zhengwen,ebax,jamesyili@yahoo-inc.com

Authors’ Instructions

Revenue-Maximizing Mechanism Design for Quasi-Proportional Auctions

Abstract

In quasi-proportional auctions, each bidder receives a fraction of the allocation equal to the weight of their bid divided by the sum of weights of all bids, where each bid’s weight is determined by a weight function. We study the relationship between the weight function, bidders’ private values, number of bidders, and the seller’s revenue in equilibrium. It has been shown that if one bidder has a much higher private value than the others, then a nearly flat weight function maximizes revenue. Essentially, threatening the bidder who has the highest valuation with having to share the allocation maximizes the revenue. We show that as bidder private values approach parity, steeper weight functions maximize revenue by making the quasi-proportional auction more like a winner-take-all auction. We also show that steeper weight functions maximize revenue as the number of bidders increases. For flatter weight functions, there is known to be a unique pure-strategy Nash equilibrium. We show that a pure-strategy Nash equilibrium also exists for steeper weight functions, and we give lower bounds for bids at an equilibrium. For a special case that includes the two-bidder auction, we show that the pure-strategy Nash equilibrium is unique, and we show how to compute the revenue at equilibrium. We also show that selecting a weight function based on private value ratios and number of bidders is necessary for a quasi-proportional auction to produce more revenue than a second-price auction.

1 Introduction

Quasi-proportional auctions [2, 9] award each bidder a fraction of the total allocation equal to the weight of their bid divided by the sum of weights of all bids, where a bid’s weight is determined by a weight function. Hence, the allocation for bidder is

| (1) |

where is the vector of bids and is the weight function. In this paper, we focus on winners-pay quasi-proportional auctions, in which bidders pay their bid times their allocation. (A well-known alternative is the all-pay auction, in which all bidders pay their full bid regardless of allocation [2]. The all-pay auction has been used as a model for disparate interests plying officials with gifts and favors in hopes of influencing policy.)

Why use quasi-proportional auctions? It is well known that the revenue-optimal auction (for a single item, non-repeated) is the second-price auction with optimal reserve prices [14, 16]. The optimal reserve prices are based on knowledge of prior distributions from which bidders draw their private values. Without this knowledge, we are in a prior-free setting [6, 7], in which it can be a challenge to set effective reserve prices [13]. If the auction is repeated and priors are stable over time, then the priors may be learnable [10, 3, 4, 8]. However, in some practical scenarios with unknown priors, either the auction is not repeated, or the priors change from auction to auction.

In the prior-free setting without reserve prices, Mirrokni et al. [12] show that a quasi-proportional auction has better worst-case performance than a second-price auction. In their worst case, the bidder with the highest private value has a much higher private value than the other bidders. In this case, they show that quasi-proportional auctions with functions and , called Tullock auctions [2], can achieve () revenue, where is the ratio of the highest private value to the next-highest private value. These results are called prior-free revenue results. Nguyen and Vojnovic [15] show that for the prior-free setting without reserve prices, there is an upper bound of o() on equilibrium revenue, where and are the two highest private values of bidders. They also give a mechanism that achieves revenue (), which is similar to the best known prior-free result with reserve prices [11].

Other than a lack of priors, some reasons why a quasi-proportional allocation might be useful include:

-

1.

The item is always awarded. For auctions with reserve prices, the item may be withheld from all bidders. This may create a problem for the seller. Quasi-proportional auctions avoid this problem.

-

2.

There is a shared allocation. The seller may desire a shared allocation if a zero allocation to runner-up bidders makes them unlikely to participate in future auctions, which can decrease competition and revenue in those auctions. A shared allocation awards a “second prize for the second price.” (A single allocation is also possible: the auctioneer can award the item at random, with each bidder’s probability of winning the item equal to its fraction of the allocation [13].)

For the winners-pay quasi-proportional auction, assume bidder has utility function

| (2) |

where is bidder ’s private value for a full allocation. Without loss of generality, in this paper we assume the weight function has the form , where the exponent is to be specified. The main contributions of this paper are:

-

1.

For all , we show that the quasi-proportional auction with weight function has a pure-strategy Nash equilibrium.

-

2.

We give lower bounds for bids at a pure-strategy Nash equilibrium. The bounds are based on and the level of competition, in terms of number of bidders and their private values. As competition increases, higher values of maximize the bounds.

-

3.

For the case of a bidder with a higher private value and one or more bidders that share a lower private value, we show that the pure-strategy Nash equilibrium is unique.

-

4.

For that case, we show how to compute equilibrium revenue, and we explore how it depends on , the ratio of higher to lower private values, and the number of bidders. We show that steeper weight functions are needed to maximize revenue as competition increases.

2 Bid Lower Bounds at an Equilibrium

In this section, we consider quasi-proportional auctions with weight functions for . For these auctions, we prove the existence of a pure-strategy Nash equilibrium, and we give lower bounds for bids at an equilibrium. Mirrokni et al. [12] show there is a unique pure-strategy Nash equilibrium for ; we show that an equilibrium also exists for . When , a bidder’s response function is not necessarily concave over the whole domain of their bids that give nonnegative utility: , where is the bidder’s private value. Thus, we cannot apply results such as those by Rosen [17], as Mirrokni et al. do, to show the existence and uniqueness of a pure-strategy Nash equilibrium. Instead, we use Brouwer’s fixed-point theorem to prove existence of an equilibrium.

First we show that each bidder’s best response is unique for all . Next we derive vectors of lower bounds, , such that if all bidders bid , where is the th component of , then the same holds for the vector of bidders’ best responses to each others’ bids. We combine that result with Brouwer’s fixed-point theorem to prove the existence of a pure-strategy Nash equilibrium. Since the bids at equilibrium are at least as great as the lower bounds , the lower bounds on bids also imply lower bounds for the auctioneer’s equilibrium revenue.

In this section, we use to represent a single bidder’s bid and to represent the vector of bidder’s bids; we drop the notation that indicates functions of , for example writing instead of for a bidder’s response function, and we use apostrophes to denote derivatives with respect to , such as for the second derivative of the weight function.

2.1 Uniqueness of the Best Response

To show that each bidder’s best response is unique, we will show that each bidder’s response curve (their utility curve given other bidders’ bids) is concave at all points that have derivative zero. Since the response curves are continuous, this implies there are no local minima. If there were multiple local maxima, there would have to be a local minimum between each successive pair of local maxima. So there can only be a single global maximum. (There is a maximum since the response curve is zero and ascending at zero bid, zero and descending at bid equal to the bidder’s private value, and the response curve and its first derivative are continuous. So we can apply Bolzano’s theorem to the derivative.)

We will use to represent a single bidder’s bid. Holding the other bidders’ bids fixed, the allocation is

| (3) |

where is the sum of weight functions of the other bidders’ bids. The bidder’s utility function is

| (4) |

where is the bidder’s private value. We have the following theorem:

Theorem 2.1

If such that , and , then .

Please refer to the appendix for the proof.

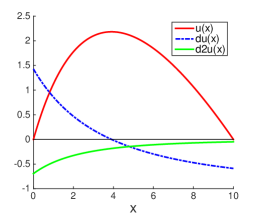

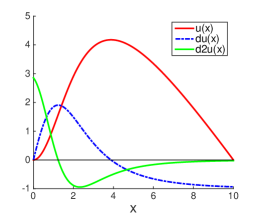

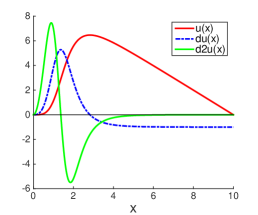

Figure 1 shows the utility function and its first two derivatives for , , and . In each case, we set , the sum of weight functions for other bids, to 7, and the bidder’s private value to 10. In Figure 1(a), with , the utility function is concave (negative second derivative) over the whole bid domain [0,10]. In Figures 1(b) and 1(c), the utility functions are not concave at , but the second derivatives are negative at the values where the first derivatives are zero. In Figure 1(a), the utility function is a smoothly rounded curve. In Figure 1(b), the utility function is still somewhat rounded, but there is a slight S-curve starting at zero, and the curve is less rounded and more linear to the right of the maximum. In Figure 1(c) these effects are more pronounced. The S-curve that makes the utility functions in Figures 1(b) and 1(c) non-concave on the left results from slow gains in allocation near bid zero, followed by quick gains due to the growth of for large , then by leveling off in the allocation as comes to dominate the denominator in .

2.2 Pure-Strategy Nash Equilibria and Bid Lower Bounds

Let be a vector of bids, with the bid for bidder . Let be bidder ’s best response to the other bidders’ bids. Define response function . Let be the valuation for bidder , and let be the weight function. We have the following theorem:

Theorem 2.2

Suppose for , and a vector meets the conditions

| (5) |

where . Then, for all such that , .

In other words, if meets the conditions of the theorem, then maps into itself. Please refer to the appendix for the proof.

Before we use this theorem to prove existence of an equilibrium and derive lower bounds for bids at an equilibrium, look at Inequality 5. The value of mediates a tradeoff. From the term , the bound gets stronger (closer to ) as increases. However, for the bidder with the greatest private value, increasing can increase the weight function of that bidder’s bid, , so much that it dominates the sum of weight functions of other bidders’ bids, , and this effect becomes more pronounced as the ratio between the highest private value and other private values increases. So we can get stronger bounds by using higher if there is enough competition to keep low.

Using Theorem 2.2, it is straightforward to prove that there exist pure-strategy Nash equilibria for quasi-proportional auction mechanisms with convex weight functions.

Theorem 2.3

For any bounds that meet the conditions of Theorem 2.2, there exists a pure-strategy Nash equilibrium in .

Proof

We now present some lower bound ’s satisfying Inequality 5. The following corollary gives lower bounds that are the same for all bidders.

Corollary 1

Let . Then Theorem 2.2 applies to lower bounds

| (7) |

Proof

Note that when , and , then Corollary 1 gives a lower bound , which is when and approaches to as . Moreover, for any , this lower bound approaches as .

Corollary 2 offers bounds based on the second-highest valuation. These bounds are stronger than those from Corollary 1 when the second-highest valuation is significantly higher than the minimum valuation.

Corollary 2

Assume, without loss of generality, . Let . For , let

| (8) |

For these values, the response function maps into itself.

Proof

We will show that these bounds meet the condition from Theorem 2.2. For each , we need to show

For :

For :

For :

In general, there are many satisfying Inequality 5, and each of them corresponds to a different lower bound. These bounds provide some insight on how the auctioneer’s revenue at the best pure-strategy equilibrium varies with and .

3 Symmetric Competition Against a High-Value Bidder

In this section, we consider a special case, where there is one bidder with a higher private value, and the other bidders have lower private values that are equal to each other. Without loss of generality, we assume that bidder has valuation , and bidders have valuations . We call this case OLOS (one larger, others symmetric). The case of two bidders is a special case of OLOS. We use OLOS to gain insight about how , the ratio between the highest valuation and lower valuations, and the number of bidders affect revenue when a single bidder with a high private value competes against a set of bidders with lower private values.

Having a single large bidder is particularly interesting since it yields a low equilibrium revenue in a second-price auction. Specifically, for OLOS, the equilibrium revenue of the second-price auction is , for any and . This is very unsatisfactory when or is large. Intuitively, we expect that higher should lead to higher equilibrium revenue, and more bidders (larger ) should spur more fierce competition, which should also increase the equilibrium revenue. In this section, we show by analysis and computational studies that we can adaptively design quasi-proportional auctions (i.e. adaptively choose exponent for each ) to achieve equilibrium revenues significantly larger than , and strictly increasing in both and .

As we will show in this section, the assumption of symmetric small bidders can significantly simplify the analysis. Specifically, this assumption allows us to (1) prove the uniqueness of the pure-strategy Nash equilibrium and (2) compute the auctioneer’s equilibrium revenue efficiently. We believe that, in practice, this assumption is not as restrictive as it seems: many practical cases in which there is one large bidder and many similar small bidders are well approximated by OLOS.

This section proceeds as follows: first, we show that for any choice of , , and , there is a unique pure-strategy Nash equilibrium for OLOS. Second, we discuss how to efficiently compute the auctioneer’s revenue at this unique pure-strategy Nash equilibrium, and provide upper and lower bounds on it. Finally, we discuss how to design the optimal quasi-proportional auction for each , and how and vary with and , where is the highest equilibrium revenue achieved by the quasi-proportional auctions for , and is the exponent achieving this highest equilibrium revenue.

3.1 Uniqueness of the Pure-Strategy Nash Equilibrium

We first prove that there is a unique pure-strategy Nash equilibrium for OLOS. The following lemma shows that in such cases, a pure-strategy Nash equilibrium must have symmetric bids among all the small bidders.

Lemma 1

Assume that is a pure-strategy Nash equilibrium, then we have

(Please refer to the appendix for the proof.) Thus, to characterize , we only need to specify and . To simplify the exposition, in the remainder of this section, we sometimes use and to respectively denote and , and define . Note that from the first-order condition for the best response, we have

| (9) |

Notice that the above equations imply that and . Dividing the first equation by the second equation111It is straightforward to prove that at a Nash equilibrium, and , so the division is well-defined., we have

| (10) |

Solving the above equation, we have

| (11) |

Substituting the above equation into the first equation of Equation 9, we have

which implies that

Combining the above equation with Equation 11, we have

which is

| (12) | |||||

where is a shorthand notation for the lefthand side of the above equation. The following lemma states that Equation 12 has no root in .

Lemma 2

for all , and for all .

Please refer to the appendix for the proof of Lemma 2. The following lemma states that Equation 12 has a unique solution in , whose proof is also available in the appendix.

Lemma 3

The equation has a unique solution . Moreover, .

Putting together all the results in this section, we have the following theorem:

Theorem 3.1

For OLOS, there is a unique pure-strategy Nash equilibrium . Moreover:

-

1.

This equilibrium is symmetric among all the small bidders in the sense that .

-

2.

At this equilibrium, and .

Proof

The symmetry among the small bidders follows from Lemma 1. From Lemma 3, equation has a unique solution in . Hence, is uniquely determined and . From Equation 11, once is uniquely determined, and are also uniquely determined. Thus, there exists a unique pure-strategy Nash equilibrium . Finally, follows from Equation 9, and follows from Corollary 1.

3.2 Auctioneer’s Equilibrium Revenue

We now characterize the auctioneer’s equilibrium revenue. Notice that

From Equation 11, we have

| (13) |

where is the unique solution of Equation 12. Thus, we can efficiently compute the auctioneer’s equilibrium revenue as follows:

-

1.

Compute by (numerically) solving Equation 12.

-

2.

Compute the auctioneer’s equilibrium revenue by Equation 13.

Since OLOS and the quasi-proportional mechanism are fully characterized by the triple , sometimes we write as to emphasize this dependence. It is straightforward to derive the following bounds on :

Corollary 3

For any , we have and

Proof

Define

it is straightforward to show that is strictly increasing in over interval . This corollary follows from the facts that (1) , and (2) .

3.3 Revenue-Maximizing Mechanism Design

Now we discuss how to design a quasi-proportional auction mechanism (i.e. how to choose the exponent ) to maximize the auctioneer’s equilibrium revenue for OLOS. Notice that for a given , this mechanism design problem is a one-dimensional optimization problem. Moreover, as we have discussed above, for a given triple , the auctioneer’s equilibrium revenue can be efficiently computed. Consequently, this mechanism design problem can be efficiently solved by line search. We present some computational analysis of , followed by some theorems about how , , and influence equilibrium revenue.

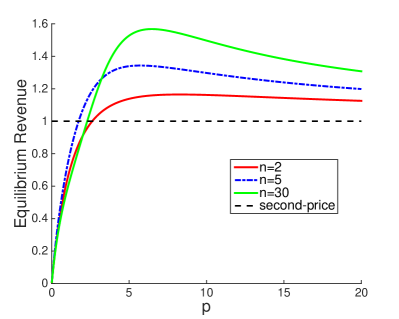

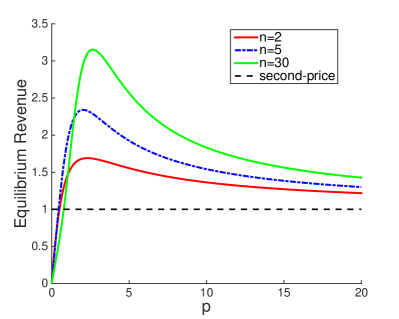

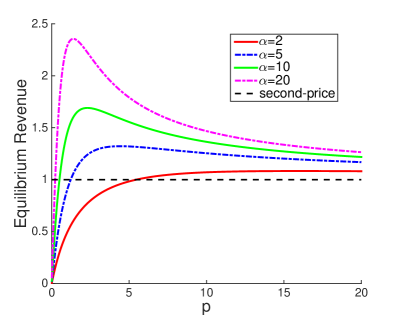

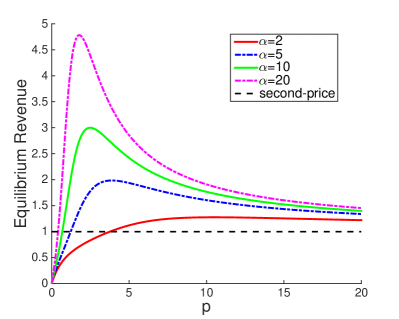

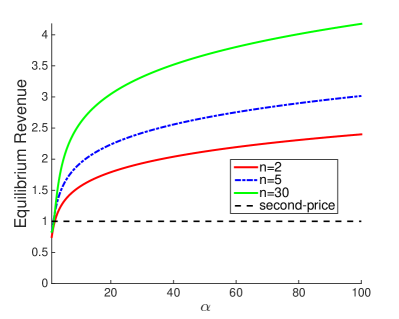

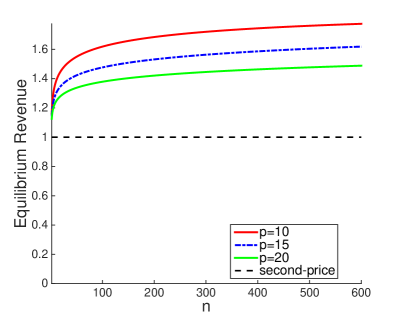

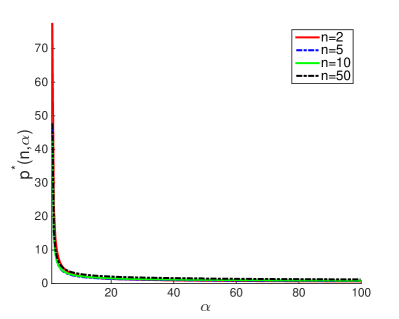

In Figure 2, we plot versus for some given ’s. Notice that the value of that maximizes revenue increases as decreases and as increases. In other words, as competition increases, steeper weight functions are needed to maximize revenue. Also notice that for all the considered ’s, there exists such that , the equilibrium revenue of the second-price auction. Moreover, for all the considered ’s, the equilibrium revenue first increases with , and then decreases with . So there is a unique revenue-maximizing (quasi-proportional mechanism).

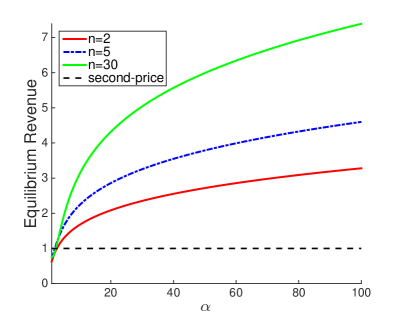

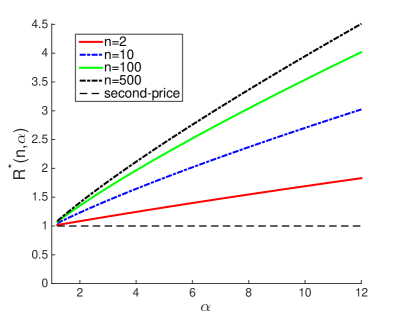

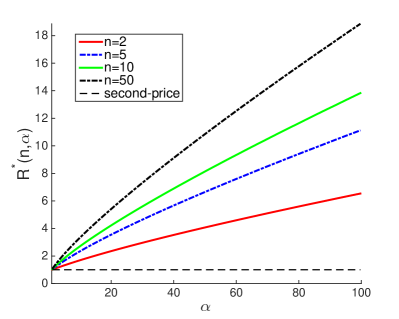

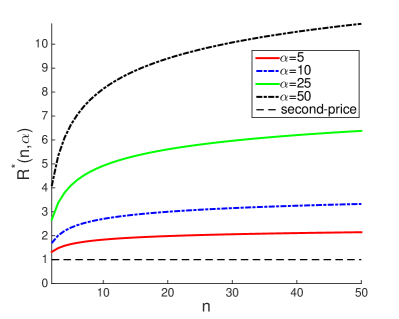

In Figure 3, we plot versus for some given ’s. We observe that is an increasing function of for all the considered ’s, which is reasonable since a higher private value for the large bidder will lead to a higher equilibrium revenue, for a fixed number of small bidders and value .

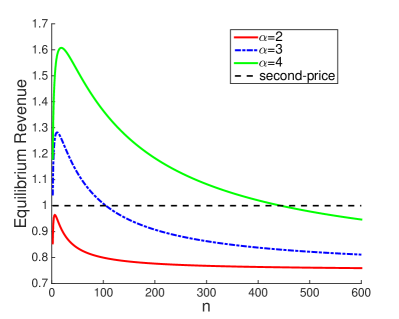

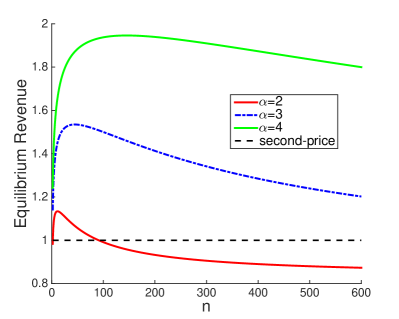

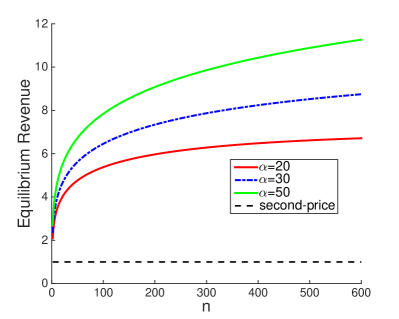

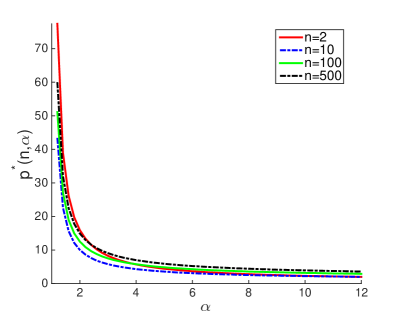

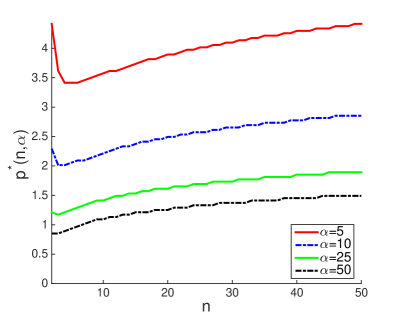

In Figure 4, we plot versus for some values. Notice that Figures 4(a) and 4(b) show that for a fixed , the equilibrium revenue first increases with and then decreases with . As more small bidders are added, their equilibrium bids increase due to increased competition. For fixed and , this can have two conflicting effects: initially, the increased bids increase the equilibrium revenue, but as more small bidders are added, the small bidders win more of the allocation, reducing the portion bought by the single high-value bidder at a higher bid. This decreases revenue. This revenue reduction can be alleviated by adapting to , that is, choosing the revenue-maximizing based on . We will discuss this later in this section. We also notice that the initial interval where increases as a function of depends on . Figures 4(c) and 4(d) show that if or is large, is monotonically increasing for .

We are interested in the highest equilibrium revenue achieved by the quasi-proportional mechanisms, and which quasi-proportional mechanism achieves the highest revenue. Thus, we define

| (14) |

Figure 5 shows how and vary with and . Specifically, Figures 5(a) and 5(c) show that for a given , is a strictly increasing function of . That is, the auctioneer’s highest equilibrium revenue increases with the large bidder’s private value. Moreover, it is interesting to observe that is almost an affine function of , and different ’s corresponds to different slopes. Figures 5(b) and 5(d) show that for a given , is a strictly decreasing function of . Moreover, the decrease rate (the negative of the first derivative) decreases as increases. Note that when is small, which implies that the revenue-maximizing weight function is convex. We also observe that is primarily determined by : for a fixed and very different ’s (e.g. and ), the variation of is small.

Figure 5(e) shows that for a given , is a strictly increasing function of . That is, more small bidders will increase the auctioneer’s equilibrium revenue. We also observe that as increases, decreases. That is, each additional small bidder makes a smaller marginal contribution to the auctioneer’s highest equilibrium revenue. Figure 5(f) shows that for a given , first decreases with and then increases with . Similar to Figures 5(b) and 5(d), Figure 5(f) demonstrates that for a given , the variation of with is relatively small, which implies the robustness of (mechanism design) to the mis-specification of parameter .

Recall that for OLOS, the equilibrium revenue from a second-price auction is always . The following theorem states that for any , the equilibrium revenue will diminish as , while the equilibrium revenue will be at least as much as that of the second-price auction as .

Theorem 3.2

For any and , we have

Proof

The following theorem shows that there does not exist a (i.e. a quasi-proportional mechanism with ) such that for all , (i.e. has an equilibrium revenue higher than the second-price auction). In other words, to achieve an equilibrium revenue higher than the second-price auction, we have to choose different quasi-proportional auction mechanisms for different ’s.

Theorem 3.3

For any

and for any

Proof

4 Discussion

This paper focuses on revenue-maximizing mechanism design for quasi-proportional auctions. Specifically, for the general bidder case, we have proved the existence of the pure-strategy Nash equilibrium and given lower bounds for bids at an equilibrium. For the OLOS case, we have also (1) proved the uniqueness of the pure-strategy Nash equilibrium, and (2) developed an approach to efficiently compute the equilibrium revenue. We have also presented how to numerically solve the revenue-maximizing mechanism design problem in the OLOS case. We used computation to show that steeper weight functions maximize revenue when there is more competition, and we used analysis to show the importance of selecting based on and, to a lesser extent, on .

In practice, the auctioneer does not know the precise value of (and perhaps ). However, the auctioneer may know that (with high probability), lies in a some subset of . Since is robust to small changes in both and (see Figure 5), if is “small”, then we can choose based on any . If is “large”, then we can choose an exponent by robust optimization:

| (15) |

Since there are only three decision variables, this (non-convex) optimization problem can be solved numerically.

One challenge for further research is to prove that there is a unique pure-strategy Nash equilibrium for . Another challenge is to produce a closed-form solution for equilibrium bids, based on bidders’ private values. Analyzing equilibria for other weight functions, such as exponentials, would be an interesting way to extend this work. (Use to avoid awarding an allocation for a bid of zero.)

It would also be interesting to explore strategies for the auctioneer’s selections of over repeated auctions. In a model where bidders need some allocation in order to learn their private values, the auctioneer may benefit from starting with a lower value to have more of an even allocation as bidders learn, then increasing from auction to auction. As the bidders learn their private values, the auctioneer may gain information about the bidders’ private values from their evolving bids. It would also be interesting to explore optimal settings for in a model where auctioneers compete against each other for bidders.

References

- [1] Brouwer, L.: ber abbildung von mannigfaltigkeiten. Math. Ann. 71, 97–115 (1912)

- [2] Buchanan, J., Tollison, R., Tullock, G. (eds.): Toward a theory of the rent-seeking society. No. 4 in Texas A & M University economics series, Texas A & M Univ. Press, College Station, Tex., 1. ed edn. (1980), http://gso.gbv.de/DB=2.1/CMD?ACT=SRCHA&SRT=YOP&IKT=1016&TRM=ppn+02063613X&sourceid=fbw_bibsonomy

- [3] Cole, R., Roughgarden, T.: The sample complexity of revenue maximization. In: Proceedings of the 46th Annual ACM Symposium on Theory of Computing. pp. 243–252. STOC ’14, ACM, New York, NY, USA (2014), http://doi.acm.org/10.1145/2591796.2591867

- [4] Dughmi, S., Han, L., Nisan, N.: Sampling and representation complexity of revenue maximization. CoRR abs/1402.4535 (2014), http://arxiv.org/abs/1402.4535

- [5] Franklin, J.N.: Methods of mathematical economics : linear and nonlinear programming, fixed-point theorems. Classics in applied mathematics, SIAM, Philadelphia (2002), http://opac.inria.fr/record=b1105716

- [6] Goldberg, A.V., Hartline, J.D., Karlin, A.R., Wright, A., , Saks, M.: Competitive auctions. Games and Economic Behavior pp. 72–81 (2002)

- [7] Hartline, J., Karlin, A.: Profit maximization in mechanism design. In: Nisan, N., Roughgarden, T., Tardos, E., Vazirani, V.V. (eds.) Algorithmic Game Theory, pp. 331–362. Cambridge University Press (2007)

- [8] Hummel, P., McAfee, P.: Machine learning in an auction environment. In: Proceedings of the 23rd International Conference on the World Wide Web (WWW). pp. 7–18 (2014), http://dl.acm.org/citation.cfm?id=2567974

- [9] Kelly, F.: Charging and rate control for elastic traffic. European Transactions on Telecommunications (1997)

- [10] Li, S.M., Mahdian, M., McAfee, R.: Value of learning in sponsored search auctions. In: Saberi, A. (ed.) Internet and Network Economics, Lecture Notes in Computer Science, vol. 6484, pp. 294–305. Springer Berlin Heidelberg (2010), http://dx.doi.org/10.1007/978-3-642-17572-5_24

- [11] Lu, P., Teng, S.H., Yu, C.: Truthful auctions with optimal profit. In: Spirakis, P.G., Mavronicolas, M., Kontogiannis, S.C. (eds.) WINE. Lecture Notes in Computer Science, vol. 4286, pp. 27–36. Springer (2006), http://dblp.uni-trier.de/db/conf/wine/wine2006.html#LuTY06

- [12] Mirrokni, V.S., Muthukrishnan, S., Nadav, U.: Quasi-proportional mechanisms: Prior-free revenue maximization. In: LATIN 2010: Proceedings of 9th Latin American Theoretical Informatics Symposium (2010), http://arxiv.org/abs/0909.5365

- [13] Muthukrishnan, S.: Ad exchanges: Research issues. In: Internet and Network Economics: 5th International Workshop, WINE 2009 (2009)

- [14] Myerson, R.B.: Optimal auction design. Mathematics of Operations Research 6(1), 58–73 (1981)

- [15] Nguyen, T., Vojnovic, M.: Prior-free auctions without reserve prices. Tech. Rep. MSR-TR-2010-91, Cornell University (July 2010), http://research.microsoft.com/apps/pubs/default.aspx?id=135075

- [16] Riley, J.G., Samuelson, W.F.: Optimal auctions. American Economic Review 71(3), 381–392 (1981)

- [17] Rosen, J.: Existence and uniqueness of equilibrium points for concave n-person games. Econometrica pp. 520–534 (1965)

Appendices

Appendix 0.A Proofs

0.A.1 Proof for Theorem 2.1

We will first prove a lemma about allocations and their derivatives, apply it to prove a lemma about weight functions, then apply that lemma to our weight functions.

Lemma 4

If , then .

Proof (of Lemma 4)

Since

| (16) |

implies (otherwise also holds and ) and

| (17) |

Since

| (18) |

combining with Equation 17, we have

| (19) |

Since and , we have .

Lemma 5

If , then .

Proof (of Lemma 5)

0.A.2 Proof for Theorem 2.2

Proof

Consider any bidder . To simplify the exposition, we drop the subscripts while we focus on that single bidder. Let be their utility function and be their lower bound . Let be the sum of the weight function over other bidders’ bids:

| (31) |

and assume bids are at least their lower bounds: . Recall from Theorem 2.1 that the utility function has a single local maximum, so at implies that the best response is at least . At ,

| (32) |

So

| (33) |

implies at . Substitute

| (34) |

| (35) |

Cancel and do some algebra:

| (36) |

Substitute and :

| (37) |

Solve for w:

| (38) |

0.A.3 Proof for Lemma 1

Proof

Similarly as the previous section, we define . From the first-order condition at a pure-strategy Nash equilibrium, we have222Notice that the results in the previous section indicate the denominator is bounded away from .

| (39) |

Notice that is a constant for all . Thus, for and any , we have . Let , we have and , hence we have

Notice that , thus, to prove , it is sufficient to prove that function is strictly monotone in interval , for any and , notice that

Hence and we have proved the lemma.

0.A.4 Proof for Lemma 2

Proof

Notice that when . we have

and

Thus, . Since and , we have and . Thus, .

Similarly, when , we have

and

Thus, . Since and , we have and . Thus, .

0.A.5 Proof for Lemma 3

Proof

Notice that from Lemma 2, the equation has no solution in interval and interval . Moreover, since function is continuous, , and , equation has at least one solution in the interval .

Note that to prove the uniqueness of the solution in the interval , it is sufficient to prove that when . That is, to prove that is strictly increasing when it is nonnegative. To simplify the exposition, we write as

where , , , and (see Equation 12). Notice that , and (note when ). Hence we have

The first observation is that in interval , we always have

Thus, implies that

which leads to

where the second inequality follows from . Thus we have

Thus, in interval , when .