Optimal Dynamic Contracts for a Large-Scale Principal-Agent Hierarchy: A Concavity-Preserving Approach

Abstract

We present a continuous-time contract whereby a top-level player can incentivize a hierarchy of players below him to act in his best interest despite only observing the output of his direct subordinate. This paper extends Sannikov’s approach from a situation of asymmetric information between a principal and an agent to one of hierarchical information between several players. We develop an iterative algorithm for constructing an incentive compatible contract and define the correct notion of concavity which must be preserved during iteration. We identify conditions under which a dynamic programming construction of an optimal dynamic contract can be reduced to only a one-dimensional state space and one-dimensional control set, independent of the size of the hierarchy. In this sense, our results contribute to the applicability of dynamic programming on dynamic contracts for a large-scale principal-agent hierarchy.

1 Introduction

A principal-agent problem is a problem of optimal contracting between two parties in an uncertain environment. One player, namely the agent, may be able to influence the value of the output process with his actions. A separate party, the principal, wants to maximize the output process, which is subject to external noise.

It would be ideal for the principal to monitor the agent and enforce a strategy which is optimal to the principal. This case if often called the first best. However, it is often costly for the principal to monitor the agent’s action. In many practical situations, the principal can only observe the output process, while the agent has perfect observations. Therefore, the agent is free to deviate from the action or control suggested by the principal, and the principal may not be able to detect this deviation. For example, the agent can shirk and attribute the resulting low output to noise.

In this setting of asymmetric information, the principal can only enforce an ‘incentive compatible’ control strategy upon the agent – a strategy which maximizes the agent’s expected utility given the compensation scheme in the contract. Then, the principal’s optimal strategy is to design the combination of a compensation scheme and a recommended control strategy such that the recommended control is optimal to the agent given the compensation scheme, and this combination maximizes the principal’s expected utility. Such a combination constitutes a contract, which is provided to the agent.

This so-called second best strategy in principal-agent problems has been one of primary interests in economic studies on contracts [12]. In particular, principal-agent problems in continuous-time have attracted considerable attention in economics, finance and engineering (e.g.,[10, 17, 26]). Mathematically, such a principal-agent problem can be considered as a special case of Stackelberg differential games [23]. While many Stackelberg differential game problems remain as a challenge in general [2], there have been remarkable advances in solution approaches for principal-agent problems.

In Sannikov [20, 21], a dynamic programming approach is developed. The key idea is to introduce another state variable, called the agent’s continuation value, which represents the agent’s expected future utility conditioned upon the information up to current time. This approach is generalized in [8] to handle more complicated dynamics of the output process and multiple agents. Another stream of research utilizes the stochastic maximum principle [25, 4, 5]. This method requires us to solve an associated forward-backward stochastic differential equation, which is a non-trivial task (e.g., [1, 18, 13]).

In this paper, we consider a hierarchical principal-agent problem with asymmetric information in the form of moral hazard. This means there exists a hierarchy of players, each of which acts as a ‘principal’ to the ‘agent’ below them in the hierarchy.

More precisely, in this hierarchy of players, Player acts as a principal with Player as his agent. Moral hazard refers to the restriction that Player can only compensate Player based upon an observable noisy output, but not upon the actions actually performed by Player . Due to usefulness of contractual hierarchies in modeling a organizational form of firms, governments and vertically-integrated economies, several contracts in a principal-agent hierarchy have been proposed (e.g., [19, 15, 14]). However, these studies focus on incentive contracts in static settings. A recent work [22] extends Holmstrom and Milgrom’s optimal linear contract [10] to the case of discrete-time hierarchical contracting by using first-order conditions. To the authors’ best knowledge, our work first develops a dynamic programming solution approach for designing optimal continuous-time dynamic contracts in a principal-agent hierarchy.

The main result in continuous-time moral hazard problems between two players is that the principal can provide a payment scheme which incentivizes the agent to act in the principal’s best interest. In [20, 6], the success of these payment schemes depends upon certain concavity conditions on the agent’s utility. The particular conditions and how to proceed when they are not met were emphasized in [8].

The main idea of this paper is to construct a payment scheme for the hierarchical principal-agent model, whereby Player 0 can incentivize all players below him to act in his best interest. At a high level, the idea is to think of all players below Player 0 as an ‘aggregate agent’ and inductively apply a generalized two player principal-agent result.

The first contribution of this work is to illustrate how Player 0 can construct an optimal dynamic contract which incentivizes the entire hierarchy to act in his best interest. Compared to [20], this result allows Player 0 to indirectly incentivize even those players whose output he cannot directly observe. Specifically, Player can only monitor the output of Player for . The main technical issue in this result is that, in general, the effective utilities of each player in the hierarchy will not be concave. To restore concavity, we develop a new concept called -concave envelopes, which play an essential role to design an optimal dynamic contract via dynamic programming.

Secondly, this work illustrates how our hierarchical principal-agent model can resolve dimensionality issues in dynamic contract problems with multiple agents. Compared the contract constructed by a single principal controlling multiple agents directly in [8], Player 0 only monitors one continuation value in a dynamic programming solution of his optimization problem. Furthermore, the maximization step is performed over a subset of efforts with dimension potentially less than . We show how to construct this subset by a novel iterative algorithm. This iterative construction allows us to characterize a stochastic optimal control problem, which is equivalent to the original contract design problem. An important feature of this stochastic optimal control problem is that it is one-dimensional and therefore an optimal dynamic contract can be designed by solving an one-dimensional dynamic programming problem.

The final contribution of this work is to characterize conditions under which the subset of efforts which Player 0 can choose is a one-dimensional sub-manifold. In particular, we show that if each effort has a utility function which is strictly concave, then we can parameterize the admissible efforts by a function which we construct. In this case, we show Player 0 can construct an optimal dynamic contract by solving an associated Hamilton-Jacobi-Bellman (HJB) equation with only one-dimensional state space and one-dimensional admissible controls. We explicitly demonstrate this HJB characterization in the case of agents with quadratic utilities.

The rest of this paper is organized as follows. In Section 2, we provide the mathematical setting of the hierarchical principal-agent problem considered in this paper. In Section 3, we define a generalized two player principal-agent problem and provide an optimal dynamic contract for the principal. This contract is iteratively constructed in Section 4 to provide an optimal dynamic contract for the hierarchical principal-agent problem. In Section 5 we consider more details about the main concavity property of each agent’s utility which much be preserved during iteration, called -concavity. In particular, we prove a major result related to dimensionality reduction. Finally, in Section 6, we consider a specific example and illustrate the steps involved in constructing an optimal dynamic contract for the hierarchical model.

2 Problem Formulation

Consider a hierarchy of players, each with a principal-agent relationship. We summarize the information asymmetry in the following diagram:

Note that Player can only monitor the output of Player for . Because the output is affected by external noise, Player is not able to correctly infer Player ’s action. For example, if output is low, Player cannot deduce if it is because Player performed little effort or due to bad luck. Each player provides payment to the player below him in the hierarchy, but the payment can only depend upon observable outputs and not the actual effort performed.

The goal of this paper is to define a payment mechanism whereby Player 0 can incentivize all players below him to act in a prescribed manner, even though Player 0 cannot directly observe their actions. The proposed payment mechanism is in the form of a contract between the principal, Player , and the aggregate agent, Players . The contract consists of a compensation scheme and a recommended control strategy for each agent, i.e., Player for . These two components must be designed before the contract starts. Player ’s interest is to design a contract such that given the compensation scheme each agent follows the recommended control strategy, and this combination maximizes Player ’s expected utility.

2.1 Mathematical Setup

We consider a continuous-time system representing the output of each player up to a terminal time, . Let be a probability space supporting a standard Brownian motion with natural filtration . We also consider output processes with dynamics given below. We denote by the filtration generated by the process .

The dynamics of the system are as follows:

-

•

Player chooses an effort process which is adapted to . The output of Player is a process defined by

-

•

For , Player chooses an effort process adapted to and terminal compensation which is -measurable. The output of Player is a process driven by

(1) Intuitively, represents the cumulative output from effort by Player and those below in the hierarchy.

-

•

Player 0 chooses a terminal compensation scheme which is -measurable.

The utilities of the players are as follows:

-

•

Player has some cost for effort, and receives a terminal compensation from :

-

•

For , Player has some cost for effort, receives a terminal compensation from Player , and pays a terminal compensation to Player :

Note that the Player ’s utility can depend on as well as because is adapted to and is driven by (1) which depends on . In other words, the utility for Player depends upon effort processes for Player through Player because these processes affect the distribution of , which affects the distribution of directly.

-

•

Player 0 has utility from the output and pays a terminal compensation to Player :

The notation represents the tuple . When , we will often use the notation to denote the tuple . The notation clarifies that we are taking expectation under a measure where the dynamics of are evolved via the choice of effort . The set of admissible control for Player is given by

for and . The set of admissible compensation for Player is given by

for and . We also let . Analogous notation is used for .

In this paper we assume that, for each , the function is concave and is decreasing and linear. Economically, these assumptions correspond respectively to aversion to uncertainty in effort and risk-neutrality over terminal payments.

2.2 Economic Problem

The goal of Player 0 is to prescribe compensation schemes, , which allow him to choose the effort for every player, . In particular, he does this so as to maximize his expected utility. However, because Player 0 cannot directly observe efforts, the choice must satisfy an incentive compatibility condition – that Player would not be better off by providing Player a different compensation scheme or by performing a different effort . Furthermore, Player 0 cannot force other players to accept a contract, so the choice must satisfy an individual rationality condition – that Player is paid more than a minimum required to accept the contract. We let be the minimum required utility for Player .

Player 0’s optimization problem can then be formulated as follows:

| (2) |

where the restrictions represents incentive compatibility and individual rationality conditions for the other players.

In summary, Player 0 proposes a set of recommended effort processes and terminal compensations in order to maximize his expected utility. The first two constraints refer to Player 1’s incentive compatibility and individual rationality respectively – for fixed , the proposed choices must maximize Player 1’s expected utility and meet a minimum utility for him to accept the contract. Each pair of constraints after that represent the analogous incentive compatibility and individual rationality constraints for each Player .

As written, Player 0’s optimization problem is non-trivial to solve primarily because it is unclear how to deal with the various incentive compatibility constraints. We will show that these constraints can be replaced by restrictions on the form of the terminal payments and admissible suggested efforts. Furthermore, the reformulation will be proven to be exact.

2.3 Main Result

The main result of this paper is to extend the continuous-time formalism described for two player Stackelberg differential games by Sannikov [20] to this hierarchical setup. We will show that for a particular choice of payment schemes, , the incentive compatibility conditions will automatically be satisfied.

We will show that Player 0’s optimization problem (2) is equivalent to the following optimization problem:

for a particular choice of , a given concave function , and a given subset , which will be characterized. Here, represents the super-gradient of , and .

The intuition is that Player 0 has an optimal effort process in mind. Player 0 provides Player 1 with a terminal compensation , which incentivizes him to cause the rest of the hierarchy to follow . The function represents the effective cost that Player 1 has to cause the hierarchy to follow , and represents the marginal cost.

There is not an explicit form for and , but the iterative algorithm defined in Theorem 2 is constructive. In Section 5, we show that if all players have utilities which are strictly concave, then is a one-dimensional manifold.

The main idea of the construction of the contract is to iteratively apply a generalization of a two player principal-agent result. The main technical condition that this generalization features over those in [6, 20] is -concavity, which was highlighted in [8]. When dealing with generalized dynamics for the output process, as in the hierarchical case, -concavity is the key condition an agent’s utility must satisfy for a principal to incentivize him to follow a given effort. We will show how this concavity condition can be preserved as we iteratively apply the two player principal-agent result. This process leads to constraints on , which are encoded in the subset .

This simplified problem is a standard stochastic control problem which may be solved by dynamic programming or, equivalently, by solving an associated Hamilton-Jacobi-Bellman equation. Then, Player 0 can explicitly construct a dynamic contract which is incentive compatible for all players, satisfies all individual rationality constraints, and maximizes his expected utility.

In particular, define the value function of Player 0 as

where , , and solves the following stochastic differential equation:

The drift function is defined in the iteration algorithm as a linear combination of each player’s utility function. The constant is the volatility of . The interpretation of is the continuation value for Player 1 – his remaining expected utility from following the proposed effort conditioned on the information up to time .

Then, is the unique viscosity solution of the following Hamilton-Jacobi-Bellman (HJB) equation:

with terminal condition , where will be characterized in the following sections. After solving the HJB, Player 0 can then construct an optimal contract by constructing an optimal feedback control and starting from the initial value which will be specified. Furthermore, the optimal feedback control will be adapted to the correct filtrations. Therefore, the proposed contract is implementable.

3 Contract for Generalized Principal-Agent Problem

In this section, we consider a generalized principal-agent problem between two players. We propose a contract and demonstrate its incentive compatibility and optimality. We will ultimately iterate this result in the full principal-agent hierarchy in Section 4.

Compared to [20, 8], this problem features generalized dynamics, lack of concavity on the agent’s utility, and constraints on what efforts the agent may choose. All three of these features will arise naturally in our iterative construction of a contract for the principal-agent hierarchy.

3.1 The Setting

As in the hierarchical model, we consider a continuous-time system with an underlying probability space supporting a standard Brownian motion with filtration . There are also two output processes and with dynamics defined below. We also take special consideration of the filtrations and which represent those generated by the processes and respectively.

In this problem, the single agent chooses an -dimensional effort process , which is restricted to be -adapted and lie in a prescribed subset almost surely. Meanwhile, the principal chooses a one-dimensional effort process , which must be -adapted, as well as a terminal payment to the agent, , which must be -measurable. The principal also receives a terminal payment, , which is -measurable – the interpretation is that this is a utility from a player higher in the hierarchy.

The dynamics of and are given by

The utilities for each party are given by

The principal’s optimization problem can then be written as follows:

| (3) |

where , and .

Intuitively, this problem represents a principal-agent problem with generalized dynamics and utilities. The agent chooses a multi-dimensional effort process to determine his output process. On the other hand, the principal chooses a one-dimensional effort process and a terminal payment based upon the agent’s output process and some external noise.

The requirement that each process be adapted to different filtrations represents the information asymmetry in the problem in the form of moral hazard. The relationship with our hierarchical problem will be that the principal represents Player , while the agent represents Player controlling the efforts of all those players below him in the hierarchy.

3.2 -Concavity and -Concave Envelopes

In this subsection, we define the key concavity condition required for the proposed contract to be incentive compatible and optimal.

Definition 1.

Let . We say a function is -concave if there exists a concave function such that

This condition was shown in [8] to be key to incentive compatibility in standard principal-agent problems. In particular, it was shown that if the agent’s utility was not -concave, then the principal is restricted to particular values of effort depending on the so-called -concave envelope of the agent’s utility.

In this paper, as we iterate along the hierarchy, there will always be restrictions on the set of admissible efforts. Therefore, we need a generalized notion of concave envelopes.

Definition 2.

Let be some function and . We say is the -concave envelope of if

-

•

is -concave,

-

•

for all , and

-

•

If is an -concave function such that for all , then for all .

When convenient, we may refer to by .

We show in Section 5 how to construct the -concave envelope of an arbitrary function. The equivalence refers to an auxillary concave function produced by the construction.

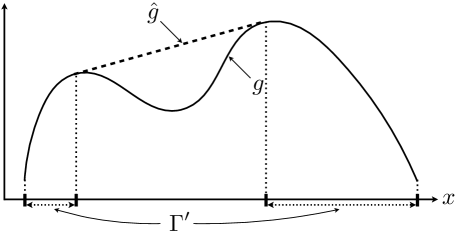

We also explicitly define the touching set to be the subset where .

Definition 3.

Let be the -concave envelope of . We define the corresponding touching set to be:

An example of the touching set is shown in Figure 1. Finally, we recall the definition of the super-gradient [3, 7] of a concave function.

Definition 4.

Let be a concave function. For any , define the super-gradient of at as the following set:

3.3 The Contract

We claim that for any desired choice of , there exists a compensation which incentivizes the agent to follow the desired effort. Furthermore, it is optimal for the principal to choose a contract of this particular form.

Let be the -concave envelope of , and let

be the corresponding touching set. We also introduce an auxiliary control variable which plays an important role in designing a compensation that satisfies the incentive compatibility and individual rationality. The set of admissible ’s is given by .

Proposition 1.

Fix . For any choice of processes such that for a.e., and such that for a.e., define

| (4) |

Then, is incentive compatible with , i.e.

and also satisfies the agent’s individual rationality constraint, i.e.

Proof.

Suppose that the agent instead follows an arbitrary choice of effort . Then, we compute

The key in this argument is that if the agent follows instead of , then the process evolves as

where is a -Brownian motion. The existence of the new probability measure is guaranteed by the Girsanov theorem (e.g., [11]). The rest follows from concavity using , , , and the definition of .

If the agent follows the suggested effort , we have

Here, the last equality holds due to the fact that is in the touching set for a.e. Therefore, is incentive compatible with and the individual rationality condition is satisfied. ∎

Note that given by (4) is not an admissible compensation scheme because it may not be -measurable. In fact, it is -measurable. However, we will show in the following subsection that any contract optimal to the principal has such that it is -measurable and therefore is implementable.

3.4 Optimality for Principal

In the previous subsection, we proved that a class of contracts is incentive compatible and individually rational for the agent. In this subsection, we prove that it is sufficient for the principal to consider only contracts of this form. In other words, the proposed class of contracts is optimal to the principal.

First, we prove two inequalities which relate to its -concave envelope and the super-gradient .

Lemma 1.

Let be the -concave envelope of and recall

Then, for any , we have

-

1.

If , then there exists such that

-

2.

If and , then there exists such that:

Proof.

Both proofs proceed by contradiction by building a better -concave envelope than .

-

1.

First, let . Then, there exists such that

Furthermore, suppose that in fact for all we have

Define a function as

Then, we have

Therefore, is -concave as the minimum of two -concave functions. However, at , we have

However, this contradicts the fact that is the -concave envelope. Therefore, there exists such that

-

2.

Next, let , but . Then, . Furthermore, suppose that in fact for all we have

Define a function as

Then, we have

Therefore, is -concave as the minimum of two -concave functions. However, at , we compute

This is contradictory to the fact that is the -concave envelope. Therefore, there should exist such that .

∎

Next, we demonstrate that any incentive compatible contract must be in the form of that defined above. This will suggest that it is in fact optimal for the principal to choose a contract of this form.

Proposition 2.

Suppose that is incentive compatible with . Then, the following must hold:

| (5) |

for some constant , where such that for a.e.

Proof.

Let and satisfy the incentive compatibility constraint. Define

By the Martingale representation theorem (e.g., [11, 16]), there exists a unique (up to a set of zero measure) process such that

where . Then, we have

Next, we show that for a.e. Suppose that for , where is a set of a strictly positive -measure. By the first claim in Lemma 1, we can find such that

Then, the agent would prefer to follow over because

But this contradicts the incentive compatibility of the contract, so for a.e. ∎

The compensation given solely by (5) is -measurable and may not be in . In Theorem 1, we will design an optimal contract in a relaxed space such that (5) holds, and show that at an optimum the compensation is in and therefore is implementable.

Next, we show that the principal should only consider contracts with the suggested effort such that for a.e. Any other suggested effort would not be incentive compatible.

Proposition 3.

For any incentive compatible contract, we have

where

Proof.

By Proposition 2, the compensation of any incentive compatible contract must be of the form

with such that for a.e. given . Suppose that for , where is a set of a strictly positive -measure. By Lemma 1, we can find such that

But we can check, the agent would prefer to follow over since

But this contradicts the incentive compatibility of the contract, so for a.e. ∎

Finally, because is strictly decreasing, we can argue that it suffices to consider contracts with . This choice makes the individual rationality constraint binding. Any larger choice of would be sub-optimal for the principal.

Up to this point, we have made no reference to the payment that the principal receives at the terminal time, which can be quite general. We have restricted the class of admissible compensation schemes for the agent, but which of the remaining the principal chooses will depend upon . In particular, the principal will solve an optimization problem summarized in the following theorem:

Theorem 1.

Proof.

By Propositions 2 and 3, incentive compatible contracts are characterized by

for , such that and such that for a.e. By the same computation as in Proposition 3, we observe that is individually rational for the agent if and only if

Now suppose has . Then, we define a new utility,

Note that both and satisfy the incentive compatibility and individual rationality conditions. However, we have

because is strictly decreasing and almost surely. Therefore, we conclude it is optimal for the principal to choose .

Let and solve the optimization problem (6). We now show that given by (7) with and is in and therefore is implementable. The problem (6) can be rewritten as the following stochastic optimal control problem:

which can be solved by dynamic programming. Its solution is given by a feedback control, . Since is adapted to , so are and . Therefore, given by (7) with and is -measurable and therefore is in . ∎

In summary, we have converted a quite general two-player principal-agent with individual rationality and incentive compatibility constraints into an equivalent stochastic optimal problem with only point-wise restrictions on the values of the effort process. The idea in the remainder of the paper will be to iterate this choice with explicit choices of to solve Player 0’s problem in the principal-agent hierarchy.

4 Contract for Principal-Agent Hierarchy

Our goal here is to inductively apply the result from above. The hope is that Player 0 can design compensation in such a way that Players 1 through Player will find it optimal to follow the desired efforts.

Theorem 2.

Suppose that for . Let

| (8) |

with , , , for . Let be the concave envelope of and . Set as -concave envelope of and as the corresponding touching set for .

The intuition behind this result is that by choosing a compensation scheme of the form , Player 0 can incentivize every player below him in the hierarchy to follow a ‘suggested effort’ process . However, it is only possible for Player 0 to incentivize the hierarchy to follow efforts .

The function represents the cost to Player 0 for incentivizing the hierarchy to perform . The constant represents a minimum expected utility Player 0 must provide to satisfy the entire hierarchy’s individual rationality contraints. Intuitively, the function encodes information about incentive compatibility conditions.

Proof.

We proceed by induction. In the base case, we fix a choice of . Player will then solve the following optimization problem:

This falls in the form of the generalized two player principal-agent problem. Therefore, we can define the compensation as

where such that for a.e., and is the standard concave-envelope of . Define the set

Due to Theorem 1, it is equivalent for Player to solve

Next, we consider the inductive step. For fixed , Player solves the following optimization problem:

The inductive assumption is that it is equivalent for Player to solve

where

| (10) |

given , concave, and

with and , .

We next fix and focus on the analogous optimization problem for Player . Player chooses and subject to incentive compatibility and individual rationality for Player through Player . By the inductive hypothesis, incentive compatibility and individual rationality for Players is equivalent to considering of the form (10). Therefore, we can write the optimization problem of Player as

We note that it is now in the form of a generalized principal-agent problem. Furthermore, with this choice of , we can re-write the utility for Player as

Define

By Theorem 1, it is equivalent for Player to solve:

where

is the -concave envelope of , and is the corresponding touching subset.

By induction, we conclude that it is equivalent for Player 0 to solve the following optimization problem:

where

where and are given by (8), is -concave envelope of , and is the corresponding touching set. ∎

Remark 1.

Although we do not explicitly state the form of in Theorem 2, the details of the proof reveal that they will each be as follows:

where

with , and , , and

| (11) |

with defined in Theorem 2. The particular choice of will not affect the utility for Player 0, whenever (11) holds, because it only depends upon . The function represents the cost that Player must pay for incentivizing the hierarchy from Player to Player to follow the suggested effort . The scalar constant represents a minimum expected utility that Player must provide to satisfy the individuality rationality constraints for Players . By using the argument in Theorem (2), we can confirm that is -measurable. Therefore, an optimal contract obtained by the proposed method is implementable. Furthermore, it is verifiable because an optimal is adapted to .

We refer to the components and as ‘suggested’ efforts and compensations because Player 0 does not have to force the other players to choose them – we have shown it is optimal for players lower in the hierarchy to construct these contracts on their own. For this reason, we do not explicitly write them down in the theorem statement.

At this point, Player 0 can solve this equivalent optimization problem via the dynamic programming principle and an associated Hamilton-Jacobi-Bellman equation. Player 0’s optimization problem has a running cost associated with the choice of and , as well as a terminal compensation associated with . Then, it is natural to introduce a state variable with the property that :

Definition 5.

Given a choice of processes , we define the continuation value of the aggregate agents as

Then, .

Remark 2.

The term ‘continuation value’ refers to the characterization of as the expected remaining utility for Player 1 at time conditioned on the information up to , assuming he follows the suggested effort. In particular, we have

Therefore,

By viewing as a state variable of a (stochastic) dynamical system, we can now apply the dynamic programming principle to solve the reformulated optimization problem (9).

Theorem 3.

Define the value function for Player 0 as

Then, is the unique viscosity solution to the following Hamilton-Jacobi-Bellman equation:

with terminal condition .

Proof.

If there exists a smooth enough solution to this HJB, then by standard stochastic control arguments, we can construct optimal feedback controls:

Then, using these feedback controls and the dynamics of , ever player in the hierarchy can compute in terms of observed values. Specifically, we have

Namely, all three processes – , , and – are adapted to , and . Therefore, the proposed contract is implementable and verifiable.

Player 0 then agrees to pay Player 1 an amount , where is evolved via the optimal feedback controls. Player 0 announces the contract and suggested efforts and compensations. Then, we have shown that it is optimal for the rest of the principal-agent hierarchy to follow and .

One major advantage of this hierarchical model is the dimensionality of the resulting PDE – only one-dimensional in space. In comparison, the model with multiple agents reporting to a single principal in [8] resulted in a PDE with one state variable for each agent. Therefore, this hierarchical model is very tractable for even large . It is worth noting, however, that this particular dimensionality result depend on the risk-neutrality of terminal payoffs between agents in the hierarchy. Another important feature of the proposed approach is that (and ’s) can be parameterized by a homeomorphism whose domain is one-dimensional when the players’ utility functions are strictly concave. This feature yields the maximization problem in the Hamiltonian of the HJB equation to be one-dimensional at each time. This additional dimensionality reduction result will be provided in Theorem 4.

5 Details on -Concave Envelopes

In the previous iterative construction of an incentive compatible contract for the principal-agent hierarchy, the key condition for iteration is -concavity. A simpler version of this condition was first highlighted in [8], but details were not provided on how to check -concavity or construct appropriate envelopes.

In this section, we provide a general construction of -concave envelopes of a function , and also provide structural results about the subset where .

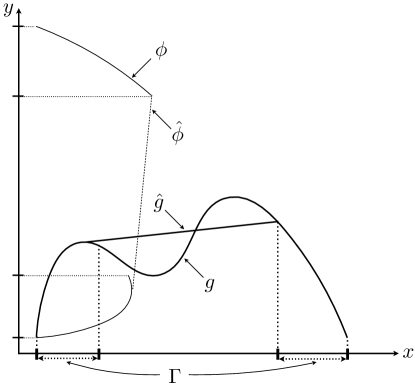

5.1 Constructing -Concave Envelopes

Recall from the definition in Section 3 that the key properties of the -concave envelope are (1) -concavity, (2) majorizing the function over , and (3) minimality. All three properties are intuitively represented by a step in the construction in this section.

We construct the -concave envelope of in the following three steps:

-

1.

Define , where we set if .

-

2.

Compute the concave envelope of , then

-

3.

Define .

An example of the proposed construction is shown in Figure 2.

Proposition 4.

For any , the function , as constructed above, is the -concave envelope of .

Proof.

By construction, is -concave and majorizes over . Suppose there exists which is -concave, majorizes over , and is smaller than at some point , i.e.,

| (12) |

Because majorizes over , we have

Then, recalling that when , we conclude that

which contradicts (12) because is the concave envelope of . ∎

5.2 Sufficient Conditions for to be One-Dimensional

In this section we prove that if all players have utilities which are strictly concave in effort, then for Player 0 is parameterized by a homeomorphism . The significance of this result is that it provides dimensionality reduction in Player 0’s optimization problem. In particular, rather than maximizing over a potentially -dimensional subset , Player 0 can maximize over values in using the map . In the lack of strict concavity, the dimension of is not necessarily reduced.

First, we prove an abstract result.

Lemma 2.

Let be continuous. Suppose that is strictly concave for each . Then, the function defined as

is continuous.

Proof.

By strict concavity of for each , we conclude that is a well-defined function.

Suppose that is not continuous at . Then there exists and a sequence such that . Define

which is strictly positive by strict concavity in .

By continuity of , we can find such that

Now, we verify two inequalities

But by strict concavity of , this implies

which contradicts . ∎

Next, we prove the main argument which will be iterated.

Lemma 3.

Let continuous. Let be parameterized by a homeomorphism such that for all . Suppose that is jointly concave and, further, that is strictly concave for all . Let , be the -concave envelope of , and the corresponding touching set be

Then, is parameterized by a homeomorphism such that for all . Furthermore, is concave.

Proof.

We note that for every , we can parameterize the set

by the map . By the strict concavity of this map, we apply Lemma 2 to conclude that the map

is continuous.

Next, we compute

By strict concavity of , we conclude that the supremum is attained at a single point for each . The pointwise supremum of the jointly concave map is concave, as shown in [3], so is concave. Therefore, , and .

Define a new function as:

By continuity of , is continuous. We can also check, , so is concave for all .

We claim that the image of is . By definition,

Finally, we confirm that

which implies is one-to-one and an open map, so we conclude is a homeomorphism. ∎

The intuition of the following main result is to apply Lemma 3 iteratively. At each step, represents the effective utility of Player over . By induction, we assume is one-dimensional and parametrized by a homeomorphism , so Player effectively maximizes over . We show under concavity assumptions that is then once again one-dimensional.

Theorem 4.

If each player’s utility function is strictly concave and , then is parameterized by a homeomorphism .

Proof.

First, recall from the iteration argument that at each stage, is a linear combination of with positive coefficients. Furthermore, at each step, is the touching set corresponding to the -concave envelope of .

We want to show that for each , is parameterized by a homeomorphism such that and is concave. We proceed by induction on .

In the base case, we know , and this can be parameterized by the identity map . The concavity condition holds by concavity of .

Now, consider the Player ’s effective utility function, which is given by

By the inductive hypothesis, there is a bijection such that and is concave.

In particular, we can confirm that

is strictly concave in and jointly concave in . The right-hand-side is jointly concave in as the composition of an affine function with , which is concave by the inductive hypothesis. Because is strictly concave, we determine the sum is strictly concave in and jointly concave in .

Furthermore, by the inductive hypothesis . Therefore, we can apply Lemma 3 to conclude the -concave envelope of has a corresponding touching set which is parameterized by a homeomorphism such that and is concave. Then, the result follows by induction. ∎

The significance of this result is in reducing dimensionality in Player 0’s optimization problem at each time step of dynamic programming from potentially -dimensional to one-dimensional. In particular, Player 0 can maximize any function by maximizing .

Practically, this result means that in the case of strictly concave utilities, not only is the HJB PDE only one-dimensional in space, but the maximization step for computing an optimal Hamiltonian at each time is also one-dimensional. This means that once is computed, Player 0’s optimal dynamic contract can be constructed in time that does not depend upon the size of the hierarchy. This result makes the model tractable even for very large and contributes significantly to the tractability of using dynamic programming to design an optimal contract in a large-scale principal-agent hierarchy.

6 Example: Quadratic Utilities

In this section, we work through a specific example, where all agents have quadratic utilities. In particular, we set

with and for all . Finally, we choose

Economically, this means each player has an increasing aversion to putting in effort personally, which is governed by the parameter . Furthermore, each player has some aversion to paying the player below him in the hierarchy, which is governed by the parameter . Player 0 is averse to uncertainty in the terminal payment to players below him.

In order to construct an optimal dynamic contract, we need to explicitly perform the iterative construction of Section 4. Because each utility function is assumed strictly concave, we can also apply the results of Section 5 to obtain a homeomorphism at each step. In the quadratic utility case, it will turn out that each will be a one-dimensional linear subspace. We will see that the iteration process only requires linear algebraic computations at each step.

Theorem 5.

There exists a strictly positive-definite, diagonal matrix , a vector with , and a real number such that it is equivalent for Player 0 to solve the following optimization problem:

with the compensation scheme given by

where:

-

•

,

-

•

, so , and

-

•

is a one-dimensional subspace parametrized the isomorphism .

Proof.

We follow the iteration argument of Theorems 2 and 4 to construct each , , and the homeomorphism . For Player , we trivially have that , , and the homeomorphism is is the identity .

Consider Player with . We know by Theorems 2 and 4 that there exist , , and a homeomorphism such that .

We suppose further that there exists a strictly positive-definite matrix and vector with the property such that and .

Then by Theorem 2, can be written:

or in the form for a strictly positive-definite, diagonal matrix.

By Theorem 4, we need to compute the functions , and . We can compute:

and then immediately, we have

for a vector computable in terms of and . Further, we have , so .

Lastly, we have

By induction, the result follows. We note that because is linear, then is a one-dimensional linear subspace. ∎

Then, as in Theorem 3, Player 0 can define a value function and characterize it as the unique viscosity solution to an HJB equation. However, in this case, the HJB equation simplifies considerably:

Corollary 1.

Define the value function for Player 0 as in Theorem 2. Then is the unique viscosity solution to the Hamilton-Jacobi-Bellman equation:

with terminal condition and .

The proof is just a particular case of Theorem 3. The significance is that, in this case, the HJB reduces to only one state variable and a one-dimensional maximization over at each time.

Acknowledgement

The authors would like to thank Professor Lawrence Craig Evans for helpful discussions on PDE approaches for principal-agent problems.

References

- [1] F. Antonelli, Backward-forward stochastic differential equations, The Annals of Applied Probability, 3 (1993), pp. 777–793.

- [2] T. Başar and G. J. Olsder, Dynamic Noncooperative Game Theory, SIAM, 1995.

- [3] S. Boyd and L. Vandenberghe, Convex Optimization, Cambridge University Press, 2004.

- [4] J. Cvitanić, X. Wan, and J. Zhang, Optimal compensation with hidden action and lump-sum payment in a continuous-time model, Applied Mathematics and Optimization, 59 (2009), pp. 99–146.

- [5] J. Cvitanić and J. Zhang, Contract theory in continuous-time models, Springer, 2013.

- [6] I. Ekeland, How to build stable relationships between people who lie and cheat, Milan Journal of Mathematics, 82 (2014), pp. 67–79.

- [7] L. C. Evans, Partial differential equations, American Mathematical Society, second ed., 2010.

- [8] L. C. Evans, C. W. Miller, and I. Yang, Convexity and optimality conditions for continuous time principal-agent problems, (in preparation).

- [9] W. H. Fleming and H. M. Soner, Controlled Markov processes and viscosity solutions, vol. 25, Springer, second ed., 2006.

- [10] B. Holmstrom and P. Milgrom, Aggregation and linearity in the provision of intertemporal incentives, Econometrica, 55 (1987), pp. 303–328.

- [11] I. Karatzas and S. E. Shreve, Brownian Motion and Stochastic Calculus, Springer, second ed., 1991.

- [12] J.-J. Laffont and D. Martimort, The Theory of Incentives: The Principal-Agent Model, Princeton University Press, 2002.

- [13] J. Ma and J. Yong, Forward-Backward Stochastic Differential Equations and their Applications, Springer-Verlag, 1999.

- [14] R. P. McAfee and J. McMillan, Organizational diseconomies of scale, Journal of Economics and Management Strategy, 4 (1995), pp. 399–426.

- [15] N. D. Melumad, D. Mookherjee, and S. Reichelstein, Hierarchical decentralization of incentive contracts, The RAND Journal of Economics, 26 (1995), pp. 654–672.

- [16] B. Øksendal, Stochastic Differential Equations, Springer, sixth ed., 2003.

- [17] H. Ou-Yang, Optimal contracts in a continuous-time delegated portfolio management problem, The Review of Financial Studies, 16 (2003), pp. 173–208.

- [18] S. Peng and Z. Wu, Fully coupled forward-backward stochastic differential equations and applications to optimal control, SIAM Journal on Control and Optimization, 37 (1999), pp. 825–843.

- [19] Y. Qian, Incentives and loss of control in an optimal hierarchy, The Review of Economic Studies, 61 (1994), pp. 527–544.

- [20] Y. Sannikov, A continuous-time version of the principal-agent problem, The Review of Economic Studies, 75 (2008), pp. pp. 957–984.

- [21] , Contracts: The theory of dynamic principal-agent relationships and the continuous-time approach, (2012).

- [22] J. Sung, Pay for performance under hierarchical contracting, Mathematics and Financial Economics, 9 (2015), pp. 195–213.

- [23] N. Van Long and G. Sorger, A dynamic principal-agent problem as a feedback Stackelberg differential game, Central European Journal of Operations Research, 18 (2010), pp. 491–509.

- [24] T. A. Weber, Optimal control theory with applications in economics, MIT Press, 2011.

- [25] N. Williams, On dynamic principal-agent problems in continuous time, Working paper, (2009).

- [26] I. Yang, D. S. Callaway, and C. J. Tomlin, Dynamic contracts with partial observations: application to indirect load control, in Proceedings of 2014 American Control Conference, 2014, pp. 1224–1230.