Optimal Multiple Stopping with Negative Discount Rate and Random Refraction Times under Lévy Models

Abstract

This paper studies a class of optimal multiple stopping problems driven by Lévy processes. Our model allows for a negative effective discount rate, which arises in a number of financial applications, including stock loans and real options, where the strike price can potentially grow at a higher rate than the original discount factor. Moreover, successive exercise opportunities are separated by i.i.d. random refraction times. Under a wide class of two-sided Lévy models with a general random refraction time, we rigorously show that the optimal strategy to exercise successive call options is uniquely characterized by a sequence of up-crossing times. The corresponding optimal thresholds are determined explicitly in the single stopping case and recursively in the multiple stopping case.

Key words: optimal multiple stopping; negative discount rate; random refraction times; Lévy processes; stock loan

JEL Classification: G32, D81, C61

Mathematics Subject Classification (2010): 60G40, 60J75

1 Introduction

We study a class of optimal multiple stopping problems driven by an underlying Lévy process. Two key features of our model are that (i) the discount rate can be negative or positive, and (ii) the sequence of admissible stopping times are separated by i.i.d. random refraction periods. The negative effective discount rate is relevant to a number of financial applications. For example, Xia and Zhou xiazhou propose a valuation model for a stock loan, where the loan interest rate is higher than the risk-free interest rate. As a result, the stock loan can be viewed as an American call option with a negative effective discount rate. An example from the real option literature DixitPindyck ; McDonald1985 is when the cost of investment grows at a higher rate than the firm’s discount rate. Moreover, while the nominal short rate cannot be negative, the real interest rate can potentially be negative, especially during low-yield regimes, according to Black black95 and references therein. Therefore, extending the discount rate to the negative domain also enables the evaluation of cash flows under the real interest rate.

In the aforementioned applications, the same option can be exercised repeatedly in the future, meaning that an investor can acquire a series of stock loans, or a firm can make an investment sequentially over time. This motivates us to incorporate multiple stopping opportunities in our analysis. The features of refraction periods and multiple exercises also arise in the pricing of swing options commonly used for energy delivery. For instance, Carmona and Touzi Carmona2008 formulate the valuation of a swing put option as optimal multiple stopping problem, with constant refraction periods, under the geometric Brownian motion model. In a related study, Zeghal and Mnif ZeghalSwing value a perpetual American swing put when the underlying Lévy price process has no negative jumps. They provide mathematical characterization and numerical solutions to the associated optimal multiple stopping problem. In contrast, we consider the successive exercises of a swing call option with random refraction times under positive or negative discount rate. We also provide a rigorous analysis of the optimal multiple stopping problem under two-sided Lévy models.

Under a wide class of two-sided Lévy models with a general random refraction time, we show that the optimal exercises of multiple perpetual call options are characterized by a non-increasing sequence of exercise thresholds (see Proposition 2.2 and Theorem 3.2 below). The corresponding optimal thresholds are determined explicitly in the single stopping case and recursively in the multiple stopping case. Our results extend the stock loans models by Xia and Zhou xiazhou as well as Cai and Sun Cai2014 from their single stock loan to sequential stock loans, and from a geometric Brownian motion xiazhou and double-exponential jump diffusion Cai2014 models to a class of general two-sided Lévy processes in our paper. As such, the minimal assumptions on the refraction times and the underlying Lévy process prevent the use of model/distribution-specific properties that are amenable for analysis and computation. We overcome this challenge through the use of Laplace transform, change of measure, martingale theory, along with other analytical techniques. Our analysis allows for the recursive computation of the optimal value function as well as all exercise thresholds, thus providing an alternative to the simulation approach commonly found in existing literature for multi-exercise options (see (Bender, ; Hambly_MF04, ), among others). We also examine the impact of refraction time distribution on the optimal exercise thresholds.

In our model, the random refraction times between consecutive exercise opportunities can also be interpreted as a result of successive randomization. To this end, Kyprianou and Pistorius kypri_Canada apply fluctuation theory of Lévy processes to study the method of maturity randomization (Canadization) for derivatives pricing. The randomization procedure turns a finite-maturity option into a perpetual one. Avram et al. Avram_2004 consider a number of exit problems of spectrally negative Lévy processes, and apply them to value Russian options with a randomized maturity. In contrast, we consider a problem with multiple exercise rights, allowing for a negative discount rate, as well as negative and positive jumps for the underlying Lévy process.

The recent work by Christensen and Lempa ChristensenLempa13 discuss an optimal multiple stopping problem driven by a strong Markov process with i.i.d. exponential refraction periods. Another related work by Christensen et al. CIJ2013 study an optimal multiple stopping problem with random waiting times in terms of a sequence of single stopping problems. They provide an explicit solution to the problem of a perpetual put option whereby the sequential exercises are refracted by the first passage times of a geometric Brownian motion. Compared to their work, our model not only allows for a negative discount rate and general random refraction times, but also incorporates jumps in the underlying process via a Lévy process with positive phase-type jumps and negative jumps from any distribution. As discussed in Asmussen2004 , Lévy processes with phase-type jumps are capable of approximating a general class of Lévy processes. Herein, the major mathematical challenge is to characterize the optimal exercise strategies given minimal distributional structures of the Lévy jumps and refraction times.

The current paper is also relevant to the growing number of financial applications that involve making sequential timing decisions. Examples include multiple-exercise options carmonaDayanik08 ; Hambly_MF04 , portfolios of employee stock options (ChristensenLempa13, ; GrasselliHenderson2008, ; LeungSircarESO_MF09, ), sequential infrastructure investments Chiara ; EricTim13 , as well as reload and shout options kowk_reload_shout08 . Since some of these applications also involve a sequence of perpetual call options, our analysis is directly applicable and provides an extension to discounting with a negative rate.

Let us provide an outline of the paper. In Section 2, we formulate the optimal multiple stopping problem and present some general mathematical properties. In Section 3, we analyze both the single and multiple stopping problems driven by a two-sided Lévy process. Section 4 discusses the numerical implementation and provides some illustrative numerical examples. Section 5 concludes the paper. Our proofs, constituting a substantial part of the paper, are included in the Appendix.

2 Problem Formulation and General Properties

In the background, we fix a probability space hosting a Lévy process characterized uniquely by its Laplace exponent

| (2.1) |

for every such that (with the real part of ) where

| (2.2) |

for some , , and a measure with its support such that

| (2.3) |

We comment that the Laplace exponent can be extended beyond the line by analytical continuation. Throughout, we assume that , and is not a subordinator.

We denote as the probability and as the expectation with initial value . When , we drop the subscripts in and . Let be the natural filtration generated by . The underlying price process is modeled by an exponential Lévy process , .

Now we describe our optimal multiple stopping problem with a refraction period between consecutive exercises. In the general setting, we can take the refraction period as a deterministic constant or a positive random variable. We will assume throughout the paper that the distribution of the random variable has no atoms.

Denote by the set of -stopping times. However, the incorporation of random refraction times requires us to expand the filtration. For any collection of positive random variables, we denote to be the smallest filtration such that all members of are stopping times (see CIJ2013 ). For each fixed , we introduce the set of admissible sequence of exercise times:

where ’s are i.i.d. copies of some positive-valued random variable , which are independent of the Lévy process . The stopping time is an admissible exercise time when there are exercise opportunities left. In particular, is the first exercise time and is the last one.

Throughout we will work with the reward function

where we call the strike price. With exercise opportunities, the optimal stopping problem is defined as

| (2.4) |

We impose a standing technical integrability condition to ensure that the problem is well defined.

Assumption 2.1.

There exists a constant , such that the Lévy process satisfies

| (2.5) |

In Section 3, we will provide the conditions on in Assumption 3.1 so that this integrability condition will hold.

One key feature of our model is that the constant parameter can be taken to be positive/negative, representing a discounting/inflating factor. In the stock loan model proposed by Xia and Zhou xiazhou , the negative effective discount rate arises when the rate charged by the bank is higher than the interest rate . To see this, we consider an investor who borrows amount from a bank, using a share of stock as collateral. The borrower has the right to redeem the stock by paying the accrued principle at any time . Hence, we write the expected discounted payoff as for , where and . In a different class of applications, the negative effective discount rate is also relevant to real option exercise timing when the investment cost grows at a rate that is higher than the firm’s discount rate .

In order to solve the optimal multiple stopping problem (2.4), we will establish its equivalence to the following recursion of optimal single stopping problems:

| (2.6) |

where

| (2.7) |

and To this end, we first present some useful properties of the value function for every .

Lemma 2.1.

For every integer and all , the function is non-decreasing, convex, and hence differentiable almost everywhere on .

As a result of the convexity and monotonicity, we obtain the existence and uniqueness of the point of continuous fit for . More specifically, using arguments as in the proof of Corollary 3.1 of xiazhou , we know that there exists a level such that if and only if . Note that we can without loss of generality rule out the possibility of (exercising out of the money).

For any , we denote by the first up-crossing time

Here and throughout the paper we define . Furthermore, for every , we define the value of discounted payoff of a threshold strategy as

| (2.8) |

When , we know that the value function of the auxiliary problem (2.6) for is given by

When , the problem is trivial and the value function is approximated by the expected value under by taking arbitrarily large. We shall now assume the former and give sufficient conditions so that similar results hold for the problem (2.6) for . To this end, we adapt the arguments from the proof of Lemma 3.2 of Carmona2008 to obtain the following result.

Lemma 2.2.

Suppose . Then for every and all , we have .

Lemma 2.2 implies that will eventually continuously fit as increases. By the convexity of and , we know that is almost everywhere bounded from above by . In turn, we deduce that is differentiable in on since the distribution of does not charge a positive measure on the (at most) countable points where is not differentiable.

Corollary 2.1.

Suppose and . For every integer , we have , a.e. and

We now establish the equivalence between (2.4) and (2.6). Let us first recursively define the set of stopping times

| (2.9) | |||||

| (2.10) |

We show below that solve the optimal multiple stopping problems (2.4) and (2.6)-(2.7).

Theorem 2.1.

We now return to the optimal multiple stopping problem (2.6)-(2.7). From Lemma 2.2 we know that, if , then for every , we can define a finite level

| (2.12) |

Then, for every , the interval must be one connected domain of the optimal stopping region for problem (2.6) with exercise opportunities. It should be noted that, in general for , the optimal stopping region can potentially be disconnected, consisting of multiple disjoint intervals, as the composite payoff function is no longer piecewise linear in . However, if is the only optimal stopping region, then the up-crossing time must be the optimal stopping time to problem (2.6), and for all .

To resolve the issue of possible multiple disconnected components of optimal stopping for , we consider the best threshold type strategy, among all first up-crossing times , and then give a sufficient condition for its optimality.

Definition 2.1.

We call a level the optimal exercise threshold for problem (2.6) with exercise opportunities, if and only if the function is maximized at for all . More specifically, if satisfies the following:

-

(a)

For any fixed , the supremum of the function is given by ;

-

(b)

For any fixed , the supremum of the function is given by .

When , we know that if the latter is finite. Notice that, for a general , the optimal exercise threshold may not exist. The following result characterizes the relationship between and , when the latter exists.

Proposition 2.1.

Suppose . Fix an integer , assume that for all , and that is the only optimal stopping region for problem (2.6) with exercise opportunities. Then we have

-

(i)

for all ;

-

(ii)

, and if exists, we also have ;

-

(iii)

If exists and the process is a -supermartingale, then and is the only optimal stopping region. Hence, the up-crossing time is optimal.

Remark 2.1.

Proposition 2.1 implies that each value function can be determined by first optimizing the expected reward over all candidate thresholds that are above , followed by verifying the supermartingale property. Consequently, as far as the optimal thresholds are concerned, we can effectively remove the sign in the payoff function . From Proposition 2.1 we conclude that is the only optimal stopping region, and each optimal exercise threshold exists and is bounded above by .

We now show that if is the only connected optimal stopping region for all for some , then is non-increasing in . To show this, we first prove that the process

is a supermartingale for any fixed .

Proposition 2.2.

Suppose that and that is the only connected optimal stopping region for all for some , then the sequence of optimal exercise thresholds is non-increasing in , i.e.

and the process is a -supermartingale of class () (ProtterBook, , Chap. 3) for any .

Proposition 2.2 tells us, if threshold type strategies are optimal for problem (2.6) with exercise opportunities for all , then the optimal exercise thresholds are non-increasing in . Hence, even if threshold type strategies are not optimal for problem (2.6) with exercise opportunities, the optimal stopping region should contain . Moreover, for any number of remaining exercise opportunities, it is always optimal to exercise above the strike price.

3 Analytical Results

In this section, we assume that is either a spectrally negative Lévy process that is not the negative of a subordinator, or a Lévy process with an arbitrary negative jump distribution and a positive phase-type jump distribution Asmussen2004 :

| (3.13) |

Here, is a spectrally negative Lévy process with or without a Brownian motion component, is a Poisson process with arrival rate , and is an i.i.d. sequence of phase-type-distributed random variables with representation . In addition, and are mutually independent. For a comprehensive study on this process and its applications in American and Russian options, we refer the reader to Asmussen2004 .

Recall that a distribution on is of phase-type if it is the distribution of the absorption time in a finite state continuous-time Markov chain consisting of one absorbing state and transient states. Thus, any phase-type distribution can be represented by , the transition intensity matrix over all transient states , and the initial distribution of the Markov chain . Without loss of generality, we assume that the positive phase-type jump distribution is minimally represented with phases. From Asmussen2004 , this guarantees that the singularities of the Laplace exponent with positive real part are eigenvalues of . Moreover, by Theorem 5b on p.58 of Widder46 , we know that defined in (2.2) is the smallest positive pole of and . Henceforth, we impose the following technical condition.

Assumption 3.1.

The Laplace exponent and the discount rate satisfy either (i) , or (ii) and .

Under these conditions, we shall show in the lemma below that the optimal stopping problem in (2.6) is well-posed for each in the sense that the integrability condition in Assumption 2.1 is met. Also, the discounted price process under has to be a supermartingle, and not a martingale when (mordecki2002, , Theorem 1). In effect, the trivial optimal strategies of perpetual waiting are excluded.

We provide a detailed proof in Appendix A.6. Next, for an , we define to be the largest positive root of , which is a real number less than , if it exists. Notice that Assumption 3.1 and imply that exists and and . We denote the finite set of roots with positive real parts by

| (3.14) |

where, for the sake of mathematical convenience, we assume that the roots are all distinct for a given . It follows that and for all . Moreover, we remark that or according to whether is a subordinator or not, respectively (Asmussen2004, , Lemma 1). We label ’s in such a way that is in ascending lexicographic order (here is the imaginary part of any complex number ). Similarly, we define a second set of roots with positive real part, labeled in the same way as elements of :

| (3.15) |

where multiple roots are counted individually. Notice that we have and .

Remark 3.1.

If is a spectrally negative Lévy process, i.e. , then, by our assumption that is not a subordinator, we have and

Fix . Let be an exponential random variable, with rate parameter , that is independent of . We follow the convention that , -a.s. Then, it is known from Lemma 1 of Asmussen2004 that the Laplace transform of is given by

| (3.16) |

with , and the partial fraction coefficients:

| (3.17) |

As a result, the distribution of is given by:

| (3.18) |

Remark 3.2.

As explained in (Asmussen2004, , Remark 4), the assumption of distinct roots is made for convenience. When there are multiple roots, the corresponding distribution will admit a form similar to that in (3.18) with different constant coefficients. Moreover, the case with multiple roots only occurs for at most countably many values of over . In other words, if one arbitrarily sets the values of and , the probability of having multiple roots as a result is zero.

In the next subsection, we derive the value function and the optimal exercise threshold for the single stopping problem for any discount rate satisfying Assumption 3.1.

3.1 Optimal Single Stopping Problem

If and , then it is known from Theorem 1 of mordecki2002 that the optimal stopping time for an American call with strike price is given by

and the value of the American call option is given by:

| (3.19) |

where ’s are defined in (3.17). The analogous expectation in (3.19) for the case with can be computed using the sets in (3.14) and in (3.15), which we shall prove in Proposition 3.1 below.

In order to address the case with a negative discount rate (), one of our main steps is to apply a change of measures. For , we define a new probability measure by

| (3.20) |

Then, for , the Laplace exponent of is given by (Kyprianou2006, , Theorem 3.9)

Under the new probability measure , the process is also a Lévy process with a negative jump distribution and a positive phase-type distribution, with a new scaled Lévy measure .

Proposition 3.1.

We extend the definition (3.16) for and define the function and partial fraction coefficients using

| (3.21) |

Then for any fixed and , we have

| (3.22) |

Using Proposition 3.1, we can compute the expected payoff of any threshold type strategy . By Theorem 5b on p.58 of Widder46 , we can extend on both sides of (3.22) to a complex number as long as . In particular, by setting in (3.22), we obtain the following result.

Corollary 3.1.

For all and and hence on , we have

| (3.23) |

Since we already know the optimal stopping time is of threshold type when , the analytic expression for the value function of the single stopping problem is then readily available to us by optimizing the exercise threshold .

Theorem 3.1.

The optimal exercise threshold for the single stopping problem is given by and that the corresponding value function is given by

| (3.24) |

where the function is defined in (2.8).

Remark 3.3.

Recently, Cai and Sun Cai2014 consider a single stock loan problem under a hyper-exponential jump diffusion model, and provide an analytic solution for the perpetual single stopping problem. In comparison, our Theorem 3.1 applies to more general Lévy models as described by (3.13) and Assumption 3.1.

Remark 3.4.

If is a spectrally negative Lévy process, then (3.24) can be simplified to

| (3.25) |

where with . Notice that for all .

3.2 Optimal Multiple Stopping Problem

In this subsection, we characterize the optimal exercise thresholds that maximize . First, recall from Proposition 3.1 that for all , and the given and ,

| (3.26) |

The distribution of can be retrieved from (3.26) via inverse Laplace transform. To this end, let us introduce

| (3.29) |

Then there exists a unique (possibly signed) measure on , , such that

| (3.30) |

Remark 3.5.

If we assume that elements in are all distinct,111This is the case, for example, when the upward jumps are hyper-exponential. then we have,

Furthermore, we define a measure on for each :

| (3.31) |

Then it can be easily verified that

| (3.32) |

As a result of (3.26) and (3.32), we have for all ,

| (3.33) | |||||

| (3.34) |

Equations (3.33) and (3.34) can be used to compute . To this end, let have the same distribution as under , but is independent of . Then, for all ,

| (3.35) |

Recall from Corollary 2.1 that is differentiable for all . As a result, the optimal exercise threshold can be characterized by the first order condition: for any . In the remaining of this subsection, we will inductively prove that, if the threshold strategy is optimal for problem (2.6) with up to exercise opportunities, for some , then there exists a unique optimal exercise threshold for problem (2.6) with exercise opportunities. To show that the threshold type strategy is indeed optimal over all -stopping times in , we further prove that the process is a supermartingale. Finally, based on the result for in Section 3.1, mathematical induction will subsequently conclude the existence and uniqueness of the optimal exercise threshold , and the optimality of the threshold type strategy , for all .

To facilitate later calculations, we define for all that

| (3.36) |

where is the right derivative of . In particular, when , we can use (3.24) and (3.36) (see also the proof of Proposition 3.3 below using and ) to obtain:

| (3.37) |

Notice that is continuous, non-positive and non-increasing on and is strictly decreasing on .

The following result characterizes the first order condition for the optimal exercise threshold .

Proposition 3.2.

In the next results, we establish the monotonicity of the function , and the uniqueness of the solution to (3.38).

Proposition 3.3.

Under the assumption of Proposition 3.2, and further assume that the function is a non-increasing function. Let be any solution to (3.38), and define

| (3.39) |

where is the right partial derivative operator. Then, is continuous, non-positive, and non-increasing on . Moreover, it can be expressed as

| (3.40) |

We now prove the existence and the uniqueness of the optimal exercise threshold .

Lemma 3.2.

Hence, Proposition 3.2 applies, and the optimal exercise threshold is uniquely determined by (3.38).

Next, we prove the supermartingale property of the process , in order to show that the optimal stopping region for problem (2.6) is one-sided, and hence, yields the optimal stopping time The main tool is to re-express the value of the threshold type strategy , by an expectation of functionals of (see alili-kyp for a similar solution approach).

We begin with the case . It can be easily seen from the proof of Proposition 3.1 that

| (3.41) |

We use (3.41) to initialize our induction step.

Proposition 3.4.

4 Numerical Examples

In this section, we present numerical examples based on our analytical results. In particular, we illustrate the sensitivity of the optimal thresholds with respect to the distribution of refraction times. The numerical implementation is generally challenging. It involves the evaluation of the expectation while the distribution of the random variable is most commonly not explicit or even unknown. As is used in ZeghalSwing , Monte Carlo simulation is the most straightforward approach. However, it is far from being practical unless is a very small number. For refracted multiple stopping problems, one needs to know the entire expected future payoff functional to carry out the backward induction. The simulation approach would require the computation of these expectations for arbitrarily large number of starting points for each step, which adds to the computational burden and limits its applicability. In particular, the payoff function of our problem is unbounded (and increases exponentially); the truncation that would be needed under the simulation method will produce non-negligible errors that would further be amplified as increases.

For our numerical examples, we assume that is Erlang distributed (i.e. a sum of i.i.d. exponential random variables), and numerically solve for the optimal exercise thresholds using the methods described in our separate paper TimKazuHZ14 . The approach utilizes the resolvent measure (or the distribution of at an independent exponential random time) and carries out repeatedly and analytically the integrations with respect to this measure. The resulting value functions are shown to be in a piecewise analytic form. The results are exact when the jump size distribution is phase-type, and can be used as an approximation to problem with other Lévy jumps thanks to the denseness of the phase-type Lévy processes. The approach can also be applied to the case with constant refraction times via the technique of Canadization. For detailed analysis on its computational performance, we refer the reader to TimKazuHZ14 .

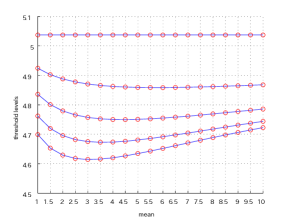

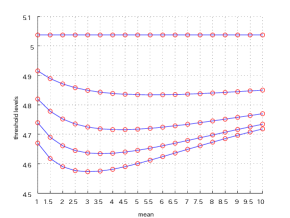

In our numerical results, we consider from (3.13) a spectrally negative Lévy process with i.i.d. exponential jumps:

for some and . Here is a standard Brownian motion, is a Poisson process with arrival rate , and is an i.i.d. sequence of exponential random variables with parameter . These processes are assumed to be mutually independent. For our studies below, we set , and . Also, we use and so that , which guarantees that Assumption 3.1 is satisfied. We consider two types of refraction times: (1) exponential and (2) Erlang with shape parameter . We compute the results for a range of the expected refraction times, denoted by .

In Figure 1, we plot the optimal exercise thresholds for against different means of the refraction time . Consistent with Proposition 2.2, the thresholds monotonically decrease as increases. In particular, the highest threshold corresponds to the last remaining exercise (). In this case, the refraction time is completely irrelevant, so the threshold value stays constant over different mean refraction times under any distribution. Interestingly, with fixed, the thresholds are not monotone in the mean refraction time. On one hand, refraction times are constraints on the stopping times, so they reduce the value functions but not necessarily the exercise thresholds. Intuitively, a very long refraction time reduces the value of subsequent exercise opportunities, and incentivizes the holder to focus more on the next immediate stopping. This helps explain that the thresholds tend to be closer for very long mean refraction times.

|

|

| (1) Exponential | (2) Erlang |

5 Conclusions

We have studied an optimal multiple stopping problem with the features of negative discount rate and random refraction times under a general class of Lévy models. In order to account for the negative discount rate, the technique of change of measure is shown to be very useful though the analysis under the new measure is challenging. As seen in Theorems 3.1 and 3.2 above, the optimal exercise thresholds are determined explicitly in the single stopping case and recursively in the multiple stopping case. While our problem setting is selected with the application to stock loans in mind, the current paper also presents a blueprint to rigorously analyze perpetual optimal refracted multiple stopping problems with alternative payoffs, such as put options. These would be natural directions for future research.

Appendix A Appendix

A.1 Proof of Lemma 2.1

We begin by noticing that, for any fixed ,

For , for any stopping time and any such that , it follows from the monotonicity of that

Similarly, from the subadditivity of supremum and the convexity of , we have, for any such that , and any , that

| (A.44) |

Hence, the convexity holds also for . This implies that is differentiable almost everywhere on .

Now suppose that the claim is true for for some ; that is, is non-decreasing and convex. By the same argument above, we conclude that is also non-decreasing and convex. This implies that and all have the monotonicity and convexity properties. By induction, we conclude.

A.2 Proof of Corollary 2.1

For we have , for a.e. , or equivalently , a.e. and , for any . Let us denote by , where and ( and , resp.) are, respectively, the right and left derivatives of (, resp.). Then we know that is at most a countable set by Lemma 2.1. On the other hand, using the fact that has no atom, we know that, for any fixed , we have for -almost every , . It follows that is almost surely differentiable at this fixed , and , -a.s. By the assumption, the nonnegative random variable has a finite expectation. Now for any , as , we have by Jensen’s inequality that

where we have used the fact that , and

and the dominated convergence theorem. It follows that is differentiable in , and

Now suppose that the claim is true for for some . Then we know that is differentiable on and its derivative admits the upper bound

That is, for all . It follows that , a.e. which implies that , a.e. By the same arguments as above, we also obtain that, for all ,

The result now follows from mathematical induction.

A.3 Proof of Theorem 2.1

First, Lemma 2.2 implies that holds provided that and is not a subordinator.

Next, following Lemma 2.1 of Carmona2008 , we deduce recursively that

| (A.45) |

for all . Hence, the single optimal stopping problem (2.6) is well defined. To ensure the existence of an optimal stopping time, we may adapt the proof of Proposition 3.2 in ZeghalSwing to the setting with possibly negative discount rate and call-like payoff. More precisely, by Lemma 2.1 and Corollary 2.1 we know that is globally Lipschitz in , which implies that, by the proof of Proposition 3.2 in ZeghalSwing , the expected jump of , at any predictable time , is zero, namely,

where . This implies that the Snell envelope is left-continuous in expectation. In turn, this allows us to apply the arguments in Theorem 2.1 of Carmona2008 to conclude (2.11). This proves (i).

To prove (ii), we first comment that the result holds trivially for the case . For , we observe from (2.11) that since are admissible candidate stopping times (see(2.9)-(2.10)). The reverse inequality can be proved by induction. To this end, notice that for any arbitrary -stopping time by (2.6) for . Now by applying (2.6), (2.7) and repeated expectations, we get

| (A.46) |

for every -stopping time and -stopping time . Maximizing (A.3) over yields that . The result now follows from mathematical induction.

Finally, for (iii), for any finite -stopping time , by the strong Markov property, we have

where the first and second inequalities follow from (A.45) and the equality is due to repeated expectations. Hence we have the uniform boundedness of elements of in . This proves (iii) and completes the proof.

A.4 Proof of Proposition 2.1

If for all , then by (2.7), we know that for all . Furthermore, if is the only optimal stopping region for problem (2.6) with exercise opportunities, then the up-crossing time is the optimal stopping time. Hence, for all , we prove (i) through the inequality

To prove (ii), we first recall from Lemma 2.2 that . Hence, for the first claim, it is sufficient to show that on . Indeed, we use the supermartingale property of value functions to obtain that for all . Therefore, for all ,

It follows that . Similarly, if the optimal exercise threshold exists, then we have

Therefore, for , we have , which implies that .

We now proceed to prove (iii) by establishing the sufficient conditions for optimality (see e.g. (alili-kyp, , Sect. 6)). If the optimal exercise level exists, then it is easily seen that

-

(a)

for all , , and by the fact that (see (ii));

-

(b)

for all , we have ;

-

(c)

for all , by the strong Markov property of , we have

That is, the stopped process is a -martingale for any fixed .

Now if we know additionally that is a supermartingale, then we can conclude that , and is the only stopping region.

A.5 Proof of Proposition 2.2

Clearly the claim holds for as we already know that , is a -supermartingale, and all random variables in the set in Theorem 2.1 are uniformly bounded in . If , suppose the claim is true for for some . That is,

Now, from the general theory of optimal stopping we know that the stopped process is a martingale (see e.g. (alili-kyp, , Sect. 6)). Therefore, for , we know that the stopped process is a martingale. Moreover, let us introduce the first down-crossing time

If , then the stopped process is equal to a stopped supermartingale less a stopped martingale, and hence a supermartingale. Finally, for all , we have that

Hence, for all and , we have

| (A.47) | |||||

where we used the assumption that is a supermartingale, and the independence between and . Combining all cases, we conclude that the process is a supermartingale.

The class (D) property of now follows from Minkowski’s inequality and the fact that the elements in , , are uniformly bounded in (see Proposition 2.1 above).

A.6 Proof of Lemma 3.1

For any satisfying , and any sufficiently large , we have

| (A.49) |

where we used Proposition 1.8 on page 259 of AsmussenBook and is the smallest positive root of

It is now sufficient to show that it is possible to choose such that , and hence the random variable has a finite expectation for . To this end, we show that for a sufficiently small . Indeed, for all , we have , where we used Jensen’s inequality for positive random variable in the last step. Hence, the smallest positive solution .

Let us first assume that . Then for sufficiently small , by the continuity of at 1, we have

On the other hand, if , and . Then for sufficiently small , we have , and

A.7 Proof of Proposition 3.1

Let us define a new measure by (3.20) for . Under this measure, is a Lévy process with Laplace exponent (Kyprianou2006, , Corollary 3.10):

| (A.50) |

Then, for any , the change of measure yields the expectation

| (A.51) | |||||

We now let in (A.51). By applying the monotone convergence theorem to the left hand side of (A.51), we obtain . Similarly, notice that the non-negative random variable in the expectation (A.51) is bounded by 1, -a.s. we can apply the bounded convergence theorem to obtain that

Now because for any we have , -a.s., the dominated convergence theorem yields that

| (A.52) |

The right hand side of (A.52) can be computed using Lemma 1 of alili-kyp . Precisely, we have

| (A.53) |

The law of under can be extracted from (3.16) and (3.18). More precisely, for any , let and be, respectively, the roots to

| (A.54) |

which are indexed in the same way as the elements of and . Then, we infer from (A.50) that , and for all . Similarly, we let be the roots to

From (3.14) and (A.50) we deduce that and , which means that

| (A.55) |

By our assumption, ’s are distinct and and for all . Moreover, the fact that the roots ’s are single implies that , and hence each branch of the mapping is locally a diffeomorphism around 0. It follows that ’s are also distinct for all sufficiently small . It follows from (3.16) and (3.18) that

As , we have that , and in particular, and for all . As a result, for ,

| (A.56) | |||||

where we used (A.55) in the second equality. Moreover, for and , the ratio

which, as , tends to

| (A.57) |

Combining (A.52), (A.53), (A.56) and (A.57), we obtain that, for all ,

| (A.58) |

This completes the proof.

A.8 Proof of Theorem 3.1

We only need to prove the assertion for the case since the case of non-negative discount rate has been addressed in mordecki2002 .

We begin by differentiating with respect to to get

| (A.59) |

Clearly, satisfies the first order condition . To show that is indeed the optimal exercise threshold, we only need to verify the followings (see, for example, xiazhou ):

-

1.

for , is decreasing for all and ;

-

2.

for , is increasing for all and is non-increasing for all , and .

Since , it follows from (A.59) that the monotonicity of for amounts to showing that

By setting in (A.56), we obtain

| (A.60) |

Similarly, it follows from (A.57) that, for all ,

| (A.61) | |||||

From (A.60) and (A.61), we obtain

| (A.62) |

To complete the proof that is indeed the optimal exercise threshold, we need to show that, for any , ; and for , . To this end, notice that for all . On the other hand, using Corollary 3.1 we have that

| (A.65) |

Thus, is indeed the optimal exercise threshold for any . Finally, (3.24) follows from (3.23) by setting .

A.9 Proof of Proposition 3.2

First, notice that (3.23) and (3.2) imply that, for any fixed , the function is differentiable in for all . Direct calculation (using (3.31)) gives the derivative

| (A.66) |

Recall the inequality (A.62) in the case with . For , we compute from (3.18) to get

Notice that, due to the linear independence of ’s, the left hand side of the above equation is strictly positive on all but a possibly finite set in . Moreover, for all , we have for all , hence . This implies that

On the other hand, for all , from the proof of Proposition 2.1 we know that . It follows that there exists at least a such that , and hence

By the assumed continuity of , we know that there exists at least one solution to (3.38). If the optimal exercise threshold exists, then we know that . For any fixed , the function is maximized at , hence for all . This implies that is a solution to (3.38).

A.10 Proof of Proposition 3.3

We will first prove an auxiliary lemma connecting measures with .

Lemma A.1.

Let and be the right derivatives of and , respectively. Then

| (A.67) |

Proof.

We will prove (A.67) by using the bivariate Laplace transform. To this end, let and that , then by (3.31) and (3.32) we have

| (A.68) |

where, in the last equality, we used that fact that, if is a subordinator, then ; otherwise, we have , and

On the other hand, by (3.30) we have, for such that ,

| (A.69) |

From (A.68) and (A.69) we know that (A.67) holds for all . ∎

We are now ready to give the proof of Proposition 3.3. Since threshold-type strategies are optimal for problem (2.6) with up to exercise opportunities by assumption, it follows that for all , and for all by comparing (3.36) and (3.39). Also, observe that for . Applying this fact to (3.39), we get

| (A.70) |

For , we use (3.33) and (3.34) to write

It follows that,

| (A.71) | ||||

| (A.72) |

Moreover, from Lemma A.1 we know that

| (A.73) |

From (A.71), (A.72) and (A.73) we have

| (A.74) |

As a result, we have for all . Combining this with (A.70) yields (3.40). Moreover, from the definition of in (3.38), we know that is non-increasing on . The first order condition (3.38) shows that is also continuous at , and thus is non-positive on .

A.11 Proof of Lemma 3.2

Suppose there are two distinct solutions to (3.38), say, . Then by Proposition 3.3 we have a non-increasing, non-positive function

Moreover, this function is strictly decreasing for all . This implies that

This contradicts the assumption that solves (3.38).

To finish the proof, we let be the unique solution to (3.38). Notice from (A.66) that

-

1.

for all fixed , the function is decreasing in for all ;

-

2.

for all fixed , the function is increasing in for all , and decreasing in for all .

We now apply a similar argument as in the proof of Theorem 3.1 to show that, for all , ; and for all , . This will allow us to conclude that is indeed the optimal exercise threshold. To this end, from (3.16), (3.21), (3.30), (3.32) and the fact that , we know that

| (A.75) |

Below we consider two cases separately:

- 1.

- 2.

A.12 Proof of Proposition 3.4

For any fixed , notice that except for a null set under measure and that on . Also, recall that for all . We thus have

| (A.80) |

Now let us denote by . Notice that and is independent of on the event , so expression (A.80) above is further equal to

| (A.81) |

In the last equality, we have applied a change of measure, along with the dominated convergence theorem (see (A.52)).

On the other hand, using the recursion (3.40) and mathematical induction we can show that there exist positive constants such that

As a result, the random variable

is dominated by the non-negative random variable

where we used the fact that in the last step.

Similarly, using (3.42) we have

| (A.82) |

By the dominated convergence theorem, we obtain from (A.81) and (A.82) that

To prove the supermartingale property, we use the fact that, on the event , we have , -a.s. and has the same law as , but is independent of . It follows from the non-negativity and the non-decreasing property of that, for any ,

Here the third inequality follows from Fatou’s lemma and the Strong Markov property of . This completes the proof.

References

- [1] L. Alili and A. E. Kyprianou. Some remarks on first passage of Lévy processes, the American put and smooth pasting. Ann. Appl. Probab., 15:2062–2080, 2004.

- [2] S. Asmussen and H. Albrecher. Ruin probabilities. World Scientific, 2010.

- [3] Søren Asmussen, Florin Avram, and Martijn R. Pistorius. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl., 109(1):79–111, 2004.

- [4] F. Avram, A. E. Kyprianou, and M. R. Pistorius. Exit problems for spectrally negative Lévy processes and applications to (Canadized) Russion options. Ann. Appl. Probab., 14:215–235, 2004.

- [5] Christian Bender. Dual pricing of multi-exercise options under volume constraints. Finance and Stochastics, 15:1–26, 2011.

- [6] Fischer Black. Interest rates as options. The Journal of Finance, 50(5):1371–1376, 1995.

- [7] N. Cai and L. Sun. Valuation of stock loans with jump risk. Journal of Economic Dynamics and Control, 2014. To appear.

- [8] R. Carmona and S. Dayanik. Optimal multiple stopping of linear diffusions. Mathematics of Operations Research, 33(2):446–460, 2008.

- [9] R. Carmona and N. Touzi. Optimal multiple stopping and valuation of swing options. Mathematical Finance, 18(2):239–268, April 2008.

- [10] N. Chiara, M. Garvin, and J. Vecer. Valuing simple multiple-exercise real options in infrastructure projects. Journal of Infrastructure Systems, 13(2):97–104, 2007.

- [11] S. Christensen and J. Lempa. Resolvent-techniques for multiple exercise problems. Working paper, 2013.

- [12] Sören Christensen, Albrecht Irle, and Stephan Jürgens. Optimal multiple stopping with random waiting times. Sequential Analysis, 32(3):297–318, 2013.

- [13] E. Dahlgren and T. Leung. An optimal multiple stopping approach to infrastructure investment decisions. Journal of Economic Dynamics and Control, 53:251–267, 2015.

- [14] M. Dai and Y.K. Kwok. Optimal multiple stopping models of reload options and shout options. Journal of Economic Dynamics and Control, 32:2269–2290, 2008.

- [15] A.K. Dixit and R.S. Pindyck. Investment Under Uncertainty. Princeton University Press, 1994.

- [16] M. Grasselli and V. Henderson. Risk aversion and block exercise of executive stock options. Journal of Economic Dynamics and Control, 33(1):109–127, January 2009.

- [17] A. E. Kyprianou and M. R. Pistorius. Perpetual options and Canadization through fluctuation theory. Annals of Applied Probability, 13(3):1077–1098, 2003.

- [18] Andreas E. Kyprianou. Introductory Lectures on Fluctuations of Lévy Processes with Applications. Universitext. Springer-Verlag, Berlin, 2006.

- [19] T. Leung and R. Sircar. Accounting for risk aversion, vesting, job termination risk and multiple exercises in valuation of employee stock options. Mathematical Finance, 19(1):99–128, January 2009.

- [20] T. Leung, K. Yamazaki, and H. Zhang. An analytic recursive method for optimal multiple stopping: Canadization and phase-type fitting. International Journal of Theoretical and Applied Finance, 2015. To appear.

- [21] R. McDonald and D. Siegel. Investment and the valuation of firms when there is an option to shut down. International Economic Review, 26(2):331–349, 1985.

- [22] N. Meinshausen and B.M. Hambly. Monte Carlo methods for the valuation of multiple-exercise options. Mathematical Finance, 14, 2004.

- [23] E. Mordecki. Optimal stopping and perpetual options for Lévy processes. Finance and Stochastics, 6:473–493, 2002.

- [24] P. Protter. Stochastic Integration and Differential Equations. Springer, 2003.

- [25] D. V. Widder. The Laplace Transform. Dover Publication, 1946.

- [26] J. Xia and X. Zhou. Stock loans. Mathematical Finance, 17(2):307–317, 2007.

- [27] A. B. Zeghal and M. Mnif. Optimal multiple stopping and valuation of swing options in Lévy models. International Journal of Theoretical and Applied Finance, 9(8):1267–1297, 2006.