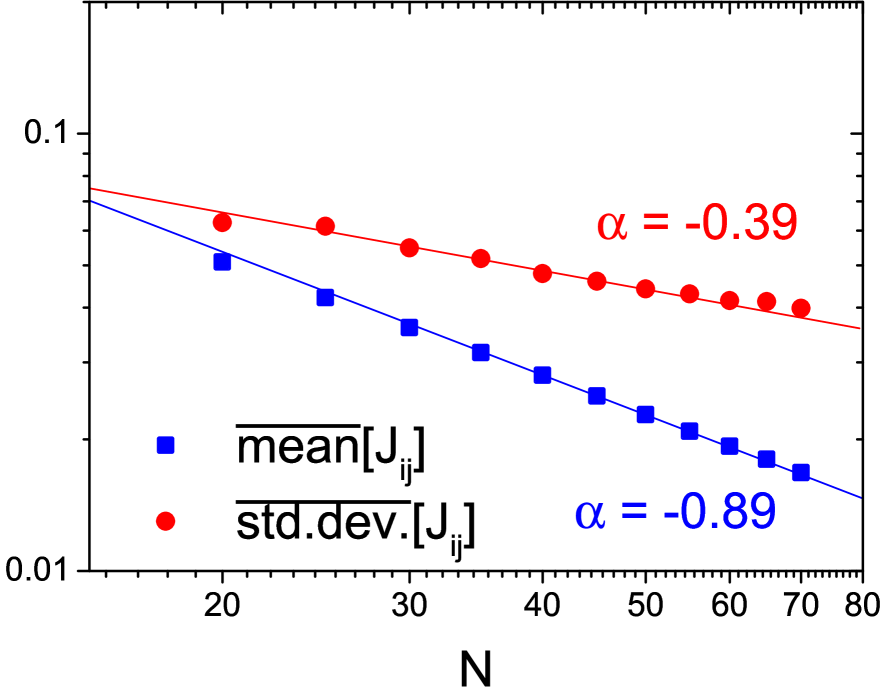

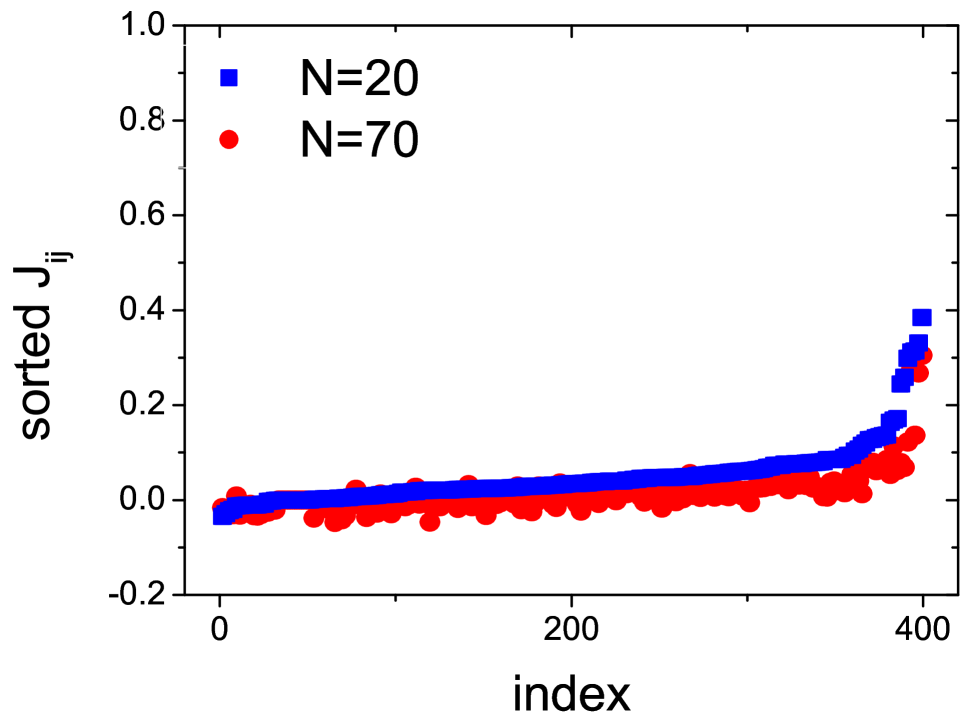

As Fig. 15 (top row) shows, the distribution of external fields does not possess any particular scaling law, except the mean, which has close to . The other moments scale similar to the corresponding moments of the external fields inferred on randomly shuffled time series. Scaling properties of distribution of couplings depends on the size of moving window (Fig. 15, bottom row). When is small, empirical couplings show similar scaling features to the couplings inferred on randomly shuffled returns. However, scaling of the mean and standard deviation becomes closer to the properties of the normal distribution with growth of . This dependence might be related to the presence of finite-size effects, when use of a small number of historical values is not enough to estimate true correlations on the market. These results are similar to the scaling properties obtained in Ref. Bury (2013b), however their SMA window dependence has been shown for the first time.

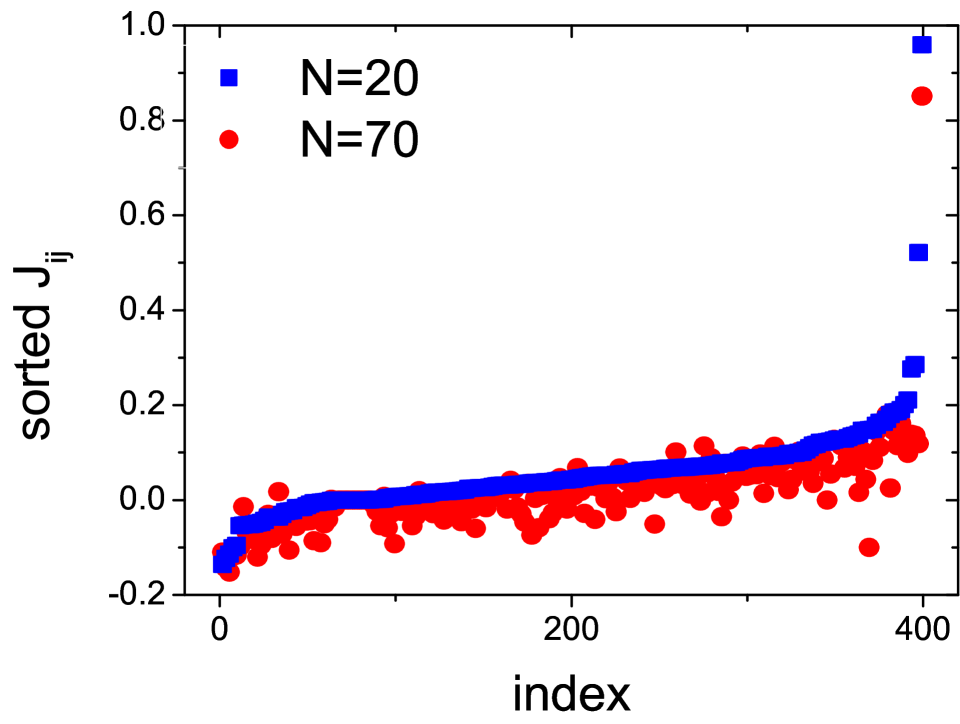

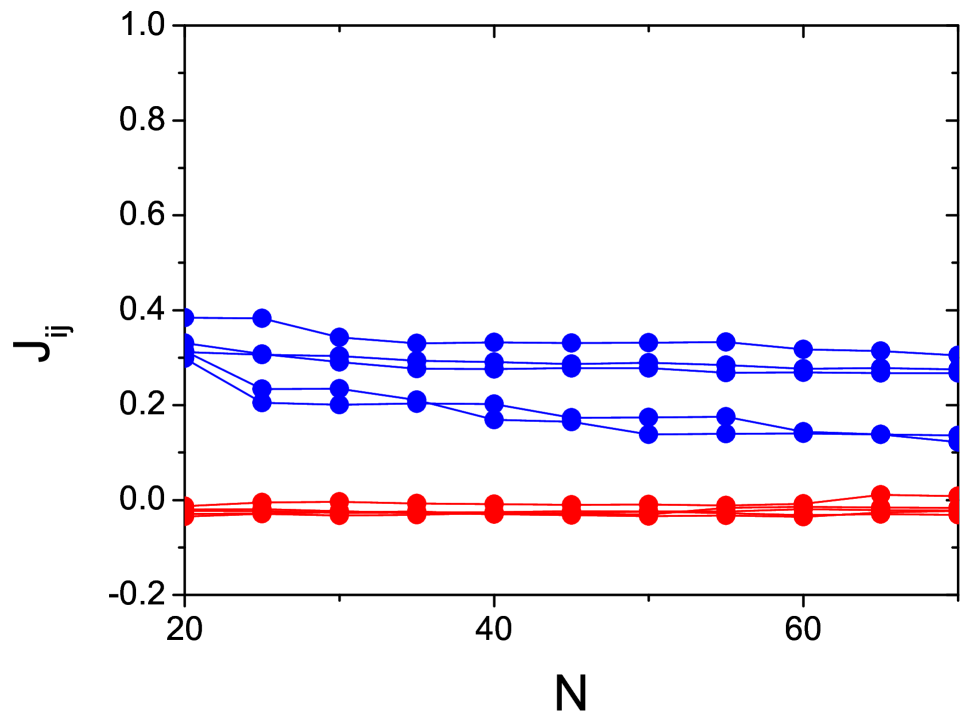

There are two extreme ways in which a change in the distribution of couplings can arise as one increases the size of the observed system. One is that the structure between the previous stocks entirely changes by adding new stocks. Alternatively, the couplings could only change their absolute magnitude, while they maintain their magnitude relative to one another. To better understand where in this spectrum our financial market exists, we performed analysis similar to Ref. Roudi et al. (2009): We chose a random subset of stocks and analyzed couplings between them for different total number of stocks taken into account for the inference (including the original 20). Figure 16 shows that the biggest/smallest values of remain the same with growth of and their scaling becomes closer to the normal distribution for bigger time windows. This behavior also suggests that important features of market connectivity are preserved with the number of stocks.

III.6 External and internal influence

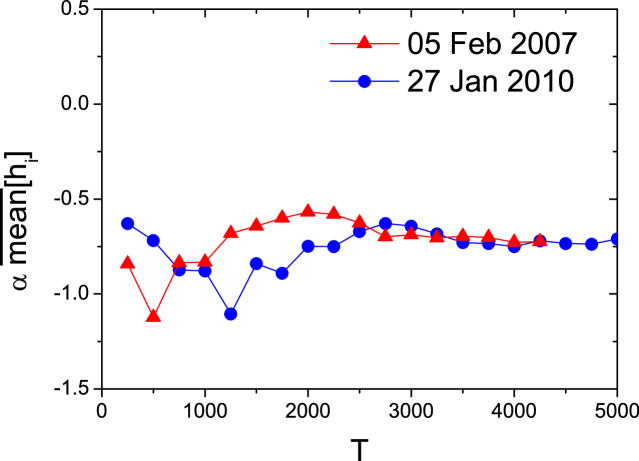

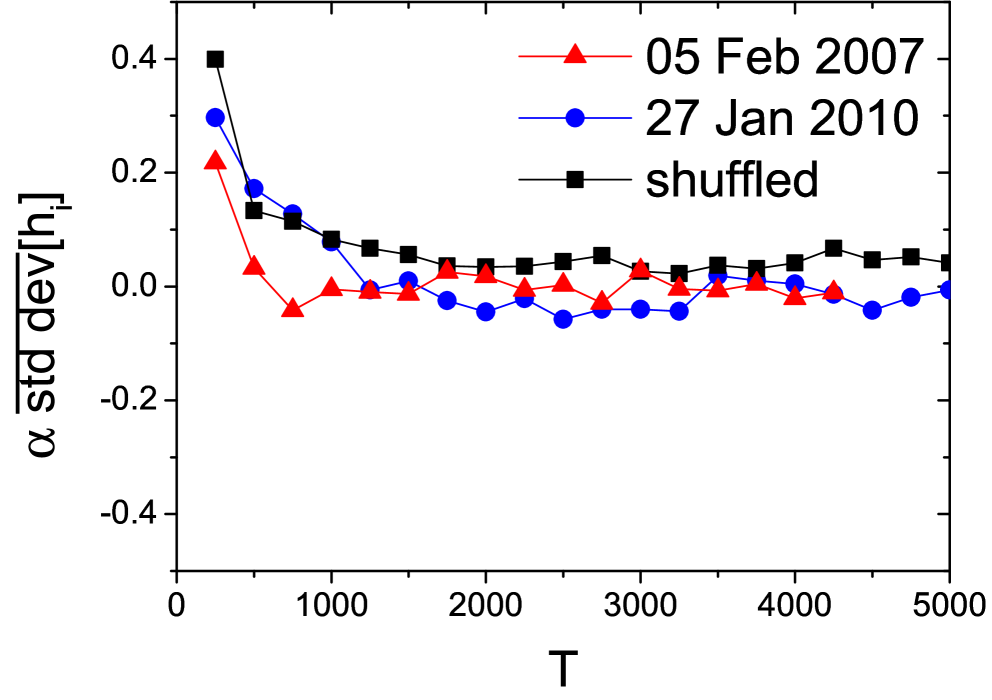

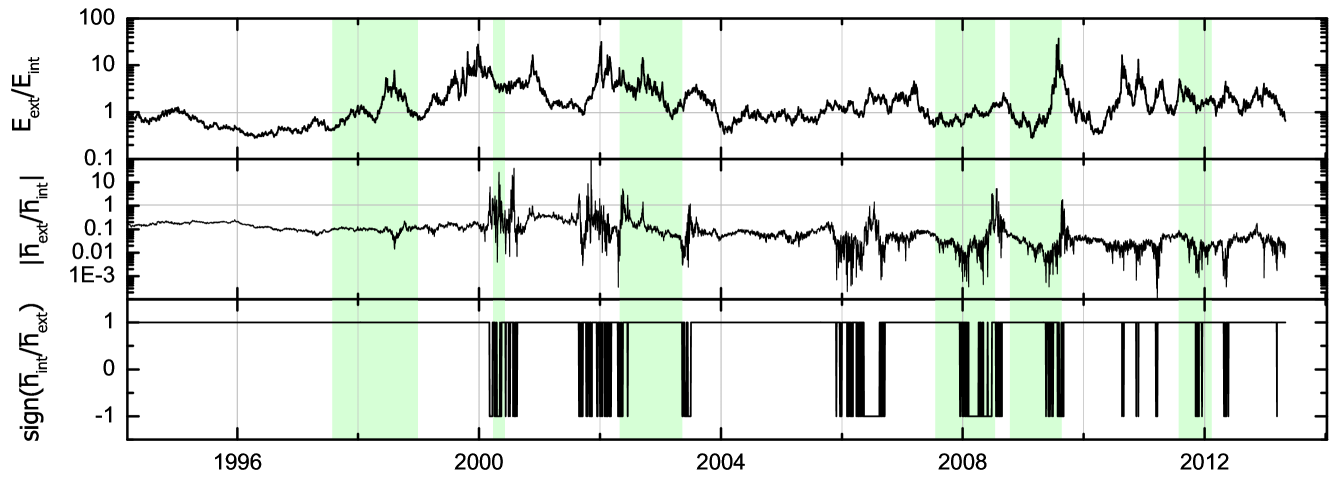

Considering the two terms in the system’s Hamiltonian [Eq. (2)], it is also possible to define internal and external influences in the market. For this purpose, external fields can be interpreted as the influence of external factors, , while couplings define internal bias, (in the MF sense) Bury (2013b). In this case, external contribution corresponds to the individual stocks biases which come from outside the market, while internal one is solely defined in terms of internal market interactions. Similarly, one can also define two energy terms as , where . Figure 17 shows that both energies have almost the same order of magnitude over the historical period considered, while near the major crashes is more than 10 times bigger than . The ratio between the mean biases also possesses interesting historical dynamics. Being in principle strongly correlated with the mean return ( for and for ) discrepancies between them might be used as a leading indicator of financial instabilities. Away from the periods of crisis, their ratio is almost stable, while divergent behavior is observed before the U.S. market crashes (two bottom panels in Fig. 17). Possible explanation of the observed behavior from a financial point of view is still an open question.

IV Conclusion

We have investigated various aspects of application of the pairwise interaction model to financial time series. The model, being parametrized by external fields and couplings, is used for the approximation of the joint equilibrium distribution of stock returns. Since the considered learning algorithms require use of binary variables, the logarithmic returns are binarized using the sign function. Effect of the binarization suggests that the distribution of binary returns captures the distributions of raw and standardized returns to a good degree, preserving information about market correlation structure, economic cycles and market crashes as well as industry-related market clustering structure.

The model parameters are inferred using approximate and exact learning algorithms. Mean field approximations nicely recover bulk of the couplings except outliers, which can be correctly inferred using small correlation expansions. External fields are in the almost perfect agreement with the exact algorithm if the diagonal-weight trick is used. The obtained results also suggest that the quality of approximate inference methods drops in the periods of financial crises due to increase of magnitude of the correlations observed. For the historical period considered, the distribution of external fields is close to the Gaussian and does not possess any outliers independently of moving window size. On the contrary, the distribution of couplings possesses a heavy positive tail, which starts to dominate over the Gaussian bulk for bigger moving window sizes. Mean of external fields decreases with the number of stocks while their standard deviation remains almost constant, corresponding to the standard deviation of the external fields inferred on randomly shuffled time series. Scaling properties of the distribution of couplings depends on the moving window size, becoming closer to the properties of the Gaussian distribution with its growth. Despite possible presence of finite-size effects, an industry-related clustering structure is observed for both exact and approximate couplings. The performed cutoff analysis suggests that the biggest positive couplings as well as eigenmodes with the biggest eigenvalues contain all information about this structure. Scaling properties of the couplings between a small random subset of stocks suggest that the underlying network structure is also preserved with the number of stocks. Finally, the pairwise interaction model also allows one for defining the external and internal biases which correspond to contribution of external fields and couplings respectively. Discrepancies between them might be used as a precursor of imminent financial instabilities and should be explained from a financial point of view. These non-trivial market properties as well as their historical evolution will be studied in the future works, where one of the natural extensions to incorporate dynamics is to consider the kinetic Ising model Roudi and Hertz (2011).

V Acknowledgments

This work is supported by Nordita, VR VCB 621-2012-2983, U.S. DOE, the Marie Curie Training Network NETADIS (FP7, grant 290038), the Kavli Foundation and the Norwegian Research Councils Centre of Excellent Scheme. We are also grateful to the anonymous referees for their valuable suggestions.

References

- Johnson et al. (2003) N. F. Johnson, P. Jefferies, and P. M. Hui, Financial Market Complexity (Oxford University Press, Oxford, 2003).

- Sornette (2009) D. Sornette, Why Stock Markets Crash: Critical Events in Complex Financial Systems (Princeton University Press, Princeton, NJ, 2009).

- Albert and Barabási (2002) R. Albert and A.-L. Barabási, Rev. Mod. Phys. 74, 47 (2002).

- Kacperski and Hołyst (1999) K. Kacperski and J. A. Hołyst, Phys. Lett. A 254, 53 (1999).

- Kiyono et al. (2006) K. Kiyono, Z. R. Struzik, and Y. Yamamoto, Phys. Rev. Lett. 96, 068701 (2006).

- Barabási and Albert (1999) A.-L. Barabási and R. Albert, Science 286, 509 (1999).

- Dorogovtsev and Mendes (2003) S. N. Dorogovtsev and J. F. F. Mendes, Evolution of Networks: From Biological Nets to the Internet and WWW (Physics) (Oxford University Press, New York, NY, 2003).

- Bornholdt and Schuster (2003) S. Bornholdt and H. G. Schuster, eds., Handbook of Graphs and Networks: From the Genome to the Internet (John Wiley & Sons, New York, NY, 2003).

- Gai and Kapadia (2010) P. Gai and S. Kapadia, Philos. Trans. R. Soc. Lond. A 466, 2401 (2010).

- Newman (2003) M. Newman, SIAM Rev. Soc. Ind. Appl. Math. 45, 167 (2003).

- Fronczak et al. (2007) P. Fronczak, A. Fronczak, and J. A. Hołyst, Eur. Phys. J. B 59, 133 (2007).

- Strogatz (2001) S. H. Strogatz, Nature 410, 268 (2001).

- Holme and Newman (2006) P. Holme and M. E. J. Newman, Phys. Rev. E 74, 056108 (2006).

- Klemm et al. (2003) K. Klemm, V. M. Eguíluz, R. Toral, and M. San Miguel, Phys. Rev. E 67, 026120 (2003).

- Bury (2013a) T. Bury, Physica A 392, 1375 (2013a).

- Jaynes (1957a) E. T. Jaynes, Phys. Rev. 106, 620 (1957a).

- Jaynes (1957b) E. T. Jaynes, Phys. Rev. 108, 171 (1957b).

- Schneidman et al. (2006) E. Schneidman, M. J. Berry, R. Segev, and W. Bialek, Nature 440, 1007 (2006).

- Roudi et al. (2009) Y. Roudi, J. Tyrcha, and J. Hertz, Phys. Rev. E 79, 051915 (2009).

- LeCun et al. (2007) Y. LeCun, S. Chopra, R. Hadsell, M. Ranzato, and F. J. Huang, in Predicting Structured Data (The MIT Press, Cambridge, MA, 2007) pp. 191–246.

- Maskawa (2002) J. Maskawa, Physica A 311, 563 (2002).

- Bury (2013b) T. Bury, Eur. Phys. J. B 86, 1 (2013b).

- Zeng et al. (2014) H.-L. Zeng, R. Lemoy, and M. Alava, J. Stat. Mech. 2014, P07008 (2014).

- Vértes et al. (2011) P. E. Vértes, R. M. Nicol, S. Chapman, N. Watkins, D. A. Robertson, and E. T. Bullmore, Front. Syst. Neurosci. 5, 75 (2011).

- Hommes (2001) C. Hommes, Quant. Financ. 1, 149 (2001).

- Mantegna (1999) R. Mantegna, Eur. Phys. J. B 11, 193 (1999).

- Onnela et al. (2003) J.-P. Onnela, A. Chakraborti, K. Kaski, J. Kertész, and A. Kanto, Phys. Scr. 2003, 48 (2003).

- Bonanno et al. (2004) G. Bonanno, G. Caldarelli, F. Lillo, S. Miccich , N. Vandewalle, and R. Mantegna, Eur. Phys. J. B 38, 363 (2004).

- (29) http://www.finance.yahoo.com/.

- Lee et al. (2013) C. Lee, J. Lee, and A. Lee, Statistics for Business and Financial Economics, 3rd ed. (Springer, New York, NY, 2013).

- Pindyck and Rubinfeld (1998) R. S. Pindyck and D. L. Rubinfeld, Econometric models and economic forecasts, Vol. 4 (Irwin/McGraw-Hill Boston, 1998).

- Utsugi et al. (2004) A. Utsugi, K. Ino, and M. Oshikawa, Phys. Rev. E 70, 026110 (2004).

- Podobnik et al. (2010) B. Podobnik, D. Wang, D. Horvatic, I. Grosse, and H. E. Stanley, EPL (Europhysics Letters) 90, 68001 (2010).

- Fenn et al. (2011) D. J. Fenn, M. A. Porter, S. Williams, M. McDonald, N. F. Johnson, and N. S. Jones, Phys. Rev. E 84, 026109 (2011).

- Amari et al. (1992) S.-I. Amari, K. Kurata, and H. Nagaoka, IEEE Trans. Neural. Netw. 3, 260 (1992).

- Tanaka (1998) T. Tanaka, Phys. Rev. E 58, 2302 (1998).

- Sessak and Monasson (2009) V. Sessak and R. Monasson, Journal of Physics A: Mathematical and Theoretical 42, 055001 (2009).

- Aurell and Ekeberg (2012) E. Aurell and M. Ekeberg, Phys. Rev. Lett. 108, 090201 (2012).

- Sohl-Dickstein et al. (2011) J. Sohl-Dickstein, P. B. Battaglino, and M. R. DeWeese, Phys. Rev. Lett. 107, 220601 (2011).

- Nguyen and Berg (2012) H. C. Nguyen and J. Berg, Phys. Rev. Lett. 109, 050602 (2012).

- Laloux et al. (1999) L. Laloux, P. Cizeau, J.-P. Bouchaud, and M. Potters, Phys. Rev. Lett. 83, 1467 (1999).

- Borysov and Balatsky (2014) S. S. Borysov and A. V. Balatsky, PLoS ONE 9, e105874 (2014).

- Coelho et al. (2007) R. Coelho, S. Hutzler, P. Repetowicz, and P. Richmond, Physica A 373, 615 (2007).

- Ravikumar et al. (2010) P. Ravikumar, M. J. Wainwright, and J. D. Lafferty, Ann. Statist. 38, 1287 (2010).

- Hagberg et al. (2008) A. A. Hagberg, D. A. Schult, and P. J. Swart, in Proceedings of the 7th Python in Science Conference (SciPy2008) (Pasadena, CA USA, 2008) pp. 11–15.

- Roudi and Hertz (2011) Y. Roudi and J. Hertz, Phys. Rev. Lett. 106, 048702 (2011).

| Ticker | Name | Sector | Ticker | Name | Sector |

|---|---|---|---|---|---|

| ABT | Abbott Laboratories | Hea | AIG | American International Group, Inc. | Fin |

| AMGN | Amgen Inc. | Hea | APA | Apache Corp. | Bas |

| APC | Anadarko Petroleum Corp. | Bas | AAPL | Apple Inc. | Con |

| AXP | American Express Company | Fin | BA | The Boeing Company | Ind |

| BAC | Bank of America Corp. | Fin | BAX | Baxter International Inc. | Hea |

| BMY | Bristol-Myers Squibb Company | Hea | C | Citigroup, Inc. | Fin |

| CAT | Caterpillar Inc. | Ind | CELG | Celgene Corporation | Hea |

| CL | Colgate-Palmolive Co. | Con | CMCSA | Comcast Corporation | Ser |

| COP | ConocoPhillips | Bas | COST | Costco Wholesale Corp. | Ser |

| CSCO | Cisco Systems, Inc. | Tec | CVS | CVS Caremark Corp. | Ser |

| CVX | Chevron Corp. | Bas | DD | E. I. du Pont de Nemours and Co. | Bas |

| DE | Deere & Company | Ind | DELL | Dell Inc. | Tec |

| DHR | Danaher Corp. | Ind | DIS | The Walt Disney Company | Ser |

| DOW | The Dow Chemical Company | Bas | EMC | EMC Corporation | Tec |

| EMR | Emerson Electric Co. | Tec | EOG | EOG Resources, Inc. | Bas |

| EXC | Exelon Corp. | Uti | F | Ford Motor Co. | Con |

| GE | General Electric Company | Ind | HAL | Halliburton Company | Bas |

| HD | The Home Depot, Inc. | Ser | HON | Honeywell International Inc. | Ind |

| HPQ | Hewlett-Packard Company | Tec | IBM | International Business Machines Corp. | Tec |

| INTC | Intel Corp. | Tec | JNJ | Johnson & Johnson | Hea |

| JPM | JPMorgan Chase & Co. | Fin | KO | The Coca-Cola Company | Con |

| LLY | Eli Lilly and Company | Hea | LOW | Lowe’s Companies Inc. | Ser |

| MCD | McDonald’s Corp. | Ser | MDT | Medtronic, Inc. | Hea |

| MMM | 3M Company | Cng | MO | Altria Group Inc. | Con |

| MRK | Merck & Co. Inc. | Hea | MSFT | Microsoft Corp. | Tec |

| NKE | Nike, Inc. | Con | ORCL | Oracle Corporation | Tec |

| OXY | Occidental Petroleum Corp. | Bas | PEP | Pepsico, Inc. | Con |

| PFE | Pfizer Inc. | Hea | PG | The Procter & Gamble Company | Con |

| PNC | The PNC Financial Services Group | Fin | SLB | Schlumberger Limited | Bas |

| SO | Southern Company | Uti | T | AT&T, Inc. | Tec |

| TGT | Target Corp. | Ser | TJX | The TJX Companies, Inc. | Ser |

| TXN | Texas Instruments Inc. | Tec | UNH | UnitedHealth Group Incorporated | Hea |

| UNP | Union Pacific Corp. | Ser | USB | U.S. Bancorp | Fin |

| UTX | United Technologies Corp. | Ind | VZ | Verizon Communications Inc. | Tec |

| WFC | Wells Fargo & Company | Fin | WMT | Wal-Mart Stores Inc. | Ser |

| XOM | Exxon Mobil Corp. | Bas |

Industry sectors are defined as Basic Materials (Bas), Conglomerate (Cng), Consumer Goods (Con), Financial (Fin), Healthcare (Hea), Industrial Goods (Ind), Services (Ser), Technology (Tec) and Utilities (Uti).