Sequential Monte Carlo for fractional Stochastic Volatility Models

Abstract

In this paper we consider a fractional stochastic volatility model, that is a model in which the volatility may exhibit a long-range dependent or a rough/antipersistent behavior. We propose a dynamic sequential Monte Carlo methodology that is applicable to both long memory and antipersistent processes in order to estimate the volatility as well as the unknown parameters of the model. We establish a central limit theorem for the state and parameter filters and we study asymptotic properties (consistency and asymptotic normality) for the filter. We illustrate our results with a simulation study and we apply our method to estimating the volatility and the parameters of a long-range dependent model for S& P 500 data.

Keywords: long memory stochastic volatility, rough stochastic volatility, parameter estimation, particle filtering.

1 Introduction

Empirical studies show that the volatility may exhibit correlations of the squared log returns that decay at a hyperbolic rate, instead of an exponential rate as the lag increases, see for example [6], [16]. This slow decay cannot be explained by a GARCH stochastic volatility model or by a stochastic volatility model with jumps. In the literature, this behavior has been described by a class of models that exhibit long-range dependence in the volatility. In contrast to the models where the dependence is introduced in the stock returns, [32], the standard assumption of absence of arbitrage opportunities is preserved. The first long memory stochastic volatility (LMSV) model was introduced in discrete time by [6] and [26]. In particular, the authors model the stock returns by:

where , are independent and identically distributed (iid) , are iid and independent with and is the memory parameter. The feature of long-memory here stems from the fractional difference , where denotes the lag operator, i.e. .

The continuous analogue of the LMSV model was introduced by Comte and Renault in [10] as a continuous-time mean reverting process in the Hull-White setting. More specifically, their model resembles a classical stochastic volatility model in which the log returns follow a Geometric Brownian Motion , however, the volatility process is described by a fractional Ornstein-Uhlenbeck process; that is the standard Ornstein-Uhlenbeck process where the Brownian motion is replaced by a fractional Brownian motion.

A large number of recent papers have considered modeling the volatility in terms of long-range dependent or antipersistent processes. In [11], the authors propose an affine version of the long memory model in [10] for option pricing and they argue that long-range dependence provides an explanation for observations of non-flat term structure in long maturities. In [8], [9], the authors propose a pricing tree algorithm in order to compute option prices in the discrete and continuous time frameworks. They also propose a calibration method for determining the memory parameter. In [3], [21], the authors propose a rough fractional stochastic volatility model, which is used to explain strong skews or smiles in the implied volatility surface for very short time maturities. In a more recent paper, [20], the authors discuss the case of small volatility fluctuations of both short and long memory models and their impact on the implied volatility and derive a corrected Black-Scholes formula.

In this article, we address two problems: filtering of the unobserved volatility and parameter estimation in the case of a stochastic volatility model that is either rough or antipersistent. Specifically, we adapt a Sequential Monte Carlo algorithm in the non-Markovian framework and then we estimate the parameters online, following an idea initially introduced by [30].

Sequential Monte Carlo (SMC) methods, also known as particle filters or recursive Monte Carlo filters, arose from the seminal work of Gordon, Salmond and Smith (1993), [22]. SMC methods are iterative algorithms that are based on the dynamic evolution and update of discrete sets of sampled state vectors, that are referred to as particles, and are associated with properly selected weights. For an introduction to the SMC literature, there are several reviews and tutorials, including, the edited volume by Doucet, Freitas and Gordon (2001), [17] and Kantas et al. (2010), [28].

In order to keep the adaptive nature of the SMC algorithm, we incorporate the parameter estimation procedure in the algorithm by treating the parameters as artificially random, sampled from a kernel density. Generally speaking, the approach relies on augmenting the unobserved state by considering the parameter as an unobserved state. We do not assume that the unknown parameter is fully random, and thus we do not have an additional MCMC step in the algorithm. We emphasize here that this is an important point, due to the heavy computational overhead caused by the long-memory issue. Also, as it is well known, using SMC for maximum likelihood based methods for estimating parameters like the Hurst parameter is difficult.

The output of the algorithm is a provably asymptotically consistent estimator along with the corresponding variance. One of the appeals of the proposed method is the simplicity in its application, which becomes in particularly important due to the memory issue. However, we do mention here that overdispersion due to the artificial random evolution of the parameter is an issue that comes up with such methods, see for example [13]. But, as we shall see, the overdispersion that the artificial random evolution of the parameter introduces, can be minimized by properly tuning the parameters of the mixture distribution used for sampling the parameter. Related works using different methods can be found in [2, 31].

The study of the asymptotic properties of SMC methods and the asymptotic properties of the filter as the number of particle increases is a quite hard problem. A form of consistency of the filter, when the number of particles tends to infinity is a common result in the majority of the literature, while central limit theorem type of results are fewer. One can refer, for example, to the work of Del Moral and Guionnet (1999), [15]. To the best of our knowledge, the most general results in the literature can be found in Chopin (2004), [12], Douc and Moulines (2008), [18], and Künsch (2005), [29]. In these works and under slightly different conditions, law of large numbers and central limit theorems are derived that apply to most sequential Monte Carlo techniques in the literature.

The rest of the paper is organized as follows: In Section 2, we introduce the mathematical formulation of the problem. In Section 3, we introduce the SISR (Sequential Importance Sampling with Resampling) method with parameter learning and we present the theoretical results for the proposed parameter estimators. In Section 4, we study the performance of both methods using simulated data. In Section 5, we apply our method in estimating the unobserved volatility of a discrete-time stochastic volatility model with long-range dependence for S& P 500 data. Finally, we summarize our results in Section 6.

2 Mathematical Framework

Consider a state-space model in which the state vector is denoted by and the observations are obtained sequentially in time. In addition, we assume that the state vector depends on an unknown, but fixed, parameter vector that we denote by . In the sequel, we use the notation or for the random variables and or for the corresponding realized values.

Unlike other models in the literature, we do not assume that the state vector is a Markovian process. Instead, we consider the case in which the unobserved process is not necessarily Markovian, with particular interest in the long-range dependent case. Formally, long-range dependence or long-memory is defined as follows:

Definition 1.

For a stationary process , there exists a parameter (Hurst index) , such that

| (1) |

where is the autocorrelation function of the process.

When , then the process is Markovian, so this is a generalization of the models that are treated in the SMC literature. Equivalently, long-range dependence implies that the autocorrelation function of a long-range dependent process is non-summable, that is . If the auto-correlation function is summable, then the process has what is called antipersistence, in which case .

Formally, at time , the state-space model is specified by the observation equation that is determined by the observation density

and the state equation given by the conditional density

where is an unknown vector of parameters, and is open. We assume that the observations are conditionally independent given and that the long-range dependent process has known initial density .

In this article, our goal is to use simulation for online filtering. In other words, we want to learn about the current state given available information up to time , which reduces to estimating the probability distribution function

where are the observations up to time . However, since we assume that the parameter is unknown, at the same time we also want to estimate .

3 Sequential Monte Carlo Filtering

As we mentioned above, apart from filtering for the unobserved states we also want to estimate the unknown parameter vector on which the state vector depends. Our approach will be to consider as an additional state and thus our goal will be to estimate the posterior distribution given by

| (2) |

where is a prior density for the parameter vector , see Subsection 3.1. If the parameter is known, then the density is degenerate. Therefore, the additional difficulty here is that we need to compute or approximate the theoretical density function .

3.1 On-line Parameter Estimation

One approach in the literature ([19], [22], [34], [30]), is to consider that is not fixed and assume that it artificially evolves in time, for example

where is an artificial white noise with decreasing variance. Then, at each time , will be updated inside the SISR algorithm in order to incorporate the additional information that is obtained.

As it was discussed in [30], this approach leads to artificial variance inflation, since the parameter is not truly random. However, the use of a kernel density estimate with shrinkage correction can control this artificial over-dispersion.

More specifically, standing at time , we approximate by a set of samples and weights using a discrete Monte Carlo. The index in is in parenthesis to indicate that does not evolve in time, but that its value is drawn from the posterior density at time . Then, the smooth kernel density with shrinkage correction will be of the form

where denotes a multivariate Normal density with mean and variance . So, essentially, is approximated by a mixture of normals with mean and variance , weighted by sample weights . The kernel location is specified by

where and denotes the average over all parameter samples (essentially a sum over ). Regarding , a typical choice would be a decreasing function of the sample size, but if one wants to control the loss of information then , where is a discount factor typically around and becomes .

Therefore, the SISR algorithm is adjusted in order to incorporate the update of . The key idea of our approach that also allows us to establish asymptotic consistency and normality of the estimators, is to re-formulate the weights so that they represent the joint posterior and update along with the state vector .

Before presenting the algorithm, let us define the un-normalized weight functions. For , and set

| (3) |

Generally for

| (4) |

Then, the algorithm is given by:

At time

-

(a)

Sampling

For , sample and . -

(b)

Re-Sampling

For , let be defined by (3), normalize , such that and re-sample

At time (step )

-

(a)

Sampling

For , setwhere , sample

and

where .

-

(b)

Re-Sampling

For , let be defined by (4), and normalize , such that .For , re-sample

and set

Output The filtering distribution is approximated by

and the estimator for is . We also record the approximation for the combined distribution which is approximated by

3.2 Convergence Results

Let us now study the convergence properties of this algorithm. Let be an appropriate test function. Notice now that the SISR algorithm provides us with the estimator

It is relatively straightforward to see that is estimating

where is the value that is drawn from the posterior density at time .

So, it is natural to quantify the performance of the algorithm by studying the convergence of to as . We define the set of appropriate test functions under which a central limit theorem can be established, appropriately formulated for our case of interest:

| (5) |

Following the proof of the central limit theorem results of [12, 27] for the Markovian case, without the parameter estimation aspect, the following result is derived.

Proposition 1.

Let us assume that there exists such that for every and consider . Then, we get

as , where at time

and for

Proof.

The proof follows from Proposition A.1.1 of [27] after making the adequate identifications. Indeed, for a general sequential importance sampling algorithm with weights , Proposition A.1.1 of [27] implies that the formula for the variance in question is given by

In our case we have

and the weights take the form

Plugging these expressions in the formula for one immediately recovers the form of , completing the proof of the proposition. ∎

3.3 Statistical properties of the parameter estimator

Essentially, is viewed as an augmented state variable. Proposition 1 quantifies the convergence of the filter, but it does not discuss the statistical properties of . Let us recall that

where

By inspecting the algorithm it becomes clear that the convergence properties of as is described by a statement very similar to that of Proposition 1 after making the choice . Proposition 2 shows that at time , the estimator for , converges to as .

Proposition 2.

Let us assume that there exists such that for every and consider the function identity , assuming that it belongs to the set of appropriate test functions defined in (5). Let us also define the mean of the posterior distribution

Then, we get

as . The asymptotic variance is defined as follows. At time

and for

| (6) |

Proof.

This proposition is essentially a special case of Proposition 1 with . We notice that

which is the mean of the posterior distribution , as claimed. ∎

The next natural question to ask is whether is a consistent estimator of as . Let us recall from Subsection 3.1 that choosing around implies for the tuning parameters . Subsequently, this means, for every fixed , that the mean and the variance , which then implies that for every , . Notice that if the tuning parameters then the distribution coincides with the posterior distribution , as the parameter does not involve artificially in time any more. Hence, in this case, by Doob’s consistency theorem, see for example Theorem 10.10 in [33], we would have that the sequence of posterior measures is consistent under if the model is identifiable, i.e., if for . In other words, in such a case, for every prior probability measure on the sequence of posterior measures is consistent for almost every . However, in the algorithm and for the purposes of dealing with the issue of degeneracy of the particles, we artificially evolve the unknown parameter which means that we take the tuning parameters to be but not exactly equal to . As we shall see from the simulation studies of Section 4, this is sufficient to guarantee that the parameter is being consistently estimated, as expected.

4 Simulation Results

4.1 Fractional ARIMA process

The fractional ARIMA (AutoRegressive Integrated Moving Average) process was proposed by Box and Jenkins, [5], in 1970 and has been very popular in applied time series. A fractional ARIMA() process is formally defined as follows (due to Granger and Joyeux, [23]):

Definition 2.

Let and be polynomials of orders and respectively and a stationary process such that

and and is a sequence of iid variables with mean and variance . Then, the process is called a fractional ARIMA() process.

In contrast to the classical ARIMA() process, where the parameter is an integer, in the fractional case is a real valued parameter with values between . It is called the fractional integration parameter and is related to the Hurst index, in (1), via . denotes the lag or backshift operator, and

where the sum is taken over an infinite number of indices. The fractional ARIMA process is long-range dependent when , while the upper bound on is needed to ensure that the process is stationary. More details regarding these models can be found in Beran [4].

In our framework, we consider a state-space model in which the unobserved process is modeled by a Fractional ARIMA process. Specifically, the state-space model is defined as follows

| (7) |

where and are two independent iid sequences of Gaussian random variables and is a known function.

4.1.1 SISR for Fractional ARIMA process with known parameter

We apply our algorithm to simulated data from an ARIMA(1, 0.3, 0) model with parameter . That is

| (8) |

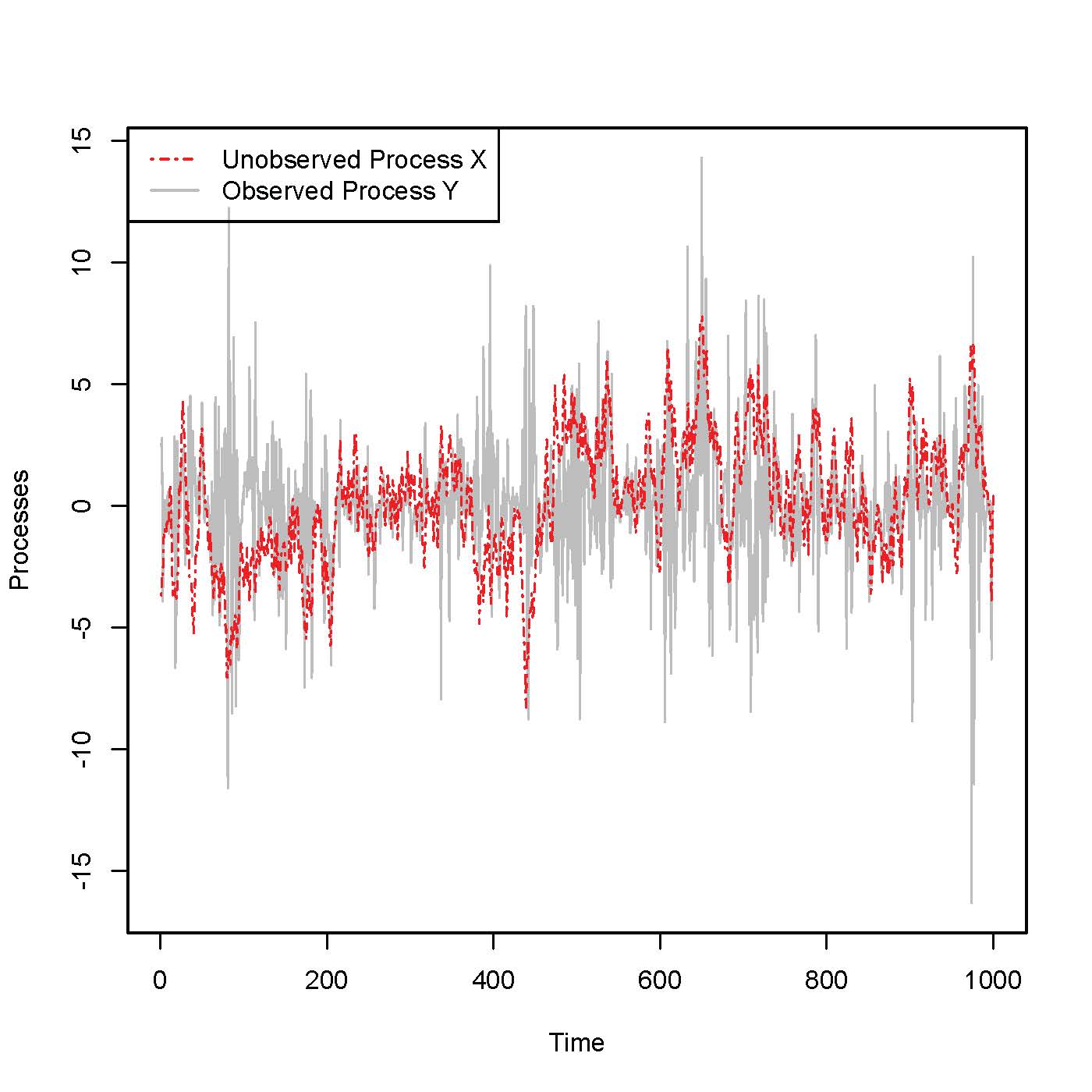

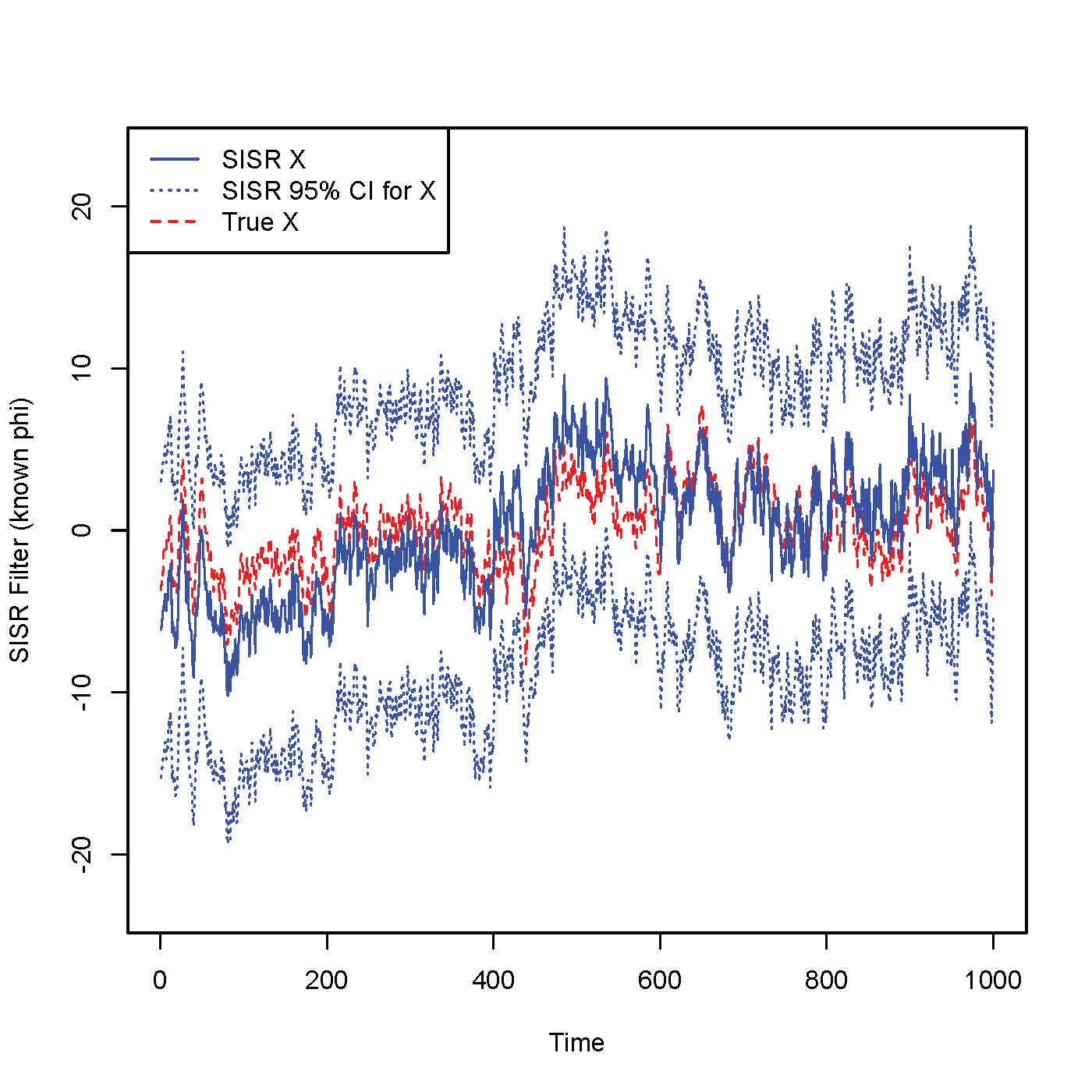

The simulated model is shown in Figure 1(a) and the estimated filter using the SISR algorithm is depicted in Figure 1(b). We choose as tuning parameters which then implies .

|

|

| (a) Simulated Model | (b) SISR Filter |

From the SISR plot (Figure 1b), we can see that the approximation of the unobserved process (solid line) follows closely the true process (dashed line). In addition, the true data, all lie within the 95% confidence interval (dotted lines) estimated using the SISR algorithm. In our simulation study, we tried different values of and the results are similar.

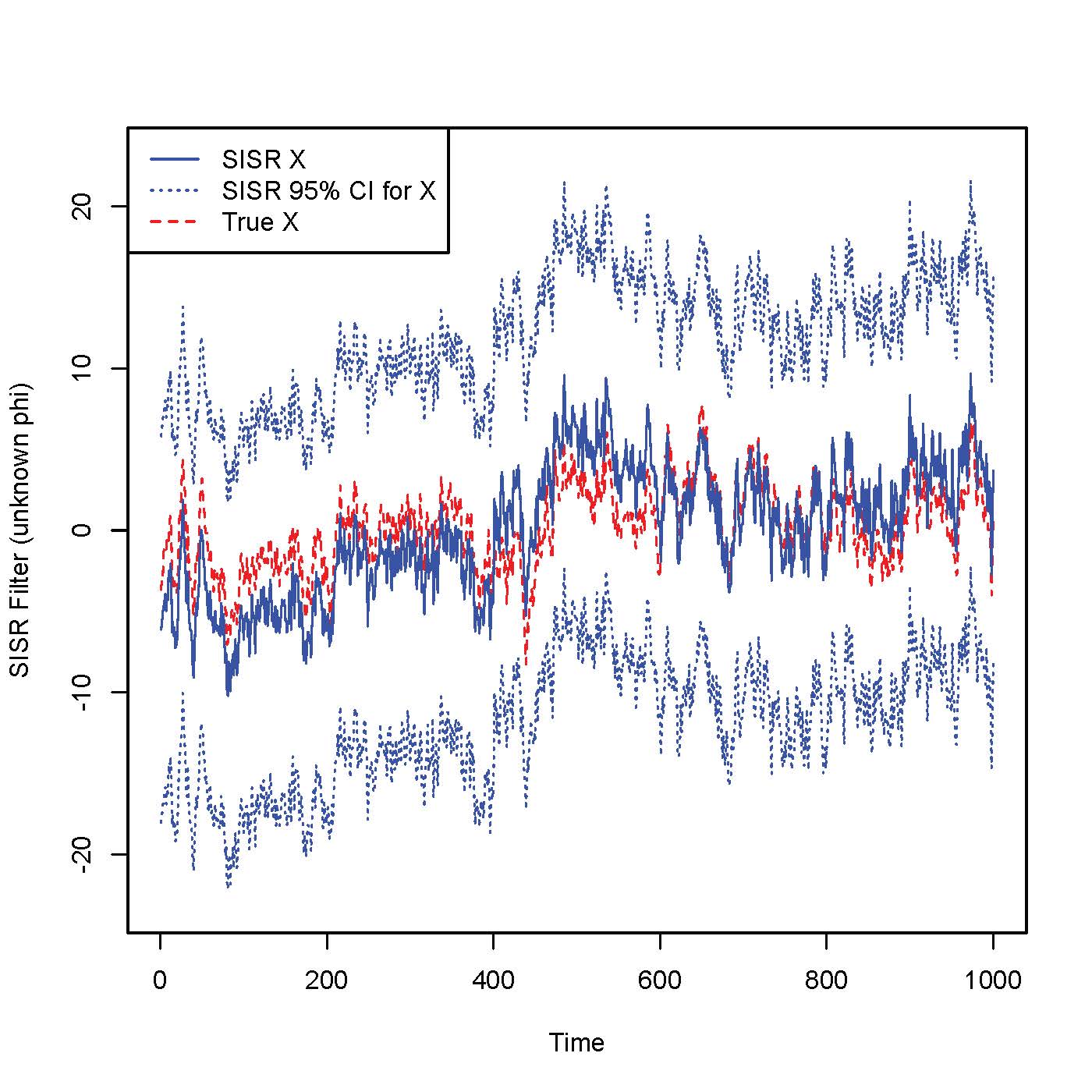

4.1.2 SISR for Fractional ARIMA process with unknown parameter

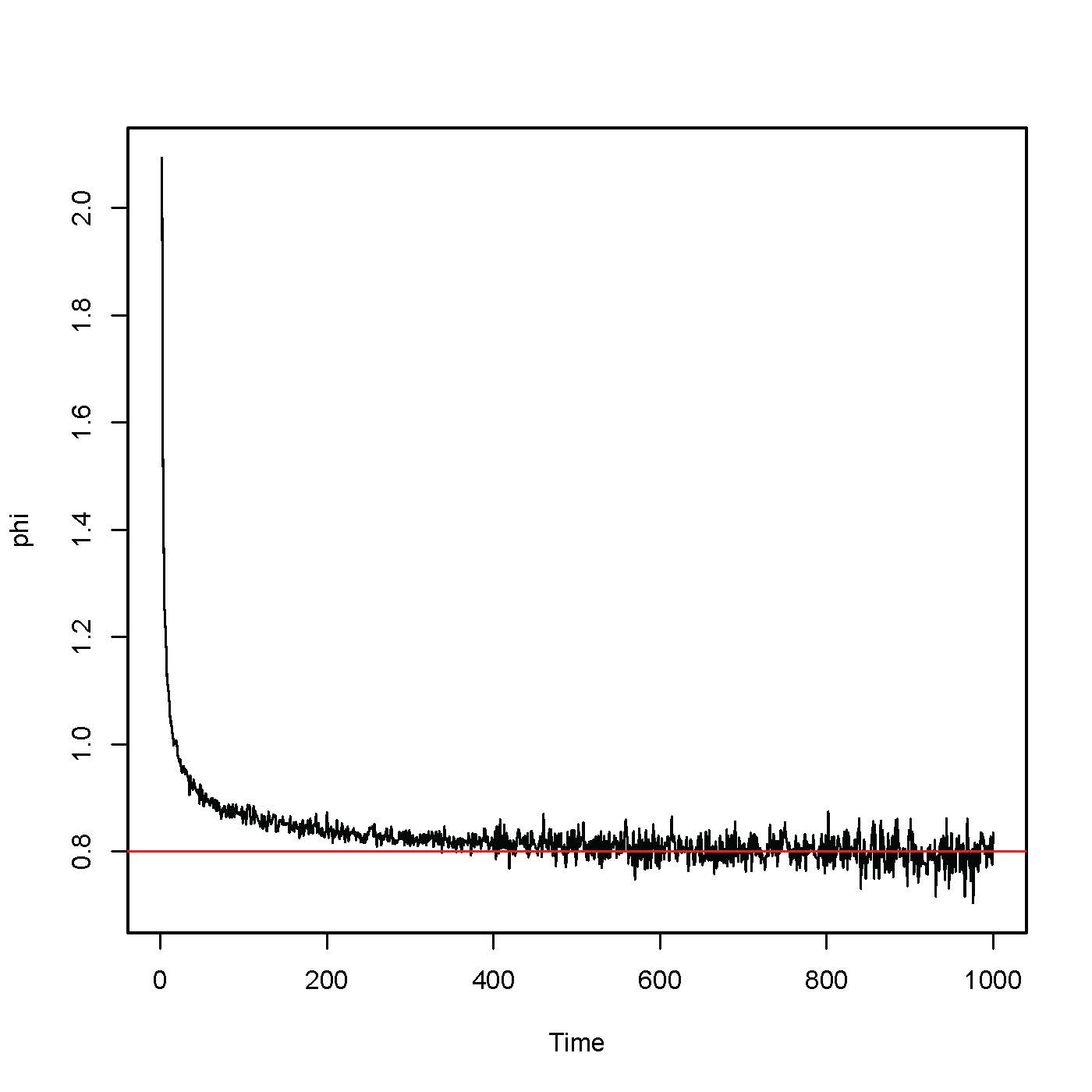

Consider again model (8), but now assume that the parameter is unknown. Our goal is to estimate using the SISR algorithm. The results are summarized in Figures 4 and 3. From Figure 4, we can see that the approximation of the unobserved process remains good, and the 95% confidence interval still captures the process.

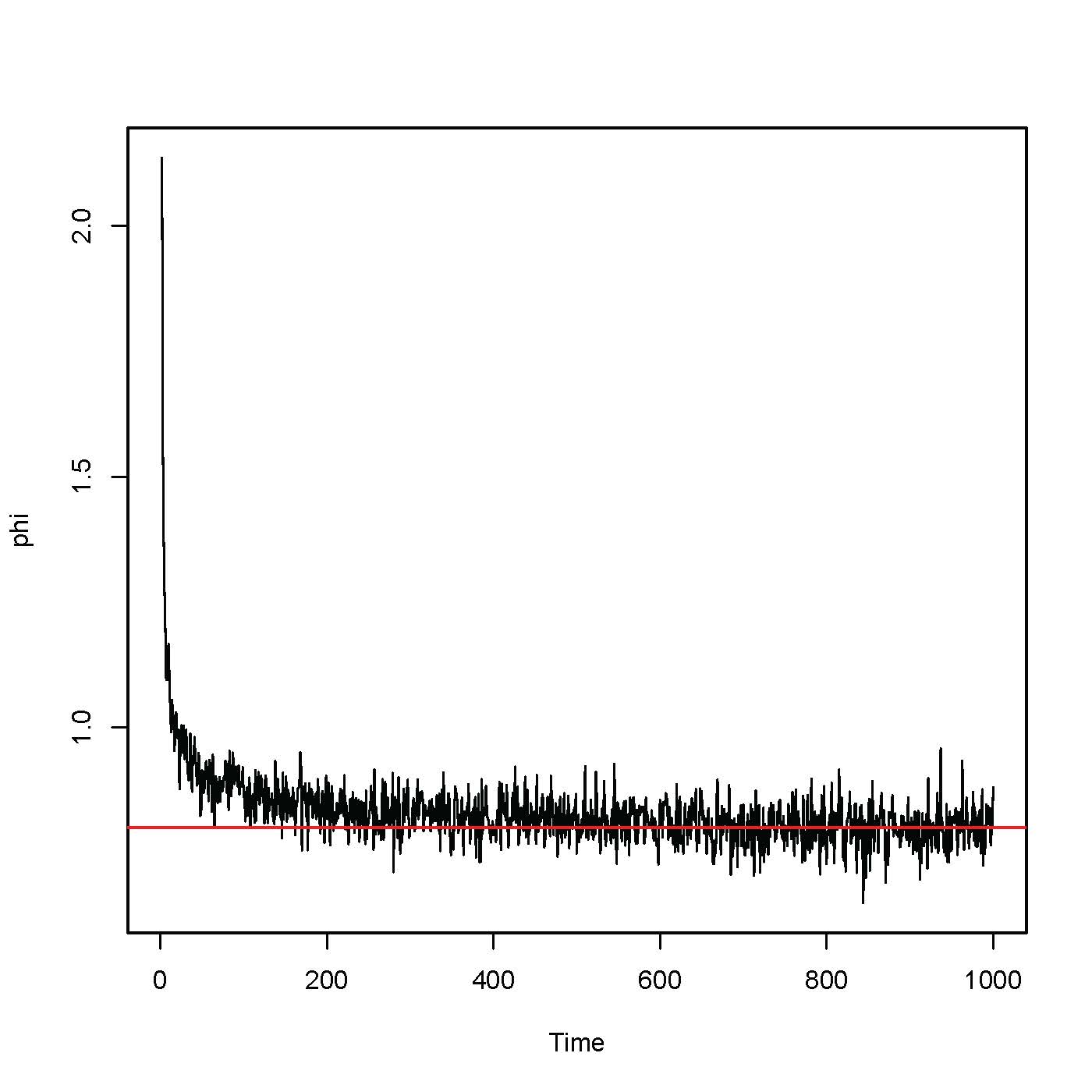

In Figure 3, we investigate the convergence of the parameter to the true value. The estimated parameter is slightly noisy, but it converges to the true value 0.8. The difference in the two graphs in Figure 3, is that the second one has a significantly larger number of simulated particles, and it seems that this slightly improves the smoothness of the curve.

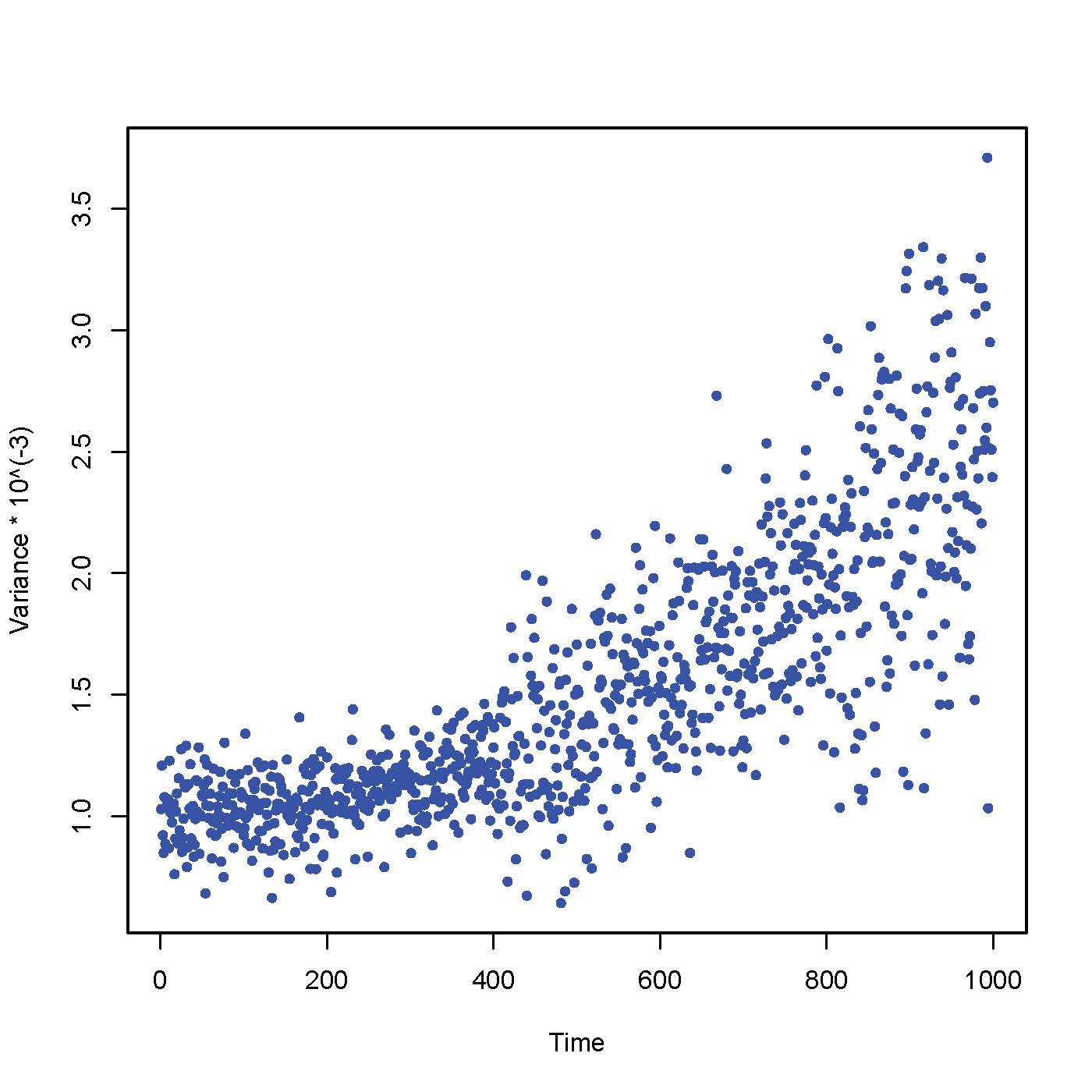

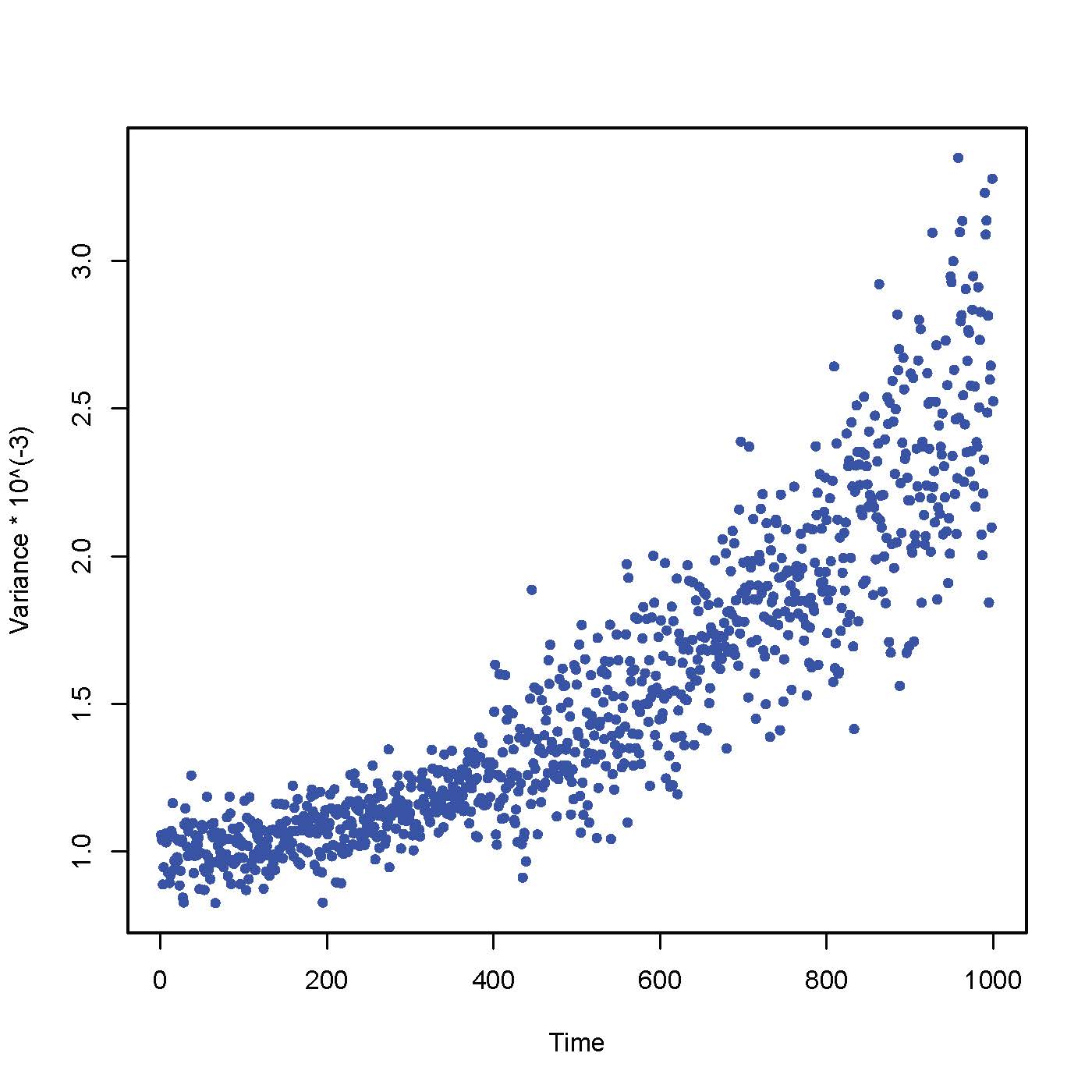

In Figure 4, we compare the empirical variance of the estimator for versus across all . It is clear that the variance decreases as N increases, but at the same time the variance does increase over time. The latter is consistent with the theoretical limiting variance as obtained in (6).

|

|

| (a) Number of Particles =500 | (b) Number of Particles =2,500 |

|

|

| (a) Number of Particles =500 | (b) Number of Particles =2,500 |

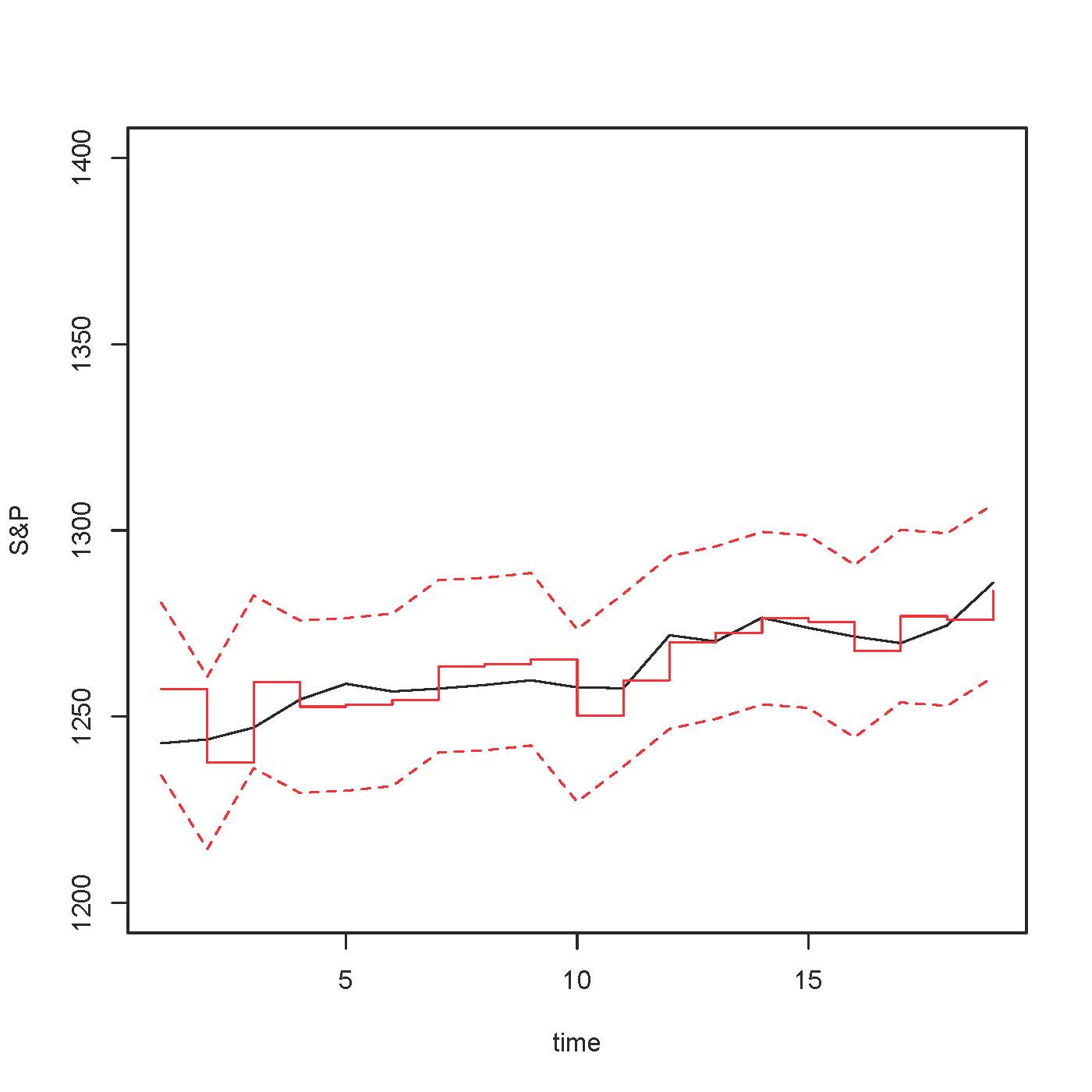

5 Application to S&P 500 Data

In this section, we apply our method to real data. As an example, we are working with a long-range dependent state-space model in finance. The observed process are the returns of the underlying asset (S& P 500 index to be precise) and the unobserved process is the asset’s volatility. Based on the financial literature ([6, 26, 9]), we assume that the volatility process is long-range dependent, and the model we focus on is the long memory stochastic volatility model in discrete time that is described by (7). This model was introduced simultaneously by Breidt et al. [6] and Harvey, [26] in 1993.

To further specify this model in practice, we need to determine the order of the polynomials and . This is a common task in time series analysis and for details we refer to Hamilton [24]. Based on a preliminary analysis, we choose to work with a Fractional ARIMA() model, which is also in accordance to the model suggested by [1]. To be precise, the model we will be working with is

where .

The data set we consider contains daily returns of the S&P 500 for one year, that is about 252 observations, starting in January 2010 until December 2010.

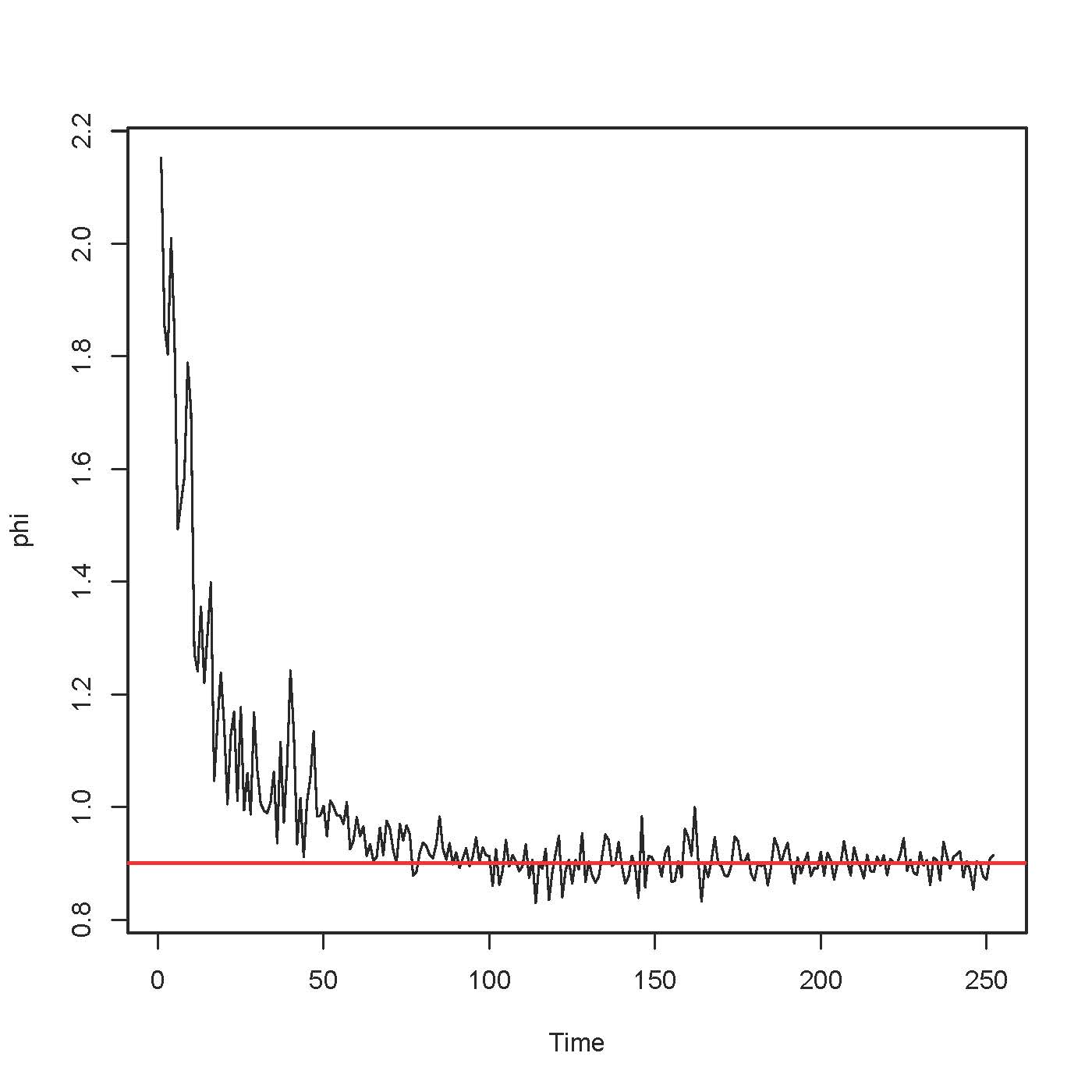

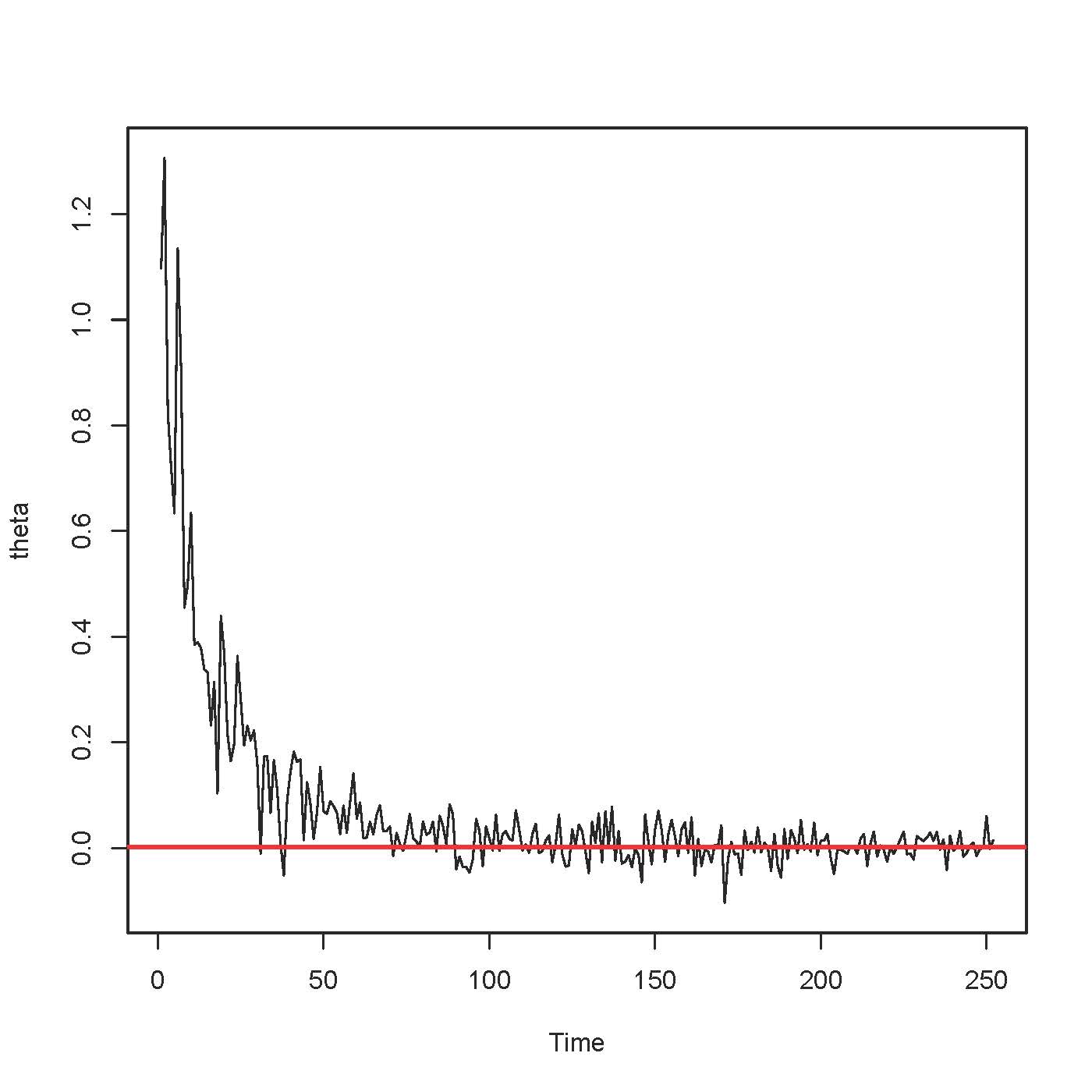

One assumption that we made in the SMC algorithm is that the parameter is known. However, when it comes to real data, this is something that we need to estimate. Here, we used the Geweke and Porter-Hudak estimator, [7], which yields . Then, we apply the SISR algorithm to estimate the remaining unknown parameters of the model and . We choose as tuning parameters which then implies .

The algorithm has two outputs. The first one is the distribution of the unobserved volatility, which is given in Figure 5, using 500 trajectories, and the second one is the estimated vector of parameters, which are plotted as a function of time in Figure 6.

]

(a) Estimator of

(b) Estimator of

(a) Estimator of

(b) Estimator of

(c) Empirical Variance of

(d) Empirical Variance of

(c) Empirical Variance of

(d) Empirical Variance of

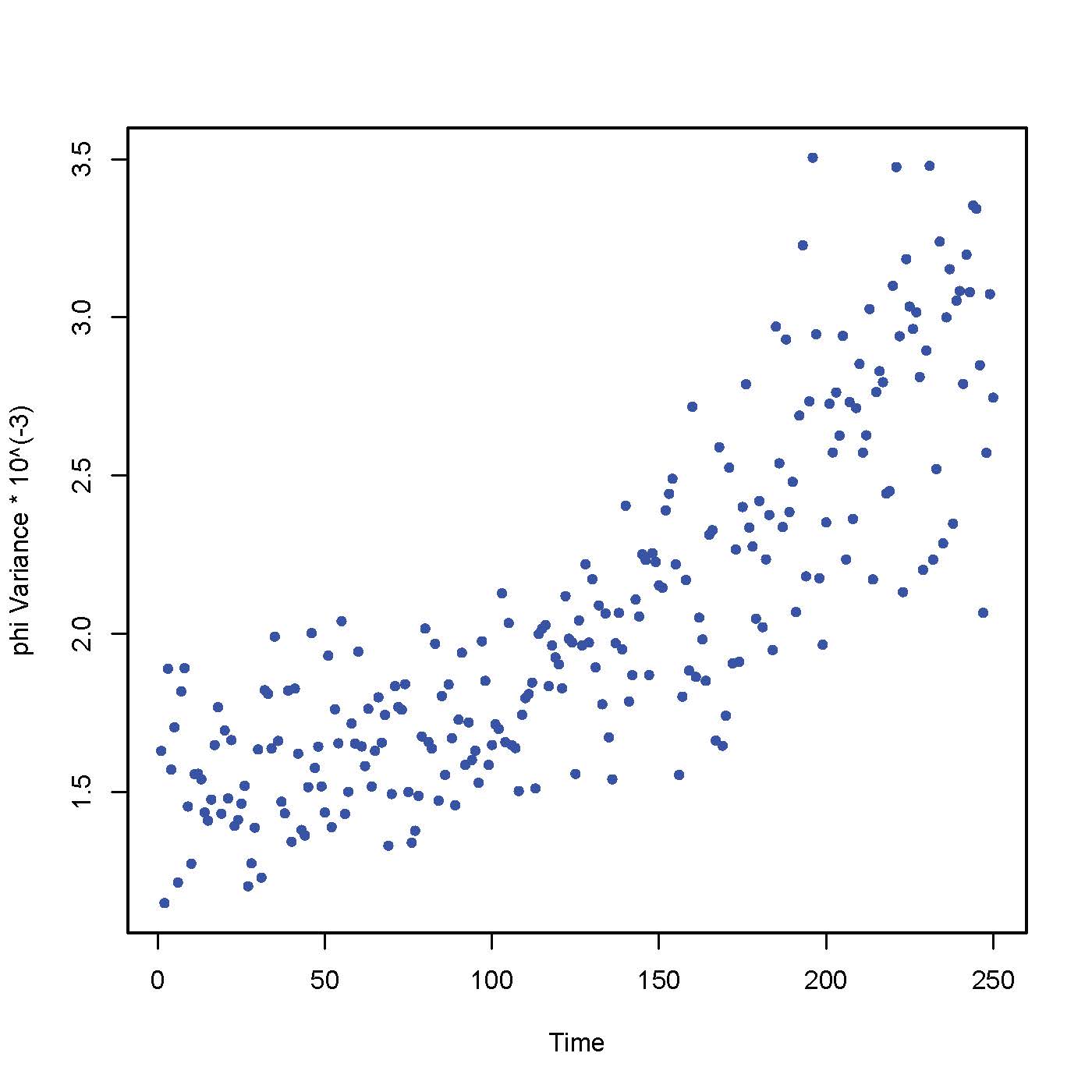

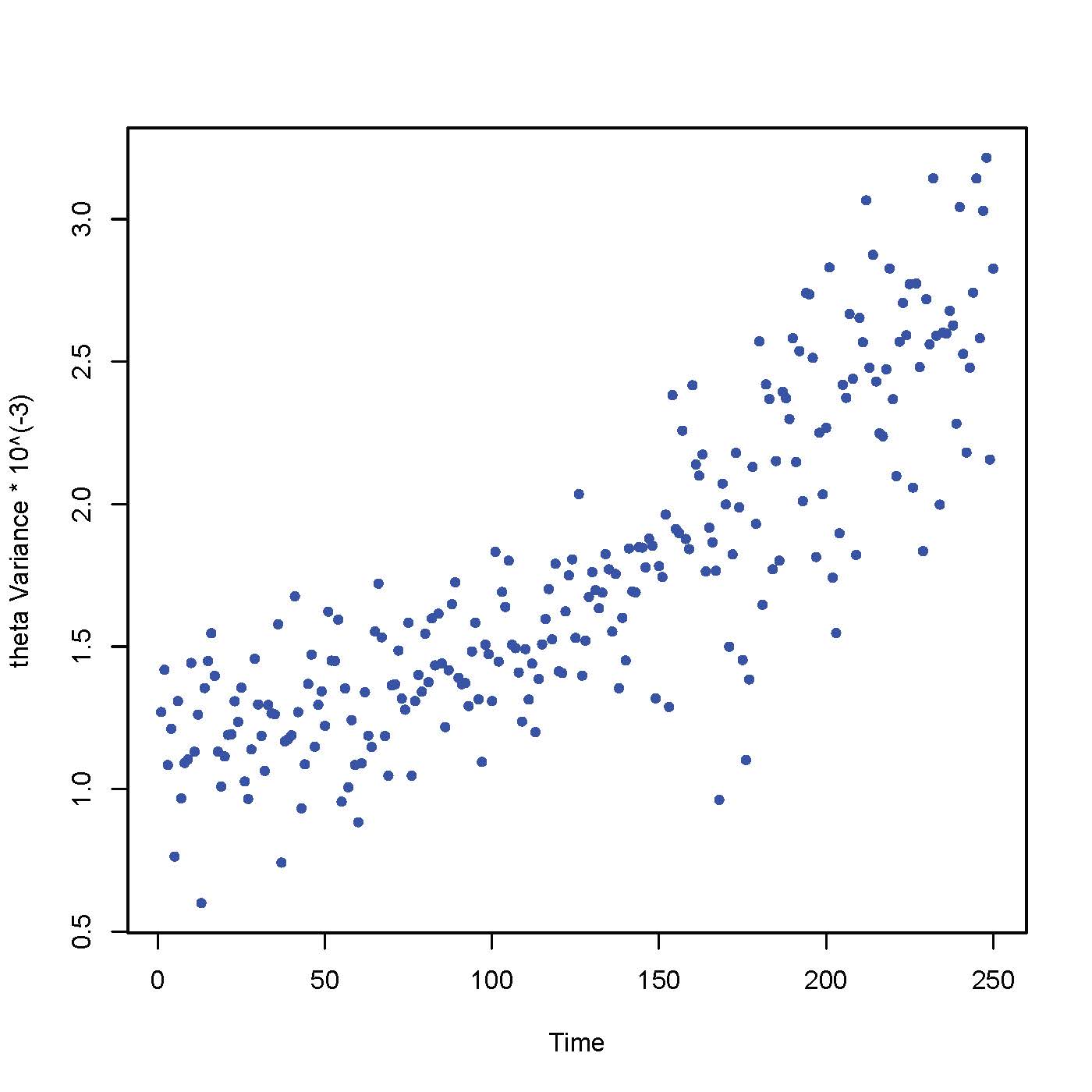

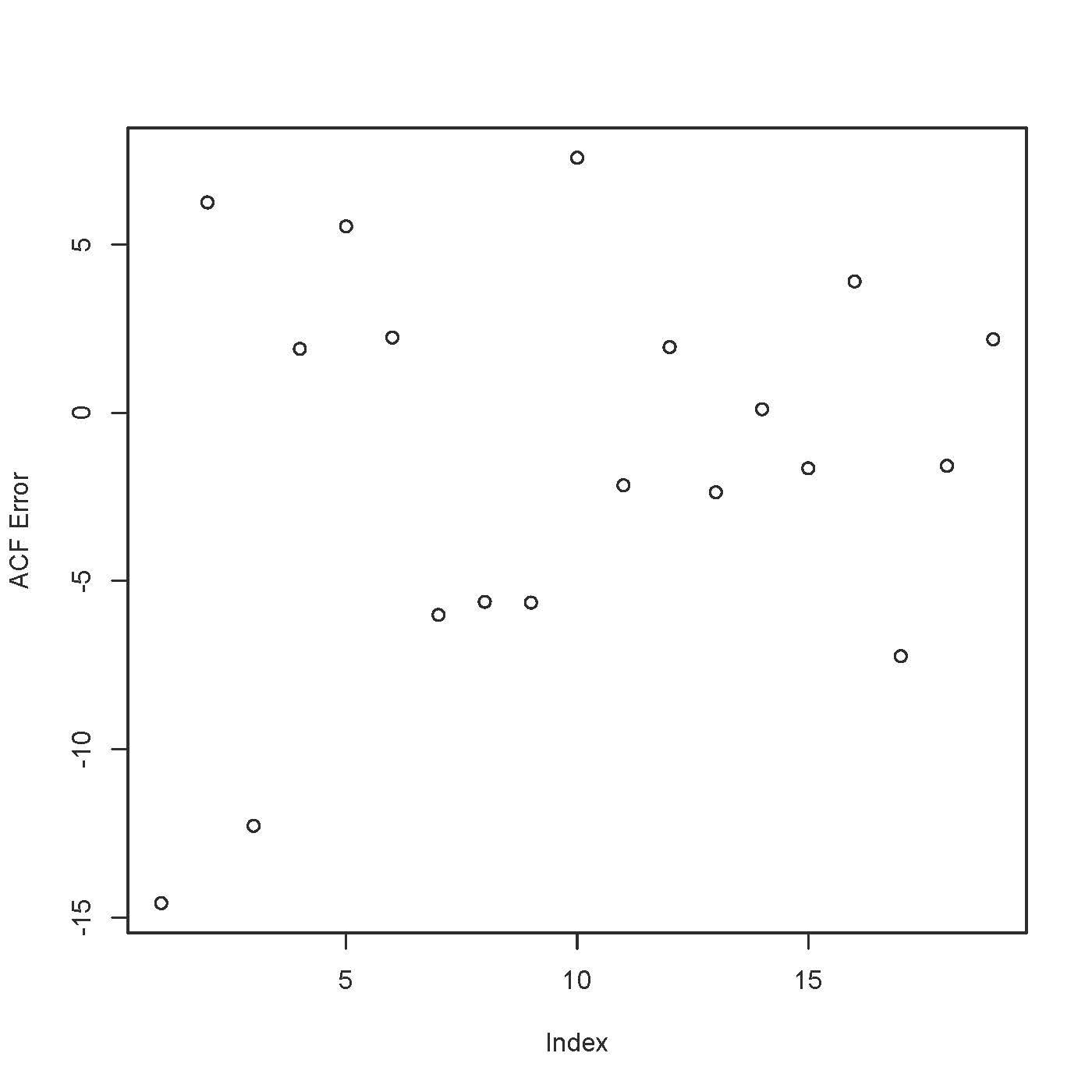

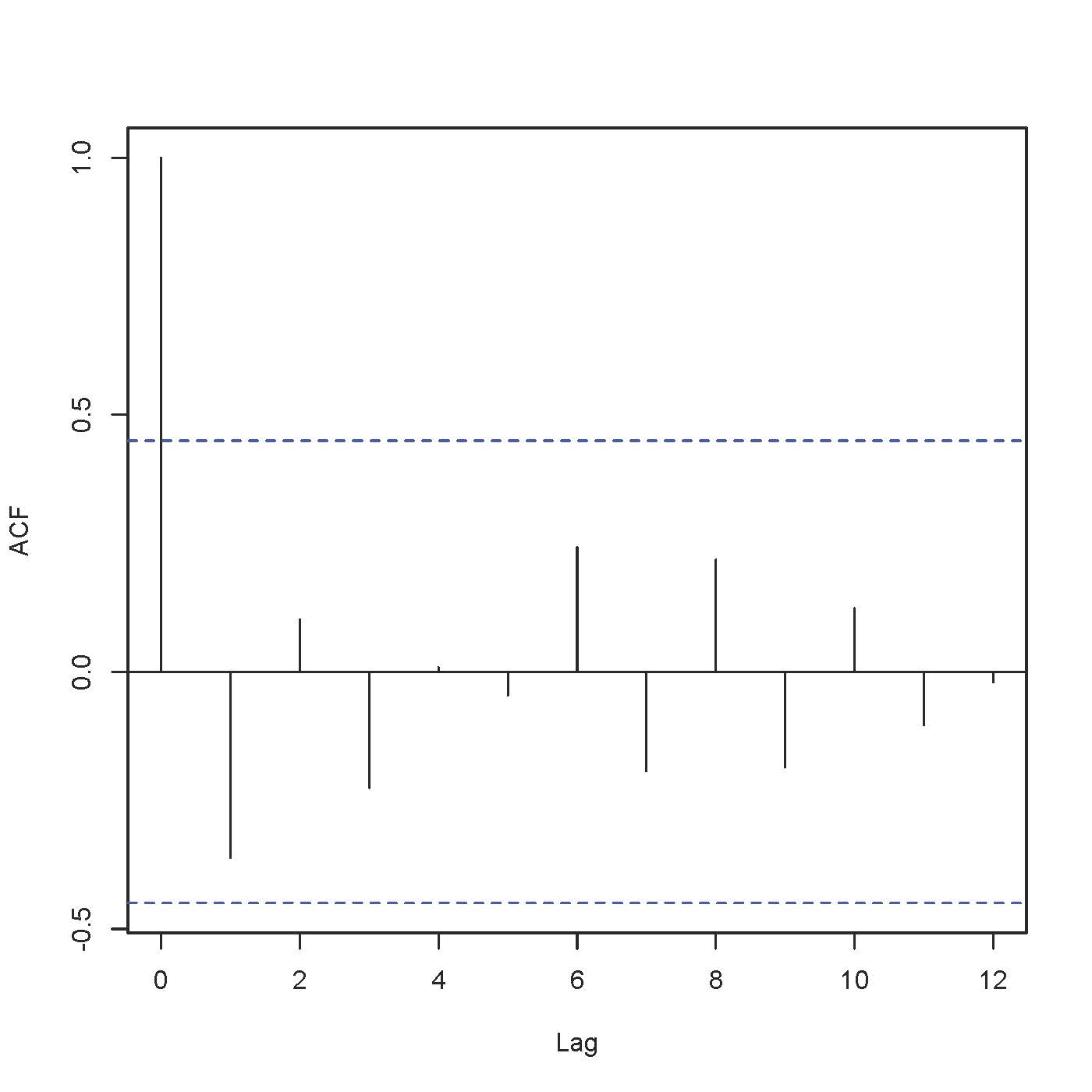

Using the model parameters we estimated, we also do an out-of-sample prediction of the values of the underlying asset, which is shown in Figure 7. By doing an one-step prediction each time, we forecast 20 daily values of the index. The 95% confidence intervals are computed using boostrap. In Figure 7 we also present the empirical variance for the estimators and . In Figure 8, we also present the residuals of the fitted model.

]

(a) Standard Residuals

(b) ACF of the Residuals

(a) Standard Residuals

(b) ACF of the Residuals

6 Conclusion

To summarize, in this article we extended the standard SISR algorithm to incorporate the case that the observations are long-range dependent. Our findings show that the results are very close to the case that the observations are independent or Markov. However, the main drawback of this method is the computational time that is required to perform the iterations. Since we need to take into account, and technically speaking to store all past values of the trajectory, this increases the computational time and complexity of the method. In addition, by naturally extending existing results in the literature, we proved that the filter converges to the true distribution of the unobserved process.

Our second outcome, was the development of an SISR algorithm that along with the estimation of the unobserved distribution of the hidden process, also estimated unknown model parameters. Our approach was dynamic, in the sense that the parameter was regarded as “time-varying” and thus the parameter estimators were updated at every step of the algorithm. We also showed that the proposed estimators for the unknown parameter are consistent and asymptotically normal and we corroborated these results with a simulation study.

There are quite a few open problems that we would like to investigate in the future. The first one is to study ways to improve the computational efficiency of the algorithm. In our approach, we used all the history of the trajectory to run the algorithm, which severely affected the computational efficiency, but it would be interesting to investigate if a “window” approach would provide us with a reasonable estimator for the filter and/or the parameter, and possibly quantify the loss that one might have by doing so in terms of accuracy.

In addition, one question that we did not address in this paper, is what happens with the long memory parameter in practice. In our approach, we assumed that (or equivalently ) is known (given or estimated from the data). However, it is an open question how one would consistently estimate the memory parameter in the scenario that the long-range dependent process is hidden.

The goal of this first paper on the topic is to lay down the algorithm, its properties and to understand the main issues that the presence of memory brings. In this paper, we formulated the algorithm and established some baseline theoretical properties. We also performed numerical experiments using both simulation data and real data, in order to test the performance of the proposed algorithm in practice. We plan to investigate the open computational and theoretical issues mentioned above in a systematic way in future works.

References

- [1] Baillie, R. T., Bollerslev, T., and Mikkelsen, H. O. (1996). Fractionally Integrated Generalized Autoregressive Conditional Heteroskedasticity. J. Econom. 74(1):3–30.

- [2] Beskos, A., Dureau, J, and Kalogeropoulos, K. (2013), Bayesian inference for partially observed SDEs driven by fractional Brownian motion, arXiv: 1307.0238.

- [3] Bayer, C., Friz, P. and Gatheral, J. (2015) Pricing under rough volatility. Preprint.

- [4] Beran, J. (1994): Statistics for Long-Memory Processes. Chapman and Hall.

- [5] Box, G.E.P. and Jenkins (1970) Time series analysis: forecasting and control. Holden Day, San Fransisco.

- [6] Breidt, F. J., Crato, N. and De Lima, P. (1998). The Detection and Estimation of Long-Memory in Stochastic Volatility. Journal of Econometrics. 83:325–348.

- [7] Casas, I. and Gao, J. (2008) Econometric estimation in long-range dependent volatility models: Theory and practice. Journal of Econometrics 147:72–83.

- [8] Chronopoulou, A. and Viens, F. (2012). Stochastic volatility and option pricing with long-memory in discrete and continuous time. Quantitative Finance 12(4):635–649.

- [9] Chronopoulou, A. and Viens, F. (2010). Estimation and pricing under long-memory stochastic volatility. Annals of Finance, 8 (2-3):379–403.

- [10] Comte, F. and Renault, E. (1998). Long Memory in Continuous-time Stochastic Volatility Models. Mathematical Finance, 8(4):291–323.

- [11] Comte, F., Coutin, L. and Renault, E. (2012) Affine fractional stochastic volatility models. Ann Finance 8: 337.

- [12] Chopin, N., (2004) Central limit theorem for sequential Monte Carlo method and its application to Bayesian inference. The Annals of Statistics, 32(6):2385–2411.

- [13] Chopin, N., Jacob, P.E., and Papaspiliopoulos, O. (2013) SMC2: A sequential Monte Carlo algorithm with particle Markov chain Monte Carlo updates. J. R. Statist. Soc. B, 75(3), 397–426.

- [14] Del Moral, P. (2004), Feynman-Kac Formulae: Genealogical and interacting particle systems with applications, In Series Probability and Applications, Springer-Verlag, New York.

- [15] Del Moral, P. and Guionnet, A. (1999) Central limit theorem for nonlinear filtering and interacting particle systems. Annals of Applied Probability, 9:275–297.

- [16] Ding,Z., C., Granger, W., J. and Engle, R. F. (1993). A Long Memory Property of Stock Market Returns and a New Model. J. Empirical Finance 1, 1.

- [17] Doucet, A., De Freitas, J.F.G. and Gordon, N.J. (eds.) (2001). Sequential Monte Carlo Methods in Practice. New York: Springer-Verlag.

- Douc and Moulines [2008] Douc, R. and Moulines, E. (2008), Limit theorems for weighted samples with applications to sequential Monte Carlo methods, Annals of Statistics, 36(5):2344–2376.

- [19] Flury, T. and Shephard, N. (2011). Bayesian inference based only on simulated likelihood: particle filter analysis of dynamic economic models. Econometric Theory, 27:933–956.

- [20] Garnier, J. and Solna, K. (2015). Correction to Black-Scholes formula due to fractional stochastic volatility. Preprint.

- [21] Gatheral, J., Jaisson, Th., and Rosenbaum, M. (2014) Volatility is rough. Preprint.

- [22] Gordon, N., Salmond, D., and Smith, A. (1993) Novel approach to non-linear/non-Gaussian Bayesian state estimation. IEE Proceedings-F, 140:107–113.

- [23] Granger, C.W., Joyeux, R., (1980). An introduction to long-memory time series models and fractional differencing. Journal of Time Series Analysis 1:15–29.

- [24] Hamilton, J.D. (1994) Time Series Analysis. Princeton University Press.

- [25] Handschin, J. and Mayne, D. (1969), Monte Carlo techniques to estimate the conditional expectation in multi-stage non-linear filtering. International Journal of Control, 9:547–559.

- [26] Harvey, A.C. (1998). Long Memory in Stochastic Volatility, in J.Knight and S. Satchell (eds.) Forecasting Volatility in Financial Markets, Butterworth-Haineman, Oxford, pp. 307-320.

- [27] Johansen, A. and Doucet, A., Auxiliary variable sequential Monte Carlo methods. Statistics group technical report, 07:09, University of Bristol, July 2007.

- [28] Kantas, N., Doucet, A., Singh, S. S., Maciejowski, J. M., Chopin, N. (2014), An overview of sequential Monte Carlo methods for parameter estimation in general state-space models. Submitted to Statistical Science.

- Künsch [2005] Künsch, H.R. (2005), Recursive Monte Carlo filters: algorithms and theoretical analysis, Annals of Statistics, 33(5): 1983–2021.

- [30] Liu, J. and West, M., Combined parameter and state estimation in simulation-based filtering, In A. Doucet, N. De Freitas and N. Gordon (Eds.), Sequential Monte Carlo methods in practice, New York: Springer, 197–223.

- [31] Lysy, M., and Pillai, N.S., (2013), Statistical inference for stochastic differential equations with memory, arXiv:1307.1164.

- [32] Rogers, L. C. G. (1997) Arbitrage with fractional Brownian motion, Mathematical Finance, 7 , 95–105.

- [33] Van der Vaart, A.W. (1998), Asymptotic Statistics, Cambridge series in statistical and probabilistic mathematics, Cambridge University Press.

- [34] West (1993), M. Approximating posterior distributions by mixtures. Journal of the Royal Statistical Society (series B), 55:409–422.