Bayesian Inference for High Dimensional Changing Linear Regression with Application to Minnesota House Price Index Data

Abstract

In many applications, the dataset under investigation exhibits heterogeneous regimes that are more appropriately modeled using piece-wise linear models for each of the data segments separated by change-points. Although there have been much work on change point linear regression for the low dimensional case, high-dimensional change point regression is severely underdeveloped. Motivated by the analysis of Minnesota House Price Index data, we propose a fully Bayesian framework for fitting changing linear regression models in high-dimensional settings. Using segment-specific shrinkage and diffusion priors, we deliver full posterior inference for the change points and simultaneously obtain posterior probabilities of variable selection in each segment via an efficient Gibbs sampler. Additionally, our method can detect an unknown number of change points and accommodate different variable selection constraints like grouping or partial selection. We substantiate the accuracy of our method using simulation experiments for a wide range of scenarios. We apply our approach for a macro-economic analysis of Minnesota house price index data. The results strongly favor the change point model over a homogeneous (no change point) high-dimensional regression model.

Keywords: Change Point Detection, High-dimensional Regression, Variable Selection, Bayesian Inference, Markov Chain Monte Carlo, Minnesota House Price Data

1 Introduction

Modern statistical modeling and inference continue to evolve and be molded by the emergence of complex datasets, where the dimension of each observation in a dataset substantially exceeds the size of the dataset. Largely due to recent advances in technology, such high dimensional datasets are now ubiquitous in fields as diverse as genetics, economics, neuroscience, public health, imaging, and so on. One important objective of high dimensional data analysis is to segregate a small set of regressors, associated with the response of interest, from the large number of redundant ones. Penalized least square approaches like Lasso (Tibshirani 1994), SCAD (Fan and Li 2001), Elastic Net (Zou and Hastie 2005), adaptive Lasso(Zou 2006) etc. are widely employed for high dimensional regression analysis. Bayesian alternatives typically proceed by using hierarchical priors for the regression coefficients aimed at achieving variable selection. Bayesian variable selection methods include stochastic search variable selection (George and McCulloch 1993), spike and slab prior (Ishwaran and Rao 2005), Bayesian Lasso (Park and Casella 2008), horseshoe prior (Carvalho et al. 2010), shrinkage and diffusion prior (Narisetty and He 2014) among others.

Most of the aforementioned approaches assume a single underlying model from which the data is generated. Such homogeneity assumptions may be violated in systems where the variables involved exhibit dynamic behavior and interactions. Common examples include economic time series (Chen and Gupta 1997; Kezim and Pariseau 2004; Lenardon and Amirdjanova 2006), climate change data (Reeves et al. 2007), DNA micro-array data (Baladandayuthapani et al. 2010) and so on. Change point models provide a convenient depiction of such complex relationships by splitting the data based on a threshold variable and using a homogeneous model for each segment. There exists enormous literature on Bayesian methodology addressing various change point problems (see for example Carlin et al. 1992; Barry and Hartigan 1993; McCulloch and Tsay 1993; Adams and MacKay 2007; Turner et al. 2009, among others).

Changing linear regression models are a subclass of change point problems, where the linear model relating the response to the predictors varies over different segments of the data. Segmentation of the dataset is typically based on unknown change points of a threshold variable like time or age or some other contextual variable observed along with the data. Economic datasets constitute a major domain of application of changing linear models. Many economic time series datasets may be collected over different political and financial regimes, thereby containing several change points with respect to the association with the predictors. In a low dimensional setting, Carlin et al. (1992) used Gibbs’ sampling techniques for changing linear models to deliver fully Bayesian inference about the location of the change points and the regression coefficients for each segment. When the set of possible predictors is high dimensional, an additional objective is to identify the (possibly different) sparse supports for each segment. Despite the abundance of Bayesian literature on high dimensional regression and on change point models, it appears there is no extant Bayesian work on high dimensional changing linear regression.

This manuscript intends to bridge this gap by proposing a hierarchical methodology for high dimensional changing linear models. We embed Bayesian variable selection techniques in a change point setup to simultaneously detect the number and location of the change points as well as to identify the true sparse support for each of the linear models. We use teh newly proposed shrinkage and diffusion priors (Narisetty and He 2014) for the regression coefficients in each segment to perform variable selection. We provide an efficient Gibbs’ sampler that delivers full posterior inference on the change points, posterior selection probabilities for each variable for all segments and posterior predictive distributions for the response. Our fully Bayesian approach is flexible to the choice of variable selection priors and offers the scope for several structural modifications tailored to specific data applications. For example, constraints like grouping the selection of a variable across all the segments can be easily achieved using group selection priors. Other constraints like partial selection within or between the segments can also be accommodated in our setup. Numerical studies reveal that for a wide range of scenarios, our proposed methodology can accurately detect the change points and select the correct set of predictors. We demonstrate the applicability of our method for a macro-economic analysis of Minnesota house price index data. The results strongly favor our change point model over a homogeneous high dimensional regression model.

Classical penalized least square approaches mentioned earlier can also be used in a change point setup. By treating the unknown change points as additional tuning parameters, one can split the data using fixed values of these change points and use some penalized loss function to achieve variable selection for each segment. For example, Lee et al. (To appear) uses Lasso penalty to estimate the coefficients for each segment. Subsequent application of cross validation or model selection techniques will yield the optimal change points from a grid of possible values. However, our fully Bayesian approach has several advantages over this. Firstly, the grid search approach is computationally highly inefficient especially for more than one change points. On the other hand, a prior specification for the change points in our Bayesian model enables standard MCMC techniques to efficiently generate posterior samples. Moreover, in many real applications, change in association between variables can occur over a range of the threshold variable. Point estimates of change points obtained from classical approaches fail to accurately depict such scenarios. Bayesian credible intervals obtained from the posterior distributions provide a much more realistic quantification of the uncertainty associated with the location of the change points, which is very difficulty to accomplish if one uses the grid search approach.

The rest of the manuscript is organized as follows. In Section 2 we present our methodology in details including extensions to unknown number of change points and alternate prior choices. Results from several simulated numerical studies are provided in Section 3. In Section 4 we present the details of a house price index data analysis using our change point methodology. We conclude this paper with a brief review and pointers to future research.

2 Method

We consider a traditional high dimensional setup with the response vector and corresponding covariate matrix where can be larger than . We further assume that for every observation we observe another quantitative variable such that the association between and depends on the values of . In a linear regression setup, this dynamic relationship between the response and the corresponding vector of covariates can be expressed as for all such that where . The change-points are typically unknown while the number of change-points may or may not be known depending on the application.

As the number of regressors () is large, our goal is to select the relevant variables for this regression. However, for this changing linear regression, the set of relevant regressors may depend on the value of the threshold variable and variable selection procedures applied disregarding the dependence on can lead to erroneous variable selection. Let denotes the support of where is typically much less than . Our goal is to simultaneously detect the change-points and estimate for all . We initially assume only one change-point i.e. . Extensions to more than one (and possibly unknown number of) change points are discussed later in Section 2.2.

2.1 One Change Point Model

We assume a changing linear regression model

| (2.3) |

where , are both sparse vectors such that and denotes the independent and identically distributed noise. In order to accomplish variable selection both before and after the change point, we use shrinking and diffusion (BASAD) priors proposed in Narisetty and He (2014) for and . To be specific, we assume for where is a vector of zeros and ones. The hyper-parameters and are scalars chosen to be very small and very large respectively. Hence, —the component of —is assigned a shrinking prior if equals and a diffusion (flat) prior if . ’s are assumed to be apriori independent each following . Hence controls the prior model size for the segment. The choices for the hyper-parameters , and are discussed in Section 3. We assume a uniform prior for the change-point and a conjugate Inverse Gamma prior for the noise variance . The full Bayesian model can now be written as:

| (2.4) |

We use Gibbs’ sampler to obtain posterior samples of , and for . Let denote the full-conditional distribution of in the Gibbs’ sampler. We use similar notation to denote the other full conditionals. Let and . For , let and denote the response vector and covariate matrix obtained by stacking up the observations . From the full likelihood in (2.1), we have

where denotes the density of standard normal distribution. We observe that the full conditionals of , and follow conjugate distributions and are easily updated via the Gibbs’ sampler. Only does not correspond to any standard likelihood and we use a Random Walk Metropolis-Hastings step within the Gibbs’ sampler to update .

2.2 Multiple change points

So far we have limited our discussion to the presence of only one change point. However, our method can be easily extended to multiple change points. If we have change points , the joint likelihood in (2.1) can be generalized to

| (2.5) |

To ensure identifiability of the change points, the prior should be supported on . To accomplish this we choose as the density of ordered statistics of a sample of size from . The Gibbs’ sampler remains essentially same as in Section 2 with the Metropolis random walk step now being used to update the entire change point vector .

2.3 Determining the number of change points

However, often in applications, the number of change points is unknown. In our fully Bayesian approach this can potentially be handled by adding a prior for the number of change points (). Introducing this additional level of hierarchy comes with the caveat that different values of yields parameter sub-spaces of different sizes and interpretations. To elucidate, a one change point model splits the data into two segments, with separate coefficient vectors and , creating a parameter space of dimension whereas a no change point model has a single of dimension with a possible interpretation that it is some average of and over the two segments. Therefore, a Markov Chain Monte Carlo sampling for will involve jumping within and between different sub-spaces.

Green (1995) proposed the extremely general and powerful reversible jump MCMC (RJMCMC) sampler for sampling across multiple parameter spaces of variable dimensions. We can seamlessly adopt an RJMCMC joint sampler to obtain the posterior distribution for the number of change points. When naively implemented, RJMCMC experiences poor acceptance rates for transitions to parameter sub-spaces with different dimensionality. This leads to widely documented convergence issues (Green and Hastie 2009; Fan and Sisson 2011). The problem will be exacerbated in our setup due to the high dimensionality of the parameter spaces.

Several improvements and alternatives to RJMCMC have been proposed over the years including efficient proposal strategies to effectuate frequent cross-dimensional jumps (Richardson and Green 1997; Brooks et al. 2003; Ehlers and Brooks 2008; Farr et al. 2015), product space search (Carlin and Chib 1995; Dellaportas et al. 2002) and parallel tempering (Littenberg and Cornish 2009). All these approaches can be adapted in our setup to determine the number of change points. However, many of these approaches are accompanied by their own computational burden such as running several chains or apriori obtaining posterior distributions for each individual model before running the joint sampler. We concur with Han and Carlin (2001) and Hastie and Green (2012) that it is often expedient to use simpler model selection approaches based on individual models. Hence, popular Bayesian model comparison metrics like DIC (Spiegelhalter et al. 2002) and l-measure (Gelfand and Ghosh 1998) remains relevant to select the number of change points in our case. For example, if is the complete set of parameters associated with the model, for each we can compute the DIC score

| (2.6) |

where is the deviance function and is interpreted as effective sample size. Hence, DIC penalizes more complex models and is particularly suitable for our change point context where higher number of change points will lead to overfitting. Parallel computing can be utilized to simultaneously run the MCMC sampler for different values of and then the optimal can be selected as the one yielding lowest DIC score.

All the methods for selecting the number of change points discussed here can be used in conjunction with our approach. It is prudent to predicate the choice on the nature of the application at hand and the computational resources available.

2.4 Alternate prior choices

We observe from Equation 2.1 that conditional on the value of the change point , the joint likelihood can be decomposed into individual likelihoods for the regression before and after the change point along with the corresponding priors for the regression coefficients. This allows for a lot of flexibility in the choice of priors for the regression coefficients.

We have focused on the BASAD prior. One can also use other priors to achieve variable selection. For example, using Laplace (double exponential) priors for the ’s will yield a Bayesian Lasso (Park and Casella 2008) with change point detection. To facilitate the discussion, consider the one change point model. By using the Laplace prior, the full hierarchical specification for the coefficient vectors for can be specified as:

| (2.7) |

The prior specification for and can be kept same as in (2.1). The Gibbs’ sampler for the Bayesian Lasso provided in Park and Casella (2008) can now be used to sample from the following full conditionals:

Additional information regarding grouping or structuring of the variables are often available in the context of variable selection. In presence of a change point, additional constraints can specify grouped selection both within and/or between the ’s. For example, in a single change point setup, it may be plausible that the set of relevant variables remain unchanged before and after the change point, with change occurring only with respect to the strength of association between and . Such additional structural constraints both within and across ’s can easily be accommodated in our setup via a suitable choice of prior. To elucidate, we can rewrite (4.2) as where and . To incorporate the constraint that ans share the same support, one can use a Bayesian group lasso (Raman et al. 2009) with M-Laplace priors on the groups for . The M-Laplace prior

has a convenient two-step hierarchical specification:

| (2.8) |

The full conditional distributions of the parameters provided in Raman et al. (2009) can now be used to implement the Gibbs’ sampler with the additional Metropolis Random walk step for updating the change point . Any other information like hierarchical selection or anti-hierarchical selection both within and between the ’s can also be accommodated via suitable priors.

Often, in real data applications, prior knowledge dictates the inclusion of certain variables in the model and variable selection is sought only for the remaining variables. Such constraints can be easily achieved in our setup by using standard Gaussian prior for that specified subset and BASAD prior for the remaining variables.

2.5 Variable selection after MCMC

When there are finite many candidate models, Bayesian model selection typically proceeds by selecting the candidate model with the highest posterior probability. However, in our setup the regression coefficients are continuous. For variable selection, we use the median probability model (Barbieri and Berger 2004) which is computationally easy and is optimal in terms of prediction. To be specific, is included in the model if the posterior probability of is greater than .

3 Numerical Studies

We conducted numerical experiments to illustrate the performance of our method both for single and multiple change points. For all the simulation studies we used MCMC iterations. Multiple chains were run with different choices of initial values and convergence was typically achieved within the first iterations. Nevertheless, we discarded the first as burn-in and used the subsequent samples for inference.

3.1 One change point

We assume and generate data from the model for and for where and . The rows of were independent and identically distributed normal random variables with zero mean and covariance . Two structures were used for — auto-regressive (AR) with and compound symmetry (CS) with . The noise variance was fixed at and the sample size was chosen to be . Two different model sizes — and were used. The change point was chosen to vary between , and . Since, the sample size is , these three choices of respectively correspond to changes in the regression model at the initial , middle or later portion of the data. We used three different prior choices for the coefficients — the BASAD prior, the Bayesian Lasso prior (Park and Casella 2008) and the Bayesian Group Lasso prior (Raman et al. 2009). The last choice was used to investigate any possible benefits of using a grouped variable selection as it is known that and has same support. The range of the uniform prior for was chosen to be and a normal proposal density with tuning variance of was used for the Metropolis update of . The prior for was chosen to be . The hyper-parameters , and were chosen as follows. Let denote the initial estimate for . Then and denotes the initial sample sizes for the two segments. We used

where was the sample variance of for . The hyper-parameters were chosen such that the prior model sizes were greater than with probability . These choices of , and were adapted from Narisetty and He (2014).

The posterior median estimates of the change points for all the scenarios are provided in Tables 1 () and 2 ().

| True | BASAD | BL | BGL | |

|---|---|---|---|---|

| 50.5 | 50.5 (50.0, 51.0) | 50.4 (48.9, 51.8) | 50.5 (49.5, 51.5) | |

| AR | 100.5 | 100.5 (100.0, 101.0) | 100.5 (100.0, 101.0) | 100.5 (100.0, 101.0) |

| 150.5 | 150.5 (150.0, 151.0) | 150.5 (150.0, 151.0) | 150.5 (150.0, 151.0) | |

| 50.5 | 50.1 (49.1, 51.9) | 50.0 (49.1, 51.8) | 50.1 (49.1, 51.9) | |

| CS | 100.5 | 100.5 (100.0, 101.0) | 100.5 (100.0, 101.0) | 100.5 (100.0, 101.0) |

| 150.5 | 150.5 (150.0, 151.0) | 150.2 (148.6, 151.0) | 150.4 (149.1, 151.0) |

| True | BASAD | BL | BGL | |

|---|---|---|---|---|

| 50.5 | 50.5 (50.0, 51.0) | 49.7 (47.6, 53.7) | 50.4 (48.2, 53.1) | |

| AR | 100.5 | 101.3 (99.3, 102.0) | 101.3 (99.1, 103.9) | 101.0 (99.1, 103.3) |

| 150.5 | 150.5 (150.0, 151.0) | 151.3 (148.7, 152.9) | 150.7 (150.0, 152.8) | |

| 50.5 | 50.3 (49.1, 51.0) | 50.1 (48.5, 51.8) | 50.2 (49.1, 51.5) | |

| CS | 100.5 | 100.3 (99.1, 101.0) | 100.0 (99.1, 100.9) | 99.9 (99.1, 100.9) |

| 150.5 | 150.5 (150.0, 151.0) | 150.5 (150.0, 151.0) | 150.5 (150.0, 151.0) |

We observe that all the 3 models estimate the change point with high accuracy.

We then turn our attention to variable selection. Let and denote the number of true and false regressors respectively selected for the segment of the data for . As discussed earlier, we used a cut-off of for the posterior probability of the binary ’s in the BASAD model to select the variables. The Bayesian Lasso and Group Lasso are devoid of such binary selection parameters and variable selection was based on the posterior confidence intervals i.e was not selected if its posterior confidence interval covered zero. Table 3 provides the and numbers for each method for .

| AR | CS | |||||||

|---|---|---|---|---|---|---|---|---|

| True | BASAD | BL | BGL | BASAD | BL | BGL | ||

| 3 | 3 | 3 | 3 | 3 | 2* | 3 | ||

| 3 | 3 | 3 | 3 | 3 | 3 | 3 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 0 | 0 | 2 | 2 | 0 | 2 | 1 | ||

| 3 | 3 | 3 | 3 | 3 | 3 | 3 | ||

| 3 | 3 | 3 | 3 | 3 | 3 | 3 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 3 | 3 | 3 | 3 | 3 | 3 | 3 | ||

| 3 | 3 | 2* | 3 | 3 | 2* | 3 | ||

| 0 | 0 | 0 | 0 | 0 | 2 | 1 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

We observe that the BASAD prior achieves perfect variable selection for all the scenarios while the Bayesian LASSO often misses out on a true variable and includes some incorrect predictors. The Bayesian Group LASSO always selects the true set of regressors but often includes one false regressor. For , (Table 4), the BASAD once again selects the exact set of predictors.

| AR | CS | |||||||

|---|---|---|---|---|---|---|---|---|

| True | BASAD | BL | BGL | BASAD | BL | BGL | ||

| 3 | 3 | 1* | 3 | 3 | 1* | 2* | ||

| 3 | 3 | 3 | 3 | 3 | 3 | 3 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 3 | 3 | 3 | 3 | 3 | 3 | 3 | ||

| 3 | 3 | 3 | 3 | 3 | 3 | 3 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 3 | 3 | 3 | 3 | 3 | 3 | 3 | ||

| 3 | 3 | 1* | 3 | 3 | 0* | 3 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

However, the performance of the Bayesian Group LASSO and especially the Bayesian LASSO worsens with the latter often being able to select only one correct predictor.

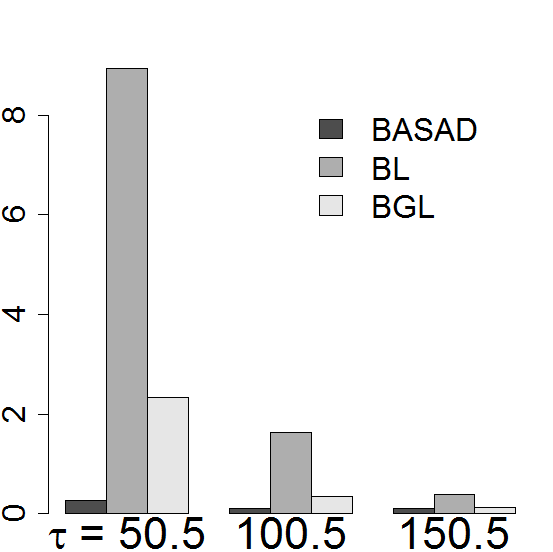

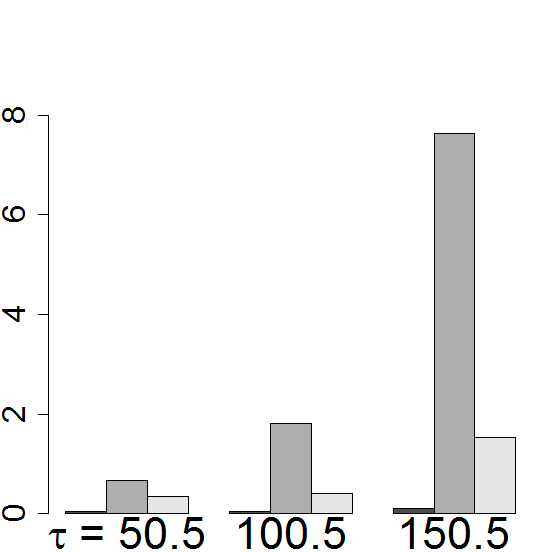

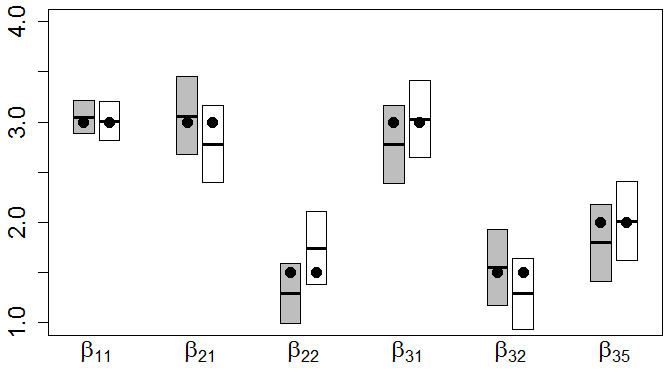

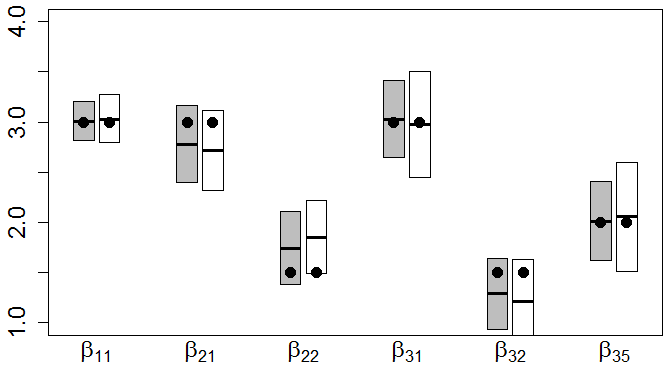

In additional to the variable selection metrics, we also assess the three methods based on the coefficient estimates for the true predictors using the Mean Squared Error truncated on the true support i.e.

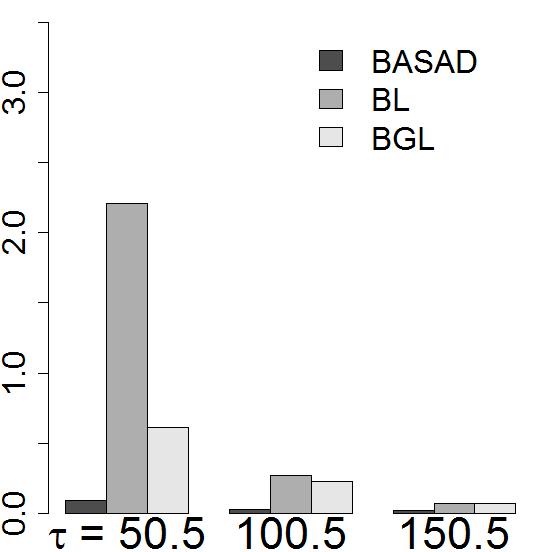

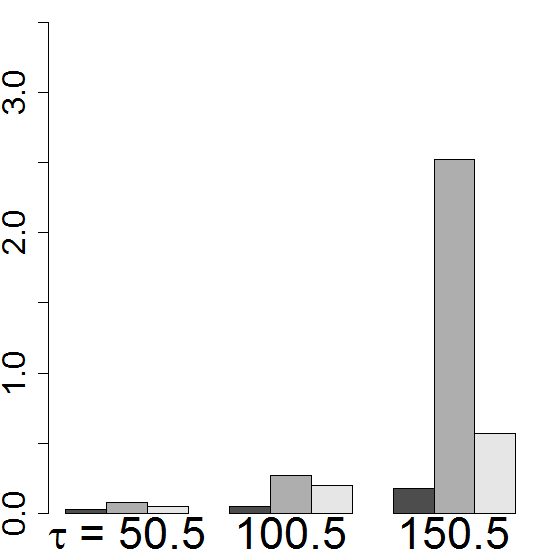

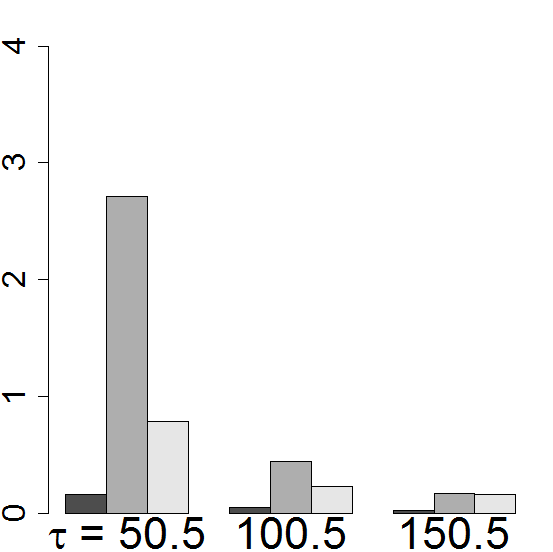

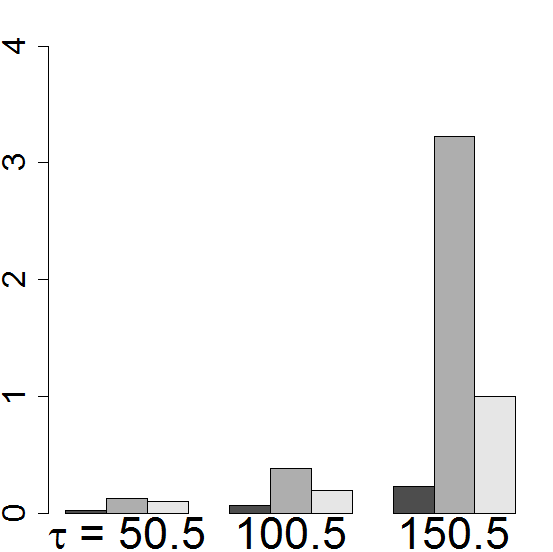

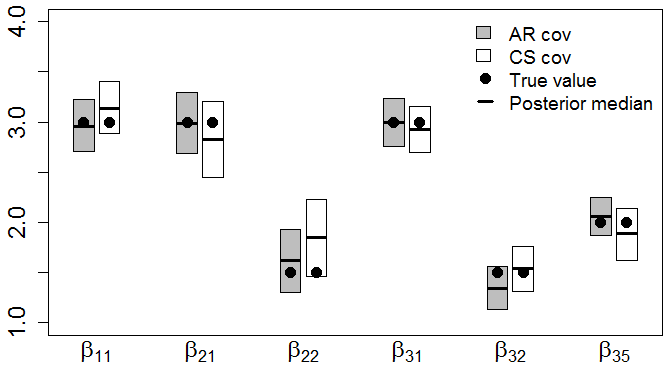

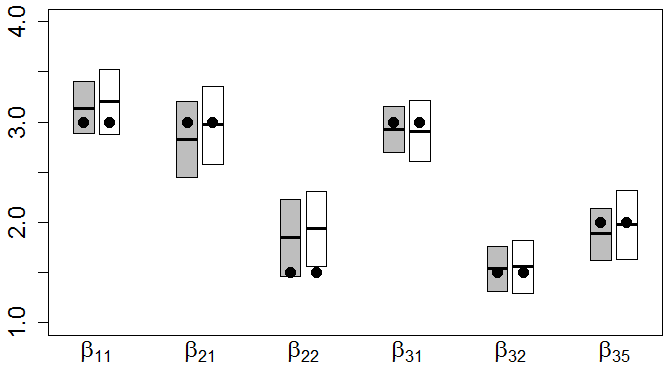

where denotes the true support of and denote its posterior estimate. Figures 1 and 2 plots the numbers for and respectively.

We observe that the BASAD stands out with uniformly lowest MSE numbers across all scenarios. It is important to note that, tends to be higher when while is higher when . This behavior is expected as for , sample size for estimating is effectively while that for is . The Bayesian Lasso seems to be worst impacted by this effective sample size. It performs worse for the Compound Symmetry covariance structure and for higher model size (). The Bayesian Group Lasso, enjoying the additional knowledge of the structural constraint, conceivably performs better than the Bayesian Lasso. However, the BASAD seems to be least impacted by effective sample size, model size or covariance structure producing accurate variable selection, change point detection and estimation across all scenarios.

3.2 Two change points

We demonstrate the applicability of our method to multiple change points using a two change point setup. The three coefficient vectors are given by

Three pairs of values for the change points are selected — , and . Other specifications including sample size, model size and covariance of the predictors are kept unchanged from Section 3.1. We observed in Figures 1 and 2, that the Bayesian Lasso becomes erratic for small effective sample sizes. For 2 change points, the effective sample size is further lowered and the Bayesian Lasso faced convergence issues in the MCMC sampler. The Bayesian Group Lasso also cannot be used here as the coefficient vectors for different segments do not share a common support. Hence, we only present the results for the BASAD prior.

Table 5 presents the change-point estimates for all the scenarios. We observe that all the change points are accurately estimated.

| (50.5,100.5) | (50.5,150.5) | (100.5,150.5) | |||

|---|---|---|---|---|---|

| AR | 50.8 (49.2, 53.9) | 50.5 (48.3, 52) | 100.6 (100, 102.7) | ||

| 101.5 (101, 103.3) | 148.6 (146.9, 151.7) | 150.1 (149, 152.5) | |||

| CS | 50.6 (45.7, 52.9) | 50.8 (49.1, 52.9) | 98.6 (92.6, 100.8) | ||

| 101.3 (97.3, 104.1) | 151.3 (148.1, 152.7) | 151 (145.4, 152.8) | |||

| AR | 50.6 (45.7, 52.9) | 50.8 (49.1, 52.9) | 98.6 (92.6, 100.8) | ||

| 101.3 (97.3, 104.1) | 151.3 (148.1, 152.7) | 151 (145.4, 152.8) | |||

| CS | 47.2 (43.3, 51.8) | 50.4 (49.1, 51.9) | 101.5 (97.6, 103.2) | ||

| 102.1 (97.9, 105.8) | 147.4 (142.1, 151.8) | 146.2 (140.3, 151.3) |

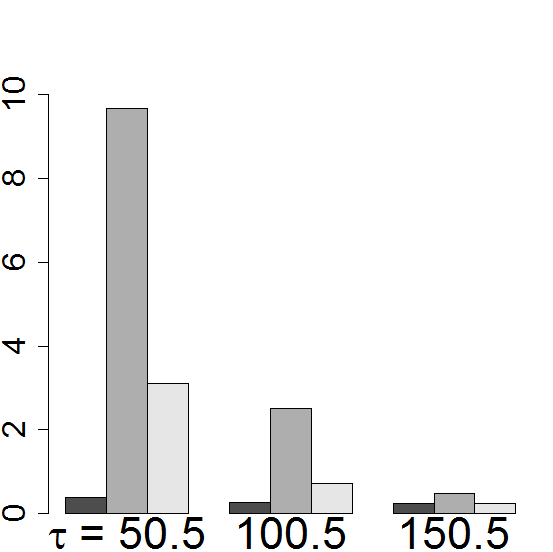

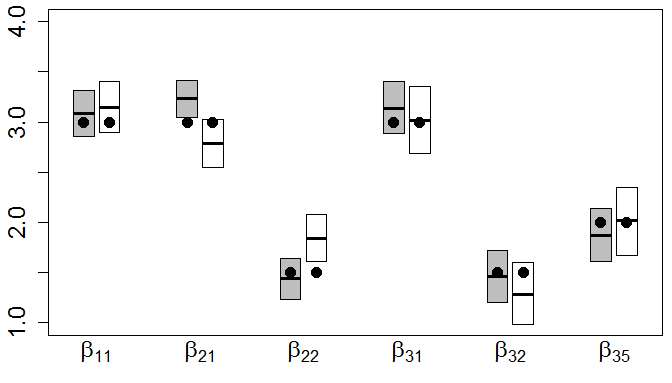

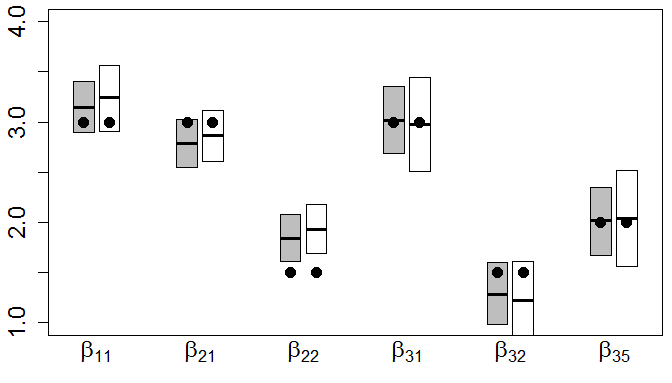

Turning to variable selection, once again, BASAD identified the exact set of predictors across all scenarios. Figure 3 provides the estimates of the non-zero coefficients in the model.

We observe that with the exception of the the second entry of , all the non-zero coefficients were well within the posterior confidence intervals. Overall, we observe that even for multiple change points, our methodology can accurately detect the change points, identify the correct sets of predictors, and estimate the regression coefficients.

4 Minnesota House Price Index Data

In this section we apply our methodology to conduct an empirical analysis of Minnesota house price index data.

4.1 Literature Review

The expansive literature on statistical analysis of house price data can be broadly classified into two major subdivisions based on their objectives. The first category of articles is aimed at forecasting individual house prices based on the constituent characteristics of the houses. Such hedonic regression models usually incorporate information regarding the structure, location, neighborhood and selling history of the house to determine its price range (refer Malpezzi 2003, for a comprehensive review on hedonic models). The second class of analysis focuses on understanding how real estate prices impact or get impacted by the economy of a country or a region. Until very recently this segment received relatively scant attention because interaction between housing market and macroeconomic variables was often deemphasized (Leung 2004). The US sub-prime mortgage crisis between 2007 and 2009 triggered by the collapse of the housing market has recuperated interest on studying this relationship.

Several empirical analysis furnish evidence for co-movements of house price indices and other macro-economic variables like Gross Domestic Product (GDP), consumer price indices, unemployment rates, interest rates, stock price indices and so on (Apergis 2003; Hofmann 2003; Tsatsaronis and Zhu 2004; Otrok and Terrones 2005; Renigier-Biłozor and Wiśniewski 2013; Panagiotidis and Printzis 2015). Multivariate regression models have been used to understand the relationship between these macro economic variables and house price index (hpi) in Ukraine (Mavrodiy 2005), Sweden (Strömberg et al. 2011) and Malaysia (Ong and Chang 2013). These analyses often assume a single underlying time-homogeneous relationship between hpi and the explanatory variables. Such an assumption may be far fetched in reality where correlation between hpi and its macroeconomic determinants may exhibit differential trends over time. For example, as noted in Ahamada and Diaz Sanchez (2013), the US stock market crash in the ‘Internet bubble burst’ of 2001-2002 was not accompanied by plummeting house prices whereas in the sub-prime mortgage crisis in 2007-2009, stocks and house prices witnessed simultaneous collapse.

While the impact of macroeconomic variables on US house prices has been analysed in the literature (Case et al. 2001; Catte et al. 2004) any relevant literature focusing on similar analysis at state level has eluded us. As housing markets are local in nature (Garmaise and Moskowitz 2002), a state level macro-analysis may reveal trends not reflected in a similar nationwide study. The state of Minnesota is home to 18 Fortune 500 companies (http://mn.gov/deed/business/locating-minnesota/companies-employers/fortune500.jsp) and has the second highest number of Fortune 500 companies per capita. Furthermore, the Minneapolis-St. Paul metropolitan area hosts the highest number of Fortune 500 companies per capita among the 30 largest metropolitan areas in US. Hence the local industries may play a significant role in determining real estate prices in Minnesota. We use a multivariate regression model with change points to investigate the relationship between the state-level hpi of Minnesota and both local and national macro-economic variables.

4.2 Data and Model

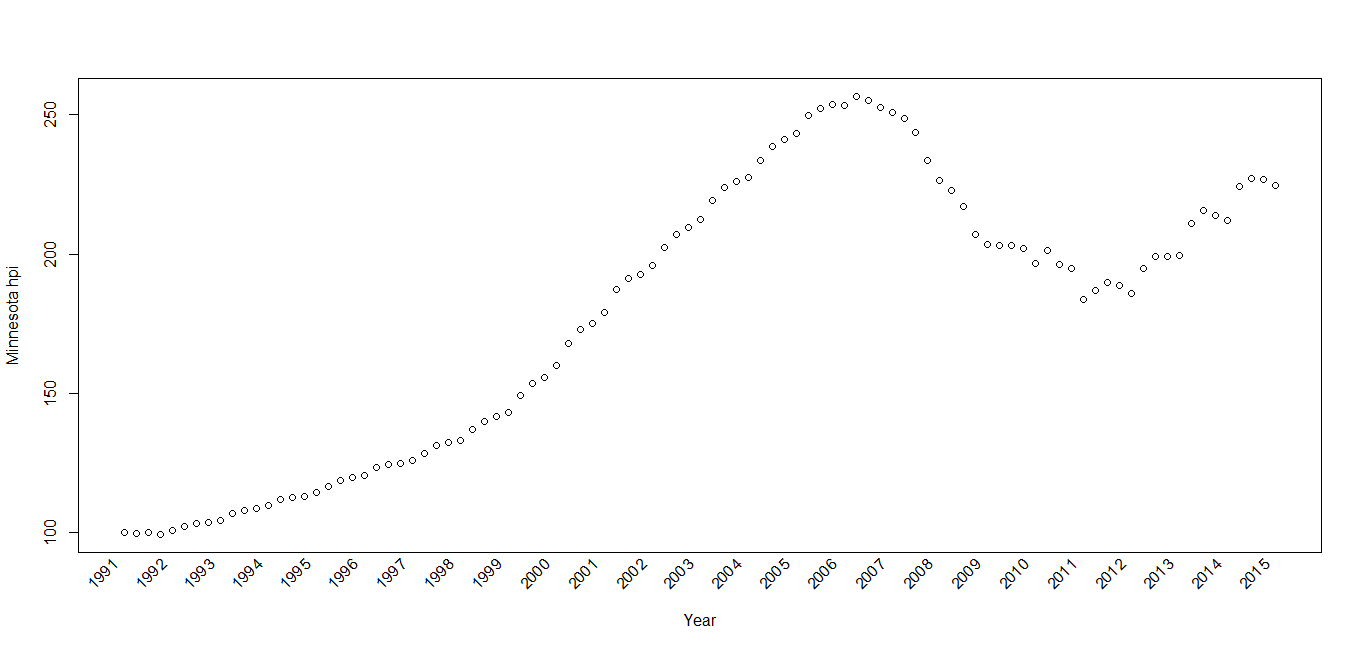

We use quarterly Minnesota hpi data published by the Federal Housing Finance Agency (FHFA) from the first quarter of 1991 to the first quarter of 2015 for our analysis. Quarterly state hpi data was obtained from http://www.fhfa.gov/DataTools/Downloads/Documents/HPI/HPI_EXP_state.txt. Figure 4 plots the hpi time series. We observe that there are two possible break points — one around 2006-2008 where hpi starts to depreciate after reaching a peak and one later around 2012 where hpi starts its revival. However, this merely suggests possible change points in terms of the overall mean level for hpi. Our focus here is the relation between house price and other economic factors. We want to see if there is a change point in time such that the model before and after the change point is different.

The macro-economic indices used as explanatory variables include national unemployment rate (unemp) and national consumer price indices (cpi). The monthly cpi data was obtained from http://inflationdata.com/inflation/consumer_price_index/historicalcpi.aspx?reloaded=true#Table?reloaded=true while the unemployment data was obtained from http://data.bls.gov/timeseries/LNS14000000. All monthly indices were averaged to convert to quarterly indices. Instead of including a national stock index in the model like the S&P 500 or the Dow Jones Industrial Average, we use the stock prices of Minnesota based Fortune 500 companies. 14 out of the 18 Minnesota-based Fortune 500 companies were publicly traded since before 1991 and we include their stock prices in the regression model. Additionally, the list of top 10 employers in Minnesota include Wal-Mart Stores Inc. and Wells Fargo Bank Minnesota (http://inflationdata.com/inflation/consumer_price_index/historicalcpi.aspx?reloaded=true#Table). Hence, the stock prices of these two companies are also included in the model. The 16 stocks used in total are listed in Table 6.

| Company Name | Ticker Symbol | Company Name | Ticker Symbol |

|---|---|---|---|

| 3M Company | MMM | St. Jude Medical, Inc. | STJ |

| Best Buy Co., Inc. | BBY | SuperValu, Inc. | SVU |

| Ecolab, Inc. | ECL | Target Corporation | TGT |

| Fastenal Co. | FAST | UnitedHealth Group Inc. | UNH |

| General Mills, Inc. | GIS | U.S. Bancorp | USB |

| Hormel Foods Corporation | HRL | Wal-Mart Stores, Inc. | WMT |

| Medtronic Plc. | MDT | Wells Fargo & Company | WFC |

| Mosaic Company | MOS | Xcel Energy Inc. | XEL |

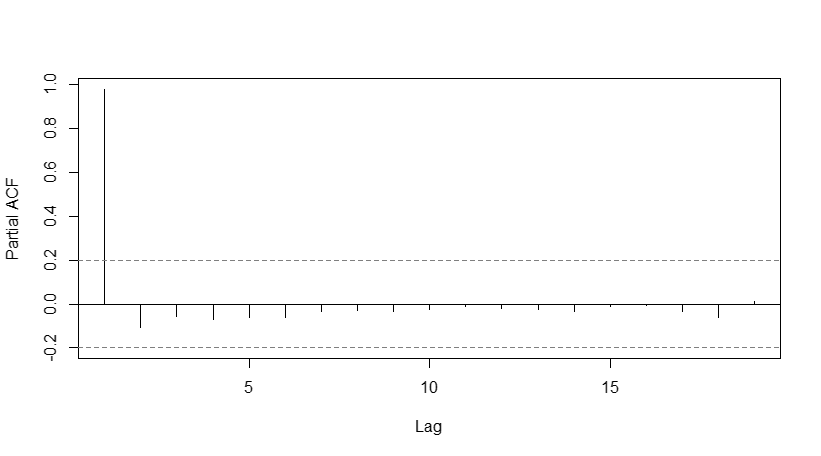

Financial indices often exhibit strong autocorrelation and consequently autoregressive components commonly feature in house price models (Nagaraja et al. 2011). Figure 5 plots the partial auto-correlation values of the hpi time series as a function of the lag.

We observe that the index lagging one quarter behind (AR(1)) has very high correlation with the hpi time series but it quickly falls off beyond the first lag and all the subsequent lagged indices have insignificant partial correlations. Consequently, we include only the AR1 term in the regression model.

Statistical analysis involving financial time series is often preceded by customary seasonality adjustment of the indices using standard time series techniques. It is well known that house price time series reveal a predictable and repetitive pattern with systematic highs in summer and lows in winter (Ngai and Tenreyro 2014). Consequently, publishers of popular house price indices like the FHFA or Standard and Poor’s (Case-Shiller index) produce a version of their indices discounting this effect (Federal Housing Finance Agency 2014). However, Minnesota is a land of extreme climates experiencing one of the widest range of temperatures in U.S. It is of interest to investigate if the impact of weather in Minnesota on its house prices extends beyond the routine pattern. Hence, we include the state level quarterly average temperatures (temp) and precipitation (precip) in the model. The data is obtained from http://www.ncdc.noaa.gov/cag/time-series.

Our model is stated as follows. Assuming -change points where is to de determined by the data, the regression model at the quarter, for is given by:

| (4.1) |

Here stockst denote the vector formed by stacking up the stock prices at time of the companies listed in Table 6 and is the corresponding coefficient vector.

4.3 Results

We used the data from the second quarter of 1991 to the second quarter to 2014 for model fitting. The first quarter data of 1991 was used for the AR(1) term, whereas the data for last 2 quarters of 2014 and first quarter of 2015 were held out for out-of-sample validation. Under the assumption of change points, separate regression models are fit to each of the segments. Hence, although the sample size () was larger than the number of predictors () in model 4.2, depending on the location of change-points, many segments may have less than 22 datapoints thereby necessitating high-dimensional regression methods. Higher values of () implies that average sample size for each segment () becomes really small and the estimates obtained may not be reliable. Hence, we restrict ourselves to the choices and and fit model 4.2 using the BASAD priors for the coefficient vectors in each segment. Note that for i.e. no change point, the model simply reduces to the traditional BASAD model. The models for different values of were assessed based on their in-sample DIC score and out-of-sample RMSPE score (Yeniay and Goktas 2002). Due to the presence of the autoregressive term, out-of-sample forecasts were obtained using one-step-ahead predictions.

Table 7 contains the DIC and RMSPE scores and estimated change points for the three choices of .

| K | DIC | RMSPE | ||

|---|---|---|---|---|

| 0 | 286.575 | 66.743 | ||

| 1 | 249.587 | 14.181 | 2008Q4 (2008Q2, 2009Q1) | |

| 2 | 269.054 | 14.967 | 2006Q2 (2005Q4, 2007Q3) | 2011Q1 (2010Q4, 2011Q2) |

Both the DIC score and the RMSPE score for were significantly worse than the scores for and justifying the use of a change point model. The single change point model detected a change point around late 2008- early 2009 which coincides with the sub-prime mortgage crisis. The two change point model detected change points in mid 2006 and early 2011. The DIC score for the single change point model was substantially better. RMSPE scores for change point models only validate the accuracy of the models after the last change point. We observed that the RMSPE score were similar for and with the former turning out to be marginally better. Hence, we present the subsequent analysis only for the single change point model as both in-sample and out-of-sample validations provide strongest evidence in favor of it.

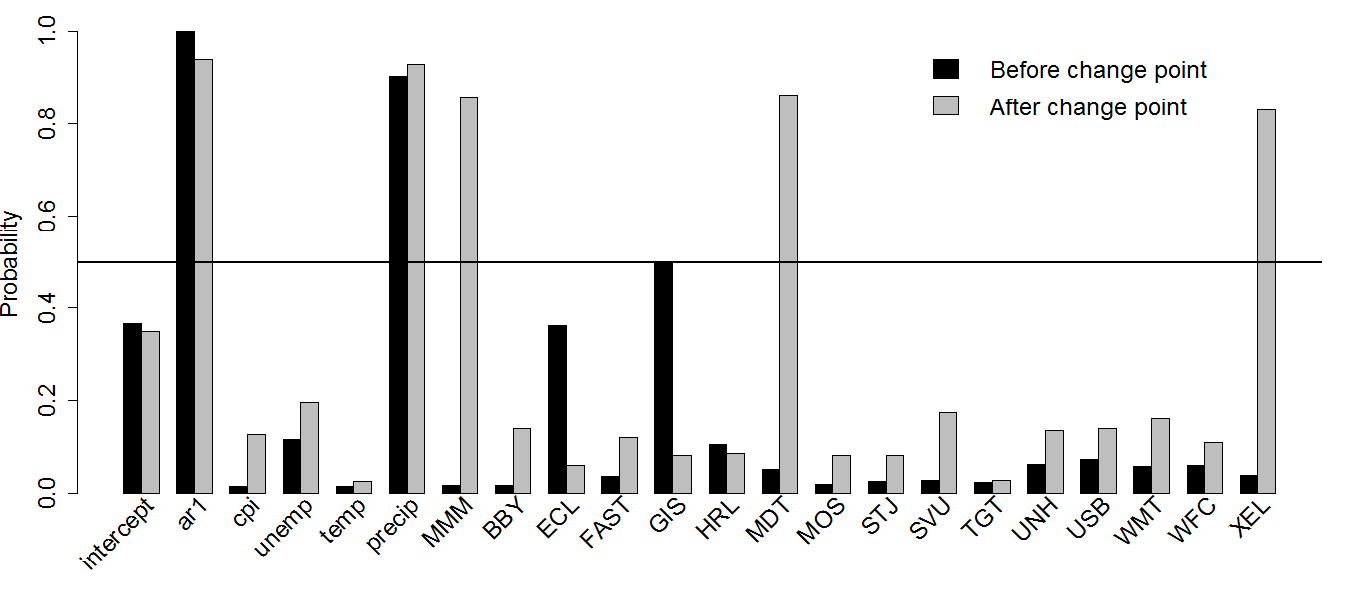

Figure 6 plots the probability of selection each of the regressors in model (4.2) before and after the change point using BASAD priors.

We observe that the set of variables selected by the median probability model differs before and after the change point. The AR(1) index and precipitation are selected with high probabilities in both segments. However, the selection of stocks differ considerably on either side of the change point. We see that prior to change point in 2008, there was little correlation between hpi and stocks with only General Mills (GIS) having a posterior median probability close to 0.5 (0.498). Perhaps this is a reflection of the fact discussed earlier that stock prices and hpi did not exhibit co-movements during the early 2000s. After the change point in 2008 the stocks of 3M (MMM), Medtronic (MDT) and Xcel Energy (XEL) are selected with high probability.

Turning to the actual coefficient values presented in Table 8 we observe that the value for coefficient for the AR(1) index drops significantly post change point indicating less autoregressive behavior after the change point.

| Before change point | After change point | |

|---|---|---|

| intercept | -0.015 (-4.537, 2.65) | 0.004 (-3.557, 4.003) |

| AR(1)* | 1.034 (0.96, 1.106) | 0.761 (0.022, 0.873) |

| cpi | 0 (-0.055, 0.054) | 0.042 (-0.07, 0.861) |

| unemp | -0.015 (-0.697, 0.137) | 0.01 (-1.063, 1.304) |

| temp | -0.02 (-0.064, 0.044) | 0.063 (-0.021, 0.121) |

| precip* | 0.964 (-0.003, 1.63) | 1.952 (-0.012, 2.806) |

| MMM* | 0.019 (-0.065, 0.107) | -0.573 (-0.832, 0.015) |

| BBY | -0.003 (-0.091, 0.088) | 0.065 (-0.071, 0.322) |

| ECL | -0.104 (-0.541, 0.048) | 0.026 (-0.09, 0.217) |

| FAST | 0 (-0.132, 0.132) | -0.033 (-0.746, 0.093) |

| GIS* | -0.151 (-0.958, 0.068) | -0.002 (-0.206, 0.185) |

| HRL | -0.013 (-0.636, 0.131) | 0.016 (-0.12, 0.438) |

| MDT* | 0.071 (-0.022, 0.168) | 1.214 (-0.073, 1.666) |

| MOS | -0.056 (-0.107, -0.004) | -0.017 (-0.413, 0.074) |

| STJ | 0.007 (-0.097, 0.107) | 0.026 (-0.101, 0.394) |

| SVU | -0.035 (-0.144, 0.07) | 0.021 (-0.129, 1.569) |

| TGT | 0.001 (-0.108, 0.11) | 0 (-0.116, 0.117) |

| UNH | -0.061 (-0.185, 0.043) | -0.042 (-0.521, 0.083) |

| USB | 0.045 (-0.071, 0.241) | -0.017 (-2.98, 0.147) |

| WMT | 0.073 (-0.016, 0.17) | 0.014 (-0.122, 1.083) |

| WFC | -0.006 (-0.154, 0.14) | 0.001 (-0.142, 2.296) |

| XEL* | -0.005 (-0.13, 0.112) | 1.279 (-0.05, 2.436) |

We also observe a positive association of hpi with precipitation. Since summer months witness significantly higher precipitation than winter (see Figure 7),

this merely corroborates the traditional ’hot season cold season’ trend of house prices. What is more interesting is the fact that this effect is much more pronounced after 2008 indicating more disparity between summer and winter house prices in the post recession bear market.

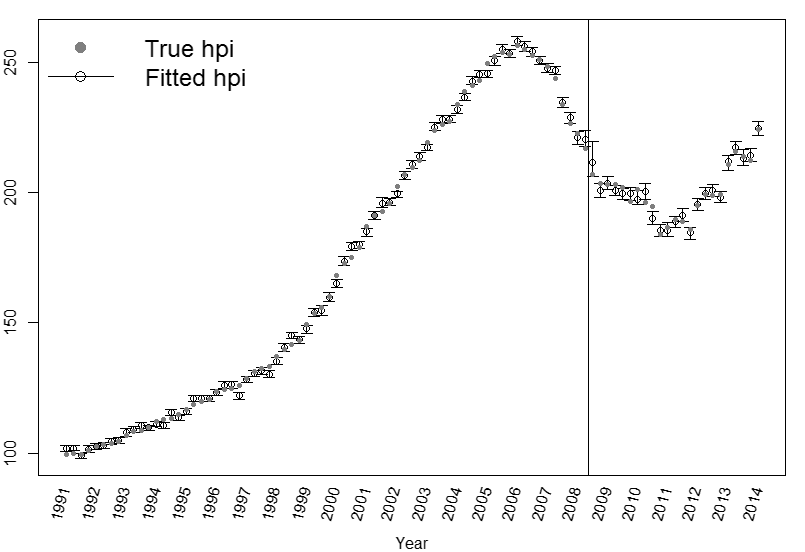

The posterior predictive distributions for the hpi at each quarter was also obtained from the MCMC sampler and Figure 8 plots the true hpi versus the in-sample median fits and confidence intervals.

We see that that the posterior confidence intervals provide substantial coverage. We also observe that the confidence intervals are wider after the change point. This is expected as there are only about 23 time points compared to around 70 before the change point.

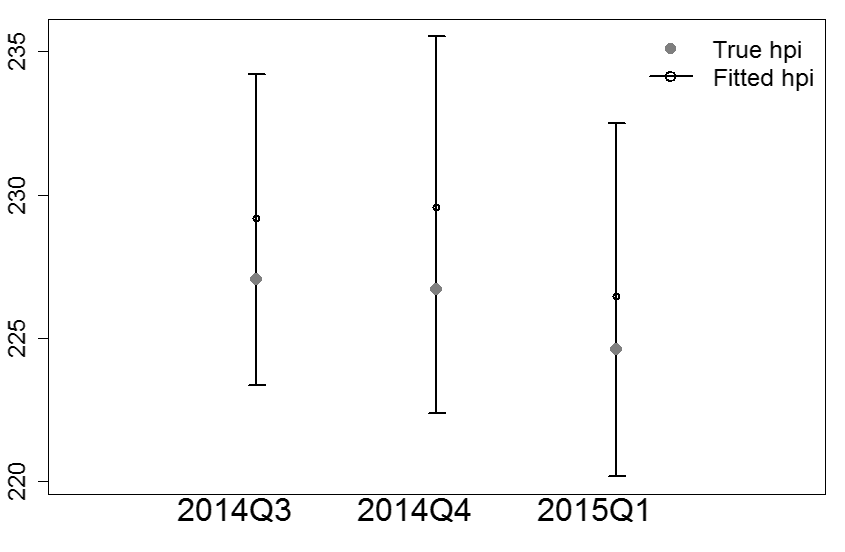

The out-of-sample posterior fits are provided in Figure 9. All the three out-of-sample predictions are very close to their true values. However, the out-of-sample confidence intervals are significantly wider reflecting the uncertainty associated with prediction.

Observe from Figure 6 that in presence of the stock prices of Minnesota based companies, national level macro-economic indicators like the cpi or unemployment were not selected in the model. This perhaps provides evidence in support of the conjecture that hpi is strongly correlated with local macro-economics (Garmaise and Moskowitz 2002). However, its worthwhile to point out that multivariate regression models, although a simple and powerful tool to determine correlation, rarely implies causality. Any confirmatory assessment of the change points detected and the variables selected by our method would require further economic research. Nevertheless, the model evaluation metrics in Table 7 provide very strong evidence in favor of one or more change points thereby justifying the use of our methodology to analyze the data.

5 Conclusion

We have presented a very general methodology for analyzing high dimensional data using changing linear regression. Our fully Bayesian approach offers several inferential advantages including quantifying uncertainty regarding the the change points as well as variable selection for each segment. Our framework is flexible to the choice of variable selection priors although the BASAD prior empirically outperformed other competing choices. A wide range of constrained variable selections like grouping or partial selection can be seamlessly accomplished in our setup. The analysis of Minnesota hpi data using our methodology revealed strong evidence for a potential change point with respect to the association with other macro-economic variables.

We have discussed several approaches for handling unknown number of change points. However, most of them comes with statutory warnings regarding computational requirements. More efficient algorithms for simultaneous detection of number of change points need to be researched. Other potential extensions include accommodating missing data, measurement errors or non-Gaussian responses in a high dimensional changing regression setup. Extensions to change point detection in high dimensional VAR models also need to be explored due to the extensive usage of VAR models in economics research (Christiano et al. 2000; Bernanke et al. 2004). In a time series context, our work is restricted to detecting historical change points. Detecting future change points in high dimensional time series is equally important to provide accurate predictions. We identify all these areas as directions for future research.

References

- Adams and MacKay (2007) Adams, R. P. and MacKay, D. J. (2007), “Bayesian Online Changepoint Detection,” arXiv preprint arXiv:0710.3742.

- Ahamada and Diaz Sanchez (2013) Ahamada, I. and Diaz Sanchez, J. L. (2013), “A Retrospective Analysis of the House Prices Macro-relationship in the United States,” The World Bank: Policy Research Working Paper Series, Jul.

- Apergis (2003) Apergis, N. (2003), “Housing Prices and Macroeconomic Factors: Prospects within the European Monetary Union,” International Real Estate Review, 6, 63–47.

- Baladandayuthapani et al. (2010) Baladandayuthapani, V., Ji, Y., Talluri, R., Nieto-Barajas, L. E., and Morris, J. S. (2010), “Bayesian Random Segmentation Models to Identify Shared Copy Number Aberrations for Array CGH Data,” Journal of the American Statistical Association, 105, 1358–1375.

- Barbieri and Berger (2004) Barbieri, M. M. and Berger, J. O. (2004), “Optimal Predictive Model Selection,” Annals of Statistics, 32, 870–897.

- Barry and Hartigan (1993) Barry, D. and Hartigan, J. A. (1993), “A Bayesian Analysis for Change Point Problems,” Journal of the American Statistical Association, 88, 309–319.

- Bernanke et al. (2004) Bernanke, B. S., Boivin, J., and Eliasz, P. (2004), “Measuring the Effects of Monetary Policy: A Factor-Augmented Vector Autoregressive (FAVAR) Approach,” Working Paper 10220, National Bureau of Economic Research.

- Brooks et al. (2003) Brooks, S. P., Giudici, P., and Roberts, G. O. (2003), “Efficient Construction of Reversible Jump Markov Chain Monte Carlo Proposal Distributions,” Journal of the Royal Statistical Society: Series B, 65, 3–39.

- Carlin and Chib (1995) Carlin, B. P. and Chib, S. (1995), “Bayesian Model Choice via Markov Chain Monte Carlo Methods,” Journal of the Royal Statistical Society: Series B, 57, 473–484.

- Carlin et al. (1992) Carlin, B. P., Gelfand, A. E., and Smith, A. F. M. (1992), “Hierarchical Bayesian Analysis of Changepoint Problems,” Journal of the Royal Statistical Society: Series C, 41, 389–405.

- Carvalho et al. (2010) Carvalho, C. M., Polson, N. G., and Scott, J. G. (2010), “The Horseshoe Estimator for Sparse Signals,” Biometrika, 97, 465–480.

- Case et al. (2001) Case, K. E., Shiller, R. J., and Quigley, J. M. (2001), “Comparing Wealth Effects: The Stock Market Versus the Housing Market,” Working Paper 8606, National Bureau of Economic Research.

- Catte et al. (2004) Catte, P., Girouard, N., Price, R., and Andre, C. (2004), “Housing Markets, Wealth and the Business Cycle.” OECD Working Paper, No 394.

- Chen and Gupta (1997) Chen, J. and Gupta, A. K. (1997), “Testing and Locating Variance Changepoints with Application to Stock Prices,” Journal of the American Statistical Association, 92, 739–747.

- Christiano et al. (2000) Christiano, L. J., Eichenbaum, M., and Evans, C. L. (2000), “Monetary policy shocks: What have we learned and to what end?” in Handbook of Macroeconomics, eds. Taylor, J. and Woodford, M., Amsterdam, Holland: Elsevier, pp. 65 – 148.

- Dellaportas et al. (2002) Dellaportas, P., Forster, J. J., and Ntzoufras, I. (2002), “On Bayesian Model and Variable Selection Using MCMC,” Statistics and Computing, 12, 27–36.

- Ehlers and Brooks (2008) Ehlers, R. S. and Brooks, S. P. (2008), “Adaptive Proposal Construction for Reversible Jump MCMC,” Scandinavian Journal of Statistics, 35, 677–690.

- Fan and Li (2001) Fan, J. and Li, R. (2001), “Variable Selection via Nonconcave Penalized Likelihood and Its Oracle Properties,” Journal of the American Statistical Association, 96, 1348––1360.

- Fan and Sisson (2011) Fan, Y. and Sisson, S. (2011), “Reversible Jump Markov chain Monte Carlo,” in Handbook of Markov Chain Monte Carlo, eds. Brooks, S. P., Gelman, A., Jones, G. L., and Meng, X.-L., Boca Raton, FL: Chapman & Hall/CRC, pp. 67–87.

- Farr et al. (2015) Farr, W. M., Mandel, I., and Stevens, D. (2015), “An Efficient Interpolation Technique for Jump Proposals in Reversible-jump Markov Chain Monte Carlo Calculations,” Royal Society Open Science, 2.

- Federal Housing Finance Agency (2014) Federal Housing Finance Agency (2014), “U.S. House Price Index Report - 3Q 2014 / September 2014,” Technical report.

- Garmaise and Moskowitz (2002) Garmaise, M. J. and Moskowitz, T. J. (2002), “Confronting Information Asymmetries: Evidence from Real Estate Markets,” Working Paper 8877, National Bureau of Economic Research.

- Gelfand and Ghosh (1998) Gelfand, A. E. and Ghosh, S. K. (1998), “Model choice: A Minimum Posterior Predictive Loss Approach,” Biometrika, 85, 1–11.

- George and McCulloch (1993) George, E. I. and McCulloch, R. E. (1993), “Variable Selection via Gibbs Sampling,” Journal of the American Statistical Association, 88, 881–889.

- Green (1995) Green, P. J. (1995), “Reversible Jump Markov chain Monte Carlo Computation and Bayesian Model Determination,” Biometrika, 82, 711–732.

- Green and Hastie (2009) Green, P. J. and Hastie, D. I. (2009), “Reversible Jump MCMC,” .

- Han and Carlin (2001) Han, C. and Carlin, B. P. (2001), “Markov Chain Monte Carlo Methods for Computing Bayes Factors,” Journal of the American Statistical Association, 96, 1122–1132.

- Hastie and Green (2012) Hastie, D. I. and Green, P. J. (2012), “Model Choice Using Reversible Jump Markov Chain Monte Carlo,” Statistica Neerlandica, 66, 309–338.

- Hofmann (2003) Hofmann, B. (2003), “Bank Lending and Property Prices: Some International Evidence.” Working papers, Hong Kong Institute for Monetary Research.

- Ishwaran and Rao (2005) Ishwaran, H. and Rao, J. S. (2005), “Spike and Slab Variable Selection: Frequentist and Bayesian Strategies,” The Annals of Statistics, 33, 730–773.

- Kezim and Pariseau (2004) Kezim, B. and Pariseau, S. E. (2004), “Bayesian Analysis of a Structural Change in Volatility Using the Gibbs Sampler with an Application to Stock Market Returns,” Journal of Business and Economic Studies, 10, 1–11.

- Lee et al. (To appear) Lee, S., Seo, M. H., and Shin, Y. (To appear), “The lasso for high dimensional regression with a possible change point,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), n/a–n/a.

- Lenardon and Amirdjanova (2006) Lenardon, M. J. and Amirdjanova, A. (2006), “Interaction Between Stock Indices via Changepoint Analysis,” Applied Stochastic Models in Business and Industry, 22, 573–586.

- Leung (2004) Leung, C. K. Y. (2004), “Macroeconomics and Housing: A Review of the Literature,” Discussion Papers 00004, Chinese University of Hong Kong, Department of Economics.

- Littenberg and Cornish (2009) Littenberg, T. B. and Cornish, N. J. (2009), “Bayesian Approach to the Detection Problem in Gravitational Wave Astronomy,” Physical Review, 80, 063007–1– 063007–19.

- Malpezzi (2003) Malpezzi, S. (2003), “Hedonic Pricing Models: A Selective and Applied Review,” in Housing Economics and Public Policy, eds. O’Sullivan, T. and Gibb, K., Malder, MA: Blackwell Science Ltd, pp. 67–89.

- Mavrodiy (2005) Mavrodiy, A. (2005), “Factor Analysis of Real Estate Prices,” EERC MA thesis.

- McCulloch and Tsay (1993) McCulloch, R. E. and Tsay, R. S. (1993), “Bayesian Inference and Prediction for Mean and Variance Shifts in Autoregressive Time Series,” Journal of the American Statistical Association, 88, 968–978.

- Nagaraja et al. (2011) Nagaraja, C. H., Brown, L. D., and Zhao, L. H. (2011), “An Autoregressive Approach to House Price Modeling,” The Annals of Applied Statistics, 5, 124–149.

- Narisetty and He (2014) Narisetty, N. N. and He, X. (2014), “Bayesian Variable Selection with Shrinking and Diffusing Priors,” The Annals of Statistics, 42, 789–817.

- Ngai and Tenreyro (2014) Ngai, L. R. and Tenreyro, S. (2014), “Hot and Cold Seasons in the Housing Market,” American Economic Review, 104, 3991–4026.

- Ong and Chang (2013) Ong, T. S. and Chang, Y. S. (2013), “Macroeconomic Determinants of Malaysian Housing Market,” Journal of Human and Social Science Research, 1, 119–127.

- Otrok and Terrones (2005) Otrok, C. and Terrones, M. E. (2005), “House Prices, Interest Rates and Macroeconomic Fluctuations: International Evidence,” Unpublished manuscript.

- Panagiotidis and Printzis (2015) Panagiotidis, T. and Printzis, P. (2015), “On the Macroeconomic Determinants of the Housing Market in Greece: a VECM approach,” LSE Research Online Documents on Economics.

- Park and Casella (2008) Park, T. and Casella, G. (2008), “The Bayesian Lasso,” Journal of the American Statistical Association, 103, 681–686.

- Raman et al. (2009) Raman, S., Fuchs, T. J., Wild, P. J., Dahl, E., and Roth, V. (2009), “The Bayesian Group-Lasso for Analyzing Contingency Tables,” in Proceedings of the 26th Annual International Conference on Machine Learning, New York, NY, USA: ACM, ICML ’09, pp. 881–888.

- Reeves et al. (2007) Reeves, J., Chen, J., Wang, X., Lund, R., and Lu, Q. (2007), “A Review and Comparison of Changepoint Detection Techniques for Climate Data,” Journal of Applied Meteorology and Climatology, 46, 900–915.

- Renigier-Biłozor and Wiśniewski (2013) Renigier-Biłozor, M. and Wiśniewski, R. (2013), “The Impact of Macroeconomic Factors on Residential Property Prices Indices in Europe,” Aestimum, 0, 149–166.

- Richardson and Green (1997) Richardson, S. and Green, P. J. (1997), “On Bayesian Analysis of Mixtures with an Unknown Number of Components (with discussion),” Journal of the Royal Statistical Society: Series B, 59, 731–792.

- Spiegelhalter et al. (2002) Spiegelhalter, D. J., Best, N. G., Carlin, B. P., and van der Linde, A. (2002), “Bayesian Measures of Model Complexity and Fit,” Journal of the Royal Statistical Society: Series B, 64, 583–639.

- Strömberg et al. (2011) Strömberg, P., Hedman, M., and Broberg, M. (2011), “Forecasting the House Price Index in Stockholm County 2011-2014: A Multiple Regression Analysis of Four Influential Macroeconomic Variables,” Bachelor’s thesis from Mälardalen University / School of Sustainable Development of Society and Technology.

- Tibshirani (1994) Tibshirani, R. (1994), “Regression Shrinkage and Selection Via the Lasso,” Journal of the Royal Statistical Society: Series B, 58, 267–288.

- Tsatsaronis and Zhu (2004) Tsatsaronis, K. and Zhu, H. (2004), “What Drives Housing Price Dynamics: Cross-country Evidence,” BIS Quarterly Review, March, 65–78.

- Turner et al. (2009) Turner, R., Saatci, Y., and Rasmussen, C. (2009), “Adaptive Sequential Bayesian Change Point Detection,” .

- Yeniay and Goktas (2002) Yeniay, O. and Goktas, A. (2002), “A Comparison of Partial Least Squares Regression with Other Prediction Methods,” Hacettepe Journal of Mathematics and Statistics, 31, 99–111.

- Zou (2006) Zou, H. (2006), “The Adaptive Lasso and Its Oracle Properties,” Journal of the American Statistical Association, 101, 1418–1429.

- Zou and Hastie (2005) Zou, H. and Hastie, T. (2005), “Regularization and Variable Selection via the Elastic Net,” Journal of the Royal Statistical Society: Series B, 67, 301–320.