arrows \pgfarrowsdeclarearcsqarcsq \pgflinewidth\pgfarrowsleftextend-4\pgflinewidth \pgfarrowsrightextend.5\pgflinewidth \pgflinewidth\pgfsetdash0pt \pgfsetroundjoin\pgfsetroundcap\pgfpathmoveto\pgfpoint00 \pgfpatharc-90-1404 \pgfusepathqstroke\pgfpathmoveto\pgfpointorigin \pgfpatharc901404 \pgfusepathqstroke

backShift: Learning causal cyclic graphs from unknown shift interventions

Abstract

We propose a simple method to learn linear causal cyclic models in the presence of latent variables. The method relies on equilibrium data of the model recorded under a specific kind of interventions (“shift interventions”). The location and strength of these interventions do not have to be known and can be estimated from the data. Our method, called backShift, only uses second moments of the data and performs simple joint matrix diagonalization, applied to differences between covariance matrices. We give a sufficient and necessary condition for identifiability of the system, which is fulfilled almost surely under some quite general assumptions if and only if there are at least three distinct experimental settings, one of which can be pure observational data. We demonstrate the performance on some simulated data and applications in flow cytometry and financial time series.

1 Introduction

Discovering causal effects is a fundamentally important yet very challenging task in various disciplines, from public health research and sociological studies, economics to many applications in the life sciences. There has been much progress on learning acyclic graphs in the context of structural equation models [1], including methods that learn from observational data alone under a faithfulness assumption [2, 3, 4, 5], exploiting non-Gaussianity of the data [6, 7] or non-linearities [8]. Feedbacks are prevalent in most applications, and we are interested in the setting of [9], where we observe the equilibrium data of a model that is characterized by a set of linear relations

| (1) |

where is a random vector and is the connectivity matrix with zeros on the diagonal (no self-loops). Allowing for self-loops would lead to an identifiability problem, independent of the method. See Section B in the Appendix for more details on this setting. The graph corresponding to has nodes and an edge from node to node if and only if . The error terms are -dimensional random variables with mean 0 and positive semi-definite covariance matrix . We do not assume that is a diagonal matrix which allows the existence of latent variables.

The solutions to (1) can be thought of as the deterministic equilibrium solutions (conditional on the noise term) of a dynamic model governed by first-order difference equations with matrix in the sense of [10]. For well-defined equilibrium solutions of (1), we need that is invertible. Usually we also want (1) to converge to an equilibrium when iterating as or in other words . This condition is equivalent to the spectral radius of being strictly smaller than one [11]. We will make an assumption on cyclic graphs that restricts the strength of the feedback. Specifically, let a cycle of length be given by and for . We define the cycle-product of a matrix to be the maximum over cycles of all lengths of the path-products

| (2) |

The cycle-product is clearly zero for acyclic graphs. We will assume the cycle-product to be strictly smaller than one for identifiability results, see Assumption (A) below. The most interesting graphs are those for which and for which the spectral radius of is strictly smaller than one. Note that these two conditions are identical as long as the cycles in the graph do not intersect, i.e., there is no node that is part of two cycles (for example if there is at most one cycle in the graph). If cycles do intersect, we can have models for which either (i) but the spectral radius is larger than one or (ii) but the spectral radius is strictly smaller than one. Models in situation (ii) are not stable in the sense that the iterations will not converge under interventions. We can for example block all but one cycle. If this one single unblocked cycle has a cycle-product larger than 1 (and there is such a cycle in the graph if ), then the solutions of the iteration are not stable111The blocking of all but one cycle can be achieved by do-interventions on appropriate variables under the following condition: for every pair of cycles in the graph, the variables in one cycle cannot be a subset of the variables in the other cycle. Otherwise the blocking could be achieved by deletion of appropriate edges.. Models in situation (i) are not stable either, even in the absence of interventions. We can still in theory obtain the now instable equilibrium solutions to (1) as and the theory below applies to these instable equilibrium solutions. However, such instable equilibrium solutions are arguably of little practical interest. In summary: all interesting feedback models that are stable under interventions satisfy both and have a spectral radius strictly smaller than one. We will just assume for the following results.

It is impossible to learn the structure of this model from observational data alone without making further assumptions. The Lingam approach has been extended in [11] to cyclic models, exploiting a possible non-Gaussianity of the data. Using both experimental and interventional data, [12, 9] could show identifiability of the connectivity matrix under a learning mechanism that relies on data under so-called “surgical” or “perfect” interventions. In their framework, a variable becomes independent of all its parents if it is being intervened on and all incoming contributions are thus effectively removed under the intervention (also called do-interventions in the classical sense of [13]). The learning mechanism makes then use of the knowledge where these “surgical” interventions occurred. [14] also allow for “changing” the incoming arrows for variables that are intervened on; but again, [14] requires the location of the interventions while we do not assume such knowledge. [15] consider a target variable and allow for arbitrary interventions on all other nodes. They neither permit hidden variables nor cycles.

Here, we are interested in a setting where we have either no or just very limited knowledge about the exact location and strength of the interventions, as is often the case for data observed under different environments (see the example on financial time series further below) or for biological data [16, 17]. These interventions have been called “fat-hand” or “uncertain” interventions [18]. While [18] assume acyclicity and model the structure explicitly in a Bayesian setting, we assume that the data in environment are equilibrium observations of the model

| (3) |

where the random intervention shift has a mean and covariance . The location of these interventions (or simply the intervened variables) are those components of that are not zero with probability one. Given these locations, the interventions simply shift the variables by a value determined by ; they are therefore not “surgical” but can be seen as a special case of what is called an “imperfect”, “parametric” [19] or “dependent” intervention [20] or “mechanism change” [21]. The matrix and the error distribution of are assumed to be identical in all environments. In contrast to the covariance matrix for the noise term , we do assume that is a diagonal matrix, which is equivalent to demanding that interventions at different variables are uncorrelated. This is a key assumption necessary to identify the model using experimental data. Furthermore, we will discuss in Section 4.2 how a violation of the model assumption (3) can be detected and used to estimate the location of the interventions.

In Section 2 we show how to leverage observations under different environments with different interventional distributions to learn the structure of the connectivity matrix in model (3). The method rests on a simple joint matrix diagonalization. We will prove necessary and sufficient conditions for identifiability in Section 3. Numerical results for simulated data and applications in flow cytometry and financial data are shown in Section 4.

2 Method

2.1 Grouping of data

Let be the set of experimental conditions under which we observe equilibrium data from model (3). These different experimental conditions can arise in two ways: (a) a controlled experiment was conducted where the external input or the external imperfect interventions have been deliberately changed from one member of to the next. An example are the flow cytometry data [22] discussed in Section 4.2. (b) The data are recorded over time. It is assumed that the external input is changing over time but not in an explicitly controlled way. The data are grouped into consecutive blocks of observations, see Section 4.3 for an example.

2.2 Notation

Assume we have observations in each setting . Let be the -matrix of observations from model (3). For general random variables , the population covariance matrix in setting is called , where the covariance is under the setting . Furthermore, the covariance on all settings except setting is defined as an average over all environments except for the -th environment, The population Gram matrix is defined as . Let the -dimensional be the empirical covariance matrix of the observations of variable in setting . More precisely, let be the column-wise mean-centered version of . Then . The empirical Gram matrix is denoted by .

2.3 Assumptions

The main assumptions have been stated already but we give a summary below.

- (A)

-

(B)

The distribution of the noise (which includes the influence of latent variables) and the connectivity matrix are identical across all settings . In each setting , the intervention shift and the noise are uncorrelated.

-

(C)

Interventions at different variables in the same setting are uncorrelated, that is is an (unknown) diagonal matrix for all .

We will discuss a stricter version of (C) in Section D in the Appendix that allows the use of Gram matrices instead of covariance matrices. The conditions above imply that the environments are characterized by different interventions strength, as measured by the variance of the shift in each setting. We aim to reconstruct both the connectivity matrix from observations in different environments and also aim to reconstruct the a-priori unknown intervention strength and location in each environment. Additionally, we will show examples where we can detect violations of the model assumptions and use these to reconstruct the location of interventions.

2.4 Population method

The main idea is very simple. Looking at the model (3), we can rewrite

| (4) |

The population covariance of the transformed observations are then for all settings given by

| (5) |

The last term is constant across all settings (but not necessarily diagonal as we allow hidden variables). Any change of the matrix on the left-hand side thus stems from a shift in the covariance matrix of the interventions. Let us define the difference between the covariance of and in setting as

| (6) |

Assumption (B) together with (5) implies that

| (7) |

Using assumption (C), the random intervention shifts at different variables are uncorrelated and the right-hand side in (7) is thus a diagonal matrix for all . Let be the set of all invertible matrices. We also define a more restricted space which only includes those members of that have entries all equal to one on the diagonal and have a cycle-product less than one,

| (8) | ||||

| (9) |

Under Assumption (A), . Motivated by (7), we now consider the minimizer

| (10) |

is the loss for any matrix and defined as the sum of the squared off-diagonal elements. In Section 3, we present necessary and sufficient conditions on the interventions under which is the unique minimizer of (10). In this case, exact joint diagonalization is possible so that for all environments . We discuss an alternative that replaces covariance with Gram matrices throughout in Section D in the Appendix. We now give a finite-sample version.

2.5 Finite-sample estimate of the connectivity matrix

Input:

Output:

In practice, we estimate by minimizing the empirical counterpart of (10) in two steps. First, the solution of the optimization is only constrained to matrices in . Subsequently, we enforce the constraint on the solution to be a member of . The backShift algorithm is presented in Algorithm 1 and we describe the important steps in more detail below.

Steps 1 & 2.

First, we minimize the following empirical, less constrained variant of (10)

| (11) |

where the population differences between covariance matrices are replaced with their empirical counterparts and the only constraint on the solution is that it is invertible, i.e. . For the optimization we use the joint approximate matrix diagonalization algorithm FFDiag [23].

Step 3.

The constraint on the cycle product and the diagonal elements of is enforced by (a) permuting and (b) scaling the rows of . Part (b) simply scales the rows so that the diagonal elements of the resulting matrix are all equal to one. The more challenging first step (a) consists of finding a permutation such that under this permutation the scaled matrix from part (b) will have a cycle product as small as possible (as follows from Theorem 3, at most one permutation can lead to a cycle product less than one). This optimization problem seems computationally challenging at first, but we show that it can be solved by a variant of the linear assignment problem (LAP) (see e.g. [24]), as proven in Theorem 3 in the Appendix. As a last step, we check whether the cycle product of is less than one, in which case we have found the solution. Otherwise, no solution satisfying the model assumptions exists and we return a warning that the model assumptions are not met. See Appendix B for more details.

Computational cost.

The computational complexity of backShift is as computing the covariance matrices costs , FFDiag has a computational cost of and both the linear assignment problem and computing the cycle product can be solved in time. For instance, this complexity is achieved when using the Hungarian algorithm for the linear assignment problem (see e.g. [24]) and the cycle product can be computed with a simple dynamic programming approach.

2.6 Estimating the intervention variances

One additional benefit of backShift is that the location and strength of the interventions can be estimated from the data. The empirical, plug-in version of Eq. (7) is given by

| (12) |

So the element is an estimate for the difference between the variance of the intervention at variable in environment , namely , and the average in all other environments, . From these differences we can compute the intervention variance for all environments up to an offset. By convention, we set the minimal intervention variance across all environments equal to zero. Alternatively, one can let observational data, if available, serve as a baseline against which the intervention variances are measured.

3 Identifiability

Let for simplicity of notation,

be the variance of the random intervention shifts at node in environment as per the definition of in (6). We then have the following identifiability result (the proof is provided in Appendix A).

Theorem 1.

Under assumptions (A), (B) and (C), the solution to (10) is unique if and only if for all there exist such that

| (13) |

If none of the intervention variances vanishes, the uniqueness condition is equivalent to demanding that the ratio between the intervention variances for two variables must not stay identical across all environments, that is there exist such that

| (14) |

which requires that the ratio of the variance of the intervention shifts at two nodes is not identical across all settings. This leads to the following corollary.

Corollary 2.

-

(i)

The identifiability condition (13) cannot be satisfied if since then for all and . We need at least three different environments for identifiability.

-

(ii)

The identifiability condition (13) is satisfied for all almost surely if the variances of the intervention are chosen independently (over all variables and environments ) from a distribution that is absolutely continuous with respect to Lebesgue measure.

Condition (ii) can be relaxed but shows that we can already achieve full identifiability with a very generic setting for three (or more) different environments.

4 Numerical results

In this section, we present empirical results for both synthetic and real data sets. In addition to estimating the connectivity matrix , we demonstrate various ways to estimate properties of the interventions. Besides computing the point estimate for backShift, we use stability selection [25] to assess the stability of retrieved edges. We attach R-code with which all simulations and analyses can be reproduced222An R-package called “backShift” is available from CRAN..

4.1 Synthetic data

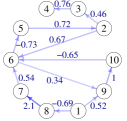

We compare the point estimate of backShift against Ling [11], a generalization of Lingam to the cyclic case for purely observational data. We consider the cyclic graph shown in Figure 1LABEL:sub@fig:sim_net and generate data under different scenarios. The data generating mechanism is sketched in Figure 1LABEL:sub@fig:sim_gen. Specifically, we generate ten distinct environments with non-Gaussian noise. In each environment, the random intervention variable is generated as , where are drawn i.i.d. from and are independent standard normal random variables. The intervention shift thus acts on all observed random variables. The parameter regulates the strength of the intervention. If hidden variables exist, the noise term of variable in environment is equal to , where the weights are sampled once from a -distribution and the random variable has a distribution. If no hidden variables are present, then , is sampled i.i.d. . In this set of experiments, we consider five different settings (described below) in which the sample size , the intervention strength as well as the existence of hidden variables varies.

[scale=.57, line width=0.5pt, minimum size=0.45cm, inner sep=0.3mm, shorten ¿=1pt, shorten ¡=1pt] \tikzstyleevery node=[font=]

(-1.5,0) node(x1) [circle, draw] ; \draw(1.5,0) node(x2) [circle, draw] ; \draw(0,2.5) node(x3) [circle, draw] ;

(-2.5,-1) node(i1) [circle, draw, blue] ; \draw(2.5,-1) node(i2) [circle, draw, blue] ; \draw(0.75,3.75) node(i3) [circle, draw, blue] ;

(-2.5,1) node(w1) [circle, dashed, draw, magenta] ; \draw(2.5,1) node(w2) [circle, dashed, draw, magenta] ; \draw(-.75,3.75) node(w3) [circle, dashed, draw, magenta] ;

(0,1) node(w) [circle, dashed, draw, magenta] ;

(-2.4,-0.3) node(ii) [blue] ; \draw(2.4,-0.3) node(ii) [blue] ; \draw(.8,3) node(iii) [blue] ;

(-.7,.775) node(ii) [magenta] ; \draw(.7,.775) node(ii) [magenta] ; \draw(-.3,1.5) node(ii) [magenta] ;

[-arcsq] (x1) – (x2); \draw[-arcsq] (x2) – (x3); \draw[-arcsq] (x3) – (x1); \draw[-arcsq, blue] (i2) – (x2); \draw[-arcsq, blue] (i3) – (x3); \draw[-arcsq, blue] (i1) – (x1); \draw[-arcsq, magenta] (w1) – (x1); \draw[-arcsq, magenta] (w2) – (x2); \draw[-arcsq, magenta] (w3) – (x3); \draw[-arcsq, magenta] (w) – (x1); \draw[-arcsq, magenta] (w) – (x2); \draw[-arcsq, magenta] (w) – (x3);

| Setting 1 | Setting 2 | Setting 3 | Setting 4 | Setting 5 | |

|---|---|---|---|---|---|

| no hidden vars. | no hidden vars. | hidden vars. | no hidden vars. | no hidden vars. | |

|

backShift |

|||||

|

Ling |

|||||

![[Uncaptioned image]](/html/1506.02494/assets/x3.png)

![[Uncaptioned image]](/html/1506.02494/assets/x4.png)

![[Uncaptioned image]](/html/1506.02494/assets/x5.png)

![[Uncaptioned image]](/html/1506.02494/assets/x6.png)

![[Uncaptioned image]](/html/1506.02494/assets/x7.png)

![[Uncaptioned image]](/html/1506.02494/assets/x8.png)

![[Uncaptioned image]](/html/1506.02494/assets/x9.png)

![[Uncaptioned image]](/html/1506.02494/assets/x10.png)

![[Uncaptioned image]](/html/1506.02494/assets/x11.png)

![[Uncaptioned image]](/html/1506.02494/assets/x12.png)

We allow for hidden variables in only one out of five settings as Ling assumes causal sufficiency and can thus in theory not cope with hidden variables. If no hidden variables are present, the pooled data can be interpreted as coming from a model whose error variables follow a mixture distribution. But if one of the error variables comes from the second mixture component, for example, the other error variables come from the second mixture component, too. In this sense, the data points are not independent anymore. This poses a challenge for Ling which assumes an i.i.d. sample. We also cover a case (for ) in which all assumptions of Ling are satisfied (Scenario 4).

Figure 2 shows the estimated connectivity matrices for five different settings and Figure 1LABEL:sub@fig:sim_metrics shows the obtained precision and recall values. In Setting 1, , and there are no hidden variables. In Setting 2, is increased to while the other parameters do not change. We observe that backShift retrieves the correct adjacency matrix in both cases while Ling’s estimate is not very accurate. It improves slightly when increasing the sample size. In Setting 3, we do include hidden variables which violates the causal sufficiency assumption required for Ling. Indeed, the estimate is worse than in Setting 2 but somewhat better than in Setting 1. backShift retrieves two false positives in this case. Setting 4 is not feasible for backShift as the distribution of the variables is identical in all environments (since ). In Step 2 of the algorithm, FFDiag does not converge and therefore the empty graph is returned. So the recall value is zero while precision is not defined. For Ling all assumptions are satisfied and the estimate is more accurate than in the Settings 1–3. Lastly, Setting 5 shows that when increasing the intervention strength to , backShift returns a few false positives. Its performance is then similar to Ling which returns its most accurate estimate in this scenario. The stability selection results for backShift are provided in Figure 5 in Appendix E.

In short, these results suggest that the backShift point estimates are close to the true graph if the interventions are sufficiently strong. Hidden variables make the estimation problem more difficult but the true graph is recovered if the strength of the intervention is increased (when increasing to in Setting 3, backShift obtains a of zero). In contrast, Ling is unable to cope with hidden variables but also has worse accuracy in the absence of hidden variables under these shift interventions.

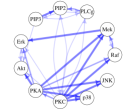

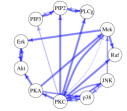

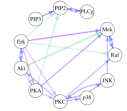

4.2 Flow cytometry data

The data published in [22] is an instance of a data set where the external interventions differ between the environments in and might act on several compounds simultaneously [18]. There are nine different experimental conditions with each containing roughly 800 observations which correspond to measurements of the concentration of biochemical agents in single cells. The first setting corresponds to purely observational data.

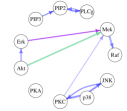

In addition to the original work by [22], the data set has been described and analyzed in [18] and [26]. We compare against the results of [26], [22] and the “well-established consensus”, according to [22], shown in Figures 3LABEL:sub@fig:cons and 3LABEL:sub@fig:mooijcyc. Figure 3LABEL:sub@fig:point shows the (thresholded) backShift point estimate. Most of the retrieved edges were also found in at least one of the previous studies. Five edges are reversed in our estimate and three edges were not discovered previously. Figure 3LABEL:sub@fig:ev5 shows the corresponding stability selection result with the expected number of falsely selected variables . This estimate is sparser in comparison to the other ones as it bounds the number of false discoveries. Notably, the feedback loops between PIP2 PLCg and PKC JNK were also found in [26].

It is also noteworthy that we can check the model assumptions of shift interventions, which is important for these data as they can be thought of as changing the mechanism or activity of a biochemical agent rather than regulate the biomarker directly [26]. If the shift interventions are not appropriate, we are in general not able to diagonalize the differences in the covariance matrices. Large off-diagonal elements in the estimate of the r.h.s in (7) indicate a mechanism change that is not just explained by a shift intervention as in (1). In four of the seven interventions environments with known intervention targets the largest mechanism violation happens directly at the presumed intervention target, see Appendix C for details. It is worth noting again that the presumed intervention target had not been used in reconstructing the network and mechanism violations.

4.3 Financial time series

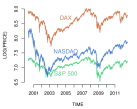

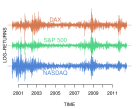

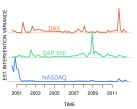

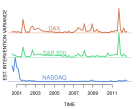

Finally, we present an application in financial time series where the environment is clearly changing over time. We consider daily data from three stock indices NASDAQ, S&P 500 and DAX for a period between 2000-2012 and group the data into 74 overlapping blocks of 61 consecutive days each. We take log-returns, as shown in panel (b) of Figure 4 and estimate the connectivity matrix, which is fully connected in this case and perhaps of not so much interest in itself. It allows us, however, to estimate the intervention strength at each of the indices according to (12), shown in panel (c). The intervention variances separate very well the origins of the three major down-turns of the markets on the period. Technology is correctly estimated by backShift to be at the epicenter of the dot-com crash in 2001 (NASDAQ as proxy), American equities during the financial crisis in 2008 (proxy is S&P 500) and European instruments (DAX as best proxy) during the August 2011 downturn.

5 Conclusion

We have shown that cyclic causal networks can be estimated if we obtain covariance matrices of the variables under unknown shift interventions in different environments. backShift leverages solutions to the linear assignment problem and joint matrix diagonalization and the part of the computational cost that depends on the number of variables is at worst cubic. We have shown sufficient and necessary conditions under which the network is fully identifiable, which require observations from at least three different environments. The strength and location of interventions can also be reconstructed.

References

References

- [1] K.A. Bollen. Structural Equations with Latent Variables. John Wiley & Sons, New York, USA, 1989.

- [2] P. Spirtes, C. Glymour, and R. Scheines. Causation, Prediction, and Search. MIT Press, Cambridge, USA, 2nd edition, 2000.

- [3] D.M. Chickering. Optimal structure identification with greedy search. Journal of Machine Learning Research, 3:507–554, 2002.

- [4] M.H. Maathuis, M. Kalisch, and P. Bühlmann. Estimating high-dimensional intervention effects from observational data. Annals of Statistics, 37:3133–3164, 2009.

- [5] A. Hauser and P. Bühlmann. Characterization and greedy learning of interventional Markov equivalence classes of directed acyclic graphs. Journal of Machine Learning Research, 13:2409–2464, 2012.

- [6] P.O. Hoyer, D. Janzing, J.M. Mooij, J. Peters, and B. Schölkopf. Nonlinear causal discovery with additive noise models. In Advances in Neural Information Processing Systems 21 (NIPS), pages 689–696, 2009.

- [7] S. Shimizu, T. Inazumi, Y. Sogawa, A. Hyvärinen, Y. Kawahara, T. Washio, P.O. Hoyer, and K. Bollen. DirectLiNGAM: A direct method for learning a linear non-Gaussian structural equation model. Journal of Machine Learning Research, 12:1225–1248, 2011.

- [8] J.M. Mooij, D. Janzing, T. Heskes, and B. Schölkopf. On causal discovery with cyclic additive noise models. In Advances in Neural Information Processing Systems 24 (NIPS), pages 639–647, 2011.

- [9] A. Hyttinen, F. Eberhardt, and P. O. Hoyer. Learning linear cyclic causal models with latent variables. Journal of Machine Learning Research, 13:3387–3439, 2012.

- [10] S.L. Lauritzen and T.S. Richardson. Chain graph models and their causal interpretations. Journal of the Royal Statistical Society, Series B, 64:321–348, 2002.

- [11] G. Lacerda, P. Spirtes, J. Ramsey, and P.O. Hoyer. Discovering cyclic causal models by independent components analysis. In Proceedings of the 24th Conference on Uncertainty in Artificial Intelligence (UAI), pages 366–374, 2008.

- [12] R. Scheines, F. Eberhardt, and P.O. Hoyer. Combining experiments to discover linear cyclic models with latent variables. In International Conference on Artificial Intelligence and Statistics (AISTATS), pages 185–192, 2010.

- [13] J. Pearl. Causality: Models, Reasoning, and Inference. Cambridge University Press, New York, USA, 2nd edition, 2009.

- [14] F. Eberhardt, P. O. Hoyer, and R. Scheines. Combining experiments to discover linear cyclic models with latent variables. In International Conference on Artificial Intelligence and Statistics (AISTATS), pages 185–192, 2010.

- [15] J. Peters, P. Bühlmann, and N. Meinshausen. Causal inference using invariant prediction: identification and confidence intervals. Journal of the Royal Statistical Society, Series B, to appear., 2015.

- [16] A.L. Jackson, S.R. Bartz, J. Schelter, S.V. Kobayashi, J. Burchard, M. Mao, B. Li, G. Cavet, and P.S. Linsley. Expression profiling reveals off-target gene regulation by RNAi. Nature Biotechnology, 21:635–637, 2003.

- [17] M.M. Kulkarni, M. Booker, S.J. Silver, A. Friedman, P. Hong, N. Perrimon, and B. Mathey-Prevot. Evidence of off-target effects associated with long dsrnas in drosophila melanogaster cell-based assays. Nature methods, 3:833–838, 2006.

- [18] D. Eaton and K. Murphy. Exact Bayesian structure learning from uncertain interventions. In International Conference on Artificial Intelligence and Statistics (AISTATS), pages 107–114, 2007.

- [19] F. Eberhardt and R. Scheines. Interventions and causal inference. Philosophy of Science, 74:981–995, 2007.

- [20] K. Korb, L. Hope, A. Nicholson, and K. Axnick. Varieties of causal intervention. In Proceedings of the Pacific Rim Conference on AI, pages 322–331, 2004.

- [21] J. Tian and J. Pearl. Causal discovery from changes. In Proceedings of the 17th Conference Annual Conference on Uncertainty in Artificial Intelligence (UAI), pages 512–522, 2001.

- [22] K. Sachs, O. Perez, D. Pe’er, D. Lauffenburger, and G. Nolan. Causal protein-signaling networks derived from multiparameter single-cell data. Science, 308:523–529, 2005.

- [23] A. Ziehe, P. Laskov, G. Nolte, and K.-R. Müller. A fast algorithm for joint diagonalization with non-orthogonal transformations and its application to blind source separation. Journal of Machine Learning Research, 5:801–818, 2004.

- [24] R.E. Burkard. Quadratic assignment problems. In P. M. Pardalos, D.-Z. Du, and R. L. Graham, editors, Handbook of Combinatorial Optimization, pages 2741–2814. Springer New York, 2nd edition, 2013.

- [25] N. Meinshausen and P. Bühlmann. Stability selection. Journal of the Royal Statistical Society, Series B, 72:417–473, 2010.

- [26] J.M. Mooij and T. Heskes. Cyclic causal discovery from continuous equilibrium data. In Proceedings of the 29th Annual Conference on Uncertainty in Artificial Intelligence (UAI), pages 431–439, 2013.

Appendix to

backShift: Learning causal cyclic graphs from unknown shift interventions

Appendix A Identifiability – Proof of Theorem 1

Proof.

“if”: Let be a solution of (10). Let us write for the -th row of and for the -th row of , . Furthermore let us define , . We will show that at most one entry of this vector is nonzero. Note that by equation (7) we have for all . By equation (7), . As solves equation (10), this implies for all . Hence the offdiagonal elements of are zero, which implies

As the are linearly independent, this implies that for all pairs , and are collinear i.e. for all there exists a such that or

Take arbitrary and choose such that (13) is satisfied. By the argumentation above, there exists a such that or . Without loss of generality let us assume the latter. Recall that both and are diagonal matrices. Now condition (13) implies that the -th or the -th entry on the diagonal of is nonzero (or both). Hence, the -th or the -th entry of s zero (or both). By repeating this argumentation for all and , at most one entry of is nonzero. Thus, is a multiple of one of the rows of .

By applying this argumentation for all , each row of is a multiple of one of the rows of . As both and are invertible, there exists a bijection between the rows of and such that the corresponding rows are collinear. Furthermore, the diagonal of and is . Hence let us consider a bijection such that the -th row of is a multiple of the -th row of , i.e. for all . We want to show that this bijection is the identity. First observe that, as the diagonal of and is , for all . Now let us consider a cycle in this permutation , i.e. , , for and with for . If this leads to a contradiction, we can conclude that is the identity. As , , i.e. for . This corresponds to a cycle in with product

| (15) |

As is a solution of (10), , hence the product on the left hand side of equation (15) is in absolute value strictly smaller than , see (2). Analogously, as for , the sequence corresponds to a cycle with product

Using the same argumentation as for , this product is in absolute value strictly smaller than , which contradicts (15). Hence such cycles of length do not exist and is the identity. Hence, .

“only if”: As above define as the -th row of and let us write for the -th unit vector for . Assume that (13) is not true, i.e. there exist such that for all ,

| (16) |

Without loss of generality let us fix a with , and define . If such a does not exist, we can apply the same argumentation as below but with the and interchanged and .

Note that the definition of does not depend on and that by equation (7) we have . Then, for we can define and and we obtain for all

In the second equation we used (16). Furthermore, for small let us scale such that the -th component of the vector is . Analogously, let us scale such that the -th component of the vector is . Then we can define the matrix as the rows of except for row and which are replaced by and . By above reasoning, this matrix satisfies

for all and is invertible. Furthermore, the diagonal elements of are . Recall that the path-products of over cycles are in absolute value smaller than , see (2). For small , is close to (in an arbitrary matrix norm) and hence the path products of over cycles are in absolute value smaller than as well. As is invertible, . Hence the solution to (10) is not unique. This concludes the proof.

∎

Appendix B Polynomial-time algorithm

Here, we provide the necessary theoretical result to show that backShift has a computational cost of . Specifically, we show that Step 3 in Algorithm 1 can be cast in terms of the classical linear sum assignment problem, having a computational complexity of .

Theorem 3.

Let be a matrix with , and for . For define

Furthermore define

| There exists a permutation of such that the -th row of | |||

Then,

Proof.

Let with . Let us write for the -th row of and analogously for the -th row of , . Now let be a permutation such that the -th row of is collinear to the -th row of . As , we have that . As diag,

It immediately follows that

As and is not the identity, . As all elements of and are nonzero, and . Hence, . This concludes the proof.

∎

Remark: We can define the relative loss function of moving row to row as

Then the linear assignment problem that minimizes this problem also yields the correct permutation for Step 3 in Algorithm 1 if it exists, i.e. the permutation on that minimizes

satisfies that is collinear to .

Remark: Allowing for self-loops would lead to an identifiability problem, independent of the method. For every model with self-loops and there is a model without self-loops and yielding the same observational distribution in equilibrium. The connectivity matrix without self-loops can thus be seen as a representative of a whole class of connectivity matrices that allow self-loops. Specifically, if the connectivity matrix with self-loops is , define matrix by , where is the operation defined in Step 3 of the backShift algorithm. Technically, is only defined for matrices that are nonzero outside of the diagonal. Using similar arguments as in Theorem 3, can be extended to arbitrary matrices with nonzero diagonal elements. To be more precise, there exists a matrix such that , and such that is the product of a diagonal scaling matrix with a permutation matrix. Then define , and for all . As is the product of a diagonal scaling matrix with a permutation matrix, assumptions (B) and (C) are still fulfilled and for all . This implies that the two matrices with self-loops and without self-loops (since it has zeroes on the diagonal by construction) have both and yield the same distribution.

Appendix C Intervention variances and model misspecification

The method allows to validate and check the assumptions to some extent. This is especially important in the data of [22] as pointed out in [26]. The interventions can mostly be thought of as not changing the concentration of a biochemical agent but rather changing the activity of the agent, for example by inhibiting the reactions in which the agent is involved [26]. Under such a mechanism change, it is doubtful whether the interventions are well approximated by our model (3) with independent shift-interventions. We can check the assumptions by the success of the joint diagonalization procedure. Specifically, we get an empirical version of (7) when plugging in the estimators and can check whether all off-diagonal elements on the right hand side of (7) are small or vanishing. We list below results for the seven experimental intervention conditions whose target is well described in [26]. The element on the right-hand side of (7) with the largest absolute value is selected. We use now the Gram instead of the covariance matrix to be also sensitive to model-violations of the additional assumption (C’), see Section D, though the results are almost identical whether using the Gram or covariance matrix. These large off-diagonal elements indicate a violated mechanism in the sense that the model (3) does not fit very well, because either the interventions have not been of the assumed shift-type or the causal mechanism in which the agent is involved has changed under the intervention.

| Experiment | Reagent | Intervention | largest mechanism violation |

|---|---|---|---|

| 3 | Akt-Inhibitor | inhibits AKT activity | PLCg PKA |

| 4 | G0076 | inhibits PKC activity | PKC PIP2 |

| 5 | Psitectorigenin | inhibits PIP2 abundance | PIP2 PKA |

| 6 | U0126 | inhibits MEK activity | MEK PKA |

| 7 | LY294002 | changes PIP2/PIP3 mechanisms | PKA JNK |

| 8 | PMA | activates PKC activity | MEK PKA |

| 9 | 2CAMP | activates PKA activity | PKA PKC |

The table above lists the results for the seven experimental conditions where we know the intervention mechanism, at least approximately. The results are interesting in that the most violated mechanism (the largest entry in the off-diagonal matrix on the right-hand side of the empirical version of (7)) occurs in 4 of the 7 experimental conditions directly at the intervention target. In 3 of these 4 cases, the violated mechanism concerns a relation that has a large entry in the estimated connectivity matrix. This corresponds well with the model of activity interventions in [26]. Note that we have not made use of the intervention targets in the estimation procedure. The interesting point is that we can use the model violations to estimate with some success where the interventions occurred.

Appendix D Beyond covariances

For the method above, we exploit differences in the covariance of observations across different environments. We can also exploit a shift in the mean of the intervention strength (and consequently in the observations ) when strengthening the condition (C) to (C’). Specifically, we require for (C’) that in each environment the shift in the mean equals zero for all variables except at most one variable. The variable with a non-zero shift in the mean can change from one environment to another. Note that the counterpart of (5) when using the Gram matrix instead of the covariance matrix reads

| (17) |

Under the stronger version (C’), the difference across environments of the right-hand side in (17) is again a diagonal matrix and we can proceed just as above, by replacing the covariance matrices with Gram matrices throughout. If the assumption (C’) is satisfied, this allows identifiability of the graph in a wider range of settings (Theorem 1 can be adapted in a straightforward manner by again replacing covariances with Gram matrices) but requires the stricter condition (C’). Since in practice it is often unclear whether the stricter condition is approximately true, we work mainly with the weaker assumption (C) and exploit only shifts in the covariance matrices.

Appendix E Additional figures

| Setting 1 | Setting 2 | Setting 3 | Setting 4 | Setting 5 | |

|---|---|---|---|---|---|

| no hidden vars. | no hidden vars. | hidden vars. | no hidden vars. | no hidden vars. | |

|

backShift |

|||||

![[Uncaptioned image]](/html/1506.02494/assets/x21.png)

![[Uncaptioned image]](/html/1506.02494/assets/x22.png)

![[Uncaptioned image]](/html/1506.02494/assets/x23.png)

![[Uncaptioned image]](/html/1506.02494/assets/x24.png)

![[Uncaptioned image]](/html/1506.02494/assets/x25.png)