A Dynamic Structure for High Dimensional Covariance Matrices and its

Application in Portfolio Allocation

***This research is supported by the Singapore National Research

Foundation under its Cooperative Basic Research Grant and administered by the

Singapore Ministry of Health’s National Medical Research Council (Grant No.

NMRC/CBRG/0014/2012) and the National Natural Science Foundation of China

(Grant No. 11271242). John Box was supported by an EPSRC funded studentship

through the University of York. Shaojun Guo was partly supported by Key

Laboratory of RCSDS, Chinese Academy of Sciences and an EPSRC research grant in United Kingdom.

Shaojun Guo

Chinese Academy of Sciences,

Beijing, People’s Republic of China

& London School of Economics,

London, United Kingdom

John Box

Department of Mathematics

University of York, United Kingdom

Wenyang Zhang

Department of Mathematics

University of York, United Kingdom

Abstract

Estimation of high dimensional covariance matrices is an interesting and

important research topic. In this paper, we propose a dynamic structure

and develop an estimation procedure for high

dimensional covariance matrices. Asymptotic

properties are derived to justify the estimation procedure and simulation

studies are conducted to demonstrate its performance when the sample size is

finite. By exploring a financial application, an

empirical study shows that portfolio allocation based on dynamic high

dimensional covariance matrices can significantly outperform the market

from 1995 to 2014. Our proposed method also outperforms portfolio allocation

based on the sample covariance matrix and the portfolio allocation

proposed in Fan, Fan and Lv (2008).

Covariance matrix estimation is an important topic

in statistics and econometrics with wide applications

in many disciplines, such as economics,

finance and psychology. A traditional approach

to estimating covariance matrices is based on the sample

covariance matrix. However, the sample covariance matrix would

not be a good choice when the dimension is large, and

especially when the inverse is required, which is often the

case when constructing a portfolio allocation

in finance. This is because the

estimation errors would accumulate when using the inverse of the sample

covariance matrix to estimate the inverse of the covariance matrix. When the

size of the covariance matrix is large, the cumulative estimation error would

become unacceptable even if the estimation error of each entry of the

covariance matrix is tiny.

In recent years there has been various attempts to address high dimensional

covariance matrix estimation. Usually, a sparsity condition is imposed

to control the trade-off between variance and bias. See, Wu and

Pourahmadi (2003), El Karoui (2008), Bickel and Levina (2008a, 2008b), Lam and

Fan (2009), Fan, Liao, and Mincheva (2011), and the references

therein. Fan, Fan and Lv (2008) considered a different approach by imposing

a factor model and estimated the covariance matrix based on this structure.

Most of the literature addressing high dimensional covariance matrix

estimation assumes that the covariance matrix is constant over time. However, in many

applications, covariance matrices are dynamic. For example,

today’s optimal portfolio allocation may not be

optimal tomorrow, or next month. Therefore, when applying the formula for

Markowitz’s optimal portfolio allocation (Markowitz 1959), the covariance matrix used should

be dynamic and allowed to change

over time.

In order to introduce a dynamic structure for covariance matrices,

one cannot simply assume each entry of a covariance matrix is a

function of time because this would not serve very well in

prediction. Instead, we start with an approach stimulated

by Fan, Fan and Lv (2008) which is based on the Fama-French three-factor

model (Fama and French, 1992, 1993)

(1.1)

where is the excess return of an asset and is

the vector of the three factors at time .

To make (1.1) more flexible, we allow a to depend on the values

of the three factors at time . To avoid the so-called

‘curse of dimensionality’, we assume this dependence is

through a linear combination of the values of the three

factors at time , which brings us to

(1.2)

This motivates a dynamic structure for the covariance matrix

of a random vector through an adaptive varying

coefficient model which we shall now introduce.

Suppose , , is a time series,

where is a dimensional vector and is a dimensional

factor. An underlying assumption throughout this paper is that

when , and is

fixed. Also, we assume that , , is a stationary Markov process.

We assume

(1.3)

where , is a factor loading matrix which is varying over , and , are random errors which are independent of , . We assume

where

(1.4)

for each and for some integers and .

Let be the algebra generated

by .

The main focus of this paper is on the conditional covariance matrix

(1.5)

where

In (1.5), , , , and

, , , are unknown and need to be

estimated. Not only does (1.5) introduce a dynamic structure for

, but also reduces the number of unknown parameters

from to unknown functions and

unknown parameters.

We remark that model (1.3) is interesting in its own

right, since it combines single-index modelling (Carroll et al., 1997,

Härdle et al., 1993, Yu and Ruppert, 2002,

Xia and Härdle, 2006, Kong and Xia, 2014) and

varying coefficient modelling (Fan and Zhang, 1999, 2000,

Fan et al., 2003,

Sun et al., 2007, Zhang et al., 2009, Li and Zhang, 2011,

Sun et al., 2014). In this paper, as a by-product,

an estimation procedure for (1.3) is proposed and an iterative algorithm

is developed for implementation purposes.

This paper is organised as follows. We begin in Section 2 with a

description of the proposed estimation procedure

for . A discussion on bandwidth

selection is given in Section 3. In

Section 4 we provide asymptotic properties of the

estimation procedure. An iterative algorithm to implement the

estimation procedure is suggested in Section 5. Using

the proposed dynamic structure for covariance matrices and the

developed estimation procedure, we outline a process for constructing a

portfolio allocation based on the formula for Markowitz’s

optimal portfolio in Section 6. The performance

of the estimation procedure and portfolio allocation

are also assessed by simulation studies in

Section 7. In Section 8, we apply the portfolio allocation

methodology to a data set consisting of 49 industry

portfolios which are freely available from Kenneth

French’s website. We find that the proposed methodology

works surprisingly well. All the detailed proofs are relegated to the appendix.

2 Estimation procedure

In this section, we are going to introduce an estimation procedure for

. We will first estimate , ,

, and , and denote the resulting estimators

by , , ,

and for and

. Let be with

and being replaced by and

respectively. We use

(2.1)

to estimate .

Throughout this paper, for any function , we use to

denote its derivative. For any functional matrix , we define

its derivative as . For any integers and

, we use to denote a matrix with each entry

being , and to denote a -dimensional vector with each component being .

2.1 Estimation of

A Taylor expansion gives, for in a neighbourhood of ,

and

for . This,

together with the idea of least squares estimation, brings us to the following local

discrepancy function

(2.2)

where: , is a kernel function;

is a bandwidth; and , , and are used to denote

, ,

and respectively. By minimising

under the conditions

we use the corresponding value of as the estimator and denote it by .

2.2 Estimation of and

Once an estimate has been obtained, the estimators of

and can be constructed row by row through a standard univariate

varying coefficient model for each component of . Let

By (1.3), and for , we have the following synthetic

univariate varying coefficient model

for

By local linear estimation for standard varying-coefficient models, and for

any given , we have

where

and is a bandwidth.

2.3 Estimation of

In order to estimate

and , for

any given u, we use the local constant estimators

(2.3)

This gives us the following estimator of

(2.4)

where

and is a bandwidth.

2.4 Estimation of

For each , , let

By (1.4), we have the following synthetic GARCH model

(2.5)

which is equivalent to

where , when ,

and when .

Once and have been estimated, by substituting

them into (2.5) and setting

for , we can obtain an estimator

of and hence an estimator

of .

For each , , let

. We are going to use a quasi-maximum likelihood approach

to estimate . We define the negative quasi log-likelihood function

of as

(2.6)

where are recursively defined by (2.5) with

initial values being either

or

By minimising with respect to on a

compact set defined in (B3) in Appendix A, we use the minimiser

to estimate .

3 Bandwidth selection

The choice of the bandwidth , used in the estimation of , is not

crucial. According to some numerical analysis not presented in

this paper for brevity, the accuracy of the estimator

is not very sensitive to , as long as is within

in a reasonable range. In the computational algorithm for

estimating , see Section 5, we recommend

choosing a bandwidth equal to around of the following range

(3.1)

where is a randomly chosen initial estimate of . We

update on subsequent iterations by replacing in (3.1) with the most recent estimate of . This

approach is employed in the simulation studies and real data analysis of

this paper.

We now focus on the selection of the bandwidth , used in the

estimation of and . The

proposed bandwidth selection is based on a -nearest neighbours bandwidth

with being selected by cross-validation. We define the cross-validation statistic by

(3.2)

where

and are the respective

estimators of and using a -nearest neighbours

bandwidth based on , , and where is a look-back integer parameter such that .

Hence, denoting the that minimises by , we use a -nearest neighbours bandwidth in the estimation of and

. The bandwidth in the estimation of or

can also be selected by cross-validation in a similar

way.

4 Asymptotic properties

In this section, we are going to present the asymptotic properties of the

proposed estimators. We first introduce the following notation which will be used throughout this paper. For any matrix , we use

and to denote respectively the

smallest and largest eigenvalues of A. The trace of A is denoted by

, the Frobenius norm of A by , and the spectral norm (also called operator norm) and element-wise norm by

respectively. We also define

and

Theorem 1.Under assumptions (A1 - A5), (B1 - B4), (C1) and

(C3) in Appendix A, there exists and a small such that

(I)

(II)

(III)

(IV)

where is a compact subset of the range of .

Remark 1. Theorem 1 shows that

when diverges to as , provided that . It indicates that the index is estimated with a rate faster than the normal rate , which is the optimal rate if is fixed. This is known as a ‘blessing of high dimensionality’.

The main interest of this paper is to estimate . To

measure the accuracy of an estimator of a matrix of size ,

we use the entropy loss norm, proposed by James and Stein (1961),

To facilitate our presentation, we focus on the convergence of , after obtaining the data .

Theorem 2.Under assumptions (A1 - A5), (B1 - B4) and (C1 - C4)

in Appendix A, there exist and such that,

with probability at least ,

Fan, Fan and Lv (2008) and Fan, Liao and Mincheva (2011) showed an estimator

of a covariance matrix based on a certain structure would achieve a higher

convergence rate than the sample covariance matrix. Theorem 2 tells us the

same story. There are three terms to measure the accuracy of . The first two terms

tell us how the nonparametric smoothing steps in estimating affect the performance of , and the third term evaluates the influence of conditional covariance matrix . It turns out that even though dimensional smoothing is required, its effect is small and often negligible if is large.

5 Computational algorithm

To implement the proposed estimation procedure for

, the hardest part is to compute an estimate of

, which is equivalent to finding the minimum of

under the conditions

We now introduce the proposed iterative algorithm which can be used to do this minimisation. Let

which is

with the in the kernel function being replaced by b. First of all,

randomly choose

an initial estimate for , denoted by , such

that and the first component of is

positive. Then, iterate between the following two steps until convergence:

(Step 1)

If this is the first iteration, let .

Otherwise, set equal to the obtained from Step 2 of

the previous iteration. Minimise

with respect to and , and denote the minimiser by

, , , , ,

, , and .

(Step 2)

Minimise

with respect to . Denote the minimiser by , and

define when the first

component of is positive and otherwise.

The resulting from the convergence is the final estimate of .

The proposed iterative algorithm is easy to implement as both minimisers in Step

1 and Step 2 have a closed form. Once an estimate of is obtained, the remaining

computation of becomes straightforward.

6 Portfolio allocation

In this section, we will briefly describe the construction of an estimated

optimal portfolio allocation based on the proposed dynamic structure and the

associated estimation procedure. Since the formula for optimal portfolio allocation

contains we shall introduce its estimator

first.

By taking conditional expectation of (1.3), we have

Our estimated optimal portfolio allocation builds on the mean-variance optimal portfolio

by Markowitz (1952, 1959). The allocation vector w of risky assets, to

be held between times and , is defined as the solution to

where is the target return imposed on the portfolio.

The solution is given by

(6.2)

where

7 Simulation studies

In this section, we are going to use a simulated example to show how well

the proposed estimation procedure and portfolio allocation works. We

shall use to denote the entry corresponding to the th row and th column of .

We generate 1000 data sets from

model (1.3) together with (1.4).

We repeat this using the following combinations

of and :

,

,

and

.

We set

For , we set

where are some fixed parameters for

and . In order to define

, we simulate them independently from a uniform distribution on

, and use these same values throughout all simulations.

For , we generate independently from a uniform

distribution on , from

-variate standard normal distribution, and

through . Once both and

have been generated, can be generated through (1.3) for

.

We will initially pretend that is unknown to us, and

this will not be used in the estimation of . The purpose of generating an

additional data point is to enable us to

calculate the 1-period simple return

(7.1)

of a portfolio allocation formed at time

based on data , .

In order to evaluate the performance of an estimator of matrix

we use the following metric

We also use the Sharpe ratio

to evaluate the performance of , where

is the standard deviation of

We assume a zero risk-free rate for simplicity.

We first examine how well the estimation procedure works. We estimate

, and use to estimate

.

The kernel function in the estimation procedure

is taken to be the Epanechnikov kernel , and the

bandwidths are selected by the methodology described in Section 3.

The results, presented in Tables 1 and 2, show both and work very well.

Table 1: Mean and Standard Deviation of

0.183

0.189

0.136

0.141

0.046

0.049

0.034

0.035

\@normalsize

In this table,

, and

is the standard deviation of .

Table 2: Mean and Standard Deviation of

0.114

0.105

0.078

0.070

0.017

0.013

0.012

0.009

\@normalsize

In this table,

, and

is the standard deviation of .

We now examine the performance of the proposed portfolio allocation, using a target return , by computing the return as described in (7.1). In order to see

how much gain can be made by making use of the dynamic structure, we make a comparison

with portfolio allocations based on Markowitz’s formula but where the covariance matrix is

estimated using the sample covariance matrix and also the estimator proposed

by Fan, Fan and Lv (2008). The mean, standard deviation and Sharpe ratio of

the returns are presented in Table 3. For each situation discussed,

we see the Sharpe ratio of the

proposed portfolio allocation is much bigger than the other

two portfolio allocations. This suggests there is significant gain from making use of the

dynamic structure of the covariance matrix.

Table 3: Means, Standard Deviations and Sharpe Ratios

0.99%

1.01%

1.03%

1.03%

0.96%

0.96%

1.02%

1.02%

0.96%

0.96%

1.02%

1.02%

0.40%

0.28%

0.39%

0.27%

1.02%

1.03%

1.03%

1.02%

0.99%

0.97%

1.02%

1.00%

2.49

3.57

2.63

3.83

0.94

0.93

0.99

1.00

0.97

0.99

1.00

1.02

\@normalsize

In this table we denote the proposed portfolio allocation by ,

the portfolio allocation formed by Markowitz’s formula using the

sample covariance matrix by , and the portfolio allocation formed by Markowitz’s formula using the estimated covariance matrix from Fan, Fan and Lv

(2008) by .

8 Real data analysis

In this section, we are going to apply the dynamic structure for

covariance matrices to a real data set. We use the term Face (Factor model with an

Adaptive-varying-coefficient-model structure

Covariance matrix Estimator) to denote the proposed

portfolio allocation. This name was chosen because the estimator

will ‘face’ the markets today based on what happened yesterday and adapt according

to the dynamic structure.

We compare Face with the allocation based on the sample covariance matrix

(denoted by Sam), and the allocation proposed by Fan, Fan and

Lv (2008) (denoted by Fan). In all three cases, we use the same target return

. We also make a comparison with the market portfolio

(denoted by Market) since this aids as an important benchmark

indicating whether we are in a bull or bear market. In this section,

the kernel function used in the construction of Face is still taken

to be the Epanechnikov kernel, and the bandwidths are selected by the method

described in Section 3.

All data used can be freely downloaded from Kenneth French’s website

http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

and was accessed on 2nd April 2015. The response variable is chosen to be the

vector of the daily returns of industry portfolios (value weighted) minus the

risk-free rate. The

observable factors , and are taken to be the

market, size and value factors respectively from the Fama-French three-factor model.

The labelling along with a brief description of

and

can be found in

Table 4 and Table 5 respectively.

There are various advantages of using the portfolio returns for as

opposed to using individual stocks: we avoid having to merge different sources

of data; we avoid survivorship bias (where we only picked companies that did

not go bankrupt); and we attempt to avoid company specific risk. A further

benefit is that the results we give are entirely reproducible

since the data is free and presented in a spreadsheet format.

To have a better idea about what the data is like, we plot the observations

from 3rd January 1995 to 31st December 2014 of

the three factors and the risk-free rate in Figure 1, and the first four components of in Figure 2

corresponding to the industrial sectors Agriculture, Food Products, Candy & Soda, and

Beer & Liquor. The plots show

clearly that there are periods of large volatility around the 2008-2009

financial crisis. We will see Face performs reasonably well even during that

period, whilst the others do not.

We compare the three portfolio allocations, (Face, Sam and Fan), along

with the market portfolio, year by year from 1995 to 2014 using a simple

trading strategy. For each year we trade

on each trading day, which is approximately trading days per year. At the

beginning of each year we assume we have an initial balance of pounds.

Although this initial choice is arbitrary, it is a useful way of comparing

the performance during the course of a year. We assume no transaction costs,

allow for short selling, and assume that all possible portfolio allocations

are attainable. Our trading strategy consists of forming a portfolio allocation

the end of each trading day and holding it until the end of the

next trading day. Between

day and day , we obtain the portfolio return

where is formed based on , , for some look-back integer . With the realised returns

, , we can calculate the annualized

Sharpe ratio

where

and is the risk-free rate on day .

Hence, for each year, and for each of the four trading strategies, we

compute an annualized Sharpe ratio and the balance at the end of the

final trading day of the year. We repeat this using , , and .

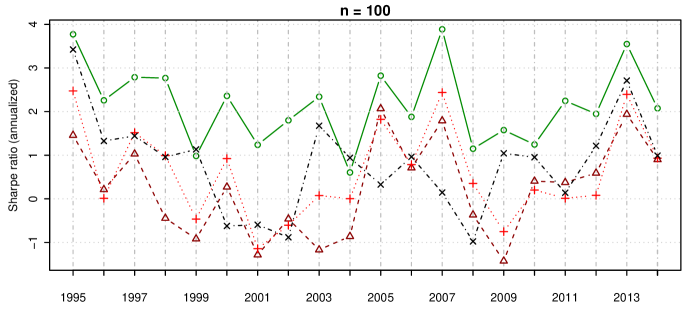

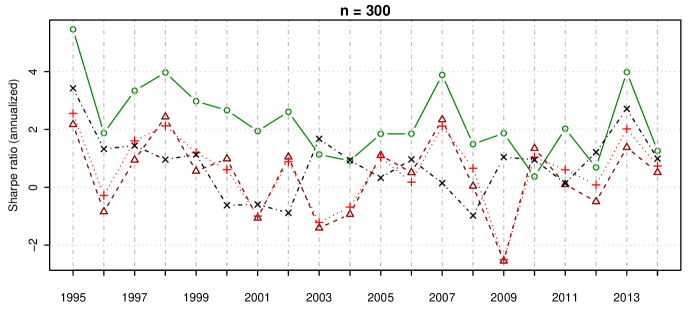

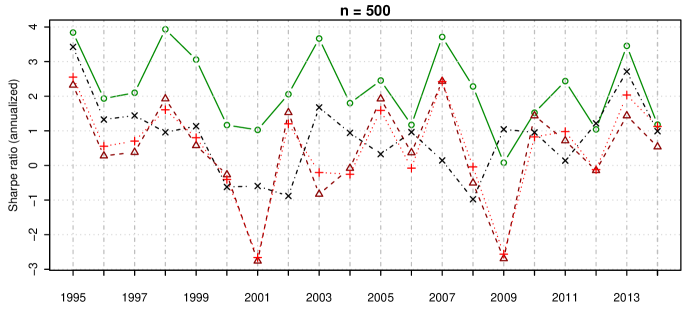

From the the annualized Sharpe ratios presented

in Figure 4 and the balances in

Table 6, it is clear that Face performs significantly better than

the other three.

We remark that although Face, Sam and Fan are all constructed based on Markowitz’s

formula, the difference between them lies in

the way to estimate the covariance matrix of

returns, which appears in Markowitz’s formula.

Both Sam and Fan do not take

into account the dynamic feature of the covariance matrix in their estimation,

but Face does. This is the fundamental reason why Face performs significantly better than Sam and Fan. One may argue that if Sam and Fan used fewer observations in their moving window

to estimate the covariance matrix they would start to take the dynamic feature

into account, potentially improving their performance. However when constructing Face, Sam and Fan,

we tried a variety of , ranging from to , and found Face

always performs better. This suggests that even if Sam and Fan only use the

observations in a carefully chosen moving window, Face still outperforms them.

To have a tangible idea about whether the covariance matrix is dynamic or not,

we plot the estimated intercept and coefficients of ,

and , interpreted as the impact of the factors, for each of the first four components of in Figure 3.

One can see that these coefficients are dynamic rather than constant,

which implies the covariance matrix is also dynamic.

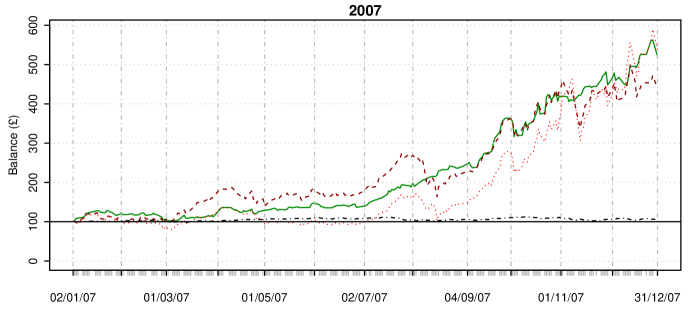

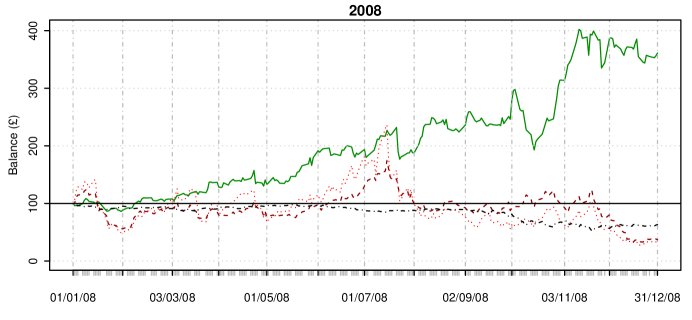

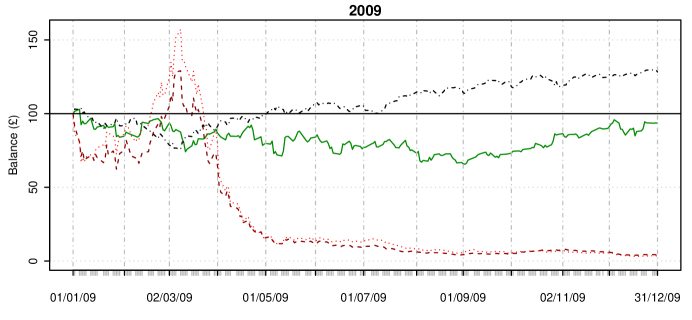

It is interesting to have a closer look at the performances of the four strategies

in the volatile time period 2007-2009 during which the financial crisis

took place. Still assuming an initial balance of 100 pounds at the start of each year,

and using , we plot the balances at the end of each trading day in Figure 5.

During 2007, Face, Sam and Fan all perform reasonably well, with Face slightly better.

The market does not make much profit, and is beaten by the other

three. In 2008, Face continuously does

well whilst the other three do not make profit at all. In 2009, although Face does not do very well

during some time periods, it adapts to the market change quickly and almost

breaks even. The reason that Face can adapt to market change quickly is because it

takes into account the dynamic feature of the covariance matrix of

returns. On the other hand, both Sam and Fan do very poorly, and in fact they

almost lose all their money at the end of the year. In 2009, the market performs best,

but still with very little profit.

Table 4: Description of the 49 industry

portfolios

Industry name

Industry name

1

Agric

Agriculture

26

Guns

Defense

2

Food

Food Products

27

Gold

Precious Metals

3

Soda

Candy & Soda

28

Mines

Industrial Metal Mining

4

Beer

Beer & Liquor

29

Coal

Coal

5

Smoke

Tobacco Products

30

Oil

Petroleum and Natural Gas

6

Toys

Recreation

31

Util

Utilities

7

Fun

Entertainment

32

Telcm

Communication

8

Books

Printing and Publishing

33

PerSv

Personal Services

9

Hshld

Consumer Goods

34

BusSv

Business Services

10

Clths

Apparel

35

Hardw

Computers

11

Hlth

Healthcare

36

Softw

Computer Software

12

MedEq

Medical Equipment

37

Chips

Electronic Equipment

13

Drugs

Pharmaceutical Products

38

LabEq

Measuring and Control Equipment

14

Chems

Chemicals

39

Paper

Business Supplies

15

Rubbr

Rubber and Plastic Products

40

Boxes

Shipping Containers

16

Txtls

Textiles

41

Trans

Transportation

17

BldMt

Construction Materials

42

Whlsl

Wholesale

18

Cnstr

Construction

43

Rtail

Retail

19

Steel

Steel Works Etc

44

Meals

Restaurants, Hotels, Motels

20

FabPr

Fabricated Products

45

Banks

Banking

21

Mach

Machinery

46

Insur

Insurance

22

ElcEq

Electrical Equipment

47

RlEst

Real Estate

23

Autos

Automobiles and Trucks

48

Fin

Trading

24

Aero

Aircraft

49

Other

Almost Nothing

25

Ships

Shipbuilding, Railroad Equipment

\@normalsize

This table gives the labelling and a brief description of industrial sectors which form the 49 Industry Portfolios data set. Precise details of their construction are given on Kenneth French’s website.

Table 5: Description of the Fama and French

factors

Name of

Description

1

Market factor

Return on the market minus the risk-free rate

2

Size factor

Excess returns of small caps over big caps

3

Value factor

Excess returns of value stocks over growth stocks

\@normalsize

This table gives the labelling and a brief description of market, size and value factors from the Fama-French factors data set. Precise details of their construction are given on Kenneth French’s website.

Figure 1: Returns plots of factors and the risk-free rate

Figure 2: Returns plots of , , , and .

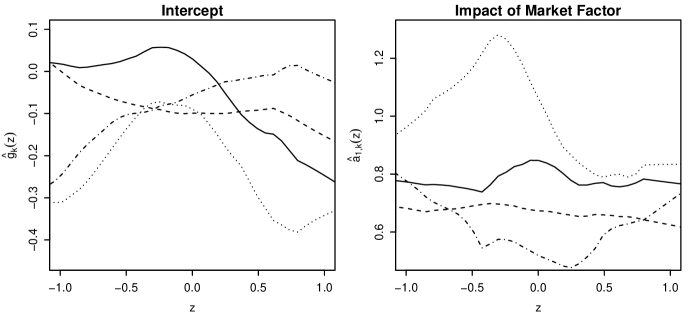

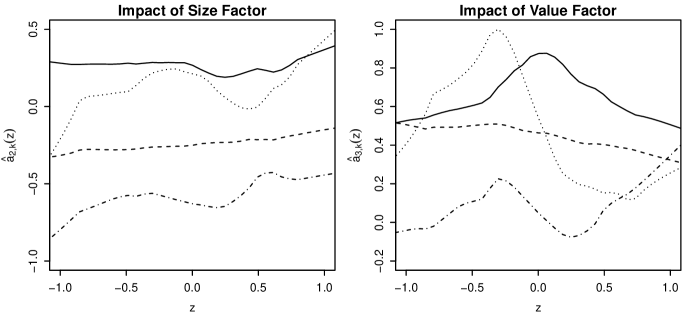

Figure 3: Estimated coefficient functions for industry portfolios 1-4

\@normalsize

This figure shows the estimated intercept and coefficient functions

for the market, size and value factors, for the first four industry portfolios

(Agriculture, Food Products, Candy & Soda, and Beer & Liquor) on the first day of trading.

Figure 4: Annualized Sharpe Ratios

\@normalsize

This figure shows the performance of the four trading strategies (Face, Sam, Fan and Market) in terms of the annualized

Sharpe ratio, using different sample sizes , and .

Figure 5: Trading strategies during the financial crisis

\@normalsize

This figure shows the performance of the four trading strategies (Face, Sam, Fan and Market) using during 2007, 2008 and 2009 in terms of the end of day balances, assuming an initial balance of 100 pounds at the start of each year.

Table 6: Comparison of Balances of Trading Strategies

Year

Market

Face

Sam

Fan

Face

Sam

Fan

Face

Sam

Fan

1995

137

224

164

216

541

277

347

423

380

466

1996

121

159

101

96

184

56

72

212

95

115

1997

131

179

138

155

303

146

207

230

98

127

1998

124

178

79

134

317

330

299

442

340

273

1999

126

121

61

78

260

117

175

329

116

135

2000

88

176

102

133

253

155

120

160

54

42

2001

89

129

53

60

167

49

49

140

10

6

2002

79

164

73

69

222

150

142

196

212

176

2003

132

161

57

97

134

40

45

271

53

75

2004

112

112

67

95

132

55

56

180

75

63

2005

106

179

194

166

184

157

151

265

295

239

2006

115

149

119

121

184

114

95

150

103

76

2007

106

233

185

231

376

305

321

521

440

537

2008

63

143

73

104

203

79

114

361

37

32

2009

128

147

48

66

188

9

5

93

4

3

2010

117

129

109

100

107

169

148

152

220

140

2011

100

177

107

93

192

88

120

283

127

154

2012

116

158

117

96

122

60

83

144

71

68

2013

135

232

200

226

412

180

275

389

225

363

2014

112

158

133

134

152

114

131

162

114

178

\@normalsize

In this table,

the first two columns show the

year and the balance on the final trading day when investing in

the market portfolio.

The balances on the final trading day for Face, Sam and Fan are grouped

according to (columns 3-5), (columns 6-8)

and (columns 9-11).

APPENDIX

Appendix A: Regularity conditions

We state the following assumptions.

Assumption A1. (i) is stationary and ergodic;

(ii) and are independent; (iii) s are bounded with support , that is, .

Let be the probability of a measurable set and

be the expectation of a random variable . The following strong mixing

condition (A2) aims at conducting asymptotic properties of the index estimator

and local linear estimators of nonparametric functions. Let and be the algebras generated

by and , respectively

and define the mixing coefficient

Assumption A2. There exist positive constants and such that for all

Assumption A3. (i) The kernel function is a symmetric density function which is bounded with a bounded support and satisfies the Lipschitz condition; (ii) The density function of is twice differentiable and bounded away from zero on with ; (iii) The density function of is bounded away from zero and twice differentiable in and the joint densities of and for all are bounded.

Assumption A4. and have continuous third derivatives in

Assumption A5. , as , for some symmetric positive definite V such that is bounded away from zero.

For the error process , the following assumptions are stated. Denote the true value for .

Assumption B1. For each , is a strictly stationary GARCH process with with .

Assumption B2. Let for each and . Then, for each the innovations ’s are and absolutely continuous with Lebesgue density being strictly positive in a neighbourhood of zero. Furthermore, , and with defined in Assumption (B1).

Assumption B3. For each , the true value is an interior point of the compact set and for a constant .

Assumption B4. Let and

for . If , and have no common roots, , and .

For the bandwidths , , and the dimension , we require the following assumptions.

Assumption C1. (i) The bandwidth and satisfy and , respectively, with .

Assumption C2. The bandwidth satisfies with .

Assumption C3. The dimension satisfies for some constants and .

Our aim is to estimate . Fan, Fan and Lv (2008) and Fan, Liao and Mincheva (2013) showed that by incorporating the factor structure into the covariance matrix, the resulting estimator has a better convergence rate than the usual sample covariance matrix under the norm . To prove the convergence rate of under the norm , we impose the following assumption:

Assumption C4.

For each , , as for some symmetric positive definite such that is bounded away from zero.

The assumptions are regular. The strong mixing condition in the Assumption (A2) can be relaxed as with a large constant . Assumption (B1) and (B2) guarantee the existence of the th moment of . For simplicity, we do not impose the conditions that ensure the finiteness of the th moment of . For more details, see Lindner (2009). Assumption (C4) requires that the factors should be pervasive, that is, impact every individual time series. It was also imposed in Fan, Fan and Lv (2008) and Fan, Liao and Mincheva (2011).

Appendix B: Proof of Theorem 1 (I)-(III)

For ease of presentation, we give some notation. Define

and

Define to be a compact set with a small .

For a random sequence , for some sequence means that

where is defined in Assumption (C3).

To prove Theorem 1, the following lemma is useful.

Lemma B.1. Assume that Conditions (A1)-(A3) and (C3) in Appendix A hold and for some ,

where is defined in (C3). Then there exists a constant such that

The proof of Lemma B.1 can be followed from the proof of Lemma 6.1 in Fan and Yao (2003). Of course, some constants involved in the proof need to be modified. For instance, we instead use .

Denote and

Let and denote

Denote , and, for ,

,

The following lemma gives the asymptotic representation of .

Lemma B.2. Suppose that Assumption (A1)-(A4) in Appendix A hold. Then we have that

Proof of Lemma B.2. For , denote and . Using a Taylor’s expansion, we obtain that

where

For , denote . Then

(I). Consider the term . Following the proof of Theorem 5.3 in Fan and Yao (2003), we have that there exists a large such that

Let . Note that

and is positive definite.

Therefore, is positive definite almost surely and

(II). Consider the term . By specific matrix calculations, we can show that

Combining (I) and (II), we obtain that

This completes the proof.

The following lemma, Lemma B.3, gives the asymptotic relationship between and , where is the th step estimator based on our procedure in Section 2.

Without loss of generality, we consider .

For each , define

Given , for , denote and

and

Lemma B.3. Suppose that Conditions (A1)-(A4), (B1)-(B4), (C1) and (C3) in Appendix A hold. Then, we have

(A.1)

where

Proof of Lemma B.3. First, consider the term . For denote

We decompose as

(a). Consider the main term . Note that

Analogous to Lemma A.2 of Xia, Tong and Li (2002), it follows that

Similarly, we obtain that

Hence, we approximate the term as

(b). With the help of asymptotic representation of and empirical approximation theories, we can show that

(c). In the similar fashion, we can also show that

Therefore,

which means that

(A.2)

This completes the proof.

Proof of Theorem 1 (I). First, by Lemma B.3, for the th step (), we have

(A.3)

where

a.s. and

a.s., with some large positive constant . Here we take and for sufficiently large .

Note that as , the bandwidth satisfies , , and . We can assume that

Then, if , then and

Note that we can choose the initial estimator which satisfies

for sufficiently large . Therefore,

Taking , it follows that the final estimator satisfies and hence

It also follows from the expression (A.3) that

This completes the proof of Theorem 1(I).

Proof of Theorem 1 (II) and (III). Lemma B.2 tells us that, for ,

where , and

for some constant .

(a). Consider the term . Following the proof of Theorem 5.3 in Fan and Yao (2003), we have that there exists a large such that

Let . Note that

and is positive definite.

Therefore, is positive definite almost surely and

(b). By Lemma B.1, we have

Therefore, combining (a) and (b), there exists a large such that

This completes the proof of Theorem 1(II). Theorem 1(III) can be proven analogously.

Appendix C: Proof of Theorem 1 (IV)

Before we prove Theorem 1(IV), we first give the convergence rate of the difference between the estimated residual and the true residual .

Lemma C.1. Suppose that Assumptions (A1)-(A5), (B1)-(B4) and (C1) and (C3) in Appendix A hold. Then there exists and small such that

Proof of Lemma C.1. For each

Note that

and

Hence, there exists a large constant such that

where is used in the last terms.

For any , we have the following inequality

Take for a large constant . It follows from parts (II) and (III) of Theorem 1 that there exists a constant such that

This completes the proof of Lemma C.1.

Now we are going to prove Theorem 1(IV). Define the quasi log-likelihood function

where is the solution of

For convenience, denote the true value of by .

First, we consider the consistency of . Recall that the observed quasi log likelihood function

where is defined in Section 2. Following the proof of Theorem 7.1 in Francq and Zokoian (2009), we shall establish the following results:

(a1)

as ;

(a2)

If there exists some such that a.s. in , then ;

(a3)

, and if , ;

(a4)

For any , there exists a neighbourhood such that

By the proof of Theorem 7.1 in Francq and Zokoian (2009), we only need to prove (a1). Denote

We have the relationship

The condition (B2) and the compactness of implies that , where means the spectral radius of B.

Furthermore, can be expressed as

Let be the vector obtained by replacing by in , and let be the vector obtained by replacing by

and by the initial values. Then we have

Denote . Then, if ,

As a result, for , we obtain that

for some constant .

We thus have

where . Note that and implies that Then

, and part (a) follows.

Next, we consider the convergence rate of . The proof of this part is based on a standard Taylor expansion of at . Since converges to , which lies in the interior of the parameter space, we thus have

where is between and .

Suppose we have shown that there exist two positive constants and such that

Take and the proof of Theorem 1(IV) follows immediately from (A.5) and (A.6).

Now we prove (A.5) and (A.6). To establish (A.5) and (A.6), it suffices to prove the following five parts:

(b1)

There exists a constant such that

(b2)

There exists a constant such that

(b3)

There exists a constant such that

(b4)

For any , we have

(b5)

For each , there exists a constant and very small constant such that

It is not hard to see that (A.5) can be proved from (b1) and (b2) and (A.6) follows from (b3)-(b5). We now prove them separately.

(b1). It is easy to show that

and

Note that are strictly stationary and mixing with geometric rate. (Also see Lindner (2009).) It follows from Theorem 2 (ii) of Liu, Xiao and Wu (2013) that, there exist positive constants , and such that for all ,

Hence, by taking for a large constant , we obtain that

(b2). Similar to (a1) in this proof, we have that

We also obtain that

As a result, for , the -th component of the difference is bounded above by

Then it follows that, for

By Markov and bulkholder inequalities for martingales, we claim that there exists a constant such that

and

Note that . Hence, it follows that there exists a constant such that

and part (b2) follows.

(b3).

can be expressed as

Note that is positive definite. It suffices to show that, for any constant ,

Similar to (b1), we claim that there exist three positive constants , and such that

Part (b3) follows.

(b4) and (b5). Together with the proof of (c) in Theorem 7.2 of Francq and Zakoian(2011), the proofs of these two parts can be proved in a similar fashion to (b2) and (b3).

Appendix D: Proof of Theorem 2

Define ,

The difference can be decomposed into four parts:

We thus bound by

To bound these terms, we first introduce the following two lemmas.

Lemma D.1. Suppose that Assumptions (A1)-(A5), (B1)-(B4) and (C1)-(C4) in Appendix A hold. Then there exists a large such that

(i)

(ii)

Proof of Lemma D.1. (i) Observe that

where is between and . As a result,

Note that Therefore, part (i) follows from Theorem 1(I) and (III).

(ii) Let and be a bounded function uniformly over . By following the proof of Theorem 5.3 in Fan and Yao (2003), we can see that there exists a large such that

By setting , part (ii) follows.

Lemma D.2. Suppose that Assumptions (A1)-(A5), (B1)-(B4) and (C1) and (C3) in Appendix A hold. Then there exists and small such that

Proof of Lemma D.2. Let be the th element of the matrix B and be the th entry of a vector A. The conditional covariance can be expressed as

where is the matrix obtained by replacing by in and and are defined accordingly.

Note that the true conditional variance

We thus have that

(a) Consider the term and observe that

Then, there exists a constant such that

Since is bounded and , this means that

and consequently, there exists a large constant such that

(b) Consider the term . Denote . By the definition of and B, it is seen that

for small . Note that and the relation for all and . We have that

Hence, by choosing a suitable but small , it follows from Theorem 1(IV) that there exists a large positive constant such that

(c) It is easy to see that

is bounded. Lemma D.2 follows.

Proof of Theorem 2.

(a). Now we bound .

Observe that

Hence, it follows from Lemma D.1 that there exists such that

(b). We bound .

Note that

Hence, we have that

and consequently, by Lemma D.1, there exists such that

(c). We bound . Note that

Hence we obtain from Lemma D.2 that there exists such that

(d). Now we bound .

Note that for two matrix A and B, , and . We have that

Hence, by Lemma D.1 , together with , it follows that there exists such that

Combining (a)-(d), Theorem 2 follows. This completes the proof of Theorem 2.

References

\@normalsize

Bosq, D. (1996). Nonparametric statistics for stochastic processes (Vol. 110). New York: Springer.

Bickel, P. and Levina, E. (2008a). Covariance regularization by

thresholding. Ann. Statist., 36, 2577-2604.

Bickel, P. and Levina, E. (2008b). Regularized estimation of large

covariance matrices. Ann. Statist., 36, 199-227.

Carroll, R. J., Fan, J., Gijbels, I. and Wand, M.P. (1997). Generalized

partially linear single-Index models. Journal of American Statistical

Association, 92, 477-489.

El Karoui, N. (2008). Operator norm consistent estimation of a large

dimensional sparse covariance matrices. Ann. Statist., 36,

2717-2756.

Fama, E. and French, K. (1992).

The cross-section of expected stock returns.

J. Finance47, 427-465.

Fama, E. and French, K. (1993).

Common risk factors in the returns on stocks and bonds.

J. Financ. Econom.33, 3-56.

Fan, J., Fan, Y. and Lv, J. (2008). High dimensional covariance matrix

estimation using a factor model. J. Econometrics, 147, 186-197.

Fan, J., Liao, Y., and Mincheva, M. (2011). High dimensional covariance matrix estimation in approximate factor models. Ann. Statist., 39(6), 3320 - 3356.

Fan, J. and Yao, Q. (2003). Nonlinear Time Series: Nonparametric and Parametric Methods. Springer.

Fan, J., Yao, Q. and Cai, Z. (2003). Adaptive varying-coefficient linear

models. Journal of Royal Statistical Society B, 65, 57-80.

Fan, J. and Zhang, W. (1999). Statistical estimation in varying

coefficient models. Ann. Statist., 27,

1491-1518.

Fan, J. and Zhang, W. (2000). Simultaneous confidence bands and

hypothesis testing in varying-coefficient models. Scandinavian Journal

of Statistics, 27, 715-731.

Francq, C. and Zakoian, J. M. (2011). GARCH models: structure, statistical inference and financial applications. John Wiley & Sons.

Härdle, W., Hall, P. and Ichimura, H. (1993). Optimal smoothing in

single-index models. Ann. Statist., 21, 157-178.

Kong, E. and Xia, Y. (2014). An adaptive composite quantile approach to

dimension reduction. Annals of Statistics, 42, 1657-1688.

Lam, C. and Fan J. (2009). Sparsistency and rates of convergence in large

covariance matrix estimation. Ann. Statist., 37, 4254-4278.

Li, J. and Zhang, W. (2011). A semiparametric threshold model for

censored longitudinal data analysis. Journal of the American Statistical

Association, 106, 685-696.

Lindner, A. M. (2009). Stationarity, mixing, distributional properties and moments of processes. In Handbook of financial time series (pp. 43-69). Springer Berlin Heidelberg.

Liu, W., Xiao, H. and Wu, W. B. (2013). Probability and moment inequalities under dependence. Statist. Sinca., 23(3), 1257-1272.

Markowitz, H.M. (1952). Portfolio selection

J. Finance, 7, 77-91.

Markowitz, H.M. (1959). Portfolio Selection: Efficient Diversification of Investments.

John Wiley & Sons, New Jersey.

Rothman, A., Levina, E. and Zhu, J. (2009). Generalized thresholding of

large covariance matrices. J. Amer. Statist. Assoc., 104, 177-186.

Sun, Y., Yan, H., Zhang, W. and Lu, Z. (2014). A semiparametric spatial

dynamic model. The Annals of Statistics, 42, 700-727.

Sun, Y., Zhang, W. and Tong, H. (2007). Estimation of the covariance

matrix of random effects in longitudinal studies. The Annals of

Statistics, 35, 2795-2814.

Wu, W. B. and Pourahmadi, M. (2003). Nonparametric estimation of large

covariance matrices of longitudinal data. Biometrika, 94, 1a 17.

Xia Y. and Härdle, W. (2006). Semi-parametric estimation of

partially linear single-index models. Journal of Multivariate Analysis,

97, 1162-1184.

Xia, Y. and Li, W.K. (1999). On single-index coefficient regression models.

J. Amer. Statist. Assoc., 94, 1275-1285.

Xia, Y., Tong, H., and Li, W. K. (2002). Single-index volatility models and estimation. Statist. Sinica., 12(3), 785-799.

Yu, Y. and Ruppert, D. (2002). Penalized spline estimation for partially

linear single-index models. Journal of the American Statistical

Association, 97, 1042-1054.

Zhang, W., Fan, J. and Sun, Y. (2009). A semiparametric model for cluster

data. The Annals of Statistics, 37, 2377-2408.

\@normalsize

\@normalsize

\@normalsize

\@normalsize

\@normalsize

\@normalsize