The Social Cost of Carbon with

Economic and Climate Risks

††thanks: We thank Kenneth Arrow, Buz Brock, Varadarajan V. Chari, Jesus Fernandez-Villaverde,

Larry Goulder, Lars Peter Hansen, Tom Hertel, Larry Karp, Tim Lenton,

Robert Litterman, Alena Miftakhova, Karl Schmedders, Christian Traeger,

Rick van der Ploeg, and Ole Wilms for comments on earlier versions

of this paper. We thank the anonymous referees for their helpful comments.

We are grateful for comments from audiences at the

2014 Minnesota Conference on Economic Models of Climate Change, the

2014 Stanford Institute for Theoretical Economics, and the 2012 IIES

Conference on Climate and the Economy. Cai acknowledges

support from the Hoover Institution and the National Science Foundation

grant SES-0951576. Financial support for Lontzek was provided by the

Zürcher Universitätsverein, the University of Zurich, and the Ecosciencia

Foundation. This research is part of the Blue Waters sustained-petascale

computing project, which is supported by the National Science Foundation

(awards OCI-0725070 and ACI-1238993) and the State of Illinois. Blue

Waters is a joint effort of the University of Illinois at Urbana-Champaign

and its National Center for Supercomputing Applications. This research

was also supported in part by NIH through resources provided by the

Computation Institute and the Biological Sciences Division of the

University of Chicago and Argonne National Laboratory, under grant

1S10OD018495-01. We also thank the HTCondor team

of the University of Wisconsin-Madison for their support. The earlier

versions of this paper include “The Social Cost of Stochastic and

Irreversible Climate Change” (NBER working paper 18704), “DSICE:

A Dynamic Stochastic Integrated Model of Climate and Economy” (RDCEP

working paper 12-02), and “Tipping Points in a Dynamic Stochastic

IAM” (RDCEP working paper 12-03).

Abstract

There is great uncertainty about future climate conditions and the appropriate policies for managing interactions between the climate and the economy. We develop a multidimensional computational model to examine how uncertainties and risks in the economic and climate systems affect the social cost of carbon (SCC)—that is, the present value of the marginal damage to economic output caused by carbon emissions. The SCC is substantially increased by economic and climate risks at both current and future times. Furthermore, the SCC is itself a stochastic process with significant variation; for example, the basic elements of risk incorporated into our model cause the SCC in 2100 to be, with significant probability, ten times what it would be without those risks. We have only imprecise information about what parameter values are best for approximating reality. To deal with this parametric uncertainty we perform extensive uncertainty quantification and show that these findings are robust for a wide range of alternative specifications. More generally, this work shows that large-scale computing can enable economists to examine substantially more complex and realistic models for the purposes of policy analysis.

Key words: Climate policy, social cost of carbon, climate tipping process, Epstein–Zin preferences, stochastic growth, long-run risk

Yongyang Cai

Becker Friedman Institute at the University of Chicago, and Hoover Institution

Stanford, CA 94305, USA

yycai@stanford.edu

Kenneth L. Judd

Hoover Institution and NBER

Stanford, CA 94305, USA

kennethjudd@mac.com

Thomas S. Lontzek

Department of Business Administration, University of Zurich

8044 Zurich, Switzerland

thomas.lontzek@business.uzh.ch

1 Introduction

Global warming has been recognized as a growing potential threat to economic well-being. This concern has lead to an increasing number of national and international discussions on how to respond to this threat. Determining which policies should be implemented will require merging quantitative assessments of the likely economic impacts of carbon emissions with models of how the economic and climate systems interact; this is the purpose of integrated assessment models (IAMs). This paper expands the scope of IAMs by adding uncertainties and risks to a canonical model of the economic and climate systems, and shows that such risks significantly raise the optimal level of carbon emission mitigation.

The impact of carbon emissions on society is measured by the social cost of carbon (SCC), defined as the marginal economic loss caused by an extra metric ton of atmospheric carbon. The Intergovernmental Panel on Climate Change (IPCC), whose reviews summarize scientific studies on climate change, reports that estimates of the SCC vary across studies with an average estimate of $43 per ton of carbon (Yohe et al. 2007).111We denote all monetary units in United States dollars. The social cost of carbon is sometimes measured in units of carbon dioxide. To convert the social-cost-of-carbon values presented in this study to units of carbon dioxide divide by 44/12. The Interagency Working Group on Social Cost of Carbon (IWG)—a joint effort involving several United States federal agencies—came to similar conclusions in a report based on often-used integrated assessment models (IWG 2010). Most IAM models assume myopic expectations. The DICE (Dynamic Integrated Climate and Economy) model of Nordhaus (2008) is one of the few forward-looking integrated assessment models222Most integrated assessment models are static and only a few, such as those of Nordhaus (2008), Manne and Richels (2005), and Nordhaus and Yang (1996), are based on dynamic models of agent decision making. and suggests a social cost of carbon of $35 per ton of carbon. This rough consensus has been challenged by Pindyck (2013) and IPCC (2014), who argue that all of these estimates are limited because they come from IAMs that ignore the considerable risk and uncertainty in both the economic and the climate system, and their interactions. Those models also assume that people are far less risk averse than indicated by economic observations of the price of risk.

This study presents Dynamic Stochastic Integration of Climate and the Economy (DSICE), a computational, dynamic, stochastic general equilibrium framework for studying global models of both the economy and the climate. We apply it to the specific issue of how the social cost of carbon depends on stochastic features of both the climate and the economy when we apply empirically plausible specifications for the willingness to pay to reduce economic risk. The examples we study demonstrate the flexibility of the DSICE framework.

We first examine how economic risks affect the social cost of carbon. Specifically, we assume that factor productivity growth displays long-run risk as modeled by Bansal and Yaron (2004) and Beeler and Campbell (2011). We calibrate the stochastic productivity growth process to match observed moments of the growth rates for per capita consumption. We combine this with recursive utility specifications of dynamic preferences that use parameter values consistent with observations about how much people are willing to pay to reduce consumption risk. This version of our model demonstrates that realistic specifications of risks in the economic system will imply substantially greater social costs of carbon; for example, the 2005 SCC in our benchmark parameter case is $61 per ton of carbon, 65 percent larger than the SCC in the absence of productivity shocks.

Current empirical analyses do not give us precise estimates of critical parameters. Therefore, following the response surface methods from the uncertainty quantification literature (see Oberkampf and Roy (2010) for a comprehensive discussion of verification, validation, and uncertainty quantification (VVUQ)), we also examine a large set of empirically plausible values for key parameters, such as the risk aversion parameter and the elasticity of inter-temporal substitution. We find that the 2005 SCC ranges from $35 to $115 per ton of carbon over the parameter values we consider. These results demonstrate that we should be skeptical of studies that rely on a single parameterization, but the application of uncertainty quantification methods supports the qualitative claim that economic risks significantly increase the SCC.

Of equal interest and greater novelty are our results on the dynamics of the future SCC. Stochastic factor productivity creates riskiness in future output and carbon emissions, which in turn makes the SCC a random process. Conventional IAMs assume no riskiness and produce a deterministic path for the future SCC. A common interpretation of results in deterministic models is that a quantity’s path represents its expectation in more realistic models. In many cases, we find that the mean path for the SCC is close to that implied by deterministic models, thereby confirming the value of deterministic models for approximating expectations. DSICE, however, can also determine the stochastic features of the SCC process and shows that the SCC is approximately a random walk with substantial variance. For example, in our benchmark case the expected SCC is $286 in 2100 but with a 10% chance of exceeding $700 and a 1% chance of exceeding $1,200. In general, the variance of the social cost of carbon grows faster than its mean. Any description of the future must recognize both the intrinsic risk in any fixed model and our uncertainty about the best values for parameters. Combining parameter uncertainty with intrinsic risk implies a substantially larger range for the future SCC.

The second source of uncertainty incorporated into DSICE is uncertainty about how the climate will respond to anthropogenic emissions. Most integrated assessment models assume that the impact of climate on productivity depends only on the contemporaneous temperature. This implies a smooth, predictable and reversible pattern of damages from global warming. The stochastic climate feature we add is based on the recent literature on climate tipping elements. These are defined as any subsystem of the Earth’s system that could exhibit critical points (tipping points) where the climate abruptly and unexpectedly jumps to a qualitatively different state (Lenton et al. 2008). The climate literature has identified several major tipping elements in the climate system. Recent projections suggest that the irreversible melting of the Greenland ice sheet could be triggered during this century (IPCC 2014); such melting could cause the global sea level to rise by 0.5–1.0 meter per century (Lenton et al. 2008). Joughin et al. (2014) argue that the collapse of the west Antarctic ice sheet is already under way. Other examples of climate tipping elements include the weakening or shutdown of the Atlantic thermohaline circulation and the dieback of the Amazon rainforest. Current temperature affects the likelihood of crossing a tipping point, but temperature reversals will not reverse the tipping event.

Tipping points bring a new dimension to the modeling of the climate’s effect on the economy. For example, once warming melts a glacier, that glacier will not reform even if the warming is reversed, and damages arising from the rising sea levels will persist. Tipping phenomena bring a qualitative new feature to climate damage in that some of the current damage to productivity is due to past warming. A recent review recommends that we should seriously consider climate tipping points in order to better anticipate and prepare ourselves for the inevitable, potentially adverse surprises they bring (National Research Council 2013).

DSICE is sufficiently flexible to incorporate tipping elements of various kinds in terms of probability, duration, and impact levels. This allows us to consider a range of beliefs about the likelihood of warming triggering a climate tipping point, and to determine how optimal policy and the social cost of carbon depend on the characteristics of a tipping element. For our benchmark parameter specification of preferences, stochastic growth, and the climate tipping process we find that the 2005 social cost of carbon is $125 per ton of carbon, but a value of $354 is also consistent with plausible specifications for climate tipping processes.

Some studies (e.g., Weitzman 2009) use the possibility of very high damage caused by a very low probability catastrophic event to advocate aggressive mitigation policies. Estimating the probability of tail events is very difficult, a fact that reduces the force of these arguments. Our DSICE results show that climate tipping specifications that imply bad, but not catastrophic, events can imply a very high social cost of carbon. Extreme disaster scenarios are not the only assumptions that justify high social costs of carbon.

Uncertainty about damage from a climate tipping event raises the social cost of carbon in a manner similar to the impact of risk in consumption-based capital asset pricing models: the social cost of carbon is proportional to the variance of uncertainty regarding damage. One interpretation of such variance is that it represents our ignorance of damage from the climate tipping process. This observation shows that DSICE could be used to determine which scientific studies would be most cost-effective in reducing the uncertainties faced by policymakers. This is just one example of how the DSICE framework could be applied in future studies.

Our models demonstrate that any discussion of the social cost of carbon must consider stochastic elements in both the climate and the economic system. We also find that these elements have nontrivial interactions. For example, in our default parameter cases each component—when studied in isolation—sharply elevates the social cost of carbon, but when both economic and climate risks are included the resulting SCC process lies in between the levels of the individual effects. One cannot just look at these risks in isolation and advance some ad hoc argument on how to aggregate results across studies.

The ability of DSICE to track the stochastic behavior of the social cost of carbon makes it a potential tool for assessing a variety of policy questions because uncertainties about the social cost of carbon will affect the ranking of alternative policies. R&D decisions are certainly one example of this. R&D decisions made today will determine the mitigation methods available in future decades. A deterministic model would compare the expected benefits with the expected costs, using the discount rate that is applied to all inter-temporal decisions. This procedure is not valid in a dynamic stochastic context. For instance, our results show that there is a good chance that the social cost of carbon will be so high in a few decades that optimal policy would not only reduce carbon emissions but would also use technologies that remove carbon from the atmosphere. The development of such technologies could take decades to complete. Policy discussions today about R&D investment in developing those technologies should not compare the expected social cost of carbon in the future with the expected results of R&D investments, but should focus instead on the present value of having such technologies in those states of the world where the SCC justifies their deployment.

The R&D illustration is just one example of a more general and important point. In deterministic models, mitigation spending is a form of investment and subjected to the same net present value criterion as all other investments. There is a consensus that the choice of discount rate is a major determinant of optimal policy (e.g., Stern 2007 and Nordhaus 2007). Some have argued that this is not the right way to think about mitigation expenditures in an uncertain and risky world. Schneider (1989), in his testimony to the Committee on Energy and Commerce in 1989, argued that investing in climate change mitigation is like "buying insurance against the real possibility of large and potentially catastrophic climate change." DSICE is the first IAM modeling framework that can capture insurance and hedging values of climate change policies. Further development of these ideas must be left to future research, but basic economic intuition suggests that real option values and insurance ideas will play significant roles in evaluating alternative policies.

This study also demonstrates the value of modern high-power computing in studying basic economics questions. The versions of DSICE that we examine are stochastic, nine-dimensional, nonlinear dynamic programming problems. Including stochastic productivity requires the use of annual time periods, and the long-run nature of climate change requires a multi-century time span. The non-stationary character of the problems makes value function iteration the only appropriate approach. The specifications of risks make these problems among the most computationally demanding ever solved in economics. We are able to solve them because we use efficient multivariate methods to approximate value functions, and reliable optimization methods to solve the Bellman equations (Cai and Judd 2010; Cai et al. 2015). Any numerical computation has numerical errors. Another theme of the VVUQ literature is that computational results should be tested to verify their accuracy. Every value function we compute passes demanding verification tests, giving us confidence that numerical errors do not affect our economic conclusions. Some examples required tens of thousands of core hours, and sensitivity analysis demanded that we examine hundreds of cases to determine the robustness of results across empirically plausible parameter values. This study required the use of a few million core hours on Blue Waters, a modern supercomputer. Our use of general purpose methods shows that many economics problems with similar computational requirements can now be solved.

The structure of this paper is as follows. Section 2 compares our work with other studies. We present the economic model in Section 3 and the climate model in Section 4. In Section 5 we formulate the dynamic programming problem, outline its solution method, and present a general calibration strategy. Sections 6, 7, and 8 present and discuss implications for the social cost of carbon from stochastic specifications of factor productivity growth and a climate tipping process; first each in isolation and then combined. Section 9 concludes.

2 Relation to the Literature

Our work contributes to the popular debate on how urgently policymakers should address climate change issues. Many cost-benefit analyses of climate change, such as that of Nordhaus (2008), suggest global climate policy should be relatively weak. Others, including Pindyck (2013), Kopits et al. (2014), Lenton and Ciscar (2013), and Ackerman et al. (2013) have criticized these analyses for their unrealistic specifications. In DSICE, we describe the uncertainty regarding economic growth and future climate impacts in more realistic ways and support recent suggestions, such as those made in Revesz et al. (2014), that the costs of carbon emissions are underestimated.

DSICE follows recent developments in macroeconomic theory and data analysis. Macroeconomists have recently argued that economic output follows processes with persistence in growth rates, and that recursive preferences do the best in terms of representing attitudes towards risk. These insights have been included in a few recent papers on global warming using simplified models. Bansal and Ochoa (2011) assume that consumption and output are exogenous stochastic processes. DSICE instead builds on a Ramsey-type, representative agent, stochastic growth model. We calibrate the stochastic factor productivity growth so that the resulting consumption process is statistically close to empirical data. Jensen and Traeger (2014) includes endogenous output but assumes much lower volatility than implied by empirical data.333See Appendix B for a detailed comparison. Moreover, Jensen and Traeger (2014) assume that carbon emissions have an immediate impact on economic productivity, whereas DSICE and most integrated assessment models assume a time lag between emissions and impacts. Ignoring this lag will likely overestimate the SCC and will create an unrealistically strong correlation between short-run fluctuations in atmospheric carbon and their economic impacts.

DSICE also adds tipping events to the standard IAM model form. The climate literature has identified several major tipping elements in the climate system. An example of a major tipping element is irreversible melting of the Greenland ice sheet. Recent projections of future global warming suggest that it is more likely than not that the Greenland ice sheet tipping point will be triggered within this century (IPCC 2014). Joughin et al. (2014) argue that marine west Antarctic ice sheet collapse is already under way. Melting of the Greenland ice sheet (which contains the equivalent of about seven meters of global sea level) could lead to a global sea level rise of up to 0.5–1 meter per century (Lenton et al. 2008). Other examples of climate tipping elements include the weakening or shutdown of the Atlantic thermohaline circulation or the dieback of the Amazon rainforest.

Economic analyses of tipping elements have used a variety of specifications, ranging from purely deterministic representations (e.g., Keller et al. 2004; Mastrandrea and Schneider 2001; Nordhaus 2012; and Weitzman 2012) to fully stochastic specifications (e.g., Polasky et al. 2011; Brock and Starrett 2003; and Lemoine and Traeger 2014). However, stochastic formulations of tipping processes have not been incorporated into major integrated assessment models such as that of Nordhaus (2008).444There are a few lower-dimensional, stochastic variants of Nordhaus (2008), such as Kelly and Kolstad (1999) and Lemoine and Traeger (2014). Our computational method can deal with this complexity.

Our tipping element specification is also the first to address the recent critique by Kopits et al. (2014) of current studies which assume that the full impact of a climate tipping point is immediate and its level is known (see, e.g., Lemoine and Traeger 2014). The nature of climate tipping point events is very different from that currently being assumed in economic models. The occurrence, or not, of the tipping point is unknown, the transition time of the tipping process is unknown, and—furthermore—the impact of the climate tipping is unknown (Lenton et al. 2008; National Research Council 2013).

The structure of DSICE and its calibration strategy enable us to retain the deterministic integrated assessment model in Nordhaus’s (2008) model as a special case of DSICE, when we eliminate all shocks to climate and the economy and adjust the preference parameters accordingly. The model in Nordhaus (2008) is currently being used by the United States government to design climate policy (IWG 2010) and we wish to compare its implications for climate policy with those obtained from our modeling approach. However, we will note that DSICE is not just a stochastic extension of earlier versions of Nordhaus (2008). Our framework can be used to solve many integrated assessment models of comparable dimensionality.

The distinctive feature of DSICE is that it combines stochastic factor productivity growth with uncertainty about adverse, irreversible climate events, uses recursive preferences, and enables us to examine and quantify the impact of economic and climate risks on the social cost of carbon. No computational framework is infinitely powerful, but it is clear that DSICE is far less limited by tractability concerns than are earlier integrated assessment models. Future work will take advantage of our framework and computational strengths to study alternative models, even ones larger than those examined below.

3 The Economic Model

Our model’s framework merges a basic dynamic stochastic general equilibrium model with a commonly used climate model. The canonical “Dynamic Integrated Climate–Economy” (DICE) model (Nordhaus, 2008) will be a special case of our dynamic stochastic integrated assessment framework. In particular, DSICE includes two stochastic processes not part of earlier integrated assessment models.

First, we include an exogenous stochastic process that affects productivity. This productivity process could represent an autoregressive productivity shock, or a process that implies consumption processes similar to those described in the literature on stochastic growth with persistence.

Second, we include a finite-state Markov process, , that also affects productivity but with transitions that are affected by temperature, making an endogenous process representing the impact of past climate change on current productivity. In this paper, models tipping elements in climate dynamics (Kriegler et al. 2009 and Lenton et al. 2008), a feature of climate change dynamics that has only recently has been studied by climate scientists.

We describe the economic model in detail in this section, including only those climate elements that directly relate to productivity. A later section gives the details of the climate system. This approach to exposition helps make clear the two distinct systems, climate and economy, and their interactions. Regarding the calibration of DSICE for numerical results, we present our calibration strategy in Section 5.2 while a list of all parameters and exogenous processes of the economic model appears in Appendices A and B.

3.1 Production

The economic side of DSICE is a simple stochastic growth model where production produces greenhouse gas emissions and productivity is affected by the state of the climate. In this section we will model the climate system in a general fashion that only describes the interactions between climate and economic productivity. The next section will give the motivation for and specification of the climate module. One advantage of this approach is that it makes clear the limited nature of the linkages between climate and economy and also makes clear how one can replace our climate module with any alternative.

We assume time is discrete, with each period equal to one year. Let be the world capital stock in trillions of dollars at time and be the world population in millions at time . We use the exogenous population path from Nordhaus (2008)

| (1) |

In the absence of any climate damage, the gross world product is described by a Cobb–Douglas production function with

where (as in Nordhaus, 2008) and is productivity at time . Productivity is decomposed into two pieces: a deterministic trend , and a stochastic productivity state , that is to say that . The deterministic trend is taken from Nordhaus (2008) and equals

| (2) |

where is the initial growth rate and is the decline rate of the growth rate. We want to examine how uncertainty in productivity interacts with climate change policies.

We use one extra state to help model the stochastic productivity state , where represents the persistence of . More specifically, we start with the formulation introduced in Bansal and Yaron (2004) with the following form:

| (3) |

| (4) |

Bansal and Yaron assumed that and , , and are parameters. Gaussian disturbances are, unfortunately, unbounded and would produce arbitrarily large growth rates and output, creating an unbounded optimal growth problem where even the existence of expected utility is unclear. Even if we could overcome the theoretical and computational challenges, results for the social cost of carbon could be driven by highly unlikely tail events. An example of this is the dismal theorem of Weitzman (2009) showing that the risk premium could be infinite for unboundedly distributed uncertainties. We do want to avoid existence issues and excessive dependence on extreme tail events. To this end, we construct a time-dependent, finite-state Markov chain for that implies conditional and unconditional moments of consumption processes calibrated to observed market data. The Markov transition processes are denoted and , where and are two serially independent stochastic processes. This approach also makes it possible to directly apply reliable numerical methods for solving dynamic programming problems. Appendix B describes these features in greater detail.

DSICE assumes that output is affected by temperature. The production function represents output in the absence of any effects of climate on output.

The impact of climate on output in DSICE will depend on two climate states : global average temperature , and a climate state denoted by . The climate state will model cumulative effects of past temperatures and is represented by a finite-state Markov chain In this paper, we parameterize to represent stages in a climate tipping processes; therefore, we will refer to it as the “tipping state.” DSICE also contains other climate states but this version assumes that only the states and directly affect economic decisions..

The function represents the impact of climate on output, and gross world product equals

where

As is common in the IAM literature, we will call the damage function. We will examine only cases where is bounded by unity, but that is not a requirement in our general framework. When , a state we will call the “pre-tipping state”, our damage function reduces to the damage function in Nordhaus (2008), which is widely used in the literature. This study generalizes the damage function to include effects of the “tipping state” and associated past cumulative effects. The definition of implies ; therefore, the numerical value of the tipping state equals the current damage caused by past tipping events, so we also call the “tipping damage level” when . The stochastic dynamic structure of is specified in more detail below in the section on the climate model.555The interaction between climate and output assumed here affects only total productivity. More generally, the impact of climate could affect the effective capital stock, the effective labor supply, or utility and still fall within our modeling framework.

The economic system affects the climate through emissions of carbon. We assume that industrial emissions are proportional to output, with proportionality factor representing the carbon intensity of output. The social planner can mitigate (i.e., reduce) emissions by a factor with . The annual industrial carbon emissions (billions of metric tons of carbon) equal

| (5) |

We follow Nordhaus (2008) and assume that mitigation expenditures equal

| (6) |

World output (net of damage) is allocated across total consumption , mitigation expenditures , and gross capital investment , that is to say

| (7) |

thus the capital stock evolves according to

| (8) |

where is the annual depreciation rate.

3.2 Epstein–Zin Preferences

The additively separable utility functions commonly used in climate-economy models do not do well in explaining the willingness of people to pay to avoid risk. Here instead, we use Epstein–Zin preferences (Epstein and Zin 1989). Let be the stochastic consumption process. Epstein–Zin preferences recursively define the social welfare as

| (9) |

where is the expectation conditional on the states at time , and is the discount factor. Here,

is the annual world utility function (assuming that each individual has the same power utility function), is the inter-temporal elasticity of substitution,666Here we assume . When , the utility function is negative, the formula becomes: While the standard formulation of Epstein-Zin preferences does not divide by in the annual world utility function , here we use this formulation in order that it is consistent with our later reformulation for the Bellman equation (16). and is the risk aversion parameter. Epstein–Zin preferences are flexible specifications of decision-makers’ preferences regarding uncertainty, and allow us to distinguish between risk preference and the desire for consumption smoothing. Even though we refer to as the risk aversion parameter, the equilibrium risk premia will depend on interactions between and . Epstein–Zin preferences are special cases of Kreps–Porteus preferences (Kreps and Porteus 1978), which were designed to model preferences over the resolution of risk. For the special case where , we have the separable utility case used in Nordhaus (2008).

Epstein–Zin preferences are used here because they better explain observed equity premia. Even though climate change risks are not directly related to equity returns, observations about the equity premia inform us about society’s willingness to pay to reduce consumption risk.777There may be other aspects of climate change that affect social welfare, but they are not included in DSICE, nor in the standard Nordhaus (2008) family of models. Therefore, we expect the optimal climate policy to be affected by uncertainty regarding the economic damage arising from climate change.

4 The Climate Model

Our climate model contains three modules. The first module is the carbon system and the second is the temperature module, both of which are deterministic and adapted from the integrated assessment model of Nordhaus (2008). The underlying idea is that industrial emissions of greenhouse gases increase atmospheric carbon concentrations, causing an increase in global average temperature, which then reduces economic productivity as specified above.

We also add a stochastic tipping element module which represents a state of the climate related to past climate conditions and events. A simple example of such a climate state is sea level. Prolonged periods of warm atmospheric temperatures will (likely) melt ice in glaciers (on land) which will then lead to a higher sea level, which can be viewed as a state variable that affects economic productivity due to, for example, flooding. The addition of the climate tipping module and its associated uncertainties adds a novel element to integrated assessment modeling.

We present our calibration strategy for these modules in Section 5.2 while a list of all parameters and exogenous processes of the model appears in Appendices A and D.

4.1 Carbon Module

We assume two sources for carbon emissions, an industrial source specified above and an exogenous source, , arising from land use. Total emissions are denoted

| (10) |

Carbon is distributed across three “boxes” representing different carbon concentrations. The three-dimensional vector represents the mass of carbon concentrations in the atmosphere, and in the upper levels of the ocean and lower levels of the ocean, respectively (in gigatons of carbon). The carbon cycle specifies how these concentrations evolve over time and is represented by the linear dynamical system

where is the matrix

| (11) |

The coefficients of the matrix have natural interpretations. The coefficient is the rate at which carbon diffuses from level to level , for {atmosphere, upper ocean, lower ocean}. Since this is a closed system except for the emission input , the column sums of must be unity.

4.2 Temperature Module

The temperature module models two temperatures in the atmosphere and the ocean, measured in degrees Celsius. That system is represented by the vector , and evolves according to

| (12) |

where the heat diffusion process between ocean and air is represented by the matrix

| (13) |

The coefficient is the heat diffusion rate from level to level , for {atmosphere, ocean}, and is the rate of atmospheric temperature change by infrared radiation to space (Schneider and Thompson 1981). Atmospheric temperature is affected by exogenous external forcing, , and by interactions between radiation and carbon in the atmosphere. Total radiative forcing at is

| (14) |

where is the preindustrial atmospheric carbon concentration and is the radiative forcing parameter.

4.3 Tipping Element Module

We next describe the dynamics of , the climate state representing the effects of past temperatures on some aspect of the climate that is not captured by the current temperatures and carbon states. We choose a Markov chain for so that the changes in model a tipping with damage as a function of that state. At each time , is one of the finite number of states in the set denoted for some positive integer . The transition probabilities depend on climate states in a general way, but this study considers tipping elements only. With this focus, we will use terminology appropriate for climate tipping elements.

At the initial time, the state of the tipping element is represented by . A common approach is to assume that a tipping point is defined by a definite (but possibly unknown to the planner) threshold, the crossing of which leads immediately to abrupt change. We instead assume that a tipping point is a probabilistic function of climate conditions. Specifically, we follow the common assumption that warming alone causes tipping (IPCC 2014; Smith et al. 2009), but assume that if , the probability that tipping does not occur in the year equals

| (15) |

where is the (linear) hazard rate parameter and is the temperature for which .

One common approach to modeling tipping events is to assume a critical (but perhaps unknown) temperature threshold such that the tipping event happens if temperature reaches the threshold (see Keller et al. 2004). With economic uncertainty, temperatures can fall or rise. If temperature were to cross a threshold, the tipping event would immediately happen even if the temperature quickly fell below the threshold. We prefer a smoother representation of how climate subsystems respond to world average temperature, such as accomplished with our specification in (15).

Once tipping has occurred, there will be more transitions of . This study assumes irreversibility, implying that all positive probability transitions increase . Integrated assessment models that include a tipping element typically assume that all impacts are realized immediately (e.g., Lemoine and Traeger 2014). In our framework, that is equivalent to assuming there are only two climate states related to tipping: . However, climate scientists do not regard this as a realistic description of the tipping elements they consider. Lenton et al. (2008) characterize the transition scales for various tipping elements, arguing, for example, that the loss of Arctic summer sea-ice could be complete after about ten years, but that the melting of the Greenland ice sheet would, once it began, continue for more than three hundred years before reaching its long-run state. In DSICE we present more appropriate specifications for the Markov chain states and the transition probabilities, and can examine the more realistic and general tipping elements preferred by climate scientists.888Lenton and Ciscar (2013) suggest that tipping elements might exhibit domino effects in the sense that several tipping elements could be sequential and the tipping of one might trigger a whole cascade of additional tipping elements. The flexibility of the Markov process approach for makes possible analysis of multiple tipping elements, but that is left for future studies. The applications of DSICE presented below will examine a variety of specifications for the details of the Markov process that represents the effects of tipping elements.

5 The Dynamic Programming Problem

We formulate the nine-dimensional, social planner’s dynamic optimization problem as a dynamic programming problem. The nine states include six continuous state variables (the capital stock , the three-dimensional carbon system , and the two-dimensional temperature vector ) and three discrete state variables (the climate shock , the stochastic productivity state , and the persistence of its growth rate, ). Let denote the nine-dimensional state variable vector and let denote its next period’s state vector.

The Epstein–Zin utility definition expressed utility in terms of consumption. We make a nonlinear change of variables999That is, . and express the Bellman equation in terms of utils, . The Bellman equation then becomes

| s.t. | (16) | ||||

for , and any .101010When , the objective function of the optimization problem is The terminal value function is given in Appendix E. In the model, consumption and emission control rate are two control variables.

5.1 The Social Cost of Carbon

In this paper, we follow the jargon of the climate literature which interprets the social cost of carbon as a marginal concept–that is to say, the monetized economic loss caused by an increase in atmospheric carbon by one metric ton. In our model, the social cost of carbon is the marginal cost of atmospheric carbon expressed in terms of the numeraire good, which can be either consumption or capital as there are no adjustment costs. We define the social cost of carbon (SCC) to be the marginal rate of substitution between atmospheric carbon concentration and capital, as in

| (17) |

It will be important to remember that the social cost of carbon is a relative shadow price–that is to say, a ratio of two marginal utilities, and does not express the total social cost of climate damage.111111Because is measured in trillions of dollars and is measured in billions of tons of carbon, the 1,000 factor is needed to express the social cost of carbon in units of dollars per ton of carbon. For example, as we change economic and/or climate risks, the social cost of carbon may go up or down because that change in risks will affect both the marginal value of carbon and the marginal cost of consumption (or, equivalently, the marginal value of investment). DSICE is a general equilibrium model where the results arise from the assumptions about tastes and technology as well as their equilibrium interactions.

Often, the social cost of carbon and the term carbon tax are used interchangeably. The optimal carbon tax is the tax on carbon that would equate private and social costs of carbon. In our model we also examine the optimal carbon tax, which is the Pigovian tax policy because the externality from carbon emissions can be directly dealt with by a carbon tax and because there are no other market imperfections. The social planner in our model chooses mitigation , which is equivalent to choosing a carbon tax equal to in units of dollars per ton of carbon. If , the carbon tax equals the social cost of carbon. However, if then the carbon tax only equals that level which will drive emissions to zero, and may be far less than the social cost of carbon. In such cases, mitigation policies have reached their limit of effectiveness. Alternative policies may reduce carbon concentrations directly, as would carbon removal and storage technologies, or reduce temperature directly, as would some solar geoengineering technologies. We do not explicitly include those technologies in our model but our social cost of carbon numbers will identify equilibrium paths along which the social cost of carbon is so high that these more direct technologies may be competitive. We leave a quantitative analysis of those issues to future studies.

5.2 General Calibration Strategy

Our calibration strategy has the purpose of enabling us to contrast how a stochastic representation of both climate and the economy along with plausible preferences will affect estimates of the social cost of carbon. For example, the United States government uses the integrated assessment model in Nordhaus (2008) as one of three (deterministic) models to calculate the social cost of carbon (IWG 2010). The United States government study thus neglects any effects of decision making under uncertainty on the optimal social cost of carbon.

For the deterministic part of DSICE we use the general model structure of Nordhaus (2008) and some of its parameters. This approach allows us to retain the Nordhaus (2008) model as a special case of our model when we eliminate all shocks to climate and the economy and adjust the preference parameters accordingly. We will compare all our results to that special case. In addition, we calibrate preferences, the long-run risk specification of stochastic growth and the stochastic climate tipping process, and the parameters governing the dynamics of the three carbon states and the two temperature states. We next summarize our calibration strategy, and provide additional technical details in Appendices B, C, and D.

Parameters of the Deterministic Part of the Economic Model

The parameters describing the deterministic part of the economic model are taken directly from Nordhaus (2008). This includes the specification of the production function as well as exogenous processes for world population and the deterministic trend in productivity. Furthermore, we retain the Nordhaus (2008) specification for the carbon intensity of output and deterministic damage from climate change.

Parameters of the Stochastic Growth Process

The parameters in the productivity process were chosen so that the solution of the stochastic growth benchmark, in the absence of any impact of climate, produces a consumption growth process whose properties, in terms of long-run variances and conditional covariances, are similar to those of U.S. data on per capita consumption growth.121212We are grateful to Ravi Bansal for providing us with the annual per capita data on real consumption used in Bansal et al. (2012) and Beeler and Campbell (2011) and obtained from the Bureau of Economic Analysis website. For this purpose we use a version of our model without stochastic climate impact because the consumption data we use comes from the 20th century when the damage to productivity, caused by climate changes was much smaller than today. In addition, the calibration of the stochastic growth process requires a careful formulation of the Markov chains for the productivity shock and the rate of its growth persistence . Markov chains with only a few states cannot represent the kind of persistence properties observed in Bansal and Yaron (2004). After examining various possibilities, we chose values of and values of at each time ; the time dependence is required due to the fact that the variance of consumption levels grows over time. In Appendix B we show that the statistics of simulation paths of our consumption growth from our calibrated parameters are close to those of the empirical data.

Parameters of the Deterministic Parts of Climate and Temperature Modules

The climate and temperature modules of DSICE are adapted from Nordhaus (2008) with the basic idea that for a given emission scenario the five-dimensional module (two dimensions for climate and three for the carbon cycle) produces paths for carbon concentrations and temperature levels which approximately match those of large, heavily-dimensional climate models. We have also used Nordhaus (2008) as the source for specifying the exogenous processes of emissions arising from biological processes and external radiative forcing. Nevertheless, Cai et al. (2012a) pointed out that the natural interpretation of the computer code in Nordhaus (2008) has future carbon concentrations causing temperature increases today, and its ten-year time step formulation produces results significantly different than results from shorter time steps. For the analyses in the present paper, we had to recalibrate the Nordhaus (2008) parameters governing the dynamics of the three carbon states and the two temperature states to fit into our dynamic programming framework with annual time steps. More precisely, using a benchmark emissions path we use the model in Nordhaus (2008) to generate time series data of ten-year time frequency for the three carbon states and the two temperature states. We then calibrate the parameters of the dynamics of our climate and carbon states so that our model, with the same benchmark emissions path, will produce paths for these five state variables that agree (at every tenth year) with the decadal data from Nordhaus (2008). The mathematical details of this calibration method are presented in Appendix C.

Parameters of the Stochastic Climate Tipping Process

For the implementation of the representative stochastic tipping point process we need to specify parameter values for the likelihood of tipping and the expected duration of the tipping process as well as the mean and variance of the post-tipping impacts.

The key parameters for the tipping element in our examples will be given values that the climate science literature considers plausible. Unfortunately, there is no consensus for these values. For the likelihood of triggering a tipping point process, Kriegler et al. (2009) state that there is a substantial lack of knowledge about the underlying physical processes of climate tipping elements. So far expert elicitation studies have been conducted to assess the character of those processes. While the subjective probabilities implied by these opinions vary greatly, they do represent the range of beliefs in the climate science literature. Any policy maker would also be presented with the same high level of uncertainty. We cannot determine which probability assessments are correct, but we use them to construct a map from the subjective beliefs of experts to the implications for policy choices and the social cost of carbon. We use the Lenton (2010) summary of the findings from Kriegler et al. (2008) and other expert elicitation studies to calibrate the likelihood of triggering the tipping point process.

We also need to choose values for climate damage associated with our tipping element. One theme of this study is the uncertainty in that damage and the rate at which post-tipping damage increases, reflecting climate scientists’ descriptions of tipping point events. We treat the trigger of the tipping event as well as its duration as a stochastic process. Tipping point events have potentially very large impacts on the economy (see IPCC 2014; Smith et al. 2009) but there is great uncertainty about their magnitude. There are few studies that attempt to estimate climate damage, so we rely on the range of views represented in the literature. Stern (2007) reviews existing models which include the risk of tipping point events and estimates impacts at the order of 5–10 percent of gross world product. Nordhaus (2008) assumes that catastrophic damage can amount up to 30 percent of gross world product, and Hope (2011) calibrates damage from tipping to include the range 5–25 percent, with a central level of 15 percent of gross world product.

Preference Parameters

The data are not definitive on the correct values for the inter-temporal elasticity of substitution , and the risk aversion parameter . Bansal and Yaron (2004) combine consumption data and asset returns to argue that is between 0.5 and 1.5, and is from to 10. Bansal and Ochoa (2011) use and . Vissing-Jørgensen and Attanasio (2003) find between 5 and 10 and . Vissing-Jørgensen (2002) and Campbell and Cochrane (1999) find evidence of . Barro (2009) uses and , and Pindyck and Wang (2013) use and . The DICE model of Nordhaus (2008) is deterministic and its utility function is equivalent to in our Epstein-Zin utility function. The absence of uncertainty in DICE implies that Epstein-Zin preferences do not depend on , and utility is time separable.

Due to the lack of precise knowledge about preferences, we solve DSICE for a broad range of values for , , and for , , and examine how the social cost of carbon depends on risk preferences. In our benchmark parameter specification we follow Bansal and Yaron (2004) and assume and . However, due to the lack of precise knowledge of preferences, we will solve our model for a broad range of values covering for the risk aversion parameter and for the inter-temporal elasticity of substitution. We will examine how the social cost of carbon depends on risk preferences.

5.3 Numerical Solution Method

We solve the nine-dimensional problem specified in (16) using value function iteration. Three state variables, , are discretized and the stochastic shocks are modeled as transitions of finite-state Markov chains. The productivity process states, , use Markov chains that have enough states to ensure that the resulting consumption processes match the conditional variance and autocorrelation observed in consumption data, and is calibrated to represent processes discussed in the climate literature. At each discrete point in space, the value function over the six continuous states, , is approximated by multivariate orthogonal polynomials. The range of each continuous state variable is chosen so that all simulation paths stay in that range. This is a large problem but the use of parallel programming methods and hardware makes this tractable. See Appendices B and E of this paper and Cai et al. (2015) for a more extended discussion of the mathematical and computational details.

5.4 A Verification Test of Code

One theme of the VVUQ literature (e.g., Oberkampf and Roy 2010)) is the value of tests that check the correctness of the computer code. One common test is to apply the code to special cases where we know the solution. If all uncertainty is removed, then our model reduces to a deterministic optimal control problem that can be solved by nonlinear programming methods. We compare these optimal control solutions to our value function iteration results to see if the value functions imply an optimal path equal to the nonlinear programming results. Our tests show that paths implied by the value functions have at least three-digit accuracy, often significantly more. See Appendix F for more details.

5.5 Presentation of Results

Our specifications of a stochastic component in factor productivity growth and a stochastic climate are each novel contributions to the economics of climate change. Therefore, we first study the implications for climate policy of each component in isolation before we investigate their interactive implications. In Sections 6, 7, and 8 respectively we analyze the implications for climate policy of only stochastic growth, only stochastic climate, and stochastic growth and stochastic climate combined.

We compare our stochastic examples with one deterministic benchmark example with CRRA utility using as in Nordhaus (2008). The DICE family of models is based on the continuous-time differential equation system in Schneider and Thompson (1981). Based on the DICE model of Nordhaus (2008), Cai et al. (2012b) analyze alternative time steps and find that one-year step size gives excellent solutions to the continuous-time system. Thus, our deterministic benchmark example is chosen to be the one in Cai et al. (2012b) with annual time steps. DSICE will also use one year time periods in all examples in this paper.

In each of the following three sections we define a benchmark parameter specification and show the distribution of optimal dynamic paths for the social cost of carbon and other variables. We also perform a sensitivity analysis on some parameters and report in tables how today’s optimal level of the social cost of carbon and other variables is affected by different parameter choices.

The simulation of optimal paths is performed as follows: At time we specify the levels of the six continuous states based on today’s observed levels of the capital stock, the three masses of carbon in the atmosphere, the upper ocean, and the lower ocean, and the two temperature levels in the atmosphere and the ocean. We also assume that today’s stochastic productivity state is at its observed mean with zero persistence of its growth rate.131313The values of the nine state variables at the initial time are given in Appendix A. We use 2005 as the first year in order to be comparable with Nordhaus (2008) and similar studies. Our experience indicates that using, e.g., 2010 as the start date will not change the qualitative results. For the climate, we also assume that a tipping point has not yet been triggered. After initializing the state space, we use the value function to compute current optimal decisions (i.e., at ). From the combination of optimal social decisions and the realization of current-period shocks we obtain next-year levels of the state variables (i.e., at ). We continue this simulation process until the terminal time. In our benchmark cases, we simulate 10,000 such paths to examine the distributions of states, decisions, and in particular the social cost of carbon.

6 The Social Cost of Carbon with (only) Stochastic Growth

This section analyzes the impact of stochastic growth and risk preferences on the social cost of carbon and other features of the combined climate and economic system. We do not incorporate the risk of a climate tipping point in any of the model runs in this section. We first describe a benchmark example with parameter specifications that produce consumption processes matching historical data. We will call this our stochastic growth benchmark. This stochastic growth benchmark allows us to exposit key features of the resulting dynamic processes, such as consumption, output, productivity, climate states, and the social cost of carbon. We then perform a sensitivity analysis for empirically plausible alternative preference parameters, focusing on how preference assumptions affect the social cost of carbon at the initial time.

6.1 The Stochastic Growth Benchmark

In this stochastic growth benchmark example we assume Epstein–Zin preferences with and and characterize the stochastic growth process by assuming , , and . As the first step we present Table 1 listing the mean and standard deviation of variables such as per capita output growth , the social cost of carbon (on scale), and per capita consumption growth at years 2020, 2050, and 2100, from our 10,000 simulation paths of the solution to the dynamic programming problem. We also perform a lag-1 linear autoregression analysis after detrending. That is, for a time series (which could represent any variable in Table 1), we assume

| (18) |

where is the mean of from the 10,000 simulation points at time . For each simulation path, by fitting with its first 100 years data, we get an estimate of , and the standard deviation of the lag-1 autoregression residuals, denoted , which is also known as the one-period-ahead conditional standard deviation. In total, we obtain 10,000 estimates of and . Table 1 also reports their mean and standard errors.

Table 1 tells us that both the mean and the standard deviation of are expanding over time. However, the standard deviation of between 2020 and 2100 more than triples, thus increasing much faster than the growth rate of its mean. Moreover, the mean of for is larger than 1, implying that is non-stationary over time. Similarly, the ratio of abatement expenditure to gross output, , is also shown to be non-stationary, with expanding mean and standard deviation over time.

Table 1 also shows that the mean and standard deviation of the other four variables (i.e., per capita output growth , per capita consumption growth , ratio of consumption to gross output , and ratio of capital investment to gross output ) are nearly independent of time. Moreover, for each of these four variables, the means of their are less than 1 with small standard errors such that their 95 percent confidence levels are also below 1. This finding suggests that the four variables are stationary and have a mean-reverting property.

| mean at 2020 | 0.013 | 0.697 | 0.302 | 1.924 | 0.014 | |

| mean at 2050 | 0.013 | 0.705 | 0.293 | 2.153 | 0.013 | |

| mean at 2100 | 0.012 | 0.704 | 0.290 | 2.457 | 0.012 | |

| standard deviation at 2020 | 0.038 | 0.027 | 0.026 | 0.087 | 0.024 | |

| standard deviation at 2050 | 0.039 | 0.028 | 0.027 | 0.184 | 0.024 | |

| standard deviation at 2100 | 0.039 | 0.029 | 0.027 | 0.279 | 0.025 | |

| mean of | 0.184 | 0.854 | 0.847 | 1.008 | 1.003 | 0.458 |

| standard error of | 0.117 | 0.057 | 0.056 | 0.077 | 0.015 | 0.135 |

| mean of | 0.037 | 0.014 | 0.013 | 0.013 | 0.021 | |

| standard error of | 0.003 | 0.001 | 0.001 | 0.001 | 0.002 |

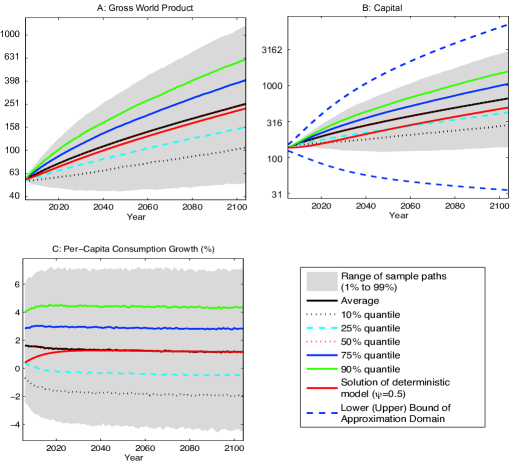

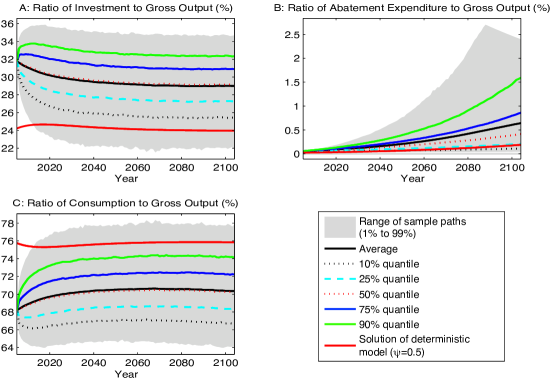

In comparison to a model with purely deterministic growth, our model implies a lower ratio of consumption to gross world output and higher ratios of investment in capital accumulation and abatement. Figure 1 presents the details, displaying the optimal dynamic distribution of the three ratios for the first 100 years with various quantiles of 10,000 simulations of the solution to the dynamic programming problem (16).

For example, the black dotted lines represent the 10 percent quantiles for each ratio. Similarly, the cyan dashed lines, the red dotted lines, the blue solid lines and the green solid lines represent the 25 percent, 50 percent, 75 percent, and 90 percent quantiles at each time respectively. The black solid lines represent the sample mean path. As explained earlier, a special case of DSICE (i.e., all variances are zero and ) makes it comparable with the deterministic model of Nordhaus (2008). We denote this special deterministic case by the red solid lines. The lower (upper) edge of the gray areas represent the 1 percent (99 percent) quantile; the gray areas represent the 98 percent probability range of each ratio.141414We will use the same graphical exposition for all plots describing stochastic processes.

From Figure 1 we see that with more than 90 percent probability will be greater than in the case of a purely deterministic model (the red solid line is below the black dotted line). Furthermore, we find that at the initial time is at 32 percent, about 8 percent higher than under the deterministic growth assumption and the expected difference is about 5 percent toward the end of this century. Overall, the assumption of stochastic factor productivity growth with persistence leads to a significant expected increase in capital investments and thus to a precautionary buildup of the capital stock.151515The simulation paths of gross world output, capital, and per capita consumption growth are shown in Figure 8 in Appendix G. Also, throughout the 10,000 simulations of our model we found to range roughly between 22 and 33 percent, expanding the distributional results reported in Table 1.

Panel C presents quite the opposite statistical picture for . We see that with more than 90 percent probability will be lower than in a purely deterministic model and that toward the end of this century appears to stabilize at about 70 percent; a reduction of about 6 percent over the deterministic model. Overall, this reduction is not fully offset by higher capital investments and, as panel B indicates, that difference is allocated to expenditures on abatement of emissions. We find that the latter, which is denoted by , is generally quite low and does not exceed 0.2 percent in this century in the deterministic case. Yet, as the black solid line in panel B indicates, there is a 50 percent probability that the expenditures on emissions abatement will be at least three times higher by the year 2100 when growth is modeled stochastically. Furthermore, with more than 20 percent probability more than 1 percent of gross world output should be devoted to mitigation by the year 2100.

The optimal allocation of gross world output is a portfolio choice problem where abatement expenditures are a form of investment. Thus, savings are split into investing in the capital stock or reducing the capital stock. In sum, Figure 1 indicates that the inclusion of stochastic growth with persistence will have significant impacts on the optimal allocation of gross world output and that deterministic specifications and, most likely, even certainty equivalent formulations will fail to account for these impacts.

We have investigated the dynamics of the economic variables, now we study the relation between them. Table 2 reports the correlation matrices of the growth rates of five economic variables: gross world output, consumption, capital investment, abatement expenditure, and the social cost of carbon, in 2020 and 2100. We see that all reported correlation numbers are almost the same in 2020 and 2100. Moreover, the growth of abatement expenditure is almost independent of all the other four variables, the growth of both consumption and capital investment are highly correlated with the growth of gross output, and the growth of the social cost of carbon is also highly correlated with the growth of consumption.

| Correlation at 2020 | Correlation at 2100 | |||||||||

| 1 | 0.90 | 0.95 | -0.02 | 0.77 | 1 | 0.90 | 0.94 | -0.00 | 0.78 | |

| 0.90 | 1 | 0.71 | -0.02 | 0.91 | 0.90 | 1 | 0.70 | -0.00 | 0.91 | |

| 0.95 | 0.71 | 1 | -0.02 | 0.58 | 0.94 | 0.70 | 1 | 0.00 | 0.57 | |

| -0.02 | -0.02 | -0.02 | 1 | -0.01 | -0.00 | -0.00 | 0.00 | 1 | 0.00 | |

| 0.77 | 0.91 | 0.58 | -0.01 | 1 | 0.78 | 0.91 | 0.57 | 0.00 | 1 | |

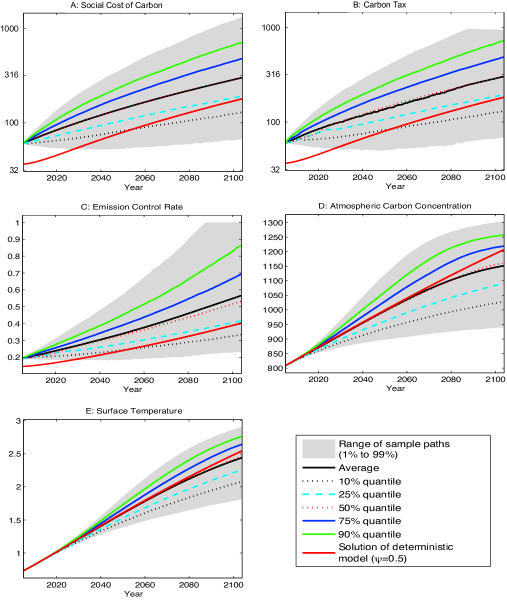

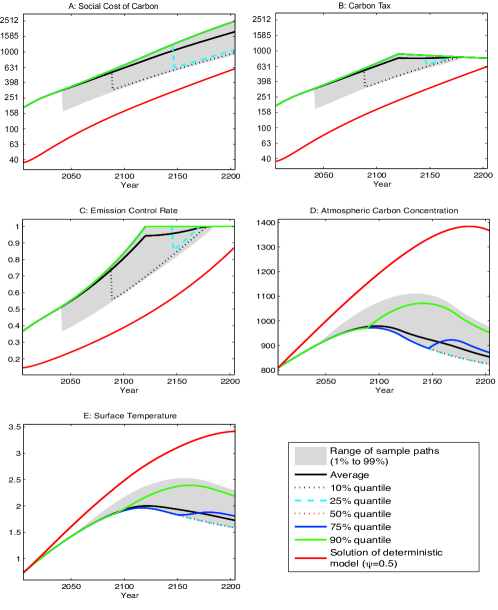

We next study how the stochastic growth specification affects the dynamics of the social cost of carbon, the carbon tax, the emission control rate, and the two most important climate states: atmospheric carbon concentration and surface temperature.

We first consider panel C in Figure 2 which shows the distribution of the rate of emission control. We observe that with 90 percent probability, the stochastic growth representation implies a higher emission control rate until the middle of this century and that by 2100 the probability is reduced to 75 percent. The generally much higher emission control rate is directly linked to the increased share of abatement expenditures to gross world output. The latter occurs because the prospects of much higher growth translate to expectations of increasing gross emissions, which in turn increase the atmospheric carbon stock and ultimately enhance global warming with its exponentially increasing damage to gross world output.

Both panels D and E indicate that on average the stochastic growth representation will lead to a slightly lower accumulation of carbon in the atmosphere and also have a small cooling effect on temperature. However, mostly due to the uncertainty about economic growth over the present century, we see that the range of atmospheric temperature in 2100 is about 1 degree Celsius, suggesting a large uncertainty about the extent of global warming and its impacts on the world economy and the environment. In fact, at the 2009 Copenhagen climate convention most climate scientists agreed that keeping changes in temperature levels below 2 degrees Celsius is necessary to prevent climate change from having dangerous impacts.

As explained earlier, the monetized impacts of climate change are expressed by the social cost of carbon which we depict in panel A (on log10 scale). The optimal initial social cost of carbon is $61 per ton of carbon, about 65 percent higher than in a purely deterministic economy, such as that assumed in Nordhaus (2008), whose study is currently being used for the design of climate policy in the United States, and to which our model compares when we eliminate the uncertainty about growth. Furthermore, the range resulting from the 1 percent and 99 percent quantiles of the simulation increases substantially over time. Here, the social cost of carbon in 2100 varies from $65 per ton of carbon to $1,200 per ton of carbon and even the 10 percent and 90 percent quantiles in 2100 show a range of $125 per ton of carbon to $660 per ton of carbon.

A major observation of our analysis is that by the year 2100 about 3 percent of our model runs produce a carbon tax (panel B) much lower than the social cost of carbon. This coincides with the simulation paths for which the emission control rate hits its upper bound of 100 percent, implying that it is optimal to have zero emissions. We obtain the social cost of carbon from the optimization framework of a social planner, and a (Pigovian) carbon tax policy in this case could be implemented to equate private and social costs of carbon in the absence of other market imperfections, and thus achieve the first best policy. When the emission control rate is at its limit, the carbon tax needs only to be large enough to eliminate all emissions, but as our results show it can be far less than the social cost of carbon. The gap between the carbon tax and the social cost of carbon can be large, with the largest carbon tax in 2100 less than $1,000 per ton of carbon while the largest social cost of carbon is $2,000 per ton of carbon among the 10,000 simulations.

A direct implication of this finding for climate policy is that with more than 3 percent probability, mitigation policies will reach the limit of their effectiveness and since the social cost of carbon will be much larger than the carbon tax can internalize, alternative policies such as carbon removal and storage or solar geoengineering technologies may become competitive.

Our findings point to one very important fact: there is great uncertainty about all aspects of the combined economic and climate system. For many variables, the mean value at each point in time is close to the solution of the purely deterministic model. Tracking the mean is all one can ask of any deterministic model, and in that sense deterministic models can be successful. However, there is great uncertainty about the future value of each key variable. This fact is of particular importance for understanding the social cost of carbon. The social cost of carbon is the marginal cost of extra carbon in terms of wealth, making it the marginal rate of substitution between mitigation expenditures and investment expenditures in physical capital. At the margin, those two uses of savings have different impacts on future economic variables, making allocation decisions between mitigation and investment essentially a portfolio choice problem; a large social cost of carbon represents the amount of investment in new capital that one is willing to sacrifice to reduce carbon emissions by a gigaton.

6.2 Uncertainty Quantification for Preference Parameters

Empirical work suggests plausible values for and , but the data do not give us precise values for the key parameters. A basic method in the uncertainty quantification literature is to recompute the social cost of carbon over a range of parameter choices that reflect the range of economic analyses. We examine different values of and to determine the sensitivity of the social cost of carbon to alternative preference specifications. Each example will differ from the stochastic growth benchmark only in the preference specification, as we will always use the benchmark stochastic growth productivity process. Thus, the following results are comparative dynamics only for changes in and .

Our sensitivity analysis will look only at the social cost of carbon at the initial time. Simulations show that the dynamic stochastic process for the social cost of carbon is qualitatively similar to the stochastic growth benchmark in all cases. The social cost of carbon at the initial time can be thought of as the initial value for the social cost of carbon process, which is volatile for any choice of preference parameters. Table 3 lists the initial optimal social cost of carbon from our model under stochastic growth assuming the values of the elasticity of inter-temporal substitution to be , 0.75, 1.25, 1.5, and 2.0, and the risk aversion parameter to be 2, 6, 10, and 20. Recall that, in our benchmark example with and , the optimal initial social cost of carbon is $61 per ton of carbon. Table 3 indicates that for our benchmark case with the social cost of carbon is almost invariant to alternative specifications of , while keeping , the social costs of carbon at the initial time will be smaller for higher levels of .

| Deterministic | ||||||

|---|---|---|---|---|---|---|

| Growth Case | 0.5 | 2 | 6 | 10 | 20 | |

| 37 | 35 | 39 | 52 | 61 | 69 | |

| 54 | 53 | 55 | 58 | 60 | 62 | |

| 82 | 83 | 77 | 65 | 61 | 56 | |

| 94 | 95 | 85 | 68 | 61 | 55 | |

| 111 | 115 | 97 | 71 | 62 | 54 | |

More generally, Table 3 shows that the social cost of carbon is sensitive to the preference parameters, ranging from $35 (in the case of and ) to $115 (in the case of and ). We see that when the inter-temporal elasticity of substitution () is less than unity, a higher will imply a higher social cost of carbon. However, when the inter-temporal elasticity of substitution is larger than 1, the social cost of carbon is decreasing in . Moreover, when a higher inter-temporal elasticity of substitution implies a higher social cost of carbon, but for the opposite is the case. An increase in the inter-temporal elasticity of substitution reduces the preference for consumption-smoothing but that tells us little about the social cost of carbon. The social cost of carbon is the value of mitigation expenditures relative to the value of capital investment, both of which are chosen. Our results show that the interplay between the inter-temporal elasticity of substitution and the risk aversion parameter in our model with stochastic growth is nontrivial for the social cost of carbon.

From Table 3, we see also that when , a higher volatility of uncertain economic growth implies a lower initial social cost of carbon for cases with , or implies an higher initial social cost of carbon for cases with (as the volatility of the deterministic case is zero). The outcomes of general equilibrium come from a mix of income and price effects, making it difficult to arrive at simple explanations. Our sensitivity analysis enables us to examine quantitatively the impact of alternative parametric assumptions.

Tables 4 and 5 report the sensitivity of the initial ratios of capital investment to gross world output () and abatement expenditure to gross world output () respectively, for the combinations of and the inter-temporal elasticity of substitution.

For example, when and , initial is 0.317 and is . From Table 4 we see that capital investment is increasing in . Table 5 displays the same pattern for abatement expenditure as that displayed for the social cost of carbon in Table 3: When the inter-temporal elasticity of substitution is less than 1, a higher will imply a higher ratio; when the inter-temporal elasticity of substitution is larger than 1, the ratio is decreasing in ; and a higher does not necessarily imply a higher or lower ratio of abatement expenditure to gross world output.

| Deterministic | ||||||

|---|---|---|---|---|---|---|

| Growth Case | 0.5 | 2 | 6 | 10 | 20 | |

| 0.242 | 0.240 | 0.249 | 0.272 | 0.291 | 0.321 | |

| 0.259 | 0.257 | 0.265 | 0.285 | 0.299 | 0.318 | |

| 0.278 | 0.276 | 0.286 | 0.303 | 0.312 | 0.322 | |

| 0.284 | 0.283 | 0.293 | 0.310 | 0.317 | 0.324 | |

| 0.293 | 0.293 | 0.305 | 0.322 | 0.328 | 0.331 | |

| Deterministic | ||||||

|---|---|---|---|---|---|---|

| Growth | 0.5 | 2 | 6 | 10 | 20 | |

We also study the effects of alternative preference specifications on the dynamics (level and distribution) of the social cost of carbon and per capita consumption growth. Table 6 lists these effects for only the extreme parameter cases of our simulations, which are or 2, and or 20. First, we verify the statistical results of per capita consumption over the large range of preference parameters. Its mean growth rate is quite stable over this century, ranging from 1.1 percent to 1.4 percent per year, close to that of the benchmark case shown in Table 1. We also report the other statistics used in Table 1 such as the statistics of and for the lag-1 autoregression (18). These numbers show that a smaller will produce a larger volatility for the per capita consumption growth . Furthermore, the volatility of is quite invariant to different values of the risk aversion parameter. In addition, all the cases show the mean-reverting property of the consumption growth: the 95% confidence level of is always below one (for lower levels, has a smaller , implying a faster reverting rate), and its mean and standard deviation are almost independent of time for each reported combination.

Regarding the sensitivity of the social costs of carbon, we recall from Figure 2 of our benchmark parameter case that the social cost of carbon is highly volatile. Here, we show that this high volatility is also persistent when we assume alternative preference specifications. More precisely, the mean and—in particular—the standard deviation of are increasing over time. Furthermore, the mean of is not less than 1, implying non-stationarity of .

| mean at 2020 | 1.632 | 2.045 | 2.171 | 1.858 | 0.011 | 0.014 | 0.013 | 0.014 |

|---|---|---|---|---|---|---|---|---|

| mean at 2050 | 1.878 | 2.369 | 2.372 | 2.069 | 0.013 | 0.013 | 0.013 | 0.013 |

| mean at 2100 | 2.211 | 2.763 | 2.656 | 2.347 | 0.012 | 0.012 | 0.012 | 0.012 |

| standard deviation at 2020 | 0.068 | 0.113 | 0.097 | 0.074 | 0.036 | 0.035 | 0.023 | 0.021 |

| standard deviation at 2050 | 0.181 | 0.251 | 0.189 | 0.161 | 0.037 | 0.037 | 0.023 | 0.022 |

| standard deviation at 2100 | 0.283 | 0.370 | 0.282 | 0.249 | 0.039 | 0.039 | 0.025 | 0.023 |

| mean of | 1.008 | 1.005 | 1.000 | 1.005 | 0.100 | 0.091 | 0.584 | 0.708 |

| standard error of | 0.012 | 0.014 | 0.017 | 0.014 | 0.116 | 0.118 | 0.148 | 0.101 |

| mean of | 0.009 | 0.016 | 0.017 | 0.011 | 0.036 | 0.036 | 0.018 | 0.015 |

| standard error of | 0.001 | 0.001 | 0.001 | 0.001 | 0.003 | 0.003 | 0.003 | 0.002 |

6.3 Impact of Growth Parameters

The deterministic productivity trend has a growth rate ) at time from Equation (2). It has two important parameters: the initial growth rate, , and the decline rate of the growth of the productivity trend, , with their default values 0.0092 and 0.001 respectively. We next carry out a sensitivity analysis on them by letting (the growth of the productivity trend is 0, i.e., ) or (the growth of the productivity trend is constant, i.e., with ).