A generalized nonlinear model for long memory

conditional heteroscedasticity

Ieva Grublytė1,2 and Andrius Škarnulis2

(

1 Université de Cergy Pontoise, Départament de Mathématiques, 95302 Cedex, France

2 Vilnius University, Institute of Mathematics and Informatics, 08663 Vilnius, Lithuania)

Abstract

We study the existence and properties of stationary solution of ARCH-type equation

, where are standardized i.i.d. r.v.’s and the conditional

variance satisfies an AR(1) equation with a

Lipschitz function and real parameters . The paper extends the model and the results in

[5] from the case to the case . We also obtain a new

condition for the existence of higher moments of which does not include the Rosenthal

constant. In the particular case when

is the square root of a quadratic polynomial, we prove that can exhibit a leverage effect and long memory. We also

present simulated trajectories and histograms of marginal density of for different values of

.

Keywords: asymmetric ARCH model, LARCH model, leverage, long memory

1 Introduction

Doukhan et al. [5] discussed the existence of stationary solution of

conditionally heteroscedastic equation

(1.1)

where are standardized i.i.d. r.v.’s, are real parameters and is a Lipschitz function of real variable . Probably, the most important

case of (1.1) is

(1.2)

where is a parameter. The model (1.1)-(1.2) includes the classical Asymmetric

ARCH(1) of Engle [7] and the Linear ARCH (LARCH) model of Robinson [16]:

(1.3)

[9] proved that the squared stationary solution of the LARCH model in (1.3)

with decaying as

may have long memory autocorrelations.

The leverage effect in the LARCH

model was discussed in detail in [10]. Doukhan et al. [5] extended the above properties

of the LARCH model (long memory and leverage) to

the model in (1.1)-(1.2) with or strictly positive volatility.

The present paper extends the results of [5] to a more general class of volatility forms:

(1.4)

where are as in (1.1) and is a parameter. The inclusion

of lagged in (1.4) helps to reduce very sharp peaks and clustering of volatility which

occur in trajectory of (1.1)-(1.2)

near the threshhold (see Fig. 1). The generalization from (1.1) to (1.4)

is similar to that from ARCH to GARCH models, see [6], [3], particularly, (1.4) with of and

reduces

to the Asymmetric GARCH(1,1) of Engle [7].

Let us describe the main results of this paper.

Sec. 2 (Theorems 4 and 5) obtain sufficient conditions for the existence

of stationary solution of (1.4) with and

. Theorem 4 extends the corresponding result

in ([5], Thm. 4) from to .

Theorem 5 is new even in the case by providing an explicit sufficient condition (2.25)

for higher-order even moments () which does not involve the absolute constant in the Burkholder-Rosenthal inequality (2.11).

Condition (2.25) coincides with the corresponding moment condition for the LARCH model and

is important for statistical applications, see Remark 2.

The remaining sec. 3-5 deal exclusively with the case of quadratic

in (1.2), referred to as the Generalized Quadratic ARCH (GQARCH) model in the sequel.

Theorem 6 (sec. 3) obtains long memory properties of the squared process of

the GQARCH model with and coefficients

decaying regularly as . Similar properties

were established in [5] for the GQARCH model with and for the LARCH model

(1.3) in [9], [10]. Quasi-maximum likelihood estimation for parametric GQARCH model with long memory was recently studied in [13].

See the review paper [11] and recent work [12]

on long memory ARCH modeling.

Sec. 4 extends to the GQARCH model

the leverage effect discussed in [5] and [10]. Sec. 5 presents some

simulations and volatility profiles for the LARCH and GQARCH models with parameters estimated from real data.

A general impression from our results

is that the GQARCH modification in (1.4), (1.2)

of the QARCH model in [5]

allows for a more realistic volatility modeling as compared to the LARCH and QARCH models,

at the same time preserving

the long memory and the leverage properties of the above mentioned models.

Let us give some formal definitions. Let be the sigma-field generated

by . A random process is called adapted (respectively, predictable)

if is -measurable for each (respectively, is -measurable for each ).

Definition 1

Let be arbitrary.

(i) By -solution of (2.6) or/and (2.7)

we mean an adapted process

with such that for any the series

converges in , the series

converges in and (2.7) holds.

(ii) By -solution of (2.8) we mean a predictable process with

such that for any the series

converges in , the series

converges in and (2.8) holds.

Define

Note .

As in [5], we use the following moment inequality, see [4], [20], [17].

Proposition 2

Let

be a sequence of r.v.’s such that for some

. If we additionally assume that is a martingale difference sequence:

. Then

there exists a constant depending only on and such that

(2.11)

Proposition 3 says that equations (2.7) and (2.8) are equivalent in the sense that

by solving one the these equations one readily obtains a solution to the other one.

Proposition 3

Let be a measurable function satisfying (2.10) with some and be an i.i.d. sequence with and satisfying

for . In addition, assume and .

(i) Let be a stationary -solution of (2.8) and let

. Then in (2.6) is a stationary

-solution of (2.7) and

(2.12)

Moreover, for , is a

martingale difference sequence with

(2.13)

(ii) Let be a stationary -solution of (2.7).

Then in (2.5) is a stationary -solution of (2.8) such that

Moreover, for

Proof. (i)

First, let . Then

Hence, using (2.10), the fact that is predictable

and

we obtain

proving (2.12) for . Next, let . Then

by stationarity and Minkowski’s inequality and hence (2.12) follows using the same argument as above. Clearly, for

is a martingale difference sequence and satisfies (2.13).

Then, the convergence in of

the series in (2.5) follows from (2.12) and Proposition 2:

In particular,

by the definition of . Hence, is a -solution of (2.7). Stationarity of follows

from stationarity of .

(ii) Since is a -solution of (2.7), so with defined

in (2.5) and satisfy (2.5), where the series converges in . The rest follows

as in [5], proof of Prop.3.

Remark 1

Let and , then by inequality (2.11),

being a stationary -solution of (2.6) is equivalent

to being a stationary -solution of (2.6) with .

Similarly, if and satisfy the conditions of Proposition 3 and ,

then being a stationary -solution of (2.5) is equivalent

to being a stationary -solution of (2.5) with .

See also ([5], Remark 1).

Theorem 4

Let satisfy the conditions of Proposition 3 and

satisfy the Lipschitz condition in (2.9).

(i) Let and

(2.15)

where is the absolute constant from the moment inequality in (2.11).

Then there exists a unique stationary -solution of (2.8) and

(ii) Assume, in addition, that

, where , and .

Then is a necessary and sufficient condition for the existence

of a stationary -solution of (2.8) with .

Proof. (i) We follow the proof of Theorem 4 in [5]. For we recurrently define a solution of (2.8) with zero initial condition at as

(2.17)

where .

Let us show that converges in to a stationary -solution

as .

First, let .

Let . Then by inequality (2.11) for any we have that

(2.18)

Using with arbitrarily close to , see [5], proof of Theorem 4,

we obtain

(2.19)

Next, using we obtain

(2.20)

Hence from the Lipschitz condition in (2.9) we have that

where .

By iterating

the last displayed equation and using

we obtain and hence

the existence of such that and

satisfying the bound in (2.16). The rest of the proof of part (i)

is similar as in [5], proof of Theorem 4, and we omit the details.

(ii) Note that is a Lipschitz function and satisfies (2.9) with . Hence by and part (i), a unique

-solution of (2.8) under the condition exists. To show

the necessity of the last condition,

let be a stationary -solution of (2.8). Then

since . Hence, unless ,

or is a trivial process.

Clearly, (2.8) admits a trivial solution if and only if or

. This proves part (ii) and the theorem.

Remark 2

Theorem 4 extends ([5], Thm. 4) from to . A major

shortcoming of Theorem 4 and the above mentioned result in [5] is the presence

of the universal constant whose upper bound given in [15] leads to

restrictive conditions on in (2.15) for the existence

of -solution, . For example, for the above mentioned bound in [15] gives

(2.23)

requiring to be very small. Since statistical inference based of ‘observable’ squares

usually requires the existence of

and higher moments of (see e.g. [13]), the question arises to derive

less restrictive conditions for the existence of these moments which do not involve the Rosenthal constant

. This is achieved in the subsequent Theorem 5. Particularly, for the sufficient condition (2.25)

of Theorem 5

for the existence of even

becomes

(2.24)

Condition (2.24)

coincides with the corresponding condition

in the LARCH case in ([10], Proposition 3).

Moreover, (2.24) and (2.25) apply to more general classes of ARCH models in (1.1)

and (1.4) to which the specific Volterra series techniques used in [9], [10] are not applicable.

In the particular case condition (2.24) becomes

which seems to be much better than condition (2.23) based on Theorem 4.

Theorem 5

Let satisfy the conditions of Proposition 3 and

satisfy the Lipschitz condition in (2.9).

Let be even and

(2.25)

Then there exists a unique stationary -solution of (2.8).

Proof. For , condition (2.25) agrees with or condition

(2.15) so we shall assume in the subsequent proof.

In the latter case (2.25) implies and the existence of a stationary -solution

of (2.8). It suffices to show that the above -solution satisfies .

Towards this end similarly as in the proof of Thm 4 (i) consider the solution with zero initial condition at

as defined in (2.17). Let . Since ,

by Fatou’s lemma it suffices to show that under condition (2.25)

(2.26)

where the constant does not depend on .

Since is even for any we have that

(2.27)

Hence using Hölder’s inequality:

we obtain

(2.28)

where and where

The last expectation in (2.28) can be evaluated similarly to (2.27)-(2.28):

Proceeding recurrently with the above evaluation results in the inequality:

Next, let us estimate the expectation on the r.h.s. of (2.29)

in terms of the expectations on the l.h.s. Using (2.10) and Minkowski’s inequalities

we obtain

where and can be chosen arbitrarily small.

Particularly, for any fixed

Example: asymmetric GARCH(1,1). The asymmetric GARCH(1,1) model of Engle [7] corresponds to

(2.32)

or

(2.33)

in the parametrization of ([18], (5)), with parameters in (2.32), (2.33) related by

(2.34)

Under the conditions that are standardized i.i.d., a stationary asymmetric GARCH(1,1) (or

GQARCH(1,1) in the terminology of [18]) process

with finite variance and exists if and only if , or

(2.35)

see Thm. 4 (ii). Condition (2.35) agrees with condition for covariance

stationarity in [18]. Under the assumptions that the distribution of is symmetric and ,

[18]

provides a sufficient condition for finiteness

of together with explicit formula

(2.36)

The sufficient condition of [18] for

is , which translates to

(2.37)

in terms of the parameters of (2.32). Condition (2.37) seems weaker than

the sufficient

condition of Theorem 5 for the existence of -solution

of (2.32).

Following the approach in [5], below we find explicitly the covariance function , including

the expression in (2.36), for stationary solution of the asymmetric GARCH(1,1) in (2.32).

The approach in [5] is based on derivation and solution of linear equations for moment functions

and .

Assume that , or

. We can write the following moment equations:

(2.38)

From equations above one can show by induction that .

Similarly,

Using and we obtain the system of equations

(2.39)

where is some constant independent of and

(2.40)

Note that the expression above coincides with (2.36) given that the relations in (2.34) hold.

Since the equation in (2) is analogous to (2), the solution to (2) is . In order to find ,

we combine

and the expression for to obtain the equation

Now can be expressed as

together with (2.40) and

giving explicitly the covariances of process .

3 Long memory

The present section studies long memory properties of the generalized quadratic ARCH model in (1.4)

corresponding to of (1.2), viz.,

(3.41)

where are real parameters, are standardized i.i.d. r.v.s, with zero mean and unit variance,

and are real numbers satisfying

(3.42)

The main result of this section is Theorem 6 which shows that under some additional conditions

the squared process of (3.41)

has similar long memory properties as in case of the LARCH model (see [9], Thm. 2.2).

Theorem 6 extends the result in ([5], Thm. 10) to the case .

In Theorem 6 and below, ,

and is beta function.

Theorem 6

Let be a stationary -solution of (3.41)-(3.42).

Assume in addition that

,

and

.

Then

(3.43)

where .

Moreover,

(3.44)

where is a fractional Brownian motion with Hurst parameter and

.

To prove Theorem 6, we need the following two facts.

Proof. It suffices to show that the difference decays faster than , in other

words, that

Clearly, . Relation

follows by the dominated

convergence theorem since and

for any fixed .

Proof of Theorem 6. We use the idea of the proof of Thm. 10 in [5].

Denote

(3.45)

By the definition of in (3.41) we have have the following decomposition (c.f. [5], (6.66))

(3.46)

where is the main term and

the ‘remainder terms’ and are given by

(3.47)

(3.48)

Using the identity the convergence in

of the series on the r.h.s. of (3.48) follows as in [5] (6.67). Hence, the series for

in (3.47) also converges in .

Let us prove that

(3.49)

where .

The second relation in (3.49) follows from see Lemma 7,

and the fact that is a moving average in stationary uncorrelated innovations

. Since is also an uncorrelated sequence, so

, and the first relation in (3.49) is a consequence

of

(3.50)

(3.51)

We have and

, where

follows from

Rosenthal’s inequality in (2.11) since

.

This proves (3.50). The proof of (3.51) is analogous to [5] (6.68)-(6.69) and

is omitted.

Next, let us prove (3.43). Recall the definition of in (3.45).

From the decomposition (3.46) we obtain

(3.52)

where are the coefficients of the power series given by ,

in particular, and the r.h.s. of (3.52)

is well-defined. Relations (3.52) and (3.53) imply that

(3.54)

see [5], (6.63). Now, (3.43) follows from (3.54) and (3.49). The invariance

principle in (3.44) follows similarly as in [5], proof of Thm. 10 from (3.52), (3.49) and , , the last fact being a consequence of a general result in

[1]. Theorem 6 is proved.

4 Leverage

For conditionally heteroscedastic model in (3.41) with consider the leverage function

Following [10], and [5],

we say that

in (3.41) has leverage of order (denoted by ) if

The study in [5] of leverage for model (3.41) with , viz.,

was based on linear equation for leverage function:

where .

A similar equation (4.55) for leverage function can be derived for model (3.41) in the general case

. Namely, using as in [5] we have that

Using (4.55) and (4.56),

the statements (i) and (ii) can be proved by induction on similarly to [5]. Since and , equation (4.55) yields

(4.58)

According to (4.56), the last sum in (4.58) does not exceed

provided .

Hence, (4.58) implies , or the statements (i) and (ii) for .

Let us prove the induction step in (i). Assume first that . Then

by the inductive assumption. By (4.55),

where and

according to (4.56), (4.57). Since and this implies

, or . The remaining cases

in (i)-(ii) follow analogously.

5 A simulation study

As noted in the Introduction, the (asymmetric) GQARCH model of (3.41) and the LARCH model of (1.3)

have similar long memory and leverage properties

and both can be used for modelling of financial data with the above properties. The main disadvantage of the latter model vs. the

former one seems to be the fact the volatility may take negative values and is not separated from below by positive constant

as in the case of (3.41). The standard quasi-maximum likelihood (QMLE) approach to estimation of

LARCH parameters is inconsistent and other estimation methods were developed

in [2], [8], [14], [19].

Consistent QMLE estimation for

5-parametric long memory GQARCH model (3.41)

with and was discussed in the recent work [13].

The parametric form of the moving-average coefficients in (3.41)

is the same as in Beran and Schützner [2] for the LARCH model.

It is of interest to compare QMLE estimates and volatility graphs

of the GQARCH and LARCH models based on real data. The comparisons are extended to the classical GARCH(1,1) model

(5.59)

We consider four data generating processes (DGP):

(5.60)

with standard normal innovations and . The first three models (L), (Q1), (Q2) have long memory and

(G) is short memory.

The parameters

(L), (Q1),

and

are obtained from real data, consisting of

daily returns of GSPC (SP500) from 2010 01 01 till 2015 01 01 with observations in total,

by minimizing the corresponding approximate log-likelihood functions. The details of the estimation procedure

can be found in [13].

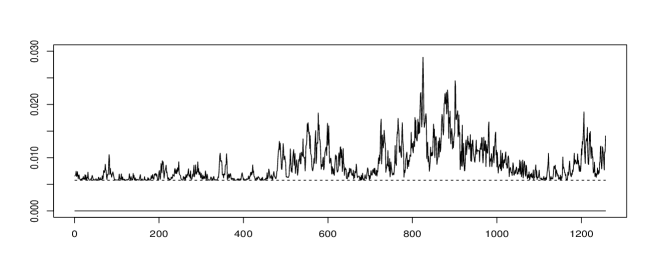

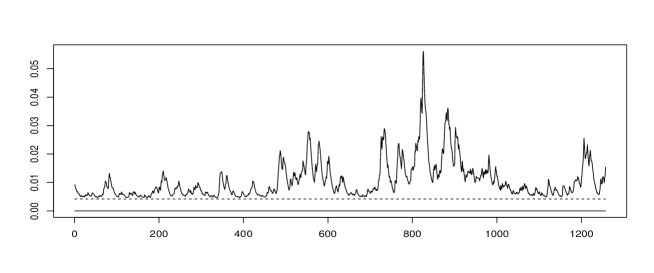

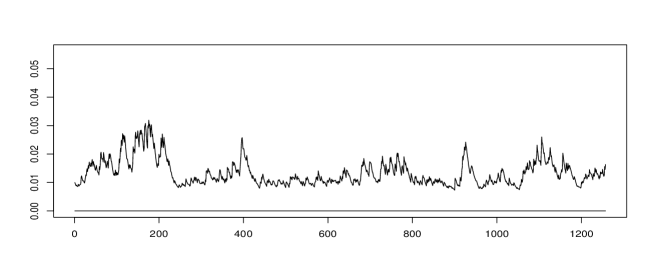

Fig. 1 presents simulated trajectories of of

four DGP in (5.60), corresponding to the same innovation sequence. Observe that the variability of volatility decreases from top

to bottom, (Q2) resembling (G) (GARCH(1,1)) trajectory more closely than

(L) and (Q1).

The graph (Q1) exhibits very sharp peaks and clustering

and a tendency to concentrate near the lower threshold

outside of

high volatility regions. This unrealistic

‘threshold effect’ is much less pronounced in (Q2) (and also in the other two DGP), due

to presence of the autoregressive parameter which also prevents

sharp changes and excessive variability of volatility series. The graph (G) has different shape and volatility peaks

from the remaining three graphs which is probably due to the short memory of GARCH(1,1).

Fig. 2 illustrates the effect of on the marginal distribution of (Q2): with increasing, the

distribution becomes less skewed and spreads to the right, indicating a less degree of volatility clustering.

Figure 1: Trajectory of DGP: From top to bottom: (L), (Q1), (Q2), (G). The dashed line

in (Q1) and (Q2) indicates the threshold

in (3.41).

Figure 2: Smoothed histograms of DGP (Q2) for different values of .

References

[1] Abadir, K.M., Distaso, W., Giraitis, L., Koul, H.L., 2014.

Asymptotic normality for weighted sums of linear processes. Econometric Th., 30, 252–284.

[2] Beran, J., Schützner, M., 2009. On approximate pseudo-maximum likelihood

estimation for LARCH processes. Bernoulli, 15, 1057–1081.

[4] Burkholder, D.L., 1973. Distribution functions inequalities for martingales.

Ann. Probab., 1, 19–42.

[5] Doukhan, P., Grublytė, I., Surgailis, D., 2015. A nonlinear model for long memory conditional

heteroscedasticity. Preprint. Available at arXiv: 1502.00095v2 [math.ST].

[6] Engle, R.F., 1982. Autoregressive conditional heterosckedasticity with estimates

of the variance of United Kingdom inflation. Econometrica, 50, 987–1008.

[7] Engle, R.F., 1990. Stock volatility and the crash of ’87. Discussion. Rev. Financial Studies 3, 103–106.

[8] Francq, C., Zakoian, J.-M., 2010.

Inconsistency of the MLE and inference based on weighted LS for LARCH models. J. Econometrics 159, 151–165.

[9] Giraitis, L., Robinson, P.M., Surgailis, D., 2000. A model for long memory conditional heteroskedasticity. Ann. Appl. Probab.,

10, 1002–1024.

[10] Giraitis, L., Leipus, R., Robinson, P.M., Surgailis, D., 2004. LARCH, leverage and long memory. J. Financial Econometrics,

2, 177-210.

[11] Giraitis, L., Leipus, R., Surgailis, D., 2009. ARCH() models

and long memory properties. In: T.G. Andersen, R.A. Davis, J.-P. Kreiss, T. Mikosch (Eds.)

Handbook of Financial Time

Series, pp. 71–84. Springer-Verlag.

[12] Giraitis, L., Surgailis, D., Škarnulis, A., 2014. Integrated AR and ARCH processes and

the FIGARCH model: origins of long memory. Preprint.

[13] Grublytė, I., Surgailis, D., Škarnulis, A., 2015. Quasi-MLE for quadratic

ARCH model with long memory. Preprint. Available at arXiv:1509.06422 [math.ST].

[14] Levine, M., Torres, S., Viens, F., 2009. Estimation for the long-memory parameter

in LARCH models, and fractional Brownian motion. Stat. Inf. Stoch. Process. 12, 221–250.

[15] Osȩkowski, A., 2012. A note on Burkholder-Rosenthal inequality. Bull. Polish Acad. Sci. Mathematics 60,

177–185.

[16] Robinson, P.M., 1991. Testing for strong serial correlation and dynamic

conditional heteroskedasticity in multiple regression. J.

Econometrics, 47, 67–84.

[17] Rosenthal, H.P., 1970. On the subspaces of spanned by the sequences

of independent random variables. Israel J. Math., 8, 273–303.