Optimal Static Quadratic Hedging

Abstract

We propose a flexible framework for hedging a contingent claim by holding static positions in vanilla European calls, puts, bonds, and forwards. A model-free expression is derived for the optimal static hedging strategy that minimizes the expected squared hedging error subject to a cost constraint. The optimal hedge involves computing a number of expectations that reflect the dependence among the contingent claim and the hedging assets. We provide a general method for approximating these expectations analytically in a general Markov diffusion market. To illustrate the versatility of our approach, we present several numerical examples, including hedging path-dependent options and options written on a correlated asset.

Keywords: static hedging, leveraged ETF options, substitute hedging

JEL Classification: C52, D81, G11, G13

Mathematics Subject Classification (2010): 91G20, 91G80, 93E20

1 Introduction

Hedging derivatives using a static portfolio of standard financial instruments is a well-known alternative to dynamically hedging with the underlying asset. A static hedging portfolio is easy to construct and requires no continuous monitoring of the underlying or rebalancing over time. As such, static hedging strategies are more robust to significant underlying movements through market turbulence. Furthermore, static hedging portfolios are often useful for establishing no-arbitrage relationships or bounds for exotic derivatives. This idea dates back to Breeden and Litzenberger (1978) for standard options, and has been applied to exotic derivatives, such as basket options (see Hobson et al. (2005)).

A fundamental result on static hedging due to Carr and Madan (1998) shows that any European-style claim written on a single underlying asset can be perfectly replicated by holding a fixed number of bonds and forwards, along with a basket of European calls and puts with the same underlying. The importance of this result is that it provides a model-free, perfect, static replicating strategy. As such, it also gives a no-arbitrage price relationship between the contingent claims and the hedging instruments. Nevertheless, there are also a number of limitations. In particular, the static hedging strategy requires an unbounded continuous strip of European calls and puts and must include the bond and forward in the portfolio. In reality, calls and puts are available only at discrete strikes in a finite interval. This leads to a practical question: how can one optimally construct a static hedge with only a finite number of calls and puts, with or without forwards on the same underlying? More generally, when there are simply not enough traded standard instruments to achieve a perfect static hedge, or when the hedger faces a binding cost constraint, the result of Carr and Madan (1998) provides no direction on how one might proceed.

In this paper, we propose a flexible framework for hedging a contingent claim by choosing static positions in vanilla European calls, puts, bonds, and forwards. We are primarily interested in applications where the perfect static hedge is not available given a set of hedging instruments. To this end, we minimize the expected squared hedging error subject to a cost constraint. Our main result is a model-free expression for the optimal static hedging strategy, which involves computing a number of expectations that reflect the dependence among the contingent claim and the hedging assets. We provide a general method for approximating these expectations analytically in a general incomplete Markov diffusion setting that includes, but is not limited to, the well-known geometric Brownian motion (GBM), Heston CEV and SABR models.

Compared to Carr and Madan (1998), our framework includes a number of additional features. First, we allow for finite upper and lower bounds on the strikes of calls/puts used. Our static portfolio can involve any subset of the hedging assets among bonds, forwards, calls and puts, as opposed to include all of them. This gives the added flexibility to apply to underlying assets on which the forward contracts or some calls/puts are not written. Also, a cost constraint is incorporated into the hedging problem. When binding, this constraint may render a perfect static hedge impossible, and force the hedger to adjust the portfolio to minimize hedging error. While our methodology does not a priori assume the hedge is perfect, it can recover the perfect static hedge when it is available. This allows us to reconcile with the results in Carr and Madan (1998) as a special case of our framework.

In the recent literature, Carr and Wu (2013) work in a single-factor model and propose a finite approximation for the static hedging portfolio whose weights are computed based on the Gauss-Hermite quadrature rule. Also, there is a wealth of static hedging results specifically for barrier options under one-dimensional diffusion models; see Derman et al. (1995); Carr and Chou (1997); Carr et al. (1998); Carr and Lee (2009); Carr and Nadtochiy (2011); Bardos et al. (2010), among others. In contrast to these works, our framework applies to other exotic derivatives and multi-dimensional diffusion models. We illustrate the static hedging strategies in three examples: Asian options, leveraged exchange-traded fund (LETF) options, and options with an illiquid underlying.

The rest of this paper proceeds as follows: In Section 2, we formulate the optimal static hedging problem. In Section 3, we present our main results on hedging a contingent claim with a static portfolio of bonds, forwards and a strip of calls/puts. We also derive the optimal portfolio that consists of a finite set of assets. In both scenarios, we provide explicit, model-free optimal hedges. In Section 4, we discuss a practical method to numerically compute the hedging strategies in a general Markov diffusion setting. Lastly, in Section 5, we implement and illustrate our static hedging strategies in a number of applications.

2 Problem formulation

In the background, we fix a complete filtered probability space , where represents the physical probability measure and the filtration represents the price history of the assets in the market. The market is assumed to be arbitrage-free but may be incomplete. We take as given an equivalent martingale (pricing) measure , inferred from current market derivatives prices. For simplicity, we also assume a zero interest rate and no dividends.

Our static hedging problem involves a group of hedging assets , with being the index set. The number of hedging assets in may be finite, countably infinite or uncountably infinite. The hedging assets could be, for example, bonds, stocks, calls, puts, forwards or other derivative securities. The price of each asset at any time is denoted by .

We define a Static Portfolio as a signed measure such that the static portfolio value at any time is given by

| (2.1) |

In other words, denotes the quantity of asset of type held in the static portfolio. Observe that may be negative, indicating a short position. Note that, while asset prices and the value of the static portfolio change with , the number of units remains constant for all .

Remark 2.1.

We will consider two main examples in this manuscript: (i) hedging with calls/puts with strikes in an interval , and (ii) hedging with a finite number of assets. In setting (i), the signed measure maps . In this case, we will assume that is absolutely continuous with respect to the Lebesgue measure and write where is a function that maps . In setting (ii), the signed measure maps . In this case, we will write where is a function that maps .

We now consider the contingent claim to be hedged at a future time . Its market price at any time is denoted by . If the claim expires at time , then is the terminal payoff. We are primarily interested in situations where perfect static replication is impossible with a given set of hedging assets. Our goal is to minimize the expected squared hedging error of the static portfolio at time subject to a possible cost constraint. We define the optimal static portfolio as the solution of the following optimization problem:

| (2.2) |

That is, is the static portfolio that minimizes the expectation subject to the cost constraint . Note that the expectation in (2.2) is evaluated under the physical probability measure . Clearly, a perfect static hedge ( -a.s.) is possible if and only if . Note that the value of a portfolio at time can be expressed as

| (2.3) |

since all assets are martingales under the pricing measure . Thus, the cost constraint involves computation under the pricing measure .

Naturally, the optimal hedging performance and the corresponding static portfolio depend on the hedging assets available in the market, as well as the underlying price dynamics. Our main objective is twofold: (i) we provide a model-free expression for the optimal static hedging strategy when the hedging assets include bonds, forwards, vanilla European calls and puts on the same underlying; (ii) we discuss the implementation of the hedging strategies for a number of claims under Markovian diffusion dynamics.

3 Methodology & Main Results

In this section, the set of hedging instruments contains a zero-coupon bond , which pays one unit of currency at time , a forward contract written on an underlying asset with payoff , and -maturity European puts and calls written on . We assume there is a put at every strike and call at every strike , with . Let us denote by the payoff the call/put with strike . That is

| (3.1) |

While we observe and in practice and in our numerical examples, our model also allows for and so that we can reconcile with the results in Carr and Madan (1998) (see Sect. 3.1 below).

The terminal value of the static portfolio, composed of bonds, forwards and units of European calls/puts with strikes in the interval , is given by

| (3.2) |

where , and may be either positive or negative (indicating a long or short position).

The cost constraint is given by

| (3.3) |

Note that, since the cost to enter a forward contract at inception is zero, the number of forward contracts in the static portfolio plays no role in the cost constraint.

With given by (3.2), and cost constraint by (3.3), algebraic calculations show that the static hedging problem (2.2) is equivalent to solving for

| (3.4) |

where

| (3.5) | ||||

| (3.6) | ||||

| (3.7) | ||||

| (3.8) |

and we have defined the expectations:

| (3.9) |

In order to state and prove the optimal hedging strategy in this setting, we need the following Lemma. As preparation, it is convenient to introduce the probability density functions of under the physical (i.e., historical) and risk-neutral probability measures

| (3.11) |

Lemma 3.1.

Assume the random variable has a strictly positive density . Recall the function as defined in (LABEL:eq:psi), and let be . Then the solution of the integral equation

| (3.12) |

is given by

| (3.13) |

Proof.

In what follows, let be the anti-derivative of and be the anti-derivative of so that and . Observe from (3.1) that

| (3.14) |

Let us further observe that . Then, equation (3.12) implies

| (3.15) | |||||

| (by (LABEL:eq:psi)) | (3.16) | ||||

| (3.17) | |||||

| (3.18) | |||||

| (3.19) | |||||

| (3.20) | |||||

| (3.21) | |||||

| (integrate by parts) | (3.22) | ||||

| (by (3.14)). | (3.23) | ||||

To obtain (3.13), simply divide (3.23) by , differentiate both sides twice, and use . ∎

Using Lemma 3.1, we can now state and prove the optimal hedging strategy. To this end, we define the function

| (3.24) |

where , , the densities and are defined in (3.11) and the function is given in (LABEL:eq:psi).

Theorem 3.2.

Assume the random variable has a strictly positive density under and a density under . Assume further that . Finally, assume the matrix inverses defined in (3.26) and (LABEL:eq:soln.3) are well defined. Then the optimal strategy that solves the optimal static hedging problem (3.4) is given by

| (3.25) |

where

| (3.26) |

and

| (3.27) |

Proof.

First, we define the Lagrangian associated with (3.4):

| (3.29) | ||||

| (3.30) | ||||

| (3.31) | ||||

| (3.32) |

where acts on functions in . The Karush-Kuhn-Tucker (KKT) conditions, necessary for optimality, are (below, is an arbitrary function satisfying )

| stationarity: | (3.33) | ||||

| (3.34) | |||||

| (3.35) | |||||

| stationarity: | (3.36) | ||||

| (3.37) | |||||

| stationarity: | (3.38) | ||||

| (3.39) | |||||

| comp. slackness: | (3.40) | ||||

| (3.41) | |||||

Note that (3.35) is of the form (3.12) with . Thus, using Lemma 3.1 we obtain

| (3.42) |

Next, noticing that

| (3.43) | ||||

| (3.44) | ||||

| (3.45) | ||||

| (3.46) | ||||

| (3.47) | ||||

| (3.48) | ||||

| (3.49) |

and substituting these expressions into (3.42), we see that in (3.42) coincided with the expression given in (3.24). Next, inserting expression (3.24) into the KKT conditions, (3.37), (3.39), and (3.41), gives the following system of three equations

| (3.50) | ||||

| (3.51) | ||||

| (3.52) |

The above system has two possible solutions corresponding respectively to the cases and . For the case , the triplet is given by (3.26). On the other hand, when , the triplet is given by (LABEL:eq:soln.3). Finally, the KKT conditions are necessary conditions. Since both the objective function and constraint are convex, and the primal problem is feasible (Slater’s condition), the KKT conditions are also sufficient for optimality (see, e.g. Zalinescu (2002, Theorem 2.9.3)). ∎

In Theorem 3.2, the solution corresponds to the unconstrained optimization problem. But if the associated cost is less than , that is,

| (3.53) |

then must coincide with the solution of the constrained optimization problem with initial cost (upper bound) . On the other hand, if the unconstrained optimization problem admits a cost greater than , then the corresponding constrained optimization problem has the solution where, by construction the constraint is binding: .

In fact, from (3.24), the first term in parenthesis in the optimal strategy can be interpreted as a conditional expectation. Heuristically, we have

| (3.54) |

In other words, the number of units of call/put held at strike involves computing the expected terminal claim conditioned on the terminal price of the underlying taking value .

Remark 3.3.

Although we considered hedging with European call/puts on a single asset , the results of this section can be extended to the case where one hedges with European calls/puts on assets . The only difficulty that may arise is in solving the equations that result by imposing the KKT conditions.

3.1 Connection to Carr and Madan (1998)

Let us recall the main result in Carr and Madan (1998): if satisfies , then

| (3.55) |

As such, a contingent claim with payoff can be perfectly hedged by holding bonds, forward contracts and a basket of puts and calls, where the weight of the put/call with strike is . The following corollary proves that equation (3.55) is indeed a special case of our Theorem 3.2.

Corollary 3.4.

Proof.

We must show that , given by (3.56), satisfies (3.50) and (3.51). First, we observe that

| (3.57) | ||||

| (3.58) |

Thus, using , we see from (3.24) that

| (3.59) |

Next, dividing equation (3.50) by two and rearranging terms we find

| (3.60) |

This equation will clearly be satisfied if and . To see this, simply take the expectation of (3.55). Next, dividing equation (3.51) by two, and rearranging terms we have

| (3.61) |

This equation will also be satisfied if and . To see this, simply multiply (3.55) by and take an expectation. ∎

3.2 Connection to static hedging with finite assets

Our framework can be related to static hedging with a finite number of assets. In this case, the set has a finite number units of hedging assets, and the static portfolio value can be expressed as a finite sum:

| (3.62) |

This is indeed the discrete version of the static portfolio in (2.1).

Assumption 3.5.

We assume that the random variables are elements of and are linearly independent. Stated in financial terms, this assumption simply requires that none of the hedging instruments is redundant, as defined in (Duffie, 2001, Chaper 2).

With given by (3.62), a direct computation shows that the static hedging problem amounts to determining the optimal strategy

| (3.63) |

where and are given by

| (3.64) |

and

| (3.65) |

Compared to the “continuous” case in (3.2)–(LABEL:eq:psi), the objective function again involves the expectations of products of payoffs, namely, and . Note that in this discrete case we can consider general claims, not limited to forwards, puts, and calls, and continue to derive explicitly the optimal static portfolio.

Proposition 3.6.

We provide a proof in Appendix A. The vector corresponds to the optimal strategy without a cost constraint. If the unconstrained optimization problem has a cost , then is the optimal strategy for the constrained optimization problem. On the other hand, if the unconstrained optimization problem has a cost , then the solution of the constrained optimization problem is given by which, by construction, has a cost equal to , that is, . Lastly, we emphasize that the optimal static hedging strategy with discrete strikes can be quite different than the optimal strategy when continuous strikes available but implemented at discretized strikes. We will visualize the difference in Section 5.1.

Remark 3.7 (Relation to Markowitz mean-variance portfolio optimization).

In his seminal work, Markowitz (1952) solves the problem of minimizing portfolio variance for a given level of expected return. Mathematically, the minimization problem is given by

| (3.67) |

where are the portfolio weights to be found, and are, respectively, the covariance matrix and expected returns of a group of assets, and is the minimum level of expected return. Interestingly, the portfolio optimization problem (3.67) has the same structure as the static hedging problem (3.63), which, in matrix notation, is given by

| (3.68) |

Though, clearly, the economic interpretations of (3.67) and (3.68) are distinct.

4 Implementation Under a Markov Diffusion Framework

Thus far, we have made no assumption about the dynamics of the underlying . To illustrate the performance of our static hedging strategies, we now present the calculations and numerical implementation under a general incomplete Markov diffusion market. The analytic approximations we present below are useful when the claim to be hedged is European-style. Specifically, the payoff may be some function of the final value of a -dimensional Markov diffusion . Note, by allowing components of to be the quadratic variation or running average of other components, our definition of European-style claims allows for path dependence and includes both Asian options and options on variance/volatility (e.g., a variance swap). Extending the approximations to cases where is a barrier-style claim or look-back option is not trivial and is well beyond the scope of this paper.

Let be a Markov diffusion satisfying the following stochastic differential equations (SDEs) under and , respectively

| (under ) | (4.1) | ||||

| (under ) | (4.2) |

Here, (resp. ) is an -dimensional Brownian motion under (resp. ), and the functions , and map

| (4.3) |

Let us suppose that the terminal values of the hedging assets from Section 3.2, the stock from Section 3 and the claim to be hedged are given by

| (4.4) |

where the function maps and for each the function maps . Since is traded, in order to preclude arbitrage, we must have

| (4.5) |

In order to implement the optimal hedging strategies (Theorems 3.2 and 3.6), we must compute the expectations defined in equations (LABEL:eq:psi) and (3.65). For general dynamics of the form (4.1)-(4.2), closed-form expressions for these expectations are not available. Moreover, computing these expectations via Monte Carlo simulation is not practical, since, in the case of Theorem 3.2, the expectations appear in the integrands of various integrals. As such, we provide here a method for obtaining analytic approximations the expectations in (LABEL:eq:psi) and (3.65). The methods that we describe below were developed first formally in a scalar setting in Pagliarani and Pascucci (2012) and later extended to multiple dimensions with rigorous error bounds in Lorig et al. (2015b) and Lorig et al. (2015a). Here, we give a concise review of these methods and also provide some extensions, which are needed to implement Theorems 3.2 and 3.6.

We fix a time and consider an expectation of the general form

| (4.6) |

Under mild conditions on the drift , diffusion coefficient and terminal data the function satisfies the Kolmogorov backward equation. Omitting -dependence below to ease notation, we have

| (4.7) |

where is the generator of under probability measure . Explicitly, the operator is given by

| (4.8) |

where we have introduced standard multi-index notation

| (4.9) |

Remark 4.1.

To compute , one would simply replace in (4.7) with

| (4.10) |

Our goal is to find an approximate solution to PDE (4.7), thereby obtaining an approximation for the expectation (4.6). To this end, we expand each coefficient as a Taylor series about a fixed point :

| (4.11) |

Here, we assume implicitly that the coefficients are analytic. However, we will see in Definition 4.2 that the th-order approximation of requires only that the coefficients be . Combining (4.8) with (4.11) we see that the operator can be written as

| (4.12) |

Inserting (4.12) into PDE (4.7) we have

| (4.13) |

and, hence, by Duhamel’s principle

| (4.14) |

where is the semigroup generated by . Explicitly, we have

| (4.15) |

where is a Gaussian kernel whose mean vector and covariance matrix are

| (4.16) | ||||

| (4.17) |

Observing that appears on both the left and right-hand side of (4.14), we iterate this expression to obtain

| (4.18) | ||||

| (4.19) | ||||

| (4.20) | ||||

| (4.21) | ||||

| (4.22) |

where, in the second equality, we have used the fact that is an infinite sum and we have partitioned on the sum of the subscripts of the operators. Expression (4.21) motivates the following definition.

Definition 4.2.

Let be the unique classical solution of (4.7). Assume the coefficients are for all . Then, the th order approximation of , denoted by , is defined as

| (4.23) |

where is the semigroup generated by and

| (4.24) | ||||

| (4.25) |

The th order approximation of the transition density is obtained by setting the terminal data equal to a -dimensional Dirac mass .

Recall from (4.15) that the semigroup operators are integral operators. Thus, as written, expression (4.25) is difficult to evaluate. The following Theorem shows the th order term can be easily computed as a differential operator acting on .

Theorem 4.3.

Theorem 4.3 provides provides a method of approximating the expectations in (LABEL:eq:psi) and (3.65) analytically. The expectations in (3.65) are sufficient to implement Theorem 3.6, which can be used compute optimal static hedges with a discrete number of hedging assets.

In order to compute optimal hedges in the case with a strip of calls/puts through Theorem 3.2, in addition to computing expectations in (LABEL:eq:psi), we need numerically evaluate

| and | (4.28) |

where and are the densities of under and , respectively, and is defined in (LABEL:eq:psi). To this end, we compute

| (4.29) |

where and are the densities of under and , respectively. We also have

| (4.30) | ||||||

| (4.31) | ||||||

| (4.32) | ||||||

| (4.33) | ||||||

where is the density of under . Note that (4.33) is in fact (see (3.54)).

4.1 Accuracy results

In order to establish the accuracy of approximation given in Definition 4.2, we must make a few assumptions about the coefficients .

Assumption 4.4.

There exists a positive constant such that the following holds:

-

1.

Uniform ellipticity: , ,

-

2.

Regularity and boundedness: the coefficients and partial derivatives with are bounded by for all .

We begin by establishing the accuracy of the approximation .

Theorem 4.5.

Let Assumption 4.4 hold and fix . Suppose the terminal datum is at most exponentially growing and for some , where denotes the space of functions that are not necessarily continuous. Then we have

| (4.34) |

where is a positive constant the depends on , , the terminal datum and .

Proof.

See (Lorig et al., 2015a, Theorem 3.10 and Remark 3.11). ∎

Next, we will derive an approximation for , which is needed to compute (3.24), and establish the accuracy of this approximation. To this end, let us define

| (4.35) |

Since we clearly have

| (4.36) |

Note that the density of can be obtained by differentiating twice with respect to strike

| (4.37) | ||||

| (4.38) |

Thus, we define , the th order approximation of , as

| (4.39) |

The following theorem gives the accuracy of

Theorem 4.6.

Let Assumption 4.4 hold and fix . Then we have

| (4.40) |

where is a positive constant the depends on , , and .

Proof.

From (4.38) and (4.39), we have

| (4.41) | |||

| (4.42) | |||

| (4.43) |

where the coefficients are integers whose precise value is not important. Next, by Theorem 4.4 of Pagliarani and Pascucci (2015), we have

| (4.44) |

where the constant depends on , , and . The accuracy result (4.40) follows directly from (4.43) and (4.44). ∎

A similar analysis yields the same order of accuracy for the approximations of and . For brevity, we do not repeat the computations here.

5 Examples

In this section, we compute the optimal static hedges, along with sensitivity analysis, in a variety of practical applications. The resulting static portfolio payoff profiles are also shown to demonstrate the effectiveness of our methodology.

5.1 Hedging an option with options on a correlated underlying

In our first example, we consider two correlated underlyings and , where the log-price pair satisfies

| (under ) | (5.1) | |||

| (under ) | (5.2) |

We assume that is traded and is therefore a martingale under . As such, we must have . Although we do not assume it, if is traded, it too must be a martingale under and in this case the drift must satisfy .

Suppose now we have sold a European call written on with maturity date and strike price . This is the claim to hedge, so we denote

| (5.3) |

We wish to statically hedge this option with bonds, forward contracts and European calls/puts written not on but on . This situation may arise for a variety of reasons. First, it could be that neither nor options on are liquidly traded, or the options are traded at very few strikes, as is common in the commodity markets. Second, even if is traded, an investor may be prohibited from trading and options written on for legal reasons. Third, the market for options on may simply have superior liquidity as compared to . For instance, one may resort to forwards and/or options on the S&P500 index in order to hedge an option written on a component or non-component stock.

Continuum of Strikes

Let us recall the setting of Section 3, in which the bond, forward on , and calls/puts are available at every strike (see (3.1)). To compute the optimal hedging strategy using Theorem 3.2 we require expressions for the expectations in (LABEL:eq:psi). For the current application, they are given by

| (5.4) | ||||||||

| (5.5) | ||||||||

| (5.6) |

where is defined in (3.1) and is defined in (5.3). For certain model dynamics, these expectations can be computed explicitly. In cases in which the expectations cannot be explicitly computed, analytic approximations can be obtained using Theorem 4.3.

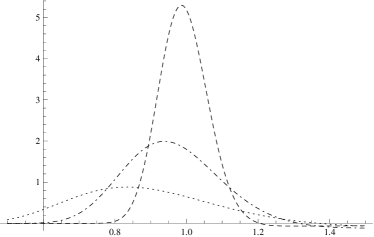

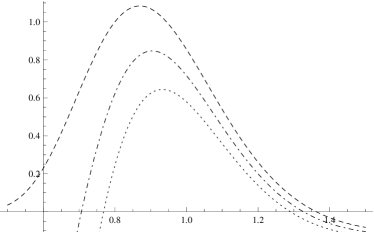

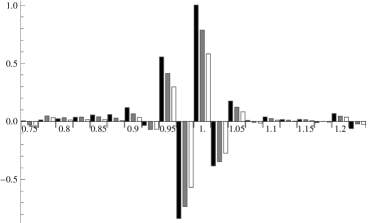

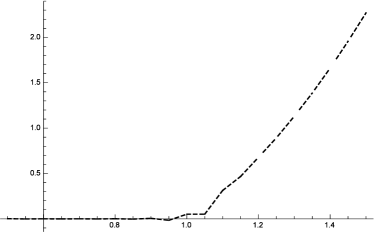

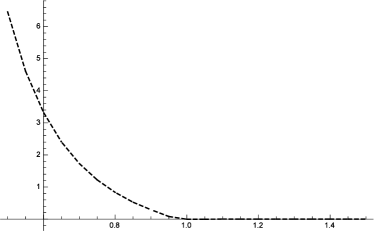

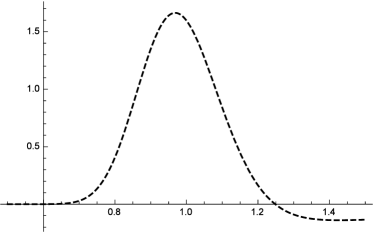

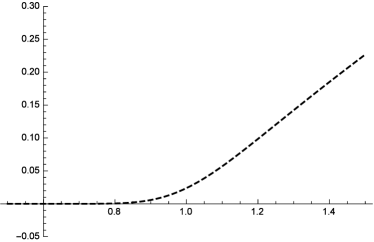

In Figure 1 we consider the case where and are correlated arithmetic Brownian motions. We assume that both and are traded assets, which requires that and . We illustrate the optimal static portfolio , and examine the effects of the correlation and the cost constraint . In addition to plotting the units of calls/puts held, that is, as a function of strike , we also plot the static portfolio’s terminal value

| (5.7) |

as a function , and compare this portfolio profile against the payoff .

From Figure 1 we see two clear effects as the correlation increases to 1. First, the density of calls/puts in the optimal hedging portfolio becomes more concentrated near . Second, the payoff function more closely matches the payoff function of the option to be hedged. This is intuitively what one would expect since, if and are perfectly correlated (i.e., ), then the two assets are identical, i.e. , so holding the call on with strike will be the optimal and perfect hedge. Somewhat less intuitive is the effect of the cost constraint on the optimal hedging portfolio . In Figure 1 we see that, as the cost constraint becomes more severe (i.e., as decreases), the optimal static hedging strategy is to sell more puts and calls with strikes far away from . Intuitively, selling those options helps reduce the hedging cost in order to satisfy the cost constraint while not increasing the hedging errors around .

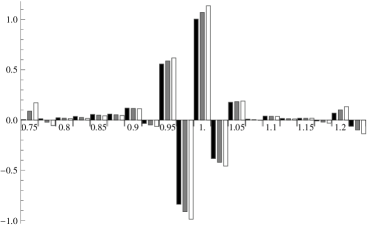

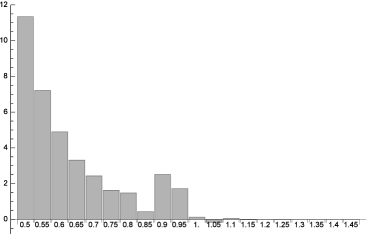

Hedging with discrete strikes

As in Section 3.2, we now assume that European-style calls/puts are available only at a discrete strikes . We set and for . In order to compute the optimal static portfolio using Theorem 3.6, we compute the expectations in (3.65), which are given by

| (5.8) | ||||||||

| (5.9) | ||||||||

| (5.10) |

For certain model dynamics, the above expectations can be computed explicitly. In cases in which the above expectations cannot be computed explicitly, they can be approximated analytically in a Markovian framework using Theorem 4.3.

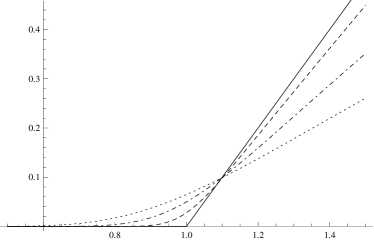

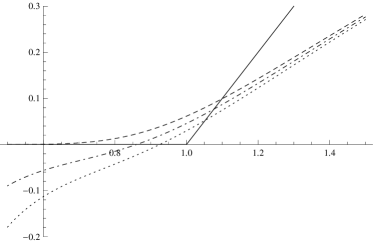

As in the previous case with continuum of strikes, we assume that the log prices and are correlated arithmetic Brownian motions. In Figure 2 (bottom), we show the optimal static portfolio weights and illustrate the effect of the correlation parameter and cost constraint . In addition, we plot the static portfolio profile (terminal value as a function of ), denoted by

| (5.11) |

As the correlation increases from 0.5 to 0.9, we see that the portfolio profile matches more closely the claim payoff , especially for large and small values of . However, in contrast to the case with continuous strikes, a perfect match is not possible due to the availability of only a limited number of strikes. On the other hand, the effect of the cost constraint on is less straightforward. Specifically, with a more stringent cost constraint (i.e., ), the optimal static portfolio tends to have a negative payoff for low strikes and a positive and increasing payoff for high strikes, resulting in a higher quadratic hedging error. Furthermore, the resulting portfolio profile is lower for all realization of when the allowed portfolio cost is reduced.

Moreover, under all conditions we observe that the magnitude of is greatest for strikes near . However, due to the fact that we have a discrete number of hedging assets, the sign of oscillates as a function of strike. In contrast, when using the optimal static strategy derived from the model with a continuous strip of calls/puts, the sign of the optimal density does not oscillate. This has important practical consequences. From the hedger’s point of view, it is far easier to take only or mostly long positions, rather than taking alternating long and short positions in options. Therefore, even though there is a finite number of strikes in practice, one can also adopt a discretized version of the optimal continuous density in Figure 1 (top), as an alternative to the optimal discrete strategy in Figure 2 (top). Hence, by discretizing the optimal static hedging strategy in Theorem 3.2 (which assumes options trade with strikes in a continuum) one obtains a useful alternative to the strategy derived from assuming discrete strikes from the onset.

5.2 Hedging an LETF option with options on the reference

An exchange traded fund (ETF) is typically designed to track a reference index, denoted by . The reference index dynamics under under the physical measure and pricing measure are given by two-dimensional SDE (5.1), where the second component now represents the driver of volatility rather than a traded asset. Now, we introduce , a leveraged exchange traded fund (LETF). An LETF is a managed portfolio that returns a pre-specified multiple of the daily return of the reference index . To illustrate this in the simplest form, with zero management fee, interest and dividend rates, the dynamics of an LETF with leverage ratio are related as follows:

| (5.12) |

The most common values for the leverage ratio are . As Avellaneda and Zhang (2010) show, the value of the LETF at any time is given by

| (5.13) | ||||

| (5.14) |

where is the quadratic variation of over the interval . Observe that the value of depends not only on the terminal value , but also on the integrated variance (quadratic variation) of . Thus, the value of depends on the entire path of .

Options on LETFs of different leverage ratios are also widely traded on the Chicago Board Options Exchange (CBOE). The pricing of these options under stochastic volatility models has been recently studied in Leung et al. (2014); Leung and Sircar (2015). In practice, significantly fewer strikes are available for LETF options, some with wider bid-ask spreads, as compared to the nonleveraged counterparts. This phenomenon is partly due to the difficulty to hedge LETF options, which in turn impedes active market making that typically narrows bid-ask spreads. Hence, we consider the static hedging problem for an LETF option using options on the reference index (nonleveraged underlying). With the optimal static portfolio, we obtain a candidate practical hedging strategy for LETF options, and can also illustrate how the LETF option price and payoff relate to those of the vanilla options

A call option written on the LETF with leverage ratio has the terminal payoff

| (5.15) |

We wish to statically hedge this option using a bond, and European call and put options written on the reference index . It is also possible to consider hedging an LETF option by dynamically trading the reference index provided it is liquidly traded, though this is beyond the scope of this paper.

Hedging with discrete strikes and a bond

We consider the setting of Section 3.2. Specifically, we assume that European-style calls/puts are available at a discrete number of strikes . We set and for we set . For simplicity, we consider the case of no cost constraints. In order to obtain the optimal static portfolio using Theorem 3.6, the expectations in (3.65) we must compute are

| (5.16) |

Remark 5.1.

If has constant drift and volatility , then

| (5.17) |

Also, the expectations in (5.16) can be computed explicitly. In fact, since is deterministic, we see from (5.13) that an option on is simply a power option on , which is also perfectly replicable with a static portfolio with a bond, a forward and calls/puts on at all strikes without cost constraint.

We wish to consider an incomplete market model under which is stochastic. This leads us to work with the Heston (1993) model:

| (5.18) |

While the joint density of is not available, the joint characteristic moment-generating function of is well known. We define

| (5.19) |

An explicit expression for is given in (Drimus, 2012, Proposition 2.1). For a suitable function we have

| (5.20) | ||||

| (5.21) |

where is a positive constant chosen to the right of any singularities in the integrand of (5.20). Note, in certain cases, one may need to fix an imaginary component of in (5.21) in order for the Fourier-Laplace transform to converge. For example, consider the function

| (5.22) |

Inserting (5.22) into (5.21) and integrating yield

| (5.23) |

The Fourier-Laplace transform allows us to compute the Fourier-Laplace transforms of

| and | (5.24) |

since these functions share the same form as in (5.22). Inserting (5.23) into (5.20) and integrating, one can compute numerically the values of the expectations appearing in (5.16).

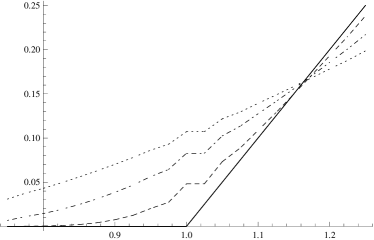

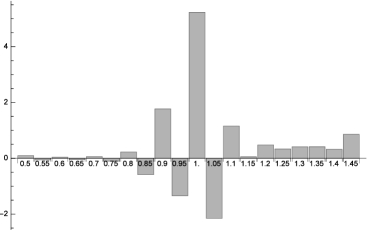

Figure 3 illustrates the optimal static portfolio weights for both the triple long LETF () and the triple short LETF (), as well as the portfolio profile given by (5.11). If the integrated variance is very small, then we see from (5.13) that . Thus, if is positive, then moves in the direction of and if , then moves in the direction opposite of . Since the claim to be hedged has a positive payoff if and only if , we expect that, for , the optimal hedge would be to hold calls on with strikes above , and for the optimal hedge would be to hold puts on with strikes below . And, indeed, this is precisely what we observe in Figure 3. Moreover, we notice that the hedging portfolio for the -LETF call involves many long positions in puts on the reference index. This is not surprising given the fact that calls on the -LETF and puts on the reference index are all bearish positions. On the other hand, for hedging the -LETF call, the static portfolio weights exhibit oscillating behavior with more long positions in OTM calls. In both cases, the weights are assigned heavily on options that realize a positive payoff when the LETF options do also.

5.3 Hedging a geometric Asian call with European options

As our last example, we consider static hedging another path-dependent derivative. First, let where

| (5.25) |

That is, has local volatility dynamics. We fix a time and introduce process where satisfies

| (5.26) |

Note that is the time average of over the interval . We consider a geometric Asian call with the terminal payoff:

| (5.27) |

Continuum of Strikes and a bond

Following the setting of Section 3 without the cost constraint, we construct a static portfolio using calls/puts available at every strike , plus bonds, if needed. In this example, the expectations that need to be computed in order to implement Theorem 3.2 are

| (5.28) | ||||||||

| (5.29) |

along with the ratio that appears in (LABEL:eq:soln.3).

If the drift and volatility of are constant, then is jointly Gaussian. The mean vector and covariance matrix of are

| (5.30) |

The approximate correlation is . In fact, all the expectations in (5.28) can be computed explicitly. Since we have already computed optimal hedges for correlated Gaussian random variables in Section 5.1, we shall consider a sophisticated model next.

We now suppose that admits the Constant Elasticity of Variance (CEV) dynamics

| (5.31) |

The density of is known in the CEV setting due to results from Cox (1975), though the joint density of has to be computed numerically. We follow the approximation methods outlined in Section 4 to compute the optimal static hedges.

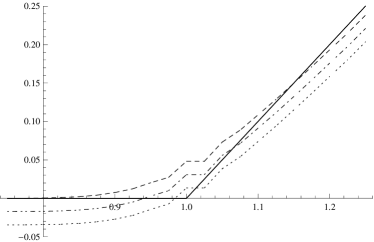

In Figure 4, we plot the optimal unconstrained static hedging portfolio as a function of . Notice that the static portfolio includes most options around the strike of the Asian call. Moreover, most of the options are held long, except for the small short positions taken for the deep OTM calls (for in the figure). The profile resembles that in the case of hedging with options on a correlated asset in Figure 1 (top left). This is not surprising given that and its geometric average are positively but not perfectly correlated. We also plot the hedging portfolio terminal value as a function of (see (5.7)), and it appears to be increasing convex, similar to a call payoff as expected. However, the slope of the payoff is significantly less than even for large because the Asian call payoff depends not only on but the average of over time.

6 Conclusion

We have considered the static hedging problem using a bond, a forward and a (possibly semi-infinite) strip of calls/puts, and a subset of these instruments. The optimal strategy is derived without assuming dynamics of the underlying asset(s), and is shown to reconcile with the result of Carr and Madan (1998), which is a special case of our framework. A useful connection is established between the optimal static hedging strategy with discrete option strikes and our proposed continuous-strike strategy implemented over discrete strikes, and we show the contrasting behaviors of these strategies. The numerical implementation of the optimal strategy is conducted in a general incomplete Markov diffusion market, with examples of exotic/path-dependent claims such as options on a non-traded asset, as well as Asian and LETF options.

For future research, one direction is to generlize our results for static hedges up to a random time, rather than a fixed terminal time considered here. This extension will provide new alternative ways to statically hedge claims such as barrier options and American options. In other related directions, one can consider semi-static hedges with finite number of rebalancing (see Carr and Wu (2013)), or incorporate static positions into portfolio optimization problems; see, for example, İlhan and Sircar (2005); Leung and Sircar (2009).

Acknowledgments

The authors are grateful to Peter Carr and Ronnie Sircar for a number of helpful discussions. Additionally, the authors would like to thank two anonymous referees whose comments improved the quality and readability of this manuscript.

Appendix A Proof of Proposition 3.6

Optimization problem (3.63) is a finite-dimensional quadratic programming problem with linear constraints. By Assumption 3.5, the matrix is positive definite, and thus, invertible. Define the Lagrangian

| (A.1) |

The Karush-Kuhn-Tucker (KKT) conditions, which are necessary and sufficient for this convex optimization (see Boyd and Vandenberghe (2004)), are

| (A.2) | |||||

| (A.3) | |||||

| (A.4) | |||||

| (A.5) | |||||

| (A.6) | |||||

In matrix notation, equation (A.4) becomes

| (A.7) | |||||||

| (A.8) | |||||||

Inserting expression (A.8) for into (A.6) we obtain

| (A.9) |

Equation (A.9) has two solutions:

| and | (A.10) |

References

- Avellaneda and Zhang (2010) Avellaneda, M. and S. Zhang (2010). Path-dependence of leveraged ETF returns. SIAM Journal of Financial Mathematics 1, 586–603.

- Bardos et al. (2010) Bardos, C., R. Douady, and A. Fursikov (2010, 3). Static hedging of barrier options with a smile: An inverse problem. ESAIM: Control, Optimisation and Calculus of Variations 8, 127–142.

- Boyd and Vandenberghe (2004) Boyd, S. and L. Vandenberghe (2004). Convex Optimization. Cambridge University Press.

- Breeden and Litzenberger (1978) Breeden, D. T. and R. H. Litzenberger (1978). Prices of state-contingent claims implicit in option prices. The Journal of Business 51(4), 621–651.

- Carr and Chou (1997) Carr, P. and A. Chou (1997). Breaking barriers. Risk 10, 139–146.

- Carr et al. (1998) Carr, P., K. Ellis, and V. Gupta (1998). Static hedging of exotic options. Journal of Finance 53(3), 1165–1190.

- Carr and Lee (2009) Carr, P. and R. Lee (2009). Put-call symmetry: Extensions and applications. Mathematical Finance 19(4), 523–560.

- Carr and Madan (1998) Carr, P. and D. Madan (1998). Towards a theory of volatility trading. In R. Jarrow (Ed.), Volatility: new estimation techniques for pricing derivatives, pp. 417–427. Risk Books.

- Carr and Nadtochiy (2011) Carr, P. and S. Nadtochiy (2011). Static hedging under time-homogeneous diffusions. SIAM Journal on Financial Mathematics 2(1), 794–838.

- Carr and Wu (2013) Carr, P. and L. Wu (2013). Static hedging of standard options. Journal of Financial Econometrics (published online), 1–44.

- Cox (1975) Cox, J. (1975). Notes on option pricing I: Constant elasticity of diffusions. Unpublished draft, Stanford University. A revised version of the paper was later published by the Journal of Portfolio Management in 1996.

- Derman et al. (1995) Derman, E., D. Ergener, and I. Kani (1995). Static options replication. Journal of Derivatives 2, 78–85.

- Drimus (2012) Drimus, G. G. (2012). Options on realized variance by transform methods: a non-affine stochastic volatility model. Quant. Finance 12(11), 1679–1694.

- Duffie (2001) Duffie, D. (2001). Dynamic Asset Pricing Theory (3 ed.). Princeton University Press.

- Heston (1993) Heston, S. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6(2), 327–343.

- Hobson et al. (2005) Hobson, D., P. Laurence, and T.-H. Wang (2005). Static-arbitrage upper bounds for the prices of basket options. Quantitative Finance 5(4), 329–342.

- İlhan and Sircar (2005) İlhan, A. and R. Sircar (2005). Optimal static-dynamic hedges for barrier options. Mathematical Finance 16, 359–385.

- Leung et al. (2014) Leung, T., M. Lorig, and A. Pascucci (2014). Leverage ETF implied volatilities from ETF dynamics. ArXiv preprint arXiv:1404.6792.

- Leung and Sircar (2009) Leung, T. and R. Sircar (2009). Exponential hedging with optimal stopping and application to ESO valuation. SIAM Journal of Control and Optimization 48(3), 1422–1451.

- Leung and Sircar (2015) Leung, T. and R. Sircar (2015). Implied volatility of leveraged ETF options. Applied Mathematical Finance 22(2), 162–188.

- Lorig et al. (2015a) Lorig, M., S. Pagliarani, and A. Pascucci (2015a). Analytical expansions for parabolic equations. SIAM Journal on Applied Mathematics 75, 468––491.

- Lorig et al. (2015b) Lorig, M., S. Pagliarani, and A. Pascucci (2015b). Explicit implied volatilities for multifactor local-stochastic volatility models. Mathematical Finance. To appear.

- Markowitz (1952) Markowitz, H. (1952). Portfolio selection. The Journal of Finance 7(1), 77–91.

- Pagliarani and Pascucci (2012) Pagliarani, S. and A. Pascucci (2012). Analytical approximation of the transition density in a local volatility model. Cent. Eur. J. Math. 10(1), 250–270.

- Pagliarani and Pascucci (2015) Pagliarani, S. and A. Pascucci (2015). The parabolic Taylor formula of the implied volatility. Available on SSRN. http://ssrn.com/abstract=2673028.

- Zalinescu (2002) Zalinescu, C. (2002). Convex Analysis in General Vector Spaces. World Scientific.

| Effect of correlation | Effect of cost constraint |

|

|

|

|

| vs | vs |

| Effect of correlation | Effect of cost constraint |

|

|

|

|

| vs | vs |

|

|

|

|

|

|