Saddlepoint methods for conditional expectations with applications to risk management

Abstract.

The paper derives saddlepoint expansions for conditional expectations in the form of and for the sample mean of a continuous random vector whose joint moment generating function is available. Theses conditional expectations frequently appear in various applications, particularly in quantitative finance and risk management. Using the newly developed saddlepoint expansions, we propose fast and accurate methods to compute the sensitivities of risk measures such as value-at-risk and conditional value-at-risk, and the sensitivities of financial options with respect to a market parameter. Numerical studies are provided for the accuracy verification of the new approximations.

Keywords: saddlepoint approximation; conditional expectation; risk management; sensitivity estimation

1. Introduction

The saddlepoint method is one of the most important asymptotic approximations in statistics. It approximates a contour integral of Laplace type in the complex plane via the steepest descent method after a deformation of the original contour in such a way to contain the path of the steepest descent near the saddlepoint. Since the development of saddlepoint approximations for the density of the sample mean of i.i.d. random variables by Daniels (1954), there have been numerous articles, treatises, and monographs on the topic. Their practical values have been particularly emphasized due to both high precision and simple explicit formulas.

Barndorff-Nielsen and Cox (1979) and Reid (1988) initiated statistical applications of the saddlepoint method in inference such as approximating the densities of maximum likelihood estimators, likelihood ratio statistic or M-estimates. The widespread applicability in statistics also includes Bayesian analysis (Tierney and Kadane, 1986; Reid, 2003) and bootstrap inference (Booth, Hall, and Wood, 1992; Butler and Bronson, 2002). Another important application is on financial option pricing and portfolio risk measurements in quantitative finance. From the opening paper of Rogers and Zane (1999), the saddlepoint method has been successfully applied in various contexts such as Lévy processes (Carr and Madan, 2009), affine jump-diffusion processes (Glasserman and Kim, 2009), credit risk models (Gordy, 2002) or value-at-risk (Martin et al., 2001), just to name a few. In such applications, one is usually concerned with obtaining approximate formulae for the density or tail probabilities of a target random variable.

Relevant to this paper, pricing of collateralized debt obligations and computation of conditional value-at-risk requires evaluating the expectation in the form of for a random variable and a constant . Saddlepoint approximations to this expectation are derived in Martin (2006) and Huang and Oosterlee (2011). See Section 2.2 for more details. Along the same line, the conditional expectations of the forms and for a bivariate random vector also appear in financial applications, but their saddlepoint approximations are not yet developed to the best of our knowledge.

Let be a continuous random vector where is a one-dimensional random variable and is a -dimensional random vector. The objective of this paper is to derive saddlepoint expansions for conditional expectations in the form of and for the sample mean and with . Here, the events and indicate the intersections of the respective univariate events. The derivation postulates the classical assumption of the existence of the joint density and the joint cumulant generating function of which is analytic at the origin. We impose an additional assumption of an analytic property for the first derivative of the joint cumulant generating function with respect to the component of evaluated at zero, .

Our first contribution is the derivation of saddlepoint approximations to the conditional expectations when up to the order . As illustrated via several examples, the expansions are simple to apply and very accurate even for the case . The terms in the expansions only require the knowledge of the saddlepoint for the variable and the derivatives of the cumulant generating function of and evaluated at the saddlepoint.

The second contribution is that the saddlepoint expansions for are extended to the multivariate setting for . While the saddlepoint method for can be directly handled as in the case , a major difficulty arises when deriving an expansion of due to the pole of the integrand. To resolve this problem, we adopt the ideas presented in Kolassa (2003) and Kolassa and Li (2010) where the authors study multivariate saddlepoint approximations. We decompose our target integrals into certain forms, for each of which the existing methods can be exploited.

Last but not least, our saddlepoint approximations are demonstrated to be quite valuable in risk management. Either for portfolio risk measurements or hedging of financial contracts, it is important for a risk manager to know their sensitivities with respect to a specific parameter in order to make decisions in a responsive manner. Specifically in this work, we focus on the two widely popular risk measures, value-at-risk and conditional value-at-risk, and propose fast computational methods for their sensitivities by applying the newly developed saddlepoint expansions. Additionally, we show that sensitivities of an option based on multiple assets can be computed via the saddlepoint method. Numerical examples illustrate the effectiveness of our expansions in comparison with simulation based estimates.

The rest of this paper is organized as follows. Section 2 first reviews classical saddlepoint approximations. Section 3 derives saddlepoint approximations to the target conditional expectations for . The results in Section 3 are then extended to the multivariate setting in Section 4. Section 5 presents various applications in risk management with numerical studies. Finally, Section 6 concludes the paper.

2. Preliminaries

2.1. Classical saddlepoint approximation

Let be i.i.d. copies of a continuous random vector in defined on a given probability space . We assume that has a bounded probability density function (PDF) and that its moment generating function (MGF) exists for in some domain containing an open neighborhood of the origin. The cumulant generating function (CGF) of is defined in the same domain .

To describe classical saddlepoint techniques, we begin by recalling the inversion formula of the PDF and the tail probability of : for ,

| (1) | |||||

| (2) |

where is the -th component of and . We consider those values of for which there exists the saddlepoint that solves the following saddlepoint equation

Throughout the paper, and of a multivariate function denote its gradient and Hessian, respectively. The derivation of saddlepoint approximations first makes use of deformation of the original contour in the inversion formulas onto another contour containing the steepest descent curve that passes through the saddlepoint. After a suitable change of variable, asymptotic expansions of Laplace-type integrals are obtained with the help of Watson’s lemma in Watson (1948).

Let be the mean of i.i.d. observations. One classical saddlepoint approximation to the PDF of for , known as Daniels’ formula in Daniels (1954), reads

| (3) |

where is the standardized cumulant of order evaluated at the saddlepoint .

For the tail probability of , the Lugannani-Rice formula developed in Lugannani and Rice (1980) states

| (4) | |||||

for away from zero where and . When is near zero, both and go to zero. Thus a different saddlepoint expansion should be employed in this case, for example, the formula (3.11) in Daniels (1987). The symbol means that there exists a positive constant such that as goes to infinity. The symbols and denote the PDF and the cumulative distribution function (CDF) of a standard normal random variable, respectively. Lastly, .

Such approximations for the PDF and the tail probability have their versions in the multivariate setting. A multivariate saddlepoint expansion of the PDF for a random vector can be easily derived by extending Daniels’ formula, and is presented as follows:

| (5) |

where the quantities , , and are multivariate skewness and kurtosis, defined by

Here, the superscripted denotes the cumulants of the tilted distribution, that is, the derivatives of evaluated at . For example, . The subscripted refers to the - entry of the inverse of the matrix formed by . The derivation of the terms is found in McCullagh (1987).

On the other hand, the multivariate extension of saddlepoint expansions for the tail probability is somewhat difficult to achieve. Recently, Kolassa (2003) and Kolassa and Li (2010) develop saddlepoint techniques to obtain an expansion up to the order ; for a bivariate vector, see Wang (1991). Details are omitted here, but the key approaches of Kolassa (2003) and Kolassa and Li (2010) appear in the multivariate version of our results in Section 4.

2.2. Saddlepoint approximation to

Interestingly, saddlepoint approximations to one special case of conditional expectation have been investigated, regarding the computation of conditional value-at-risk or also known as expected shortfall, a well-known risk measure defined as for a continuous random loss and value-at-risk of at level .

When as in Section 2.1, one approach is to apply saddlepoint techniques to the integral

We first write as , , and replace by Daniels’ formula (3). And then an approximation to the integral of the form

for some function can be employed from Temme (1982). This leads to the following formula which is also observed in Martin (2006) up to the order :

Moreover, Butler and Wood (2004) obtain approximations to the MGF and its logarithmic derivatives of a truncated random variable with the density for a distribution of . Setting and and evaluating their approximation for the logarithmic derivative at zero produce another expansion:

Broda and Paolella (2010) summarize the above mentioned methods in detail.

3. Saddlepoint approximation to conditional expectations

Consider a continuous multi-dimensional random vector where is a one-dimensional random variable and is a -dimensional random vector. We define the multivariate MGF of to be and the corresponding CGF to be for and . Classical assumptions are imposed: the joint PDF of exists and the convergence domain of the CGF contains an open neighborhood of the origin. The marginal CGFs of and are denoted by and , respectively.

The goal of this section is to derive saddlepoint approximations to conditional expectations in the form of and for where and are the means of i.i.d. copies of and , respectively. Thanks to the known formulas for PDFs and tail probabilities, the problem is reduced to utilizing saddlepoint techniques for and .

We first derive multivariate inversion formulas for and which resemble (1) and (2), respectively. We adopt the measure change approach of Huang and Oosterlee (2011).

Lemma 3.1.

For a continuous multivariate random vector , the following relations hold for in the domain of .

| (7) |

for ; and

| (8) |

for where is the -th component of .

Proof.

See Appendix A. ∎

In Sections 3.1 and 3.2, we focus only on a bivariate random vector where for its practical importance. In general, bivariate saddlepoint approximation requires to have a pair of saddlepoints that solve a system of saddlepoint equations, each of which depends on its respective variable. See, for example, Daniels and Young (1991). However, in our development, only one saddlepoint of is needed. Throughout the section, the saddlepoint of is assumed to exist as a solution of the saddlepoint equation

| (9) |

The conditions for the existence of a saddlepoint are discussed in Section 6 of Daniels (1954).

3.1. Saddlepoint approximation to

Before moving onto the derivation of an approximation to , we shall present Watson’s lemma which is the main technique to obtain an asymptotic expansion in powers of in the classical approach. Our derivation relies on Watson’s lemma applied to our new inversion formula in Lemma 3.1. Here, its rescaled version is stated.

Lemma 3.2 (Lemma 4.5.2 in Kolassa (2006)).

If is analytic in a neighborhood of containing the path with , then

is an asymptotic expansion in powers of , provided the integral converges absolutely for some .

From the inversion formula (7) and the relations and , the first target integral (7) is changed to

| (10) |

for some . For notational simplicity, we define

We exploit the classical results to approximate (10) but need to be careful when dealing with in front of the exponential term. The next theorem is our first saddlepoint expansion for conditional expectation.

Theorem 3.3.

Suppose that is analytic in a neighborhood of . The conditional expectation of a continuous bivariate random vector can be approximated via saddlepoint techniques by

where is the saddlepoint that solves (9) and is the standardized cumulant of order evaluated at .

Furthermore, if is also approximated by Daniel’s formula (3), we have the following simple expansion:

| (11) |

Proof.

We integrate on the exactly same contour that is used in Daniels (1954). In Section 3 of Daniels (1954), the original path of integration is deformed into an equivalent path containing the steepest descent curve through the saddlepoint. On the steepest descent curve, the imaginary part of is a constant and its real part decreases fastest near . The contribution of the rest of the path to the target integral is negligible since some of them contribute a pure imaginary part and the others are bounded and converge to zero geometrically as goes to infinity.

Rewrite (10) using the closed curve theorem as

The quantity in the exponent of the integrand, , is an analytic function, and at it is zero and has zero first derivative.

Handling of the integrand in (3.1) can be done via the classical approach well documented in, e.g., Kolassa (2006). Specifically, we make the same substitution (3.2) in Daniels (1954) so that we have

Note that is an analytic function of for for some , and by inverting the series of we obtain an expansion of , the inverse of . Furthermore, it can be shown that

| (13) |

whose verification is outlined in p.86 of Kolassa (2006).

Then we re-parameterize (3.1) in terms of as

| (14) |

Define

From the assumption on and the composition theorem of analytic functions, has an expansion in a neighborhood of . And together with (13), such an expansion leads us to conclude that has a convergent series expansion in ascending powers of . Then an asymptotic expansion of (14) is obtained directly from Lemma 3.2, by inserting the expansion of in (14) and integrating term-by-term:

The first coefficient is . The second term is calculated from

differentiating (13) with respect to , and evaluating at . Detailed computations are omitted as they are straightforward. ∎

In what follows, we illustrate some elementary examples in which the conditional expectation can be exactly calculated.

Example 3.4 (Independent case).

When and are independent, we have . Since , we have and Then (11) turns out to be which is exact.

Example 3.5.

Example 3.6 (Bivariate normal with correlation ).

Let be a bivariate normal random variable, say , with the CGF

and correlation . Note that . Thus,

On the other hand, , and . The saddlepoint is and the 3rd order standardized cumulant is zero. Therefore, (11) yields the exact result as .

3.2. Saddlepoint approximation to

Under the setting of Section 3.1, the second target integral can be rewritten by the inversion formula (8) as

| (15) |

for . Following the approach in Martin (2006), we divide the singularity in the integrand as

Then, (15) becomes the sum of two tractable parts, namely, for

| (16) |

The second complex integral is treated in the similar fashion as in Theorem 3.3, using Lemma 3.2.

Theorem 3.7.

Suppose that is analytic in a neighborhood of and that is continuous at . The conditional expectation of a continuous bivariate random vector can be approximated via saddlepoint techniques by

where solves (9), , and .

When , we have an expansion

Proof.

Let and first we suppose that , or equivalently . Again, we only focus on the integration on the steepest descent curve and take the new variables and as in the proof of Theorem 3.3. To expand , we closely follow the approach in p.92 of Kolassa (2006). First, we integrate the expansion in (13) to obtain

| (18) |

Then, dividing (13) by (18) yields

| (19) | |||||

where . Note that the coefficients of the odd order terms of should be determined since it does not disappear in our derivation, whereas they are removed in the classical approach. See (101) of Kolassa (2006).

Define

whose convergent series exists at by (19) and the analytic property of . Then the second term in (16) becomes

| (20) | |||||

by Watson’s lemma. The coefficients in the expansion (20) are calculated by expanding about . By combining (13), (18) and (19), and taking their derivatives, we compute , and

The desired result is then immediate.

Now suppose that . We set and observe that

For the second term on the right hand side, the saddlepoint that satisfies is . Working with the CGF of and transforming back to , an expansion for can be found. And the final formula turns out to be the same formula as (3.7).

When , equivalently , and

Thus, is analytic at . This yields the following approximation to (20) for by applying Watson’s lemma centered at :

∎

Remark 3.8.

The saddlepoint approximation to the lower-tail expectation can be obtained simply by considering and by using for the second term. Alternatively, we can obtain an approximation to the integral directly by applying (3.7) by replacing with . In either case, the resulting formula is the same.

Example 3.9 (Bivariate normal with correlation ).

Remark 3.10.

4. Multivariate extension

In this section, we consider the case . The saddlepoint of is assumed to exist as the solution to the system of saddlepoint equations

| (22) |

where and for . As before, define

4.1. Extension of Theorem 3.3

Finding an analog of Theorem 3.3 for the case raises no additional difficulty because we can utilize a multivariate version of Watson’s lemma, which is also useful when deriving multivariate saddlepoint approximations to multivariate PDFs. To be specific, we take a differentiable function via the change of variable

| (23) |

which is employed in Kolassa (1996). This function is proved to be analytic for in a neighborhood of , and the detailed construction will be given for in the next subsection. Using the change of variable (23) in (8) with , and applying multivariate Watson’s lemma B.1 with a particular care for , we arrive at the following result.

Theorem 4.1.

Let be a solution to the saddlepoint equation (22) and suppose that is analytic in a neighborhood of . The conditional expectation of a continuous random vector can be approximated via saddlepoint techniques by

The coefficients , and evaluated at satisfy

respectively.

Furthermore, if is also approximated by Daniel’s formula (5), we have the following simple expansion:

Proof.

See Appendix B. ∎

On the other hand, a major concern arises when deriving the extension of Theorem 3.7. Due to the factor in the denominator of (2) which is apparently not a simple pole, multivariate saddlepoint approximation to the tail probability is difficult to compute. Among various methods to tackle the problem, Kolassa and Li (2010) suggest an approach to extend the method of Lugannani and Rice (1980) to the multivariate case. The authors obtain a tractable formula up to the relative order . We essentially adopt their framework but particular attention should be paid to the multiplying factor in computing . Under a suitable assumption on , we decompose in such a way that each corresponding integral can be approximated separately. In the next subsection, the extension of Theorem 3.7 is stated for the case for an illustration and practical usefulness. The entire idea is still applicable when but it is computationally heavy.

4.2. Extension of Theorem 3.7

With , the inversion formula is written as

| (24) |

for . In order to identify the pole in the integrand of (24), we adopt the following explicit functions constructed in Kolassa and Li (2010).

Define as the minimizer of when the first component is fixed, i.e.,

The analytic function satisfying (23) is further specified as

The sign of is chosen for to be increasing in . By the inverse function theorem, there exists an inverse function . To identify the pole after a change of variable, define a function to be the value of that makes zero when is fixed, that is,

Since is defined not to depend on , the determinant of is the product of its diagonals. We can now rewrite (24) as

| (25) | |||||

where

and

We closely follow the program set by Kolassa and Li (2010) and Li (2008), but we face additional difficulties because of the term . Decompose as

where and . It is proved that and that

are analytic. Then, (25) is decomposed into four terms denoted by , and , depending on the respective superscript of .

In order to compute each integral, we impose the assumption that is analytic in a neighborhood of containing , , and . The simplest part, and , can be obtained by applying multivariate Watson’s lemma after modifying the integrand of . High-order terms of (4.2) can be computed, but since the order of and is limited to , we present the result up to .

Lemma 4.2.

The sum of integrals and is expanded as

Proof.

See Appendix C. ∎

For and , we do a change of variable with and set , , and . Let denote the function in terms of . After the change of variable , and are written as

| (27) | |||||

| (28) |

respectively, where , , and an analytic function

Now, we decompose into four terms as

| (29) | |||||

By the assumption on and by the composition theorem of complex variables, there exists a region such that is analytic in and contains , , , and . Partial derivatives , , and are also analytic in . Furthermore,

and

are analytic as well. By plugging (29) into (27) and (28), the integral can be rewritten as

| (30) | |||||

where

and

The terms with analytic integrands disappear as we apply multivariate Watson’s lemma since their contributions are of order .

The importance of the decomposition (30) lies in that and are now the sum of certain integrals such that each term can be treated separately via, e.g., the method proposed in Kolassa (2003). The special case for a bivariate random vector is well described in Chapters 3 and 5 of Li (2008). To approximate the first term in (30), the author approximates by a linear function of , namely since is usually intractable. Then it is proved that the derived saddlepoint expansion using the linear function is equivalent to the saddlepoint expansion without the linear approximation up to the order . As for the second and third integrals, one can expand about and integrate termwise, dropping the terms that contribute the error of with . The same treatments applied to and in Li (2008) lead us to saddlepoint expansions of the second and third integrals, respectively. We do not report the procedure in detail, but summarize the outcome below.

In the rest of this section, we define some auxiliary variables that appear in our expansion. Let and let and be the first and second derivative of evaluated at . They can be specifically computed as

Here,

with . Then we have and . Moreover, let , , , , and .

Theorem 4.3.

Let solve the equation (22) with for , and suppose that is analytic in a neighborhood of containing , , and . With all the notation defined above, of a continuous random vector can be approximated via saddlepoint techniques by

where

and

for . Here, with the CDF of a bivariate standard normal variable .

Remark 4.4.

We omit the cases where or at least one component of is negative due to complexity. However, both can be argued just as bivariate saddlepoint approximations, after applying the decomposition (30).

5. Applications in risk management

Saddlepoint techniques have been successfully applied in various problems of quantitative finance such as vanilla option pricing, portfolio risk measurements. The newly developed saddlepoint approximations allow us to extend the applicability to other important problems in risk management. In particular, we consider fast and accurate computations of risk and option sensitivities which are indispensable in responsive decision making.

First of all, we consider a random portfolio loss , and compute the sensitivities of certain risk metrics utilizing Theorems 3.3 and 3.7. We particularly investigate Euler contributions to risk measures in Section 5.1 and risk sensitivities with respect to an input parameter under a delta-gamma portfolio model in Section 5.2. The second application is on option sensitivities. This exercise is done under two different asset pricing models as described in Section 5.3. Numerical illustrations shall confirm the accuracy and effectiveness of saddlepoint approximations.

5.1. VaR and CVaR risk contribution

Suppose that there is a portfolio with continuous random loss , consisting of assets or sub-portfolios ’s with units of asset (portfolio) for , so that . For a risk measure, say , it is important to know how much the sub-portfolio contributes to from a risk management point of view. Risk measures of our interest are the most frequently used measures, namely, value-at-risk (VaR) , a quantile function of the distribution of , and conditional value-at-risk (CVaR) , also called expected shortfall (ES). Fix , typically taken to be or . Then and are given by and . If necessary, we write or to specify the underlying random loss variable.

For a risk measure that is homogeneous of degree 1 and differentiable in an appropriate sense, the Euler allocation principle can be applied. We refer the reader to Tasche (2008) for more information where the author defines the Euler contributions to VaR and CVaR as and .

As such risk metrics have drawn much attention from researchers and practitioners, saddlepoint approximations to VaR and CVaR risk contributions have been studied in the literature. For example, see Martin et al. (2001) or Muromachi (2004). The VaR risk contribution formula in Martin et al. (2001) is simple to apply and is nothing but the first order approximation. On the other hand, the approximations provided in Muromachi (2004) are rather complex to compute. In particular, the expansions make use of an auxiliary function which acts like a CGF, and thus it is difficult to guarantee the existence of saddlepoints.

5.1.1. A portfolio composed of correlated normals

Suppose that random losses follow a multivariate normal distribution with an -dimensional mean vector and an covariance matrix whose entries are and with . We apply Theorems 3.3 and 3.7 to the Euler contributions with . The resulting formulas are actually the same as the true values:

where is the -th column of , and .

For comparison, we note that the approach of Martin et al. (2001) yields the same result whereas Muromachi’s formula for the VaR contribution results in

Here, is defined as , different from the CGF of . In this example, it is given by

Moreover, is the saddlepoint of , that is, the solution of the following cubic polynomial equation

Lastly, is the standardized cumulant for of order evaluated at .

5.1.2. A portfolio of proper generalized hyperbolic distributions

Consider a proper generalized hyperbolic (GH) distribution which is a GH distribution with the restricted range of parameters and . This excludes some cases such as variance gamma distribution, but still continues to nest hyperbolic and normal inverse gaussian distributions. Let denote a random variable that has a proper GH distribution with the parameter set . The MGF of the proper GH is expressed as

Here, is the modified Bessel function of the third kind with index for .

Let be independent random variables. The target portfolio loss is given by where for each . By the scaling property of GH distributions, it is not difficult to check that has the proper GH distribution with the parameter set and that the CGF is given by

where . Finally, . Thanks to the relation

for and , the first derivative of is seen to be

where . The saddlepoint needs to be numerically computed by solving . The solution is unique in the convergence interval of the CGF of ,

The VaR or CVaR risk contribution of the portfolio for the asset , , requires to compute the joint CGF of in order to apply Theorems 3.3 and 3.7. The joint CGF can be easily derived as

where

Then a bit of work shows that

which yields so that is analytic at . By calculating the cumulants needed for Theorems 3.3 and 3.7, we can obtain the VaR and CVaR risk contributions analytically except for the saddlepoint which can be efficiently found by any root-finding method.

For the rest of this subsection, we conduct some numerical experiments with an NIG distribution which is a special case of proper GH distributions. The CGF of is reduced to

The cumulants of at are easily computed. We also have .

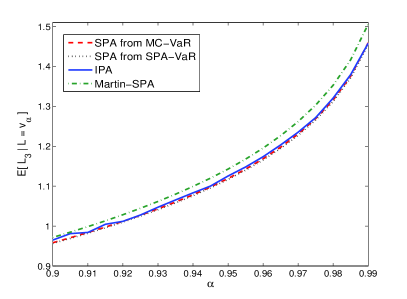

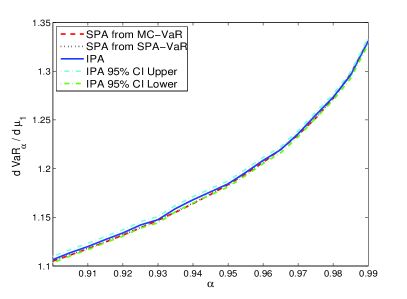

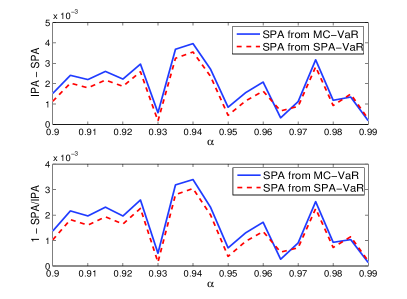

More specifically, we set , and , , and . Figures 1 and 2 show the estimated risk contributions of VaR and CVaR for . We obtain two estimates of VaR using Monte Carlo simulation and saddlepoint techniques, denoted by ‘MC-VaR’ and ‘SPA-VaR’ respectively. Then the VaR contribution is computed first using MC-VaR, denoted by ‘SPA from MC-VaR’, and second using SPA-VaR, denoted by ‘SPA from SPA-VaR’. We also plot the approximate VaR contribution, ‘Martin-SPA’, given in Martin et al. (2001). For comparison, we compute Monte Carlo estimates based on infinitesimal perturbation analysis, or simply IPA estimates, developed in Hong (2008) using random outcomes. The batch size for each VaR contribution estimate is set equal to .

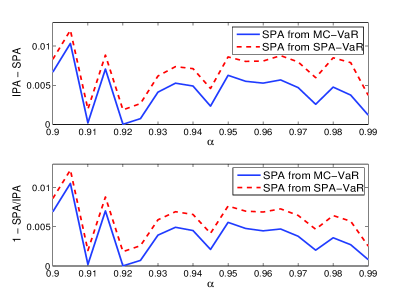

Figure 1 shows that our approximation formulas give very accurate values and that there is a notable difference between Martin-SPA and the others. For a better comparison, the differences between the SPA based estimates and the IPA estimates are shown in the right panel (ii) of Figure 1. In the monitoring interval of , those absolute or relative differences stay small. For example, the average relative difference between the IPA estimates and SPA from SPA-VaR is . The fluctuating behavior of the difference between the estimates is due to the strong dependence of the IPA estimator on the batch size.

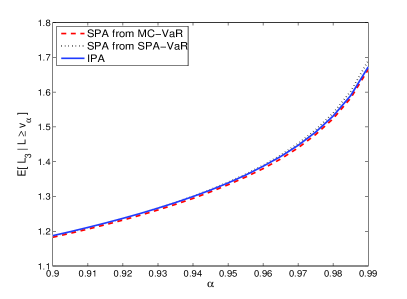

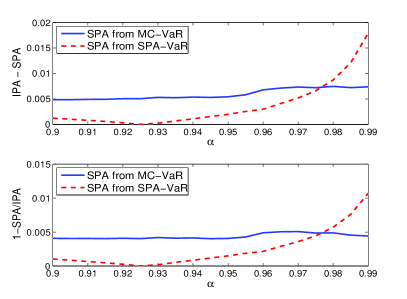

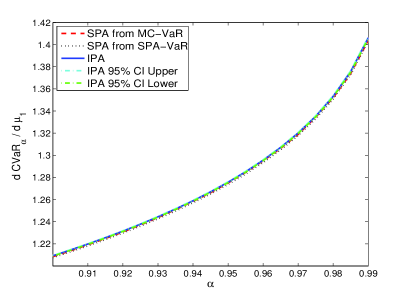

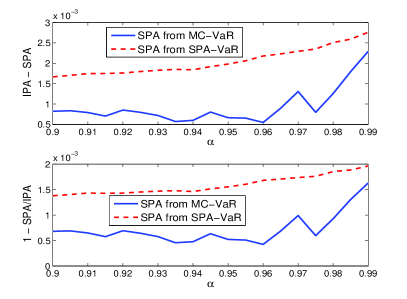

Figure 2 plots the CVaR sensitivities computed by saddlepoint approximations using two VaR estimates, MC-VaR and SPA-VaR, and the results are again denoted by (red) SPA from MC-VaR and (black) SPA from SPA-VaR, respectively. As seen from the figure, our SPA formulas from both MC-VaR and SPA-VaR provide highly accurate approximations to the CVaR contribution. For instance, the average relative difference between the IPA estimates and SPA from SPA-VaR is .

5.2. VaR and CVaR sensitivities of delta-gamma portfolios

A delta-gamma portfolio can be understood as a quadratic approximation to portfolio returns and it has been widely employed in quantitative risk management. For example, it is useful in computing VaR of a portfolio loss that could occur in a short period of time. In this section, we extend the existing results on delta-gamma portfolios by computing VaR and CVaR sensitivities with respect to an input parameter.

Hong (2008) and Hong and Liu (2009) show that the sensitivities of and with respect to a general input parameter can be described as conditional expectations. Let the random loss of a portfolio be a function of and a random variable , where is the parameter with respect to which we differentiate. Under certain technical assumptions in Hong (2008), the VaR sensitivity with respect to can be written as

On the other hand Hong and Liu (2009) prove that the CVaR sensitivity with respect to is simply

as long as certain conditions are met. And the authors develop IPA based estimators using Monte Carlo sampling.

5.2.1. Delta-gamma portfolios

We first present a setting for a delta-gamma portfolio according to Feuerverger and Wong (2000). Let a random vector represent the underlying risk factors in a financial market over a given time period. As often done in the literature, we assume that follows a multivariate normal distribution with mean vector and covariance matrix . These parameters are assumed to be known, but in practice they need to be estimated from either historical data or market data. We are concerned with a portfolio loss due to the random factor , which we simply denote by for some functional .

Taking the Taylor expansion of at up to the second order yields a delta-gamma portfolio loss for the given time horizon as

| (31) |

where is an column vector and is a symmetric matrix. In order to compute the CGF of , rewrite with zero-mean vector multivariate Gaussian as

where . Let with an column vector of independent standard normal random variables using an matrix such that . Performing an eigenvalue decomposition gives us , where diag is the diagonal matrix of eigenvalues, and is an orthonormal matrix whose -th column is the -th eigenvector associated with the -th eigenvalue . This decomposition finally allows us to have

where and . Note that consists of independent standard normal entries for .

Writing where stands for the -th element of , we can compute the MGF and the CGF of as follows:

| (32) |

Note that both of them are analytic near the origin and we can explicitly obtain the convergence region. The saddlepoint of is obtained by solving , which turns out to be equivalent to solving an -th order polynomial equation. The existence of a unique saddlepoint in a delta-gamma portfolio is always guaranteed.

5.2.2. VaR and CVaR sensitivities with respect to the mean vector

In this subsection, we obtain more detailed formulas for risk sensitivities by specifying as the mean vector . In addition to the direct implications that risk sensitivities provide, such computations are helpful in assessing the robustness of the estimates of risk measures when the estimation error of is not negligible as pointed out by Hong and Liu (2009).

The variable of our interest is then

where is the -th element of , is the -th component of , and represents the -th component of a matrix . The joint CGF of a bivariate random vector ( is evaluated using the representation (5.2.2) as

Here, we denote as for brevity. Furthermore, we directly get

which can be shown to be analytic at . Consequently, we have

Now, we are ready to compute the VaR sensitivity and CVaR sensitivity with respect to as

All the assumptions in Hong (2008) and Hong and Liu (2009) are satisfied in this setting. Any root-finding algorithm can be applied to locate the unique saddlepoint . Once we find with the CGF (32) of , we are able to derive saddlepoint approximations of risk sensitivities utilizing Theorems 3.3 and 3.7, as summarized in the following theorem.

Theorem 5.1.

The VaR and CVaR sensitivities with respect to , the mean of a risk factor, of a delta-gamma portfolio loss in (31) are approximated via saddlepoint techniques by

and

respectively. The saddlepoint is the unique solution of

Here, , , and the standardized cumulants are , .

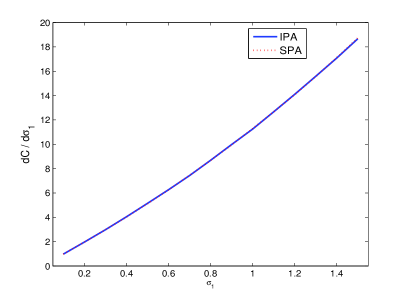

To check numerical performances of our expansions, let us take the same example as appeared in Section 5.1 in Hong and Liu (2009). Let , and The risk factor follows with and For comparison, we compute IPA estimates using observations of with the batch size . An asymptotically valid confidence interval of the VaR sensitivity is also reported, see Section 6 in Hong (2008).

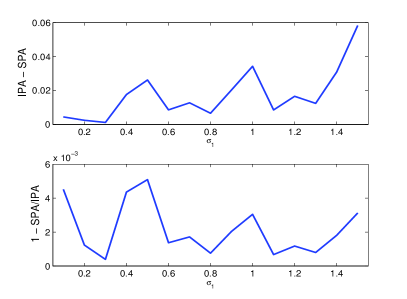

Figure 3 (i) depicts the VaR sensitivities with respect to varying from to . As in Section 5.1, two saddlepoint approximations are given based on VaR estimates using simulation and saddlepoint techniques; We denote them by ‘SPA from MC-VaR’ and ‘SPA from SPA-VaR’, respectively.

The blue curve is the IPA estimates together with 95% confidence interval; ‘CI Upper’ for the upper bound and ‘CI Lower’ for the lower bound of the interval. The batch size has been chosen to make the sample variance reasonably small, specifically, . The differences and relative differences of SPA based estimates compared to IPA estimates are shown in Figure 3(ii). This figure tells us that Theorem 5.1 provides a highly accurate approximation to the sensitivity of VaR regardless of whether we use saddlepoint methods or Monte Carlo simulation for the estimation of . For example, the averaged relative difference for SPA from MC-VaR is reported as . The average (relative) difference between the two VaR sensitivities from MC-VaR and SPA-VaR is even smaller as ().

Figure 4 (i) plots the CVaR sensitivities with respect to varying from to . Similarly as above, we estimate by IPA or saddlepoint methods, denoting the results by (red) SPA from MC-VaR, (black) SPA from SPA-VaR. We also draw IPA estimates as well as interval estimates. Part (ii) of the figure shows the errors and the relative differences of saddlepoint approximations compared to IPA estimates. As seen from Figure 4, we again see that the expansion in Theorem 5.1 gives very fast and accurate results. We, however, note that there are larger differences between the two SPA based estimates (MC-VaR vs. SPA-VaR) than in the case for the VaR sensitivity. The average difference between SPA from MC-VaR and the IPA estimates is whereas SPA from SPA-VaR gives .

5.3. Option sensitivity

Computing sensitivities or greeks of an option price with respect to market parameters is another important application in financial risk management. An option price is typically expressed in terms of the expectation of a payoff functional of underlying asset prices under the risk neutral measure. And its sensitivities can also be expressed as expectations of derivatives of the payoff functional. For instance, Theorem 1 in Hong and Liu (2011) proves that under certain technical conditions the sensitivity of with respect to a parameter is given by

where denotes the underlying asset process. This problem has been extensively studied in the literature both by academics and practitioners. Popular methods include finite difference scheme, the pathwise method (equivalent to IPA), the likelihood ratio method, Malliavin calculus, etc. Our objective is to tackle the problem by employing our saddlepoint expansions.

We choose to work on financial options with two underlying assets and study their sensitivities with respect to volatilities, so called vega. This is for an illustrative purpose and we note that there are many other possibilities. Furthermore, a bivariate geometric Brownian motion process and an exponential variance gamma model are adopted for the underlying asset processes.

5.3.1. Two-asset correlation call option under geometric Brownian motions

Suppose that an underlying asset of an option is a bivariate geometric Brownian motion such that each price process is given by

where is a standard Brownian motion with for under the risk neutral measure . We consider an option based on whose price is

Then the sensitivity of with respect to can be computed by

where and .

Let and . Under , the CGF of is given by . Let be defined by the Radon-Nikodym derivative

It then follows that

| (34) |

Thus, we can approximate the expectation under in (34), , by Theorem 4.3. The second term is also approximated by the existing multivariate tail probability approximation and thus we skip its discussion.

The CGFs of and under are computed as follows:

The saddlepoint of is obtained as

Similarly, and . The assumption of Theorem 4.3 is satisfied since is analytic at . All the variables that appear in Theorem 4.3 can be explicitly computed in this setting.

As the saddlepoint equation is solved analytically and the CGFs under consideration are at most quadratic functions, the relations among the variables , , and are tractable. Therefore, we can easily compute so that . In addition, by employing the inverse functions of and , which are and . With , and . Finally, we arrive at the following saddlepoint expansion:

| (35) |

The true value of can be computed as follows a bivariate normal distribution under , namely,

| (36) |

where is a joint PDF of . And it turns out that (35) and (36) coincide.

5.3.2. Exchange option under exponential variance gamma models

In the second example, we consider an exchange option whose risk neutral valuation formula is given by

based on two assets . Each is assumed to be an exponential variance gamma process, e.g., where is an independent variance gamma process. The CGF of under the risk neutral measure is

for the parameter set . Note that can be interpreted as a time-changed Brownian motion such that where is a gamma process independent of with unit drift and volatility . We also denote the CGF of under by .

We are interested in the sensitivity of the option price with respect to . It can be computed by

| (37) | |||||

where and is again defined by the Radon-Nikodym derivative Take and . The CGF of is ; the CGF of is ; and the joint CGF of then is obtained by under .

The convergence domain of the above CGFs contain zero. And the saddlepoint of is the solution of a polynomial equation of degree four, which can be numerically found by the Newton-Raphson method. Moreover, is an analytic function in the convergence domain of and is given by

Then by applying the saddlepoint formula (21) in Remark 3.10, we can finally compute

in (37). We omit the details of this computation due to its complexity.

Figure 5 shows numerical results of the sensitivity of with respect to under the parameter set given in Table 1 with for brevity. IPA estimates are obtained based on simulated samples of the variance gamma processes under . The average of the estimated relative differences of two approaches is reported as , which also shows great performance of the developed approximations.

| 90 | 100 | 1 | 0.02 | 0.2 | 0.4 | 1 | 0.2 | 0.25 | 0.1 | 0.32 |

6. Conclusion

Saddlepoint approximations for and were derived for the sample mean of a continuous bivariate random vector whose joint moment generating function is known. The extensions of the approximations to the case of a random vector were also investigated. The newly developed expansions were applied to several problems associated with risk measures and financial options. We specifically focused on risk contributions of asset portfolios and risk sensitivities of delta-gamma portfolios. Sensitivities of an option based on two assets with respect to a market parameter were also computed via the proposed saddlepoint approximations. We have performed numerical experiments, showing that the new approximations are not only computationally efficient but also very accurate compared to simulation based estimates. As a whole, our developments have broadened the applicability of saddlepoint techniques by providing explicit and accurate approximations to certain conditional expectations.

Appendix A Proof of Lemma 3.1

We first prove the second inversion formula (8). Suppose that has a non-negative lower bound.

where the density of under is .

The MGF of under is then

where denotes the MGF of under , , and denotes the integration under the new probability having the density . The third equality holds by the Fubini theorem due to the non-negativity of the integrand.

On the other hand, the MGF of under can also be computed as

Therefore,

so that

Thus we obtain the CGF under as

since . By substituting to the inversion formula (2), i.e.

we have the desired result.

In the case that has a negative lower bound with , define so that has a non-negative lower bound. Then the marginal CGF of is and the joint CGF of is where denotes the CGF of . Note that

from the result for the non-negative case. This immediately leads to (8).

Finally, for an unbounded , we take where is a constant. The assumption imposed on the MGF of implies that the MGF also exists in an open neighborhood of the origin. Since is bounded from below,

| (38) |

But, we have

The change of integration and differentiation in the first equality is justified by the continuity of the integrand. Thus, with it decreases monotonically as decreases, and as we have

Since converges to almost surely and monotonically as , we obtain (8) by applying the monotone convergence theorem to both sides of (38).

Appendix B Proof of Theorem 4.1

We first demonstrates a rescaled and multivariate version of Watson’s lemma, Theorem 6.5.2 in Kolassa (2006).

Lemma B.1.

Suppose that ’s are analytic functions from a domain to for , and let

Take such that . Then

where

for .

By a change of variable in (8) with and by the closed curve theorem, we write as

We take unless and . Applying Lemma B.1 to (B) with , and . Obtaining only requires to compute the first and second derivatives of and with respect to , evaluated at . Since computation of coefficients is messy, we here omit the details but report the following formula in Kolassa (2006):

From this formula, all the desired quantities can be derived in a messy but straightforward manner.

Appendix C Proof of Lemma 4.2

The sum of two integrals is expressed as

| (40) | |||||

Let as a function of ; next we decompose as

Then (40) can be computed as

where

The last equality holds by applying multivariate and univariate Watson’s lemma, namely Lemma B.1 and Lemma 3.2. This can be done because and are analytic near ; then we retain the first order terms only.

The proof ends by evaluating the meaningful coefficient as

See (3.1.5) and (3.1.14) of Li (2008) for more details.

References

- Barndorff-Nielsen and Cox (1979) Barndorff-Nielsen, O. and Cox, D. R. (1979). Edgeworth and saddlepoint approximations with statistical applications. J. R. Statist. Soc. B 41(3) 279–312.

- Booth, Hall, and Wood (1992) Booth, J. G., Hall, P., and Wood, A. (1992). Bootstrap estimation of conditional distributions. Ann. Statist. 20(3) 1594–1610.

- Broda and Paolella (2010) Broda, S. A. and Paolella, M. S. (2010). Saddlepoint approximation of expected shortfall for transformed means. Preprint. Available at http://hdl.handle.net/11245/1.327329.

- Butler (2007) Butler, R. W. (2007). Saddlepoint Approximations with Applications. Cambridge: Cambridge University Press.

- Butler and Bronson (2002) Butler, R. W. and Bronson, D. A. (2002). Bootstrapping survival times in stochastic systems by using saddlepoint approximations. J. R. Statist. Soc. B 64(1) 31–49.

- Butler and Wood (2004) Butler, R. W. and Wood, A. T. A. (2004). Saddlepoint approximation for moment generating functions of truncated random variables. Ann. Statist. 32(6) 2712–2730.

- Carr and Madan (2009) Carr, P. and Madan, D. (2009). Saddlepoint methods for option pricing. J. Comp. Finance 13(1) 49–61.

- Daniels (1954) Daniels, H. E. (1954). Saddlepoint approximations in statistics. Ann. Math. Statist. 25(4) 631–645.

- Daniels (1987) Daniels, H. E. (1987). Tail probability approximations. Internat. Statist. Rev. 55(1) 37–46.

- Daniels and Young (1991) Daniels, H. E. and Young, G.A. (1991). Saddlepoint approximation for the studentized mean, with an application to the bootstrap Biometrika 78(1) 169–179.

- Feuerverger and Wong (2000) Feuerverger, A. and Wong, A. C. M. (2000). Computation of value-at-risk for nonlinear portfolios. J. Risk. 3(1) 37–55.

- Glasserman and Kim (2009) Glasserman, P. and Kim, K. (2009). Saddlepoint approximations for affine jump-diffusion models. J. Econ. Dyn. Control 33(1) 15–36.

- Gordy (2002) Gordy, M. B. (2002). Saddlepoint approximation of CreditRisk+. J. Bank. Financ. 26(7) 1335–1353.

- Hong (2008) Hong, L. J. (2008). Estimating quantile sensitivities. Oper. Res. 57(1) 118–130.

- Hong and Liu (2009) Hong, L. J. and Liu, G. (2009). Simulating sensitivities of conditional value-at-risk. Manage. Sci. 55(2) 281–293.

- Hong and Liu (2011) Hong, L. J. and Liu, G. (2011). Kernel estimation of the greeks for options with discontinuous payoffs. Oper. Res. 59(1) 96–108.

- Huang and Oosterlee (2011) Huang, X. and Oosterlee, C. W. (2011). Saddlepoint approximations for expectations and an application to CDO pricing. SIAM J. Financial Math. 2(1) 692–714.

- Jensen (1995) Jensen, J. L. (1995). Saddlepoint Approximations. Oxford: Oxford University Press.

- Kolassa (1996) Kolassa, J. (1996). Higher-order approximations to conditional distribution functions. Ann. Statist. 24(1) 353–364.

- Kolassa (2003) Kolassa, J. (2003). Multivariate saddlepoint tail probability approximations. Ann. Statist. 31(1) 274–286.

- Kolassa (2006) Kolassa, J. (2006). Series Approximation Methods in Statistics. 3rd ed. New York: Springer.

- Kolassa and Li (2010) Kolassa, J. and Li, J. (2010). Multivariate saddlepoint approximations in tail probability and conditional inference. Bernoulli 16(4) 1191–1207.

- Li (2008) Li, J. (2008). Multivariate Saddlepoint Tail probability Approximations, for Conditional and Unconditional Distributions, based on the Signed Root of the Log Likelihood Ratio Statistic. PhD dissertation, Rutgers Univ., Dept. Statistics and Biostatistics.

- Lugannani and Rice (1980) Lugannani, R. and Rice, S. (1980). Saddlepoint approximations for the distribution of the sum of independent random variables. Adv. in Appl. Probab. 12(2) 475–490.

- Martin (2006) Martin, R. (2006). The saddlepoint method and portfolio optionalities. Risk 19(12) 93–95.

- Martin et al. (2001) Martin, R, Thompson, K, and Browne, C. (2001). VAR: who contributes and how much? Risk 14(8) 99–102.

- McCullagh (1987) McCullagh, P. (1987). Tensor Methods in Statistics. New York: Chapman and Hall.

- Muromachi (2004) Muromachi, Y. (2004). A conditional independence approach for portfolio risk evaluation. J. Risk 7(1) 27–53.

- Reid (1988) Reid, N. (1988). Saddlepoint methods and statistical inference. Statist. Sci. 3(2) 213–227.

- Reid (2003) Reid, N. (2003). Asymptotics and the theory of inference. Ann. Statist. 31(6) 1695–1731.

- Rogers and Zane (1999) Rogers, L. C. G. and Zane, O. (1999). Saddlepoint approximations to option prices. Ann. Appl. Probab. 9(2) 493–503.

- Tasche (2008) Tasche, D. (2008). Capital allocation to business units and sub-portfolios: the Euler principle. In Pillar II in the New Basel Accord: The Challenge of Economic Capital 423–453.

- Temme (1982) Temme, N. M. (1982). The uniform asymptotic expansion of a class of integrals related to cumulative distribution functions. SIAM J. Math. Anal. 13(2) 239–253.

- Tierney and Kadane (1986) Tierney, L. J. and Kadane, J. B. (1986). Accurate approximations for posterior moments and marginal densities. J. Amer. Statist. Assoc. 81(393) 82–86.

- Wang (1991) Wang, S. (1991). Saddlepoint approximation for bivariate distribution. J. Appl. Probab. 27(3) 586–597.

- Watson (1948) Watson, G. N. (1948). Theory of Bessel Functions. Cambridge: Cambridge Univ. Press.